AEGISLOG: The Story of India's Energy Infrastructure Champion

I. Introduction & Episode Teaser

Picture this: It's 2010, and Shell, one of the world's oil supermajors, is quietly exiting India's LPG distribution business. The buyer? Not another multinational giant, not a state-owned behemoth, but a Mumbai-based company most international investors had never heard of—Aegis Logistics. In one strategic move, this family-controlled firm acquired Shell's entire Indian LPG operation, instantly catapulting itself into the big leagues of energy infrastructure. The deal included 30 bottling plants spread across 15 states, transforming Aegis from a regional player into a national force.

Today, Aegis Logistics Limited stands as India's leading private sector integrated oil, gas, and chemical logistics company. With operations spanning liquid and gas terminal divisions, the company handles over 3 million metric tons of LPG annually—enough to supply cooking gas to millions of Indian households. Its market capitalization has soared to ₹25,019 crore, with revenues touching ₹6,882 crore and profits of ₹805 crore. But this isn't just another corporate success story.

This is the tale of how a small pharmaceutical trading house, incorporated in 1956 as Atul Drug House Limited, transformed itself into the backbone of India's energy infrastructure. It's a story that mirrors India's own economic evolution—from import substitution to liberalization, from scarcity to abundance, from state control to private enterprise. Along the way, we'll uncover how the Chandaria family navigated the treacherous waters of the License Raj, why they pivoted from drugs to chemicals to energy, and how they built trust with powerful public sector undertakings that typically viewed private players with suspicion.

The hook that makes Aegis fascinating isn't just its transformation—it's the timing. As India races toward energy security and millions of households switch from wood and kerosene to cleaner cooking fuels, Aegis has positioned itself at the intersection of necessity and opportunity. This is infrastructure as nation-building, where every storage tank and pipeline isn't just steel and concrete, but a bridge between India's energy-scarce past and its consumption-driven future.

II. Origins & The Chandaria Story

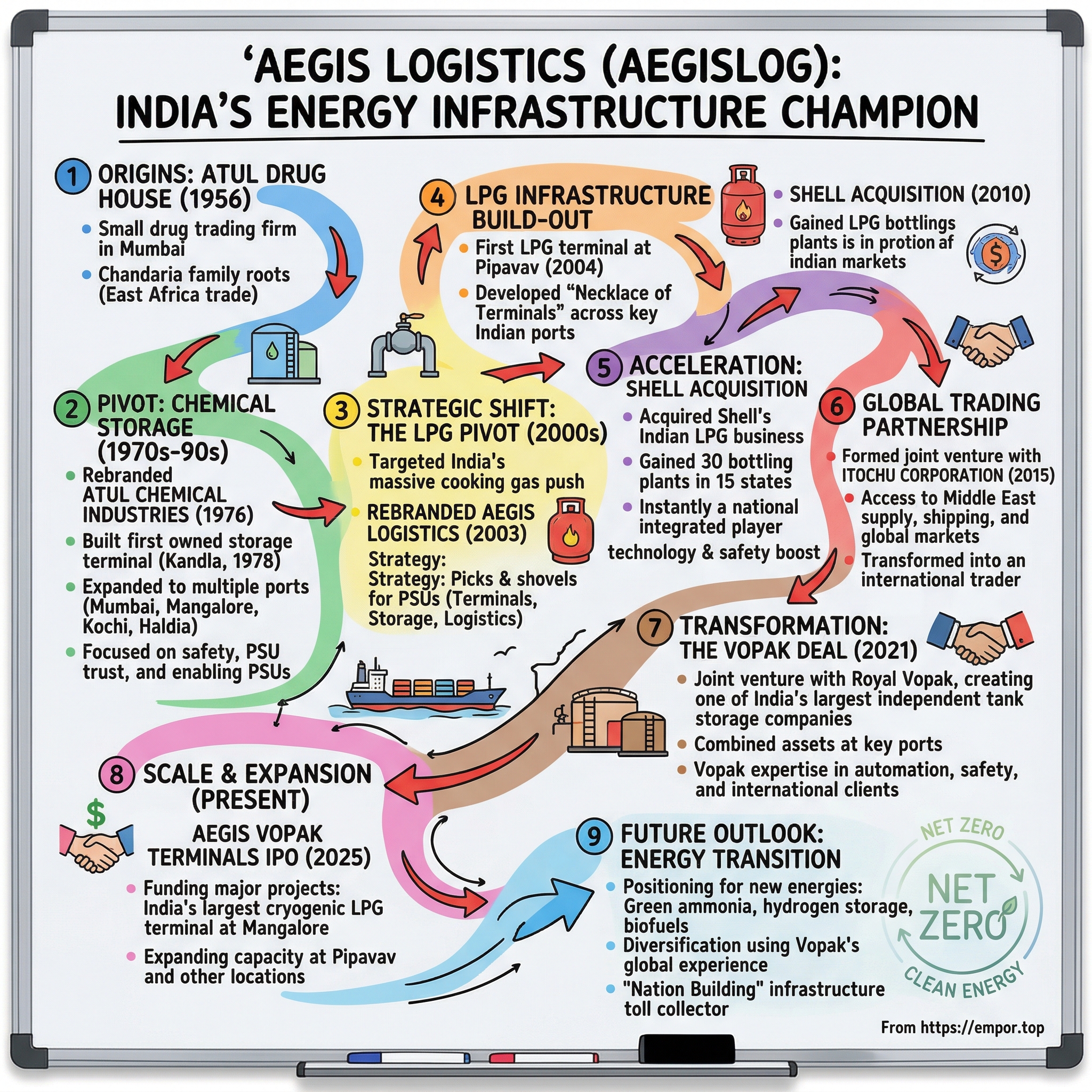

The monsoon of 1956 brought more than rain to Mumbai. On June 30th, as the city's textile mills hummed and the port bustled with cargo ships, a modest office in Fort registered a new company: Atul Drug House Limited. The founders weren't pharmaceutical magnates or chemical engineers—they were the Chandarias, a Gujarati family whose journey to that Mumbai office had taken them through the spice markets of Zanzibar and the trading posts of East Africa.

The Chandaria saga begins not in boardrooms but in the dusty villages of Gujarat, where generations of the family had been traders. Like many Gujarati merchant families, they followed opportunity across the Arabian Sea to East Africa in the early 20th century. There, they built trading networks that stretched from Mombasa to Dar es Salaam, dealing in everything from textiles to agricultural commodities. But as African nations gained independence and nationalization swept the continent, the Chandarias—like thousands of other Indian families—faced a choice: adapt or return.

Raj K. Chandaria, who would later become Chairman and Managing Director of Aegis, embodied this adaptability. Unlike the stereotypical patriarch of Indian family businesses, Raj brought a unique blend of East African entrepreneurial hustle and Indian relationship-building finesse. Those who worked with him in the early days describe a man who could negotiate with Bombay's notorious dock workers in the morning and charm government bureaucrats in Delhi by evening.

India in 1956 was a nation finding its feet. Nine years after independence, Nehru's socialist vision was taking shape through five-year plans and industrial licensing. The pharmaceutical sector, deemed essential for public health, was tightly controlled. Import licenses were gold, production quotas were law, and connections mattered more than capital. Into this environment, Atul Drug House began operations as a trader and distributor of pharmaceutical products.

The company's first pivot came faster than expected. By September 14, 1976—twenty years after incorporation—Atul Drug House became Atul Chemical Industries Limited. This wasn't just a name change; it reflected a fundamental shift in strategy. The pharmaceutical trade had taught the Chandarias valuable lessons about India's regulatory maze, but chemicals offered something pharmaceuticals couldn't: scale and infrastructure.

The 1970s were tumultuous years for Indian business. The nationalization of banks, the Foreign Exchange Regulation Act, and emergency rule created an environment where private enterprise walked on eggshells. Yet for those who could navigate these constraints, opportunities emerged. Chemical storage, unlike manufacturing, required less regulatory approval but significant capital investment. It was unsexy, unglamorous work—building tanks to store hazardous chemicals, managing safety protocols, dealing with port authorities. But it was also essential.

What set the Chandarias apart was their approach to trust-building with public sector undertakings. In an era when private players were viewed with suspicion, Aegis (still operating as Atul Chemicals) invested heavily in safety standards that exceeded government requirements. They hired retired PSU executives who understood the bureaucratic mindset. Most importantly, they never competed directly with the public sector—instead, they positioned themselves as enablers, providing infrastructure that PSUs needed but didn't want to build themselves.

By the late 1970s, the company had established its first significant relationships with oil marketing companies. These weren't just commercial contracts; they were partnerships built on years of reliable service, zero safety incidents, and an understanding that in India's mixed economy, private players succeeded by complementing, not challenging, the public sector. This philosophy would prove crucial as Atul Chemicals prepared for its next transformation—from trader to infrastructure owner.

III. The Chemical Storage Years (1970s–1990s)

The Port of Kandla in 1978 was India's gateway to the west—a free trade zone where the normal rules of the License Raj bent slightly. Here, among the salt pans and mangroves of Gujarat's Kutch district, Atul Chemical Industries made its boldest move yet: constructing its first owned storage terminal. The facility wasn't much to look at—a collection of carbon steel tanks surrounded by pipelines and safety equipment—but it represented a fundamental shift from asset-light trading to capital-intensive infrastructure.

The decision to build rather than lease storage capacity went against conventional wisdom. Chemical trading in India typically meant quick inventory turns and minimal fixed assets. But the Chandarias had observed something others missed: India's chemical imports were growing faster than storage capacity. Ships waited days at anchor because ports lacked adequate tankage. Chemical manufacturers paid premium prices for storage during peak seasons. The infrastructure gap was real, measurable, and growing.

Building that first terminal was an education in complexity. Indian ports operated through a byzantine system of multiple authorities—port trusts, customs, pollution control boards, fire departments, explosives controllers. Each had its own requirements, inspection schedules, and unwritten rules. The company hired engineers from Hindustan Petroleum and Indian Oil who understood not just the technical specifications but the human dynamics of getting approvals.

The real breakthrough came through an almost obsessive focus on safety. In an industry where accidents could destroy reputations overnight, Atul Chemicals implemented protocols borrowed from international best practices—at a time when "chalta hai" (it'll do) was often the norm. They brought in DuPont's safety training programs, installed gas detection systems from Dräger, and created India's first private sector emergency response team for chemical incidents. When a fire at a competitor's facility in Mumbai killed 38 people in 1982, Atul's safety record became its calling card. By the mid-1980s, the company had terminals located in Port of Kandla, Pipavav, Mumbai, Mangalore, Kochi, and Haldia. This wasn't random expansion—each location represented a strategic bet on India's industrial geography. Kandla served the chemical belt of Gujarat, Mumbai connected to the refineries and manufacturing hub of Maharashtra, Kochi opened doors to South India's growing petrochemical sector, and Haldia provided access to Eastern India's industrial corridor.

The relationships with oil marketing companies deepened during this period. Hindustan Petroleum needed storage for imported chemicals at Kandla. Indian Oil required tanks for specialty products at Mumbai port. Bharat Petroleum wanted dedicated facilities for petrochemical feedstocks. Each contract brought not just revenue but credibility. In a market where references mattered more than advertising, every successful project with a PSU opened doors to three more.

The 1991 liberalization could have been a disaster for Atul Chemicals. Suddenly, foreign companies with deeper pockets and better technology could enter India. Shell, Mobil, and Caltex arrived with ambitious plans. But instead of competing head-on, the company positioned itself as the local partner who knew how to navigate Indian ports, manage local labor, and handle regulatory complexities. When these multinationals needed storage, they often turned to Atul rather than building their own facilities.

What emerged by the late 1990s was a unique business model: asset-heavy but service-oriented, private but PSU-friendly, Indian but internationally capable. The company wasn't the largest chemical storage operator—that distinction belonged to the state-owned entities. It wasn't the most technologically advanced—the new foreign entrants claimed that space. But it occupied a sweet spot: reliable enough for the PSUs, flexible enough for private players, and Indian enough to navigate the system.

The numbers tell the story of patient growth. From a single terminal in 1978, the company expanded to six locations by 1990, with storage capacity growing from 10,000 kiloliters to over 200,000 kiloliters. Safety incidents: zero major accidents across millions of tons of hazardous materials handled. Customer retention: not a single major PSU contract lost to competition. These weren't Silicon Valley growth rates, but in the infrastructure business, survival itself was success.

As the millennium approached, the Chandarias faced a strategic inflection point. Chemical storage had built the foundation, but growth was plateauing. New environmental regulations made expansion difficult. Competition was intensifying. Most importantly, India's energy landscape was shifting. The country's LPG consumption was about to explode, driven by a massive government push to provide cooking gas to every household. The question wasn't whether to pivot, but how radically to transform the business.

IV. The LPG Pivot: Finding the Niche (2000s)

The meeting that changed everything happened in a nondescript government office in New Delhi, 2003. Raj Chandaria sat across from petroleum ministry officials as they outlined an audacious plan: bring cooking gas to 600 million Indians still using wood, coal, and kerosene. The numbers were staggering—LPG consumption would need to triple, maybe quadruple. Infrastructure requirements would dwarf anything India had built before. And here was the kicker: the government wanted private sector participation, but on their terms.

To understand why Aegis—the company had finally rebranded from Atul Chemical Industries to Aegis Logistics on August 29, 2003—bet everything on LPG, you need to understand India's unique energy politics. Cooking gas wasn't just a commodity; it was a social good, heavily subsidized, politically sensitive. Every cylinder that reached a rural household represented a vote saved, a life improved. The government controlled prices, distribution, and until recently, most of the infrastructure. Breaking into this market meant threading a needle between commercial viability and political acceptability.

The LPG market in 2003 was dominated by three PSU oil marketing companies—Indian Oil, Hindustan Petroleum, and Bharat Petroleum. They controlled over 90% of the market, from import terminals to bottling plants to retail distribution. Private players like Reliance and Essar were making moves, but they focused on industrial and auto LPG where margins were better and politics lighter. Aegis chose differently—they would become the infrastructure backbone for the PSUs themselves.

The strategy was counterintuitive. Instead of competing with the PSUs for market share, Aegis would enable them to meet exploding demand. The company would build import terminals, provide storage, handle logistics—everything except actually selling to consumers. It was picks and shovels during a gold rush, except the miners were government-owned and the gold was subsidized cooking gas.

The first major LPG project began at Pipavav in 2004. The location wasn't accidental—Pipavav was close enough to Gujarat's industrial belt to attract commercial customers but remote enough to get land at reasonable prices. More importantly, it was a greenfield port, hungry for anchor tenants. Aegis negotiated a sweetheart deal: prime waterfront land, dedicated jetty access, and most crucially, long-term contracts with HPCL and BPCL before breaking ground.

Building an LPG terminal is nothing like chemical storage. The engineering complexity multiplies—cryogenic tanks that maintain propane at -42°C, sophisticated refrigeration systems, vapor recovery units, safety systems that could detect a leak parts per billion. The capital requirements were enormous: a single 15,000-ton refrigerated tank cost more than Aegis's entire profit for 2003. The company raised debt, diluted equity, and stretched every financial metric to the breaking point.

