EnerSys: The Hidden Giant Powering the Industrial World

I. Introduction & Episode Roadmap

Picture this: Somewhere deep in a nondescript warehouse in Reading, Pennsylvania, sits a battery that has traveled to space, orbited Mars, and now powers the James Webb Space Telescope—humanity's most powerful eye into the cosmos. That same company's products keep your Amazon orders moving through fulfillment centers, ensure your phone call doesn't drop when the grid fails, and provide backup power to every major telecom tower you've ever driven past.

EnerSys is a global leader in stored energy solutions for industrial applications and designs, manufactures, and distributes energy systems solutions and motive power batteries, specialty batteries, battery chargers, power equipment, battery accessories and outdoor equipment enclosure solutions to customers worldwide. Yet despite being the largest industrial battery manufacturer on Earth, with customers in over 100 countries, most people have never heard of them.

Here's the hook that makes this story worth telling: How did a private equity carve-out from a Japanese battery company transform into a $3.6 billion revenue industrial technology leader and become the backbone of critical infrastructure that modern society literally cannot function without?

For fiscal 2025, ENS reported net revenues of $3.62 billion, which increased 1% year over year. The company's adjusted earnings were $10.15 per share, up 21.6% year over year. Those numbers represent a remarkable twenty-year journey from a leveraged buyout to a publicly traded industrial powerhouse.

The company goes to market through four lines of business: Energy Systems, Motive Power, Specialty and New Ventures. Each segment tells a different story about critical infrastructure: Energy Systems, which combine power conversion, power distribution, energy storage, and enclosures, are used in the telecommunication, broadband and utility industries, uninterruptible power supplies, and numerous applications requiring stored energy solutions. Motive power batteries and chargers are utilized in electric forklift trucks and other industrial electric powered vehicles. Specialty batteries are used in aerospace and defense applications.

The themes we'll explore form a masterclass in industrial consolidation: the roll-up strategy that private equity loves, the "boring but essential" market that creates durable competitive advantages, the lead-acid to lithium transition that threatens and enables legacy players simultaneously, and how mission-critical infrastructure creates moats that competitors struggle to breach.

This is a story about patience, about strategic M&A executed over decades, and about betting on the infrastructure that powers everything else. Let's begin.

II. The Battery Industry Context: Why Industrial Batteries Matter

Walk into any modern warehouse and watch the electric forklifts glide silently between towering racks of inventory. Those vehicles run on industrial batteries—not the lithium packs you'd find in a Tesla, but heavy-duty lead-acid or thin-plate pure-lead cells designed to endure thousands of charge-discharge cycles in demanding environments. When one fails unexpectedly, an entire distribution center can grind to a halt, costing retailers millions in delayed shipments.

That's the industrial battery market: unglamorous, absolutely essential, and invisible until something goes wrong.

Understanding the difference between consumer and industrial batteries is crucial to appreciating EnerSys's position. Consumer batteries power your smartphone, laptop, or electric vehicle—high-profile applications that attract venture capital and magazine covers. Industrial batteries, by contrast, provide backup power to data centers, keep telecom towers operational during outages, power the forklifts that move global commerce, and enable military systems that must never fail.

Motive power batteries and chargers are utilized in electric forklift trucks and other commercial electric powered vehicles. Reserve power batteries are used in the telecommunication and utility industries, uninterruptible power supplies, and numerous applications requiring stored energy solutions including medical, aerospace and defense systems. Outdoor equipment enclosure products are utilized in the telecommunication, cable, utility, transportation industries and by government and defense customers.

Consider what happens when data center backup power fails. In 2017, a British Airways IT system failure grounded flights for three days and cost the airline an estimated £80 million. The cause? A power surge that compromised backup systems. This is why companies pay premium prices for reliable industrial batteries—the cost of failure far exceeds the cost of quality.

The telecom sector provides another window into this market's criticality. Every cell tower requires backup power to maintain service during grid outages—a requirement that became starkly visible during natural disasters like Hurricane Maria in Puerto Rico, where tower failures left millions without communication for weeks. Telecom operators don't negotiate aggressively on battery prices; they negotiate on reliability guarantees and service-level agreements.

EnerSys and its predecessor companies have been manufacturers of industrial batteries for over 125 years. That century-plus heritage matters in an industry where customers need assurance that their supplier will still be around in twenty years to service equipment, honor warranties, and provide replacement parts.

The market's fragmented nature before the late 1990s created the opportunity that would eventually define EnerSys. Industrial battery manufacturing was scattered across dozens of regional players, each with limited scale, inconsistent quality standards, and incomplete geographic coverage. Global customers—telecom giants, logistics companies, defense contractors—increasingly needed suppliers who could serve them worldwide with consistent products and support.

This fragmentation was a classic private equity opportunity: identify an industry ripe for consolidation, acquire the best assets, achieve economies of scale, and create a platform that provides value customers cannot get elsewhere. The question was who would execute it.

For investors, the industrial battery market offers characteristics rarely found together: recession-resistant demand (backup power needs don't disappear in downturns), high switching costs (customers don't change battery suppliers lightly), and exposure to secular growth trends (5G deployment, data center expansion, warehouse automation). Understanding these dynamics is essential to evaluating EnerSys's competitive position.

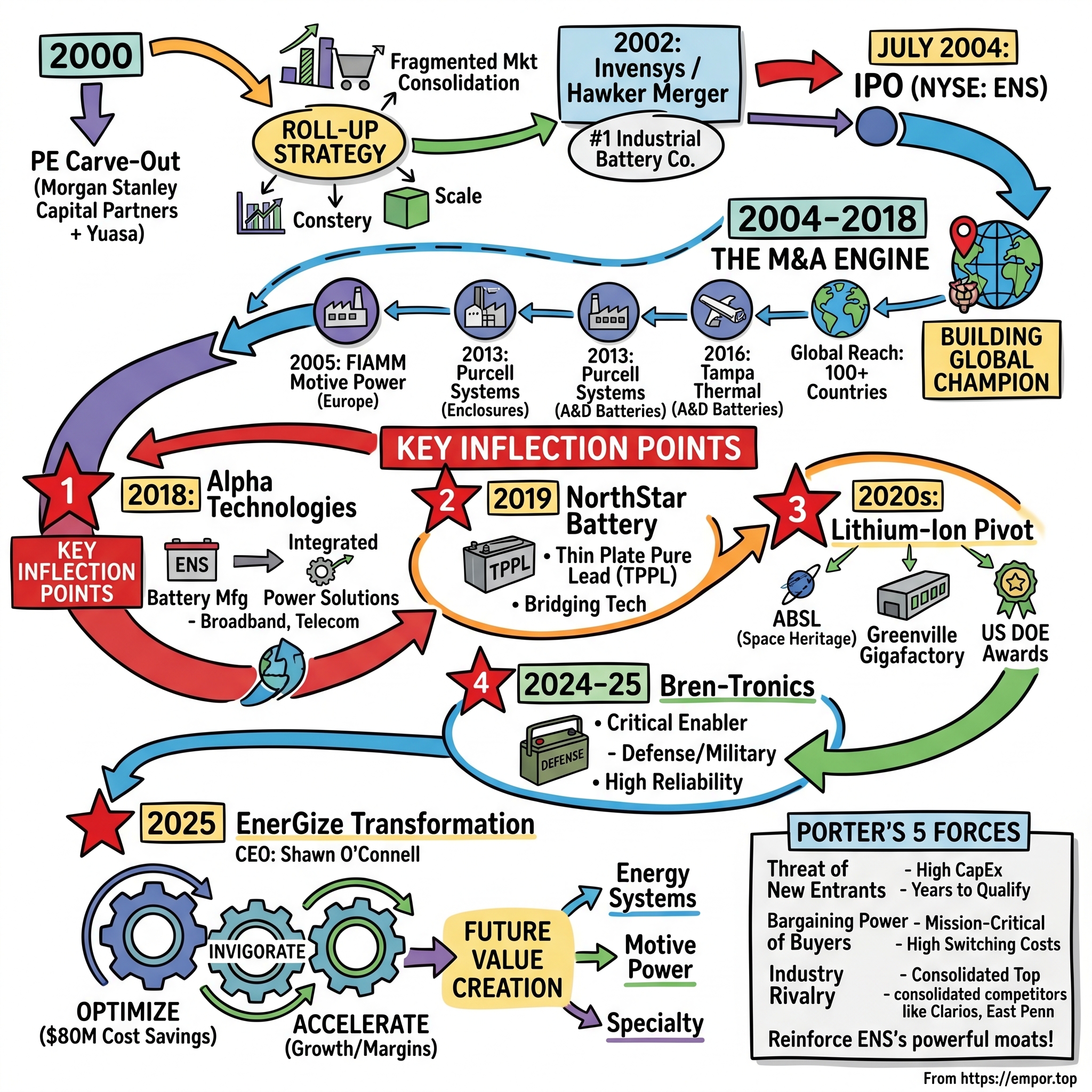

III. Origins: The Private Equity Playbook (2000–2004)

In late 2000, a small team at Morgan Stanley Capital Partners identified an opportunity hiding in plain sight within Japan's Yuasa Corporation. Yuasa, one of Japan's premier battery manufacturers, held substantial industrial battery operations across North and South America—operations that weren't core to Yuasa's strategic priorities but represented exactly the foundation needed to build a global industrial battery champion.

EnerSys and its predecessor companies have been manufacturers of industrial batteries for over 90 years. Morgan Stanley Capital Partners teamed with the management of Yuasa Inc. in late 2000 to acquire from Yuasa Corporation (Japan) its reserve power and motive power battery businesses in North and South America.

It originated through the acquisition, primarily driven by Morgan Stanley Private Equity, acquiring the industrial battery businesses of Yuasa Corporation and, shortly after, divisions of Exide Technologies. John Craig was the founding CEO. Formed through a leveraged buyout facilitated by private equity investment.

John Craig, the founding CEO, had spent decades in the battery industry and understood both the technical requirements and the commercial dynamics that would make consolidation work. His vision went beyond mere financial engineering—he saw the opportunity to reunite fragmented pieces of what had once been a more integrated global industry.

The initial acquisition from Yuasa represented approximately $400 million in net sales—a solid foundation, but far from the global leader Morgan Stanley envisioned. The real magic would come from what happened next.

The Hawker Group merged with EnerSys in 2002. In 2002 EnerSys acquired Energy Storage Products Group of Invensys for $505 million.

The Invensys acquisition was transformational. John Craig, chairman, president and CEO of EnerSys, stated, "This acquisition significantly enhances the strategic positioning and scale of EnerSys. The combining of the US-based EnerSys and the European-based Energy Storage Products Group will result in the world's largest industrial battery company. The expanded product portfolio, which includes leading brand names such as Exide, Hawker, General and Powersafe, will offer customers the widest product selection available from any one manufacturer."

The European Commission would eventually approve the US$505 million acquisition by U.S. company EnerSys Holdings Inc. of Invensys's Energy Storage Business in March 2002.

In a single stroke, EnerSys had transformed from a regional American operator into a genuinely global industrial battery powerhouse. The Invensys acquisition brought European manufacturing, established relationships with European telecom and utility customers, and a portfolio of brand names that carried significant equity in industrial markets.

The initial carve-out and consolidation strategy was fundamental. Reuniting major industrial battery businesses under one roof created immediate scale and market focus.

The roll-up thesis was elegant in its simplicity: industrial battery customers valued reliability, service, and global coverage. Fragmented suppliers couldn't provide consistent global service. By consolidating the best assets under unified management, EnerSys could offer something competitors couldn't match—a true global partner for mission-critical power needs.

Morgan Stanley's private equity playbook involved aggressive cost synergies from combining manufacturing operations, eliminating duplicate overhead, and standardizing product platforms. But the real value creation came from revenue synergies: global customers could now source from a single supplier worldwide, simplifying their procurement and ensuring consistent quality across operations.

In March 2002, we acquired the Energy Storage Group of Invensys plc. We have made over 30 acquisitions since our formation, including the most recent acquisitions of NorthStar Batteries and the Alpha Group of companies in the power electronics markets.

By 2004, EnerSys had achieved something rare in private equity-backed companies: it had built a genuine strategic asset rather than just a financial vehicle. The company possessed #1 or #2 market positions across major industrial battery segments, a global manufacturing footprint, relationships with the largest industrial customers worldwide, and a management team that understood both the technical and commercial aspects of the business.

The stage was set for the next chapter: accessing public markets to fund continued expansion.

IV. Going Public: The IPO and Growth Era (2004–2010)

July 30th, 2024, marked EnerSys' 20th anniversary of our Initial Public Offering (IPO).

EnerSys completed its initial public offering (IPO) July 30, 2004 on the New York Stock Exchange.

When EnerSys rang the opening bell at the New York Stock Exchange in July 2004, it marked more than just a liquidity event for Morgan Stanley's private equity funds. It represented the transformation of a financial thesis into a permanent industrial enterprise—one with access to public capital markets for continued expansion.

We anticipate that the initial public offering price of our common stock will be between $15 and $17 per share. We have applied to list our common stock on the New York Stock Exchange under the trading symbol "ENS".

The IPO prospectus told a compelling story: EnerSys had emerged from consolidation as the clear global leader in industrial batteries, with established positions in every major end market and geography. But the prospectus also disclosed the risks that would shape the company's evolution—cyclical industrial demand, raw material volatility (particularly lead), environmental liabilities from battery manufacturing, and the constant threat of new technologies disrupting lead-acid chemistry.

As of the completion of the offering, assuming no exercise by the underwriters of their over-allotment option, investment funds affiliated with Morgan Stanley & Co. Incorporated, one of the representatives of the underwriters of this offering, will own 61.0% of our common stock.

Morgan Stanley maintained substantial ownership post-IPO, providing stability and ensuring alignment between private equity sponsors and new public shareholders. This staged exit—rather than a complete sale—allowed the company to benefit from continued Morgan Stanley support while accessing public market capital.

The IPO unlocked financing that would fuel the acquisition machine's next phase. Unlike private equity structures constrained by fund timelines and leverage limitations, a public company could pursue strategic acquisitions opportunistically, using stock as currency when appropriate and debt when conditions favored cash transactions.

We have made over 30 acquisitions since our formation.

The acquisition cadence accelerated post-IPO. In 2005, EnerSys acquired FIAMM's motive power battery business, strengthening its European position. We acquired the reserve and motive power business of the Energy Storage Group of Invensys plc. In 2005, we acquired the motive power battery business of FIAMM, S.p.A.. We also made smaller global acquisitions in areas of specialty nickel-based batteries, lithium power sources, lead-acid batteries, and industrial batteries.

Each acquisition followed a consistent thesis: fill geographic gaps, add technical capabilities, or acquire customer relationships that would be difficult to develop organically. The company became expert at integrating acquisitions—rationalizing manufacturing footprints, standardizing products, and capturing synergies while retaining the customer relationships that made targets valuable in the first place.

The 2008 financial crisis tested this strategy. Industrial demand collapsed as global trade contracted. Warehouse automation projects were delayed or cancelled. Telecom carriers froze capital spending. EnerSys's cyclical exposure became painfully apparent.

Yet the crisis also validated the company's strategic positioning. Customers who had considered switching to lower-cost suppliers discovered the value of reliable partners during disruption. EnerSys's global service capabilities—the ability to support customers across geographies—proved invaluable when supply chains fragmented. The company emerged from recession with stronger customer relationships and a renewed commitment to the value proposition that differentiated it from commodity competitors.

For investors evaluating EnerSys today, the 2004–2010 period established patterns that continue defining the company: disciplined capital allocation, strategic M&A as a core competency, and resilience through economic cycles.

V. The Acquisition Engine: Building Scale Through M&A (2010–2018)

Between 2010 and 2018, EnerSys executed a systematic expansion that transformed it from a consolidated industrial battery company into an integrated power solutions provider. Each acquisition filled specific gaps—geographic, technological, or customer-facing—that management had identified in their strategic planning.

In October 2013, EnerSys acquired Purcell Systems, a company based in Washington State. They are a leading designer, manufacturer, and marketer of thermally managed electronic equipment and battery cabinet enclosures for customers globally in telecommunication, broadband, utility, rail, and military applications.

The Purcell acquisition illustrated EnerSys's evolving vision. Batteries alone weren't enough—customers needed complete power systems including enclosures, thermal management, and integration services. By acquiring Purcell, EnerSys moved up the value chain from component supplier to solutions provider, capturing more revenue per customer relationship.

Based in Tampa, Florida. Acquired in April 2016. A manufacturer of molten salt "thermal" batteries used in powering a multitude of electronics, guidance, and other electrical loads on many of today's advanced weapon systems.

The Tampa thermal battery acquisition signaled EnerSys's growing focus on aerospace and defense—a segment that would become increasingly strategic in subsequent years. Defense applications required specialized batteries with extreme reliability requirements, long qualification cycles, and premium pricing that rewarded technical excellence over cost competition.

Geographic expansion continued in parallel. Acquired in January 2014 with its subsidiaries Battery Power International Pte. Ltd. and IE Technologies Pte. Ltd. based in Singapore. Manufacturer of Motive and Reserve power batteries. The Asia-Pacific acquisitions strengthened EnerSys's position in the world's fastest-growing industrial markets.

The acquisition thesis evolved during this period. Early deals focused on consolidating fragmented markets—buying competitors to achieve scale. Later acquisitions increasingly targeted adjacent technologies and capabilities that would position EnerSys for industry transitions. Management recognized that lead-acid chemistry, while still dominant, faced long-term pressure from lithium-ion alternatives. Rather than ignore this threat, they began systematically building lithium capabilities.

The company acquired a German lithium-ion systems manufacturer in 2011, gaining expertise in space, naval, and renewable energy applications—markets where lithium already commanded premium positions. This wasn't EnerSys betting against its core business; it was hedging against technological disruption while building capabilities for the future.

Throughout this period, EnerSys maintained discipline that many serial acquirers abandon. Integration teams followed standardized playbooks. Synergy targets were publicly disclosed and achieved. Management's compensation tied to both acquisition performance and organic growth prevented the empire-building that destroys value in so many rollup stories.

The M&A engine created competitive advantages that compound over time. With each acquisition, EnerSys expanded its customer relationships, added technical capabilities, and increased scale economies. Competitors faced a growing gap—they couldn't match EnerSys's geographic coverage, product breadth, or service capabilities without their own ambitious acquisition programs.

By 2018, the foundation was set for transformational deals that would fundamentally redefine what EnerSys meant to customers.

VI. KEY INFLECTION POINT #1: The Alpha Technologies Acquisition (2018)

On October 29, 2018, EnerSys announced a deal that would fundamentally transform its strategic positioning. EnerSys announced that it has entered into an agreement to acquire all issued and outstanding shares and certain assets of select entities belonging to the Alpha Technologies group of companies ("Alpha"). Based in Bellingham, Washington, Alpha is a global industry leader in the comprehensive commercial-grade energy solutions for broadband, telecom, renewable, industrial and traffic customers around the world.

Alpha generated $591 million in revenue for the twelve months ending June 30, 2018 and adjusted EBITDA of $67 million, or 11% adjusted EBITDA margin. The transaction enterprise value is 11.1x Alpha's LTM adjusted EBITDA (pre-synergies).

The total acquisition consideration is $750 million, which consists of $650 million in cash, with the remaining $100 million in either cash or EnerSys (ENS) shares, depending on the average share price prior to closing.

The $750 million price tag represented EnerSys's largest acquisition ever—a bet that required conviction about both Alpha's standalone value and the strategic logic of combination. This wasn't a small tuck-in acquisition; it was a transformational move that would reshape EnerSys's business model.

EnerSys President and Chief Executive Officer David M. Shaffer stated, "EnerSys' combination with Alpha creates the only fully-integrated DC power and energy storage solution provider for broadband, telecom and energy storage systems, enabling us to offer a uniquely differentiated value proposition to the marketplace."

Understanding why this combination mattered requires appreciating what Alpha Technologies brought to the table. Alpha wasn't primarily a battery company—it was a power electronics and systems integration specialist. Alpha designed, manufactured, and supported the equipment that converted utility power to DC, managed battery charging, and integrated multiple power sources into reliable backup systems.

Before the acquisition, EnerSys sold batteries that went into Alpha's systems. After the acquisition, EnerSys could offer customers complete solutions: batteries, power electronics, enclosures, software, and ongoing service. This vertical integration created value for customers (single point of accountability) while capturing margin that previously went to intermediaries.

Expands footprint in broadband and telecom markets exposed to favorable growth trends: 5G, DOCSIS3.1, and FTTx. Diversifies revenue and meaningfully expands EnerSys' total addressable market to +$20B.

The timing aligned with massive infrastructure investment cycles. 5G network deployment required thousands of new cell sites and small cells, each requiring backup power. Cable companies upgrading to DOCSIS 3.1 needed power systems at every node. Fiber-to-the-home deployments multiplied the number of powered network elements. Alpha's products addressed all these applications.

Shaffer added, "Our acquisition of Alpha will allow EnerSys to achieve meaningful economies of scale in the short term, while simultaneously increasing our leadership position in a growing market with attractive secular trends. With an expanded total addressable market of approximately $20 billion, combined with an extremely robust product and service offering following the Alpha transaction, we are well positioned to deliver long-term growth and value for our shareholders."

EnerSys expects the acquisition to generate annual run-rate synergies in excess of $25 million and to be accretive to EnerSys' earnings, excluding any one-time or acquisition related costs.

EnerSys announced today that it has completed its acquisition of the Alpha Technologies Group of companies (the "Alpha Group"). The deal closed on December 10, 2018—remarkably fast execution that demonstrated EnerSys's acquisition capabilities.

The strategic significance went beyond immediate financial metrics. By owning both batteries and power electronics, EnerSys could optimize systems holistically—designing batteries that worked better with specific charger profiles, creating software that extended battery life through intelligent charge management, and offering service contracts that covered complete systems rather than individual components.

This integration strategy also raised barriers to entry. Competitors could offer batteries or power electronics, but few could provide both with the depth of integration EnerSys achieved. Customers evaluating backup power solutions increasingly faced a choice: deal with multiple vendors and manage integration complexity themselves, or partner with EnerSys for a complete solution.

The Alpha acquisition marked EnerSys's evolution from battery manufacturer to power solutions provider—a transition that would define its strategic positioning for years to come.

VII. KEY INFLECTION POINT #2: The NorthStar Acquisition and TPPL Strategy (2019)

Less than a year after closing Alpha Technologies, EnerSys announced another significant acquisition that would reshape its technology positioning. On September 19, 2019, the company unveiled plans to acquire NorthStar Battery Company from Altor Fund II.

EnerSys announced that it has entered into an agreement to acquire all issued and outstanding shares of N Holding AB, the parent company of NorthStar, from Altor Fund II. With two production facilities in Springfield, Missouri, NorthStar manufactures and distributes batteries nearest in design and performance to EnerSys TPPL products.

With $78 million cash consideration and the assumption of $104.5 million in debt this acquisition combines world-class complementary products and expedites $500 million of Thin Plate Pure Lead (TPPL) production capacity.

The NorthStar deal was smaller than Alpha in dollar terms but equally significant strategically. It centered on a technology called Thin Plate Pure Lead (TPPL)—an advanced lead-acid chemistry that delivered many benefits associated with lithium-ion batteries while maintaining lead-acid's cost advantages and established recycling infrastructure.

Understanding TPPL's importance requires context about the broader battery technology landscape. Traditional lead-acid batteries—the workhorses of industrial applications for over a century—faced legitimate criticism: heavy weight, limited cycle life, sensitivity to partial state-of-charge operation, and relatively slow recharge rates. Lithium-ion batteries addressed many of these limitations but came with their own challenges: higher costs, thermal management requirements, nascent recycling infrastructure, and supply chain dependencies on minerals sourced from geopolitically complex regions.

TPPL occupied a strategic middle ground. By using pure lead (rather than lead alloys) in thinner plates, TPPL batteries achieved longer cycle life, faster recharge capability, and better performance in demanding applications than traditional lead-acid—while maintaining compatibility with existing charging infrastructure and established recycling processes.

"In line with our previously disclosed strategy to increase sales of premium products we are excited to announce the acquisition of NorthStar, which will enable EnerSys to dramatically accelerate our sales for TPPL batteries."

This transaction will allow a rebalancing of factory loading and a dramatic reduction in inventory, freight, duty and currency risks. It will also allow us to better match the rate and amount of future capital expenditure to specific market requirements." Shaffer continued, "Our premium TPPL core technology distinguishes EnerSys in various vertical markets."

The transaction is predicted to generate annual run-rate synergies in excess of $40 million to EnerSys and to be accretive to EnerSys' earnings, excluding any one-time or acquisition related costs.

The synergy math was compelling. NorthStar's Missouri facilities provided immediately available capacity for EnerSys's high-speed TPPL production line, eliminating the need to build greenfield manufacturing. The acquisition reduced transoceanic shipping—EnerSys had been importing significant TPPL volumes from European factories—cutting costs while improving responsiveness to U.S. customers.

The EnerSys acquisition means it is the only major company to make TPPL batteries.

This competitive positioning mattered enormously. With NorthStar's acquisition, EnerSys consolidated control over TPPL manufacturing, eliminating the only comparable producer. Customers seeking TPPL's performance advantages had one primary supplier: EnerSys.

EnerSys also provides aftermarket and customer support services to its customers in over 100 countries through its sales and manufacturing locations around the world. With the recent NorthStar acquisition, EnerSys has solidified its position as the market leader for premium Thin Plate Pure Lead batteries, which are sold across all three lines of business.

The TPPL strategy represented EnerSys's answer to the lithium-ion challenge—not by abandoning lead-acid, but by pushing the technology's boundaries to maintain relevance in applications where customers weren't yet ready for lithium's costs and complexity. This bridging strategy bought time while EnerSys simultaneously built lithium capabilities.

For investors, the NorthStar acquisition illustrated EnerSys's sophisticated approach to technology transitions. Rather than betting everything on one chemistry winning, management positioned the company across multiple technologies, allowing customer needs—not ideological preferences—to drive product adoption.

VIII. KEY INFLECTION POINT #3: The Lithium-Ion Pivot (2020–Present)

While executing the TPPL strategy, EnerSys leadership recognized that lithium-ion's long-term trajectory was clear even if near-term adoption remained selective. Rather than waiting for disruption to arrive, management began proactive investment in lithium capabilities that would position the company for whatever transition pace materialized.

The lithium pivot accelerated in 2021. ABSL is a world leader in the supply of Lithium-ion batteries for space applications with contracts for over 300 spacecraft and launch vehicles. Today, over 250 spacecraft are powered by ABSL Lithium-ion battery technology.

EnerSys's existing lithium expertise, particularly through its ABSL space battery heritage, provided technical credibility that pure-play lead-acid competitors lacked. This wasn't a company scrambling to learn lithium chemistry—it was expanding lithium applications into commercial and industrial markets where it already possessed relevant expertise.

EnerSys today announced that it has entered into a non-binding Memorandum of Understanding with Verkor SAS, a European leader in battery technology, to explore the development of a lithium battery gigafactory in the United States. Under the Memorandum of Understanding, the companies are developing plans, determining the optimal new factory location, and evaluating various funding and operating structures for this manufacturing facility. This new factory represents a long-term opportunity that will enable growth for both companies and allow EnerSys to optimize cell sizing in battery solutions for its customers, providing independence from non-domestic cell suppliers.

The Verkor partnership, announced in June 2023, signaled EnerSys's commitment to domestic lithium manufacturing at scale. Verkor brought European lithium expertise; EnerSys provided U.S. market access, customer relationships, and financial strength to fund a gigafactory.

EnerSys has announced that it has selected Greenville, South Carolina to develop a lithium-ion cell gigafactory to advance battery production in the United States.

EnerSys has applied for a comprehensive incentive package through $200 million, which includes a combination of short-term and long-term incentives. The Company intends to use a portion of these proceeds, along with the Inflation Reduction Act (IRA) IRC 45X tax benefits and potential additional federal funding, to make a $500 million investment with the potential to create 500 high-quality new jobs.

The operation, which would be the company's second in South Carolina, would manufacture various form factors of lithium-ion cells for commercial, industrial and defense applications, with a production capacity of four gigawatt hours (GWh) per year.

This final agreement secures a $199 million award from the DOE's Office of Manufacturing and Energy Supply Chains, which will support the construction of EnerSys' state-of-the-art lithium-ion cell production facility in Greenville, South Carolina. The Greenville facility will span 500,000 square feet and is set to produce advanced lithium-ion cells for critical applications across commercial, industrial, and defense end markets. The factory will be dedicated to manufacturing cells exclusively for EnerSys products, advancing the Company's ambitions of shaping the future of energy storage and strengthening the U.S. energy supply chain.

The new factory will support the needs of critical customers including the U.S. Department of Defense (DOD), which has specific requirements for domestically sourced batteries. The Company intends to begin construction of the facility in 2025, with commercial production expected to commence in 2028.

The DOE award underscored EnerSys's strategic importance to U.S. energy security. Defense applications increasingly required domestically manufactured batteries—a requirement that Chinese-dependent lithium supply chains couldn't satisfy. By investing in U.S. manufacturing, EnerSys positioned itself as the preferred supplier for customers with national security requirements.

The battery manufacturer, which has operated its Verkor Innovation Center (VIC) in Grenoble since 2023, said EnerSys had recently signed an agreement which will see Verkor develop a new format for the US business' ENS1 battery and produce the product.

French battery maker Verkor, which is planning a 16 GWh gigafactory in Dunkirk, announced, on October 30, 2024, Dutch investor ING Sustainable Investments and US-based EnerSys – which makes batteries for industrial uses – had come on board as shareholders.

The October 2024 equity investment in Verkor deepened the partnership beyond contractual arrangements, aligning incentives between the companies as they pursued joint lithium manufacturing ambitions.

For investors, EnerSys's lithium strategy reflects management's pragmatic approach to technology transitions. Rather than making binary bets on one chemistry winning, the company maintains leadership in advanced lead-acid (TPPL) while building lithium capabilities for applications where the technology's benefits justify its costs. This optionality—rare among industrial companies facing technological disruption—provides downside protection if lithium adoption proves slower than expected while ensuring upside participation if adoption accelerates.

IX. KEY INFLECTION POINT #4: Defense & Aerospace Expansion – Bren-Tronics (2024–2025)

EnerSys today announced it has entered into a definitive agreement to acquire Bren-Tronics, Inc. in an all-cash transaction of $208 million.

The purchase price represents approximately 8.7x Bren-Tronics' adjusted EBITDA for the twelve months ending December 31, 2023. Bren-Tronics, headquartered in Commack, N.Y., is a privately held company with a legacy of innovation since 1973. Bren-Tronics is a leading manufacturer of highly reliable portable power solutions, including small and large format lithium batteries and charging solutions, for military and defense applications. It has approximately 280 employees across the U.S., France, and the U.K., with 2023 sales of approximately $100 million. Bren-Tronics will be integrated within EnerSys' Specialty line of business.

"The acquisition of Bren-Tronics is a strategic move that will strengthen our position as a critical enabler of the energy transition and supports our growth in the attractive and growing military and defense end market," said EnerSys President & CEO David M. Shaffer. "Having partnered with Bren-Tronics to support the Department of Defense (DOD) for over five years, we know the company well. We have tremendous respect for Bren-Tronics' outstanding products that support our military every day and which help save lives on the front lines."

EnerSys announced today that it has completed its acquisition of Bren-Tronics. The acquisition of Bren-Tronics marks a significant milestone in EnerSys' strategic growth and expansion initiatives.

The Bren-Tronics acquisition closed in July 2024, adding a 50-year leader in military portable power to EnerSys's expanding defense portfolio. The deal accelerated EnerSys's lithium expertise while opening new customer relationships within Department of Defense programs.

Defense represents EnerSys's most attractive growth vertical. Military budgets remain robust regardless of economic cycles. Defense customers prioritize reliability over cost. Qualification processes create multi-year switching costs. And domestic manufacturing requirements increasingly exclude foreign suppliers.

Bren-Tronics is a leading manufacturer of highly reliable portable power solutions, including small and large format lithium batteries and charging solutions, for military and defense applications. It has approximately 280 employees across the U.S., France, and the U.K., with 2023 sales of approximately $100 million.

Our product portfolios are highly complementary, with minimal overlap in our product lines. We are excited to integrate Bren-Tronics' exceptional engineering and product development capabilities with our own to drive innovation, deliver enhanced services, and strengthen our relationship with the DOD.

The Bren-Tronics integration delivered results faster than expected. EnerSys delivered 7% revenue growth, our second-highest revenue quarter ever, with performance highlights including record Motive Power margins, significant margin expansion in Energy Systems and Specialty, and strong contributions from the Bren-Tronics acquisition.

EnerSys's defense heritage extends beyond Bren-Tronics to its space battery operations. Pioneering EnerSys ABSL™ products are the space industry's most demonstrated Li-ion batteries. EnerSys ABSL™ supplied the longest operating rechargeable Li-ion battery in space, the first to orbit Earth, Mars and Venus, the closest to orbit the sun and trusted to power the James Webb Telescope.

EnerSys® batteries have been on incredible journeys, orbiting Earth, Mars, Venus, and even powering NASA's Parker Solar Probe on its daring mission to the sun. Over the years, these batteries have accumulated an astonishing 6.8 billion operational cell hours in space as of February 2022, all without a single mission failure, proving reliability beyond measure.

This track record—6.8 billion cell hours without a mission failure—represents the ultimate reliability credential. When Defense Department procurement officers evaluate suppliers, they see a company whose batteries literally power humanity's most demanding space missions.

For investors, the Bren-Tronics acquisition and broader defense positioning offer several attractive characteristics: counter-cyclical demand (defense spending often increases during economic uncertainty), high barriers to entry (years-long qualification processes), premium pricing power (reliability matters more than cost), and alignment with reshoring trends that favor domestic manufacturing.

X. The EnerGize Transformation (2025)

The May 2025 leadership transition from David Shaffer to Shawn O'Connell marked more than a CEO succession—it signaled a strategic pivot toward operational intensity that would reshape EnerSys for its next growth phase.

We have launched EnerGize, our strategic framework to shape the next era of growth for EnerSys. We began executing the first phase of this transformation in July with a workforce reduction and strategic organizational realignment expected to deliver approximately $80 million in annualized cost savings.

The centerpiece of EnerSys' earnings presentation was the introduction of "EnerGize," a comprehensive strategic framework designed to transform and grow the company. This initiative is structured around three key pillars: Optimize, Invigorate, and Accelerate.

EnerSys today announced a workforce reduction affecting approximately 575 employees, or 11% of its non-production global workforce, and is focused primarily on corporate and management positions. This action is part of a strategic restructuring plan under the Company's new leadership to better align resources with current business priorities and long-term objectives.

"Today's actions, while difficult, are necessary for EnerSys to remain competitive in our markets," said Shawn O'Connell, President and Chief Executive Officer of EnerSys. "We've spent the past six months listening, evaluating, and testing how we can best serve our customers, deliver stronger returns, and build a more agile organization."

The workforce reduction targeted management layers rather than production workers—a deliberate choice that preserved operational capabilities while eliminating bureaucratic overhead. This action is more than a cost reduction, this reduces layers of management, enabling us to be much more agile and focused.

As part of the optimization efforts, EnerSys is restructuring for operational efficiency, including an 11% workforce reduction expected to generate $80 million in annualized savings. The company has established Centers of Excellence (CoEs) for Lead Acid, Power Electronics, and Lithium-Ion technologies to drive innovation and operational improvements.

The Centers of Excellence model concentrates technical expertise in focused groups, accelerating decision-making and reducing the complexity that comes with distributed organizations. Each CoE—Lead Acid, Power Electronics, and Lithium-Ion—becomes responsible for advancing its technology while maintaining coordination across business segments.

Capital allocation also received renewed focus. EnerSys announced today that its Board of Directors has approved a $1 billion increase to its stock repurchase authorization, to be executed over the next five years. This authorization brings the Company's total outstanding repurchase authorization to an aggregate of $1.06 billion, including $58 million available under the Board's previous repurchase authorizations.

The $1 billion buyback authorization—massive relative to EnerSys's market capitalization—signals management's confidence in the company's intrinsic value while providing a mechanism to return capital when investment opportunities don't meet hurdle rates. Combined with a 9% dividend increase, EnerGize demonstrates disciplined capital stewardship alongside operational transformation.

For investors, EnerGize represents the kind of self-directed transformation that creates value: cost reductions that fund growth investments, organizational changes that improve execution speed, and capital allocation discipline that ensures returns on invested capital remain attractive. The framework positions EnerSys to weather near-term headwinds while building capabilities for long-term growth.

XI. Business Model Deep Dive

It operates through the following segments: Energy Systems, Motive Power, and Specialty. The Energy Systems segment combines enclosures, power conversion, power distribution, and energy storage used in the telecommunication, broadband, and utility industries. It includes uninterruptible power supplies, and other applications requiring stored energy solutions. The Motive Power segment includes batteries and chargers that are utilized in electric forklift trucks and other industrial electric powered vehicles. The Specialty segment, which is used in aerospace and defense applications, includes large over-the-road trucks, automotive, medical, and security systems applications.

Segment Performance Analysis:

The Energy Systems segment's sales (accounting for 40.9% of total sales) were $399 million, up 8% year over year.

Energy Systems Revenue: Adjusted operating earnings were $35 million, growing by $17 million, with margin up 400 basis points to 8.7%. Motive Power Revenue: $392 million, flat versus prior year due to FX and flat volumes offset by positive price mix; adjusted operating earnings were $67 million, up 15%, with margin at 17.1% (up 240 basis points).

The Specialty segment's sales were $178 million (accounting for 18.9% of total sales), up 21% year over year. The consensus estimate was $165 million. While volume increased 1%, acquisitions had a positive impact of 22% on sales.

The segment dynamics reveal EnerSys's strategic evolution. Energy Systems benefits from data center expansion and telecommunications infrastructure investment. Motive Power generates consistent margins from warehouse automation and material handling. Specialty—now including Bren-Tronics—delivers the highest growth rates driven by defense spending.

Geographic and Supply Chain Positioning:

EnerSys identified approximately $92 million in current direct tariff exposure, with about 65% of global revenue coming from the U.S. The company has implemented a comprehensive mitigation strategy, including a dedicated tariff task force, supply chain and pricing adjustments, and structural buffers such as regional production and dual sourcing.

To put our tariff exposure in perspective, about two-thirds of our global revenue comes from the U.S., in which 80% of our U.S. supply is either domestic or USMCA trade compliant. Only 5% of this is sourced from China, where the highest tariff rates still exist.

As we've previously shared, approximately 22% of our U.S. sourcing is from countries affected by direct tariff costs. Our estimated direct tariff exposure is now some $70 million annualized for fiscal year '26. This has improved from our prior estimate of $94 million as a result of supply chain mitigation activities.

The supply chain positioning reflects decades of strategic footprint decisions. "Produce in region for region" isn't just a slogan—it's embedded in manufacturing strategy, insulating EnerSys from tariff volatility while maintaining responsiveness to local customer needs.

Distribution Model:

EnerSys maintains a dual distribution approach: direct sales teams target Tier 1 enterprise customers requiring custom solutions and technical support, while a global network of authorized distributors serves smaller accounts. This model captures high-value relationships directly while achieving broad market coverage through distribution partners.

Recurring Revenue and Service:

Industrial batteries require ongoing service: maintenance, monitoring, replacement planning, and emergency support. EnerSys's service capabilities create recurring revenue streams that extend beyond initial equipment sales while deepening customer relationships. The Alpha acquisition significantly expanded service revenues by adding power electronics maintenance to the portfolio.

For investors, EnerSys's business model combines characteristics rarely found together: exposure to secular growth trends (5G, data centers, defense modernization, warehouse automation), recession-resistant demand from mission-critical applications, high switching costs from integration complexity and certification requirements, and recurring service revenues that provide visibility into future results.

XII. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

EnerSys and its predecessor companies have been manufacturers of industrial batteries for over 125 years.

Industrial battery manufacturing requires massive capital investment: lead smelting and recycling facilities, precision manufacturing equipment, testing and quality infrastructure, global distribution networks, and technical service capabilities. The capital requirements alone create significant barriers.

But capital is only part of the equation. Customer qualifications take years to complete, particularly in defense and aerospace applications where batteries must meet stringent reliability requirements. EnerSys's track record—including billions of cell hours in space without mission failure—represents decades of accumulated credibility that new entrants cannot replicate quickly.

Regulatory complexity adds another layer. Battery manufacturing involves hazardous materials that require environmental permits, worker safety programs, and waste disposal certifications. Established players have navigated this regulatory landscape; new entrants face lengthy approval processes before they can even begin manufacturing.

2. Bargaining Power of Suppliers: MODERATE

Lead, the primary raw material for most EnerSys products, trades as a commodity on global exchanges. The company hedges a portion of lead exposure through forward contracts, reducing vulnerability to price spikes while maintaining flexibility to benefit from price declines.

Lithium-ion materials present different dynamics. Critical minerals like lithium, cobalt, and nickel face supply chain constraints and geopolitical complexities (cobalt sourcing from Democratic Republic of Congo, lithium concentration in Chile and Australia). EnerSys's Greenville gigafactory investment partially addresses these concerns by establishing domestic lithium cell manufacturing, but the company will remain dependent on upstream mineral suppliers.

Vertical integration through acquisitions has reduced supplier dependency in power electronics and enclosure components—areas where EnerSys previously sourced from third parties now manufactured internally.

3. Bargaining Power of Buyers: LOW-MODERATE

Mission-critical applications fundamentally alter buyer power dynamics. When battery failure means data center outages, manufacturing shutdowns, or military equipment failures, customers don't negotiate aggressively on price—they negotiate on reliability guarantees, service-level agreements, and supplier financial stability.

High switching costs reinforce EnerSys's position. Batteries integrate with specific chargers, monitoring systems, and enclosures. Changing suppliers requires requalifying entire systems—a costly and time-consuming process that customers avoid unless absolutely necessary.

Customer concentration remains modest. EnerSys serves diverse end markets—telecom, data centers, material handling, defense, transportation—with no single customer representing an outsized share of revenue. This diversification prevents any customer from exercising disproportionate power.

4. Threat of Substitutes: MODERATE (but manageable)

The lead-acid to lithium-ion transition represents the primary substitution threat. EnerSys addresses this proactively through TPPL technology (bridging traditional lead-acid and lithium performance), direct lithium investments (Greenville gigafactory, Verkor partnership, Bren-Tronics acquisition), and maintaining chemistry-agnostic customer relationships that position the company regardless of which chemistry wins specific applications.

Alternative energy storage technologies—flow batteries, hydrogen fuel cells, supercapacitors—remain niche in industrial applications where EnerSys competes. None currently offers the combination of cost, reliability, and established infrastructure that lead-acid and lithium-ion provide.

5. Industry Rivalry: MODERATE

Companies such as EnerSys (US), Clarios (US), East Penn Manufacturing Company (US), GS Yuasa International Ltd. (Japan), and Exide Industries Ltd. (India) fall under the winners' category. These are leading players globally in the automotive lead acid battery market.

EnerSys is a key player in industrial batteries, offering motive power and reserve power solutions. East Penn Manufacturing competes strongly in North America.

As the forerunner of the most advanced battery technologies and a global leader with 130+ years of experience in battery manufacturing, Clarios produces more than 150 million batteries every year and powers 1 in 3 of the world's vehicles. Clarios is the world's largest lead-acid battery manufacturer.

The competitive landscape is consolidated at the top. Clarios dominates automotive batteries; EnerSys leads industrial applications; East Penn competes strongly in North American markets. This segmentation reduces direct rivalry in EnerSys's core markets while creating clear competitive differentiation.

Asian manufacturers present increasing competition, particularly in commodity segments. However, defense and aerospace applications—where EnerSys holds strongest positions—require domestic manufacturing and extensive qualification that protect premium market segments.

XIII. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

EnerSys is a global leader in stored energy solutions, specializing in industrial batteries and related technologies. The company manufactures a wide range of energy storage systems, including lead-acid, lithium-ion, and other advanced batteries for various sectors such as telecommunications, electric vehicles (EVs), and renewable energy. The company is recognized for its expertise in energy storage solutions and is the world's largest provider of industrial batteries. It offers products for both backup power and motive power applications.

As the largest industrial battery manufacturer globally, EnerSys achieves unit cost advantages unavailable to smaller competitors. Scale enables efficient manufacturing facilities, favorable raw material purchasing, and comprehensive R&D investment that smaller players cannot match.

This transaction will allow a rebalancing of factory loading and a dramatic reduction in inventory, freight, duty and currency risks. It will also allow us to better match the rate and amount of future capital expenditure to specific market requirements.

The global manufacturing footprint enables "produce in region for region" strategies that minimize transportation costs while maximizing responsiveness to local customer needs.

2. Network Effects: WEAK

Traditional battery businesses exhibit limited network effects—each customer's decision to purchase EnerSys batteries doesn't directly increase value for other customers. However, as EnerSys expands IoT monitoring and predictive maintenance capabilities, modest network effects could emerge from aggregated data improving service for all customers.

3. Counter-Positioning: MODERATE

EnerSys' combination with Alpha creates the only fully-integrated DC power and energy storage solution provider for broadband, telecom and energy storage systems.

The integrated solutions approach—combining batteries, power electronics, enclosures, and service—creates differentiation that pure-play battery makers cannot easily replicate without cannibalizing existing channel relationships or making substantial acquisitions. Competitors who have built their businesses as component suppliers face organizational and strategic barriers to matching EnerSys's integrated approach.

4. Switching Costs: STRONG

Mission-critical applications create enormous switching costs. Custom battery integrations, system certifications, service contract dependencies, and operational familiarity all lock in customer relationships. Defense and aerospace qualifications—which take years to achieve—represent particularly powerful switching cost moats.

Consider a telecom operator with EnerSys batteries installed across thousands of cell sites, integrated with EnerSys chargers and monitoring systems, supported by EnerSys service contracts, and operated by technicians trained on EnerSys equipment. Switching suppliers would require requalifying equipment, retraining personnel, renegotiating service agreements, and managing transition risk—costs that far exceed any potential savings from alternative suppliers.

5. Branding: MODERATE

EnerSys produces reserve-power batteries, marketed and sold principally under the Alpha, PowerSafe, DataSafe, Hawker, Genesis, ODYSSEY and CYCLON brands. Motive-power batteries are marketed and sold principally under the Hawker, NexSys, IRONCLAD, General Battery, Fiamm Motive Power, Oldham and Express brands.

EnerSys's brand portfolio carries significant equity in B2B industrial markets. The ODYSSEY brand commands premium positioning in transportation segments; ABSL represents gold-standard reliability in space applications; Alpha dominates mindshare in broadband power solutions.

However, B2B branding operates differently than consumer markets—relationships and performance matter more than advertising impressions.

6. Cornered Resource: MODERATE-STRONG

Technical talent in industrial battery engineering is scarce and concentrated among established players. EnerSys's engineering teams possess accumulated expertise from over a century of industrial battery development—knowledge embedded in processes, designs, and manufacturing know-how that cannot be replicated quickly.

EnerSys® batteries have been on incredible journeys, orbiting Earth, Mars, Venus, and even powering NASA's Parker Solar Probe on its daring mission to the sun. Over the years, these batteries have accumulated an astonishing 6.8 billion operational cell hours in space as of February 2022, all without a single mission failure.

The space battery track record represents a cornered resource of proven reliability that competitors simply cannot match without decades of mission heritage.

7. Process Power: MODERATE

Manufacturing excellence in battery production requires optimized processes that deliver consistent quality at scale. EnerSys's high-speed TPPL production lines, refined through continuous improvement over years, achieve productivity levels that competitors cannot match without similar investment timelines.

XIV. Investment Considerations: Key Risks and Critical KPIs

Bull Case:

-

Secular tailwinds converging: 5G infrastructure deployment, data center expansion, warehouse automation, defense modernization, and energy transition all drive demand for EnerSys's products across multiple business segments simultaneously.

-

Margin expansion runway: EnerGize cost initiatives, manufacturing optimization, and mix shift toward higher-value products suggest continued margin improvement potential.

-

Lithium optionality: The Greenville gigafactory positions EnerSys to participate in lithium adoption while maintaining lead-acid leadership—optionality that pure-play competitors in either chemistry lack.

-

Defense positioning: Bren-Tronics acquisition, ABSL heritage, and domestic manufacturing create defensible position in counter-cyclical defense market with premium economics.

-

Capital allocation discipline: $1 billion buyback authorization, dividend growth, and continued M&A capability demonstrate shareholder-friendly capital allocation.

Bear Case:

-

Technology transition risk: Accelerated lithium-ion adoption could commoditize lead-acid markets faster than EnerSys can build profitable lithium positions.

-

Execution risk on gigafactory: Large capital projects carry construction delays, cost overruns, and technology ramp challenges; the Greenville facility represents a significant concentration of execution risk.

-

Tariff and trade policy uncertainty: Despite mitigation efforts, extended trade tensions or policy changes could pressure margins in ways difficult to fully offset.

-

Cyclical exposure: Material handling and industrial markets correlate with economic cycles; recession would pressure Motive Power and portions of Energy Systems.

-

Competition from Asian manufacturers: In commodity segments, Chinese and other Asian battery makers compete aggressively on price, potentially pressuring margins in less differentiated product categories.

Critical KPIs to Monitor:

-

Adjusted Operating Margin (excluding IRC 45X benefits): This metric isolates underlying operational performance from government incentive programs. Fiscal 2025 achieved 11.1% on this basis; improvement toward 14-16% target range would validate EnerGize execution.

-

Maintenance-Free Product Mix: The percentage of Motive Power revenue from TPPL and lithium products (reached record 29% in Q4 FY25) indicates progress shifting toward higher-value offerings that command premium pricing and create customer stickiness.

-

Defense/Specialty Segment Growth: Double-digit growth in Specialty segment validates the defense positioning strategy and Bren-Tronics integration success; deceleration would signal competitive pressure or execution challenges.

Material Regulatory Considerations:

-

IRA 45X Production Tax Credits: EnerSys benefits meaningfully from Inflation Reduction Act manufacturing credits for domestic battery production. Political changes to IRA programs could impact profitability, though the company's earnings power extends beyond these credits.

-

Tariff Policy Volatility: Management has demonstrated tariff mitigation capabilities, but policy changes remain outside company control and create ongoing uncertainty.

-

Environmental Compliance: Battery manufacturing involves hazardous materials subject to environmental regulation; compliance costs and potential liability represent ongoing considerations, though EnerSys's established operations have navigated these requirements historically.

XV. Conclusion: The Power Behind Power

EnerSys represents something rare in today's market: an industrial company that has successfully navigated technological disruption, consolidated a fragmented industry, and positioned itself at the intersection of multiple secular growth trends—all while maintaining disciplined capital allocation and generating consistent returns.

From its private equity origins in 2000 through twenty years of public company evolution, EnerSys has demonstrated that "boring" industrial businesses can create extraordinary shareholder value through patient execution, strategic M&A, and relentless focus on customer needs.

The Alpha Technologies acquisition transformed the company from battery manufacturer to integrated power solutions provider. The NorthStar deal consolidated TPPL technology leadership. The Bren-Tronics acquisition accelerated defense positioning while adding lithium expertise. And the Greenville gigafactory represents a bold bet on domestic lithium manufacturing that positions EnerSys for whatever chemistry mix emerges in industrial markets.

The company's products power humanity's most demanding applications—from the James Webb Space Telescope observing the universe's origins to the forklifts moving packages through Amazon warehouses. That range illustrates EnerSys's fundamental value proposition: when power absolutely cannot fail, customers turn to the company that has proven reliability across decades and billions of operational hours.

Under Shawn O'Connell's leadership, the EnerGize transformation signals operational intensity that should drive continued margin expansion while investing in capabilities for future growth. The $80 million in annualized cost savings, combined with Centers of Excellence consolidating technical expertise, positions the company to weather near-term headwinds while building for long-term value creation.

For investors seeking exposure to critical infrastructure—the power systems that enable modern telecommunications, commerce, and defense—EnerSys merits serious consideration. The company's competitive position, built over 125 years and protected by scale economies, switching costs, and accumulated technical expertise, creates durable advantages that should compound value over time.

The hidden giant powering the industrial world remains hidden in plain sight—quietly essential, consistently profitable, and positioned for continued relevance as the world demands more reliable, resilient, and increasingly intelligent power solutions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube