Kimberly-Clark: From Paper Mills to Consumer Products Empire

I. Introduction & Episode Teaser

Picture this: It's 1971, and a mild-mannered corporate lawyer with thick glasses and zero CEO experience walks into the boardroom of Kimberly-Clark. The company's stock has dropped 36% over two decades. Traditional paper mills are bleeding cash. Board members are skeptical—this man "lacks the qualifications" to lead. Two months later, that same lawyer, Darwin Smith, is diagnosed with nose and throat cancer. Doctors give him less than a year to live.

Twenty years later, Smith would retire having delivered returns of 4.1 times the general market, transforming a dying paper company into one of the world's most powerful consumer products empires. Jim Collins would later call it "one of the best examples in the 20th century of taking a good company and making it great."

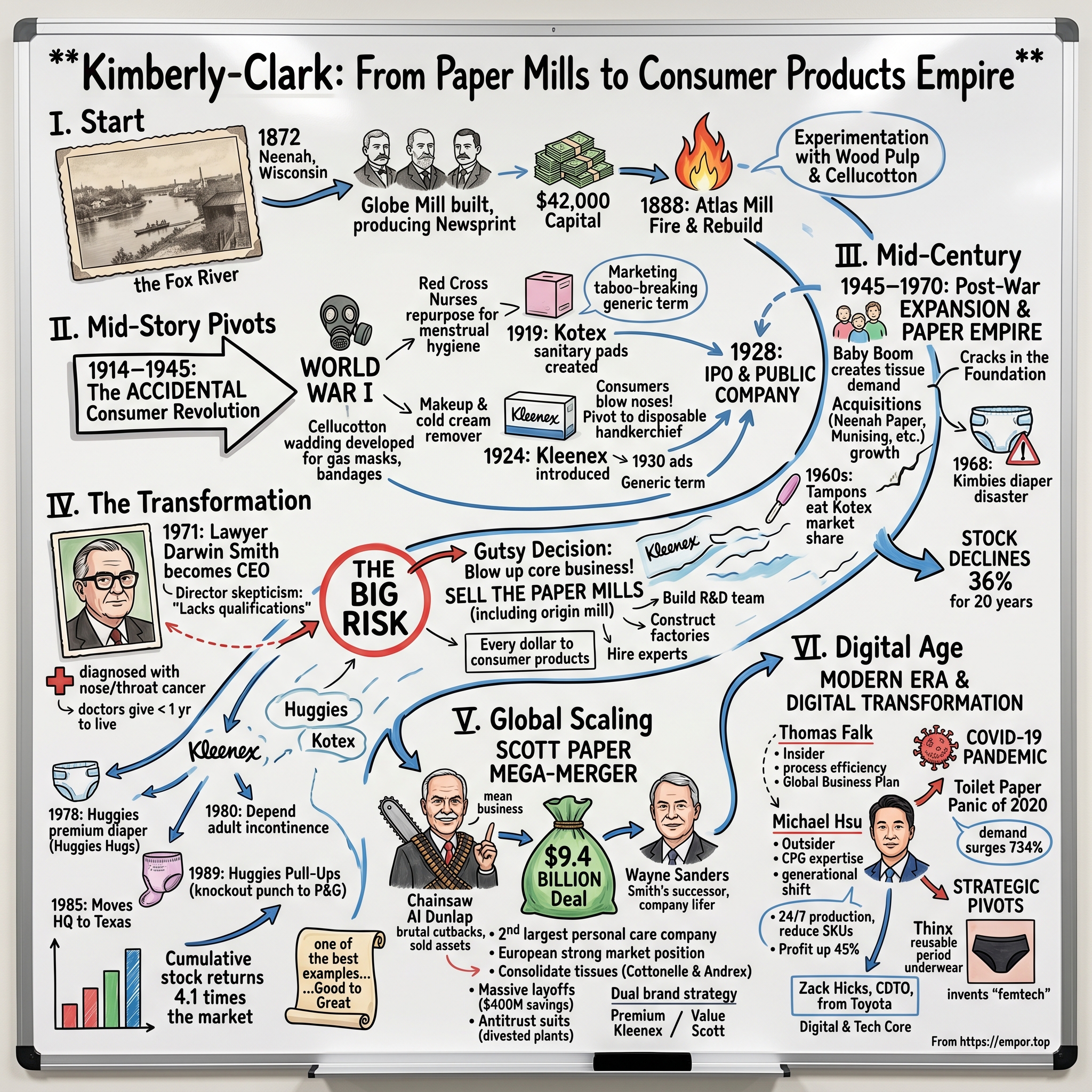

Founded in 1872 with just $42,000 of capital scraped together by four entrepreneurs in Neenah, Wisconsin, Kimberly-Clark today generates over $20 billion in annual revenue. Its brands—Kleenex, Huggies, Kotex, Scott, Pull-Ups—have become so ubiquitous that several have transcended trademark to become the generic terms for their categories. When you ask for a Kleenex, you're not asking for a brand; you're asking for the thing itself.

The central question that drives this story: How did a Wisconsin paper mill, founded to make newsprint from cotton rags, become the tissue and personal care giant that would challenge Procter & Gamble's century-long dominance? The answer involves accidental innovations born from war, a CEO who sold the company's original business entirely, and a series of strategic pivots that would make any Silicon Valley founder envious.

This is a story about transformation—not the buzzword kind that consultants sell, but the real kind where you literally blow up your core business and rebuild from scratch. It's about leaders who saw around corners, products that emerged from military necessity to become household staples, and the audacity to compete with companies ten times your size.

What makes Kimberly-Clark particularly fascinating is that unlike tech disruption stories where the old guard gets displaced by nimble startups, this is a story of self-disruption—a 150-year-old company that repeatedly killed its past to secure its future. From paper mills to feminine care, from industrial products to baby diapers, each transformation required not just strategic vision but the institutional courage to abandon what made you successful.

As we'll see, the company's history reads like a series of unlikely pivots: cellulose wadding developed for World War I gas masks becomes Kotex sanitary pads. A failed cold cream tissue becomes Kleenex. A diaper disaster in the 1970s leads to market dominance a decade later. Each setback contained the seeds of the next breakthrough.

II. The Paper Mill Origins (1872–1920)

The Fox River Valley in Wisconsin, 1872. Four men gather around a table in Neenah, a small town whose main claim to fame is water—specifically, the powerful currents of the Fox River that could turn mill wheels. John A. Kimberly, a wholesale grocer with entrepreneurial ambitions, has convinced three partners to pool their resources: Havilah Babcock, Charles B. Clark, and Franklyn C. Shattuck. Together they scrape together $42,000 in capital—roughly $1 million in today's dollars—to build the Globe Mill.

Their timing couldn't have been worse. The Panic of 1873 would strike within a year, triggering a six-year depression that would destroy thousands of businesses. But these four men had picked the right product for the wrong time: newsprint made from linen and cotton rags. As America urbanized and literacy rates soared, newspapers were exploding in circulation. The Wisconsin frontier offered something California's gold rush couldn't: renewable resources and waterpower.

John Kimberly emerged as the driving force—a man who would serve as president until his death at age 90, still showing up to the office daily. His management philosophy was simple but radical for the era: treat workers fairly, invest aggressively in technology, and always look for the next innovation. When other mills ran single shifts, Kimberly ran around the clock. When competitors stuck with traditional rag paper, he experimented with wood pulp.

The 1888 Atlas mill fire should have ended everything. The company's newest and largest facility burned to the ground, taking with it much of their production capacity and capital investment. Insurance covered only a fraction of the losses. Most partners wanted out. But Kimberly saw opportunity in disaster—within five months, they had rebuilt the mill with 50% greater capacity than before, incorporating every modern innovation they couldn't afford to retrofit into the old building.

This Phoenix-like recovery became part of company lore, but it also established a pattern: Kimberly-Clark would repeatedly bet everything on transformation. The rebuilt Atlas mill didn't just make paper; it made better paper. By the 1890s, they were producing specialized papers for rotogravure printing—a technology that allowed newspapers to print photographs with unprecedented clarity.

The town of The Cedars recognized John Kimberly's impact by renaming itself Kimberly in 1889. It wasn't just honorary—Kimberly had essentially built the town's economy, providing stable jobs and investing in local infrastructure. This symbiotic relationship between company and community would define Kimberly-Clark's culture for the next century.

By 1906, the company was experimenting with something revolutionary: creped cellulose wadding. The material was five times more absorbent than cotton, softer, and could be mass-produced from wood pulp. They called it Cellucotton, and while they didn't know it yet, this innovation would completely transform their business. Initially marketed for industrial uses—gas mask filters, bandages—it seemed like just another specialty paper product.

The company went public in 1928 as Kimberly-Clark Corporation, capitalizing on the Roaring Twenties stock market boom. John Kimberly, now in his eighties, rang the opening bell himself. The IPO raised capital for expansion but more importantly, it forced the company to professionalize—implementing modern accounting, establishing clear governance, and thinking beyond the Fox River Valley.

When John Kimberly died in 1928, still serving as president, he left behind more than a paper company. He had built an innovation engine, a culture of experimentation, and most importantly, a willingness to cannibalize existing products for better ones. The paper mill had grown from four men and $42,000 to a public corporation with thousands of employees and millions in revenue.

But paper was becoming a commodity business. Margins were shrinking. Competition was fierce. The company needed something new—and they were about to find it in the most unlikely place: the battlefields of World War I.

III. The Accidental Consumer Products Revolution (1914–1945)

The Great War was raging across Europe in 1914. Cotton, that essential material for bandages and surgical dressings, was becoming scarce and expensive. In a laboratory in Neenah, Wisconsin, far from the trenches, Kimberly-Clark researchers working with bagasse—a pulp byproduct of processed sugar cane—created something revolutionary: creped cellulose wadding that was five times more absorbent than cotton and cost half as much to produce. They called it Cellucotton.

Ernst Mahler, the company's chief chemist hired in April 1914, championed the material and even traveled to Washington D.C. to convince the U.S. government it could be used as wound dressing. The timing was perfect. By January 1918, Kimberly-Clark was producing nine tons of Cellucotton; by October, with orders from the Army and Red Cross, production had exploded to 138 tons per month.

Here's where the story takes its unexpected turn. Red Cross nurses in field hospitals discovered that Cellucotton worked exceptionally well as makeshift sanitary pads. Word of this unauthorized use filtered back to company headquarters, where it might have been dismissed as irrelevant. Instead, it sparked one of the most important strategic pivots in American business history.

Kimberly-Clark made no profits from selling Cellucotton to the U.S. military during the war—a patriotic gesture that cost them dearly. When the armistice came in November 1918, the Army and Red Cross canceled orders for about 750 tons of Cellucotton. The company faced a crisis: massive production capacity with no customer.

In 1919, they hired Walter Luecke from Sears, Roebuck with a singular mission: find new uses for Cellucotton. Having learned about the nurses' improvisation, he and the company's chemists convinced management to pursue the "feminine products" market. The obstacles were immense. Manufacturing partners refused to produce sanitary napkins, arguing they were "too personal and could never be advertised".

Undeterred, Kimberly-Clark decided to manufacture the product themselves. In October 1919, the first box of Kotex—short for "cotton texture"—was sold at a Woolworth's department store in Chicago in what might have been an embarrassing interaction between a male store clerk and a female customer. The price: 60 cents for a 12-pack.

The marketing challenge was unlike anything American business had faced. How do you advertise a product that society refuses to acknowledge exists? Kimberly-Clark created a separate sales company, International Cellucotton Products, to distance the parent company from these "unmentionable" products. They pioneered discrete purchasing methods—silent sales where women could take a box and leave money without interaction, and later, vending machines in women's restrooms.

Marketing legend Albert Lasker, representing Kotex, visited Edward Bok, editor of the Ladies Home Journal in 1921. The magazine initially refused to accept advertising, until Ladies Home Journal finally agreed, breaking a taboo that had kept feminine hygiene in the shadows. The ads were revolutionary in their subtle directness—they never mentioned menstruation but everyone understood.

Just as Kotex was gaining traction, the company stumbled onto another accidental innovation. In 1924, Kimberly-Clark introduced Kleenex as a disposable makeup and cold-cream remover. The name cleverly borrowed from Kotex—the "K" sound and "ex" ending creating brand synergy. But consumers had other ideas.

Women started complaining that their husbands were blowing their noses in their Kleenex. A survey revealed consumers preferred using it as a disposable handkerchief. Rather than fight this unexpected use case, Kimberly-Clark pivoted entirely. Nationwide advertisements promoting Kleenex as a handkerchief replacement began in 1930, and sales doubled within a year.

The genius of this pivot cannot be overstated. In an era when handkerchiefs were washed and reused—often spreading germs—Kleenex offered a hygienic, disposable alternative. The marketing emphasized health: "Don't put a cold in your pocket!" The product became so successful that "Kleenex" transcended brand to become the generic term for facial tissue.

The company contracted Margaret Buell, creator of the cartoon strip "Little Lulu," to promote Kleenex. Little Lulu would appear in Kleenex ads well into the 1960s, making the brand friendly and approachable to families. This was sophisticated brand building—using a beloved character to normalize a product category that hadn't existed a decade earlier.

The international expansion began early. During the 1920s, the company built the Spruce Falls Power and Paper Company in Kapuskasing, Ontario, and in 1925 formed what would become Canadian Cellucotton Products Limited for marketing cellucotton products internationally. This wasn't just about sales—it was about securing raw materials and production capacity for what they correctly anticipated would be explosive growth.

By the 1930s, Kimberly-Clark faced a paradox. Kotex held a market share of 50% or more for decades and was for most women synonymous with sanitary napkins. Kleenex was becoming equally dominant. Yet the bulk of the company's revenues (but not always profits) continued to come from making commodity papers. The consumer products were more profitable but still viewed internally as side businesses.

World War II changed the equation again. Kimberly-Clark directly developed camouflage paper, decontamination suits, waterproof shipping containers, and disposable bad weather clothing, while serving as a subcontractor for piston rings, gun sight assemblies, and bomb dies. With more women working in factories, Kotex pads were sold in vending machines, greatly improving visibility.

This period from 1914 to 1945 established a pattern that would define Kimberly-Clark: accidental innovation leading to category creation. Cellucotton wasn't designed for feminine hygiene or facial tissue—yet these applications transformed a paper company into a consumer products innovator. The company had learned to listen to unexpected use cases, to pivot when consumers showed them a better way, and most importantly, to have the courage to enter entirely new markets.

The foundation was set for an even more dramatic transformation. The tissue empire had been built almost by accident, but what came next would be entirely deliberate.

IV. Post-War Expansion & The Paper Empire (1945–1970)

America in 1945 emerged from war victorious but transformed. Millions of GIs returned home, married, and began families in what would become the Baby Boom. Suburbs sprawled outward from cities. Consumer spending exploded. For Kimberly-Clark, this meant unprecedented demand for its tissue products—but also intense competition from giants like Scott Paper and new challenges managing a sprawling paper empire.

After the war, Kimberly-Clark initiated a growth program to handle revived consumer product demand. Facilities were built or acquired in Balfour, North Carolina, and Memphis, Tennessee, in 1946, and in Fullerton, California, and New Milford, Connecticut, in the late 1950s. Pulp production at Terrace Bay, Ontario, was launched in 1948, and in 1949 the company, along with a group of investors and newspaper publishers, began the large Coosa River Newsprint Company in Coosa Pines, Alabama.

The acquisition spree accelerated through the 1950s. Kimberly-Clark acquired the Michigan-based Munising Paper Company in 1952, Neenah Paper Company in 1956, Peter J. Schweitzer, Inc.--which had mills in France and the United States--in 1957, and the American Envelope Company in 1959. International Cellucotton Products Company formally merged with its parent company in 1955, as did Coosa River Newsprint Company in 1962.

This was empire building on a massive scale. Peter J. Schweitzer alone brought mills in France, giving Kimberly-Clark its first European manufacturing footprint. The Neenah Paper Company acquisition was particularly symbolic—the company was buying its hometown competitor, consolidating the Fox River Valley paper industry under one roof.

The firm expanded internationally during the 1950s, opening plants in Mexico, West Germany and the United Kingdom. It began operations in 17 more foreign locations in the 1960s. Each new market required not just capital investment but cultural adaptation—learning how to sell intimate products in countries with different attitudes toward hygiene and women's health.

Yet even as the company grew globally, cracks were appearing in the foundation. Through the next thirty years, into the late 1960s, Kimberly-Clark tried to be both a major book and other paper producer in commodity markets, as well as the makers of Kotex and Kleenex for the public. Still the paper industry remained largely a commodity business, subject to price wars and swings from undercapacity to overcapacity when new paper mills were built.

The schizophrenia was evident in capital allocation. Despite leaving the highly competitive newsprint business in 1916, Kimberly-Clark later re-entered the business, partnering in an Alabama mill with Southern newspaper publishers and another massive operation in Canada, a joint venture with The New York Times. These mills required huge capital investments, new machines and technologies, acquisitions of timberlands, and plenty of management attention. While product improvements were made in Kotex and Kleenex, those product lines often received less attention and less research and development money.

Meanwhile, consumer products faced new threats. Throughout the 1960s the tampon, first manufactured by Tampax, gained favor among women and ate into Kotex's market share. The tampon was a classic disruptive innovation—initially inferior in many ways but offering convenience that pads couldn't match. Kimberly-Clark's response revealed the dangers of divided attention.

Enter the Kimbies disaster—a cautionary tale of what happens when a company rushes into a market without proper preparation. In 1968 the company introduced Kimbies, a disposable diaper with tape closures. Initial sales were strong despite competition from Procter & Gamble's Pampers.

The initial optimism was warranted. The disposable diaper market was exploding—working mothers needed convenience, and cloth diapers were labor-intensive. Procter & Gamble's Pampers had proven the concept. Kimberly-Clark had the distribution, the brand trust, and the manufacturing expertise. What could go wrong?

Everything, as it turned out. While K-C tended to its diverse operations, however, it failed to keep up with early disposable diaper improvements and market innovations. As a result of continued poor sales and leakage problems, Kimbies were withdrawn from the market in the mid-1970s.

The Kimbies failure was more than a product setback—it was an existential crisis. Procter & Gamble, with its singular focus on consumer products and legendary marketing prowess, was eating Kimberly-Clark's lunch. The message was clear: you couldn't compete with P&G while half your management attention was focused on commodity paper mills.

Little Lulu continued promoting Kleenex into the 1960s, but even this success story couldn't mask the fundamental problem. Despite the company's growth and success, it was dwarfed by industry giant International Paper, formed during the trust era of the 1890s. At its 1898 founding by merging seventeen papermakers, "IP" made 60% of the newsprint in America, while newspaper readership and circulation were skyrocketing. The company had twenty-five times the capital of Kimberly-Clark.

By 1970, Kimberly-Clark was stuck between two worlds. In commodity paper, it was a minnow swimming with whales like International Paper and Weyerhaeuser. In consumer products, it was being outmaneuvered by focused competitors like P&G. The stock market rendered its verdict: shares had declined 36% over twenty years, even as the broader market soared.

The company needed more than new products or better marketing. It needed a complete transformation—someone willing to blow up a century of tradition and start over. That someone was about to walk through the door, though nobody would have predicted it from his resume.

V. The Darwin Smith Transformation (1971–1991)

The Neenah boardroom, January 1971. Darwin E. Smith walks in—not with the swagger of a newly appointed CEO, but with the tentative steps of a man who wasn't sure he belonged. The company's mild-mannered in-house lawyer, thick glasses perched on his nose, had just been named chief executive of a stodgy old paper company whose stock had fallen 36% behind the general market over the previous twenty years. A director pulled him aside after the meeting: "You know you lack some of the qualifications for this position."

Smith, the company's mildmannered in-house lawyer, wasn't so sure the board had made the right choice—a feeling further reinforced when a director pulled Smith aside and reminded him that he lacked some of the qualifications for the position.

Smith's background hardly screamed "transformational CEO." Smith grew up on an Indiana farm and put himself through night school at Indiana University by working the day shift at International Harvester. One day, he lost a finger on the job. The story goes that he went to class that evening and returned to work the very next day. After graduating with honors from Indiana University in 1950 and Harvard Law School cum laude in 1955, he'd joined Kimberly-Clark's legal department in 1958 at a salary of $15,000 a year, intending to stay only long enough to gain corporate experience.

Two months after becoming CEO, the universe delivered another blow. Later in life, two months after becoming CEO, doctors diagnosed Smith with nose and throat cancer, predicting he had less than a year to live. He informed the board but made it clear that he was not dead yet and had no plans to die anytime soon. Smith held fully to his demanding work schedule while commuting weekly from Wisconsin to Houston for radiation therapy and lived twenty-five more years, most of them as CEO.

A Wall Street Journal reporter once asked Smith to describe his management style. After a long, uncomfortable silence, he replied with one word: "Eccentric." He spent vacations on his Wisconsin farm operating a backhoe, digging holes and moving rocks. His favorite companions were plumbers and electricians. This was not the celebrity CEO archetype—this was something entirely different.

But beneath the humble exterior burned fierce resolve. Smith and his leadership team spent months analyzing Kimberly-Clark's position. Their conclusion was brutal: The value of its stock had fallen by some 40% over the previous twenty years as its principal business—the production of coated paper—had become an enterprise with low margins. Smith concluded that coated paper as a business was in inexorable decline, whereas consumer paper-products, though highly competitive, was on the upswing.

The strategic insight was simple but terrifying: If Kimberly-Clark were to go toe-to-toe with world-class competitors like Procter & Gamble, it would force the company to achieve greatness or perish. There was no middle ground.

"We're going to sell the mills." The decision had grown out of one of Smith's dialogues in which a fellow executive noted that Kleenex, a sideline product, had become a brand synonymous with its category, like Coke or Band-Aid. In what a Kimberly-Clark director called the "gutsiest decision I've ever seen a CEO make," Smith jettisoned 100 years of corporate history, right down to the original mill in Kimberly, Wis.

Within one year of taking control of the company, Smith initiated changes that included the sale or closure of six paper mills and the sale of more than 300,000 acres of prime northern California land. With cash reserves of more than $250 million, primarily from the land sale, Smith then inaugurated an aggressive research campaign.

The reaction was savage. Analysts derided the loss of revenue. The stock took a hit. Forbes predicted disaster. Wall Street called it "stupid." The business media excoriated him. How could a mediocre paper company take on Procter & Gamble, a company with marketing in its DNA?

Coming home from work during this particularly difficult period, Smith told his wife: "If you have a cancer in your arm, you've got to have the guts to cut off your arm." It was an apt metaphor from a man who'd beaten his own cancer diagnosis.

Smith's transformation strategy had three pillars. First, talent acquisition: He assembled a talented research and development team by hiring specialists away from competitors. Second, marketing investment: The company's advertising budget was increased substantially, and plans were made for the construction of additional production facilities. Third, complete commitment: every dollar from the mill sales went into consumer products.

The redemption of the Kimbies failure came with Huggies. A new premium-priced diaper in an hourglass shape with refastenable tapes was introduced in 1978 under the name Huggies. By 1984, Huggies had captured 50 percent of the higher quality disposable diaper market. The sudden popularity caught even Kimberly-Clark by surprise, forcing rapid production expansion.

The diaper wars with P&G turned vicious. Just before this move Kimberly-Clark was sued by Procter & Gamble, who claimed that Kimberly-Clark had unlawfully infringed on its patented disposable diaper waistband material. Huggies had increased its market share to 31 percent, upsetting Procter & Gamble's Pampers. After nearly two years of litigation, a federal grand jury ruled against Procter & Gamble.

The knockout punch came in 1989: Kimberly-Clark enjoyed further successes in its ongoing diaper rivalry with Procter & Gamble later in the decade when it introduced the extremely popular Huggies Pull-Ups disposable training pants in 1989. This product extension helped Kimberly-Clark trim Procter & Gamble's market share lead, as well as propel Huggies into the number one position in the disposable diaper market.

Smith also launched Depend adult incontinence products in 1980 through aggressive television advertising—another taboo broken, another market created. Just as Kotex had addressed feminine hygiene decades earlier, Depend tackled adult incontinence head-on. The company now had products spanning "cradle to grave."

One of Smith's most unusual moves was creating an airline. With six planes in 1969, Smith, then an executive vice-president for finance, suggested that company air travel be converted from a "cost center into a profit center" by offering corporate aircraft maintenance services. K-C Aviation, as the subsidiary was called, later remodeled three DC-9s and in June 1984 initiated flight service between Appleton and Milwaukee, Wisconsin; Boston; and Dallas, Texas.

The airline, Midwest Express, had a rocky start with a 1985 crash and large operating losses. By 1989, however, the operation was in the black, with planes at 66 percent capacity; a $120 million expansion increased the number of destinations to 15 cities and the airline boasted a fleet of 11 DC-9s. The company later sold its stake for over $40 million in profit.

In 1985, Smith relocated Kimberly-Clark's headquarters from Wisconsin to Irving, Texas, citing the state's better business climate. It was another break with tradition—leaving the Fox River Valley that had nurtured the company for over a century.

European expansion accelerated under Smith's leadership. From that year to 1992, the company invested nearly $1 billion in European plants. The investments initially hurt profits—net income fell from $435.2 million in 1991 to $150.1 million in 1992—but laid the foundation for global dominance.

The numbers tell the story: Under his stewardship, Kimberly-Clark generated cumulative stock returns 4.1 times the general market, handily beating its direct rivals Scott Paper and Procter & Gamble and outperforming such venerable companies as Coca-Cola, Hewlett-Packard, 3M, and General Electric.

When Smith retired in 1991 after twenty years as CEO, Kimberly-Clark became the leading company in the consumer paper industry, eventually beating Procter & Gamble in six of eight product categories and owning outright its previous main competitor, Scott Paper. Smith had transformed a dying industrial giant into the number one paper-based consumer products company in the world.

Jim Collins would later write that Smith's transformation was "one of the best examples in the 20th century of taking a good company and making it great." Collins rated Smith among the ten greatest CEOs of all time, calling him a "Level 5 leader"—someone who blends extreme personal humility with intense professional will.

Smith died of a heart attack in 1995, four years after retiring. He never sought the spotlight, never wrote a memoir, never became a business celebrity. But his legacy was undeniable: he had taken a dying paper company and transformed it into a consumer products powerhouse that could go toe-to-toe with anyone.

The transformation wasn't complete—commodity paper operations still existed. But Smith had irreversibly changed Kimberly-Clark's trajectory. The company that entered 1971 bleeding cash and losing to competitors emerged from 1991 as an industry leader. It was, as Smith might say in his understated way, "adequate."

VI. The Scott Paper Mega-Merger (1992–1996)

Philadelphia, April 1994. Albert J. Dunlap walked into the executive suite of Scott Paper Company like a gunslinger entering a saloon. The company was hemorrhaging money, its stock price in free fall, morale destroyed. Scott, founded in 1879 and credited as being the first to market toilet paper sold on a roll, was dying. The board had brought in Dunlap for one reason: to perform radical surgery.

The value of Scott stock has increased 135 percent since Dunlap, in his eighth rescue project, took over in April 1994 as the company's first outsider CEO in 115 years. His methods were brutal but effective. He cut 11,200 jobs, sold $2.4 billion in assets and disposed of a lavish corporate headquarters in Philadelphia in favor of leased quarters in Boca Raton, Fla.

They called him "Chainsaw Al" and "Rambo in Pinstripes"—the latter after he posed for a photo wearing an ammo belt across his chest. Dunlap embraced the nicknames. Where Darwin Smith had been quiet and eccentric, Dunlap was loud and theatrical. Smith sold mills to transform a company; Dunlap sold everything that wasn't nailed down to pump up the stock price.

He said he had turned Scott from "a stodgy old paper company that had lost its way, that was virtually comatose" into a "fast-moving consumer products company." In fifteen months, Dunlap had performed what looked like a miracle turnaround. Now he needed an exit—and Wayne Sanders, Smith's successor at Kimberly-Clark, was about to give him one.

Sanders had taken over as CEO in 1992 after Smith's retirement. Unlike Smith's unlikely path from legal department to corner office, Sanders was a company lifer who had worked his way up through operations. He had spearheaded the risky development of Huggies Pull-Ups as an executive. He understood consumer products, but he also understood that Kimberly-Clark needed scale to compete globally.

The strategic rationale was compelling. Kimberly-Clark was a premium brand with strong market power in the United States. Scott Paper had the largest market share of tissues in Europe and was positioned as a value-oriented brand. Scott's European strength would give Kimberly-Clark instant global reach. Scott's value positioning would allow Kimberly-Clark to compete at multiple price points.

July 17, 1995, New York City. The press conference was packed. Kimberly-Clark Corp. announced today plans for a $6.8 billion merger with its revived paper products rival, Scott Paper Co., to create the world's largest manufacturer of tissue paper. The merger, a triumph for Scott's troubleshooter chief executive and Chairman Albert J. Dunlap, would create a consumer products company with $11 billion in annual revenue -- second only to $30 billion Procter & Gamble Co. among U.S. household and personal care companies.

Dunlap, who turns 58 next week, and Kimberly-Clark chief executive and Chairman Wayne R. Sanders, 48, told a conference for press and analysts here today that Scott shareholders will receive 0.765 shares of Kimberly-Clark common stock for each share of Scott they own.

The numbers were staggering. The actual price tag ended up at $9.4 billion when the deal closed in December 1995. He said he would earn about $100 million from rescuing and merging Scott, including $20 million from Kimberly-Clark for promising not to go to a competing company. Dunlap's payday was obscene by any measure—but Sanders wasn't buying Dunlap, he was buying Scott's assets and market position.

The integration challenges were immediate and brutal. Kimberly-Clark has about 43,000 employees and Scott about 20,000. Sanders said the merger would allow for nearly $400 million in savings—code for massive layoffs. The cultures couldn't have been more different: Kimberly-Clark's methodical, research-driven approach versus Scott's slash-and-burn mentality under Dunlap.

Antitrust concerns emerged quickly. The State of Texas and Department of Justice filed joint suit to enjoin the merger of Kimberly Clark and Scott Paper Corporation which DOJ and Texas alleged would substantially lesson competition in the manufacturing and sale of baby wipes and facial tissue. Matter settled with Defendants agreeing to divest a plant, two mills & related licenses and marketing assets.

The divestitures were painful but necessary. As part of the sale of the company, the Baby Fresh baby wipes brand was sold to Procter & Gamble and is now sold under the Pampers brand. The Scotties facial tissue brand in the United States was sold to Irving Tissue. Kimberly-Clark essentially handed ammunition to its biggest competitor to get the deal done.

Sanders said Kimberly-Clark's success with facial tissue and industrial wipes would fit well with Scott's strong sales of bathroom tissues and kitchen towels. The product portfolio synergies were real—Kimberly-Clark strong in facial tissue and diapers, Scott dominant in toilet paper and paper towels.

The geographic complementarity was even more compelling. Kimberly-Clark dominated North America but was weak in Europe. Scott held the number one tissue position in Europe but struggled in other categories. Together, they would be a global powerhouse.

The market reaction was mixed. Kimberly-Clark shares rose $4.87 1/2 today, to $63.50, while Scott, the most active issue on the New York Stock Exchange, fell $2.75 to $48.37 1/2. Investors understood the strategic logic but worried about execution risk.

The human cost was severe. Beyond the headline job cuts, there were plant closures, relocations, and the inevitable culture clashes when two organizations merge. Scott employees who had survived Dunlap's chainsaw now faced integration into Kimberly-Clark's more structured environment.

The brand decisions were complex. Which Scott brands to keep? How to position them versus existing Kimberly-Clark products? The Scott brands were re-invigorated, often offering lower-priced alternatives to the P&G and Kimberly-Clark products. This dual-brand strategy—premium Kleenex and value Scott—would become a competitive advantage.

This merger created the second largest personal care company in the United States. More importantly, it created a company with the scale to compete globally with P&G. The combined entity could negotiate better with retailers, achieve greater manufacturing efficiencies, and spread R&D costs across a larger base.

The integration took years. Systems had to be merged, cultures blended, redundancies eliminated. Some Scott innovations were adopted company-wide; others were discarded. The European operations, Scott's crown jewel, had to be carefully integrated without disrupting market leadership.

Looking back, the merger was transformative but messy. Sanders had paid a premium price—arguably overpaying given Dunlap's financial engineering—but gained critical mass. The deal proved that even in mature industries like paper products, consolidation could create value through scale and scope.

The bitter irony: Dunlap, who walked away with $100 million, would go on to destroy Sunbeam with accounting fraud that would land him in legal trouble. His "turnaround" at Scott, while real in terms of cost-cutting, was later revealed to include aggressive accounting practices that inflated the company's apparent health.

The once powerful (and profitable) Scott Paper Company made acquisition mistakes and lost its dominance, descending into large losses. In 1995, Kimberly-Clark acquired Scott Paper for $9.4 billion. The company that had invented toilet paper on a roll, that had dominated the tissue industry for decades, ceased to exist as an independent entity.

For Kimberly-Clark, the merger marked the end of one transformation and the beginning of another. Darwin Smith had turned a paper company into a consumer products company. Sanders had turned a North American player into a global giant. The question now was whether bigger would actually prove to be better.

VII. Modern Era: Global Dominance & Digital Age (1997–Present)

The transition from Wayne Sanders to Thomas Falk in 2002 marked a new chapter—the consolidation of the mega-merger gains and the push for global optimization. Falk, who has served as Chief Executive Officer since 2002 and Chairman of the Board of Directors since 2003, was the consummate insider, having been with the company since the 1980s. Born in 1958 in Waterloo, Iowa, the oldest of nine children in a modest family, Falk rose through operations with the methodical precision of someone who understood every lever of the business.

Falk led the creation of the company's Global Business Plan, which prioritizes growth opportunities and applies greater financial discipline to operations. The plan was launched in mid-2003 and has allowed the company to generate sustainable growth and shareholder returns. This wasn't revolutionary thinking—it was execution excellence. Where Darwin Smith had blown things up, Falk optimized what remained.

The geographic expansion continued relentlessly. In 1997, Kimberly-Clark sold its 50% stake in Canada's Scott Paper to forest products company Kruger Inc. and bought diaper operations in Spain and Portugal and disposable surgical masks maker Tecnol Medical Products. Augmenting its presence in Germany, Switzerland and Austria, in 1999 the company paid $365 million for the tissue business of Swiss-based Attisholz Holding.

The medical products push intensified. Expanding its offerings of medical products, the company bought Ballard Medical Products in 1999 for $774 million and examination-glove maker Safeskin in 2000 for about $800 million. These weren't sexy acquisitions, but they diversified revenue streams beyond consumer products.

Asia became the new frontier. Also in 2000, the company bought virtually all of Taiwan's S-K Corporation; the move made Kimberly-Clark one of the largest manufacturers of packaged goods in Taiwan. The company later purchased Taiwan Scott Paper Corporation for about $40 million and merged the two companies, forming Kimberly-Clark Taiwan.

The acquisition spree continued into the 2000s. In 2001, Kimberly-Clark bought Italian diaper maker Linostar and announced it was closing four Latin American manufacturing plants. In 2002, Kimberly-Clark purchased paper-packaging rival Amcor's stake in an Australian joint venture. In 2003, Kimberly-Clark added to its global consumer tissue business by acquiring the Polish tissue maker Klucze.

In early 2004, chairman and chief executive officer Thomas Falk began implementation of a global business plan that the company has detailed in July 2003. The firm combined its North American and European groups for personal care and consumer tissue under North Atlantic groups. This reorganization streamlined operations but also signaled the end of geographic fiefdoms.

The final break with the past came in 2012. Founded in Neenah, Wisconsin, in 1872 and based in the Las Colinas section of Irving, Texas, since 1985, the company operated its own paper mills around the world for decades, but closed the last of those in 2012. After 140 years, Kimberly-Clark no longer made paper from pulp. The transformation Darwin Smith had started was complete.

Under Falk's steady hand, the company delivered consistent if unspectacular results. His tenure delivered consistent shareholder returns, outperforming the S&P 500 while growing sales to $19 billion by 2015. Innovation continued with products like Kleenex Anti-Viral tissues in 2004, but nothing revolutionary.

The leadership transition to Michael Hsu in 2019 represented a generational shift. Hsu succeeds Thomas J. Falk, 60, who has served as Chief Executive Officer since 2002 and Chairman of the Board of Directors since 2003. Prior to joining Kimberly-Clark in 2012, Hsu was Executive Vice President and Chief Commercial Officer at Kraft Foods. Before Kraft, he spent six years at H.J. Heinz, holding the positions of Vice President, Marketing for Ore-Ida and Frozen Meals, and later as President for Foodservice.

Hsu was the first outsider CEO since Darwin Smith—a signal that fresh thinking was needed. His background at Kraft and Heinz brought consumer products expertise from beyond the paper products world. Earlier this year, Kimberly-Clark announced a $1.5 billion cost-cutting plan that would eliminate up to 5,500 jobs over the next four years. On Monday, the company said workforce reductions and supply chain improvement should result in pretax savings of up to $550 million by the end of 2021.

Then came COVID-19—the black swan event that nobody could have predicted. Taking leadership just before the COVID-19 pandemic, he guided Kimberly-Clark through unprecedented demand surges—with toiletry item panic buying.

March 13, 2020. Before executives at consumer-goods giant Kimberly-Clark rushed to shut their offices on Friday the 13th of March, they convened for one last emergency meeting. Commuting home that final time, Arist Mastorides, president of family care for North America, stopped at his local Walmart, on the edge of Lake Winnebago in Neenah, Wis., to see the emergency firsthand. Mastorides oversees toilet paper brands like Cottonelle and Scott, but that evening he could find none of his own products. "A long gondola shelf that's completely empty of bathroom and facial tissue, I never in my life thought I would ever see that," he says.

The previous day, March 12, TP sales had ballooned 734% compared with the same day the previous year, becoming the top-selling product at grocery stores by dollars spent, according to NCSolutions, which tracks consumer packaged goods (CPG). The Great Toilet Paper Panic of 2020 had begun.

In April 2020, the Financial Times reported that panic-buying during the COVID-19 pandemic led to a 13 percent increase in sales of Kimberley-Clark's consumer tissues in the first quarter of 2020 compared with the previous year. Toilet paper lifted Kimberly-Clark's worldwide sales by 8% and by 12% in North America, where pantry loading has become the new shopping mode during the initial weeks of the coronavirus pandemic. Profit was up 45% in the first three months ending in March for the Irving-based company, which operates in 175 countries.

The response required wartime-level mobilization. After leaving the office that March Friday, Kimberly-Clark's Mastorides spent the weekend deciding which kinds of TP to stop producing—cutting "SKUs" by at least half. The company has focused on six-packs of Cottonelle "mega rolls" versus 12-packs; that keeps plants from having to stop the machines as often to switch out materials, minimizing downtime.

"We are producing and shipping 24 hours a day, seven days a week." The company's operations went into overdrive, with office workers taking factory shifts to meet demand.

But COVID also exposed the two-sided nature of the tissue business. There's also uncertainty in Kimberly-Clark's operations that sell to other businesses until people go back to work. Some of the company's capacity that supplies offices and hotels may be shifted to meet consumer demand, he said. Office use of bathroom products is down 80%, travel and leisure is down with hotel capacity at only 21%, and seated restaurant business is down 100% globally.

The pandemic accelerated trends that were already emerging. Digital commerce exploded. Work-from-home became permanent for millions. Consumer behavior shifted in ways that may never fully reverse. "I think we'll have a very different assortment as we exit this," Mastorides says.

In this new environment, Hsu made a bold move reminiscent of earlier pivots. Kimberly-Clark Corporation (NYSE: KMB), the pioneer of menstrual hygiene products, announced that it has completed its acquisition of a majority stake in Thinx, Inc., an industry disruptor and the leader in reusable period and incontinence underwear category. The company made an initial minority investment in Thinx in 2019.

The Thinx acquisition represented a recognition that consumer preferences were shifting toward sustainability and reusability. The personal hygiene company — which includes the Huggies, Kleenex, Kotex, Cottonelle, Depend and Pull-Ups brands in the greater portfolio, among others — previously made a minority investment of $25 million in Thinx in 2019. By 2022, they acquired majority control, though terms weren't disclosed.

"Kimberly-Clark invented the 'femcare' category 100 years ago and Thinx invented the 'femtech' category nine years ago. It's fitting that we will be working more closely with a like-minded organization to realize our mission and vision, and to enable Thinx underwear to more quickly become a mainstream product for period and bladder leak needs," Thinx CEO Maria Molland said in a statement.

The digital transformation accelerated under Hsu. As Chief Digital and Technology Officer for Kimberly-Clark, Zack Hicks leads at the intersection of digital and business transformation, delivering value through K-C's digital core as well as providing innovative next-generation technology solutions that deliver growth, build brands and create competitive advantage for the company. Mr. Hicks joined Kimberly-Clark in 2022 after 26 years of leadership at Toyota Motors North America.

Today, With recent annual revenues topping $18 billion per year, Kimberly-Clark is regularly listed among the Fortune 500. As of March 2020, the company had approximately 40,000 employees. The company that started with four men and $42,000 now operates in 175 countries.

The portfolio remains focused but powerful. Our portfolio of brands, including Huggies, Kleenex, Scott, Kotex, Cottonelle, Poise, Depend, Andrex, Pull-Ups, GoodNites, Intimus, Neve, Plenitud, Sweety, Softex, Viva and WypAll, hold the No. 1 or No. 2 share position in 80 countries.

The modern era has been about optimization rather than transformation. Geographic expansion continues, but incrementally. Digital capabilities grow, but evolutionarily. The company that Darwin Smith radically transformed has settled into middle age—profitable, stable, but no longer revolutionary.

Yet challenges loom. Private label competition intensifies. Sustainability pressures mount on disposable products. Birth rates decline in developed markets. Digital natives create new categories that bypass traditional retail entirely.

The question for Kimberly-Clark's future isn't whether it can maintain its current position—it's whether it can find its next Darwin Smith moment, its next radical pivot that redefines what the company can be. History suggests it's possible. The company has reinvented itself before. Whether it has the institutional courage to do so again remains to be seen.

VIII. Playbook: Strategic Lessons

The Kimberly-Clark story offers a masterclass in corporate transformation, but the lessons aren't always what they first appear. Let's dissect the strategic moves that actually mattered.

The Power of Accidental Innovation

The greatest breakthroughs often come from unintended use cases. Cellucotton wasn't designed for feminine hygiene—Red Cross nurses discovered that application in field hospitals. Kleenex wasn't meant for noses—consumers repurposed it from cold cream removal. Huggies Pull-Ups emerged from parents jury-rigging regular diapers for potty training.

The strategic lesson: Build systems to capture and capitalize on unexpected use cases. Kimberly-Clark's genius wasn't inventing these applications—it was recognizing them, validating them, and scaling them. Most companies would have ignored nurses using surgical wadding for menstruation as an edge case. Kimberly-Clark built a billion-dollar business from it.

Modern parallel: Instagram started as Burbn, a location check-in app. The photo-sharing was a minor feature until users showed them otherwise. The best strategies often emerge from customer behavior, not boardroom planning.

When to Abandon Your Core Business

Darwin Smith's decision to sell the paper mills remains one of the gutsiest moves in corporate history. The conventional wisdom says diversify to reduce risk. Smith did the opposite—he concentrated to increase focus.

The key insight: Your historical core business is often your biggest strategic liability. It consumes capital, management attention, and emotional energy that should go toward the future. The paper mills weren't just unprofitable—they were an anchor preventing Kimberly-Clark from competing effectively in consumer products.

The timing mattered enormously. Smith didn't sell when the mills were worthless—he sold when they still had value to others. The $250 million from land sales funded the consumer products transformation. Too many companies wait until their legacy business is worthless before pivoting.

Counter-example: Kodak invented the digital camera but couldn't abandon film until it was too late. They knew the future but couldn't kill the past. Smith killed the past while it still had value.

Building Brands That Become Generic Terms

Kleenex. It's not just a brand—it's the word for facial tissue. This level of brand dominance creates a moat that's nearly impossible to breach. When your brand becomes the generic term, you've achieved something money can't buy.

But here's the paradox: You can't plan for this. It emerges from a combination of being first, being better, and most importantly, being simple. "Facial tissue" is clunky. "Kleenex" flows. The phonetics matter as much as the product.

The strategic imperative: Invest disproportionately in the brands that show signs of becoming category-defining. Kimberly-Clark spent decades advertising Kleenex when it already dominated. Why? Because maintaining generic status requires constant reinforcement. The moment you take it for granted, private label erodes your premium.

The Acquisition Integration Playbook

The Scott Paper merger could have been a disaster. Different cultures, overlapping products, massive redundancies. Instead, it created lasting value. How?

First, clarity of purpose. This wasn't about diversification—it was about scale and geographic reach. Scott's European position and value-tier positioning perfectly complemented Kimberly-Clark's premium North American business.

Second, speed of integration. The $1.4 billion in charges and 6,000 layoffs happened immediately, not dragged out over years. Rip the band-aid off. The longer integration takes, the more value destroys.

Third, brand portfolio strategy. Rather than force everything into one positioning, they maintained Scott as value and Kleenex/Cottonelle as premium. This dual-brand strategy let them compete at multiple price points without cannibalizing themselves.

Modern lesson: Most mergers fail because companies try to preserve too much. The successful ones are ruthless about elimination and clear about synergies. You're not buying a company—you're buying specific assets and capabilities.

Managing Portfolio Complexity

Kimberly-Clark operates across baby care, feminine care, adult incontinence, facial tissue, toilet paper, paper towels, and professional products. That's massive complexity. How do they manage it?

The answer: Shared technology platforms. Absorbency technology developed for diapers applies to feminine pads and adult incontinence. Manufacturing processes for facial tissue translate to toilet paper. Distribution networks serve all categories.

The strategic principle: Portfolio diversity works only when there are genuine synergies. P&G can sell both diapers and laundry detergent because they share retail channels and consumer marketing capabilities. If you can't identify specific, measurable synergies, you're not diversified—you're distracted.

The Conglomerate Discount vs. Focused Player Debate

Should Kimberly-Clark split into separate companies? Activists periodically propose this. Feminine care as one company, baby care as another, tissue as a third. The sum of parts would theoretically be worth more than the whole.

The bull case for staying together: Retailer negotiating power, shared R&D, manufacturing scale, and cross-category innovation. When Walmart sits across the table, being a $20 billion company matters more than being three $7 billion companies.

The bear case: Each category has different growth rates, margin profiles, and strategic needs. Tissue is mature and defensive. Baby care faces declining birth rates. Feminine care has new competition from reusables. Bundling them together forces compromise.

The resolution: Kimberly-Clark threads the needle by maintaining operational integration while allowing strategic differentiation. Shared back-end, distinct front-end. It's not elegant, but it works.

Capital Allocation Through Cycles

Over 150 years, Kimberly-Clark has survived multiple recessions, two world wars, and countless competitive threats. How? Countercyclical capital allocation.

During downturns, they invest. The 1888 fire rebuild during a recession. Darwin Smith's transformation during 1970s stagflation. The Scott merger during 1990s uncertainty. When others retreat, they advance.

During booms, they harvest. The 2000s saw fewer big moves and more optimization. Return cash to shareholders, pay down debt, prepare for the next crisis.

The principle: Market timing matters less than competitive timing. The best time to invest is when competitors can't. The best time to acquire is when others are selling. The best time to transform is when the market expects nothing.

The Innovation Paradox

Kimberly-Clark's greatest innovations were accidents, yet they spend billions on formal R&D. Is planned innovation worthless?

No, but it serves a different purpose. Formal R&D creates incremental improvements—softer tissue, better absorbency, improved fit. These matter enormously for maintaining share and premium pricing. You can't accidentally discover a 10% improvement in diaper leakage protection.

But breakthrough innovation—the category-creating kind—usually emerges from the edges. It's nurses in field hospitals, consumers misusing products, or entrepreneurs in garages. The strategic challenge is building systems to capture both.

Kimberly-Clark's solution: Maintain massive formal R&D for optimization while staying porous enough to recognize external innovation. The Thinx acquisition exemplifies this—they couldn't have invented reusable period underwear internally, but they could recognize its potential and acquire it.

The Platform Power Play

The real moat isn't any single brand—it's the platform underneath. Manufacturing expertise, distribution relationships, regulatory knowledge, consumer understanding. These capabilities compound over decades and become nearly impossible to replicate.

A startup can create better period underwear (Thinx), better diapers (Honest Company), or better toilet paper (Who Gives a Crap). But they can't match Kimberly-Clark's ability to produce at scale, distribute globally, and innovate across categories.

The strategic lesson: Invest in capabilities, not just products. Products can be copied. Capabilities compound. Kimberly-Clark's ability to take Thinx from startup to global brand leverages 150 years of accumulated capability.

The Sustainability Transition

The elephant in the room: Kimberly-Clark's core products are disposable in an increasingly sustainability-conscious world. How do you transform when your business model is under existential threat?

The playbook is still being written, but early moves are instructive. The Thinx acquisition signals openness to reusable alternatives. Investment in sustainable sourcing and manufacturing reduces environmental impact. Premium positioning allows charging more for sustainable options.

But the real answer might be uncomfortable: Sometimes transformation means managed decline. If disposable products become socially unacceptable, Kimberly-Clark might need another Darwin Smith moment—selling the disposable business while it still has value and pivoting to something entirely new.

The meta-lesson of the playbook: Great companies don't just execute strategies—they evolve them. What worked for John Kimberly wouldn't work for Darwin Smith. What worked for Smith might not work for Michael Hsu. The only constant is the willingness to change.

IX. Power & Competition Analysis

Brand Power: When Your Product Name Becomes the Generic Term

"Pass me a Kleenex." Nobody says "pass me a facial tissue." This linguistic dominance represents the highest form of brand power—when your trademark transcends into everyday language. It's a moat that new entrants simply cannot cross.

But this power is fragile. "Xerox" used to mean photocopy; now it's just another printer company. "Kodak moment" disappeared with film photography. The lesson: Brand genericide is both the ultimate achievement and constant threat. You must defend it aggressively while appearing not to care.

Kimberly-Clark walks this tightrope brilliantly. They maintain trademark enforcement (you'll notice ® symbols everywhere) while allowing colloquial use. They invest heavily in advertising not to gain share—they already dominate—but to maintain mental availability. When someone thinks "tissue," the brain autocompletes to "Kleenex."

The economics are staggering. Private label facial tissue might be 40% cheaper, but consumers still reach for Kleenex. That premium pricing on billions of units annually creates a profit pool competitors can't match. It funds R&D, marketing, and innovation that further extends the lead.

Scale Economies in Manufacturing and Distribution

A diaper factory costs $200+ million to build. It needs to run 24/7 at 85%+ capacity to be economical. You need multiple factories for geographic coverage. The working capital requirements are massive—raw materials, inventory, receivables.

This creates a brutal math problem for new entrants. To achieve competitive unit costs, you need massive scale. To get massive scale, you need competitive pricing. To offer competitive pricing without scale, you lose money on every unit. It's a catch-22 that protects incumbents.

But here's the nuance: Scale advantages are category-specific. Kimberly-Clark's tissue manufacturing doesn't help with diapers. Different machines, materials, processes. This is why focused competitors can sometimes win in single categories—P&G's diaper scale beats Kimberly-Clark's diversified scale.

The distribution scale, however, does transfer. When Kimberly-Clark's truck delivers to Walmart, it carries Kleenex, Huggies, Kotex, and Scott. The cost per SKU drops. A startup delivering just diapers can't match this efficiency. This is why most successful new brands eventually sell to incumbents—independent distribution doesn't scale.

The P&G Rivalry: David vs. Goliath Dynamics

Procter & Gamble is the Death Star of consumer products—$80 billion revenue, unlimited resources, marketing excellence. Kimberly-Clark is one-fourth the size. By all logic, P&G should dominate every category they both compete in.

Yet Huggies beats Pampers in multiple markets. Kotex holds its own against Always. Scott competes with Charmin. How?

First, focus. P&G manages everything from laundry detergent to shampoo. Kimberly-Clark just does paper-based absorbent products. Their entire R&D budget goes toward making things softer, more absorbent, better fitting. That focus compounds.

Second, positioning. P&G typically plays premium—Pampers, Charmin, Always are all positioned as the best. Kimberly-Clark occupies multiple price points with different brands. When P&G zigs premium, Kimberly-Clark zags value with Scott. When P&G goes mass market, Kimberly-Clark goes ultra-premium with Huggies Special Delivery.

Third, speed. Smaller companies can move faster. When pull-up training pants emerged as a category, Kimberly-Clark's Pull-Ups beat P&G's Easy Ups to market by years. First-mover advantage in new categories often proves decisive.

The rivalry drives both companies forward. P&G innovations force Kimberly-Clark to improve. Kimberly-Clark's agility forces P&G to speed up. Consumers benefit from better products at competitive prices. It's capitalism at its best.

Private Label Threats and Premium Positioning

Costco's Kirkland diapers. Amazon's Mama Bear. Every retailer now has private label tissue and baby products. They're 30-40% cheaper and increasingly competitive on quality. This is the existential threat.

The standard response—innovate to stay ahead—only partially works. How much better can toilet paper get? There's a natural ceiling to product improvement in mature categories. At some point, private label catches up on quality while maintaining price advantage.

Kimberly-Clark's real defense is emotional, not functional. Parents buy Huggies because they signal caring about their baby. Women buy Kotex because it makes them feel secure. These emotional jobs-to-be-done can't be fulfilled by generic products.

But this requires constant investment in brand building. The moment you go quiet, private label gains share. It's an exhausting, expensive treadmill. Marketing spend that could go to R&D or shareholders instead defends against commoditization.

The long-term solution might be to concede certain price points entirely. Let private label have the bottom 30% of the market. Focus on premium segments where brand still matters. Better to have 40% share at 40% gross margin than 60% share at 20% margin.

Emerging Market Expansion Opportunities and Challenges

China. India. Indonesia. Nigeria. These markets represent billions of consumers entering the middle class. As incomes rise, they shift from cloth to disposable diapers, from rags to sanitary pads, from newspaper to toilet paper. It's a massive growth opportunity.

But it's not that simple. Local competitors know the market better. Unicharm dominates in Asia. Local brands are trusted and affordable. Distribution is fragmented—millions of small shops rather than consolidated retail. Consumer preferences differ—Asian babies are shaped differently than Western babies, requiring different diaper designs.

Kimberly-Clark's approach has been mixed. Joint ventures provide local knowledge but reduce control. Acquisitions are expensive and integration is difficult. Organic expansion is slow and requires massive investment. There's no easy answer.

The bear case: Emerging markets are a value trap. Growth looks attractive but margins are terrible. Competition is brutal. Currency fluctuations destroy returns. Better to focus on defending profitable developed markets.

The bull case: This is where the next billion consumers are. Missing this wave means accepting permanent decline as developed markets mature. Early investment creates switching costs and brand loyalty that compound over decades.

Sustainability Pressures in Paper-Based Products

A typical baby uses 6,000 diapers. Each takes 500 years to decompose. The environmental math is devastating. As climate consciousness grows, disposable products face increasing scrutiny.

This isn't just about consumer preference—it's about regulation. Cities are banning single-use plastics. Extended producer responsibility laws make manufacturers responsible for disposal. Carbon taxes increase production costs. The regulatory walls are closing in.

Kimberly-Clark's response has been incremental. Sustainable sourcing, reduced packaging, manufacturing efficiency. But these are band-aids on a fundamental problem: the business model depends on people throwing things away.

The Thinx acquisition signals recognition of this threat. Reusable period underwear is a tiny market today but could be the future. The challenge is cannabalization—every Thinx customer is potentially lost Kotex sales. But better to cannibalize yourself than let others do it.

The existential question: Can a disposable products company become a sustainable products company? History suggests it's possible—Netflix went from DVDs by mail to streaming. But it requires willingness to destroy your existing business. Does Kimberly-Clark have that courage?

The Direct-to-Consumer Disruption Question

Dollar Shave Club. Harry's. Quip. The DTC playbook is proven: Pick a category, create a hip brand, acquire customers online, deliver via subscription. No retailers, no middlemen, better margins.

So where's the Kleenex killer? The Huggies disruptor? They exist—Honest Company for diapers, Rael for feminine care, Who Gives a Crap for toilet paper. But none have achieved true scale. Why?

First, the economics are brutal. Customer acquisition costs for a $20 diaper pack are unsustainable. Shipping costs destroy margins—toilet paper is bulky and heavy. Subscribe-and-save sounds great until you have 10,000 diapers in your garage because the baby grew faster than expected.

Second, these are immediate-need products. When you run out of toilet paper, you need it now, not in two days. When the baby has a blowout, you can't wait for next month's shipment. Physical retail availability remains essential.

Third, brand trust matters more for intimate products. Parents want Huggies because pediatricians recommend them and friends use them. That social proof takes decades to build and can't be manufactured through Instagram ads.

The real DTC threat isn't new brands—it's Amazon. They have the logistics, the customer base, and increasingly, the private label products. When Amazon Basics diapers achieve Huggies quality at 70% of the price with next-day delivery, that's the ballgame.

Network Effects and Ecosystem Lock-in

This isn't software—there are no traditional network effects. One person using Kleenex doesn't make it more valuable for others. But there are subtle ecosystem dynamics at play.

Retailer relationships compound over time. The Walmart buyer who's worked with Kimberly-Clark for 20 years trusts them to deliver, innovate, and support promotions. That relationship is a moat.

Professional channels create switching costs. Hospitals that use Kimberly-Clark surgical products also use their patient care products. Hotels using Scott towels also use Kleenex tissues. These bundled relationships are sticky.

Innovation spillovers accelerate development. Absorbency research for diapers improves feminine pads. Manufacturing improvements for tissue reduce costs across categories. Knowledge compounds across the portfolio.

The platform dynamics mean the whole is greater than the sum of parts. This is why breaking up the company might destroy value rather than create it. The interconnections aren't visible in financial statements but they're real.

The Power Gradient

Not all power is created equal. Let's rank Kimberly-Clark's power sources:

- Brand Power (Kleenex, Huggies, Kotex): Nearly unassailable in the medium term but vulnerable to generational shifts

- Scale Economies: Strong but replicable by other large players

- Switching Costs: Moderate for consumers, high for professional channels

- Network Effects: Minimal in traditional sense, moderate as ecosystem

- Cornered Resource: None—anyone can buy pulp and petroleum

- Process Power: Moderate—manufacturing excellence but not revolutionary

The diagnosis: Kimberly-Clark's power is real but fragile. It depends on brand strength and scale advantages that could erode with technological or social change. There's no structural moat like a patent or network effect. Continued success requires continued execution.

This is both weakness and strength. Companies with structural moats often become complacent. Kimberly-Clark knows it must earn its position every day. That paranoia drives innovation and efficiency. The lack of a permanent moat might be the best moat of all.

X. Bear vs. Bull Case

Bull Case: The Resilient Giant

Irreplaceable Brands with 150+ Years of Trust

When your grandmother used Kleenex, your mother used Kleenex, and you use Kleenex, that creates a psychological moat no startup can cross. These aren't just products—they're part of the cultural fabric. Kleenex has been there for every cold, every tear, every spill for five generations. That emotional equity is priceless.

The trust factor multiplies for intimate products. Parents won't experiment with unknown diaper brands when Huggies has kept millions of babies dry. Women stick with Kotex because it's never failed them. This isn't price-sensitive consumption—it's trust-dependent. And trust compounds over decades, creating switching costs that economists underestimate.

Consider the alternative: Would you trust your baby to "DisruptoDiaper" because it's 20% cheaper? Would you switch to "TechTissue" because it has an app? The absurdity of these questions proves the point. In categories touching human bodies, brand heritage matters enormously.

Essential Products with Recession Resilience

People might skip restaurant meals or delay car purchases, but they won't stop using toilet paper. These products are defensive by nature—demand is need-driven, not want-driven. This creates remarkable earnings stability through economic cycles.

The COVID-19 panic buying proved this definitively. When society feared collapse, what did they hoard? Toilet paper. Not jewelry, not electronics—toilet paper. It revealed a fundamental truth: these products are perceived as survival essentials. That perception creates pricing power even in recessions.

The subscription-like revenue model—people buy tissue and diapers monthly—provides predictable cash flows that the market undervalues. It's not sexy, but it's reliable. In a world of increasing volatility, boring stability becomes increasingly valuable.

Emerging Market Growth Runway

The math is compelling: 2 billion people in emerging markets will enter the middle class by 2040. Each represents a lifetime customer for diapers, feminine care, and tissue products. Even capturing 10% of this growth creates a multi-billion dollar opportunity.

The transition from cloth to disposable diapers in India and Indonesia mirrors what happened in China twenty years ago. Kimberly-Clark learned from that experience. They now know how to price for affordability while maintaining margins, how to distribute through fragmented retail, how to adapt products for local preferences.

Rising female workforce participation drives feminine care adoption. Urbanization drives tissue consumption. These are structural trends that will play out over decades, not quarters. Patient investors who understand demographic inevitability will be rewarded.

Pricing Power in Inflationary Environment

When inflation hits, consumers trade down in cars and clothes, but not in personal care. The percentage of household budget spent on these products is too small to drive switching behavior. A 10% price increase on a $10 pack of diapers is $1—not enough to change behavior for a product preventing messy disasters.

Kimberly-Clark has successfully pushed through multiple price increases post-COVID with minimal volume impact. This pricing power was underestimated by markets expecting elasticity that never materialized. When your product is 0.5% of household spending but prevents significant inconvenience, price becomes secondary.

The input cost pressures (pulp, petroleum, labor) affecting Kimberly-Clark also affect competitors, especially private label. This allows coordinated industry pricing that preserves margins. It's not collusion—it's economic reality. When everyone's costs rise, everyone's prices rise.

Bear Case: The Declining Incumbent

Mature Categories with Limited Growth

Toilet paper consumption per capita hasn't grown in developed markets for twenty years. People don't suddenly start using twice as much tissue. These categories are ex-growth, fighting for share in a flat pie. That's a recipe for margin compression, not expansion.

The diaper market faces a darker reality: declining birth rates. U.S. births have fallen 20% since 2007. Japan, Europe, and even China face demographic cliffs. Fewer babies means fewer diapers—it's that simple. You can't innovate your way around demographic decline.

Adult incontinence offers some offset, but it's a smaller, more fragmented market. The crossover point where adult diaper demand exceeds baby diapers might be decades away. Banking on aging populations is morbid and uncertain. Growth investors should look elsewhere.

Private Label Competition Intensifying

Kirkland diapers are now 80% as good as Huggies at 60% the price. For budget-conscious families, that math is compelling. As private label quality improves through better manufacturing and technology transfer, the quality gap narrows while the price gap remains.

Amazon's private label push is particularly threatening. They have perfect data on purchase patterns, unlimited capital for development, and control the shopping interface. When Amazon recommends their brand with "Compare to Huggies" messaging, conversion rates are devastating.

The generational shift accelerates this trend. Millennials and Gen Z show less brand loyalty, more price consciousness, and greater willingness to try alternatives. They didn't grow up with "Kleenex moments"—to them, it's just tissue. This cultural unbundling will accelerate share losses.

ESG Pressures on Paper Products

Disposable diapers are environmental disasters—500 years to decompose, 3.5 million tons of waste annually in the U.S. alone. As climate consciousness grows, these products become indefensible. No amount of "sustainable sourcing" marketing can overcome the fundamental wastefulness.

Regulatory pressure is building. Europe is implementing extended producer responsibility—manufacturers must pay for disposal. Plastic taxes add costs. Environmental lawsuits loom. The regulatory trajectory is clear and negative. Political winds have shifted against single-use anything.

The sustainable alternatives are improving rapidly. Cloth diapers with modern designs. Period underwear like Thinx. Bidets replacing toilet paper. These aren't fringe anymore—they're mainstream among environmentally conscious consumers. And that segment is growing faster than any demographic Kimberly-Clark targets.

P&G's Superior Innovation Engine

Procter & Gamble spends $2 billion annually on R&D versus Kimberly-Clark's $300 million. That 7x difference compounds over time. P&G can afford more bets, bigger bets, and longer-term bets. In innovation-driven categories, capital advantages matter.

P&G's marketing sophistication exceeds Kimberly-Clark's. They invented brand management. They have relationships with the best agencies. Their digital capabilities are superior. When the game is brand building, the better marketer usually wins.

The scale differences are becoming more pronounced. P&G's size gives them better retail terms, lower media costs, and stronger negotiating position. As retail consolidates (Amazon, Walmart, Costco), scale becomes even more important. Being number two becomes progressively harder.

The Verdict: A Value Trap or Value Play?

The bull case rests on resilience and stability. These are defensive qualities that preserve wealth but don't create it. The brands are strong but not strengthening. The moats are real but not widening. It's a melting ice cube melting slowly.

The bear case identifies structural headwinds that won't reverse. Demographic decline, environmental pressure, and competitive dynamics all point toward gradual erosion. The question isn't if decline happens, but how fast.

For value investors, the stock might be attractive at the right price. The company generates significant cash flow, has strong returns on capital, and management is shareholder-friendly. If the market overreacts to temporary headwinds, opportunity emerges.

For growth investors, look elsewhere. This isn't a compounding machine. It's a mature business managing decline while returning cash to shareholders. That's perfectly respectable but won't generate market-beating returns.

The meta-lesson: Investment merit depends on price, not just quality. Even declining businesses can be good investments if priced for worse decline than actually occurs. Even growing businesses can be poor investments if priced for perfection.

Kimberly-Clark is what it is: A well-managed, mature consumer products company with strong brands facing structural headwinds. Whether that's investable depends entirely on what the market thinks it's worth versus what it's actually worth. That gap—perception versus reality—is where returns hide.

XI. Recent News***

Latest Quarterly Earnings and Guidance***

Kimberly-Clark Corporation (NYSE: KMB) reported third quarter 2024 earnings results today. Net sales of $5 billion were down 4% year-over-year. Organic sales grew 1%. Net income attributable to Kimberly-Clark Corporation rose 55% to $907 million, or $2.69 per share, compared to last year.

The Q3 2024 results present a mixed picture. While organic growth remained positive, total sales declined due to currency headwinds and inventory adjustments. Kimberly-Clark Corp (NYSE:KMB) has achieved meaningful gross margin expansion, tracking ahead of pre-COVID levels, supported by strong productivity and cost management strategies.

CEO Michael Hsu highlighted transformation progress: "Our third quarter results reflect strong execution across the business as we transform our organization," said Kimberly-Clark Chairman and CEO, Mike Hsu. The company is implementing what it calls its "Powering Care" strategy, aimed at accelerating innovation and improving commercial execution.

Market share trends are encouraging. The company is seeing positive market share trends, particularly in the U.S., where it is up or even in seven of eight categories. This suggests the competitive position remains strong despite P&G's continued pressure.