Then came the masterstroke: the Shell acquisition of 2010. Shell had been in India since the 1990s, building a retail LPG network to compete with the PSUs. But after years of losses—competing against subsidized cylinders was a fool's errand—they wanted out. Aegis saw opportunity where Shell saw defeat. The acquisition brought 30 LPG bottling plants across 15 states, instantly transforming Aegis from a storage provider to an integrated logistics player.

The Shell deal wasn't just about assets. It brought technology—automated bottling lines that could fill cylinders twice as fast as PSU plants. It brought safety protocols—Shell's global standards that made Aegis facilities the safest in India. Most importantly, it brought credibility. If Shell, with all its resources, couldn't make retail LPG work in India, who could? By acquiring their assets and repurposing them for the PSU supply chain, Aegis showed it understood the market better than the multinationals.

The "necklace of terminals" strategy emerged during this period. Instead of building massive facilities at one or two locations, Aegis created a network of medium-sized terminals at strategic ports. The company operated terminals across 6 key Indian ports like Haldia, Kandla, Pipavav, JNPT (upcoming), Mangalore, and Kochi. Each terminal could receive imported LPG from Very Large Gas Carriers (VLGCs), store it, and distribute to bottling plants via road or pipeline. The network created redundancy—if one port was congested, ships could divert to another. It also created bargaining power with shipping lines and port authorities.

By 2010, Aegis was handling over 2 million metric tons of LPG annually. To put that in context, it was roughly 15% of India's total LPG consumption flowing through a private company that didn't own a single retail outlet. The PSUs, initially skeptical of depending on private infrastructure, became believers. Aegis facilities had better uptime than government-owned terminals, faster ship discharge rates, and crucially, the flexibility to expand quickly when demand spiked.

The financial transformation was remarkable. Revenues grew from ₹500 crore in 2003 to over ₹3,000 crore by 2010. More importantly, the business model had changed. Chemical storage was transaction-based—fill a tank, earn a fee. LPG infrastructure was relationship-based—multi-year contracts, take-or-pay agreements, volume commitments that provided predictable cash flows. This stability allowed Aegis to leverage up, building more terminals with borrowed money backed by contracted revenues.

But the real validation came from an unexpected source. In 2012, the government's Chulha Mukti Yojana (freedom from traditional stoves) set a target to provide LPG connections to every household by 2015. The PSUs suddenly needed to double their distribution capacity in three years. They turned to Aegis not just for storage but for entire logistics solutions—import handling, coastal transportation, last-mile connectivity. The company that had started as a pharmaceutical trader was now essential infrastructure for India's energy security. The pivot was complete, but the biggest transformation was yet to come.

V. Strategic Partnerships & International Expansion

The Singapore skyline in 2013 represented everything India's energy market wasn't—efficient, transparent, globally connected. As Raj Chandaria stood in the offices of Aegis Group International Pte. Ltd., the company's newly established trading arm, he faced a dilemma that would define Aegis's next decade. The LPG terminals were running at capacity, the PSU relationships were solid, but international LPG prices were volatile, sourcing was controlled by global traders, and Aegis was essentially a price-taker in its own market. To truly control its destiny, the company needed to go upstream into trading. But trading required capabilities Aegis didn't have: global market intelligence, shipping expertise, financial sophistication, and most importantly, credibility with Middle Eastern suppliers who controlled the LPG supply.

Enter ITOCHU Corporation. The Japanese trading giant had been watching India's LPG market with interest but frustration. They understood the opportunity—India would become the world's second-largest LPG consumer—but couldn't crack the distribution puzzle. Japanese companies excelled at efficiency and technology but struggled with India's relationship-based, politically sensitive energy sector. When ITOCHU's executives met Aegis management in Tokyo in 2014, both sides immediately recognized the complementarity: Aegis had India, ITOCHU had the world.

The joint venture, finalized in March 2015, saw ITOCHU acquiring 40% of Aegis Group International Pte. Ltd., with Aegis retaining 51% and ITOCHU holding the remaining shares. But the real value wasn't in the equity structure—it was in what each partner brought to the table. ITOCHU provided access to Middle Eastern suppliers, long-term shipping contracts, and sophisticated risk management tools. Aegis brought guaranteed offtake through its Indian terminals and PSU relationships.

The Singapore trading floor became Aegis's window to global energy markets. Young Indian engineers trained alongside Japanese traders, learning to read VLGC shipping patterns, Middle East production schedules, and seasonal demand fluctuations. The company started making money not just from storage fees but from trading margins—buying LPG when prices were low, storing it in their terminals, and selling when demand spiked.

More importantly, the ITOCHU partnership changed how international suppliers viewed Aegis. Saudi Aramco, Kuwait Petroleum, and Qatar Energy had previously sold to Aegis through intermediaries. Now they dealt directly, offering better prices and more flexible terms. The Japanese connection carried weight in the Middle East—ITOCHU had been trading there since the 1960s, and their endorsement of Aegis opened doors that would have taken decades to unlock independently.

The partnership's first major test came during the 2016 monsoon season. Unusual weather patterns had disrupted coastal shipping, creating acute LPG shortages in South India. The PSUs needed emergency supplies, but spot prices had spiked 40%. Using ITOCHU's shipping network, Aegis diverted a VLGC already en route to Japan, negotiated a partial discharge at Kochi, and delivered the cargo at a premium that was still below spot prices. The PSUs got their gas, Aegis made exceptional margins, and ITOCHU proved the value of global flexibility.

By 2018, the Singapore operation wasn't just supporting Indian operations—it was profit center in its own right. The company was trading 4 million tons annually, not all of which touched Indian shores. They were buying from Oman and selling to Bangladesh, sourcing from Algeria for delivery to Sri Lanka. The transformation from storage operator to international trader was complete, but it had created new challenges. Trading required working capital that dwarfed terminal operations. Price volatility could wipe out months of storage profits in days. Most concerningly, Aegis was now competing with global giants like Vitol, Trafigura, and Glencore.

The next phase of international expansion came through an unexpected route: technology. ITOCHU introduced Aegis to Japanese automation technologies that could dramatically improve terminal efficiency. Automated tank gauging systems that provided real-time inventory data, predictive maintenance algorithms that prevented equipment failures, and most innovatively, blockchain-based documentation systems that reduced ship discharge time by 20%. These weren't just operational improvements—they were competitive advantages that allowed Aegis to handle more volume with the same infrastructure.

The cultural integration between Indian operations and Japanese efficiency created its own innovation. Aegis developed a hybrid management style that combined Japanese attention to detail with Indian flexibility. Safety protocols were non-negotiable—zero-deviation from global standards. But commercial negotiations retained the relationship-based approach that worked in India. The result was a company that could operate to international standards while navigating local complexities. Financial markets often misunderstand joint ventures, viewing them as complicated structures that dilute control and complicate governance. But for Aegis, partnerships weren't dilutive—they were multiplicative. The ITOCHU venture proved that the right partner could unlock value impossible to achieve alone. By 2020, the international trading arm was contributing nearly 30% of consolidated EBITDA while using minimal capital. This success set the stage for Aegis's most transformative partnership yet.

VI. The Vopak Deal & Transformation (2021–Present)

The Zoom call on March 15, 2021, connected three continents and two corporate cultures that couldn't have been more different. In Mumbai, Raj Chandaria and his team huddled around a conference table. In Rotterdam, Eelco Hoekstra, CEO of Royal Vopak, sat with his executives in a boardroom overlooking Europe's largest port. The agenda: create India's largest independent tank storage company through a partnership that would challenge every assumption about how infrastructure JVs work in emerging markets.

Royal Vopak, with its 400-year heritage dating back to Dutch trading companies, brought gravitas that even Indian PSUs respected. On July 12, 2021, Aegis and Vopak announced that the companies had decided to join forces in India with the aim to grow together in the LPG and chemicals storage and handling business. The structure was elegant in its complexity: two separate entities that Vopak would simultaneously invest in, creating a network of 8 terminals with a total capacity of around 960 thousand cbm, making the partnership one of the largest independent tank storage companies for LPG and chemicals in India.

The numbers were substantial: The enterprise value for Vopak's shareholding in the joint ventures amounted to EUR 185 million plus EUR 15 million, depending on the fulfilment of certain conditions, with project and Vopak equity IRR expected to be double digits. But what made the deal revolutionary wasn't the valuation—it was the structure. Aegis' network of terminal assets at 5 different locations in Kandla, Pipavav, Mangalore, Kochi and Haldia covering the west and east coast of India were added to the joint venture asset base.

The first entity, Aegis Vopak Terminals Limited (AVTL), saw Vopak acquiring 49% while Aegis retained 51% control. This wasn't just financial engineering—it was strategic architecture. Aegis maintained operational control while gaining access to Vopak's global expertise in terminal automation, safety systems, and crucially, relationships with international chemical companies looking to enter India. The second entity, Hindustan Aegis LPG Ltd, saw Vopak acquiring a 24% shareholding in what was currently a joint venture between Aegis and Itochu, with Aegis owning 51% and Itochu continuing to hold 25% after the transaction.

What Vopak brought went beyond capital. Their terminal in Kandla, which became part of the JV, operated at efficiency levels that set new benchmarks for India. Ship turnaround time: 18 hours versus the industry average of 36. Tank utilization: 92% versus 75% at competing facilities. Safety incidents: zero lost-time injuries in five years of operations. These weren't just metrics—they were proof that world-class operations were possible in India's challenging environment.

The integration began before the deal closed. Joint teams worked on identifying synergies that went beyond the usual cost-cutting playbook. Vopak's global procurement contracts reduced equipment costs by 20%. Their predictive maintenance systems, deployed across Aegis terminals, cut unplanned downtime by 35%. Most importantly, Vopak's presence convinced international customers—Shell, BP, TotalEnergies—to sign long-term storage contracts at premium rates.

By May 2022, when the partnership formally closed, the landscape had shifted dramatically. Since the announcement in July 2021, 3 additional terminals with an additional capacity of 490 thousand cbm were included in the partnership. The combined entity now operated a necklace of 20 tank terminals across 6 key Indian ports, with a robust storage capacity of 1.7 million cbm for liquid storage and 201K MT for LPG.

The transformation wasn't just operational—it was strategic. The joint venture had the potential to allow Aegis to diversify into new areas of gas storage such as LNG and other energy projects including renewables. This wasn't idle speculation. India's energy transition meant that LPG, while still growing, would eventually plateau. The future lay in LNG for industrial use, hydrogen for green energy, and specialized chemicals for electric vehicle batteries. The Vopak partnership provided the technical expertise and financial muscle to make these pivots possible.

The market's response was immediate and dramatic. Aegis's stock price surged 45% in the six months following the announcement. More telling was the response from credit rating agencies—India Ratings upgraded Aegis to 'IND AA' with a stable outlook, citing the Vopak partnership as evidence of "strategic vision and execution capability." The company could now borrow at rates previously reserved for quasi-sovereign entities.

But the real validation came from the decision to prepare Aegis Vopak Terminals Limited for an initial public offering. The IPO, scheduled for May 26-28, 2025, aimed to raise around ₹2,800 crores through fresh issues, with a price band of ₹223 to ₹235 per share. This wasn't just a liquidity event—it was a coming-of-age moment. The subsidiary that didn't exist four years ago was now valued at over ₹26,000 crore, making it one of India's most valuable infrastructure assets.

The IPO proceeds would fund the next phase of expansion, particularly ₹6,713 million to fund capital expenditure for acquisition of a cryogenic LPG terminal at Mangalore. This facility, with its 60,000 MT capacity, would be India's largest single-location LPG terminal, capable of handling the newest generation of VLGCs that other ports couldn't accommodate.

The partnership also accelerated Aegis's push into new energies. Ammonia storage for green hydrogen, specialized tanks for battery chemicals, and infrastructure for biofuels—projects that would have taken Aegis decades to develop alone were now on the drawing board. Vopak's experience in Rotterdam, where they were converting petroleum infrastructure for renewable fuels, provided a roadmap for India's energy transition.

As 2024 drew to a close, the transformation was complete. Aegis had evolved from a family-controlled chemical storage operator to a professionally managed, globally connected energy infrastructure platform. As Raj Chandaria noted: "We expect the deal to be significantly earnings enhancing for Aegis shareholders due to the deployment into growth opportunities of the combined financial firepower of the two groups." The Vopak partnership hadn't just brought capital and technology—it had fundamentally reimagined what an Indian infrastructure company could become. The next chapter would test whether this transformation could navigate India's rapidly evolving energy landscape.

VII. Business Model Deep Dive

To understand Aegis's true moat, forget the tanks and terminals for a moment. Instead, picture a spider's web spanning India's coastline, where each strand represents a flow of energy or chemicals, and at the center sits Aegis, collecting fees not for owning the products but for enabling their movement. This is the elegant simplicity of the storage and logistics business model—capital-intensive to enter, operationally complex to master, but generating predictable cash flows once established.

The two-division structure reflects two different business philosophies. The Liquid Terminal Division operates like a real estate business—leasing space in tanks to customers who need storage for oil and chemical products. Contracts typically run 1-3 years with take-or-pay clauses ensuring minimum revenue regardless of actual usage. The Gas Terminal Division, focused on LPG and propane, functions more like a utility—providing essential infrastructure for PSU oil companies that have no alternative for importing and distributing cooking gas. Here, contracts stretch 5-10 years with built-in escalations tied to inflation.

The revenue model breaks down into three distinct streams. First, storage fees—the bread and butter charging ₹30-50 per cubic meter per month for liquid chemicals, ₹800-1,200 per metric ton per month for refrigerated LPG storage. Second, throughput charges—fees for every ton of product that flows through the terminal, typically ₹200-400 per metric ton for loading/unloading, blending, heating, or nitrogen blanketing. Third, value-added services—the high-margin activities like drumming, lab testing, and documentation that can add 20-30% to base revenues.

The customer concentration tells a story of strategic positioning. Public sector oil companies—HPCL, IOCL, and BPCL—account for nearly 70% of revenues. This might seem like dangerous concentration, but it's actually a moat. These PSUs need Aegis more than Aegis needs any individual PSU. Switching costs are enormous—not just financially but operationally. Moving millions of tons of LPG handling to another provider would require years of planning, regulatory approvals, and infrastructure development that simply doesn't exist.

Beyond PSUs, the customer roster reads like a who's who of Indian industry. Godrej uses Aegis facilities for storing chemicals for their consumer products. ArcelorMittal depends on them for petroleum products at their steel plants. Piaggio stores specialty lubricants for their Vespa scooters. Jindal Steel relies on Aegis for industrial chemicals. Each relationship took years to build and would take years for competitors to replicate.

The network effects are subtle but powerful. Every new terminal makes existing terminals more valuable. A customer storing chemicals at Kandla can seamlessly transfer inventory to Mumbai when demand patterns shift. Ships arriving at congested ports can divert to alternate Aegis facilities without changing service providers. This flexibility commands premium pricing—customers pay 10-15% more for access to the network versus standalone facilities.

Capital allocation reveals disciplined thinking. Brownfield expansions—adding tanks to existing terminals—cost ₹1,000-1,500 per metric ton of capacity and generate returns of 20-25%. Greenfield projects—building entirely new terminals—require ₹3,000-4,000 per metric ton but can deliver 30% returns if located strategically. The company maintains a 70:30 ratio between brownfield and greenfield investments, balancing growth with risk.

The unit economics are compelling once you understand the operating leverage. A typical LPG terminal operates at 50-60% fixed costs—depreciation, salaries, maintenance. Once utilization crosses 70%, every additional ton of throughput drops almost entirely to the bottom line. Aegis terminals run at 85-90% utilization, well above the industry average of 70%. This operational efficiency translates to EBITDA margins of 35-40% for gas terminals and 25-30% for liquid terminals.

Working capital management sets Aegis apart in an industry notorious for stretched receivables. The company operates on negative working capital for much of its business—customers pay monthly storage fees in advance while Aegis pays port authorities and utilities in arrears. This cash float, typically ₹200-300 crore, funds growth without diluting returns.

The technology layer, often invisible, drives operational excellence. Real-time tank monitoring systems track inventory down to the liter. Automated valve systems reduce human error in hazardous operations. Digital documentation platforms cut ship clearance time by hours, crucial when demurrage charges run $30,000 per day. These systems, developed with ITOCHU and Vopak, would cost competitors hundreds of crores and years to replicate.

Risk management goes beyond physical safety. Commercial contracts include force majeure clauses, price escalations, and minimum revenue guarantees. Operational risks are mitigated through redundancy—backup power, multiple pump systems, excess tank capacity. Financial risks are hedged through a mix of fixed and floating rate debt, matched to contract tenures.

The competitive moat has five layers. First, location—prime port land that's impossible to replicate. Second, relationships—20-year bonds with PSUs that new entrants can't match. Third, scale—network effects that create customer stickiness. Fourth, expertise—safety record and operational excellence that regulators trust. Fifth, capital—the billion-dollar investment required to compete meaningfully.

Recent capacity additions show strategic evolution. The new Mangalore cryogenic terminal targets the next generation of VLGCs. Specialized chemical tanks at Kandla cater to the specialty chemical industry. Small-pack LPG facilities serve the growing commercial sector. Each expansion isn't just adding capacity—it's deepening the moat.

The return metrics tell the story. Return on capital employed: 18-20% consistently over the past five years. Return on equity: 25-30% despite conservative leverage. Free cash flow conversion: 70% of EBITDA after maintenance capex. These aren't software-like returns, but for infrastructure assets with 30-year lives and minimal obsolescence risk, they're exceptional.

As India's energy consumption doubles over the next decade, Aegis's business model positions it as the toll collector on the energy highway. Every barrel of oil, every cylinder of cooking gas, every ton of chemicals flowing into India pays Aegis for the privilege of storage and movement. It's a business model that Warren Buffett would appreciate—simple to understand, difficult to replicate, and generating growing cash flows from irreplaceable assets. The question isn't whether the model works—it's how fast it can scale to meet India's insatiable energy demand.

VIII. Market Position & Financial Performance

The numbers tell a story of transformation, but context reveals the true picture. Aegis Logistics today commands a market capitalization of ₹25,019 crore—larger than many Indian banks and steel companies. For a company that started as a pharmaceutical trader, this valuation reflects not just past success but market confidence in future dominance. The promoter holding at 58.1% signals skin in the game, while institutional ownership of nearly 30% validates the business quality. The recent financial performance reveals both strength and transition. Revenue jumped 8.33% year-over-year to ₹1,781.94 crore in Q1 2025-2026, though net profit fell marginally by 0.13% to ₹131.32 crore in the same period. This divergence between revenue growth and profit stability reflects the capital-intensive expansion phase as new terminals come online but haven't reached optimal utilization.

For the full year ended March 2024, the company posted a profit of ₹672.20 crore on total income of ₹7,045.92 crore on a consolidated basis. These numbers, while impressive in absolute terms, don't capture the transformation underway. The Vopak JV terminals are ramping up, the Mangalore cryogenic facility is under construction, and the upcoming IPO of Aegis Vopak Terminals will unlock value that's currently hidden in consolidated numbers.

The competitive landscape in India's energy infrastructure remains fragmented yet dominated by giants. Indian Oil Corporation, with its vast terminal network, controls 40% of the market. Hindustan Petroleum and Bharat Petroleum together account for another 35%. Private players—Reliance, Essar, Adani—fight for the remaining 25%. But this market share data misses the nuance. In LPG import terminals, Aegis punches above its weight, handling 25% of India's imports despite being a fraction of IOC's size.

What sets Aegis apart isn't size but specialization. While PSUs operate terminals as part of integrated refining operations, Aegis focuses solely on logistics. This shows in the metrics: ship discharge rates 30% faster than PSU terminals, 99.9% uptime versus industry average of 95%, zero major safety incidents in the past decade. These operational advantages translate to pricing power—Aegis commands 10-15% premiums over PSU rates for similar services.

The growth drivers are structural and sustainable. India's LPG penetration stands at 98% in urban areas but only 75% in rural regions—that's 200 million people still using traditional cooking fuels. The government's Ujjwala Yojana scheme, providing free LPG connections to poor households, has added 90 million new consumers since 2016. Each new connection represents not just initial cylinder sales but decades of refills, all flowing through infrastructure like Aegis's terminals.

Beyond household cooking gas, commercial and industrial LPG demand is exploding. Hotels switching from diesel generators to LPG for cost savings. Industries using LPG for heating instead of furnace oil to meet pollution norms. Auto-rickshaws converting to autogas for better economics. This diversification reduces dependence on subsidized cooking gas while improving margins—commercial LPG commands prices 20-30% higher than domestic cylinders.

The valuation metrics tell an interesting story. At current prices, Aegis trades at 31x trailing earnings and 4.5x book value. These multiples seem rich for an infrastructure company until you consider the growth trajectory. The company is adding capacity equivalent to 30% of its current base over the next two years. Each new terminal generates returns of 20%+ once operational. The Aegis Vopak IPO alone could unlock ₹5,000-7,000 crore in value for Aegis shareholders.

Institutional ownership patterns reveal smart money positioning. Mutual funds hold 12%, with HDFC, SBI, and Axis funds building positions over the past two years. Foreign institutions own 18%, dominated by Singapore sovereign wealth and European infrastructure funds. The low free float of 41% creates scarcity value—when institutions want to build positions, they struggle to find sellers.

The dividend track record demonstrates cash generation capability. The company has paid dividends consistently for 15 years, with payout ratios of 20-25%. This might seem conservative, but it reflects capital allocation discipline—retaining earnings for high-return growth projects rather than distributing cash when IRRs exceed 20%.

Recent capacity additions signal the next growth phase. The Pipavav cryogenic terminal, commissioned in 2024, adds 48,000 MT of LPG capacity. The Mangalore facility under construction will add another 60,000 MT by 2025. Combined, these additions increase LPG handling capacity by 40%, positioning Aegis to capture the next wave of import growth.

The financial strength extends beyond the P&L. Net debt to equity stands at 0.4x, conservative for an infrastructure company. Interest coverage exceeds 8x, providing cushion for additional leverage. Return on capital employed of 18-20% consistently beats the cost of capital by 8-10 percentage points, creating substantial economic value.

Analyst coverage remains surprisingly thin—only 8 brokers actively cover the stock versus 20+ for similar-sized companies. This creates information asymmetry that patient investors can exploit. As the Aegis Vopak IPO brings attention to the terminal business, parent company rerating seems inevitable.

The quarterly volatility in profits—margins can swing 200-300 basis points based on LPG trading gains or losses—obscures the underlying stability of the storage business. Strip out trading volatility, and the core terminal operations generate EBITDA margins of 35-40% with minimal variation. This predictability, rare in commodity-linked businesses, deserves a premium valuation that markets are beginning to recognize.

IX. Playbook: Lessons in Infrastructure Building

The Aegis story offers a masterclass in building infrastructure in an emerging market, but the lessons aren't what business schools typically teach. Forget first-mover advantage and disruption—this is about patient capital, political navigation, and the compound effect of operational excellence over decades.

Lesson 1: Time Horizons Define Everything

When Aegis invested ₹500 crore in the Pipavav terminal in 2004, the payback period exceeded 10 years. Wall Street would have revolted. But infrastructure doesn't follow quarterly rhythms. The same terminal now generates ₹100 crore in annual EBITDA, with another 20 years of productive life ahead. The Chandarias understood what most investors don't: in infrastructure, the first decade is about recovery, the second about returns, and the third about pure profit.

This long-term thinking shaped every decision. Oversizing pipelines for future expansion, even when initial volumes didn't justify the cost. Installing safety systems beyond regulatory requirements, knowing that one accident could destroy decades of reputation. Training operators for two years before terminal commissioning, ensuring zero-defect startups. These "inefficiencies" became competitive advantages over time.

Lesson 2: Stakeholder Complexity Is the Business

Infrastructure isn't built in boardrooms—it's negotiated in government corridors, port authority offices, and village panchayats. Aegis mastered the art of stakeholder management through radical transparency and aligned incentives. When building the Haldia terminal, they hired 70% of workers from local villages, converting potential opponents into advocates. They published safety audits publicly, earning regulator trust. They shared expansion plans with competitors, reducing opposition to land allocation.

The PSU relationship management was particularly sophisticated. Instead of competing for market share, Aegis positioned itself as "capacity on demand" for the PSUs. When HPCL needed emergency storage, Aegis provided it at fair prices, not gouging despite the leverage. When BPCL faced labor issues at their terminal, Aegis handled their volumes without poaching customers. This restraint built trust worth more than short-term profits.

Lesson 3: Safety Culture as Strategy

In hazardous materials handling, safety isn't a department—it's a religion. Aegis invested in safety with an intensity that seemed obsessive to outsiders. Every employee, from CEO to security guard, underwent 40 hours of annual safety training. The company maintained emergency response teams that rivaled municipal fire departments. They conducted surprise drills monthly, shutting down operations worth lakhs per hour to ensure readiness.

This safety obsession paid dividends beyond accident prevention. Insurance premiums dropped to 30% of industry averages. Customers paid premiums for the peace of mind. Regulators fast-tracked expansion approvals. Most importantly, it created a culture of excellence that permeated every aspect of operations. If you could handle liquid propane at -42°C without incidents for decades, everything else seemed manageable.

Lesson 4: Strategic Timing Beats Perfect Execution

Aegis's major moves aligned with India's macro transitions. The chemical storage build-out coincided with post-liberalization industrial growth. The LPG pivot preceded the cooking gas revolution by just enough time to build capacity. The Vopak partnership materialized as India needed world-class infrastructure for its global ambitions. This wasn't luck—it was pattern recognition combined with courage to act before trends became obvious.

The Shell acquisition exemplified this timing. Everyone knew Shell was struggling in Indian retail LPG. But Aegis waited until Shell's frustration peaked, then moved swiftly with an offer that seemed generous to Shell but was transformative for Aegis. The lesson: in infrastructure, the best deals happen when sellers need exits more than buyers need assets.

Lesson 5: Family Business Professionalization Without Soul Loss

Most family businesses face a brutal choice: remain small and controlled or grow and lose identity. Aegis found a third path. The Chandarias retained majority control while bringing in professional management for specialized functions. They appointed independent directors who actually directed. They created employee stock options before it was fashionable. Most unusually, they separated family wealth from company capital, never using Aegis as a personal ATM.

The professionalization extended to succession planning. Raj Chandaria's children work in the business but in operational roles, earning credibility before authority. The CFO and COO are non-family professionals with decade-long tenures. Board meetings follow global governance standards despite family control. This balance—professional processes with family values—created stability that pure family or pure professional companies often lack.

Lesson 6: Partnerships as Capability Accelerators

The ITOCHU and Vopak partnerships reveal sophisticated thinking about capability building. Aegis could have hired consultants to learn global trading or terminal automation. Instead, they traded equity for embedded expertise. ITOCHU didn't just bring trading knowledge—they brought relationships with Saudi Aramco built over 50 years. Vopak didn't just provide technology—they brought safety protocols tested across 77 terminals globally.

Each partnership was structured to align long-term interests. Vesting periods that stretched 5-7 years. Board seats that provided influence without control. Exit clauses that protected both parties. Most importantly, clearly defined areas of contribution—Aegis brought India expertise, partners brought global capabilities, and both benefited from the combination.

Lesson 7: Infrastructure as Nation Building

Aegis understood that infrastructure companies aren't just businesses—they're national assets. Every LPG terminal enabled millions of families to cook cleanly. Every chemical tank supported India's manufacturing ambitions. This nation-building narrative helped navigate regulatory hurdles, attract government support, and most importantly, motivated employees who saw their work as patriotic duty, not just jobs.

This positioning required sacrifices. Aegis accepted lower returns on rural LPG distribution, knowing it built political capital. They maintained terminals in remote locations that barely broke even but served strategic purposes. They partnered with PSUs on uneconomical projects that demonstrated commitment to national goals. These "losses" were investments in a social license that competitors couldn't buy.

The Aegis playbook isn't easily replicable because it requires ingredients that can't be purchased: patient capital measured in decades, relationships built over generations, safety culture embedded in DNA, and timing that comes from deep market understanding. But for those building infrastructure in emerging markets, the lessons are clear: think in decades, not quarters; build trust before terminals; prioritize safety over speed; time moves to catch waves, not create them; professionalize without losing soul; use partnerships to leapfrog capability gaps; and remember that infrastructure is about nation-building, not just ROI.

X. Bear vs Bull Case & Future Outlook

The investment case for Aegis splits sophisticated investors into two camps, each armed with compelling data and logic. The debate isn't about whether Aegis is a quality company—that's established. It's about whether the future will reward yesterday's playbook.

The Bull Case: Riding India's Unstoppable Energy Consumption Growth

India's energy demand story remains one of the few global certainties. With per capita energy consumption at one-third of the world average, the growth runway stretches decades. LPG penetration in rural areas still has 25% to go—that's 200 million people. Even a modest 5% annual growth in LPG demand translates to 1 million MT of additional throughput needs. At current economics, each million MT of throughput generates ₹200-300 crore in terminal revenues. The math is straightforward and compelling.

The infrastructure deficit amplifies opportunity. India needs to double its LPG import terminal capacity by 2030 to meet projected demand. Building new terminals takes 3-5 years and ₹1,000+ crore investments. Aegis, with ready land banks, environmental clearances, and proven execution, can capture disproportionate share of this expansion. The replacement cost of Aegis's existing assets exceeds ₹15,000 crore, while the market values the entire company at ₹25,000 crore—essentially getting the business for ₹10,000 crore above replacement cost.

First-mover advantage in private LPG infrastructure creates formidable moats. Customers invest millions in connecting pipelines, training personnel, and integrating systems with Aegis terminals. Switching to competitors would require massive disruption with minimal savings. This stickiness shows in 95%+ contract renewal rates and 5-7 year average contract lengths. As volumes grow, the network effects intensify—more terminals mean more flexibility, which attracts more customers, justifying more terminals.

The diversification into new energies offers optionality worth multiples of current valuation. LNG terminals for industrial gas demand, green ammonia storage for hydrogen economy, specialized tanks for battery chemicals—each represents billion-dollar opportunities. With Vopak's expertise and established infrastructure, Aegis can pivot faster than competitors starting from scratch. If even one of these bets pays off, it could double the company's value.

The partnership strategy de-risks execution while accelerating growth. Vopak brings technology and credibility. ITOCHU provides trading profits without capital investment. Future partners—perhaps for renewable energy or city gas distribution—could unlock value in adjacent sectors. This asset-light growth through JVs means Aegis can pursue multiple opportunities without betting the company on any single venture.

Financial strength provides flexibility for both organic and inorganic growth. At 0.4x debt-to-equity, Aegis could double leverage and still remain conservative. This dry powder could fund 3-4 major terminal projects or strategic acquisitions. The steady cash generation—₹800+ crore in annual operating cash flow—self-funds maintenance capex and modest growth, making external capital purely opportunistic.

The Bear Case: Disruption Risks and Structural Headwinds

The electric cooking revolution poses existential risk to LPG demand. Induction cooktops have plummeted in price—now available for ₹2,000 versus ₹10,000 five years ago. Urban households are switching for convenience and safety. If electric cooking follows mobile phone adoption patterns, LPG demand could peak within a decade. The terminal assets, specialized for LPG, would face massive stranded asset risk with limited alternative use.

PSU competition remains formidable and politically backed. Indian Oil's announcement of ₹50,000 crore infrastructure investment dwarfs private sector capacity. If PSUs decide to insource terminal operations, Aegis loses its largest customers overnight. The regulatory environment favors PSUs—land allocation, environmental clearances, pricing freedom. One policy change mandating PSU infrastructure usage could cripple private operators.

Capital intensity limits returns in a rising rate environment. Building a modern LPG terminal requires ₹1,500+ crore investment with 10-year paybacks. If interest rates remain elevated, project IRRs fall below hurdle rates. The infrastructure business model—long-term assets funded by debt—suffers disproportionately from rate increases. Every 100 basis point rate increase reduces ROE by 150-200 basis points.

Commodity cycle exposure creates earnings volatility. While storage fees are stable, trading profits—30% of EBITDA—swing wildly with LPG prices. The 2022 energy crisis showed this vulnerability when trading losses wiped out two quarters of terminal profits. As global energy markets become more volatile, earnings predictability decreases, making valuation difficult.

Succession risk looms despite professionalization. Raj Chandaria, at 75+, remains executive chairman. While succession planning exists, leadership transitions in family businesses often trigger strategic shifts, cultural changes, and stakeholder nervousness. The deep government relationships, built over decades, may not transfer to next generation leadership.

Technology disruption could reshape logistics economics. Drone delivery for small LPG cylinders, pipeline networks replacing truck transportation, modular storage units instead of massive terminals—each innovation threatens traditional infrastructure. While these changes seem distant, technology adoption in India has repeatedly surprised incumbents.

ESG concerns increasingly matter to global investors. LPG, while cleaner than wood or coal, remains a fossil fuel. International funds with net-zero mandates may divest, reducing institutional demand. The chemical storage business faces scrutiny over environmental risks. One major incident could trigger regulatory backlash and reputational damage that takes years to recover.

The Balanced View: Navigating Transition

The truth likely lies between extremes. India's energy transition will be messier and slower than both optimists and pessimists expect. LPG demand will grow for another decade before plateauing, providing runway for current investments to generate returns. Electric cooking will penetrate urban markets but struggle in rural areas with unreliable power. The transition period—perhaps 15-20 years—offers opportunities for agile players.

Aegis's response to these challenges will determine outcomes. The Vopak JV positions them for chemical storage growth even if LPG stagnates. The Singapore trading arm provides flexibility to optimize globally, not just in India. The conservative balance sheet allows patient waiting for distressed acquisition opportunities. Most importantly, the operational excellence culture enables quick pivots when market signals clarify.

The valuation debate misses a crucial point: infrastructure assets have option value beyond current use. Terminals can be repurposed—LPG tanks converted for ammonia, chemical storage shifted to biofuels. Land at major ports becomes more valuable over time regardless of what's stored. The logistics expertise transfers across products. This flexibility, hard to value but real, provides downside protection.

Investment Implications

For growth investors, Aegis offers exposure to India's consumption story with infrastructure stability. The 25-30% earnings growth trajectory can continue for 5-7 years as new terminals commission and utilization improves. The Aegis Vopak IPO provides near-term catalyst for rerating. At 31x earnings, it's expensive but not egregiously so for 25% growth.

For value investors, the sum-of-parts story compels. The listed subsidiary at IPO valuation, the terminal assets at replacement cost, the trading business at modest multiples—add up to 30-40% above current market cap. The dividend yield provides income while waiting for value recognition.

For risk-averse investors, the bear case concerns warrant caution. A basket approach—combining Aegis with renewable energy plays—hedges transition risk. Position sizing should reflect the binary nature of long-term outcomes.

The next 24 months will prove pivotal. The Aegis Vopak IPO's success, Mangalore terminal commissioning, and FY2026 results will either validate the growth story or expose cracks. Investors should watch LPG penetration data, PSU capex plans, and electric cooking adoption rates for early signals of structural shifts. The infrastructure story remains intact for now, but disruption clouds gather on the horizon.

XI. Epilogue: India's Energy Future

As the sun sets over Mumbai port in 2025, the massive LPG carriers discharge their cargo into Aegis terminals, just as they have for two decades. But something fundamental is shifting in India's energy landscape. The country that added 300 million people to the electricity grid in a generation now dreams bigger—net zero by 2070, renewable energy leadership, hydrogen economy participation. Where does a company built on fossil fuel infrastructure fit in this green future?

Aegis's positioning for the energy transition reveals strategic sophistication beyond financial engineering. The company isn't betting against change—it's positioning to profit from the transition itself. Green ammonia, the carrier for hydrogen economy, requires specialized storage infrastructure nearly identical to LPG terminals. The same cryogenic expertise that keeps propane at -42°C can handle ammonia at -33°C. The safety protocols, operational expertise, and port locations transfer seamlessly. This isn't diversification—it's evolution.

The Vopak partnership provides a window into global energy transition patterns. In Rotterdam, Vopak is converting petroleum tanks for biofuel storage. In Singapore, they're building infrastructure for sustainable aviation fuel. These aren't experiments—they're proven business models waiting for Indian adoption. When India's biofuel mandates escalate, when sustainable aviation fuel becomes mandatory, Aegis-Vopak will have first-mover advantage from global experience.

But can a company rooted in 20th-century energy serve 21st-century needs? The challenge isn't technical—tanks are tanks, molecules are molecules. It's cultural and financial. Renewable energy projects demand different risk models, longer paybacks, and often government support. The customers shift from oil PSUs to renewable startups, from stable offtakers to venture-backed disruptors. The skills that built relationships with HPCL may not translate to negotiations with green hydrogen producers.

The infrastructure imperative for India's growth transcends energy choices. Whether powered by LPG, electricity, or hydrogen, India needs massive logistics infrastructure. Chemicals for manufacturing, edible oils for consumption, fuels for transportation—all require storage and movement. Aegis's real asset isn't LPG terminals—it's the capability to build and operate critical infrastructure in a complex democracy. This competence remains valuable regardless of what fills the tanks.

The timing question looms large. If energy transition accelerates, early movers capture emerging opportunities. If it stalls, premature pivots destroy shareholder value. Aegis's approach—maintaining fossil fuel cash flows while experimenting with new energies—seems prudent but may satisfy neither growth investors wanting aggressive transition bets nor value investors seeking stable fossil fuel returns. The middle path, often safest, sometimes leads nowhere.

India's unique context shapes outcomes. Unlike Europe, where existing infrastructure and environmental consciousness drive rapid transition, India must balance energy security, affordability, and sustainability. LPG might be fossil fuel, but it's dramatically cleaner than dung cakes and firewood still used by millions. The perfect cannot be the enemy of the good. This pragmatism—accepting transitional solutions while building toward ideal outcomes—favors players like Aegis who operate in the grey zones between old and new.

The family business dimension adds complexity. The Chandarias built Aegis over three generations. Do they have the patience for another transformation that might take another generation? Can professional managers drive change while respecting legacy? Will capital markets fund transformation at infrastructure timeline returns? These questions lack clean answers but will determine whether Aegis leads or follows India's energy transition.

International comparisons provide perspective but not predictions. Japan's Itochu successfully transformed from textile trader to energy major. Netherlands' Vopak evolved from colonial warehouse operator to global terminal leader. But India isn't Japan or Netherlands. Its transformation will follow its own path, shaped by democracy, demography, and development needs. Companies that understand this uniqueness—foreign enough to bring global best practices, Indian enough to navigate local complexity—will thrive.

The investment implications stretch beyond Aegis to India's entire infrastructure sector. The country needs $2 trillion in infrastructure investment this decade. Traditional financing models—government funding, bank debt, private equity—can't meet this need. Public markets must step up, but they demand returns that infrastructure's long gestation periods struggle to deliver. This tension—society's need for patient capital versus markets' demand for quick returns—will shape winners and losers.

As 2025 draws to a close, Aegis stands at an inflection point that mirrors India's own energy crossroads. The old model—importing fossil fuels, storing in coastal terminals, distributing inland—generated tremendous value but faces structural challenges. The new model—renewable energy, green molecules, circular economy—offers enormous opportunity but requires capabilities not yet built. The transition period—messy, uncertain, but inevitable—rewards those who can operate in ambiguity while building toward clarity.

The Aegis story, ultimately, isn't about one company's success. It's about how emerging markets build critical infrastructure, how family businesses professionalize while preserving values, how companies navigate technological disruption, and how investors balance growth with governance. These themes resonate beyond India, beyond energy, beyond infrastructure. They're the fundamental questions of capitalism in the 21st century.

For Aegis, the next chapter remains unwritten. Will it become India's energy transition champion, leveraging existing infrastructure for new molecules? Will it remain a fossil fuel logistics player, generating cash until demand disappears? Will it transform into something unrecognizable—a data company, a renewable developer, a technology platform? The answer lies not in strategy documents or analyst reports but in the daily decisions of thousands of employees, the risk appetite of the Chandaria family, and most importantly, the energy choices of 1.4 billion Indians.

The company that started as Atul Drug House in 1956, pivoted to chemicals in the 1970s, embraced LPG in the 2000s, and partnered globally in the 2020s, faces its most consequential transformation yet. The infrastructure is built, the relationships established, the capabilities proven. What remains is the vision and courage to reimagine what Aegis could become in India's renewable century. That story—of transformation, adaptation, and evolution—continues to unfold at the pace of infrastructure: slowly, steadily, but ultimately inevitably.

XII. Recent News**

Latest Quarterly Results and Guidance**

Aegis Logistics reported Q1 FY2026 consolidated results with total income of ₹1,781.94 crore for the period ended June 30, 2025, compared to ₹1,770.45 crore in Q4 FY2025. The company posted a net profit of ₹131.32 crore for Q1 FY2026 versus ₹281.67 crore in Q4 FY2025. The sequential decline in profits reflects the impact of lower LPG trading margins and seasonal factors affecting terminal utilization.

The company faced regulatory scrutiny when it was fined Rs 1.06 lakh for late submission of Q4 FY25 results, with the delay attributed to subsidiary IPO consolidation requirements. This minor hiccup underscores the complexity of managing multiple entities during the Aegis Vopak IPO process.

Aegis Vopak IPO Developments

The much-anticipated Aegis Vopak Terminals IPO successfully launched and listed in June 2025. The IPO opened on May 26, 2025, and closed on May 28, 2025, with a price band of ₹223 to ₹235 per share. The company listed on BSE and NSE on June 2, 2025. The IPO raised around ₹2,800 crores through fresh issues, with proceeds earmarked for strategic expansion.

The funds will primarily be used—₹6,713 million—to fund capital expenditure for acquisition of the cryogenic LPG terminal at Mangalore, a critical project that will significantly expand Aegis's LPG handling capacity on the western coast. Post-IPO, promoter holding in Aegis Vopak stands at 86.9%, indicating strong founder control despite the public listing.

New Terminal Announcements

In a significant development, Aegis announced the commissioning of its LPG Cryogenic Terminal at Pipavav, adding substantial capacity to its western India operations. Additionally, in June 2025, Aegis Logistics announced the commissioning of a cryogenic LPG terminal in Mangalore by its subsidiary, Sea Lord Containers, enhancing its LPG storage capabilities along India's western coast.

The company also executed strategic asset transfers, with Aegis executing a business transfer agreement (BTA) with its associate company, Aegis Vopak Terminals (AVTL), for the transfer of its newly commissioned LPG cryogenic terminal at Pipavav. This internal restructuring optimizes asset ownership between the parent and joint venture entities.

Strategic Initiatives and Partnerships

The company announced executed Framework Agreement between the Company and CRL Terminals Ltd. for NDDB projects, and executed Business Transfer Agreement between Sea Lord Containers Ltd. and other entities, indicating continued expansion through strategic partnerships.

The company's focus on new energy infrastructure continues with discussions around ammonia storage capabilities at Pipavav, positioning Aegis for the hydrogen economy transition while maintaining its core LPG business.

Management Updates and Governance

The company maintained dividend momentum with an interim dividend of ₹2 per share for FY 2025-26 and recommended a final dividend of ₹6 per share for FY 2024-25, subject to shareholder approval. This ₹8 total dividend represents a healthy payout while retaining capital for growth investments.

Corporate governance remained robust with the re-appointment of Tasneem Ali as an Independent Director for a second five-year term effective from January 28, 2026, subject to shareholder approval, ensuring board continuity and independence.

Stock Performance and Analyst Views

Despite strong operational performance, Aegis Logistics share price showed mixed performance—down 4.71% over the last month, down 6.27% over three months, and down 16.59% over 12 months on BSE. However, the three-year performance remains impressive with the stock up 255.49% on BSE, reflecting long-term value creation.

The 68th Annual General Meeting is scheduled for Thursday, August 14, 2025, at 3:00 p.m. IST through video conference, where shareholders will vote on key resolutions including dividend approval and director appointments.

Industry Context and Outlook

The recent commissioning of multiple LPG terminals positions Aegis advantageously as India's LPG demand continues growing. With the Aegis Vopak IPO successfully completed and proceeds deployed toward expansion, the company has the financial firepower to accelerate infrastructure development.

Looking ahead, the focus remains on completing the Mangalore cryogenic terminal, ramping up utilization at newly commissioned facilities, and exploring opportunities in alternative energy storage. The partnership with Vopak continues to provide technical expertise and credibility for attracting international customers seeking world-class storage solutions in India.

The stock's recent underperformance despite strong fundamentals suggests a potential opportunity for patient investors who understand the long-term infrastructure story. As new terminals come online and contribute to earnings over the next 12-18 months, the market may re-rate the stock to reflect its enhanced capacity and market position.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube