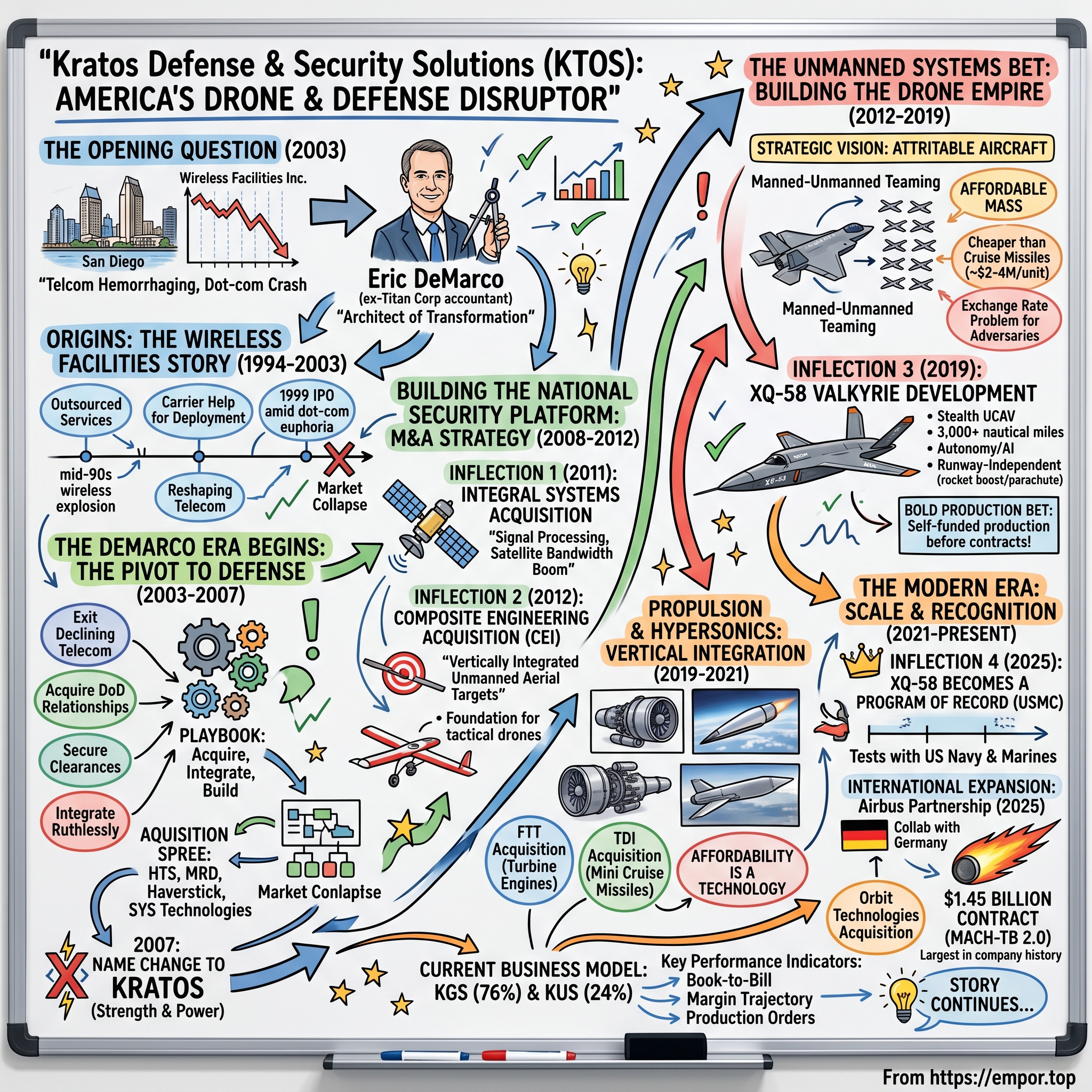

Kratos Defense & Security Solutions: America's Drone and Defense Disruptor

The Opening Question

Picture San Diego in late 2003. A telecom company called Wireless Facilities Inc. is hemorrhaging value, its stock having cratered from dot-com highs as the wireless infrastructure boom collapsed. Into this wreckage walks a former Arthur Andersen accountant named Eric DeMarco—a man who had already helped build one defense giant from scratch at Titan Corporation. What happens next is one of the most audacious corporate pivots in modern defense industry history: the complete transformation of a dying telecom services firm into a Pentagon darling now worth approximately $14.5 billion.

"Since joining Kratos, Mr. DeMarco has been instrumental in leading the company's efforts to successfully transition from a commercial communication business through the sale and disposition of assets, to build and grow, both organically and through strategic acquisition, a leading national security-focused technology, product, and systems provider for the U.S. and its allies."

Today, Kratos stands at the nexus of multiple transformative defense trends: the "attritable drone" revolution, hypersonic weapons development, propulsion technology, and the fundamental reimagining of how America wages air warfare. The company's XQ-58 Valkyrie drone—designed to cost around $2 million per unit, cheaper than many cruise missiles—recently became "a program of record and will be the first CCA [Collaborative Combat Aircraft] in production and fielded for the Marines," marking a watershed moment for both the company and the concept of affordable, expendable combat aircraft.

This is the story of how a failing telecom company became one of the most important—and controversial—bets in American defense technology.

Origins: The Wireless Facilities Story (1994-2003)

Birth of a Telecom Player

The company that would become Kratos began its life far from the defense industry's classified world of stealth aircraft and hypersonic missiles. "Wireless Facilities, Inc. is an independent provider of outsourced services for the wireless communications industry. We were incorporated in the state of New York on December 19, 1994 and began operations in March 1995."

The timing was auspicious. The mid-1990s wireless explosion was reshaping telecommunications, and carriers desperately needed help deploying infrastructure. "The principal services we provide include, but are not limited to, project planning, design, deployment and the overall management of wireless telecommunications networks. This work primarily involves radio frequency engineering, site development, project management and the installation of radio equipment networks."

The company was founded by Masood Tayebi and Massih Tayebi, who built WFI into a significant player in the wireless services market. The company reincorporated in Delaware in 1998 and "consummated our initial public offering on November 5, 1999"—timing that placed the IPO squarely amid the dot-com euphoria, when anything touching telecommunications commanded premium valuations.

The Crash

Like countless telecom services companies, WFI rode the wave up—then suffered the devastating crash. The NASDAQ collapse of 2000-2002 devastated the wireless infrastructure market. Carriers that had been building networks frantically suddenly froze capital expenditures. Companies like WFI, whose entire business model depended on carrier spending, found themselves adrift.

By the early 2000s, the company faced an existential crisis. Its core market was declining, customer spending had evaporated, and the stock had lost most of its value. The board needed a turnaround artist with vision—someone who could see opportunity where others saw only wreckage.

The DeMarco Era Begins: The Pivot to Defense (2003-2007)

Enter the Architect

"Eric DeMarco is President and Chief Executive Officer of Kratos Defense & Security Solutions, Inc. Mr. DeMarco joined the company in November 2003 when it was Wireless Facilities, Inc., a commercial wireless communications system infrastructure provider, as President and Chief Operating Officer."

To understand what happened next, you need to understand DeMarco's background. "Before Titan, Mr. DeMarco served in a variety of public accounting positions, primarily focusing on large multinational corporations and publicly traded companies. He holds a Bachelor of Science, Business Administration and Finance, summa cum laude, from the University of New Hampshire."

But the critical experience came at Titan Corporation. "Prior to Kratos, Mr. DeMarco was the President and Chief Operating Officer of the Titan Corporation, which was later acquired by L-3. Under his leadership, Titan grew from approximately $150 million in annualized revenue to $1.5 billion, with a backlog of over $4 billion. Mr. DeMarco's efforts were instrumental in creating one of the largest government information technology companies in the U.S."

This was the playbook: acquire strategically, integrate ruthlessly, and build a defense technology company through M&A. DeMarco had done it once at Titan, growing the company by a factor of ten. Now he would attempt the same feat at WFI—with an even more dramatic starting point.

"In April 2004, he assumed the role of CEO and was appointed as a director on the company's Board."

The Strategic Pivot

The transformation DeMarco orchestrated was nothing short of remarkable. Prior to his arrival, the company had no business with the Department of Defense or other federal agencies. Within a few years, the federal government would become Kratos's dominant customer.

The strategy had multiple components. First, exit the declining telecom services business by selling or shuttering non-strategic assets. Second, acquire companies with existing DoD relationships, security clearances, and established contract vehicles. Third, integrate aggressively to realize synergies and build critical mass.

From 2004 to 2009, the company executed a rapid-fire acquisition spree. The targets included High Technology Solutions (HTS) for communications systems engineering; Madison Research (MRD) for engineering and IT services; Haverstick Consulting for engineering and program management; and SYS Technologies for information technology products and wireless communication systems serving the Department of Defense and Department of Homeland Security.

Each acquisition added capabilities, contract vehicles, and cleared personnel—the essential building blocks of a defense contractor. "From June 1986 to January 1997, he held various positions at Arthur Andersen LLP, as a Senior Manager." DeMarco's accounting background gave him a sharp eye for identifying accretive targets and structuring deals to maximize value.

The Name Change: Becoming Kratos

In September 2007, the transformation became official. The company changed its name from Wireless Facilities Inc. to Kratos Defense & Security Solutions, with the NASDAQ ticker symbol changing from "WFII" to "KTOS."

The name itself carried symbolic weight. In Greek mythology, Kratos (Κράτος) represents the personification of strength and power—an appropriate rebrand for a company positioning itself as a force multiplier for American national security.

The name change signaled to investors, customers, and employees that the telecom chapter was closed. This was now a defense technology company, with all the strategic focus that implied.

Building the National Security Platform: M&A Strategy (2008-2012)

The Integral Systems Acquisition (2011) – First Major Inflection Point

If DeMarco's early acquisitions built the foundation, the 2011 merger with Integral Systems represented the company's emergence as a serious defense technology player.

"On July 27, 2011, Integral Systems merged with Kratos. Integral Systems provided services regarding the handling of data from space and terrestrial-based platforms into networks for military, government, and commercial satellite and aerospace customers. Integral Systems employed about 800 people in 14 locations."

The deal brought critical satellite-related capabilities. "Integral's signal processing systems are used by approximately 80 percent of United States' space missions, and Integral Systems is a leader in satellite signal monitoring and interference detection." Key subsidiaries included Lumistar (telemetry products), Newpoint Technologies (communications infrastructure management), and RT Logic (signal processing systems for space and aerospace communications).

"Under terms of the deal, Kratos is paying $90.6 million in cash and $144.9 million in stock for Integral, or $13 per share. The purchase price is a nearly 17 percent premium over the closing price of Integral's common stock."

The strategic rationale went beyond revenue. "Eric DeMarco, President and CEO of Kratos, said, 'In Operation Desert Storm 1991, the military used approximately 140 bits per second of satellite bandwidth per deployed person. During Operation Noble Anvil in Kosovo, the U.S. component of this mission increased to almost 3,000 bits per second. In operation Enduring Freedom in Afghanistan bps usage per person increased to approximately 8,300, and by the launch of operation Iraqi Freedom in 2004 bps per person had reached 13,800.'"

DeMarco was positioning Kratos for the inexorable growth in military satellite communications—a bet that has proven prescient given the subsequent explosion in space-based military capabilities.

The Composite Engineering Acquisition (2012) – Second Major Inflection Point

While Integral Systems established Kratos in space systems, the 2012 acquisition of Composite Engineering Inc. (CEI) laid the foundation for everything that followed in unmanned aerial systems.

"On 08 May 2012 Kratos Defense & Security Solutions Inc. agreed to buy Composite Engineering Inc. (CEI) in a deal that provided CEI's owners with $20 million in Kratos stock and $135 million in cash. Composite Engineering is a vertically integrated manufacturer and developer of unmanned aerial targets."

"Eric DeMarco, Kratos' President and CEO, said, 'CEI is clearly a world leader in the design, engineering, development, manufacturing and production of leading edge unmanned aerial targets and airframe structures.'"

The deal's strategic importance extended far beyond its immediate financials. "Composite Engineering's current backlog is approximately $160 million, with a qualified bid pipeline in excess of $1 billion. The company expected future organic growth rate is expected to be at least 20 percent."

CEI specialized in building target drones—unmanned aircraft designed to mimic enemy threats for military training and weapons testing. "CEI aircraft are made from composite materials and are designed to replicate some of the most lethal threats facing this nation's Warfighters and strategic assets."

This capability—building sophisticated, high-performance unmanned aircraft at affordable prices—would prove transformative. The same core competencies required to build realistic threat targets would later enable Kratos to develop combat-capable tactical drones that could change the face of aerial warfare.

Internal Reorganization

Following the CEI acquisition, "Kratos also announced today that it has completed an internal reorganization of its business to better align Kratos' resources for enhanced focus on the corporation's strategic priority areas of unmanned systems, electronic warfare, satellite communications, cyber security & warfare, tactical & ballistic missile systems, intelligence, surveillance & reconnaissance and critical infrastructure security."

The reorganization created five operating divisions, including Unmanned Systems Solutions (housing CEI), Electronic Products, Defense & Rocket Support Services, Technology & Training Solutions, and Public Safety & Security. This structure would evolve over time, but the strategic emphasis on unmanned systems was now explicit.

The Unmanned Systems Bet: Building the Drone Empire (2012-2019)

Strategic Vision: Attritable Aircraft

The concept of "attritable" aircraft represents one of the most important—and controversial—ideas in modern military aviation. The basic premise: develop sophisticated unmanned combat aircraft cheap enough that losing them in combat is acceptable.

This directly challenges decades of Pentagon procurement philosophy, which emphasized ever-more-capable (and expensive) platforms designed to survive in contested environments. The F-35 Joint Strike Fighter, with a per-unit cost exceeding $80 million, exemplifies this approach.

Kratos bet on the opposite strategy. What if you could build a stealthy, capable combat drone for $2-4 million? Instead of one F-35, you could field 20-40 attritable aircraft. The math for adversary air defenses suddenly becomes very unfavorable—shooting down cheap drones with expensive missiles is an exchange rate problem that benefits the drone operator.

The military term for this is "affordable mass." And Kratos, with its target drone heritage and composite manufacturing expertise, was uniquely positioned to deliver it.

The XQ-58 Valkyrie Development – Third Major Inflection Point

"The Kratos XQ-58 Valkyrie is an experimental stealth unmanned combat aerial vehicle (UCAV) designed and built by Kratos Defense & Security Solutions for the United States Air Force's Low Cost Attritable Strike Demonstrator (LCASD) program, under the USAF Research Laboratory's Low Cost Attritable Aircraft Technology (LCAAT) project portfolio. It was initially designated the XQ-222. The Valkyrie completed its first flight on 5 March 2019 at Yuma Proving Ground, Arizona."

The development timeline was remarkable by defense industry standards. "The XQ-58's first flight took place on 5 March 2019, about two and a half years after Kratos received the contract." In an industry where major aircraft programs routinely take decades, Kratos moved from contract to first flight in roughly 30 months.

"The XQ-58 Valkyrie fell within the USAF Research Laboratory's Low Cost Attritable Aircraft Technology (LCAAT) portfolio, whose objectives included designing and building unmanned combat aerial vehicles (UCAVs) faster, by developing better design tools and maturing and using commercial manufacturing processes to reduce production time and cost. The LCAAT was to escort the F-22 or F-35 during combat missions and to deploy weapons or surveillance systems."

Technical Innovation

The Valkyrie's specifications reveal an aircraft designed from the ground up for a different kind of warfare. "The Valkyrie can travel more than 3,000 nautical miles (approximately 5,666 kilometers) and reach speeds of 0.86 Mach with altitude up to 45,000 feet."

"The XQ-58 Valkyrie is a collaborative-combat aircraft designed to help Joint and Allied Forces be more lethal and more survivable against near-peer adversaries. Using autonomy and artificial intelligence (AI), the Valkyrie can operate independently or seamlessly integrate into manned-unmanned teaming operations."

Multiple launch configurations add operational flexibility. The original design uses rocket-boosted rail launch and parachute recovery—completely runway-independent. Later variants include a trolley launch system and, most recently, "Kratos has released a rendering offering the first look at a version of its stealthy XQ-58A Valkyrie drone with built-in landing gear. The company first announced that this new version, which might present certain advantages over the original runway-independent design, was in the works last year."

The Bold Production Bet

Perhaps the most remarkable aspect of Kratos's Valkyrie strategy was the company's decision to fund production without a guaranteed contract. Kratos invested its own capital to begin manufacturing Valkyries, betting that demonstrating actual production capability would win customers that simulation and PowerPoint could not.

"Kratos officials have said the company could produce 250 to 500 Valkyries per year. It can be produced at a unit cost of $4 million at an annual production rate of 50 aircraft, and possibly for less than $2 million if over 100 airframes are built per year."

This approach—self-funding to demonstrate capability—reflects DeMarco's philosophy: in defense procurement, showing rather than telling creates differentiation. While competitors submitted proposals and waited, Kratos built and flew actual aircraft.

Propulsion & Hypersonics: Vertical Integration (2019-2021)

Florida Turbine Technologies Acquisition (2019)

Kratos recognized that controlling the propulsion supply chain was essential for its unmanned systems strategy. "In February 2019, Kratos purchased Florida Turbine Technologies."

"Kratos Defense & Security Solutions, Inc. announced that it has acquired an 80.1% interest in Florida Turbine Technologies, Inc. and FTT Core, LLC, a leading technology company and innovation leader in advanced turbine engines, for $60 million, consisting of $33 million in cash and $27 million in Kratos common stock. Kratos has an option to acquire the remaining 19.9% of FTT at a future date."

"FTT, based in Jupiter, FL, with offices in Oklahoma, Puerto Rico, Canada, Germany, and the United Kingdom, was founded in 1998 by Shirley and Joseph Brostmeyer." The acquisition brought "a world-class turbine engine company" with focus on "the development of small, affordable, highly-efficient, turbojet and turbofan engines that we believe will transform the engine market for jet powered tactical weapon systems and unmanned aerial systems."

Beyond traditional jet engines, "we are also focused on developing advanced, affordable engines for hypersonic systems that will demonstrate a new class of hypersonic propulsion system."

Technical Directions Inc. (TDI) Acquisition (2020)

"On February 24, 2020, Kratos bought small turbojet manufacturer, Technical Directions Inc. (TDI), based in Detroit, Michigan."

TDI brought specific engine expertise with immediate commercial applications. "Technical Directions Inc. TDI has developed and refined turbine engine technologies for military applications in Michigan since 1983—providing unique features in support of low-cost, expendable turbojet engine applications, such as miniature cruise missiles and other Unmanned Aerial Vehicles. With the engineering, manufacturing, and system integration employees in the Oxford, Michigan facility, TDI's subject matter experts have experience that encompasses all aspects of this turbine engine class."

The TDI engines have since won significant applications. "Kratos Defense & Security Solutions has announced a memorandum of understanding between Technical Directions (TDI), a business unit within Kratos Unmanned Systems Division, and Boeing for the TDI-J85 turbine engine to provide propulsion for the Powered Joint Direct Attack Munition (JDAM). Boeing's Powered JDAM combines a 500lb ordnance and the conventional JDAM guidance kit, with a wing kit and a Kratos TDI-J85 engine to expand the potential range of the weapon system."

Strategic Rationale: "Affordability is a Technology"

Kratos's acquisition of propulsion companies reflects a core philosophy that DeMarco articulates repeatedly: "affordability is a technology." By controlling the engine supply chain, Kratos can ensure its drones and missiles aren't constrained by expensive third-party propulsion systems.

This vertical integration differentiates Kratos from competitors who must source engines externally, often from the same major aerospace companies that compete with them for unmanned systems contracts.

The Modern Era: Scale & Recognition (2021-Present)

XQ-58 Becoming a Program of Record – Fourth Major Inflection Point

After years as an experimental program, the Valkyrie achieved a crucial milestone in 2025. "U.S. defense officials confirmed July 16 that a new version of the Kratos XQ-58 Valkyrie UAV will transition into a program of record for the U.S. Marine Corps, opening a path to production for the autonomous fighter."

"In December 2022, the United States Marine Corps ordered two XQ-58s for testing under the Marine Corps Penetrating Affordable Autonomous Collaborative Killer – Portfolio (PAACK-P) program, and conducted first test flights at Eglin Air Force Base in October 2023." "In January 2023, the United States Navy ordered two XQ-58s for tests similar to those being undertaken by the Marines."

"On January 21, 2025, Kratos Defense & Security Solutions, Inc. announced a $34,856,449 cost-plus-fixed-fee contract modification granted by the United States Marine Corps. This contract extension is intended to integrate mission systems and subsystems as part of the development of the Marine Air-Ground Task Force Unmanned Aerial System Expeditionary (MUX) tactical drone program."

International Expansion: The Airbus Partnership (2025)

"Munich, Germany / San Diego, USA 16 July 2025 – Airbus Defence and Space and US based Kratos Defense and Security Solutions have entered into a partnership based on the Kratos XQ-58A Valkyrie, a flight-proven UCCA (uncrewed collaborative combat aircraft), which will be equipped with an Airbus made mission system, combat ready for the German Air Force by 2029."

"'In the given disruptive geopolitical context, our customers have expressed an urgent demand for both attritable and non-attritable Collaborative Combat Aircraft. The collaboration of Kratos and Airbus, based on an existing and proven UAS platform and featuring a sovereign multi-platform mission system, will deliver crucial capabilities for our warfighters in Europe before the end of the decade. This partnership will help to accelerate Europe's ability to defend itself while fostering NATO's transatlantic ties,' said Mike Schoellhorn, CEO of Airbus Defence and Space."

"The programme forms part of a broader Bundeswehr procurement initiative to introduce a stealthy, subsonic, deep-strike drone capable of ranges exceeding 540 nmi by 2029."

Valkyrie Variants & the CCA Ecosystem

"At least two mission configurations of the system were announced to exist in a production status at Kratos' Oklahoma facilities, with Kratos indicating readiness to accept a more substantial production order. At least five XQ-58 variants are in development."

"The MQ-58B, which is intended to fulfill the role of suppression of enemy air defenses, or SEAD, is one of at least five variants of the XQ-58 under development by Kratos. This news comes alongside an announcement that the future variants of the Valkyrie will include underwing hardpoints for munitions."

Hypersonic Systems: The $1.45 Billion Contract

In January 2025, Kratos secured the largest contract in company history. "Kratos Defense & Security Solutions, Inc. announced today that it has been awarded a five-year OTA contract for the Multi-Service Advanced Capability Hypersonic Test Bed (MACH-TB) 2.0 under Task Area 1. The total value of this award, if all options are exercised over the five-year period, is $1.45B."

"The Pentagon awarded defense-technology firm Kratos a contract worth up to $1.45 billion to help increase its hypersonic flight-testing cadence. The five-year contract is part of the second phase of the Pentagon's Multi-Service Advanced Capability Hypersonic Test Bed program."

"Eric DeMarco, President & CEO of Kratos Defense & Security Solutions, Inc., said, 'Kratos is honored to receive the largest contract award in our company's history, a testament of the value Kratos' employees and team bring both to our Company and United States National Security. This programmatic milestone underscores our unwavering commitment to making upfront investments for rapidly developing, and being first to market with affordable, mission-critical solutions.'"

"Kratos was a subcontractor for MACH-TB 1.0, which supported more than 25 test flights. For the program's next phase, the firm will play a prime integration role, leading a team of contractors that includes Leidos, Rocket Lab and Purdue University."

Additional hypersonic investments followed. "Known internally to Kratos as Project Helios, the contract to Kratos for the leading technology facility has a total projected value of $68.3 million. Once complete, the facility will address current critical gaps in U.S. Defense Industrial Base capabilities by providing essential testing infrastructure for thermal protection systems used in hypersonic vehicles."

Recent Acquisitions & Expansion

The acquisition strategy continues. "Kratos Defense & Security Solutions, Inc. announced today that it has signed a definitive agreement to acquire 100 percent of the ordinary shares of Orbit Technologies Ltd for $356.3 million, which is expected to be funded via cash on Kratos' balance sheet."

"Orbit is a leading global provider of mission-critical satellite-based communication systems for mobile and unmanned aerial, seaborne, undersea and land systems, military vehicles and other systems. Orbit provides its hardware, products and systems to major air forces, traditional prime contractors and emerging new defense and space companies."

"Kratos expects the acquisition to close by the end of March 2026, assuming completion of regulatory matters related to an acquisition of an Israel-based national security company by a non-Israel based company."

Capital Raise for Growth

"Kratos Defense & Security Solutions, Inc. today announced that it intends to offer for sale $500,000,000 of shares of its common stock in an underwritten offering pursuant to an effective shelf registration statement filed with the Securities and Exchange Commission. The underwriters will have a 30-day option to purchase up to an additional $75,000,000 of shares of common stock from Kratos."

"The net proceeds are expected to fund investments related to national security priorities, finance acquisitions, and cover general corporate expenses such as debt repayment."

Current Business Model & Financial Performance

Business Segments

Kratos operates through two reportable segments: Kratos Government Solutions (KGS) and Unmanned Systems (KUS).

"The primary driver behind last 12 months revenue was the Kratos Government Solutions segment contributing a total revenue of US$865.8m (76% of total revenue)."

The KGS segment encompasses microwave electronic products, space and satellite systems, training and cybersecurity solutions, C5ISR/modular systems, turbine technologies, and defense and rocket support services. The Unmanned Systems segment covers unmanned aerial, ground, and seaborne platforms along with related command, control, and communications systems.

Financial Performance

"Full year revenues reached $1.136 billion, showing 9.6% growth from 2023's $1.037 billion. The company achieved net income of $16.3 million with EPS of $0.11 per share."

"Q4 2024 highlights include revenues of $283.1 million, operating income of $3.0 million, and a robust book-to-bill ratio of 1.5 to 1. The company generated significant cash flow with $45.6 million from operations and $32.0 million in free cash flow."

"Notable segment performance includes Unmanned Systems revenue growth of 27.5% to $270.5 million and Government Solutions segment growth of 5.0% to $865.8 million. The company's total backlog reached $1.445 billion with a substantial bid pipeline of $12.4 billion."

Third quarter 2025 results showed continued momentum. "Third quarter 2025 Revenues of $347.6 million increased $71.7 million, reflecting 23.7 percent organic growth from third quarter 2024 Revenues of $275.9 million."

"Organic revenue growth was reported in our Unmanned Systems segment of 35.8 percent and in our KGS segment of 20.0 percent. The most notable growth in our KGS Segment was in our Defense Rocket Systems and Space, Training and Cyber businesses, with organic revenue growth rates of 47.2 percent and 21.2 percent, respectively."

Forward Guidance

"Increased Full Year 2026 Organic Revenue Growth Rate Forecast To 15 Percent to 20 Percent Above 2025 Forecast Full Year Revenue with Projected 100BP Increase in Adjusted EBITDA Margin Over 2025."

"Looking ahead, revenue is forecast to grow 14% p.a. on average during the next 3 years, compared to a 6.9% growth forecast for the Aerospace & Defense industry in the US."

Competitive Position & Industry Dynamics

The CCA Competitive Landscape

Kratos occupies a unique position in the emerging Collaborative Combat Aircraft (CCA) market. While the company was not selected for the U.S. Air Force's Increment 1 CCA program, "On April 24, 2024, the Air Force announced the most significant CCA milestone to date: a contract award that will take two companies, Anduril and General Atomics, to the next stage of the program."

However, "The Kratos XQ-58 Valkyrie was developed for the United States CCA program, but was considered insufficient for USAF requirements. Still, it has been a leading experimental aircraft for the USAF to develop its CCA doctrine and requirements."

"The USAF determined the XQ-58 airframe was too small to meet the requirements of the Collaborative Combat Aircraft program." Yet this apparent setback obscures a more nuanced reality.

"The U.S. Air Force has indicated that it may now be leaning toward cheaper and simpler designs for the second iterative development phase, or Increment 2, of its Collaborative Combat Aircraft program. Kratos, which was notably absent from the CCA program's Increment 1 competition, has said on several occasions that it is interested in taking part in Increment 2."

The company has also developed additional designs. "Two new drone designs, Apollo and Athena, are in development at Kratos with a particular focus on collaborative operations with other crewed and uncrewed aircraft, and an eye toward sales in Europe. The modular Apollo and Athena designs are smaller than the company's XQ-58 Valkyrie, and could be configured to carry weapons, electronic warfare systems, or additional sensors."

Competitive Advantages

Kratos's positioning reflects several structural advantages:

First-mover in attritable aircraft: The company has been flying CCA-type aircraft since 2015. "Kratos Defense & Security Solutions, Inc. announced today another recent successful flight from its family of Collaborative Combat Aircraft—flying and demonstrating capabilities since 2015. Kratos' family of CCA's include more than four different aircraft types, with each having been flying for several years."

Vertical integration: From airframes to engines to ground control systems, Kratos controls critical supply chains that competitors must source externally.

Affordability focus: "Kratos rail-launched and runway-independent CCAs are developed to maximize performance per cost rather than being at the exquisite end of the capability and cost level. Therefore, they are ideal for 'large mass, high quantity' scenarios."

Proven production: Unlike competitors showing renderings and simulations, Kratos has actual production aircraft flying with U.S. military operators.

Industry Tailwinds

The broader defense environment strongly favors Kratos's positioning. "The military UAV market has entered a new phase as defense planners weave uncrewed aircraft into core force-structure blueprints. Current doctrine prizes airframes that survive dense air-defense zones, pass data across secure networks, and deploy in numbers large enough to stretch enemy interceptors."

"Such priorities have attracted fresh public funding, best illustrated by the US Department of Defense's Replicator initiative, which fast-tracks low-cost, autonomous, and ultimately expendable drones into service... Growing acceptance that some vehicles must be sacrificed in high-threat battles is also fuelling demand for 'attritable' systems that can absorb losses without derailing the mission."

"Defense interest in small UAVs has surged, with low-cost FPV drones being prioritized by the USA Department of Defense, inspired by lessons from Ukraine. Contracts are being pursued by startups, but large procurement deals are expected to be won by only a few firms due to scalability and capability demands."

Bull and Bear Cases

Bull Case

Structural tailwinds: The fundamental shift toward attritable, autonomous aircraft represents a multi-decade opportunity. Kratos is positioned as the premier "affordable mass" provider, with proven production capability and operational experience that competitors lack.

Hypersonics leadership: The $1.45 billion MACH-TB 2.0 contract validates Kratos's hypersonic capabilities. As the Pentagon accelerates hypersonic development to counter China and Russia, Kratos's testing infrastructure and systems engineering expertise become increasingly valuable.

International expansion: The Airbus partnership demonstrates global demand for attritable CCA capabilities. European defense budgets are expanding, and Kratos offers a proven, affordable solution that can be fielded years before indigenous alternatives.

Vertical integration moat: Controlling propulsion (Florida Turbine Technologies, TDI), airframes (CEI heritage), and ground systems creates competitive barriers that pure-play drone developers cannot match.

M&A execution track record: DeMarco's two decades of successful acquisition integration reduces execution risk on the Orbit Technologies deal and future M&A.

Bear Case

CCA program exclusion: The Air Force's selection of Anduril and General Atomics for CCA Increment 1 raises questions about whether Kratos can win the largest autonomous aircraft contracts. If Increment 2 also excludes Kratos, the company's drone business may remain subscale.

Prime contractor risk: Kratos remains a mid-tier contractor competing against well-capitalized primes (Boeing, Lockheed Martin, Northrop Grumman) and well-funded new entrants (Anduril, Shield AI). These competitors can absorb losses and invest in R&D at levels Kratos cannot match.

Customer concentration: The U.S. government represents the vast majority of revenue. Budget instability, continuing resolutions, or policy changes could significantly impact results. "A U.S. Government budget was not passed by October 1, 2024, the beginning of Federal Fiscal Year 2025, and as a result, Kratos and others in our industry are operating under a Continuing Resolution Authorization."

Valuation: At current prices, the stock prices in substantial future growth. Any execution stumbles or contract losses could trigger significant multiple compression.

Margin pressure: "KUS's Adjusted EBITDA for the second quarter of 2025 was $3.6 million, compared to $7.2 million for the second quarter of 2024, reflecting the impact of the revenue volume and continued impact of increased material and subcontractor and labor costs on multi-year fixed price production contracts." Fixed-price contract legacy issues may continue pressuring margins.

Porter's Five Forces Analysis

Supplier Power (Moderate): Kratos's vertical integration in propulsion reduces supplier power in critical areas. However, aerospace-grade components and specialized materials still require external sourcing.

Buyer Power (High): The U.S. government is the dominant customer with significant negotiating leverage. However, Kratos's unique capabilities in certain niches provide some pricing power.

Threat of New Entrants (Moderate-High): Well-funded startups like Anduril and Shield AI are entering the autonomous aircraft market with substantial venture backing. However, security clearances, production capability, and operational track records create meaningful barriers.

Threat of Substitutes (Low-Moderate): Crewed aircraft remain substitutes, but the cost differential increasingly favors unmanned systems. The greater threat is classification of drone missions as purely expendable (handled by cheaper systems) versus reusable (handled by more capable platforms).

Competitive Rivalry (High): Intense competition exists across all segments. Traditional primes, mid-tier specialists, and new entrants all pursue overlapping opportunities.

Hamilton Helmer's 7 Powers Framework

Counter-Positioning: Kratos's "affordability as technology" philosophy directly contradicts traditional defense contractor approaches emphasizing capability over cost. Legacy primes cannot easily shift to attritable/expendable business models without cannibalizing existing programs.

Scale Economies: Production volume advantages exist in drone manufacturing, but Kratos has not yet achieved the scale to fully capture these benefits. The Valkyrie production ramp will be critical.

Switching Costs: Moderate. Once a military service integrates a particular drone ecosystem (ground control, mission systems, training), switching costs increase. The Marine Corps' investment in Valkyrie infrastructure creates meaningful retention value.

Network Effects: Limited direct network effects. However, a growing fleet of Valkyries operating with different services and allies creates indirect benefits through data sharing and operational learning.

Cornered Resource: Kratos's deep expertise in target drone development—translating to combat drone capability—represents institutional knowledge that took decades to develop. The CEI engineering team and manufacturing processes are difficult to replicate.

Process Power: The company's ability to move rapidly from concept to flight—30 months for Valkyrie—reflects embedded process advantages that traditional defense contractors struggle to match.

Branding: Limited relevance in government procurement, though Kratos's reputation for delivering working systems on schedule creates valuable credibility.

Key Performance Indicators to Monitor

For investors tracking Kratos's ongoing performance, three metrics deserve particular attention:

1. Unmanned Systems Segment Book-to-Bill Ratio

"KUS's book-to-bill ratio for the third quarter of 2025 was 0.6 to 1.0 and 1.1 to 1.0 for the twelve months ended September 28, 2025."

This ratio reveals whether Kratos is winning new drone contracts at a pace that supports growth projections. A sustained ratio above 1.0 indicates growing backlog; below 1.0 signals potential revenue deceleration. Given the lumpy nature of defense procurement, tracking the trailing twelve-month figure provides better signal than quarterly snapshots.

2. Adjusted EBITDA Margin Trajectory

Management has projected 100 basis points of margin expansion in both 2026 and 2027. "We are also expecting EBITDA margin expansion for both 2026 and 2027, as we scale the business and transition to more profitable contracts."

Margin improvement depends on transitioning from legacy fixed-price contracts (negotiated when inflation was lower) to new contracts with appropriate pricing. Failure to achieve margin expansion would suggest structural challenges in the business model.

3. XQ-58/MQ-58 Production Orders

The conversion of Valkyrie from experimental program to program of record should generate production orders. Tracking announced contract values and delivery quantities will indicate whether the attritable aircraft thesis is translating to commercial reality. The Airbus partnership's progress toward German procurement provides additional data points on international demand.

Regulatory and Legal Considerations

Export Controls

As a defense contractor dealing in advanced unmanned systems and hypersonic technologies, Kratos operates within stringent export control regimes. International sales require ITAR (International Traffic in Arms Regulations) or EAR (Export Administration Regulations) approvals, which can delay or prevent certain transactions.

The Airbus partnership structures around these constraints by having Airbus provide mission systems (potentially containing European-controlled technology) integrated with Kratos's airframe. Similar approaches may be required for other international opportunities.

Security Clearances

Kratos employees working on classified programs hold various levels of security clearance. The company's ability to win and execute classified contracts depends on maintaining appropriate facility and personnel clearances—a process that involves significant government oversight and can be affected by workforce changes or security incidents.

Government Contract Compliance

Defense contractors face extensive regulatory requirements around cost accounting, quality systems, and contract execution. The company notes in filings that it operates under continuous government oversight and audit, with potential for contract adjustments or penalties.

Conclusion: The Story Continues

Kratos Defense & Security Solutions represents one of the most dramatic corporate reinventions in modern business history. Eric DeMarco's transformation of a failing telecom services company into a $14.5 billion defense technology leader required two decades of disciplined acquisition, strategic vision, and willingness to bet the company on emerging technologies.

The company now stands at an inflection point. The "attritable drone" concept that Kratos championed when it seemed radical has become Pentagon doctrine. The XQ-58 Valkyrie—developed on Kratos's own dime when no contract existed—is becoming a program of record. International partners like Airbus are licensing Kratos technology for their own CCA programs. The $1.45 billion MACH-TB 2.0 contract validates hypersonic capabilities.

Yet significant questions remain. Can Kratos scale production to meet the "affordable mass" promise? Will the company win CCA Increment 2 or remain relegated to specialized niches? Can margins expand as legacy contracts roll off? How will competition from well-funded entrants like Anduril evolve?

The answers will determine whether Kratos becomes one of the defining defense companies of the autonomous warfare era—or a pioneer whose innovations were ultimately commercialized by larger competitors. For investors, the company offers exposure to genuinely transformative defense technologies, led by a management team with an extraordinary track record of value creation.

"By progressing to actual flight and actual demonstration with high capability-per-cost, yet affordable, systems faster than traditional and conventional platform providers can achieve, Kratos is changing the status quo. We believe in being disruptive and are investing our own resources at an industry-leading, unmatched rate to ensure the warfighter has increased capabilities sooner for less cost."

The story of Kratos—from telecom wreckage to drone disruptor—continues to be written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube