Marvell Technology: The Architect of the AI Backbone

I. Introduction: The "Other" AI Company

Picture the inside of a modern AI data center. Not the marketing version with glowing blue racks, but the real thing: a windowless hall the size of several football fields, the air thick with the roar of fans, the floor humming with the heat of tens of thousands of processors all firing at once. Everyone knows what sits at the center of that picture. The graphics chips. The "brains." The trillion-dollar darling whose name has become shorthand for the entire artificial-intelligence boom.

But spend a minute looking past the brains, and a different question emerges. A single AI model in 2026 is too big to fit on one chip, or ten chips, or even a thousand. Training it means lashing together tens of thousands of processors so tightly that they behave like one gigantic computer. For that to work, every chip has to talk to every other chip — constantly, at almost unimaginable speed, with almost no delay. If the brains are the neurons, something has to be the nervous system. Something has to carry the signal.

That something is, more often than not, built by a company most people outside the semiconductor world have never heard of: Marvell Technology, the chip designer trading on the Nasdaq under the ticker MRVL.

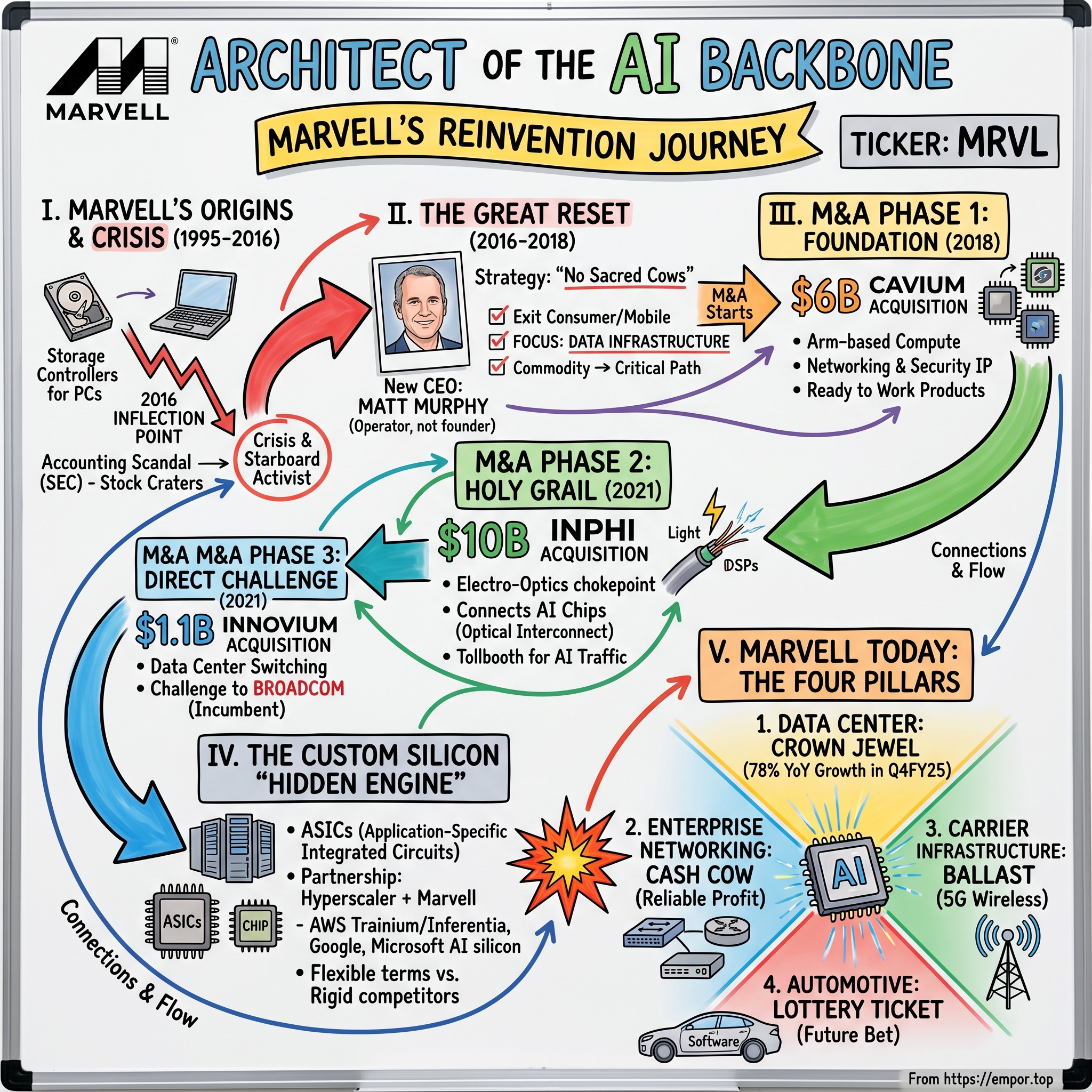

Here is the irony at the heart of this story. The company that became indispensable to the AI era did not set out to be an AI company. It spent its first two decades making the unglamorous controllers that ran the spinning hard drives inside laptops and the network chips inside cheap routers. By 2016 it was a corporate near-corpse: a chipmaker mired in an accounting scandal, run by a feuding founding family, with an activist investor circling and a stock the market had all but given up on. The U.S. Securities and Exchange Commission would eventually charge the company with misleading investors through a scheme to "pull in" sales from future quarters to mask declining revenue.3

What happened next is one of the great corporate reinventions of the semiconductor age. A new chief executive arrived, took an axe to the businesses that had defined the company, and made a series of audacious bets — most famously a $10 billion acquisition that critics swore was reckless and which, with the benefit of hindsight, looks like one of the shrewdest deals of the decade.1

This is the story of how a disk-drive company became the architect of the AI backbone. It is a story about three things: the 2016 reset that pulled the company back from a death spiral, the operator who engineered it, and the "hidden" businesses — optical interconnects and custom silicon — that turned a second-tier chipmaker into one of the most important infrastructure partners of the hyperscaler era. Let's start at the bottom, in the year everything nearly ended.

II. The 2016 Inflection Point: The Great Reset

To understand how far Marvell fell, you have to understand how high it had once flown. The company was founded in 1995 in Santa Clara by a remarkable trio: Sehat Sutardja, a brilliant Indonesian-born engineer; his wife, Weili Dai, a force of nature on the business side; and Sehat's younger brother, Pantas Sutardja, the technical co-founder. The name itself was a portmanteau — "Marvell," from the marriage of Marvelous and the family that ran it. They took the company public in 2000, at the absolute peak of the dot-com frenzy, and for a while it was magic. Marvell's read-channel chips and storage controllers ended up inside a huge share of the world's hard drives. If you owned a laptop in 2008, there was a good chance a Marvell chip was quietly managing the spinning platter inside it.

But the Sutardjas ran Marvell like a family fiefdom, and by the mid-2010s the cracks were everywhere. The storage market was maturing as the world shifted from spinning disks to solid-state drives. A costly patent dispute with Carnegie Mellon University produced an eye-watering jury verdict. And then came the accounting. In 2015, the company disclosed that its audit committee was investigating its revenue recognition practices. The findings were ugly: under intense pressure to hit guidance, employees had accelerated — "pulled in" — sales originally scheduled for future quarters, booking them early to close the gap between real and forecast revenue and mask a decline that management did not want investors to see.3

For a public company, this is close to an original sin. Revenue is the one number the market trusts least to be fudged, and Marvell had been fudging it. The stock cratered. Into that vacuum stepped Starboard Value, the activist hedge fund run by Jeff Smith with a reputation for surgical interventions in tired, undermanaged companies. Starboard built a stake, agitated for change, and won board seats. In the spring of 2016, the founding family's grip finally broke: Sehat Sutardja and Weili Dai were removed from the board. The company they had built over two decades was, for the first time, no longer theirs.

A wounded chipmaker with a discredited management team and an activist in the boardroom is not an obviously attractive job. But in June 2016, the board found its outsider. Matthew Murphy — known to everyone as Matt — was named president and chief executive, effective July 11, 2016.4 He came from Maxim Integrated, a respected analog chipmaker in Silicon Valley, where he had spent the better part of two decades climbing through sales and business-unit leadership.13 He was not a celebrity founder or a visionary technologist in the Nvidia mold. He was an operator. And in 2016, an operator was exactly what Marvell needed.

Murphy's diagnosis was blunt: Marvell was spread too thin, chasing too many low-margin consumer markets where it would never win, and starving the few businesses where it actually had an edge. The company was making chips for everything from Wi-Fi to printers to mobile handsets — fighting brutal price wars in commodity markets against larger, hungrier rivals. The new strategy had a nickname inside the company: "no sacred cows."

What followed was a methodical dismantling. Marvell exited mobile and wireless. It wound down or sold off the consumer-facing businesses that generated revenue but little profit and no strategic advantage. To a Wall Street trained to worship the top line, deliberately shrinking revenue looks like surrender. Murphy understood it differently. He was trading low-quality dollars for high-quality ones — pulling capital and engineering talent out of dead-end markets and redeploying them into a single idea: data infrastructure. The plumbing of the cloud. The chips that move, store, and process data inside the data centers that the world's largest technology companies were building at a furious pace.

It was a bet on a mindset shift as much as a market. The "old Marvell" thought like a commodity supplier — win the socket, ship the volume, fight on price. The "new Marvell" would think like a critical-path partner: find the places in the data center where a chip is hard to build, where being early and being best creates a durable hold on the customer, and own those places. That reframing — from commodity to critical path — is the through-line of everything that came after. But a strategy is only as good as the person executing it, so before we follow the bets, we need to understand the operator placing them.

III. The Matt Murphy Playbook: Leadership & Incentives

There is a certain kind of executive that business journalists struggle to make interesting, because they do not generate drama. Matt Murphy is one of them. He does not tweet provocations or stage theatrical product launches. In an industry that loves its founder-genius archetype — the Jensen Huangs and the Lisa Sus who are inseparable from the chips they design — Murphy is the anti-founder. He is, by trade and by temperament, a manager. And at Marvell, that turned out to be the rarer and more valuable thing.

His reputation in the industry rests on a phrase you hear over and over from analysts who cover the company: he under-promises and over-delivers. In a sector addicted to hype cycles, where executives routinely talk their order books into the stratosphere, Murphy built credibility the slow way — by setting targets the market thought conservative and then beating them. Barron's, profiling him in 2021, framed the turnaround as the story of an operator who "fixed a broken chipmaker" by imposing discipline where there had been chaos.5 The praise was not for vision in the abstract. It was for execution: hitting numbers, integrating acquisitions, allocating capital like an owner rather than a steward.

That last point — allocating capital like an owner — is where the incentive structure becomes the story. The way a company pays its CEO tells you what it actually wants, as opposed to what it says in press releases. Marvell's executive compensation is heavily tilted toward long-term, performance-based equity rather than guaranteed cash. The largest share of Murphy's pay comes in the form of performance stock units that only vest if the company hits specific multi-year goals — most importantly relative total shareholder return, measured against a basket of semiconductor peers, alongside operational milestones tied to design wins in the company's growth markets.[^16] In plain terms: if Marvell's stock does not beat its competitors over a span of years, a large slug of the CEO's theoretical pay simply evaporates.

This matters for a fundamental investor because it shapes behavior at the top. A CEO paid mostly in salary and time-vesting stock is incentivized to stay employed. A CEO whose fortune is lashed to multi-year relative outperformance is incentivized to make bets that compound — even uncomfortable ones, like shrinking revenue in 2016 or paying up for a strategic asset that won't pay off for years. Murphy is also a meaningful shareholder in his own right; his personal holdings, disclosed in the company's annual proxy statements, run well into the seven figures by share count, putting real money alongside the equity grants.[^16] When the person steering the ship has that much of their net worth riding on where it ends up, the alignment with outside shareholders is more than a slide in an investor deck.

The cultural mark Murphy left is subtler but just as important. He set out to build what insiders call a "best of breed" engineering culture — recruiting and retaining the kind of specialized talent that can design the hardest chips in the data center, and, crucially, keeping that talent through the acquisitions to come. Because the next chapter of Marvell's story was not built organically in a lab. It was bought. And the art of acquisition is not writing the check — it is keeping the engineers who make the acquired company worth buying in the first place. That brings us to the deals.

IV. The M&A Masterclass: Benchmarking the Bets

Every great corporate transformation has a few decisions on which everything hinges. For Marvell, those decisions were acquisitions — three of them, made in a remarkably tight window, that collectively rewired what the company was. To appreciate them, you have to hold a difficult truth in mind: at the moment each deal was announced, a large and intelligent chunk of Wall Street thought at least one of them was a mistake. The verdict of history is kinder than the verdict of the day. That gap is where the lesson lives.

Cavium (2018): The Foundation. The first big swing came in late 2017, when Marvell agreed to acquire Cavium, a Silicon Valley chipmaker founded by Syed Ali, for roughly $6 billion in cash and stock; the deal closed on July 6, 2018.6 Cavium made processors based on Arm architecture, along with security and networking silicon used in data centers and carrier equipment. What Marvell bought was not just products but capability: a beachhead in compute and a deep bench of networking and security IP that meshed with its own.

Here the benchmarking is instructive. Think about what ソフトバンク SoftBank had paid for the entire Arm ecosystem in 2016 — north of $30 billion for the IP licensor whose designs sit at the heart of nearly every smartphone. SoftBank bought the blueprint and the long-term option on an entire computing architecture, at a valuation that only made sense on a decade-plus horizon. Marvell took the opposite, more pragmatic route. Rather than buy the architecture, it bought a company that had already built working, shipping, Arm-based networking and security silicon — productized, in market, generating revenue — at a multiple of roughly six times sales. It was the difference between buying a quarry and buying finished stone. For a company that had just clawed its way out of a financial scandal, "ready to work" at a reasonable multiple was exactly the right risk posture.

Inphi (2021): The Holy Grail. Then came the bet that defined the modern company. On October 29, 2020, Marvell announced it would acquire Inphi Corporation in a cash-and-stock deal valued at roughly $10 billion; it closed on April 20, 2021, with Inphi holders receiving $66 in cash plus 2.323 Marvell shares for each Inphi share.17 As part of the transaction, Marvell redomiciled from Bermuda to Delaware, planting itself firmly as a U.S. company.

To understand why this deal matters, you need to understand what Inphi did — and to understand that, you need a quick detour into physics. Inside a data center, data has to travel between racks of equipment that may be tens or hundreds of meters apart. Pushing high-speed electrical signals down copper wire over those distances is a losing battle; the signal degrades, the power burns, the heat builds. The solution is to convert the electrical signal into pulses of light, send the light down a thin glass fiber at the speed of, well, light, and convert it back to electricity at the other end. That conversion — electricity to light and back again, billions of times per second, without garbling the data — is the dark art of electro-optics. And Inphi was the best in the world at the specific chips, called DSPs, that make it work, particularly using a signaling technique known as PAM4 that crams more data into each pulse.

Critics looked at the price tag and recoiled. Inphi was a fast-growing but still modestly sized company, and roughly $10 billion worked out to something like fifteen times forward revenue — a nosebleed multiple for a chip company at the time. The bears called it a classic case of a newly confident management team overpaying at the top.

They were looking at the wrong denominator. What Marvell actually bought was a tollbooth on the one road that AI traffic would be forced to travel. As AI models exploded in size over the following years, the bottleneck in the data center began migrating — away from the raw compute and toward the connections between compute. The optical modules that link AI chips together raced from 400 gigabits per second to 800G and on toward 1.6 terabits, and at the heart of each of those modules sat the kind of DSP that Inphi pioneered. Measured against the explosion of 800G and 1.6T optics that followed, the price that looked insane in 2020 came to look like one of the best semiconductor acquisitions of the decade.[^10] Marvell had not overpaid for revenue; it had bought a cornered resource at the exact moment before the world discovered it needed it.

Innovium (2021): The Direct Challenge. The third deal was the smallest and the most aggressive in its intent. In August 2021, Marvell agreed to acquire Innovium, a maker of cloud data-center switching chips, in an all-stock transaction valued at about $1.1 billion.8 Switching chips are the traffic cops of the data center — they direct the flood of packets between thousands of servers — and the market had long been dominated by one company. Innovium's Teralynx switch architecture gave Marvell a credible, high-performance alternative to put in front of cloud customers who wanted a second source. It was, in effect, a declaration of war on the incumbent we'll meet properly later: 博通 Broadcom.

Three deals, one logic. Each filled a gap in the same picture — compute from Cavium, optical interconnect from Inphi, switching from Innovium — and together they assembled the full toolkit needed to build the inside of an AI data center. But the most valuable thing Marvell acquired in this period wasn't a product line at all. It was a business model that barely shows up in the segment tables: building bespoke chips for the largest technology companies on earth. That hidden engine deserves its own chapter.

V. The "Hidden" Business: Custom Silicon

For most of computing history, building a chip meant buying one off the shelf. A company like Intel or, later, Nvidia would design a processor, manufacture it in enormous volume, and sell the identical part to everyone — your laptop, your neighbor's server, a bank's data center. Economies of scale did the rest. The chip was a product, sold to a market.

But the largest technology companies in the world — the hyperscalers, in industry jargon, meaning the handful of firms that operate planet-scale cloud infrastructure — eventually grew big enough to break that model. When you are buying chips by the millions and running them around the clock, even a small inefficiency in a general-purpose part translates into billions of dollars of wasted electricity and capital. At a certain scale, it becomes cheaper and better to design your own chip, tuned to exactly your workload, than to buy someone else's compromise. The trouble is that designing a leading-edge chip is one of the hardest things humans know how to do. The hyperscalers had the money and the motivation, but most lacked the deep silicon engineering muscle to do it alone.

This is the gap Marvell stepped into, and it is the company's least understood and most important business: custom silicon, or ASICs — application-specific integrated circuits. The idea is a partnership. The hyperscaler brings the architecture and the workload knowledge; Marvell brings the hard parts — the advanced manufacturing process, the interconnect IP from Inphi, the high-speed networking, the physical design expertise needed to actually turn a concept into a working chip at the bleeding edge. Together they produce a chip that belongs to the customer, optimized for that customer alone.

The customers are exactly who you would expect. Marvell has positioned itself as a key custom-silicon partner to the giants building their own AI accelerators — the family of chips that 亚马逊 Amazon brands as Trainium and Inferentia, the AI silicon programs at 谷歌 Google, and efforts at 微软 Microsoft, among others. These are the in-house alternatives to buying Nvidia GPUs, and the companies building them have been racing to scale up. In late 2024, Marvell deepened this trajectory with a multi-year, multi-generational agreement with Amazon Web Services spanning custom AI silicon and the optical and networking products that surround it — a signal of just how strategic these relationships had become.[^14]

Why does this matter for an investor? Because of the growth math. Marvell's legacy storage business — the controllers descended from the old disk-drive empire — is cyclical, mature, and frankly boring; it rises and falls with the broader data-storage market and grows slowly at best. The custom-compute business is the opposite. As AI capital spending surged, Marvell's data-center segment — of which custom silicon and optics are the core — exploded. By the third quarter of its fiscal 2025, data-center revenue had reached roughly $1.1 billion in a single quarter, up about 98% year over year and accounting for nearly three-quarters of total company revenue.12 A doubling in a year, from a business that barely registered a decade earlier. That is the hidden engine, and it had stopped being hidden.

The natural question is why a hyperscaler would pick Marvell over the incumbent. The custom-ASIC market has a thousand-pound gorilla in 博通 Broadcom, which built the original business designing chips for Google's TPUs and others. Marvell's counter-positioning is built on a single word: flexibility. The pitch to customers is that Marvell will partner more openly, license its IP more flexibly, and give the hyperscaler more control over the final design — versus a rival some customers perceive as more rigid and more inclined to dictate terms. In a market where the buyers are the most powerful technology companies on earth, being the accommodating partner is itself a strategy.

It is worth naming the competitive field honestly, because this is a crowded and rising arena. Beyond Broadcom, the custom-silicon space includes specialized design houses like 世芯電子 Alchip Technologies of Taiwan, which has won meaningful AI-accelerator business of its own, and the broader ecosystem in which Marvell's own China operations — known locally as 美满电子 Marvell — participate amid an intensifying U.S.–China contest over advanced chips. The point is that Marvell's custom-silicon moat is real but contested; it is widening, but it is not unassailable. That tension — a genuinely strong position in a genuinely competitive market — runs through the rest of this story. To see the full shape of the business, we need to step back and look at all four of its pillars.

VI. Segment Breakdown: The Four Pillars

If you want to understand a diversified chip company, it helps to stop thinking about products and start thinking about which businesses are growing, which are paying the bills, and which are options on the future. Marvell organizes itself around a handful of end markets, but they fall naturally into four strategic roles. Think of it as a portfolio with one star, one workhorse, one slow-and-steady earner, and one long-dated lottery ticket.

Data Center: The Crown Jewel. This is everything we have been building toward — the custom AI accelerators, the optical DSPs descended from Inphi, the switching from Innovium. It is the fastest-growing part of the company by a wide margin and now the dominant share of revenue. For the full fiscal year ended in early 2025, Marvell reported total net revenue of $5.767 billion, and the data-center segment had grown to be the clear center of gravity, with the fourth quarter alone showing data-center revenue up 78% year over year.2 When investors talk about Marvell as an "AI company," this is the segment they mean. Its fortunes will make or break the stock.

Enterprise Networking: The Cash Cow. Every company needs a business that throws off reliable profit to fund the moonshots, and for Marvell that role falls largely to enterprise networking — the Ethernet switches, controllers, and connectivity chips that go into the routers, switches, and corporate infrastructure sold by equipment makers. It is a solid, established, decent-margin business tied to the broader enterprise IT cycle. It will never double in a year, but it does not need to. Its job is to be dependable, to generate the cash that funds the research and development behind the crown jewel. When the enterprise market softens — as cyclical markets do — this segment is where the pain shows up first, a reminder that not all of Marvell rides the AI rocket.

Carrier Infrastructure (5G): Slow and Steady. Marvell supplies silicon into the base stations and network equipment built by the telecom-gear giants — companies like Nokia and Ericsson — that form the backbone of 5G wireless networks. This is patient, infrastructure-grade business: long design cycles, long product lives, and demand tied to the capital-spending plans of the world's telecom operators. Those plans have been uneven, and the carrier segment has had soft stretches as 5G buildouts matured. It is neither a growth engine nor a worry; it is ballast.

Automotive: The New Initiative. And then there is the lottery ticket. Modern cars are turning into computers on wheels — "software-defined vehicles," in the industry's phrase — and a computer needs an internal network to move data between its dozens of processors, cameras, and sensors. Marvell makes the high-speed automotive Ethernet that serves as the nervous system of these vehicles. If the data center is the company's present, automotive is a bet on the future: Marvell aims to be the plumbing of the modern car, supplying the in-vehicle networking that every automaker will eventually need.10 It is small today and years from mattering to the financials, but it is the kind of optionality that, like Inphi once was, could look obvious in hindsight.

Four pillars, four very different roles. The investor's job is to watch the right one. Which raises the deeper question this whole story has been circling: is Marvell's position in that crown-jewel business actually defensible, or is it renting a moment in the sun? To answer that, we need to bring in the frameworks.

VII. Hamilton's 7 Powers & Porter's 5 Forces

Strip away the excitement of the AI boom and the fundamental question for any long-term owner of Marvell is unglamorous: what, exactly, stops a competitor from doing what Marvell does? A great business is not one that is winning today. It is one that has a structural reason competitors cannot easily take its winnings away. Two frameworks help pressure-test that — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and Marvell is a genuinely interesting case because it scores high on some and worryingly low on others.

Start with the powers Marvell clearly has. The first is what Helmer would call a cornered resource — control of a coveted asset that produces outsized value. The optical electro-optics IP that came with Inphi is close to a textbook example. You cannot build a leading-edge AI cluster without converting electrical signals to light and back at extreme speed, and the population of companies that can design those DSPs at the cutting edge is vanishingly small. For years, Marvell's portfolio in this domain has been the asset that competitors most wished they had and could least easily replicate. It is the closest thing in this story to a chokepoint on the AI build-out.[^10]

The second is switching costs, and they are formidable in the custom-silicon business. When a hyperscaler co-designs a bespoke AI chip with Marvell, it is not a transaction; it is a marriage that lasts years. The two companies spend eighteen months or more developing the chip, then it ships in volume for years after that, often spawning a next-generation follow-on that builds on the same shared foundation. Ripping Marvell out mid-lifecycle would mean throwing away an enormous joint investment and starting over. That stickiness — the multi-year, multi-generation nature of each design win — is why a single custom-silicon relationship can be worth far more than its first chip suggests, and why the late-2024 multi-generational AWS agreement was such a meaningful signal of durability.[^14] There is also a quieter dose of scale economies and process power in the mix: integrating Cavium, Inphi, and Innovium gave Marvell a breadth of interconnect, compute, and switching IP that is hard to assemble from scratch and expensive to match.

Now turn to Porter's forces, where the picture gets more sober. The bargaining power of buyers is, frankly, enormous. Marvell's most important customers are among the largest and most sophisticated companies in the world — the handful of hyperscalers who account for a huge share of data-center revenue. These are not buyers you push around. They have armies of engineers, deep pockets to fund alternatives, and every incentive to commoditize their suppliers. Marvell's only real defense against that power is the cornered resource and switching costs above: customers tolerate the relationship because they cannot easily get the unique IP elsewhere, not because they lack the muscle to squeeze. Lose the IP edge, and the buyer power becomes overwhelming.

Then there is rivalry, and here one name dominates: 博通 Broadcom, the $1-trillion-plus colossus run by Hock Tan that is both the largest player in custom AI silicon and a giant in networking and optics. Broadcom is bigger, more profitable, and more entrenched. Marvell cannot beat it on scale, so it does not try. Instead it counter-positions — the strategic power of being the deliberately open, flexible, customer-friendly alternative to an incumbent that some customers find too dominant and too rigid. It is the same playbook a nimble challenger always runs against a category king: don't fight the giant's strength, exploit the resentment the giant's strength creates. The remaining forces are less acute — the threat of new entrants into leading-edge chip design is low, because the capital and expertise required are staggering, and substitutes are limited because there is no other way to move AI data than through the kind of silicon Marvell makes. The competitive pressure that matters is the rivalry and the buyer power, and they are real.

So Marvell is a company with two powerful moats — a cornered resource and high switching costs — facing two powerful threats — concentrated, sophisticated buyers and a bigger rival. That is not a contradiction; it is the actual shape of the business. Whether the moats outlast the threats is the entire debate, and it is time to lay out both sides of it.

VIII. Analysis: Bear vs. Bull Case

Every compelling investment is an argument, and the smartest version of that argument requires steelmanning the other side. With Marvell the two cases are unusually well-matched, because the very things that make the bull case thrilling are the same things that make the bear case credible. Let's give each its full due.

The Bear Case. The first and most serious worry is customer concentration. Marvell's spectacular data-center growth rests on a small number of enormous customers, and when a handful of hyperscalers drive the majority of your fastest-growing segment, you are exposed to their every decision. If one of them pushes out a build, designs you out of a next-generation chip, or simply decides to bring more of the work in-house, the revenue line can lurch. These customers also possess, as we've seen, formidable bargaining power, and they will use it. Concentration cuts both ways: it has been the engine of the boom, and it is the single biggest vulnerability underneath it.

The second bear argument is cyclicality. For all the AI glamour, Marvell still carries a meaningful legacy business — storage controllers and other mature product lines — that is tied to the lumpy, boom-and-bust rhythm of the broader semiconductor cycle. When enterprise and consumer chip demand turns down, those segments shrink, and they can mask or partly offset the data-center growth in any given quarter. A company that is part rocket ship and part cyclical industrial is harder to value, and the market periodically punishes that ambiguity.

The third is the simplest and perhaps the hardest to rebut: Broadcom is just too big to beat. In the custom-silicon and optical markets where Marvell competes, it faces a rival with more scale, more profit, more customer relationships, and more financial firepower to outspend it on research or outbid it on a deal. The bear says Marvell will always be the number two — winning some sockets, yes, but structurally capped, with thinner margins and a permanent disadvantage in any war of attrition. Being a strong number two in a great market is a fine business. It is not the same as being the king.

The Bull Case. Now the other side, and it begins with a phrase that captures the whole thesis: the golden age of optics. The bull's central insight is about where the bottleneck in AI is moving. For years the constraint was compute — not enough processing power. But as AI models scale to trillions of parameters, training them requires lashing together so many chips that the limiting factor shifts from how fast each chip computes to how fast the chips can talk to one another. The bottleneck migrates from the brains to the nervous system — from the GPU to the connection. And the connection is precisely where Marvell is strongest. In this telling, every dollar of additional AI investment flows disproportionately toward the interconnect, and Marvell sits in the path of that flow.[^10] The cornered resource isn't just defensible; it becomes more valuable the bigger AI gets.

The second bull pillar is the custom-silicon flywheel. Each design win is multi-year and multi-generational, so today's wins lock in years of future revenue, and a strong reputation as a flexible partner attracts the next hyperscaler that wants an alternative to Broadcom. The business compounds on itself. And there is a capital-allocation chapter to the bull case too. The Marvell of 2018–2021 was a serial acquirer, reshaping itself through Cavium, Inphi, and Innovium. The Marvell of the mid-2020s has shifted from acquirer to organic-growth engine — the integration work is largely done, and the company is now harvesting the portfolio it assembled rather than constantly buying new pieces. That maturation, the bull argues, means more free cash flow returned to shareholders and less integration risk, all while the AI tailwind does the heavy lifting.

Where does that leave a fundamental investor? Not at a verdict — this story is too genuinely contested for that, and the future of AI capital spending is unknowable. It leaves you with a small number of things actually worth watching. If you track nothing else about Marvell, track these: data-center segment revenue growth, the single clearest readout of whether the AI thesis is playing out or stalling; the pace and breadth of custom-silicon design wins, because each one is a multi-year annuity and a tell about whether the flywheel is still turning; and customer concentration, the risk that sits underneath everything — whether the hyperscaler base is broadening over time or narrowing into dangerous dependence on one or two names. Those three numbers, watched over several years, will tell you more than any quarter's headline ever could.

IX. Epilogue & Lessons

Step back from the chips and the segments and the frameworks, and Marvell's story resolves into something almost archetypal. Here was a company that, by 2016, had every reason to fade — a maturing core market, a founding family forced out, an accounting scandal that drew a federal rebuke, an activist at the gates. Companies in that position usually become acquisition fodder or slow-motion declines. Marvell instead became one of the indispensable suppliers of the most important technology build-out of its generation.

The lesson for anyone who studies businesses is that reinvention does not require being first or being biggest. Marvell was never the genius founder's company or the category-defining innovator; it was a second-tier chipmaker that reinvented itself through surgical capital allocation. It read where the value in the data center was migrating — from the storage it knew toward the interconnect it didn't yet own — and it bought its way to the front of that migration, paying up for Inphi when the conventional wisdom said it was reckless, and being proven right by a wave almost no one had fully priced. The transformation was engineered, not inspired. In an industry that mythologizes invention, Marvell is a monument to the underrated power of knowing what to buy, what to kill, and what to become.

As for what comes next, the frontier is, fittingly, even faster light. The industry's march from 800-gigabit toward 1.6-terabit optical connections continues, and beyond it looms the integration of silicon photonics — building the optical machinery directly onto the chip itself, fusing the electronics and the light into a single package rather than bolting them together. If that transition unfolds the way the optics transition did, the company that controls the electro-optics IP will be standing, once again, at exactly the chokepoint the rest of the industry has to pass through. Marvell's whole modern history has been a bet that the connection matters as much as the computation. The coming decade of AI will be the test of whether that bet was a moment or a moat.

References

-

Marvell to buy Inphi for $10 billion in cloud, 5G push — Reuters, 2020-10-29 ↩↩

-

Marvell Technology, Inc. Form 8-K — Q4 and Full Year Fiscal 2025 Results — SEC.gov, 2025 ↩

-

SEC Charges Silicon Valley-Based Issuer With Misleading Disclosure Violations (Marvell, Press Release 2019-175) — SEC.gov, 2019-09-16 ↩↩

-

Marvell Technology Group Ltd. Announces Appointment of Matthew J. Murphy as President and Chief Executive Officer — Marvell, 2016-06 ↩

-

The New Marvell: How Matt Murphy Fixed a Broken Chipmaker — Barron's, 2021-03-26 ↩

-

Marvell Technology Group Completes Acquisition of Cavium — Marvell, 2018-07-06 ↩

-

Marvell Technology, Inc. Form 8-K12B — Completion of Inphi Acquisition — SEC.gov, 2021-04-20 ↩

-

Marvell to Acquire Innovium — Accelerates Cloud Growth with Expanded Ethernet Switching Portfolio — Marvell, 2021-08-03 ↩

-

Marvell shares surge on optimism over AI spending by tech giants — Bloomberg, 2023-05-25 ↩

-

Marvell Technology, Inc. Form 10-K (Fiscal Year Ended February 3, 2024) — SEC.gov, 2024 ↩

-

Marvell Technology (MRVL) Q1 Fiscal 2025 Earnings Call Transcript — The Motley Fool, 2024-05-30 ↩

-

Marvell Q3 FY2025: AI & Cloud Growth Amid Restructuring — The Futurum Group, 2024 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube