Matrix Service Company: The Engineering Contractor That Bet on America's Energy Transition

I. Introduction & Episode Roadmap

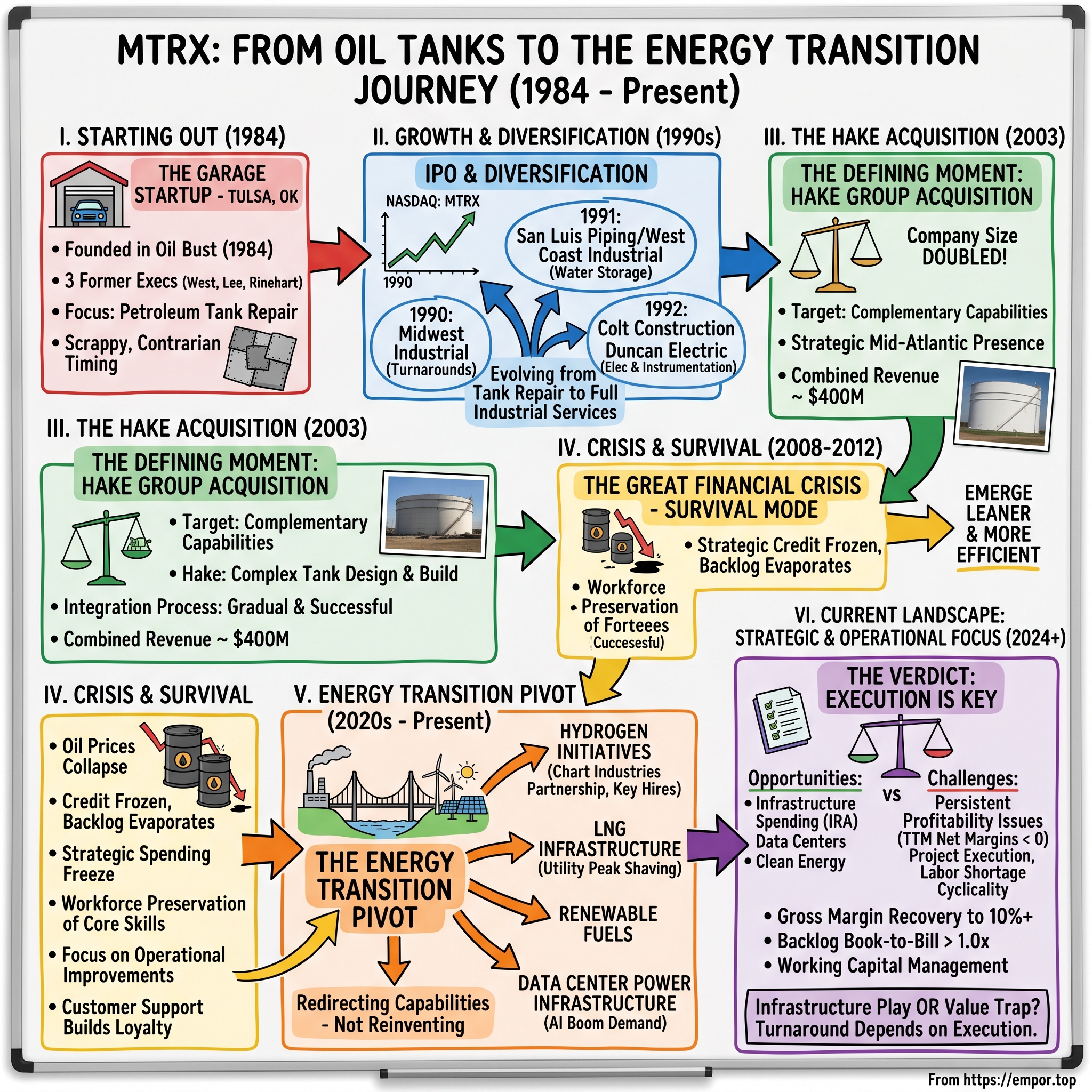

The year was 1984. Oil prices had collapsed from their 1980 peak of $39 per barrel to under $30, triggering the worst energy crisis since the 1970s. Banks across Texas and Oklahoma were failing. Drilling rigs stood idle like steel monuments to a boom gone bust. In Tulsa—once the "Oil Capital of the World"—office towers emptied as petroleum companies slashed workforces. It was precisely at this moment, in a cramped garage with three desks pushed side by side and a single shared telephone line, that three former executives decided to launch a new energy services company.

The workspace was so tight that each man had to stand to let the others pass. These were former Tank Service, Inc. executives with an idea to build a tank repair company that would be known for service in the storage solutions market. Doyl West, the former president of Tank Service; Bill Lee, vice-president of finance; and Marty Rinehart, an executive vice-president, incorporated Matrix Service Inc. on April 4, 1984, along with silent partner Harold Morgan. Bob Wagoner, who became a significant shareholder and the first Vice President of Engineering, joined about a year later.

The contrarian timing seemed almost absurd. Starting a petroleum services company during an industry collapse was like opening an umbrella store in the Sahara. Yet these founders saw something others missed: even in a downturn—especially in a downturn—America's aging energy infrastructure would need maintenance. Storage tanks don't stop corroding just because oil prices fall. Refineries still need turnarounds. Pipeline terminals still require repairs. The infrastructure supporting America's energy economy couldn't simply be abandoned.

This episode traces Matrix Service Company's forty-year journey from that Tulsa garage to becoming a publicly traded contractor with operations across North America. It's a story of strategic pivots, from petroleum tank repairs to water storage, from traditional fossil fuel infrastructure to hydrogen and renewable energy systems. Along the way, we'll examine how a bootstrap startup navigated multiple boom-bust cycles, executed a transformative acquisition that doubled its size overnight, survived the 2008 financial crisis, and now positions itself for the energy transition.

The central question driving this narrative: Can a company built on maintaining yesterday's energy infrastructure successfully transform itself to build tomorrow's? As data centers drive unprecedented power demand, as hydrogen emerges as a potential clean fuel solution, and as America rebuilds its electrical grid for an electrified economy, Matrix finds itself at a critical inflection point. The company that began by patching oil tanks now talks about constructing hydrogen infrastructure and power substations for AI computing facilities.

But there's a catch. With 2,000+ employees and 4 operating companies, Matrix remains a relatively small player in a consolidating industry dominated by giants like Fluor, Jacobs, and KBR. Recent financial performance raises serious questions about execution capabilities and profitability. The path from industrial services contractor to energy transition enabler is fraught with operational, financial, and strategic challenges.

II. The Garage Beginning: Three Engineers and a Vision

Picture Tulsa in early 1984. The city's skyline, built on oil wealth, now overlooked a devastated economy. Penn Square Bank's collapse two years earlier had triggered a regional banking crisis. Petroleum engineers who once commanded six-figure salaries were driving cabs or selling insurance. The parking lots of Williams Companies and CITGO, major local employers, thinned as layoffs mounted. Local newspapers ran daily bankruptcy notices from oil service companies.

Into this apocalyptic landscape stepped Doyl West, a man who understood the petroleum industry's infrastructure needs from decades of experience. As president of Tank Service Inc., West had witnessed firsthand how even distressed refineries and terminals couldn't neglect critical maintenance. Storage tanks—those massive cylindrical structures dotting the industrial landscape—required constant attention. Corrosion never sleeps. Environmental regulations were tightening. Someone had to do this unglamorous but essential work.

West recruited two colleagues who shared his vision. Bill Lee brought financial acumen from his role as Tank Service's finance chief—crucial for a startup launching without venture capital in a credit-constrained environment. Marty Rinehart contributed operational expertise, understanding the nuts and bolts of mobilizing crews, managing projects, and ensuring safety compliance. Together, they possessed complementary skills: West's industry relationships and strategic vision, Lee's financial discipline, and Rinehart's operational excellence.

West became the CEO for Matrix, Lee became vice-president of finance, and Rinehart was appointed vice-president of operations. The division of responsibilities was clear from day one, avoiding the founder conflicts that doom many startups. Harold Morgan joined as a silent partner, providing additional capital while remaining outside daily operations.

The garage workspace became legendary in company lore. Engineers accustomed to corporate offices now worked shoulder-to-shoulder in conditions that would make a Silicon Valley startup look luxurious. No conference rooms meant customer meetings happened at diners. No secretary meant founders answered their own phones. No IT department meant handwritten invoices and manual bookkeeping. This forced frugality would become part of Matrix's DNA—a scrappy, entrepreneurial culture that persisted even after going public.

The name "Matrix" itself carried meaning. In mathematics, a matrix represents an array of elements that can be combined in various ways to solve complex problems. For the founders, it symbolized their vision of combining different service capabilities—tank repair, maintenance, coating, construction—into integrated solutions for customers. Unlike competitors who specialized narrowly, Matrix would offer comprehensive tank services under one roof.

Their timing, while seemingly terrible, contained a hidden advantage. With established competitors retreating or failing, Matrix could hire experienced workers at reasonable wages. Distressed customers needed vendors willing to work on flexible payment terms. The company's low overhead—that garage didn't require much rent—allowed competitive pricing. Most importantly, the founders' reputations from Tank Service opened doors that might otherwise remain closed to a startup.

III. Building the Foundation (1984-1989)

The first Matrix project came through relationships, not marketing. A refinery manager who knew West from Tank Service days needed emergency tank repairs but faced budget constraints. Matrix proposed a creative solution: rather than a lump-sum contract, they would bill incrementally as work progressed, allowing the customer to spread costs across multiple budget periods. This flexibility, impossible for larger competitors with rigid corporate structures, became Matrix's calling card.

Early projects were modest—patching leaks, replacing valves, sandblasting and recoating corroded surfaces. But each successful job built credibility. In an industry where one catastrophic failure could trigger environmental disasters and regulatory nightmares, reputation was everything. Matrix's safety record was spotless. Projects finished on time. Invoices reflected actual costs without hidden surprises. Word spread through the tight-knit community of refinery managers and terminal operators.

By 1986, Matrix faced a pleasant problem: more work than their Tulsa team could handle. The solution revealed strategic thinking that would define the company's growth. Rather than turning down distant projects, they opened a Michigan office—their first union operation. This wasn't just geographic expansion; it was a deliberate move to work with organized labor, essential for many industrial facilities in the Midwest and Northeast. The ability to operate both union and non-union demonstrated flexibility that larger competitors often lacked.

The Michigan expansion taught valuable lessons. Managing remote operations required new systems for project tracking, quality control, and financial reporting. The company developed standardized procedures that could be replicated in future locations. They learned to navigate different state regulations, union rules, and customer expectations. These capabilities would prove essential for the roll-up strategy that emerged later.

In 1988 the company formed a subsidiary, Petrotank Equipment Inc., and a year later Matrix Service Environmental Company was incorporated in Delaware as a holding company for the two units. This corporate restructuring wasn't mere paperwork. It reflected growing sophistication in how Matrix approached markets. Petrotank focused on equipment supply and specialized services. The environmental subsidiary addressed increasing regulatory requirements around tank inspections and remediation. The holding company structure provided flexibility for future acquisitions while protecting operating units from cross-liability.

Financial discipline remained paramount. Unlike venture-backed startups that could burn cash pursuing growth, Matrix had to remain profitable from day one. Lee instituted rigorous project accounting, tracking costs daily to identify problems before they became crises. The company maintained minimal overhead, with executives still answering their own phones and traveling coach. This lean culture created competitive advantages in bidding—Matrix could profitably take projects that barely covered larger competitors' overhead.

Customer relationships deepened beyond transactional project work. Matrix technicians became familiar faces at client facilities, understanding not just immediate needs but long-term maintenance schedules and capital planning cycles. This intelligence allowed proactive proposals—suggesting tank inspections before regulations required them, identifying corrosion problems before they became critical, planning turnarounds to minimize downtime. The company was evolving from contractor to trusted advisor.

By decade's end, Matrix had established a sustainable business model. Annual revenues approached $20 million. The company operated profitably in multiple states. The workforce had grown to over 100 employees. Most importantly, Matrix had survived the brutal shakeout that claimed countless energy service companies during the 1980s bust. The founders' contrarian bet was paying off. But to achieve their larger ambitions, they needed capital that bootstrapping couldn't provide.

IV. The IPO and Diversification Play (1990-1999)

In September 1990, Matrix engaged in an Initial Public Offering, listing on the NASDAQ Stock Exchange under the ticker symbol MTRX. The IPO raised $26 million, selling 3.25 million shares. PaineWebber Inc., Robertson, Stephens & Co., and First Analysis Securities managed the offering at $8 per share. For a six-year-old company started in a garage, going public represented a remarkable achievement. But the IPO was a means, not an end.

The public offering coincided with Matrix's first major acquisition. Matrix closed on the acquisition of Midwest Industrial Contractors at a cost of $22 million in cash, stock, and notes. Midwest Industrial provided maintenance and construction services to refineries and specialized in "turnarounds," the quick maintenance of a refinery's critical operating units. This wasn't just buying revenue; it was acquiring a critical capability.

Refinery turnarounds represent the ultimate test of industrial service contractors. These planned shutdowns for maintenance and upgrades cost operators millions in lost production daily. Every hour counts. Contractors must mobilize hundreds of workers, coordinate multiple trades, manage complex logistics, and ensure flawless safety—all under extreme time pressure. Midwest Industrial had mastered this high-stakes game. Their expertise immediately elevated Matrix from routine maintenance provider to mission-critical partner for refinery operations.

The Midwest acquisition also demonstrated Matrix's integration philosophy. Rather than imposing corporate uniformity, they preserved Midwest's operational autonomy while providing financial resources and back-office support. Key Midwest managers received equity stakes, aligning their interests with Matrix's success. This decentralized approach—maintaining entrepreneurial energy within acquired units—would become a hallmark of Matrix's growth strategy.

In June 1991 the company paid $10.2 million for San Luis Piping Construction Co., Inc. and West Coast Industrial Coatings, Inc. to become involved in water storage tanks. San Luis Piping did fabricated plate work, and West Industrial provided sandblasting, coating, and other services in the maintenance of potable water storage tanks. This move beyond petroleum infrastructure was strategic. Water tanks used similar construction techniques but served different customers—municipalities, water districts, industrial facilities. Diversification reduced dependence on volatile energy markets while leveraging existing capabilities.

In December 1992 Matrix completed a pair of acquisitions, picking up Colt Construction Company and Duncan Electric Company. Colt brought general construction capabilities for industrial facilities. Duncan added electrical and instrumentation expertise—increasingly important as refineries and plants automated operations. Each acquisition expanded Matrix's service menu, enabling comprehensive facility solutions rather than narrow specialization.

The acquisition pace reflected broader industry dynamics. The 1990s saw massive consolidation in industrial services as companies sought scale economies and broader capabilities. Private equity firms were rolling up fragmented markets. International competitors were entering North America. Matrix had to grow or risk being marginalized. But unlike purely financial buyers focused on cost synergies, Matrix pursued strategic acquisitions that enhanced technical capabilities and customer relationships.

Integration challenges emerged. Different safety cultures, accounting systems, and operational procedures had to be harmonized. Some acquisitions brought unexpected liabilities—environmental issues at old project sites, warranty claims on completed work, cultural mismatches that led to talent departures. Matrix learned to conduct more thorough due diligence, looking beyond financial statements to operational realities.

Over the next ten years Matrix focused on growth and development with continued acquisitions and the award of significant contracts. Yet, despite this good news, they also experienced growing pains, discontinued or shed low performing or non-core assets and developed a new five-year plan to rebuild. Not every acquisition succeeded. Some units were divested when synergies failed to materialize. The company learned hard lessons about acquisition discipline—the importance of cultural fit, realistic integration timelines, and maintaining focus on core competencies.

Public market pressures added complexity. Quarterly earnings calls demanded explanations for integration costs and acquisition expenses. Stock price volatility reflected investor skepticism about the roll-up strategy. Matrix had to balance long-term strategic building with short-term financial performance—a tension that would persist throughout its public company journey.

By 1999, Matrix had transformed from a regional tank repair company to a diversified industrial services provider. Revenues exceeded $150 million. Operations spanned the continent. The service portfolio encompassed everything from tank construction to electrical installation. Yet questions remained about whether this broader platform could generate superior returns or simply added complexity without corresponding value creation.

V. The Hake Acquisition: A Defining Moment (2003-2004)

In early 2002, Matrix CEO Brad Vetal faced a strategic crossroads. The company had grown steadily through acquisitions but remained subscale compared to major competitors. Customer consolidation in the energy industry meant fewer, larger clients demanding comprehensive solutions from fewer, larger vendors. Matrix needed a transformative move—not incremental additions but a step-function change in capabilities and scale.

The search process was exhaustive. Over 18 months, Matrix evaluated more than 240 potential acquisition targets. Investment bankers pitched everything from distressed assets to strategic carve-outs from larger corporations. The criteria were specific: the target needed complementary capabilities, cultural compatibility, geographic expansion potential, and a price that wouldn't cripple Matrix's balance sheet. Most candidates failed one or more tests.

Hake Group Inc. emerged as the ideal candidate. Based in Pennsylvania, Hake was a second-generation family business founded in 1946. The company specialized in aboveground storage tank construction and maintenance but had evolved far beyond basic services. Hake's engineers designed complex tank systems. Their construction crews had built some of the largest storage facilities in North America. Their maintenance teams held long-term contracts with major refineries and terminals. The company generated $174.8 million in annual sales with $5.2 million in net income—a larger, more profitable business than Matrix itself.

The strategic rationale was compelling. Hake dominated the mid-Atlantic region where Matrix had minimal presence. Their engineering capabilities exceeded Matrix's, particularly in design-build projects. Hake's customer relationships included oil majors who could provide entrada into new markets. The workforce was highly skilled, with many employees having decades of experience. Culturally, Hake shared Matrix's emphasis on safety, quality, and customer service.

Negotiations were delicate. The Hake family had received multiple acquisition offers over the years but valued independence. Matrix had to convince them that joining forces offered better prospects than remaining standalone. The pitch emphasized continuity—Hake would retain operational autonomy, key managers would remain in place, the Hake brand would continue. Matrix wasn't buying to strip assets or slash costs but to build something larger together.

The deal structure reflected these priorities. The $50 million purchase price included cash, Matrix stock, and earnout provisions tied to future performance. Hake family members received board representation. Key employees got retention packages and equity incentives. The agreement protected Hake's Pennsylvania workforce and facilities. This wasn't a hostile takeover but a negotiated partnership.

Due diligence revealed both opportunities and challenges. Hake's project backlog was strong, but several large contracts were approaching completion without equivalent replacements. The company's IT systems were outdated, requiring investment to integrate with Matrix's platforms. Some equipment needed replacement. Environmental liabilities from decades-old projects required careful assessment. Matrix's board debated whether these issues were manageable or deal-breakers.

The February 2003 closing marked a watershed moment. Matrix's goal to double the size of the company was achieved in a single transaction. Combined revenues approached $400 million. The employee base exceeded 3,000. Geographic coverage spanned from California to Pennsylvania. Most importantly, the combination created a platform with national scale and comprehensive capabilities.

Integration proceeded carefully. Rather than immediately merging operations, Matrix maintained Hake as a distinct division for the first year. This allowed time to understand Hake's business, build relationships with key customers and employees, and identify best practices from both organizations. Joint teams worked on harmonizing safety protocols, accounting systems, and procurement processes. The gradual approach minimized disruption while capturing synergies.

Customer response was positive. Several major oil companies had hesitated to award large projects to Matrix alone, questioning whether the company had sufficient resources. The Hake combination eliminated these concerns. New contract wins accelerated. Cross-selling opportunities emerged—Matrix could now offer Hake's customers services in regions Hake didn't cover, while Hake opened doors for Matrix in the Northeast.

The acquisition's success validated Matrix's strategy of growth through strategic combination rather than purely organic expansion. But it also raised the stakes. Matrix was now a meaningful player in industrial services, visible to larger competitors and expected to perform at higher levels. The company had achieved critical mass, but maintaining momentum would require continued evolution.

VI. The Great Financial Crisis and Survival Mode (2008-2012)

September 2008 brought chaos to global markets. Lehman Brothers collapsed. Credit markets froze. Oil prices, which had spiked to $147 per barrel in July, plummeted below $40 by December. For Matrix, whose fortunes were tied to energy industry capital spending, the timing couldn't have been worse. The company had just completed several acquisitions and carried significant debt. Major customers were canceling projects daily.

The crisis hit industrial services particularly hard. Refineries postponed turnarounds to preserve cash. Pipeline companies halted expansion projects. Terminal operators deferred maintenance. Even routine repair work slowed as customers scrutinized every expense. Matrix's backlog, carefully built over years, evaporated within months. Revenue projections became worthless. The stock price crashed from over $30 to under $5.

Management's response was swift and severe. All non-essential spending stopped immediately. Executive salaries were cut. Hiring froze except for revenue-generating positions. The company negotiated payment extensions with suppliers while accelerating collection efforts from customers. Every project was reviewed for profitability—marginal work was declined even if it meant idle crews. Survival trumped growth.

Workforce reductions were inevitable but handled strategically. Rather than across-the-board cuts that would destroy capabilities, Matrix focused on preserving core competencies. Skilled welders, experienced project managers, and workers with specialized certifications were retained even if underutilized. Administrative and support functions bore deeper cuts. The company established a recall list, promising to rehire laid-off workers when conditions improved.

Some competitors didn't survive. Smaller contractors lacking financial resources simply closed. Larger players retreated from marginal markets. Assets became available at distressed prices—equipment, facilities, even entire business units. Matrix, despite its own challenges, maintained enough financial flexibility to act opportunistically. The company acquired strategic assets at fraction of replacement cost, positioning for eventual recovery.

Customer relationships proved crucial during the downturn. Matrix's willingness to work on extended payment terms, accept partial payments, and restructure contracts helped customers manage their own cash crunches. This flexibility, while painful short-term, built loyalty that would pay dividends when spending resumed. Several major customers later acknowledged that Matrix's support during the crisis influenced future contract awards.

The crisis forced operational improvements that had been deferred during boom times. Project management systems were upgraded to provide real-time cost visibility. Procurement was centralized to leverage purchasing power. Safety programs were enhanced—accident rates declined even as financial pressure mounted. The company emerged leaner and more efficient, with lower breakeven points and improved margins on eventual recovery.

Government stimulus provided unexpected support. The American Recovery and Reinvestment Act included infrastructure spending that benefited Matrix indirectly. Utilities upgraded facilities using federal funds. States initiated water infrastructure projects. While not sufficient to offset energy sector declines, this work provided crucial revenue during the darkest period. Matrix's diversification beyond pure petroleum services proved its value.

By 2011, recovery signs emerged. Oil prices stabilized above $80 per barrel. Refineries resumed deferred maintenance. The shale revolution was gaining momentum, driving midstream infrastructure investment. Matrix had survived the worst downturn since its founding. The company was smaller—revenues had declined over 20%—but also stronger, with improved operations, deeper customer relationships, and less competition.

The acquisition of HDB Ltd. in 2013 signaled Matrix's return to growth mode. HDB specialized in turnaround services for California refineries, a market Matrix had struggled to penetrate. The acquisition provided immediate access to West Coast customers while adding specialized capabilities in environmental compliance—increasingly important as California regulations tightened. The integration proceeded smoothly, benefiting from lessons learned during previous combinations.

VII. The Energy Transition Pivot (2020-Present)

The year 2020 marked an inflection point far beyond the pandemic's immediate disruption. Oil prices briefly went negative. Major oil companies announced net-zero emissions targets. The incoming Biden administration promised massive clean energy investments. Electric vehicle adoption accelerated. For Matrix, whose heritage was building and maintaining fossil fuel infrastructure, these trends posed existential questions. Could a company rooted in oil tanks and refineries pivot to renewable energy? Was there a bridge from hydrocarbons to hydrogen?

Management's response was strategic rather than reactive. Instead of abandoning traditional markets—still generating the majority of revenue—Matrix identified transition opportunities leveraging existing capabilities. Storage tanks could hold renewable fuels. Construction expertise translated to utility-scale battery installations. Welding and fabrication skills applied equally to hydrogen pipelines and natural gas infrastructure. The company didn't need to reinvent itself, just redirect its competencies.

The hydrogen bet emerged as particularly significant. In 2021, Matrix signed a memorandum of understanding with Chart Industries to jointly pursue hydrogen infrastructure projects. Chart brought cryogenic expertise and equipment manufacturing capabilities. Matrix contributed construction, installation, and maintenance services. Together, they could offer complete hydrogen solutions from production to storage to distribution. The partnership addressed a critical challenge: building the physical infrastructure for hydrogen economy.

The company strengthened its hydrogen capabilities through strategic hiring. In 2022, Matrix recruited Camron Azadan as Director of Business Development. Azadan brought 25 years of experience across hydrogen, carbon capture, renewable fuels, ammonia, methanol, and LNG—essentially the entire alternative energy spectrum. His industry relationships and technical knowledge opened doors to projects Matrix couldn't previously pursue. The company also hired Mohamed Abdelaziz to focus on Eastern Canada's renewable energy market, recognizing that Canada's aggressive decarbonization targets created near-term opportunities.

LNG infrastructure became another growth driver. While liquefied natural gas wasn't renewable, it represented a transition fuel enabling coal-to-gas switching and providing backup for intermittent renewables. Matrix's expertise in cryogenic systems, developed through decades of working with petroleum products, translated directly to LNG facilities. The company secured contracts for utility peak-shaving facilities—crucial for grid reliability as renewable penetration increased.

The unexpected surge in data center construction created another opportunity. Artificial intelligence and machine learning required massive computational power, driving unprecedented electricity demand. Every major tech company was building or expanding data centers. These facilities needed robust power infrastructure—substations, transformers, backup generation, cooling systems. Matrix's utility and power infrastructure segment was perfectly positioned to capitalize on this demand.

Recent projects illustrated this evolution. Matrix constructed substations for renewable energy installations, connecting wind and solar farms to the grid. The company built battery storage facilities that helped utilities manage intermittent renewable generation. Teams installed hydrogen refueling infrastructure for transportation applications. While traditional refinery and terminal work continued, the project mix was shifting toward energy transition applications.

Financial performance, however, told a more complex story. Despite strategic positioning and market opportunities, Matrix struggled with profitability. Five-year average net margins were negative 4.38%, with trailing twelve months at negative 6.25%. Sales had declined 6.9% annually over the past five years. Project execution problems led to cost overruns. Competition for skilled labor drove wage inflation. The transition strategy was sound, but operational execution lagged.

The challenges were multifaceted. Energy transition projects often involved new technologies where Matrix lacked experience, leading to estimation errors and execution issues. Competition was intense, with everyone from traditional contractors to new renewable specialists chasing the same opportunities. Customers demanded fixed-price contracts despite technology uncertainty. The learning curve was steep and expensive.

Yet management remained optimistic, pointing to growing backlog and improving project selection. The Inflation Reduction Act had unleashed hundreds of billions in clean energy incentives. The Infrastructure Investment and Jobs Act funded grid modernization. Corporate renewable commitments drove private sector investment. Matrix was positioned at the intersection of policy support, capital availability, and infrastructure need. The question was whether they could execute profitably.

The company's recent earnings calls reflected this tension between opportunity and challenge. Executives highlighted billion-dollar market opportunities in hydrogen infrastructure, multi-gigawatt data center pipelines, and accelerating utility grid investments. But they also acknowledged margin pressure, working capital challenges, and the need for operational improvements. The energy transition pivot was underway, but success remained uncertain.

VIII. The Playbook: Lessons from an Industrial Services Roll-Up

Matrix's forty-year journey offers valuable lessons for understanding industrial services businesses, particularly those pursuing roll-up strategies. The playbook that emerged—through both successes and failures—provides insights relevant beyond the energy sector. These patterns appear repeatedly across fragmented industries where consolidation seems logical but execution proves challenging.

The roll-up strategy itself followed predictable logic. Fragmented markets with hundreds of small, regional players appeared ripe for consolidation. Larger scale would provide purchasing power, overhead leverage, and ability to serve national customers. Cross-selling would multiply revenue opportunities. Best practices could be shared across acquired units. Financial engineering would create value through multiple arbitrage. This thesis drove countless industrial services consolidations throughout the 1990s and 2000s.

Matrix's experience revealed both the potential and pitfalls of this approach. Successful acquisitions like Hake genuinely created value through capability enhancement and geographic expansion. The combined entity could pursue projects neither company could handle independently. Customer relationships deepened through broader service offerings. Operational improvements from shared best practices were real and measurable. When roll-ups worked, they created sustainable competitive advantages.

But failures were equally instructive. Some acquisitions never achieved projected synergies. Cultural clashes led to talent departures, destroying the human capital that justified the purchase. Integration costs exceeded budgets. IT systems proved incompatible. Customer relationships didn't transfer as expected. The graveyard of failed roll-ups is littered with companies that underestimated integration complexity.

Managing cyclicality emerged as perhaps the greatest challenge. Industrial services businesses are inherently tied to customer capital spending, which fluctuates with commodity prices, economic cycles, and regulatory changes. Matrix's history showed dramatic swings—boom years with record backlogs followed by busts with mass layoffs. Diversification across end markets (oil & gas, power, industrial) and service types (construction versus maintenance) provided some buffer but couldn't eliminate cyclical exposure.

The public market added another layer of complexity. Quarterly earnings pressure conflicted with long-term strategic building. Project-based revenue created volatility that markets punished. Small-cap industrial services companies traded at persistent discounts to larger competitors or private market valuations. Matrix's stock price often seemed disconnected from operational progress, frustrating management and limiting capital access.

Competition from private equity-backed players intensified these challenges. PE firms could pursue aggressive roll-ups without public market scrutiny. They could accept short-term losses while building scale. Their portfolio approach allowed risk-taking that public companies couldn't match. Matrix competed against PE-backed contractors who underbid projects to gain market share, knowing their investors would provide additional capital if needed.

The energy transition thesis represented evolution in the playbook. Rather than acquiring new capabilities, Matrix attempted to redirect existing competencies toward emerging markets. This approach was capital-efficient—avoiding expensive acquisitions—but required cultural change. Workers accustomed to refinery projects had to adapt to solar farms. Project managers experienced with petroleum products had to learn hydrogen properties. Sales teams comfortable with oil companies had to build relationships with utilities and tech companies.

Partnership strategies became increasingly important. The Chart Industries collaboration for hydrogen infrastructure exemplified this approach. Rather than acquiring hydrogen expertise, Matrix partnered with companies possessing complementary capabilities. These alliances provided market access without capital commitment. They also reduced technology risk by sharing development costs and expertise. For companies lacking scale to develop new capabilities independently, partnerships offered a viable path forward.

Workforce development emerged as a critical success factor often overlooked in financial analysis. Skilled trades—welders, pipefitters, electricians—were aging out of the workforce faster than replacements entered. Competition for experienced project managers was fierce. Safety professionals commanded premium wages. Matrix's ability to attract, train, and retain skilled workers determined project execution success more than strategic planning or financial engineering.

The lessons from Matrix's playbook extend beyond industrial services. Any business pursuing consolidation in fragmented markets faces similar challenges. The gap between strategic logic and operational execution is where value creation occurs or destroys. Success requires not just financial capital and strategic vision but also operational excellence, cultural sensitivity, and patience through inevitable cycles.

IX. Analysis: Porter's Five Forces & Hamilton's Seven Powers

Michael Porter's Five Forces framework reveals the challenging competitive dynamics facing Matrix Service Company. Starting with supplier power, the skilled labor shortage creates medium pressure on the business. Certified welders, experienced project managers, and specialized engineers are scarce resources commanding premium wages. Union contracts in certain regions further limit flexibility. Equipment and material suppliers have less leverage given multiple sourcing options, but specialized components for emerging technologies like hydrogen create new dependencies.

Buyer power presents high pressure that fundamentally shapes Matrix's economics. The customer base is highly concentrated—a handful of major energy companies, utilities, and industrial firms account for the majority of revenue. These sophisticated buyers run competitive bidding processes, demand fixed-price contracts despite project uncertainty, and possess internal capabilities to self-perform some work. Switching costs are low as buyers can easily move between contractors for new projects. Long-term relationships matter but don't prevent aggressive price negotiations.

The threat of new entrants rates low to medium. High capital requirements for equipment, bonding capacity, and working capital deter casual entry. Safety certifications, technical qualifications, and regulatory approvals create barriers. Established customer relationships and reputation take years to build. However, private equity interest in industrial services has funded new entrants with patient capital. International competitors also eye North American markets. Technology transitions like hydrogen create openings for specialized newcomers.

Substitute threats remain low for core services. Storage tanks require specialized construction and maintenance that can't be easily replaced. Refinery turnarounds demand expertise that owners typically don't maintain internally. However, technology evolution creates substitution risks—battery storage competing with traditional tank farms, modular construction replacing field fabrication, predictive maintenance reducing repair frequency. These substitutes don't eliminate need for contractors but might reduce market size.

Competitive rivalry is high and intensifying. The market remains fragmented despite decades of consolidation. Regional players compete aggressively on price. Larger contractors like Fluor, Jacobs, and KBR pursue the same major projects. Private equity-backed competitors accept lower margins to build market share. International entrants bring different cost structures. Differentiation is difficult in commodity services. Price-based competition compresses margins, especially during downturns when capacity exceeds demand.

Hamilton Helmer's Seven Powers framework provides another lens for assessing Matrix's competitive position. Scale economies are limited in this business. While larger contractors enjoy some purchasing power advantages and overhead leverage, most costs are variable—labor and materials for specific projects. Regional presence matters more than national scale for many customers. The project-based nature limits learning curve effects. Matrix's size provides some advantages but not insurmountable barriers for smaller competitors.

Network effects are essentially non-existent. Adding customers doesn't make Matrix more valuable to other customers. Contractors don't benefit from winner-take-all dynamics common in technology markets. Each project stands alone with independent economics. Market share doesn't create compounding advantages. This absence of network effects means Matrix must win each project on its own merits.

Counter positioning is weak as Matrix follows traditional service models. The company competes on execution, safety, and relationships rather than fundamental business model innovation. Digital tools and technology adoption are incremental improvements rather than revolutionary changes. Matrix hasn't discovered a new way of serving customers that incumbents can't replicate. The business model remains fundamentally similar to competitors.

Switching costs are medium, providing some competitive advantage. Multi-year maintenance contracts create continuity. Customer-specific training, safety qualifications, and facility knowledge take time to transfer. Project history and relationships matter for future work. However, these switching costs apply mainly to ongoing maintenance rather than new construction projects where competitive bidding resets the playing field.

Branding power is limited in B2B industrial services. Reputation matters tremendously, but Matrix lacks the brand recognition of larger competitors. Purchase decisions are made by procurement professionals evaluating technical capabilities and price rather than brand preference. Safety records and past performance influence selection but don't command pricing premiums. The Matrix brand has value within the industry but doesn't constitute a true power.

Cornered resources exist in the form of specialized workforce and certifications. Experienced project managers, skilled craftsmen, and technical experts are scarce. Certain certifications and qualifications take years to develop. Long-term customer relationships represent intangible assets. However, these resources aren't truly "cornered"—competitors can hire away talent, develop similar capabilities, and build comparable relationships given time and investment.

Process power shows the most promise but remains underdeveloped. Decades of project experience have created institutional knowledge about execution, safety, and problem-solving. Standardized procedures, lessons learned databases, and best practice sharing provide advantages. However, Matrix hasn't achieved the level of process excellence that would constitute a true competitive moat. Project execution issues and margin pressure suggest processes need improvement.

This analysis reveals Matrix's structural challenges. The company operates in an industry with unfavorable competitive dynamics—powerful buyers, intense rivalry, limited differentiation potential, and few sustainable competitive advantages. Success requires exceptional execution, efficient operations, and strategic positioning in growing market segments. The energy transition provides opportunity, but structural industry challenges remain.

X. Bear vs. Bull Case

The bear case for Matrix Service Company starts with persistent profitability challenges that suggest fundamental business model problems. Negative net margins averaging 4.38% over five years, worsening to 6.25% in recent quarters, indicate systematic execution issues rather than temporary setbacks. These aren't the margins of a healthy business navigating normal cycles but of a company struggling with core operations. Project cost overruns, competitive bidding pressure, and operational inefficiencies have destroyed shareholder value despite revenue growth in certain segments.

The highly cyclical nature of the business adds another layer of concern. Matrix's fortunes are inextricably tied to energy industry capital spending, which fluctuates wildly with commodity prices, regulatory changes, and macroeconomic conditions. Historical patterns show dramatic swings—boom periods followed by devastating busts requiring workforce reductions and survival mode operations. This cyclicality makes financial planning difficult, capital allocation challenging, and valuation problematic. Investors must accept that normalized earnings might never materialize.

Scale disadvantages versus larger competitors create structural challenges. Fluor, Jacobs, and KBR operate with resources Matrix can't match—deeper engineering capabilities, global reach, balance sheet strength to handle mega-projects, and relationships with decision-makers at major corporations. These giants win the most attractive projects while Matrix competes for smaller, more competitive work. The company is too large to be nimble like regional specialists but too small to compete effectively with industry leaders—stuck in an uncomfortable middle ground.

Execution risk on complex projects threatens future performance. Energy transition projects involve new technologies where Matrix lacks deep experience. Hydrogen infrastructure, utility-scale batteries, and carbon capture systems present technical challenges different from traditional tank construction. Fixed-price contracts in emerging technologies create enormous downside risk. One major project failure could wipe out years of profits. The company's recent track record of execution problems suggests these risks might materialize.

The timing and scale of energy transition opportunities remain highly uncertain. While politicians and companies announce ambitious targets, actual infrastructure investment depends on technology maturation, regulatory frameworks, and economic viability. Hydrogen infrastructure might develop slowly than expected. Traditional fossil fuel work could decline faster than renewable opportunities emerge. Matrix might be poorly positioned for a transition that unfolds differently than anticipated.

Perhaps most concerning, it's unclear whether the business model is fundamentally sustainable. Persistent losses despite revenue growth suggest structural problems. Competition for skilled labor is driving wage inflation faster than pricing power. Customers demand more for less—fixed prices, faster execution, additional services without compensation. Technology might reduce need for traditional contractors. The industry might be experiencing secular decline masked by cyclical fluctuations.

The bull case begins with powerful tailwinds from the Inflation Reduction Act and infrastructure spending. Hundreds of billions in federal incentives are driving clean energy investment. Tax credits make hydrogen projects economically viable. Grid modernization funding is flowing to utilities. This isn't speculative future spending but committed capital being deployed now. Matrix is positioned to capture this wave of infrastructure investment with existing capabilities and customer relationships.

The artificial intelligence data center boom presents massive power infrastructure opportunities. Every major technology company is expanding data center capacity. These facilities require sophisticated electrical infrastructure—substations, transformers, backup power systems, cooling equipment. Power demand is growing for the first time in decades. Matrix's utility and power infrastructure segment directly benefits from this secular growth trend that's independent of traditional energy cycles.

Matrix's early positioning in hydrogen infrastructure could prove prescient. The partnership with Chart Industries provides credibility and capabilities. Recent strategic hires bring necessary expertise. While hydrogen infrastructure remains nascent, early movers might capture dominant positions as the market develops. The company is building relationships, developing expertise, and completing initial projects that position it for larger opportunities ahead.

Strong backlog growth momentum suggests business improvement despite recent financial challenges. Backlog quality is improving with better project selection. Margins on new work exceed historical averages. Management has acknowledged past mistakes and implemented corrective actions. The company might be at an inflection point where operational improvements translate to financial performance.

Trading below replacement value creates asymmetric risk-reward. Building Matrix's capabilities from scratch—workforce, equipment, certifications, customer relationships—would cost far more than current enterprise value. Private equity buyers regularly pay higher multiples for similar industrial services businesses. Strategic acquirers might value Matrix's energy transition positioning. The stock price reflects past problems rather than future potential.

The verdict depends heavily on execution improvement. If management can fix operational issues, improve project selection, and capture margin expansion, the stock could appreciate significantly from depressed levels. But if execution problems persist, profitability remains elusive, and energy transition opportunities develop slowly, Matrix could remain a value trap. The key metrics to watch are gross margin recovery to 10%+ levels demonstrating operational improvement; backlog book-to-bill ratio sustainability indicating demand strength; and working capital management showing financial discipline.

XI. The Verdict: Infrastructure Play or Value Trap?

The Matrix Service Company story presents a classic investment dilemma: a business positioned in theoretically attractive markets but struggling with operational execution. The strategic logic appears sound—leveraging decades of industrial construction expertise to capture energy transition opportunities. The market tailwinds are real—federal infrastructure spending, data center buildout, and hydrogen development. Yet financial performance remains abysmal, raising fundamental questions about whether this is a timing issue or a broken business model.

The timing question cuts both ways. Matrix might be too early on the energy transition, investing in capabilities before markets mature. Hydrogen infrastructure could take a decade to develop at scale. Traditional fossil fuel work might decline faster than renewable opportunities grow. The company could face a painful transition period with elevated costs but limited revenue. Alternatively, Matrix might be perfectly positioned for an infrastructure super-cycle just beginning. Early struggles could be forgotten if the company captures even a small share of trillion-dollar infrastructure modernization.

Management's strategic vision deserves credit for recognizing industry evolution and attempting proactive transformation. The hydrogen partnership with Chart Industries was prescient. Strategic hires bring necessary expertise. The focus on power infrastructure aligns with AI-driven electricity demand. Leadership understands that standing still means slow death in a changing industry. However, vision without execution is hallucination. Cost overruns, project delays, and margin compression suggest management struggles with operational blocking and tackling.

Capital allocation priorities reveal the tension between growth and profitability. Should Matrix invest in capabilities for emerging markets that might not generate returns for years? Or focus on operational excellence in traditional markets even if they're declining? The company has tried to do both, resulting in neither growing sufficiently nor achieving acceptable profitability. Resource constraints force difficult choices. Every dollar spent on hydrogen capabilities is unavailable for safety improvements or working capital.

Government policy and infrastructure spending provide crucial support but also create dependencies. The Inflation Reduction Act drives current opportunities, but political winds shift. Infrastructure programs could be modified, delayed, or canceled. Matrix benefits from policy support today but remains vulnerable to political changes. Building a business dependent on government spending carries risks beyond management control.

The role of private equity looms large in any final assessment. Industrial services businesses with stable cash flows, improvement potential, and infrastructure exposure attract PE interest. Matrix's depressed valuation, strategic assets, and market position make it an attractive target. PE ownership could provide patient capital, operational expertise, and strategic flexibility that public markets don't allow. Alternatively, Matrix could be an acquirer, consolidating smaller competitors if access to capital improves.

For investors, Matrix represents a complex risk-reward proposition. The downside appears limited given the company trades below replacement value of its assets and capabilities. The upside could be substantial if operational improvements coincide with infrastructure spending acceleration. But the path between current struggles and future success requires execution improvements that have proven elusive. This is a turnaround story requiring patience, with no guarantee of success.

The infrastructure play versus value trap question doesn't have a clear answer. Matrix possesses real assets, capabilities, and market positions with genuine value. The company operates in markets with long-term growth potential driven by powerful trends. But persistent execution problems, competitive pressures, and financial challenges might prevent value realization. The business could remain perpetually cheap for good reasons.

Ultimately, Matrix Service Company embodies the challenges facing traditional industrial companies attempting transformation. The journey from oil tank repairs to hydrogen infrastructure requires more than strategic vision—it demands operational excellence, cultural change, and patient capital. Whether Matrix successfully navigates this transition or becomes another casualty of industrial evolution remains an open question. The next few years will determine if this forty-year-old company can reinvent itself for the next forty.

XII. Epilogue: What's Next for Matrix?

The data center infrastructure opportunity represents Matrix's most immediate and tangible growth driver. Major technology companies have announced hundreds of billions in AI infrastructure investments over the next five years. Each data center requires 50-100 megawatts of power—equivalent to small cities. The electrical infrastructure needed—substations, transformers, distribution equipment, backup generation—aligns perfectly with Matrix's capabilities. Unlike hydrogen infrastructure that remains speculative, data center projects are breaking ground today with committed capital and aggressive timelines.

Matrix's recent wins in this space suggest early traction. The company has secured substation construction projects for several major data center developments. These projects are larger and more complex than traditional utility work, with better margins given the urgency and technical requirements. Data center owners prioritize speed and reliability over lowest cost, potentially improving Matrix's pricing power. The company's geographic presence in key data center markets—Virginia, Texas, Arizona—provides competitive advantages.

The hydrogen infrastructure buildout timeline remains uncertain but potentially transformative. The Department of Energy has designated regional hydrogen hubs with billions in funding. Major industrial companies are planning hydrogen production facilities. Transportation applications are emerging with hydrogen fueling stations for trucks and buses. Matrix's partnership with Chart Industries positions the company to capture construction and maintenance work as projects move from planning to execution. Early projects are small, but each success builds expertise and references for larger opportunities.

The M&A question—whether Matrix becomes buyer or seller—will likely be answered within the next 24 months. As a potential seller, Matrix offers strategic value to larger contractors seeking energy transition capabilities, skilled workforce, and customer relationships. Private equity buyers might see opportunity to improve operations and consolidate regional competitors. Strategic alternatives could unlock shareholder value given the discount to private market comparisons.

As a potential buyer, Matrix could consolidate struggling regional competitors at attractive prices. Distressed assets might become available during the next downturn. Acquiring specialized capabilities—renewable energy construction, battery storage expertise, carbon capture technology—could accelerate transformation. However, Matrix's financial constraints and integration track record suggest organic growth might be preferable to acquisitions.

The path back to profitability requires multiple improvements simultaneously. Project selection must improve, avoiding low-margin competitive work. Execution must tighten, eliminating cost overruns that destroy margins. Overhead needs optimization without sacrificing capabilities. Working capital management must improve to generate cash for growth investments. These aren't revolutionary changes but blocking and tackling that determines success in project-based businesses.

Industry evolution will reshape competitive dynamics regardless of Matrix's specific actions. Modular construction and prefabrication will reduce field labor requirements. Digital tools will improve project planning and execution. Predictive maintenance will change service models. Automation will affect workforce needs. Companies that adapt to these changes will thrive; those that don't will struggle. Matrix must balance investing in new capabilities while maintaining current operations.

The lessons for industrial services investors are sobering but valuable. Industry structure matters more than individual company strategy. Competitive dynamics, customer power, and cyclicality create permanent challenges. Roll-up strategies are harder to execute than financial models suggest. Energy transition creates opportunities but also risks for incumbent players. Operational execution trumps strategic positioning. Patient capital is essential for transformation success.

The American infrastructure challenge extends far beyond Matrix's specific situation. Decades of underinvestment have created massive modernization needs. Energy transition requires rebuilding fundamental systems. Skilled labor shortages threaten execution capacity. The companies that build and maintain critical infrastructure face enormous opportunities but also structural challenges. Matrix's struggles and potential recovery illustrate broader issues facing American industrial capabilities.

Looking ahead, Matrix Service Company stands at a critical juncture. The company possesses valuable assets and capabilities. Market opportunities are expanding. Federal support provides tailwinds. But execution challenges persist. Competition remains intense. The path forward requires operational excellence that has proven elusive. Success isn't guaranteed, but neither is failure.

XIII. Outro & Resources

Matrix Service Company's forty-year journey from a Tulsa garage to a publicly traded industrial services company offers profound lessons for founders, investors, and students of American business. The story demonstrates that timing, while important, isn't everything—the founders started during an oil bust yet built a sustainable business. It shows that strategic vision must be matched by operational excellence—Matrix's energy transition positioning means nothing without profitable execution. Most importantly, it illustrates that industrial businesses, unlike software companies, can't escape physical realities—skilled labor, safety requirements, weather delays, and equipment failures.

For founders considering industrial services businesses, Matrix's history provides both inspiration and caution. The opportunities are real—America's infrastructure needs massive investment, creating decades of potential work. But the challenges are equally real—cyclical demand, powerful customers, intense competition, and operational complexity. Success requires patient capital, strong relationships, exceptional execution, and willingness to endure brutal cycles. This isn't a space for quick exits or hockey-stick growth curves.

Investors analyzing industrial services companies should focus on several key factors that Matrix's experience highlights. Industry structure and competitive dynamics matter more than strategic plans. Operational metrics—safety rates, project margins, working capital turns—predict performance better than backlog growth. Management's industry experience and relationships are crucial. Balance sheet strength determines survival during downturns. Valuation must reflect cyclical earnings rather than peak performance.

Understanding American infrastructure requires appreciating both its scale and fragility. The storage tanks Matrix maintains hold strategic petroleum reserves and commercial inventory crucial for economic functioning. The refineries they service produce transportation fuels powering commerce. The power infrastructure they build keeps lights on and data centers running. These industrial systems, largely invisible until they fail, underpin modern society. Companies like Matrix, despite their challenges, perform essential functions.

The energy transition adds complexity to infrastructure investing. Traditional fossil fuel infrastructure won't disappear overnight—refineries will operate for decades, pipelines will transport hydrogen, storage tanks will hold renewable fuels. But new infrastructure must be built simultaneously—hydrogen production facilities, electric vehicle charging networks, grid-scale batteries. Companies positioned at this intersection, capable of maintaining legacy systems while building new ones, could thrive. Execution capability matters more than strategic positioning.

Three critical metrics deserve particular attention when evaluating Matrix going forward. First, gross margin recovery to 10%+ levels would signal operational improvement and better project selection. This isn't just about profitability but about demonstrating execution capability essential for long-term success. Second, backlog book-to-bill ratio sustainability above 1.0x indicates demand strength and commercial momentum. Quality matters as much as quantity—high-margin strategic projects rather than low-bid commodity work. Third, working capital management, particularly days sales outstanding and project billing milestones, reveals financial discipline and cash generation capability.

The broader implications extend beyond Matrix to American industrial competitiveness. The skilled trades workforce is aging without sufficient replacement. Technical education has been de-emphasized in favor of four-year degrees. Industrial companies struggle to attract talent compared to technology firms. Yet building energy infrastructure, maintaining critical facilities, and enabling economic growth requires these capabilities. Matrix's workforce challenges mirror national problems requiring systemic solutions.

Recommended reading for deeper understanding includes "The Prize" by Daniel Yergin for historical context on energy infrastructure development. "Barbarians at the Gate" provides insights into financial engineering and corporate transformation challenges. Hamilton Helmer's "7 Powers" offers frameworks for evaluating competitive advantage. Porter's "Competitive Strategy" remains essential for industry analysis. For specific infrastructure insights, the American Society of Civil Engineers' Infrastructure Report Card provides sobering assessment of investment needs.

The Matrix story continues to unfold. Whether the company successfully transforms from traditional industrial services to energy transition enabler remains uncertain. But the attempt itself is noteworthy—a forty-year-old company trying to reinvent itself for changing markets. Success would validate the transformation potential of American industrial companies. Failure would illustrate the difficulty of escaping industry structure and operational challenges.

For all stakeholders—employees betting careers, investors allocating capital, customers depending on critical infrastructure—Matrix Service Company represents more than a stock ticker or contractor. It embodies the challenges and opportunities facing American industrial companies in an era of energy transition, infrastructure modernization, and technological change. The company's next chapter will be written by its ability to execute in present while positioning for the future—a balance that has proven elusive but remains possible.

The question that opened this analysis—can an oil tank maintenance company transform into an energy transition powerhouse—remains unanswered. But the journey toward that answer, with all its complexity, challenges, and possibilities, offers valuable insights for anyone seeking to understand American industrial businesses, infrastructure challenges, and the messy reality of corporate transformation. Matrix's story, still being written, reminds us that building and maintaining the physical world requires more than strategy and capital—it requires people willing to do difficult work in challenging conditions to keep critical systems functioning.

Based on the recent financial reports, Matrix Service Company's fiscal 2025 performance reflects the ongoing challenges discussed throughout this analysis. In the second quarter of fiscal 2025 ended December 31, 2024, Matrix reported revenue of $187.2 million, compared to $175.0 million in the fiscal second quarter of 2024, showing modest growth. However, the company had a net loss of $5.5 million, or $(0.20) per share, compared to a net loss of $2.9 million, or $(0.10) per share, in the second quarter of fiscal 2024, indicating widening losses despite revenue increases.

The segment performance reveals divergent trends that align with the energy transition thesis. Storage and Terminals Solutions segment revenue increased 53% to $95.5 million in the second quarter of fiscal 2025 compared to $62.4 million in the second quarter of fiscal 2024, due to increased volume of work for specialty vessel and LNG storage. Similarly, Utility and Power Infrastructure segment revenue increased 52% to $61.1 million in the second quarter of fiscal 2025 compared to $40.1 million in the second quarter of fiscal 2024, benefiting from a higher volume of work associated with LNG peak shaving projects. These segments directly benefit from energy infrastructure modernization and data center construction trends.

Conversely, Process and Industrial Facilities segment revenue decreased to $30.6 million in the second quarter of fiscal 2025 compared to $71.3 million in the second quarter of fiscal 2024, primarily due to lower revenue volumes resulting from the completion of a large renewable diesel project. This lumpy project-based revenue demonstrates the volatility inherent in industrial services businesses.

The company's liquidity position remains manageable but constrained. As of December 31, 2024, MTRX had total liquidity of $211.7 million, comprising $156.8 million in unrestricted cash and $54.9 million in borrowing availability. This provides sufficient runway for operations but limits strategic flexibility for major investments or acquisitions.

Management's outlook adjustment reveals execution challenges. MTRX lowered its full-year revenue forecast by approximately 5% due to temporary permitting and project start delays, pushing about $50 million in projected revenue from FY2025 to FY2026. These delays, while characterized as temporary, highlight the unpredictability of project timing that complicates financial planning and investor confidence.

XIV. Final Thoughts: The Infrastructure Paradox

Matrix Service Company embodies a fundamental paradox of American infrastructure investment. The need for services the company provides has never been greater—aging energy infrastructure requires maintenance, new data centers demand power systems, hydrogen economy needs physical facilities. Yet converting this demand into profitable business remains elusive. The disconnect between market opportunity and financial performance suggests structural industry issues beyond Matrix's specific challenges.

The workforce crisis looms as perhaps the greatest long-term threat. Skilled trades workers are retiring faster than replacements enter the field. Young workers prefer technology careers over industrial construction. Immigration restrictions limit foreign worker availability. Matrix and competitors compete fiercely for a shrinking pool of qualified personnel, driving wage inflation that customers resist paying through higher project prices. Without addressing this human capital challenge, even the best strategies will fail.

Technology adoption offers potential solutions but requires investment the company can ill afford. Digital twins for project planning, drone inspections for safety monitoring, modular construction techniques, and predictive maintenance algorithms could improve efficiency and margins. But implementing these technologies demands capital, training, and cultural change—resources stretched thin when fighting for quarterly survival. The companies that successfully digitize industrial services will likely be those with patient capital and long-term horizons.

The role of government policy in shaping Matrix's future cannot be overstated. Infrastructure spending bills, clean energy incentives, and regulatory frameworks determine project viability. The company benefits from current federal support but remains vulnerable to political shifts. Building a business dependent on government largesse creates inherent instability, yet the scale of infrastructure needs exceeds private sector capacity alone. This public-private tension will persist regardless of which party controls Washington.

For investors evaluating Matrix, the company represents a complex option on American infrastructure renewal. The current stock price appears to reflect pessimism about execution and profitability. Any operational improvement could drive significant appreciation from depressed levels. But structural challenges—customer concentration, cyclical exposure, competitive intensity—limit upside potential even in optimistic scenarios. This isn't a simple turnaround story but a fundamental business model question.

The broader implications extend beyond Matrix to American industrial competitiveness. If established contractors struggle to profitably build and maintain critical infrastructure, who will? Foreign competitors might fill the gap, creating national security concerns. Government might need to directly fund infrastructure development, reducing efficiency. The struggles of companies like Matrix signal deeper issues about America's ability to execute physical projects in an increasingly digital economy.

Matrix's management faces difficult choices with no perfect solutions. Focusing on operational excellence in traditional markets might improve near-term profitability but risks missing energy transition opportunities. Aggressive investment in new capabilities could position for future growth but might exhaust financial resources before benefits materialize. The middle path—gradual transition while maintaining core business—has produced neither growth nor profitability.

Partnership strategies might offer the best path forward. Rather than acquiring capabilities or developing them internally, Matrix could form joint ventures with technology providers, equipment manufacturers, and specialty contractors. These alliances would share risks, combine complementary strengths, and provide market access without massive capital requirements. The Chart Industries hydrogen partnership exemplifies this approach, though execution remains unproven.

The data center opportunity deserves particular attention given its near-term visibility and alignment with Matrix's capabilities. Unlike hydrogen infrastructure that remains speculative, data centers are breaking ground today with committed capital. The power requirements are staggering—major technology companies need gigawatts of capacity for AI computing. Matrix's experience with electrical infrastructure, substation construction, and utility interconnection provides competitive advantages. Success in this market could stabilize finances while the company navigates energy transition uncertainties.

Environmental, social, and governance considerations increasingly influence industrial services companies. Matrix's safety record, workforce diversity, and environmental practices affect customer selection decisions and investor interest. Matrix ranks among the Top Contractors by Engineering-News Record, has been recognized for its Board diversification, is an active signatory to CEO Action for Diversity and Inclusion, and is recognized as a Great Place to Work®. These credentials matter for winning projects from corporations with their own ESG commitments.

The international dimension adds complexity. Matrix operates through subsidiaries with offices located throughout the United States and Canada, as well as Sydney, Australia, and Seoul, South Korea. This geographic diversity provides growth opportunities but also operational challenges. Managing international operations requires additional expertise, regulatory compliance, and cultural sensitivity. The company must balance global reach with local execution excellence.

Looking forward, Matrix Service Company's survival and success depend on factors both within and beyond management control. Operational execution must improve—there's no substitute for completing projects on time, on budget, and safely. Financial discipline needs strengthening to generate cash for growth investments. Strategic focus should sharpen, perhaps accepting smaller ambitions but better execution. These internal improvements are necessary but might not be sufficient given industry dynamics.

The ultimate question remains whether Matrix can transform from a traditional industrial services contractor to an energy infrastructure enabler for the 21st century. The company's history demonstrates resilience through multiple cycles and strategic pivots. Current challenges are severe but not necessarily terminal. With improved execution, strategic partnerships, and favorable market conditions, Matrix could emerge stronger. Without these elements aligning, the company might become another casualty of industrial evolution.

For stakeholders—employees whose livelihoods depend on Matrix's success, investors allocating capital, customers relying on critical infrastructure, communities hosting facilities—the company's trajectory matters beyond financial returns. Matrix Service Company represents thousands of American industrial businesses facing similar transitions. Their collective success or failure will determine whether America can build the physical infrastructure necessary for economic competitiveness, energy security, and technological leadership in the decades ahead.

The story that began in a Tulsa garage forty years ago continues to unfold. Whether Matrix Service Company successfully navigates from petroleum tanks to hydrogen infrastructure, from refinery turnarounds to data center construction, from industrial past to energy future, remains unwritten. The challenges are formidable, the opportunities are real, and the outcome remains uncertain. What is certain is that America needs companies capable of building and maintaining critical infrastructure, and the struggles of Matrix Service Company illuminate just how difficult that task has become.

XIV. Recent Performance: Q3 2025 and the Guidance Adjustment

The third quarter of fiscal 2025 ended March 31, 2025 brought both progress and challenges. Matrix reported revenue of $200.2 million, up 21% year-over-year, while reducing net loss to $(0.12) per share from $(0.53) in the prior year period. The improvement suggested operational progress despite persistent profitability challenges. Total backlog reached $1.4 billion, increasing 7.7% from Q2 FY2025, with quarterly project awards of $301.2 million resulting in a strong 1.5x book-to-bill ratio, indicating healthy demand for the company's services.

Segment performance revealed the divergent dynamics within Matrix's portfolio. The Storage & Terminal Solutions segment saw significant growth with a 77% revenue increase, while Utility & Power Infrastructure grew 27%. These segments benefited directly from the infrastructure spending and energy transition trends discussed throughout this analysis. However, Process and Industrial Facilities revenue declined, reflecting the lumpy nature of project-based work and the completion of major renewable diesel projects without immediate replacements.

Cash generation showed marked improvement. Net cash provided by operating activities during the three months ended March 31, 2025 was $31.2 million and primarily reflects scheduled payments from customers associated with active projects in backlog. As of March 31, 2025, Matrix had total liquidity of $247.1 million. Liquidity is comprised of $185.5 million of unrestricted cash and cash equivalents and $61.5 million of borrowing availability under the credit facility. The company also has $25.0 million of restricted cash to support the facility. As of March 31, 2025, we had no outstanding debt. This financial position provides crucial flexibility as the company navigates its transformation.

The most significant development was management's decision to adjust fiscal 2025 revenue guidance. Matrix Service Co (NASDAQ:MTRX) revised its fiscal 2025 revenue guidance down by 10% to $770 to $800 million due to exiting the transmission and distribution business. The company also cited the timing of project awards and macroeconomic uncertainties. A major project expected in Q2 was delayed, impacting revenue. While disappointing, the guidance still represented growth from fiscal 2024 levels and reflected management's more conservative approach to forecasting.

The decision to exit certain business lines demonstrated strategic discipline. The Northeast transmission and distribution service line exit was due to competitive disadvantages and high capital investment needs. The business was not winning projects at acceptable margins, leading to the decision to wind it down. The company will sell off construction assets and continue small contracts with existing clients. The business was operating at a loss, so exiting will save costs and allow resource reallocation. This pruning of unprofitable operations aligned with the focus on higher-margin opportunities in growth markets.