Abbott Laboratories: From Chicago Pharmacy to Global Healthcare Giant

I. Cold Open & Company Overview

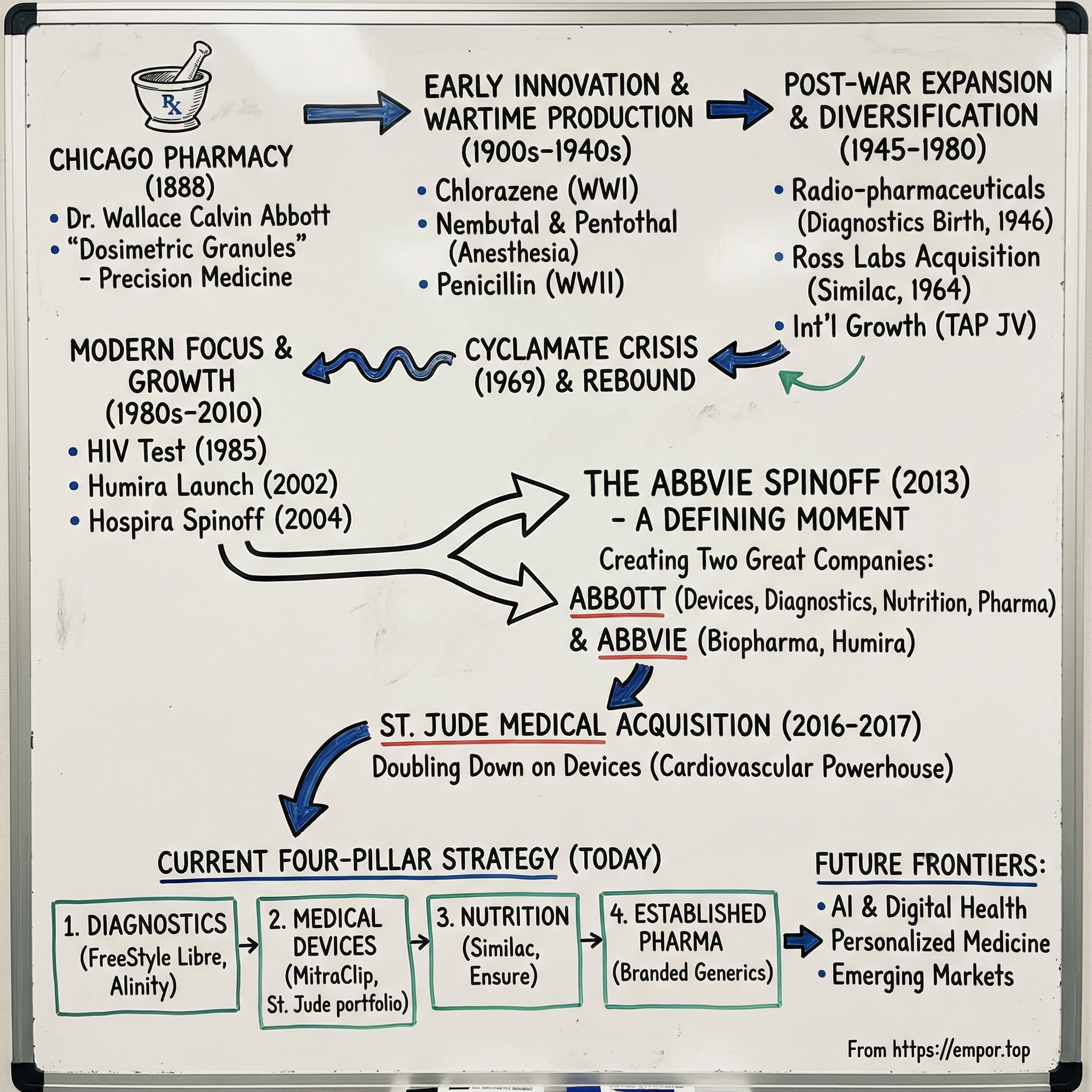

Picture this: Chicago, 1888. A 30-year-old physician named Wallace Calvin Abbott stands in the back room of his People's Drug Store, meticulously measuring alkaloid compounds into tiny granules. He's frustrated—frustrated with the inconsistent potencies of medicines, frustrated with patients suffering from improper dosing, frustrated with an industry that seems content with "good enough." His solution? Transform the very nature of pharmaceutical manufacturing by applying scientific precision to every pill.

Fast forward 135 years. That backroom operation has morphed into Abbott Laboratories—a $43 billion revenue healthcare colossus that touches one in three people on Earth every single day. From the glucose monitors checking blood sugar in Mumbai to the heart devices saving lives in Manhattan, from infant formula nourishing babies in São Paulo to diagnostic tests that detected COVID-19 in billions of samples worldwide—Abbott's transformation represents one of healthcare's most remarkable evolution stories.

The burning question isn't just how a Chicago pharmacy became a global healthcare giant. It's how Abbott repeatedly reinvented itself through wars, depressions, regulatory disasters, and industry upheavals while competitors fell by the wayside. How did it build, acquire, and sometimes courageously spin off entire divisions worth tens of billions? And perhaps most intriguingly—in an era when investors reward pure-play focus, how does Abbott thrive as one of healthcare's last great conglomerates?

This is the story of strategic pivots executed with surgical precision. Of betting the company on anesthetics in the 1920s, antibiotics in the 1940s, diagnostics in the 1970s, and medical devices in the 2010s. It's about knowing when to double down and when to let go—like the momentous decision to spin off AbbVie with its blockbuster drug Humira, creating two Fortune 500 companies from one.

Today's Abbott operates through four roughly equal pillars: diagnostics that revolutionized continuous glucose monitoring, medical devices dominating cardiovascular markets, nutrition brands feeding generations from birth through old age, and established pharmaceuticals serving emerging markets. It's a portfolio approach that defies modern corporate orthodoxy—and consistently delivers.

What we'll uncover is a masterclass in portfolio management, strategic timing, and the delicate art of managing diverse businesses under one roof. We'll explore how Abbott navigated the cyclamate crisis that nearly destroyed its artificial sweetener business, weathered the 2022 infant formula recall that shook consumer confidence, and emerged from each crisis somehow stronger. We'll dissect the $25 billion St. Jude Medical acquisition that doubled its devices growth rate overnight, and understand why spinning off AbbVie—which took Abbott's most profitable drugs—actually unlocked value for both companies.

This journey takes us from alkaloidal granules to AI-powered diagnostics, from a doctor's frustration to a healthcare empire, from one man's vision to impacting billions of lives. Welcome to the Abbott Laboratories story—where scientific rigor meets strategic brilliance, where patience meets opportunism, and where a 135-year-old company keeps reinventing what healthcare can be.

II. The Wallace Abbott Era & Early Innovation (1888–1921)

The rain drummed against the windows of the People's Drug Store as Dr. Wallace Calvin Abbott hunched over his workbench, grinding medicinal plants with a mortar and pestle. It was 1888, and the 30-year-old physician had grown increasingly frustrated with the medicines available to his Chicago patients. Liquid extracts varied wildly in potency. Powders were messy and imprecise. Pills were inconsistent. Patients suffered not from lack of treatment, but from treatments that couldn't be properly dosed.

Abbott's breakthrough came from a simple observation: plants contained specific active ingredients—alkaloids—that produced their medicinal effects. What if, instead of using the whole plant with its variable potency, he could isolate these alkaloids and create precisely measured doses? Working in the cramped back room of his pharmacy at the corner of North Avenue and Larrabee Street, Abbott began producing what he called "dosimetric granules"—tiny pills containing exact amounts of active ingredients.

The concept was revolutionary for its time. While other pharmacists were still mixing tonics and tinctures with more art than science, Abbott applied rigorous standardization to every batch. Each granule was tested, measured, and guaranteed to contain a specific dose. For physicians accustomed to guessing whether their prescriptions would be too weak or dangerously strong, Abbott's granules were a revelation. That first year—1888—sales totaled just $2,000, barely enough to keep the lights on. But Abbott possessed something more valuable than capital: conviction. He believed the future of medicine lay not in mixing potions but in manufacturing precision. While established pharmaceutical companies dismissed his granules as a novelty, practicing physicians began to notice something remarkable—their patients were getting consistent results for the first time. Abbott's income leaped from $2,000 in 1888 to $8,000 in 1890, a quadrupling in just two years. Word spread through medical journals and physician networks about these revolutionary "dosimetric granules" that actually delivered what they promised. By 1905, annual sales had reached $200,000, and by 1923 they hit $2 million—a ten-fold increase in less than two decades.

The company's growth wasn't just financial; it was philosophical. In 1900, Abbott incorporated as the Abbott Alkaloidal Company, bringing in other physicians as shareholders who believed in his scientific approach. Abbott wasn't just selling pills—he was evangelizing a revolution in pharmaceutical practice. Through self-published magazines like "The Alkaloidal Clinic," he educated doctors nationwide about the benefits of standardized dosing, building a community of believers who became both customers and advocates. The name change to Abbott Laboratories in 1915 reflected something deeper than corporate evolution—it signaled the transformation from a pharmacy operation to a research-driven enterprise. The company's growing research orientation and move into synthetic compounds drove this rebranding, positioning Abbott as a scientific innovator rather than merely a drug compounder.

World War I became Abbott's first major test as a national supplier. In 1916, Abbott produced Chlorazene, its first synthetic medicine—a breakthrough antiseptic developed by British chemist Dr. Henry Dakin to treat wounded World War I soldiers. The war created unprecedented demand for antiseptics and anesthetics that had previously been imported from Germany. With those supply lines cut, Abbott stepped into the breach, developing not just Chlorazene but also procaine (a replacement for German novocaine) and barbital (a substitute for veronal).

The war years proved that Abbott could innovate under pressure and scale production rapidly. But they also revealed something more profound: the company's ability to pivot from being a supplier of existing medicines to becoming a creator of new ones. This wasn't just wartime opportunism—it was the birth of Abbott's research culture that would define its next century.

By 1921, when Wallace Abbott died at age 63, he had built more than a company—he had established a philosophy. His insistence on scientific rigor, standardized manufacturing, and physician education created a foundation that would support decades of growth. Annual sales rose from about $200,000 in 1905 to $2 million by 1923, but the numbers only told part of the story. Abbott had proven that American pharmaceutical companies could compete on innovation, not just production. The small Chicago pharmacy had become a research-driven manufacturer with international ambitions, setting the stage for its emergence as a major force in anesthetics, antibiotics, and beyond.

III. Building the Foundation: Anesthesia & Early Pharmaceuticals (1920s–1940s)

The boardroom at Abbott Laboratories fell silent on that October day in 1921. Dr. Wallace Abbott was dead, and with him went the only leader the company had ever known. Into this void stepped Dr. Alfred Stephen Burdick, a man who understood that Abbott's future lay not in mourning its founder but in accelerating his vision. Burdick faced an immediate choice: play it safe during the turbulent 1920s, or double down on research and innovation. He chose the latter—a decision that would transform Abbott from a successful regional player into a pharmaceutical powerhouse.

In 1921, Dr. Alfred Stephen Burdick was named president of the company. Eight years later Abbott was listed on the Chicago Stock Exchange—the offering was 20,000 shares for $32 each. The timing seemed catastrophic—going public in 1929, the very year of the Wall Street crash that triggered the Great Depression. Yet what appeared to be terrible timing became a testament to Abbott's resilience and strategic positioning. The 1920s marked Abbott's golden age of anesthesia innovation. The development of Butyn, a butyl alcohol-based anesthetic, marked the beginning of Abbott's long, productive and ground-breaking involvement in the field of anesthesia. But the real breakthrough came from the laboratories of Ernest Volwiler and Donalee Tabern, two Abbott chemists whose work would revolutionize surgery worldwide.

Nembutal, developed by Ernest H. Volwiler and Donalee L. Tabern of Abbott Laboratories in 1930, was a novel barbiturate that could induce sleep within 20 minutes. It had the advantage of rarely producing hangovers or other side effects. For surgeons accustomed to the unpredictable effects of ether and chloroform, Nembutal represented a quantum leap in patient safety and comfort. The drug became Abbott's best-known and longest-lived product, establishing the company as the global leader in anesthetics. But the most revolutionary moment came in 1935 with the introduction of Pentothal. Volwiler and Tabern had spent three years screening over 200 compounds searching for a substance that could be injected directly into the bloodstream to produce unconsciousness. Sodium thiopental, which they discovered in 1934, was first used in human beings on March 8, 1934, by Dr. Ralph M. Waters in an investigation of its properties. The drug revolutionized intravenous anesthesia—it was smooth, pleasant, and didn't cause the muscle twitching or psychic side effects of earlier anesthetics.

Pentothal would become known colloquially as "truth serum" for its tendency to make patients talk freely. More importantly, it transformed surgery from a race against time while patients suffered under ether to a controlled, manageable procedure. For their achievement, Volwiler and Tabern were inducted into the National Inventors Hall of Fame in 1986, joining luminaries like Henry Ford, Thomas Edison, and the Wright Brothers.

By 1932, even as the Great Depression ravaged the economy, Abbott was expanding thanks to its leadership in new fields such as vitamins and intravenous solutions. "Few of the leading industrial organizations of the country," notes Nation's Commerce magazine, "can show a sounder record for the past year than the Abbott Laboratories." The company's stock, despite being issued at the worst possible moment in 1929, grew in value from that first day—approximately 10,000 times over by modern times.

World War II presented Abbott with its greatest challenge and opportunity yet. In 1942, Abbott joined a consortium of pharmaceutical makers, at the behest of the U.S. Government, to ramp up production of penicillin for wartime use. Together they increased production more than 20,000%. The first pharmaceutical companies to commit were Merck and Squibb, joined a year later by Pfizer. Later, the Midwest group—Eli Lilly, Abbott Laboratories, Upjohn, and Parke, Davis—entered into a similar arrangement for information exchange.

The penicillin project revealed something crucial about Abbott's character: when national need called, the company could mobilize its research and manufacturing capabilities at unprecedented scale. By 1945, U.S. production had soared to 4 million sterile packages of penicillin per month. Abbott's participation in this wartime consortium established it as a trusted partner to government and positioned it perfectly for the antibiotic boom that would follow.

The period from the 1920s through the 1940s transformed Abbott from a successful regional pharmaceutical company into a national powerhouse. Through the Depression, it grew. Through war, it innovated. Through crisis, it scaled. By 1945, Abbott had proven it could develop breakthrough drugs, manufacture at massive scale, and collaborate when necessary while competing when appropriate. The foundation was set for its emergence as a global healthcare leader.

IV. Post-War Expansion: Diagnostics, International Growth & Diversification (1945–1980)

The mushroom cloud over Hiroshima marked more than the end of World War II—it signaled the dawn of the atomic age, and with it, an entirely new frontier for medicine. In 1946, while other pharmaceutical companies celebrated victory and returned to peacetime production, Abbott made a curious move: it became the first pharmaceutical company to establish a special laboratory for radiopharmaceuticals. To most observers, radioactive medicine seemed like science fiction. To Abbott, it looked like the future.

In 1946, Abbott became the first pharmaceutical company to have a special laboratory for radiopharmaceuticals—a move that led to the creation of the world's leading immunodiagnostics business. This wasn't just adding another product line; it was Abbott's first major step outside traditional pharmaceuticals, a decision that would fundamentally reshape the company's identity over the next three decades.

The radiopharmaceutical lab produced Radiocaps in 1953—capsules containing an accurately controlled, invisible film of radioiodine that simplified the diagnosis and treatment of thyroid disorders. For the first time, doctors could trace the path of medicine through the human body in real-time. Abbott had entered the diagnostics business not through acquisition but through innovation, establishing a pattern that would define its diversification strategy for decades. In 1952 Abbott developed erythromycin, which represented a significant portion of Abbott's prescription drug business for several decades. This antibiotic became one of the most important alternatives to penicillin, particularly for patients with allergies. Abbott's entry into the antibiotic market beyond penicillin demonstrated its ability to compete in the rapidly evolving pharmaceutical landscape of the 1950s.

The company's diversification strategy accelerated dramatically in the 1960s. In the 1960s Abbott began to pursue a new strategy that would place less emphasis on the pharmaceutical business by diversifying into other fields such as consumer goods. This wasn't diversification for its own sake—it was a calculated bet that healthcare extended beyond prescription drugs into everyday health and nutrition products. In 1964, it merged with Ross Laboratories, making Ross a wholly owned subsidiary of Abbott, and Richard Ross gained a seat on Abbott's board of directors. The acquisition of Ross brought Similac under the Abbott umbrella. This wasn't just adding a product—it was Abbott's entry into infant nutrition, a market that would become central to its identity. Ross Laboratories had been founded in 1903 as the Moores & Ross Milk Company in Columbus, Ohio, and had created Similac in 1925. The merger instantly made Abbott a leader in pediatric nutrition.

The Ross acquisition proved prescient. In the years following, Pedialyte and Ensure were introduced as nutritional products by Ross Laboratories while under Abbott's leadership. By 1973, Ross introduced Ensure, which would become the world's leading adult nutritional product. Abbott had discovered that healthcare extended from birth through old age, from acute care to daily nutrition.

Abbott also developed Murine eye drops, Selsun Blue hair shampoo, Faultless golf balls, Glad Hands rubber gloves, and Pream non-dairy creamer. Some of these ventures seem bizarre in retrospect—what was a pharmaceutical company doing making golf balls? But they reflected Abbott's belief that health and wellness extended beyond prescription drugs into everyday consumer products.

The company's biggest consumer success—and disaster—came with Sucaryl, a cyclamate sugar substitute. Initially marketed to diabetics in the 1950s, it became phenomenally successful in the 1960s as diet consciousness swept America. By 1969, cyclamate sales had grown so dramatically that they accounted for one-third of Abbott's consumer product revenues—about $50 million. Then disaster struck. In October 1969, researchers hired by Abbott Laboratories found possibly malignant tumors in rats that were fed high doses of cyclamates. The doses required to produce the tumors were equivalent to an individual drinking 350 bottles of diet cola per day, but that nuance was lost in the ensuing panic. On October 18, 1969, Health, Education, and Welfare Secretary Robert Finch announced that cyclamate would be banned, effective February 1, 1970.

The cyclamate ban was a catastrophe for Abbott. One-third of its consumer product revenues evaporated overnight. Millions of dollars in inventory had to be destroyed. The company's stock plummeted. But more importantly, the crisis exposed the risks of Abbott's diversification strategy. Moving beyond pharmaceuticals into consumer products meant exposure to different regulatory frameworks, consumer preferences, and political pressures.

The early 1970s brought more troubles. In 1971, Abbott was forced to recall 3.4 million bottles of intravenous solution due to contamination concerns. The company faced questions about quality control across its sprawling operations. Critics wondered if Abbott had grown too fast, diversified too broadly, lost focus on its core competencies.

Yet from this crisis came clarity. Abbott Diagnostics Division was formed in 1973, consolidating the company's various diagnostic initiatives into a focused business unit. That same year, it introduced Ausria, a breakthrough radioimmunoassay test for detecting serum hepatitis, marking the beginning of Abbott's modern diagnostics business. The company was learning to manage diversity through structure, to turn breadth into strength rather than weakness. International expansion became critical to Abbott's growth strategy. In 1962 Abbott entered into a joint venture with Dainippon Pharmaceutical Co., Ltd., of Osaka, Japan, to manufacture radio-pharmaceuticals. Then in 1977 Abbott entered into a joint venture with Takeda Chemical Industries, Ltd. of Japan called TAP Pharmaceuticals Inc. The TAP joint venture was created by Takeda and Abbott in 1977 and became one of the most successful joint ventures in the history of American business.

TAP launched blockbuster drugs Lupron (leuprorelin) in 1985, then Prevacid (lansoprazole) in 1995. The venture demonstrated Abbott's ability to partner effectively across cultures and markets, accessing Japanese innovation while providing American commercialization expertise. The partnership would last over 30 years, generating billions in revenue before its dissolution in 2008.

By 1980, Abbott had transformed from a domestic pharmaceutical company into a global healthcare conglomerate. Its presence spanned pharmaceuticals, diagnostics, medical devices, nutrition, and consumer products. It operated in dozens of countries, partnered with companies worldwide, and had learned to navigate different regulatory environments, cultural contexts, and market dynamics.

The period from 1945 to 1980 saw Abbott evolve from a wartime penicillin producer to a diversified healthcare leader. Through strategic acquisitions like Ross Laboratories, bold moves into new technologies like radiopharmaceuticals, and successful international partnerships like TAP, Abbott proved it could grow beyond its pharmaceutical roots. The cyclamate crisis taught hard lessons about risk management and regulatory compliance. But more importantly, this era established the template for Abbott's future: a willingness to enter new markets, the ability to manage diverse businesses, and the strategic vision to see healthcare as more than just pills and prescriptions.

V. The Modern Abbott Takes Shape: Focus & Growth (1980–2010)

The conference room at Abbott headquarters fell silent as the new CEO took his position at the head of the table. It was 1998, and Miles D. White, at just 43 years old, was about to become one of the youngest chief executives of a major pharmaceutical company. The challenges facing him were immense: Abbott's stock had underperformed for years, R&D productivity was declining, and larger competitors threatened to swallow the company whole in an era of mega-mergers. White's solution would be audacious—transform Abbott from a traditional pharmaceutical company into something entirely new.

Miles D. White was elected chief executive officer in 1998. Later in 1999, White was named chairman as well. White had joined Abbott in 1984 and worked his way up through the diagnostics division, giving him a unique perspective on the company's non-pharmaceutical businesses. His appointment signaled a strategic shift—Abbott would no longer define itself primarily as a drug company but as a diversified healthcare enterprise.

The late 1990s pharmaceutical industry was consolidating rapidly. Pfizer acquired Warner-Lambert for $90 billion. Glaxo Wellcome merged with SmithKline Beecham to form GlaxoSmithKline. The conventional wisdom was clear: get bigger in pharmaceuticals or get acquired. White chose a third path—get more diverse and more focused simultaneously.

Abbott's first major move under White came through international expansion. In February 2010, Abbott acquired the pharmaceuticals unit of Solvay S.A. for US$6.2 billion, gaining many additional pharmaceutical products and an increased presence in emerging markets. That year Abbott said it would buy Piramal Healthcare of India's large generic drugs unit for $3.72 billion. These weren't just acquisitions—they were strategic repositioning moves, betting that emerging markets would drive healthcare growth in the 21st century.

But the most dramatic transformation came earlier, in 2004, when Abbott spun off its hospital products division into a new 14,000 employee company, Hospira. This move puzzled many analysts. Why would Abbott divest a profitable business? The answer revealed White's strategic vision: Abbott would focus on higher-margin, differentiated products while shedding commodity businesses, even profitable ones.

The diagnostics division became a centerpiece of Abbott's transformation. In 1985, Abbott had developed the first diagnostic test for AIDS, one of its greatest achievements and the first significant medical victory against what had seemed an unstoppable threat. This breakthrough established Abbott as a leader in infectious disease diagnostics, a position it would leverage repeatedly over the coming decades.

Throughout the 2000s, Abbott continued to build its diagnostics capabilities through both internal development and acquisition. The division evolved from selling individual tests to providing complete laboratory solutions, from reactive diagnostics to predictive health management. By 2010, Abbott's diagnostics business generated over $3 billion in annual revenue, making it one of the world's largest diagnostics companies.

The nutrition business also flourished under focused investment. Building on the Ross Laboratories foundation, Abbott expanded its portfolio beyond Similac and Ensure. In 1998, Abbott introduced Glucerna, a group of cereals, health shakes and snack bars formulated specifically for diabetics and others with dietary restrictions. The company recognized that nutrition was becoming medicalized—food as medicine rather than mere sustenance.

Abbott's pharmaceutical business, while no longer the sole focus, continued to produce important innovations. In 2002, FDA approved Humira, the first fully-human monoclonal antibody drug. Humira would become one of the world's best-selling drugs, generating billions in annual revenue. But even as Humira succeeded, White was planning something unprecedented—the complete separation of Abbott's pharmaceutical business.

The seeds of the AbbVie spinoff were planted years before its announcement. White recognized that pharmaceutical development and medical products operated on fundamentally different timelines, required different capabilities, and attracted different investors. Pharmaceutical companies lived and died by their drug pipelines, with massive R&D investments and binary outcomes. Medical device and diagnostics companies needed consistent innovation across broader portfolios. Nutrition required consumer marketing skills. Managing all these under one roof was becoming increasingly difficult.

By 2010, Abbott had revenues exceeding $35 billion but faced a critical decision. Humira was nearing peak sales, but its patent would eventually expire. The pharmaceutical pipeline, while promising, required massive investment. Meanwhile, the medical products businesses offered more predictable growth but lower margins. Something had to give.

The period from 1980 to 2010 transformed Abbott from a diversified conglomerate struggling to find focus into a strategically positioned healthcare leader. Under White's leadership, Abbott proved that diversification could work—if managed with discipline, strategic clarity, and willingness to make bold moves. The company entered 2010 generating substantial revenues across four distinct businesses, with strong positions in emerging markets and a clear vision for the future. But the biggest transformation was yet to come.

VI. The AbbVie Spinoff: A Defining Moment (2011–2013)

Miles White stood before a packed auditorium of analysts and journalists on October 19, 2011, about to announce the most radical restructuring in Abbott's 123-year history. "Today," he began, "we're not talking about breaking up Abbott. We're talking about creating two great companies from one." The room erupted with questions. Why split a successful company? Why now? Why give away Humira, one of the world's most profitable drugs?

In October 2011, Abbott announced that it was separating into two independent companies, as its businesses evolved into two different investment identities. The research-focused biopharmaceutical company would be called AbbVie, taking with it all of Abbott's big-name drugs, including Humira, a product worth about $8 billion at the time. Abbott would retain medical devices, diagnostics, nutrition, and branded generic pharmaceuticals.

The strategic logic was compelling but counterintuitive. Humira alone generated nearly 20% of Abbott's revenue and an even higher percentage of profits. Conventional wisdom suggested keeping your most profitable assets. But White saw it differently: Humira's very success was distorting Abbott's valuation and strategic options. Investors valued Abbott as a pharmaceutical company, applying pharmaceutical multiples to medical device revenues. The conglomerate discount was real and growing.

The separation mechanics were elegantly simple. On November 28, 2012, Abbott's board of directors declared a special dividend distribution of all outstanding shares of AbbVie common stock. For every 1 share of Abbott common stock held as of close of business on December 12, 2012, Abbott shareholders received 1 share of AbbVie common stock on January 1, 2013. No shareholder vote required. No tax consequences for investors. Just one company becoming two.

But simplicity in structure masked complexity in execution. Separating a 125-year-old company required untangling decades of shared services, splitting research facilities, dividing international operations, and allocating debt. Over 20,000 employees had to be assigned to one company or the other. Supply chains had to be separated. IT systems had to be replicated or divided. All while maintaining business continuity and regulatory compliance.

The allocation of assets revealed the strategic thinking behind the split. AbbVie took the entire proprietary pharmaceutical business, including not just Humira but also promising pipeline drugs in immunology, oncology, and neuroscience. It also inherited Abbott's pharmaceutical research infrastructure, including major facilities in Illinois and Massachusetts. AbbVie would be a pure-play biopharmaceutical company, focused entirely on discovering and developing new drugs.

Abbott kept everything else—four businesses of roughly equal size: diagnostics, medical devices, nutritionals, and branded generic pharmaceuticals. This portfolio might seem random, but it reflected a coherent strategy. These businesses shared common characteristics: they required continuous innovation rather than blockbuster breakthroughs, they served diverse customer bases from hospitals to consumers, and they offered predictable, sustainable growth.

The financial engineering was sophisticated. Abbott retained approximately $8 billion in debt while AbbVie started with a cleaner balance sheet, reflecting the different capital needs of the businesses. Abbott would generate steady cash flows from established products; AbbVie needed flexibility for R&D investment and potential acquisitions. The market initially valued the combined entities at roughly the same as pre-split Abbott, but this would change dramatically.

Critics questioned the timing. Why split when Humira was still growing? Why not wait until closer to patent expiry? White's answer was strategic: splitting while both companies were strong gave each the best chance for success. AbbVie would have time to develop Humira successors without Abbott's other businesses suffering from pharmaceutical patent cliffs. Abbott could pursue medical device acquisitions without worrying about pharmaceutical pipeline setbacks.

The human dimension was carefully managed. Richard Gonzalez, who had run Abbott's pharmaceutical business, became AbbVie's CEO. He took with him a team deeply familiar with the pharmaceutical assets and strategy. White remained at Abbott's helm, leading the medical products company he had been building toward for years. Employees knew their leadership, maintaining continuity despite the massive change.

AbbVie was formed in 2012 as a corporate spin-off from Abbott Laboratories. It became a public company in January 2013. On its first day of trading, AbbVie's market capitalization exceeded $54 billion. Abbott's stood at $56 billion. Together, they were worth more than $110 billion—nearly 40% more than Abbott's pre-announcement valuation.

The immediate aftermath validated the strategy. AbbVie could now pursue aggressive pharmaceutical R&D and acquisitions without affecting Abbott's medical device strategy. It acquired Pharmacyclics for $21 billion in 2015, adding cancer drug Imbruvica to its portfolio. Meanwhile, Abbott was free to make its own bold moves.

Abbott began its 125th year with approximately $22 billion in revenues generated throughout 150 countries. The company was comprised of four businesses of roughly equal size—diagnostics, medical devices, nutritionals and branded generic pharmaceuticals. This wasn't the Abbott of Wallace Abbott, or even of five years prior. It was a new kind of healthcare company, one built for the realities of 21st-century medicine.

The spinoff's success went beyond financial metrics. It proved that sometimes the best way to create value isn't to combine but to separate. It demonstrated that strategic focus could coexist with business diversity—if that diversity was carefully curated. Most importantly, it showed that even 125-year-old companies could reinvent themselves fundamentally while maintaining their core identity.

Looking back, the AbbVie spinoff represents a masterclass in corporate strategy. It required courage to give up the company's most profitable product, wisdom to recognize that different businesses need different strategies, and execution excellence to separate a complex organization without disruption. The fact that both companies thrived post-separation—with combined market value exceeding $400 billion by 2023—vindicated what seemed like a risky bet. The spinoff didn't break up Abbott; it allowed two great companies to emerge from one good one.

VII. The St. Jude Medical Acquisition: Doubling Down on Devices (2016–2017)

The investment community gathered in New York on April 28, 2016, expecting a routine earnings call. Instead, Miles White dropped a bombshell: Abbott would acquire St. Jude Medical for $25 billion, the largest acquisition in Abbott's 128-year history. The deal would instantly transform Abbott into a cardiovascular device powerhouse, but it came with significant risks—regulatory scrutiny, integration challenges, and cyber-security concerns that had recently plagued St. Jude. The bet was massive: could Abbott successfully integrate a company nearly half its size while maintaining operational excellence?

Abbott announced it had completed the acquisition of St. Jude Medical, Inc., establishing the company as a leader in the medical device arena. The strategic rationale was compelling. St. Jude Medical's strong positions in fast-growing areas such as atrial fibrillation, heart failure, structural heart and chronic pain perfectly complemented Abbott's leading positions in coronary interventions and mitral valve disease. Together, the combined company would compete in nearly every area of the $30 billion cardiovascular market and hold the No. 1 or 2 positions across large and high-growth cardiovascular device markets.

The deal's genesis traced back to the AbbVie spinoff. With pharmaceuticals gone, Abbott needed scale in medical devices to compete with giants like Medtronic and Boston Scientific. Organic growth alone wouldn't suffice. St. Jude offered not just size but strategic fit—minimal product overlap, complementary technologies, and strong positions in high-growth markets Abbott didn't serve.

But the path to closure was anything but smooth. In August 2016, just months after the deal announcement, cybersecurity firm MedSec Holdings released a report claiming St. Jude's cardiac devices were vulnerable to potentially fatal hacking. St. Jude's stock plummeted. Some speculated Abbott would walk away or renegotiate. Instead, Abbott stood firm, expressing confidence in St. Jude's products and cybersecurity protocols. This loyalty during crisis would prove crucial for post-merger integration.

Regulatory scrutiny was intense. The FTC's complaint alleged that without a remedy, the proposed acquisition would harm competition in the U.S. markets for vascular closure devices, which are used to close holes in arteries from the insertion of catheters, and for "steerable" sheaths used in certain procedures. Abbott agreed to divest two small product lines to satisfy regulators—a small price for the broader strategic prize.

The integration philosophy departed from traditional acquisition playbooks. Rather than impose Abbott systems on St. Jude, White mandated a "best of both" approach. Teams from both companies evaluated every process, system, and practice, selecting the superior option regardless of origin. This respectful integration accelerated buy-in from St. Jude employees who feared being absorbed and forgotten.

Geographic complementarity accelerated emerging market expansion. St. Jude was strong in markets where Abbott was weak, and vice versa. Combined, they could offer comprehensive cardiovascular solutions globally. In China, India, and Brazil—markets growing at double-digit rates—the combined portfolio resonated with hospitals seeking single-vendor solutions.

The numbers told the story. "Our devices business had a spectacular year, exceeding many expectations," said Robert Ford, Abbott's executive vice president, Medical Devices. "Just one year since the acquisition of St. Jude Medical, we have doubled the growth rate of that business." Pre-acquisition, St. Jude was growing at 3-4% annually. Within a year under Abbott, the combined medical device business was growing at 7-8%.

Product innovation accelerated post-merger. Abbott leveraged St. Jude's expertise in electrophysiology with its own imaging capabilities to create new integrated solutions. The Confirm Rx insertable cardiac monitor, launched post-acquisition, combined technologies from both companies. The synergies weren't just cost-based—they were innovation-based.

The cultural integration succeeded through deliberate effort. Abbott retained key St. Jude leadership, maintaining institutional knowledge. The St. Jude brand was preserved on many products, respecting its 40-year heritage. Town halls, integration committees, and clear communication prevented the uncertainty that often derails mergers. Employee retention exceeded targets, with less than 5% unwanted attrition in the first year.

Financial discipline matched strategic ambition. Abbott achieved $500 million in cost synergies by year two, ahead of schedule. But cost-cutting didn't compromise growth investment. R&D spending increased post-merger, with Abbott investing in next-generation technologies like bioresorbable stents and leadless pacemakers. The balance between efficiency and innovation was carefully maintained.

The acquisition's timing proved fortuitous. The medical device industry was consolidating, with scale increasingly important for R&D investment and hospital negotiations. By moving decisively, Abbott preempted competitors and achieved critical mass in cardiovascular devices. The combined entity could now compete for large integrated delivery network contracts that neither company could have won alone.

One year post-close, the transformation was evident. Abbott's medical device business generated over $10 billion in annual revenue, making it one of the world's largest. More importantly, it was growing faster than the market, gaining share, and generating returns above the cost of capital. The acquisition that some called too expensive was delivering ahead of expectations.

The St. Jude acquisition demonstrated Abbott's evolution as an acquirer. Unlike the cautious approach of earlier decades, this was bold and decisive. Unlike the scattered diversification of the 1960s, this was strategically focused. The company had learned from both its successes and failures, developing an acquisition capability that could handle complexity at scale.

Looking back, the St. Jude Medical acquisition represents a watershed moment in Abbott's transformation. It proved that the post-AbbVie Abbott could execute large-scale M&A successfully. It established Abbott as a legitimate competitor to medical device giants. Most importantly, it validated the strategy of building leadership positions in attractive markets through disciplined acquisition and excellent integration. The medical device business that seemed secondary to pharmaceuticals just a decade earlier had become Abbott's growth engine.

VIII. Modern Abbott: The Four-Pillar Strategy (2017–Present)

Robert Ford stepped into the CEO role on March 31, 2020, just as the world was shutting down from COVID-19. His first day leading Abbott coincided with one of humanity's greatest health crises. Within weeks, Abbott would launch multiple COVID tests, scale production to unprecedented levels, and cement its reputation as more than a medical device company—it was an essential healthcare infrastructure provider. The pandemic didn't disrupt Abbott's four-pillar strategy; it validated it.

The modern Abbott operates through four equally-sized businesses, each generating roughly $10 billion in annual revenue: Diagnostics, Medical Devices, Nutrition, and Established Pharmaceuticals. This balanced portfolio isn't accidental—it's architected. Each business serves different customers, operates on different innovation cycles, and provides natural hedging against market volatility.

The Diagnostics division became Abbott's unexpected hero during COVID-19. Within months of the pandemic's onset, Abbott launched multiple COVID-19 tests, from high-throughput molecular assays to the credit-card-sized BinaxNOW rapid test that became ubiquitous in American homes. At peak production, Abbott manufactured 100 million tests per month. But COVID testing was just the accelerant for a business already transforming healthcare delivery.

The FreeStyle Libre continuous glucose monitor revolutionized diabetes management. Unlike traditional finger-stick tests, Libre allows patients to scan a sensor on their arm to instantly check glucose levels. By 2024, over 5 million people worldwide used Libre, making it the world's leading continuous glucose monitoring system. The product generates over $5 billion in annual revenue, growing at 20%+ annually—remarkable for a medical device in a mature market.

Abbott's diagnostics strategy extends beyond individual products to integrated health management. The company's informatics platforms connect devices, aggregate data, and provide actionable insights to clinicians. In hospitals, Abbott's Alinity systems don't just run tests—they optimize laboratory workflows, predict maintenance needs, and integrate with electronic health records. This systems approach creates switching costs and customer loyalty that transcend any individual product.

The Medical Devices business, supercharged by the St. Jude acquisition, holds leading positions across cardiovascular care. The MitraClip, a device that repairs leaky heart valves without open-heart surgery, has treated over 150,000 patients globally. The HeartMate 3 left ventricular assist device, essentially an artificial heart pump, offers hope to end-stage heart failure patients. These aren't just products—they're life-saving innovations that command premium pricing and generate recurring revenue through replacements and servicing.

Abbott's approach to medical devices emphasizes minimally invasive solutions. Why? Because they reduce hospital stays, lower total care costs, and improve patient outcomes—aligning with healthcare's shift toward value-based care. The Portico transcatheter aortic valve, which replaces diseased heart valves through a catheter, exemplifies this philosophy. As populations age globally, demand for such solutions grows exponentially.

The Nutrition business might seem pedestrian compared to high-tech medical devices, but it's Abbott's cash cow and growth driver in emerging markets. Similac remains a leading infant formula brand despite 2022's recall crisis. Ensure dominates adult nutrition globally. Glucerna serves the growing diabetic population. These brands generate predictable cash flows that fund innovation across Abbott's portfolio.

In emerging markets, nutrition products serve as Abbott's entry point. Parents who trust Similac for their infants later trust Abbott's diagnostics and devices. This brand halo effect is particularly powerful in markets like India and China, where Abbott's nutrition products have achieved household-name status. The business generates 40% of its revenue from emerging markets, providing exposure to faster-growing economies.

Established Pharmaceuticals—branded generics sold in emerging markets—represents Abbott's bet on global healthcare access. These aren't cutting-edge biologics but proven medicines for cardiovascular disease, pain management, and women's health sold under Abbott branding in markets where brands matter. In India, Abbott is among the top 10 pharmaceutical companies. In Russia and Latin America, it holds leading positions in key therapeutic areas.

The genius of this business is its capital efficiency. No massive R&D spending on novel drugs—just reliable medicines marketed effectively in underserved markets. Margins are healthy, growth is steady, and the business provides natural hedging against developed market volatility.

Geographic diversification amplifies the four-pillar strategy. Abbott generates roughly 40% of revenue from emerging markets, approaching the 50% target set years ago. This isn't just about growth—it's about resilience. When developed markets slowed during COVID, emerging markets compensated. When China locked down, India accelerated. This geographic hedging protected Abbott from regional shocks.

Robert Ford's leadership has emphasized operational excellence alongside strategic vision. Manufacturing productivity improved 5% annually through automation and lean initiatives. Digital transformation accelerated, with artificial intelligence optimizing everything from R&D to supply chain management. The company's 2024 operating margin of 20%+ reflects this operational discipline.

Innovation investment remains robust, with R&D spending at 7% of sales—high for a diversified healthcare company. But it's targeted innovation. Abbott doesn't chase moonshots; it pursues adjacent innovations that leverage existing capabilities. The Libre 3, even smaller and more accurate than its predecessors, exemplifies this incremental innovation philosophy that delivers consistent returns.

The modern Abbott has achieved what seemed impossible: the benefits of diversification without the conglomerate discount. How? Through strategic coherence. All four businesses serve the same mission—helping people live fuller lives through better health. They share technologies, leverage common infrastructure, and cross-sell to overlapping customers. This isn't random diversification; it's carefully orchestrated portfolio management.

Today's Abbott generates over $43 billion in annual revenue, employs 115,000 people globally, and serves patients in more than 160 countries. Its market capitalization exceeds $180 billion, making it one of the world's most valuable healthcare companies. But numbers only tell part of the story. The modern Abbott has proven that diversified healthcare companies can thrive in an era of specialization—if they're diversified strategically, managed operatively, and focused relentlessly on improving health outcomes.

IX. Playbook: Abbott's Business & Strategic Lessons

The art of portfolio management resembles conducting an orchestra more than playing a solo instrument. Each section must excel individually while harmonizing collectively. Abbott's 135-year journey offers a masterclass in this delicate balance—when to add instruments, when to remove them, and how to ensure the music never stops even during transitions.

The Power of Strategic Portfolio Management: When to Diversify, When to Focus

Abbott's portfolio evolution reveals a counterintuitive truth: successful diversification requires periodic focus. The company didn't randomly accumulate businesses; it deliberately built positions in attractive markets, then pruned when those positions no longer fit the strategic symphony. The 1960s consumer products expansion into golf balls and rubber gloves? Abandoned when Abbott recognized healthcare demanded specialized expertise. The hospital products division that generated steady profits? Spun off as Hospira when commoditization eroded strategic value.

The key insight: diversification works when businesses share underlying capabilities, customers, or economic characteristics. Abbott's four pillars seem disparate but share common threads—long product development cycles, heavy regulation, technical complexity, and customers who prioritize quality over price. A company selling both heart valves and infant formula might seem unfocused, but both require uncompromising quality, regulatory expertise, and trusted brands.

Successful M&A Integration: From Ross Labs to St. Jude Medical

Abbott's acquisition track record reveals evolved thinking about integration. Early acquisitions like Ross Laboratories in 1964 were fully absorbed, with the Abbott way imposed wholesale. Later deals showed more nuance. The St. Jude Medical integration's "best of both" philosophy preserved valuable capabilities while achieving synergies. The lesson: integration approach should match strategic intent. If you're buying capabilities, preserve them. If you're buying scale, consolidate aggressively.

Cultural compatibility matters more than strategic fit. Ross Laboratories succeeded because its scientific culture aligned with Abbott's. The TAP joint venture thrived for 30 years because both partners respected boundaries. Conversely, consumer product acquisitions in the 1960s struggled because their marketing-driven cultures clashed with Abbott's research orientation. Due diligence must evaluate cultural fit as rigorously as financial projections.

The Spinoff Decision Framework: Creating Value Through Separation

The AbbVie spinoff demonstrated that sometimes 1+1 equals 3 when the equation becomes 1 and 1. Abbott's framework for separation decisions centers on three questions: Do the businesses have different investment theses? Do they attract different investors? Do synergies justify complexity? When pharmaceuticals required massive R&D bets while medical devices needed consistent innovation, when biotech investors wanted pipeline exposure while device investors sought predictability, and when synergies proved minimal, separation became value-creative.

Timing matters enormously. Abbott split while both businesses were healthy, giving each runway for success. Waiting until crisis would have destroyed value. The lesson: proactive portfolio management beats reactive restructuring. Regular strategic reviews should question every business's fit, even successful ones.

Building in Emerging Markets: The Branded Generics Strategy

Abbott's emerging markets success stems from recognizing these aren't just "poor countries needing cheap products." They're rapidly growing economies where brands matter, quality varies wildly, and trust is paramount. Abbott's branded generics strategy—selling proven medicines under the Abbott name—leverages brand equity while avoiding commodity competition.

Local presence matters more than low cost. Abbott manufactures locally, hires locally, and adapts products for local needs. In India, it offers smaller package sizes for affordability. In China, it emphasizes quality to address safety concerns. In Latin America, it provides patient education programs. This localization requires investment but generates loyalty that transcends price competition.

Managing Through Crisis: From Cyclamate to Baby Formula Recalls

Every Abbott crisis reveals the same pattern: initial shock, transparent communication, systematic remediation, and emergence stronger. The 1970 cyclamate ban could have destroyed Abbott's consumer business. Instead, it prompted strategic refocusing on healthcare. The 2022 infant formula recall and plant shutdown created nationwide shortages and congressional hearings. Abbott's response—accepting responsibility, investing in quality improvements, and diversifying production—restored trust while improving resilience.

Crisis management requires balancing short-term damage control with long-term reputation. Abbott consistently chose long-term reputation, even when costly. Maintaining cyclamate inventory hoping for reversal would have saved money but signaled denial. Fighting the formula recall would have avoided headlines but destroyed trust. Accepting responsibility and fixing problems, while painful, preserved the brand equity that enables premium pricing.

Capital Allocation Across Diverse Businesses

Abbott's capital allocation framework balances growth investment with return generation. High-growth businesses like continuous glucose monitoring receive disproportionate investment despite lower current returns. Mature businesses like adult nutrition generate cash but receive maintenance investment. The portfolio approach allows patient capital—using nutrition's cash flows to fund diagnostics R&D.

The key is avoiding peanut butter spreading—giving every business equal resources regardless of opportunity. Abbott's dynamic allocation adjusts with market conditions. During COVID, diagnostics received surge investment. Post-St. Jude, medical devices got integration resources. This flexibility requires strong corporate oversight and willingness to make tough tradeoffs.

R&D Investment Philosophy in a Conglomerate Structure

Abbott spends 7% of revenue on R&D—less than pure-play pharmaceutical companies but more than most medical device companies. The philosophy: invest enough to lead but not so much that failures cripple the company. This measured approach suits a diversified portfolio where no single product determines success.

R&D focuses on adjacent innovation rather than breakthrough discovery. The Libre sensor builds on existing glucose monitoring technology. The MitraClip adapts surgical techniques to catheter delivery. This incremental innovation generates consistent returns while avoiding pharmaceutical-style binary outcomes. When breakthrough innovation is needed, Abbott acquires it—as with St. Jude Medical—rather than building from scratch.

The Importance of Timing in Major Strategic Moves

Abbott's major moves demonstrate exquisite timing. Going public in 1929 seemed disastrous but provided capital for Depression-era growth. Entering diagnostics in the 1940s preceded the molecular biology revolution. Spinning off AbbVie in 2013 came before pharmaceutical pricing became politically toxic. Acquiring St. Jude in 2017 preceded the medical device consolidation wave.

This timing isn't luck—it's strategic foresight combined with execution capability. Abbott studies long-term trends, positions accordingly, then acts decisively when conditions align. The company missed opportunities too—waiting too long to enter biotechnology, arriving late to digital health. But more often than not, Abbott's timing has been prescient.

The playbook's meta-lesson: there is no permanent playbook. Abbott's strategies evolved with circumstances, capabilities, and competition. What remained constant was disciplined analysis, decisive action, and relentless focus on improving health outcomes. The company that started with standardized pills in 1888 now uses artificial intelligence to predict disease. The tactics changed; the mission endured.

X. Bear vs. Bull Case & Competitive Analysis

Bull Case: The Diversification Premium

Abbott has achieved what modern portfolio theory suggests is impossible: a diversification premium rather than discount. The four-pillar strategy provides multiple growth drivers, reducing dependence on any single product cycle. When pharmaceutical patents expire, devices grow. When developed markets slow, emerging markets accelerate. When elective procedures decline, diagnostics compensate. This isn't random hedging—it's strategic portfolio construction.

The numbers validate the strategy. Abbott has delivered 57 consecutive years of dividend increases, a record few companies match. Revenue grew from $22 billion post-AbbVie spinoff to $43 billion today, nearly doubling in a decade. Return on invested capital consistently exceeds 15%, remarkable for a capital-intensive healthcare company. These aren't biotech lottery tickets—they're predictable, sustainable returns.

Leadership positions across all segments provide competitive moats. Number one in continuous glucose monitoring with FreeStyle Libre. Top two in cardiovascular devices post-St. Jude. Leading infant formula brand with Similac. These aren't marginal players fighting for scraps—they're market leaders with pricing power, customer loyalty, and innovation capabilities that create barriers to entry.

Emerging market exposure approaching 50% of sales positions Abbott for demographic megatrends. As billions enter the middle class in India, China, and Africa, they'll need infant nutrition, diabetes management, and cardiovascular care. Abbott is already there, with brands, distribution, and local manufacturing. Competitors trying to enter these markets face an entrenched incumbent with decades of relationships.

The innovation pipeline remains robust across all businesses. Libre 3 and future generations will extend glucose monitoring leadership. Next-generation heart pumps and valves will drive device growth. Digital health initiatives will modernize diagnostics. This isn't one-hit-wonder innovation but systematic capability across multiple platforms.

Management quality under Robert Ford has been exceptional. Operating margins expanded 200 basis points despite inflation. Free cash flow exceeded $7 billion annually. The company navigated COVID testing surge and decline without operational disruption. This execution excellence suggests Abbott can deliver on ambitious growth targets.

Bear Case: The Complexity Discount

Managing four distinct businesses in 160 countries creates overwhelming complexity. Each business faces different competitors, regulations, and market dynamics. Diagnostics battles Roche and Siemens. Medical devices fights Medtronic and Boston Scientific. Nutrition competes with Nestlé and Danone. Pharmaceuticals faces local generic manufacturers. No management team can master such diversity.

The conglomerate discount is real and persistent. Pure-play competitors command higher multiples because investors can construct their own portfolios. Why own Abbott at 18x earnings when you can buy best-in-class specialists at similar valuations? The supposed diversification benefit is a management myth—investors diversify themselves more efficiently.

Regulatory risks multiply across businesses. FDA medical device regulations. USDA nutrition standards. DEA pharmaceutical controls. European MDR requirements. Chinese NMPA approvals. Any regulatory change in any geography for any business creates headlines and stock volatility. The 2022 formula recall demonstrated how single-plant issues can become national crises.

Competition from specialized players intensifies. Dexcom focuses solely on continuous glucose monitoring with superior technology. Medtronic has triple Abbott's medical device R&D budget. Roche's diagnostics division dwarfs Abbott's. In every segment, Abbott faces competitors with greater focus, resources, and expertise. Being good at everything means being best at nothing.

Integration complexity and execution risk remain high. The St. Jude integration succeeded, but future acquisitions might not. As Abbott grows through M&A, integration challenges multiply. Cultural clashes, system incompatibilities, and customer disruption could destroy value. The bigger Abbott gets, the harder it becomes to integrate acquisitions successfully.

Healthcare pricing pressures globally threaten all segments. Government price controls on devices and diagnostics. Pharmacy benefit manager pressure on pharmaceuticals. Retail competition in nutrition. Every business faces margin compression from powerful buyers demanding lower prices. Diversification doesn't protect against systematic healthcare cost pressures.

Competitive Positioning

Against Johnson & Johnson, Abbott is more focused. J&J's consumer products and pharmaceutical divisions create even greater complexity. Abbott's four healthcare-focused pillars provide more strategic coherence. However, J&J's $100 billion revenue and AAA credit rating provide resources Abbott lacks.

Versus Medtronic, Abbott is more diversified. Medtronic's pure-play medical device focus allows deeper expertise, but Abbott's diagnostics and nutrition businesses provide stability Medtronic lacks. The St. Jude acquisition closed the device portfolio gap, making Abbott competitive in most categories.

Compared to Roche, Abbott has broader reach. Roche's diagnostics/pharmaceutical combination generates higher margins, but Abbott's nutrition and device businesses access different growth vectors. Roche dominates oncology and specialty diagnostics; Abbott leads in point-of-care and consumer-facing products.

Against Nestlé Health Science, Abbott has medical credibility. Nestlé's consumer marketing prowess and global scale dwarf Abbott's nutrition business. But Abbott's medical heritage and clinical evidence provide differentiation in medical nutrition that Nestlé struggles to match.

The competitive reality: Abbott doesn't need to dominate every competitor in every category. It needs to maintain strong positions in attractive markets while leveraging portfolio benefits. The diversification that bears criticize provides resilience that specialists lack. When Medtronic's spine business struggled, the entire company suffered. When Abbott's formula business faced recalls, other divisions compensated.

The verdict: both bull and bear cases have merit. Abbott's diversification provides stability and multiple growth options but creates complexity and prevents specialized focus. The company trades at a discount to pure-plays but generates superior returns through the cycle. Whether this represents opportunity or value trap depends on execution—can management continue navigating complexity while delivering growth? History suggests yes, but past performance, as every investor knows, doesn't guarantee future results.

XI. Epilogue: What's Next for Abbott?

Standing in Abbott's innovation center in Silicon Valley, you glimpse healthcare's future. Engineers train artificial intelligence to predict heart attacks from subtle ECG patterns. Scientists develop biosensors that continuously monitor multiple biomarkers through a single wearable patch. Digital health specialists create algorithms that transform raw diagnostic data into personalized treatment recommendations. This isn't the Abbott of alkaloid pills and test tubes—it's a healthcare technology company that happens to have 135 years of medical expertise.

The convergence of artificial intelligence and diagnostics represents Abbott's most promising frontier. The company's vast diagnostic database—billions of test results across multiple conditions—provides the training data AI requires for pattern recognition. Imagine FreeStyle Libre not just measuring glucose but predicting hypoglycemic events hours in advance. Consider diagnostic panels that identify disease signatures before symptoms appear. This isn't speculative—Abbott's partnerships with technology companies and universities are developing these capabilities today.

Digital therapeutics blur the lines between Abbott's traditional segments. A future Libre system might not just monitor glucose but automatically adjust insulin pump delivery, recommend dietary changes, and alert physicians to concerning patterns. This integrated ecosystem locks in customers while generating recurring revenue streams from subscriptions, supplies, and services. The device becomes a platform, not just a product.

Personalized medicine will reshape Abbott's entire portfolio. Pharmacogenomic testing will determine which branded generics work for specific patients. Diagnostic biomarkers will identify which heart failure patients benefit from specific devices. Nutritional genomics will customize infant formulas and adult supplements. Abbott's diversification suddenly becomes an advantage—it can personalize across the health spectrum. Recent financial performance validates Abbott's strategy. Full-year 2024 sales of $42.0 billion increased 9.6 percent on an organic basis, excluding COVID-19 testing-related sales. Abbott projects full-year 2025 organic sales growth to be in the range of 7.5% to 8.5%. The company projects full-year 2025 adjusted diluted EPS of $5.05 to $5.25, which reflects double-digit growth at the midpoint. These aren't biotech moonshot projections—they're the confident forecasts of a diversified leader executing consistently.

Potential acquisition targets reveal strategic priorities. In diagnostics, point-of-care testing companies offering rapid, accurate results outside traditional labs fit Abbott's decentralization thesis. In medical devices, companies developing minimally invasive solutions for structural heart disease or neuromodulation align with demographic trends. In nutrition, brands serving aging populations or specific medical conditions complement existing portfolios. The pattern is clear: Abbott seeks assets that enhance its ability to serve patients across the care continuum.

Emerging market healthcare transformation offers Abbott's greatest growth opportunity. As countries like India and China build modern healthcare systems, they need comprehensive solutions, not just products. Abbott's ability to provide everything from diagnostic equipment to infant formula to cardiac devices positions it uniquely. While pure-plays must partner or build capabilities, Abbott arrives complete.

The regulatory environment presents both challenges and opportunities. Increasing FDA scrutiny demands higher quality standards—which advantages companies with Abbott's resources and experience. Digital health regulations remain undefined, creating uncertainty but also opportunity for companies that can navigate ambiguity. Global regulatory harmonization, while slow, ultimately benefits multinational companies over local players.

Climate change and sustainability increasingly influence healthcare. Abbott's 2030 sustainability goals—carbon neutrality, sustainable packaging, water stewardship—aren't just corporate responsibility. They're business imperatives as customers, particularly in Europe, demand environmental accountability. The company that began with natural alkaloids returns to nature-inspired solutions, now informed by 135 years of science.

Key lessons for healthcare entrepreneurs emerge from Abbott's journey. First, timing matters more than technology—enter markets when they're emerging, not mature. Second, portfolio diversification works if thoughtfully constructed around common capabilities. Third, crisis creates opportunity for companies with resources and resilience. Fourth, emerging markets reward patience and local presence over quick profits. Finally, healthcare is ultimately about trust—build it consistently over decades, and temporary setbacks won't destroy it.

For investors, Abbott presents a paradox. It's a 135-year-old startup, a diversified specialist, a global company with local presence. The stock won't deliver biotech-style multiples, but it offers something rarer—predictable growth through economic cycles. The four-pillar strategy that confounds pure-play advocates provides resilience that specialists lack. In a world of black swans, Abbott is a company built for surprises.

The Abbott story continues evolving. From Wallace Abbott's dosimetric granules to AI-powered diagnostics, from Chicago pharmacy to global healthcare infrastructure, the journey spans three centuries of medical progress. Yet the mission remains unchanged: helping people live fuller lives through better health. The methods evolved; the purpose endured.

What's next for Abbott? The same thing that's always been next—adaptation. Markets will shift, technologies will disrupt, regulations will change, competitors will emerge. But if history is any guide, Abbott will evolve, survive, and thrive. Not through revolution but through evolution. Not by abandoning its past but by building on it. The company that survived the Great Depression, won World War II, and emerged from COVID stronger isn't betting on any single future. It's preparing for all of them.

In Silicon Valley, they talk about "10x thinking"—solutions ten times better than existing ones. Abbott practices something different: 10-decade thinking—building businesses that endure across generations. In a world obsessed with disruption, Abbott offers something radical: consistency. In an industry chasing moonshots, Abbott delivers base hits. And after 135 years, those base hits have added up to something remarkable—a company that has improved billions of lives while creating hundreds of billions in value.

The final lesson from Abbott's journey isn't about strategy or execution—it's about purpose. Companies that survive centuries don't just make products; they solve human problems. They don't just generate profits; they create value for all stakeholders. They don't just adapt to change; they drive it. Wallace Abbott didn't set out to build a $180 billion company. He set out to make better medicine. Everything else followed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube