Leidos: From Science Startup to Defense Tech Giant

I. Introduction & Episode Roadmap

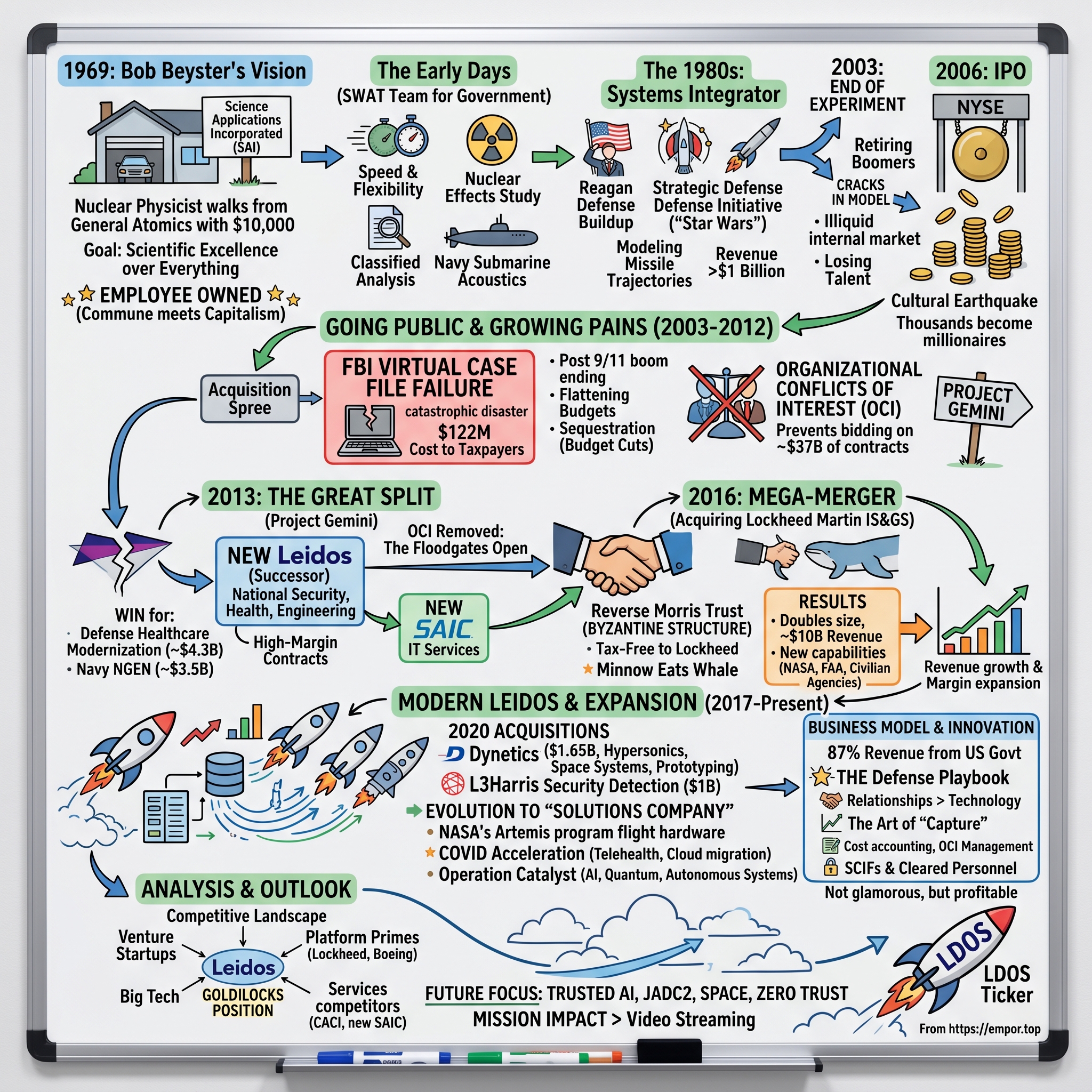

Picture this: It's 1969, and a nuclear physicist named Bob Beyster walks away from a comfortable position at General Atomics in La Jolla, California. He's got $10,000 in savings, a handful of fellow scientists willing to join him, and what many would call a quixotic dream—to build a company where the employees own the business and scientific excellence trumps everything else. Fast forward to 2024, and that "crazy little company" has morphed into Leidos, a defense technology titan generating $16.7 billion in annual revenue with 47,000 employees spread across the globe.

The transformation from Science Applications Incorporated to Leidos reads like a corporate thriller—complete with billion-dollar mergers, spectacular government contract failures, strategic splits that defied conventional wisdom, and a reverse Morris Trust transaction so complex it made Wall Street's head spin. This is the story of how a physicist's experiment in employee ownership became one of the most important companies you've probably never heard of—unless you work in defense, intelligence, or homeland security, where Leidos touches nearly everything.

Today's journey will take us through seven distinct eras of evolution. We'll start in Bob Beyster's garage-like beginnings, witness the cultural earthquake of going public after 34 years of employee ownership, dissect the FBI Virtual Case File disaster that cost taxpayers $122 million, unpack the brilliant financial engineering behind Project Gemini's corporate split, analyze the audacious Lockheed Martin acquisition that doubled the company overnight, and explore how modern Leidos navigates the intersection of Silicon Valley innovation and Pentagon procurement.

What makes this story particularly fascinating for investors and operators alike is the series of counterintuitive decisions that shaped Leidos. Why would a successful $11 billion company voluntarily split itself in half? How did a services business manage to acquire a chunk of Lockheed Martin rather than the other way around? And perhaps most intriguingly—in an era where tech companies chase consumer markets and advertising dollars, how did Leidos build one of the most profitable businesses in America by having essentially one customer: the U.S. government?

The central question we're exploring isn't just how a company grows from startup to Fortune 500. It's how an organization maintains its innovative edge while scaling into the bureaucratic labyrinth of defense contracting, how it balances classified work that can't be discussed with the transparency demands of public markets, and ultimately, whether the Leidos model represents the future of defense technology or the last gasp of an old guard about to be disrupted by venture-backed upstarts.

Buckle up. This isn't your typical Silicon Valley success story—it's something far more complex, controversial, and consequential.

II. The Bob Beyster Era: Building SAIC (1969–2003)

The year was 1969. While Woodstock defined a generation and Neil Armstrong walked on the moon, J. Robert "Bob" Beyster was having his own moon shot moment in a nondescript office park in La Jolla, California. The 45-year-old physicist had just done something that his colleagues at General Atomics thought was career suicide—he'd walked away from a senior position to start Science Applications Incorporated with little more than a vision and a radically unconventional business philosophy.

Beyster wasn't your typical entrepreneur. With a PhD in nuclear physics from the University of Michigan and years of experience in the defense establishment, he understood something crucial: the Cold War was creating an insatiable demand for scientific expertise that traditional defense contractors couldn't meet. The big primes—Lockheed, Boeing, Northrop—built hardware. But who would help the government understand the science behind Soviet weapons systems? Who would model nuclear blast effects? Who would turn theoretical physics into practical intelligence?

On February 3, 1969, Beyster founded Science Applications Incorporated (SAI) in the La Jolla neighborhood of San Diego, California. But here's where Beyster's genius—or madness, depending on your perspective—kicked in. Rather than following the venture capital playbook or seeking institutional investors, he structured SAI as an employee-owned company. Every scientist who joined would become a shareholder. Every project manager who delivered would earn equity. It was capitalism meets commune, and it was absolutely unprecedented in the defense industry.

"I wanted to create a company of owners, not employees," Beyster would later write in his autobiography. The model was simple but revolutionary: smart people solving hard problems should own the value they create. No outside investors. No Wall Street pressure. Just scientists and engineers building their own future one classified contract at a time.

The early days were lean—almost comically so. SAI's first "headquarters" was a small office above a massage parlor in La Jolla, a detail that became company lore. The initial team consisted of Beyster and a handful of fellow physicists who'd followed him from General Atomics. Their first contracts came from relationships Beyster had cultivated over years in the nuclear weapons community. A study on nuclear effects here, a classified analysis there—nothing glamorous, but each project built trust with government program managers who valued scientific rigor over corporate polish.

What set SAI apart wasn't just technical excellence—it was speed and flexibility. While the big defense contractors took months to mobilize teams, Beyster could put PhD physicists on a problem within days. When the Navy needed rapid analysis of Soviet submarine acoustics, SAI delivered. When the Air Force required complex modeling of missile trajectories, SAI's scientists were already cleared and ready. The company became the government's scientific SWAT team—expensive per hour but invaluable when intellectual firepower mattered more than manufacturing scale.

By 1975, SAI had grown to 700 employees and $25 million in revenue. But growth brought challenges to Beyster's employee-ownership model. How do you value shares in a private company with no market? How do you prevent wealth concentration among early employees while still rewarding performance? Beyster's solution was characteristically complex: an internal market where employees could buy and sell shares at prices set by a formula based on revenue and earnings. It was part stock market, part kibbutz, and it worked—sort of.

The 1980s marked SAI's transformation from boutique consultancy to systems integrator. The Reagan defense buildup meant budgets were flush, and the Strategic Defense Initiative (SDI, or "Star Wars") created demand for exactly the kind of complex systems analysis SAI specialized in. The company won massive contracts to study space-based missile defense, design command and control systems, and integrate disparate military technologies. Revenue exploded from $150 million in 1980 to over $1 billion by 1990.

But here's where the story gets interesting from a business model perspective. Unlike traditional defense contractors who made money manufacturing things, SAI made money from minds. Their "product" was expertise, delivered through time-and-materials contracts that paid for every hour a cleared scientist worked on classified problems. Margins were thin—typically 5-7%—but predictable. And because switching costs were enormous (you can't easily replace a team that's spent years understanding your classified systems), customer retention was extraordinary.

The employee-ownership culture created fascinating dynamics. Program managers who won big contracts could see their net worth jump by hundreds of thousands of dollars. Scientists who published groundbreaking classified research (that no one outside government would ever read) were rewarded with stock grants. But it also created perverse incentives. Why take risks on new technologies when steady government contracts paid the bills? Why invest in R&D when the government would pay you to do it through contracts?

Through the 1990s, SAI continued its steady march toward becoming indispensable to the national security establishment. The company provided technical support for virtually every major weapons system, ran classified programs whose names still can't be mentioned, and embedded thousands of cleared personnel inside intelligence agencies. By 2000, SAI had 42,000 employees and $5.9 billion in revenue. Beyster, now in his mid-70s, had built one of the largest employee-owned companies in American history.

But cracks were showing in the employee-ownership model. Younger employees couldn't afford to buy shares from retiring baby boomers. The internal stock market was becoming illiquid. And most problematically, SAI was losing talent to competitors who could offer stock options with real upside potential. Something had to change.

The decision to go public was agonizing for Beyster. It meant abandoning the principle that had defined SAI for 34 years. But the board—composed largely of long-time employees with millions in illiquid shares—saw no alternative. In 2003, after months of preparation and soul-searching, Beyster agreed. The physicist's experiment in employee capitalism was ending, but SAI's transformation into a public company would prove even more dramatic than anyone anticipated.

III. Going Public & Growing Pains (2003–2012)

October 13, 2006. The opening bell rings at the New York Stock Exchange, and for the first time in 37 years, shares of Science Applications International Corporation (it had added "International" and "Corporation" to its name) trade on public markets. The IPO priced at $15 per share, valuing the company at $5.7 billion. Bob Beyster, now 82, rang the bell himself—a bittersweet moment for the physicist who'd spent nearly four decades building an employee-owned empire. Within hours, thousands of SAIC employees became paper millionaires. The employee-ownership experiment was over; the public company era had begun.

The timing seemed perfect. Post-9/11 America was pouring unprecedented resources into defense and intelligence. The newly created Department of Homeland Security needed everything from border surveillance systems to bioterrorism detection. The wars in Iraq and Afghanistan demanded real-time intelligence analysis, logistics support, and technology integration on a massive scale. SAIC was perfectly positioned—it had the clearances, the personnel, and most importantly, the trust of government decision-makers who'd worked with the company for decades.

Wall Street loved the story. Here was a proven government contractor with predictable revenue streams, deep customer relationships, and exposure to the fastest-growing segments of federal spending. The stock quickly rose above $20, validating the IPO pricing and enriching employees who'd waited decades for liquidity. But beneath the surface, the transition from employee-owned to publicly-traded was creating cultural earthquakes that would define the next chapter of SAIC's story.

The first shock came in executive compensation. As a private company, Beyster had famously paid himself modestly—never more than a few hundred thousand dollars annually. But public company boards demanded "market-competitive" packages. The new CEO, Ken Dahlberg (Beyster had finally stepped aside in 2004), received a compensation package worth over $10 million. For employees who'd grown up in Beyster's egalitarian culture, it was jarring. The company that once prided itself on scientist-owners was suddenly paying Wall Street salaries to executives who'd never written a line of code or analyzed a weapons system.

Then came the growth mandate. Public markets wanted expansion, and SAIC delivered—aggressively. The company went on an acquisition spree, buying 15 companies between 2007 and 2010 for a combined $1.2 billion. Each acquisition brought new capabilities: cybersecurity firms, healthcare IT companies, energy consultancies. But integration proved challenging. SAIC's decentralized culture—where individual business units operated like fiefdoms—made it nearly impossible to achieve synergies. The company was getting bigger but not necessarily better.

The cracks really showed in execution. In December 2001, SAIC had won a $122 million contract to build the Virtual Case File (VCF) system for the FBI—a digital case management platform meant to modernize the Bureau's paper-based investigation processes. It was exactly the kind of complex systems integration project SAIC claimed to excel at. Five years and hundreds of millions of dollars later, the system was a catastrophic failure.

A 2005 Inspector General report found the VCF system had "400 problems"—from basic functionality issues to fundamental architecture flaws. FBI agents trying to use the system found it slower than paper files. Documents disappeared into digital black holes. Search functions didn't work. The FBI ultimately scrapped the entire system, writing off $122 million in taxpayer money. The failure made headlines, with Senator Patrick Leahy calling it "a stunning reversal of fortune" and demanding accountability.

For SAIC, the VCF debacle was more than just a financial hit—it was a reputational crisis. The company that had built its brand on technical excellence had delivered a lemon on one of the most visible government IT projects of the decade. Competitors pounced, using the failure to challenge SAIC's position on new contracts. Government auditors began scrutinizing SAIC's work more carefully. The aura of invincibility that Beyster had carefully cultivated over decades was shattered.

Meanwhile, the post-9/11 spending boom that had fueled SAIC's growth was ending. The Iraq War was winding down. Defense budgets were flattening. The Budget Control Act of 2011 imposed automatic spending cuts (sequestration) that threatened to slash billions from defense and intelligence budgets. SAIC's stock, which had peaked above $25 in 2010, fell below $15 as investors worried about the company's exposure to government austerity.

Leadership turmoil added to the challenges. Ken Dahlberg retired in 2009, replaced by Walt Havenstein, a former BAE Systems executive. Havenstein lasted just two years before being replaced by John Jumper, a retired Air Force general. Each leadership change brought new strategies, reorganizations, and cultural shifts that left employees confused and demoralized. The company that once prided itself on stability and scientific culture was becoming just another government contractor—bloated, bureaucratic, and struggling to grow.

By fiscal year 2012 (ended January 31, 2013), SAIC reported $11.17 billion in revenue and $525 million in net income. On paper, these were impressive numbers—the company had nearly doubled revenue since going public. But margins were compressing, organic growth was negative, and the stock was trading at just 10 times earnings, a valuation that suggested investors had lost faith in SAIC's future.

Behind closed doors, the board was discussing radical options. The company's organizational structure—a mishmash of overlapping business units serving both government and commercial customers—was creating conflicts of interest that prevented SAIC from bidding on billions in new contracts. Federal procurement rules meant that if one part of SAIC advised the government on a program, another part couldn't bid to execute it. In the interconnected world of government contracting, these conflicts were becoming existential threats.

The solution being contemplated was audacious: split SAIC in two. It would be one of the most complex corporate separations ever attempted, requiring the untangling of thousands of contracts, the division of 40,000 employees, and the creation of two independent public companies from one. Critics called it financial engineering gone mad. But John Jumper and his team saw it differently—as the only way to unlock the value trapped in SAIC's conflicted structure. Project Gemini, as it would be known internally, was about to begin.

IV. Project Gemini: The Great Split (2012–2013)

February 2012. In a nondescript conference room at SAIC's McLean, Virginia headquarters, CEO John Jumper dropped a bombshell on his senior leadership team. "We're going to split this company in two," he announced, his drawl betraying years in Texas and the Air Force. The room went silent. After a moment, someone asked the obvious question: "Why would we voluntarily make ourselves smaller when every competitor is trying to get bigger?"

Jumper's answer was counterintuitive but compelling. SAIC's organizational conflicts of interest were preventing the company from bidding on approximately $37 billion in annual contracts. The federal government's procurement rules were clear: if you advised on a program's requirements, you couldn't bid to implement it. If you evaluated contractor proposals, you couldn't submit your own. SAIC's sprawling portfolio meant it was conflicted out of massive opportunities. "We're leaving billions on the table," Jumper explained, "because we're trying to be everything to everyone."

Internal discussions about splitting SAIC had actually begun in February 2012 and progressed remarkably quickly by corporate standards. The board hired investment bankers from Citigroup and Morgan Stanley to analyze options. Management consultants from McKinsey swarmed the headquarters, mapping every contract, every customer relationship, every capability. The complexity was staggering—SAIC had over 9,000 active contracts, many with classified elements that couldn't be discussed in normal business settings.

The strategic logic crystallized around a clean break: one company would focus on technical services and solutions (keeping the Leidos name), while the other would provide IT services and support (retaining the SAIC brand). But here's where it got interesting—rather than a simple spin-off where shareholders would receive stock in both companies, SAIC's board opted for something more creative: they would first change SAIC's name to Leidos, then spin off a new company that would take the SAIC name. Critically, Leidos would be the legal successor to the original SAIC, maintaining its corporate history and contracts.

Why this Byzantine structure? Taxes, mostly. The reverse spin-off allowed the transaction to qualify as tax-free to shareholders, saving hundreds of millions in potential tax liability. It also meant that Leidos, as the legal continuation of the original company, would retain certain contract vehicles and past performance credentials that would have been difficult to transfer to a new entity.

The name "Leidos" itself became a minor corporate legend. Marketing consultants created it by clipping the word "kaleidoscope"—meant to evoke constant change and infinite possibilities. Employees had other interpretations, with jokes about "Let's Ensure Investors Deliver Our Severance" making the rounds on internal message boards. But Jumper pressed forward, selling the vision of two focused companies better able to serve their distinct markets.

By September 2012, the plan was public, and the financial engineering was breathtaking in its complexity. Leidos would emerge as a $6 billion company focused on national security, health, and engineering. The new SAIC would be a $4 billion firm providing IT services and technical support. Each company would receive approximately 20,000 employees, though the division was far from equal—Leidos got most of the classified work and higher-margin contracts, while new SAIC inherited more commoditized IT services.

The separation process itself was a masterclass in corporate surgery. Teams worked around the clock to divide everything from office leases to coffee machines. The IT separation alone cost $300 million—enterprise systems that had grown organically over 40 years had to be cloned, separated, and secured. Classified programs presented special challenges; some required approval from intelligence agencies just to discuss which company they'd belong to.

Employee morale during this period was, to put it mildly, complex. Imagine showing up to work not knowing which company you'd be working for in six months, whether your boss would still be your boss, or if your closest colleagues would become competitors. The rumor mill ran overtime. Some divisions lobbied hard to land in Leidos (seen as getting the better assets), while others saw opportunity in new SAIC's fresh start.

The human dynamics were fascinating. Long-time employees who'd joined Beyster's original company found themselves choosing sides in what felt like a corporate divorce. Research teams were split down the middle. Customer relationships that had been cultivated over decades had to be carefully managed to ensure continuity. The cleared workforce—people with top-secret clearances who couldn't easily move between companies—became pawns in a complex chess game of capability allocation.

September 27, 2013. The split was complete. At 4:01 PM Eastern Time, SAIC (now Leidos) distributed shares of new SAIC to its shareholders. Every investor who owned one share of the old SAIC now owned one share of Leidos and approximately 0.73 shares of new SAIC. Combined, the two companies were worth roughly what old SAIC had been worth—about $7 billion in market cap. Wall Street yawned.

But Jumper was playing a longer game. With organizational conflicts removed, Leidos could now bid on massive contracts it had been locked out of. The Defense Healthcare Management Systems Modernization contract, worth up to $4.3 billion. The Navy's Next Generation Enterprise Network, worth $3.5 billion. The floodgates were open.

The initial results were promising. In the first year post-split, Leidos won $7.5 billion in new contracts, a 40% increase over historical rates. Revenue grew organically for the first time in three years. The stock, which had languished in the low teens, climbed above $40. The split, it seemed, had worked.

But John Jumper wasn't done. Even as Leidos was finding its footing as an independent company, he was already planning the next transformation—one that would shock the defense industry and create overnight one of the largest government services companies in the world. The target? Lockheed Martin's Information Systems & Global Solutions business. The price tag? $4.6 billion. The structure? A reverse Morris Trust transaction so complex it would make Project Gemini look simple by comparison.

V. The Mega-Merger: Acquiring Lockheed Martin IS&GS (2016)

January 26, 2016, 6:00 AM. The press release hit the wires before markets opened, and defense industry executives across the Beltway nearly spit out their coffee. Leidos had announced a definitive agreement to combine with Lockheed Martin's Information Systems & Global Solutions business in a Reverse Morris Trust transaction valued at approximately $4.6 billion. David swallowing Goliath. The minnow eating the whale. Pick your metaphor—this wasn't supposed to happen.

To understand the audacity of this deal, consider the players. Lockheed Martin: the world's largest defense contractor, $46 billion in revenue, builder of F-35 fighters and Aegis combat systems. Leidos: a recent spinoff with $5 billion in revenue, primarily a services company, still finding its identity post-split. Yet somehow, Leidos had engineered a transaction where it would acquire a business nearly its own size from a company eight times larger.

The backstory was pure Marillyn Hewson—Lockheed's CEO who'd taken the helm in 2013 with a mandate to focus the sprawling conglomerate. IS&GS was Lockheed's IT services division, providing everything from air traffic control systems to NASA mission support. It generated $5.6 billion in revenue and employed 16,000 people. But in Hewson's vision of Lockheed as a platform-centric defense company, IS&GS was a distraction—lower margin, different customer buying patterns, minimal synergies with building fifth-generation fighters.

Enter Roger Krone, who'd replaced John Jumper as Leidos CEO in 2014. Krone was an aerospace industry veteran—former Boeing executive, engineer by training, and importantly, someone who understood both the defense platform and services worlds. When Lockheed quietly shopped IS&GS in late 2015, Krone saw opportunity where others saw impossibility.

The financial engineering required to make this deal work deserves its own business school case study. A straight acquisition was impossible—Leidos couldn't raise $5 billion in cash, and taking on that much debt would have destroyed its balance sheet. A traditional merger would have created tax liabilities that would kill the economics. The solution was a Reverse Morris Trust structure where Lockheed would receive a $1.8 billion special cash payment and its shareholders would receive approximately 50.5% of the combined company.

Here's how it worked, simplified (though nothing about this was simple): Lockheed would spin off IS&GS to its shareholders as a separate company. Simultaneously, that new company would merge with Leidos, with Leidos technically being the acquirer but Lockheed shareholders ending up with majority ownership. The structure allowed the transaction to be tax-free to Lockheed and its shareholders while giving Leidos operational control of the combined entity.

The negotiation dynamics were fascinating. Lockheed held most of the cards—they were selling a profitable, growing business with blue-chip contracts. But Krone had leverage too: few other buyers could handle IS&GS's classified work, and private equity firms would struggle with the regulatory approvals required for foreign ownership restrictions. The negotiations stretched through the fall of 2015, with teams of lawyers and bankers camped out in secure facilities to review classified contract details.

The deal would nearly double Leidos's size to approximately 33,000 employees and $10 billion in revenue. But size was just part of the story. IS&GS brought capabilities Leidos desperately needed: a massive presence at NASA, including the contract to operate IT for the International Space Station; the FAA's En Route Automation Modernization program, managing air traffic control for the entire United States; and deep relationships with civilian agencies that Leidos had never successfully penetrated.

The cultural integration challenge was immense. IS&GS employees were used to being part of Lockheed Martin—the gold standard of defense contractors, with its prestigious heritage and platform-building prowess. Now they were joining Leidos, a company many had never heard of, with a funny name and a reputation as a services shop. The day the deal was announced, IS&GS facilities buzzed with anxiety. Would there be layoffs? Would benefits change? Would the Lockheed security clearance premium disappear?

Krone moved quickly to address concerns. He flew to IS&GS facilities in Houston, Denver, and Gaithersburg, holding town halls where he promised minimal layoffs and respect for IS&GS's culture. "We're not acquiring you to break you apart," he told employees. "We're acquiring you because you're excellent at what you do." Behind the scenes, integration teams worked to identify synergies without destroying what made IS&GS valuable—its customer relationships and technical expertise.

The regulatory approval process was its own adventure. The Department of Justice worried about competition implications—the combined company would be the largest provider of IT services to the federal government. The Committee on Foreign Investment in the United States (CFIUS) had to ensure no classified information would be compromised. Intelligence agencies conducted security reviews of the new ownership structure. Each approval required extensive documentation, testimony, and in some cases, agreeing to divest certain contracts to preserve competition.

August 16, 2016. After seven months of regulatory review, integration planning, and financial gymnastics, the deal closed. The transaction was immediately recognized as one of the biggest thus far in the consolidation of the defense sector. Leidos stock, which had traded around $50 before the announcement, initially dropped to $45 as investors digested the complexity and integration risk. Lockheed shares, conversely, jumped 5% as investors applauded Hewson's focus on core platforms.

The first hundred days post-merger were crucial. Krone and his team had to deliver on promised synergies—$120 million annually—while maintaining operational excellence on thousands of critical government contracts. They reorganized the combined company into four divisions: Defense & Intelligence, Civil, Health, and Advanced Solutions. Each division got a mix of heritage Leidos and IS&GS assets, forcing integration from day one.

The wins came quickly. The combined company's scale allowed it to bid on contracts neither company could have won alone. The DISA Encore III contract, worth up to $17.5 billion. The Navy's NGEN-R contract, worth $7.7 billion. The synergies weren't just about cost cutting—they were about capability. IS&GS's air traffic control expertise combined with Leidos's security cleared workforce opened entirely new markets.

But the real test would come in the following years. Could Krone successfully integrate two companies with different cultures, systems, and approaches to business? Could Leidos maintain IS&GS's blue-chip contracts while improving margins? Could a services company thrive in an era where everyone was talking about artificial intelligence, autonomous systems, and commercial technology disrupting traditional defense?

The answer would reshape not just Leidos, but the entire government services industry. The merger had created a new model—a services company with the scale to compete with platform builders, the technical depth to tackle complex integration challenges, and the financial strength to invest in next-generation capabilities. The question now was whether Krone could execute on that vision while navigating an increasingly complex defense market.

VI. Modern Expansion & Acquisitions (2017–Present)

January 2020. While the world was about to discover COVID-19, Roger Krone was in Huntsville, Alabama, shaking hands on Leidos's acquisition of Dynetics for approximately $1.65 billion. The timing seemed almost surreal—as global markets prepared for pandemic-induced chaos, Leidos was doubling down on hardware capabilities with its largest acquisition since the Lockheed Martin deal. But Krone saw something others missed: the future of defense wasn't just about services or platforms—it was about rapidly prototyping solutions that blurred the line between both.

Dynetics wasn't your typical government contractor. Founded in 1974 by Herschel Matheny and Steve Gilbert in a Huntsville pizza parlor (apparently pizza parlors and massage parlor-adjacent offices were a theme in defense contracting origin stories), the company had built a reputation as the skunk works for companies that already had skunk works. When Lockheed needed help with hypersonic systems, they called Dynetics. When NASA needed innovative solutions for space launch systems, Dynetics delivered. The company's 2,100 employees weren't just engineers—they were problem-solving artists.

The strategic logic was compelling. Leidos had successfully integrated IS&GS and proven it could handle large-scale M&A. But the company was still seen as primarily a services player in a market increasingly enamored with high-tech hardware. Dynetics brought instant credibility in hypersonics, space systems, and weapon prototyping—exactly the capabilities the Pentagon was prioritizing in its pivot toward great power competition with China and Russia.

Just months later, in May 2020, Leidos announced the acquisition of L3Harris Technologies' Security Detection and Automation business for $1 billion. While the world was locked down, Krone was building an empire. The L3Harris business brought market-leading airport security screening technology—those CT scanners that had become ubiquitous in the post-9/11 world. With air travel decimated by COVID, the price was right, and Krone bet correctly that travel would eventually rebound.

The integration of these acquisitions during a global pandemic presented unique challenges. Town halls became Zoom calls. Integration meetings happened in virtual reality. Due diligence on classified programs required elaborate protocols to maintain security while working remotely. Yet somehow, Leidos made it work. The company's distributed workforce—already accustomed to working at customer sites—adapted more readily than traditional manufacturers who required physical presence.

The pandemic also accelerated trends that benefited Leidos. The government's push for modernization went into overdrive as agencies realized their technical infrastructure couldn't handle remote work. The Department of Veterans Affairs needed to scale telehealth from thousands to millions of appointments. The CDC required real-time data integration systems for tracking COVID spread. The Defense Department accelerated cloud migration timelines by years. Leidos was perfectly positioned—it had the contracts, clearances, and capabilities to deliver at pandemic speed.

By 2021, the transformation was remarkable. Leidos had evolved from a pure services company to what Krone called a "solutions company"—capable of designing, building, and operating complex systems. The company's work on NASA's Artemis program exemplified this evolution. Leidos wasn't just providing IT support; it was building critical flight hardware for humanity's return to the moon. The company that Bob Beyster started to analyze nuclear weapons was now building spacecraft.

The financial results reflected this transformation. Revenue grew to $16.7 billion in 2024, with a backlog of $43.6 billion—roughly 2.6 years of revenue visibility. More importantly, the mix had shifted. High-margin technology solutions now represented 40% of revenue, up from less than 20% before the Lockheed merger. The company was winning larger, longer-duration contracts that provided stable cash flows for reinvestment.

The competitive landscape had also shifted in Leidos's favor. Traditional competitors like SAIC (the new version) and CACI lacked Leidos's scale and breadth. Platform-focused companies like Lockheed and Northrop were pulling back from services markets. New venture-backed entrants like Palantir and Anduril had buzz but lacked the cleared workforce and past performance credentials needed for large contracts. Leidos occupied a sweet spot—big enough to compete for massive contracts, agile enough to adopt new technologies, and trusted enough to handle the government's most sensitive work.

But Krone wasn't resting on his laurels. In 2022, he launched Operation Catalyst, an internal innovation program designed to accelerate technology adoption across the company. The initiative funded internal startups, partnered with commercial technology companies, and created innovation labs where engineers could experiment with AI, quantum computing, and autonomous systems. It was Bob Beyster's scientific culture meets Silicon Valley's move-fast ethos.

The culture transformation was perhaps the most remarkable achievement. Through multiple mergers and acquisitions, Leidos had somehow maintained an identity. Employee engagement scores improved. Voluntary turnover decreased. The company regularly appeared on "best places to work" lists—not bad for an organization that had been through corporate splits, massive mergers, and a global pandemic in less than a decade.

As 2024 drew to a close, Leidos stood at another inflection point. Krone had announced his retirement, set for May 2024, passing the torch to Tom Bell, a company veteran who'd run the Defense & Intelligence segment. The transition felt symbolic—from an era of transformation through acquisition to one of organic innovation and growth. Bell inherited a company dramatically different from the one Krone had taken over a decade earlier: larger, more capable, and positioned at the intersection of every major defense technology trend.

The question now wasn't whether Leidos could compete—it had proven that definitively. The question was whether it could lead. Could a company born from government services become a true innovation engine? Could it bridge the gap between Silicon Valley's technology and Washington's requirements? Could it maintain its cultural cohesion while continuing to grow? The next chapter would provide answers, but first, it's worth understanding exactly how this $16.7 billion machine actually makes money.

VII. Business Model & Customer Concentration

Step inside Leidos's Reston, Virginia headquarters, and you'll find a wall displaying the company's major contracts—each represented by a small placard with a code name, dollar value, and duration. It looks like a trophy case, but it's actually a risk map. Because here's the thing about Leidos's business model that would terrify most CEOs: approximately 87% of revenue comes from contracts with the U.S. federal government. The Department of Defense alone accounts for nearly 60%. It's customer concentration that would make any MBA professor reach for the red pen.

Yet this concentration is precisely what makes Leidos valuable. In the peculiar economics of government contracting, having one customer with thousands of buying offices, multi-year funding authorizations, and essentially zero credit risk isn't a bug—it's a feature. The U.S. government spent $765 billion on defense in 2024. It's the world's largest, most reliable customer. And once you're embedded in its operations, switching costs create moats that Warren Buffett would envy.

The company operates through four main segments. Defense & Intelligence, the largest at roughly 45% of revenue, handles everything from maintaining military communications networks to analyzing satellite imagery for the CIA. Civil, about 30% of revenue, includes air traffic control systems, NASA mission support, and federal agency IT modernization. Health, 20% of revenue, manages electronic health records for the Defense Department and supports CDC disease surveillance. Advanced Solutions, the smallest but fastest-growing at 5%, develops hypersonic systems, directed energy weapons, and other classified technologies that can't be discussed in polite company.

The contract structure is where things get interesting. About 60% of Leidos's revenue comes from cost-reimbursable contracts—the government pays all allowable costs plus a fee. It's like being a lawyer billing by the hour, except your client has a $800 billion annual budget and pays on time. These contracts transfer minimal risk to Leidos; if costs increase, the government pays. The trade-off is lower margins—typically 6-8%—but predictable cash flows that Wall Street loves.

The remaining 40% comes from fixed-price contracts, where Leidos agrees to deliver a capability for a set price. Miss your budget? That's your problem. Deliver under budget? You keep the difference. These contracts can generate margins above 10% when executed well but can also become money pits when requirements change or technical challenges emerge. The art is in the bidding—price too high and lose to competitors; price too low and lose your shirt.

But here's the secret sauce: indefinite delivery/indefinite quantity (IDIQ) contracts. These are essentially hunting licenses—multi-year agreements where the government can order services as needed. Leidos holds several massive IDIQs, including the DISA Encore III (potential $17.5 billion value) and SEWP V (potential $10 billion). Once you're on an IDIQ, you're competing against a small group of pre-approved vendors rather than the entire market. It's like being admitted to an exclusive club where members get first dibs on billions in government spending.

The sales cycle in this business would drive a Silicon Valley startup founder insane. Major contracts can take 18-24 months from initial request for proposal (RFP) to award. The proposal for a billion-dollar contract might run 10,000 pages, require input from hundreds of employees, and cost millions to prepare. Leidos submitted over 2,000 proposals in 2023, winning approximately 40%—an impressive rate in an industry where 25% is considered good.

The competitive dynamics are fascinatingly complex. On Monday, Leidos might partner with Booz Allen on a homeland security contract. On Tuesday, they're competing head-to-head for a Navy IT modernization program. On Wednesday, they're subcontractors to each other on a classified intelligence program. These "co-opetition" relationships require careful management—share too much with partners and lose competitive advantage; share too little and lose the contract.

International business, while only 5% of revenue, represents both opportunity and challenge. The UK Ministry of Defence is Leidos's largest international customer, primarily through the company's logistics support for the British Army. Australia, where Leidos provides maritime systems, is growing rapidly as that country increases defense spending to counter China. But international expansion is complicated by export controls, security clearance requirements, and the need for local partnerships. Every country wants industrial offsets—if Leidos wins a $100 million contract in Saudi Arabia, it might need to invest $30 million in local capabilities.

The working capital dynamics would make a CFO at a normal company weep. Leidos routinely has billions in unbilled receivables—work completed but not yet invoiced due to government contracting rules. The company might deliver services in January but not receive payment until June. This creates a constant need for working capital financing, typically through revolving credit facilities. The upside? Once you're in the payment system, the U.S. government never defaults.

Pricing discipline is crucial but complicated. The government audits everything—labor rates, overhead allocation, profit margins. The Defense Contract Audit Agency (DCAA) has permanent offices at Leidos facilities, reviewing costs in real-time. Price too aggressively and face protests from competitors. Price too conservatively and leave money on the table. The company maintains elaborate cost accounting systems that would make Amazon's logistics look simple.

The business model creates interesting investor dynamics. Revenue visibility is exceptional—that $43.6 billion backlog provides years of predictability. But growth is inherently limited by government spending patterns. Leidos can't suddenly double revenue by launching a viral product or expanding internationally. Growth comes through winning share from competitors, expanding into adjacent markets, or benefiting from increased government spending. It's a marathon, not a sprint.

The capital requirements are surprisingly light for a $16 billion revenue company. Unlike platform manufacturers who need massive factories, Leidos's primary assets are people and security clearances. Capital expenditures run about 1% of revenue—mostly IT systems and secure facilities. This creates impressive cash generation, with free cash flow typically exceeding $1 billion annually. The challenge isn't generating cash but deploying it effectively in a business where organic growth is constrained.

This model has created a fascinating paradox. Leidos is simultaneously one of the most stable businesses in America (try finding another company where 87% of revenue comes from contracts with the world's most creditworthy customer) and one of the most complex (navigating thousands of contracts across classified and unclassified programs with constantly changing requirements). It's a business model that rewards patience, process excellence, and deep customer relationships over disruption and rapid scaling. Not exactly the Silicon Valley playbook, but generating returns that would make many tech companies envious.

VIII. Technology & Innovation Strategy

Walking through Leidos's Innovation Center in San Diego, you encounter something unexpected in a government contractor: a quantum computer. Not a mockup or a presentation slide, but an actual, operational quantum system humming away at near absolute zero. Next door, engineers are training AI models on classified datasets. Down the hall, a team is developing directed energy weapons that sound like science fiction. This isn't your grandfather's government contractor—it's where DARPA's wild ideas meet operational reality.

The innovation challenge facing Leidos is unique. Unlike commercial tech companies that can iterate quickly and fail fast, every line of code Leidos writes might end up in a weapons system or critical infrastructure. Unlike traditional defense contractors that spend decades developing platforms, Leidos needs to deliver technology solutions in months. The company sits at an uncomfortable intersection—too slow for Silicon Valley, too fast for traditional defense.

Tom Bell, who took over as CEO in 2024, articulated the strategy simply: "We're not trying to out-Google Google or out-Lockheed Lockheed. We're building trusted AI and autonomous systems for missions where failure isn't an option." It's a narrow target, but a lucrative one. The Pentagon's AI budget alone is projected to reach $30 billion by 2030. Someone needs to make that technology work in classified environments, with legacy systems, under adversarial conditions. That someone is increasingly Leidos.

The R&D approach differs radically from both commercial tech and traditional defense. Leidos spends about 3% of revenue on internal R&D—roughly $500 million annually. That's less than half what a commercial software company might spend, but here's the kicker: the government funds another $2 billion in R&D through contracts. It's like having venture capitalists who pay you to develop technology they'll then buy. The DARPA model on steroids.

Take the company's work on AI-enabled intelligence analysis. The National Geospatial-Intelligence Agency generates petabytes of satellite imagery daily—far more than human analysts can review. Leidos developed machine learning systems that can identify objects, detect changes, and flag anomalies across millions of images. But unlike commercial computer vision that might misidentify a cat as a dog (embarrassing but not catastrophic), misidentifying a missile launcher as a truck could start a war. The technology needs to be explainable, auditable, and reliable at levels commercial AI never attempts.

The partnerships strategy reflects this hybrid approach. Leidos doesn't try to build everything internally. In 2023, the company partnered with Microsoft on secure cloud services, with Amazon on AI tools, and with dozens of startups on specific capabilities. But integration is everything. Commercial technology rarely works out-of-the-box in classified environments. Leidos's value-add is making consumer-grade innovation work in defense-grade applications.

The classified technology portfolio remains largely mysterious, hidden behind security clearances and need-to-know restrictions. But hints emerge in contract awards and carefully worded press releases. Leidos is working on hypersonic defense systems that can track and potentially intercept weapons traveling at Mach 5+. The company's directed energy programs are developing laser systems that can disable drones and missiles at the speed of light. Its cyber capabilities allegedly include tools that make corporate penetration testing look like child's play.

One of the most interesting innovation areas is what Leidos calls "digital modernization"—essentially, dragging government IT systems from the mainframe era into the cloud age. This isn't sexy work, but it's insanely lucrative and technically challenging. Imagine migrating a 40-year-old COBOL system that processes nuclear launch codes to a modern architecture. You can't have downtime. You can't lose data. You can't introduce vulnerabilities. The technical complexity rivals anything Silicon Valley attempts, but with zero margin for error.

The Advanced Solutions segment represents Leidos's bet on next-generation capabilities. Born from the Dynetics acquisition, this group operates more like a traditional defense contractor—building prototypes, testing systems, breaking things. The segment's crown jewel is its hypersonics work, where Leidos is developing both offensive and defensive systems. The physics involved—managing plasma fields at Mach 20, maintaining communications through ionized air, surviving temperatures that melt most materials—pushes the boundaries of current technology.

Space represents another frontier. Leidos isn't building satellites (leave that to Lockheed and SpaceX) but rather the ground systems that control them, process their data, and integrate their capabilities into military operations. The company's work on the Space Force's ground control systems positions it at the center of the military's pivot to space as a warfighting domain. As one executive noted, "Everyone focuses on what's flying overhead. We focus on making it useful to the warfighter on the ground."

The cybersecurity portfolio spans from defensive (protecting government networks) to offensive (capabilities that remain classified). Leidos operates one of the largest Security Operations Centers in the government contracting space, monitoring thousands of networks for intrusions. But the real innovation is in automated response—AI systems that can detect, analyze, and neutralize threats faster than human operators can react. In cyber warfare, milliseconds matter.

The innovation culture faces constant tension between commercial speed and government process. Engineers recruited from Google or Facebook often struggle with the pace—what takes weeks in Silicon Valley takes months in government contracting. But they're also working on problems that matter. As one engineer who left Netflix for Leidos explained, "I went from optimizing video streaming to protecting the nation. The code reviews take longer, but the mission impact is incomparable."

The intellectual property strategy is deliberately minimal. Unlike commercial tech companies that patent everything, Leidos files relatively few patents—maybe 50-100 annually. Why? Most of the innovative work is classified, and patents require public disclosure. The company's IP moat comes from trade secrets, security clearances, and integration expertise rather than patent portfolios. You can't disrupt what you can't see.

Investment allocation reflects portfolio thinking. About 40% of R&D goes to evolutionary improvements—making existing systems better, faster, cheaper. Another 40% funds next-generation capabilities—AI, autonomy, quantum. The final 20% is reserved for what executives call "wild bets"—technologies so advanced they might not work but could be game-changing if they do. It's a portfolio approach that would be familiar to any venture capitalist, just applied to national security rather than consumer apps.

The measurement of innovation success differs from commercial metrics. Leidos doesn't track daily active users or app store ratings. Success is measured in mission outcomes—satellites launched successfully, cyber attacks prevented, soldiers returned home safely. It's harder to quantify but ultimately more meaningful. As one program manager noted, "Our products don't go viral, but they do keep the country safe."

Looking ahead, Leidos's innovation strategy faces both opportunities and threats. The opportunity: government demand for advanced technology is exploding, and Leidos is perfectly positioned to deliver. The threat: venture-backed defense startups are attacking traditional contractors with commercial technology and Silicon Valley speed. The question isn't whether Leidos can innovate—it clearly can. The question is whether it can innovate fast enough to maintain its competitive position as the boundaries between commercial and defense technology continue to blur.

IX. Playbook: Lessons in Defense Contracting

In 2019, a Silicon Valley startup with cutting-edge AI technology and $500 million in venture funding decided to pursue a major Defense Department contract. They had superior technology, lower costs, and moved at startup speed. Leidos was the incumbent—slower, more expensive, using older technology. Eighteen months later, Leidos won the contract extension worth $7.5 billion. The startup didn't even make the final round. Welcome to the bizarre physics of government contracting, where being better, faster, and cheaper often isn't enough.

The first lesson in the defense contracting playbook is deceptively simple: relationships trump technology. The startup's CEO had never served in the military, never held a security clearance, never navigated the Pentagon's five-sided maze. Leidos's capture team included three retired generals, former senior intelligence officials, and executives who'd worked with the customer for decades. They knew not just what the customer said they wanted (the RFP requirements) but what they actually needed (the unstated mission priorities). In Silicon Valley, the best product wins. In Washington, the most trusted partner wins.

Consider the art of "capture"—defense-speak for business development. It starts years before an RFP is released. Leidos maintains a capture budget exceeding $100 million annually, funding teams that do nothing but build relationships with potential customers. They attend industry days, sponsor conferences, hire retired officials who understand agency priorities. When the RFP finally drops, Leidos has already shaped its requirements through months of "helping" the customer think through their needs. It's not corruption—it's completely legal and expected. But it creates massive advantages for incumbents who understand the game.

The proposal process itself is orchestrated warfare. For a major contract, Leidos might assign 200 people full-time for six months. Writers, designers, cost analysts, technical experts, and "pink teams" that review everything with fresh eyes. The proposal center operates like a military command post—war rooms with requirements matrices covering entire walls, color-coded schedules tracking thousands of deliverables, security officers ensuring no classified information leaks into unclassified sections. The final proposal might cost $10 million to produce. Startups simply can't match this resource intensity.

Then there's the black art of pricing. Government contracting isn't about offering the lowest price—it's about offering the best value within extremely specific parameters. Leidos maintains teams of cost estimators who understand exactly how government evaluators score proposals. Price too low and you're deemed "unrealistic" and disqualified. Price too high and you lose on value. The sweet spot is typically 5-7% below the government's internal estimate—close enough to be credible, low enough to win. But finding that spot requires intelligence gathering that borders on corporate espionage (though always within legal bounds).

Organizational Conflicts of Interest (OCI) management is another crucial capability. If Leidos advises the Army on requirements for a new system, it typically can't bid to build that system—that would be an OCI. But the rules are labyrinthine, with exceptions, waivers, and workarounds. Leidos maintains a dedicated OCI management office that tracks every contract, every customer interaction, every potential conflict. They've turned OCI management into a competitive weapon, structuring deals to lock out competitors while preserving their own eligibility.

The contract protest system adds another layer of complexity. Lose a major contract? You can protest to the Government Accountability Office (GAO), effectively freezing the award for months while GAO investigates. Leidos protests strategically—not every loss (that would damage relationships) but enough to keep competitors honest. They've also mastered defensive protests, structuring proposals to minimize protest grounds. It's lawfare at its finest, where legal maneuvering matters as much as technical excellence.

Managing cleared personnel represents a unique challenge. Leidos employs thousands of people with top-secret clearances, some with access to Sensitive Compartmented Information (SCI) that requires special facilities. These clearances can take 12-18 months to obtain and cost $15,000+ per person. Once cleared, these employees become incredibly valuable—and mobile. Competitors constantly poach cleared staff. Leidos responds with retention bonuses, career development programs, and most importantly, interesting work. As one executive noted, "Cleared employees are like professional athletes—you need to constantly recruit them, even your own."

The facilities infrastructure is another hidden moat. Leidos operates dozens of SCIFs (Sensitive Compartmented Information Facilities)—specially constructed spaces where classified work can be performed. Building a SCIF costs millions, requires government certification, and takes months. You can't just rent WeWork space and start doing classified work. This physical infrastructure creates massive barriers to entry for new competitors and switching costs for customers who've integrated their operations with Leidos facilities.

Program execution is where the rubber meets the road. Unlike commercial contracts where you might negotiate changes or pivot strategies, government contracts are carved in stone. Miss a milestone? Face liquidated damages. Deliver late? Risk termination for default—the death penalty of government contracting that effectively bars you from future work. Leidos has mastered the art of risk-managed execution, using earned value management systems that track thousands of variables in real-time. They know weeks in advance if a program is drifting off track and can surge resources to recover.

The M&A integration playbook deserves special attention. Leidos has acquired and successfully integrated multiple large businesses—a rarity in government contracting where cultural clashes often destroy value. The key is rapid customer engagement. Within days of closing an acquisition, Leidos executives visit every major customer to assure continuity. Program managers are retained with golden handcuffs. Systems integration is phased to avoid disruption. Most importantly, they preserve what made the acquired company valuable while adding Leidos's scale advantages.

Capital allocation in this industry follows different rules than commercial businesses. You can't just invest in growth—the government budget cycle constrains expansion. Instead, Leidos focuses on capability investments that increase win rates and margins. A new SCIF in Huntsville might only generate $10 million in direct revenue but enables $500 million in classified contracts. An AI lab might lose money for years but positions the company for next-generation contracts. It's patient capital allocation for a patient industry.

The international expansion playbook is still being written. Unlike U.S. contracts where processes are standardized, every country has unique requirements. The UK wants industrial partnerships. Australia demands local content. Middle Eastern countries expect offset investments. Leidos is learning to navigate these requirements while maintaining profit margins, but it's slow going. As one executive admitted, "We've been spoiled by the U.S. market. International is like learning a new language for every country."

Perhaps the most important lesson is about time horizons. In Silicon Valley, strategies are measured in quarters. In defense contracting, they're measured in decades. The relationships Leidos builds today will generate contracts in 2030. The clearances they sponsor now will provide competitive advantages in 2035. The technologies they're developing might not see operational use until 2040. It requires a patience that public markets struggle to understand but generates returns that compound over time.

The playbook ultimately comes down to trust. The U.S. government is handing Leidos the keys to critical national security capabilities. They're not just buying technology or services—they're buying confidence that Leidos will be there in crisis, will protect classified information, will deliver when American lives are on the line. That trust, built over decades and validated through thousands of successful programs, is Leidos's true competitive advantage. It can't be disrupted by better technology or lower prices. It can only be earned through consistent execution over time—something no startup, no matter how innovative, can accelerate.

X. Analysis & Investment Case

Let's cut through the government contracting complexity and ask the question that matters: Is Leidos a good investment? The bull case is compelling—dominant market position, massive barriers to entry, predictable cash flows, and exposure to secularly growing defense technology spending. The bear case is equally valid—customer concentration risk, margin pressure from competition, and disruption threats from venture-backed startups. Like most interesting investment decisions, the answer isn't obvious.

Start with competitive positioning. Leidos sits in an enviable spot—too big for small competitors to challenge directly, too agile for large platform manufacturers to compete with effectively. Against pure-play government services competitors like Booz Allen Hamilton ($11 billion market cap) or CACI ($10 billion market cap), Leidos has clear scale advantages. Its $16.7 billion in revenue provides leverage in contract negotiations, deeper resources for capture activities, and the ability to bid on massive contracts that smaller players can't handle. SAIC 2.0, the company Leidos spawned, has struggled to find its identity with just $7.5 billion in revenue and narrower capabilities.

The comparison with General Dynamics' IT services unit (GDIT) is more interesting. GDIT generates similar revenue (~$13 billion) but benefits from being part of a $70 billion defense platform giant. Yet Leidos often beats GDIT on major contracts because it can move faster without the bureaucracy of a massive parent. It's the Goldilocks position—big enough to compete, small enough to be nimble.

Financial metrics tell a story of steady, unspectacular excellence. Revenue growth averaged 6% annually over the past five years—not tech-like growth, but remarkable consistency through COVID, government shutdowns, and budget sequestration. EBITDA margins hover around 10-11%, respectable for services but below the 15%+ that platform manufacturers achieve. Return on invested capital runs 12-14%, above the cost of capital but not spectacular. It's a business that generates solid returns without fireworks.

The cash generation is where Leidos shines. Free cash flow exceeds $1 billion annually, representing a 6-7% yield on the current $20 billion market cap. The company returns most of this to shareholders through dividends (2.5% yield) and buybacks ($500-700 million annually). It's not growth investor catnip, but for yield-focused investors in a low-rate environment, it's attractive. The cash flow is also remarkably stable—government contracts provide visibility, cost-plus structures limit risk, and working capital needs are predictable.

But let's address the elephant in the room: customer concentration. With 87% of revenue from the U.S. government, Leidos is essentially a leveraged bet on federal spending. Budget cuts would devastate results. A government shutdown disrupts operations. Political changes affect spending priorities. Yet this risk might be overstated. Defense spending has grown through Republican and Democratic administrations, through wars and peace, through boom and bust. The U.S. spends more on defense than the next nine countries combined—that's unlikely to change given China's rise and global instability.

The competition from venture-backed defense startups deserves serious consideration. Anduril, Palantir, Shield AI—these companies are attacking traditional contractors with commercial technology and Silicon Valley speed. They're winning some contracts, generating buzz, and attracting top talent. But here's what the headlines miss: most are losing money, burning cash, and discovering that government contracting is harder than it looks. Palantir, the most successful, generates just $2.5 billion in revenue after 20 years—Leidos adds that much revenue every two years through organic growth and acquisitions.

The real competitive threat might come from big tech. Amazon, Microsoft, and Google are increasingly interested in defense work. They have unlimited capital, cutting-edge technology, and growing comfort with government contracts. If they decided to seriously compete in Leidos's markets, it could be problematic. But they face their own challenges—employee resistance to defense work, lack of cleared personnel, and unfamiliarity with government procurement. For now, they seem content to partner with companies like Leidos rather than compete directly.

Margin pressure is a legitimate concern. As contracts get larger and competition intensifies, margins are being squeezed. The days of 15% EBITDA margins on services work are gone. Leidos is responding by mixing in higher-margin technology work, but this transition takes time. The company needs to evolve from labor-intensive services to technology-enabled solutions—easier said than done when you have 47,000 employees and most revenue comes from billing hours.

The regulatory and political risks are real but manageable. Contract protests can delay revenue. Regulatory changes can increase costs. Political pressure on defense spending creates uncertainty. But Leidos has navigated these challenges for decades. Management knows how to work with both parties, maintains relationships across government, and structures contracts to minimize political risk. It's not risk-free, but it's risk-understood.

The bull case ultimately rests on three pillars. First, the secular growth in defense technology spending. As warfare becomes increasingly digital, countries need companies that can integrate complex technologies into military operations. Leidos is perfectly positioned. Second, the barriers to entry are massive and growing. Security clearances, past performance, customer relationships, and infrastructure create moats that protect margins. Third, the M&A opportunity remains significant. The defense industry continues consolidating, and Leidos has proven it can successfully acquire and integrate large businesses.

The bear case is equally straightforward. Customer concentration means a single budget cut could crater results. Technology disruption from startups or big tech could erode competitive position. Margin pressure from competition could compress returns. And execution risk on large contracts or acquisitions could destroy value. These aren't theoretical risks—they're real challenges that management faces daily.

The valuation question is complex. At roughly 12x forward earnings, Leidos trades at a discount to the S&P 500 despite more predictable cash flows. The enterprise value to EBITDA multiple of 11x is reasonable for a services business but cheap for a technology company. If you believe Leidos is successfully transitioning to higher-margin technology work, the stock is undervalued. If you think it remains a commoditized services business, it's fairly priced.

For fundamental investors, Leidos offers an interesting proposition. It's a stable, cash-generative business with dominant market position in a growing industry. It won't double overnight, but it also won't disappear in disruption. In a portfolio context, it provides defense exposure, government stability, and yield—attractive characteristics in uncertain times. The key question isn't whether Leidos is a good company (it clearly is) but whether it's a good stock at current prices. That depends on your view of defense spending, technology evolution, and management's ability to execute.

The investment case ultimately comes down to time horizon and risk tolerance. For long-term investors comfortable with government exposure, Leidos offers predictable returns and limited downside. For growth investors seeking the next multi-bagger, look elsewhere. It's a singles and doubles stock in a market obsessed with home runs—boring, perhaps, but profitable. In investing, as in defense contracting, boring often beats exciting.

XI. Future Outlook & Closing Thoughts

The year is 2030. The U.S. Space Force just awarded Leidos a $25 billion contract to operate its entire constellation of surveillance satellites—managed not from ground stations but from a distributed cloud architecture that didn't exist five years ago. The company's AI systems are processing exabytes of sensor data in real-time, identifying threats before humans even know to look for them. Hypersonic interceptors designed by Leidos engineers protect major cities from weapons that travel at 15 times the speed of sound. Science fiction? Perhaps. But if Leidos's trajectory continues, this future isn't just possible—it's probable.

The macro tailwinds are impossible to ignore. Global defense spending is accelerating after decades of relative decline. China's military modernization is driving the largest peacetime buildup in U.S. defense capability since the Cold War. Russia's invasion of Ukraine reminded Europe that hard power still matters. The Middle East remains unstable. Space is becoming militarized. Cyber warfare is constant. In this environment, demand for Leidos's capabilities—systems integration, technology development, mission support—will only grow.

The Space Force opportunity alone could reshape Leidos. As America's newest military branch builds out its capabilities, it needs everything—satellite control systems, data processing capabilities, cyber defense, and technologies that remain classified. Leidos is uniquely positioned with existing space contracts, cleared personnel who understand the domain, and relationships with both traditional space contractors and new commercial providers. The company's work on NASA programs provides additional credibility. As one executive noted, "Space is where defense was in the 1960s—enormous opportunity for those positioned to capture it."

Joint All-Domain Command and Control (JADC2)—the Pentagon's effort to connect every sensor, shooter, and decision-maker across all military branches—represents another massive opportunity. It's essentially building the military's nervous system from scratch, requiring integration expertise that few companies possess. Leidos is already working on multiple JADC2 components. If the program reaches its potential $50+ billion scale, Leidos could capture billions in integration work that plays to its core strengths.

Zero trust architecture—the cybersecurity framework assuming no user or system should be trusted by default—is becoming mandatory across government. Every agency needs to rebuild its security infrastructure, a multi-year effort requiring both technology and implementation expertise. Leidos's cybersecurity credentials and cleared workforce position it to capture significant share of what could be a $100 billion market over the next decade.

But the future isn't without challenges. The venture-backed defense technology ecosystem is maturing rapidly. Companies like Anduril are moving from demonstrations to production, winning real contracts with real revenue. While they're not existential threats yet, they're forcing traditional contractors to innovate faster. Leidos's response—partnering with some, competing with others, acquiring the best—shows adaptability, but the pressure will intensify.

The talent war represents perhaps the biggest long-term challenge. Leidos needs to attract AI researchers who could make millions at Google, systems engineers who could join SpaceX, and cybersecurity experts courted by every company in America. The mission matters—working on national security has unique appeal—but mission alone isn't enough when competitors offer 10x compensation. Leidos is responding with innovation labs, flexible work arrangements, and equity compensation, but it's fighting an uphill battle.

Geopolitical risks are evolving in unexpected ways. A Taiwan crisis could drive massive defense spending—or trigger economic chaos that constrains budgets. Peace breaking out (unlikely but possible) could slash defense spending. Climate change is creating new security challenges that don't fit traditional defense paradigms. Leidos needs to navigate these uncertainties while making long-term capability investments. It's like playing three-dimensional chess where the rules keep changing.

The technology disruption question looms large. Will quantum computing make current encryption obsolete? Will artificial general intelligence eliminate the need for human analysts? Will commercial space companies make traditional defense contractors irrelevant? These aren't immediate threats, but they're real enough that Leidos is investing in quantum, AI, and commercial partnerships. The company that adapted from nuclear physics consulting to AI-enabled warfare will need to evolve again.

Tom Bell's leadership will be crucial in navigating these challenges. Unlike his predecessors who focused on M&A and integration, Bell faces the challenge of organic innovation in a rapidly changing market. His background running the Defense & Intelligence segment provides credibility with customers, but he'll need to balance operational excellence with strategic vision. Early signs are promising—he's increased R&D spending, accelerated partnerships with commercial tech companies, and pushed decision-making lower in the organization.

The cultural evolution continues to fascinate. Leidos has somehow maintained entrepreneurial energy through multiple mergers, thousands of hiring cycles, and constant change. The company that Bob Beyster founded on employee ownership principles has become a public corporation, yet it retains an owner's mentality. Employees still talk about mission impact rather than stock price. Program managers still take personal responsibility for customer success. It's a culture that can't be replicated overnight—perhaps Leidos's most sustainable competitive advantage.

Looking back at the journey from Beyster's $10,000 investment to today's $20 billion enterprise, several lessons emerge. First, timing matters less than persistence—Leidos survived multiple defense downturns by adapting rather than abandoning its market. Second, culture compounds—the scientific excellence Beyster instilled in 1969 still drives innovation today. Third, strategic courage pays off—the decisions to go public, split the company, and acquire Lockheed's business were all contrarian bets that created enormous value.

But perhaps the most important lesson is about purpose. In an era where many companies struggle to articulate why they exist beyond making money, Leidos has clarity: enabling national security and scientific advancement. That purpose attracts talent, focuses strategy, and provides resilience during challenges. It's why a nuclear physicist's "crazy little company" became indispensable to American defense.

The Leidos story isn't finished. The next chapters will be written by technologies not yet invented, conflicts not yet imagined, and leaders not yet identified. But if history is any guide, Leidos will adapt, evolve, and endure. In the strange economics of defense contracting—where relationships matter more than technology, trust trumps efficiency, and patience beats speed—Leidos has mastered the game.

For investors, Leidos represents a bet on American power projection, technological advancement, and the continuing need for companies that can bridge the gap between scientific possibility and operational reality. It's not a glamorous bet—you won't impress anyone at cocktail parties talking about your government contractor holdings. But in a world growing more dangerous and complex, the boring business of keeping America secure might be the most interesting investment of all.

The physicist's experiment that began in 1969 has become something Bob Beyster probably never imagined—a Fortune 500 company, a technology leader, and a cornerstone of American defense. From Science Applications Incorporated to Leidos, from employee ownership to public markets, from nuclear physics to artificial intelligence, it's been a remarkable journey. And somehow, you get the feeling the best chapters are still being written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube