Las Vegas Sands: The Macau Miracle and Singapore Splendor

I. Introduction & Episode Roadmap

Picture this: January 2009. The global financial system is in freefall. Lehman Brothers has collapsed. Credit markets are frozen. And in a Las Vegas boardroom, a 75-year-old billionaire is writing personal checks totaling $1 billion to save his casino empire from bankruptcy. The stock that traded at $144 just 15 months earlier now changes hands for less than $2. Wall Street has written the obituary. Yet this near-death experience would become the prelude to one of the most spectacular geographic pivots in business history.

Las Vegas Sands today stands as the world's largest casino operator by market value, but not because of Las Vegas. The company that bears the name of America's gambling capital generates virtually zero revenue from the Strip—having sold its namesake properties in 2022. Instead, this $40 billion empire rules from 7,000 miles away, where the South China Sea meets the Pearl River Delta, and where a tiny former Portuguese colony generates more gaming revenue than the entire United States.

How did a computer trade show entrepreneur with no casino experience build a global gaming empire that would fundamentally redefine what a casino could be? The answer involves three audacious bets: first, that Las Vegas conventions mattered more than gambling; second, that Macau would become the world's gaming capital; and third, that Singapore—where chewing gum was illegal—would embrace casino resorts.

This is the story of Sheldon Adelson's Las Vegas Sands—a tale of immigrant ambition, leveraged bets, regulatory capture, and the transformation of gambling from vice to "integrated resort." It's about building palaces in the desert, then abandoning them for islands across the Pacific. Most importantly, it's about recognizing that in the casino business, the house always wins—but only if you know which house to build, and where.

II. Origins: From Street Corners to COMDEX

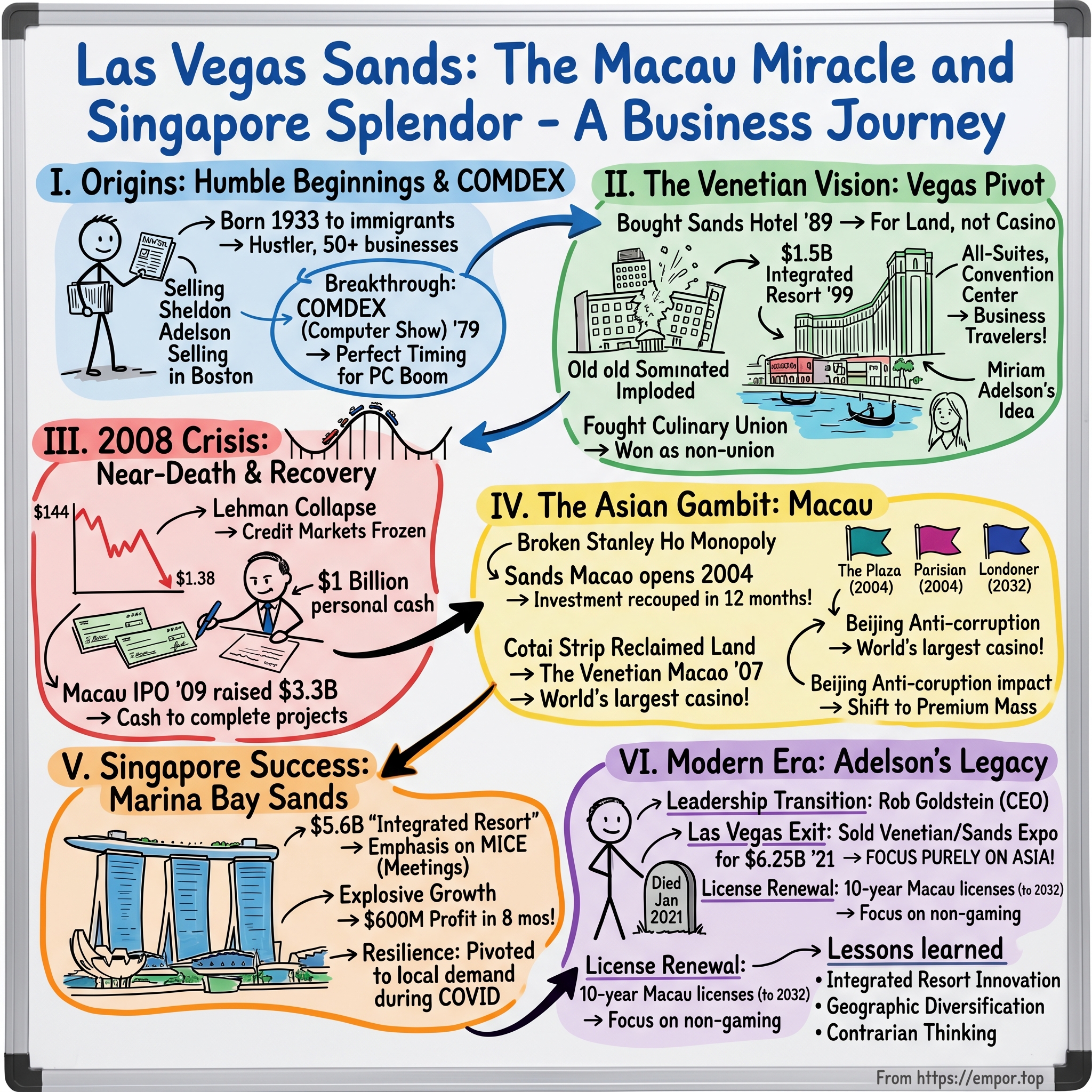

Sheldon Gary Adelson's path to casino mogul began not at a blackjack table, but in the tenements of Boston's Dorchester neighborhood. Born in 1933 to Ukrainian-Jewish immigrants, his father drove a taxi and his mother ran a knitting shop. By age 12, Adelson was already hustling—borrowing $200 from his uncle to buy a corner newspaper stand license. The kid who sold papers on Boston street corners would one day be worth $35 billion.

The entrepreneurial bug never left. Adelson dropped out of City College of New York, served in the Army, tried court reporting, sold toiletry kits to motels, even attempted to market spray-on deicing for windshields. By his own count, he started over 50 businesses, most of them failures. "I never thought about becoming wealthy," he'd later say. "I thought about being my own boss."

The breakthrough came in 1979, not with dice or cards, but with computers. Adelson and four partners launched COMDEX (Computer Dealers Exhibition) with $20,000 in seed capital. The timing was perfect—personal computers were about to explode, and nobody had created the definitive trade show. Within a decade, COMDEX became the computer industry's Super Bowl, drawing 200,000 attendees to Las Vegas each November. Bill Gates launched Windows 3.0 there. Every major tech announcement ran through Adelson's show.

But Adelson saw something others missed. In 1989, while COMDEX was printing money, he and partners bought the aging Sands Hotel and Casino for $128 million. The Sands was legendary—Sinatra's Rat Pack had made it their headquarters in the 1960s—but by 1989, it was a tired relic. Adelson didn't care about the casino. He wanted the land next door. In November 1990, Adelson opened his 1.2 million square foot Sands Expo and Convention Center, the largest privately owned convention facility in the world. The $700 million project wasn't about gambling—it was about transforming Las Vegas from a weekend destination to a Tuesday-through-Thursday business hub. While competitors chased high-rollers with comped suites and private jets, Adelson chased corporate America with loading docks and breakout rooms.

The strategy seemed insane to casino veterans. Convention attendees don't gamble much. They go to bed early. They expense modest dinners instead of ordering $500 bottles of champagne. But Adelson understood something fundamental: the strategy keeps mid-week occupancy strong and delivers greater bottom line returns from conventions than from gambling. Fill your rooms Tuesday through Thursday with conventioneers paying rack rates, then let the gamblers fill weekends. The combined yield beats either model alone. Then came the masterstroke. In February 1995, Adelson sold COMDEX to Japan's SoftBank for $800 million. But here's what everyone forgets: Adelson didn't just sell a trade show. He sold at the absolute peak, right before the internet would begin destroying physical trade shows. COMDEX would be dead within a decade, but Adelson walked away with over $500 million in personal proceeds—the capital that would transform him from convention king to casino mogul.

III. The Venetian Vision: Reinventing Las Vegas

The honeymoon changed everything. In 1991, Sheldon Adelson married Dr. Miriam Ochshorn, an Israeli physician who had immigrated to America. For their honeymoon, they chose Venice. Gliding through the canals in a gondola, Miriam turned to her new husband with an idea that would reshape Las Vegas: "If you can combine the romantic atmosphere of Venice with all of the luxuries that can only be found in Las Vegas, then it can be a winner."

Back in Vegas, Adelson faced a decision. The old Sands Hotel sat on prime Strip real estate, but it was bleeding money—a has-been from the Rat Pack era trying to compete with Mirage's white tigers and Bellagio's fountains. In November 1996, Adelson made the call: demolish it. The implosion made headlines—the Sands had hosted everyone from Sinatra to JFK—but Adelson saw only the future. On that 15-acre footprint, he would build something unprecedented: a $1.5 billion resort that wasn't really about gambling at all. The Venetian opened on May 3, 1999, with Italian actress Sophia Loren joining Adelson for the celebration—singing gondoliers, sounding trumpets, and a flutter of white doves. But this wasn't just theater. The Venetian includes a 120,000 sq ft casino and opened with 3,036 suites in a 35-story tower. Every room was a suite—minimum 650 square feet—at a time when most Vegas rooms were 350 square feet. When it opened 25 years ago, it had 3,036 suites, and today they remain the largest standard hotel room on the Strip.

The genius wasn't the suites themselves but what they represented: a complete reimagining of the Vegas value proposition. Adelson wasn't selling gambling with a room attached. He was selling luxury business travel with a casino downstairs. The all-suite concept meant business travelers could hold meetings in their rooms. The massive convention center meant they never had to leave the property. The upscale retail meant their spouses had something to do. And the Venice theme? That was the permission structure that let corporate America expense a Vegas trip as a legitimate business meeting.

But building a union-free property in Las Vegas was like opening a steakhouse in India. The Culinary Workers Union had organized virtually every major Strip property since the 1930s. The Venetian also feuded with the Culinary Workers Union regarding Adelson's decision to open the property as a non-union resort. thousands of Culinary members protested at the resort's grand opening. Adelson didn't blink. He hired directly, paid above union scale, and fought every legal challenge. The union picketed for years. Adelson outlasted them.

The early years were brutal. Construction ran over budget. More than $230 million in mechanic's liens were filed, including $145 million from Lehrer McGovern Bovis, which also filed a fraud lawsuit against the resort. The property didn't receive a permanent certificate of occupancy until June 2001, two years after opening. Wall Street questioned whether a convention-focused model could work in Vegas.

Then came validation. In 2003, Adelson opened the Venezia tower with another 1,013 suites. In December 2007, Palazzo, attached to The Venetian and continuing the theme of the city of Venice, opens, adding 3,064 suites and bringing the total to 7,092. The combined complex became the world's largest hotel, with 7,000 all-suite rooms across 17 million square feet. More importantly, it proved the model: "more than any other company, they transformed Las Vegas Sunday through Thursday, and that, of course, is because of the convention space."

IV. The IPO and Early Success

Wall Street finally got its chance to value Adelson's empire in December 2004. Las Vegas Sands completed its initial public offering on the New York Stock Exchange at $29 per share, with the ticker LVS. But this wasn't your typical tech IPO with founders cashing out. Las Vegas Sands completed its initial public offering at a price of $29 per share, with 6.8% of the company put on the market. Adelson maintained 87.9% ownership of the company; management and directors owned the remaining 5.3%. Adelson barely sold anything. He wanted the money for expansion, not personal liquidity.

The timing was perfect. The Venetian had proven the integrated resort model. Macau had just opened to foreign operators. Singapore was considering casinos. The IPO provided capital without diluting Adelson's iron grip on control. He recovered his initial $265-million investment in one year and, because he owned 69% of the stock, he increased his wealth when he took the stock public in December 2004. Following the opening of the Sands Macao, Adelson's personal wealth multiplied more than fourteen times.

What followed was one of the most spectacular runs in casino history. By October 2007, less than three years after the IPO, the company's market capitalization peaked at $52 billion at $144.56 a share. To put that in perspective: Adelson's 87.9% stake was worth over $45 billion. The son of a cab driver had become one of the richest men in America, all from a business model that Wall Street initially thought was crazy—prioritizing convention centers over slot machines.

The early success validated everything Adelson believed. The Venetian was printing money from convention business. The Palazzo construction was on schedule. But the real action was happening 7,000 miles away, where Adelson was about to make the biggest bet of his career. Not on a card game or a roll of dice, but on the idea that Chinese gamblers would spend more in one night than Americans spent in a week.

V. The Asian Gambit: Macau and Singapore

Stanley Ho had ruled Macau's casinos for forty years. The 82-year-old tycoon held a government-granted monopoly since 1962, operating every casino in the territory through his company STDM. But in 2002, as Macau prepared to celebrate its return to Chinese sovereignty, the government decided to break Ho's stranglehold. They would issue new licenses to foreign operators. Sheldon Adelson saw the opportunity of a lifetime. Macau sits just 40 miles west of Hong Kong, a tiny peninsula that had been a sleepy Portuguese colony for 450 years. But Adelson saw what others didn't: 1.3 billion Chinese with rising incomes, a cultural affinity for gambling, and no legal alternatives. "At the time of its opening, Las Vegas Sands chairman Sheldon Adelson had said that his company would soon be a mainly Chinese enterprise, and that Las Vegas should be called 'America's Macau'."

Sands Macao opened on May 18, 2004, at a cost of $240 million—pocket change compared to the billions Adelson would later spend. It was Macau's first American-operated casino, a 229,000 square foot gaming floor that looked nothing like the smoky, crowded gambling dens that Stanley Ho operated. This was Las Vegas transplanted to China: bright lights, wide aisles, modern slot machines, and most importantly, transparency in gaming operations that mainland Chinese visitors had never experienced.

The opening day was chaos. Scuffles broke out and elderly people fainted after false reports of free gaming chips lured 15,000 to the opening. But the real shock came in the counting room. All of the mortgage bonds that were issued to finance construction were paid off in May 2005—less than a year after opening. Adelson had recouped his entire investment in 12 months. Wall Street had never seen anything like it.

But Sands Macao was just the appetizer. Adelson's real vision lay across the water in Cotai, a district of reclaimed land created through public works projects and designated for hotels and casinos. While competitors built in established areas, Adelson bet on empty land between two islands. Adelson's vision helped ignite construction of the Cotai Strip, where Sands would open its first Asian convention-based integrated resort in 2007 – The Venetian Macao

The Venetian Macao opened on August 28, 2007, and it wasn't just big—it was preposterous. At 10.5 million square feet, it dwarfed its Las Vegas namesake. The 550,000 square foot casino floor made it the world's largest gaming space, with 3,400 slot machines and 800 gaming tables. The property included 3,000 suites, 1.2 million square feet of convention space, and a 15,000-seat arena. Adelson had essentially built a small city on reclaimed land.

The numbers defied belief. Construction cost $2.4 billion, but the property generated $1.8 billion in EBITDA in its first full year. The Venetian Macao alone was generating more profit than most entire casino companies. By 2008, Macau's gaming revenue had surpassed the entire Las Vegas Strip, and Adelson's properties were capturing the lion's share of the growth.

While Macau was printing money, Adelson was already eyeing his next conquest: Singapore. The island nation had banned gambling since independence, but facing competition from regional capitals, the government decided to allow two integrated resorts. The bidding process was fierce—every major operator wanted in. But Adelson had an ace: his convention expertise. Singapore's bid documents told a different story than any other casino pitch in history. The government wanted an integrated resort that would enhance tourism, create jobs, and position Singapore as a global business hub. Gaming was almost an afterthought. Adelson's proposal for Marina Bay Sands wasn't about gambling—it was about creating Asia's premier convention destination with a casino attached. At a development cost of $5.6 billion, it would become the world's most expensive standalone casino property.

Construction started in 2006, originally planned to open in 2009, but the project faced delays due to the economic recession, labor shortages, and material pricing, with soft openings throughout 2010 and 2011. The architectural marvel, designed by Moshe Safdie, featured three 55-story towers connected by a SkyPark that defied engineering logic—a 340-meter-long observation deck cantilevered 64.92 meters at a height of 198.11 meters above ground.

The first phase's soft opening came on April 27, 2010, with the official opening on June 23, 2010, and the rest of the complex opening after a grand opening on February 17, 2011. But the real shock came in the accounting department. Las Vegas Sands expected the casino to generate at least $1 billion in annual profit. They were being conservative. Within eight months of opening, Marina Bay Sands posted a $600 million operating profit—not annually, but in just eight months. Singapore tourism increased 20% within a year of the resort's opening.

Meanwhile, back in Macau, Adelson wasn't resting. Following the Venetian's success, he continued building out the Cotai Strip. The Four Seasons opened in 2008. The Plaza followed in 2012. Then came The Parisian Macao in 2016, complete with a half-scale Eiffel Tower replica that lit up the Cotai skyline. The Londoner Macao, a $2.2 billion expansion and rebrand of the Sands Cotai Central, fully opened in February 2021, bringing a taste of British elegance to the Chinese gaming capital.

By 2019, Macau had become the undisputed gaming capital of the world, generating seven times Las Vegas's gaming revenue. And Las Vegas Sands owned the crown jewels—five interconnected properties on Cotai that functioned as a small city, with over 12,000 hotel rooms, 2 million square feet of retail space, and enough gaming tables to outfit every casino in Atlantic City.

VI. The 2008 Crisis: Near-Death Experience

September 15, 2008. Lehman Brothers collapsed. Within hours, credit markets froze worldwide. For Las Vegas Sands, with billions in construction loans and half-built casinos across Asia, the timing couldn't have been worse. The stock plummeted from its $144 peak to $36.11 in a matter of weeks. Adelson, watching his paper fortune evaporate, made his first move: a $475 million investment through a convertible note to shore up liquidity.

But this was just the appetizer to the main course of disaster. By November, construction had stopped on multiple Macau projects. Banks were calling loans. Suppliers demanded cash on delivery. The company's bonds traded at 30 cents on the dollar—the market was pricing in bankruptcy. Las Vegas Sands faced $2.5 billion in debt maturities in 2009 with no ability to refinance. Wall Street obituary writers sharpened their pencils.

Then came March 2009, the darkest hour. The stock hit $1.38 intraday. The company's market capitalization—which had peaked at $52 billion just 18 months earlier—sank to approximately $1 billion. To put that in perspective: the Marina Bay Sands construction alone cost more than five times the company's entire market value. Adelson's 69% stake, once worth $36 billion, was now worth less than $700 million on paper.

Adelson's response was unprecedented in casino history. Rather than negotiate with banks or seek bankruptcy protection, he opened his personal checkbook. In November 2008, the Adelson family injected $525 million, purchasing preferred stock and warrants. Then another $475 million. By the time the bleeding stopped, Adelson had invested $1 billion of his personal fortune—money from selling COMDEX, real estate holdings, and liquidating other investments—to keep Las Vegas Sands alive.

"I had commitments to finish projects," Adelson would later say. "I couldn't walk away from 20,000 construction workers in Macau and Singapore." But there was more to it. Adelson understood something the market didn't: Asian gamblers hadn't disappeared. They were waiting. While Americans were losing homes to foreclosure, Chinese manufacturers were still printing money, and they wanted somewhere to spend it.

The lifeline came from an unexpected source. In November 2009, Las Vegas Sands spun off its Macau operations through an IPO of Sands China Ltd. on the Hong Kong exchange. The offering raised $3.3 billion by selling just 29% of the subsidiary. The valuation stunned Wall Street—investors valued the Macau operations at over $11 billion while the parent company's entire market cap was still under $5 billion. The cash injection saved the company, allowing it to complete Marina Bay Sands and restart frozen Macau projects.

By December 2009, LVS stock had recovered to $17. Adelson's billion-dollar bet had paid off spectacularly. Those who bought at the March bottom saw returns of over 1,000% within a year. The near-death experience had become one of the greatest comeback stories in corporate history. More importantly, it proved Adelson's thesis: the future of gaming wasn't in America—it was in Asia.

VII. The Macau Miracle: Becoming the World's Gaming Capital

The transformation of Cotai from mudflat to the world's gaming epicenter happened so fast that satellite images from 2005 to 2015 look like time-lapse photography of bacterial growth. Where once there was only water between Taipa and Coloane islands, Adelson's vision had sparked a construction frenzy that would make Macau the undisputed gambling capital of the planet.

The numbers were staggering. In 2006, Macau gaming revenue surpassed Las Vegas for the first time. By 2013, Macau's $45 billion in gaming revenue was seven times larger than Vegas. VIP baccarat alone—high-stakes games in private rooms—generated more revenue than all of America's casinos combined. But Adelson saw beyond the VIP model that competitors chased. His "premium mass" strategy targeted the emerging Chinese middle class: entrepreneurs from Guangzhou, factory owners from Shenzhen, professionals from Shanghai who wanted to gamble but didn't need private jets and million-dollar credit lines.

The Venetian Macao proved the model. Unlike the cramped, smoky VIP rooms of old Macau, this was gambling as theater—gondoliers singing while players tried their luck at baccarat, high-end shopping between gaming sessions, Michelin-starred restaurants for celebration dinners. The property generated more EBITDA in one quarter than most Vegas casinos produced in a year.

Then came the portfolio expansion. The Four Seasons Macao, opening in 2008 despite the financial crisis, targeted ultra-luxury travelers. The Plaza Macao followed in 2012, adding 360 suites and reinforcing Sands' dominance of Cotai. But the masterstroke was The Parisian Macao, opening September 2016 with 3,000 rooms and a half-scale Eiffel Tower that became Cotai's most photographed landmark.

The Londoner Macao represented Adelson's final Macau vision before his death—a $2.2 billion transformation of Sands Cotai Central that brought British sophistication to Chinese gaming. David Beckham attended the opening. Gordon Ramsay opened a restaurant. The property featured replicas of Big Ben and the Houses of Parliament. Fully opening in February 2021, it was Adelson's last major project, a fitting capstone to his transformation of Asian gaming.

By 2019, Las Vegas Sands' Macau operations were generating over $13 billion in annual revenue—more than three times what the entire company had been worth at its 2009 nadir. The five interconnected Cotai properties functioned as an integrated ecosystem: guests could walk between properties through air-conditioned walkways, choosing from 12,000 hotel rooms, 850 luxury retail outlets, 150 restaurants, and gaming options that ranged from penny slots to private salons where single hands of baccarat could exceed $1 million.

But success bred scrutiny. Beijing watched nervously as mainland money flowed to Macau. Anti-corruption campaigns targeted government officials who gambled. Junket operators—the middlemen who brought VIP players and extended credit—faced investigations. Union Pay cards were restricted. Yet through each regulatory tightening, Sands' premium mass strategy proved resilient. Middle-class Chinese gamblers weren't corrupted officials. They were entrepreneurs and professionals spending their own money, and they kept coming.

VIII. The Singapore Success Story

While Macau grabbed headlines with astronomical VIP numbers, Marina Bay Sands quietly became Las Vegas Sands' most reliable profit engine. The property that skeptics dismissed as too expensive became a case study in operational excellence. Marina Bay Sands was projected to stimulate an addition of $2.7 billion or 0.8% to Singapore's Gross Domestic Product by 2015, employing 10,000 people directly and 20,000 jobs being created in other industries.

The property's performance defied every projection. Where analysts expected steady returns from a mature, regulated market, Marina Bay Sands delivered explosive growth. By 2019, the property was generating annual EBITDA approaching $2 billion—from a single integrated resort. The secret wasn't just gambling. Marina Bay Sands had become Asia's premier MICE destination, hosting over 1,750 new-to-Singapore events since opening. CEOs held board meetings in the SkyPark. Fashion houses launched collections at the ArtScience Museum. The world's 50 best restaurants held their awards ceremony there. When COVID-19 hit in early 2020, Singapore's swift response initially seemed like a blessing. But as the pandemic dragged on, Marina Bay Sands faced unprecedented challenges. The property temporarily closed in mid-May 2021 after two casino dealers tested positive, underwent deep cleaning, and tested its entire workforce of 7,450 team members and 800 contractors—all results came back negative. Table games were limited to two players, dine-in service was suspended, and international travel—the lifeblood of Singapore's tourism—evaporated.

Yet Marina Bay Sands demonstrated remarkable resilience. The retail mall registered an occupancy of 99% in the first quarter of 2021, even as international visitors remained absent. The property pivoted to serve local demand, introduced new safety protocols, and maintained operational excellence despite the constraints. More importantly, it continued investing—a $1 billion renovation program proceeded through the pandemic, upgrading rooms and facilities for the eventual recovery.

The recovery, when it came, was spectacular. By Q2 2023, Marina Bay Sands was achieving record-breaking revenue, significantly surpassing pre-COVID figures. Room revenue surged by 85.7 per cent to US$104 million, food and beverage revenue spiked by 75 per cent to US$84 million, and convention, retail, and other revenue climbed by 55 per cent to US$31 million. The property had not just survived—it had emerged stronger. The expansion story continues to evolve. On April 3, 2019, Sheldon Adelson announced that Marina Bay Sands had "achieved amazing success for both Singapore and our company and we plan to create even more with this expansion." The initial plan called for a $3.3 billion investment in a new hotel tower with approximately 1,000 all-suite rooms and a sky roof with swimming pool and signature restaurant, plus a 15,000-seat arena to attract top entertainers from Asia and around the world.

But the vision has grown dramatically. By 2024, Las Vegas Sands revealed it would spend a massive US$8 billion on what is now dubbed "Marina Bay Sands IR2", positioning it not as an expansion but as an entirely new full-scale integrated resort development. The project will feature 570 luxury suites, its own casino including "sky gaming" in the tower, 110,000 square feet of MICE space, its own SkyPark, and a 15,000-seat arena designed to be the leading live entertainment venue in Asia.

Construction is scheduled to commence in June 2025, with completion expected by June 2030 and an estimated official opening set for January 2031. The economics are compelling: CEO Robert Goldstein expects Singapore GGR to grow from US$6.5 billion in 2024 to as much as US$11 billion long-term, with the new project adding another US$1 billion in annual EBITDA.

IX. The Las Vegas Exit: Strategic Pivot to Asia

The announcement came just two months after Sheldon Adelson's death. On March 3, 2021, Las Vegas Sands revealed it would sell The Venetian Resort Las Vegas and the Sands Expo and Convention Center for $6.25 billion. Apollo Global Management would acquire the operations for $2.25 billion, while VICI Properties would purchase the land and real estate for $4 billion. The transaction closed on February 23, 2022, ending Las Vegas Sands' presence on the Strip after more than three decades.

By the end of 2020, Las Vegas Sands sought to focus on its Macau properties, which include The Venetian Macao. The logic was clear. COVID had devastated Las Vegas—visitation dropped from 42 million in 2019 to just 19 million in 2020. Meanwhile, Asia was expected to recover faster, and the company's Macau and Singapore properties generated far superior returns even in normal times.

Robert Goldstein, who succeeded Adelson as CEO, explained the strategic rationale: "Asia remains the backbone of this company and our developments in Macao and Singapore are the center of our attention." It was a remarkable pivot—the company that bore Las Vegas's name and had revolutionized the Strip with the integrated resort concept was abandoning its birthplace entirely.

The sale marked more than just a geographic shift. It represented the culmination of Adelson's vision that gambling's future lay not in America but in Asia. The Venetian and Palazzo, which Adelson had built as monuments to luxury and convention business, would continue under new ownership. But Las Vegas Sands itself would become a purely Asian operator, focused on the markets where a single VIP player might wager more in an evening than an entire Las Vegas casino floor generated in a week.

For George Markantonis, who had spent seven years running the Vegas properties and would continue as CEO under Apollo, the transition was bittersweet. "We have an exciting opportunity to build on our past successes while capturing future opportunities," he said. But for Las Vegas Sands, the future lay 7,000 miles away, in the baccarat salons of Macau and the skyline of Singapore.

X. Leadership Transition & Modern Challenges

Sheldon Gary Adelson died on January 11, 2021, at his home in Malibu, California, at the age of 87, after long-term illnesses. The man who had started with a $200 loan to buy a newspaper stand had built an empire worth $35 billion at its peak. But his death came at a critical juncture—Las Vegas Sands was still reeling from COVID-19, with a 97.1% decrease in revenue and a second-quarter fiscal loss of $985 million.

Robert Goldstein, 65, who had been serving as acting CEO during Adelson's medical leave, was named permanent CEO and chairman on January 26, 2021. Goldstein had joined Sands in 1995 and worked in various roles including president and chief operating officer of The Venetian and The Palazzo Las Vegas, and most recently as president and chief operating officer for the casino group.

The transition wasn't just about replacing a founder—it was about navigating existential challenges. Macau remained under China's zero-COVID policy, with border restrictions that eliminated the VIP business overnight. Singapore faced repeated closures and capacity restrictions. The company that had survived 2008 by Adelson's sheer force of will now faced an even more uncertain future.

Goldstein's approach differed markedly from his predecessor's. Where Adelson had been ideologically opposed to online gambling, believing it fostered problem gambling, Goldstein began talking to potential partners about a role for Sands in sports betting, either by licensing its brands or building its own online platform. He accelerated the Vegas sale, recognizing that Asia's recovery would drive the company's future. But the biggest challenge loomed in Macau. The gaming licenses for all six operators—including Las Vegas Sands—were set to expire in June 2022. For nearly two years, uncertainty hung over the market as Beijing signaled its intent to tighten oversight and reduce the industry's reliance on VIP gambling. In September 2021, shares of Sands China dropped 28% in a single day when Macau's economy secretary announced strengthened oversight measures.

The anxiety was palpable. Three US operators—Las Vegas Sands, MGM Resorts, and Wynn Resorts—had invested billions in Macau. If Beijing decided to punish American companies amid deteriorating US-China relations, Las Vegas Sands stood to lose everything that mattered.

Goldstein struck a careful tone during investor calls. "I see no chance of that whatsoever," he said when asked about worst-case scenarios. "I think the government recognizes we've been a good licensee." Behind the scenes, the company pledged massive new investments—Sands China promised to invest approximately $3.5 billion over the next decade, with more than 90% going toward non-gaming projects.

The relief came in November 2022. All six incumbent operators received 10-year license renewals. But the terms reflected Beijing's new priorities: operators committed to invest a total of $15 billion, with the vast majority directed toward non-gaming attractions. The era of VIP rooms and junket operators was officially over. The future would be about theme parks, conventions, and family entertainment—ironically, closer to Adelson's original vision for integrated resorts.

XI. Playbook: Business & Investing Lessons

The Las Vegas Sands story offers a masterclass in contrarian thinking, leverage, and geographic arbitrage. Adelson's playbook wasn't about gambling—it was about recognizing that casinos were merely the cash engine for a larger real estate and entertainment business model.

The Integrated Resort Innovation: Adelson didn't invent casinos or conventions. He combined them in a way nobody had imagined. The Venetian proved that business travelers would pay premium rates for luxury suites where they could hold meetings, that their spouses would shop while they attended conferences, and that the casino would capture whatever entertainment budget remained. This wasn't gambling with a hotel attached—it was a self-contained city where the casino subsidized everything else.

Geographic Diversification as Survival Strategy: When Adelson bet on Macau in 2004, skeptics called him crazy. Why leave Vegas for an unknown market? But Adelson understood that geographic diversification wasn't just about growth—it was about survival. When 2008 nearly killed the company, Asian operations provided the lifeline. When COVID shut down Macau, Singapore kept generating cash. The lesson: in capital-intensive businesses, geographic diversity isn't optional.

The Art of Leverage: Adelson's relationship with debt was extraordinary. He leveraged everything—assets, relationships, his own reputation. The 2008 crisis should have killed Las Vegas Sands. With $2.5 billion in debt coming due and no ability to refinance, bankruptcy seemed inevitable. But Adelson understood that when you owe the bank $100, it's your problem; when you owe $2.5 billion, it's their problem. By investing his own billion, he bought time for markets to recover and assets to appreciate.

Building in Regulated Markets: While tech entrepreneurs disrupted unregulated industries, Adelson thrived in the most regulated business imaginable. Gaming licenses are literally licenses to print money—if you can get them. Adelson mastered the art of working with governments, whether convincing Singapore to legalize casinos or navigating Macau's opacity. High barriers to entry meant that once you were in, competition was limited and returns were extraordinary.

The Premium Mass Strategy: While competitors chased whales with private jets and million-dollar credit lines, Adelson focused on the "premium mass"—successful professionals who might gamble $10,000 in a weekend rather than $10 million. This segment was more stable, less regulated, and ultimately more profitable. When China cracked down on VIP gambling, Sands' premium mass focus proved prescient.

Capital Allocation in Capital-Intensive Businesses: Every Adelson property was a multi-billion-dollar bet. Marina Bay Sands cost $5.6 billion. The Parisian Macao ran $2.9 billion. These weren't iterative software products you could test and pivot. One wrong bet could destroy the company. Yet Adelson's hit rate was extraordinary because he understood his customer better than anyone—not the gambler, but the entire family on vacation.

Founder Control and Succession: Adelson maintained iron grip control through super-voting shares and personal relationships. This allowed long-term thinking and massive bets that public company CEOs could never make. But it also created succession challenges. The company that was synonymous with Sheldon Adelson had to reinvent itself without him.

XII. Analysis & Bear vs. Bull Case

Bull Case:

The bullish thesis for Las Vegas Sands rests on Asian demographics and the irreplaceability of its assets. Macau and Singapore hold duopoly/oligopoly positions in their respective markets with regulatory moats that make new competition virtually impossible. The Macau license renewal through 2032 provides a decade of certainty in the world's largest gaming market.

Marina Bay Sands' $8 billion expansion will add another $1 billion in annual EBITDA according to management projections. Singapore's GDP per capita exceeds $80,000, and the country serves as the financial hub for Southeast Asia's 700 million people. The property already generates industry-leading margins; expansion simply multiplies a proven model.

Chinese middle-class growth remains the mega-trend. Despite recent economic challenges, hundreds of millions of Chinese have disposable income for the first time in history. When China eventually relaxes COVID policies and restores normal travel, the pent-up demand could drive a gaming super-cycle. Sands owns the best-positioned assets to capture this recovery.

The balance sheet has been restructured and strengthened. The company has $4.45 billion in available credit facilities and generates substantial free cash flow even at reduced capacity. Unlike 2008, Sands can weather extended downturns without existential risk.

Bear Case:

The bearish view focuses on regulatory risk and structural challenges to the business model. Beijing's crackdown on Macau gaming isn't over—it's evolving. The shift from gaming to entertainment sounds appealing but destroys returns. Theme parks and concerts don't generate 90% margins like VIP baccarat. Sands is being forced to become a lower-return business to maintain its licenses.

China's relationship with gambling is fundamentally conflicted. The government tolerates Macau as a source of tax revenue but sees gambling as social poison. Any economic downturn or political shift could trigger new restrictions. The era of mainlanders flooding Macau with suitcases of cash is over permanently.

Singapore's expansion costs $8 billion but adds only 570 suites. That's $14 million per room—impossible math without massive gaming revenue. But Singapore actively discourages local gambling and international travel remains below pre-pandemic levels. The expansion could become a white elephant.

Digital disruption looms larger than incumbents admit. Online gambling, cryptocurrency casinos, and virtual experiences are attracting younger demographics. The integrated resort model—flying thousands of miles to pull slot machine handles—may be approaching obsolescence. Sands has no digital strategy and cultural DNA that resists online gambling.

The company trades at premium valuations despite facing its most uncertain period since 2008. Investors are betting on a return to 2019 performance that may never materialize. The world that made Sheldon Adelson a billionaire—Chinese VIP gambling, unlimited credit, and regulatory tolerance—no longer exists.

XIII. Epilogue & "If We Were CEOs"

The story of Las Vegas Sands is really three stories: the rise of Sheldon Adelson from newspaper boy to billionaire, the transformation of gambling from vice to entertainment, and the shift of economic gravity from West to East. Each story contains lessons about ambition, timing, and the price of success.

If we were running Las Vegas Sands today, the strategic imperatives would be clear but execution would be enormously complex. First, accept that the VIP era is dead and build for the premium mass future. This means smaller rooms, more restaurants, and entertainment options that appeal to families rather than high-rollers. The Singapore expansion already reflects this shift—it's not really about gambling at all.

Second, develop a digital strategy that doesn't cannibalize physical properties but extends the brand to younger demographics. This doesn't mean online casinos—it means gaming-adjacent experiences like esports venues, NFT collectibles tied to properties, and virtual concerts in the metaverse. The customers who will drive profits in 2040 are teenagers today playing Fortnite, not sitting at slot machines.

Third, explore new markets while they're still available. Japan's integrated resort licenses remain unclaimed. The UAE is liberalizing gaming laws. India's supreme court opened doors for casino licensing. The next Macau exists—but the window to enter will be narrow. Sands needs to move fast while its balance sheet and reputation still open doors.

Fourth, radically restructure the cost base for a lower-margin future. The days of 60% EBITDA margins are over. Beijing has made clear that Macau's future is as a family entertainment destination, not a gambling den. That means operating leverage must come from efficiency, not pricing power.

Finally, consider the unthinkable: a merger with another Macau operator. The market is being forced toward lower returns and higher capital requirements. Consolidation could provide scale advantages and reduce duplicate investments in non-gaming amenities. Regulators might even encourage it as a path to stability.

Sheldon Adelson built Las Vegas Sands on a simple insight: gambling was just the engine for a much larger hospitality and entertainment business. That insight remains valid, but the engine is being replaced. The question isn't whether Las Vegas Sands can survive without gambling at the center—it's whether any company can generate Adelson-like returns in the new world Beijing is creating.

The house always wins, Adelson liked to say. But he knew the real trick wasn't owning the house—it was knowing which house to build, where to build it, and when to walk away. His greatest genius may have been selling the Venetian just before his death, ensuring his legacy would forever be tied to creation rather than decline. The company that bears Las Vegas's name but owns nothing there stands as a monument to geographic arbitrage, regulatory capture, and the eternal human desire to beat the odds.

In the end, Las Vegas Sands is a meditation on capitalism itself—the ability to spot inefficiencies, deploy capital, and extract returns that seem impossible until someone proves they're not. Adelson did that repeatedly, turning borrowed money into billions, empty land into cities, and a dying hotel into a global empire. The question for his successors isn't whether they can repeat his success—it's whether anyone could in a world that no longer allows such audacious bets.

The chips are down. The cards are dealt. The next chapter of Las Vegas Sands will be written by leaders who never met a gangster, never built a casino from scratch, and never risked personal bankruptcy for their vision. Whether that's a weakness or a strength will determine if the company Sheldon Adelson built can outlive the era that created it.

XIV. Recent News**

Financial Performance Update (2024-2025):**

Las Vegas Sands reported full year 2024 net income attributable to Las Vegas Sands of $1.45 billion, or $1.96 per diluted share, compared to $1.22 billion, or $1.60 per diluted share, in 2023. Revenue for full year 2024 reached US$11.3 billion (up 8.9% from FY 2023), with net income of US$1.45 billion (up 18% from FY 2023) and profit margin improving to 13% from 12% in FY 2023.

For Q1 2025, operating income was $609 million compared to $717 million in the prior year quarter, with net income of $408 million compared to $583 million in Q1 2024, and consolidated adjusted property EBITDA of $1.14 billion compared to $1.21 billion in the prior year quarter.

Capital Returns Program:

The LVS Board of Directors has authorized $2.0 billion of share repurchases in the future and raised the annual dividend to $1.00 per share for the 2025 calendar year, with the company looking forward to utilizing share repurchase and dividend programs to continue to return excess capital to stockholders. During Q1 2025, the company repurchased $450 million of common stock (approximately 10 million shares at a weighted average price of $44.59), with the Board subsequently authorizing an increase in the remaining share repurchase amount from $1.10 billion to $2.0 billion.

Market Conditions:

In Macao, the ongoing recovery continued during Q4 2024, although spend per visitor in the market remains below the levels reached prior to the pandemic, with the company's decades-long commitment to investments positioning it well as the recovery in travel and tourism spending progresses. In Q1 2025, while market growth has softened in Macao in the current environment, the company's decades-long commitment to making investments that enhance the business and leisure tourism appeal of Macao positions it well for future growth.

In Singapore, Marina Bay Sands continued to deliver outstanding financial and operating performance. The property remains a key profit driver as the company executes its $8 billion expansion plan.

Ownership Changes:

During Q4 2024 and January 2025, Las Vegas Sands purchased $250 million of SCL common stock (103 million shares at an average price of HK$18.93), increasing the company's ownership percentage of SCL to 72.3% as of January 7, 2025.

XV. Links & Resources

Key SEC Filings: - Las Vegas Sands Corp. Investor Relations: www.investor.sands.com - Annual Reports (10-K) and Quarterly Reports (10-Q) - Proxy Statements and Material Event Filings (8-K)

Books on Sheldon Adelson and Las Vegas Sands: - "The Last Tycoon: The Many Lives of Sheldon Adelson" by Christina Binkley - "Winner Takes All" by Christina Binkley - "Roll the Dice" by Wayne Barrett

Macau Gaming Industry Reports: - Macau Gaming Inspection and Coordination Bureau (DICJ) Monthly Reports - Morgan Stanley Asia Gaming Research - JP Morgan Macau Gaming Analysis - Credit Suisse Macau Gaming Sector Reports

Singapore Tourism and Gaming Studies: - Singapore Tourism Board Annual Reports - Marina Bay Sands Impact Studies - National University of Singapore Business School Gaming Research

Academic Papers: - "The Economics of Casino Gaming" - Journal of Economic Perspectives - "Integrated Resort Development in Asia" - Cornell Hotel School Research - "Gaming License Valuation Models" - Journal of Gambling Studies

Documentary Resources: - "Casino Jack" (2010) - Documentary on lobbying and casino politics - Bloomberg Documentaries on Macau Gaming Industry - CNBC Specials on Asian Gaming Markets

Regulatory Framework Documents: - Macau Gaming Law and Concession Agreements - Singapore Casino Control Act - Nevada Gaming Control Board Regulations

Architecture and Design: - Safdie Architects Portfolio - Marina Bay Sands Design - Architectural Digest Features on Integrated Resorts - Engineering Case Studies on Marina Bay Sands Construction

Financial Crisis Case Studies: - Harvard Business School Case: "Las Vegas Sands Corp. - The Venetian" - Stanford Business Case: "Surviving the 2008 Financial Crisis" - Wharton Study: "Leverage and Survival in Gaming Industry"

Industry Analyst Coverage: - Union Gaming Analytics - Macquarie Research Gaming Reports - Deutsche Bank Gaming Sector Analysis - Bernstein Research Asia Gaming Coverage

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube