Lumentum Holdings: The Light Behind the Data Age

The Deep Roots: JDSU and the Dot-Com Bubble

Garage Beginnings and the Telecom Dream

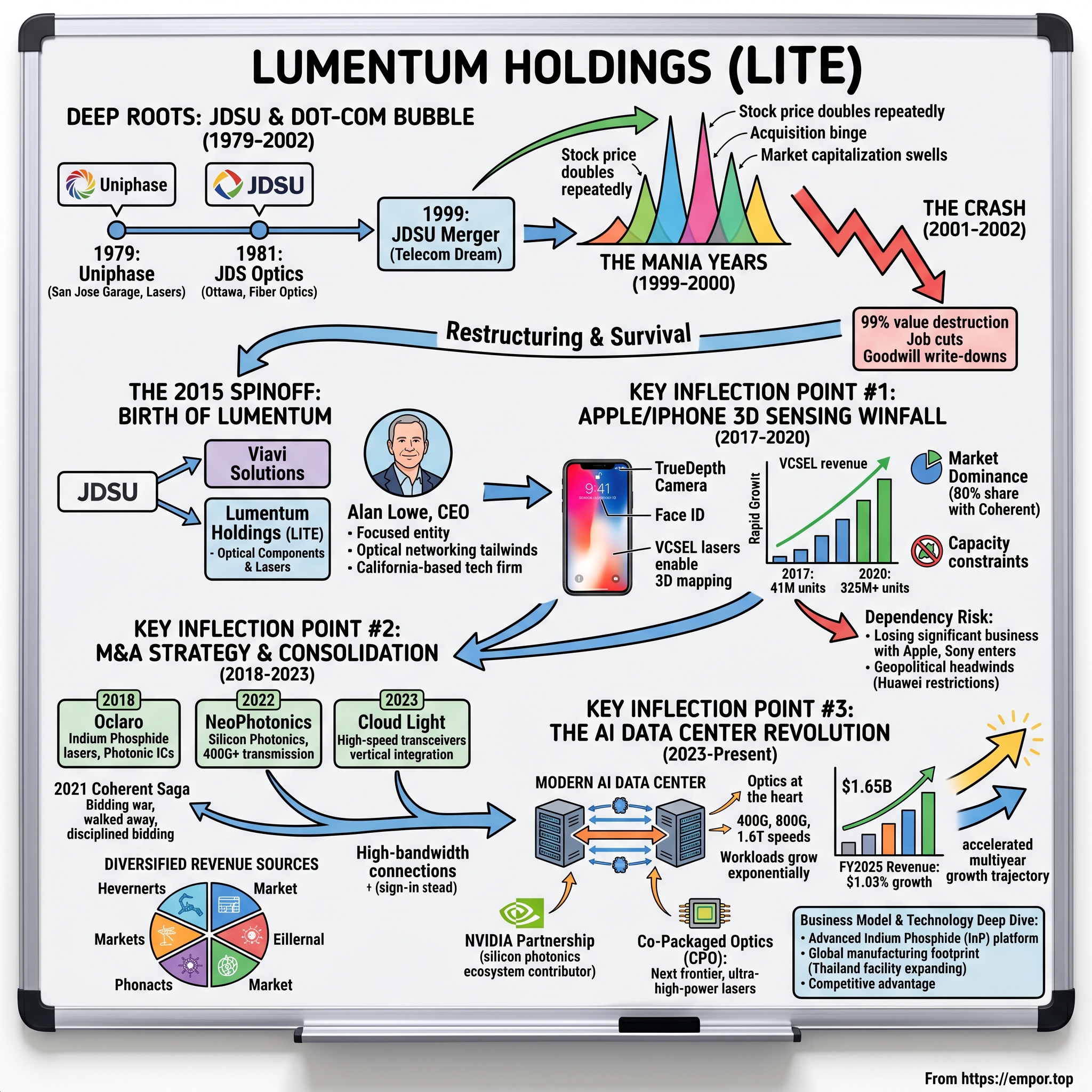

The story begins not in the gleaming corridors of modern AI data centers, but in the far more modest setting of a San Jose garage in 1979. Uniphase was started in 1979 in a San Jose, California garage, and made lasers for chip makers and scanners. Two years later, across the continent in Ottawa, another venture was taking shape. In 1981, JDS Optics was founded in Ottawa, Ontario by Philip Garel-Jones, Gary Duck, Jozef Straus, and Bill Sinclair. The "JDS" is short for Jones, Duck and Straus/Sinclair. The company became JDS Fitel when it formed a partnership with Fitel, a fiber optic and optical connector company. In 1999, JDSU was formed by the merger between JDS Fitel and Uniphase.

These humble origins belied the strategic importance of what these companies were building. Optical networking—the technology of moving data at the speed of light through glass fibers—was becoming the backbone of the emerging internet economy. As the 1990s progressed and the World Wide Web transformed from academic curiosity to commercial imperative, demand for optical components exploded.

The Mania Years

What happened next remains one of the most instructive cautionary tales in technology investing history. Its stock price doubled three times and three stock splits of 2:1 occurred roughly every 90 days during the last half of 1999 through early 2000, making millionaires of many employees who were stock option holders, and further enabling JDS Uniphase to go on an acquisition and merger binge.

The mechanics of this mania were self-reinforcing. Rising stock prices created acquisition currency. Acquisition currency enabled deals that further inflated perceived growth. Employee stock options created paper wealth that attracted more talent, which enabled more deals. The virtuous cycle seemed unstoppable.

The dot-com bubble (or dot-com boom) was a stock market bubble that ballooned during the late 1990s and peaked on Friday, March 10, 2000. This period of market growth coincided with the widespread adoption of the World Wide Web and the Internet, resulting in a dispensation of available venture capital and the rapid growth of valuations in new dot-com startups. Between 1995 and its peak in March 2000, investments in the Nasdaq Composite stock market index rose by 600%, only to fall 78% from its peak by October 2002, giving up all its gains during the bubble.

JDSU became emblematic of this era—not just as a participant, but as perhaps its purest expression. The company's fiber optic components were the literal plumbing of the internet infrastructure build-out. Every telecom operator racing to deploy fiber was a potential customer. Every acquisition added capabilities. Every stock split created the illusion of ever-ascending value.

The Crash That Defined an Era

When the music stopped, JDSU's fall was as spectacular as its rise. After a downturn in the telecom industry as part of the dot com bubble, JDS Uniphase announced in late July 2001 the largest (up to then) write-down of goodwill. Employment soon dropped as part of the Global Realignment Program from nearly 29,000 to approximately 5,300, many of its factories and facilities were closed around the world, and the stock price dropped from $153 per share to less than $2 per share.

Consider the magnitude: a 99% destruction of shareholder value. An 82% reduction in headcount. Factories around the world shuttered. The largest goodwill write-down in corporate history to that point. JDSU became shorthand for dot-com excess, its name invoked in business school case studies alongside Pets.com and Webvan.

The crash saw the Nasdaq index plunge 76.81%, from a peak of 5,048.62 on March 10, 2000, to 1,139.90 on October 4, 2002, culminating in the majority of dot-com stocks going bust and evaporating trillions of dollars of investment capital in its wake. It would take 15 years for the Nasdaq to retrieve its peak, which it did on April 24, 2015.

But here's what makes the JDSU story relevant to understanding Lumentum: the company survived. Unlike Pets.com, unlike the hundreds of startups that simply evaporated, JDSU endured through a brutal decade and a half of restructuring, technology transitions, and strategic repositioning. The optical communications technology remained valuable; the company retained genuine engineering expertise and manufacturing capabilities. The challenge was separating these assets from the crushing weight of goodwill impairments and organizational complexity accumulated during the mania.

The lesson for investors is profound: even in the wreckage of the most excessive valuations, real value can persist when underlying technology matters. The question becomes how to unlock that value.

The 2015 Spinoff: Birth of Lumentum

The Strategic Logic of Separation

By 2015, JDSU had evolved into a sprawling conglomerate with disparate business lines: optical communications components, commercial lasers, network test and measurement equipment, and optical security products. The strategic coherence that justified acquisitions during the bubble years had long since dissipated. Each segment served different customers, faced different competitive dynamics, and required different capital allocation priorities.

In August 2015, JDSU split into two different companies – Viavi Solutions and Lumentum Holdings. The spin-off was designed to create two distinct and focused companies, with Lumentum taking over the optical components and commercial lasers businesses while Viavi retained the network and service enablement and optical security businesses.

The mechanics were straightforward: each stockholder received one share of Lumentum common stock for every five shares of JDSU common stock held on July 27, 2015. JDSU was renamed Viavi Solutions and, at the time of the distribution, retained ownership of approximately 19.9% of Lumentum's outstanding shares.

Lumentum Holdings Inc is a California-based technology firm. The company was incorporated in 2015 and is headquartered in San Jose, California. The company began trading on the NASDAQ under the ticker LITE on July 23, 2015.

Alan Lowe Takes the Helm

The choice of leadership for the newly independent company proved crucial. Since 2015, Mr. Lowe has served as president and chief executive officer of Lumentum Holdings Inc., a designer and manufacturer of optical and photonic products enabling optical networking and laser applications worldwide. Prior to Lumentum's separation from Viavi Solutions Inc. in 2015, Mr. Lowe was employed by Viavi. Mr. Lowe joined Viavi in September 2007 as senior vice president of the Lasers business and became executive vice president and president of Viavi's communications and commercial optical products business in October 2008.

Lowe understood the assets he was inheriting and the opportunity ahead. "Leading the talented Lumentum team for the past 18 years – first at our predecessor company and then over the last decade as a standalone public company – has been both a privilege and a joy," commented Lowe. "In that time, our business has undergone tremendous transformation and growth in both existing and new markets. We have intensely focused on serving our customers, invested in market-leading innovation, and entered new markets, and are now on a clear growth trajectory."

The Inheritance

At its formation, Lumentum inherited decades of optical innovation history dating back to the original companies that formed JDS Uniphase, including substantial intellectual property and manufacturing capabilities in optical technologies. This included expertise in indium phosphide fabrication, precision optics assembly, and the institutional knowledge accumulated through serving the world's largest telecommunications equipment manufacturers.

The initial vision for Lumentum was to create a focused entity capable of effectively innovating and competing in the rapidly evolving optical and photonic markets. This strategic separation allowed Lumentum to concentrate on its core competencies in optical networking and commercial lasers without the distractions of unrelated businesses.

For investors, the spinoff created a cleaner investment thesis: Lumentum would rise or fall based on its ability to execute in optical communications and lasers—markets with genuine secular tailwinds driven by data growth—rather than being subsumed within a conglomerate structure where capital allocation trade-offs obscured the value of individual assets.

Key Inflection Point #1: The Apple/iPhone 3D Sensing Windfall (2017-2020)

The TrueDepth Revolution

The transformation of Lumentum from telecom component supplier to consumer electronics powerhouse happened faster than almost anyone anticipated. Apple's new TrueDepth camera in iPhone X uses a dot projector to achieve its magic and a new report claims that US-based laser diode supplier Lumentum is now the only company that has won orders from the Cupertino giant for that crucial part. According to a recent DigiTimes report, Lumentum has subcontracted Taiwan's Win Semiconductors to manufacture the vertical-cavity surface-emitting laser (VCSEL) component that the TrueDepth camera's dot projector uses for Face ID and to sense depth. The dot projector sprays your face with more than 30,000 invisible dots. A dedicated infrared camera then takes the image of your face and analyzes the dots to create a 3D mesh representing the unique geometry of your face. Prior reports mentioned multiple suppliers as possible producers of the VCSEL part, but market sources said that Lumentum has beaten several competitors to become the sole supplier of the component as part of 3D sensing modules for iPhone X.

Evidence that Apple is planning to bring Face ID to its new smartphones this year continues to mount, this time thanks to a quarterly update from VCSEL supplier Lumentum. As a provider of vertical cavity surface emitting laser technology, Lumentum is a key supplier for Apple's flagship facial recognition system, which is designed to create a 3D map of a given user's face using a projected infrared grid.

The Scale of Opportunity

The numbers tell the story of the transformation. Since the adoption of VCSEL solutions for 3D sensing modules in smartphones, Apple consumed the majority of VCSELs produced by Lumentum. In 2017, 41 million units were implemented in iPhones, and by 2020, more than 325 million VCSELs were expected to be used in iPhones.

Lumentum Holdings serves as Apple's primary supplier of vertical-cavity surface-emitting laser components, or VCSEL. This component is what's used in the iPhone's front-facing camera for its Face ID and Animoji technology.

Perhaps most notable here is that Apple has yet again secured a large portion of VCSEL orders for the year. Such 3D sensing and augmented reality components continue to be highly supply constrained, and Apple placing such large orders with company's like Lumentum makes it hard for Android manufacturers to get in on the technology. Given Lumentum and other VCSEL suppliers continue to be capacity constrained, we believe Apple has once again secured the majority of all VCSELs produced in 2018, further expanding their lead in AR.

Market Dominance

The combination of first-mover advantage and capacity constraints created an extraordinary market position. Analyst report shows duo have cornered 80% of the market, largely thanks to Apple's iPhones. Duopoly: Lumentum and Coherent dominate VCSEL market. The market for vertical cavity surface-emitting lasers (VCSELs) is dominated by two companies with a combined market share of 80 per cent. That's according to the latest analysis from Yole Intelligence and sister company PISÉO, which estimates that the 2022 market for the devices will be worth $1.6 billion. The total is almost entirely the result of deployments in short-range datacom links and Apple iPhones. Yole estimates that Lumentum is the market leader, with a share of 42 per cent, closely followed by Coherent (until recently II-VI) with 37 per cent. Trumpf, which acquired the VCSEL expertise of Philips Photonics in 2019, sits a distant third with a 6 per cent share.

Yole explains that Lumentum was the only supplier qualified by Apple five years ago, at which point Finisar was "struggling to qualify" products for the consumer electronics giant. "These two players, Lumentum and [Coherent], are still the only players qualified by Apple for 3D sensing," adds the analyst company, also pointing out that a series of acquisitions has reinforced their positions in the optical communications market, vertically integrating from the VCSEL device to the entire transceiver module.

The Dependency Risk Materializes

Yet concentration risk—the perennial danger of supplier relationships with powerful customers—eventually materialized. The past several years held unique challenges for the company, including the loss of significant business with Apple Inc. as the smartphone maker split its iPhone VCSEL business among multiple suppliers.

Sony will replace Lumentum (design) / Win Semi (production) as the exclusive ToF VCSEL (Time-of-Flight, Vertical-Cavity Surface-Emitting Laser) supplier for iPhone 15 Pro and Pro Max. Lumentum/Win Semi will face long-term structural risks in the VCSEL market. The critical design of Sony's ToF VCSEL solution is integrating VCSEL & driver IC, which can reduce power consumption (beneficial for battery life) or provide better ToF performance under same power consumption. Lumentum/Win Semi's iPhone Face ID VCSEL market share will decrease from 50% in the iPhone 14 series to 30-40% in the iPhone 15 series due to Sony and II-VI's increased supply ratio. Losing significant iPhone VCSEL orders means Lumentum/Win Semi will face structural risks due to Sony's technological advantages.

Simultaneously, geopolitical headwinds struck from an unexpected direction. Lumentum today announced it intends to fully comply with the recent United States Department of Commerce imposed license requirements for the export, reexport and/or in-country transfer of all items subject to U.S. export control regulations to Huawei Technologies Co., Ltd. and designated affiliates of Huawei. Lumentum has discontinued all shipments to Huawei effective as of the date the licensing requirements went into effect and cannot predict when it will be able to resume shipments. The financial guidance ranges Lumentum provided for its fourth quarter 2019 did not contemplate this Department of Commerce order, the discontinuation of sales to Huawei, or the time required to repurpose manufacturing capacity to other customers.

For the fiscal year ended June 30, 2018, sales to Huawei represented 11% of total revenue. For the fiscal third quarter of 2019, ended March 30, 2019, sales to Huawei represented approximately 18% of total revenue and for fiscal year 2019 year to date sales to Huawei represented approximately 15% of total revenue.

Huawei sales make up 15% of optical maker Lumentum's revenue. Its stock plummeted nearly 12%.

The lesson for investors is clear: supplier relationships with dominant customers create extraordinary growth opportunities but also existential concentration risk. Lumentum's subsequent strategy—aggressive M&A to diversify revenue sources and acquire technology capabilities—reflected management's awareness of this vulnerability.

Key Inflection Point #2: M&A Strategy and Consolidation (2018-2023)

The Oclaro Acquisition (2018): Building Scale

Lumentum's M&A strategy began in earnest in 2018, when the company announced what would become a defining transaction for its optical communications business. SAN JOSE, Calif., March 12, 2018 /PRNewswire/ -- Lumentum Holdings Inc. and Oclaro, Inc., a leader in optical components and modules for the long-haul, metro, and data center markets, today announced that the two companies have signed a definitive agreement, unanimously approved by the boards of directors of both companies, pursuant to which Lumentum will acquire all of the outstanding common stock of Oclaro.

On March 12, 2018, Lumentum Holdings, a leading provider of photonics products for optical networking and lasers for industrial and consumer markets, announced that it has entered into a definitive agreement to purchase Oclaro, a leader in optical components and modules for the long-haul, metro, and data center markets, for $1.8 billion in cash and stock.

The strategic rationale was compelling. Oclaro brings its leading Indium Phosphide laser and Photonic Integrated Circuit and coherent component and module capabilities to Lumentum. The combined company will drive innovation faster and accelerate the development of products to enable our customers to win.

Lowe explained that ever since Lumentum became a standalone company three years earlier, the firm had concentrated on addressing the increase in optical communications demand. Execution on major M&As had to wait. The company investigated potential acquisitions and evaluated several key technologies including silicon photonics and indium phosphide. This analysis led to Oclaro with its indium phosphide and photonic integrated circuit expertise.

MILPITAS, Calif., Dec. 10, 2018 /PRNewswire/ -- Lumentum Holdings Inc. today announced that it has completed its previously announced acquisition of Oclaro, Inc. Oclaro's stockholders previously approved the merger agreement relating to Lumentum's acquisition of Oclaro. As a result of the completion of the acquisition, trading in Oclaro common stock on the NASDAQ Stock Market will cease today. "I'm excited to close the acquisition and now move forward with realizing the strong potential of the combined company. The combined scale, resources, talent, and breadth of technologies will help us accelerate innovation and the development of the products our customers and network operators around the world need to handle the tremendous and unrelenting growth in network bandwidth," said Alan Lowe, president and CEO of Lumentum.

The Coherent Saga (2021): The One That Got Away

The most dramatic chapter in Lumentum's M&A history was the bidding war for Coherent—a saga that demonstrated both the opportunities and pitfalls of large-scale consolidation in the photonics industry.

Over the past few weeks Santa Clara-based Coherent, one of the best-known and historic brands in the laser business, has been subject to a bidding war between rivals Lumentum, MKS Instruments, and II-VI. That was sparked by the initial merger agreement between Lumentum and Coherent back in January, a cash-plus-stock deal valuing Coherent at $5.7 billion. Although the figure represented a 50 per cent premium on Coherent's stock price valuation at the time, subsequent unsolicited bids from MKS and II-VI, plus a series of revisions as the rival bidders upped the ante on the initial Lumentum deal, drove the acquisition price beyond $7 billion.

The timeline of escalating bids reads like corporate warfare:

- January 2021: Coherent accepts $5.7 billion offer from Lumentum

- February 8: MKS Instruments offers $6 billion

- February 12: II-VI offers $6.4 billion

- March 8: II-VI's revised $6.5 billion offer deemed superior

- March 9: Lumentum agrees to amended $6.6 billion merger

- March 12: II-VI offers $6.8 billion

- March 17: Both Lumentum ($6.9 billion) and II-VI ($7.01 billion) submit new offers

- March 22: Lumentum raises to $7.03 billion

- March 25: Coherent terminates Lumentum agreement in favor of II-VI

Lumentum noted Coherent's Board of Directors chose to accept an offer that is inferior in overall value and cash consideration. Using the closing prices as of March 24, 2021, Lumentum's offer had a value of $283.12 while the value of II-VI Incorporated's offer was $281.21. Lumentum's offer consisted of $230 in cash and 0.6724 shares of Lumentum stock for each share of Coherent. II-VI's offer consisted of $220 in cash and 0.9100 shares of II-VI for each share of Coherent.

Coherent's rejection of the Lumentum merger also means that a termination fee of $217.6 million will now be payable to the latter, in accordance with a clause in the original merger agreement from January. Coherent has confirmed that it will make this payment.

The termination fee of over $200 million provided meaningful compensation for a deal that ultimately didn't close. For investors, the Coherent saga illustrates the importance of disciplined bidding in contested M&A situations—Lumentum walked away rather than overpay, preserving capital for future opportunities.

NeoPhotonics Acquisition (2022): Silicon Photonics Capabilities

Lumentum agreed to acquire NeoPhotonics for $16 per share in cash (a total equity value of about $918m).

Lumentum Holdings Inc of San Jose, CA, USA has completed its acquisition (announced on 3 November) of San Jose-based NeoPhotonics Corp. NeoPhotonics is a vertically integrated designer and manufacturer of silicon photonics and hybrid photonic integrated circuit (PIC)-based lasers, modules and subsystems for high-speed communications.

SAN JOSE, Calif., Aug. 3, 2022 /PRNewswire/ -- Lumentum Holdings Inc. today announced that it has completed its previously announced acquisition of NeoPhotonics Corporation. "I am excited to unite NeoPhotonics' differentiated products and technology and talented team with those of Lumentum," said Alan Lowe, Lumentum President and CEO. "This acquisition better positions us for attractive growth opportunities created by the digital transformation of work and life, which is driving relentless growth in the needed volumes and performance of cloud and network infrastructure. I welcome our new colleagues to the Lumentum team."

NeoPhotonics had been hit badly by the long-running US campaign against Huawei. Unable to sell most products to a company that was previously its biggest customer, it had suffered a 31% year-on-year drop in sales for the first nine months of 2021, to about $210 million. This created an acquisition opportunity for Lumentum at a reasonable valuation while adding critical 400G and greater transmission technology, including silicon photonics, narrow-linewidth tunable lasers, and RF integrated circuits.

Cloud Light Acquisition (2023): Entering the Transceiver Business

The most strategically significant recent acquisition positioned Lumentum squarely in the AI data center build-out. SAN JOSE, Calif.--(BUSINESS WIRE)-- Lumentum Holdings Inc. today announced that it has completed its previously announced acquisition of Cloud Light Technology Limited. "I am excited to add Cloud Light's high-speed optical transceiver products, differentiated technology, and talented team to Lumentum," said Alan Lowe, Lumentum President and CEO. "Cloud operators have embraced this transaction, recognizing the enhanced customer value proposition it brings through leading-edge technology, a broader product portfolio, and strengthened supply chain security, all at a time when Artificial Intelligence is driving data center compute capacity to its limits." Under terms of the merger agreement, Lumentum acquired Cloud Light with a transaction value of approximately $750 million.

The transaction is expected to be immediately accretive to Lumentum's non-GAAP earnings per share and is expected to more than double Lumentum's cloud data center infrastructure revenue in the 12-month period following the transaction close. The highly complementary combination squarely positions Lumentum as a leader in providing photonics to cloud operators, enabling more than a five-fold expansion in the company's served opportunity inside of data centers. In the last twelve months, over 90 percent of Cloud Light's more than $200 million in revenue was derived from 400G and higher speed products, and in their most recent quarter, over half of Cloud Light's optical transceiver revenue was derived from 800G transceivers.

The Cloud Light acquisition strengthened Lumentum's datacom transceiver business and expanded its vertical integration across lasers, chips, assemblies, and fully packaged optical modules.

Key Inflection Point #3: The AI Data Center Revolution (2023-Present)

The Infrastructure Imperative

The explosive growth of artificial intelligence workloads has created unprecedented demand for data center connectivity—and optical networking sits at the heart of this transformation. Across cloud providers, data center power consumption is increasing at nearly a 20% CAGR through 2029. Within the data center, optical lane counts are expected to grow more than 45% annually.

As AI workloads grow exponentially, optical link speeds in AI back-end networks are doubling approximately every two years — driving a critical need for innovation in leading-edge photonic technologies.

As the digital world accelerates its transformation, data centers must evolve to keep pace. Lumentum's Cloud and Networking solutions—ranging from high-speed lasers, photonic chips, and pluggable transceivers, to scalable optical switching and CPO—provide a path to a more energy-efficient and sustainable future.

The NVIDIA Partnership

The validation of Lumentum's technology leadership came through a strategic partnership announcement that reverberated through the industry. SAN JOSE, Calif.--(BUSINESS WIRE)-- Lumentum Holdings Inc., a market-leading designer and manufacturer of innovative optical and photonic products for cloud, networking and industrial applications, has been selected as a key contributor in NVIDIA's silicon photonics ecosystem. Lumentum's high-power, high-efficiency lasers have a crucial role in the development and deployment of new NVIDIA Spectrum-X Photonics networking switches. This collaboration highlights Lumentum's differentiated laser technology and commitment to scale AI infrastructure through photonic advancements. Scaling AI factories presents significant power consumption challenges. NVIDIA's newly announced Spectrum-X Photonics and Quantum-X Photonics networking switches integrate photonic innovations, including Lumentum's high-power, high-efficiency lasers, to significantly reduce power consumption, enhance resilience, and enable faster deployment.

"Photonics switch technology will revolutionize data centers and advance a new wave of AI factories," said Gilad Shainer, Senior Vice President of Networking at NVIDIA.

Lumentum was recently selected as an NVIDIA silicon photonics ecosystem partner and Lumentum's ultra-high-power, high-efficiency lasers are integrated into NVIDIA's newly announced Spectrum-X Photonics and Quantum-X Photonics networking switches. InP photonic technology is a critical enabler of AI data center compute capacity growth. Lumentum continues to innovate and be at the forefront of InP photonic technology and is collaborating closely with industry leaders to shape long-term technology roadmaps.

Technology Roadmap

At the core of Lumentum's innovation lies its advanced indium phosphide (InP) platform, enabling ultra-high-speed optical links—up to 200 Gbps per lane today and expected to scale to higher rates in the near future. Lumentum's energy-efficient InP technology underpins pluggable optical transceivers operating at 400 Gbps, 800 Gbps, 1.6 Tbps, and beyond.

Lumentum has long been a leader in high-performance indium phosphide laser solutions for data infrastructure. This new laser technology complements its existing electro-absorption modulated lasers (EMLs), which power many of today's 400Gb/s, 800Gb/s, and upcoming 1.6Tb/s optical transceivers in cloud and AI data centers.

Lumentum is demonstrating 400 Gbps-per-lane photonic technologies poised to enable the 3.2T generation of optical transceivers at OFC 2025 in live demonstrations and partner announcements, including: 448G EML: Lumentum will demonstrate 448 Gbps data transmission using a 224 GBaud PAM4 externally modulated laser (EML) technology in collaboration with Keysight Technologies and NTT Innovative Devices. Lumentum's high-bandwidth InP EML will enable next generation power-efficient, high-speed optical interconnects for AI and cloud infrastructure. 450G PAM4 DFB-MZI: A live demonstration of Lumentum's 450 Gbps PAM4 distributed feedback (DFB) laser with an integrated Mach-Zehnder (MZI) modulator will highlight another of Lumentum's 400 Gbps-per-lane technologies.

Co-Packaged Optics: The Next Frontier

These solutions are essential for scaling today's AI infrastructure that powers everything from large language models to real-time data analytics. Looking ahead, one of the most exciting developments on the horizon is the move toward co-packaged optics (CPO). The concept of CPO is to integrate optical connectivity in the same package as the host IC (GPU, CPU, Ethernet switch or any other ASIC). This integration brings the ability to support very high bandwidth density links with very low power consumption over extended distances, enabling larger AI compute clusters spanning multiple equipment racks. Although its initial applications will be for AI scale-out networks, this innovation is key to supporting the next generation of AI accelerator scale-up.

Lumentum is a primary supplier to the industry of ultra-high-power (UHP) lasers, essential components in Co-Packaged Optics (CPO) platforms. The UHP laser—an ultra-reliable indium phosphide product—is designed and manufactured at Lumentum's Rose Orchard Way semiconductor facility in San Jose, California. Backed by decades of experience in high-power telecom lasers, the UHP laser supports low-power, highly resilient optical networking systems that are foundational to modern AI data centers. "This investment is a testament to our leadership in laser and photonic technologies," said Michael Hurlston, president and CEO of Lumentum. "Our commitment to expanding domestic manufacturing not only supports a robust AI infrastructure supply chain but also reinforces America's role in global technology leadership."

It also continued shipments of ultrahigh-power lasers for co-packaged optics (CPO) solutions (prior to a broader ramp expected in calendar second-half 2026). "We just received the largest single purchase commitment in company history for our ultra-high power lasers, and we have already announced additional investment in our US-based indium phosphide wafer fab to support it. Our investments in this facility will position us for a significant revenue ramp in CPO by 2026," says Hurlston.

Leadership Transition and New Strategic Direction

Michael Hurlston Takes Command

In February 2025, Lumentum announced a significant leadership transition. Lumentum Holdings Inc of San Jose, CA, USA has appointed Michael Hurlston as president & CEO and director, effective 7 February. He succeeds Alan Lowe, who has served as president & CEO since 2015 and will continue to serve on the board of directors and as an advisor. Hurlston has over 30 years of senior leadership experience within the industry. He joins Lumentum from Synaptics Inc, a pioneer of human interface hardware and software, where he was president & CEO and a member of its board of directors since joining the company in August 2019. From January 2018 to August 2019, he was CEO and a member of the board of optical communications firm Finisar Corp, where he oversaw its acquisition by II-VI Inc.

Hurlston's background was particularly relevant: his experience at Finisar meant he understood the optical communications industry intimately, including as a competitor to Lumentum. His tenure at Broadcom brought semiconductor industry operational discipline.

"We are delighted to welcome Michael as Lumentum's CEO as we exit a strong first half of our fiscal year," said Penny Herscher, Chair of Lumentum's Board of Directors. "We are confident he will help us continue and grow our current strong momentum in our cloud/AI data center strategy and build upon our success in the networking and industrial markets – contributing to an accelerated multiyear growth trajectory. Michael's global experience, with his combined background in semiconductors and the optical communications industry, and his proven ability to lead through sustained periods of profitable growth, makes him uniquely qualified to lead our company in this specialized segment of the industry."

"In my first 90 days as CEO, it's become clear that Lumentum is uniquely positioned to lead as the convergence of optics and electronics accelerates AI data center scaling. Our innovations—from advanced EMLs to ultra-high-power lasers—are driving transformative power efficiencies across cloud, AI, and long-haul networks, making us an essential partner in this next era of connectivity," said Michael Hurlston, President and CEO. "In Q3, we exceeded the high end of our guidance for both revenue and EPS, fueled by strong demand from cloud customers and a recovering networking market. Despite ongoing macroeconomic volatility, we believe AI-driven cloud growth will continue to drive our financial momentum into Q4 and beyond."

Business Model and Technology Deep Dive

Product Portfolio

Lumentum is an industry leading designer and manufacturer of innovative photonics-based solutions that accelerate the speed, scale, and sustainability of global communication networks and commercial laser-based applications. Lumentum optical components and subsystems are part of virtually every type of telecom, enterprise, and data center network. Lumentum commercial lasers enable advanced manufacturing techniques and diverse applications including next-generation imaging and sensing capabilities.

Lumentum's portfolio spans photonic components such as EML and DML lasers, CW lasers, VCSELs, pump lasers, coherent components, and various wavelength-management devices, as well as complete systems including high-speed cloud transceivers, ZR/ZR+ DCI modules, optical circuit switches, and industrial lasers.

Segment Structure

Prior to the 2024 fiscal year, Lumentum divided its products into two reportable segments—Optical Communications ("OpComms") and Commercial Lasers ("Lasers"). The company now classifies its products as Cloud & Networking and Industrial Tech.

Lumentum Holdings Inc. manufactures and sells optical and photonic products in the Americas, the Asia-Pacific, Europe, the Middle East, and Africa. The company operates through two segments: Cloud & Networking and Industrial Tech. The Cloud & Networking segment offers components, modules, and subsystems to support the high-speed transmission of data over high-capacity fiber optic links in cloud data center, AI/ML, enterprise and communications services networking applications. It offers high-speed transceivers, reconfigurable optical add/drop multiplexers, coherent dense wavelength division multiplexing pluggable transceivers, and tunable small form-factor pluggable transceivers.

For its fiscal full-year 2025, Lumentum Holdings Inc. has reported revenue of $1645m, up 21% on $1359.2m in fiscal 2024. Specifically, Cloud & Networking segment revenue rose by 30% from $1084.9m to $1410.8m. Industrial Tech segment revenue fell by 14.6% from $274.3m to $234.2m. Fiscal fourth-quarter 2025 revenue was $480.7m, up 13.1% on $425.2m last quarter and 55.9% on $308.3m a year ago.

Manufacturing Footprint

The company operates globally with significant manufacturing presence in the US, Canada, China, Hong Kong, Thailand, the Netherlands, Taiwan, Switzerland, Israel, and Japan.

Photonics company says 'skyrocketing' bandwidth demands of AI data centers is behind strategic investment. Since acquiring the Hong Kong-based transceiver business Cloud Light - originally a TDK spin-off - last November, Lumentum has been able to target the fast-growing AI data center market with both transceiver products and laser components. Lowe and his team believe that the Thailand facility ramp will enable the firm to lead an initial wave of 1.6 Tb/s transceivers that will end up becoming the "workhorse" of next-generation data centers. "High-speed data center demand is skyrocketing."

Lumentum, a leading US semiconductor firm, has announced plans to expand its manufacturing base in Thailand and establish a new photonics chip R&D and design centre. The investment focuses on high-performance photonics chips used in AI, fibre optics, and data centre technologies. The latest project approved by the BOI will see Lumentum invest more than 2.3 billion baht to expand its Thai operations with a new facility producing ultra-high-power chip-on-carrier light-emitting chips. These advanced chips will be used in high-precision or high-performance applications such as AI processors (GPUs), laser-based medical devices, and intelligent vehicles. Beyond manufacturing, Lumentum has played a key role in building Thailand's photonics chip ecosystem by attracting over 20 global suppliers to establish production bases in the country.

In 2024, exports from the Thai plant were worth over 14 billion baht, with the company forecasting that output will more than double in 2025.

To prepare for expected demand, Lumentum is investing heavily in building out production capacity at its production facility in Thailand. As most of Cloud Light's existing transceiver manufacturing is done in China, the focus on the Thai facility will help the company offer outside-of-China manufacturing that customers increasingly demand amid geopolitical tensions.

Competitive Landscape and Strategic Analysis

Key Competitors

Lumentum operates in the highly competitive optical communications and photonics markets. In the optical communications segment, Lumentum's primary competitors include Coherent Corp. (formerly II-VI), Ciena Corporation, and Applied Optoelectronics. In the commercial lasers segment, Lumentum competes with IPG Photonics, nLIGHT which specializes in high-power semiconductor and fiber lasers, and MKS Instruments.

Consolidation Wave

The industry has undergone significant consolidation over the past decade. Since 2015, Lumentum has grown through the acquisitions of rival Oclaro in 2018, component maker NeoPhotonics in 2022, and transceiver specialist Cloud Light in 2023. Coherent (formerly II-VI) has similarly grown through acquisitions including Finisar and the old Coherent laser business.

Porter's Five Forces Analysis

Threat of New Entrants: LOW-MEDIUM

High barriers exist due to decades of accumulated IP and manufacturing know-how inherited from JDSU. Capital intensity of InP wafer fabs and precision manufacturing creates substantial entry costs. Customer qualification cycles can take 12-24 months. Specialized talent is scarce. However, well-funded Asian competitors (especially Chinese) are investing heavily in domestic optical capabilities.

Bargaining Power of Suppliers: MEDIUM

Specialty semiconductor materials (indium phosphide, gallium arsenide) have limited suppliers globally. Supply chain volatility, particularly in semiconductor materials, continues to affect lead times. Lumentum's vertical integration strategy helps mitigate this risk.

Bargaining Power of Buyers: MEDIUM-HIGH

Major customers include hyperscale cloud providers (Amazon, Microsoft, Google, Meta) and large telecommunications equipment manufacturers. These buyers have significant purchasing power and can exert pressure on pricing. However, the technical complexity and qualification requirements create switching costs.

Threat of Substitutes: LOW

Optical connectivity has no practical substitute for high-bandwidth, long-distance data transmission. Copper connectivity is reaching physical limits in data centers, creating tailwinds for optical solutions. Co-packaged optics represents an evolution, not a substitution threat.

Competitive Rivalry: HIGH

Intense competition from Coherent, Infinera, and Applied Optoelectronics among others. Price pressure is persistent. However, technology differentiation in areas like EML performance and CPO positioning can create competitive moats.

Hamilton Helmer's 7 Powers Framework

Process Power: Lumentum has accumulated decades of manufacturing expertise in indium phosphide fabrication—a capability that is extremely difficult to replicate. The precision required for optical components creates process advantages that compound over time.

Scale Economies: Industry consolidation has created scale advantages in R&D and manufacturing. Lumentum's acquisitions have built a portfolio of capabilities that would be prohibitively expensive for new entrants to assemble.

Network Effects: Limited direct network effects, though relationships with ecosystem partners like NVIDIA create indirect benefits.

Counter-Positioning: Lumentum's focus on premium, high-performance components positions it differently from commodity-focused competitors. The company's willingness to walk away from the Coherent bidding war demonstrates disciplined positioning.

Switching Costs: Customer qualification cycles of 12-24 months create meaningful switching costs. Once designed into a customer's products, Lumentum components become sticky.

Branding: Limited relevance in B2B component markets.

Cornered Resource: Access to specialized talent and intellectual property accumulated over decades represents a meaningful cornered resource.

Financial Performance and Investment Considerations

Recent Results

Lumentum Holdings demonstrated robust performance in Q4 2025, with a 21% increase in full-year revenue compared to FY24, reaching $1.65 billion. The company's strategic focus on optical hardware, driven by the AI and cloud revolution, has positioned it well within the industry. Lumentum Holdings Inc. reported strong financial results for the fourth quarter of fiscal year 2025, surpassing analysts' expectations with an earnings per share (EPS) of $0.88, compared to the forecasted $0.80. The company also reported revenue of $480.7 million, exceeding the expected $467.31 million.

According to InvestingPro data, LITE has demonstrated remarkable momentum with a 166% return over the past year, making it one of the top performers in its sector. The company's market capitalization now stands at $8.29 billion.

Q4 Revenue: $480.7 million, exceeding forecasts and previous guidance. Full Year FY25 Revenue: $1.65 billion, up 21% from FY24. Q4 Non-GAAP EPS: $0.88, a 10% surprise over the forecast. Q4 Non-GAAP Gross Margin: 37.8%, up 260 basis points sequentially. Q4 Non-GAAP Operating Margin: 15%, up 420 basis points sequentially. Cash and Short-Term Investments: $877 million.

Forward Guidance

Looking ahead, we expect continued strong demand for our AI data center and long-haul solutions, giving us confidence in surpassing $600 million in quarterly revenue by June 2026 or earlier.

For fiscal first-quarter 2026, Lumentum expects revenue to grow to a record $510–540m, driven by sequential growth in the Cloud & Networking segment (with strong growth across the portfolio of products addressing cloud and AI applications), as Industrial Tech segment revenue will be roughly flat. Operating margin should rise to 16–17.5%. Diluted earnings per share should increase to $0.95–1.10.

Lumentum's ability to expand both gross and operating margins while investing in capacity and innovation supports a structurally higher earnings base and greater flexibility for future growth initiatives. Management projects fiscal Q1 2026 non-GAAP revenue of $510 million to $540 million, non-GAAP operating margin of 16% to 17.5%, and non-GAAP diluted EPS of $0.95 to $1.10. Quarterly revenue (non-GAAP) is expected to surpass $600 million by fiscal Q4 2026 or earlier, with non-GAAP gross margin anticipated to approach 40% at that run-rate.

Key Performance Indicators to Monitor

For long-term fundamental investors evaluating Lumentum's ongoing performance, three KPIs warrant particular attention:

-

Cloud & Networking Segment Revenue Growth Rate: This metric captures Lumentum's success in the AI data center build-out. Sequential and year-over-year growth in this segment reflects design wins, capacity expansion success, and market share gains against competitors.

-

Gross Margin Trajectory: Lumentum's gross margin reflects product mix (higher-margin components vs. lower-margin modules), manufacturing efficiency, and pricing power. The path from current mid-30s percentages toward the targeted 40% level will indicate whether the business is achieving the scale and mix benefits management anticipates.

-

Book-to-Bill Ratio and Backlog Commentary: In a demand environment characterized by capacity constraints, the relationship between orders and shipments provides visibility into future revenue and customer commitment levels.

Bull and Bear Case Analysis

Bull Case

AI Infrastructure Spending Persistence: The capital expenditure plans of hyperscale cloud providers suggest AI infrastructure spending will continue at elevated levels for years. Lumentum's positioning in high-speed transceivers, EML chips, and CPO lasers places it at the center of this spending wave.

Technology Leadership in CPO: The largest purchase commitment in company history for ultra-high-power lasers, combined with the NVIDIA partnership, suggests Lumentum has secured a leading position in co-packaged optics—a technology transition that could represent a multi-billion-dollar market within five years.

Vertical Integration Benefits: The Cloud Light acquisition provides Lumentum with transceiver manufacturing capability, enabling fuller value chain capture and reducing dependency on third-party module makers.

Operating Leverage: As revenue scales toward management's $600 million quarterly target, gross margins approaching 40% and operating margins approaching 20% would transform the earnings power of the business.

Geopolitical Tailwinds: Demand for non-China manufacturing positions Thailand facilities favorably as customers seek supply chain diversification.

Bear Case

Customer Concentration Risk: Hyperscale cloud providers represent significant revenue concentration. A pause in spending by major customers—whether due to economic conditions, technology transitions, or competitive dynamics—would materially impact results.

Technology Transition Execution: The shift to CPO and higher-speed transceivers requires flawless execution on new product development and manufacturing ramp. Any delays could allow competitors to capture share.

China Export Restrictions: Ongoing and potentially expanding US export controls limit addressable market in China and create uncertainty for customer relationships.

Industrial Tech Weakness: The Industrial Tech segment, while smaller, has shown weakness. Continued softness in industrial laser markets would offset some of the Cloud & Networking strength.

Valuation: Strong stock performance has expanded multiples. Any disappointment in growth trajectory could result in multiple compression.

Risk Factors

Material Regulatory Overhang: US-China technology tensions continue to evolve. Additional export restrictions could impact both revenue (lost sales to Chinese customers) and costs (supply chain disruptions).

Competition: Coherent and other competitors are investing heavily in similar technologies. Market share in components is never permanently secured.

Apple Dependency (Historical): While reduced from peak levels, Apple-related VCSEL revenue remains meaningful. Further share loss would pressure Industrial Tech segment.

Conclusion: The Light at the End of the Fiber

Lumentum's journey from dot-com casualty to AI infrastructure essential encapsulates the dynamics of technology investing across market cycles. The company emerged from the ashes of JDSU through patient restructuring, strategic spinoff, and disciplined execution. It rode the smartphone 3D sensing wave while building optical communications capabilities through targeted M&A. And it has positioned itself at the nexus of the AI data center build-out that now commands hundreds of billions of dollars in capital expenditure.

The latest closing stock price for Lumentum Holdings as of November 04, 2025 is 188.36. The all-time high Lumentum Holdings stock closing price was 214.28 on October 29, 2025. The Lumentum Holdings 52-week high stock price is 214.50, which is 13.9% above the current share price.

The company's technology leadership in indium phosphide—accumulated over decades—creates process power that is genuinely difficult to replicate. Its manufacturing footprint, spanning US-based fabs for critical components and Thailand facilities for assembly and test, provides both scale and geographic diversification. Its customer relationships with hyperscale cloud providers and partnerships with NVIDIA validate the strategic positioning.

Yet the competitive landscape remains intense. Coherent, formed through the combination of II-VI and the old Coherent laser business, represents a formidable competitor with broad capabilities. Technology transitions in optical networking require continuous innovation. And the cyclicality inherent in technology capital spending means that today's capacity constraints can become tomorrow's overcapacity.

For investors, Lumentum offers exposure to one of the most compelling secular trends in technology—the explosive growth of data requiring ever-faster optical connectivity. The company's heritage, technology portfolio, and strategic positioning create a differentiated investment thesis. The question is whether execution continues to match opportunity as the AI infrastructure build-out unfolds.

The light behind the data age, as it turns out, comes from San Jose—by way of Ottawa and a garage startup in 1979—through indium phosphide lasers operating at the absolute frontier of what photonics can achieve.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube