MRPL: The Refinery That Rode India's Energy Wave

I. Introduction & Episode Setup

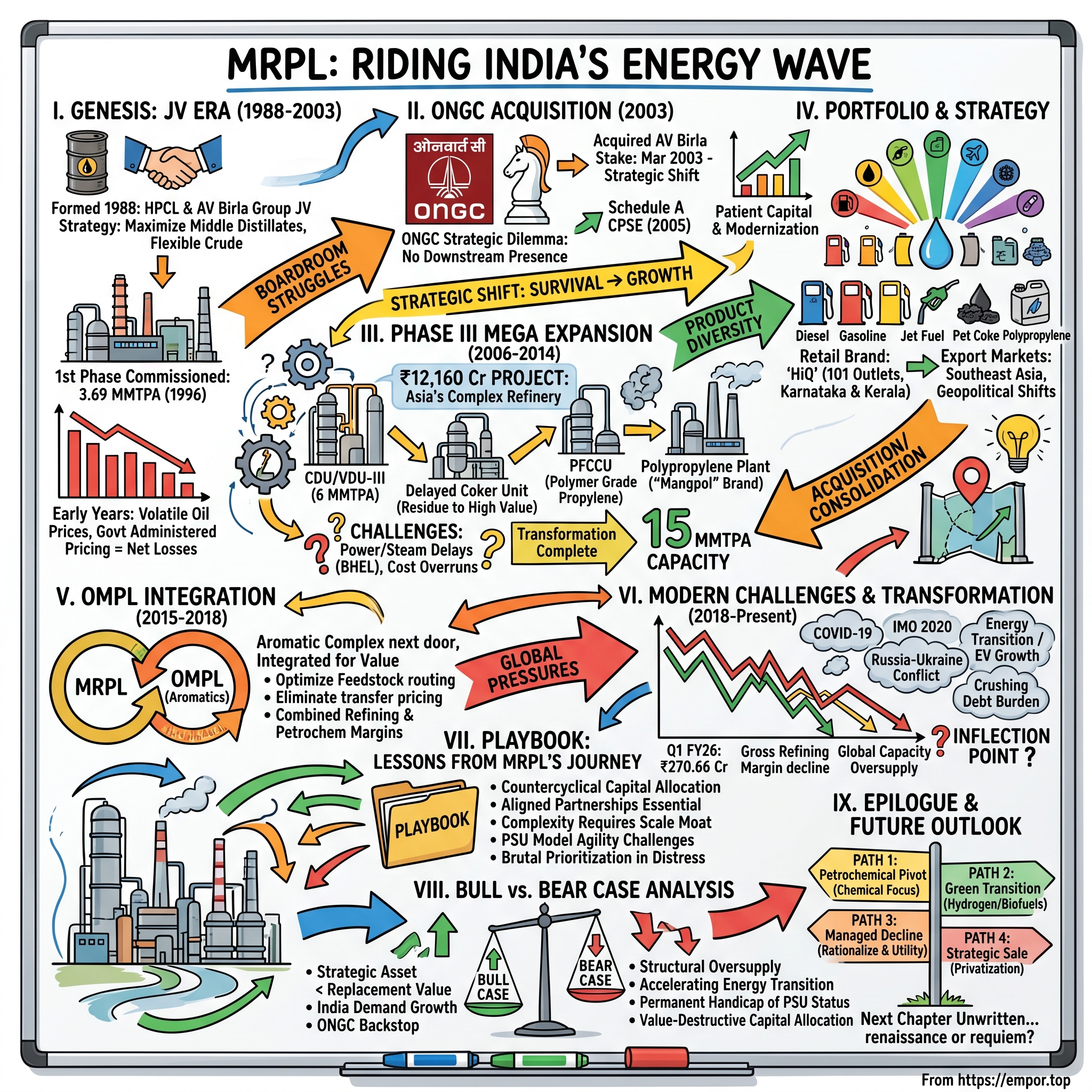

Picture this: It's March 1996, and in the coastal town of Katipalla, just north of Mangalore, a massive industrial complex springs to life. Five villages—Bala, Kalavar, Kuthetoor, Katipalla, and Adyapadi—have made way for what would become one of India's most sophisticated refineries. The first drops of crude oil begin their transformation journey through gleaming distillation columns. This is the birth of Mangalore Refinery and Petrochemicals Limited, or MRPL—a company that would ride the waves of India's energy ambitions for nearly three decades.

Today, MRPL stands as a Category 1 schedule 'A' Miniratna, Central Public Sector Enterprise under the Ministry of Petroleum & Natural Gas, operating a 15 Million Metric Tonne refinery with versatile design and complex secondary processing units. With a market cap of ₹21,583 crore, the company processes crude from 38 different sources worldwide, manufactures everything from bitumen to polypropylene, and runs 101 retail outlets across Karnataka and Kerala under its HiQ brand.

But here's the central question that drives our story: How did a joint venture refinery conceived in the late 1980s—born from the partnership of a public sector oil company and a private industrial house—transform into India's strategic energy asset? And perhaps more intriguingly, why is this once-profitable enterprise now facing its most challenging period, with a net loss of ₹270.66 crore in Q1 FY26?

The MRPL story is really three stories woven together. First, it's a tale of India's post-liberalization energy ambitions—how a nation dependent on oil imports sought to build refining capacity that could process the world's most challenging crudes. Second, it's a case study in public-private partnerships gone awry, leading to one of India's largest oil companies stepping in as a white knight. And third, it's a cautionary tale about timing, capital allocation, and the perils of expansion in commodity businesses.

Over the next few hours, we'll trace MRPL's journey from its inception as a joint venture between HPCL and the AV Birla Group, through its acquisition by ONGC, its ambitious Phase III expansion that pushed capacity to 15 million tonnes, and its current struggles amid global margin pressures and energy transition headwinds. We'll explore how a refinery that is the only one in India to have two hydrocrackers producing premium diesel finds itself battling for survival in an increasingly competitive market.

This isn't just another corporate history—it's a window into India's energy security strategy, the complexities of running capital-intensive businesses under government ownership, and the challenges traditional refiners face as the world pivots toward cleaner energy. So let's begin where all great industrial stories start: with a vision, a partnership, and the promise of transforming raw crude into the lifeblood of a growing economy.

II. Genesis: The Joint Venture Era (1988-2003)

The late 1980s in India were a time of contradictions. The economy was still largely closed, but whispers of liberalization were growing louder. In boardrooms across Mumbai and Delhi, industrialists and bureaucrats alike recognized a fundamental problem: India's refining capacity was woefully inadequate for its ambitions. Enter two unlikely partners with a shared vision.

MRPL was set up in 1988 as a joint venture oil refinery promoted by HPCL, a public sector company, and Indian Rayon & Industries Limited (IRIL) of the AV Birla Group, with an initial processing capacity of 3.0 million metric tonnes per annum. The partnership made strategic sense—HPCL brought petroleum sector expertise and market access, while the Birla Group brought private sector efficiency and capital mobilization capabilities.

The location choice was no accident. Mangalore offered proximity to the Arabian Sea for crude imports, a natural harbor at New Mangalore Port, and enough land for future expansion. But progress came at a cost. The refinery was established after displacing five villages: Bala, Kalavar, Kuthetoor, Katipalla, and Adyapadi. Hundreds of families had to relocate, their agricultural lands transformed into an industrial landscape of towers, pipes, and storage tanks.

The technical ambition was remarkable for its time. The refinery was conceived to maximise middle distillates, with the capability to process light to heavy and sour to sweet crudes with 24 to 46 API gravity. This flexibility would prove to be MRPL's greatest strength in the decades to come. Unlike refineries designed for specific crude types, MRPL could switch between different grades based on economics and availability—a crucial advantage in volatile oil markets.

Construction began in the early 1990s, but like many infrastructure projects of that era, it faced delays. The company went public in 1993 with a massive issue, raising funds through secured redeemable partly convertible debentures worth ₹582.66 crores and non-convertible debentures worth ₹560 crores. The capital markets response was lukewarm—India's equity culture was still nascent, and industrial projects were viewed with skepticism.

Finally, the 1st phase of the Refinery of capacity 3.69 MMTPA was commissioned in 1996. The facility included a crude distillation unit, vacuum distillation unit, and basic secondary processing capabilities. But even as the first phase came online, management knew they needed scale to compete. In 1999, MRPL commissioned the second phase and increased the Refining capacity to 9.69 MMTPA.

The early operational years were brutal. Global oil prices were volatile, ranging from $10 to $30 per barrel through the 1990s. Refining margins—the spread between crude costs and product prices—were thin. The Indian government's administered pricing mechanism meant MRPL couldn't fully pass on cost increases to consumers. The company bled money year after year.

By 2002, cracks in the partnership had become chasms. The AV Birla Group, facing its own financial pressures and seeing no path to profitability for MRPL, wanted out. HPCL lacked the resources for a buyout. The refinery, with nearly 10 million tonnes of capacity, modern equipment, and strategic coastal location, needed a savior.

III. The ONGC Acquisition: Strategic Shift (2003)

The boardroom at ONGC's Dehra Dun headquarters buzzed with tension in early 2003. India's largest oil exploration company was flush with cash from high crude prices but faced a strategic dilemma. While ONGC excelled at finding and extracting oil, it had no downstream presence—no refineries, no petrochemical plants, no direct access to consumers. Every barrel of crude it produced was sold to other refiners who captured the value addition.

The opportunity at MRPL was tantalizing but risky. Here was a modern refinery with expansion potential, but also one that had never turned a sustainable profit. The due diligence reports painted a mixed picture: excellent assets, strategic location, but serious financial stress and operational challenges.

On 28 March 2003, ONGC acquired A.V. Birla Group's stake and further infused equity capital of ₹600 crore, making MRPL a majority-owned subsidiary of ONGC, enabling it to embark on a path of modernization, capacity enhancement, and operational excellence. The deal structure was complex—beyond the equity infusion, lenders agreed to a debt restructuring package that included conversion of up to ₹3,65,54,884 of the company's loans into equity.

The transformation under ONGC wasn't immediate, but it was methodical. New management systems were installed. Operational inefficiencies were identified and eliminated. Most importantly, ONGC provided something MRPL had always lacked: patient capital and a long-term vision. The new parent company wasn't looking for quick returns—it wanted to build India's most sophisticated refinery.

The integration revealed interesting synergies. ONGC's Mumbai High crude, with its specific characteristics, was perfectly suited for MRPL's configuration. Transportation costs dropped as ONGC could now move crude directly from its offshore platforms to its own refinery. The combined entity could negotiate better terms with international crude suppliers.

By 2005, MRPL was designated a Schedule A CPSE, recognizing its turnaround and strategic importance. The company finally started reporting modest profits, helped by rising global refining margins and better capacity utilization. But ONGC's ambitions for MRPL went far beyond just stabilizing operations.

Internal strategy documents from this period reveal the grand vision: transform MRPL from a simple refinery into an integrated refining and petrochemical complex. The plan called for massive capacity expansion, addition of sophisticated secondary units that could convert low-value residues into high-value products, and eventual integration with petrochemical production.

The board approved a phased approach. First, stabilize existing operations and improve reliability. Second, undertake debottlenecking to squeeze more capacity from existing units. Third, and most ambitiously, launch a Phase III mega-expansion that would add another 6 million tonnes of capacity plus complex upgrading units.

This strategic shift from survival to growth marked a fundamental change in MRPL's trajectory. No longer was it just another mid-sized refinery struggling to stay afloat. Under ONGC's ownership, it was being positioned as a national strategic asset—a refinery that could process the most challenging crudes, produce the cleanest fuels, and eventually integrate into high-value petrochemicals.

IV. Building Complexity: Phase III Mega Expansion (2006-2014)

The year 2010 opened with oil prices hovering around $80 per barrel and India's GDP growing at 8.5%. In MRPL's Mangalore offices, project teams worked around the clock finalizing what would become one of India's most ambitious refinery expansions. The Phase III project wasn't just about adding capacity—it was about fundamentally transforming MRPL into one of Asia's most complex refineries.

The numbers were staggering: ₹12,160 crore project cost, funded through a 2:1 debt-equity ratio. The expansion would increase capacity from 9.69 to 15 MMTPA while adding secondary units that could crack, reform, and upgrade every molecule of crude into valuable products. The technical scope included a new crude distillation unit, vacuum distillation unit, delayed coker unit, petrochemical fluid catalytic cracking unit (PFCCU), and India's first integrated polypropylene plant within a refinery complex.

As of September 1, 2012, MRPL achieved an overall progress of 96.5 per cent in Phase III project. The crude unit came first—CDU/VDU-III commissioned on March 29, 2012, adding 6 million tonnes of primary distillation capacity. But this was just the beginning of a complex orchestration of industrial commissioning.

The real game-changer was the delayed coker unit (DCU). In April 2014, MRPL commissioned the 3.00 MMTPA Delayed Coker Unit, which converts short residue (bottoms), a low value product, into high value products like Gasoil, Naphtha, and LPG. The technology, supplied by Lummus Technology, operates with four drums and two heaters, allowing continuous operation through batch processing.

But the commissioning wasn't smooth. A sustained unavailability of steam and power from a captive power plant at the refinery site delayed the coker's start-up. The power plant, being built by BHEL, became the project's Achilles heel. As of January 15, 2014, overall project progress reached 99.50%, with work progress of CPP by BHEL continuing to be a major factor for delayed commissioning.

The PFCCU represented another technological leap. MRPL's PFCCU, with design capacity of 2.2 MMTPA, is the second such unit in the country and can produce about 20% of its product as polymer grade propylene apart from almost 25% as LPG. When it achieved feed-cut on August 27, 2014, MRPL could finally produce the propylene feedstock for its polypropylene plant.

The polypropylene unit itself was a marvel of integration. Commissioned in June 2015 with an annual production capacity of 440 KTPA, it used technology from Novolen, Germany, with two reactors and single extruder. The plant could produce the entire range of homopolymer grades, marketed under the brand name "Mangpol."

What made Phase III special wasn't just individual units but their integration. Vacuum gasoil from the crude unit fed the hydrocracker. Naphtha went to the catalytic reformer to produce high-octane gasoline. Heavy residue entered the delayed coker, which sent coker gasoil back to the hydrocracker and coker naphtha to the PFCCU. The PFCCU produced propylene for the polypropylene plant. Every stream had a destination, every molecule was upgraded.

The human drama behind these technical achievements was intense. Engineers worked 18-hour days. Specialists from licensors—UOP, Lummus, Technip, Axens—flew in from Houston, Paris, and Amsterdam. The Mangalore summer heat made work inside units unbearable, yet commissioning deadlines couldn't slip. When the BHEL power plant failed to deliver steady steam, the entire commissioning schedule had to be rewritten.

Cost overruns mounted. The original budget ballooned as equipment prices rose, contractor claims piled up, and delays triggered penalty clauses. By project completion, actual costs exceeded initial estimates by nearly 20%. Yet when the last unit came online, MRPL had achieved something remarkable: it now operated the only refinery in India with two hydrocrackers, could process the sourest, heaviest crudes available, and had flexibility to shift product slate based on market demand.

The transformation was complete. From a simple topping refinery in 1996, MRPL had evolved into one of Asia's most sophisticated refining complexes. But as management would soon discover, building complexity is one thing—making it profitable is another challenge entirely.

V. Product Portfolio & Market Strategy

Step inside MRPL's sprawling Katipalla complex today, and you'll encounter an industrial symphony—crude oil entering from the sea through a single point mooring, flowing through a maze of units, emerging as dozens of distinct products. This product diversity isn't accidental; it's the result of deliberate strategic choices made over two decades.

The product slate reads like a petroleum dictionary: Naphtha, LPG, Motor Spirit, High-Speed Diesel, Kerosene, Aviation Turbine Fuel, Sulphur, Xylene, Bitumen, Pet Coke, and Polypropylene. But MRPL's real differentiation lies in its ability to produce specialty grades. The two hydrocrackers produce premium diesel with high cetane numbers—crucial for meeting India's evolving emission norms. The aromatics complex churns out 0.905 MMTPA of Para Xylene and 0.273 MMTPA of Benzene, essential petrochemical building blocks.

The market strategy evolved significantly post-ONGC acquisition. Initially, MRPL operated as a merchant refiner, selling products to oil marketing companies who handled retail distribution. But management recognized that direct market access could capture additional margins and provide demand visibility.

Enter 'HiQ'—MRPL's retail brand launched in the late 2010s. The company entered the retail fuel service stations business under the brand 'HiQ', and as of FY24, has a network of 101 retail outlets across Karnataka and Kerala. The brand positioning was deliberate: "High Quality" fuel and service, targeting quality-conscious consumers willing to pay a premium for assured quality.

The retail expansion followed a calculated geographic strategy. With 72 retail outlets in Karnataka and 28 in Kerala, MRPL focused on markets where it had supply chain advantages. The April 2024 milestone was particularly symbolic—MRPL commissioned its 100th HiQ retail outlet in Yeliyur of Sira, Tumkur District, incidentally named "Century Fuel Services".

But retail was just one piece of the market puzzle. MRPL's ability to process diverse crudes—from light to heavy, sweet to sour, across a wide API gravity range of 24° to 46°—became a significant competitive advantage. When Middle Eastern crudes became expensive, MRPL could switch to Latin American heavy crudes. When Venezuelan supplies were sanctioned, it could process Russian Urals. This flexibility meant MRPL could optimize its crude basket based on global price differentials.

The export market became increasingly important. MRPL's coastal location and jetty infrastructure allowed easy access to international markets. When domestic demand softened, products could be redirected to Southeast Asian markets. During periods of high global prices, exports provided crucial margin uplift.

The polypropylene business deserves special attention. MRPL's 440 KTA Novolen gas-phase plant can produce the complete range of homopolymer grades, with a solvent-free process featuring dual parallel reactors capable of making bimodal molecular weight distribution PP grades. The "Mangpol" brand competed directly with established players like Reliance and Haldia, focusing on consistent quality and technical support to build market share.

Aviation turbine fuel (ATF) became another strategic focus. Shell MRPL Aviation Fuels and Services Limited, a 50:50 joint venture between MRPL and Shell Gas B.V., markets ATF to airlines, both domestic and international carriers. The JV leverages Shell's global aviation network while providing MRPL assured offtake for its ATF production.

Geographic advantages multiplied over time. The Mangalore location offered proximity to consumption centers in Karnataka, Kerala, and Tamil Nadu. The Western Ghats provided a natural barrier against competition from refineries in Mumbai and Gujarat. The New Mangalore Port could handle VLCCs (Very Large Crude Carriers), reducing transportation costs.

Infrastructure investments supported market access. MRPL developed two captive jetties, a single point mooring facility, rail wagon loading silos for petcoke, truck loading silos, and marketing infrastructure depots in Kasargod (Kerala), Hindupur (Andhra Pradesh), and Hosur (Tamil Nadu).

Yet challenges persisted. Private refiners like Reliance and Nayara operated larger, more efficient complexes. Public sector peers like IOC and BPCL had extensive retail networks. MRPL found itself in a squeeze—too small to compete on scale, too constrained by government ownership to match private sector agility.

The product portfolio strategy ultimately reflected MRPL's hybrid identity—sophisticated enough to produce specialty products, flexible enough to adapt to market changes, but lacking the scale and market presence to fully capitalize on these capabilities. As we'll see, this strategic middle ground would prove both a strength and weakness as market conditions evolved.

VI. The OMPL Integration Story (2015-2018)

The conference room at MRPL's headquarters hummed with anticipation on a humid February morning in 2015. Board members reviewed a proposal that would fundamentally reshape the company's petrochemical ambitions. On the table: acquiring control of ONGC Mangalore Petrochemicals Limited (OMPL), the aromatic complex literally next door that had been struggling since its delayed commissioning.

MRPL Board, in its 193rd meeting held on 09/02/2015, approved acquisition of major stake in OMPL, increasing the holding from 3% to 46% by purchasing fully paid up equity shares from individual shareholders. By year-end, MRPL would hold 51% of OMPL, with ONGC retaining 49%. The structure was unusual—a subsidiary acquiring control of what was essentially a sister company—but it made operational sense.

OMPL's story was one of ambition meeting reality. Incorporated on 19 December 2006, the complex was designed as the largest single stream unit in Asia to produce 914 KTPA Para-xylene and 283 KTPA Benzene. Located in 442 acres of land in the Mangalore Special Economic Zone, it was fully integrated with MRPL. Naphtha and aromatic streams from MRPL would feed OMPL, which would return fuel gas and other streams back to the refinery.

But OMPL's commissioning had been a nightmare. Initially scheduled for 2010, the complex did not begin production until 2014. Cost overruns, technical challenges, and market timing had left OMPL financially stressed. Para-xylene prices had collapsed from over $1,400 per tonne in 2011 to under $800 by 2015. The standalone economics looked dire.

MRPL's management saw opportunity where others saw disaster. The merger was poised to create higher shareholder value over and above the sum of two companies—a classic case of one plus one equals three. The synergies were compelling: integrated operations would eliminate transfer pricing issues, optimize feedstock routing, reduce duplicate administrative costs, and provide flexibility to maximize combined refining and petrochemical margins.

The board formally approved the amalgamation scheme in July 2015, with MRPL holding 51% and ONGC 49%. The merger rationale, as explained to shareholders, was multifaceted. Operating the aromatic plant integrated with the refinery would provide higher returns, add value to refinery streams, optimize resources through pooling of management and technical skills, and improve overall working culture.

Integration challenges emerged immediately. OMPL had operated as an independent entity with its own systems, procedures, and culture. Merging two plants with different technologies, separate control rooms, and distinct operating philosophies required delicate management. Employee concerns about job security had to be addressed. Technical integration—connecting pipelines, integrating utilities, harmonizing control systems—took months.

The market dynamics added complexity. Para-xylene is a globally traded commodity with prices set by Northeast Asian markets. When PX prices were high, OMPL wanted maximum naphtha allocation. When gasoline cracks were strong, MRPL preferred sending naphtha to its reformer. These conflicts, previously resolved through commercial negotiations, now became internal optimization challenges.

Operational integration proceeded in phases. First, utility systems were connected—steam, power, nitrogen, instrument air. Then, feedstock and product pipelines were integrated, allowing seamless transfer without truck or rail movement. Control room integration followed, with operators trained to view the complex as one integrated unit rather than separate plants.

The financial engineering was equally complex. OMPL's debt had to be restructured. Inter-company transactions needed elimination. Transfer pricing mechanisms were replaced with internal cost allocations. The consolidated financial statements had to reflect the new reality while maintaining transparency for minority shareholders.

By 2017, integration benefits started materializing. Combined optimization increased aromatic yields by 3-5%. Administrative cost savings exceeded ₹50 crore annually. Most importantly, the integrated complex could respond dynamically to market signals—when petrochemical margins were strong, maximize aromatics production; when fuel margins dominated, shift toward transportation fuels.

The OMPL integration became a template for ONGC's downstream strategy. It demonstrated how stranded petrochemical assets could be revived through refinery integration. But it also highlighted the complexity of managing integrated refining-petrochemical complexes, where optimization decisions ripple across multiple units and products.

As 2018 dawned, MRPL had successfully absorbed OMPL, creating one of India's few truly integrated refining and petrochemical complexes. The aromatics capacity provided a natural hedge against fuel margin volatility. Yet as management would soon discover, even this integration couldn't shield MRPL from the storm clouds gathering in global energy markets.

VII. Modern Challenges & Transformation (2018-Present)

The smartphone screen glowed with red numbers in MRPL's war room on a July morning in 2025. Crude oil prices, refining margins, product cracks—every metric that mattered was flashing warning signals. The Q1 FY26 results had just been finalized: a net loss of ₹270.66 crore, with total income declining 23% year-on-year to ₹21,026.06 crore. The transformation from profitable refiner to loss-making enterprise had been swift and brutal.

The roots of crisis traced back to 2018, when global refining entered a new paradigm. Massive capacity additions in China and the Middle East created a structural oversupply. The IMO 2020 regulations mandating low-sulfur marine fuels, initially expected to boost complex refinery margins, instead triggered demand destruction as shipping companies installed scrubbers or switched to alternative fuels.

Then came the polycrisis of the 2020s. COVID-19 decimated transportation fuel demand just as MRPL had completed capacity expansions. The Russia-Ukraine conflict initially seemed like an opportunity—Russian crude trading at deep discounts—but geopolitical pressures forced Indian refiners to recalibrate. MRPL, which had optimized operations around Russian grades, suddenly had to switch to more expensive alternatives.

The numbers tell a story of steady deterioration. Gross Refining Margin dropped to US$ 3.88 per barrel in Q1 FY26, compared to US$ 4.70 a year ago. For context, MRPL needs roughly $6-7 per barrel to break even given its cost structure. Every dollar below that threshold translates to hundreds of crores in losses.

Competition intensified from unexpected quarters. Reliance's Jamnagar complex, already the world's largest, announced further expansions and pivots toward chemicals. Nayara Energy (formerly Essar Oil) leveraged Russian ownership to access advantaged crude. Even public sector peers like IOC and BPCL operated more efficient refineries with better market access.

The energy transition cast a long shadow. Electric vehicle adoption in India, while still nascent, grew exponentially in two-wheelers and three-wheelers—segments that consumed significant gasoline volumes. Corporate ESG commitments drove industrial customers toward renewable energy. International oil companies started exiting downstream assets, signaling long-term pessimism about refining.

MRPL's strategic responses revealed both ambition and constraint. The retail expansion accelerated, with the network growing to 101 outlets, but each station required ₹3-5 crore investment with uncertain returns. The petrochemical pivot through OMPL integration provided some stability, but aromatics markets proved equally volatile. Attempts at producing specialized grades—like winter-grade diesel for Ladakh or premium lubricant base oils—showcased technical capability but lacked commercial scale.

Operational challenges compounded financial stress. Total throughput dropped to 3.52 MMT in Q1 FY26 from 4.35 MMT a year earlier due to planned maintenance shutdowns. When you operate a 15 MMTPA refinery at 70% capacity, unit costs skyrocket. Fixed costs—salaries, maintenance, interest—remain constant while revenue shrinks.

The government ownership paradox became acute. As a PSU, MRPL couldn't match private sector agility in crude procurement or marketing strategies. Board approvals for major decisions went through multiple bureaucratic layers. Yet the government also couldn't allow a strategic refinery to fail, creating moral hazard where losses were implicitly backstopped.

Management changes reflected the crisis. Senior executives rotated frequently, each bringing new strategies that required time to implement—time the market didn't provide. The workforce, once proud of operating India's most complex refinery, grappled with uncertainty. Campus recruitment dried up; experienced engineers sought opportunities elsewhere.

Environmental regulations added another layer of complexity. The shift to BS-VI fuel standards required massive investments in desulfurization capacity. Carbon border adjustments threatened export competitiveness. State pollution control boards imposed increasingly stringent emission norms. Each compliance requirement meant capital expenditure with no corresponding revenue uplift.

The debt burden became crushing. Interest coverage ratios turned negative. Credit rating agencies placed MRPL on watch. The parent ONGC, itself facing upstream challenges, had limited capacity for further support. The stock price reflected investor pessimism, declining over 38% in one year despite a broader market rally.

Yet amidst the crisis, glimpses of resilience emerged. MRPL achieved its highest-ever crude processing for April at 1,512 TMT in 2025, demonstrating operational capability when market conditions aligned. The polypropylene business remained profitable, benefiting from import substitution trends. The retail network, while subscale, commanded premium pricing in local markets.

As 2025 progresses, MRPL stands at an inflection point. The traditional refining model—process crude, sell fuels, hope for favorable cracks—is broken. The future demands reinvention: perhaps as a specialty chemicals producer, a biofuels pioneer, or a green hydrogen hub. But transformation requires capital, which losses have eroded, and time, which competitive pressures don't allow.

The modern MRPL story is thus one of structural challenges meeting operational excellence, where technical capability cannot overcome commercial reality. It's a preview of pressures all traditional refiners will face as the energy transition accelerates—a canary in the coal mine of India's petroleum sector.

VIII. Playbook: Lessons from MRPL's Journey

Every industrial saga teaches lessons, but MRPL's journey offers a masterclass in complexity—both technical and organizational. As we distill three decades of refinery operations into actionable insights, patterns emerge that transcend the petroleum sector.

Lesson 1: Timing Expansion Cycles in Commodity Businesses

MRPL's Phase III expansion, initiated when refining margins were robust, came online just as global capacity surged and margins collapsed. The project took six years from conception to completion—in commodity businesses, that's an eternity. By the time the delayed coker and PFCCU were operational, the market had fundamentally shifted.

The playbook insight: In capital-intensive commodity businesses, capacity additions should be countercyclical. Build when others are retrenching, not when margins are peak. MRPL's expansion aligned with industry-wide capacity growth in China and the Middle East, guaranteeing oversupply. The companies that win in commodities are those that have capacity ready when demand recovers, not those that complete projects just as cycles turn.

Lesson 2: The Partnership Paradox

The original HPCL-AV Birla joint venture seemed ideal—public sector market access married to private sector efficiency. Yet it failed precisely because neither partner could fully commit during distress. HPCL lacked capital; Birla lacked patience. The JV structure meant decisions required consensus, slowing responses to market changes.

Contrast this with post-ONGC acquisition: single ownership enabled quick decisions, patient capital, and integrated strategy. The lesson? In capital-intensive industries facing volatile markets, partnerships work only when partners share not just vision but also financial capacity and time horizons. Misaligned partners amplify challenges rather than mitigate them.

Lesson 3: Complexity as Competitive Moat—And Trap

MRPL's technical complexity is remarkable—two hydrocrackers, delayed coker, PFCCU, aromatics complex. This complexity theoretically enables processing of challenging crudes and production of premium products. But complexity also means higher maintenance costs, more potential failure points, and need for specialized expertise.

The playbook teaches that complexity must match market structure. In India's regulated fuel market with limited premium pricing, MRPL's sophistication doesn't translate to proportional margin capture. Reliance succeeds with complexity because it has scale; smaller Gulf refineries succeed with simplicity because they have advantaged feedstock. MRPL sits in an uncomfortable middle—too complex for its scale, too small for its complexity.

Lesson 4: Government Ownership in Commercial Businesses

MRPL's PSU status creates perpetual tension. Government ownership provides implicit financial backing and strategic importance, but also imposes bureaucratic decision-making and political pressures. The company cannot match private sector agility in crude procurement or flexibility in workforce management, yet must compete directly with private refiners.

The lesson extends beyond oil: Government ownership works best in natural monopolies or strategic sectors where commercial returns are secondary. In competitive markets, the PSU model struggles. MRPL's challenges mirror those of Air India, BSNL, and other government enterprises competing with private players—technical competence undermined by structural disadvantages.

Lesson 5: Integration Versus Focus

The OMPL integration seemed logical—combine refining with petrochemicals for margin stability. But integration increased operational complexity and capital intensity without proportional return improvement. When para-xylene margins collapsed, MRPL couldn't simply exit; it was committed to operating an integrated complex.

The strategic lesson: Integration makes sense when it provides genuine operational synergies or market power. MRPL's integration was subscale—not large enough to influence prices or achieve significant cost advantages. In commodity businesses, focus often beats integration unless you can achieve dominant scale.

Lesson 6: The Retail Gambit

MRPL's HiQ retail network represents classic forward integration—capturing additional margin by reaching end consumers. But building retail presence requires massive capital, brand investment, and operational capabilities distinct from refining. With 101 outlets versus thousands for established players, MRPL lacks scale for meaningful impact.

The playbook suggests that forward integration works when you have either unique product differentiation or significant scale advantages. MRPL has neither—its fuels are commodity products, and its network is subscale. The retail expansion dissipates capital that could strengthen core refining operations.

Lesson 7: Managing Technology Transitions

MRPL built capabilities for the previous energy paradigm—fossil fuel refining with incremental efficiency improvements. The energy transition demands fundamentally different capabilities: renewable energy integration, hydrogen production, carbon capture, biofuel processing. Retrofitting existing assets for new energy forms is often more expensive than greenfield development.

The lesson for industrial companies: Technology transitions require proactive capability building before markets shift. Companies that wait for market signals find themselves responding from positions of weakness. MRPL's current struggles partly reflect delayed recognition of energy transition implications.

Lesson 8: Capital Allocation in Distress

As losses mounted, MRPL faced impossible choices: invest in maintenance to sustain operations, expand retail for market access, upgrade units for compliance, or preserve cash for survival. Each decision involved trade-offs with no clear optimal path. The company chose to continue all initiatives at subscale, satisfying no objective fully.

The playbook teaches brutal prioritization during distress. Either fix the core business or pivot decisively. Half-measures prolong agony without solving fundamental problems. MRPL's attempt to simultaneously maintain refining excellence, expand retail, and integrate petrochemicals spread resources too thin.

These lessons from MRPL's journey echo across industries facing disruption—whether traditional automotive confronting electrification, brick-and-mortar retail battling e-commerce, or legacy media adapting to digital. The specifics vary, but patterns repeat: timing matters, ownership structure shapes strategy, complexity requires scale, and transitions demand decisive action.

IX. Bull vs. Bear Case Analysis

The investment community remains sharply divided on MRPL's future. At ₹123 per share, the stock trades at historic lows, yet analysts can't agree whether this represents deep value or a value trap. Let's examine both sides of this debate with the rigor it deserves.

The Bull Case: Strategic Asset at Distress Valuation

Bulls begin with replacement value. Building a 15 MMTPA refinery with MRPL's complexity would cost at least ₹50,000 crore today. With a market cap of just ₹21,583 crore, MRPL trades at less than half of replacement cost. In any other industry, this would scream value.

The strategic importance cannot be ignored. India's petroleum product demand continues growing at 3-4% annually, driven by increasing vehicle ownership and industrial activity. MRPL provides 7-8% of South India's fuel requirements—a region with limited refining capacity and growing consumption. Geographic advantage remains intact: coastal location, established infrastructure, and proximity to deficit markets.

The complexity that seems a burden today could become tomorrow's advantage. As the only Indian refinery with two hydrocrackers, MRPL can produce ultra-low sulfur diesel that meets the most stringent environmental standards. As emission norms tighten globally, this capability becomes increasingly valuable. The 440 KTA polypropylene plant provides non-fuel revenue diversification.

ONGC's parentage provides implicit support. The parent company, with its substantial upstream cash flows, won't allow MRPL to fail. This backstop limits downside risk while preserving upside optionality. Historical precedent supports this—ONGC injected ₹600 crore during the 2003 acquisition and has supported MRPL through previous downturns.

Refining margins are cyclical, not secular declining. Current GRMs of $3-4 per barrel represent cyclical lows driven by capacity overhang. As older, inefficient refineries shut down and demand recovers post-pandemic, margins should normalize to $6-8 per barrel. Even modest margin recovery would restore profitability given MRPL's operational leverage.

The energy transition timeline is overstated. While electric vehicles grab headlines, India's passenger vehicle penetration remains under 50 per 1,000 people versus 800+ in developed countries. The next two decades will see massive growth in conventional vehicles before EVs dominate. Diesel demand from trucking, agriculture, and industry has no near-term alternative. Petrochemicals demand continues growing regardless of energy transition.

The Bear Case: Structural Decline in Sunset Industry

Bears counter with brutal financial reality. Q1 FY26's ₹271 crore loss isn't an aberration—it's the new normal. Global refining capacity exceeds demand by 3-4 million barrels per day, and this oversupply is structural, not cyclical. Chinese and Middle Eastern mega-refineries operate at lower costs with better technology. MRPL cannot compete on cost, scale, or efficiency.

The energy transition is accelerating beyond expectations. India's EV sales grew 70% year-on-year in 2024. Two-wheelers, which consume 60% of India's gasoline, are rapidly electrifying. Industrial customers are switching to natural gas and renewable energy. Peak oil demand for India might arrive by 2035, leaving MRPL with stranded assets.

Government ownership is a permanent handicap. PSU status means MRPL cannot restructure quickly, cannot optimize workforce, cannot match private sector procurement practices. Every decision filters through bureaucratic layers. The company becomes a employment program rather than commercial enterprise. History shows few PSUs successfully compete with private players in competitive markets.

Competition is intensifying, not moderating. Reliance continues expanding, leveraging its scale for better crude deals and market access. New refineries in Bangladesh and Sri Lanka target MRPL's export markets. Even domestic PSU peers like IOC and BPCL operate more efficiently. MRPL's subscale retail network cannot compete with established players' thousands of outlets.

Capital allocation has been value-destructive. The Phase III expansion destroyed shareholder value—₹12,000+ crore invested for assets generating losses. The OMPL integration added complexity without commensurate returns. The retail expansion requires continuous capital injection with uncertain payback. Good money continues chasing bad.

The debt burden is unsustainable. With negative interest coverage and mounting losses, MRPL edges toward debt spiral. Credit rating downgrades increase borrowing costs, which worsen losses, triggering further downgrades. Without ONGC support, MRPL would already face solvency concerns.

Technology disruption accelerates. Green hydrogen, sustainable aviation fuel, and bioplastics threaten traditional refining. MRPL lacks capital and capabilities for energy transition. Retrofitting existing assets for new energy forms is prohibitively expensive. The company risks becoming a stranded asset before loans are repaid.

The Verdict: A Binary Outcome

The bull-bear debate ultimately reduces to a binary question: Will refining margins recover before energy transition kills demand? Bulls bet on mean reversion and India's growth story. Bears see structural decline and technological disruption.

Both cases have merit, but timing is everything. If margins recover within 2-3 years, MRPL survives and potentially thrives. If recovery takes 5+ years, accumulated losses and debt burden become insurmountable. The stock price reflects this uncertainty—too risky for value investors, too distressed for growth investors.

For fundamental investors, MRPL represents a complex option on India's energy future. The asymmetry is clear: limited downside (thanks to ONGC backing) but potentially massive upside if conditions align. Whether that option is worth exercising depends on your view of energy transition timing, India's growth trajectory, and global refining dynamics.

X. Epilogue & Future Outlook

As the sun sets over the Arabian Sea, casting long shadows across MRPL's refinery complex, the control room operators maintain their vigilant watch. Crude oil continues flowing through distillation columns, molecules splitting and recombining in processes perfected over decades. The industrial symphony plays on, but the audience is departing, and the theater itself faces renovation or demolition.

MRPL's next chapter remains unwritten, but the constraints are clear. The company needs $6+ per barrel GRMs to break even—a level last seen consistently before 2019. Global refining capacity additions of 2-3 million barrels per day planned through 2027 suggest margins will remain pressured. The energy transition, while gradual, is irreversible. The strategic options narrow with each passing quarter of losses.

Path 1: The Petrochemical Pivot

One future sees MRPL doubling down on chemicals. India imports $30+ billion of chemicals annually, providing import substitution opportunity. The OMPL integration offers a template—convert more fuel molecules into chemical building blocks. This requires massive capital investment in crackers, derivative units, and specialty chemical plants. ONGC could partner with international chemical majors, bringing technology and market access. But this transformation would take a decade and ₹30,000+ crore—resources MRPL doesn't have.

Path 2: The Green Energy Transition

Another scenario involves radical transformation into new energy forms. The coastal location and industrial infrastructure could anchor green hydrogen production using offshore wind power. Existing units could be retrofitted for biofuel production. The aromatics complex could produce bio-based chemicals. This positions MRPL for the post-fossil fuel era but requires writing off existing assets and essentially building a new company. The question: Why use MRPL as the vehicle rather than create something new?

Path 3: Managed Decline

The most likely path may be gradual rationalization. Operate existing assets for cash generation while minimizing new investment. Shut subscale businesses like retail. Focus on core refining for regional markets. Eventually, merge with HPCL or another PSU refiner for synergies. This path preserves employment and energy security but offers no growth. MRPL becomes a industrial utility—necessary but uninspiring.

Path 4: Strategic Sale

A bold option involves privatization or strategic sale. International oil companies seeking Indian market entry might value MRPL's infrastructure and complexity. Middle Eastern national oil companies could use MRPL for crude outlet and market access. Private Indian conglomerates might see opportunity in distressed asset turnaround. But political considerations make PSU privatization challenging, especially for strategic assets.

The macro context shapes all scenarios. India's petroleum product demand will grow through 2040, but growth rates decline each year. Electric vehicles will capture increasing market share, first in two-wheelers, then cars, eventually commercial vehicles. Industrial fuel switching accelerates with carbon pricing. International climate commitments constrain fossil fuel expansion.

Yet India's energy security imperatives persist. Import dependence exceeds 85% for crude oil. Geopolitical volatility—whether Russia-Ukraine, Iran-Israel, or China-Taiwan—can disrupt supplies. Domestic refining capacity provides strategic buffer. MRPL's ability to process various crudes offers supply flexibility. These considerations may preserve MRPL despite commercial challenges.

The human dimension deserves recognition. Thousands of families depend on MRPL—employees, contractors, suppliers, retailers. Mangalore's economy significantly relies on refinery operations. The social cost of closure exceeds financial metrics. This reality influences government decision-making, potentially sustaining operations beyond commercial logic.

For investors, MRPL embodies the classical disruption dilemma. The business model faces existential threat, but the timeline remains uncertain. Assets have value, but that value declines daily. Recovery is possible but requires multiple favorable factors aligning. The risk-reward calculation depends entirely on time horizon and transition assumptions.

As we conclude this exploration, MRPL stands as a monument to India's industrial ambitions and a cautionary tale about timing, scale, and technological change. Born from post-liberalization optimism, built with world-class technology, expanded with aggressive vision, the refinery now confronts forces beyond its control. Whether MRPL emerges transformed or becomes a industrial relic will be determined in the next five years.

The story continues, written daily in crude processed, products sold, and margins earned or lost. For now, the refinery operates, the operators monitor, and India's energy needs are met. But in boardrooms from Mumbai to Delhi, difficult decisions await—decisions that will determine whether MRPL rides the next energy wave or is submerged by it.

The Mangalore Refinery and Petrochemicals Limited story is far from over. But whether the next chapter is renaissance or requiem remains an open question—one that reflects broader uncertainties about India's energy future, the pace of global transition, and the fate of industries caught between legacy and transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube