Entegris: The Invisible Backbone of the Semiconductor Revolution

I. Introduction & Episode Roadmap

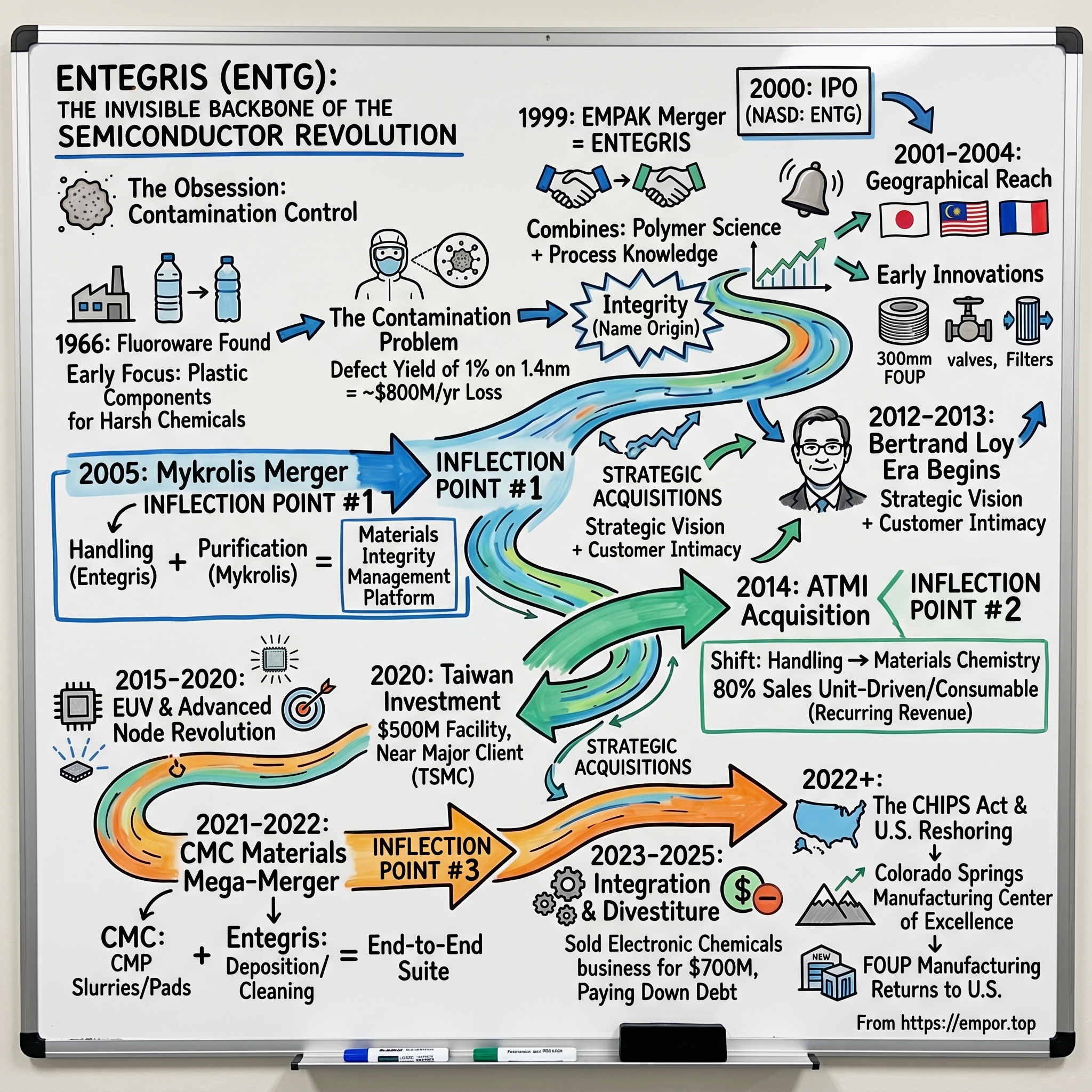

Picture this: a single speck of dust, invisible to the human eye, lands on a silicon wafer in the midst of fabrication. That microscopic particle—just a few nanometers across—destroys what would have been a cutting-edge processor worth hundreds of dollars. Now imagine this happening thousands of times across millions of wafers, and you begin to understand why contamination control is the silent, existential obsession of the semiconductor industry.

Entegris, Inc. is a supplier of materials for the semiconductor and other high-tech industries. Approximately 80% of the company's products are used in the semiconductor industry. Yet despite being essential to the manufacture of virtually every advanced chip on the planet, Entegris operates in near-total obscurity outside of industry circles. You've never heard of them, but no modern chip can be made without them.

Entegris achieved approximately $3.5 billion in sales for fiscal year 2023, making it one of the largest pure-play semiconductor materials companies in the world. The company employs approximately 8,200 people worldwide and has a market capitalization of approximately $11.873 billion.

The hook of this story is how a small plastic container maker from Minnesota became essential to the most advanced manufacturing process on Earth. The journey from fabricating simple wafer trays in 1966 to producing the nanoscale purification systems that enable 2-nanometer chips is one of strategic acquisitions, relentless innovation, and an unerring bet on the inexorable march of Moore's Law.

"It has been an exciting journey for us that began with the emergence of Moore's law and that has tracked the growth of the semiconductor industry into a $330 billion market," noted CEO Bertrand Loy in 2016, marking the company's 50th anniversary.

Three themes dominate Entegris's six-decade history: contamination control as the company's technical raison d'être, an aggressive acquisition strategy that transformed a components supplier into a comprehensive solutions provider, and a relentless attachment to riding the semiconductor industry's technological escalator. Follow those threads, and the full narrative emerges.

II. Origins: The Birth of Semiconductor Materials Handling (1966-1999)

Fluoroware's Founding

In 1966, the semiconductor industry barely existed as we know it today. Fairchild Semiconductor had introduced the first commercial integrated circuit just five years earlier. The industry was a collection of startups and corporate labs, and the chips themselves were measured in microns, not nanometers.

Entegris traces its origins to Fluoroware, Inc., which was founded in 1966 in Chaska, Minnesota, by Victor Wallestad as a custom fabricator serving the burgeoning electronics industry. The company emerged during the early days of semiconductor manufacturing, providing essential plastic components to protect sensitive materials from contamination in cleanroom environments. Wallestad, recognizing the need for reliable handling solutions amid the rapid advancement of microelectronics, established Fluoroware to address the challenges faced by pioneering chip producers.

Entegris was founded in 1966 as Fluoroware, a small manufacturer of plastic components for the emerging semiconductor industry based in Chaska, Minnesota. The company initially focused on producing specialized plastic products that could withstand the harsh chemicals used in semiconductor manufacturing.

What made Fluoroware's products special wasn't glamorous—it was about chemistry and precision. Fluoroware's initial products included screw-top plastic bottles for secure chemical storage and wafer trays designed to safeguard silicon wafers during processing and transport. These weren't ordinary plastics; they were engineered to resist corrosion from the harsh acids used in chip fabrication while not shedding particles that could contaminate the wafers.

The Contamination Problem

Understanding why Fluoroware's mundane-sounding products mattered requires understanding the semiconductor industry's central obsession: contamination.

A modern semiconductor fab is perhaps the cleanest environment humans have ever created. The air is filtered to remove particles down to nanometer scales. Workers wear full-body suits ("bunny suits") not to protect themselves from the environment, but to protect the environment from them. Every surface, every tool, every container that touches a silicon wafer must be engineered to prevent contamination.

This obsession didn't emerge overnight. The industry began with clean room technology initially developed for the aerospace industry. However, these techniques proved inadequate as chip manufacturing scaled and feature sizes shrank. Clean room technology had to evolve alongside chip development, with designs and densities advancing together. The industry's growth capability has consistently depended on solving contamination issues for each generation of chips.

Why is contamination existential for semiconductors? Consider that a single fingerprint contains oils and salts that, at nanometer scales, represent massive chemical contamination. A particle of dust on a 28nm chip would be like dropping a boulder onto a highway—it destroys the circuit paths completely.

As chips get smaller, the margin of error also gets smaller. The margin of error for defects has shrunk from 7nm on 14nm nodes to 0.7nm on 1.4nm nodes. Solid, liquid, or gaseous impurities that come into contact with wafers can become an expensive mistake. Entegris estimates that a defect yield of 1% on a 1.4nm node process can cost a fab up to $800M per year.

The EMPAK Merger and Birth of Entegris

EMPAK was founded in 1980, focusing on wafer handling. While Fluoroware concentrated on containers and bottles, EMPAK developed specialized systems for transporting and handling silicon wafers—the crown jewels of any fab operation.

The company was incorporated in 1999 as the combined entity of Fluoroware, Inc., which began operating in 1966, and EMPAK, Inc. The 1999 merger forming Entegris was pivotal, consolidating complementary strengths in materials handling within the semiconductor ecosystem.

The name "Entegris"—derived from "integrity"—captured the company's core proposition: maintaining the purity and integrity of critical materials throughout the semiconductor manufacturing process. The merger combined Fluoroware's polymer science expertise with EMPAK's process knowledge, creating a company with deeper capabilities in materials handling than either could have achieved alone.

By 1999, the combined company had already established a global footprint: manufacturing operations began in Japan in 1984, ISO 9001 certification was received in 1993, and manufacturing in Malaysia began in 1997.

III. Going Public & Early Growth (2000-2004)

The IPO and Dot-Com Storm

The company went public in 2000. It began trading on the NASDAQ under the ENTG symbol on July 10, 2000.

The timing couldn't have been worse—or perhaps more character-building. The dot-com bubble had already begun deflating when Entegris hit the public markets, and by 2001, the semiconductor industry was in freefall. The NASDAQ lost 78% of its value from peak to trough. Semiconductor equipment companies were devastated.

Yet Entegris survived. The key was the nature of its business: while capital equipment purchases could be delayed or cancelled, chip manufacturers still needed consumable materials to keep existing fabs running. Filters need replacing. Chemicals need replenishing. Wafer carriers wear out. This consumable-focused business model provided a floor under Entegris's revenues even as capital spending collapsed.

Building Global Manufacturing Presence

The early 2000s saw Entegris methodically expand its geographical reach. The company's Japanese manufacturing presence, established in 1984, proved crucial as Japanese chipmakers remained significant players. The Malaysian facility, opened in 1997, positioned Entegris near the growing cluster of semiconductor assembly operations in Southeast Asia.

The expansion wasn't just about being close to customers—it was about understanding local requirements. Semiconductor manufacturing is a highly customized business; what works for one fab may not work for another. Local presence meant local relationships, local technical support, and the ability to co-develop solutions with customers.

Early Acquisitions and Product Innovation

In May 2004, Entegris acquired SNEF's Precision Parts Cleaning Business with an offsite cleaning facility in Montpellier, France. This acquisition marked an early step in Entegris's strategy of expanding from pure materials handling into adjacent services.

Over its 50-year history, Entegris has brought hundreds of innovations to its markets, including many technology "firsts." Among its notable products are Integra® valves, Spectra™ FOUPs, PrimeLock® fittings, Torrento® liquid filters, SDS® safe gas delivery systems and NOWPak® liquid dispense systems.

Industry "firsts" include the first linear wafer carrier, first wafer shipper, first wafer suspension system and the first 300mm FOUP (wafer carrier).

The 300mm FOUP innovation deserves special attention. When the industry transitioned from 200mm to 300mm wafers in the early 2000s, everything about wafer handling had to be reinvented. Larger wafers meant heavier loads, different contamination profiles, and new handling challenges. Entegris's ability to develop the first 300mm FOUP demonstrated its position at the leading edge of materials handling technology.

By 2004, Entegris had established itself as a essential supplier to the semiconductor industry, but it was still primarily a materials handling company. The next phase would transform it into something far more comprehensive.

IV. Inflection Point #1: The Mykrolis Merger (2005)

The Deal That Changed Everything

In August 2005, Entegris merged with Mykrolis Corporation, a publicly held supplier of filtration products to the semiconductor industry. Mykrolis was spun-out of Millipore Corporation in 2000.

Entegris, of Chaska, Minnesota, and Mykrolis announced a definitive agreement to combine in a merger-of-equals transaction that creates a combined company valued at approximately $1.3 billion.

The companies closed their merger on August 6, 2005. Company officials say that the union of these two technology companies creates the world's largest materials integrity management company.

Entegris, formed by the 1999 merger of Fluoroware Inc. (founded in 1966 by the late Victor Wallestad) and Empak Inc., had been a public company listed on NASDAQ since July 2000. Mykrolis, formerly the microelectronics division of Millipore Corporation, separated from Millipore in March 2001 and was listed on the New York Stock Exchange in August 2001.

Strategic Rationale: Combining Handling with Purification

The logic of the merger was elegant. Entegris specialized in materials handling—the containers, carriers, and systems that protect and transport critical materials. Mykrolis specialized in filtration and purification—removing contaminants from the liquids and gases used in chip manufacturing.

Mykrolis was founded through Millipore Spin-Off in March 2001, bringing liquid and gas purification and contamination control expertise.

In August 2005, Entegris as we know it today was formed through the merger of Entegris, Inc. and Mykrolis Corporation, combining complementary capabilities in materials handling and microcontamination control.

The merger brings together two established enterprises that serve virtually every major player in the semiconductor industry and with products and services that have little overlap. Entegris, whose fiscal year 2004 sales related to consumables were about 60 percent of total sales, provides products and services used by the semiconductor, data storage, life science and fuel cell markets to protect and transport critical materials.

Creating a Platform Company

The merger represented a fundamental strategic shift. Before Mykrolis, Entegris was a component supplier—an important one, but a supplier of individual products. After Mykrolis, Entegris could position itself as a solutions provider, offering comprehensive contamination control across multiple stages of the manufacturing process.

The combined company will have combined trailing annual revenue in excess of $650 million, and combined trailing annual operating income of approximately $75 million. It will have a strong balance sheet, including approximately $284 million of cash and marketable securities.

The integration process following the merger proceeded smoothly, and the company raised its expected annualized cost savings from the merger to approximately $20 million from the original estimate of $15 million. The company expects these cost synergies to be fully in place by the middle of calendar year 2006.

The Mykrolis merger also brought critical personnel. Among them was Bertrand Loy, who had served as Mykrolis's Chief Financial Officer since 2001. He would go on to become the architect of Entegris's transformation over the next two decades.

V. The Bertrand Loy Era Begins & Strategic Expansion (2008-2013)

A New Kind of Leader

Bertrand Loy had been the Chief Operating Officer for Entegris since July 2008. Prior to that, he was the Chief Administrative Officer for Entegris from August 2005 to July 2008, and was the Chief Financial Officer of Mykrolis from January 2001 until the 2005 Merger with Entegris.

On November 1, 2012, Bertrand Loy was promoted to president and elected to the Entegris Board of Directors and assumed the position of chief executive officer effective November 27, 2012.

Loy brought a rare combination of skills to the CEO role. He holds a Master of Business Administration (MBA) from ESSEC Business School, one of the leading business schools in Europe. Additionally, Loy earned a Bachelor of Science degree in Business Administration from the University of Paris-Dauphine. His educational background includes a TGMP from Harvard Business School completed in 2004.

Having served as the Company's chief executive officer for over 12 years, Mr. Loy provides the Board with unique insight into the Company's strategic vision, customer expectations and operational management. Mr. Loy's past global experiences as an operations, finance and information technology executive based in Europe, Japan and the Americas provide him with a deep understanding of the Company's opportunities and risks across a broad range of functional areas and in international business.

Surviving the Financial Crisis

The 2008-2009 financial crisis hit the semiconductor industry particularly hard. End demand for electronics collapsed, and chip manufacturers slashed capital spending. For a company like Entegris, this meant managing through a sharp downturn while preserving the capabilities needed for recovery.

Loy's financial background proved invaluable during this period. Rather than cutting into muscle, Entegris maintained its R&D investments while managing costs carefully. The company emerged from the crisis with its technical capabilities intact.

Poco Graphite Acquisition

In August 2008, Entegris acquired Poco Graphite, Inc., a Decatur, Texas supplier of specialized graphite and silicon carbide products for use in semiconductor, EDM, glass bottling, biomedical, aerospace, and alternative energy applications.

This acquisition marked a departure from Entegris's traditional focus on polymer-based products. Graphite and silicon carbide materials are used in different applications within semiconductor manufacturing—particularly in high-temperature processes where polymers can't survive. The acquisition expanded Entegris's addressable market and demonstrated a willingness to venture beyond the company's historical comfort zone.

Building R&D Capabilities and Customer Intimacy

The years between the financial crisis and Loy's assumption of the CEO role were spent building the foundations for future growth. Entegris invested in R&D facilities, expanded its global footprint, and deepened relationships with leading chipmakers.

The company's strategy centered on what it called "customer intimacy"—working closely with fab engineers to understand their contamination challenges and co-developing solutions. This wasn't simply a sales technique; it was a product development methodology. The best new products came from understanding the problems customers would face in the next generation of manufacturing.

By 2012, when Loy formally took the CEO role, he had a clear vision for Entegris's future: grow the company aggressively through acquisition while deepening its position in the most critical processes at the leading edge of semiconductor manufacturing.

VI. Inflection Point #2: The ATMI Acquisition (2014)

The Deal

On April 30, 2014, Entegris acquired Danbury, Connecticut-based ATMI, a publicly held company providing critical materials and materials-handling solutions to the semiconductor industry, in a $1.1 billion transaction.

Entegris announced that the Boards of Directors of both companies had unanimously approved a definitive merger agreement under which Entegris would acquire ATMI for a total equity value of approximately $1.15 billion on a fully-diluted basis, or approximately $850 million net of cash acquired.

The price represents a premium of 26.3 percent to ATMI's closing price of $26.93 on February 3, 2014. The transaction was expected to yield approximately $30 million in annualized cost synergies.

The Strategic Shift from Handling to Materials Chemistry

The ATMI acquisition represented a pivotal strategic shift. ATMI wasn't just another materials handling company—it specialized in advanced deposition materials, specialty gases, and delivery systems. These are the exotic chemicals that get deposited onto wafers to create the actual circuit structures.

The combination brings together two key suppliers in the semiconductor industry to create a technology leader in advanced process materials, contamination control and wafer handling. By leveraging ATMI's market-leading critical products, global infrastructure and expertise in key processes, Entegris will have an even stronger platform to serve the demanding technology needs of the world's largest semiconductor makers and other electronics companies.

"Upon closing, approximately 80% of our product sales will be unit-driven and focused on the most rapidly growing and critical areas of the semiconductor fab," said Loy at the time.

This "unit-driven" focus is crucial to understanding Entegris's business model. Unlike capital equipment, which is purchased occasionally when fabs expand or upgrade, unit-driven products are consumed during manufacturing. Every wafer processed requires filters, chemicals, and gases. Every batch of chemicals requires purification. This creates recurring revenue that grows with wafer production volume—a more stable and predictable business than equipment sales.

Creating Scale

"The combined company, which employs 3,500 people worldwide, has pro forma 2013 revenues of more than $1 billion and adjusted EBITDA of approximately $248 million, adjusted for targeted annualized synergies."

The scale achieved through the ATMI acquisition mattered for several reasons. First, it gave Entegris the R&D resources to compete at the leading edge. Second, it provided the global footprint to serve customers wherever they manufactured. Third, it created the financial muscle to pursue further acquisitions.

Acquiring Mykrolis in 2005 and ATMI in 2014 were key steps in building a comprehensive portfolio covering multiple critical semiconductor manufacturing processes, moving beyond just handling solutions.

VII. The EUV & Advanced Node Revolution (2015-2020)

The EUV Inflection Point

Between 2015 and 2020, the semiconductor industry underwent its most significant technological transition in decades: the adoption of extreme ultraviolet (EUV) lithography. This transition would make contamination control even more critical—and more valuable.

The sustained pursuit of high density in semiconductors for both logic and memory applications has seen the rapid adoption of EUV lithography, and after decades of development, this technology has reached the majority as device manufacturers employ EUV for critical layer patterning at sub-7 nm nodes.

For advanced nodes at and below 7 nm, EUV lithography is an enabling technology for streamlining the patterning process. Reliable pattern making at such a fine scale requires ultraclean reticles.

Why does EUV change the contamination equation? The shorter wavelength of EUV light (13.5 nm versus 193 nm for previous-generation immersion lithography) means that smaller particles can interfere with the patterning process. A particle that was invisible to older lithography systems becomes a killer defect under EUV.

To maintain the scaling roadmap that EUV affords, innovation in defectivity mitigation strategies is critical. Entegris' expertise in materials science, contamination control, and defect-free delivery allows the company to partner on the most complex defect challenges facing the industry.

Celebrating 50 Years

By 2016, with approximately 3,500 employees worldwide and more than $1 billion in annual revenue, Entegris stands as one of the largest global, high-performance, specialty chemical companies serving the microelectronics industry.

"Our success has been built on strong corporate values and has centered around teamwork, innovation and dedication to excellence, which have allowed us to introduce a number of market-leading product platforms throughout the years. We could not have achieved this milestone without the support of our customers and suppliers, and the dedication of our employees."

Taiwan Investment

In December 2020, Entegris announced an investment of US$500 million, building a state-of-the-art facility in Taiwan. The project was expected to complete in three years in Kaohsiung Science Park.

According to Bertrand Loy, expanding the company's manufacturing capacity reflects the increased and growing demand for its products and services from leading global manufacturers of semiconductors in Taiwan and the broader Asia Pacific region. Based on IC Insights' Global Wafer Capacity report in 2020, nearly 22% of the global semiconductor wafer fab capacity is in Taiwan while the Asia region produces approximately 75% of all global semiconductors.

Industry observers believe Entegris' ramped-up investment in southern Taiwan is aimed primarily at better meeting the needs of its major client, the Taiwan Semiconductor Manufacturing Company (TSMC).

The Taiwan investment reflected a simple reality: to serve leading-edge customers, Entegris needed to be physically close to their fabs. TSMC's dominance of leading-edge manufacturing made proximity to Taiwan essential.

VIII. Inflection Point #3: The CMC Materials Mega-Merger (2021-2022)

The Deal

Entegris and CMC Materials announced a definitive merger agreement under which Entegris would acquire CMC Materials in a cash and stock transaction with an enterprise value of approximately $6.5 billion at announcement.

In July 2022, Entegris acquired another US semiconductor chemicals company, CMC Materials Inc, for $5.7 billion.

The total purchase price for the acquisition amounted to $5.7 billion, including $3.8 billion paid in cash to CMC shareholders, 12.9 million Entegris shares and approximately $900 million of debt retired and $200 million of acquired cash.

CMC Materials had approximately 2,200 employees globally.

Understanding CMC Materials

CMC, which until recently was known as Cabot Microelectronics, is the world's leading producer of chemical mechanical planarization (CMP) slurries, used to smooth the surfaces of circuit-laden silicon wafers between semiconductor chip fabrication steps. It has annual sales of about $1.2 billion.

CMC Materials itself had been an aggressive acquirer. In 2018, CMC purchased KMG Chemicals for $1.6 billion, taking it into the business of high-purity chemicals for cleaning wafers between fabrication steps.

The Strategic Rationale

In a presentation to stock analysts, Loy provided an example of how the two companies fit together. Entegris produces organometallic precursor chemicals that are deposited onto chip surfaces via chemical vapor deposition or atomic layer deposition, creating ultra-thin films. CMC supplies the slurries and polishing pads needed to smooth those films to be ultra-flat. Entegris comes back in the process with slurry containers and filtration devices as well as post-CMP cleaning chemicals, filters, and brushes.

Overall, Entegris will be the second-largest supplier of CMP consumables after DuPont, the leading pad supplier, and will have a 25% share of the global market.

The addition of CMC Materials' leading CMP slurries and pads provides Entegris' customers with an end-to-end suite of CMP solutions – which also include liquid filtration, post-CMP cleaning chemistries and brushes, CMP pad conditioners, chemical monitoring, and chemical packaging products – while enabling shorter development times for these solutions.

The Competitive Battle

Both CMC and Entegris have been aggressive acquirers of electronic materials businesses in recent years. The year before the CMC deal, Entegris had battled Merck KGaA to acquire another electronic materials maker, Versum Materials. Merck won that contest, purchasing Versum for about $6 billion.

Losing Versum may have been a blessing in disguise. It forced Entegris to find alternative paths to growth, ultimately leading to the CMC acquisition which was arguably a better strategic fit. CMC's CMP expertise complemented Entegris's existing capabilities more precisely than Versum's broader portfolio would have.

The 2022 acquisition of CMC Materials marked a major transformation, nearly doubling the company's size and establishing it as a more dominant player in advanced materials science, particularly in Chemical Mechanical Planarization (CMP).

IX. Integration, Divestitures & Debt Paydown (2023-2025)

Strategic Portfolio Streamlining

Following the CMC acquisition, Entegris faced two immediate priorities: integrating the acquired business and managing the debt taken on to complete the deal.

Entegris announced the closing of the sale of its Electronic Chemicals business to Fujifilm. Entegris sold the Electronic Chemicals business for $700 million in cash, subject to customary adjustments. The transaction was originally announced on May 10, 2023.

The Electronic Chemicals business was a part of the company's Advanced Planarization Solutions (APS) division and was acquired by Entegris with the acquisition of CMC Materials in July 2022. The sale of this business further streamlines Entegris' portfolio following the CMC Materials acquisition.

In 2022, Entegris' Electronic Chemicals business had pro-forma sales of approximately $360 million.

The decision to sell the Electronic Chemicals business revealed important strategic thinking. Not every business acquired through CMC was a strategic fit. The Electronic Chemicals business, while profitable, didn't offer the same differentiation as CMP slurries and pads. Selling it allowed Entegris to accelerate debt repayment while focusing resources on more strategic assets.

Debt Management

The CMC acquisition created a significant debt burden that required careful management.

At the end of Q1 2024, gross debt was approximately $4.3 billion, and net debt was approximately $3.9 billion. Gross leverage was 4.6 times and net leverage was 4.3 times. The company expected gross leverage to be below 4 times at the end of 2024.

The company successfully executed on its debt reduction targets. The focus on deleveraging reflects management's disciplined approach to capital allocation—grow through acquisition when opportunities arise, but return to a conservative balance sheet promptly.

CMP Success Validates the Strategy

The success of CMC-derived products validated the strategic logic of the acquisition. CMP products experienced strong growth, driven by cross-selling, innovation, and solution-selling strategies. The ability to offer customers an integrated CMP solution—from deposition materials through slurries to post-CMP cleaning—proved valuable.

X. The CHIPS Act & U.S. Reshoring

A New Chapter in American Manufacturing

The CHIPS and Science Act of 2022 allocated $280 billion in new funds to boost research and manufacturing of semiconductors in the United States. For Entegris, this represented a transformational opportunity to reshape its manufacturing footprint.

Entegris announced a preliminary agreement with the U.S. Department of Commerce for up to $75 million in funding from the federal CHIPS and Science Act. Entegris will put that money toward the construction of a $600 million manufacturing facility in Colorado Springs; it's a facility company leaders say will help the U.S. semiconductor supply chain rely less on facilities in foreign countries.

Entegris and the U.S. Department of Commerce entered into a definitive agreement providing for up to $77 million in funding under the CHIPS and Science Act.

The Colorado Springs Manufacturing Center of Excellence

On November 5, 2025, Entegris celebrated the grand opening of its new Colorado Springs Manufacturing Center of Excellence. The opening ceremony brought together leaders from across the semiconductor ecosystem, including key industry partners Samsung and Intel that have also committed to expanding their U.S. manufacturing footprint.

The 135,000-square-foot site increases the company's production capabilities for its most advanced products for filtration and purification, as well as semiconductor wafer carriers known as Front-Opening-Unified Pods (FOUPs) that are essential for chip purity and yield. The facility marks the return of Entegris' FOUP manufacturing to the U.S. for the first time in decades.

Entegris broke ground on the facility in 2023 and began initial commercial operations earlier this year. The Colorado Springs manufacturing facility expands Entegris' long-standing presence in Colorado, where it has operated for more than 30 years.

Construction and operation of the new facility has created several hundred direct and indirect jobs in the region, supported by up to $100 million in local and U.S. government incentives. Entegris is committed to helping build the local workforce by collaborating with the University of Colorado Colorado Springs, the School of Mines, and District 20 schools to provide scholarships, co-op programs, and career pathways for students in science and engineering fields.

Geopolitical Considerations

The Colorado Springs investment reflects broader geopolitical realities. The COVID-19 pandemic exposed supply chain vulnerabilities across the semiconductor industry. The pandemic years led to massive shortages of the critical — and usually foreign-sourced — computer chips. This led to backups in everything from cars to video games to healthcare devices.

The new facility will produce front opening unified pods, which are currently entirely produced abroad. The highly specialized containers secure semiconductor wafers while they are handled and transported during the manufacturing process. The internal transportation systems have helped customers such as Intel, TSMC, Micron and GlobalFoundries.

The move to reshore FOUP manufacturing reflects a strategic recognition that customers increasingly value supply chain resilience alongside price and quality.

XI. Business Model Deep Dive: How Entegris Makes Money

Segment Breakdown

Entegris operates across two primary business segments, each serving critical needs in semiconductor manufacturing.

The Materials Solutions (MS) segment provides materials-based solutions, such as chemical vapor and atomic layer deposition materials, chemical mechanical planarization slurries and pads, ion implantation specialty gases, formulated etch and clean materials, and other specialty materials.

The Advanced Purity Solutions (APS) segment offers filtration, purification, and contamination-control solutions for the semiconductor manufacturing processes, semiconductor ecosystem, and other high-technology industries.

Product Portfolio

Entegris products include: filtration products that purify gases, fluids, and the ambient fab environment; liquid systems and components that dispense, control, analyze, or transport process fluids; gas delivery systems that safely store and deliver toxic gases; specialty chemistries for deposition and cleaning at advanced nodes; and wafer carriers and shippers that protect semiconductor wafers from contamination and breakage.

The company seeks to help manufacturers increase their yields by improving contamination control in several key processes, including photolithography, wet etch and clean, chemical-mechanical planarization, thin-film deposition, bulk chemical processing, wafer and reticle handling and shipping, and testing, assembly and packaging.

Customer Base

Entegris serves a diverse customer base across the semiconductor value chain. This includes logic and memory semiconductor device manufacturers, semiconductor equipment makers, gas and chemical manufacturing companies, and wafer grower companies. The company also serves flat panel display equipment makers, hard disk drive manufacturers, and suppliers in the solar, life science, and aerospace industries.

Revenue Performance

In the year 2024, Entegris had annual revenue of $3.24B, down -8.02%. The decline reflected the impact of divestitures following the CMC acquisition and a challenging semiconductor market environment.

In Q4 2024, net sales (as reported) of $850 million increased 5% from the prior year. Adjusted net sales (excluding the impact of divestitures) increased 11% from prior year.

The divergence between reported and adjusted sales growth highlights the impact of portfolio optimization following the CMC acquisition. Excluding divestitures, the underlying business showed strong growth.

The Unit-Driven Model

Entegris offers investors a unique way to gain exposure to growing semiconductor demand – semiconductor consumables. Unlike other equipment manufacturers, 75% of Entegris' sales are unit-driven, with the remaining 25% coming from capex requirements.

This unit-driven model is the key to understanding Entegris's economics. When chip production increases, Entegris's revenue increases—regardless of whether fabs are making capital investments. This creates more predictable revenue than capital equipment companies experience, though still subject to the semiconductor cycle.

XII. Global Operations & Manufacturing Footprint

Geographic Presence

Entegris has manufacturing, customer service and/or research facilities in the United States, Canada, China, Germany, Israel, Japan, Malaysia, Singapore, South Korea, and Taiwan. The company's corporate headquarters are in Billerica, Massachusetts.

Key U.S. manufacturing and R&D sites include Chaska, Minnesota (the historical home of Fluoroware); Chandler, Arizona; Fremont, California; and the newly opened Colorado Springs, Colorado facility. These U.S. locations are strategically positioned near major semiconductor clusters.

Taiwan Investments

Entegris has opened a new facility in Southern Taiwan's Kaohsiung Science Park to support manufacturing the most advanced semiconductors and increase production capabilities for advanced liquid filters, high-purity drums, and advanced deposition materials. Entegris plans to invest approximately $500 million in the 54,000 square-meter facility.

All of Entegris' divisions are now combined in the Kaohsiung Science Park. This creates a locally integrated supply chain that addresses the geographic gaps between the company and some of its most important partners.

Entegris has nearly 720 full-time employees in Taiwan and expects to add several hundred more over the next few years as the new facility becomes fully operational.

The Kaohsiung facility represents Entegris's largest manufacturing site globally—a testament to the importance of Taiwan in the semiconductor supply chain and TSMC's dominant role in leading-edge manufacturing.

XIII. Leadership Transition & Future Strategy

The End of the Loy Era

Entegris announced that Bertrand Loy will retire as President and Chief Executive Officer after 13 years in those roles, effective August 18, 2025. David Reeder will succeed Mr. Loy as President and CEO at that time.

Mr. Loy will serve as Executive Chair of the Board through the end of the second quarter of 2026 to facilitate a smooth transition.

"Bertrand's vision and leadership have shaped Entegris into the global industry leader it is today," said James F. Gentilcore, Lead Independent Director. "Under his leadership and through a rapidly evolving technological and geopolitical landscape, Entegris' revenue and market capitalization grew nearly five times and over 10 times, respectively."

Since Loy became CEO in 2012, Entegris' revenue increased over 200% and profits grew nearly 500%.

David Reeder Takes the Helm

David Reeder became president and CEO of Entegris in August 2025, having served as a member of the board of directors since March 2024. With more than 20 years of executive leadership experience, including in the semiconductor industry across IDMs, fabless, foundry, systems, and component companies, David brings a unique combination of financial and operational leadership experience to Entegris.

Mr. Reeder brings to his new role a unique combination of financial and operational leadership experience with large public companies, including extensive semiconductor industry expertise. He most recently served as CFO of Chewy Inc., and previously in leadership roles at global semiconductor companies, including as CFO of GlobalFoundries.

Reeder's background as CFO of GlobalFoundries is particularly relevant—he understands the customer perspective, having worked for one of the world's largest chip foundries. This customer intimacy may prove valuable as Entegris continues to deepen relationships with leading-edge manufacturers.

XIV. Competitive Positioning & Investment Analysis

Competitive Landscape

Entegris operates in a fragmented competitive landscape where different companies specialize in different product categories.

In 2024, DuPont maintained its position as the leader in the semiconductor consumables market, generating an estimated $2.85 billion in revenue. This strong performance reflects its dominance in critical segments such as CMP pads, photolithography materials, and advanced cleaning solutions.

For the slurry segment, Fujifilm Electronic Materials currently holds the highest share of the market at 31% due to their strong position in Cu slurry. Entegris is ranked second in market share, largely due to their acquisitions of Sinmat, Chemetall Precision Microchemicals (was BASF) and CMC. For the pad segment, DuPont continues to be the dominant supplier, representing over 50% of the market.

Pall, a Danaher company, competes in liquid filtration; Versum Materials, a Merck company, competes in deposition materials and gases; DuPont competes on advanced cleans and chemical slurries. Under a conglomerate, business segments that are not the focal point of the business run the risk of being underinvested in. Entegris is solely focused on semiconductors, with all R&D spending going directly towards innovative new solutions in this industry.

Porter's Five Forces Analysis

Threat of New Entrants: Low. Entegris benefits from high barriers to entry. The semiconductor industry requires extensive process qualification—once a supplier's products are validated in a customer's manufacturing process, switching is expensive and risky. New entrants would need decades of accumulated know-how and substantial R&D investment.

Bargaining Power of Suppliers: Moderate. Entegris sources specialty chemicals and raw materials from various suppliers. While no single supplier dominates, certain specialty materials have limited sources.

Bargaining Power of Buyers: Moderate. Customers are sophisticated, large corporations (Intel, TSMC, Samsung) with significant purchasing power. However, contamination control products are mission-critical and represent a small portion of total fab costs, limiting price sensitivity.

Threat of Substitutes: Low. There are no viable substitutes for contamination control in semiconductor manufacturing. The laws of physics require purity levels that only advanced filtration and handling systems can provide.

Competitive Rivalry: High. Competition is intense in most product categories. However, Entegris's breadth of portfolio and focus on the most advanced nodes provides differentiation.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Entegris benefits from manufacturing scale, particularly following acquisitions. Larger production volumes reduce unit costs for filters, chemicals, and containers.

Network Effects: Limited. Unlike platforms, Entegris's products don't become more valuable as more customers use them.

Counter-Positioning: Entegris's pure-play focus on semiconductors represents counter-positioning versus diversified competitors like DuPont and Danaher who must allocate capital across multiple businesses.

Switching Costs: High. Process qualification creates significant switching costs. Once a filter or chemical is validated in a manufacturing process, changing suppliers risks yield loss.

Cornered Resource: Entegris has accumulated proprietary know-how in contamination control that is difficult to replicate. Decades of working with leading chipmakers on their most challenging problems has built institutional knowledge.

Process Power: The company's ability to develop solutions for next-generation manufacturing processes—before customers fully understand their needs—demonstrates process power.

Branding: Limited importance in B2B semiconductor materials.

Bull Case

The bull case for Entegris rests on several pillars:

-

Secular growth in semiconductor complexity. As nodes shrink and chip architectures become more complex, contamination control becomes more critical and more valuable.

-

EUV and beyond. Each lithography transition increases filtration and purity requirements, expanding Entegris's addressable market.

-

Unit-driven revenue model. Growing wafer production drives Entegris revenue regardless of capital spending cycles.

-

Geographic expansion. Investments in Taiwan, Colorado Springs, and other locations position Entegris to benefit from semiconductor supply chain reshoring.

-

Integration success. Successful integration of CMC Materials could unlock revenue synergies beyond initial targets.

Bear Case

The bear case centers on:

-

Cyclicality. Despite the unit-driven model, Entegris remains exposed to semiconductor cycles.

-

Leverage. The CMC acquisition increased debt substantially, though the company has made progress on deleveraging.

-

Geopolitical risk. Heavy exposure to Taiwan creates concentration risk in a volatile geopolitical environment.

-

Competition. DuPont's electronics spin-off could create a more focused competitor.

-

Technology disruption. Future manufacturing approaches could require different contamination control methods.

XV. Key Performance Indicators

For investors tracking Entegris's ongoing performance, two metrics deserve primary attention:

1. Adjusted Revenue Growth (Excluding Divestitures): This shows underlying business momentum by removing noise from portfolio changes. Adjusted net sales (excluding the impact of divestitures) increased 11% from prior year in Q4 2024—a more meaningful indicator than reported revenue growth.

2. Net Leverage Ratio: Given the significant debt from the CMC acquisition, the pace of deleveraging signals management discipline and free cash flow generation. The company's progress toward sub-4x leverage demonstrates execution capability.

XVI. Conclusion

Entegris's journey from a small plastic container maker in Minnesota to the world's largest pure-play semiconductor materials company encapsulates the history of the semiconductor industry itself. Every inflection point—the transition to 300mm wafers, the adoption of EUV lithography, the rise of advanced packaging—has created new contamination challenges that Entegris has been positioned to solve.

Better contamination control can significantly improve yield, and a one percent yield improvement can mean up to $150 million per year in net profit. This simple economic reality explains why chipmakers pay careful attention to their materials suppliers and why those suppliers command solid margins.

The CMC acquisition transformed Entegris from a leading contamination control company into a comprehensive electronic materials provider. The Colorado Springs facility positions the company for the reshoring of semiconductor supply chains. The leadership transition to David Reeder brings fresh perspective while preserving institutional continuity.

Between now and 2030, the semiconductor industry is anticipated to double to $1 trillion, fueled by leading-edge technology to support the ever-growing needs of the data economy with advanced manufacturing. If that forecast proves accurate, Entegris stands to benefit handsomely as the invisible backbone enabling that growth.

The company Bertrand Loy built over 13 years is far larger, more diversified, and more technologically sophisticated than the Entegris he inherited. Whether David Reeder can continue that trajectory—and navigate the geopolitical complexities that now overlay the semiconductor industry—will determine whether Entegris becomes not just an essential supplier but a dominant one.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube