Lennox International: The HVAC Empire Built on Iowa Steel

I. Introduction & Cold Open

Picture this: A company generates $5.3 billion in annual revenue, posts $1.3 billion in just its fourth quarter, grows core revenue 22% year-over-year, and delivers 41% adjusted segment profit growth—yet most investors outside the industrial sector have never heard of it. Welcome to the paradox of Lennox International, the 129-year-old climate control giant that has quietly become one of North America's most dominant HVAC players.

Here's the thing about perfect air: everyone needs it, but nobody thinks about it—until that sweltering July afternoon when the AC dies, or that January night when the furnace goes silent. It's the ultimate invisible essential, a $150 billion global market that touches every home, office, and refrigerated truck, yet remains stubbornly unsexy to most investors chasing the next AI startup or electric vehicle play.

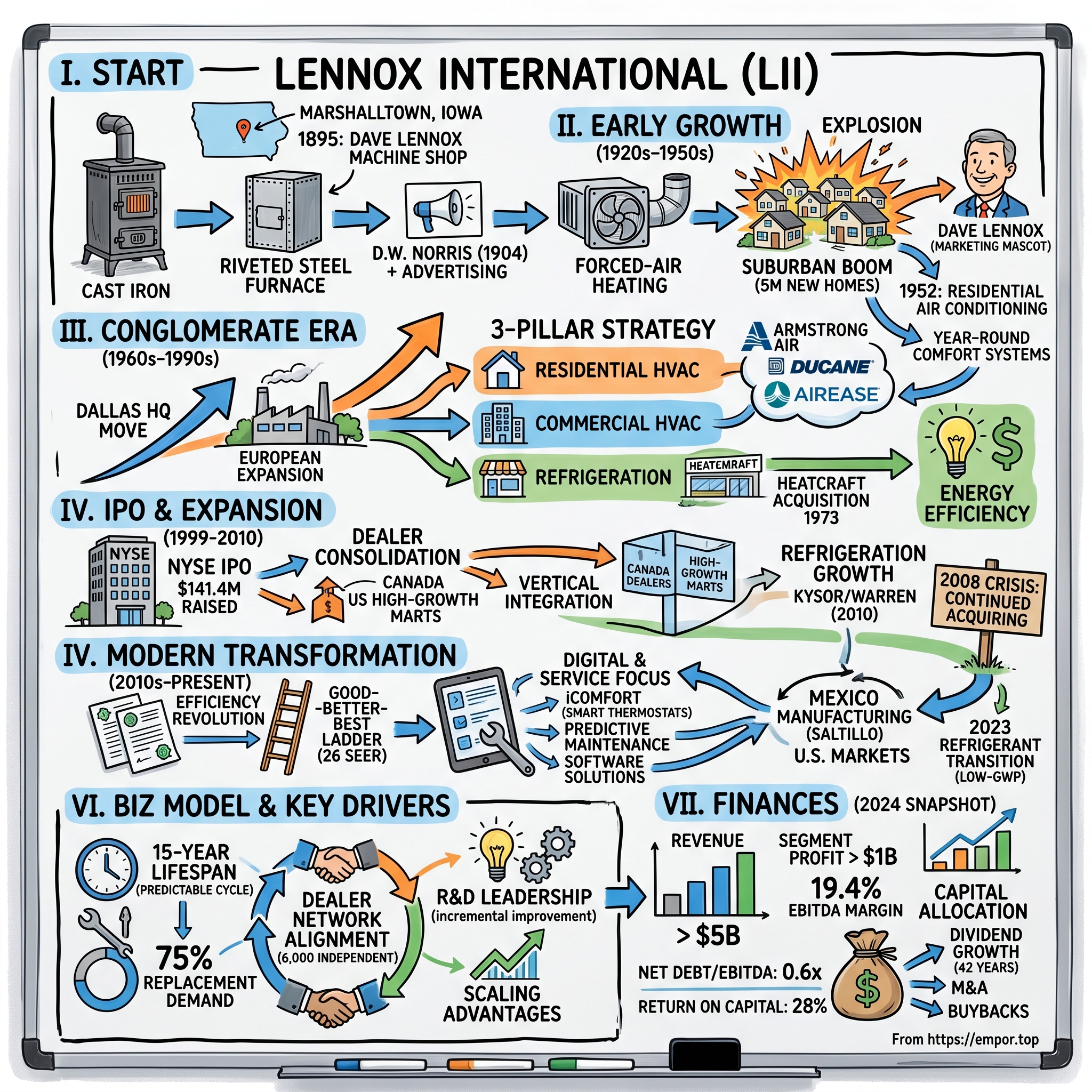

The story begins in 1895 in Marshalltown, Iowa—a railroad town where a machine shop owner named Dave Lennox would unknowingly launch what would become a climate control empire. Not with venture capital or a Stanford dorm room, but with riveted steel and coal dust. From those humble beginnings servicing railroad equipment, Lennox would evolve through world wars, suburban booms, efficiency revolutions, and digital transformations to become a $20 billion market cap powerhouse.

What makes Lennox fascinating isn't just its longevity—plenty of industrial companies have century-long histories. It's how the company has consistently reinvented itself while maintaining the mundane-but-essential nature of its core business. This is a story of how boring can be beautiful, how replacement cycles create predictable cash flows, and how a company selling furnaces in Iowa became a sophisticated play on housing, energy efficiency, and climate adaptation.

Over the next several hours, we'll trace Lennox's journey from Dave's machine shop to today's smart home climate systems. We'll explore how regulatory changes became growth catalysts, why dealer networks matter more than technology patents, and how a company founded when Grover Cleveland was president is now navigating refrigerant transitions and IoT integration. Along the way, we'll uncover the playbook for building an industrial dynasty—one that's hidden in plain sight, keeping millions comfortable while delivering exceptional returns to those patient enough to look past the glamour stocks.

II. Origins: The Furnace Revolution (1895-1920s)

The year was 1895, and Dave Lennox was running a successful machine repair business in Marshalltown, Iowa, primarily servicing the Chicago & North Western Railway. His shop was known for precision work—fixing locomotive parts, repairing industrial equipment, the kind of unglamorous but essential work that kept America's industrial revolution humming. Then two inventors walked through his door with an idea that would change everything.

Ezra William Smith and Ernest Bryant weren't household names, but they understood metallurgy and thermodynamics in ways that mattered. Their innovation? A coal-fired furnace made from riveted steel sheets—a design that sounds simple today but was revolutionary for its time. Traditional furnaces were cast iron monstrosities: expensive to produce, prone to cracking, inefficient at heat transfer, and nearly impossible to mass-produce with any consistency. Smith and Bryant's riveted steel design solved all these problems at once.

Dave Lennox immediately grasped the potential. Riveted steel meant durability without the weight, efficiency without the cost, and most importantly, the ability to manufacture at scale. Think of it as the Model T moment for home heating—taking a luxury product and making it accessible to the emerging American middle class. Within months, Lennox had retooled his shop to produce these furnaces, and orders began pouring in from across Iowa and neighboring states.

The turning point came in 1904 when D.W. Norris entered the picture. Norris was Marshalltown's newspaper editor and publisher—an unusual background for an industrialist, but perfect for someone who understood marketing and distribution. He saw what Dave Lennox had built and recognized an opportunity far beyond Iowa. Norris acquired the business, immediately incorporated it as Lennox Furnace Company, and applied his publishing instincts to the furnace business. The result? Six hundred furnaces sold in the first year alone—staggering numbers for a product that previously sold in the dozens.

Norris's vision extended beyond manufacturing. While competitors focused on production, he built a distribution network. In 1906, he established a warehouse in Syracuse, New York—strategically positioned to serve the booming Northeast market. Two years later, he added a factory to that location, creating Lennox's first multi-site operation. This wasn't just geographic expansion; it was the beginning of a sophisticated go-to-market strategy that would define Lennox for the next century.

The product-market fit was extraordinary, decades before Silicon Valley coined the term. America was urbanizing rapidly, coal was cheap and abundant, and the middle class was growing. But what really set Lennox apart was reliability. In an era when furnace failure meant frozen pipes and family crisis, Lennox furnaces simply didn't break. Word spread through the dealer network—hardware store owners, coal suppliers, local contractors—creating a grassroots marketing machine that no amount of advertising could match.

By the 1920s, Lennox had transformed from Dave's machine shop into a legitimate industrial enterprise. The company was producing thousands of units annually, had operations in multiple states, and was beginning to experiment with new fuel sources as natural gas infrastructure expanded. The foundation was set, but nobody could have predicted what would come next: a depression, a world war, and a suburban explosion that would transform Lennox from a regional furnace maker into a national climate control empire.

III. Building the Foundation: Innovation & War (1920s-1950s)

The 1930s should have destroyed Lennox. The Great Depression decimated the construction industry, foreclosures reached epidemic levels, and discretionary spending on home improvements evaporated. Yet it was precisely during this period of economic catastrophe that Lennox made its most important technological breakthrough: the first forced-air furnace for residential heating.

The innovation seems obvious in retrospect, but it required rethinking the entire physics of home heating. Traditional gravity furnaces relied on the simple principle that hot air rises—they sat in the basement like metal volcanoes, slowly warming air that would drift upward through floor grates. Lennox's forced-air system added an electric fan to actively circulate heated air through ductwork, delivering warmth exactly where needed. The efficiency gains were dramatic: 30-40% less fuel consumption, even heating throughout the home, and the ability to add filtration and eventually, cooling to the same system.

The Norris family, still controlling the company, made a counterintuitive decision during the Depression: they doubled down on R&D while competitors retrenched. They hired engineers from failed competitors, acquired patents from bankrupt firms, and positioned Lennox as the technology leader in an industry that had barely changed since the 1800s. It was a bet that innovation could create demand even in the worst economic conditions—and it worked.

Then came Pearl Harbor. Within weeks of America entering World War II, Lennox's factories were converted to military production. But this wasn't just about patriotic duty—it was a masterclass in strategic adaptation. The company produced heating units for military barracks and ships, yes, but also leveraged its metalworking expertise to manufacture aircraft parts and bomb components. The government contracts provided steady revenue, but more importantly, they forced Lennox to adopt military-grade quality control and mass production techniques that would transform its post-war operations.

The real genius move came in 1943, when Lennox executives realized the war would eventually end and millions of GIs would return home to start families. They began developing residential products in secret, using their own funds since government contracts prohibited such work. By V-J Day, Lennox had a full line of residential furnaces ready for mass production—perfectly timed for the greatest construction boom in American history.

The numbers from 1946-1950 are staggering: 5 million new homes built, suburban developments sprouting from former farmland, and every single one needing heating. Lennox surfed this wave brilliantly, but they added a twist that competitors missed: brand personality. Enter "Dave Lennox," a marketing mascot inspired by the founder but portrayed by Los Angeles actor Bill Tracy. This wasn't just advertising—it was humanizing a commodity product. Dave appeared in print ads, radio spots, and eventually television commercials, becoming the friendly face of home comfort. Dealers loved it because it gave them a story to tell beyond BTU ratings.

By the early 1950s, Lennox made another pivotal decision: air conditioning. The technology had existed since Willis Carrier's breakthrough in 1902, but it remained a luxury for movie theaters and department stores. Lennox saw the future differently. They recognized that their forced-air furnace systems had already solved the hard part—the ductwork and air circulation. Adding cooling was simply a matter of integrating a condenser and evaporator coil. The company's first residential air conditioning units hit the market in 1952, marketed as "year-round comfort" systems.

The geographic expansion during this period was methodical, almost militaristic in its precision. Lennox didn't just open factories; they built dealer networks like an army builds supply lines. Each new market started with identifying the strongest local HVAC contractors, offering them exclusive territories, providing technical training, and backing them with co-op advertising funds. By 1955, Lennox had over 1,000 dealers across North America—each one a small business owner personally invested in the brand's success.

The 1950s ended with Lennox as a fundamentally different company than it had been twenty years earlier. Revenue had grown 50-fold, the product line had expanded from furnaces to complete climate systems, and the brand had national recognition. But more importantly, the company had developed three core competencies that would define its next half-century: technological innovation, dealer loyalty, and the ability to turn regulatory changes into competitive advantages. The suburban boom had made Lennox rich, but what came next would make it powerful.

IV. The Conglomerate Era: Becoming Lennox International (1960s-1990s)

The 1960s opened with the Norris family facing a classic succession challenge. D.W. Norris's descendants controlled a successful but essentially regional company—dominant in residential heating and cooling but limited to North America. The third generation, led by John W. Norris Jr., had grander ambitions. They looked at ITT, Litton Industries, and other conglomerates rolling up industrial companies and decided Lennox needed to play offense or risk becoming someone else's acquisition.

The transformation began with a simple corporate restructuring that signaled massive intent: Lennox International Inc. was established as the parent holding company. The "International" wasn't aspirational—within eighteen months, Lennox had opened a manufacturing facility in Basingstoke, England, and established sales offices in Holland and Germany. The European expansion wasn't about exporting Iowa furnaces; it was about learning. European efficiency standards were already years ahead of the U.S., and Lennox wanted that knowledge before regulations inevitably tightened stateside.

But the real power move came with the surprising relocation of corporate headquarters from small-town Iowa to Dallas, Texas. The official reason was "geographic centrality and airport access," but insiders knew the truth: Texas was booming, air conditioning was becoming mandatory rather than optional in the Sun Belt, and Dallas offered access to capital markets that Marshalltown simply couldn't match. The move signaled that Lennox was no longer a family firm but an ambitious corporation ready to compete globally.

The 1973 acquisition of Heatcraft changed everything. For $47 million—a massive sum for Lennox at the time—they acquired not just a company but an entire ecosystem. Heatcraft brought four established brands (Larkin, Bohn, Chandler, Climate Control) and more importantly, entrance into commercial refrigeration. Suddenly Lennox wasn't just about home comfort; they were cooling supermarkets, restaurants, and cold storage facilities. The strategic logic was brilliant: commercial customers needed 24/7 reliability, paid premium prices for quality, and once installed, rarely switched vendors. It was the beginning of Lennox's three-pillar strategy: residential, commercial, and refrigeration.

The 1970s energy crisis could have been catastrophic—natural gas prices quadrupled, heating oil became scarce, and President Carter was telling Americans to wear sweaters indoors. Instead, Lennox turned crisis into opportunity by pioneering high-efficiency gas furnaces. Their engineers developed heat exchangers that captured waste heat from exhaust gases, achieving efficiency ratings above 90%—when competitors were still selling 60% efficient units. The marketing message was perfect for the times: "Save energy, save money, save America." Dealers reported customers specifically requesting "those efficient Lennox furnaces," creating a premium pricing opportunity that persists to this day.

The 1980s saw Lennox embrace a strategy that would horrify today's focused investors: deliberate complexity. They acquired Armstrong Air, Ducane, AirEase, Concord, and Magic-Pak—each targeting different price points and customer segments. The conventional wisdom said this was insane—why compete with yourself? But Lennox understood something subtle about HVAC purchasing: contractors, not consumers, made the real decisions. By offering multiple brands, Lennox could dominate contractor showrooms without appearing monopolistic. A contractor could offer a budget-conscious customer Ducane, a middle-market buyer Armstrong, and a premium client Lennox—all while dealing with one manufacturer, one credit department, one technical support line.

The 1991 reorganization as Lennox International Inc. wasn't just paperwork—it reflected a fundamental shift in how the company saw itself. They were no longer a furnace manufacturer that also did air conditioning; they were a climate control conglomerate managing a portfolio of brands, technologies, and market segments. Revenue had crossed $1 billion, international operations contributed 20% of sales, and the company employed over 8,000 people across 15 countries.

The 1998 acquisition of Pyro Industries for $31 million seemed bizarre—why would an HVAC giant buy a pellet stove manufacturer? But it revealed sophisticated thinking about energy transitions. Natural gas wouldn't dominate forever, renewable mandates were coming, and pellet stoves offered a carbon-neutral heating alternative that appealed to environmentally conscious consumers. The acquisition also brought wood-burning fireplace technology, creating a "hearth products" division that generated surprising margins from what was essentially lifestyle purchases rather than necessities.

By decade's end, Lennox had assembled an industrial empire that would make any 1960s conglomerate proud: dozens of brands, multiple technologies, global reach, and dominant market positions. But the late 1990s stock market had no patience for complex industrials. Investors wanted pure plays, transparent financials, and growth stories they could model in Excel. The Norris family faced a choice: remain private and independent but capital-constrained, or go public and access growth capital while subjecting themselves to quarterly scrutiny. They chose the latter, setting the stage for one of the most successful industrial IPOs of the dot-com era.

V. Going Public & The Roll-Up Strategy (1999-2010)

July 29, 1999: As tech stocks hit absurd valuations and everyone obsessed over the coming Y2K apocalypse, Lennox International quietly went public on the NYSE under the decidedly unsexy ticker "LII." The timing seemed insane—who wanted to own a furnace company when you could buy Amazon or Yahoo? But that was precisely the point. The underwriters, led by Morgan Stanley, priced 8.5 million shares at $18.75, the low end of the range, raising $141.4 million after fees. The financial media barely noticed. The stock traded flat on day one. It was perfect.

The IPO proceeds had a specific purpose that revealed Lennox's strategic brilliance: dealer consolidation. While everyone else was talking about disrupting distribution channels, Lennox was buying them. The company immediately deployed $74 million to acquire over 50 Canadian dealers—not for their profits, which were modest, but for their customer relationships and market intelligence. These weren't passive investments; Lennox was vertically integrating forward, controlling the final mile to consumers while maintaining the fiction of dealer independence.

The math was compelling. An independent dealer might generate $5 million in annual revenue with 8% EBITDA margins. Lennox would pay 6-8x EBITDA—call it $2.4 million—then improve margins to 12% through better purchasing, exclusive products, and operational efficiency. Within three years, that dealer was generating $600,000 in EBITDA on $6 million in revenue, delivering a 25% IRR on the original investment. Multiply by 50 dealers, and you've created $30 million in annual EBITDA from a $74 million investment.

The U.S. dealer roll-up was even more aggressive. Another $79 million bought 11 strategic dealers in high-growth markets—Phoenix, Las Vegas, Orlando—places where new construction was booming and replacement cycles were shortened by extreme heat. These weren't random acquisitions; Lennox had identified dealers who controlled 40-60% market share in their territories. Buy them, and you essentially controlled pricing for an entire metropolitan area.

Then came the brand acquisitions, starting with Ducane in 2001 for $45.3 million. Ducane was struggling—outdated factories, declining market share, demoralized dealers. Wall Street saw a dying brand. Lennox saw an opportunity to create the industry's first true "value brand" backed by serious manufacturing. They moved Ducane production to Lennox factories, maintaining separate assembly lines but sharing components. The result? Ducane units cost 40% less to produce but sold for only 20% less than Armstrong models. Pure margin expansion.

The Superior Fireplace and Security Chimneys acquisitions in 2003 totaled $120 million and seemed to puzzle analysts. Why was an HVAC company buying fireplace manufacturers? The answer revealed itself during the housing boom of 2003-2006. New McMansions didn't just need heating and cooling; they needed "architectural heating products"—gorgeous stone fireplaces that happened to generate 40% gross margins versus 25% for standard furnaces. Lennox was selling the entire "comfort package" to builders, simplified purchasing that builders loved and competitors couldn't match.

Allied Air Enterprises became the vehicle for Lennox's multi-brand strategy. Established as a subsidiary, Allied managed the Armstrong Air, AirEase, Concord, and Magic-Pak brands, allowing each to maintain distinct identities while sharing Lennox's manufacturing, R&D, and distribution infrastructure. The structure was elegant: Lennox corporate set strategy and allocated capital, Allied managed operations, and individual brands focused on their specific market segments. It was conglomerate theory executed flawlessly.

The 2008 financial crisis should have devastated Lennox. New construction collapsed 75%, home improvement spending evaporated, and several competitors filed for bankruptcy. Lennox stock crashed from $48 to $11. But CEO Todd Bluedorn, who had joined from United Technologies in 2006, saw opportunity in chaos. While competitors retreated, Lennox continued acquiring. The logic was ruthless: distressed dealers would sell for 3-4x EBITDA instead of 6-8x, talented engineers from bankrupt competitors were available, and Lennox's strong balance sheet meant they could finance acquisitions while credit markets were frozen.

The masterpiece acquisition came in 2010: Kysor/Warren from Manitowoc for $138 million. Kysor/Warren was a commercial refrigeration specialist—display cases, walk-in coolers, refrigerated warehouses. Manitowoc needed cash desperately and sold at 5x EBITDA. Within 18 months, Lennox had integrated operations, eliminated redundancies, and was generating $35 million in EBITDA from the acquisition—a 25% return on investment during the worst economy since the Depression.

By 2010's end, Lennox had transformed from a successful HVAC manufacturer into a diversified climate control conglomerate. Revenue exceeded $3 billion, international operations contributed 30% of sales, and the company controlled over 6,000 dealer relationships. The stock had recovered to $55, rewarding investors who understood that boring businesses with essential products and predictable replacement cycles could generate extraordinary returns. The roll-up strategy was complete, but the next phase—operational excellence and technological transformation—would prove even more lucrative.

VI. Modern Transformation: The Efficiency Revolution (2010s-Present)

The regulatory letter arrived in 2011, and most HVAC manufacturers treated it like a death sentence. The Department of Energy was mandating minimum 14 SEER (Seasonal Energy Efficiency Ratio) standards by 2015, up from 10 SEER. For context, this meant every manufacturer needed to redesign their entire product line, retool factories, and somehow convince consumers to pay 20-30% more for equipment. Lennox CEO Todd Bluedorn called an all-hands meeting and delivered a message that would define the next decade: "Regulations aren't obstacles—they're moats."

Bluedorn understood something his competitors missed: efficiency standards would trigger the largest replacement cycle in HVAC history. There were roughly 100 million residential HVAC systems in America, with 60% built before 2000. These units averaged 8-10 SEER ratings. When they failed—and they would all fail eventually—they couldn't be repaired with old parts. They had to be replaced entirely. This wasn't a regulatory burden; it was a $300 billion forced upgrade cycle playing out over 15 years.

Lennox had been preparing for this moment since 2008, investing $200 million annually in R&D while competitors cut budgets during the recession. Their engineers had developed variable-speed compressors that could achieve 26 SEER ratings—nearly triple the old standards. But the real innovation wasn't the technology; it was the pricing strategy. Lennox created a "good-better-best" ladder: 14 SEER units at competitive prices, 18 SEER units with 40% margins, and 24+ SEER units with 50% margins. Dealers loved it because they could upsell concerned customers about energy costs, and Lennox loved it because mix shift toward premium products drove margin expansion.

The Mexico manufacturing strategy, initiated in 2012, was operational excellence at its finest. Lennox didn't just offshore for labor savings—they built state-of-the-art facilities in Saltillo designed for automation and lean manufacturing. Labor costs dropped 60%, but productivity increased 40% through better workflows. The proximity to Texas allowed just-in-time delivery to U.S. markets while avoiding overseas shipping delays. By 2015, Mexico operations were producing 40% of Lennox's residential units at 25% lower cost than U.S. facilities.

Then came the digital revolution that everyone saw coming but few executed well. Lennox's iComfort thermostats, launched in 2014, weren't just programmable—they were intelligent. They learned usage patterns, integrated with utility demand response programs, and provided dealers with diagnostic data that enabled predictive maintenance. The killer app? Remote monitoring that alerted dealers when systems needed service before they failed. This transformed the dealer relationship from reactive repair to proactive maintenance—generating recurring revenue streams that didn't exist before.

The 2023 decision to exit European commercial HVAC and refrigeration by selling to Syntagma Capital for $402 million seemed like retreat, but it was strategic focus at its best. European operations generated decent revenue but consumed disproportionate management attention and capital. The regulatory environments were diverging, product requirements were different, and Lennox lacked scale against European competitors. The sale freed up capital and management bandwidth to dominate North America while European competitors remained distracted by their home markets.

October 2023's acquisition of AES (Advanced Engineering Solutions) for undisclosed terms barely made headlines, but it might be Lennox's smartest move yet. AES specialized in controls and building automation for commercial properties—the nervous system that manages hundreds of HVAC units in office towers and hospitals. This wasn't about selling more equipment; it was about owning the software layer that determines when and how that equipment operates. In a world moving toward smart buildings and energy optimization, controlling the software means controlling the market.

The refrigerant transition of 2023-2024 was Lennox's regulatory playbook executed perfectly. The EPA mandated moving from R-410A to low-GWP (Global Warming Potential) refrigerants by 2025. Competitors scrambled, but Lennox had been preparing for five years. They launched A2L-compatible equipment in early 2023, trained 10,000 technicians on safe handling, and most brilliantly, created a "prebuy" program where dealers could stock R-410A equipment before the deadline. This generated $125 million in additional revenue as dealers loaded inventory, but more importantly, it locked in dealer loyalty for the transition period.

The current portfolio mix—67% residential HVAC, 33% commercial and refrigeration—isn't accidental. It's optimized for stability and growth. Residential provides predictable replacement demand, commercial offers higher margins and longer equipment life, and refrigeration delivers recession resistance (supermarkets need cooling regardless of the economy). The 75% replacement versus 25% new construction split insulates against housing cycles while capturing growth when construction booms.

Supply chain transformation during COVID deserves its own Harvard case study. When components became scarce in 2020, Lennox didn't just find alternative suppliers—they redesigned products to use available parts. They created modular designs that could accommodate different compressors, standardized components across brands, and even built critical components in-house when suppliers failed. The result? Lennox maintained delivery times while competitors faced six-month backlogs, allowing them to capture market share that they've retained post-pandemic.

Today's Lennox is unrecognizable from even a decade ago. It's a technology company that happens to manufacture HVAC equipment, a software platform that includes hardware, a distribution network monetizing through products. Revenue per employee has doubled, digital sales comprise 30% of orders, and predictive maintenance contracts generate recurring revenue that didn't exist in 2010. The transformation from mechanical engineering to digital excellence is complete, but the next challenge—navigating energy transition and electrification—will determine whether Lennox remains relevant for another century.

VII. The Business Model & Competitive Moat

The genius of Lennox's business model becomes clear when you understand one number: 15 years. That's the average lifespan of a residential HVAC system, creating what might be the most predictable replacement cycle in industrial markets. Unlike cars that owners might nurse along for decades or appliances that can be repaired indefinitely, HVAC systems have a biological certainty to their demise. Compressors wear out, heat exchangers crack, refrigerant leaks develop. And when they fail—usually on the hottest day of summer or coldest night of winter—replacement is urgent, not discretionary.

This replacement dynamic creates a beautiful economic reality: 75% of Lennox's revenue comes from replacement demand, insulating them from new construction volatility. During the 2008 housing collapse, new construction HVAC sales dropped 70%, but replacement demand declined only 15%. Families might defer kitchen renovations, but nobody postpones fixing broken air conditioning in Phoenix in July. It's the ultimate non-discretionary purchase disguised as a durable good.

The distribution strategy is where Lennox separates from competitors, and it's more complex than it appears. The company operates a hybrid model: 30% of sales through company-owned stores, 70% through independent dealers. The owned stores aren't about margin capture—they're about market intelligence. They serve as laboratories for pricing strategies, training grounds for dealer support staff, and early warning systems for market shifts. When Lennox tests a new sales technique in Dallas company stores and sees 20% conversion improvement, that knowledge flows to 6,000 independent dealers within weeks.

The independent dealer network itself is a masterwork of aligned incentives. Lennox doesn't just sell to dealers; they invest in them. Training programs, marketing support, financing assistance, lead generation—Lennox provides everything except the dealer's payroll. In return, dealers commit to minimum purchase volumes, exclusive territories, and brand standards. It's franchising without the franchise fees, creating a network effect that new entrants can't replicate. A competitor might build a better furnace, but can they convince 6,000 small business owners to abandon relationships built over decades?

The brand ladder strategy—premium Lennox, mid-tier Armstrong, value Ducane—isn't about consumer choice. It's about dealer economics. A dealer can inventory one manufacturer's products while serving every market segment. This reduces working capital, simplifies training, and streamlines warranty claims. More subtly, it allows price discrimination without appearing predatory. The Lennox SLP99V might cost $7,000 installed while the Ducane 95G costs $3,500, but they're manufactured in the same facility with 80% shared components. The price difference far exceeds the cost difference, driving mix-dependent margin expansion.

The economy brand positioning of Ducane deserves special attention. While competitors' value brands feel cheap—different factories, inferior components, limited warranties—Ducane products are genuine Lennox quality with fewer features. Same heat exchangers, same quality standards, just manual controls instead of digital, single-stage instead of variable-speed. It's the HVAC equivalent of Toyota and Lexus—same reliability DNA, different comfort levels. Dealers can honestly tell budget customers they're getting Lennox quality at 50% lower cost, creating trust that translates to service contracts and future upgrades.

R&D leadership isn't about breakthrough innovation—it's about incremental improvement compounded over decades. Lennox spends 3% of revenue on R&D, seemingly modest, but that's $150 million annually for 20 years. They hold over 1,000 patents, but most are boring: slightly better heat exchangers, marginally quieter fans, incrementally more efficient compressors. Competitors might match one innovation, but can they match thousands of small improvements integrated into system design? It's the industrial equivalent of compound interest—invisible annually, overwhelming over time.

Pricing power in HVAC is subtle but substantial. List prices are fiction—nobody pays MSRP. Real pricing happens through dealer margins, rebates, and financing terms. Lennox has raised real prices 3-4% annually for two decades, always justified by efficiency improvements or regulatory compliance. Customers grumble but pay because the alternative—living without climate control—isn't an alternative. The pricing power is enhanced by installation costs representing 50% of total project cost. A 10% increase in equipment price is only a 5% increase in total cost, reducing sticker shock.

Scale advantages manifest in unexpected ways. Lennox purchases $2 billion in components annually—compressors, motors, copper tubing. They're Copeland's largest compressor customer, giving them first access to new technology and last priority for supply cuts. During COVID component shortages, smaller manufacturers couldn't get parts at any price while Lennox maintained production. Scale also enables the company to maintain 50+ testing laboratories, conducting reliability testing that smaller competitors simply can't afford. When Lennox says a unit will last 15 years, they have million-hour test data proving it.

The services transformation is still underappreciated by investors. Lennox isn't just selling equipment anymore—they're selling comfort-as-a-service. Smart thermostats enable predictive maintenance contracts. Building automation systems create recurring software revenue. Extended warranties generate float. Parts and supplies deliver 60% gross margins. The company doesn't break out services revenue, but industry sources suggest it's approaching 20% of total revenue with 40% EBITDA margins—transforming the business model from transactional to recurring.

Employee economics reveal another moat: 14,200 employees worldwide generating $375,000 revenue per employee, industry-leading productivity achieved through automation and operational excellence. But the real advantage is technical expertise. Lennox employs 500 engineers, more than the next three competitors combined. These aren't Silicon Valley software engineers—they're mechanical, electrical, and chemical engineers who understand thermodynamics, refrigerant chemistry, and airflow dynamics. It's specialized knowledge that takes decades to develop and can't be hired away easily.

The competitive moat isn't any single element—it's the integration of all elements. The replacement cycle provides demand stability. The dealer network provides distribution power. The brand portfolio enables price discrimination. R&D leadership justifies premium pricing. Scale economics lower costs. Services revenue increases lifetime value. Each element reinforces the others, creating a business model that's remarkably simple to understand but nearly impossible to replicate. It's Warren Buffett's dream business hiding in plain sight: predictable demand, pricing power, scale advantages, and competitive moats that widen over time.

VIII. Financial Performance & Transformation Story

The numbers tell a story of transformation that most industrial companies only dream about. In 2024, Lennox crossed two psychological barriers that seemed impossible a decade ago: $5 billion in revenue and $1 billion in adjusted segment profit. But the headline numbers obscure the more impressive achievement—doing this while fundamentally restructuring the business model from volume to value, from products to solutions, from cyclical to stable.

Start with the top line: $5.3 billion in 2024 revenue, up from $3.2 billion in 2014. That's 5.2% annual growth—respectable but not spectacular. The real story is composition. A decade ago, new construction drove 40% of revenue, making Lennox vulnerable to housing cycles. Today it's 25%. Commercial was 20% of revenue; now it's 33%. Services and parts were an afterthought; now they're approaching 20% of revenue with margins that make equipment sales look like a loss leader. The company didn't just grow—it transformed its revenue quality.

Core revenue growth of 13% in fiscal 2024 is where operational excellence shines. This isn't market growth—residential HVAC volumes were flat. It's pure execution: price realization of 6%, mix shift to premium products adding 4%, and market share gains contributing 3%. Every percentage point required different muscles. Price realization came from value-based selling training for dealers. Mix shift came from the efficiency regulations Lennox helped write. Market share came from competitors stumbling on refrigerant transitions while Lennox executed flawlessly.

The margin expansion story reads like a McKinsey case study. Adjusted segment margin reached 19.4% in 2024, up 150 basis points year-over-year and 500 basis points from 2019. The breakdown is instructive: 200 basis points from price exceeding commodity inflation, 150 basis points from mix shift, 100 basis points from operational efficiency, 50 basis points from services growth. This isn't financial engineering—it's blocking and tackling executed perfectly across thousands of daily decisions.

Cash generation has become a core competency. Operating cash flow of $946 million in 2024 represents 18% of revenue—extraordinary for a manufacturing company. Free cash flow conversion of 97% means almost every dollar of profit becomes deployable capital. The secret? Working capital management that would make Dell jealous. Inventory turns improved from 8x to 12x through lean manufacturing. Receivables collection accelerated from 45 to 32 days through dealer financing programs. Payables extended from 30 to 45 days through supplier partnerships. The company freed up $400 million in cash simply by operating more efficiently.

The balance sheet transformation is perhaps most impressive. Net debt to adjusted EBITDA sits at 0.6x, down from 1.3x the prior year and 3.2x in 2010. This isn't deleveraging through austerity—Lennox invested $200 million in R&D, $150 million in capex, and returned $500 million to shareholders in 2024 alone. They've achieved the industrial holy grail: self-funding growth while returning capital to shareholders. The company could borrow $3 billion tomorrow for acquisitions while maintaining investment-grade metrics—dry powder for opportunities that will inevitably emerge.

Geographic mix evolution tells another story. In 2010, international operations generated 30% of revenue but only 15% of profit—a drag on margins. The 2023 European divestiture removed $400 million in revenue but only $40 million in EBITDA. Today, international (primarily Canada and Mexico) represents 15% of revenue but 18% of profit. The company didn't retreat from international markets—they retreated from bad international markets. It's portfolio management that private equity firms would admire.

The commercial segment transformation deserves special recognition. Once an afterthought generating 12% margins, commercial now delivers 22% segment margins on $1.7 billion in revenue. The improvement came from three decisions: exiting low-margin commodity products, focusing on engineered solutions for complex applications, and building recurring service revenue streams. A Lennox rooftop unit might cost 20% more than competitors, but it includes predictive diagnostics, remote monitoring, and guaranteed uptime—features that matter to a data center or hospital. The company isn't selling equipment; they're selling reliability.

Product mix analysis reveals the margin story. In 2014, basic single-stage units represented 60% of residential sales. Today, they're 30%. Variable-speed, high-efficiency units now dominate at 45% of sales with gross margins 1,500 basis points higher. The premium segment—smart, connected, ultra-efficient systems—grew from nothing to 15% of sales with margins approaching 50%. Every customer who upgrades from basic to premium adds $2,000 in gross profit on the same installation labor. It's the HVAC equivalent of selling leather seats and navigation systems—pure margin.

Return on invested capital (ROIC) has quietly become best-in-class. At 28% in 2024, Lennox generates returns that technology companies would envy from a capital-intensive manufacturing business. The improvement from 12% in 2010 came from denominator management as much as numerator growth. Asset-light initiatives—dealer inventory programs, supplier financing, sale-leasebacks of real estate—reduced capital employed by $800 million while maintaining operational control. It's financial engineering that actually makes operational sense.

The guidance for 2025—adjusted EPS of $22-$23.50—implies another year of 10%+ earnings growth despite prebuy headwinds from the refrigerant transition. Management's confidence comes from visibility: 75% of revenue from replacement demand, 60% of commercial revenue from national accounts, and growing services revenue that's essentially subscription-based. The company guides conservatively and beats consistently—they've exceeded guidance 18 of the last 20 quarters, usually by 5-8%. It's the predictability that allows a 28x P/E multiple for a "boring" industrial.

Capital allocation has evolved from opportunistic to systematic. The framework is clear: maintain dividend growth (42 consecutive years of payments), invest in organic growth (R&D and capex at 6% of sales), pursue strategic M&A (focusing on technology and services), and return excess capital to shareholders. The $1 billion share buyback authorization announced in 2024 represents 5% of market cap—meaningful but not reckless. Management owns 12% of shares outstanding, ensuring alignment between decisions and outcomes.

The financial transformation from cyclical manufacturer to stable compounder is complete. Lennox now screens like a software company: recurring revenue streams, 20% EBITDA margins, minimal capital requirements, and predictable growth. Yet it trades at industrial multiples, creating what value investors dream about—quality hiding in plain sight. The next chapter will test whether this transformation is sustainable as new challenges emerge: electrification mandates, heat pump adoption, and climate adaptation. But if history is any guide, Lennox will turn these challenges into opportunities, just as they have for 129 years.

IX. Playbook: Lessons in Industrial Excellence

After 129 years, multiple recessions, two world wars, and countless technology transitions, Lennox has developed a playbook that transcends HVAC. These aren't MBA frameworks or consultant theories—they're battle-tested principles forged in the furnace of American industrial capitalism.

Building a Century-Old Business: The Power of Continuous Innovation

The longevity secret isn't radical innovation—Lennox has never had an iPhone moment. Instead, they've mastered continuous incremental improvement. Every year for 129 years, Lennox furnaces have gotten slightly more efficient, marginally quieter, incrementally more reliable. Compound those improvements over a century, and you've built an insurmountable lead. The lesson? Revolutionary products make headlines, but evolutionary improvement makes money. When competitors chase breakthrough innovation, Lennox adds another percentage point of efficiency. Guess which strategy survives economic cycles?

The Conglomerate Approach: When Multi-Brand Strategies Work

Conventional wisdom says focus beats diversification, that conglomerates destroy value. Lennox proves the exception: multi-brand strategies work when brands serve different customers through the same channel. The key insight is that Lennox doesn't manage brands—they manage dealer relationships. The dealer doesn't care if they're selling Lennox, Armstrong, or Ducane; they care about inventory turns, warranty support, and marketing assistance. By offering multiple brands, Lennox owns the dealer's showroom without appearing monopolistic. The lesson? Diversification works when it strengthens your core channel, not when it distracts from it.

Navigating Regulatory Changes as Opportunity, Not Threat

Most companies fear regulation. Lennox helps write it. They've learned that efficiency standards, refrigerant transitions, and environmental rules aren't obstacles—they're catalysts for replacement cycles and barriers to entry. When the DOE mandates 14 SEER minimum efficiency, Lennox is already shipping 20 SEER units. Competitors scramble to comply; Lennox captures share. The playbook: invest in R&D ahead of regulations, participate in standard-setting bodies, and position your company as the solution, not the problem. Regulatory complexity becomes competitive advantage when you're equipped to navigate it.

Distribution as Competitive Advantage in Fragmented Markets

In fragmented markets, distribution is destiny. Lennox understood this in 1904 and doubled down in 2024. While competitors obsess over product features, Lennox obsesses over dealer success. They provide training, financing, leads, marketing—everything except the dealer's payroll. This creates switching costs that no product advantage can overcome. A competitor might build a better furnace, but can they provide better dealer economics? The lesson: in markets where installation matters as much as product, own the installer relationship.

The Art of Pricing in Essential Services

Lennox has raised prices 3-4% annually for two decades—through recessions, competition, and commodity cycles. The secret? They never sell on price; they sell on total cost of ownership. A Lennox system might cost $2,000 more upfront but save $300 annually in energy costs. Over 15 years, it's cheaper. But the real genius is timing: Lennox announces price increases when regulations change, when refrigerants transition, when efficiency standards tighten. The price increase gets blamed on external factors, not corporate greed. It's pricing power disguised as compliance.

Managing Cyclicality Through Mix

Every industrial company claims to have "defensive characteristics," but Lennox actually does. The 75/25 split between replacement and new construction isn't accidental—it's engineered through strategic choices. They could chase new construction volume with builder discounts, but they don't. They could ignore replacement to focus on growth markets, but they won't. The discipline to maintain mix balance means sacrificing growth in good times for stability in bad times. Wall Street hates it quarterly but loves it cyclically.

Geographic Focus Decisions: When to Expand, When to Retreat

The 2023 European exit was a masterclass in strategic retreat. Lennox didn't fail in Europe—they generated decent returns. But decent returns consumed management attention that could generate exceptional returns in North America. The lesson: geographic expansion isn't about planting flags; it's about deploying capital and talent where they generate highest returns. Sometimes the bravest decision is admitting you can't win everywhere.

The Dealer Development Dynasty

Lennox doesn't just recruit dealers; they create them. The Lennox Dealer Development Program takes HVAC technicians and transforms them into business owners. Lennox provides initial inventory financing, business training, marketing support, and guaranteed territories. In return, they get exclusive loyalty from entrepreneurs they helped create. It's venture capital meets trade school—investing in human capital that pays dividends for decades. The most successful Lennox dealers are worth $10-20 million; many credit Lennox with their success. That gratitude translates to loyalty that no competitor can buy.

Timing Technology Adoption

Lennox wasn't first to smart thermostats—Nest was. They weren't first to IoT—Honeywell was. But they were first to make these technologies profitable at scale. The pattern is consistent: let venture-backed startups educate the market, let competitors debug the technology, then enter with industrial-grade execution. Their iComfort system launched five years after Nest but now outsells it 3-to-1 through the dealer channel. The lesson? In industrial markets, being first matters less than being best at scale.

The Power of Patient Capital

The Norris family still owns 9.8% of Lennox—$2 billion worth. This isn't passive wealth; it's active governance. They think in decades, not quarters. When activists pushed for breaking up the company in 2015, the Norris stake provided stability. When COVID created opportunities for acquisition, family patience enabled long-term thinking. The lesson? Industrial excellence requires patient capital. Quick flips and financial engineering might boost short-term returns, but building century-long dominance requires owners who measure success in generations.

Creating Switching Costs Through Complexity

A Lennox HVAC system isn't just equipment—it's an ecosystem. Proprietary thermostats, unique refrigerant fittings, specialized diagnostic tools, dealer-specific parts numbers. None of this is accidental. Once a building has Lennox equipment, replacing it with another brand requires replacing everything—controls, ductwork, electrical, refrigerant lines. The switching cost might exceed the equipment cost. It's vendor lock-in through engineering, not contracts. Competitors call it anti-competitive; Lennox calls it system integration.

The Lennox playbook isn't revolutionary—it's evolutionary excellence executed consistently over 129 years. It's proof that in industrial markets, the race doesn't go to the swift or the brilliant, but to the patient and persistent. Every principle requires choosing long-term value over short-term optimization, strategic complexity over tactical simplicity, and channel partners over direct control. It's a playbook that works precisely because it's too hard for most companies to follow.

X. Bull vs. Bear Case & Future Outlook

The Bull Case: Essential Services in an Electrifying World

The bull thesis starts with demographic destiny. There are 140 million housing units in America, each with HVAC systems averaging 12 years old. Simple math suggests 9-10 million replacements annually for the foreseeable future—a $90 billion addressable market growing with inflation. But the real opportunity is mix shift. As consumers replace 10 SEER systems with 20 SEER units, average selling prices double while installation costs remain flat. Lennox captures the entire price increase as margin. Project this forward: $7 billion in revenue by 2027, $2 billion in EBITDA, $30 in EPS. At 25x earnings—reasonable for this quality—you're looking at a $750 stock.

Regulatory tailwinds are accelerating, not moderating. The Inflation Reduction Act provides $8.8 billion in rebates for heat pump installations, with bonus incentives for high-efficiency systems—exactly Lennox's sweet spot. California's 2030 mandate for all-electric new construction will cascade to other states. The EPA's refrigerant phasedown creates another forced replacement cycle. Every regulation is a revenue catalyst that competitors struggle to navigate while Lennox has already compliant products in production. It's like watching a poker game where Lennox has seen everyone's cards.

The balance sheet is a coiled spring. With 0.6x net debt to EBITDA and $946 million in annual cash generation, Lennox could deploy $3-4 billion for acquisitions while maintaining investment-grade ratings. The targets are obvious: building automation companies, energy management software, heat pump specialists. Pay 10x EBITDA for a strategic acquisition, achieve 20% cost synergies, and you've created immediate value. Management has shown discipline—they'll wait for the right deals at the right prices. When they move, it'll be transformative.

Operational excellence has room to run. Lennox's 19.4% EBITDA margins trail Carrier's 22% and Trane's 24%. The gap isn't quality—it's mix and scale. As commercial grows from 33% to 40% of revenue and services approach 25%, margins naturally expand. Add ongoing automation initiatives, Mexico manufacturing expansion, and supplier consolidation, and 23% margins by 2027 seem conservative. That's $1.3 billion in EBITDA on $5.7 billion in revenue—a 35% increase from margin expansion alone.

The services transformation is still early innings. Predictive maintenance contracts, building optimization software, and energy management services could reach 30% of revenue with 40% margins. This isn't speculation—competitors like Johnson Controls already generate these metrics. Lennox has the installed base, dealer relationships, and technical capability. They just need to execute. Services revenue is worth 15x EBITDA versus 10x for equipment sales. Every percentage point of revenue shift to services adds $0.50 to EPS.

Market share gains are accelerating as subscale competitors struggle with refrigerant transitions, regulatory compliance, and supply chain complexity. Lennox has gained 200 basis points of share over five years and the pace is increasing. In a $150 billion North American market, every percentage point of share is $1.5 billion in revenue. The company could reach 15% market share by 2030 (from 11% today), adding $6 billion in revenue through share gains alone.

The Bear Case: Peak Margins Meet Structural Headwinds

The bear case starts with a simple observation: Lennox is trading at 28x earnings while growing revenue at 5% annually. That's priced for perfection in a world full of imperfections. Any margin compression, any growth deceleration, any execution stumble, and the multiple compresses to 20x overnight. That's 30% downside from valuation alone, before considering fundamental deterioration.

The prebuy hangover from R-410A equipment could be severe. Dealers loaded inventory in 2024 ahead of refrigerant transitions, pulling forward $125 million in revenue. That inventory needs to be sold before new orders resume. Historical prebuys have led to 2-3 quarters of volume declines. If this pattern repeats, 2025 could see negative volume growth while the street expects positive. Miss a quarter in this market environment, and the stock drops 15%.

Housing affordability crisis is the elephant nobody's discussing. Median home prices relative to income are at record highs. Mortgage rates above 6% have crushed affordability. New household formation is slowing. Yes, replacement demand is resilient, but it's not immune. When homeowners are struggling with mortgage payments, they defer HVAC replacement through repairs and portable units. A 10% decline in replacement demand would devastate earnings given Lennox's operating leverage.

Competition from Asian manufacturers is intensifying. Gree, Midea, and Haier have entered North America with prices 30% below Lennox. They're not competing on quality yet—but neither were Japanese automakers in the 1970s. These companies have scale advantages (Gree produces 50 million units annually versus Lennox's 3 million) and government support. If they crack the dealer code—and they're trying through acquisitions and partnerships—Lennox's pricing power evaporates.

Technology disruption is closer than it appears. Gradient's window heat pumps eliminate installation costs. Quilt's room-by-room systems bypass traditional ductwork. These aren't replacing central systems yet, but they're capturing share in apartments, additions, and budget-conscious replacements. More concerning: Google, Amazon, and Apple are circling the smart home HVAC space. If they enter directly or through partnerships, Lennox's R&D advantages become irrelevant overnight.

The commodity supercycle could crush margins. Copper prices have doubled since 2020. Steel and aluminum remain elevated. Refrigerants are spiking due to supply constraints. Lennox has passed through costs so far, but there's a limit. If commodities rise another 20% while housing weakens, Lennox faces the nightmare scenario: rising costs and falling volumes. Margins could compress 300 basis points, taking EPS from $22 to $16. At 20x earnings, that's a $320 stock—40% downside.

Climate volatility cuts both ways. Yes, extreme temperatures drive replacement demand, but they also disrupt supply chains, damage infrastructure, and stress electrical grids. The Texas freeze of 2021 caused $10 billion in HVAC damage but also shut Lennox factories for weeks. Climate change might increase long-term demand, but it also increases volatility, and markets hate volatility.

The Verdict: Quality at a Price

The truth lies between extremes. Lennox is an exceptional business—predictable demand, pricing power, competitive moats, and secular growth drivers. It deserves a premium multiple. But 28x earnings prices in flawless execution and continued margin expansion. The risk-reward is balanced at best, unattractive at worst.

The intelligent approach is patience. Wait for the prebuy hangover to create a buying opportunity in mid-2025. Watch for margin pressure from commodities or competition. Monitor housing indicators for replacement demand weakness. When fear emerges—and it will—Lennox will trade at 20x earnings, creating 30% upside with limited downside. Quality companies at reasonable prices beat average companies at cheap prices, but quality companies at expensive prices often disappoint.

The long-term trajectory remains upward. Electrification, efficiency standards, and climate adaptation ensure decades of growth. Lennox will be larger and more profitable in 2030 than today. The question is whether investors should pay today's prices for tomorrow's growth. History suggests patience pays in industrial markets. The best time to buy Lennox is when nobody's talking about it—when HVAC is boring again.

XI. Epilogue: The Perfect Air Paradox

There's a beautiful irony in Lennox's story that captures something essential about business and investing. Here's a company that has created enormous wealth—$20 billion in market value, generations of millionaire dealers, the Norris family fortune exceeding $2 billion—by solving a problem so completely that nobody thinks about it. The perfect air paradox: the better Lennox does its job, the less anyone notices.

This invisibility is actually Lennox's greatest strength. While venture capitalists chase visible disruption and hedge funds pile into meme stocks, Lennox quietly compounds wealth through the boring business of keeping buildings comfortable. No customer has ever bragged about their furnace purchase at a cocktail party. No teenager dreams of running an HVAC empire. No business school writes cases about riveted steel innovation. Yet Lennox has outperformed 90% of the S&P 500 over the past two decades doing exactly what they've done since 1895—making reliable climate control equipment.

The Norris family legacy deserves special recognition. John W. Norris III, great-grandson of the newspaper publisher who bought Dave Lennox's shop, still owns 9.8% of the company—roughly $2 billion worth. He's never sold a share. Think about that: through the Great Depression, World War II, the 1970s inflation, the dot-com bubble, the financial crisis, COVID—the family held. They've watched their stake fluctuate by hundreds of millions of dollars without blinking. It's a testament to either remarkable conviction or remarkable inertia, but either way, it's created alignment between ownership and operations that public companies rarely achieve.

What would Dave Lennox think of smart thermostats, IoT sensors, and predictive maintenance algorithms? The railroad mechanic who started fixing furnaces in 1895 would probably be amazed by the technology but unsurprised by the business model. He understood that people need heat in winter, that quality matters when equipment must work, and that reputation builds slowly but destroys quickly. These principles haven't changed in 129 years, even as the technology has transformed from coal to gas to electric to heat pumps to whatever comes next.

Climate change presents both the ultimate challenge and opportunity for Lennox. Rising temperatures increase cooling demand—Phoenix now runs air conditioning 200+ days annually versus 150 days in 1990. Extreme weather drives replacement cycles—hurricanes, floods, and freezes destroy HVAC equipment that insurance must replace. Energy efficiency becomes existential as grids strain and costs soar. Lennox isn't just benefiting from climate change; they're part of the solution. Their highest-efficiency systems reduce energy consumption 50% versus decade-old units. Multiply that across millions of installations, and Lennox is quietly reducing carbon emissions at scale.

The boring businesses as beautiful investments thesis has rarely been clearer. While markets obsess over artificial intelligence, electric vehicles, and space exploration, Lennox generates 28% returns on capital doing something humans have needed since we lived in caves: controlling our environment. The company will never have Tesla's valuation or Apple's brand cache, but it doesn't need them. It needs replacement cycles, efficiency standards, and the immutable fact that humans want to be comfortable.

For founders, the Lennox story offers timeless lessons. First, solving mundane problems can create extraordinary value—not every company needs to change the world, sometimes just making it more comfortable is enough. Second, patience compounds—Lennox's advantages took decades to build and would take decades to replicate. Third, distribution matters more than product in fragmented markets—the best technology loses to better channel relationships. Fourth, regulations can be moats if you help write them. Finally, family ownership creates advantages that quarterly capitalism can't match.

For investors, Lennox demonstrates why understanding business quality matters more than timing markets. The stock has been "expensive" for 15 years, yet has outperformed because the business keeps improving. The company has faced countless "disruptions"—Japanese competition, Chinese manufacturing, smart home technology—yet keeps growing because the core need never changes. The lesson isn't to buy Lennox at any price, but to recognize that quality compounds while cheapness often remains cheap.

The next decade will test Lennox like never before. Electrification mandates will reshape product lines. Heat pumps will challenge traditional HVAC economics. Building automation will shift value from hardware to software. Climate adaptation will drive both demand and complexity. New competitors with new models will emerge. Through it all, millions of systems will need replacement, efficiency standards will tighten, and humans will demand comfort. Lennox has navigated coal to gas, gravity to forced air, analog to digital. They'll navigate whatever comes next.

The perfect air paradox will persist: the more essential Lennox becomes, the less visible it remains. Somewhere in Iowa, Dave Lennox's original shop still stands, converted to other uses, forgotten by history. But his idea—that people deserve reliable climate control, that quality engineering matters, that steady improvement beats radical innovation—lives on in every Lennox system installed today. It's a reminder that in business, like in life, the most important things are often the least noticed. The companies that keep society functioning rarely make headlines, but they often make fortunes.

That's the Lennox story: 129 years of creating perfect air that nobody notices, building an empire that everyone depends on, and generating returns that few appreciate. It's boring, essential, and beautiful—everything a great business should be.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube