Cognizant Technology Solutions: From D&B Spinoff to Global IT Services Giant

Origins and Founding Context (1994-1996)

To understand Cognizant, you first have to understand Dun & Bradstreet, or D&B, one of the oldest business information companies in America. Founded in 1841, D&B had spent over a century and a half collecting data on businesses, initially to help merchants assess the creditworthiness of potential trading partners.

By the early 1990s, D&B had evolved into a sprawling conglomerate that included Nielsen Media Research (the TV ratings company), IMS Health (pharmaceutical data), and a host of other information services businesses. It was a classic American conglomerate of the era, diversified to the point of unwieldiness, sitting on vast troves of data but struggling to keep up with the pace of technological change.

Enter Kumar Mahadeva. Born into a prominent Tamil family in Sri Lanka, the Ponnambalam-Coomaraswamy family, Mahadeva had already carved an impressive career across multiple continents and industries. He had worked at the BBC, spent time at McKinsey, and joined AT&T in 1985 to work on the massive restructuring that followed the Bell System divestiture.

From AT&T, he moved to Dun & Bradstreet, where he was eventually tasked with leading the company's expansion into Asia.

It was during his time in Asia that Mahadeva discovered something that would change his life and, ultimately, the trajectory of an entire industry. He visited the software factories that were beginning to spring up across India and immediately recognized the arbitrage opportunity.

Here were highly educated engineers, many trained at the Indian Institutes of Technology and other world-class institutions, who could write software just as well as their American counterparts but at a fraction of the cost. An experienced Indian software professional might earn fifteen thousand dollars a year. The equivalent American professional would cost seventy-five thousand or more. The math was irresistible.

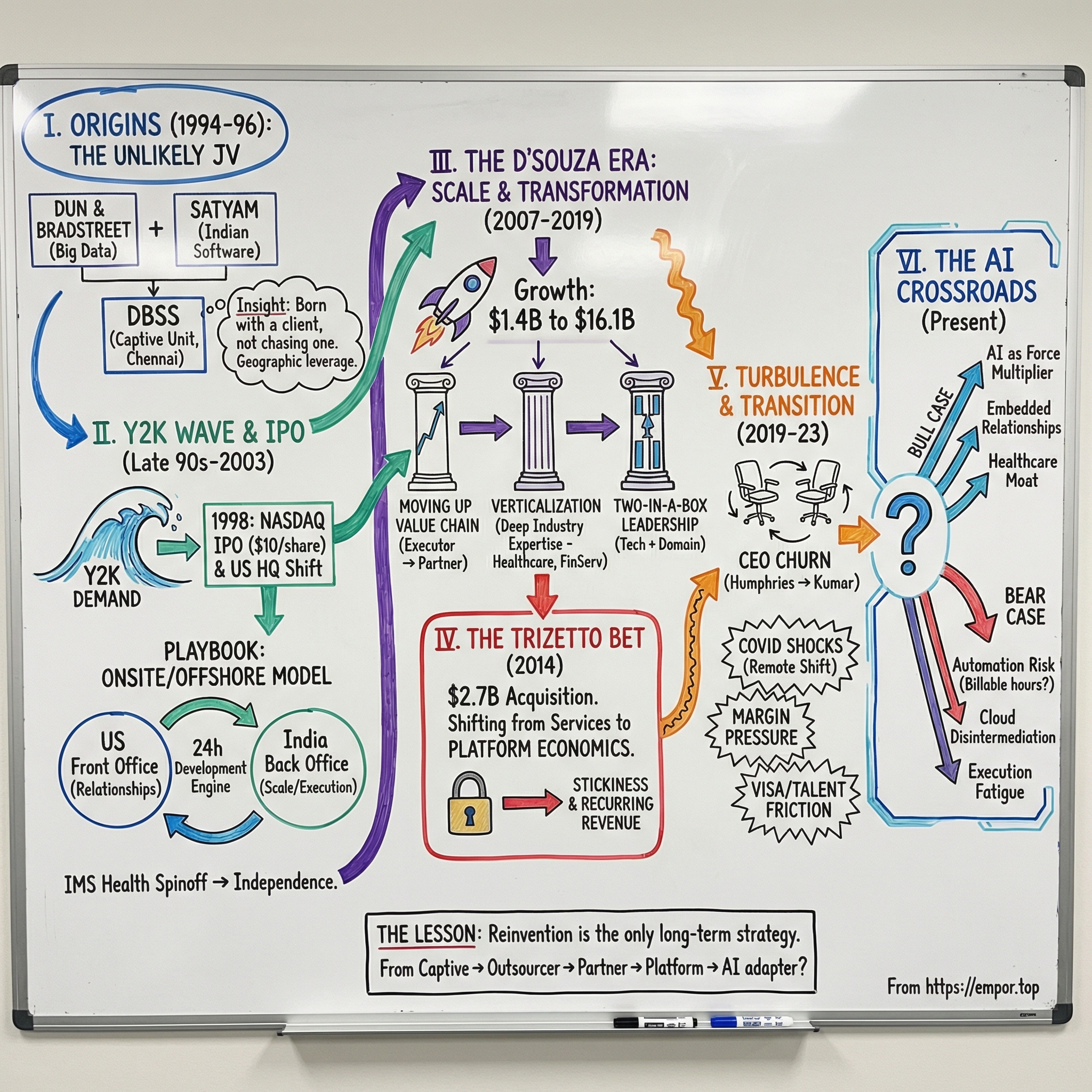

Mahadeva convinced D&B to put up two million dollars for a joint venture with Satyam Computer Services, one of India's emerging IT firms. The partnership was structured as a 76-24 split, with D&B holding the majority stake. They called it Dun & Bradstreet Satyam Software, or DBSS, and set up shop in Chennai in January 1994 with fifty employees.

Mahadeva served as the founding CEO alongside Srini Raju, who came from the Satyam side.

Raju brought his own impressive credentials. Born in 1961 in Khajipalem, a village in Andhra Pradesh's Guntur district, he had earned honors in civil engineering from NIT Kurukshetra before heading to Utah State University for his master's degree. He returned to India to join Satyam Computer Services, which had been founded by his close relative B. Ramalinga Raju, and rose to serve as COO and later CEO of Satyam Enterprise Solutions. While Mahadeva provided the American corporate connections and strategic vision, Raju contributed deep knowledge of Indian software delivery and engineering culture.

The initial mandate was straightforward: DBSS would serve as D&B's internal technology arm, implementing large-scale IT projects for the parent company's various business units. But from the very beginning, Mahadeva had a grander vision. He saw the joint venture not just as a cost center for D&B, but as the kernel of something that could serve external clients as well. The offshore development model, with teams in India working while America slept, creating a twenty-four-hour development cycle, was central to this vision from day one.

India's IT services landscape in the mid-1990s was still in its formative stages. Infosys, founded in 1981, was still a relatively small company with revenues of just a few hundred million dollars. TCS, the Tata Group's technology arm, was larger but not yet the behemoth it would become. Wipro was transitioning from a vegetable oil company into an IT services firm, a corporate metamorphosis that remains one of the more improbable pivots in business history.

The Indian government, under the liberalization reforms initiated by Prime Minister Narasimha Rao and Finance Minister Manmohan Singh in 1991, had begun opening the economy to foreign investment and reducing the bureaucratic barriers that had long constrained Indian businesses. The so-called "License Raj," the complex system of regulations and permits that had strangled Indian enterprise for decades, was finally being dismantled.

The timing was propitious. India was producing hundreds of thousands of engineering graduates each year, English was widely spoken, and the cost of telecommunications was falling rapidly, making it feasible to connect development teams in Chennai or Bangalore with project managers in New York or London. A satellite link that would have cost millions in the 1980s was now affordable, and the internet was beginning to make real-time collaboration across continents practical for the first time.

What made DBSS different from its Indian-born competitors was its corporate DNA. While Infosys and Wipro were building their businesses from the ground up, winning clients one at a time through relentless sales efforts and the slow accumulation of reference accounts, DBSS had a captive parent with deep pockets and a guaranteed flow of work. D&B's various business units needed software built and maintained, and DBSS was the designated provider. This gave the young company stability and credibility that a pure startup would have struggled to achieve. It also provided something equally valuable: exposure to the operational complexities of large American corporations. DBSS engineers were not building generic software. They were building systems that processed business credit data, managed research databases, and handled the information infrastructure of a Fortune 500 company. This experience with enterprise-scale complexity would prove invaluable when the company began pursuing external clients.

But the captive model also created a dependency that would need to be broken if the company was ever to reach its full potential. As long as D&B was the primary client, Cognizant's growth would be constrained by D&B's own technology budget. And the relationship created a perception problem: external clients might view the company as a D&B subsidiary rather than an independent technology partner.

That break came sooner than expected, driven not by Cognizant's ambitions but by D&B's own corporate strategy. By the mid-1990s, D&B had concluded that its conglomerate structure was destroying shareholder value. The market was not giving the company credit for the sum of its parts, a classic conglomerate discount. The solution was disaggregation. In 1996, D&B decided to spin off several of its subsidiaries, including DBSS, Erisco, IMS International, Nielsen Media Research, Pilot Software, and Strategic Technologies, into a new holding company called Cognizant Corporation. The spin-off completed on November 1, 1996.

Then, in July 1997, D&B bought out Satyam's 24 percent stake for just 3.4 million dollars, an amount that would later look comically small given what the company would become. To put this in perspective, Satyam's stake, purchased for 3.4 million dollars, would eventually represent ownership in a company worth tens of billions. It was one of the great missed opportunities in the history of Indian technology. DBSS renamed itself Cognizant Technology Solutions, and the company that would one day cross twenty billion dollars in annual revenue had its name.

But it did not yet have its independence. The newly formed Cognizant Corporation was itself about to be restructured, setting up one more corporate reshuffling before the company we know today could truly emerge.

Early Years and IPO (1996-2003)

In March 1998, Kumar Mahadeva was formally named CEO of Cognizant Technology Solutions, and headquarters were moved from India to the United States. The new headquarters would be in Teaneck, New Jersey, a quiet suburban town just across the Hudson River from Manhattan. The choice was deliberate: close enough to Wall Street and the financial services clients who would become Cognizant's bread and butter, but far less expensive than a Manhattan address.

This decision to establish American headquarters would prove strategically significant for decades to come. Unlike its Indian-origin competitors, which remained headquartered in Bangalore, Mumbai, or Hyderabad, Cognizant would present itself as an American company with deep Indian delivery capabilities. It was a subtle but powerful distinction.

When a Fortune 500 CIO was evaluating whether to entrust critical systems to an offshore provider, the fact that Cognizant was headquartered in the same country, subject to the same regulations, and led by executives who operated in the same corporate culture made a difference. The company was governed by US securities law, filed with the SEC, and could be sued in US courts. These were not trivial considerations for risk-averse corporate buyers.

The timing was fortuitous. The Y2K bug was creating an unprecedented surge in demand for IT services. For those who do not remember the Y2K scare, the problem was deceptively simple: decades of legacy software had been written with two-digit year fields to save memory, meaning that when the calendar rolled from 1999 to 2000, computers might interpret "00" as 1900 rather than 2000. The consequences could range from minor glitches to catastrophic failures in banking systems, air traffic control, power grids, and virtually every computer-dependent industry. Every major corporation needed armies of programmers to review, test, and fix millions of lines of legacy code, much of it written in COBOL and other ancient languages. Indian IT companies were ideally positioned to meet this demand, offering large numbers of skilled engineers at prices that Western companies could not match.

Cognizant dove into Y2K work with enthusiasm, and at its peak, Y2K-related projects accounted for nearly half of the company's revenue. But here is where Mahadeva's strategic acumen showed itself. While many competitors gorged on Y2K work, knowing it would eventually end, Mahadeva began strategically diversifying early. The company bid on and won two landmark external accounts, Northwest Airlines and Aetna, neither of which were D&B affiliates. It also won a Y2K compliance project for the Pacific Exchange and delivered it a full month ahead of the May 1997 deadline, building a reputation for reliability that would pay dividends for years.

By the first quarter of 1999, Cognizant had reduced its Y2K exposure to just 26 percent of revenue, while growing its applications management business to 37 percent. This foresight insulated the company from the post-Y2K cliff that devastated many competitors who had become too dependent on remediation work.

Meanwhile, the corporate reshuffling continued. In 1998, Cognizant's parent, Cognizant Corporation, split into two separate companies: IMS Health, the pharmaceutical data business, and Nielsen Media Research, the TV ratings company. Cognizant Technology Solutions became a public subsidiary of IMS Health.

Then, on June 19, 1998, IMS Health partially spun off Cognizant through an initial public offering on the NASDAQ. The stock opened at ten dollars per share. At that price, the entire company was valued at a few hundred million dollars, a rounding error in the context of the late-1990s technology boom, when companies with no revenue and a vague internet business plan were commanding billion-dollar valuations.

It was a modest debut for a company that would one day be worth tens of billions. But the IPO gave Cognizant the public market currency it needed to attract talent, incentivize employees with stock options, and establish the financial credibility required to win larger contracts.

For investors who bought in at the IPO and held, the returns would be extraordinary. By the time of Cognizant's twentieth anniversary on the NASDAQ in 2018, the market value had increased more than four hundred times from its IPO valuation. A ten-thousand-dollar investment at the IPO would have been worth more than four million dollars two decades later, handily outperforming virtually every technology stock of that era.

The dot-com bust of 2000 and 2001 posed a different kind of test. While many technology companies were decimated, their stock prices cratering and their workforces slashed, Cognizant survived by doing something counterintuitive: it eagerly took on the maintenance and support work that larger, more prestigious IT services firms did not want. Think about what was happening in the market at that moment. The Accentures and IBMs of the world were chasing the next big systems integration project, the next ERP implementation, the next digital strategy engagement. They viewed routine application maintenance as low-margin, unglamorous work beneath their strategic ambitions. Cognizant saw it differently. Every maintenance contract was a foothold inside a major corporation, a relationship that could be expanded once the company had demonstrated reliability. When the glamorous work of building new systems dried up during the downturn, Cognizant was happy to keep existing systems running. This humility, this willingness to do the unglamorous work, built relationships with clients who would later entrust the company with far more strategic projects.

The numbers told the story of a company that was growing rapidly even as the broader market suffered. Revenue climbed from roughly 59 million dollars in 1998 to 89 million in 1999, then 140 million in 2000, 180 million in 2001, and 230 million in 2002. By the end of 2002, Cognizant had no balance sheet debt and more than 100 million dollars in cash, a fortress balance sheet that gave it flexibility while competitors were retrenching. During the twelve months from October 2001 to October 2002, a period when the NASDAQ had lost nearly 80 percent of its value from its 2000 peak and the broader stock market was in freefall, Cognizant's stock price rose 170 percent. It was a staggering divergence, a testament to the fact that the company's business model was fundamentally disconnected from the technology bubble and its aftermath.

The company had built something genuinely valuable: a repeatable, scalable delivery model that could take American corporate IT work, disaggregate it into components, ship the appropriate pieces to India for execution, and deliver results at a fraction of what it would cost to do everything domestically. The onsite-offshore model, as it came to be known, was not unique to Cognizant. But the company had refined it into something approaching an art form, with what it called the "Two-in-a-Box" approach. For every major engagement, Cognizant would place a senior manager onsite with the client, typically in the United States, paired with an equal-level manager in India who oversaw the delivery team. This pairing ensured that client needs were understood at a deep level while work was executed efficiently offshore.

The year 2003 brought two pivotal changes. First, IMS Health sold its entire 56 percent stake in Cognizant through an exchange offer, making Cognizant a fully independent public company for the first time. To protect itself from hostile takeover attempts, the newly independent company instituted a poison pill provision.

Second, Kumar Mahadeva resigned as CEO and was succeeded by Lakshmi Narayanan. The transition was significant not just for the personnel change but for what it said about the company's maturity. Mahadeva's intense, razor-sharp focus had been exactly what Cognizant needed in its startup phase, when every client win mattered and every dollar counted. Narayanan's more collaborative, consensus-building leadership style was better suited to the next phase: scaling a company that was growing by more than 50 percent annually without losing the entrepreneurial culture that had made it special.

Narayanan understood that at Cognizant's stage of growth, the CEO's job was not to win individual deals but to build the organizational machinery that would win thousands of deals simultaneously. He invested in delivery processes, talent development, and the management systems that would allow the company to absorb thousands of new hires every quarter without degrading quality.

From the IPO at ten dollars a share to full corporate independence, Cognizant had navigated one of the most tortuous corporate genealogies in business history. Born from a joint venture, spun off into a holding company, subjected to multiple corporate restructurings, partially floated via IPO as a subsidiary, and finally set free, the company had emerged with its identity intact and its growth trajectory undiminished. Now, under new leadership and with complete independence, it was ready for its next chapter.

The Francisco D'Souza Era: Transformation and Scale (2007-2019)

If Kumar Mahadeva was Cognizant's founding visionary and Lakshmi Narayanan was its stabilizing force, then Francisco D'Souza was the leader who transformed a fast-growing Indian IT services company into a global technology powerhouse. When D'Souza was named CEO in January 2007 at the age of thirty-eight, Cognizant was generating about 1.4 billion dollars in annual revenue and employed roughly 39,000 people. When he stepped down twelve years later, the company had grown nearly tenfold to over 16 billion dollars in revenue and its workforce had swelled to 282,000. It was one of the most remarkable scaling stories in the history of professional services.

D'Souza's background was unconventional, even by the standards of a company with an unconventional origin story. Born in Nairobi, Kenya, to Placido D'Souza, an Indian Foreign Services officer, young Francisco grew up in eleven different countries, attending seven different schools in places as varied as Panama, Zaire, New Delhi, New York, Trinidad, and Hong Kong. This peripatetic childhood gave him an unusual gift: the ability to operate comfortably across cultures, languages, and business environments. He earned his undergraduate degree from the University of East Asia in Macau and later obtained an MBA from Carnegie Mellon University's Tepper School of Business.

D'Souza had joined Dun & Bradstreet as a management associate in 1992, two years before Cognizant even existed. He was involved in the creation of the company from its inception in 1994 and rose steadily through the ranks: director of US operations, vice president of North American operations, senior vice president, chief operating officer, and finally CEO. In other words, he was not a hired gun brought in from outside. He was a Cognizant lifer who understood the company's culture, its client relationships, and its operational DNA at a cellular level.

His strategic priorities were clear from the start. First, D'Souza recognized that Cognizant could not remain primarily a labor arbitrage play. The cost advantage of Indian engineers over American ones was real and significant, but it was also replicable. Every major Indian IT services company had the same basic cost structure. If cost was your only differentiator, then you were in a race to the bottom, and there would always be someone willing to underbid you.

To differentiate, Cognizant needed to move up the value chain, from writing and maintaining code to advising clients on technology strategy, implementing complex transformations, and building proprietary intellectual property. D'Souza wanted Cognizant to be in the room when the CIO made strategic decisions, not just waiting in the hallway to be handed implementation work after the decisions were made.

Second, D'Souza organized the company around deep industry verticals. Rather than being a generalist IT services firm that could do a bit of everything for everyone, Cognizant built specialized practices in banking and financial services, insurance, healthcare, manufacturing, retail, and communications, media, and technology.

Each vertical had its own leadership, its own domain experts, and its own go-to-market strategy. A Cognizant team working with a major health insurer would not just understand Java or Oracle databases. They would understand claims adjudication, provider credentialing, HIPAA compliance, and the specific pain points of running a health plan. This domain depth became a powerful competitive weapon.

Cutting across these verticals were horizontal capability areas: analytics, mobile computing, business process outsourcing, and testing. The matrix structure allowed Cognizant to bring both industry depth and technical breadth to every client engagement.

The financial trajectory under D'Souza was stunning. Revenue grew from 2.1 billion dollars in 2007 to 2.8 billion in 2008. Even the global financial crisis, which devastated the banking and financial services clients that were Cognizant's largest revenue source, only slowed the company to 3.3 billion in 2009, a 16 percent increase in a year when many professional services firms were shrinking. The logic was simple: during a downturn, CIOs face pressure to cut costs, and one of the most effective ways to cut technology costs is to shift work from expensive domestic resources to less expensive offshore ones. Recessions, counterintuitively, were good for the Indian IT services model.

Then came the real acceleration. Revenue exploded to 4.6 billion in 2010, 6.1 billion in 2011, 7.4 billion in 2012, 8.8 billion in 2013, and surpassed the ten-billion-dollar mark in 2014 at 10.3 billion. The growth continued, albeit at a somewhat slower pace, through 12.4 billion in 2015, 13.5 billion in 2016, 14.8 billion in 2017, and 16.1 billion in 2018. In twelve years, D'Souza had grown revenue more than tenfold. The company entered the Fortune 500 in 2011 and would later rise to Fortune 200 status. It had been added to the NASDAQ-100 index in 2004 and joined the S&P 500 in 2014, a remarkable achievement for a company that had been a captive D&B unit just two decades earlier. For eleven consecutive years, Cognizant was named one of Fortune's Most Admired Companies.

D'Souza was also an aggressive acquirer. During his tenure, Cognizant made upwards of forty acquisitions, ranging from small tuck-in deals to bolster specific capabilities to the transformational 2.7 billion dollar purchase of TriZetto in 2014. Early acquisitions were focused on building geographic and domain capabilities: Strategic Vision Consulting in media and entertainment in 2008, Pepperweed Advisors for business consulting in 2009, the C1 Group's six companies in Germany and Switzerland in 2012. Later deals targeted digital capabilities, cloud expertise, and analytics firms as the industry shifted from traditional outsourcing toward digital transformation.

The pivot to digital was perhaps D'Souza's most consequential strategic move. By the mid-2010s, it was becoming clear that the traditional IT outsourcing model, taking over and running clients' existing technology environments at lower cost, was a mature business with limited growth potential. Every major Indian IT company could offer roughly the same value proposition: skilled engineers, offshore delivery, lower costs. The commoditization pressure was relentless. The real growth was in helping clients transform their businesses using cloud computing, artificial intelligence, data analytics, and modern software development practices. This was a fundamentally different kind of work, requiring different skills, different engagement models, and different relationships with clients.

D'Souza invested heavily in building these capabilities, both organically and through acquisition. He hired senior leaders from traditional consulting firms, acquired digital agencies and analytics companies, and began framing Cognizant not as an outsourcing company but as a digital transformation partner. The message to clients was clear: do not come to us just to run your existing systems cheaper. Come to us to reimagine your business for the digital age. It was an ambitious repositioning that required changing not just the company's capabilities but its brand identity in the minds of CIOs who had long thought of Cognizant primarily as a low-cost offshore provider.

But there were also challenges during this era. Growth rates, while impressive in absolute terms, began to decelerate from the torrid pace of the early D'Souza years. Revenue growth slipped from the 30-50 percent range in 2007-2011 to single digits by 2016-2018. This deceleration was partly natural: it is far easier to grow 40 percent when you are a two-billion-dollar company than when you are a fourteen-billion-dollar company. The law of large numbers is unforgiving. But it also reflected increasing competition, pricing pressure, and the difficulty of pivoting a massive workforce of more than 250,000 people trained in traditional IT services toward higher-value digital work. You cannot simply retrain a COBOL maintenance programmer to become a cloud architect overnight. The transformation of the workforce had to be gradual, creating a period of awkward transition where the company was neither fully a traditional outsourcer nor fully a digital transformation firm.

Then came Elliott Management. In February 2016, the activist hedge fund, led by the legendary and feared Paul Singer, disclosed a 1.4-billion-dollar stake in Cognizant and began pushing for changes. Elliott's arrival sent shockwaves through the organization. The fund had a reputation for aggressive tactics and a track record of forcing management changes, operational restructurings, and massive capital returns at target companies.

Elliott's thesis was straightforward: Cognizant was prioritizing revenue growth over profitability, and its margins lagged well behind Indian peers like TCS and Infosys. The fund demanded that Cognizant initiate a dividend, commit to returning 75 percent of annual US free cash flow through share repurchases, and buy back 2.5 billion dollars in stock. The implied message was blunt: stop hoarding cash and start rewarding shareholders.

In February 2017, Cognizant settled with Elliott, agreeing to return 3.4 billion dollars to shareholders over two years, initiating quarterly cash dividends, and adding three new independent directors to the board. Elliott sold its entire stake later that year, having achieved its objectives in remarkably short order.

The Elliott episode was a turning point, and the debate over whether it was ultimately positive or negative for the company continues to this day. On one hand, the company became more disciplined in its capital allocation, and the stock price benefited from the buybacks and dividends. On the other hand, some argued that the pressure to boost margins in the near term came at the expense of long-term investments in digital capabilities, talent, and innovation that could have better positioned the company for the transformation era ahead. The question of whether activist interventions help or hurt companies with long-term technology investment needs is one of the great unresolved debates in corporate governance.

By the time D'Souza announced in February 2019 that he would be stepping down as CEO, Cognizant was a fundamentally different company than the one he had inherited. It was vastly larger, more diversified, and more profitable. But it also faced a more challenging competitive environment, with cloud providers like AWS, Azure, and Google Cloud moving into services territory, and traditional competitors like Accenture investing billions in digital capabilities. The question for D'Souza's successor would be whether Cognizant could maintain its momentum in this new landscape.

The TriZetto Acquisition: Healthcare Dominance (2014)

On a September morning in 2014, Cognizant announced the largest acquisition in its history: the purchase of TriZetto Corporation for 2.7 billion dollars in cash. It was a bold bet, one that would reshape Cognizant's identity and cement its position as the dominant technology player in American healthcare IT. For a company that had grown primarily through organic expansion and small tuck-in acquisitions, this was a declaration of strategic ambition on an entirely different scale.

To understand why this deal mattered, you need to understand both TriZetto and the healthcare market that Cognizant was trying to own.

TriZetto had been founded in 1997 as a healthcare payer software company. For those unfamiliar with the healthcare industry's terminology, a "payer" is the entity that pays for medical services, typically an insurance company or government program. Think of it this way: when you go to a doctor, there is a Byzantine process behind the scenes where your insurance company processes claims, adjudicates benefits, manages provider networks, and handles everything from enrollment to billing. Every time you swipe your insurance card, data flows through a complex chain of systems that determines what is covered, what you owe, and what the provider gets paid.

TriZetto built the software platforms that powered these processes for approximately 350 health plans, with solutions that touched nearly 245,000 healthcare providers covering about 180 million Americans. In other words, TriZetto's software was the plumbing of American healthcare administration, invisible to patients but absolutely essential to the functioning of the system.

The company had gone public before being taken private by Apax Partners in April 2008 for about 1.4 billion dollars. By 2014, Apax was looking for an exit, and Cognizant was looking for a way to transform its healthcare practice from a services business into a platform-plus-services business. The 2.7 billion dollar price tag valued TriZetto at nearly four times its annual revenue of approximately 700 million dollars, a premium that reflected the strategic value of owning the platform layer rather than just providing services around someone else's platform.

The strategic logic was compelling but carried significant execution risk. Healthcare was already Cognizant's largest vertical, representing about 26 percent of total revenue. But the healthcare services business was showing signs of maturation. Growth was decelerating, and clients were increasingly looking for integrated solutions rather than piecing together services from multiple vendors. The problem with a pure services model in healthcare, or any industry, is that you are always one procurement cycle away from being replaced by a cheaper competitor. Owning the platform changes that dynamic entirely. When your software is processing a health plan's claims, managing its provider network, and handling its enrollment, the switching costs become enormous. The client is not just buying labor hours that can be sourced from anyone. They are running their business on your software.

By acquiring TriZetto, Cognizant could offer something no competitor could match: end-to-end healthcare technology solutions that combined proprietary software platforms with implementation services, systems integration, and ongoing management. The combined entity was expected to generate roughly three billion dollars in healthcare revenue and deliver revenue synergies of 1.5 billion dollars over five years. The deal was designed to be immediately accretive to earnings, excluding one-time integration costs. Cognizant financed the acquisition with a combination of its substantial cash reserves and committed debt financing of one billion dollars.

The timing was significant. The Affordable Care Act, signed into law in 2010, was in its implementation phase, and healthcare organizations were spending aggressively on technology to comply with new regulations, modernize their infrastructure, and manage the influx of newly insured patients. The ACA had expanded insurance coverage to millions of previously uninsured Americans, creating a surge in claims volume and administrative complexity that strained legacy systems. Health plans needed to modernize their technology stacks, and TriZetto's platforms were among the most widely deployed in the industry. Healthcare IT spending was growing faster than overall IT spending, and the companies that could help payers and providers navigate this transition were in high demand.

But the deal also carried risks that were less obvious at the time. Integrating a 3,700-person software company into a 190,000-person services company is inherently challenging. The cultures are fundamentally different.

Software companies are product-oriented: they build something once and sell it many times, with engineering teams focused on features, releases, and product roadmaps. Services companies are project-oriented: they sell customized work to individual clients, with teams focused on deliverables, milestones, and client satisfaction. The compensation structures differ, the career paths differ, and even the definition of success differs.

There was also the question of whether Cognizant, which had built its reputation on services execution, had the organizational DNA to operate a software business effectively. Running a product company requires continuous investment in R&D, long-term roadmap planning, and the discipline to say no to client-specific customization requests that would fragment the platform.

The integration produced mixed results over time. On the positive side, TriZetto's platform capabilities gave Cognizant a genuine competitive moat in healthcare payer technology. The company could now walk into a major health plan and offer not just staff augmentation or project work, but an integrated platform that would run core business processes. This made client relationships deeper and stickier, with higher switching costs.

On the negative side, the software business brought complexity. Software products require ongoing investment in research and development, generate revenue through license fees and subscriptions rather than billable hours, and create maintenance obligations that differ fundamentally from services contracts. Some industry observers noted that while Cognizant had purchased a leading platform, it struggled at times to cross-sell effectively between the TriZetto product suite and its broader services business.

The TriZetto acquisition also foreshadowed a challenge that would haunt Cognizant years later. In late 2024, hackers gained unauthorized access to TriZetto Provider Solutions, and the intrusion was not discovered until October 2025, an eleven-month exposure window during which sensitive data including Social Security numbers, financial account information, and home addresses were compromised. As of early 2026, Cognizant faces multiple proposed class-action lawsuits related to the breach. The incident is a reminder that owning platform infrastructure brings not just revenue benefits but also security responsibilities and potential liabilities.

Despite these complications, the TriZetto deal fundamentally altered Cognizant's competitive position. Before the acquisition, Cognizant was one of several Indian IT services companies that happened to have a large healthcare practice. After it, Cognizant was arguably the most important technology company in American healthcare administration, a company that industry observers began comparing to IBM in terms of its healthcare IT footprint. For investors evaluating Cognizant's long-term competitive position, the TriZetto acquisition remains perhaps the single most important strategic decision in the company's history.

Leadership Transitions and Modern Challenges (2019-Present)

The announcement in February 2019 that Francisco D'Souza would step down as CEO and be replaced by Brian Humphries marked the beginning of a turbulent period for Cognizant, one characterized by leadership instability, slowing growth, pandemic disruption, and ultimately, a dramatic boardroom upheaval. After twelve years of D'Souza's leadership, the transition felt like the end of an era.

Humphries, an Irish businessman who had most recently served as CEO of Vodafone Business, officially took over on April 1, 2019. He was the first CEO in Cognizant's history who had not come up through the company's ranks or the broader Indian IT services industry. His appointment signaled the board's desire to bring in a leader with deep European and telecom experience who could diversify Cognizant beyond its traditional North American stronghold and its heavy reliance on financial services and healthcare.

D'Souza transitioned to the role of Executive Vice Chairman before eventually departing. The transition was outwardly amicable, but the selection of an outsider with no IT services background raised eyebrows among Cognizant veterans and industry observers alike.

The early months of the Humphries era were consumed by restructuring and cost optimization rather than the growth-oriented strategy that had characterized D'Souza's tenure. Humphries implemented operational changes designed to improve margins and streamline the organization. But within a year of his appointment, the COVID-19 pandemic struck, throwing every IT services company into chaos.

The pandemic's impact on Cognizant was complex and, in many ways, revealing. On one hand, COVID-19 accelerated many of the digital transformation trends that should have been tailwinds for the business: cloud migration, remote work infrastructure, e-commerce platforms, and healthcare digitization. Every company in the world suddenly needed to digitize operations that had been paper-based or office-dependent. This was precisely the kind of work that Cognizant and its peers were built to do.

On the other hand, the immediate disruption was severe. Cognizant's delivery model depended on large, centralized offices in India where thousands of engineers worked side by side. When lockdowns hit, the company had to scramble to enable remote work for hundreds of thousands of employees, many of whom did not have reliable internet connections or quiet workspaces at home.

Revenue dipped from 16.8 billion dollars in 2019 to 16.7 billion in 2020, a modest decline in absolute terms but a significant underperformance relative to peers who managed to grow through the downturn. Infosys and HCLTech, for example, both posted positive revenue growth in calendar year 2020.

The deeper problem was that Cognizant was losing ground to competitors at an alarming rate. In 2022, the company's revenue growth lagged the peer average by approximately 800 basis points, a gap that was difficult to explain away as a temporary blip. To put that in context, 800 basis points of underperformance in a twenty-billion-dollar business means roughly 1.6 billion dollars of revenue growth that should have happened but did not. Attrition rates soared during the post-pandemic talent war, with experienced engineers leaving for competitors or for the booming startup ecosystem. In the IT services industry, people are the product. When your best people leave, your ability to deliver and your relationships with clients deteriorate. Client satisfaction metrics weakened. Large deal wins declined. The company that had once been the fastest-growing major IT services firm was now the slowest among its peer group.

On January 12, 2023, the board acted. Humphries was terminated without cause. The press release was diplomatically worded, as these things always are, but the message was clear: the board had lost confidence in Humphries' ability to close the growth gap and restore Cognizant's competitive position. Board Chairman Stephen J. Rohleder communicated the decision to employees directly. Humphries received a severance package of 16.5 million dollars.

His replacement was already in position, having been quietly maneuvered onto the stage. Ravi Kumar Singisetti, known professionally as Ravi Kumar S., had been hired just a month earlier, in December 2022, as President of Cognizant Americas. His elevation to CEO in January 2023 happened with a speed that suggested the board had been planning the transition for some time, even as Humphries remained in the role.

Ravi Kumar brought precisely the credentials that Cognizant needed at that moment. He had spent more than two decades at Infosys, Cognizant's most direct competitor, rising to the position of President and serving as a key member of the executive leadership team. He understood the Indian IT services model at a molecular level. He knew how to build large deal pipelines, manage global delivery at scale, and navigate the complex client relationships that drive revenue growth in this industry.

The new CEO moved quickly, with the decisiveness of someone who understood exactly what needed to change and had no time for consensus-building. He restructured the workforce, eliminating roughly 3,500 positions in 2023, primarily among non-billable corporate personnel. Total headcount declined by 7,600 that year, including 4,500 reductions in India.

The cuts were painful, and the optics were difficult. Laying off thousands of employees in your first year as CEO is never a popular move. But Kumar argued that the cuts were necessary to reset the cost structure, eliminate organizational layers that were slowing decision-making, and free up resources to invest in growth areas like AI, cloud, and engineering services. He also moved to flatten the management hierarchy, reducing the number of reporting layers between frontline engineers and the C-suite.

More importantly, Kumar rebuilt the large deal engine. In the IT services industry, large deals are the lifeblood of sustained growth. A large deal, typically defined as a multi-year engagement worth 50 million dollars or more in total contract value, provides years of predictable revenue and often opens the door to additional work within the same client organization. Under Humphries, Cognizant had struggled to win these transformational engagements. The pipeline had dried up, and the company was increasingly dependent on smaller, shorter-duration projects that provided less revenue visibility.

Kumar's experience at Infosys, where he had been responsible for some of the largest deals in that company's history, proved directly applicable. He reorganized the sales function, invested in industry-specific solution development, and personally engaged with the CEOs and CIOs of major clients. The results were tangible. In 2024, Cognizant signed a record 29 large deals. In 2025, it signed 28 more, including five mega deals with total contract values of 500 million dollars or more, and one deal valued at over a billion dollars. The total value of large deal wins grew nearly 50 percent year over year in 2025, a dramatic acceleration.

The acquisition strategy also shifted dramatically. Rather than the scattershot approach of acquiring small digital agencies and consulting firms, Kumar pursued larger, more strategic deals designed to enter entirely new markets or establish category leadership in existing ones.

The acquisition of Belcan in August 2024 for approximately 1.3 billion dollars was a case in point. Belcan brought over 6,500 engineers and technical consultants focused on aerospace, defense, space, marine, and industrial engineering. This was not a technology consulting firm in the traditional sense. These were mechanical engineers, electrical engineers, and systems engineers who designed aircraft components, tested propulsion systems, and solved the kinds of hard physics problems that cannot be offshored to a developer in Bangalore.

With expected annualized revenue of over 800 million dollars, the deal instantly gave Cognizant a leadership position in the fast-growing engineering research and development services market. It also diversified the company's revenue base into defense and aerospace, sectors with multi-year spending tailwinds and high barriers to entry.

In November 2025, Cognizant announced the acquisition of 3Cloud, one of the largest independent Microsoft Azure services providers, to accelerate its AI and cloud transformation capabilities. The deal complemented the earlier acquisition of Thirdera, a ServiceNow specialist, demonstrating Kumar's strategy of acquiring leading partners in specific technology ecosystems rather than trying to build expertise from scratch.

The H-1B visa issue, long a background risk for Indian IT services companies operating in the United States, moved to the foreground during this period. In October 2024, a California federal jury found that Cognizant had engaged in a pattern of intentional discrimination against non-South Asian and non-Indian employees, favoring Indian and South Asian workers, particularly H-1B visa holders, for project staffing while leaving others "benched" and subject to termination. The class includes approximately 2,200 employees terminated between 2013 and October 2022, and the jury determined that punitive damages were warranted. Then, in December 2025, a federal judge ruled that Cognizant's "Visa Readiness" and "Visa Utilization" staffing practices had a discriminatory disparate impact on US workers. The company had routinely applied for excess H-1B visas to build a pipeline of travel-ready workers before actual US job openings existed. Phase two of the litigation, covering individual remedies including back pay and reinstatement, is set to proceed in early 2026. In October 2025, the US Senate Judiciary Committee sent letters to Cognizant questioning its hiring and layoff practices. This litigation represents a material legal overhang that investors should monitor carefully.

The financial results under Kumar tell a story of genuine operational improvement. After flat revenue in 2023, the company grew 2 percent in 2024 and then accelerated to 7 percent growth in 2025, crossing the twenty-billion-dollar revenue mark for the first time at 21.1 billion dollars. Adjusted operating margins expanded from approximately 15.3 percent to 15.8 percent. Adjusted earnings per share grew 11 percent to 5.28 dollars. Free cash flow reached 2.7 billion dollars, representing 120 percent of net income. The revenue growth gap versus peers, which had been negative 800 basis points in 2022, improved to roughly positive 50 basis points in 2024, suggesting that the turnaround is gaining traction.

For 2026, management has guided for revenue of 22.1 to 22.7 billion dollars, representing growth of roughly 5 to 7 percent, with further adjusted operating margin expansion of 10 to 30 basis points. Trailing twelve-month bookings reached 28.4 billion dollars, up 5 percent year over year, with a book-to-bill ratio of 1.4 times, providing reasonable visibility into near-term growth.

Business Model and Competitive Dynamics

To truly understand Cognizant, you need to understand the economics of the Indian IT services business model, because despite its American headquarters, Cognizant runs on fundamentally the same engine as TCS, Infosys, and Wipro. The model is elegantly simple in concept but operationally complex to execute at scale.

Here is how it works. A large American or European corporation, say a major bank or insurance company, decides that it needs to modernize its technology infrastructure, build a new digital platform, or simply keep its existing systems running more efficiently. It issues a request for proposals, often to multiple vendors simultaneously.

Cognizant responds with a team structure that typically involves a relatively small number of senior consultants and project managers stationed onsite with the client, usually in New York, Boston, Chicago, or wherever the client is headquartered. These onsite resources are expensive, billing at rates that can range from 150 to 300 dollars per hour or more, comparable to what a Big Four consulting firm might charge. Their job is to understand the client's business, translate requirements into technical specifications, manage stakeholder relationships, and ensure that the work being done offshore meets expectations.

But here is the key: the majority of the actual work, the coding, testing, data migration, systems integration, and ongoing support, is performed by a much larger team based in India, primarily in cities like Chennai, Bangalore, Hyderabad, and Pune. These offshore resources cost Cognizant a fraction of what the onsite resources cost.

An experienced Indian software professional might earn fifteen to twenty thousand dollars per year, compared to seventy-five thousand or more for a comparable professional in the United States. The margin between what the client pays for the blended onsite-offshore team and what it costs Cognizant to deliver that team is where the profit sits. A typical engagement might have a ratio of one onsite consultant for every three to five offshore engineers, creating a blended cost that is significantly lower than what a purely domestic provider would charge.

Cognizant refined this model with its "Two-in-a-Box" approach, pairing an onsite senior manager who oversees client interaction with an equal-level manager in India who oversees delivery. The model creates a twenty-four-hour work cycle: the onsite team defines requirements during the US business day, the offshore team executes overnight, and the onsite team reviews results the next morning. When it works well, clients get faster turnaround and lower costs than they would from a purely domestic provider.

As of the end of 2025, Cognizant employed approximately 351,600 people, of whom roughly 257,000, or about 73 percent, were based in India. Another 42,000 were in North America, 16,000 in Continental Europe, and 8,500 in the United Kingdom, with the remainder scattered across other locations. This workforce distribution is the engine that powers the entire business model.

Revenue is heavily concentrated in North America, which accounts for approximately 75 percent of the total at 15.8 billion dollars. The United Kingdom contributes about 9 percent, Continental Europe another 10 percent, and the rest of the world roughly 6 percent.

This geographic concentration is both a strength and a vulnerability. It reflects Cognizant's deep client relationships with the largest American corporations, but it also means the company is disproportionately exposed to US economic cycles, US regulatory changes, and US immigration policy. By contrast, TCS derives roughly 50 percent of its revenue from North America and has significantly more diversified geographic exposure, particularly in Europe and Asia.

By industry vertical, Health Sciences is the largest segment at about 30 percent of revenue, followed closely by Financial Services at 29 percent, Products and Resources at 25 percent, and Communications, Media and Technology at 16 percent.

The heavy weighting toward healthcare and financial services, which together account for roughly 60 percent of revenue, gives Cognizant deep domain expertise in these sectors but also creates concentration risk. A regulatory change in US healthcare policy, a major banking downturn, or even a single large client loss in either sector could have outsized effects on revenue.

In 2025, Financial Services grew 7 percent, its fastest pace since 2016, while Health Sciences grew 7 percent and Products and Resources surged nearly 11 percent, boosted by the Belcan acquisition. The laggard was Communications, Media and Technology, which grew only 1 percent, reflecting softness in the telecom sector and reduced spending by media companies undergoing their own digital disruption.

The competitive landscape is both crowded and hierarchical. At the top sits Accenture, the Dublin-headquartered global consulting and technology services firm, with roughly 65 billion dollars in annual revenue, more than three times Cognizant's size. Accenture is in a class by itself, combining traditional management consulting with technology implementation at a scale that no other firm can match. It competes with Cognizant but also occupies a somewhat different strategic position, with more consulting and advisory work and higher billing rates.

Below Accenture, TCS, the Tata Group's technology subsidiary, generates around 30 billion dollars in revenue and is the most profitable major IT services company, with operating margins consistently in the 24 to 25 percent range. TCS's margin superiority stems from its Indian headquarters, its massive scale, and its rigorous focus on operational efficiency.

Infosys, at roughly 19 billion dollars, is Cognizant's closest competitor in size and often competes head-to-head for the same deals. The two companies share a similar client base and service portfolio, making every large deal a direct competitive battle. HCLTech at 14 billion dollars and Wipro at 11 billion dollars round out the top tier. Cognizant has publicly stated its ambition to break into the top four IT services companies globally by 2027, a goal that would require sustained growth outperformance versus peers.

Cognizant's operating margins, at around 15.8 percent adjusted, are notably below those of TCS and Infosys. This margin gap has been a persistent concern for investors and was a central element of the Elliott Management activism. There are structural reasons for the gap. Cognizant's US headquarters creates higher corporate overhead costs, including executive compensation, real estate, and regulatory compliance expenses that are lower for companies headquartered in India. Its larger onsite workforce ratio relative to peers is inherently more expensive, since onsite employees are paid at local market rates. And its investment in moving up the value chain toward consulting and digital services carries higher costs than traditional outsourcing work, requiring more experienced and therefore more expensive talent.

To illustrate the magnitude of this gap: TCS consistently operates at 24 to 25 percent margins, roughly 900 basis points above Cognizant. On a revenue base of 21 billion dollars, that margin difference translates to roughly 1.9 billion dollars in operating income that TCS would generate but Cognizant does not. Even Infosys, at approximately 20 to 21 percent margins, generates significantly more profit per dollar of revenue. Management has set a target of expanding margins by 10 to 30 basis points annually, a pace that would take decades to close the gap entirely. Whether Cognizant can accelerate this trajectory without sacrificing growth investments remains an open question.

What differentiates Cognizant from its Indian peers? Three things stand out. First, its US headquarters gives it a cultural proximity to American clients that its competitors must work harder to achieve. When an American CIO calls a meeting, Cognizant's senior leadership is in the same time zone, speaks the same corporate language, and can be onsite within hours. This matters more than many investors realize. Technology services relationships are built on trust, and trust is built through proximity and shared context. Second, its deep domain expertise in healthcare, anchored by the TriZetto platform, creates a competitive moat that is difficult to replicate. No amount of engineering talent can quickly substitute for a platform that processes claims for hundreds of health plans. Third, its recent push into engineering services through the Belcan acquisition positions it in the high-growth aerospace and defense market where Indian IT services firms have historically been underrepresented, partly due to security clearance requirements that favor US-based workforces.

The shift from staff augmentation to transformation partner is the central strategic tension in the IT services industry today. In the old model, IT services companies essentially rented out engineers by the hour. The client said "I need twenty Java developers for twelve months," and the IT services company supplied them. The value proposition was simple: our developers cost less than yours. In the new model, clients are not buying bodies. They are buying outcomes. "Help me migrate my entire infrastructure to the cloud." "Build me an AI-powered customer service platform." "Transform my supply chain operations." This shift demands different skills, different pricing models, and different client relationships. It also demands different kinds of people. You cannot win a digital transformation engagement with an army of junior developers. You need architects, strategists, data scientists, and industry experts who can credibly advise a Fortune 500 C-suite.

Cognizant has invested heavily in making this transition, but it remains a work in progress, as it does for every company in the sector. The company has described its approach as the "Hollywood model," where rather than maintaining permanent teams, it assembles project-specific teams of specialists, much like a film production brings together directors, actors, cinematographers, and editors for a specific movie. Whether this metaphor becomes operational reality will be one of the defining challenges of the next several years.

Playbook: Business and Investing Lessons

Cognizant's three-decade journey from a two-million-dollar joint venture to a twenty-one-billion-dollar global technology company offers several instructive lessons for business builders and investors alike.

The first and perhaps most important lesson is about timing markets. Cognizant was born at exactly the right moment in India's economic liberalization, grew up during the Y2K boom that created explosive demand for Indian IT services, matured during the offshoring wave of the 2000s, and pivoted during the digital transformation era of the 2010s.

At each inflection point, the company positioned itself to ride the wave rather than fight it. This is not to say that timing alone was sufficient. Dozens of other Indian IT companies had the same timing advantages and failed to build anything of comparable scale. Timing creates the opportunity; execution determines who captures it.

The Y2K example is particularly instructive. Many IT services companies gorged on Y2K work, knowing it was temporary, and then suffered when it ended. Cognizant's leadership had the discipline to start diversifying away from Y2K work well before the wave crested, building a sustainable applications management business that provided the foundation for the next decade of growth. The lesson is not just about being in the right place at the right time. It is about having the foresight to prepare for what comes after the wave breaks.

The second lesson is about the power of corporate spinoffs. Cognizant's convoluted birth, from a D&B joint venture to a subsidiary of Cognizant Corporation to a subsidiary of IMS Health to a standalone public company, might seem like corporate complexity for its own sake.

But at each stage, the separation gave Cognizant more freedom to pursue its own strategy, attract its own talent, and build its own client relationships. Under D&B and IMS Health, Cognizant's budget was controlled by a parent with different priorities. Its best employees could not receive equity compensation tied to the subsidiary's performance. And its strategic decisions were subject to approval by executives whose primary focus was elsewhere.

The final separation from IMS Health in 2003, which gave Cognizant complete independence, unleashed a growth trajectory that would have been impossible under a parent company focused on pharmaceutical data. The lesson for investors: pay attention to spinoffs. Freed subsidiaries often dramatically outperform their former parents, precisely because independence unlocks latent energy that was suppressed by the conglomerate structure.

The third lesson involves managing founder transitions, a challenge that trips up many companies. Cognizant navigated three CEO transitions in its first two decades, from Mahadeva to Narayanan to D'Souza, each one smooth and each matched to the company's evolving needs.

Mahadeva was the visionary founder who saw the opportunity and built the initial business. Narayanan was the steady hand who scaled the company without losing its culture. D'Souza was the strategic thinker who transformed it from an outsourcing company into a digital services firm. Each leader was right for their moment, and each had the self-awareness to know when it was time to pass the baton.

The Humphries interlude demonstrated what happens when this pattern breaks: a CEO mismatched with the company's culture and competitive needs can quickly erode years of progress. The lesson is not that outside hires are always wrong, but that leadership fit matters enormously in professional services companies where client relationships and institutional knowledge are the primary assets.

The fourth lesson is about building trust with Fortune 500 clients as a company from an emerging market. In the 1990s and early 2000s, many American CIOs were reluctant to entrust critical systems to Indian IT companies. There were legitimate concerns about intellectual property protection, communication challenges across time zones, and the quality of work produced by engineers they had never met in offices they had never visited. Cognizant's decision to headquarter in the United States, combined with its Two-in-a-Box delivery model that kept senior relationship managers close to clients, helped overcome this resistance. The company invested heavily in understanding clients' industries, not just their technology needs, building domain expertise that made it a trusted partner rather than just a low-cost vendor. Over time, Cognizant's client retention rates became among the highest in the industry, with many of its largest relationships spanning more than a decade. In the services business, client relationships compound like interest. A ten-year client that trusts you with small projects eventually trusts you with their largest, most strategic initiatives.

The fifth lesson concerns capital allocation, a topic that does not get enough attention in discussions of IT services companies. For most of its history, Cognizant reinvested virtually all of its profits into growth, maintaining zero debt and accumulating cash. This approach worked brilliantly during the high-growth years but became less optimal as growth decelerated and the company's cash pile grew.

The Elliott Management activism forced a shift toward returning capital to shareholders through dividends and buybacks, a transition that most maturing growth companies must eventually make. The key insight is that different stages of a company's life require different capital allocation strategies. What works for a startup does not work for a mature company, and leaders who cannot make this transition eventually face pressure from shareholders who will make it for them.

The subsequent acquisition-driven strategy under Ravi Kumar represents yet another evolution, deploying capital for strategic M&A to enter new markets and build new capabilities. The Belcan and 3Cloud acquisitions suggest that Kumar views capital allocation as an offensive weapon, not just a defensive obligation.

Finally, the Cognizant story illustrates both the power and the limitations of the labor arbitrage model. For two decades, the cost advantage of Indian engineers was the foundation of Cognizant's value proposition. But as India's economy has developed, wage inflation has gradually eroded this advantage. An Indian software engineer who earned fifteen thousand dollars in 2000 might earn forty or fifty thousand today, narrowing the gap with Western counterparts.

Meanwhile, automation and artificial intelligence are beginning to reduce the need for large teams of engineers doing routine coding and testing work. The IT services companies that will thrive in the next decade are those that can successfully transition from selling labor hours to selling outcomes, platforms, and intellectual property.

Cognizant's investments in generative AI, with a billion-dollar commitment announced in 2024, approximately 500 projects in production, and an AI research lab in San Francisco with 75 issued and pending patents, represent its bet on this future. The company that started as a fifty-person captive unit doing code maintenance must now reinvent itself once again, this time as an AI-powered transformation partner. The stakes have never been higher.

Analysis: Bear vs. Bull Case

The bull case for Cognizant rests on several structural advantages that are often underappreciated by the market.

The company operates in a market, global IT services, that is large and growing, driven by the ongoing digitization of enterprise operations and the adoption of cloud, data, and AI technologies. This is not a cyclical market that will peak and decline. Every year, more business processes become digital, more data is generated, and more systems need to be built, integrated, and maintained. The global IT services market is estimated at well over a trillion dollars, and Cognizant's share, while significant, still leaves enormous room for growth.

Cognizant's client base is dominated by Fortune 500 companies with deeply embedded technology relationships that create high switching costs. Once a company like Cognizant is running your core healthcare claims processing system or managing your banking infrastructure, the cost and risk of switching providers is enormous. Migrations fail. Data gets corrupted. Systems go down. The institutional knowledge that Cognizant's teams accumulate about a client's specific technology environment is virtually impossible to transfer to a competitor. This creates a form of customer captivity that provides revenue visibility and stability.

The healthcare IT business, anchored by TriZetto, provides a genuine competitive moat. No other major IT services company owns and operates the software platforms that process healthcare claims for hundreds of health plans covering tens of millions of Americans. This is not just a services relationship that can be competed away on price. It is a platform position that generates recurring revenue and creates cross-selling opportunities for higher-value consulting and transformation work.

The Belcan acquisition opens a new growth vector in engineering research and development services, a market where Cognizant had limited presence and where the aerospace and defense spending cycle is favorable. The combination of Belcan's engineering expertise with Cognizant's scale and offshore delivery capabilities could create a differentiated offering that neither pure-play engineering firms nor generalist IT services companies can easily replicate.

Under Ravi Kumar, the turnaround is showing real results. The revenue growth gap versus peers has closed, margins are expanding, bookings are at record levels, and the company is generating strong free cash flow. The stock, trading near the bottom of its fifty-two-week range at roughly 65 dollars with a market capitalization of about 31 billion dollars, is priced at a significant discount to the company's trailing twelve-month bookings of 28.4 billion dollars, suggesting that the market is not yet giving full credit for the operational improvement.

Now for the bear case. The most existential risk for Cognizant and the entire Indian IT services industry is generative AI. These companies have built massive businesses by deploying hundreds of thousands of engineers to write, test, and maintain code. Their revenue is fundamentally a function of the number of people they deploy multiplied by the rate they charge per person.

If AI can automate a significant portion of this work, and the evidence increasingly suggests that it can, then the fundamental unit economics of the labor arbitrage model may be undermined. Think about it this way: if an AI coding assistant can make a single engineer twice as productive, then clients need half as many engineers. Cognizant itself has acknowledged that its AI initiatives have automated roughly 12,000 roles internally. That is not a hypothetical future scenario. That is happening right now.

The question is whether the company can redeploy these resources into higher-value work faster than the efficiency gains eat into revenue. History offers some comfort: when ATMs were introduced, many predicted the end of bank branches and bank tellers. Instead, ATMs lowered the cost of running a branch, leading banks to open more branches and hire more people in advisory roles. A similar dynamic could play out in IT services, where AI handles routine coding while humans focus on architecture, strategy, and client relationships. But there is no guarantee that history will repeat.

Margin pressure is another concern. Even after the recent improvement, Cognizant's adjusted operating margin of 15.8 percent trails TCS by nearly 900 basis points and Infosys by roughly 400 to 500 basis points. Some of this gap is structural, but it also reflects less efficient operations and higher overhead. Closing this gap while simultaneously investing in AI and new capabilities is a delicate balancing act.

The H-1B visa litigation represents a material legal and regulatory risk. The finding of intentional discrimination and disparate impact, if upheld through appeals, could result in significant financial liabilities and force changes to Cognizant's staffing practices that increase costs. More broadly, any tightening of US immigration policy that restricts the ability of Indian IT services companies to deploy workers in the United States would be disproportionately damaging to Cognizant given its heavy revenue concentration in North America.

CEO turnover is a legitimate concern. Four CEOs in eight years, counting D'Souza through Ravi Kumar, creates organizational whiplash. While Kumar appears to be the right leader for this moment, the frequency of leadership changes raises questions about board governance and strategic continuity.

Through the lens of Porter's Five Forces, the competitive dynamics are mixed but instructive.

The threat of new entrants is moderate. Building an IT services business of Cognizant's scale requires massive investment in delivery capabilities, client relationships, and domain expertise, creating significant barriers. You cannot simply hang out a shingle and start competing for billion-dollar outsourcing contracts. But cloud hyperscalers like AWS, Azure, and Google Cloud are moving up the stack into professional services territory, and they bring capabilities, including proprietary AI tools and platform lock-in, that traditional IT services companies cannot easily match. This is perhaps the most underappreciated competitive threat. When Microsoft or Amazon can bundle consulting services with their cloud platforms, and offer AI tools that are deeply integrated with their infrastructure, the traditional IT services intermediary is at risk of being disintermediated.

The bargaining power of suppliers is relatively low in this industry. Cognizant's primary input is talent, and while skilled engineers are in demand, the supply of technical graduates in India remains enormous. The bigger supplier risk is actually the US government, which controls the H-1B visa supply that Cognizant and its peers depend on to staff onsite teams.

The bargaining power of clients is high and increasing. Large enterprises are sophisticated buyers of IT services, often employing dedicated vendor management teams and running competitive procurement processes. The shift toward outcome-based pricing, where clients pay for results rather than hours, transfers risk from the buyer to the provider and can compress margins.

The threat of substitutes is growing, primarily from AI and automation tools that can perform some of the routine work currently done by human engineers. Low-code and no-code platforms also enable business users to build simple applications without engaging IT services firms at all.

Rivalry among existing competitors is intense. Accenture, TCS, Infosys, Wipro, HCLTech, and Capgemini all compete for the same clients with similar capabilities, creating pricing pressure. Differentiation increasingly comes from domain expertise, proprietary platforms, and the ability to deliver AI-powered transformation, areas where Cognizant's investments in TriZetto, Belcan, and generative AI may provide an edge.

Applying Hamilton Helmer's 7 Powers framework, Cognizant's strongest power is arguably switching costs. Once embedded in a client's critical systems, running their healthcare claims processing or managing their banking infrastructure, the cost of migration to a competitor is prohibitive for all but the most dissatisfied clients. The migration risk alone, the chance that something breaks during the transition, is enough to keep most clients in place.

The company has some scale economies from its massive offshore workforce, though these are shared with Indian-headquartered competitors who have even larger scale. TCS, with over 600,000 employees, has meaningfully greater scale than Cognizant.

The TriZetto platform creates a form of cornered resource in healthcare IT, a proprietary asset that competitors cannot easily replicate. No other IT services company owns the software platforms that process claims for hundreds of health plans.

What Cognizant largely lacks is counter-positioning: the company's model is well understood and can be replicated by well-funded competitors. There is no structural reason why an Accenture or an Infosys could not build similar capabilities given sufficient time and investment. The moat, such as it is, comes primarily from the accumulation of client relationships, domain expertise, and platform assets rather than from any single defensible advantage.

For investors tracking Cognizant's ongoing performance, two metrics matter most.

First, the revenue growth gap versus peers. This single metric captures whether Cognizant is gaining or losing market share and serves as a barometer for the effectiveness of the company's strategy and execution. The improvement from negative 800 basis points in 2022 to roughly flat in 2024 was the clearest signal that the turnaround was working. Any reversal of this trend would be a warning sign. This metric is particularly important because absolute revenue growth can be misleading in an industry where all players benefit from secular digitization trends. What matters is whether Cognizant is growing faster or slower than its peer group.

Second, trailing twelve-month bookings growth and book-to-bill ratio. Bookings are a leading indicator of future revenue, and the book-to-bill ratio indicates whether demand is accelerating or decelerating. A book-to-bill ratio above one means the company is signing more new business than it is recognizing as revenue, suggesting the pipeline is expanding. In 2025, trailing twelve-month bookings of 28.4 billion dollars at a 1.4 times book-to-bill ratio suggested healthy demand momentum heading into 2026. If this ratio drops below one for consecutive quarters, it would signal that growth is at risk.

Epilogue: If We Were CEOs

The most consequential question facing Cognizant's leadership today is not whether generative AI represents a threat or an opportunity. It is both. The real question is how quickly the company can pivot from selling human labor to selling AI-augmented solutions, and whether it can do so without destroying its existing revenue base in the process.

Consider the dilemma. Cognizant employs over 350,000 people, the vast majority of whom are engineers and technologists who write, test, and maintain software. If generative AI can automate 20, 30, or 40 percent of the routine work these engineers do, then the company's revenue per employee should rise, but total headcount needs may fall, and clients may begin demanding price reductions that reflect the efficiency gains.

The companies that navigate this transition most skillfully will be those that redeploy freed-up capacity into higher-value work: AI strategy consulting, complex systems architecture, and proprietary AI solution development. The winners in this transition will be the companies that figure out how to charge for outcomes rather than hours, so that when AI makes their teams more productive, they capture the value rather than passing it all through to clients as lower prices.

Cognizant's billion-dollar investment in generative AI, its San Francisco AI research lab, and its Neuro AI Multi-Agent Accelerator platform suggest that management understands this imperative. The company claims approximately 500 AI projects in production and holds 75 issued and pending patents. Whether this positions Cognizant as a leader or merely a fast follower in enterprise AI remains to be seen.

Geographic diversification is another strategic priority. With 75 percent of revenue from North America, Cognizant is overly dependent on a single market. Europe, which accounts for roughly 19 percent combined between the UK and the continent, represents a significant growth opportunity, particularly as European enterprises accelerate their own digital transformation journeys. The Asia-Pacific region, including Japan, Australia, and Southeast Asia, is even more underpenetrated, and the rapid digitization of Asian economies could provide decades of growth runway.

The platform versus services debate will also shape Cognizant's future. The TriZetto acquisition demonstrated that owning platforms creates stickier client relationships and higher margins than pure services. The question is whether Cognizant should pursue additional platform acquisitions in other verticals, such as financial services or manufacturing, or whether it should focus on building AI-native platforms internally. Given the pace of change in AI, where today's cutting-edge model is tomorrow's commodity, there is a strong argument for building rather than buying.

Perhaps the most surprising element of the Cognizant story is how a company born as a captive technology unit inside a nineteenth-century data company managed to survive multiple corporate restructurings, navigate the Y2K boom and bust, build a twenty-one-billion-dollar business, and position itself at the forefront of the AI era.

The journey from DBSS in Chennai to CTSH on the NASDAQ is a testament to the power of the Indian IT services model, the importance of strategic timing, and the enduring value of institutional knowledge and client relationships built over decades. It is also a reminder that great companies are not born. They are forged through crisis, competition, and the relentless pursuit of relevance in a world that never stops changing.