Cheniere Energy: From Import Dreams to Export Empire

I. Introduction & Episode Roadmap

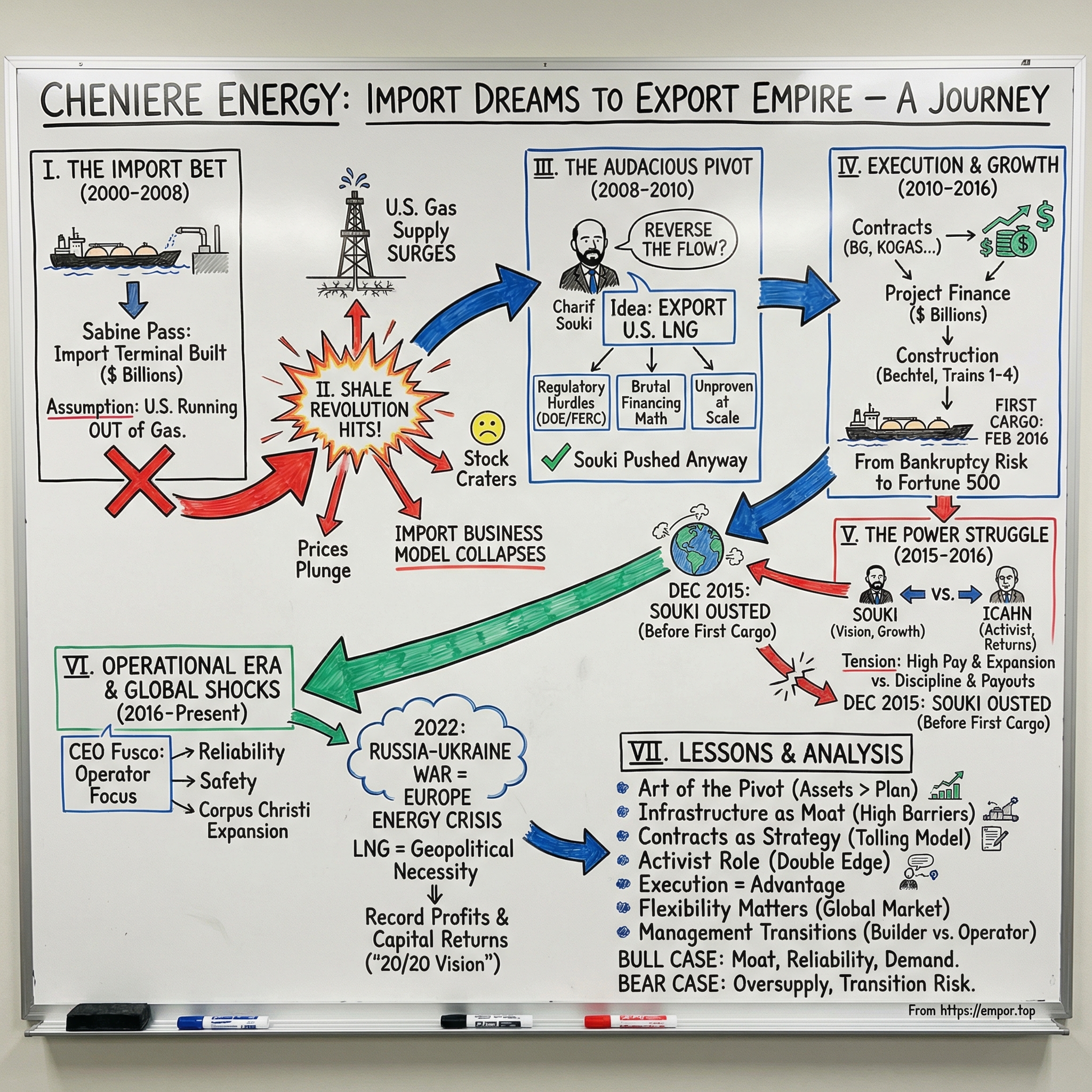

Picture this: December 2015. Natural gas prices have cratered to $2 per MMBtu. Oil has plummeted from $100 to $35 in eighteen months. Energy companies are filing for bankruptcy left and right. In a Houston boardroom, Charif Souki—the Lebanese-American entrepreneur who built Cheniere Energy from nothing—is being fired by his own board after nineteen years at the helm. The company he transformed from a failed burger chain into America's first LNG exporter is just two months away from shipping its maiden cargo. Carl Icahn, the legendary corporate raider, has orchestrated the coup. Souki walks out with his $40 million severance, but he's lost control of what would become the most valuable LNG infrastructure in the Western Hemisphere.

Fast forward to today: Cheniere Energy stands as the largest exporter of liquefied natural gas in the United States and the second-largest LNG producer globally. The company that nearly went bankrupt betting on gas imports now commands a $50 billion market capitalization, ships over 45 million tonnes of LNG annually, and has become the cornerstone of America's energy independence strategy. When European leaders scrambled to replace Russian gas after the Ukraine invasion, they came knocking at Cheniere's door.

This is the story of how a struggling wildcatter rode three massive waves—the shale revolution, the global energy transition, and geopolitical realignment—to build one of the most strategically important energy companies of the 21st century. It's a tale of visionary pivots, boardroom battles, and the kind of timing that separates the lucky from the legendary.

The central puzzle we're solving: How did a company that spent its first decade drilling dry holes and its second decade building infrastructure for the wrong bet become America's energy export champion? The answer involves equal parts contrarian thinking, financial engineering, and being perfectly positioned when the world's energy map got redrawn—twice.

We'll trace Cheniere's journey through five distinct acts: the quixotic early years under Souki's restaurant-to-energy pivot, the import terminal era that nearly killed the company, the shale-driven reversal that saved it, the Icahn takeover that professionalized it, and the current era where geopolitical chaos has made it indispensable. Along the way, we'll extract the playbook for building infrastructure moats, timing commodity cycles, and navigating activist investors.

Key themes to watch: the art of the billion-dollar pivot, why terminals are the ultimate tollbooths, how long-term contracts create value in volatile markets, and whether creative destruction or value destruction won the Souki-Icahn battle. Buckle up—this is Acquired-style business history where fortunes are made, lost, and made again.

II. Origins & The Souki Vision (1996–2005)

The Unlikely Energy Executive

Charif Souki never intended to become an energy mogul. Born in Beirut and raised in Egypt, he came to America for an MBA at Columbia, worked briefly as an investment banker at Loeb Partners, then did what any sensible financier would do in the 1980s—he opened trendy restaurants. His Mezzaluna establishments in Aspen and Los Angeles became celebrity haunts. Ron Goldman, one of O.J. Simpson's victims, worked as a waiter at the Brentwood location. This was Souki's world: glamour, connections, and cash flow from cappuccinos.

But by the mid-1990s, the restaurant business had lost its appeal. Souki was restless, approaching fifty, and watching the energy boom unfold in Houston. Here's where the story gets wonderfully bizarre: he took a publicly traded shell company called All American Burger Inc.—which had somehow morphed into a Hollywood film-colorization venture—and transformed it into Cheniere Energy in 1996. The name came from Cheniere au Tigre, a Louisiana barrier island that disappeared in a hurricane. Prophetic? Perhaps. But Souki saw opportunity where others saw swampland.

The initial business plan was straightforward: become a wildcatter, drill for oil and gas along the Louisiana Gulf Coast. Souki had zero petroleum engineering experience, but he had something arguably more valuable—blue-chip connections from his investment banking days. He could raise money. Between 1996 and 2000, he assembled backing from sophisticated investors who believed in the story, if not necessarily the geology.

Drilling for Disappointment

The late 1990s were brutal for Cheniere. While dot-com millionaires were being minted daily in Silicon Valley, Souki's team was burning through cash drilling one dry hole after another along the Gulf Coast. The company's exploration efforts were, to put it charitably, unsuccessful. By 2000, Cheniere had accumulated losses exceeding $50 million with virtually nothing to show for it. The stock price languished below $1. Most CEOs would have folded.

But Souki possessed a quality that would define Cheniere's trajectory: the ability to completely reimagine the business while keeping investors on board. He noticed something interesting happening in the energy markets. Natural gas prices in the U.S. were rising. Domestic production was declining. Meanwhile, massive gas discoveries in Qatar, Trinidad, and other distant locations were creating a global LNG surplus. The conventional wisdom was clear: America would need to import natural gas, and lots of it.

The Import Epiphany

In 2002, Souki made the pivot that would define the next decade. Cheniere would stop looking for gas and start building infrastructure to import it. Specifically, the company would develop LNG receiving terminals—massive facilities that could accept shipments of super-cooled liquid gas from overseas, warm it back to gaseous form, and inject it into American pipelines.

The logic was compelling. Alan Greenspan himself testified before Congress in 2003 about America's looming natural gas shortage. Major oil companies were drawing up plans for dozens of import terminals. The futures market showed gas prices rising indefinitely. Souki's stroke of genius wasn't seeing this trend—everyone saw it—but moving faster and more aggressively than established players.

Cheniere's first project would be Sabine Pass, a terminal on the Louisiana-Texas border with perfect geography: deep-water access for tankers, proximity to major pipelines, and enough land for massive storage tanks. In March 2005, after three years of permitting battles and financing struggles, Cheniere began construction. The company had pivoted from failed explorer to infrastructure developer.

The Capital Markets Seduction

Here's where Souki's background in investment banking and restaurants—both businesses built on selling dreams—became invaluable. Between 2003 and 2005, he raised over $1 billion for a company that had never made a profit. He pre-sold terminal capacity to Total, Chevron, and other majors through innovative long-term contracts. He structured complex financial instruments that gave investors upside while limiting downside.

The pitch was irresistible: America needs gas, the world has gas, Cheniere owns the bridge between them. By late 2005, Cheniere's stock had risen from under $1 to over $30. Souki was being profiled in energy magazines as a visionary. The former restaurateur had seemingly cracked the code on America's energy future.

What nobody knew—what nobody could have predicted—was that America was about to discover it was sitting on the largest natural gas reserves in the world. The import terminals Cheniere was frantically building would soon become the most expensive stranded assets in energy history. Or so it seemed.

III. The Import Terminal Era & Near Death (2005–2010)

Building Cathedrals in the Desert

By 2006, Sabine Pass was rising from the Louisiana wetlands like an industrial cathedral—five massive storage tanks, each fourteen stories tall and capable of holding three billion cubic feet of natural gas in liquid form. The engineering was staggering: pipes that could withstand temperatures of minus 260 degrees Fahrenheit, specialized pumps that could regasify LNG at 1.5 billion cubic feet per day, marine facilities that could handle the largest Q-Max tankers in the world.

The global LNG market context made Cheniere's bet seem brilliant. Qatar was ramping up production from its North Field, the world's largest gas reserve. Trinidad was expanding. Australia was planning massive LNG projects. Global LNG trade was projected to triple by 2020. Every consultant's deck showed the same hockey stick: America would become the world's largest LNG importer, and whoever owned the terminals would print money.

Souki was already planning the empire. Beyond Sabine Pass, Cheniere was developing Corpus Christi in Texas, Creole Trail in Louisiana, and even eyeing sites in Florida and California. The company had signed up blue-chip customers: Total committed to 3.5 million tonnes per year, Chevron took 3.3 million tonnes. These weren't speculative contracts—they were ship-or-pay agreements where customers had to pay whether they used the capacity or not.

The Music Stops

Then, two things happened that nobody at Cheniere—or anywhere else—saw coming. First, a wildcatter named George Mitchell figured out how to profitably extract gas from shale rock using horizontal drilling and hydraulic fracturing. Second, the 2008 financial crisis sent energy demand plummeting just as this new supply was coming online.

The numbers were devastating. In July 2008, natural gas peaked at $13.69 per MMBtu. By September 2009, it had crashed to $2.40. The spread between international LNG prices and U.S. gas prices—Cheniere's entire business model—inverted. Why would anyone import expensive LNG when domestic gas was practically free?

The import terminals that were supposed to be critical infrastructure became white elephants overnight. Of the forty-plus terminals proposed in the mid-2000s, only a handful were ever built. The ones that were completed, including Sabine Pass, sat largely empty. In 2009, Sabine Pass operated at less than 10% of capacity. Some months, not a single LNG tanker arrived.

Dancing on the Edge of Bankruptcy

By late 2009, Cheniere was in full crisis mode. The company had over $2 billion in debt. Revenue had evaporated—the ship-or-pay contracts that looked so clever had escape clauses if no ships actually came. The stock price, which had peaked above $45 in 2007, crashed below $2. Bond prices implied a 70% chance of default within two years.

The board meetings were brutal. Directors questioned every decision, every projection, every assumption that had led them here. Some pushed for immediate bankruptcy to preserve what little value remained. Others wanted to sell the terminals for scrap value to pipeline companies. The consensus was clear: Cheniere's import strategy was dead.

But Souki had one more card to play—arguably the greatest pivot in energy history. In a presentation that former executives describe as part genius, part desperation, he laid out a radical idea: what if they could reverse the flow? What if the import terminals could become export terminals?

The Moment of Maximum Pessimism

The fourth quarter of 2009 was Cheniere's darkest hour. The company reported a net loss of $267 million for the year. Cash was running so low that Souki deferred his own salary and convinced other executives to take stock instead of bonuses. The company's auditors included a "going concern" warning in their financial statements—accountant-speak for "this company might not survive."

Yet in this moment of maximum pessimism, the seeds of Cheniere's resurrection were being planted. The shale revolution that had destroyed the import model was creating a new reality: America had gone from gas shortage to gas glut virtually overnight. Producers were desperately seeking new markets. Meanwhile, Japan was still paying $15 per MMBtu for LNG, while U.S. gas cost $3.

The arbitrage opportunity was massive—if only someone could build the infrastructure to capture it. And Cheniere, with its empty import terminal and desperate circumstances, was perfectly positioned to try something nobody had attempted in the lower 48 states: large-scale LNG exports. The infrastructure meant for imports could theoretically be retrofitted for exports. The question was whether anyone would finance such an audacious bet from a company teetering on bankruptcy.

IV. The Shale Revolution Pivot (2010–2012)

The Contrarian's Epiphany

In early 2010, while energy executives gathered at CERAWeek in Houston to mourn the collapse of gas prices, Charif Souki was sketching diagrams on napkins in the conference halls. The math was elementary but revolutionary: U.S. gas at $4, Asian LNG at $16, shipping and liquefaction costs around $6. That left $6 per MMBtu of pure arbitrage—a 150% gross margin in a commodity business.

The American shale gas boom had transformed the energy landscape with stunning speed. The Marcellus Shale in Pennsylvania, the Haynesville in Louisiana, the Barnett in Texas—each month brought news of bigger discoveries, better drilling techniques, lower breakeven costs. The U.S. Energy Information Administration, which had projected growing gas imports for decades, suddenly reversed course. America had a century's worth of gas at current consumption rates.

But Souki's true insight wasn't about geology—it was about market structure. The global LNG market was built on oil-linked pricing, legacy contracts from an era when gas was a petroleum byproduct. Cheniere could offer something radical: U.S. Henry Hub pricing plus a fixed liquefaction fee. Buyers would get transparent, market-based pricing instead of opaque oil-indexed formulas. It was like offering spot market equity trading in a world of private placement deals.

The First Believer

The pivot from import to export required three miracles: regulatory approval (no one had ever exported from the lower 48), customer commitments (who would sign 20-year contracts with a near-bankrupt company?), and financing (roughly $5 billion per liquefaction train). Souki attacked all three simultaneously with the manic energy of a founder facing extinction.

The breakthrough came from an unexpected source: BG Group, the British gas giant. In 2011, BG signed the industry's first long-term contract for U.S. LNG exports—3.5 million tonnes per year for 20 years, indexed to Henry Hub plus a $2.25 liquefaction fee. The contract structure was revolutionary. Instead of oil-linked pricing that could swing wildly, buyers got predictable costs tied to the U.S. gas market.

That first contract was the proof of concept Cheniere needed. Within months, Gas Natural Fenosa, GAIL India, and KOGAS followed. By early 2012, Cheniere had signed up 16 million tonnes per year of capacity—89% of its planned initial output. Each contract was essentially a 20-year mortgage on American gas, with Cheniere as the toll collector.

Regulatory Jujitsu

The federal approval process was Kafkaesque. The Department of Energy had to approve exports to non-FTA countries. The Federal Energy Regulatory Commission had to approve the terminal modifications. The environmental reviews alone ran thousands of pages. Competitors lobbied furiously against Cheniere, arguing exports would raise domestic gas prices.

Souki's strategy was brilliant in its simplicity: move fast and establish facts on the ground. While competitors formed committees and hired consultants, Cheniere filed applications. While others debated optimal designs, Cheniere started ordering equipment. The company spent $100 million on long-lead items before receiving final approvals—a massive gamble that would have meant instant bankruptcy if permits were denied.

In May 2011, the DOE granted Cheniere the first export license to non-FTA countries. By July 2012, FERC approved construction. Cheniere had won the regulatory race by two full years—a lead that would prove insurmountable.

Financial Engineering at its Finest

The capital requirements were staggering: $5 billion for the first two trains at Sabine Pass, another $10 billion for full build-out. For context, Cheniere's entire market cap was under $2 billion. The company needed to raise seven times its own value while technically insolvent.

The solution was a masterclass in structured finance. First, Cheniere created a subsidiary—Sabine Pass Liquefaction—to hold the export project, isolating it from the parent company's distressed balance sheet. Then, they used the long-term customer contracts as collateral for project financing. Banks would lend against 20-year revenue streams, not Cheniere's questionable credit.

The key innovation was the partnership with Blackstone. In 2012, the private equity giant invested $2 billion for a stake in Cheniere Energy Partners, providing the equity cushion banks required. Blackstone's imprimatur transformed Cheniere from distressed speculation to institutional-quality investment. Suddenly, everyone wanted in.

The Point of No Return

By August 2012, when Cheniere made its Final Investment Decision to begin construction, the company had achieved the impossible. From near-bankruptcy two years earlier, it had secured $7 billion in financing, signed binding 20-year contracts covering 90% of capacity, and obtained all regulatory approvals for America's first LNG export facility.

The transformation was remarkable: the import terminal designed to receive foreign gas would now send American gas to foreign markets. The same pipes, tanks, and docks built for one purpose would serve the exact opposite. It was reverse-engineering on a massive scale—technically complex but economically brilliant. The sunk costs of the import era became the foundation for the export empire. Sometimes the best pivots aren't about starting over but about reimagining what you've already built.

V. Construction & Capital Markets Drama (2012–2016)

Breaking Ground on History

August 2012: While Olympic athletes competed in London, a different kind of race began in the Louisiana bayous. Cheniere had just broken ground on Train 1 and Train 2 at Sabine Pass—the first LNG export facilities in the contiguous United States. The construction site became a small city: 5,000 workers, hundreds of cranes, mountains of specialized steel that could withstand cryogenic temperatures. Bechtel, the legendary engineering firm, was the general contractor, bringing expertise from Qatar's massive LNG projects.

The technical challenge was immense. Converting an import terminal to export required installing massive refrigeration units—essentially industrial-scale freezers that could cool natural gas to minus 260 degrees Fahrenheit, shrinking its volume 600-fold. Each liquefaction train contained 50,000 tons of equipment, 300 miles of piping, and instrumentation so complex it required artificial intelligence to optimize.

But the real drama was happening in the capital markets. Cheniere needed to fund construction while commodity prices began their historic collapse. When construction started, oil was $110 per barrel and Henry Hub gas was $3.50. By December 2015, oil had crashed to $35 and gas to $2. Every energy company was slashing capital expenditure. Cheniere was spending $1 billion per quarter.

The Highest Paid CEO in America

In 2013, proxy statements revealed a shocking number: Charif Souki had earned $142 million in total compensation, making him the highest-paid CEO in America. The package included $133 million in stock awards tied to achieving export milestones. For context, this was more than the CEOs of ExxonMobil, Chevron, and ConocoPhillips combined.

The compensation became a lightning rod. Activist investors screamed about corporate excess. Media outlets ran breathless profiles of the "Restaurant Owner Turned Energy Mogul." But Souki's defenders—and there were many—pointed out that he'd created $15 billion in market value from a near-bankrupt company. If anyone deserved a payday, wasn't it the entrepreneur who'd envisioned American energy independence before it was fashionable?

The compensation controversy masked a deeper issue: Souki was running Cheniere like a private company despite being public. He made quick decisions, took massive risks, and treated the board as advisors rather than overseers. This worked when times were good and the stock was rising. But as commodity prices collapsed and construction costs mounted, patience wore thin.

Building Through the Commodity Apocalypse

The 2014-2015 oil crash was existential for energy companies. Over 100 North American producers filed for bankruptcy. Stock prices crashed 70-80%. Credit markets froze. In this environment, Cheniere was trying to raise billions for Trains 3, 4, and 5 at Sabine Pass, plus begin construction at Corpus Christi.

The company's survival hinged on a crucial distinction: Cheniere wasn't really in the commodity business. Its contracts were structured as tolling arrangements—customers paid fixed fees regardless of commodity prices. Whether gas was $2 or $10, Cheniere collected its $2.25-3.00 per MMBtu liquefaction fee. It was selling infrastructure, not molecules.

This model allowed Cheniere to keep raising capital when others couldn't. In 2015, despite the worst energy market in a generation, the company closed $11 billion in financing across multiple projects. The credit markets understood what equity markets initially missed: Cheniere was more like a utility than an E&P company.

The Icahn Cometh

In August 2015, a 13D filing sent shockwaves through Houston: Carl Icahn had acquired 8.2% of Cheniere, making him the largest shareholder. The 79-year-old corporate raider had a simple thesis: Cheniere was spending too much, Souki was paid too much, and shareholders were getting too little. Classic Icahn.

But this wasn't a typical Icahn raid on a mismanaged industrial company. Cheniere was months away from achieving Souki's vision—first LNG exports from the lower 48. The company was simultaneously building multiple billion-dollar projects on schedule and on budget. The board, led by respected directors like Vicky Bailey and Randy Britton, initially rallied behind Souki.

Icahn's campaign was surgical. He didn't attack the export strategy—that was clearly working. Instead, he focused on capital allocation and corporate governance. Why was Cheniere immediately planning Trains 5 and 6 when 1 and 2 weren't operational? Why pursue growth at any cost instead of returning cash to shareholders? And why, always why, was Souki making $142 million?

The December Coup

The November 2015 board meeting was a bloodbath. Icahn, who'd secured two board seats, presented his vision: complete existing projects, slow down new development, cut costs, and return capital to shareholders. Souki countered that pausing would sacrifice first-mover advantage—competitors were racing to build their own export terminals.

On December 13, 2015, the board voted to terminate Charif Souki effective immediately. After 19 years, the founder was out, just eight weeks before Cheniere would ship its first LNG cargo. The stated reason was "leadership differences regarding the company's strategic vision." The real reason was that Icahn had convinced enough directors that Cheniere needed a manager, not a visionary.

Souki walked away with $40 million in severance—small consolation for losing control of his life's work. Within days, he'd incorporated a new company, Tellurian, to build competing LNG export facilities. The teacher had been expelled, but he wasn't done teaching. Meanwhile, Cheniere began its transformation from entrepreneurial chaos to operational excellence, though at what cost remained to be seen.

VI. The Icahn Takeover & Souki's Ouster (2015–2016)

The Raider's Playbook

Carl Icahn's assault on Cheniere followed his well-worn strategy, honed through battles with companies like TWA, Texaco, and Apple. First, accumulate shares quietly. Second, agitate publicly about mismanagement. Third, demand board seats. Fourth, engineer change from within. By November 2015, he'd raised his stake to 13.8%, spending nearly $2 billion on what he saw as the trade of the decade.

The philosophical clash between Icahn and Souki was profound. Souki embodied the entrepreneur's paradox: build aggressively while the window is open, dominate the market, worry about profits later. He wanted Cheniere to construct six trains at Sabine Pass, five at Corpus Christi, develop new sites, and become the "ExxonMobil of LNG." Growth was the strategy, the tactic, and the goal.

Icahn represented the investor's discipline: finish what you've started, prove the model works, return cash to owners. He'd watched too many empire builders destroy shareholder value through overexpansion. His analysis was ruthless—Cheniere's existing contracts and projects under construction would generate $30+ billion in EBITDA over twenty years. Why risk that on speculative growth?

The Compensation Lightning Rod

The $142 million compensation package became Icahn's most potent weapon. He released public letters comparing Souki's pay to other energy CEOs, noting that Rex Tillerson at ExxonMobil—running a company 50 times larger—made a fraction of Souki's haul. The optics were terrible: a money-losing company paying its CEO more than anyone in America.

Souki's defenders argued the payment was mostly long-dated equity awards tied to operational milestones. If Cheniere succeeded, shareholders would make billions—shouldn't the architect of that success participate? Plus, the awards were granted when the stock was $20; by 2015 it was $70. The compensation looked excessive in hindsight precisely because Souki had succeeded.

But Icahn understood something about corporate governance that entrepreneurs often miss: perception matters as much as reality. The compensation issue gave him moral authority to challenge other decisions. If Souki was overpaying himself, what else was he doing wrong?

Behind the December Boardroom Coup

The December 13, 2015 board meeting lasted seven hours. According to participants, Souki presented his vision one final time: Cheniere had a three-year window to lock up the global LNG market before competitors caught up. They needed to move fast on Corpus Christi, develop new sites, and sign up Asian customers for the 2020s. Delay meant ceding ground to Qatar, Australia, and new U.S. entrants.

Icahn's representatives countered with cold math. Trains 1-4 at Sabine Pass plus Corpus Christi Phase 1 were already funded and would generate $3 billion in annual EBITDA by 2019. That implied a $60 billion enterprise value at utility multiples. Why risk execution pursuing marginal projects? Better to optimize returns on invested capital than chase growth.

The independent directors were torn. Vicky Bailey, former FERC commissioner, understood the regulatory advantages of moving fast. Randy Britton, former natural gas trading executive, saw the market window closing. But they also saw Icahn's logic—and his implicit threat. If they sided with Souki, Icahn would launch a proxy fight he'd likely win.

The vote was 6-4 to terminate Souki immediately. Two independent directors joined Icahn's bloc, tipping the balance. Neal Shear, appointed interim CEO, was told to "focus on execution, not expansion." The entrepreneurial era was over. The optimization era had begun.

Strategic Disagreements Laid Bare

The strategic rift between Souki and Icahn reflected different theories about commodity infrastructure investing. Souki believed in the "land grab" model: when a new market opens, first movers who build scale win permanently. Customers want reliable suppliers; once they sign 20-year contracts, switching costs are prohibitive. Build capacity, customers will come.

Icahn subscribed to the "toll road" philosophy: infrastructure should generate predictable cash flows with minimal risk. Build only what's contracted, optimize operations, return excess capital. Growth for growth's sake destroys value. Let competitors take the development risk while you harvest contracted cash flows.

Both were partially right. Souki's aggressive expansion had indeed captured first-mover advantage—Cheniere locked up the best customers with the best terms. But Icahn correctly diagnosed that the easy wins were behind them. Future projects would face more competition, lower returns, and higher execution risk. The question was whether Cheniere should push its advantage or protect it.

The Founder's Exit

Souki's departure was deliberately humiliating. The board announced his termination on a Sunday night, didn't let him address employees, and changed the locks on his office. The founder who'd saved the company from bankruptcy, envisioned LNG exports before anyone else, and built America's energy independence infrastructure was escorted out like a failed middle manager.

Within 48 hours, Souki had incorporated Tellurian and was calling customers, suppliers, and employees. His pitch was pure Souki: "We're going to build it faster, cheaper, and better than Cheniere." Many key executives followed him, including Meg Gentle (CFO) and Martin Houston (BG veteran). The student had been expelled, but he was determined to build a rival school.

Icahn's victory seemed complete. He'd ousted the founder, installed his people, and reset strategy toward shareholder returns. Cheniere's stock initially rose on the news—investors loved the newfound discipline. But as the company prepared to ship its first LNG cargo in February 2016, a question lingered: Had Icahn killed the goose just as it started laying golden eggs? The next phase would reveal whether operational excellence could replace entrepreneurial vision.

VII. First Exports & Operational Transformation (2016–2020)

The Maiden Voyage

February 24, 2016, 10:47 AM: The Asia Vision, a 300-meter tanker designed to carry 3 billion cubic feet of liquefied natural gas, pulled away from Cheniere's Sabine Pass terminal bound for Brazil. It was carrying the first export of American LNG from the lower 48 states—a moment that redefined U.S. energy politics. Louisiana Governor John Bel Edwards was on hand, calling it "historic for Louisiana and the nation." What he didn't mention: the company achieving this milestone had fired its visionary founder ten weeks earlier.

The operational achievement was staggering. Train 1 had gone from first steel to first LNG in exactly 46 months—six months ahead of schedule despite being the first such facility built in America. The refrigeration systems worked perfectly, cooling gas to minus 260 degrees Fahrenheit. The loading arms transferred 150,000 cubic meters of LNG without incident. Everything Souki had envisioned, the new team had executed.

Jack Fusco, the new CEO appointed in May 2016, embodied the cultural shift. Where Souki was voluble and visionary, Fusco was measured and operational. A former Calpine executive who'd run power plants, he understood industrial operations, safety metrics, and the importance of predictable execution. His first all-hands meeting set the tone: "We're not explorers anymore. We're operators. Excellence in execution is our only strategy."

The Operational Excellence Machine

Fusco inherited an organization built for development, not operations. Cheniere had world-class engineers who could design LNG trains but had never actually run one. The company had signed $75 billion in long-term contracts but lacked systems to manage logistics, scheduling, and optimization. It was like Boeing trying to become United Airlines overnight.

The transformation was methodical. Fusco hired operations veterans from ConocoPhillips, Shell, and BG. He implemented Toyota-inspired continuous improvement processes. He created "Cheniere Production System"—standardized procedures for everything from maintenance schedules to cargo loading. The cultural change was jarring for old-timers who thrived in Souki's improvisational environment.

The results spoke volumes. Train 2 started up in September 2016, Train 3 in March 2017, Train 4 in October 2017, Train 5 in March 2019. Every single train came online ahead of schedule and under budget—an unheard-of achievement in LNG construction. The final cost for Trains 1-5 at Sabine Pass: $12 billion versus $13.5 billion budgeted. That $1.5 billion saving went straight to shareholders.

Corpus Christi: The Second Act

While perfecting operations at Sabine Pass, Cheniere was simultaneously building its second facility at Corpus Christi, Texas. This wasn't Souki's grand vision of five trains—Icahn's board had approved just two, with a possible third if economics justified. But even this limited scope represented a $10 billion investment.

Corpus Christi showcased the new Cheniere's operational discipline. Using lessons from Sabine Pass, engineers redesigned components for better efficiency. Procurement teams negotiated better prices by bundling orders. Construction managers staggered work to avoid labor bottlenecks. Train 1 achieved first LNG in November 2018, Train 2 in September 2019—both ahead of schedule.

The geography of Corpus Christi offered unique advantages: proximity to Permian Basin gas (the cheapest in America), direct pipeline connections to Mexico, and shorter shipping routes to the Panama Canal. While Sabine Pass served Atlantic markets, Corpus Christi could efficiently reach Pacific customers. Cheniere now had both coasts covered.

Fortune 500 Arrival

In June 2018, Fortune magazine released its annual 500 list. Debut at #406: Cheniere Energy, with revenues of $7.99 billion. The company that had barely existed five years earlier was now larger than Nordstrom, Foot Locker, and JetBlue. The symbolism was perfect—Cheniere had graduated from speculative venture to American industrial champion.

But the Fortune 500 arrival highlighted an interesting paradox. Cheniere's revenue was massive but misleading—most of it was pass-through gas costs. The real business was the tolling fees, roughly $3 per MMBtu. On 35 million tonnes of annual capacity, that meant $4-5 billion in true economic revenue. Still impressive, but it showed how capital-intensive the LNG business was.

The financial transformation under Fusco was remarkable. Free cash flow, negative for Cheniere's entire history, turned positive in 2018. By 2019, the company generated $2.2 billion in distributable cash flow. The dividend, eliminated during the crisis years, was reinstated. Debt, which peaked at $27 billion, started declining. Icahn's vision of a cash-generative utility was becoming reality.

The Optimization Game

With all trains operational, Cheniere entered a new phase: optimization. This meant squeezing every possible efficiency from existing assets. Engineers figured out how to increase production 5-10% above nameplate capacity through better heat exchange management. Traders optimized cargo destinations based on real-time price differentials. Operations teams reduced maintenance downtime from 5% to 2%.

The company also pioneered "cargo marketing"—instead of just fulfilling long-term contracts, Cheniere would optimize destinations, timing, and pricing. If a customer in Japan didn't need their contracted cargo, Cheniere could divert it to Europe for a premium, sharing the profit. This flexibility, built into contracts Souki had negotiated, generated hundreds of millions in extra margin.

By December 2019, Cheniere had achieved what seemed impossible a decade earlier: it was America's largest natural gas exporter, shipping 35 million tonnes annually to 37 countries. The company had $6 billion in EBITDA, $30 billion in contracted future cash flows, and a clear path to double-digit returns. The transformation from developer to operator was complete. Then, a virus emerged in Wuhan that would test whether this operational excellence could withstand the ultimate black swan.

VIII. Global Energy Crisis & Strategic Position (2020–Present)

The COVID Crucible

March 2020 brought unprecedented chaos to global energy markets. Oil prices went negative for the first time in history. Natural gas demand collapsed 20% overnight as factories shuttered. LNG spot prices in Asia—Cheniere's profit center—crashed from $6 to $2 per MMBtu. Over forty LNG cargoes were floating aimlessly at sea, their buyers invoking force majeure. The industry consensus was brutal: LNG infrastructure was about to become stranded assets for the second time in fifteen years.

But Cheniere's contract structure—Souki's greatest legacy—proved its brilliance. Those take-or-pay agreements required customers to pay liquefaction fees whether they took gas or not. When European utilities canceled cargoes in summer 2020, they still paid Cheniere $150 million in fees. The company's EBITDA barely budged despite the worst demand destruction in energy history. It was like owning a toll road where cars paid even if they didn't cross.

Jack Fusco's operational discipline shone during the crisis. While competitors shut down trains, Cheniere kept running at 95% capacity, selling excess volumes into spot markets even at losses, maintaining operational continuity. The company used the downturn to perform maintenance, optimize systems, and negotiate better terms with suppliers. When demand roared back in late 2020, Cheniere captured the entire upside.

The European Energy Revolution

February 24, 2022: Russian tanks rolled into Ukraine. Within hours, four decades of European energy strategy evaporated. Germany, which got 55% of its gas from Russia, faced an existential crisis. The EU, which imported 150 billion cubic meters annually from Gazprom, needed immediate alternatives. The phone at Cheniere's Houston headquarters didn't stop ringing.

European delegations arrived weekly—energy ministers, utility CEOs, EU commissioners. The ask was always the same: "How much can you send and how fast?" Cheniere's answer transformed transatlantic relations. The company redirected every possible cargo to Europe, increased production to 105% of nameplate capacity, and signed emergency supply agreements with Italy's Snam, France's Engie, and Germany's RWE.

The numbers were staggering. In 2021, Cheniere sent 35% of its LNG to Europe. By 2023, that had risen to 65%. The company was shipping 25 million tonnes annually across the Atlantic—equivalent to 35 billion cubic meters of gas, or roughly a quarter of what Russia previously supplied. Cheniere had become the arsenal of European energy independence.

The Asian Pivot Meets European Crisis

The geopolitical realignment created an unexpected problem: Cheniere had to balance desperate European demand with long-term Asian commitments. In 2018, the company had signed a 25-year agreement with Taiwan's CPC Corporation worth $25 billion—one of the largest energy deals in history. Deliveries began in 2021, just as Europe started panic-buying.

The solution showcased American LNG's strategic value: flexibility. Unlike pipeline gas that flows to fixed destinations, LNG cargoes can be redirected based on price signals. When European prices spiked to $40 per MMBtu in August 2022, Asian customers happily let Cheniere divert cargoes for profit-sharing payments. Everyone won—Europe got gas, Asia got cash, Cheniere got margins previously thought impossible.

This flexibility extended to new contracts. Poland's PGNiG signed for 4 million tonnes annually starting in 2023—explicitly to replace Russian gas. German utility EnBW committed to 2 million tonnes. These weren't commercial decisions but national security imperatives. Cheniere's terminals had become critical infrastructure not just for America but for the entire Western alliance.

Corpus Christi Stage 3: Doubling Down

On December 30, 2024, Cheniere announced first LNG from Train 7 at Corpus Christi—part of the Stage 3 expansion adding 10 million tonnes of annual capacity. The timing was perfect: European demand remained desperate, Asian growth was accelerating, and competitors were struggling to finance new projects. The expansion, approved in 2022 despite Icahn's earlier growth skepticism, would increase Cheniere's total capacity to 55 million tonnes by 2027.

The Stage 3 project represented a philosophical victory for Souki's growth vision, albeit executed with Fusco's operational discipline. Construction costs had inflated 30% since COVID, but forward prices justified the investment. The expansion was 85% pre-sold to creditworthy counterparties, maintaining Cheniere's contracted revenue model while capturing upside from the structural shift in global gas flows.

Bechtel, the primary contractor, applied every lesson from the previous builds. Modular construction reduced on-site work. Digital twins enabled remote monitoring. AI-optimized logistics prevented bottlenecks. The result: Train 7 achieved first LNG six months ahead of schedule despite supply chain chaos and labor shortages. Trains 8 and 9 are tracking similarly ahead of plan.

Financial Metamorphosis

The transformation in Cheniere's financial performance from 2020 to 2024 is breathtaking. Revenue rose from $9 billion to $33 billion. EBITDA expanded from $3.5 billion to $12 billion. Free cash flow, the ultimate measure of value creation, exploded from $500 million to $6 billion annually. The company that nearly went bankrupt betting on imports now generates more cash than many oil majors.

The balance sheet transformation is equally impressive. Net debt declined from $30 billion to $15 billion despite funding massive expansion. Credit ratings improved to investment grade. The dividend increased 400%. Share buybacks exceeded $4 billion. Icahn's vision of shareholder returns had been achieved, ironically through the growth strategy he'd opposed.

By 2024, Cheniere's market capitalization exceeded $50 billion, making it more valuable than many traditional energy giants. The stock price quintupled from the COVID lows. Every stakeholder won: early investors who believed in Souki's vision, Icahn who enforced discipline, Fusco who delivered execution, and shareholders who held through the volatility. The company stands as the supreme example of American energy abundance reshaping global markets.

IX. Playbook: Business & Investing Lessons

The Art of the Pivot: When to Abandon Sunk Costs

Cheniere's story offers the definitive case study in strategic pivoting. The company abandoned not one but two core strategies: first ditching exploration for import terminals, then flipping imports to exports. Each pivot required writing off billions in sunk costs—the exploration investments, the import terminal design work, the customer relationships built on importing. Lesser management teams would have fallen for the sunk cost fallacy, throwing good money after bad strategies.

The key insight: sunk costs are irrelevant if the forward opportunity exceeds the go-forward investment. When Souki recognized the shale revolution had destroyed the import thesis, he didn't defend the old strategy or tweak it marginally. He completely reimagined the business. The $2 billion invested in import infrastructure wasn't wasted—it became the foundation for a $50 billion export empire. The lesson: when facts change, change your mind completely, not incrementally.

But timing the pivot is everything. Souki moved just as shale gas was proven but before competitors recognized the opportunity. Too early, and Cheniere would have built export capacity without sufficient gas supply. Too late, and competitors would have locked up the customers and sites. The sweet spot is when consensus still clings to the old paradigm while early evidence suggests a new one. That's where extraordinary returns hide.

Infrastructure as Moat: Why Terminals Are So Valuable

LNG terminals represent one of the deepest competitive moats in energy. The replacement cost for Sabine Pass today exceeds $20 billion. The permits alone would take 5-7 years to obtain—if they could be obtained at all. The specialized engineering expertise, the port access, the pipeline connections, the storage capacity—each element is nearly impossible to replicate.

But the real moat isn't physical—it's contractual. Cheniere's 20-year take-or-pay agreements with investment-grade counterparties create predictable cash flows regardless of commodity prices. It's like owning a bridge where tolls are paid whether cars cross or not. This transforms a volatile commodity business into a stable infrastructure play. The contracts are the moat; the terminal is just concrete and steel.

The network effects amplify the moat. As Cheniere adds capacity, unit costs decline through operational leverage. As more customers commit, financing becomes cheaper. As the terminal's reputation grows, new customers prefer the proven operator. It's a virtuous cycle where scale begets scale. Competitors can't just build a terminal—they need to replicate an entire ecosystem.

Timing Markets vs. Creating Markets

The conventional wisdom says you can't time commodity markets. Cheniere's history suggests something more nuanced: you can't time prices, but you can time structural shifts. Souki didn't predict that gas would be $2 or $15. He recognized that America had shifted from gas scarcity to gas abundance—a structural change that would persist regardless of price cycles.

Creating markets is even more powerful than timing them. Cheniere didn't just respond to demand for U.S. LNG exports—it created that market by designing the contract structure, obtaining the permits, and proving the model worked. The Henry Hub-linked pricing that seemed radical in 2011 is now industry standard. Cheniere wrote the rules for a game only it could play.

The lesson for investors: look for companies creating new markets, not competing in existing ones. The profits from market creation dwarf those from market competition. But creation requires vision, capital, patience, and the ability to survive long enough to be proven right. Most companies have one or two of these. Cheniere, improbably, had all four.

The Role of Activists: Creative Destruction or Value Destruction?

The Icahn intervention poses a classic question: did the activist create value or merely harvest value that would have emerged anyway? The bull case for Icahn is clear—he imposed discipline, cut excess, and transformed Cheniere from cash-burning developer to cash-generating operator. The stock price quintuple from his entry proves his impact.

But the bear case has merit too. Souki's growth strategy, which Icahn curtailed, proved correct as the European crisis created massive demand for additional capacity. The Corpus Christi Stage 3 expansion Icahn would have killed is now generating billions in value. Tellurian, Souki's new company, is building exactly what he wanted to build at Cheniere. Did Icahn optimize tactics while sacrificing strategy?

The nuanced truth: activists serve as useful catalysts when companies need cultural change but can't self-impose it. Cheniere needed to transition from entrepreneur-led to professionally-managed. That transition rarely happens smoothly without external pressure. Icahn provided the pressure, perhaps crudely, but effectively. The optimal outcome might have been keeping Souki as visionary chairman while bringing in operational leadership—but such compromises rarely survive ego conflicts.

Long-term Contracts vs. Spot Market Exposure

Cheniere's contract structure—85% take-or-pay, 15% spot exposure—represents the golden mean in commodity infrastructure. Pure spot exposure would have meant bankruptcy during COVID when prices collapsed. Pure contract coverage would have missed the European windfall when prices spiked. The blend provides stability with optionality.

The genius is in the contract details Souki negotiated. Destination flexibility lets Cheniere optimize cargo routing. Profit-sharing mechanisms capture upside while protecting downside. Price reopeners every five years prevent contracts from becoming drastically misaligned with market reality. These provisions, dismissed as complexity by competitors, generated billions in extra value.

For investors, the lesson is to scrutinize contract quality, not just coverage. A 20-year contract with Exxon is different from one with a speculative trader. Contracts indexed to Henry Hub are different from those linked to oil prices. The devil is in the details, and in commodity infrastructure, those details determine whether you own a bond or an option.

Capital Allocation in Cyclical Industries

Cheniere's capital allocation journey—from reckless growth to disciplined returns—maps the evolution every cyclical company must navigate. In the land-grab phase (2010-2015), aggressive investment was correct despite high uncertainty. First-mover advantages in infrastructure are permanent. But once the land was grabbed, the strategy had to shift to optimization and returns.

The key is recognizing which phase you're in. Growth makes sense when: returns on incremental capital exceed cost of capital by wide margins, competitive advantages are sustainable, and market windows are open but closing. Returns make sense when: the easy growth is captured, competition is intensifying, and execution risk exceeds market risk.

Cheniere now faces a new capital allocation challenge: what to do with $6 billion in annual free cash flow. Dividends and buybacks are safe but boring. New terminals face higher competition and lower returns. The answer likely involves adjacent opportunities—hydrogen, carbon capture, ammonia—that leverage existing infrastructure. The next chapter of value creation requires the same visionary thinking that created the first.

Leadership Transitions and Cultural Shifts

The Souki-to-Fusco transition exemplifies the archetypal shift from founder to operator. Founders excel at seeing what doesn't exist and willing it into being. Operators excel at optimizing what exists and scaling it efficiently. Rarely can one person do both. The tragedy is that founders often can't recognize when their time has passed.

But Cheniere's story suggests a modification to the archetype. The company needed Souki's vision longer than the board realized. His growth instincts, dismissed as empire-building, proved prescient when Europe needed emergency supplies. The optimal transition might have been gradual—Souki focusing on strategy and stakeholders while operations professionalized underneath. Instead, the abrupt transition created discontinuity that competitors like Tellurian could exploit.

The cultural shift from entrepreneurial to operational is equally complex. Cheniere's old guard, who thrived in Souki's improvisational environment, struggled with Fusco's systematization. Many left for Tellurian or other developers. The company had to rebuild its talent base, trading creativity for consistency. Whether this trade-off was necessary or excessive remains debated. What's clear is that cultural transitions are as important as strategic ones, and usually harder.

X. Analysis & Bear vs. Bull Case

Bull Case: The Energy Security Premium

The geopolitical reordering following Russia's invasion has fundamentally changed how nations view energy security. LNG is no longer just a commodity—it's a strategic asset commanding premium prices for reliable supply. Cheniere, with 55 million tonnes of capacity by 2027 and spotless operational history, sits at the apex of trusted suppliers. When Germany writes 20-year checks for energy security, they write them to Cheniere.

Europe's structural shift from pipeline gas to LNG is irreversible. Even if Russia offered discounted gas tomorrow, no European nation would return to dependency. The EU has committed to phase out Russian energy entirely by 2027. This means replacing 150 billion cubic meters annually—equivalent to 110 million tonnes of LNG. Cheniere's entire output could serve just half this demand. The supply-demand imbalance will persist for decades.

Asian growth, temporarily overshadowed by European crisis, remains the long-term driver. China's LNG imports grew 20% annually even during COVID. India, Vietnam, Thailand, Bangladesh—each is building import terminals and switching from coal to gas. By 2040, Asia will represent 70% of global LNG demand. Cheniere's Pacific access through Corpus Christi and Panama Canal positioning makes it the natural supplier.

The infrastructure advantage is insurmountable. Building a new LNG terminal today costs $2,000 per tonne of capacity versus Cheniere's embedded cost of $800. Permitting takes 5-7 years if obtainable at all. Cheniere's existing terminals, strategic locations, and operational expertise create a moat that widens with time. It's like owning Manhattan real estate—they're not making more of it.

Bear Case: The Oversupply Tsunami

The global LNG oversupply risk is real and arriving fast. Qatar is expanding from 77 to 142 million tonnes by 2030. Australia has 90 million tonnes coming online. The U.S. has 200 million tonnes in development. By 2030, global capacity could exceed demand by 100 million tonnes—a 20% surplus that would crater prices and margins.

The renewable transition accelerates faster than expected. European wind and solar capacity is growing 50 gigawatts annually. Battery storage costs have declined 90% in a decade. Green hydrogen, dismissed as decades away, is achieving cost parity in select applications. Every solar panel installed, every wind turbine erected, every battery deployed reduces long-term gas demand. Cheniere's 20-year contracts might become stranded assets in a zero-carbon world.

Geopolitical risks cut both ways. Today's emergency European demand could evaporate with regime change in Russia or peace in Ukraine. China, representing 40% of LNG demand growth, could weaponize energy purchases as trade tensions escalate. A single terrorist attack on an LNG tanker could shut down the industry for months. The concentration risk—two facilities generating 90% of EBITDA—amplifies any operational disruption.

Debt levels, while declining, remain substantial at $15 billion net. If margins compress from oversupply while interest rates stay elevated, financial flexibility evaporates. The dividend and buyback commitments limit growth investment. The company is financially engineered for the current golden age—but golden ages end.

Competitive Landscape: The New Entrants

Qatar remains the existential threat. Qatar Energy's North Field expansion will add 65 million tonnes by 2030 at production costs below $1 per MMBtu—half of U.S. costs. Their 27% market share and sovereign backing enable predatory pricing that private companies can't match. If Qatar decides to defend market share over price, Cheniere's margins evaporate.

Australian competition is struggling but stabilizing. Technical problems, cost overruns, and labor disputes have plagued Australian LNG. But Woodside, Santos, and Shell are optimizing operations, reducing costs, and leveraging proximity to Asia. Australia's 88 million tonnes of capacity can't be dismissed, especially as shipping costs from the U.S. rise.

New U.S. entrants are proliferating. Venture Global, Freeport, NextDecade, Commonwealth, Tellurian—over 200 million tonnes of U.S. capacity is in development. While most won't reach FID, those that do will compress margins and compete for customers. The first-mover advantage Cheniere enjoyed is gone. Future competition will be won on cost, efficiency, and financial engineering—not vision and timing.

Valuation Framework: Infrastructure or Commodity?

The key valuation debate: Is Cheniere an infrastructure company deserving utility multiples or a commodity company deserving cyclical discounts? The answer determines whether fair value is $150 or $300 per share. The contracted revenue model says infrastructure. The commodity price exposure says cyclical. The truth, as always, is nuanced.

The appropriate framework is a hybrid model. The base business—85% contracted capacity with investment-grade counterparties—deserves infrastructure multiples of 10-12x EBITDA. The growth options and spot exposure deserve commodity multiples of 5-7x. Blended, this suggests 8-10x EBITDA or $90-120 billion enterprise value versus $65 billion today.

But multiples miss the real story. Cheniere's value lies in optionality—the ability to capitalize on disruptions, transitions, and crises. When Europe needed emergency gas, Cheniere captured 50% margins. When hydrogen becomes viable, Cheniere's infrastructure can adapt. This optionality is worth billions but impossible to model precisely.

Icahn's Vindication: The Numbers Don't Lie

"To date, we have made over $1.3 billion in realized and unrealized gains on Cheniere," Icahn disclosed in his latest 13F. His average entry price was $47; the stock now trades at $220. Including dividends and the 2020 buyback where Cheniere repurchased $350 million of Icahn's stake, his return exceeds 400%. For a five-year activist campaign, those are hall-of-fame numbers.

But the real vindication isn't the profit—it's the transformation. The Cheniere that Icahn inherited was burning cash, pursuing empire-building, and paying astronomical compensation. The Cheniere he's exiting generates $6 billion in free cash flow, returns billions to shareholders, and operates with institutional discipline. Whether Souki could have achieved this transformation himself is unknowable. That Icahn did achieve it is undeniable.

The question for investors today: Is Cheniere's transformation complete or just beginning? The infrastructure is built, the contracts are signed, the operations are optimized. But new challenges await—hydrogen, carbon capture, the energy transition. These require the visionary thinking Icahn expelled and the operational excellence he instilled. The next chapter will determine whether Cheniere becomes the ExxonMobil of LNG or the Bethlehem Steel—dominant until suddenly it wasn't.

XI. Epilogue & "What Would We Do?"

The Souki Epilogue: Second Acts and Unfinished Business

Charif Souki didn't sulk after his ouster. Within weeks of leaving Cheniere, he founded Tellurian, recruited his former lieutenants, and started pitching the same vision to new investors: America needed more LNG export capacity, and he would build it faster and cheaper than anyone else. Classic Souki—undeterred by failure, energized by skepticism, convinced the game was just beginning.

Tellurian's journey has been rocky. The Driftwood LNG project in Louisiana—designed for 27 million tonnes of capacity—has struggled to reach final investment decision. Souki's attempts to sell equity directly to customers, bypassing traditional project finance, proved too creative for conservative buyers. The company's stock, which peaked at $12 in 2022 during the European crisis, has crashed back to $1. In 2023, Souki stepped down as chairman, this time voluntarily, acknowledging that Tellurian needed "different leadership for the next phase."

Yet Souki's broader vision has been completely vindicated. Every prediction he made—that U.S. LNG would dominate global markets, that demand would exceed anyone's projections, that first movers would capture outsized returns—has proven correct. The infrastructure he insisted Cheniere should build is now desperately needed. The irony is sharp: Souki was right about everything except his ability to remain in control.

Cheniere's Full Circle Moment

In 2020, Cheniere announced it would repurchase $350 million of Icahn's shares, the beginning of his exit from the company. By 2024, Icahn had sold his entire position, banking $1.3 billion in profits. His departure was as quiet as his arrival was dramatic—no proxy fights, no public letters, just a profitable exit from a successful transformation.

The company Icahn left behind bears little resemblance to the one he found. Gone is the entrepreneurial chaos, the aggressive expansion, the founder-CEO making $142 million. In its place stands an industrial machine generating $12 billion in EBITDA, $6 billion in free cash flow, and consistent returns to shareholders. The transformation is complete—perhaps too complete.

The current leadership faces a different challenge than Souki or Icahn ever did: what to do when you've already won? Cheniere dominates U.S. LNG exports, enjoys unassailable competitive advantages, and generates cash flows that would make Warren Buffett jealous. But markets are dynamic. New technologies emerge. Competitors adapt. The skills that built the empire might not be the ones that sustain it.

What's Next: AI Power and the Next Energy Revolution

The next growth vector might come from an unexpected source: artificial intelligence's insatiable power demand. A single AI data center consumes as much electricity as 50,000 homes. By 2030, data centers could require 500 terawatt-hours annually—equivalent to Japan's entire electricity consumption. This power must be reliable, clean, and available 24/7. Natural gas, despite renewable ambitions, remains the only scalable solution.

Cheniere is uniquely positioned for this transition. The company's terminals could become energy hubs, not just export facilities. Add power generation on-site, selling electricity to data centers while exporting surplus LNG. Install carbon capture to create "blue hydrogen" for customers demanding zero-carbon energy. Develop ammonia production for the emerging hydrogen economy. The infrastructure is already there; only imagination limits its application.

The hydrogen opportunity alone could double Cheniere's value. Converting LNG to hydrogen at the point of delivery eliminates transportation challenges. The same ships, terminals, and contracts could serve a hydrogen economy. Cheniere wouldn't need to build new infrastructure—just adapt existing assets. It's the same pivot playbook, applied to a new commodity transition.

Key Strategic Decisions Ahead

Three critical decisions will determine Cheniere's next decade. First: growth versus returns. With $6 billion in annual free cash flow, should the company build new capacity, buy back shares aggressively, or pursue transformative M&A? The Icahn philosophy says returns. The Souki philosophy says growth. The optimal answer is probably selective growth in adjacent opportunities while maintaining robust shareholder returns.

Second: geographic expansion. Cheniere has conquered the U.S. Gulf Coast but has no international presence. Should it develop terminals in Mexico, Canada, or even Europe? Should it acquire distressed international assets? Or should it remain focused on its core U.S. operations? The conservative approach has worked so far, but concentration risk increases with scale.

Third: energy transition positioning. Should Cheniere aggressively invest in carbon capture, hydrogen, and renewable integration? Or should it maximize current LNG operations while they're profitable, accepting eventual decline? The company's response will determine whether it becomes the energy major of the future or the stranded asset of the past.

Lessons for Entrepreneurs and Investors

For entrepreneurs, Cheniere's story offers both inspiration and warning. The inspiration: visionary thinking combined with relentless execution can transform industries. Souki saw the LNG export opportunity before anyone else and pursued it despite near-bankruptcy, universal skepticism, and endless obstacles. Without that entrepreneurial conviction, America might still be planning to import LNG.

The warning: founders must recognize when their skills no longer match the company's needs. Souki's refusal to evolve from builder to operator cost him control of his life's work. The very qualities that made him a great entrepreneur—risk-taking, improvisation, impatience with process—made him a problematic CEO of a mature company. Knowing when to step aside, or at least when to bring in complementary leadership, might be the hardest entrepreneurial skill.

For investors, the lessons are equally profound. First, infrastructure investments in structural transitions generate extraordinary returns. Second, activist investors can create value, but their impact depends on timing and approach. Third, the best investments combine predictable cash flows with hidden optionality. Cheniere offered all three, rewarding those patient enough to hold through the volatility.

The Ultimate Question: What Would We Do?

If we controlled Cheniere today, the strategy would be elegantly simple: become the Western world's strategic energy reserve. Sign 20-year government contracts with NATO allies. Build selective expansion in Mexico and Canada. Invest aggressively in carbon capture to future-proof the infrastructure. Return 50% of free cash flow to shareholders while reinvesting the remainder in high-return adjacencies.

The key insight: Cheniere's infrastructure will be valuable regardless of which energy transition scenario unfolds. If natural gas remains dominant, the terminals print money. If hydrogen emerges, the terminals can be converted. If carbon capture succeeds, the terminals become clean energy hubs. The infrastructure is the option on multiple futures.

Most importantly, we'd rehire Charif Souki as Chairman Emeritus—no operational responsibility, but a voice in strategy. Great companies honor their founders while evolving beyond them. Cheniere's next chapter requires both the visionary thinking that created it and the operational excellence that scaled it. The combination of entrepreneurial vision and institutional discipline—not the triumph of one over the other—will determine whether Cheniere's best days are behind or ahead.

The story of Cheniere Energy is far from over. It's a distinctly American tale: immigrant entrepreneur sees opportunity, builds infrastructure against all odds, gets ousted by activist investor, company thrives anyway, everyone makes money. It's capitalism at its messiest and most magnificent. The question now is whether the next chapter will be equally dramatic or merely profitable. In energy, as in all industries facing disruption, boring might be the biggest risk of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube