Diamondback Energy: The Story of America's Shale Revolution Champion

I. Introduction & Episode Roadmap

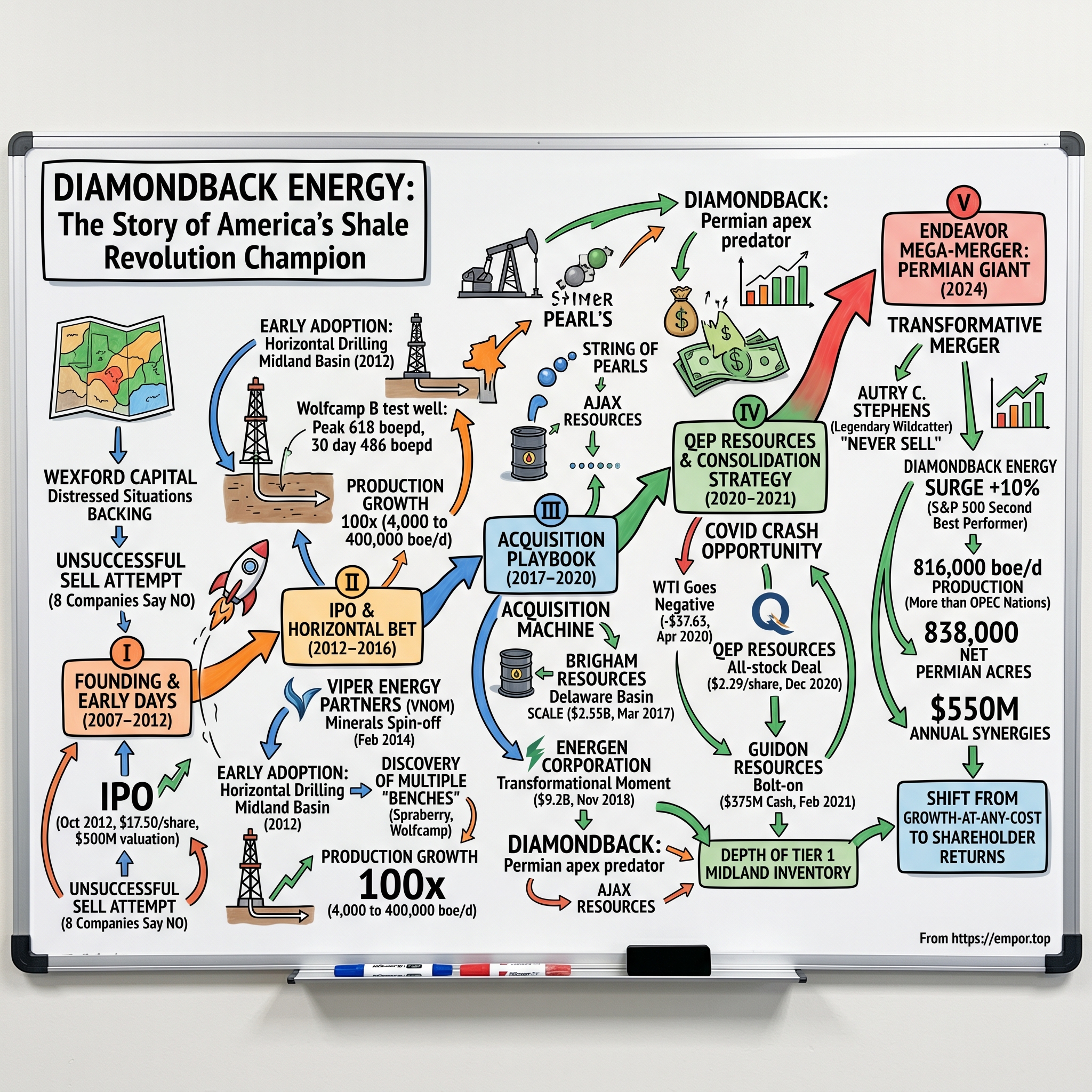

Picture this: It's 2007, the financial world is melting down, oil prices are whipsawing from $147 to $33 a barrel, and a geologist named Travis Stice is trying to convince anyone—anyone—to buy his fledgling oil company in West Texas. Eight potential buyers look at his assets. Eight say no thanks. Fast forward seventeen years, and that same company, Diamondback Energy, just closed a $26 billion acquisition to become the undisputed king of the Permian Basin, pumping out more oil per day than several OPEC nations.

This is the story of how Diamondback Energy (ticker: FANG—yes, really) transformed from a crisis-era startup that nobody wanted into America's most efficient shale operator. Today, ranked 383rd on the Fortune 500 and 471st on the Forbes Global 2000, Diamondback isn't just another oil company. It's the embodiment of American energy independence, a master class in capital allocation, and perhaps most importantly, the canary in the coal mine for whether the U.S. shale revolution has finally hit its limits.

The journey we're about to trace isn't just about drilling holes in Texas dirt. It's about how a company built during the worst financial crisis in generations became the template for modern energy companies—balancing growth with returns, efficiency with scale, and somehow managing to thrive through oil prices that ranged from negative $37 to over $120 per barrel. Along the way, we'll explore how Diamondback pioneered new business models (ever heard of a minerals spin-off?), perfected the art of the oil patch acquisition, and why its CEO recently dropped a bombshell that sent shockwaves through energy markets: American oil production may have already peaked.

What makes Diamondback fascinating isn't just its operational excellence—though drilling wells 50% faster than competitors certainly helps—it's how the company embodies every major theme of the modern energy era: the shale revolution that turned America from energy importer to exporter, the shift from growth-at-any-cost to shareholder returns, the consolidation wave sweeping through the Permian, and now, the uncomfortable question of what happens when the miracle of shale finally runs out of room to run.

So buckle up. We're about to dive deep into the Permian Basin, where fortunes are made and lost based on the price of a barrel of oil, where technology and geology collide, and where one company's story illuminates the entire trajectory of American energy. This is Diamondback Energy—the acquisition machine, the efficiency champion, and possibly the last great growth story of the shale era.

II. The Founding Story & Early Days (2007–2012)

The rain was sideways, the kind of West Texas storm that turns the Permian Basin into a muddy wasteland and makes you wonder why anyone would drill for oil here in the first place. It was late 2011, and Travis Stice was sitting in a cramped metal field office outside Midland, staring at a laptop screen that might as well have been showing his professional obituary. Eight oil companies had looked at Diamondback Energy's assets. Eight had walked away. Nobody wanted what they were selling.

Stice wasn't new to the oil patch—he'd started his career with Mobil Oil in 1985, working his way through the industry's consolidation waves at Burlington Resources and ConocoPhillips before landing at Apache Corporation. But this was different. This was supposed to be his shot at building something from scratch, and it was dying before it could even properly live.

The story of Diamondback Energy begins not with a grand vision or breakthrough technology, but with desperation and a bet that nobody else wanted to make. The company began operations in December 2007 with the acquisition of 4,174 net acres in the Permian Basin—a modest foothold in what would become America's most prolific oil field. The timing couldn't have been worse. Within months, oil prices would crater from $147 to $33 per barrel, Lehman Brothers would collapse, and the entire financial system would teeter on the edge of oblivion.

Yet here's the thing about crisis: it creates opportunities for those crazy enough to see them. Stice and his team weren't drilling vertical wells like everyone else in the Midland Basin. They were betting on something called horizontal drilling—a technique that involved drilling down, then sideways through the rock formation, exposing far more of the oil-bearing rock to the wellbore. In 2007, this wasn't revolutionary technology globally, but in the Midland Basin where vertical wells were perfectly economic, it was considered unnecessary and expensive. Why fix what wasn't broken?

The private equity backing came from Wexford Capital, run by Charles Davidson, who had a knack for finding oil and gas opportunities in distressed situations. But even Wexford's patience had limits. Stice recalled that they "had tried to sell the company about six months prior and were unsuccessful – no one wanted our assets." The company had been marketed to eight other producers and did not receive any bids. Having no other choice – his private equity backers had exhausted their intended investments in Diamondback and were unwilling to invest more – an IPO was decided upon.

Think about that for a moment. This wasn't a triumphant march to Wall Street. This was a Hail Mary, a last-ditch effort to keep the lights on. The company that would eventually become worth tens of billions of dollars couldn't find a single buyer when it needed one most.

Stice would later reflect: "It doesn't seem that long ago when I was working on a laptop in the kitchen of a small metal field office trying to figure out how to get the company off the ground. It took quite a few twists and turns, but we were able to IPO" at a "$500 million valuation producing just 3,000 BOE/d. There were some really tough days early on, but as they say – you can't climb a smooth mountain."

The decision to go public wasn't just about survival—it was about transformation. In October 2012, the company became a public company via an initial public offering, issuing 12,500,000 shares of common stock at a price of $17.50 per share. For context, at that price, the entire company was valued at less than what it would spend on a single acquisition just a few years later.

But the real genius wasn't the IPO itself—it was what Stice did next. The second milestone was the decision to become an early adopter of horizontal drilling in the Midland Basin, where vertical wells were economic. The success of that program let the company grow its inventory materially. While competitors stuck with tried-and-true vertical drilling, Diamondback was figuring out how to drill wells faster, cheaper, and with better production rates than anyone thought possible.

The numbers tell the story: Diamondback grew production by a factor of 100, from under 4,000 barrels a day to 400,000 barrels a day. But numbers alone don't capture the cultural DNA that was being encoded in those early days. "Even as it has made its acquisitions, Diamondback has focused on both execution and being a low-cost operator. In the commodities market where you don't control the price of the commodity you produce, you better be good at both execution and being low-cost".

This wasn't Silicon Valley disruption through software and network effects. This was disruption through pure operational excellence—doing the dirty, difficult work of drilling for oil better than anyone else. And in an industry where a 10% improvement in drilling efficiency could mean the difference between profit and bankruptcy, Diamondback was achieving improvements of 30%, 40%, sometimes 50% over industry averages.

"And third was the creation of a brand-new investor segment, a minerals company named Viper Energy Partners that 'unintentionally' transformed the entire minerals space". This move—spinning off the mineral rights into a separate publicly traded entity—would become a template copied across the industry. It was financial engineering at its finest, creating value not through drilling more wells but through restructuring how investors could access different parts of the oil value chain.

Looking back, those early years from 2007 to 2012 weren't just about survival. They were about establishing a playbook that would guide Diamondback through the boom-bust cycles that define the oil business. Start lean, stay disciplined, focus relentlessly on costs, and never forget that in commodities, you don't control the price—you can only control your response to it.

"Each event helped us grow the company from a capitalization of $500 million at the time of the IPO to over $30 billion today". But that growth was still to come. In 2012, as Diamondback's newly minted public shares began trading on the NASDAQ, the real test was just beginning. The shale revolution was about to kick into high gear, and Diamondback had positioned itself perfectly to ride the wave—if it could execute on the promise of those early horizontal wells.

III. The IPO & Early Horizontal Drilling Bet (2012–2016)

The trading floor at the New York Stock Exchange was buzzing with unusual energy on October 17, 2012. Travis Stice stood there in his best suit, watching the digital ticker flash "FANG" for the first time as a public company. The company became a public company via an initial public offering, issuing 12,500,000 shares of common stock at a price of $17.50 per share. But this wasn't a victory lap—it was a last resort dressed up as a celebration.

"The reason that is significant is that we had tried to sell the company about six months prior and were unsuccessful – no one wanted our assets," he recalled. He said the company had been marketed to eight other producers and did not receive any bids. Having no other choice – his private equity backers had exhausted their intended investments in Diamondback and were unwilling to invest more – an IPO was decided upon.

Think about the audacity of what happened next. Here's a company that couldn't find a buyer at any price six months earlier, now asking public market investors to value it at over $200 million. Even more audacious? Stice immediately took the IPO proceeds and doubled down on a technology that most Permian operators thought was unnecessary: horizontal drilling in the Midland Basin.

The first test well told the story. Diamondback's 1st horizontal Wolfcamp B test well was drilled in June 2012 in Upton County with a peak rate of 618 boepd and a 30 day initial production ("IP") rate of 486 boepd (86% oil) from a 3,842 foot lateral. The Company's 2nd horizontal Wolfcamp B test well, a non-operated well in Midland County, had a peak rate of 892 boepd and a 30 day IP of 428 boepd (90% oil) from a 3,733 foot lateral.

To understand why these numbers mattered, you need to understand the economics of oil drilling. A vertical well in the Midland Basin might cost $2 million and produce 100-200 barrels per day. These horizontal wells cost $7-8 million but were producing 400-900 barrels per day. The math was compelling, but only if you could execute. And execution was where Diamondback separated itself from the pack.

When normalizing on a per foot of lateral completed, Diamondback believes that these two Wolfcamp B wells are performing at or near the top of all of the Wolfcamp B wells in the Midland Basin. This wasn't luck—it was the result of obsessive focus on operational efficiency that would become Diamondback's calling card.

By early 2013, the transformation was accelerating. The company was using two horizontal drilling rigs as of March 31, 2013, and currently intended to add a third horizontal rig in July 2013 and a fourth horizontal rig in the fourth quarter of 2013. The company that nobody wanted was now growing at a pace that defied industry norms.

The numbers tell the story of this transformation. During the third quarter of 2013, 7,500 foot laterals averaged approximately $7.2 million, down from $7.6 million in the previous quarter and now average approximately 14 days from spud to total depth ("TD") for a 7,500 foot lateral with one 7,500 foot lateral well reaching TD in 12 days. In an industry where time literally equals money—rigs cost $25,000 per day—shaving even a single day off drilling time was worth celebrating. Diamondback was shaving weeks.

But the real genius move came in February 2014, with something that seemed like financial engineering but was actually strategic brilliance. "And third was the creation of a brand-new investor segment, a minerals company named Viper Energy Partners that 'unintentionally' transformed the entire minerals space".

The Viper spinoff was elegant in its simplicity. Diamondback carved out its mineral rights—the subsurface ownership that entitled it to royalties on any oil produced—into a separate publicly traded entity. Viper Energy Partners LP, a Permian Basin oil and gas E&P spun out of Diamondback Energy, filed on Wednesday with the SEC to raise up to $100 million in an initial public offering. The Midland, TX-based company, which was formed in September 2013 and booked $15 million in royalty revenue for the three months ended December 31, 2013, plans to list on the NASDAQ under the symbol VNOM.

Wall Street loved it. "While shares have outperformed recently ahead of the potential IPO, we believe the IPO creates tremendous shareholder value yet to be fully reflected," said Gabriele Sorbara, analyst for Topeka Capital Markets, in a June 3 report. Sorbara said the offering could be worth $1.2 billion.

This wasn't just financial engineering—it was a new way of thinking about oil and gas assets. By separating the minerals from the operating business, Diamondback created two distinct investment vehicles: one for investors who wanted exposure to operational excellence and drilling returns, another for those who wanted the steady, no-capex-required cash flows from mineral royalties. It was a template that would be copied across the industry.

Meanwhile, the horizontal drilling program was exceeding all expectations. The Company's first horizontal Middle Spraberry test well, the Sarah Ann 3814H, a non-operated well in Midland County, had a peak 24 hour initial production ("IP") rate of 733 Boe/d (90% oil) on electric submersible pump. This Middle Spraberry test defines a new horizontal bench that has meaningfully increased the Company's identified potential horizontal drilling Spraberry locations to 360 gross (276 net) from 181 gross (139 net).

What this meant was revolutionary: Diamondback wasn't just drilling better wells, it was discovering that the Permian Basin had multiple layers of oil-bearing rock that could be exploited with horizontal drilling. Each new "bench" or layer effectively multiplied the company's drilling inventory without requiring new land acquisitions.

The efficiency gains were staggering. The company claims to have lowered operating costs by more than 50% since the third quarter of 2012. In a commodity business where you don't control prices, being the low-cost producer is the ultimate competitive advantage.

By 2014, the market was taking notice. Diamondback's stock had roughly tripled in value since its IPO. And with the expansion of share count through secondary offerings, Diamondback's market cap -- roughly $250 million in October of 2012 -- had swollen by a factor of 10 to more than $2.5 billion.

Initially, Diamondback was a vertical Wolfberry operator, and shifted aggressively to horizontal drilling soon after the influx of public funds. That move, made ahead of its peers, who were still drilling vertical wells, garnered production growth of 150% in 2013, forecast for more than 110% this year.

The transformation was complete. The company that nobody wanted in 2012 had become one of the most closely watched names in energy by 2016. It has also helped Diamondback grow production by a factor of 100, from under 4,000 barrels a day to 400,000 barrels a day.

But this was just the beginning. Diamondback had proven it could drill wells better than anyone else. Now it was time to prove it could buy companies better than anyone else too. The acquisition playbook was about to begin.

IV. The Acquisition Playbook Begins (2017–2020)

The conference room at the St. Regis Hotel in Houston was electric with nervous energy on a sweltering August day in 2017. Travis Stice sat across from Gene Shepherd, CEO of Brigham Resources, knowing that what happened in the next few hours would determine whether Diamondback could transform from a mid-sized Permian operator into something much bigger. The asking price was staggering: $1.62 billion in cash and 7.69 million shares of Diamondback common stock for Brigham's Delaware Basin assets.

Just five years after going public as a company nobody wanted, Diamondback was now writing billion-dollar checks. But this wasn't reckless expansion—it was calculated consolidation. The Company closed its previously announced acquisition of leasehold interests and related assets from Brigham Resources for an aggregate purchase price of $2.55 billion in March 2017, marking Diamondback's entry into the Delaware Basin at scale.

The Brigham deal represented a philosophical shift in the Permian Basin. For years, the play had been dominated by hundreds of small operators, each drilling their piece of the puzzle. Now, consolidation was beginning. And Diamondback, with its proven ability to drill wells faster and cheaper than anyone else, was perfectly positioned to be the consolidator.

"With Diamondback's proven ability to execute, we now believe we have the resource and acreage base to efficiently support 15 to 20 operated rigs", Stice stated after the deal. "We believe our near-term acceleration across our asset base, along with the production from this acquisition, will put us in a position to achieve over 60% production growth in 2017 at the midpoint of our current guidance range".

The operational thesis was simple: take Brigham's good rocks and apply Diamondback's superior execution. Recent horizontal wells on and surrounding the properties had confirmed geochemical data that indicates four primary targets: Wolfcamp A, Wolfcamp B, 3rd Bone Spring and the 2nd Bone Spring. Diamondback believes that development potential within the footprint of the acquisitions includes 1,213 net horizontal locations.

But the real masterstroke came eighteen months later. In August 2018, while oil prices hovered around $70 per barrel and Permian euphoria was reaching new heights, Stice made his boldest move yet. Diamondback announced it would acquire Energen Corporation in an all-stock transaction valued at $9.2 billion, with consideration of 0.6442 shares of Diamondback common stock for each share of Energen common stock, representing an implied value to each Energen shareholder of $84.95 per share.

The Energen deal was different. This wasn't just buying acreage—it was buying a competitor with nearly a century of operating history. "This transaction represents a transformational moment for both Diamondback and Energen shareholders as they are set to benefit from owning the premier large cap Permian independent with industry leading production growth, operating efficiency, margins and capital productivity", said Travis Stice.

The numbers were compelling. The combination brought more than 266,000 net tier one acres in the Permian Basin, an increase of 57 percent from Diamondback's current tier one acreage of approximately 170,000 net acres. Pro forma production would exceed 222,000 barrels of oil equivalent per day, making Diamondback the third-largest pure-play Permian producer.

But what really excited Stice were the synergies. Diamondback and Energen officials estimate the combination of the two will save $2 billion with drilling, completion and equipment cost savings of up to $200 per lateral foot across over 2,000 net operated locations in the Midland Basin. Think about that—$200 per foot of savings across thousands of wells. In an industry where a typical horizontal well might have 10,000 feet of lateral, that's $2 million per well in savings.

The market initially hated it. Diamondback's stock fell 12% on the announcement, with investors worried about dilution and integration risk. But Stice had learned something crucial in his years building Diamondback: in commodities, scale matters. Being able to negotiate better rates with service providers, optimize drilling schedules across a larger asset base, and spread fixed costs over more production—these advantages compound over time.

By November 2018, Diamondback announced that it has completed its acquisition of Energen Corporation. The merger was previously approved by Diamondback stockholders and Energen shareholders at special meetings held on November 27, 2018.

Between these headline deals, Diamondback was also executing a "string of pearls" strategy—smaller bolt-on acquisitions that filled in its acreage map and eliminated drilling hazards. In October 2018, the company acquired the assets of Ajax Resources for $1.25 billion, adding critical acreage in the Northern Midland Basin.

The transformation was remarkable. "In a world where capital discipline is now the primary theme across North American energy and companies are discussing what they plan to do, look no further than what Diamondback has done over the past three years", Stice said. The company had grown production 45% while generating positive free cash flow—a feat almost unheard of in the shale patch.

But the acquisition playbook wasn't just about getting bigger. It was about getting better. Each deal brought new techniques, new data, new relationships. Energen's employees, many with decades of Permian experience, joined Diamondback's ranks. The combined company now had the intellectual capital of multiple organizations, all focused on a single goal: becoming the lowest-cost, most efficient operator in the Permian.

The financial engineering was equally sophisticated. Rather than loading up on debt like many peers, Diamondback funded acquisitions through a mix of equity, cash flow, and modest borrowing. As of Sept. 30, Diamondback had $492 million in standalone cash and no outstanding borrowings under its revolving credit facility even after completing billions in acquisitions.

"Our operating philosophy has not changed: Maximize production growth within cash flow, maintain best-in-class operating metrics, low leverage and execute on acquisitions accretive to our current acreage position and per share metrics", Stice explained.

The 2017-2020 period established Diamondback as the Permian's apex predator. But this was just the prelude. The real test would come when oil prices collapsed, capital markets froze, and the industry faced its greatest crisis in a generation. COVID-19 was about to change everything.

V. The QEP Resources Deal & Consolidation Strategy (2020–2021)

The phone rang at 3:47 AM on April 20, 2020, in Travis Stice's Midland home. His operations chief was on the line, voice shaking: "Travis, you need to see this. WTI just went negative. Negative thirty-seven dollars." Stice sat up in bed, sure he'd misheard. In nearly four decades in the oil business, he'd never imagined oil could trade below zero. But there it was on his Bloomberg terminal: At one point on 20 April 2020, the West Texas Intermediate (WTI) benchmark of crude oil prices dropped to US$–$37.63 per barrel.

This was the nightmare scenario every oil executive had secretly feared but never truly believed possible. In the first half of 2020, responses to the COVID-19 pandemic led to steep declines in global petroleum demand and to volatile crude oil markets. The second half of the year was characterized by relatively stable prices as demand began to recover.

For Diamondback, the COVID crash wasn't just a crisis—it was an opportunity to prove whether all that talk about being a low-cost operator actually meant something when oil prices literally went negative. The company had just closed the massive Energen acquisition sixteen months earlier. Now, with the world shutting down and the pandemic reducing global demand for oil by about 29 million barrels a day from about 100 million a year ago, the entire thesis of Permian consolidation was being tested in real-time.

But while the rest of the industry panicked, Stice saw opportunity. On December 21, 2020, as oil prices still languished below $50 per barrel and most companies were slashing budgets, Diamondback announced it would acquire QEP Resources in an all-stock transaction. Under the terms of the definitive merger agreement, stockholders of QEP will receive 0.05 shares of Diamondback common stock in exchange for each share of QEP common stock, representing an implied value to each QEP stockholder of $2.29 per share based on the closing price of Diamondback common stock on December 18, 2020.

The deal structure was telling. No cash. No premium. Just a stock-for-stock merger at market prices. This wasn't a bailout—it was consolidation at its most disciplined. "Diamondback's expectations for capital allocation in 2021 remain unchanged: we are expecting to hold pro forma fourth quarter 2020 oil production flat through 2021 in the most capital efficient manner possible, which has improved with today's announcements", Stice stated.

Think about the contrarian nature of this move. While other companies were fighting for survival, Diamondback was playing offense. The QEP deal brought about 49,000 net acres in Midland basin. The company reported third-quarter 2020 average production of 48,300 bo/d, with average Permian basin production of 30,500 bo/d (47,600 boe/d). But perhaps more importantly, it brought 48 current drilled but uncompleted wells (DUC), which it plans to work down along with its own DUC balance in 2021.

Those DUCs—drilled but uncompleted wells—were like money in the bank. Wells that had already been drilled when costs were higher, waiting to be completed when prices recovered. For a company obsessed with capital efficiency, this was the ultimate arbitrage: acquire wells drilled at $70 oil and complete them as prices recovered from the COVID trough.

The integration was swift and ruthless in its efficiency. Diamondback announced that it has completed its previously announced acquisition of QEP Resources, Inc. in an all-stock merger following approval by the QEP stockholders at their special meeting held on March 16, 2021.

But the QEP deal was just part of a broader consolidation strategy. In February 2021, the company acquired leasehold interests and assets from Guidon Resources for $375 million in cash and 10.68 million shares. The Guidon acquisition was another bolt-on, filling in Diamondback's Northern Midland position with contiguous acreage that could be developed with longer laterals and better economics.

"This deal, along with our recently completed acquisition of certain assets from Guidon Operating LLC (the "Guidon acquisition") bolsters our depth of Tier 1 Midland Basin inventory and positions us to allocate a majority of our capital to the high-returning Midland Basin for the foreseeable future," stated Travis Stice.

The philosophy was clear: while others were retrenching, Diamondback was consolidating. But this wasn't the growth-at-any-cost mentality of the pre-2020 shale era. This was disciplined, returns-focused consolidation. "Our differentiated cost structure, combined with the addition of this top quartile resource, will allow Diamondback to consistently generate free cash flow and grow our return of capital program to our stockholders".

The market dynamics during this period were fascinating. "The deal is structured with no premium and all-stock consideration. It focuses on immediately boosting cash flow to fund shareholder capital returns and debt reduction," Dittmar said. This was a new playbook for oil and gas M&A—no premiums, no bidding wars, just disciplined consolidation at market prices.

What made Diamondback's COVID-era strategy so effective was its financial flexibility. Diamondback remains committed to conservative financial management and is expected to maintain its Investment Grade credit ratings pro forma for the transaction. While competitors were negotiating with banks to avoid covenant breaches, Diamondback was shopping for assets.

The operational discipline during this period was equally impressive. Rather than shutting in wells completely during the price collapse—which can damage reservoirs permanently—Diamondback carefully managed production, reducing activity but maintaining operational continuity. This meant that when prices recovered, the company could ramp up quickly without the operational hiccups that plagued competitors who had completely shut down.

Tim Cutt, President and Chief Executive Officer of QEP, captured the strategic logic: "The large contiguous Tier-1 acreage position in the Northern Midland Basin is expected to lead to operational synergies and deliver capital efficiencies beyond what each company could achieve independently".

By the time oil prices recovered to $70 per barrel in mid-2021, Diamondback had emerged from the COVID crisis stronger than ever. The pending QEP acquisition, together with the previously announced pending acquisition of assets from Guidon Operating LLC ("Guidon"), will bring Diamondback's total leasehold interests to over 276,000 net surface acres in the Midland Basin (429,000 Midland and Delaware Basin net acres).

The transformation was complete. The company that couldn't find a buyer in 2012 had become the consolidator of choice in the Permian Basin. But this was about to be tested at an entirely new scale, as Diamondback prepared for its biggest acquisition yet.

VI. The Endeavor Mega-Merger: Creating a Permian Giant (2024)

The boardroom on the 27th floor of Diamondback's Midland headquarters was hushed as Travis Stice reviewed the numbers one more time. February 11, 2024, 11:47 PM. In less than eight hours, he would announce the biggest deal of his career—a $26 billion merger with Endeavor Energy Resources, the company literally across the street that had been the white whale of Permian acquisitions for over a decade.

But this wasn't just another acquisition. This was the culmination of everything Diamondback had built—a deal so transformative it would create the largest pure-play Permian operator in America. The transaction consideration would consist of approximately 117.3 million shares of Diamondback common stock and $8 billion of cash, a structure that spoke to both the magnitude of the opportunity and the discipline Diamondback had maintained even at this scale.

The story of how this deal came together reads like a West Texas epic. On one side stood Travis Stice, the geologist who couldn't give his company away in 2012. On the other, Autry Carl Stephens, who founded Endeavor Energy Resources in 1979, a legendary wildcatter born to watermelon and peanut farmers who had built one of the last great independent oil companies in America. The fact that the acquiring company is headquartered across the street, with a boss in Travis Stice whom Stephens has known for many years, were key to making the deal happen.

Stephens, at 85 years old, had never sold anything. His mantra throughout decades in the oil business was simple: "Never sell." Although Stephens signed a deal in February to divest his Endeavor Energy Resources to downtown Midland neighbor and peer Diamondback Energy for $26 billion in cash and stock, his mantra over the decades was "never sell". But he told the Wall Street Journal in February 2024 that he had been diagnosed with prostate cancer, which made him willing to sell Endeavor.

The announcement on February 12, 2024, sent shockwaves through the energy world. Diamondback Energy Inc. surged more than 10% after agreeing to buy fellow Permian Basin driller Endeavor Energy Resources LP, making it the day's second-best performer in the S&P 500 Index—an unusual reaction for an acquirer in such a massive transaction. Wall Street's enthusiasm reflected something deeper: this wasn't just consolidation for consolidation's sake. This was strategic brilliance.

"We are pleased to announce the closing of this transformative merger, creating a 'must own' North American independent oil company," said Travis Stice. The numbers backed up the rhetoric. The newly combined entity has pro forma production of about 816,000 barrels of oil equivalent per day and total Permian acreage of about 838,000 net acres. To put that in perspective, the combined company would produce more oil than several OPEC nations.

But what made the Endeavor acquisition truly special wasn't just the scale—it was the fit. Diamondback's and Endeavor's assets compliment each other very well, paving the way for the combined company to produce crude more efficiently. Endeavor brought around 470,000 net acres across various basins, including a concentrated 344,000 net acres in the Core 6 counties of the Midland Basin—acreage that perfectly interlocked with Diamondback's existing position.

The synergies were staggering. The strategic benefit of the merger is evidenced by substantial cost and revenue synergies estimated at $550 million annually, representing a $3.0 billion NPV10 over the next decade. Detailed breakdowns indicate approximately $325 million for capital and operating cost synergies, $150 million for capital allocation and land synergies, and $75 million for financial and corporate cost synergies.

Endeavor employs 1,200 people and guaranteeing no layoffs was important for the founder, as was keeping the company in Midland. This wasn't the slash-and-burn consolidation that had characterized earlier industry mergers. This was about combining two organizations with similar DNA—both obsessed with operational excellence, both committed to the Permian, both understanding that in commodities, efficiency is everything.

The regulatory scrutiny was intense. The merger withstood extensive reviews by the Federal Trade Commission — which also carefully scrutinized ExxonMobil's purchase of Pioneer Natural Resources, Chevron's acquisition of Hess Corp. and Occidental Petroleum's deal to purchase CrownRock. But on September 10, 2024, Diamondback announced that it has closed its merger with Endeavor Energy Resources.

The closing marked not just the end of one era but the beginning of another. Following the merger, Diamondback's existing shareholders own approximately 60.5% of the combined entity while Endeavor's equity holders own the remaining 39.5% interest. For Stephens and his family, who had never sold a single asset in 45 years, this represented not an exit but a transformation—from operators to major shareholders in what had become the Permian's dominant force.

The combined companies will deploy fewer drilling rigs overall but still deliver output growth at some point in the future, said Diamondback President Kaes Van't Hof. "Our shareholders are not paying us for growth these days," Van't Hof said. "They want return of capital". This philosophy—returns over growth—represented the maturation not just of Diamondback but of the entire shale industry.

The market implications were profound. The agreement swells the value of recent shale takeovers to roughly $150 billion as oil executives scramble to pad portfolios with future drilling sites and shore up cash flows. The impacts will be felt far afield from the Permian Basin of West Texas and New Mexico, where rampant output growth is challenging the OPEC+ alliance's efforts to curb global crude supplies and prop up prices.

But perhaps the most poignant moment came on August 16, 2024, just weeks before the merger closed. Endeavor Energy Resources announced the passing of its Founder and Chairman of the Board, Autry C. Stephens, age 86. The wildcatter who had started with a single well in 1979, who had survived the busts of the 1980s, 1990s, and 2000s, who had built a company worth $26 billion, wouldn't see the final closing. But his legacy—1,200 jobs, billions in value creation, and a template for independent oil operations—would live on in the combined company.

"Our high-quality inventory located in the heart of the Permian Basin gives us the running room to do what we do best: turn rock into cash flow", Stice said after the closing. The Endeavor merger wasn't just about getting bigger. It was about securing Diamondback's position for the next decade and beyond, ensuring it had the scale, the inventory, and the operational excellence to thrive regardless of where oil prices went.

The combined company now controlled more Permian acreage than ExxonMobil had before its Pioneer acquisition. It had more production than Continental Resources. It had lower costs than almost any operator in North America. Diamondback had transformed from a company nobody wanted into the company everyone had to own.

VII. The Shale Revolution & Technology Evolution

Stand on the caliche roads cutting through the Permian Basin today, and you'll see a landscape that would be unrecognizable to the wildcatters of even twenty years ago. Where lone pump jacks once bobbed lazily in the West Texas heat, massive drilling rigs now march across the desert like mechanical armies, capable of drilling wells two miles down and three miles sideways in less than two weeks. This is the shale revolution in physical form, and Diamondback Energy has been both its beneficiary and its architect.

The transformation of American energy independence through shale is one of the great technological and economic stories of the 21st century. The Permian Basin is the cornerstone of oil-production growth in the US. The nation's output surged to a record high last year — besting Saudi Arabia by about 45% — thanks largely to wells in the Permian that can be drilled and fracked cheaper and faster than those in many other regions.

To understand Diamondback's role in this revolution, you need to understand what makes shale different. Conventional oil sits in underground pools, waiting to be tapped like an underground lake. Shale oil is trapped in rock so tight that a drop of water would take a million years to move an inch through it. The oil is there—the Permian has always had oil—but it was locked away, inaccessible, worthless.

The revolution came through the marriage of two technologies: horizontal drilling and hydraulic fracturing. Horizontal drilling let operators turn the drill bit sideways, following the thin layers of oil-bearing rock for miles underground. Hydraulic fracturing—fracking—used high-pressure water, sand, and chemicals to crack open the rock, creating pathways for the oil to flow. Neither technology was new, but their application to shale, at scale, in places like the Permian, changed everything.

Diamondback didn't invent these technologies, but it perfected their application. When the company went public in 2012, a typical horizontal well in the Midland Basin took 30 days to drill and cost $9 million. By 2024, Diamondback could drill the same well in 12 days for $6 million, while extracting 50% more oil. This wasn't incremental improvement—it was revolution through repetition.

The operational innovations were countless, each one seemingly minor but collectively transformative. Walking rigs that could move from well to well without being disassembled, saving days of rig time. Zipper fracking, where multiple wells were fracked simultaneously, cutting completion times in half. Automated drilling systems that could maintain perfect well trajectories without human intervention. Big data analytics that could predict the best spots to drill based on microscopic analysis of rock samples.

"We've been pushing the limits of efficiency," became Diamondback's unofficial motto. But this wasn't efficiency for its own sake—it was efficiency as survival mechanism. In the commodity business, the only sustainable competitive advantage is being the lowest-cost producer. Every dollar saved per barrel was a dollar of cushion against the next price crash, which in oil markets was never a question of if but when.

The Permian Basin itself was the perfect laboratory for this revolution. Its geology was a layer cake of oil-bearing formations—the Spraberry, the Wolfcamp A, B, and C, the Bone Spring—each one a separate target that could be developed with horizontal wells. A single surface location could host a dozen wells, each one diving down and then spreading out in different directions like the roots of a tree, each one tapping a different layer of rock.

Diamondback's acreage position, built through years of acquisitions, gave it the scale to innovate. With hundreds of wells drilling at any given time, the company could test new techniques, measure results, and rapidly deploy successful innovations across its entire operation. A 5% improvement in drilling speed, multiplied across hundreds of wells, translated to millions in savings.

The technology evolution wasn't just about drilling. It was about data. Every well generated terabytes of information—pressure readings, flow rates, chemical compositions. Diamondback built systems to capture, analyze, and learn from this data. Machine learning algorithms could predict which combination of factors would produce the best wells. Reservoir simulations could model how wells would interact with each other over decades.

The environmental side of the technology evolution was equally important, though less celebrated. Despite its reputation, modern shale drilling was remarkably efficient in its use of land. A single pad, no bigger than a football field, could host 20 wells that would drain oil from 10,000 acres underground. Water recycling systems could reuse 90% of the water used in fracking. Automated leak detection systems could identify and fix methane leaks before they became problems.

But the real revolution was in the speed of the learning curve. In conventional oil fields, it might take decades to optimize production. In shale, with thousands of wells being drilled each year, the industry could iterate and improve at Silicon Valley speeds. Techniques that were cutting-edge in 2020 were obsolete by 2024.

The implications went far beyond the oil patch. The shale revolution turned the United States from an energy importer to an energy exporter, fundamentally altering global geopolitics. OPEC's ability to control oil prices was permanently weakened. American manufacturers gained a competitive advantage from cheap energy. The entire structure of global energy markets was rewritten.

For Diamondback, being at the forefront of this revolution meant more than just profits. It meant being part of one of the great American industrial success stories. The company that couldn't find a buyer in 2012 had become a master of the technology that reshaped global energy markets.

Yet even as Diamondback celebrated its technological achievements, questions loomed. How much more efficient could drilling become? How many more layers of rock could be exploited? How long could the revolution continue? The answers to these questions would determine not just Diamondback's future, but the future of American energy independence itself.

VIII. Peak Shale Debate & Market Dynamics (2025–Present)

The letter landed like a bombshell in energy markets on May 5, 2025. Travis Stice, CEO of Diamondback Energy, told investors bluntly: "It is likely that U.S. onshore oil production has peaked and will begin to decline this quarter." "This will have a meaningful impact on our industry and our country."

For an industry that had spent fifteen years proving the pessimists wrong, transforming America from energy importer to the world's largest producer, this was heresy. But coming from Stice—the CEO of the Permian's most efficient operator, fresh off closing the largest pure-play merger in basin history—the words couldn't be dismissed as doom-mongering.

"We believe we are at a tipping point for U.S. oil production at current commodity prices," Stice wrote in his shareholder letter, his last before transitioning to Executive Chairman. The numbers backed up his pessimism. Adjusted for inflation, there have only been two quarters since 2004 when front-month oil prices have been as cheap as they are now, excluding 2020 when the Covid-19 pandemic swept the world.

The drilling activity collapse was already underway. The number of crews fracking shale for oil and gas had already fallen 15% in 2025, with crews in the Permian Basin down 20% from a peak in January. Rigs focused on oil production were expected to decline nearly 10% by the end of the second quarter and fall further in the third.

But this wasn't just about low prices. This was about the maturation of a miracle that couldn't last forever. "Over the past decade, the cost of supply for the average barrel of oil produced in the U.S. has increased," Stice wrote, noting that geologic barriers now outweigh the marginal uplifts provided by technological improvements and operating efficiencies.

The efficiency gains that had powered the shale revolution were hitting their limits. "We've tripled oil production in the last 15 years, and we have doubled natural gas production. But there's not a lot of gas left in the tank," warned Wil VanLoh, chief executive of Quantum Energy Partners.

Stice wasn't alone in sounding the alarm. At CERAWeek in Houston, Occidental CEO Vicki Hollub said she expects U.S. oil production to peak between 2027 and 2030. ConocoPhillips chief Ryan Lance gave a similar timeline. Even the eternally optimistic Harold Hamm of Continental Resources acknowledged the slowdown.

The immediate catalyst for Diamondback's warning was economic. Trump's steel tariffs were the biggest cost headwind the oil producer was fighting, increasing well costs by about 1% or $40 million annually. Combined with recession fears and OPEC+ flooding the market with supply, the economics of drilling new wells had turned negative for many operators.

Diamondback cut its capital budget by about $400 million to $3.4 billion to $3.8 billion for the year. The company dropped three rigs and one completion crew, expecting to remain at these levels through the majority of the third quarter.

"To use a driving analogy, we are taking our foot off the accelerator as we approach a red light," Stice said. "If the light turns green before we get to the stoplight, we will hit the gas again, but we are also prepared to brake if needed." The green light, he explained, would be oil prices returning to $65-70 per barrel—$5-10 higher than current levels.

The philosophical shift was profound. For fifteen years, the shale industry had been about growth—proving doubters wrong, adding rigs, drilling faster, producing more. Now, it was about preservation. Diamondback President Kaes Van't Hof, taking over as CEO from Stice, said more decisions were being made to "preserve precious inventory"—future drilling opportunities—and not just to save money.

"The marginal barrel in the U.S. is just not being produced today," Van't Hof stated bluntly. "We don't have a crystal ball on the rest of the world, but we have a very good view of what the U.S. looks like, and right now, that's a business that's slowing dramatically and likely declining in terms of production."

The implications rippled far beyond Diamondback's earnings call. Over the past 15 years, the industry had grown U.S. oil production by 8 million barrels per day to over 13 million barrels per day. This growth alone would make the United States the third largest oil producer in the world. Combining both oil and gas production, the United States produces more than the second and third largest producers, Russia and Saudi Arabia, combined.

"This has transformed our economy and given the United States a level of energy security not thought possible at the beginning of this century," Stice told investors. "Today's prices, volatility and macroeconomic uncertainty have put this progress in jeopardy."

The debate over peak shale wasn't academic—it had real-world consequences. A decline in domestic production would affect both U.S. and global consumers, increasing U.S. net oil imports and potentially restoring dependence on foreign supplies while intensifying competition with other buyers.

Yet there were skeptics. The Energy Information Administration revised its forecasts, noting that US oil production has continued to expand despite weaker prices and lower rig counts. Shale drillers were signaling there is still space to grow, so those expecting a decline after the peak will have to wait longer.

The debate reflected a fundamental tension in the shale business. On one hand, the geological and economic realities were becoming harder to ignore—the best rocks had been drilled, the easy efficiency gains captured, the costs rising. On the other hand, the industry had defied predictions of peak production before, always finding new ways to squeeze more oil from the rocks.

Depending on how much oil prices fall, the amount of capital needed for the U.S. to produce 13 million barrels per day and for the Permian to produce 6 million bpd "might be an untenable lift for the business model that we put in place, where we're returning so much back to our investors who own the company," Stice explained.

This was the crux of the issue: the shale revolution had succeeded so thoroughly that it had changed its own economics. Investors no longer wanted growth at any cost—they wanted returns. "Our shareholders are not paying us for growth these days. They want return of capital," Van't Hof emphasized.

The energy transition added another layer of complexity. While politicians debated green new deals and net-zero targets, the immediate reality was that global oil demand might require an additional 5% more oil annually than previously estimated from 2035 onwards, due to the slower-than-planned transition. By 2050, the world would need an extra 100 billion barrels of both oil and gas to balance supply with demand.

For Diamondback, navigating this new era required a different playbook than the one that had brought it success. The company that had grown production by a factor of 100 was now focused on maintaining flat production while maximizing cash flow. The consolidator was done consolidating. The growth story had become a returns story.

As Stice prepared to hand over the CEO role to Van't Hof, his final message to shareholders was both a warning and a reflection: "This will have a meaningful impact on our industry and our country"—a reminder that the future of the US energy industry and perhaps worldwide oil production growth rates hung in the balance.

The question was no longer whether American shale production would peak—it was whether it already had.

IX. Playbook: Business & Investing Lessons

If you had to distill Diamondback Energy's journey from unwanted startup to $50 billion Permian giant into actionable lessons, you'd start with a simple truth: in commodity businesses, you don't control the product price, so you must control everything else with religious fervor. This isn't Silicon Valley, where network effects and software margins can paper over operational mediocrity. This is oil and gas, where a 5% cost advantage can mean the difference between fortune and bankruptcy.

Lesson 1: The Low-Cost Producer Always Wins Eventually

From day one, Diamondback understood that being the low-cost operator wasn't just an advantage—it was the only sustainable moat in commodities. When oil was at $100 per barrel, everyone made money. When it went negative in 2020, only the efficient survived. Diamondback's obsession with costs meant it could generate free cash flow at $40 oil while competitors needed $60 just to break even.

The numbers tell the story: drilling costs fell from $9 million per well in 2012 to $6 million in 2024, while production per well increased 50%. This wasn't luck or geological advantage—it was thousands of micro-optimizations compounding over time. Walking rigs that saved three days per move. Zipper fracking that cut completion times in half. Supply chain negotiations that shaved 10% off sand costs. Individually minor, collectively transformative.

Lesson 2: Scale Matters, But Only If You Can Execute

The conventional wisdom in oil and gas was that bigger meant less nimble, more bureaucratic, slower to adapt. Diamondback proved the opposite. Each acquisition—from Brigham to Energen to Endeavor—made the company more efficient, not less. Why? Because scale in the Permian meant bargaining power with service companies, better data from more wells, and the ability to deploy best practices across a larger asset base.

But scale without execution is just obesity. Diamondback's genius was maintaining startup-level efficiency at major-company scale. They kept headquarters lean—fewer than 500 employees running a company producing 850,000 barrels per day. They integrated acquisitions ruthlessly, taking the best from each company and discarding the rest. They never confused activity with progress.

Lesson 3: Capital Allocation Is Everything

Travis Stice's greatest insight wasn't geological or operational—it was financial. In an industry notorious for destroying capital, Diamondback became a capital allocation machine. During boom times, they bought assets. During busts, they bought more assets, cheaper. When investors wanted growth, they grew. When investors wanted returns, they pivoted to dividends and buybacks without missing a beat.

The Viper Energy spinoff exemplified this thinking. Rather than keeping mineral rights buried in the operating company, they created a separate vehicle that appealed to income investors. Value wasn't created through drilling—it was unlocked through structure. The same assets, arranged differently, were worth billions more.

Lesson 4: Timing Beats Genius

Diamondback went public not because it wanted to, but because it had to—nobody would buy the company privately. That apparent failure became its greatest success. Being public in 2012 meant access to capital just as the shale revolution accelerated. Being disciplined when others were reckless meant having dry powder when assets came up for sale.

The Endeavor acquisition in 2024 was masterful timing. Oil prices were strong enough to justify the deal but not so strong that Endeavor's owners would hold out for more. The regulatory environment was still permissive. The capital markets were receptive. Six months earlier or later, the deal might not have happened.

Lesson 5: Culture Compounds

Every oil company talks about operational excellence. Diamondback lived it. The culture wasn't about working harder—it was about questioning everything. Why does it take 20 days to drill a well? Why not 15? Why not 12? Why do we need three crews for this job? Why not two?

This wasn't cost-cutting for its own sake. It was intellectual honesty about what actually created value. In Silicon Valley, founders talk about "first principles thinking." In Midland, Texas, Diamondback was doing it with drill bits and fracking fluid.

Lesson 6: The Shift from Growth to Returns

Perhaps the most important lesson is knowing when to change strategy. For a decade, Diamondback was a growth story. Production increased 100-fold. Acreage expanded from 4,000 to 800,000 acres. But by 2020, the game had changed. Investors no longer wanted the next barrel—they wanted returns on the current barrel.

Lesser companies would have kept drilling, kept acquiring, kept growing until they hit a wall. Diamondback recognized the shift and adapted. Growth capex became return of capital. The acquisition machine became a cash flow machine. The company that couldn't find a buyer became the company returning billions to shareholders.

Lesson 7: Consolidation Creates Value

In fragmented industries, consolidation isn't just about getting bigger—it's about reducing redundancy, optimizing operations, and creating economies of scale. Every Diamondback acquisition followed a playbook: identify operational inefficiencies, apply best practices, eliminate redundancy, optimize drilling schedules, renegotiate service contracts.

The Endeavor merger alone was expected to generate $550 million in annual synergies. That's not from drilling more wells or finding more oil—it's from doing the same thing better. In commodities, where you don't control price, operational efficiency is the only source of sustainable value creation.

Lesson 8: Technology Enables, Execution Delivers

Horizontal drilling and fracking weren't Diamondback innovations—they were industry-wide technologies. But Diamondback applied them better. They drilled longer laterals, fracked more stages, optimized proppant loads, reduced water usage. The technology was the same; the execution was superior.

This extends beyond drilling. Data analytics, machine learning, automation—every company had access to these tools. But Diamondback integrated them into operations rather than treating them as side projects. A machine learning model that could predict optimal well spacing wasn't a research project—it was deployed across hundreds of wells, saving millions.

Lesson 9: Manage Through the Cycle

Oil prices went from $147 to $33 to negative $37 to $120 during Diamondback's public life. Lesser companies would have been whipsawed, growing aggressively during booms and retrenching during busts. Diamondback maintained discipline throughout. They grew when it made sense, acquired when assets were cheap, and returned capital when growth wasn't valued.

This wasn't luck or prescience—it was process. The company built a balance sheet that could survive $30 oil. They hedged production to protect against downside. They maintained credit facilities for opportunity. They were always prepared for the next phase of the cycle, whatever it might be.

Lesson 10: Know When the Game Has Changed

Travis Stice's declaration that U.S. oil production had peaked wasn't defeatism—it was realism. The easy gains had been captured. The best rocks had been drilled. The efficiency improvements were reaching diminishing returns. Fighting these realities would destroy value, not create it.

The playbook that worked from 2007 to 2024—growth through drilling and acquisitions—wouldn't work from 2025 forward. The new playbook—capital returns, operational excellence, and inventory preservation—reflected new realities. Great companies don't just execute well; they recognize when the rules have changed and adapt accordingly.

These lessons extend far beyond oil and gas. Any commodity business—mining, agriculture, chemicals—faces the same fundamental challenge: you don't control price, only cost. Any industry consolidation—from banking to airlines to technology—follows similar patterns. Any company transition—from growth to maturity—requires similar pivots.

Diamondback's story isn't just about drilling holes in Texas. It's about building a machine that could thrive regardless of external conditions, that could grow when growth was valued and return capital when it wasn't, that could consolidate an industry while maintaining operational excellence. It's a playbook for succeeding in the hardest kind of business: one where you don't control the most important variable.

X. Analysis & Bear vs. Bull Case

Standing at the precipice of what might be peak shale, evaluating Diamondback Energy requires confronting two radically different futures for American oil. Is this the beginning of the end for the shale revolution, or merely a pause before the next act? The answer determines whether Diamondback is a mature cash cow or a stranded asset.

Bull Case: The Premier Permian Machine

The optimists' case starts with an undeniable fact: Diamondback has assembled the finest collection of Permian assets ever held by an independent operator. As of December 31, 2024, the company had 3,557 million barrels of oil equivalent of estimated proved reserves, up 63% year over year. Proved undeveloped reserves increased to 1,173 MMBOE, a 72% increase over year-end 2023, and are comprised of 1,381 horizontal locations.

This isn't just about quantity—it's about quality and execution. The company's ability to generate returns at current commodity prices remains unmatched. Diamondback's exploration and development costs in 2024 were $10.51/BOE, among the lowest in the industry. This cost structure provides a buffer that few competitors can match.

The scale achieved through the Endeavor merger creates operational advantages that compound over time. With 838,000 net acres of largely contiguous Permian acreage, Diamondback can optimize drilling schedules, negotiate better service contracts, and deploy technology improvements across a massive asset base. The $550 million in annual synergies from the Endeavor deal alone could fund significant shareholder returns even at depressed commodity prices.

Capital allocation discipline sets Diamondback apart. Unlike the cowboys of the early shale era, management has proven it can pivot from growth to returns without destroying value. The company increased its annual base dividend by 11% to $4.00 per share even while warning about peak production, demonstrating confidence in its ability to generate cash flow regardless of growth prospects.

The balance sheet remains fortress-like, with investment-grade ratings providing financial flexibility that most competitors lack. This matters enormously in a cyclical industry—when the next upturn comes, Diamondback will have the firepower to capitalize while overleveraged competitors struggle to survive.

Technology and efficiency gains, while slowing, haven't stopped entirely. The Company expects to drill between 446-471 gross wells and complete between 557-592 gross wells with an average lateral length of approximately 11,500 feet in 2025. Longer laterals, better completion techniques, and optimized spacing continue to improve recovery rates and reduce costs incrementally.

Finally, the global context supports the bull case. Despite the energy transition narrative, oil demand continues to grow. The slower-than-expected adoption of electric vehicles, continued industrialization in developing nations, and the lack of viable alternatives for aviation and shipping mean oil will remain essential for decades. In this world, the lowest-cost producers with the best assets—companies like Diamondback—will be the last ones standing.

Bear Case: The Twilight of Shale

The pessimists' case begins with Travis Stice's own words: "It is likely that U.S. onshore oil production has peaked and will begin to decline this quarter". When the CEO of the Permian's most successful operator declares the game is ending, investors should listen.

The geological reality is increasingly difficult to ignore. "Over the past decade, the cost of supply for the average barrel of oil produced in the U.S. has increased," with geologic barriers outweighing the marginal uplifts provided by technological improvements and operating efficiencies. The best acreage has been drilled. The easy efficiency gains have been captured. What's left is increasingly marginal.

Commodity price volatility poses an existential threat. U.S. crude oil prices have tumbled about 17% this year as recession fears due to President Donald Trump's tariffs weigh on demand expectations. At the same time, OPEC+ producers led by Saudi Arabia are rapidly increasing supply to the market. In a world of $50 oil, even Diamondback's superior cost structure gets tested.

The capital allocation dilemma is becoming acute. The amount of capital needed for the U.S. to produce 13 million barrels per day "might be an untenable lift for the business model that we put in place, where we're returning so much back to our investors". The company can't simultaneously maintain production, return cash to shareholders, and preserve inventory for the future. Something has to give.

Regulatory and legal challenges are mounting. In January 2024, a class action lawsuit was filed accusing Diamondback, along with seven other US oil and gas producers, of an illegal price fixing scheme. Environmental regulations continue to tighten, and the social license to operate in the oil and gas industry faces increasing scrutiny.

The efficiency gains that powered Diamondback's rise are reaching their limits. "We've tripled oil production in the last 15 years... But there's not a lot of gas left in the tank". Without the ability to continually reduce costs, Diamondback becomes just another commodity producer at the mercy of global oil prices.

Peak shale production threatens the entire investment thesis. If U.S. production begins declining, Diamondback transforms from a growth story to a melting ice cube. The company might generate cash for years, but without growth or the potential for growth, multiples compress and the stock becomes a value trap.

The Verdict: A Transition Story

The truth likely lies between these extremes. Diamondback isn't facing imminent collapse, nor is it poised for another decade of explosive growth. Instead, it's transitioning from adolescence to maturity—a process that rewards different skills and strategies than those that brought initial success.

The company's greatest strength—operational excellence—remains intact. Even in a declining production environment, being the lowest-cost operator means being the last one standing. Diamondback can generate significant cash flow at prices that would bankrupt competitors, providing a margin of safety that few energy investments offer.

The key question isn't whether U.S. shale production has peaked—it probably has or soon will. The question is whether Diamondback can successfully navigate the transition from a growth company to a cash-return vehicle. The early evidence is promising. Management has shown the discipline to cut activity when economics don't support drilling, the wisdom to preserve inventory for better days, and the commitment to return cash to shareholders regardless of growth prospects.

Full year 2025 oil production guidance of 485-498 MBO/d represents roughly flat production, signaling that management has accepted the new reality and is optimizing for returns rather than barrels. This isn't capitulation—it's adaptation.

For investors, Diamondback represents a fascinating risk-reward proposition. The downside seems limited by the company's superior asset base, low cost structure, and strong balance sheet. The upside depends on commodity prices and whether efficiency gains can surprise to the upside one more time. It's not the moonshot investment it was in 2012, but it might be exactly the kind of steady, cash-generating machine that energy investors need in an uncertain world.

The bear case is real and shouldn't be dismissed. But betting against the company that has consistently defied pessimists for nearly two decades requires believing that this time really is different. Maybe it is. Maybe the miracle of shale has finally run its course. But if there's one lesson from Diamondback's history, it's that writing off American ingenuity and operational excellence is usually a losing bet.

XI. Epilogue & "If We Were CEOs"

The West Texas sun sets blood orange over the Permian Basin, casting long shadows from the pump jacks that dot the landscape like mechanical monuments to American ambition. Travis Stice stands in his Midland office, looking out at a view that hasn't changed much in twenty years—except for the density of wells, the size of the rigs, and the fundamental transformation of global energy markets that happened right here, in this unlikely desert.

The journey from that desperate IPO in 2012 to today's $50 billion behemoth isn't just Diamondback's story—it's the story of American energy independence, of technological innovation defeating geological pessimism, of operational excellence triumphing over commodity volatility. But as Stice hands the CEO reins to Kaes Van't Hof, the question isn't what was accomplished, but what comes next.

The Next Decade: Three Scenarios

The future of Diamondback—and American energy—likely follows one of three paths:

Scenario 1: The Slow Decline - U.S. shale production peaks and gradually declines as the best rocks are exhausted and efficiency gains plateau. Oil prices stabilize at $70-80, high enough to generate cash but not high enough to justify aggressive drilling. Diamondback becomes a cash machine, returning billions to shareholders while slowly harvesting its remaining inventory. The company trades like a utility—stable, boring, profitable.

Scenario 2: The Innovation Surprise - Just as horizontal drilling and fracking unlocked resources thought impossible to extract, a new technology emerges. Perhaps it's AI-optimized drilling that finds bypassed pay. Perhaps it's enhanced oil recovery techniques that double recovery rates. Perhaps it's carbon capture that makes oil production carbon-neutral. Diamondback, with its technical expertise and financial resources, leads this next revolution. Production grows again, and the company enters a new golden age.

Scenario 3: The Energy Transition Acceleration - Climate policies accelerate, electric vehicle adoption hits an inflection point, and oil demand peaks sooner than expected. Prices collapse to $40 and stay there. Even Diamondback's low costs can't generate adequate returns. The company pivots, using its cash flow to transform into an energy company rather than just an oil company—investing in geothermal, carbon capture, or even renewable energy where its operational excellence can create value.

If We Were CEOs: The Playbook for 2025-2035

Standing in Travis Stice's shoes—or rather, Kaes Van't Hof's—what would we do? The strategy would focus on optionality, resilience, and intelligent capital allocation:

1. Preserve the Core, Explore the Edges Maintain disciplined development of Tier 1 acreage while experimenting aggressively with enhanced recovery techniques on Tier 2 and 3 assets. The goal isn't to grow production but to extend the runway of profitable drilling. Every 5% improvement in recovery rates adds years to the company's life.

2. Technology as Salvation Double down on technology investments, but not in drilling—that game is largely played out. Focus on production optimization, artificial lift efficiency, and especially on reducing operating costs. If Diamondback can reduce lifting costs by 30% through automation and AI, it changes the entire economic equation.

3. The Power Play The Permian has oil, gas, land, and sun. It also has a desperate need for power as data centers and industrial facilities seek cheap energy. Diamondback should leverage its surface acreage and gas production to become an integrated energy provider. Build gas-fired power plants on-site. Partner with tech companies needing reliable power for data centers. Create a second leg of earnings that isn't dependent on commodity prices.

4. International Optionality While staying focused on the Permian, selectively evaluate international opportunities where Diamondback's operational excellence could unlock value. The company's DNA—low-cost operations, technological sophistication, capital discipline—would translate well to other mature basins needing rejuvenation.

5. The Capital Allocation Barbell Implement a barbell strategy for capital allocation. On one end, return 75% of free cash flow to shareholders through dividends and buybacks—reward the investors who've stayed loyal. On the other end, invest 10% in moonshot technologies or adjacent businesses that could provide the next S-curve of growth. The remaining 15% goes to maintaining base production.

6. The Transition Hedge Accept that the energy transition is real but likely slower than advertised. Create optionality by investing in transition technologies that leverage existing competencies. Carbon capture and storage uses similar subsurface expertise. Geothermal requires drilling skills. These aren't abandoning oil and gas—they're expanding the definition of energy.

7. M&A Discipline in a Declining Market As U.S. production peaks, there will be distressed sellers. Resist the temptation to be the consolidator of last resort. Only acquire assets that are immediately accretive to cash flow per share and that don't significantly increase the denominator for per-share metrics. The goal is to get better, not bigger.

8. The Culture Challenge The hardest task might be maintaining operational excellence in a mature industry. When growth slows, talent leaves for the next hot sector. Combat this by becoming the "Google of oil and gas"—the place where the smartest engineers want to work because the problems are interesting, the culture is innovative, and the company is defining the future of energy, not just managing decline.

The Uncomfortable Truth

Here's what nobody in the C-suite wants to say publicly: The American shale revolution, as we've known it, is probably over. Not because we're running out of oil, but because we've extracted most of the easy value. The next decade will be about optimization, not revolution; about returns, not growth; about managing maturity, not chasing adolescence.

But this isn't necessarily bad news. Some of the world's best investments are mature companies that generate predictable cash flows and return them to shareholders. Diamondback has the assets, the operational capabilities, and the management culture to be one of these rare success stories—a growth company that successfully transitioned to a value company without destroying shareholder value in the process.

The Final Analysis

If we were running Diamondback, we'd embrace the transition. We'd stop fighting the narrative of peak shale and start defining what comes next. We'd position the company not as the last of the wildcatters but as the first of the new energy companies—disciplined, technological, profitable, and essential.

The Permian Basin will produce oil for decades to come. The question is who will produce it most efficiently, most profitably, and most responsibly. Diamondback has spent seventeen years proving it can be that company. The next decade is about proving it can remain that company as the world changes around it.

The sun has set on the growth era of American shale. But for companies like Diamondback, smart enough to adapt and disciplined enough to return capital, the twilight might be the most profitable time of all.

XII. Recent News

The story continues to unfold in real-time as Diamondback navigates the complexities of 2025's volatile energy markets. Here are the key developments shaping the company's trajectory:

Q2 2025 Financial Results: Resilience Amid Volatility

On August 4, 2025, Diamondback announced financial and operating results for the second quarter ended June 30, 2025. Despite challenging market conditions, the company demonstrated its operational resilience with net cash provided by operating activities of $1.7 billion and Operating Cash Flow Before Working Capital Changes of $2.1 billion.

Production remained robust with average oil production of 495.7 MBO/d (919.9 MBOE/d), staying within the company's guided range despite the activity reductions announced earlier in the year.

Capital Allocation: Returns Over Growth

The company's commitment to shareholder returns remained unwavering even as it warned about peak production. Diamondback's Board of Directors declared a base cash dividend of $1.00 per common share for the second quarter of 2025, maintaining the increased dividend despite market headwinds.

Share buybacks accelerated as the stock price declined. During the second quarter of 2025, Diamondback repurchased ~3.0 million shares of common stock at an average share price of $133.15 for a total cost of approximately $398 million. To date, Diamondback has repurchased ~32.9 million shares of common stock at an average share price of $137.86 for a total cost of approximately $4.5 billion.

Activity Adjustments: Responding to Price Signals

In response to commodity price volatility, Diamondback is reducing activity in order to prioritize free cash flow generation. The Company believes this revised plan enhances capital efficiency and provides flexibility to (i) cut additional capital if prices weaken further or (ii) resume its original 2025 plan if commodity prices strengthen.

The company is narrowing full year oil production guidance to 485 - 492 MBO/d and increasing annual BOE guidance by 2% to 890 - 910 MBOE/d, demonstrating its ability to maintain production levels despite reduced drilling activity through operational efficiency.

Strategic Consolidation: Double Eagle Acquisition

Diamondback announced the closing of its Double Eagle acquisition, further consolidating its Midland Basin position. This bolt-on acquisition follows the company's established playbook of acquiring assets during periods of market weakness.

Debt Management: Strengthening the Balance Sheet

In a notable move, Diamondback repurchased $252 million in aggregate principal amount across its Senior notes due 2031, 2051, 2052 and 2054 at a weighted average price of 76.8% of par (~$196 million), taking advantage of distressed debt prices to reduce future interest obligations.

Operational Excellence Continues

Despite market challenges, Diamondback maintained its operational edge. During the first quarter of 2025, Diamondback drilled 124 gross wells in the Midland Basin and 10 gross wells in the Delaware Basin. The Company turned 116 operated wells to production with an average lateral length of 11,978 feet.

Market Warnings Persist

The company continues to flag significant headwinds, with management highlighting concerns about inflationary pressures on the cost of products or services used in operations due to the imposition of tariffs, actions taken by OPEC and Russia affecting the production and pricing of oil, and instability in the financial markets.

The Viper Advantage

Diamondback's subsidiary Viper Energy continued its own growth trajectory, closing the acquisition of Sitio Royalties, further expanding its minerals and royalty portfolio and providing a steady stream of non-operated cash flow to the parent company.

Looking Ahead