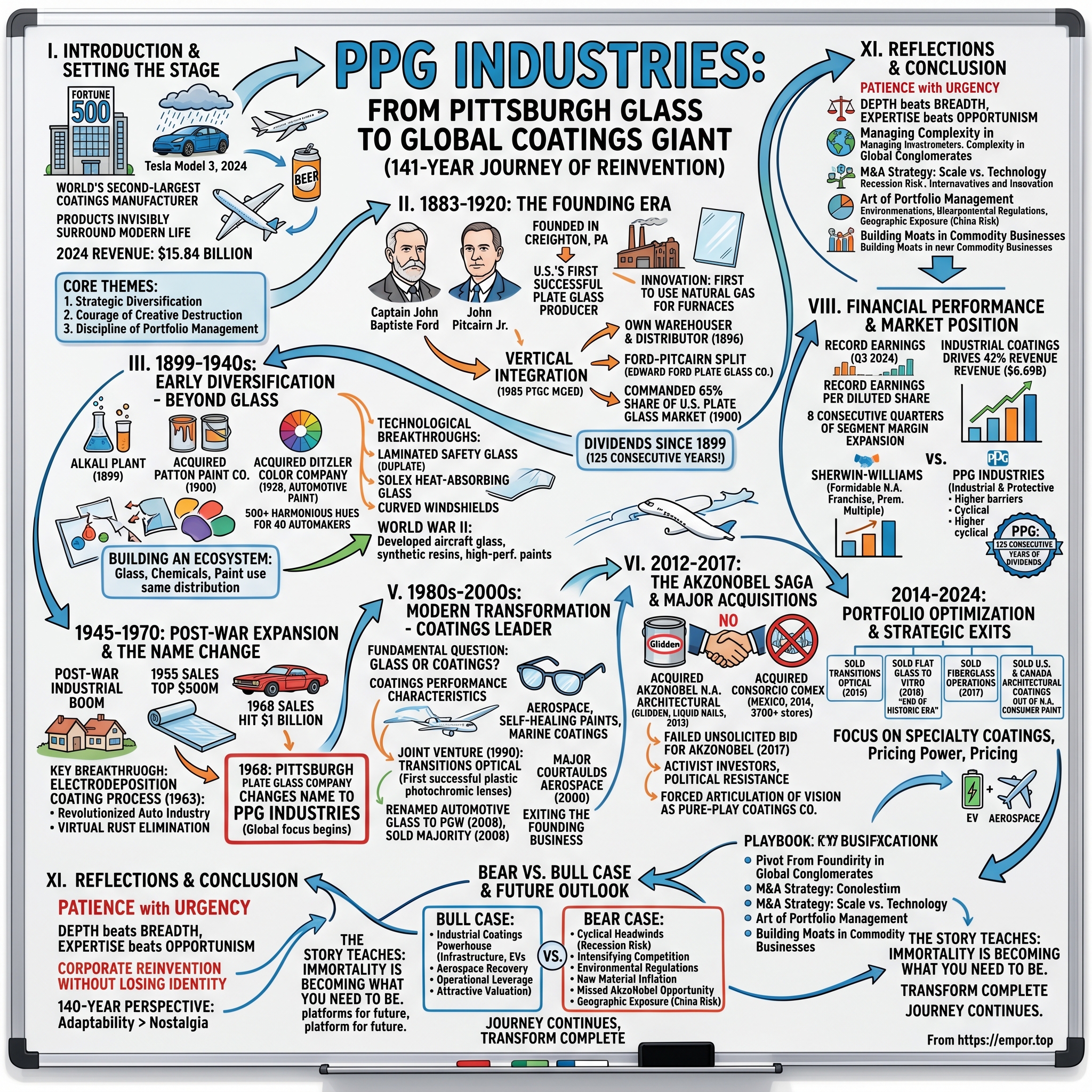

PPG Industries: From Pittsburgh Glass to Global Coatings Giant

I. Introduction & Setting the Stage

The rain pelts against the windshield of a Tesla Model 3 rolling through downtown Pittsburgh on a gray November morning in 2024. That windshield—and the sophisticated coatings protecting the car's aluminum body from corrosion—likely came from PPG Industries, a company whose products touch nearly every aspect of modern life yet remains curiously invisible to most consumers. From the paint on Boeing 787 Dreamliners to the protective coatings inside beer cans, from the color-changing lenses in transition glasses to the anti-fouling paint on container ships, PPG's chemistry surrounds us.

Today, PPG Industries stands as an American Fortune 500 company and the world's second-largest coatings manufacturer, trailing only Sherwin-Williams. With 2024 revenues of $15.84 billion and operations spanning more than 70 countries, PPG has transformed itself from a regional glass manufacturer into a global industrial powerhouse. But this isn't just another corporate success story—it's a 141-year masterclass in strategic reinvention, a company that literally sold off its founding business to become something entirely different.

The transformation is staggering: PPG no longer makes the plate glass that gave it its original name. In fact, the company that once pioneered American glass manufacturing exited the glass business entirely by 2017. Instead, PPG has metamorphosed into a sophisticated chemical company specializing in protective and decorative coatings—a journey that required not just operational excellence but the courage to abandon its very identity. The company's recent financial performance underscores this transformation. In 2024, PPG generated revenue of $15.8 billion (down 2.4% from 2023) but increased net income to $1.34 billion (up 9.9%), pushing profit margins to 8.5% from 7.5% the prior year, with earnings per share rising to $5.75 from $5.18. The Industrial Coatings segment now drives 42% of total revenue at $6.69 billion, highlighting how far the company has traveled from its glass-making origins.

This episode explores three central themes that define PPG's journey. First, the art of strategic diversification—how a company methodically builds new capabilities while maintaining its core business. Second, the courage of creative destruction—knowing when to abandon your founding identity for something better. And third, the discipline of portfolio management—understanding that in industrial conglomerates, what you don't do is as important as what you do.

Consider this: PPG has paid uninterrupted annual dividends since 1899—through two world wars, the Great Depression, multiple recessions, and a complete business model transformation. That's 125 consecutive years of shareholder returns while completely reinventing the company. How many businesses can claim that?

II. The Founding Era: Pittsburgh Plate Glass (1883-1920)

The year is 1883, and America is importing virtually all its high-quality plate glass from Europe. Belgian and French manufacturers control the market with an iron grip, charging premium prices to American builders erecting the skyscrapers and department stores of the Gilded Age. Into this monopoly steps Captain John Baptiste Ford, a Civil War veteran turned industrialist, and John Pitcairn Jr., a Scottish immigrant with deep pockets and deeper ambitions. Together, they would shatter Europe's glass ceiling—literally.

Ford wasn't your typical Victorian entrepreneur. A riverboat captain turned soldier turned businessman, he had already failed once in the glass business when his Keystone Glass Works went bankrupt. But Ford possessed something more valuable than capital: an obsessive belief that America could manufacture its own plate glass. Pitcairn, meanwhile, brought the financial backing and connections that Ford lacked. Their partnership would prove combustible—in both good and bad ways. In 1883, Pitcairn teamed up with Captain John Baptiste Ford and several others to establish the Pittsburgh Plate Glass Company at Creighton, Pennsylvania (about 20 miles north of Pittsburgh along the Allegheny River), and PPG soon became the United States' first commercially successful producer of high-quality, thick flat glass using the plate process. PPG was also the world's first plate glass plant to power its furnaces with locally produced natural gas, an innovation that would prove revolutionary. While other American glass ventures had failed trying to replicate European techniques with coal-fired furnaces, Ford and Pitcairn recognized that western Pennsylvania's abundant natural gas deposits offered a cleaner, more controllable heat source.

The technical challenges were immense. Plate glass manufacturing required maintaining furnace temperatures above 2,700 degrees Fahrenheit for weeks at a time. The molten glass had to be poured onto iron tables, rolled flat, then painstakingly ground and polished on both sides—a process that could take days for a single sheet. European manufacturers had perfected this over centuries; PPG's workers were learning on the fly.

But the real innovation wasn't just technical—it was strategic. Prior to the 1880s more than a dozen plate glass makers had tried unsuccessfully to compete with their European counterparts. Despite U.S. technical ability in the field, plate glass for growing U.S. cities continued to be imported from Belgium, England, France, and Germany. Ford and Pitcairn understood that success required more than just manufacturing capability; it demanded vertical integration, distribution control, and relentless quality improvement. The company moved its headquarters to Pittsburgh in 1895, recognizing that the city was becoming the industrial heart of America. Manufacturing profits on glass were inconsistent partly due to the independents who controlled glass distribution, and in 1896 Pitcairn established a commercial department so PPG became its own warehouser and distributor. This decision would prove fateful. In 1896 Pitcairn established a commercial department and PPG became its own warehouser and distributor. Due to disagreements with Pitcairn regarding distribution, John Ford's sons sold their PPG interests and formed the Edward Ford Plate Glass Company.

The split was more than a business disagreement—it was a philosophical divide about what kind of company PPG should become. Ford believed in pure manufacturing excellence; Pitcairn saw the future in controlling the entire value chain. Ford's departure in 1896 left Pitcairn firmly in control, and his vision would shape PPG for the next century.

By 1900, PPG had become known as the "Glass Trust," controlling ten plants and commanding a 65 percent share of the U.S. plate glass market. The company had also diversified to become the nation's second largest producer of paint. This wasn't the scrappy startup anymore—it was an industrial empire. Pitcairn, who served as president from 1897 to 1905 and chairman from 1894 until his death in 1916, had built PPG over a 33-year period into the largest plate glass manufacturer in the United States while diversifying its product line and developing sources of raw material.

The technological innovations kept coming. PPG perfected techniques that would define American glassmaking for decades: using natural gas instead of coal, developing proprietary grinding and polishing methods, and creating distribution networks that bypassed traditional middlemen. By World War I, PPG glass was in virtually every major building project in America—from the skyscrapers of Manhattan to the storefronts of Main Street.

What's remarkable about this founding era is how it established patterns that would define PPG for the next century: technical innovation, vertical integration, strategic diversification, and a willingness to abandon founding partnerships when visions diverged. Ford and Pitcairn didn't just build a glass company—they created a template for American industrial success that would endure long after both men were gone.

III. Early Diversification: Beyond Glass (1899-1940s)

The year 1899 marked a pivotal moment when PPG made a decision that would seem obvious in hindsight but was radical at the time: why buy raw materials from suppliers when you could make them yourself? In 1899, the business diversified with the construction of an alkali plant in Barberton, Ohio, to supply raw materials for glassmaking – the precursor to PPG's chemicals businesses. This wasn't just about saving money on soda ash—it was about controlling destiny. If you made your own chemicals, you couldn't be held hostage by suppliers. If you understood chemistry deeply, you could innovate in ways competitors couldn't match.

But the real genius move came a year later. A year later, PPG started building its coatings business by acquiring an interest in Wisconsin-based Patton Paint Co. which proved a good fit for the company because paint and glass products typically reach the customers through the same distribution channels. Think about the logic: PPG already had relationships with every major builder and architect in America through its glass business. Why not sell them paint too? Same trucks, same salesmen, same relationships—different product. It was synergy before anyone used that word.

The strategic expansion accelerated through the 1920s, a decade when America was literally reaching for the sky. As steel-cage and concrete-reinforced construction became standard, architects could design structures with larger window units, and glass consumption reached record levels. But PPG's leadership saw something else emerging: the automobile revolution. In 1928, PPG purchased Ditzler Color Company, a Detroit automotive color concern that had been established in 1902. Ditzler wasn't just any paint company—it was the color authority for Detroit's booming auto industry. PPG acquires Ditzler Color Company and begins producing more than 500 "harmonious hues" for 40 automakers. By 1929, PPG was supplying those "harmonious hues" to virtually every major American car manufacturer. In an era when Henry Ford supposedly said customers could have any color they wanted as long as it was black, PPG was betting that Americans would want their cars in technicolor.

The technological breakthroughs of this era were stunning. In 1928, PPG first mass-produced sheet glass using the Pittsburgh Process, which improved quality and sped production by drawing a continuous sheet of molten glass from a tank vertically up a four-story forming and cooling line. That same year, the company developed the Creighton Process, an economical method for laminating glass for automobile windshields, introducing Duplate laminated safety glass.

Then came 1934, when PPG introduces SOLEX heat-absorbing glass and perfected glass-bending techniques for car windshields. These weren't incremental improvements—they were revolutionary advances that would define automotive glass for decades. The curved windshield, which seems so basic today, required PPG to essentially reinvent glassmaking physics.

But the real strategic genius was how these pieces fit together. PPG wasn't randomly diversifying—it was building an ecosystem. The alkali plant made chemicals for glass production. The glass went into buildings and cars. The paint went onto those same cars and buildings. The distribution network sold all of it together. Each business reinforced the others, creating competitive advantages that standalone competitors couldn't match.

World War II accelerated everything. PPG developed laminated aircraft glass and began converting much of its production to military materials, developing synthetic resins that would lead to plastics, high-performance paints, and industrial coatings. The war wasn't just a business opportunity—it was a massive R&D program funded by the government that pushed PPG into entirely new technological frontiers.

By the end of the 1940s, PPG had transformed from a glass company that made some paint into a diversified industrial conglomerate with deep expertise in materials science. The foundation was set for the next phase: becoming a truly global industrial power.

IV. Post-War Expansion & The Name Change (1945-1970)

The morning of August 15, 1945, marked more than just V-J Day for PPG—it signaled the beginning of an unprecedented industrial boom that would transform America and the company along with it. GIs were coming home, suburbs were sprouting like mushrooms after rain, and every family wanted a car, a house with picture windows, and all the modern conveniences. PPG was positioned perfectly: they made the glass for those ranch house windows, the paint for those new Chevrolets, and increasingly, the advanced materials that defined modern life.

The numbers tell the story of explosive growth. In 1955, PPG's sales topped $500 million. PPG employed 33,000 people in seven glass plants, three glass-fabricating plants, two specialty plants, two fiberglass plants, 17 coating and resins plants, and five chemical plants. By 1968, sales would double to reach $1 billion—a psychological milestone that meant you had truly arrived as an American industrial giant. But the real revolution came in automotive coatings. Cars get a new lease on life as PPG revolutionizes the auto industry with the commercialization of the electrodeposition coating process, virtually eliminating rust. As the company that pioneered electrocoat in 1963, PPG continues to set the global standard for e-coat performance, innovation and technical service. This wasn't just an incremental improvement—it fundamentally changed how cars were made. More efficient than other dip applications, e-coat is highly automated and delivers 98 percent transfer efficiency, color consistency and uniform film build on even the most complex metal parts.

Think about what this meant for American consumers. Throughout the 1950s and early 1960s, rust was the cancer of the automobile industry. Cars in the Rust Belt states might last only five or six years before corrosion ate through floor pans and quarter panels. PPG's electrocoat technology changed that equation entirely—suddenly cars could last a decade or more, even in harsh climates. It was a technology that literally saved the American auto industry billions of dollars and gave consumers vehicles that lasted years longer.

The diversification accelerated through the 1960s. In 1963, PPG became the first U.S. company to manufacture float glass, used in place of plate glass by architects. The float process, where molten glass floats on a bed of molten tin, produced glass so smooth it didn't need grinding or polishing—a massive cost savings that would eventually make the plate glass process obsolete.

By 1968, the transformation was complete enough to demand acknowledgment. Reflecting its diversification, Pittsburgh Plate Glass Company changes its name to PPG Industries. As a bonus, the company reaches $1 billion in sales. A result of its diversification, growth and increasingly global presence, the company changed its name to PPG Industries in 1968. The name change wasn't just cosmetic—it was a declaration that PPG was no longer primarily a glass company. PPG's businesses are diverse. A number of foreign production operations and strategic planning moves the company toward a global focus. At the same time, the historic plate process for making flat glass is becoming obsolete with the adoption of the much more efficient float process.

The timing was perfect. America was at the height of its post-war economic dominance, and PPG was supplying the materials that built the American Dream: the glass for suburban office parks, the paint for muscle cars, the coatings that protected industrial infrastructure. The company had successfully navigated the transition from a single-product manufacturer to a diversified materials science company.

What's striking about this era is how PPG managed growth without losing focus. Every expansion—whether into fiberglass, chemicals, or advanced coatings—leveraged existing expertise in materials science and existing customer relationships. They weren't randomly conglomerating like some 1960s companies; they were methodically building an integrated industrial platform.

V. Modern Transformation: Becoming a Coatings Leader (1980s-2000s)

The 1980s dawned with America in recession, Japanese competition threatening traditional industries, and a new philosophy of shareholder capitalism taking hold. For PPG, this meant a fundamental question: were they a glass company that made coatings, or a coatings company that happened to make glass? The answer would reshape the company entirely.

The strategic shift began subtly. Throughout the 1980s and early 1990s, PPG's coatings business was quietly outperforming glass in both growth and margins. Paint and coatings were becoming increasingly sophisticated—no longer just protective layers but engineered materials with specific performance characteristics. PPG was developing coatings that could withstand extreme temperatures for aerospace applications, self-healing paints for automobiles, and specialized marine coatings that prevented barnacle growth on ship hulls.A pivotal moment came in 1990 when PPG founded Transitions Optical as joint venture with Essilor. PPG formed a joint venture with Essilor, with PPG holding 51 percent and Essilor 49 percent, and Transitions Optical introduced the first commercially successful plastic photochromic lenses in 1990. In 1991, Transitions Optical became the first company to commercialize and manufacture plastic photochromic lenses. This wasn't just another product launch—it was PPG applying its deep expertise in photochromic chemistry (developed for aerospace and automotive applications) to an entirely new market. The lenses that automatically darken in sunlight and fade back to clear indoors became one of the most successful specialty materials businesses in PPG's history.

The late 1990s and early 2000s saw PPG making increasingly bold moves in coatings while quietly questioning its commitment to glass. The company was developing cutting-edge products: coatings for beer cans that prevented flavor transfer, aerospace transparencies that could withstand ballistic impacts, and marine paints using nanotechnology to prevent fouling. Each innovation moved PPG further from its commodity glass roots toward high-margin specialty materials. In October 2000, PPG Industries announced it had agreed to buy Courtaulds Aerospace for $512.5 million. Based in Glendale, California, the aerospace business has annual sales of approximately $240 million, employs 1,200 people. The acquisition transformed PPG into a major supplier of coatings and sealants to the aircraft industry, adding high-margin aerospace products to its portfolio. This was strategic acquisitions at its best—buying technology and market position that would take decades to build organically. The signal of transformation came in 2008. In 2008, PPG renamed their automotive glass division PGW (Pittsburgh Glass Works) and sold a majority of it to Kohlberg & Company. PPG retained 40% ownership of PGW until March 2016 when they sold their stake to automotive parts salvage company LKQ Corporation. This wasn't just selling a division—it was PPG beginning to exit the very business that gave it its name. The automotive glass business had been central to PPG's identity for over a century, but management recognized that coatings offered better growth and margins.

By the end of the 2000s, PPG had fundamentally transformed. It was still called Pittsburgh Plate Glass Industries, but glass was increasingly a smaller part of the portfolio. The future was in engineered materials, sophisticated coatings, and specialty chemicals. The company that had broken Europe's glass monopoly was now competing in entirely different arenas.

VI. The AkzoNobel Saga & Major Acquisitions (2012-2017)

The boardroom at PPG headquarters in Pittsburgh hummed with tension in early 2017. CEO Michael McGarry and his team were about to launch the most audacious move in the company's 134-year history: an unsolicited takeover bid for Dutch rival AkzoNobel, maker of Dulux paints and one of Europe's most prestigious chemical companies. It would be a $25 billion bet that would either create a global coatings colossus or end in humiliating failure.

But first, let's rewind to understand how PPG got here. The transformation accelerated with bold acquisitions in the mid-2010s. In April 2013, PPG completed the acquisition of AkzoNobel North American architectural coatings business including Glidden, Liquid Nails, and Flood brands for $1.05 billion. This was the second-largest acquisition in company history at that time, instantly making PPG a major player in the North American architectural coatings market. The Glidden brand alone—with its iconic logo and retail presence—gave PPG credibility with consumers who had never heard of the parent company. Then came the Mexico play. In November 2014, PPG finalized the acquisition of Consorcio Comex, S.A. de C.V. ("Comex"), an architectural coatings company with headquarters in Mexico City, in a transaction valued at $2.3 billion. This wasn't just buying market share—it was buying an entire distribution system. Comex operated through more than 3,700 stores independently owned and operated by more than 700 concessionaires across Mexico and Central America. PPG was essentially acquiring a paint franchise system that would take decades to build from scratch.

These acquisitions set the stage for the big swing. By 2017, PPG had proven it could successfully integrate large acquisitions and had the balance sheet to support an even bigger deal. The company's leadership looked across the Atlantic at AkzoNobel—a company struggling with its own strategic direction and under pressure from activist investors.

In March 2017, the company launched an unsolicited takeover bid of €20.9 billion, which was promptly rejected by AkzoNobel's management. Days later, the company launched an increased bid of €24.5 billion, which was again rejected by AkzoNobel's management. The drama that unfolded was worthy of a business thriller. A number of shareholders urged AkzoNobel to explore the offer and subsequent negotiations. In April, activist investor Elliott Investors called for the removal of the Chairman of Akzo, Antony Burgmans, following Akzo's refusal to enter talks with PPG.

The battle lines were drawn: PPG and activist shareholders on one side, AkzoNobel's management and Dutch politicians (who feared job losses) on the other. The Dutch company argued PPG's offer undervalued the business and raised antitrust concerns. Behind closed doors, it was also about culture—a brash American company trying to acquire a European institution dating back to 1646.

Ultimately, PPG's takeover attempt failed. AkzoNobel's board successfully resisted, promising shareholders better returns through its own restructuring plan. For PPG, it was a rare public defeat, but also a statement of intent. The company that once made plate glass was now confident enough to attempt one of the largest chemical industry takeovers in history.

The failed AkzoNobel bid wasn't entirely a loss. It forced PPG to articulate its vision as a pure-play coatings company and demonstrated to investors the company's ambition and financial firepower. It also accelerated PPG's strategic review of its own portfolio—if they couldn't buy growth, they would have to create it by divesting non-core assets and doubling down on high-margin businesses.

VII. Portfolio Optimization & Strategic Exits (2014-2024)

Michael McGarry stood before investors at PPG's 2017 analyst day with a clear message: "We're going to be a coatings company, period." After the failed AkzoNobel bid, PPG embarked on one of the most dramatic portfolio transformations in its history—systematically selling off businesses that had defined the company for over a century.

The transformation had actually begun years earlier with a crucial decision. On April 1, 2014, PPG finalized the sale of Transitions Optical to its joint venture partner, Essilor International of France. The sale of the 51% stake brought PPG approximately $1.7 billion, marking the end of a highly successful 24-year partnership. PPG's technical center in Monroeville will continue to provide research and development services for Transitions, but the company was out of the photochromic lens business. It was profitable, growing, and technologically advanced—exactly the kind of business most companies would keep. But it wasn't coatings. The big moment came in July 2016. In July 2016, PPG announced its sale of the flat glass business to Vitro, a glass manufacturer based in Mexico, for $750 million. "This transaction represents the end of an historic era for PPG as a manufacturer of flat glass, and it is another major step in our portfolio transformation to focus on paints, coatings and specialty materials," McGarry said in the announcement. The business that gave Pittsburgh Plate Glass its name—the business that Captain Ford and John Pitcairn had built from nothing—was gone.

The symbolism was profound. PPG was literally selling its birthright. But the numbers made sense: the flat glass business generated about $1 billion in sales but with much lower margins than coatings. In the brutally competitive construction glass market, PPG was a subscale player competing against global giants. Better to take the $750 million and invest it in higher-return coatings businesses.

The divestiture train kept rolling. In September 2017, PPG announced the sale of its remaining fiberglass operations to Nippon Electric Glass for $541 million. This was following PPG's 2016 sale of its European fiberglass operations to NEG, and divesting its ownership in two other Asian fiberglass joint ventures. Another business that PPG had pioneered and grown for decades—gone.

But PPG wasn't just selling—it was also buying strategically. In May 2021, PPG completed the acquisition of Wörwag, a leading global manufacturer of coatings for industrial and automotive applications headquartered in Germany. The acquisition strengthened PPG's position in Europe and added sophisticated coating technologies for electric vehicles—a critical growth market.

The most recent chapter in this transformation came in late 2024. In October 2024, PPG announced it had entered into a definitive agreement to sell its architectural coatings business in the U.S. and Canada to American Industrial Partners for $550 million. The business, which includes brands acquired in the 2013 AkzoNobel deal, generated approximately $2 billion in net sales in 2023. By December 2024, the deal was complete—PPG was officially out of the North American consumer paint business.

The strategic logic was clear: architectural coatings in mature markets like the U.S. faced intense competition from Sherwin-Williams and Home Depot's private labels. Margins were under pressure, and growth was limited. Meanwhile, PPG's industrial coatings—for aerospace, automotive, and protective applications—offered better margins, stronger competitive positions, and clearer paths to growth.

This decade of portfolio optimization transformed PPG from a diversified industrial conglomerate into a focused coatings specialist. The company that once made everything from glass to fiberglass to photochromic lenses now had a laser focus on protective and functional coatings. It was creative destruction on a corporate scale—and Wall Street was taking notice.

VIII. Financial Performance & Market Position

The numbers tell a story of focused execution despite market headwinds. PPG's 2024 revenue of $15.8 billion was down 2.4% from 2023, but net income rose to $1.34 billion (up 9.9%), pushing profit margins to 8.5% from 7.5% the prior year, with earnings per share rising to $5.75 from $5.18. The Industrial Coatings segment drove 42% of total revenue at $6.69 billion, underscoring how thoroughly PPG has transformed from its glass-making origins.

The margin expansion story is particularly compelling. PPG reported record earnings per diluted share of $2.00 (reported) and $2.13 (adjusted) in Q3 2024, with segment margins improving 60 basis points year over year, marking eight consecutive quarters of margin expansion. This isn't just operational excellence—it's the payoff from years of portfolio optimization, exiting lower-margin businesses and focusing on specialty coatings with pricing power.

Against Sherwin-Williams, the comparison is illuminating. As of August 2025, Sherwin-Williams commanded an $88.2 billion market capitalization with a price-earnings ratio of 35.2 and trailing 12-month revenue of $23.1 billion with an 11.0% net profit margin. PPG's price-earnings ratio stood at 19.4, with trailing 12-month revenue of $15.6 billion and a 6.5% net profit margin, while maintaining a 2.6% dividend yield.

The valuation gap reflects different strategic positions. Sherwin-Williams has maintained its focus on architectural coatings and retail distribution, building a formidable North American franchise through its 4,000-plus company-operated stores. PPG, by contrast, has bet on industrial and protective coatings—markets with higher barriers to entry but also more cyclical exposure. The market clearly prefers Sherwin's stability and retail presence, awarding it a premium multiple.

But PPG's dividend history stands out. PPG has paid uninterrupted annual dividends since 1899—a 125-year streak that survived world wars, depressions, and complete business model transformations. That's not just financial discipline; it's a covenant with shareholders that transcends any single strategy or market cycle.

The geographic and end-market diversification also differentiates PPG. While Sherwin-Williams generates the majority of its revenue from North America, PPG operates across 70 countries with meaningful exposure to emerging markets. In aerospace coatings, PPG holds dominant positions with Boeing and Airbus. In automotive, they're deeply embedded with global OEMs transitioning to electric vehicles. These aren't markets you enter casually—they require decades of technical expertise and customer relationships.

IX. Playbook: Key Business Lessons

After 141 years, PPG's journey offers a masterclass in corporate evolution. These aren't just business school case studies—they're battle-tested strategies that transformed a regional glass maker into a global industrial leader.

The Power of Patient Diversification

PPG didn't wake up one day and decide to become a coatings company. The transformation took decades, starting with that 1899 alkali plant in Barberton. Each expansion built on existing capabilities: glass manufacturing required chemicals, so they made chemicals. Chemicals led to paints. Paints led to coatings. Coatings led to specialty materials. It's the compound interest of capabilities—each new skill making the next expansion easier.

Compare this to the conglomerate crazes of the 1960s and 1980s, where companies bought random businesses for financial engineering. PPG's diversification was always strategic, always leveraging existing knowledge. When they bought Ditzler in 1928, they already knew automotive customers from selling them glass. When they entered aerospace coatings, they had decades of experience with high-performance materials. Patient, logical, interconnected growth.

When to Pivot from Your Founding Business

The hardest decision any company faces: abandoning what made you successful. PPG's exit from glass wasn't impulsive—it was a decades-long recognition that coatings offered better economics. The writing was on the wall by the 1990s: glass was becoming commoditized, with Chinese manufacturers adding massive capacity. Coatings, meanwhile, offered differentiation through chemistry, customer intimacy through technical service, and margins through specialization.

The lesson? Don't wait for crisis to force change. PPG sold its glass businesses from positions of relative strength, getting reasonable valuations rather than fire-sale prices. They also maintained strategic patience—keeping 40% of the auto glass business for eight years after the initial sale, extracting value while completing their transformation.

Managing Complexity in Global Conglomerates

Running a company with operations in 70 countries, dozens of product lines, and thousands of SKUs is organizational nightmare fuel. PPG's solution: radical decentralization with common platforms. Each business unit operates with significant autonomy, but they share technology platforms, raw material purchasing, and distribution networks where it makes sense.

This isn't the GE model of financial controls and forced rankings. It's more subtle—creating innovation networks where the aerospace team's anti-icing coating technology helps the automotive team develop better windshield treatments. Or where learnings from marine anti-fouling paints inform industrial maintenance coatings. It's complexity with connection, diversity with synergy.

M&A Strategy: Scale vs. Technology

PPG's acquisition history reveals two distinct strategies. Sometimes they bought for scale—like the $2.3 billion Comex acquisition that instantly made them a player in Mexico. Other times they bought for technology—like the $512 million Courtaulds Aerospace deal that brought sophisticated sealants and transparencies.

The key insight: know which type of deal you're doing and price accordingly. Scale deals should be immediately accretive, with clear cost synergies. Technology deals might dilute near-term earnings but open new markets or capabilities. PPG's failed AkzoNobel bid was ultimately a scale play at a technology price—which is why walking away was the right decision.

The Art of Portfolio Management

In industrial conglomerates, what you don't do is as important as what you do. PPG's 2014-2024 divestiture program wasn't just financial engineering—it was strategic focus. Every business they sold—Transitions Optical, flat glass, fiberglass, North American architectural—was profitable. But none were core to the future vision of a specialty coatings leader.

This requires extraordinary discipline. Transitions Optical was growing, technologically advanced, and generated excellent returns. But it wasn't coatings. The flat glass business literally gave PPG its name. But it wasn't the future. The courage to sell good businesses to focus on great ones separates exceptional companies from merely good ones.

Building Moats in Commodity Businesses

Coatings might seem like a commodity—it's just paint, right? PPG's genius has been creating differentiation in seemingly undifferentiated markets. In aerospace, their coatings must withstand temperature extremes from -65°F to 120°F while maintaining perfect adhesion at 500 mph. That's not paint—it's materials science.

The moats come from three sources: technical specifications that take years to qualify, switching costs from integrated supply chains, and customer relationships built over decades. When Boeing specs PPG coatings for the 787, they're not just buying paint—they're buying 50 years of flight data, technical support, and warranty backing. Try competing with that as a new entrant.

X. Bear vs. Bull Case & Future Outlook

Bull Case: The Industrial Coatings Powerhouse

The optimist sees PPG as perfectly positioned for the next decade's megatrends. Start with infrastructure: America's Infrastructure Investment and Jobs Act allocates $1.2 trillion for roads, bridges, and public works—all requiring protective coatings. PPG's industrial coatings protect everything from bridge spans to water towers, markets where their technical expertise commands premium pricing.

The automotive transformation to EVs presents massive opportunity. Electric vehicles require specialized coatings for battery thermal management, electromagnetic interference shielding, and weight reduction through advanced composites. PPG's decade-long investment in EV coatings technologies positions them as a critical supplier to this transition. Their Wörwag acquisition specifically targeted these capabilities.

Aerospace recovery provides another tailwind. After COVID decimated air travel, Boeing and Airbus face multi-year backlogs. Every new aircraft needs 300-600 gallons of specialized coatings. PPG's dominant position in aerospace coatings—they're on virtually every Western commercial aircraft—means predictable, high-margin growth as production ramps.

The focused portfolio post-divestitures creates operational leverage. Without the drag of commodity glass operations or competitive architectural coatings, management can concentrate resources on highest-return opportunities. The company's nine consecutive quarters of margin expansion demonstrates this focus bearing fruit.

Finally, valuation looks compelling relative to Sherwin-Williams. Trading at 19x earnings versus Sherwin's 35x, PPG offers similar exposure to coatings growth at a significant discount. If PPG can close even half the margin gap to Sherwin-Williams, the stock could see substantial multiple expansion.

Bear Case: Cyclical Headwinds and Structural Challenges

The pessimist sees storm clouds gathering. Industrial coatings are inherently cyclical—when manufacturing slows, coating demand craters. With recession risks elevated and industrial production already softening, PPG faces potential volume and margin pressure. Unlike consumer paints that benefit from steady repaint cycles, industrial coatings are discretionary and deferrable.

Competition intensifies across every segment. Sherwin-Williams isn't standing still, aggressively expanding in industrial coatings through acquisition. Asian competitors, particularly Chinese coating manufacturers, are moving upmarket with "good enough" products at significant discounts. PPG's premium pricing depends on technical differentiation that's slowly eroding.

Environmental regulations pose existential challenges. The push toward zero-VOC coatings, elimination of hazardous materials, and carbon neutrality requires massive R&D investment with uncertain returns. European REACH regulations and potential PFAS bans could obsolete entire product lines. The regulatory treadmill never stops, and compliance costs only increase.

Raw material inflation remains problematic. Titanium dioxide, the key white pigment, faces structural supply constraints. Petrochemical-based resins link PPG's costs to volatile oil prices. While PPG has pricing power, there are limits to what industrial customers will accept, especially in competitive bidding situations.

The missed AkzoNobel opportunity looms large. PPG needed that deal for European scale and technology access. Without it, they remain subscale in key European markets while facing a reinvigorated AkzoNobel as a competitor. The consolidation window may have closed, leaving PPG strategically disadvantaged.

Geographic exposure brings additional risks. China represents both PPG's biggest growth opportunity and largest threat. Chinese nationalism increasingly favors domestic suppliers. Technology transfer requirements risk creating future competitors. The geopolitical tensions make long-term planning nearly impossible.

XI. Reflections & Lessons for Founders

The story of PPG Industries isn't just corporate history—it's a meditation on time, change, and the courage to destroy what you've built to build something better. For 141 years, this company has reinvented itself repeatedly while maintaining an unbroken commitment to shareholders. What can founders learn from this epic journey?

Strategic Patience vs. Strategic Urgency

PPG teaches us that transformation isn't an event—it's a process measured in decades. The shift from glass to coatings took 50 years. But within that patience lived moments of decisive action: selling Transitions at peak value, walking away from AkzoNobel when the price was wrong, exiting glass entirely despite the emotional attachment.

The lesson for founders: Have a long-term vision but recognize inflection points. PPG's leadership understood that industrial evolution happens slowly, then suddenly. They prepared for decades, then acted decisively when the moment arrived. It's not patience or urgency—it's patience with urgency embedded within it.

Building Lasting Industrial Enterprises

In an era obsessed with software and asset-light business models, PPG reminds us that making physical things still matters. Their coatings protect civilization's infrastructure, enable transportation, and preserve industrial assets. This isn't as sexy as social media or AI, but it's foundational to modern life.

The durability comes from depth. PPG doesn't just make coatings—they understand the chemistry, application technology, customer processes, and failure modes. This systems-level knowledge takes generations to build and is nearly impossible to replicate. For founders, the lesson is clear: depth beats breadth, expertise beats opportunism.

Corporate Reinvention Without Losing Identity

PPG changed everything except what mattered most: the commitment to materials science, operational excellence, and shareholder returns. They're no longer Pittsburgh Plate Glass, but they're still quintessentially PPG—methodical, technical, reliable. The company that pioneered American glass manufacturing now pioneers advanced coatings, but the innovative spirit remains.

This is the paradox of corporate transformation: change everything while changing nothing. PPG shows it's possible to completely pivot your business model while maintaining cultural continuity. The employees who once perfected glass chemistry now perfect coating chemistry. The customer relationships evolved from construction to aerospace, but the trust remained.

The 140-Year Perspective

Perhaps PPG's greatest lesson is about time horizons. When you're building for centuries, not quarters, different strategies emerge. You diversify gradually, not frantically. You maintain dividends through world wars because reputation compounds over generations. You sell founding businesses because adaptation beats nostalgia.

Most startups think in runway months and exit years. PPG thinks in decades and centuries. This isn't just about patient capital—it's about building institutions that outlast their founders, their industries, even their original purposes. In 1883, John Baptiste Ford and John Pitcairn couldn't have imagined aerospace coatings or electric vehicle batteries. But they built something flexible enough to evolve into those markets.

For today's founders, obsessed with disruption and revolution, PPG offers a counternarrative: evolution beats revolution, compound improvements beat quantum leaps, and the companies that last aren't always the ones that move fastest—they're the ones that adapt most intelligently.

XII. Conclusion: The Transformation Complete, The Journey Continues

PPG Industries stands at a fascinating inflection point in 2024. The company that began making plate glass in 1883 has completely exited the glass business. The transformation from Pittsburgh Plate Glass to a pure-play coatings company is complete. Yet in many ways, the journey is just beginning.

The next chapter will test whether PPG's focused strategy can deliver the premium multiples that pure-play positioning promises. Can they close the margin gap with Sherwin-Williams? Will their industrial focus prove prescient as infrastructure spending accelerates? Can they navigate the Chinese market's opportunities and threats? These questions will define PPG's next decade.

What's certain is that PPG has proven something remarkable: a company can completely reinvent itself while maintaining its essential character. They've shown that patient transformation beats dramatic disruption, that selling your founding business can be the ultimate act of corporate courage, and that 141 years of evolution can position you perfectly for the future.

For investors, PPG represents a fascinating dichotomy. It's simultaneously a 141-year-old industrial incumbent and a newly focused specialty chemicals growth story. It offers the dividend reliability of a Dividend Aristocrat with the transformation potential of a restructuring play. Whether that combination justifies investment depends on your view of industrial coating markets, your patience for operational improvement, and your belief in management's ability to execute their focused strategy.

For business historians, PPG demonstrates that American industrial excellence isn't dead—it just looks different than it did a century ago. The same innovative spirit that broke Europe's glass monopoly now develops coatings that protect spacecraft and enable electric vehicles. The company that once employed thousands in massive plate glass factories now employs scientists developing molecular-level material solutions.

The PPG story ultimately teaches us that corporate immortality isn't about preserving what you were—it's about becoming what you need to be. From glass to coatings, from regional to global, from commodity to specialty, PPG has consistently chosen transformation over stagnation. After 141 years, they're still painting the future—just not with the materials their founders would recognize.

And perhaps that's the ultimate lesson: the most successful companies aren't monuments to their past but platforms for their future. PPG Industries has proven that even the oldest industrial companies can reinvent themselves for new centuries. The only question now is what they'll become next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube