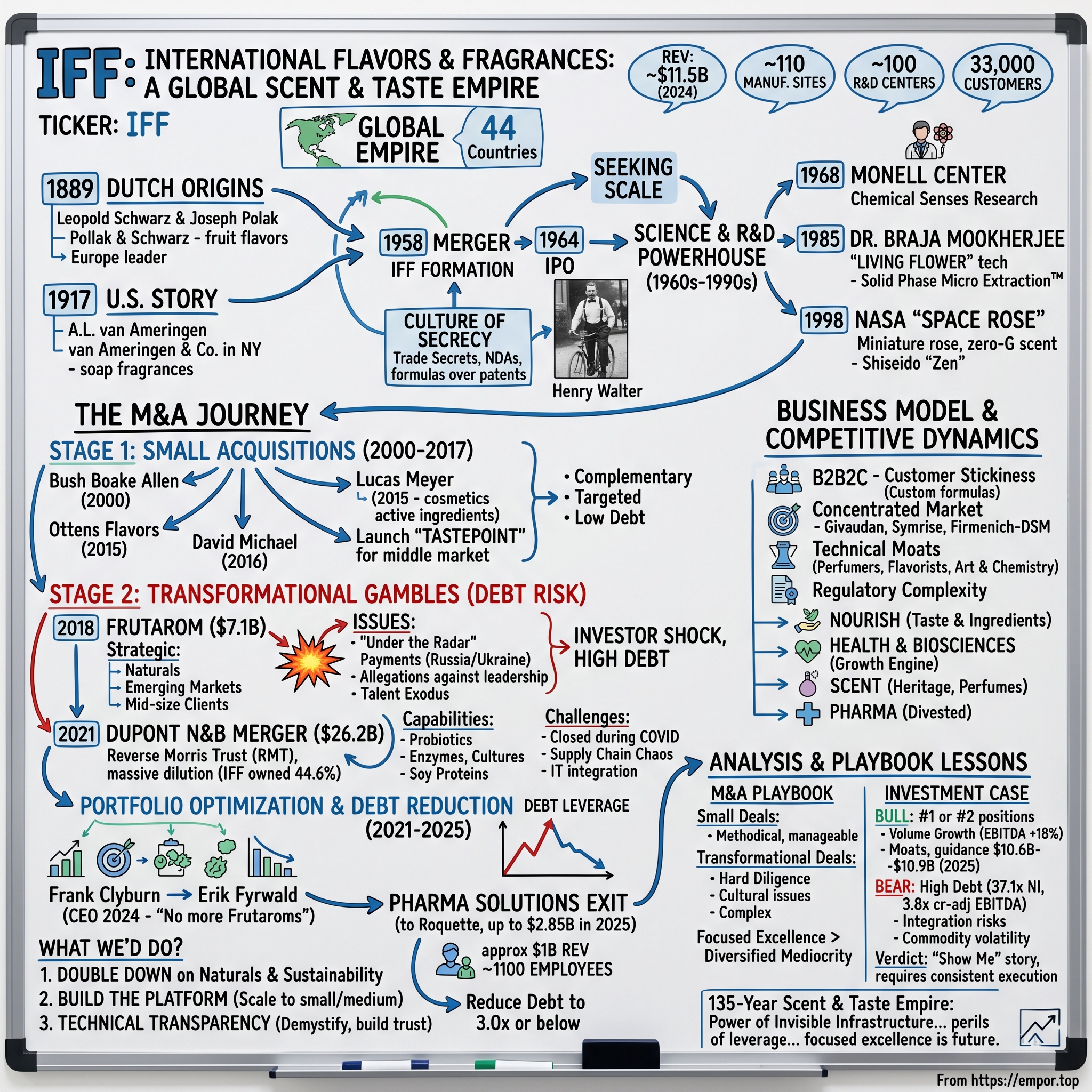

International Flavors & Fragrances: The Story of a Global Scent and Taste Empire

I. Introduction & Episode Roadmap

Picture this: You wake up, brush your teeth with mint-flavored toothpaste, shower with lavender-scented soap, put on clothes washed in fresh-scented detergent, grab a vanilla latte, and head to work. By 9 AM, you've already encountered at least a dozen products touched by one company you've probably never heard of—International Flavors & Fragrances.

IFF is a global company with a revenue of over USD 12 Billion as of 2022. International Flavors & Fragrances's revenue for the twelve months ending Dec 31, 2024 was $11.48 billion, making it one of the invisible giants of the consumer products world. This is a company that has, for over a century, been the secret ingredient in billions of products, yet remains largely unknown to the consumers who experience their work every single day.

From its roots in 19th-century Dutch spice trading to becoming a 21st-century biotechnology innovator, IFF's story is one of relentless M&A activity, scientific pioneering, and the art of creating experiences that define how we taste and smell the world around us. It's a tale of two companies becoming one, of formula secrecy rivaling Coca-Cola's, and of a business model so essential yet so hidden that most of its 33,000 customers' customers have no idea it exists.

Today, we're going to pull back the curtain on this $11.5 billion empire of the senses. We'll explore how a company built on the ephemeral—taste and smell—created one of the most durable businesses in consumer products. We'll examine their aggressive M&A playbook, including the transformative but troubled Frutarom acquisition and the massive DuPont Nutrition & Biosciences merger. And we'll analyze how new CEO Erik Fyrwald is attempting to reshape this sprawling conglomerate while managing a debt burden that has become the company's greatest challenge.

This is the story of how IFF became the company that flavors your food, scents your perfume, and increasingly, engineers the future of nutrition itself.

II. Origins: Two Companies, One Destiny (1889–1958)

The year is 1889. In the small Dutch town of Zutphen, where medieval towers still watched over cobblestone streets, two brothers-in-law sat at a kitchen table with an ambitious plan. Leopold Schwarz, who had an interest in spices, flavors, and fragrances, and his brother-in-law, Joseph Polak were about to launch what would become Pollak & Schwartz, a producer of fruit flavors and oil essences.

This wasn't just another trading company riding the coattails of Dutch colonial commerce. The brothers-in-law had a vision: to industrialize and democratize the world of flavor and fragrance. It wasn't long before this Netherlands-based start-up became the most important essence producer of the time in Europe. By the early 20th century, P&S quickly grew to 36 sites globally.

But our story takes a dramatic turn in 1917, across the Atlantic. Arnold Louis (A.L.) van Ameringen was hired by Polak & Schwarz to open P&S's U.S. office in 1917 before losing his job with them. The reason for his firing? He suggested a now-common American practice--a profit-sharing plan for employees. This progressive idea was apparently too radical for the Dutch parent company.

But van Ameringen was not one to be deterred. Relieved of his duties, he opened van Ameringen & Co. in 1918, starting with just 500 square feet of office space in New York. What followed was a stroke of marketing genius that would revolutionize American consumer products. In 1920s, he persuaded American soap manufacturers to add fragrances to products, revolutionizing the industry.

Think about that for a moment. Before van Ameringen, soap was just... soap. Functional, utilitarian, unscented. He didn't just sell fragrances; he created an entirely new consumer expectation—that cleaning products should smell pleasant. This single insight would spawn a multi-billion dollar industry.

The two companies developed along complementary paths. While both companies managed flavors and fragrances, Polak & Schwarz had particular strengths in flavors and van Ameringen-Haebler built a powerful reputation in fragrances. It was as if they were two pieces of a puzzle, separated by an ocean and a corporate firing, destined to eventually unite.

World War II brought devastation to Europe and significant challenges for P&S's operations. Meanwhile, van Ameringen's American business thrived, supplying fragrances to a booming post-war consumer economy. The stage was set for a reunion—not of the men who had parted ways decades earlier, but of the companies they had built.

III. The Merger and Going Public (1958–1964)

In 1958, forty-one years after that fateful firing, the corporate descendants of Polak & Schwarz and van Ameringen finally came together. International Flavors & Fragrances was formed in 1958 by the merger between Polak & Schwarz (P&S) and van Ameringen-Haebler. The irony wasn't lost on anyone—van Ameringen, the man P&S had fired in 1917, would become president of the merged entity.

The new venture, named International Flavors & Fragrances Inc., proved an instant success and immediately found such broad markets in the European food industry that new facilities in Holland, Switzerland, France, and Brazil were added to augment the company's older American factories. The numbers told a compelling story: Within two years foreign manufacturers of cake mixes, pharmaceutical products, gelatin desserts, candies, and soft drinks were using IFF flavorings at a rate that brought the division's sales figures to 35 percent of the $34.2 million total in 1960.

In 1958, the two companies announced their merger to become International Flavors & Fragrances Inc. IFF was listed on the New York Stock Exchange in 1964. But before the IPO, a leadership transition would set the tone for IFF's culture for decades to come.

Enter Henry Walter—one of the most colorful executives in corporate America. A rather eccentric man, Walter was daring enough to brave Manhattan's rush-hour traffic on a bicycle and, even as the head of a fragrance company, to wear red suspenders brandishing hand-embroidered skunks. Although Walter could boast a law degree from Columbia University plus almost 30 years of legal practice, he had little knowledge of the fragrance and flavor business, which he often referred to as the 'sex and hunger trade.'

Walter's leadership style was as distinctive as his fashion choices. Just as Van Ameringen had done, Walter also made secrecy his top requirement. This wasn't just corporate paranoia—in the flavor and fragrance business, formulas were everything. In one 1963 action, he chose to emphasize this mandate by suing the Cott Beverage Corporation--which had just employed a former IFF employee as their new director of research and information--maintaining that IFF's formulas for ginger ale and several other soda flavors had been usurped.

This culture of secrecy would become a defining characteristic of IFF. Unlike tech companies that patent everything, IFF's formulas remained trade secrets, passed down through generations of flavorists and perfumers like ancient recipes, protected by NDAs and a corporate culture that valued discretion above almost everything else.

IV. Building the Science Empire (1960s–1990s)

While Henry Walter rode his bicycle through Manhattan traffic, IFF was quietly building one of the most sophisticated R&D operations in the chemical industry. From the late 1960's to the 1980's, IFF soared to new heights, as the clear international leader in flavors and fragrances. The Company began investing heavily in research and development, a practice that would become its legacy.

The company's commitment to science went beyond typical corporate R&D. In 1968, in conjunction with the Monell Foundation, IFF established the Monell Chemical Senses Center, dedicated to the research of taste and smell. This wasn't just product development—it was fundamental research into how humans perceive sensory experiences.

But the breakthrough that would define IFF's innovative culture came in 1985. Dr. Braja D. Mookherjee, a scientist at IFF, pioneered Living Flower technology. Through the use of Solid Phase Micro Extraction™, which enabled IFF to capture and study the aroma components of a flower at its peak and re-create the fragrance, changing the way perfumes were created.

Think about the audacity of this innovation. For millennia, perfumers had been limited to extracting scents through distillation, expression, or chemical synthesis. Mookherjee's technology allowed IFF to capture the actual molecules a living flower releases at its peak bloom—not the scent of dead petals, but the fragrance of life itself.

Then came one of the most unusual R&D projects in corporate history. IFF sends a miniature rose plant, "Overnight Scentsation," aboard NASA's STS-95 Discovery to determine how the flower's scent changes in zero gravity. International Flavors and Fragrances (IFF), Inc., of New York, New York, discovered this new scent, known as the "space rose" note, by flying a miniature rose plant, called the "Overnight Scentsation," aboard NASA's Space Shuttle Discovery Flight STS-95.

The space rose experiment wasn't just a publicity stunt. They found that the rose was affected by the zero-gravity environment, and the overall fragrance it generated was completely different, producing an entirely new scent that was definitely not of this Earth. IFF ultimately used their findings to create a scent they called 'space rose'. The unique space rose note was extracted from the fragrant oils of 'Overnight Scentsation', and it is now a perfume ingredient. IFF commercialized the space rose scent, and the new fragrance has since been incorporated into a perfume introduced by Shiseido Cosmetics called "Zen".

By the start of the 1970's more than half of IFF sales would come from international markets. The company had transformed from a merger of two regional players into a global science-driven powerhouse, with tentacles reaching into every corner of the consumer products industry.

V. The First Wave of M&A: Small Acquisitions (2000–2017)

As the new millennium dawned, IFF faced a changing competitive landscape. Consolidation was sweeping through the industry, and the company needed scale to compete. The response was a methodical acquisition strategy that would transform IFF from a large player into the industry leader.

The first major move came in 2000. IFF acquired Bush Boake Allen, Inc.(BBA), an international chemical company with $499 million in annual sales. The acquisition made IFF the largest flavors and fragrances company in the world, with annual sales just under $2 billion, and strengthened its global position, particularly in India.

This acquisition set the template for IFF's M&A strategy: buy companies with complementary capabilities, strong regional presence, or unique technologies. Over the next 15 years, IFF would execute a series of smaller, targeted acquisitions:

In 2015, IFF announced that it completed the acquisition of Ottens Flavors. This was followed in 2016 with the acquisition of David Michael & Company. These weren't headline-grabbing deals, but they were strategically important, adding capabilities in natural ingredients and specialty flavors.

In 2015, IFF acquired Lucas Meyer Cosmetics, a cosmetic actives firm based in Canada that develops, manufactures and markets innovative ingredients for the cosmetic and personal care industry. This marked IFF's push beyond traditional fragrances into active cosmetic ingredients—substances that actually affect skin biology, not just scent.

Using this merger as a catalyst, they have since launched Tastepoint by IFF to serve dynamic middle-tier customers. This was crucial—while IFF had always served the Pepsis and Unilevers of the world, the middle market was increasingly important, filled with fast-growing brands that needed sophisticated flavors but couldn't afford IFF's traditional high-touch service model.

Each acquisition was relatively small, digestible, and integrated without major disruption. It was a conservative, deliberate approach that delivered steady growth without taking on significant debt. But by 2017, IFF's board was getting restless. Competitors were making bigger moves, and organic growth was slowing. The company needed to think bigger.

VI. The Frutarom Gamble: Betting Big (2018–2019)

On May 7, 2018, IFF announced a deal that would fundamentally alter its trajectory. The company would acquire Israeli flavor and fragrance company Frutarom for $7.1 billion—by far the largest acquisition in IFF's history.

The strategic rationale was compelling. Frutarom brought three things IFF desperately wanted: a leading position in natural ingredients (riding the clean label trend), a strong presence in emerging markets, and deep relationships with small and mid-sized customers that IFF had historically struggled to serve cost-effectively. The deal would also deliver significant synergies—IFF projected $145 million in annual cost savings by year three.

But almost immediately, there were problems. During the integration of Frutarom, IFF was made aware of allegations that two Frutarom businesses operating principally in Russia and Ukraine made improper payments to representatives of a number of customers. This wasn't just a minor compliance issue. key members of Frutarom's senior management were aware of it.

The revelations sent shockwaves through IFF. The preliminary results of IFF's investigation revealed that Frutarom had a mechanism for payments the company wanted to "make under the radar," according to sources. The scandal implicated Frutarom's top leadership, including CEO Ori Yehudai, who had received a controversial $20 million bonus just before the deal closed.

In a lawsuit filed Tuesday to Tel Aviv district court via Israel-based law firm Gornitzky & Co., IFF and Frutarom are contesting a $20 million bonus Frutarom's board approved for Yehudai prior to the completion of the company's acquisition by IFF in 2018. IFF and Frutarom are demanding that Yehudai return the bonus.

The financial impact seemed manageable—the estimated affected sales represented less than 1% of IFF's and Frutarom's combined net sales for 2018—but the reputational damage was severe. IFF's stock fell over 15% on the news, and investors began questioning whether the company had done adequate due diligence.

Beyond the scandal, integration challenges mounted. According to several people familiar with the matter who spoke to Calcalist on condition of anonymity, most of Frutarom's key management in Israel has left the company once the year-long employee retention agreements ended. The talent exodus included crucial executives who held deep customer relationships and technical knowledge.

Despite these challenges, IFF pressed forward with integration, achieving some of its promised synergies through facility consolidations and procurement savings. But the Frutarom acquisition had fundamentally changed IFF—it now carried significant debt, and investor confidence was shaken. Many on Wall Street concluded that IFF had overpaid, chasing growth at any cost.

VII. The DuPont Mega-Merger: Transformation at Scale (2019–2021)

Even as IFF was still digesting Frutarom, CEO Andreas Fibig was orchestrating an even more audacious transaction. On December 15, 2019, IFF announced it would merge with DuPont's Nutrition & Biosciences business in a complex transaction that would fundamentally reshape the company.

IFF and DuPont today announced that they have entered into a definitive agreement for the merger of IFF and DuPont's Nutrition & Biosciences (N&B) business in a Reverse Morris Trust transaction. The deal values the combined company at $45.4 billion on an enterprise value basis, reflecting a value of $26.2 billion for the N&B business.

The structure was as complex as the strategic rationale. The combination will be executed using a tax-efficient structure called a Reverse Morris Trust. This arcane tax maneuver would allow DuPont to spin off N&B to its shareholders tax-free, with those shareholders immediately owning a majority of the combined IFF. Effective at transaction close, DuPont shareholders own 55.4% of the combined company and IFF's shareholders own 44.6%.

For IFF's existing shareholders, this meant massive dilution. They would go from owning 100% of a $10 billion company to owning 44.6% of a much larger entity. The bet was that the combined company would be worth far more than the sum of its parts.

N&B brought capabilities IFF had never possessed: probiotics, enzymes, cultures, soy proteins—the building blocks of the future of food. The combination of IFF and N&B creates a global leader in high-value ingredients and solutions for the Food & Beverage, Home & Personal Care and Health & Wellness markets, with estimated 2020 pro forma revenue of more than $11 billion and EBITDA of approximately $2.5 billion, excluding synergies. The complementary portfolios give the company leadership positions within the Taste, Texture, Scent, Nutrition, Enzymes, Cultures, Soy Proteins and Probiotics ingredient categories.

The timing could not have been worse. The deal closed on February 1, 2021, in the midst of the COVID-19 pandemic. Integration teams that should have been working side-by-side were forced to collaborate virtually. Supply chains were in chaos. Customer visits were impossible.

Yet somehow, IFF managed to execute the integration while keeping the business running. The company reorganized into four divisions: Nourish (the combined taste and food ingredients business), Health & Biosciences, Scent, and Pharma Solutions. Each division was given significant autonomy, a recognition that IFF was now too complex to run as a monolithic entity.

But the debt burden was crushing. DuPont received a one-time $7.3 billion cash payment, which IFF had to finance. Combined with the Frutarom debt, IFF was now one of the most leveraged companies in its peer group. Something would have to give.

VIII. Portfolio Optimization & The Pharma Exit (2021–2025)

By 2023, the weight of IFF's debt-fueled expansion was becoming unsustainable. The company's net debt to EBITDA ratio had ballooned to dangerous levels, and rating agencies were threatening downgrades. New CEO Frank Clyburn, and later his successor Erik Fyrwald, faced a stark choice: drastically cut costs and investments, or sell assets.

They chose the latter, embarking on what they euphemistically called "portfolio optimization"—corporate speak for selling off pieces of the empire to pay down debt.

The crown jewel of the divestiture program was Pharma Solutions, a business that had come with the DuPont acquisition. IFF today announced that it has entered into a definitive agreement to sell its Pharma Solutions business unit to French leader of plant-based ingredients Roquette for an enterprise value of up to $2.85 billion, which represents an enterprise value to EBITDA multiple of approximately 13x. IFF's Pharma Solutions business is a well-established developer and manufacturer of pharmaceutical excipients.

The sale, completed in May 2025, was bittersweet. Pharma Solutions was a good business with strong margins and growth prospects. Pharma Solutions operates 10 research and development and/or production sites globally, with approximately 1100 employees, and generated approximately $1B revenue in 2023. But it was also non-core—IFF's expertise was in flavors and fragrances, not pharmaceutical excipients.

The new CEO, Erik Fyrwald, who took the helm in February 2024, brought a different philosophy. Fyrwald brings to IFF more than four decades of executive and operational experience driving innovation and profitable, sustainable growth at leading corporations in the nutrition, agriculture and chemicals industries. He most recently served as Chief Executive Officer of Syngenta, where he spearheaded the strategy that ultimately doubled the business and delivered exceptional shareholder value during his tenure.

Fyrwald was blunt about the company's predicament. The Frutarom acquisition, in particular, had been problematic. Sources indicated he assured investors: "I can assure you, we will not do anything like another Frutarom," emphasizing a commitment to acquisitions that align with IFF's strategic priorities rather than growth at any cost.

The sale of Pharma Solutions, along with other recent actions such as our dividend rightsizing, represents a significant step towards our commitment to reducing debt leverage to 3.0x or below. This also enables us to increase focus on the core drivers of long-term profitable growth and maximize value for our shareholders.

The divestitures were working. By late 2024, IFF had sold several businesses for combined proceeds exceeding $3.5 billion. The debt ratios were improving, and the company was regaining its financial flexibility. But the cost had been high—IFF was now a smaller, more focused company, having sold businesses that could have been growth platforms for the future.

IX. Business Model & Competitive Dynamics

To understand IFF's enduring success despite its recent challenges, you need to understand the unique dynamics of the flavor and fragrance industry. This is a business model unlike almost any other in the corporate world.

It is headquartered in New York City and has creative, sales, and manufacturing facilities in 44 countries. With approximately 110 manufacturing facilities and 100 R&D centers serving 33,000 customers globally, IFF operates at a scale that creates significant barriers to entry.

The business model is fundamentally B2B2C—IFF's customers are businesses, but its ultimate consumer is you and me. When Pepsi develops a new beverage, IFF's flavorists work hand-in-hand with Pepsi's product developers, creating custom flavors that become trade secrets. The same flavor is never sold to Coca-Cola. This creates incredible customer stickiness—once a flavor is in a successful product, it almost never changes.

The competitive landscape is surprisingly concentrated for such a large market. IFF estimates it has approximately 50 competitors globally, but only three real peers at scale: Switzerland's Givaudan (the largest), Germany's Symrise, and the newly merged Firmenich-DSM. Together, these four companies control roughly 50% of the global market.

The technical moats are formidable. Creating a new flavor or fragrance requires not just chemistry, but artistry. IFF employs perfumers and flavorists who train for years, like chefs or sommeliers, developing their sensory acuity and creative abilities. In 1985 he invented the Living Flower technology. His pioneering work in this field gained him international recognition. These innovations take decades to develop and cannot be easily replicated.

Regulatory complexity adds another barrier. A flavor that's approved in the US might be banned in the EU. A fragrance component that's safe for soap might be prohibited in food. IFF maintains massive regulatory affairs teams that navigate these complexities across 150+ countries—a capability that would take competitors years and millions of dollars to replicate.

The company is organized into distinct segments, each with its own dynamics:

-

Nourish (the former Taste division plus food ingredients): The largest division, serving everything from beverages to baked goods. Growth is steady but unspectacular, tied closely to global food consumption.

-

Health & Biosciences: The growth engine, riding trends in probiotics, plant-based proteins, and enzyme technology. This is where IFF is betting its future.

-

Scent: The heritage business, still creating fragrances for everything from luxury perfumes to laundry detergent. High margins but mature growth.

-

Pharma Solutions (now divested): Was a steady, high-margin business that IFF sacrificed for debt reduction.

The business model's beauty is its recurring revenue nature. Once IFF's flavor is in Oreos or its fragrance is in Tide, it generates revenue for years, often decades. The challenge is that growth requires constant innovation and either winning new customers (difficult in a concentrated market) or helping existing customers launch new products.

X. Playbook: Lessons in M&A and Integration

After nearly two decades of aggressive M&A activity, IFF's experience offers a masterclass in what works—and what doesn't—in acquisition-driven growth strategies.

The Small Acquisition Playbook (2000-2017): IFF's early acquisitions were textbook examples of successful M&A. Bush Boake Allen, Lucas Meyer, David Michael—these were digestible deals that added specific capabilities without transforming the company overnight. Integration was methodical: maintain separate sales forces initially, integrate back-office functions gradually, preserve key talent with retention packages, and achieve synergies through procurement and manufacturing optimization.

The Transformational Deal Trap (2018-2021): The Frutarom and DuPont deals represented a dramatic shift in strategy. The playbook changed from "string of pearls" to "bet the company." The lessons are sobering:

Due diligence at scale is exponentially harder. During the integration of Frutarom, IFF was made aware of allegations that two Frutarom businesses operating principally in Russia and Ukraine made improper payments—issues that somehow escaped detection during due diligence despite months of investigation and millions in advisory fees.

Cultural integration cannot be rushed. The exodus of Frutarom's Israeli management team after their retention agreements expired showed that financial incentives alone cannot preserve institutional knowledge. The entrepreneurs who built Frutarom had a different DNA than IFF's corporate managers.

Complexity compounds geometrically. Managing the integration of Frutarom while simultaneously executing the DuPont merger during COVID was like performing surgery while running a marathon. Even the best integration teams have limits.

The Portfolio Management Reality: Post-crisis, IFF has learned perhaps the most important lesson: not all revenue is good revenue. The Pharma Solutions divestiture—selling a profitable, growing business—would have been unthinkable in the growth-at-any-cost era. But Fyrwald's approach recognizes that focused excellence beats diversified mediocrity.

The new playbook emphasizes: - Maintaining debt at manageable levels (targeting 3x EBITDA or below) - Preserving investment-grade credit ratings as non-negotiable - Accepting lower growth if it means higher quality - Building versus buying where possible - Walking away from deals if the price doesn't make sense

This is less exciting than the moonshot acquisitions, but it's ultimately more sustainable. As Fyrwald noted, there will be no more Frutaroms—a tacit admission that the era of transformational M&A at IFF is over.

XI. Analysis & Investment Case

As we stand in late 2024, IFF presents a fascinating investment case—a company with world-class assets recovering from a near-death experience of excessive leverage.

The Bull Case: IFF's fundamental competitive position remains strong. The company has leading market positions in attractive end markets, with the #1 or #2 position in most of its categories. The innovation pipeline is robust—from sustainable ingredients to bioengineered proteins, IFF is investing in the right megatrends.

On a comparable basis, adjusted operating EBITDA grew 18% led by primarily volume growth and productivity gains. The company's guidance for 2025 shows continued recovery, with sales expected in the range of $10.6 billion to $10.9 billion, representing 1% to 4% comparable currency-neutral growth, and adjusted operating EBITDA expected between $2 billion to $2.15 billion.

Customer relationships remain strong. Despite the turmoil, IFF hasn't lost any major customers. In fact, the company continues to win new business, particularly in high-growth areas like plant-based proteins and natural fragrances. The technical moats—decades of formula libraries, regulatory expertise, and sensory science capabilities—remain intact.

The Bear Case: The debt burden, while improving, remains substantial. Total debt to trailing twelve months net income at the end of the fourth quarter was 37.1x. While the net debt to credit-adjusted EBITDA has improved to 3.8x, this is still elevated for a company that should be investing heavily in R&D and capacity expansion.

Integration risks persist. While the major mergers are behind IFF, the company is still working through operational challenges. The IT systems integration from the DuPont merger won't be complete until 2025. Manufacturing footprint optimization is ongoing, with facility closures disrupting operations and customer relationships.

Commodity exposure is a perpetual challenge. IFF's raw materials—from vanilla beans to petrochemical derivatives—are subject to volatile pricing. While the company has some pricing power, passing through costs to customers like Pepsi or Unilever is never easy, especially in an inflationary environment.

The Verdict: IFF is a "show me" story. The assets are valuable, the market positions are strong, and the new management team under Fyrwald seems to have learned from past mistakes. But trust, once lost, takes time to rebuild. The company needs several quarters of consistent execution—hitting guidance, reducing debt, and demonstrating organic growth—before investors will give it the premium multiple it once commanded.

For long-term fundamental investors, IFF offers an interesting risk-reward. You're buying a collection of leading businesses at a discounted valuation due to self-inflicted wounds that appear to be healing. The question is whether Fyrwald can execute the turnaround while navigating an uncertain macro environment and intense competition.

XII. Epilogue & "What Would We Do?"

Standing back and looking at IFF's 135-year journey, from a kitchen table in Zutphen to a global ingredients platform, several lessons emerge that transcend this specific company.

First, the power of invisible infrastructure. IFF built a business on something most people never think about—how things taste and smell. By becoming essential but invisible, they created a moat that's nearly impossible to replicate. The lesson for other businesses: sometimes the best position is behind the scenes, enabling others' success.

Second, the perils of financial engineering. IFF's near-disaster with leverage is a cautionary tale for the age of cheap money. When capital is free, every acquisition looks accretive. But when rates rise and growth slows, leverage becomes a straightjacket. The survivors of the next decade will be those who respected the cyclicality of capital markets.

Third, the importance of core identity. IFF lost its way when it tried to become everything—flavors, fragrances, nutrition, pharma, cosmetics ingredients. The companies that endure know what they are and, equally important, what they're not. Fyrwald's portfolio optimization is really about rediscovering IFF's core identity.

Looking forward, if we were running IFF, we would focus on three priorities:

Double Down on Naturals and Sustainability: The consumer megatrend toward clean labels and sustainable products isn't going away. IFF should be the unquestioned leader in natural flavors and fragrances, even if it means accepting lower margins in the short term.

Build the Platform Business: IFF has traditionally served large customers with bespoke solutions. But the growth is in the long tail—thousands of smaller food and personal care companies that need sophisticated ingredients but can't afford custom development. The Tastepoint platform is a start, but it needs to become a core growth driver.

Embrace Technical Transparency: The culture of secrecy served IFF well in the 20th century, but modern consumers want to know what's in their products. IFF should lead the industry in demystifying flavors and fragrances, turning technical expertise into a marketing advantage rather than hiding behind NDAs.

The next decade will determine whether IFF's current challenges were a temporary setback or the beginning of a long decline. The ingredients for success are there—world-class capabilities, essential products, and recovering financial health. The question is whether management can blend them into something greater than the sum of the parts.

For a company that has spent 135 years making things taste and smell better, the ultimate test is whether it can make its own story more palatable to investors. The early signs under Fyrwald are promising, but as any flavorist will tell you, the proof is in the tasting.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube