L3Harris Technologies: The Defense Contractor's Trusted Disruption

I. Introduction & Cold Open

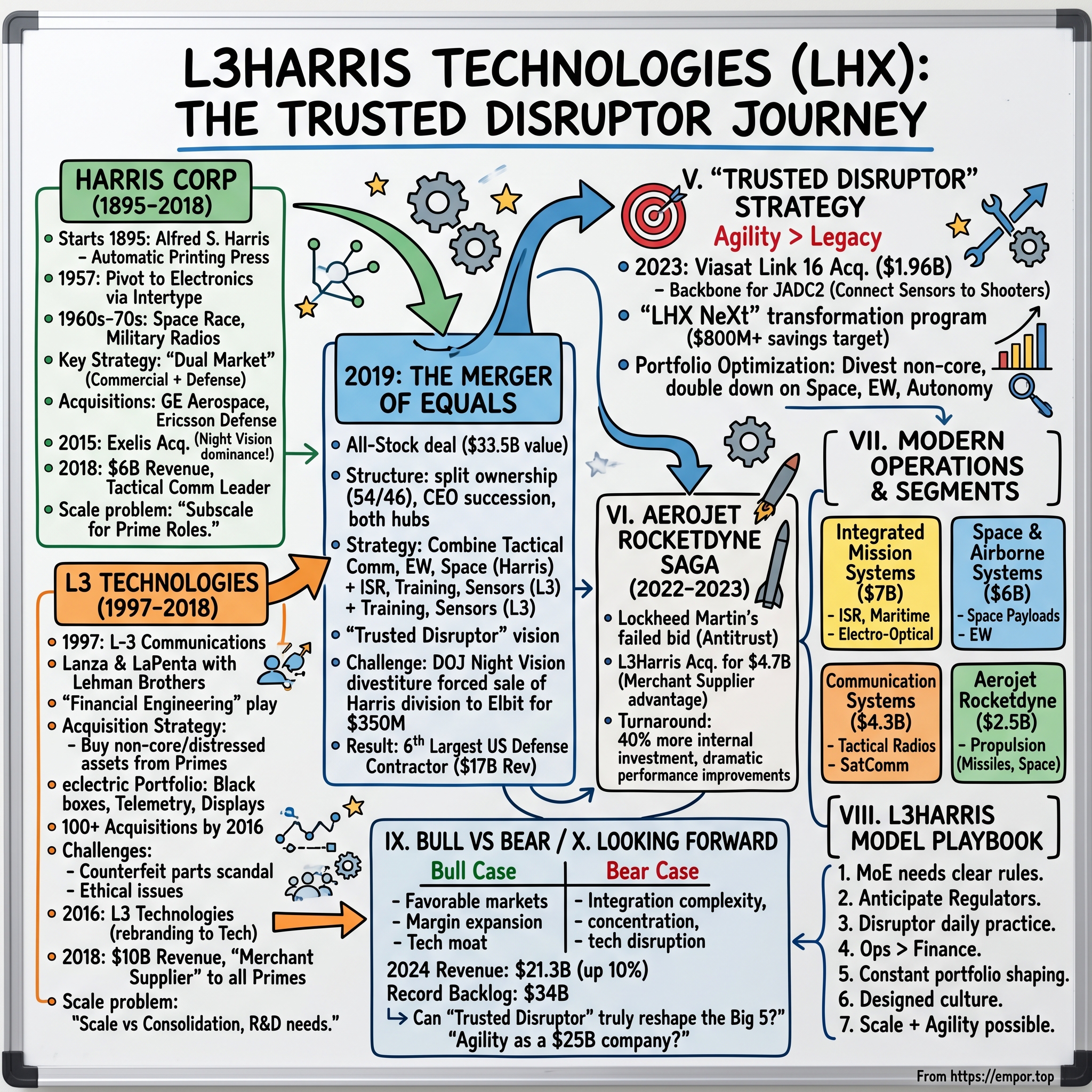

Picture this: June 29, 2019. Melbourne, Florida. Two mid-tier defense contractors—neither a household name, neither in the pantheon of Lockheed Martin or Boeing—shake hands on a deal that would reshape the defense industrial landscape. The "merger of equals" between L3 Technologies and Harris Corporation created something unprecedented: the sixth-largest defense contractor in the United States, seemingly overnight.

But here's what makes this story fascinating: while the defense primes were busy protecting their turf, two companies with wildly different DNA—one born from Lehman Brothers' financial engineering, the other from 19th-century printing presses—combined to create a $17 billion revenue powerhouse that would dare to call itself a "Trusted Disruptor. "The question everyone asks: How does a company formed from an investment banker's roll-up strategy and another that once made printing presses suddenly threaten the established order? The combined entity became the sixth-largest defense contractor in the United States, with approximately $17 billion in revenue and 50,000 employees, including 20,000 engineers and scientists.

This isn't just another defense consolidation story. It's about how the industry's middle market seized an opportunity while the giants were looking elsewhere. It's about challenging not just competitors, but the very nature of how defense innovation happens. And most importantly, it's about proving that in the modern defense landscape, agility might matter more than legacy.

So let's rewind 130 years and understand how we got here—starting with a printing press company in Ohio that would somehow become half of today's most intriguing defense contractor.

II. The Harris Story: From Printing Press to Defense Electronics (1895-2018)

Alfred S. Harris couldn't have imagined it. Standing in his Niles, Ohio workshop in 1895, watching his newly invented automatic sheet-feeding press revolutionize the printing industry, the idea that his company would one day build encrypted radios for special forces or night vision goggles for Army Rangers would have seemed like pure fantasy.

The "Harris Automatic Press Company" was founded by Alfred S. Harris in Niles, Ohio, in 1895. The early business was straightforward: build better printing presses. Harris's innovation—an automatic sheet-feeder that dramatically increased printing speed—made his company a darling of the booming newspaper and publishing industry.

The company spent the next 60 years developing lithographic processes and printing presses before acquiring typesetting company Intertype Corporation. This acquisition in 1957 marked Harris's first major transformation. Intertype didn't just bring typesetting technology; it brought electronic controls and early automation systems. Suddenly, Harris engineers were working with electronics, not just mechanical presses.

The real pivot came in the 1960s, driven by an unlikely catalyst: the Space Race. Harris Corporation (as it was renamed in 1974) recognized that the same precision electronics controlling their printing presses could control satellite communications. They began developing microwave and broadcast equipment, then tactical radios. By the 1970s, Harris was building secure communications systems for the military—encrypted radios that could survive battlefield conditions.

Here's where Harris's strategy diverged from typical defense contractors: they didn't abandon their commercial roots. While Lockheed and Boeing focused almost exclusively on military contracts, Harris maintained dual markets. Their broadcast division supplied TV stations while their defense division equipped soldiers. This diversification would prove crucial during defense spending downturns.

The 1990s and 2000s saw Harris aggressively acquiring complementary technologies. They bought GE's aerospace electronic systems. They acquired portions of Ericsson's defense electronics. Each acquisition added capabilities: electronic warfare systems, avionics, satellite communications. Harris was methodically building a portfolio of mission-critical, high-margin defense electronics.

The masterstroke came in 2015 with the $4.75 billion acquisition of Exelis, itself a spinoff from ITT Corporation. Exelis brought something Harris desperately wanted: night vision dominance. The company controlled roughly 80% of the U.S. military's night vision market—a position so dominant it would later complicate the L3Harris merger. Exelis also brought radar systems, electronic warfare capabilities, and most importantly, deep relationships with Special Operations Command.

By 2018, Harris Corporation was a $6 billion revenue company, far removed from its printing press origins. Based in Melbourne, Florida, it had become the Pentagon's go-to provider for tactical communications, with radios in virtually every U.S. military vehicle and aircraft. The company's Falcon radio family had become the standard for secure battlefield communications.

But CEO Bill Brown saw a problem: scale. In the consolidating defense industry, Harris was successful but subscale. Too small to compete for prime contractor roles on major programs, too specialized to diversify into new markets alone. Brown needed a partner—or a target. He found both in L3 Technologies.

III. The L3 Story: Lehman Brothers' Defense Play (1997-2018)

Wall Street, 1997. While the dot-com boom consumed most investment bankers' attention, a different opportunity caught the eye of Lehman Brothers. The end of the Cold War had triggered massive defense consolidation—Lockheed merged with Martin Marietta, Boeing acquired McDonnell Douglas, Northrop grabbed Grumman. But in selling off non-core assets to satisfy regulators, these giants were creating an opportunity.

The company was founded by, and named for, Frank Lanza and Robert LaPenta in partnership with Lehman Brothers. Lanza and LaPenta weren't typical defense executives—they were dealmakers who had helped orchestrate Loral Corporation's transformation into a defense electronics powerhouse before its acquisition by Lockheed Martin.

Their pitch to Lehman was audacious: create a new defense contractor through pure financial engineering. No factories, no legacy programs, no pension obligations. Just identify undervalued defense assets being divested by the primes, acquire them with leveraged buyouts, improve operations, and roll them up into something bigger.

L3 was formed as L-3 Communications in 1997 to acquire ten business units from Lockheed Martin that had previously been part of Loral Corporation. The initial portfolio was eclectic: aviation recorders (the famous "black boxes"), microwave components, telemetry systems, and display systems. Combined revenue: $650 million. The units had one thing in common—they were considered non-core by Lockheed but were actually critical subsystems used across multiple platforms.

Lanza and LaPenta's strategy was brilliant in its simplicity. They targeted three types of acquisitions: 1. "Orphaned" divisions of large contractors that no longer fit strategic priorities 2. Family-owned defense suppliers looking for exits 3. Distressed assets that could be turned around

The execution was relentless. Between 1997 and 2016, L3 completed over 100 acquisitions. They bought Cincinnati Electronics' infrared detector business. They acquired Titan Corporation's intelligence solutions for $2.65 billion. They picked up Wescam's electro-optical/infrared turrets. Each deal added capabilities, but more importantly, gave L3 content on hundreds of different platforms.

The company continued to expand through mergers and acquisitions to become one of the top ten U.S. government contractors. By 2010, L3 had grown to $15 billion in revenue—a 23-fold increase in just 13 years.

But this aggressive growth came with challenges. In 2010, L3 was caught in a counterfeit parts scandal, having unknowingly supplied fake Chinese-made electronic components for military equipment. The incident exposed weaknesses in L3's decentralized structure—with so many acquired companies operating semi-independently, quality control and compliance varied wildly across divisions.

The company also faced ethical controversies. Several former employees were convicted of passing classified information to competitors. L3 paid millions in settlements for overcharging on government contracts. Critics argued the company's roll-up strategy prioritized financial engineering over operational excellence.

At the end of 2016, the company changed its name from L-3 Communications Holdings, Inc. to L3 Technologies, Inc. to better reflect the company's wider focus since its founding in 1997. The rebranding signaled a shift—L3 was no longer just a communications company but a broad technology provider spanning ISR (Intelligence, Surveillance, Reconnaissance), electronic warfare, training systems, and sensors.

By 2018, under CEO Chris Kubasik (who had joined from Lockheed Martin), L3 was generating $10 billion in revenue with impressive 10% operating margins. The company had successfully positioned itself as the "merchant supplier" of choice—providing critical subsystems to all the primes without competing against them for major platform wins.

But like Harris, L3 faced a scale problem. The defense industry was consolidating further. New threats—hypersonics, cyber warfare, space—required massive R&D investments. L3 needed to get bigger or risk being acquired itself. Kubasik began looking for a transformational deal. Harris Corporation was simultaneously reaching the same conclusion.

IV. The Merger of Equals: Creating L3Harris (2018-2019)

October 14, 2018. A Sunday. The news broke before markets opened Monday: L3 Technologies and Harris Corporation would merge in an all-stock "merger of equals" valued at $33.5 billion. Defense industry watchers were stunned—not by consolidation itself, but by the structure. True mergers of equals are rare; usually one company clearly acquires another. But this deal split everything down the middle: Harris shareholders would own 54%, L3 shareholders 46%.

The strategic logic was compelling. Harris brought tactical communications, electronic warfare, and space systems. L3 brought ISR, training systems, and platform electronics. Combined, they'd have the scale to compete for prime contractor positions while maintaining their merchant supplier relationships. The companies projected $500 million in annual cost synergies and $1.9 billion in revenue synergies over three years.

But the real innovation was in addressing the cultural challenge. Rather than one company imposing its culture on the other, they agreed to build something new. Harris CEO Bill Brown would become Chairman and CEO of the combined company. L3's Chris Kubasik would be President and COO, with a clear succession plan to become CEO in 2021. Board seats were split evenly. Even the headquarters stayed in Harris's Melbourne, Florida, but L3's Arlington, Virginia offices remained a major hub. The regulatory review revealed a critical snag. The proposed acquisition would eliminate competition between the only two suppliers of U.S. military-grade image intensifier tubes, which are the key component in night vision devices such as goggles and weapon sights purchased by the Department of Defense (DoD) for the United States military. The Department of Justice's message was clear: divest or face antitrust action.

As part of that deal, Harris was required to sell its night vision division. The reasoning was that a merger of Harris and L3's night vision departments would create an effective monopoly on the night vision industry. Harris quickly reached a deal to sell its night vision business to Elbit Systems for $350 million—a fraction of its strategic value but a necessary sacrifice to complete the larger merger.

The companies navigated regulatory approvals across multiple jurisdictions—the U.S., European Union, Australia, Canada, and Turkey. Each required careful negotiation, demonstrating how the combined entity would enhance rather than reduce competition. The merger finally closed on June 29, 2019, creating the sixth largest defense company in the U.S., and a top 10 defense company worldwide – with approximately $17 billion in revenue and 50,000 employees, including 20,000 engineers and scientists.

The new L3Harris organized into four business segments: Integrated Mission Systems ($4.9 billion revenue), Space & Airborne Systems ($4.0 billion), Communication Systems ($3.8 billion), and Aviation Systems ($3.8 billion). Each segment leader came from the legacy companies, ensuring continuity while driving integration.

But the real test wasn't regulatory approval or organizational structure—it was proving the merger could deliver on its promises. The defense industry had seen too many "mergers of equals" become acquisitions in disguise, with one culture dominating and synergies evaporating. L3Harris needed to be different.

V. The Trusted Disruptor Strategy & Early Execution (2019-2022)

Chris Kubasik had a problem. As the newly appointed CEO of L3Harris in June 2021 (after serving as President and COO since the merger), he inherited a company with immense potential but no clear identity. The legacy companies had distinct reputations—Harris for reliability, L3 for agility—but what was L3Harris?

His answer came in two words that seemed contradictory: "Trusted Disruptor."

The logic was elegant. Traditional defense primes were "trusted" but slow to innovate. Silicon Valley defense startups were "disruptors" but lacked the security clearances, past performance, and scale to win major programs. L3Harris would be both—bringing commercial innovation speed to classified programs, venture-style investment to traditional capabilities. The first major validation came in January 2023 with the completion of the Viasat Link 16 Tactical Data Links (TDL) business acquisition for approximately $1.96 billion in cash. Link 16 is the military's primary tactical data exchange network—think of it as the secure WhatsApp for fighter jets, warships, and ground forces. The buy consists of Link 16 Multifunctional Information Distribution System platforms, their associated terminals, which are installed in tens of thousands of U.S. and allied systems worldwide, and space assets.

The strategic brilliance wasn't just acquiring a profitable business with approximately $400 million of revenue and an estimated $125 million of Adjusted EBITDA for the 12 months ended June 30, 2022. It was recognizing that Link 16 would be the backbone of the Pentagon's Joint All-Domain Command and Control (JADC2) initiative—the military's ambitious plan to connect every sensor to every shooter across all domains. Kubasik didn't just talk about being disruptive—he delivered. The LHX NeXt transformation program became the operational backbone of the strategy. Through our LHX NeXt initiative, we exceeded our cost-savings target for 2024, achieving $800 million, and are raising our overall cost-savings goal to $1.2 billion by the end of 2025, a year ahead of schedule. This wasn't just cost-cutting; it was a complete reimagining of how a defense contractor operates—consolidating facilities, standardizing processes, digitizing workflows.

The early results validated the approach. By 2022, L3Harris had secured positions on critical new programs: the Air Force's Advanced Battle Management System, the Army's Integrated Visual Augmentation System, and the Space Force's satellite communications architecture. The company was proving it could compete for and win next-generation programs, not just maintain legacy positions.

Portfolio optimization became another key lever. L3Harris divested non-core businesses while doubling down on areas aligned with Pentagon priorities. They sold commercial aviation assets but invested heavily in space, electronic warfare, and autonomous systems. Every move was calculated to increase exposure to high-growth, high-margin segments while reducing dependence on mature programs.

The "Trusted Disruptor" positioning was paying off. L3Harris could tell the Pentagon: "We're large enough to deliver at scale, experienced enough to execute reliably, but agile enough to innovate rapidly." It was a compelling pitch that resonated in an era where threats were evolving faster than traditional acquisition cycles could address.

VI. The Aerojet Rocketdyne Saga: From Lockheed's Loss to L3Harris's Win (2022-2023)

December 2022. The defense industry was watching closely as Aerojet Rocketdyne—the last independent U.S. supplier of rocket propulsion systems—remained in play after Lockheed Martin's failed acquisition attempt. The stakes couldn't be higher: whoever controlled Aerojet would dominate critical propulsion technology for everything from Patriot missiles to NASA's Artemis program. The backstory was crucial. Lockheed Martin's previous attempt at acquiring Aerojet for $4.4 billion ran aground amid federal regulator's antitrust concerns. The Federal Trade Commission sued to block that deal in January 2022, and the following month, Lockheed canceled plans to buy Aerojet. The FTC's logic was straightforward: Lockheed, as a major missile manufacturer, would gain the ability to cut off competitors from critical propulsion components.

L3Harris Technologies and Aerojet Rocketdyne Holdings, Inc. together announced the signing of a definitive agreement for L3Harris to acquire Aerojet Rocketdyne for $58 per share, in an all-cash transaction valued at $4.7 billion, inclusive of net debt. The December 2022 announcement shocked the industry—not because another buyer emerged, but because of who that buyer was.

Why could L3Harris succeed where Lockheed failed? The answer lay in L3Harris's unique position. Unlike Lockheed, L3Harris didn't manufacture competing missiles. They were the ultimate merchant supplier—providing subsystems to everyone without competing against anyone. The FTC's antitrust concerns evaporated. L3Harris could argue, credibly, that they would actually enhance competition by ensuring Aerojet remained an independent supplier to all missile manufacturers.

But Kubasik saw something deeper. Aerojet wasn't just a propulsion company—it was the propulsion company for next-generation threats. Hypersonic weapons, space-based interceptors, advanced missile defense—all required Aerojet's expertise. And the company was struggling. Years of ownership uncertainty had led to underinvestment, quality issues, and frustrated customers. Raytheon's CEO publicly complained about Aerojet's declining performance.L3Harris Technologies (NYSE:LHX) has completed its acquisition of Aerojet Rocketdyne, forming a fourth business segment at the company on July 28, 2023. The integration immediately showed results. L3Harris increased internal investments in Aerojet Rocketdyne by 40% year-over-year, including the expansion and modernization of manufacturing to enhance production across its product lines. Performance improvements since the acquisition include record-setting months of deliveries for five programs and reducing late deliveries by nearly half.

The turnaround was dramatic. Within a year, Aerojet went from industry laggard to performance leader. L3Harris didn't just inject capital—they brought operational discipline, modern manufacturing techniques, and most importantly, stability. Employees who had weathered years of ownership uncertainty suddenly had clear direction and resources.

The strategic value extended beyond fixing operational issues. Aerojet gave L3Harris a seat at the table for next-generation defense programs: hypersonic weapons, missile defense interceptors, space propulsion. These weren't just contracts—they were decade-long commitments that would anchor L3Harris's growth through the 2030s.

VII. Modern Operations & Business Segments (2023-Present)

Walk into L3Harris headquarters in Melbourne today, and you'll find a company transformed. The merger that created it is now five years old, the Aerojet integration complete. The question is no longer whether L3Harris can compete with the primes—it's whether the primes can keep up with L3Harris.

The company now operates through four distinct segments, each a powerhouse in its own right:

Integrated Mission Systems (~$7 billion revenue): The intelligence hub, specializing in ISR systems, maritime solutions, and electro-optical technologies. This is where L3Harris's "eyes and ears" live—the sensors and systems that provide battlefield awareness from seabed to space.

Space & Airborne Systems (~$6 billion revenue): The high-tech crown jewel, delivering space payloads, classified intelligence systems, and electronic warfare capabilities. If it flies above 50,000 feet or operates in orbit, this segment likely has a hand in it.

Communication Systems (~$4.3 billion revenue): The backbone of battlefield communications, from tactical radios to satellite communications. Every U.S. military branch depends on this segment's products for secure, reliable communications.

Aerojet Rocketdyne (~$2.5 billion revenue): The propulsion powerhouse, now firing on all cylinders after years of underinvestment. From Javelin missiles to NASA's Artemis program, this segment powers America's most critical defense and space programs. As of August 2025 L3Harris Technologies's TTM revenue is of $21.37 Billion USD. 2024 revenue of $21.3 billion, up 10%, and 4% organically, with orders of $24.2 billion and a book-to-bill ratio of 1.14x, creating a record backlog of $34 billion.

The LHX NeXt transformation program has become the engine of margin expansion. We are making impressive progress on our LHX NeXt initiative and expect to exceed the 2024 cost savings target of $400 million. As a result, we are updating our 2024 savings target to at least $600 million and now expect to reach the overall target of $1 billion a year early. By the end of 2024, the company achieved $800 million in cost savings, raising the overall goal to $1.2 billion by the end of 2025.

The operational improvements aren't just about cost-cutting. L3Harris has fundamentally reimagined how a defense contractor operates. Digital engineering reduces development cycles by 30%. Automated manufacturing increases throughput while improving quality. Predictive maintenance prevents production delays. These aren't incremental improvements—they're transformational changes that allow L3Harris to deliver faster and cheaper than competitors stuck with legacy processes.

International expansion, particularly in NATO markets, has accelerated. The Ukraine conflict highlighted the importance of interoperable systems among allies. L3Harris's communications and electronic warfare systems have become the NATO standard, opening doors to multi-billion dollar opportunities across Europe and the Indo-Pacific.

The company's positioning in emerging domains—space, cyber, hypersonics—ensures relevance for the next decade. While traditional platforms like fighter jets and ships face budget pressures, these new domains are seeing explosive growth. L3Harris has content on virtually every major space program, from missile warning satellites to lunar communications systems.

VIII. Playbook: The L3Harris Model

If you're running a mid-tier defense contractor, or thinking about consolidation in any industrial sector, the L3Harris playbook offers crucial lessons. Not all are obvious, and some contradict conventional M&A wisdom.

Lesson 1: True Mergers of Equals Can Work—With Clear Rules Most "mergers of equals" aren't. One culture dominates, executives from one side take control, and synergies evaporate in the power struggle. L3Harris avoided this by establishing clear rules upfront: split board representation, predetermined CEO succession, both headquarters remain operational. The structure forced collaboration rather than conquest.

Lesson 2: Regulatory Navigation Is Strategic, Not Reactive L3Harris didn't just respond to regulatory concerns—they anticipated them. Before announcing the Aerojet deal, they had already mapped out why their position as a merchant supplier eliminated antitrust concerns. They understood that in concentrated industries, being the arms dealer to all sides is more valuable than being another combatant.

Lesson 3: The "Disruptor" Label Must Be Earned Daily Calling yourself innovative doesn't make it true. L3Harris backs up the "Trusted Disruptor" positioning with concrete actions: 40% investment increases in acquired companies, digital transformation initiatives, willingness to exit legacy businesses. The label works because employees and customers see tangible changes, not just marketing slogans.

Lesson 4: Operational Excellence Enables Financial Engineering The Aerojet turnaround wasn't financial wizardry—it was blocking and tackling. Modernizing facilities, implementing quality systems, stabilizing the workforce. L3Harris understood that in industrial businesses, operational improvements drive financial results, not the other way around.

Lesson 5: Portfolio Shaping Never Stops Even after major acquisitions, L3Harris continues reshaping its portfolio. Divesting commercial aviation while acquiring tactical data links. Exiting low-margin businesses while investing in high-growth areas. The company treats its portfolio like an active investor, not a passive owner.

Lesson 6: Cultural Integration Requires Intentional Design L3Harris didn't let culture evolve organically post-merger. They deliberately created a new culture that borrowed the best from both companies: Harris's operational discipline with L3's entrepreneurial spirit. This required active management, from leadership messaging to compensation structures to decision-making processes.

Lesson 7: Scale Matters, But Agility Matters More At $21 billion in revenue, L3Harris has the scale to compete for major programs. But they've maintained the agility of a smaller company through decentralized decision-making, rapid prototyping capabilities, and willingness to kill underperforming programs. They've proven that size and speed aren't mutually exclusive.

IX. Power & Analysis: Bull vs. Bear Case

Bull Case: The Momentum Continues

The bullish thesis on L3Harris rests on multiple reinforcing factors:

Favorable End Markets: Global defense spending is in a multi-year upcycle. The Ukraine conflict, China tensions, and Middle East instability are driving NATO members to increase defense budgets. The U.S. defense budget continues growing above inflation. L3Harris has high exposure to priority areas: space, electronic warfare, missile defense, and secure communications.

Integration Excellence: The company has proven it can successfully integrate large acquisitions. Aerojet's turnaround from problem child to star performer demonstrates L3Harris's operational capabilities. Future acquisitions could see similar improvements.

Margin Expansion Runway: With LHX NeXt targeting $1.2 billion in savings by 2025, margins should expand from mid-15% to high-16% or beyond. This isn't speculation—the company is already delivering ahead of schedule.

Technology Moat: L3Harris's position in critical technologies—Link 16, electronic warfare, space payloads—creates significant barriers to entry. These aren't commodities that can be easily replaced or competed away.

Capital Flexibility: With strong free cash flow generation ($2.3 billion in 2024) and manageable debt levels, L3Harris has flexibility for shareholder returns, organic investment, or strategic acquisitions.

Bear Case: The Challenges Ahead

The skeptical view identifies real risks:

Integration Complexity: L3Harris is essentially running four major integrations simultaneously (original merger, Viasat TDL, Aerojet, plus ongoing LHX NeXt). This complexity creates execution risk, particularly as the company pursues aggressive cost savings.

Customer Concentration: Despite diversification, L3Harris remains heavily dependent on U.S. government spending. Any budget cuts, program cancellations, or shifts in priorities could materially impact results.

Competitive Dynamics: The defense industry continues consolidating. Larger primes have more resources for R&D and lobbying. Smaller, venture-backed companies are more agile in emerging technologies. L3Harris must fight on two fronts.

Technology Disruption: Traditional defense contractors face disruption from commercial space companies, AI startups, and software-defined systems. L3Harris's hardware-centric portfolio could become less relevant.

Geopolitical Risks: While current tensions drive demand, any de-escalation could reduce defense spending. Peace, ironically, is bad for business in the defense sector.

Valuation: After strong performance, L3Harris trades at premium multiples. Any execution stumbles or market weakness could drive multiple compression.

The Verdict

The bull case appears stronger near-term. L3Harris has clear catalysts (LHX NeXt savings, Aerojet improvements, record backlog) and favorable industry dynamics. The bear case represents longer-term risks that may take years to materialize.

The key question: Can L3Harris maintain its "Trusted Disruptor" positioning as it grows larger? History suggests that scale and innovation rarely coexist in defense contractors. But then again, L3Harris has already defied conventional wisdom multiple times.

X. Looking Forward: The Next Chapter

Standing at the threshold of 2025, L3Harris faces its most interesting chapter yet. The scrappy challenger has become an established force. The question is no longer whether L3Harris belongs among the defense industry elite—it's whether the company can reshape what that elite looks like.

The evolving threat landscape plays to L3Harris's strengths. Modern warfare increasingly depends on sensors, communications, electronic warfare, and missiles—all L3Harris specialties. The traditional platform-centric model (building aircraft carriers and fighter jets) is giving way to a network-centric model where L3Harris's technologies are essential nodes.

Emerging technologies present both opportunity and risk. Artificial intelligence will revolutionize ISR and electronic warfare—areas where L3Harris has strong positions but must continue investing. Autonomous systems could reduce demand for traditional platforms while increasing demand for sensors and communications. Space is transitioning from government-dominated to commercially-driven, requiring new business models.

The path to challenging the "Big 5" defense primes (Lockheed Martin, Boeing, Raytheon, Northrop Grumman, General Dynamics) is becoming clearer. L3Harris doesn't need to match their size—it needs to be more agile, more innovative, and more essential. The "Trusted Disruptor" positioning, if executed well, could redefine what leadership means in defense.

Key milestones to watch include reaching $23 billion revenue by 2026 (requiring ~4% organic growth), achieving 16%+ operating margins through LHX NeXt, and successfully integrating any future acquisitions while maintaining operational excellence. The company must also navigate the next administration's defense priorities and potential budget dynamics.

The ultimate test will be whether L3Harris can maintain its cultural edge as it scales. Can a $25 billion company still act like a startup when needed? Can operational excellence coexist with innovation? Can a company born from financial engineering become a technology leader?

These aren't just questions for L3Harris—they're questions for the entire defense industry as it grapples with rapid technological change, evolving threats, and budget constraints. L3Harris's answer, whatever it turns out to be, will likely shape the industry's future direction.

The printing press company and the investment banker's roll-up have come a long way. What started as two separate journeys through American industrial history has merged into something unprecedented: a defense contractor that's both massive and agile, reliable and innovative, traditional and disruptive.

Whether this paradox is sustainable remains to be seen. But for investors, customers, and competitors alike, L3Harris Technologies has become impossible to ignore. The company that didn't exist six years ago is now rewriting the rules of defense contracting.

In an industry where change happens slowly and tradition matters deeply, L3Harris has proven that transformation is possible. The next few years will determine whether that transformation becomes permanent—whether the Trusted Disruptor can truly disrupt an industry that has resisted disruption for decades.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube