Modine Manufacturing: The Century-Old Thermal Management Pioneer Riding the AI Wave

I. Introduction & Episode Roadmap

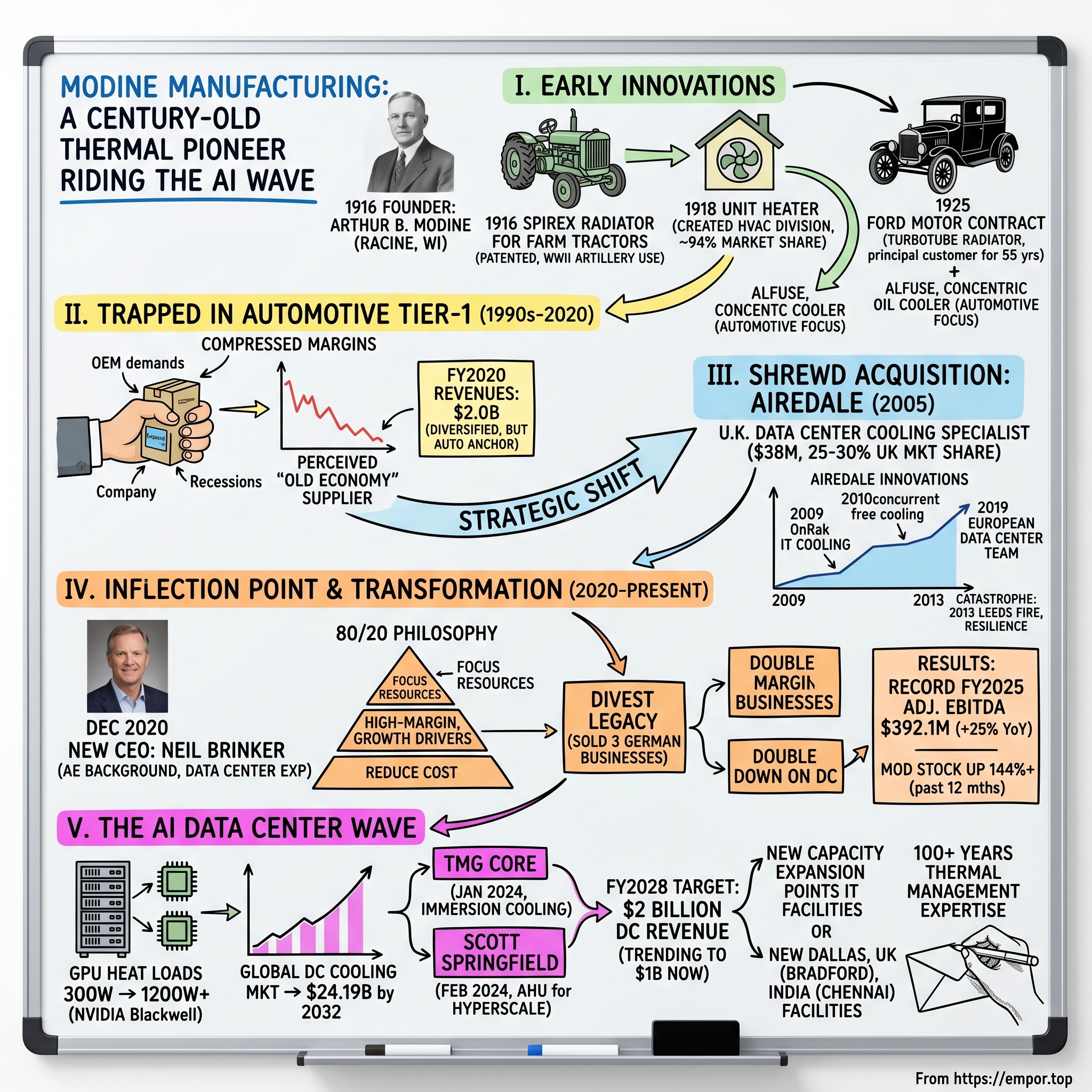

Picture this: A thermal management company founded in 1916 to make radiators for farm tractors—the kind of business you might expect to find quietly fading into obsolescence alongside steam engines and rotary phones. Instead, Modine Manufacturing, though the smallest public player in the data center cooling space, has become a near-perfect proxy for NVIDIA in equity growth.

How does a 108-year-old tractor radiator company become a pure-play bet on the AI revolution? The answer lies in a century of engineering excellence, a shrewd 2005 acquisition most analysts overlooked, and a CEO who arrived in December 2020 with a transformation playbook that would fundamentally rewire the company's DNA.

Modine Manufacturing annual revenue for 2025 was $2.584 billion, a 7.3% increase from 2024. Annual revenue for 2024 was $2.408 billion, a 4.78% increase from 2023. And annual revenue for 2023 was $2.298 billion, a 12.09% increase from 2022. But the headline numbers don't capture the seismic shift underway beneath the surface. Record adjusted EBITDA of $392.1 million in fiscal 2025 increased $77.8 million, or 25 percent, from the prior year. The company delivered a third consecutive year of record revenue and adjusted EBITDA, demonstrating the power of its 80/20 transformation.

MOD stock is up 144.17% over the past 12 months. The stock has transformed from a forgotten old-economy manufacturer trading in single digits during the 2020 pandemic low to a company with an $8 billion market capitalization. What happened?

The story of Modine is really two stories intertwined. The first is the tale of Arthur B. Modine, an engineer who revolutionized thermal management and built a company that would serve as a cornerstone supplier to Ford Motor Company for more than 55 years. The second is the tale of Neil Brinker, a transformation-minded CEO who took over in late 2020 and applied a ruthless 80/20 discipline to shed low-margin automotive businesses and double down on the explosive data center cooling opportunity.

Just days after announcing a planned $100 million investment to support its data center business, the company's CEO said it aims to reach $2 billion in data center revenue by fiscal 2028. Already, Modine is trending towards $1 billion in data center revenue this year.

The through-line connecting 1916 to 2025 is expertise in managing heat. Whether it's a Model T engine, a World War II tank, or an NVIDIA Blackwell GPU cluster, the fundamental physics remain the same: high-performance systems generate heat, and that heat must be managed efficiently or the system fails. Modine has spent over a century mastering that challenge. Now, the AI revolution is making thermal management more critical than ever—and Modine finds itself perfectly positioned.

II. Founding Era: Arthur B. Modine & The Birth of Thermal Management (1908-1916)

In the winter of 1912, a young engineer named Arthur B. Modine found himself at a crossroads in Racine, Wisconsin. Modine had graduated from the University of Michigan, Ann Arbor, in 1908 with a degree in engineering and became involved in a Chicago-based radiator repair business where he began experimenting with various radiator designs. In 1912, A.B. Modine moved to Racine, Wisconsin, and became a principal partner in Perfex Radiator, where he was actively involved in research, testing, and design of radiators.

Racine in the 1910s was emerging as a hub of American manufacturing innovation. The city would eventually become home to companies like SC Johnson, J.I. Case, and Modine Manufacturing—industrial pioneers drawn by access to Great Lakes shipping, a skilled workforce, and the entrepreneurial energy of the Midwest.

Following a business disagreement with a silent partner at Perfex over how that company should be managed and capitalized, Modine decided to establish his own company. This seemingly minor dispute would prove fateful. Rather than compromise his vision, Arthur Modine struck out on his own.

A.B. Modine founded Modine Manufacturing in 1916 to make radiators for farm tractors. He became president and treasurer of the company, which opened a one-room office adjacent to a small workshop in Racine. The timing was fortuitous: America's agricultural sector was mechanizing rapidly, and tractors were replacing horses across the Great Plains. But these early tractors had a problem—their engines overheated constantly, limiting their utility in the field.

Arthur Modine's genius lay in his approach to the problem. Instead of focusing on the best way to cool the water flowing through the radiator, he focused on the best way to heat the air passing through the radiator. With that simple shift in thought, he made significant advancements in radiator engineering technology. He called the new radiator Spirex.

The Spirex radiator featured a spiral fin design placed in the radiator cells that dramatically improved heat transferability. In December 1916, Modine filed for a patent (issued seven years later) on his Spirex radiator and, in 1917, his radiator was literally called into service by the United States when it became standard equipment on World War I artillery tractors.

This government contract established a pattern that would repeat throughout Modine's history: developing innovative thermal solutions for demanding applications, then leveraging that expertise across commercial markets. By the end of 1918, the majority of leading tractor manufacturers were using the company's radiators.

Arthur Modine wasn't merely an inventor—he was prolific. Arthur B. Modine was one of Racine's most prolific inventors, who was awarded 122 U.S. patents during his lifetime and built an international manufacturing business. This patent portfolio would become a crucial competitive moat, protecting Modine's innovations and forcing competitors to license or work around the company's intellectual property.

Arthur Modine was awarded his final U.S. patent for a heat exchanger at age 92 in 1977. He kept actively inventing into his 90s. Sketches and notes were done on old envelopes and pieces of scratch paper while he lived in retirement in Florida. The image of a nonagenarian inventor scribbling heat exchanger designs on envelope backs captures something essential about the company's culture: relentless engineering innovation across generations.

The transition from tractors to automobiles marked Modine's first major strategic pivot. During the early 1920s, Modine Manufacturing tried to market its Spirex radiator to Ford Motor Company, but because of the way the radiator's frame was designed, the Spirex was unsuitable for automobiles. By 1925, though, A.B. Modine had designed an automotive radiator, called the Turbotube, which helped Modine Manufacturing land its first major automotive contract that year when Ford adopted the radiator as standard equipment for the Model T. Ford quickly became Modine's principal customer and its major source of income, a role the auto maker would play in Modine's operations for the next 55 years.

The Ford relationship illustrates both the blessing and curse of becoming a Tier-1 automotive supplier—reliable revenue streams but dangerous customer concentration. This dynamic would shape Modine's strategic challenges for the next century.

For investors: The founding era establishes Modine's DNA: engineering innovation, patent protection, and the ability to adapt thermal management expertise across applications. These capabilities would prove essential a century later when data centers emerged as the company's growth engine.

III. Building a Century-Old Institution: Growth Through World Wars & Beyond (1916-1990s)

The Unit Heater: A Second Act

In the winter of 1918, frigid Wisconsin temperatures and inadequate heating options caused Arthur B. Modine to develop a revolutionary new heating product. Armed with ingenuity and a need to improve the comfort of employees, Modine combined an automotive radiator, a fan, and steam pipes to construct the first unit heater, thus creating Modine's Heating Division.

The unit heater innovation demonstrates Arthur Modine's ability to see adjacent applications for his core heat transfer technology. Rather than viewing Modine Manufacturing as a "radiator company," he understood it as a thermal management company—a distinction that would prove prophetic over a century later.

Within ten years of its rudimentary beginnings, the Modine Heating Division had developed additional unit heaters, including regular, vertical, and power throw configurations. Modine also licensed the patented technology to 15 companies and controlled more than 94% of the unit heater market. The Modine name was so synonymous with the unit heater that many contractors and builders used "Modine" as the generic product name.

Becoming the generic name for a product category—the "Kleenex" or "Xerox" phenomenon—reflects extraordinary market dominance. This HVAC business would eventually become a critical platform for Modine's data center cooling expansion.

World War II: Industrial Capacity Meets National Need

In 1940, Modine Manufacturing developed a vehicular wind tunnel and after the United States entered World War II, the company's technology was again enlisted by the government, with the wind tunnel used to test combat vehicles. During the war, while the wind tunnel was working on domestic soil, the company's convectors took to the sea, having been adapted to Naval vessels. The company also produced radiators for military tanks, tractors, trucks, and bulldozers during the war.

The war effort cemented Modine's role as a critical supplier to the U.S. military-industrial complex and demonstrated the company's ability to scale production rapidly while maintaining quality. This wartime experience would inform future capacity expansions.

Post-War Prosperity and Leadership Transition

In 1946, A.B. Modine gave up his post as president and became chair of the board. Walter Winkel, who had been actively running the company since 1936 while A.B. Modine was involved in research and product development, succeeded the company founder as president.

The transition reveals an important aspect of Arthur Modine's character: he preferred the laboratory to the executive suite. While Winkel managed operations, Modine continued inventing. Modine Manufacturing benefited from the postwar boom in automobile sales, which helped to push annual revenues above $25 million in 1951.

The Innovation Machine: Patents and Products

The 1950s and 1960s witnessed relentless product innovation:

During the 1950s, the company began using aluminum to produce heat exchangers and, with the advent of air conditioning, it began producing all-aluminum brazed air-conditioning coils for passenger cars and trucks in 1956. That year, Modine Manufacturing received a patent for its concentric oil cooler, a device destined to become standard equipment on cars with automatic transmissions.

In 1961, Modine Manufacturing received a patent for its Alfuse chemical process, a means of fusing aluminum to aluminum that was used to produce condensers. That same year the company received a patent for its light-weight louvered serpentine radiator fin.

The Debt Decision: A Pivotal Cultural Moment

In order to facilitate such growth, in 1967 the company engaged in its first long-term borrowing. A.B. Modine, who was still a director, was adamantly against the company taking on debt, but the company's top management convinced the founder that the loan was necessary in order to accommodate the company's growth.

This moment captures a generational tension common in founder-led companies. Arthur Modine had built the business conservatively, avoiding debt during the Depression and war years. But the growth opportunities of the 1960s required capital investment beyond what retained earnings could support. The founder's eventual acceptance of leverage marked a transition from entrepreneurial startup to modern corporation.

First Acquisition: Diversification Begins

In 1969, Modine Manufacturing received a patent for its Flora-Guard unit heater for greenhouses. That same year the company made its first acquisition, Schemenauer Manufacturing, a privately-owned Ohio maker of unit ventilators and rooftop air-conditioning units.

The Schemenauer acquisition established the template for future M&A: acquiring complementary thermal management businesses that extended Modine's product portfolio and customer reach.

For investors: The mid-century growth phase established Modine's competencies in manufacturing scale, engineering innovation, and strategic M&A. However, deep dependence on Ford and the automotive cycle created structural vulnerability that would eventually force transformation.

IV. The Automotive Trap: Struggling as a Tier-1 Supplier (1990s-2020)

The automotive supply chain is one of the most brutally competitive industries on earth. OEMs like Ford, GM, and Chrysler wield enormous purchasing power, constantly demanding price reductions while expecting ever-higher quality and just-in-time delivery. Tier-1 suppliers like Modine find themselves squeezed between powerful customers and their own commodity suppliers, with margins compressed from both directions.

Economic recessions and shifts in the automotive industry have presented competitive threats. Modine has navigated these by diversifying its product lines.

By the 2000s, Modine had become a classic example of an automotive supplier trapped by its own success. The Ford relationship that had powered growth for 55 years now represented dangerous concentration risk. Every time the Big Three sneezed, Modine caught pneumonia.

The 2008-2009 financial crisis exposed these vulnerabilities brutally. Tom Burke accepted the CEO position in the midst of the 2008-09 financial crisis and acted with a sense of urgency to fortify Modine's operations and ensure that the company weathered the economic downturn.

Modine, with fiscal 2020 revenues of $2.0 billion, specializes in thermal management systems and components, bringing highly engineered heating and cooling components, original equipment products, and systems to diversified global markets through its four complementary segments: CIS; BHVAC; HDE; and Automotive.

The four-segment structure reflected attempts at diversification, but the automotive business remained the anchor dragging on profitability. Modine specializes in thermal management systems and components, bringing highly-engineered heating and cooling components, original equipment products and systems to diversified global markets through its four complementary segments: Commercial and Industrial Solutions, Building HVAC Systems, Heavy Duty Equipment, and Automotive.

The stock reflected the market's skepticism. Throughout the 2010s, Modine shares languished, trapped in "old economy" manufacturing perception. Analysts viewed the company as a commodity supplier in a declining industry. The multiple compression was severe—investors simply weren't willing to pay much for uncertain automotive earnings.

But hidden within the corporate structure was a gem that few appreciated: the Airedale business, acquired in 2005, was quietly building expertise in an emerging market that would soon explode.

For investors: The automotive trap illustrates the challenge of legacy businesses: even competent execution can't overcome structural industry headwinds. The need for transformation was clear, but the strategic direction required the right leader with the right vision.

V. The Strategic Pivot Begins: Airedale Acquisition (2005)

The Hidden Gem

In May 2005, Modine made an acquisition that would ultimately prove transformational—though it took nearly two decades for the full value to become apparent. In 2005, Airedale was bought by US firm Modine for a reported $38 million. That same year, Alan Duttine retired after 39 years and was recognised with an OBE for his services to the industry.

Airedale was formed in 1974 by two Leeds based entrepreneurs Alan Duttine and Peter Midgley who recognised the opportunity for air conditioning for specialist computer and healthcare environments at the dawn of a new technological era. Alan and Peter who both worked for Calverley based Thermatank barely knew each other, but met by chance, at Leeds Bradford Airport when their flights were delayed.

The serendipitous founding story—two future partners meeting during a flight delay—has the flavor of startup legend. But the substance was serious: Duttine and Midgley saw that computing environments would require precision cooling far beyond standard HVAC systems.

Modine announced that it has acquired privately held Airedale International Air Conditioning Limited of Leeds, England for approximately $38 million in cash. Founded in 1974 in Leeds and with 2004 revenues of about $75 million, Airedale is a leading designer and manufacturer of specialty air conditioning systems sold in more than 50 countries worldwide. While the majority of its sales are in the United Kingdom, about 40 percent of Airedale's 2004 revenues were principally to North America, Europe, South Africa and Asia.

The turning point came in 2005 when Modine acquired Airedale, a U.K.-based specialist in data center cooling. Airedale brought not just technological expertise but also a solid market presence in the FLAP region (Frankfurt, London, Amsterdam, Paris) with a 25-30% market share in the U.K. This $38 million acquisition allowed Modine to pivot just as AI and cloud computing were driving demand for more advanced cooling solutions.

Building Data Center Expertise

Airedale didn't rest on its laurels after the acquisition. The company continued innovating, establishing first-mover advantages in critical technologies:

In 2009, Airedale launches first IT cooling system the OnRak™. In 2010, first to develop a concurrent free cooling chiller with centrifugal compressor, the TurboChill FreeCool. In 2011, first to apply microchannel heat exchangers, concurrent free cooling and centrifugal compressors in the same chiller system.

In 2019 Airedale announced the formation of a European data center team, aimed at growing their hyperscale data center portfolio of references across the EU, with particular focus on the important growth areas of Frankfurt, Amsterdam, Paris and Dublin.

The FLAP markets (Frankfurt, London, Amsterdam, Paris) plus Dublin represent the core of European data center activity. Airedale's established relationships with operators in these markets provided a foundation for capturing the coming explosion in hyperscale demand.

Resilience Through Crisis

In 2013 the company suffered its largest setback to date, the company's factory in Leeds, UK, suffering a catastrophic fire that left the premises almost completely destroyed. However, through the loyalty of staff and customers alike, Airedale survived, operating out of temporary facilities for three years while the Rawdon site was redeveloped.

The fire could have killed Airedale. Instead, the crisis revealed organizational resilience that would prove essential during subsequent rapid growth phases.

For investors: The $38 million Airedale acquisition looks, in retrospect, like one of the great strategic steals in industrial history. Modine paid roughly half Airedale's annual revenue for a business that would eventually drive billions in growth. The lesson: hidden value often exists in unglamorous industrial acquisitions that require years of patient development.

VI. Inflection Point: Neil Brinker & The 80/20 Transformation (2020-Present)

The New CEO Arrives

On August 4, 2020, Tom Burke stepped down as Modine's CEO after 12 years. The leadership changes at Modine come at a pivotal time for the company, as Modine completes the divestiture of its longstanding automotive thermal solutions business. "As Modine works to complete the divestiture of its legacy automotive business and further pivots toward its long-term vision to become a true industrial thermal management solutions provider, we have reached a natural inflection point. Now is the right time to find a new leader that can drive our industrial transformation strategy."

Modine announced that its Board of Directors has appointed Neil D. Brinker as the Company's President and Chief Executive Officer, effective December 1, 2020. "We are very excited to name Neil as our next President and CEO. Neil is a proven leader with strong global public company experience across multiple industries. In particular, Neil's commitment to operational excellence and his diverse experience, along with success executing profitable growth strategies provide him with the skills needed to drive Modine's transformation to a diversified industrial company."

Brinker's background made him ideally suited for the transformation ahead. He was previously President and Chief Operating Officer of Advanced Energy Industries, Inc. since May of 2020, and joined AE in June of 2018 as its Executive Vice President & Chief Operating Officer, where he led global sales, marketing, engineering and operations for the Company's semiconductor, telecom and networking, data center, industrial, and medical markets. He oversaw a global team of 12,000 employees and led the consolidation of the Company's global operations to identify and capture organizational synergies. Mr. Brinker brings to Modine extensive transactional experience leading M&A integration at AE and doubling inorganic revenue while divesting non-core assets.

Crucially, Brinker had direct experience with data center markets at Advanced Energy. He understood the explosive demand trajectory and the premium margins available to suppliers who could deliver reliable, high-performance cooling solutions.

Mr. Brinker holds a Bachelor of Science in Mechanical Engineering from Michigan State University, a Master of Engineering from the University of Michigan, and a Master of Business Administration from Eastern Michigan University.

The 80/20 Philosophy

Brinker immediately implemented what would become the defining framework of Modine's transformation: the 80/20 principle.

80-20 is driving important strategic decisions and is beginning to yield tangible improvements across the business. The change in vehicular strategy is just one element. We're also providing additional resources to grow other key businesses that have strong market drivers, including data centers, heating, indoor air quality and coatings. Collectively these initiatives will help Modine become a higher growth, higher margin and less capital-intensive business.

The 80/20 principle—the observation that 80% of outputs result from 20% of inputs—became the lens through which every business decision was evaluated. Which products generated the most profit? Which customers were most valuable? Which markets offered the best growth trajectories? Resources were ruthlessly reallocated toward high-return activities.

"Our strong third quarter earnings growth demonstrates the ongoing power of our cultural transformation and 80/20 initiatives. The targeted growth and 80/20 improvements are resulting in substantial margin increases, with adjusted EBITDA margin up 370 basis points in the quarter." – Modine President and Chief Executive Officer, Neil D. Brinker.

Divesting Legacy, Doubling Down on Growth

The transformation required uncomfortable decisions about legacy businesses. Modine announced that it has signed a definitive agreement to sell three Modine businesses based in Germany to affiliates of Regent LP. The businesses are located in Neuenkirchen, Pliezhausen and Wackersdorf. "The sale of these businesses is in line with our strategy to focus our resources on high-margin technologies with strong growth drivers," said Neil Brinker. "These businesses produce and service non-strategic parts for internal combustion diesel and gasoline engines in the European automotive market."

The businesses manufacture exhaust gas recirculation coolers, radiators and charge air cooler modules for automotive internal combustion engine applications in Europe. In Fiscal Year 2023, the combined revenue from the businesses was between $80-$90 million.

Selling $80-90 million of revenue might seem counterintuitive for a company seeking growth. But the logic was clear: low-margin, declining businesses consume management attention and capital that could be better deployed in high-growth markets. The divestitures freed resources for aggressive investment in data centers.

Results of Transformation

"Our fiscal 2024 results were among the best in the company's history, clearly benefiting from our actions to transform Modine and drive sustainable margin improvement," said Neil D. Brinker. "We delivered another year of record sales and adjusted EBITDA, led by our data center business with revenues increasing 69 percent from the prior year. Performance Technologies showed tremendous improvement, with gross margin increasing by 600 basis points to 20 percent in the fourth quarter and delivering a gross margin of 18.2 percent for the fiscal year. Our adjusted EBITDA margin of 13.1 percent in fiscal 2024 was comfortably above the high end of the 10 to 12 percent range we laid out at our 2022 Investor Day."

For investors: Brinker's arrival and the 80/20 transformation represent a textbook case of operational turnaround. The strategy is straightforward—exit low-margin businesses, invest in high-growth markets—but execution requires discipline and courage. Modine's results demonstrate both.

VII. The AI Data Center Moment: Right Place, Right Time, Right Product

Why Data Center Cooling is Critical

The data center industry is undergoing a seismic shift. As artificial intelligence (AI) and high-performance computing (HPC) demand exponential growth in processing power, the need for advanced thermal management has become a critical bottleneck.

The physics are unforgiving: every watt of computing power consumed by GPUs and CPUs becomes heat that must be dissipated. GPU heat loads increasing from 300W in 2017 to more than 1,200W with NVIDIA's Blackwell chips expected in 2024. The progression from 300W to 1,200W represents a fourfold increase in heat per chip—a thermal management challenge that traditional air cooling simply cannot address efficiently.

The global data center cooling market is projected to grow from USD 11.08 billion in 2025 to USD 24.19 billion by 2032, at 11.8% CAGR from 2025 to 2032.

Strategic Acquisitions to Capture the Opportunity

Brinker accelerated Modine's data center strategy through a series of targeted acquisitions:

TMG Core (January 2024): Modine announced that it had purchased the intellectual property and other specific assets of TMG Core, a specialist in single- and two-phase liquid immersion cooling technology for data centers with high-density computing requirements. "Modine's investment in liquid immersion cooling technology advances our strategy to expand our global data center product offering and capture market opportunities that help us achieve our long-term growth targets."

Eric McGinnis, president of Modine Climate Solutions, said the investment would allow the company to "cover air, liquid, and hybrid systems."

Scott Springfield Manufacturing (February 2024): Modine announced that it had entered into a definitive agreement to acquire Scott Springfield Manufacturing, a leading manufacturer of air handling units (AHU). With this transaction, Modine will gain immediate access to a highly complementary product portfolio and a blue-chip customer base in several strategic end markets, including hyperscale and colocation data centers.

Scott Springfield Manufacturing expects to report final revenue for their fiscal 2023 of more than $100 million (USD). Total consideration for the transaction is based on an enterprise value of approximately $190 million (USD).

Explosive Growth

Modine's data center business hit $294 million in sales in 2024—a 69% YoY growth, with an EBITDA margin of 18.3%.

Modine announced $180 million in orders for Airedale by Modine™ data center cooling systems from a new customer that is a leading AI infrastructure developer.

Modine reported strong results for its second quarter of its 2025 fiscal year, with sales for its climate solutions segment rising 27% year over year to $366.4 million. The company is focused on meeting demand for high-performance chillers from colocation and hyperscale customers.

Within climate solutions, data center revenue growth "continues to exceed management expectations," more than doubling from the prior year.

The $2 Billion Target

"With the increasing demand for our solutions and this investment in additional manufacturing and testing capacity, we believe that our total data centers revenue can approach $2 billion in our Fiscal 2028."

Currently, Modine operates with an estimated $1.3-$1.5 billion in revenue capacity. The latest investment is projected to unlock an additional $1 billion in capacity. By fiscal 2028, Modine anticipates reaching $2.5 billion in total production capacity. This will allow the company to operate at approximately 80% utilization, ensuring it can meet its $2 billion revenue target.

Capacity Expansion

"We're in an era of enormous growth in digital infrastructure in the U.S. and Modine is committed to growing with demand to deliver value for our customers and shareholders." The $100 million investment over the next 12-18 months will expand manufacturing at four sites to support data center growth, including a new facility in the Dallas, TX, area, expansion in Grenada, MS, and considering repurposing existing Performance Technologies' sites in Franklin, WI, and Jefferson City, MO. The investment also will enhance engineering, product development, and testing capabilities, create new jobs, and support the redeployment and retraining of existing Modine employees.

Airedale by Modine opens its third and largest (14.6 acres) manufacturing facility in Bradford, UK, in response to industry demand for sustainable, high-quality data center cooling systems across Europe and beyond.

Modine has officially opened a new 100,000 square foot manufacturing facility in Chennai, India to produce Airedale by Modine™ data center cooling equipment. The facility marks the beginning of full-scale production to serve the growing data center market across the Asia-Pacific (APAC) region.

For investors: Modine's data center growth is not accidental—it reflects two decades of capability building through the Airedale acquisition, followed by aggressive capacity expansion when the AI opportunity emerged. The company has moved from trailing to leading in its response to market demand.

VIII. Business Model & Segment Deep Dive

Two-Segment Structure

Modine now operates through two segments that reflect its strategic priorities:

Climate Solutions: This segment houses the high-growth data center cooling business along with HVAC systems for commercial buildings, indoor air quality products, and coils/coolers for refrigeration. Modine's Climate Solutions segment is the star of its Q1 2025 results, delivering a 25% revenue surge to $357.3 million.

The margin story here is critical. Gross margins expanded 180 basis points to 28.2%, as the company prioritized sales of premium cooling solutions for AI and cloud infrastructure. These products command pricing power in a sector where uptime and energy efficiency are existential concerns for tech giants.

Performance Technologies: This segment includes powertrain cooling for automotive and commercial vehicles, thermal management for heavy-duty equipment, and emerging EV thermal products. The Performance Technologies segment (vehicular and industrial markets) faces a 10% revenue decline to $309 million, reflecting softness in automotive and construction equipment sectors. However, Modine's focus on cost discipline turned this into a margin triumph.

Climate Solutions: The Growth Engine

"Our strong second quarter results benefited from continued momentum in some of our key end markets," said Modine President and Chief Executive Officer, Neil D. Brinker. "Data center revenue growth continues to drive top-line improvement, including the significant impact from the Scott Springfield acquisition. This more than offset lower volumes in both our vehicular end markets and in our heat transfer product business."

"Organic growth in Climate Solutions continues to gain momentum and is projected to accelerate in the second half of the fiscal year," said Brinker. "We now anticipate Data Centers revenue to grow by more than 60 percent year-over-year, reflecting strong demand and strategic execution."

Performance Technologies: The Transformation Story

Enabling the development of zero-emission vehicles while also improving the efficiency of internal combustion engines.

The Performance Technologies segment represents Modine's heritage business, now being reshaped for relevance in the electrification era. While automotive thermal management faces headwinds from the ICE-to-EV transition, battery thermal management and electronics cooling for EVs present growth opportunities.

The segment reported gross margin of 20.2 percent, up 310 basis points from the prior year, primarily due to higher average selling prices, improved operating efficiencies, and the recognition of sales tax credits in Brazil.

Financial Trajectory

Modine reported financial results for the quarter and fiscal year ended March 31, 2025. Record adjusted EBITDA of $392.1 million increased $77.8 million, or 25 percent, from the prior year. Earnings per share of $3.42 increased $0.39, or 13 percent, from the prior year. "Our team delivered a third consecutive year of record revenue and adjusted EBITDA in fiscal 2025, demonstrating the power of our 80/20 transformation and our ability to deliver results despite challenging conditions in our vehicular markets," said Neil D. Brinker. "The record results were led by our data center business where our investments are driving strong returns and above-market growth."

For investors: The two-segment structure provides diversification while maintaining strategic focus. Climate Solutions drives growth and commands premium margins; Performance Technologies provides cash flow while being transformed for the EV era.

IX. Competitive Landscape & Market Position

The Data Center Cooling Universe

The data center cooling market, especially for public equity investment, is a relatively small universe, with the top five players controlling over 50% of the market. Ranked by size, these include Schneider Electric, Vertiv, Eaton, Legrand, and Modine. Among them, Modine and Vertiv are closely tied to AI growth and NVIDIA's stock performance due to their focus on advanced cooling solutions for high-density AI workloads.

In contrast, Schneider Electric, Legrand, and Eaton, although they occupy a larger share of the data center cooling market, are less correlated with NVIDIA and AI trends due to their diversified portfolios, which focus on energy management, power distribution, and digital infrastructure across multiple sectors. Although they play key roles in data center operations, their broader focus dilutes their direct connection to the AI-specific cooling needs that Modine and Vertiv target.

Modine's Differentiation

Modine, through its Airedale division, is known for its strong air-based cooling systems and is transitioning towards liquid cooling. Vertiv, on the other hand, offers a broader range of solutions, including chilled water systems and innovative technologies like EconoPhase for smaller data centers.

"We're also pleased to announce the development of a cooling distribution unit (CDU) that will enable direct-to-chip liquid cooling. The development of that CDU is coming along strongly and we will be offering prototypes to critical strategic customers."

Private Competitors

The private data center cooling companies like Munters, Stulz, Nortek Air Solutions (air cooling), Asetek, ZutaCore, CoolIT Systems (liquid cooling), and Submer, Green Revolution Cooling (GRC), Iceotope, and LiquidStack (immersion cooling) have a more niche, regional focus compared to larger public players like Vertiv and Modine. These smaller firms often concentrate on specific regions such as Europe (Stulz, Iceotope, Submer) or North America (Nortek, GRC, CoolIT), though many are expanding globally. They focus on specialized cooling technologies like precision liquid and immersion cooling, catering to high-density workloads and edge computing.

Valuation Context

When it comes to price, Modine and Vertiv aren't exactly cheap. Their overall revenue growth is solid but not mind-blowing—around 12-20% from 2022 to 2023. However, what's really wild is the multiple expansion. Both companies' price-to-sales (P/S) ratios have surged by 10x since 2022. You can't argue with market sentiment.

For investors: Modine occupies a favorable position as a pure-play on data center cooling within public markets. While larger than specialized startups, it lacks the diversification that dilutes Schneider and Eaton's AI exposure. This positioning makes it a leveraged bet on continued data center infrastructure build-out.

X. Bull Case vs. Bear Case

The Bull Case

1. Secular Tailwind in Data Center Cooling: The global data center liquid cooling market is projected to grow from USD 2.84 billion in 2025 to USD 21.15 billion by 2032, at a CAGR of 33.2% from 2025 to 2032. Modine is positioned directly in the path of this growth.

2. First-Mover Advantages: The Airedale acquisition in 2005 gave Modine nearly two decades of capability building before the AI explosion. Competitors now face the challenge of catching up to established customer relationships and technical expertise.

3. Capacity Expansion at Scale: Over the next year, Modine will invest more than $140 million of capital on the data center side of its business. "What's driving the expansion is accelerated growth of our customers as well as onboarding new customers. We're gaining share in this market."

4. Management Execution: The 80/20 transformation has delivered three consecutive years of record results. Brinker's track record suggests continued disciplined capital allocation.

5. Technology Portfolio Completion: "Stay tuned. There's plenty more to come from us – we're air, we're hybrid, we're liquid, and we're growing." Modine can now address the full spectrum of cooling requirements.

The Bear Case

1. Execution Risk on Capacity Expansion: Modine's gross margin declined 290 basis points to 22.3%, primarily due to increased costs related to capacity expansion for data center products. Rapid expansion can strain operations and compress margins temporarily.

2. Customer Concentration: Large orders from hyperscalers are lumpy and create concentration risk. The $180 million order from a single AI infrastructure developer illustrates both opportunity and vulnerability.

3. Competitive Response: Vertiv, Schneider, and others are investing aggressively in data center cooling. If competition intensifies, pricing power could erode.

4. Valuation Concern: From a valuation perspective, MOD appears overvalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 2.39, higher than the industry's 2.11.

5. Technology Risk: The transition from air to liquid cooling represents a fundamental technology shift. If Modine's liquid cooling products underperform competitors, the company could lose share in the fastest-growing segment.

Porter's Five Forces Analysis

Supplier Power (Moderate): Modine sources commodity components but requires specialized manufacturing capabilities. Vertical integration provides some insulation.

Buyer Power (High): Hyperscalers and colocation providers are sophisticated buyers with enormous purchasing power. However, the criticality of cooling for uptime creates switching costs.

Threat of Substitutes (Low): Cooling is physics—there's no substitute for managing heat. The question is which cooling technology wins, not whether cooling is needed.

Threat of New Entrants (Moderate): The data center cooling market is attracting venture capital to startups. However, scale manufacturing, customer relationships, and track record create barriers.

Competitive Rivalry (High): Well-capitalized competitors are pursuing the same opportunity. Market growth provides room for multiple winners, but share battles will intensify.

Hamilton Helmer's 7 Powers Framework

Scale Economies (Developing): Modine's $100 million capacity expansion should generate scale advantages as utilization rises. However, competitors are also investing at scale.

Network Effects (Weak): Cooling is a product business without strong network effects.

Counter-Positioning (Strong): Modine's 80/20 focus on data centers represents counter-positioning against diversified competitors who can't match its specialization.

Switching Costs (Moderate): Installed base creates some stickiness through service relationships and system familiarity. But customers can and do switch suppliers.

Branding (Moderate): The Airedale brand carries weight in European data center markets. Global brand building is underway.

Cornered Resource (Weak): No obvious cornered resources exist—the key inputs are engineering talent and manufacturing capability, both of which can be acquired.

Process Power (Developing): Modine's 107-year heritage in thermal management represents accumulated process knowledge. Whether this translates to sustainable advantage in data center cooling remains to be demonstrated.

XI. Key Performance Indicators for Ongoing Monitoring

For investors tracking Modine's ongoing performance, three KPIs deserve particular attention:

1. Data Center Revenue Growth Rate (Quarterly YoY)

This is the single most important metric for evaluating Modine's transformation thesis. The company has guided for 60%+ data center revenue growth in fiscal 2026, building toward the $2 billion fiscal 2028 target. Quarterly momentum—acceleration or deceleration—will signal whether the thesis is playing out as expected.

What to watch: Organic growth rate excluding acquisitions. The Scott Springfield contribution makes headline growth look stronger than underlying organic momentum. True demand signal requires separating organic from inorganic.

2. Climate Solutions Adjusted EBITDA Margin

Margin trajectory reveals whether Modine is capturing value from the data center boom or simply trading dollars. The transition from capacity building (margin compression) to capacity utilization (margin expansion) will be visible in this metric.

What to watch: Quarterly progression. Near-term margin pressure from capacity expansion is expected. The question is whether margins rebound as new facilities achieve target utilization.

3. Data Center Backlog/Order Book

Unlike many industrial businesses, Modine's data center customers often place large, multi-quarter orders. The order backlog provides forward visibility into revenue realization.

What to watch: Commentary on backlog quality (customer type, technology mix, geographic distribution) in addition to absolute levels. Large orders from AI infrastructure developers signal premium pricing opportunity.

XII. Regulatory and Accounting Considerations

Environmental Liabilities

Modine Manufacturing has undertaken remediation activities primarily at former U.S. manufacturing sites contaminated by historical operations, with significant efforts focused on the Camdenton, Missouri facility, where trichloroethylene (TCE) and related volatile organic compounds impacted soil, groundwater, and indoor air.

Investors should monitor environmental provisions and any changes in regulatory requirements that could increase remediation costs. However, current disclosures suggest manageable exposure.

Revenue Recognition

Large data center orders with extended delivery schedules create revenue recognition complexity. Investors should pay attention to management commentary on timing of revenue recognition and any changes in customer delivery schedules that could shift revenue between periods.

Goodwill and Acquisition Accounting

The Scott Springfield acquisition at $190 million enterprise value for $100 million+ of revenue implies meaningful goodwill creation. Any impairment risk depends on whether the acquired business performs to expectations. Given strong post-acquisition performance commentary, this appears manageable.

XIII. Conclusion: The Next Century Begins

In 1916, Arthur B. Modine looked at a tractor radiator problem and saw an opportunity to build better thermal management solutions. That engineering vision has sustained Modine through world wars, automotive industry cycles, and corporate transformations spanning more than a century.

Today, the same fundamental challenge—managing heat generated by high-performance machines—has become more critical than ever. The AI revolution is generating unprecedented thermal loads, and Modine's century of expertise positions it to capture this opportunity.

The transformation under Neil Brinker represents a deliberate repositioning from automotive supplier to data center specialist. The 80/20 framework has provided discipline for difficult decisions: divesting legacy businesses, investing aggressively in growth markets, and relentlessly focusing on margin improvement.

Modine is fascinating—how a small, old company has strategically transformed into an AI data center cooling pure player over the last decade, all thanks to a smart acquisition. Who doesn't love a great makeover and growth story?

The risks are real. Execution on rapid capacity expansion, competition from well-capitalized rivals, and the inherent cyclicality of infrastructure spending all present challenges. Valuation reflects significant optimism about future growth.

But the opportunity is equally compelling. Data center cooling is mission-critical infrastructure for the AI economy. Modine has assembled the technology portfolio, manufacturing capacity, and customer relationships to compete for a meaningful share of this growing market.

Arthur Modine, sketching heat exchanger designs on envelope backs at age 92, would likely appreciate the continuity: a century later, his company still solves thermal management challenges for the most demanding applications. The machines have changed from tractors to GPU clusters, but the physics remain the same.

The next chapter of Modine's story will be written by whether the company can execute on its ambitious growth targets while maintaining the engineering excellence that has defined its first 108 years. For investors willing to accept the execution risk, Modine offers rare exposure to the infrastructure powering the AI revolution—from a company that has been preparing for this moment, whether it knew it or not, since 1916.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube