Mohawk Industries: From Shuttleworth Looms to Global Flooring Empire

I. Introduction & Episode Roadmap

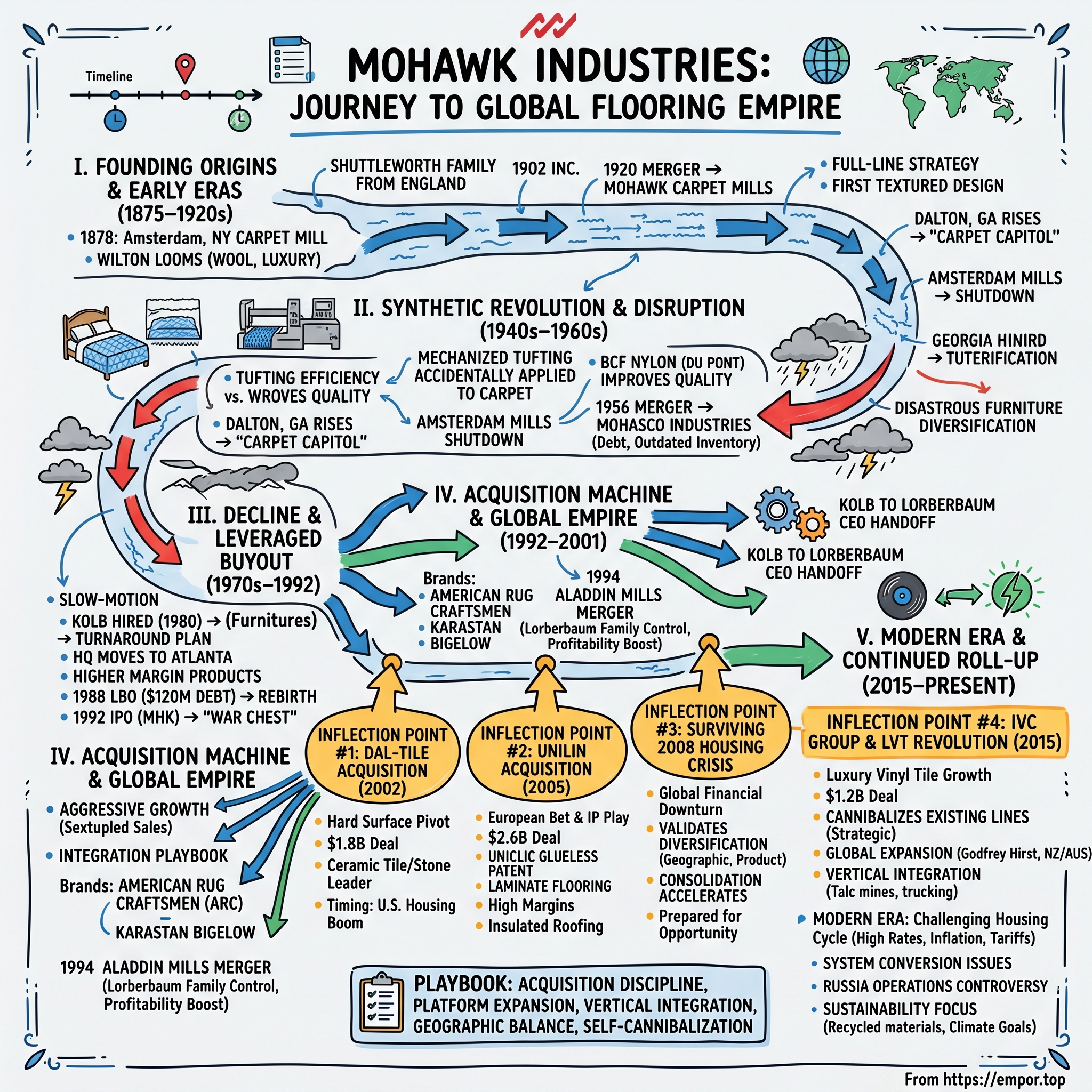

The story of Mohawk Industries reads like a business school case study in corporate reinvention—and a compelling lesson in how to survive disruptions that should have killed a company multiple times over. A Fortune 500 company, Mohawk is the world's largest flooring manufacturer. The company employs 43,000 people in operations in Australia, Brazil, Canada, Europe, Malaysia, Mexico, New Zealand, Russia and the United States.

The central question that animates this deep dive: How did a 19th-century carpet mill from upstate New York—one that nearly went bankrupt in the 1970s, got rescued by a leveraged buyout in the 1980s, and faced existential threats from technological disruption not once but twice—become the undisputed global leader in flooring? The answer lies in a relentless acquisition strategy that has reshaped an entire industry, a willingness to cannibalize its own carpet business to capture hard surface growth, and a leadership team that understood one fundamental truth: in flooring, as in life, what's underfoot matters enormously.

The themes that emerge from Mohawk's 147-year journey are universal to any investor studying mature industries: survival through industry disruption, mastery of the roll-up strategy, navigating brutal housing market cyclicality, and the transformation from a single-product company into a total platform play. Mohawk Industries annual revenue for 2024 was $10.837B, a 2.68% decline from 2023. Yet this number, while down from the company's peak, represents a company that has grown from $280 million in sales to over $10 billion through methodical empire-building.

This is the story of wool looms becoming obsolete, of Georgia housewives accidentally destroying an industry, of Belgian engineers inventing click-lock flooring, and of a family business from Dalton, Georgia seizing control of a legacy northeastern corporation. It's a story that matters because the lessons—about platform expansion timing, geographic diversification, and the patience required to consolidate fragmented industries—apply far beyond floor coverings.

II. Founding Origins & The Shuttleworth Family (1875–1920)

Picture upstate New York in the autumn of 1875: the Civil War barely a decade past, the Gilded Age just beginning, and a family of English carpet makers stepping off a ship onto American shores with plans to recreate the only trade they knew. William Shuttleworth and his four sons arrived in the United States in 1875 and set up a carpet mill in the Hudson Valley upon arrival.

William Shuttleworth had spent his career in England's textile mills, and he believed—correctly, as it turned out—that America's rapidly expanding middle class would soon demand carpets for their homes. After William Shuttleworth died, the four sons moved to Amsterdam, New York in 1878 and took over an empty factory there. The city of Amsterdam, nestled along the Mohawk River, had already established itself as part of New England's textile corridor. The company was founded in 1878 by four brothers in the Shuttleworth family. That year, the family shipped 14 used Wilton looms from Great Britain to Amsterdam, New York and launched their own carpet mill.

Those fourteen Wilton looms—purchased secondhand and transported across the Atlantic—represented the state of the art in carpet manufacturing. Named for the English town where they were developed, Wilton looms produced intricate, cut-pile carpets by weaving colored yarns on a jacquard mechanism. At the time, New England, with its corresponding emphasis on textile mills, was the carpet capital of the nation. For most of its history, Mohawk and its competitors wove floor coverings from wool, a naturally waterrepellent and insulating fiber.

Understanding the carpet industry of this era helps explain why the Shuttleworths' bet was both audacious and lucrative. For most of its history, Mohawk and its competitors wove floor coverings from wool, a naturally water-repellent and insulating fiber. In fact, little about the industry changed from the time of the invention of the power loom in the mid-19th century until after World War II. Even with mechanization, carpetmaking was a highly labor-intensive prospect using massive, complicated machinery. Manufacturers' dependence on unpredictable wool production added another variable to the equation, making for steep fluctuations in expenses.

Carpeting in Victorian America was a luxury good. For most families, carpeting was an expensive luxury, so costly that per household shipments peaked at four square yards in 1899 and did not exceed that mark until the mid-1960s. That's roughly the size of a small rug—hardly the wall-to-wall coverage we take for granted today. This context makes the Shuttleworths' early growth more impressive: they were selling to the wealthiest Americans, competing with established northeastern mills, and operating with the constant uncertainty of wool price volatility.

The Shuttleworth family business was not incorporated until a generational shift in leadership probably precipitated the move in 1902, when the company became known as Shuttleworth Brothers Company. The formal incorporation signaled maturity and ambition—the brothers were building something meant to outlast them.

Three generations of Shuttleworths dominated the carpet mill's first century in business. In 1920, they guided the first of what would become many mergers and acquisitions. That year, the family combined its firm with carpetmakers McCleary, Wallin and Crouse to form a leading force in the then fragmented industry. Renamed Mohawk Carpet Mills, Inc., the company was the country's only weaver with a full line of domestic carpets, encompassing the Wilton, Axminster, Velvet, and Chenille weaves.

This full-line strategy—offering every weave style a customer might want—became Mohawk's first competitive moat. Mohawk did not rest on its laurels, creating the industry's first textured design, Shuttlepoint; the first sculptured weave, Raleigh; and Woven Interlock, "the first successful application of the knitting principle to the manufacture of carpet."

The name "Mohawk" itself—drawn from the river running through Amsterdam—would prove fortuitously durable. It evoked American heritage, suggested ruggedness and quality, and was infinitely more marketable than "Shuttleworth Brothers." The family had built a significant enterprise, a pioneer in carpet innovation with prestigious brands. But forces were already gathering in rural Georgia that would fundamentally challenge everything they had built.

III. The Synthetic Fiber Revolution & Tufting Disruption (1940s–1960s)

Eighty miles north of Atlanta, in a Depression-era Georgia town called Dalton, a fifteen-year-old girl named Catherine Evans Whitener was about to inadvertently revolutionize an entire industry. In 1895 fifteen-year-old Catherine Evans Whitener revived a colonial practice by hand tufting a bedspread, and those who saw it began requesting their own.

What Evans Whitener created wasn't a carpet—it was a bedspread. But the technique she revived, called tufting, would eventually destroy the economic foundations of companies like Mohawk Carpet Mills. To create a tufted bedspread, the craftsperson inserted raised tufts of yarn into a pre-woven piece of backing material (generally cotton sheeting) to form a pattern, then boiled the sheeting to shrink it and lock in the tufts of yarn. Catherine Evans, a young woman living near Dalton, Georgia, saw an old hand tufted bedspread at a friend's house in 1895.

Interest grew in young Catherine's bedspreads, and in 1900, she made the first sale of a spread for $2.50. Demand became so great for the spreads that by the 1930s, local women entrepreneurs had "haulers" who would take the stamped sheeting and yarns to front porch workers. Often, entire families worked to hand tuft the spreads for 10 to 25 cents per spread. The local term for the sewing process was "turfin" among the nearly 10,000 area cottage tufters—men, women, and children.

Dalton was one of the very few towns in Georgia that was not as badly affected by the Depression, because the bedspreads continued to be popular and brought money into the town. This cottage industry became a regional economic engine, with families earning supplemental income through hand-tufting on their front porches. The bedspreads became so popular that tourists on the Dixie Highway would stop to buy them directly—hence the highway's nickname, "Bedspread Alley."

In the 1930s, as a result of the demand for more bedspreads, Glen Looper Foundry of Dalton developed the first mechanized tufting machine. Looper modified the single needle commercial Singer machine so that it would tuft the thick yarn into unbleached muslin without tearing the fabric and attached a knife to cut the loop. Machines quickly developed into four, then eight, twenty-four, and more needles to make the parallel rows of tufting known as "chenille."

The leap from bedspreads to carpet happened almost accidentally. The effort to produce a tufting machine wide enough to mass-produce bedspreads combined with the growing popularity of scatter rugs to inspire the most ambitious, and successful, innovation of the Dalton industrial complex: a carpet tufting machine. Around 1950 old spread-making firms like Cabin Crafts and brand new maverick companies like E. T. Barwick Mills began using tufting machines to cover the entire surface of a room-sized piece of backing material with raised tufts of yarn. Working primarily with cotton, the new manufacturers could produce carpets that resembled woven goods. The new tufting process was much more efficient. A tufted cotton carpet sold for about half the cost of a similar woven wool product.

Cotton carpets were of poorer quality, however, and woven manufacturers derided the new products as glorified bedspreads. Du Pont helped the new industry solve this problem by introducing bulked continuous filament (BCF) nylon in 1957. Du Pont's nylon fibers proved comparable to wool in performance but remained inexpensive. The marriage of the new production technology with synthetic fibers like BCF nylon created an economic boom in northwest Georgia.

The numbers tell the disruption story starkly. In 1950, only ten percent of all carpet and rug products were tufted, and ninety percent were woven. Today, tufted products are more than 90 percent of the total, followed by less than 2 percent that are woven. In a single generation, the entire manufacturing paradigm of the carpet industry had inverted.

During the 1960s, there were more millionaires per capita in Dalton, Georgia than anywhere else in the United States. Mohawk's ancestral home in Amsterdam, New York was becoming an industrial ghost town, while scrappy entrepreneurs in northern Georgia were building fortunes on superior manufacturing economics.

Mohawk's response was a merger that created scale but also problems. In 1956, Mohawk merged with Alexander Smith, Inc. to form Mohasco Industries. Though the acquisition made Mohasco the world's largest carpet company, it proved to be poorly timed. The troubled Alexander Smith brought with it a high level of debt and a large inventory of outdated carpeting at a time when competition from imports was gaining steam. Tariff relaxations during the 1950s increased importers' share of the U.S. industry from 2 percent to 25 percent by the end of the decade. At the same time, Mohasco was compelled by industry imperatives to consolidate its mills in the South.

Mohasco faced competition from new tufted carpet operations in Georgia, which used synthetic fibers such as nylon and polyester rather than the traditional wool used in woven carpets. To compete in a changing industry, Mohasco gradually moved manufacturing south into the Carolinas and eventually Georgia.

The geographic migration was painful and protracted. Carpet manufacturing at the Amsterdam site ended by 1968 and the last corporate offices left by 1987. The Shuttleworth family's century-old connection to upstate New York was severed, one closed mill at a time. Notwithstanding these problems, Mohasco President Herbert L. Shuttleworth II, the third and last of the family to lead the business, was able to stabilize the business enough to purchase high-ranking Firth Carpet in 1962. Dreaming of "a home furnishings empire," Shuttleworth turned his attention to the furniture industry in 1963, acquiring nine furniture makers by 1970.

This diversification into furniture would prove disastrous—a distraction from the core business at precisely the moment when focus was most needed. The lesson for investors: when disruption hits, the wrong response is to diversify into adjacencies you don't understand. The right response, as Mohawk would eventually demonstrate, is to embrace the disruptive technology rather than fight it.

IV. The Mohasco Decline & LBO Rebirth (1970s–1992)

By the mid-1970s, Mohasco Corporation was a cautionary tale in slow-motion decline. The furniture diversification had consumed capital and management attention without generating meaningful returns. The carpet business, still headquartered in the wrong geography and operating the wrong manufacturing technology, was hemorrhaging market share to nimble Georgia competitors.

In 1980, Mohasco hired David Kolb, an attorney who had served as comptroller and director of the nylon carpet fibers division at Allied Fibers, as CEO. Kolb was charged with turning the then unprofitable company around. The new chief undertook a five-year modernization program that encompassed plant and systems modernizations, cost reductions, and development of new managers. He even moved the company's headquarters from Amsterdam, New York to Atlanta, Georgia, to be nearer to what had become the "carpet capitol of the world," Dalton, Georgia. He also shifted the company to higher margin products and increased direct distribution to retailers (thereby cutting out the middleman).

Kolb's background was unusual for a carpet CEO—he was a lawyer and financial professional rather than an operations or sales executive. But this outsider perspective gave him the clarity to make ruthless decisions that industry veterans couldn't bring themselves to make. He joined the Company in 1980 to take over as president of Mohawk Carpet, which was losing money and struggling as a weak competitor. Dave has led Mohawk in its growth from a small $200 million revenue company to the leader in the floorcovering industry with annual sales in excess of $5 billion.

Having achieved his profit goals, Kolb took the carpet division private via a $120 million leveraged buyout in 1988. In 1988, Mohasco was purchased by MHS Holdings in a leveraged buyout, and the company's carpet business was spun off from Mohasco to form Mohawk Industries.

The LBO was simultaneously a fresh start and a financial straitjacket. The $120 million in debt forced operational discipline, but it also constrained growth. Kolb ran the company with meticulous cost consciousness, preparing for the next stage.

In 1992, Mohawk went public with its shares traded first on the NASDAQ Stock Exchange under the ticker symbol "MWK" and currently on the New York Stock Exchange under the ticker symbol "MHK."

The IPO was not merely a liquidity event—it was the opening of the acquisition war chest. Kolb used the $38 million proceeds of Mohawk's 1992 public stock offering to reduce the company's LBO debt in preparation for a rapid-fire series of acquisitions funded in part by new debt. Four key acquisitions from 1992 to 1994 catapulted Mohawk from eleventh in the industry to number two, increased its sales from less than $300 million to nearly $1.5 billion, and multiplied its market share from less than four percent to 17 percent. In addition, Mohawk's growth rate ranked it second among the Fortune 500's fastest growing companies in 1993.

The Lorberbaum family's entry into Mohawk's orbit would prove transformational. Jeffrey S. Lorberbaum is the son of Shirley and Alan Lorberbaum, migrants to the South from New York City. In 1957, his parents founded Aladdin Mills, Inc., in Dalton, Georgia. Aladdin initially produced bathmats and rugs for discount retailers and during the 1970s expanded into tufted carpet manufacturing, eventually growing the business into one of the largest carpet manufacturers in the country.

Jeffrey joined the family business, carpet and rug manufacturer Aladdin Mills, in 1976, after graduating from the University of Denver. Lorberbaum held a number of leadership positions, eventually serving as vice president of operations from 1986 to 1994. In 1994, Aladdin merged with Mohawk Industries, which had gone public in 1992, creating one of the largest flooring manufacturers in the United States—and his father became Mohawk's largest shareholder. Jeffrey and Alan Lorberbaum then joined Mohawk's board of directors. In 1995, Lorberbaum became president of Mohawk; and, in 2001, he became CEO.

The Aladdin merger illustrated the peculiar dynamics of industry roll-ups. In 1994, the carpetmaker merged with highly profitable and privately held Aladdin Mills Inc. via a $430 million "pooling-of-interests." Mohawk paid a premium price for Aladdin but felt justified by the target's comparatively high profitability. Aladdin's compound sales growth had averaged 20 percent from 1988 to 1993, and after the merger, the "subsidiary" contributed 40 percent of sales and 50 percent of net income. Because Aladdin was more profitable than Mohawk, the privately held company's owners, the Lorberbaum family, ended up with a controlling 39 percent stake in Mohawk.

The acquired company's family became the acquirer's controlling shareholder—a merger of equals disguised as an acquisition. This structure would prove brilliant: the Lorberbaums brought operational excellence from Dalton, while Kolb's team contributed public company discipline and acquisition expertise. The combination positioned Mohawk to dominate the consolidation that was reshaping the industry.

V. The Acquisition Machine: Building a Carpet Empire (1992–2001)

The 1990s represent Mohawk's aggressive transformation from regional carpet maker into industry titan. As one of the carpet industry's oldest players, Mohawk has a history that echoes that of its trade, from its foundation in 19th-century New England to its move to Georgia in the 1980s. A period of intense growth through acquisition sextupled Mohawk's sales from $280 million in 1991 to nearly $1.8 billion by 1996. In 1995, it held 17 percent of the $9.8 billion wholesale carpet and rug market, compared to leader Shaw Industries' 26 percent share. Mohawk's acquisition spree gave it a family of more than a dozen brands and made it the nation's largest manufacturer of machine-made rugs, a key segment of the maturing, consolidating market. By the mid-1990s, the company had a presence in virtually every segment of the industry, from mass-produced area rugs sold at promotional prices to custom-made wool carpets.

The integration playbook that emerged from this period became Mohawk's distinctive competence. The company acquired distressed competitors, kept their brand identities and often their management teams, but extracted operational synergies through consolidated purchasing, manufacturing rationalization, and distribution network optimization.

Less than eight months later, Kolb engineered the acquisition of American Rug Craftsmen (ARC), a ten-year-old manufacturer of area rugs. ARC made Mohawk the nation's leading producer of mass-market rugs. Hoping to capitalize on fragmentation within the area rug segment, the new parent boosted ARC's manufacturing and distribution capacity. Under the care of its doting new parent, ARC's sales burgeoned from $50 million in 1993 to $150 million in 1996. The August 1993 purchase of Karastan Bigelow from Fieldcrest Cannon added two of the industry's best known and most valuable brands. In fact, Bigelow was named for Erastus B. Bigelow, the 19th century "Father of the Modern Carpet Industry," so named for his invention of the power loom. The addition of Karastan Bigelow pushed Mohawk past competitor Beaulieu of America to become the United States' second largest carpet company.

Mergers and acquisitions reduced the number of carpet producers from more than 300 in 1980 to 100 by the mid-1990s, with vertically integrated—and, in Mohawk's case, well-diversified—"mega-mills" emerging at the top of the heap.

This consolidation dynamic—from 300 producers to 100, and eventually to an industry dominated by a handful of mega-players—is a pattern that repeats across manufacturing industries. The key insight for investors: timing matters enormously. Mohawk bought at the right moment, when sellers were desperate and multiples were reasonable.

Since 1992, the company has completed twelve strategic acquisitions. These acquisitions, coupled with internal growth, have increased sales from $279 million in 1991 to a current level of $3.2 billion, while market share has increased from 3% to 28%.

By 2000, when David Kolb announced his retirement, Mohawk had been transformed. David L. Kolb, 61, Chairman and Chief Executive Officer, will retire from his position as Chief Executive Officer effective January 1, 2001. David will remain as Chairman of the Board and will continue to be actively involved in the strategic direction of the Company. Jeffrey S. Lorberbaum, currently President and Chief Operating Officer, has been chosen by the Board of Directors to succeed David as Chief Executive Officer. Jeffrey Lorberbaum, 46, joined the Company in 1994 in the merger with Aladdin Mills, where he was President and Chief Executive Officer. He held various executive positions with Aladdin before the merger and has served as President and Chief Operating Officer of Mohawk since 1995. He has over 24 years of experience in the carpet and floor covering industry.

The handoff from Kolb to Lorberbaum was remarkably smooth—unusual in corporate successions. The reason: they had worked in tandem for six years, and their skills were complementary. Kolb was the financial engineer who enabled the roll-up strategy; Lorberbaum was the operational master who made acquisitions work.

But for all the growth, Mohawk remained fundamentally a carpet company—and carpet was mature at best, threatened at worst. The next act would require transcending that identity entirely.

VI. INFLECTION POINT #1: Dal-Tile Acquisition – The Hard Surface Pivot (2002)

Jeffrey Lorberbaum's first major strategic initiative as CEO was also his most audacious: Mohawk would enter hard surface flooring through the largest acquisition in the company's history. The logic was straightforward but the execution was risky—a carpet company buying a ceramic tile company had no obvious operational synergies. The bet was on distribution, brand, and market timing.

Mohawk Industries, Inc. today announced that it completed the previously announced acquisition of Dal-Tile International Inc. Under the terms of the acquisition agreement, Mohawk paid $11 in cash and .2213 of a share of Mohawk common stock for each outstanding share of Dal-Tile common stock. The total value of the acquisition is approximately $1.8 billion which includes approximately $710 million of cash, approximately 15 million shares of Mohawk common stock and stock options together valued at approximately $920 million as of closing and the repayment or assumption of approximately $200 million of Dal-Tile's debt.

Jeffrey S. Lorberbaum, President and Chief Executive Officer of Mohawk stated, "The Dal-Tile merger creates the largest floorcovering manufacturer and distributor in the world with the largest ceramic tile operation in the U.S. and the second largest carpet and rug operation. Dal-Tile adds approximately $1 billion in annual sales of ceramic tile and stone products offering the broadest selection of products and the most recognized brands in the industry. The Dal-Tile distribution channels, which include over 200 sales service centers, independent distributors and home center retailers, offer synergistic opportunities to increase sales."

The company, now a division of Mohawk Industries, grew from a one-building operation in the postwar years to a worldwide manufacturer, processor and distributor of tile, natural stone and quart surfaces through 300 company-owned sales service centers, stone slab yards and design studios as well as through independent distributors and leading home center retailers nationwide.

The Dal-Tile acquisition is Mohawk's 14th since 1992, and the company has maintained a pace of acquiring at least one business annually over the past 10 years. Its most recent purchase was the 2000 acquisition of Crown Crafts' $85 million woven products division, a deal that positioned Mohawk as the nation's largest throw supplier. Likewise, the purchase of Dallas-based Dal-Tile—the largest U.S. manufacturer and marketer of ceramic tile—immediately makes Mohawk Industries the leader in the growing hard surface business and a more formidable presence in the floor coverings industry. Dal-Tile holds about a 33 percent share of the commercial tile market, but only about 15 percent of the residential market, according to an analyst report from Credit Suisse First Boston. Mohawk can expand that residential business through its distribution network of 20,000 independent dealers of residential replacement carpet.

The timing proved fortuitous—perhaps luckier than Lorberbaum anticipated. The U.S. housing market was about to enter its most spectacular boom since the 1950s. Home construction soared, renovation spending exploded, and ceramic tile rode the wave. The housing bubble, which would later prove so destructive, first delivered extraordinary returns to hard surface flooring manufacturers.

The strategic rationale extended beyond the current housing cycle. Ceramic tile had demographic tailwinds: aging baby boomers preferred hard surfaces to carpet for maintenance reasons, while design trends favored the aesthetic versatility of tile. The Dal-Tile acquisition positioned Mohawk to benefit from a multi-decade shift in consumer preferences.

For investors, the Dal-Tile deal illustrates a crucial principle: the best acquisition timing often occurs when a company is transforming its identity. Mohawk was still perceived as a carpet company, which meant it wasn't competing with strategic premiums against other ceramic players. The market hadn't yet recognized Mohawk's ambitions.

VII. INFLECTION POINT #2: Unilin Acquisition – The European Bet & IP Play (2005)

If Dal-Tile was about hard surface diversification, the Unilin acquisition was about something more subtle: acquiring technology and geography simultaneously. The Belgian company brought patents that would transform the laminate flooring industry, plus a European footprint that reduced Mohawk's dependence on the U.S. housing market.

Unilin had annual sales in Belgian GAAP of approximately euro 837 million (US$1.0 billion) and EBITDA margins in excess of 29%. The transaction is valued at approximately euro 2.2 billion (US$2.6 billion), including net cash balances of euro 28 million (US$33 million).

Unilin is a leading manufacturer, distributor and marketer of laminate flooring in Europe and the United States. Unilin is one of the leaders in laminate flooring technology, having developed the patented Uniclic glueless installation system and a variety of other groundbreaking technologies. The company also produces insulated roofing and other wood-based panels. Headquartered in Belgium, the Company has over 2,400 employees located principally in Belgium, France, the Netherlands and the United States. Unilin sells its laminate flooring products marketed under the Quick-Step brand through independent distributors.

Unilin's legacy of innovation brings to Mohawk many of the key technologies that have driven consumer demand for laminate flooring over the past decade, including the company's technologies for direct pressure laminate, patented Uniclic glueless installation systems, beveled edge, scraped surface look, and many others.

The Uniclic patent deserves special attention because it represented a genuine competitive moat. Traditional laminate flooring required glue during installation—messy, time-consuming, and prone to failure. The Uniclic system allowed planks to click together mechanically, dramatically simplifying DIY installation. This wasn't incremental improvement; it was category transformation.

"Laminate flooring has demonstrated exceptional growth and market share gains in Europe over the last decade and the 2004 U.S. market of $1.2 billion, which grew at 24 percent from 2003, is currently anticipated to grow in excess of 15 percent per annum," Lorberbaum said. He said Mohawk also prizes Unilin's management team, and its chairman, Frans De Cock, would be elected to Mohawk's board. The acquisition, unanimously approved by Mohawk's board and Unilin shareholders, is expected to close in the fourth quarter of 2005 and is subject to regulatory approvals and other closing conditions.

Jeffrey S. Lorberbaum, Chairman and Chief Executive Officer of Mohawk stated, "With the acquisition of Unilin, Mohawk has strengthened its market position as a total flooring company. As we did through the acquisition of Dal-Tile in early 2002, we have further diversified our product base, distribution strategy and geographical footprint through the addition of Unilin. Over the past few months, we have been impressed by Unilin's operating team and the strength of the Quick-Step strategy, as well as the company's attractive growth prospects going forward. Laminate flooring is exceptionally popular in Europe and is rapidly gaining market share in the U.S." Mr. Lorberbaum continued, "Unilin's experience in the European flooring market and its relationships with retailers will contribute invaluably to the Company. Unilin also boasts a growing share of the U.S. market.

Unilin also has leading positions in roofing and other wood-based panels in Europe. This diversification into adjacent building materials—insulation, roofing panels—gave Mohawk additional European revenue streams less correlated with flooring cycles.

The EBITDA margins tell the story of why Mohawk paid up for Unilin. At 29%+ operating margins, the business was substantially more profitable than carpet manufacturing. The combination of intellectual property protection (patents), brand strength (Quick-Step), and operational efficiency created a business model worth acquiring at premium multiples.

For investors evaluating platform expansion, the Unilin template is instructive: the best acquisitions bring more than revenue. They bring technology, talent, and access to markets the acquirer couldn't organically penetrate. Unilin delivered all three.

VIII. INFLECTION POINT #3: Surviving the 2008 Housing Crisis

The housing crash of 2008-2009 was, for flooring companies, an extinction-level event. The American subprime mortgage crisis was a multinational financial crisis that occurred between 2007 and 2010, contributing to the 2008 financial crisis. It led to a severe economic recession, with millions becoming unemployed and many businesses going bankrupt. The collapse of the United States housing bubble and high interest rates led to unprecedented numbers of borrowers missing mortgage repayments and becoming delinquent. This ultimately led to mass foreclosures and the devaluation of housing-related securities.

The US housing bubble and the ensuing 2008 financial crisis marked the most severe global financial downturn since the Great Depression. While the epicentre was the American housing market, the crisis exposed vulnerabilities across international banking systems and financial markets. Complex financial instruments, flawed risk assumptions and a widespread belief in the durability of housing prices combined to create a deeply interconnected crisis.

For Mohawk, the crisis validated two strategic decisions from the preceding years: geographic diversification and product diversification. A company entirely dependent on U.S. carpet sales would have faced bankruptcy. Mohawk's European operations, its ceramic tile business, and its laminate division provided offsetting revenue streams that kept the company solvent through the worst housing downturn in a generation.

The recovery proved painfully slow. Unlike other sectors that rebounded within a few years, flooring remained depressed because the replacement cycle depends heavily on home sales. Americans who weren't moving or remodeling weren't buying flooring. This "lock-in effect" meant that even as the economy recovered, housing turnover—and therefore flooring demand—remained suppressed for years.

The crisis also accelerated industry consolidation. Weaker competitors failed, and Mohawk emerged in an even stronger relative position. The company's conservative balance sheet management through the 2002-2007 boom meant it had capacity for opportunistic acquisitions during the downturn—a classic case of preparedness meeting opportunity.

For investors, the 2008 experience established Mohawk's cyclical character permanently. This is a company whose fortunes are inextricably linked to housing, and no amount of diversification eliminates that fundamental exposure. The question is whether the company manages the cyclicality intelligently—and Mohawk's survival through 2008-2009 suggests the answer is yes.

IX. INFLECTION POINT #4: IVC Group & The LVT Revolution (2015)

By 2015, a new flooring category was disrupting the industry: Luxury Vinyl Tile (LVT). Like tufted carpet in the 1950s or laminate flooring in the 1990s, LVT represented a technology shift that threatened established product categories while creating enormous opportunities for manufacturers who captured the wave early.

Mohawk Industries announced that the company has entered into a definitive agreement to acquire the IVC Group. The IVC Group is a major manufacturer of sheet vinyl, luxury vinyl tile (LVT) and laminate, with operations in Europe and the U.S. and sales of approximately $700 million. Mohawk will acquire IVC for approximately $1.2 billion.

Jeff Lorberbaum, Mohawk's chairman and chief executive officer, stated, "There are many potential synergies between IVC and Mohawk in both Europe and the U.S. Our greatest opportunities are in LVT, which has increased globally around 18% in the past year. IVC is the fastest growing manufacturer of LVT in Europe, and their manufacturing expertise will help start up our new Belgian LVT factory faster. This new plant will allow IVC to further expand their European sales. In the U.S., LVT now represents about 5% of the total flooring market, and sales are projected to grow more than 15% annually through the end of the decade. Their new LVT plant in Dalton, Ga. will be one of the world's largest, most efficient production lines with leading technology and will position us to meet the rapidly growing U.S. market."

"LVT, which replicates the look of natural hardwood planks, mosaic tile and stone, is about a $1 billion market in the United States, and it is taking share from laminate, sheet and ceramic flooring for both residential and commercial customers. "The greatest opportunities from the IVC acquisition are in LVT, which has increased globally around 18 percent in the past year," Lorberbaum said.

The IVC Group was founded in Belgium in 1997 by Filip Balcaen, who is IVC's chairman and primary shareholder. In Europe, IVC built the first high-speed LVT production line in the world to compete with imports and it is building a luxury vinyl plank and tile facility in Dalton, Ga. that will have a capacity of $200 million. Overseas on IVC's home turf, Mohawk is constructing an LVT factory with about $150 million of capacity in Belgium.

In 2022 Unilin & IVC Group joined forces in flooring and went to market under the Unilin umbrella. Both compagnies were acquired respectively in 2006 and 2015 by Mohawk Industries, the largest floorcovering manufacturer in the world. Founded in 1997, IVC Group was Europe's leading manufacturer of Carpet Tiles, Luxury Vinyl Tiles (LVT), Sheet Vinyl, and Laminate. With 1,500 employees and 7 production units in Belgium, Luxembourg, and Russia, IVC Group produced over 130 million m² of flooring per year.

The IVC acquisition illustrated Mohawk's willingness to cannibalize its own product lines. LVT was taking share from laminate (where Mohawk already held significant market share through Unilin), from ceramic tile (where Dal-Tile dominated), and even from carpet. A less disciplined company might have resisted promoting a product that competed with existing winners. Mohawk's approach was pragmatic: if the category is growing, lead it, even if it hurts existing product lines.

This willingness to self-cannibalize distinguishes the best platform companies from declining incumbents. Mohawk understood that vinyl flooring would grow regardless of their participation—better to lead the category than cede it to competitors.

X. Global Expansion & Continued Roll-Up Strategy (2015–2023)

Through 2016, Mohawk Industries has acquired 34 companies into its conglomerate, and now operates manufacturing facilities in 15 countries—the U.S., Mexico, Brazil, Ireland, the U.K., Belgium, France, the Netherlands, Luxembourg, Spain, Italy, the Czech Republic, Bulgaria, Russia and Malaysia.

The company's geographic expansion accelerated through targeted acquisitions in key markets:

Mohawk Industries today announced that the Company has agreed to acquire Godfrey Hirst Group, the leading flooring company in Australia and New Zealand, further extending Mohawk's global position. Mohawk anticipates that the transaction will be accretive to EPS in the first twelve months. Established in 1865, Godfrey Hirst is the premier flooring manufacturer in Australia and New Zealand as well as the market leader in design and innovation. The company has been owned and operated by the McKendrick family for the last 50 years and will continue to be led by R.G. (Kim) McKendrick, the CEO and Chairman.

Jeffrey S. Lorberbaum, Mohawk's chairman and chief executive officer, stated, "Mohawk's strategy in Australia and New Zealand has been to build a leading position in the flooring market. Godfrey Hirst's marketing, manufacturing and distribution leadership will complement our current hard surface distribution and strengthen our portfolio. We will leverage our global flooring resources and talent to support Godfrey Hirst's outstanding management and accelerate their growth strategies." Lorberbaum added, "Mohawk is using its strong management team and balance sheet to increase its participation in the global flooring market. With Godfrey Hirst, Mohawk will become the leader in flooring products in both Australia and New Zealand with a platform for significant growth."

Godfrey Hirst acquired Feltex Carpets of New Zealand as an ongoing concern in 2006. In 2018, the Godfrey Hirst business was acquired by Mohawk Industries, the world's largest flooring company, expanding its product offering and capabilities to a global scale.

Bremworth has agreed a takeover with US-based Mohawk Industries, through its local subsidiary Floorscape, which already owns leading local brands Godfrey Hirst and Feltex. It follows the launch of a strategic review in February. Even as recently as 2025, Mohawk continues consolidating the Australian/New Zealand market.

The vertical integration strategy also expanded. Mohawk acquired raw material suppliers—nylon polymerization facilities, talc mines—to control input costs and secure supply chains. The company operates its own trucking fleet for distribution, eliminating reliance on third-party logistics.

The pattern is consistent: Mohawk acquires strong regional brands, retains local management, extracts back-office synergies, and uses global scale for purchasing leverage. This approach contrasts sharply with acquirers who impose headquarters culture on targets, often destroying the very capabilities that made the target valuable.

XI. Modern Era: The Challenging Housing Cycle (2022–2025)

The fourth quarter environment was an extension of conditions our industry faced throughout last year. Consumers continued to limit large discretionary purchases, and consumer confidence remained constrained by cumulative inflation, economic uncertainty and geopolitical tensions. During 2024, home sales around the world stayed suppressed, U.S. homeowners remained locked in place with low mortgage rates, and existing U.S. home sales fell to a 30-year low. Central banks in the U.S., Europe and other regions lowered interest rates during the later part of last year, though the impact on housing turnover was negligible in most regions. New home construction was also constrained across the world, with higher home costs and interest rates impacting starts. Throughout the year, investments in the commercial sector slowed, though they remained stronger than residential remodeling.

Mohawk Industries, Inc. today announced fourth quarter 2024 net earnings of $93 million and earnings per share ("EPS") of $1.48; adjusted net earnings were $123 million, and adjusted EPS was $1.95. Net sales for the fourth quarter of 2024 were $2.6 billion, an increase of 1.0% as reported and a decrease of 1.0% on an adjusted basis versus the prior year. During the fourth quarter of 2023, the Company reported net sales of $2.6 billion, net earnings of $140 million and earnings per share of $2.18; adjusted net earnings were $125 million, and adjusted EPS was $1.96. For the year ended December 31, 2024, net earnings and EPS were $518 million and $8.14, respectively; adjusted net earnings were $617 million, and adjusted EPS was $9.70. Net sales for the year ended December 31, 2024 were $10.8 billion, a decrease of 2.7% as reported and 3.3% on an adjusted basis versus the prior year.

The company faces multiple headwinds simultaneously: the housing market remains frozen as homeowners with sub-4% mortgages refuse to sell, inflation has compressed discretionary spending on home improvement, and new tariff pressures threaten import economics.

Our fourth quarter results exceeded our expectations as sales actions, restructuring initiatives and productivity improvements benefited our performance. Additionally, the negative sales impact from U.S. hurricanes was limited to approximately $10 million. While residential demand remained soft in our markets, our product introductions last year and our marketing initiatives contributed to our sales performance around the globe.

January 24, 2025, the Flooring North America Segment implemented a new order management system that had more issues than anticipated. The conversion did not impact our manufacturing or financial systems. The majority of the system processes have been corrected, and our shipments are currently aligned with our order rates. Our invoicing was delayed, and we are addressing shipping and invoicing errors with customers that mainly occurred in the beginning of the implementation. At this point, we estimate the impact on our first quarter operating income from the missed sales and extraordinary costs will be between $20 to $30 million. We are working closely with our customers to remediate any issues or concerns. We believe the impact of the extraordinary costs will be limited to the first quarter. It is difficult to estimate the sales impact on future quarters, though we do not anticipate the system conversion issues will have a meaningful long-term effect on our customer relationships.

The company's Russia operations remain a source of controversy: Despite international sanctions and corporate withdrawals following the Russian invasion of Ukraine in 2022, Mohawk Industries has continued its business operations in Russia. According to Leave Russia, a project tracking companies still engaged in the Russian market, Mohawk Industries has not exited the country.

In Russia, Mohawk has continued its existing operations, but it is not investing more in the country, and it is evaluating its options for the future. "At this point, as our hopes for near-term peace have diminished, we are taking actions within the business," Mohawk said in its statement. "In Russia, we have suspended new investments, advertising, promotions and other activities."

But Mohawk Industries, the world's biggest floor covering firm with an estimated $400 million in Russian sales last year, said it has suspended new investments in Russia and suspended operations in Ukraine, the company said in an earlier statement. The Chief Executive Leadership Council, a Yale School of Management group urging U.S. businesses to quit doing business in Russia, gave Mohawk a letter grade "D" on Wednesday for "buying time" on pulling out of Russia. Mohawk is among 56 U.S. companies holding off new investments in Russia but are not pulling out or cutting operations in Russia as 369 other U.S. companies have already done.

This ESG controversy creates headline risk, though the financial materiality remains limited given Russia represents roughly 4% of consolidated revenues.

XII. Sustainability & Innovation Strategy

Mohawk Industries, Inc. today published its 16th annual impact report, which highlights progress toward the Company's sustainability goals, new environmentally friendly residential and commercial products, and activities that benefit the Company's people and communities as well as the planet. "At Mohawk, we invest in what works—solutions that reduce our environmental impact, strengthen our business and benefit our customers," said Chairman and Chief Executive Officer Jeff Lorberbaum. "We engineer our products to reduce carbon emissions, increase recycled content, achieve circular design and extend their useful life. Our mission is to deliver eco-friendly products that captivate and inspire architects, designers, builders and, of course, consumers."

In 2024, Mohawk exceeded its Scope 1, 2 and biogenic emissions intensity goal with a reduction of 30% from its 2010 baseline, leading to recognition as one of America's climate leaders. Last year, Mohawk increased its renewable energy consumption by 117%, with a 53% increase in solar energy generated through rooftop panels. Mohawk's 2024 global water withdrawal intensity improved 45% from its 2010 baseline, reflecting millions of gallons of wastewater reused in or eliminated from manufacturing processes, particularly in its global ceramic tile operations.

Beyond billions of plastic bottles recycled into flooring, during 2024, the Company repurposed almost 1.5 billion pounds of waste wood into chipboards and upcycled almost 50 million pounds of discarded tires into decorative mats.

Mohawk incorporates recycled plastics and waste wood into products, with some flooring containing up to 63 recycled plastic bottles per square yard.

The sustainability initiatives serve dual purposes: they address genuine environmental concerns while reducing raw material costs. Recycled plastic is often cheaper than virgin resin; waste wood transformed into chipboard creates value from byproducts. This is sustainability as competitive advantage rather than mere compliance—the strongest form of corporate environmental strategy.

Among Mohawk's 41,900 associates around the world, 10.5% have worked with the Company for 25 or more years, contributing to Mohawk's recognition as one of America's top large employers.

Innovation continues driving product differentiation. The company has introduced waterproof wood flooring, PVC-free resilient products, and carpet tile with built-in carbon offsets. In a commodity-prone industry, these innovations sustain margin premiums.

XIII. Playbook: Business & Investing Lessons

The Roll-Up Mastery

Mohawk's 30+ year acquisition strategy offers a masterclass in industry consolidation:

Patience over urgency: The company never competed aggressively for "hot" acquisition targets. It waited for distressed sellers, management succession opportunities, or unique strategic fits.

Integration discipline: Acquired brands were preserved, local management was retained, but back-office functions were consolidated. This approach captures synergies without destroying the capabilities that made targets valuable.

Brand portfolio management: From mass-market rugs to premium Karastan wool carpets, from builder-grade ceramic to designer stone, Mohawk offers products at every price point. This prevents channel conflict and captures diverse consumer segments.

Platform Expansion Timing

The three transformational acquisitions—Dal-Tile (2002), Unilin (2005), and IVC (2015)—each captured emerging category growth:

Dal-Tile rode the housing boom into hard surfaces when ceramic was accelerating.

Unilin brought intellectual property (Uniclic patents), not just manufacturing capacity. Technology acquisition proves more durable than capacity acquisition.

IVC caught the LVT wave before it peaked, despite LVT cannibalizing existing Mohawk products. Self-cannibalization is better than being cannibalized by competitors.

Geographic Diversification

The U.S. remains approximately 70% of Mohawk's business, but European operations provide partial countercyclical balance. The Australian/New Zealand expansion demonstrates the template: acquire regional leaders, retain local management, leverage global purchasing scale.

Vertical Integration Strategy

Mohawk controls substantial portions of its value chain: raw material production (nylon polymerization), manufacturing across all flooring types, distribution networks, and an owned trucking fleet. This integration provides cost advantages, supply security, and competitive barriers.

Surviving Cyclicality

Flooring is inescapably tied to housing cycles. Mohawk's approach:

Conservative balance sheet through boom times: The company didn't lever up during good years, preserving capacity for downturn opportunities.

Capacity flexibility: Manufacturing lines can be idled during downturns without destroying capabilities.

Product mix evolution: Hard surfaces and commercial applications reduce volatility compared to a carpet-only portfolio.

XIV. Competitive Analysis & Investment Framework

Porter's Five Forces Analysis

Supplier Power: Moderate Mohawk's vertical integration (nylon production, wood sourcing) reduces supplier leverage. However, certain raw materials remain commodity-priced, exposing the company to input cost volatility.

Buyer Power: Moderate to High Retailers (Home Depot, Lowe's) and commercial specifiers hold significant negotiating leverage. Mohawk's brand portfolio and product breadth provide some countervailing power.

Threat of Substitutes: Moderate New flooring technologies continually emerge (polished concrete, bamboo, alternative materials). Mohawk's multi-product platform allows participation in emerging categories rather than defending obsolete ones.

Threat of New Entrants: Low Scale economies, distribution networks, and brand recognition create substantial barriers. Capital requirements for modern manufacturing facilities run into hundreds of millions of dollars.

Competitive Rivalry: High The market is highly competitive, dominated by key players such as Beaulieu International Group, Gerflor, Interface, Milliken, Mohawk Industries, Oriental Weavers, Shaw, Tarkett, The Dixie Group, and Victoria. The top five manufacturers—Mohawk Industries, Shaw Industries, Tarkett, Armstrong Flooring, and Interface hold a major market share in 2024 revenue.

Shaw Industries, owned by Berkshire Hathaway, represents Mohawk's most formidable competitor—a company with similar scale, geographic reach, and product breadth, plus access to Berkshire's patient capital.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Mohawk benefits from purchasing leverage (raw materials), manufacturing efficiency (utilization rates), and distribution economics (fleet optimization). This power is genuine but shared with Shaw and other large competitors.

Network Effects: Limited. Flooring isn't a network business—one customer's purchase doesn't make the product more valuable to others.

Counter-Positioning: Not applicable. Major competitors offer similar product portfolios.

Switching Costs: Low for consumers, moderate for commercial specifiers who develop relationships with Mohawk's design consultants and technical support.

Branding: Moderate power. Brands like Karastan, Dal-Tile, and Quick-Step command recognition and price premiums in their categories, but flooring remains largely a considered purchase where brand loyalty is limited.

Cornered Resource: The Uniclic patents provided temporary cornered resource power, now largely expired or widely licensed. Current IP portfolio provides modest differentiation.

Process Power: Mohawk's integration competence—the ability to acquire and efficiently integrate targets—constitutes genuine process power. Few competitors execute acquisitions as effectively.

Key Performance Indicators to Monitor

1. Flooring North America Segment Operating Margin: This segment, representing the majority of revenues, reveals underlying competitive position. Watch for margin trends versus housing cycle position—margin expansion during downturns signals operational excellence; margin compression during upturns signals competitive pressure.

2. Residential Remodeling vs. New Construction Mix: These end markets have different growth trajectories and profitability profiles. Shifts in mix signal changing market dynamics and forecasting accuracy.

XV. Myth vs. Reality

Myth: Mohawk is a carpet company. Reality: The company manufacturing portfolio consists of soft flooring products (broadloom carpet, carpet tiles, carpet cushion and rugs), hard flooring products (ceramic and porcelain tile, natural stone and hardwood flooring), laminate flooring, sheet vinyl and luxury vinyl tile, natural stone and quartz countertops. In Europe, the company also produces and sells insulation, panels and mezzanine flooring. Carpet is now a minority of revenues; Mohawk is better understood as a flooring platform company.

Myth: Flooring is a commodity business. Reality: While commodity pressures exist, differentiation occurs through design, technology (waterproofing, click-lock installation), sustainability attributes, and service levels. Premium products command meaningful price premiums.

Myth: Housing cycles make Mohawk uninvestable. Reality: Housing cyclicality is a feature, not a bug, for patient investors. Understanding cycle positioning enables opportunistic entry points. Mohawk has survived every housing cycle since 1878, emerging stronger from each downturn.

XVI. Bull Case & Bear Case

Bull Case

The U.S. housing market represents coiled spring potential. Millions of homeowners have been "locked in" by their low-rate mortgages, deferring moves and major renovations. When rates eventually normalize, pent-up demand for flooring should drive multi-year growth. Mohawk's product breadth ensures participation across price points and categories.

Demographic tailwinds favor hard surfaces: aging populations prefer low-maintenance flooring, sustainability concerns favor durable products over disposable ones, and design trends favor authentic materials or convincing imitations (LVT's specialty). Mohawk is positioned across all growing categories.

The acquisition pipeline remains attractive. Industry fragmentation persists in emerging markets, and Mohawk's integration competence enables value-creating deals at reasonable multiples. Unlike many serial acquirers, Mohawk has demonstrated disciplined capital allocation through multiple cycles.

Bear Case

Housing market normalization may take longer than optimists anticipate. If elevated mortgage rates persist through 2026-2027, Mohawk's North American business faces continued pressure. The "lock-in effect" could become permanent structural change rather than temporary dislocation.

Tariff uncertainty creates margin risk. LVT imports from Asia face potential duties, and Mohawk's ability to pass through costs depends on competitive dynamics. The company anticipates ongoing market softness in Q1 2025 due to elevated interest rates and weakness in housing. They are navigating challenges such as new U.S. tariffs on LVT, estimated at an annualized cost of $50 million.

The Russia situation creates ESG risk and potential operational complications. Continued operations could trigger customer or investor boycotts; exit could destroy significant value. Neither outcome is attractive.

Carpet continues secular decline as a category. Even with diversification, Mohawk's legacy business faces structural headwinds that offset growth elsewhere.

XVII. Conclusion

The story of Mohawk Industries is ultimately about adaptability—a company that survived the death of woven carpets, the geographic shift from New England to Georgia, the transition from private ownership to public markets, and multiple housing cycles that destroyed lesser competitors.

Jeffrey Lorberbaum (born October 24, 1954) is an American billionaire and the chairman and chief executive officer of Calhoun, Georgia-based Mohawk Industries, the world's largest flooring company. Under his 24-year tenure as CEO, Mohawk has evolved from a U.S. carpet manufacturer into a global flooring platform, creating billions in shareholder value through disciplined acquisitions and strategic diversification.

The central lesson for investors: industry leadership requires continuous reinvention. The Shuttleworth family built a woven carpet business; that business became obsolete. Mohasco tried diversification into furniture; that strategy failed. Kolb executed a turnaround through operational excellence. Lorberbaum transformed the company through strategic acquisitions. Each era required different capabilities and different visions.

What remains constant is the fundamental dependence on shelter—humanity's need to live and work in spaces with floors beneath their feet. That elemental demand ensures flooring's relevance even as technologies, materials, and aesthetics evolve. Mohawk's 147-year history suggests the company has learned how to evolve alongside those changes.

Mohawk Industries is a leading global flooring manufacturer, providing products that enhance residential and commercial spaces in approximately 180 countries. From fourteen used Wilton looms shipped across the Atlantic to operations spanning five continents, from $280 million in 1991 revenues to over $10 billion today—the transformation is complete. But for a company that has reinvented itself repeatedly across nearly fifteen decades, the next transformation is likely already underway.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube