Rollins Inc.: The First LBO That Built a Pest Control Empire

I. Introduction & Episode Roadmap

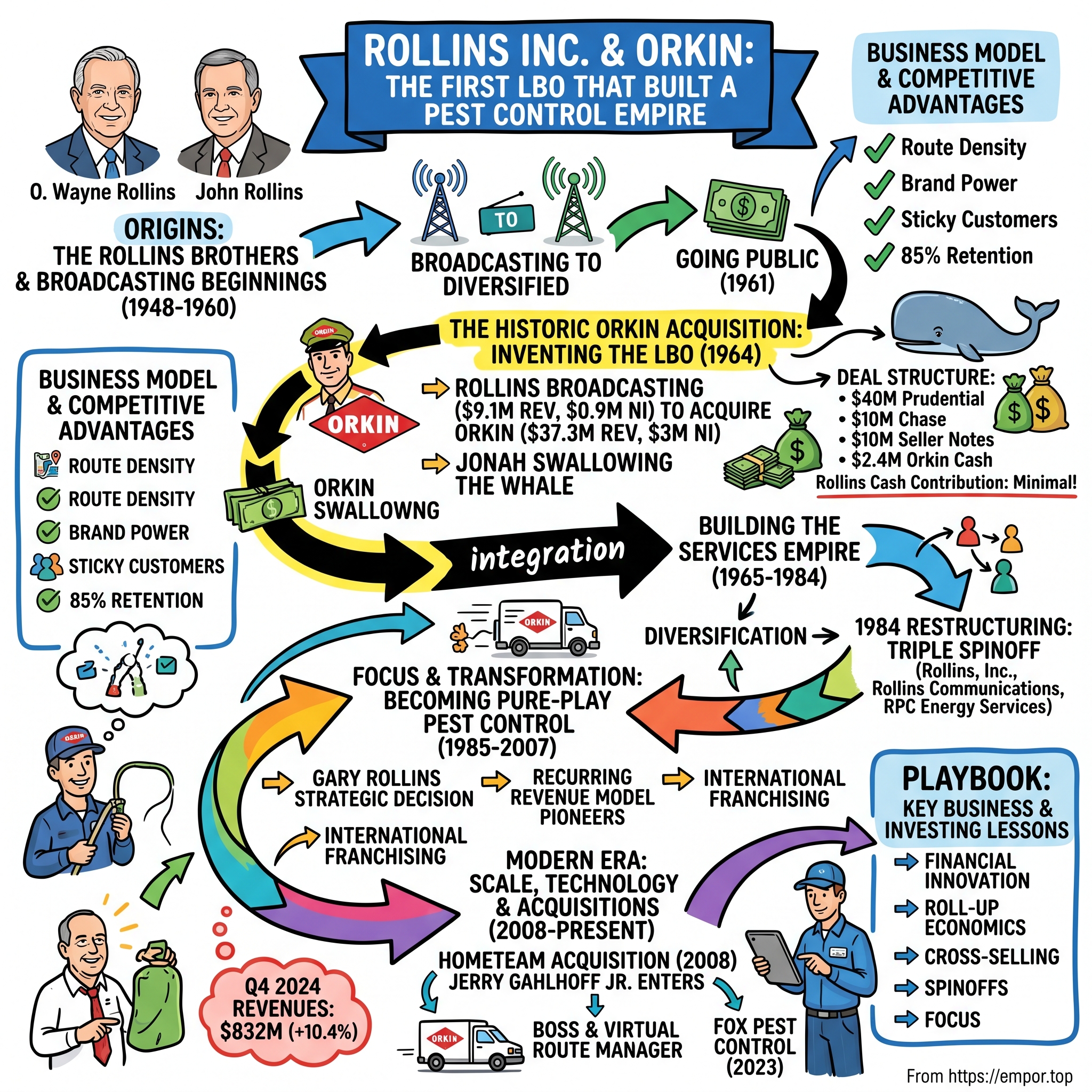

Picture this: A small radio broadcasting company worth $9 million orchestrating a $62.4 million acquisition of the nation's leading pest control business—using virtually none of its own money. It sounds impossible, yet in 1964, this exact scenario unfolded to become the first leveraged buyout in American business history. The architect? Wayne Rollins, a Depression-era farm boy turned media entrepreneur who would transform a hodgepodge of radio stations into what is today a $3.38 billion revenue company, Rollins Inc.

Today, Rollins stands as the undisputed king of pest control, with its crown jewel Orkin serving more than 2.8 million customers in North America, South America, Europe, Asia, Africa, and Australia, with more than 20,000 employees from more than 800 locations. The company posted revenues of $832 million in Q4 2024, an increase of 10.4% over the prior year with organic revenues increasing 8.5%, demonstrating the enduring power of its subscription-based business model.

But this isn't just a story about financial engineering or corporate conquest. It's about two brothers from rural Georgia who parlayed a single radio station into a business empire spanning broadcasting, pest control, and energy services. It's about family dynasties maintaining control while navigating public markets. And perhaps most remarkably, it's about how a deal structure invented out of necessity in 1964 would become the template for thousands of private equity transactions that followed.

The genius of Rollins lies not in any single breakthrough but in its methodical execution across decades: building dense route networks, perfecting the recurring revenue model before SaaS was even a concept, and executing hundreds of tuck-in acquisitions with surgical precision. As we'll see, the company that invented the LBO also pioneered the modern roll-up strategy in pest control, turning a fragmented industry of mom-and-pop exterminators into a professionally managed, technology-enabled services powerhouse.

II. Origins: The Rollins Brothers & Broadcasting Beginnings (1948-1960)

The story begins not in corporate boardrooms but in the red clay hills of Ringgold, Georgia, where O. Wayne Rollins and his younger brother John grew up during the depths of the Great Depression. John Rollins moved to Delaware, where he had a car dealership. Wayne Rollins joined his brother in Delaware, and in 1948 they purchased the radio station WRAD in Radford, Virginia.

The brothers' partnership was elegantly simple: John needed cheap advertising for his auto dealerships, and Wayne saw an opportunity in the emerging medium of radio. He started a radio station to provide cheaper advertising for his brother's Virginia automobile dealership. Rollins Broadcasting was formed in 1948, and grew to control ten radio and four television stations.

What set the Rollins brothers apart wasn't just their appetite for growth but their sophistication in understanding cross-marketing opportunities. While other broadcasters focused solely on selling airtime, the Rollins saw their stations as platforms for promoting their other ventures—a philosophy that would later prove crucial when they entered the pest control business.

By 1956, sensing television's disruptive potential, Rollins Broadcasting expanded into the television industry, becoming one of the first companies to create programming targeted at specific community markets. This wasn't spray-and-pray broadcasting; it was precision marketing before the term existed.

The transformation from regional broadcaster to diversified conglomerate accelerated in 1961 when Wayne Rollins took the company public on the American Stock Exchange. This move gave them currency for acquisitions and set the stage for what would become their defining transaction. By this point, they had also begun experimenting with adjacent businesses—outdoor advertising through the acquisition of Tribble Advertising Company of Texas, citrus groves in Florida, even a cosmetics company called Satin Soft.

To outsiders, this looked like unfocused empire-building. But Wayne Rollins was following a specific logic: he was assembling businesses that could benefit from shared marketing expertise and customer relationships. Every acquisition was a test of his theory that operational excellence in one domain could transfer to another. Some experiments failed—the cosmetics venture quickly fizzled—but each taught valuable lessons about what made a good services business.

By 1964, Rollins Broadcasting had grown to ten radio and four television stations with $9.1 million in annual revenue and $900,000 in annual net income. Respectable numbers for a regional broadcaster, but nothing that suggested the company was about to pull off one of the most audacious acquisitions in business history.

III. The Historic Orkin Acquisition: Inventing the LBO (1964)

The pest control industry in 1964 was dominated by one name: Orkin. Founded in 1901 by 14-year-old Otto Orkin, a Latvian immigrant who started by selling homemade rat poison door-to-door, the company had grown into a nationwide operation. Otto, who branded himself as "Otto the Rat Man", had built the business through a combination of shrewd marketing (he was among the first to advertise pest control on television) and genuine innovation in pest management techniques.

But by 1964, the Orkin family was in chaos. The family-run Atlanta-based pest control business was beset with squabbles that at one juncture led family members to commit the company founder, who was known as "Otto the Rat Man," to a mental institution. The dysfunction created an opportunity, but the asking price seemed impossible: $62.4 million.

Consider the audacity of what Wayne Rollins proposed: His company, worth roughly $9 million, would acquire Orkin, which had $37.3 million in annual revenue and $3 million in annual net income. BusinessWeek would later call it "Jonah swallowing the whale".

The deal structure Wayne Rollins engineered was unprecedented. The total purchase price broke down as follows: $40 million from Prudential Insurance, $10 million from Chase Manhattan Bank, $10 million in seller notes from the Orkin family (with payments deferred for four years), and $2.4 million of Orkin's own excess cash. Rollins Broadcasting's actual cash contribution? Essentially nothing—they pledged $10 million of their own assets as collateral but put up virtually no equity.

Rollins Broadcasting's purchase of Orkin was considered the first major LBO in American business history, and by all historic accounts, Wayne Rollins and Henry Tippie were the architects. Henry Tippie, Rollins' financial advisor and a pioneer in his own right, later reflected: "[It] sort of seems like the mouse swallowing the lion".

What made institutions like Prudential and Chase willing to back such an audacious deal? Wayne Rollins had cultivated relationships with the Du Pont family and other East Coast establishment figures through his Delaware connections. But relationships alone didn't close the deal. The buyout served as a case study at the Harvard Business School, representing the first time that large institutional investors backed a smaller firm buying a larger company and lent money on the basis of potential earnings rather than on the base value of Orkin.

The immediate market reaction validated Rollins' thesis: within seven months of closing on the Orkin deal, shares in Rollins Broadcasting would go from $50 a share to $153. Investors recognized what Rollins had seen—Orkin was dramatically undervalued and underutilized. Under professional management and with access to capital, it could become the platform for rolling up the fragmented pest control industry.

The integration was swift and strategic. Randall was named the head of Orkin while he continued to work on expanding Rollins Broadcasting. The brothers divided responsibilities: Randall focused on operations while Wayne handled strategy and capital allocation. This division of labor would define the company's management structure for decades.

IV. Building the Services Empire (1965-1984)

With Orkin as its foundation, Rollins embarked on an acquisition spree that would transform it from a broadcasting company that happened to own a pest control business into a diversified services conglomerate. The strategy was deceptively simple: acquire family-owned service businesses in the South, professionalize their operations, and cross-sell between divisions.

In 1967 the Rollins home office moved from Delaware to the Orkin headquarters in Atlanta, signaling that pest control, not broadcasting, was now the company's center of gravity. The company's stock began trading on the New York Stock Exchange (NYSE) the following year, providing both prestige and liquidity for further expansion.

The 1970s saw Rollins push into adjacent services. They acquired lawn care companies, building maintenance firms, and security services providers. Each acquisition followed the Orkin playbook: identify a fragmented industry dominated by small operators, acquire the best regional players, standardize operations, and leverage Rollins' scale for purchasing and marketing.

Leadership transitions began early in this period. R. Randall Rollins, the son of Wayne Rollins, succeeded his father as president in 1975 while the company cofounder remained as chair and CEO. This wasn't mere nepotism—Randall had been groomed for leadership since joining the company, working his way through various divisions to understand every aspect of the business.

The brothers—Randall and his younger sibling Gary—brought complementary skills. Randall, nicknamed "Triple R," focused on operations and acquisitions. Gary, who started as an Orkin technician to learn the business from the ground up, became the marketing visionary. Together, they modernized Orkin's brand, creating the iconic "Orkin Man" character that would become one of the most recognizable figures in American advertising.

By the early 1980s, Rollins had become a sprawling conglomerate. By 1969, Rollins' revenues had grown to over 106 million. The company operated in three distinct sectors: consumer services (led by Orkin), media (broadcasting and outdoor advertising), and industrial services (including a growing oil field services division that capitalized on the 1970s energy boom).

But conglomerate structures were falling out of favor on Wall Street. Investors struggled to value companies that combined pest control with oil drilling and television stations. The sum-of-the-parts was worth less than the individual pieces. Something had to change.

The solution came in 1984 with a bold restructuring. Rollins Inc. split into three companies, all publicly traded. Rollins, Inc. (pest control via Orkin), Rollins Communications (media and advertising), and RPC Energy Services Inc. (oil and gas services). Randall was named the president and chief operating officer of Rollins Communications, the chairman of the board of Rollins Inc., and the chairman of the board, chief executive officer, president, and chief operating officer of RPC Energy Services.

This triple spinoff was financial engineering at its finest. Each company could now be valued on its own merits, management could focus on their core competencies, and the Rollins family maintained significant ownership stakes in all three entities. It was a masterclass in creating value through corporate structure—a lesson learned from their pioneering LBO twenty years earlier.

V. Focus & Transformation: Becoming Pure-Play Pest Control (1985-2007)

Post-spinoff, Rollins Inc. faced an identity crisis. Freed from the distractions of managing a conglomerate, leadership could finally answer a fundamental question: what business were they really in?

The answer came from studying Orkin's economics. While other divisions required constant capital investment—security systems needed equipment updates, lawn care demanded seasonal labor—pest control offered something unique: recurring revenue with minimal capital requirements. A technician with a sprayer could service dozens of customers per day, and once a customer signed up, they rarely switched providers.

Gary Rollins, now president of the slimmed-down Rollins Inc., made a strategic decision that would define the company's next chapter: Rollins would become the world's premier pest control company. Everything else was a distraction.

This focus coincided with a broader transformation in pest control. Environmental regulations were tightening, pushing out smaller operators who couldn't afford compliance. Customers were becoming more sophisticated, demanding integrated pest management rather than just chemical spraying. Technology was enabling route optimization and customer management at scale.

Rollins positioned itself at the forefront of these trends. They invested heavily in training, establishing Orkin University to professionalize their workforce. They pioneered computer-based routing systems when most competitors still used paper maps. Most importantly, they began shifting from one-time treatments to subscription-based service contracts.

The subscription model transformation cannot be overstated. In the 1980s, most pest control was reactive—customers called when they saw bugs. Rollins pushed preventative maintenance contracts, convincing customers that regular service was like insurance against infestations. This shift smoothed revenue, improved customer lifetime value, and created predictable cash flows that could fund further expansion.

International expansion began through franchising, a capital-light way to export the Orkin brand. Rather than deploying capital overseas, Rollins licensed its methods, training, and brand to local operators who understood their markets. By the late 1990s, Orkin franchises operated from Saudi Arabia to Singapore.

The dot-com boom and bust barely affected Rollins. While tech companies imploded, people still needed pest control. In fact, economic uncertainty often helped Rollins—when times were tough, regional competitors sold out at reasonable prices. The company's acquisition pace accelerated, picking up dozens of small operators annually.

By 2007, on the eve of the financial crisis, Rollins had transformed itself from a diversified conglomerate into a focused pest control powerhouse. Revenue exceeded $1 billion, operating margins approached 15%, and the company generated so much cash it didn't know what to do with it all. The stage was set for the next phase of growth.

VI. Modern Era: Scale, Technology & Acquisitions (2008-Present)

The 2008 financial crisis should have been devastating for Rollins. Consumer spending collapsed, housing starts plummeted, and commercial real estate froze. Yet the company didn't just survive—it thrived by making its smartest acquisition yet.

Gahlhoff joined Rollins during the company's 2008 acquisition of HomeTeam, where he served in a variety of leadership roles, including president. HomeTeam Pest Defense wasn't just another regional operator. It had pioneered a revolutionary approach: installing pest control systems directly into new home construction. Their Taexx system—tubes in the walls that could deliver treatment without entering the home—gave them exclusive relationships with major homebuilders.

The acquisition brought more than technology. It brought Jerry Gahlhoff Jr., who would prove to be the leader Rollins needed for its next chapter. Gahlhoff understood both operations and technology, having built HomeTeam into a modern, data-driven organization. His rise through Rollins was swift but earned: He was named president and COO of Rollins in 2020 and joined the board of directors in 2021.

Under Gahlhoff's operational leadership and Gary Rollins' strategic vision, the company accelerated its digital transformation. They launched BOSS (Branch Office Support System), a proprietary platform that managed everything from routing to inventory. Virtual Route Manager used algorithms to optimize technician paths, reducing drive time and fuel costs. Customer portals allowed scheduling and payment online—table stakes today but revolutionary for pest control.

The acquisition machine kept humming. But now, armed with data analytics, Rollins could identify targets with surgical precision. They knew which markets had the best demographics, which companies had the most valuable customer lists, and exactly how much to pay. Integration became formulaic: retain the local brand and relationships, but immediately plug acquisitions into Rollins' back-office systems.

The Fox Pest Control acquisition in 2023 demonstrated this evolved strategy. The transaction is valued at $350 million, including $32 million of contingent payments based upon the attainment of future growth and profitability levels. The Company had annual revenues in excess of $120 million in 2022. Fox had built a modern, digitally-native pest control business that appealed to younger consumers. Rather than compete, Rollins bought them and kept the founders involved to maintain the entrepreneurial culture.

Leadership transition came in 2023 when Jerry Gahlhoff Jr. became Rollins' president and CEO, effective Jan. 1, 2023. Gary Rollins remained as chairman, ensuring continuity while bringing fresh perspective to the CEO role. Gahlhoff's appointment signaled Rollins' commitment to technology and operational excellence over financial engineering.

The numbers tell the story of successful execution. For full-year 2024, revenues grew 10.3% to $3.4 billion, with organic revenues increasing 7.9%. More impressively, Operating income rose 12.7% to $657 million, with operating margin expanding 40 basis points to 19.4%. In a mature industry, Rollins was still finding ways to grow faster than the market while expanding margins.

VII. The Business Model & Competitive Advantages

To understand Rollins' dominance, you must understand the beautiful economics of pest control done right. Start with the recurring revenue model: Full-year 2024 sees $3.4B revenue, 19.4% margins, and 15% higher cash flow. Unlike most services, pest control is sticky. Switching providers requires scheduling new inspections, risking service gaps, and potentially paying termination fees. Customer retention rates exceed 85% annually.

The route density advantage compounds over time. Imagine two pest control companies operating in the same neighborhood. Company A has 10 customers; Company B has 100. Company B's technician can service 20 customers per day just by walking door-to-door, while Company A's technician spends half the day driving between scattered appointments. This density translates directly to margins—every additional customer in an existing route is almost pure profit.

Rollins has perfected the science of density. Their routing algorithms consider not just distance but time-of-day traffic patterns, customer preferences, and technician specializations. A termite expert isn't sent to handle a rodent problem. Commercial routes are separated from residential. The result: technicians spend more time servicing and less time driving.

Brand power matters more than you'd think in pest control. Orkin's century-old reputation means customers call them first when they see bugs. The "Orkin Man" advertising has created awareness that would cost billions to replicate. This brand strength allows premium pricing—Orkin often charges 20-30% more than local competitors, and customers happily pay for peace of mind.

The acquisition integration playbook has been refined over hundreds of deals. When Rollins buys a local operator, they typically retain the selling owner for 12-24 months, keep the local brand alive for customer continuity, and gradually migrate back-office functions to Rollins' systems. The acquired company's trucks might keep their paint job, but the scheduling, purchasing, and training all convert to Rollins' standards.

Capital efficiency sets Rollins apart from other service businesses. Unlike HVAC or plumbing, pest control requires minimal equipment. A $40,000 truck and $5,000 in equipment can generate $500,000 in annual revenue. This asset-light model means that growth capital goes toward customer acquisition and geographic expansion rather than machinery.

The regulatory moat is underappreciated. Every state has different licensing requirements for pest control operators. Many require years of experience before allowing independent practice. Chemicals are heavily regulated, requiring careful documentation and disposal. These barriers don't stop competition, but they slow it, giving established players like Rollins tremendous advantages in compliance and training.

Technology investments, once a weakness, have become a strength. Rollins spent over $100 million on digital transformation between 2015-2020. Today, their techs use tablets that identify pests through image recognition, automatically generate treatment plans, and capture customer signatures digitally. This tech stack would cost new entrants tens of millions to replicate.

VIII. Playbook: Key Business & Investing Lessons

The Rollins story offers a masterclass in value creation across multiple dimensions. First, the power of financial innovation: The 1964 Orkin LBO didn't just acquire a company; it created an entirely new way of thinking about acquisitions. Before Rollins, banks lent against assets. After Rollins, they lent against cash flows. This shift enabled the entire private equity industry that followed.

The family control dynamic presents fascinating lessons about patient capital. The Rollins family has maintained significant ownership for over 75 years across multiple public companies. This long-term orientation allowed them to make investments—like the digital transformation—that might have been rejected by quarterly-focused leadership. When you're building for grandchildren, not quarterly earnings, you make different decisions.

The roll-up economics demonstrate when consolidation truly works. Pest control was perfect: fragmented market, meaningful economies of scale, limited technological disruption risk, and sticky customer relationships. Rollins didn't just buy companies; they bought route density, customer lists, and local expertise. Each acquisition made the next one more valuable through network effects.

The subscription transformation preceded the SaaS revolution by decades. While software companies get credit for recurring revenue models, Rollins was converting one-time pest control visits to annual contracts in the 1980s. They understood that predictable revenue was worth accepting lower margins initially. A customer paying $30 monthly for preventative treatment was worth more than one paying $200 for emergency extermination.

Cross-selling through density creates compound advantages. When Rollins adds mosquito treatment to an existing pest control route, the marginal cost is minimal—the technician is already there. This allows them to underprice single-service competitors while maintaining higher margins. It's the physical-world equivalent of software's zero marginal cost.

The acquisition integration framework could be taught at business schools. Rollins doesn't immediately rebrand acquisitions or slash costs. They focus first on revenue retention, keeping the selling owners involved and maintaining local relationships. Cost synergies come gradually through purchasing power, route optimization, and system standardization. This patient approach minimizes customer churn and preserves value.

Perhaps most importantly, Rollins demonstrates the power of focus. The 1984 spinoffs freed management to concentrate on pest control. While competitors diversified into landscaping or cleaning services, Rollins went deeper into pest control. This focus allowed them to build capabilities—like the specialized technician training programs—that diversified competitors couldn't match.

IX. Bull vs. Bear Case Analysis

The Bull Case:

The bull thesis starts with margins. Operating margins improved 40 basis points in 2024, with adjusted margins approaching 20%. In a mature industry, margin expansion of this magnitude suggests either pricing power or operational improvements—Rollins has both. As route density increases and technology investments mature, margins should continue expanding toward 22-23%.

Climate change, paradoxically, benefits pest control companies. Warmer winters mean longer pest seasons and geographic expansion of species like termites and mosquitoes. The Asian giant hornet, spotted lanternfly, and other invasive species create new revenue opportunities. Environmental disruption drives demand for professional pest management.

Urbanization trends provide a long-term tailwind. Dense urban living creates ideal conditions for pest infestations—shared walls, food waste, and warmth. As more people move to cities globally, demand for professional pest control grows. Rollins' international expansion positions them to capture this global urban growth.

The acquisition pipeline remains robust. Management noted "demand for our services is solid and our pipeline for acquisitions is robust" heading into 2025. With thousands of small operators in the U.S. alone, Rollins has decades of consolidation opportunity ahead. Rising compliance costs and technology requirements will force more independents to sell.

Pricing power remains strong. Pest control is a small expense for most customers but provides significant peace of mind. Annual price increases of 3-5% rarely trigger cancellations. This pricing power, combined with volume growth, drives consistent revenue growth above inflation.

The Bear Case:

The bear thesis starts with market maturity. Rollins already controls an estimated 20% of the U.S. pest control market through its various brands. Doubling market share from here seems unlikely without regulatory scrutiny. Organic growth will naturally slow as the company scales.

Labor challenges threaten the model. Pest control technicians are skilled workers requiring extensive training and licensing. The U.S. faces a shortage of such workers, driving wage inflation. Rollins' labor costs are rising faster than revenue growth, pressuring margins despite operational improvements.

Technology disruption, while limited so far, could accelerate. Smart home devices can detect pests earlier. DIY solutions are becoming more effective. Companies like Amazon could enter with tech-enabled solutions that bypass traditional service models. Rollins' physical route-based model could become a liability in a digital-first world.

Economic sensitivity might be underestimated. While pest control proved resilient in past recessions, the next downturn could be different. Commercial customers, who represent 40% of revenue, might slash pest control budgets. Residential customers facing job losses might attempt DIY solutions.

Environmental regulations pose long-term risks. Pressure to reduce chemical usage could force expensive reformulations or limit treatment options. Europe's aggressive pesticide bans could spread to the U.S., forcing the industry to fundamentally change its approach.

Competition from private equity-backed roll-ups is intensifying. While Rollins pioneered the model, new entrants like Anticimex (backed by EQT) are applying similar strategies with fresh capital. These competitors can pay higher multiples for acquisitions, potentially shutting Rollins out of deals.

X. Epilogue & Future Outlook

As we look toward 2025 and beyond, Rollins stands at an inflection point. Jerry Gahlhoff Jr., President and CEO, noted "Our team delivered a strong finish to the year, exceeding our own revenue expectations and delivering healthy earnings growth for the full year. As we look to 2025, demand for our services is solid and our pipeline for acquisitions is robust".

The company that invented the leveraged buyout has proven remarkably adaptable across seven decades. From broadcasting to pest control, from family ownership to public markets, from chemical spraying to integrated pest management—Rollins has navigated each transition while maintaining its core identity as a services company built on recurring revenue and operational excellence.

The next chapter will likely focus on technology and international expansion. Artificial intelligence could revolutionize route optimization, predictive maintenance, and customer service. Internet of Things sensors could enable preventative treatment before infestations occur. International markets, particularly in Asia and Latin America, offer decades of growth potential.

ESG considerations will shape strategy. Rollins must balance effective pest control with environmental stewardship. This might mean more biological controls, targeted treatments rather than broad spraying, and transparent reporting on chemical usage. The company that adapts best to these pressures will dominate the next generation of pest control.

The family ownership structure, now in its third generation of leadership, faces eventual succession questions. Will the fourth generation maintain the same long-term orientation? Will family control eventually dilute through inheritance and stock sales? These governance questions matter for a company where patient capital has been a competitive advantage.

For investors, Rollins represents a fascinating study in compound growth. A $1,000 investment at the 1968 NYSE listing would be worth over $500,000 today, excluding dividends. This 500-fold return came not from revolutionary technology or lucky breaks, but from methodical execution of a simple strategy: provide essential services on a subscription basis, achieve route density, and reinvest cash flows into accretive acquisitions.

The boy from rural Georgia who borrowed against radio stations to buy an extermination company created more than just wealth. Wayne Rollins created a template—for leveraged buyouts, for service industry roll-ups, for building recurring revenue businesses. That template, refined and executed over 75 years, built an empire that started with rats and roaches but ended up teaching American business how to create enduring value.

As Rollins enters 2025, the fundamental question isn't whether the company will grow—with its competitive advantages and market position, growth seems assured. The question is whether it can maintain the operational excellence and acquisition discipline that transformed a small broadcaster into a global services giant. Based on the track record, betting against Rollins seems unwise. After all, they've been eliminating pests—and pessimists—for over a century.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube