JPMorgan Chase: The Empire That Runs Wall Street

I. Introduction & Episode Roadmap

Picture this: It's March 2008, and the American financial system is teetering on the brink of collapse. Bear Stearns, once the fifth-largest investment bank in the United States, is hemorrhaging cash at a rate that would bankrupt it within hours. The Federal Reserve is scrambling for solutions. Treasury Secretary Hank Paulson is fielding frantic calls. And in the eye of this hurricane sits one man: Jamie Dimon, CEO of JPMorgan Chase, about to make a decision that would either save Wall Street or destroy his own bank.

This moment—this single weekend—would cement JPMorgan Chase's position as the fortress of American finance. But to understand how we got here, we need to go back 209 years earlier, to a scheme so audacious it involved dueling founding fathers and a fake water company.

Today, JPMorgan Chase stands as a colossus: over $800 billion in market capitalization, more than twice their nearest competitor. It's the most valuable company east of the Mississippi River. It serves 84 million American consumers and 7 million small businesses. When other banks fail, JPMorgan Chase buys them. When the government needs a private partner to stabilize markets, they call Jamie Dimon.

But here's what's fascinating: This empire wasn't built through a master plan. It's the product of over 1,200 mergers and acquisitions, political intrigue spanning three centuries, and a cast of characters that includes everyone from Alexander Hamilton to John D. Rockefeller to a working-class kid from Queens who would become the most powerful banker in modern history.

How did a water company chartered in 1799 become the institution that essentially is the American financial system? How did Jamie Dimon transform from Sandy Weill's protégé—fired from Citigroup in a boardroom coup—into the only banker who emerged from 2008 stronger than before? And what does it mean for capitalism when one institution becomes so powerful that its failure would trigger global economic collapse?

This is the story of empire-building in its purest form. It's about power, ambition, and the paradox of being simultaneously too big to fail and too important to break up. It's about how banking dynasties rise and fall, and how one institution has managed to absorb them all.

We'll trace the journey from Aaron Burr's clever legal maneuvering in 1799 through J.P. Morgan personally bailing out the U.S. Treasury, from David Rockefeller's globe-trotting diplomacy to Jamie Dimon's fortress balance sheet philosophy. We'll examine how regulatory changes meant to constrain banks actually created opportunities for the smartest operators. And we'll explore what it means when a single institution holds $3.9 trillion in assets—larger than the GDP of Germany.

The threads we'll follow include the original sin of American banking (that water company charter), the age of titans when J.P. Morgan was more powerful than presidents, the modern merger mania that created today's megabanks, and the Dimon era that has redefined what it means to be "systemically important."

Along the way, we'll unpack the paradoxes: How JPMorgan Chase is simultaneously the most regulated and most profitable bank. How it's both a source of systemic risk and systemic stability. How Jamie Dimon became the "least-hated banker" while running the most powerful financial institution on Earth.

This isn't just a business story—it's the story of American capitalism itself, told through the lens of its most essential institution. Because to understand JPMorgan Chase is to understand how money, power, and influence really work in the modern world.

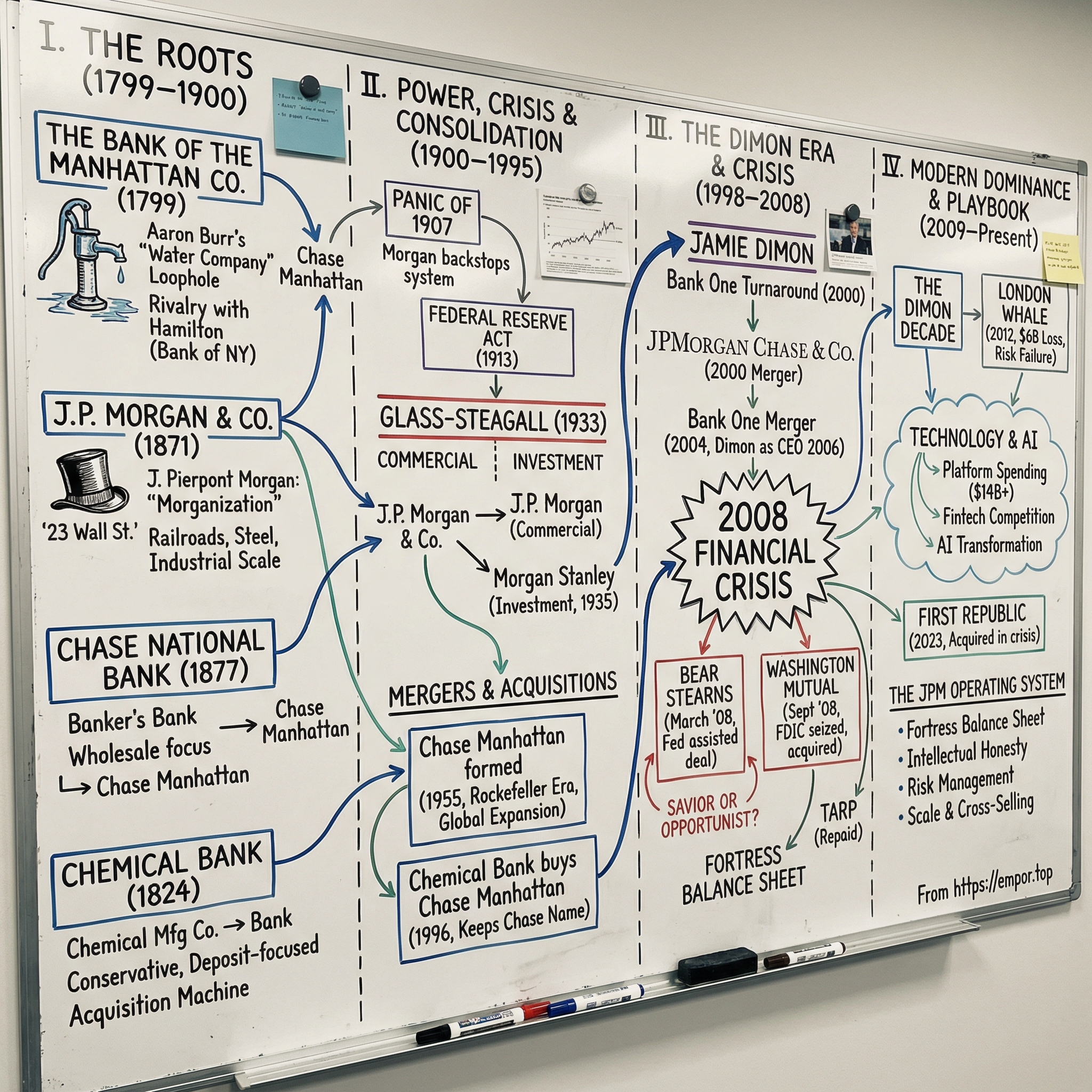

II. The Roots: From Water Company to Banking Dynasty (1799–1900)

The greatest banking empire in history began with a lie about water.

In 1799, yellow fever was ravaging New York City. The disease, spread through contaminated water, had killed thousands. The city desperately needed clean water infrastructure, but there was a problem: only the state legislature could charter a water company, and the legislature was controlled by Federalists who had no interest in helping their political rivals in New York City.

Enter Aaron Burr—Revolutionary War hero, sitting Vice President, and one of the craftiest political operators in American history. Burr saw an opportunity that went far beyond public health. He assembled an unlikely coalition: himself (a Democratic-Republican), Alexander Hamilton (a Federalist and his bitter rival), and a group of prominent New Yorkers. Their pitch was simple: charter a private water company to save the city from disease.

Hamilton, despite his suspicions of Burr, couldn't oppose a measure that would save lives. The Federalist-controlled legislature, seeing Hamilton's support, approved the charter for The Manhattan Company in April 1799. But buried in the charter's text was a clause so innocuous it seemed like boilerplate—and so explosive it would reshape American finance.

The provision, crafted by Burr, stated that surplus capital not needed for water operations could be used for "moneyed transactions." In other words, The Manhattan Company could function as a bank. Within months, Burr had raised $2 million in capital (roughly $40 million in today's dollars), spent a mere $100,000 on wooden pipes and a reservoir, and opened an "Office of Discount and Deposit" with the remaining $1.9 million.

Hamilton was apoplectic. He'd been tricked into helping create a rival to his own Bank of New York. The betrayal was complete—and it was brilliant. Burr had just created New York's third bank and broken the Federalist monopoly on finance. The wooden water pipes would rot within a decade, but the Bank of The Manhattan Company would endure for centuries.

This deception added fuel to an already burning rivalry. Five years later, on July 11, 1804, Hamilton and Burr would face each other with pistols in Weehawken, New Jersey. Hamilton would die from his wounds. Burr would flee, his political career destroyed. But the bank born from their conflict would outlive them both by centuries.

While Burr's Manhattan Company was finding its footing, a very different kind of financial power was emerging. In 1835, a young man named Junius Spencer Morgan left Massachusetts for London to join George Peabody's merchant banking firm. Junius had a son, John Pierpont—J.P. to his friends—who showed an early aptitude for mathematics and an almost supernatural ability to read balance sheets.

Young Pierpont Morgan was educated in Europe, studying at the University of Göttingen, where he became fluent in German and French. This cosmopolitan education would prove invaluable—American business in the 19th century was fundamentally about connecting European capital with American opportunity, and Morgan could speak to both worlds.

In 1871, at age 34, J.P. Morgan partnered with Anthony Drexel of Philadelphia to establish Drexel, Morgan & Co. The timing was perfect. America was industrializing at breakneck speed. Railroads needed financing. Steel mills needed capital. The country was transforming from an agricultural backwater into an industrial powerhouse, and that transformation required money—lots of it.

Morgan understood something fundamental: in the chaos of post-Civil War American capitalism, trust was the scarcest commodity. While other bankers made quick profits from speculation, Morgan built relationships. He didn't just provide capital; he provided credibility. When Morgan backed a deal, European investors knew their money was safe.

His method was simple but revolutionary: he would take control. When he financed a railroad, he demanded board seats. When companies he backed struggled, he sent in his own managers. He called it "Morganization"—the process of bringing order to chaos through financial discipline and centralized control. Critics called it monopolistic. Morgan called it necessary.

By the 1880s, Morgan wasn't just financing American business—he was reshaping it. He orchestrated the merger that created General Electric in 1892. He formed U.S. Steel in 1901, the world's first billion-dollar corporation. He didn't just move money; he moved industries.

Meanwhile, in 1877, an 75-year-old former banker named John Thompson was starting his final act. Thompson had already lived several lives—teacher, banker, creator of the bank note detection system that helped establish paper currency in America. Now he founded Chase National Bank, named after Salmon P. Chase, Lincoln's Treasury Secretary who had put "In God We Trust" on American currency.

Thompson's vision for Chase was distinctly American: while Morgan served titans of industry, Chase would serve the emerging middle class. It would be a commercial bank, taking deposits and making loans to businesses and individuals. Where Morgan represented concentrated power, Chase represented distributed prosperity.

The parallel evolution of these institutions—The Manhattan Company with its origins in deception, Morgan with its aristocratic bearing, Chase with its democratic aspirations—would define American finance for the next century. Each represented a different vision of what banking could be.

But there was a fourth player emerging from the chemical industry. In 1823, The New York Chemical Manufacturing Company was founded to produce medicines, paints, and dyes. The company's directors quickly realized that their real asset wasn't their factory—it was their cash flow. In 1824, they created the Chemical Bank of New York, initially just to manage their own funds.

Chemical would grow quietly, steadily, avoiding the spectacular rises and falls that characterized 19th-century banking. While other banks chased glory, Chemical chased deposits. While others built marble palaces, Chemical built branches. It was boring, profitable, and built to last.

By 1900, these four streams—The Manhattan Company's political savvy, Morgan's financial power, Chase's commercial ambition, and Chemical's operational excellence—were flowing separately through American capitalism. None could have imagined they would eventually merge into a single institution.

The 19th century had established the templates: banking as political tool (Manhattan Company), banking as power broker (Morgan), banking as public utility (Chase), and banking as steady business (Chemical). The 20th century would test which model would survive—or whether they would need to combine to endure.

What emerged from this era wasn't just a collection of banks but a new form of American power. While European banks were creatures of governments and aristocracies, American banks were something novel: private institutions with public power, beholden to shareholders but essential to the state. This tension—between private profit and public purpose—would define everything that followed.

III. The House of Morgan Era: Power & Influence (1900–1935)

In the autumn of 1907, J.P. Morgan was attending an Episcopal convention in Richmond, Virginia, when he received an urgent telegram. The Knickerbocker Trust Company, New York's third-largest trust, was failing. Depositors were lining up to withdraw their money. The panic was spreading. America's financial system was collapsing.

Morgan, then 70 years old, immediately boarded his private rail car back to New York. What followed was perhaps the most extraordinary display of private financial power in American history. For two weeks, Morgan essentially became America's central bank, operating from his library at Madison Avenue and 36th Street.

The library became a war room. Morgan summoned the presidents of New York's major banks and trust companies. He locked them in his library's East Room—literally locked them in—and informed them they wouldn't leave until they'd pledged enough money to stop the panic. At one point, exhausted bankers found Morgan playing solitaire at 3 AM, refusing to speak until he'd figured out his next move. The message was clear: Morgan was in control.

He deployed money with surgical precision. When the New York Stock Exchange nearly closed because brokers couldn't access credit, Morgan raised $25 million in 10 minutes. When trust companies teetered, he organized rescue funds. When New York City itself ran out of money, Morgan underwrote $30 million in city bonds.

But Morgan did more than just provide money—he provided judgment. He personally decided which institutions would live and which would die. Knickerbocker Trust, despite triggering the panic, was allowed to fail. Morgan had examined its books and deemed it unsalvageable. The Trust Company of America, however, received his backing after Benjamin Strong, one of Morgan's lieutenants, spent a sleepless night reviewing its assets and declared it solvent.

The government was helpless. President Theodore Roosevelt, who had built his reputation as a trust-buster opposing Morgan's monopolies, had to acquiesce to Morgan's rescue. Treasury Secretary George Cortelyou traveled to New York and essentially placed $25 million in government funds at Morgan's disposal. The ironies were lost on no one: the government's greatest antagonist had become its savior.

When the panic finally ended in November, Morgan had personally prevented the collapse of the American economy. But he had also demonstrated something terrifying: one man had more financial power than the United States government. This couldn't stand in a democracy.

Morgan himself seemed to understand this. In testimony before Congress in 1912, he was asked about the concentration of financial power. His response was revealing: "I do not think any man has the power to control the money market." When pressed about what drove banking, he famously replied: "The first thing is character...before money or property or anything else. Money cannot buy it."

This philosophy—that banking was fundamentally about trust between individuals—was already becoming antiquated. The world was becoming too complex for one man, however powerful, to manage through force of personality.

Morgan died in Rome on March 31, 1913, just months before the Federal Reserve was created to ensure that never again would America's financial system depend on a single private citizen. When his estate was valued, observers were shocked: Morgan was worth "only" $68 million (about $2 billion today). John D. Rockefeller supposedly quipped, "And to think, he wasn't even a rich man."

But Morgan's true wealth wasn't in his personal accounts—it was in his network, his reputation, and the institutions he built. J.P. Morgan & Co. didn't just survive his death; it thrived under the leadership of his son, Jack Morgan Jr.

Jack was a different creature than his father—less imperious, more collaborative, but equally committed to the Morgan legacy. Where J.P. had ruled through sheer force of will, Jack ruled through systematic organization. He transformed J.P. Morgan & Co. from a partnership dependent on one man's genius into a modern financial institution.

The 1920s should have been the Morgan decade. The firm financed European reconstruction after World War I, floating billions in bonds for Britain, France, and Germany. It led the syndicate that stabilized the German mark. It was, effectively, the world's central bank for international finance.

But the very success contained the seeds of destruction. The same interconnected global financial system that Morgan had helped create amplified the 1929 crash. When stocks collapsed in October, Morgan partners tried to reprise 1907, organizing a pool to support prices. Richard Whitney, the Stock Exchange president and brother of a Morgan partner, strode onto the exchange floor and ostentatiously bought U.S. Steel at above-market prices—a theatrical gesture meant to restore confidence.

It didn't work. The world had changed. The market was too big, the crisis too deep, the public too skeptical. The Morgan mystique, built on the belief that a small group of men could control markets through wisdom and capital, shattered against the reality of the Great Depression.

The political backlash was swift and severe. In 1933, Ferdinand Pecora's Senate investigation exposed the cozy relationships between commercial and investment banking. The public learned that while ordinary Americans lost their savings, Morgan partners had received special stock allocations at below-market prices. Jack Morgan's defense—that these were rewards for good clients, standard practice in the industry—fell on deaf ears.

The coup de grâce came with the Glass-Steagall Act of 1933. Commercial banks could no longer engage in investment banking. Investment banks couldn't take deposits. The House of Morgan, which had built its power on being both, had to choose.

The choice split the firm literally in two. J.P. Morgan & Co. chose to remain a commercial bank, keeping the prestigious name and the client relationships. The investment banking operations were spun off as Morgan Stanley, led by Harold Stanley and Henry Morgan (Jack's son).

This wasn't just a regulatory reorganization—it was the end of an era. The age of financial titans, of private citizens wielding quasi-governmental power, was over. In its place would emerge a new model: banks as regulated utilities, supervised by government agencies, their power diffused and controlled.

Yet even diminished, the Morgan institutions remained formidable. J.P. Morgan & Co. became the gentleman's commercial bank, serving corporations and wealthy individuals with a discretion and sophistication unmatched by competitors. Morgan Stanley became the blue-chip investment bank, maintaining the Morgan tradition of serving only the finest clients.

The splitting of the House of Morgan marked a fundamental shift in American capitalism. Never again would a private banker lock government officials in a library and dictate terms. Never again would one man's judgment determine which businesses lived or died. The age of the imperial banker was over, replaced by the age of the regulated financial institution.

But the DNA remained. The Morgan emphasis on relationship banking, on quality over quantity, on being a trusted advisor rather than a mere provider of capital—these principles survived the regulatory revolution. They would lie dormant through decades of change, waiting for the right moment and the right leader to reunite the empire that regulation had split apart.

IV. Building the Modern Conglomerate (1935–1995)

David Rockefeller's helicopter descended onto the Chase Manhattan Plaza on a gray Manhattan morning in 1969. The heir to America's greatest fortune had just returned from meeting with Gamal Abdel Nasser in Cairo, part of his self-appointed mission to open Middle Eastern markets to American banking. No one had elected him. No government had appointed him. Yet here he was, conducting parallel diplomacy, armed with something more powerful than any official title: the chairmanship of Chase Manhattan Bank.

This was the era of the banker-statesman, and no one embodied it more than Rockefeller. But while he was building Chase's international empire, meeting with Zhou Enlai in Beijing and dining with the Shah in Tehran, the ground was shifting beneath his feet. The age of gentlemen's banking—of long lunches and relationship-building—was giving way to a more ruthless, metrics-driven world.

The story of how America's disparate banking institutions merged into today's megabanks begins, ironically, with their attempts to stay separate and distinct. Each major bank had its identity, its culture, its way of doing business. Chase Manhattan, formed in 1955 from the merger of Chase National Bank and the Bank of the Manhattan Company (yes, Aaron Burr's water company), epitomized establishment banking. Its board read like a Who's Who of American industry. Its headquarters at One Chase Manhattan Plaza, a 60-story tower in lower Manhattan, announced its ambitions architecturally.

Under Rockefeller's leadership from 1969 to 1981, Chase became less a bank than a parallel state department. Rockefeller maintained files on 200,000 individuals he'd met worldwide. He could call any major government or business leader directly. When the Shah of Iran fell in 1979, it was Rockefeller who lobbied the Carter administration to grant him asylum—a decision that triggered the Iranian hostage crisis.

But Rockefeller's globe-trotting masked problems at home. While he focused on prestigious international relationships, Chase was losing ground in basic banking. Its loan portfolio was deteriorating. Its technology was antiquated. Its bureaucracy was legendary—decisions that took hours at competitors took weeks at Chase.

The contrast with Chemical Bank couldn't have been starker. While Chase cultivated prestige, Chemical cultivated profits. Under the leadership of Donald Platten and later Walter Shipley, Chemical pioneered the unglamorous but profitable business of processing transactions. They invested heavily in technology, launching one of the first ATM networks. They focused on middle-market companies that Chase considered beneath its attention.

Chemical's 1986 acquisition of Texas Commerce Bank, led by future U.S. Secretary of State James Baker's family, signaled its ambitions. This wasn't about prestige—it was about deposits, loans, and fee income. When Chemical absorbed Manufacturers Hanover in 1991, it became New York's second-largest bank, though still overshadowed by Chase's brand.

Meanwhile, J.P. Morgan & Co. was experiencing its own identity crisis. Restricted by Glass-Steagall from investment banking, it had evolved into the thinking man's commercial bank. Its client list was exclusive—perhaps 5,000 corporations worldwide. Its bankers were the best-educated, best-paid in the industry. The firm pioneered derivatives, structured finance, and other complex products that required PhD-level mathematics.

But exclusivity had a price. J.P. Morgan was brilliant but small, innovative but capital-constrained. In a world where size increasingly mattered, being the smartest bank wasn't enough. The firm that had once saved America's financial system now struggled to compete with larger, less sophisticated rivals.

The 1990s brought crisis and opportunity in equal measure. The commercial real estate collapse of 1990-1991 devastated bank balance sheets. Chase, despite its illustrious history, was particularly exposed. Its stock price collapsed from $36 to $9. Rumors of insolvency swirled. The New York Times ran articles questioning whether David Rockefeller's bank would survive.

The solution came from an unexpected source: Chemical Bank. In 1995, Chemical's CEO Walter Shipley proposed what was termed a "merger of equals" but was effectively Chemical's acquisition of Chase. The combined entity would keep the Chase name—a recognition that while Chemical had the stronger balance sheet, Chase had the stronger brand.

The merger was a cultural earthquake. Chemical bankers, used to quick decisions and profit focus, clashed with Chase bankers accustomed to deliberation and prestige. The integration took years and cost thousands of jobs. But what emerged was something new: a bank with Chase's global reach and Chemical's operational discipline.

This pattern—stronger bank buys weaker bank but takes the better-known name—would repeat throughout the industry. It reflected a deeper truth about modern banking: operations and technology mattered more than relationships and pedigree, but brand still had value in attracting customers and talent.

The regulatory environment was shifting too. The walls between different types of financial services, erected during the Depression, were crumbling. Banks wanted to sell insurance. Insurance companies wanted to offer banking. Investment banks wanted deposits. Everyone wanted everything.

J.P. Morgan & Co. had been pushing these boundaries for years, using regulatory loopholes to edge back into investment banking. By 1989, it received permission to underwrite corporate bonds. By 1991, it could underwrite stocks. The firm was slowly reassembling capabilities it had lost in 1935.

But incremental change wasn't enough. The global financial system was consolidating rapidly. European banks, unrestricted by Glass-Steagall-type regulations, were becoming "universal banks" offering every financial service. American institutions risked being left behind.

The conventional wisdom was that size and scope were destiny. To compete globally, American banks needed to match the scale of Deutsche Bank, UBS, and the emerging Japanese giants. This drove a merger frenzy that would culminate in the creation of today's megabanks.

Yet for all the talk of synergy and efficiency, many mergers were driven by more primal motivations: ego, fear, and the simple desire not to be left behind. CEOs who had spent careers building institutions suddenly faced the choice: buy or be bought. Most chose to buy, regardless of price or strategic logic.

By 1995, the stage was set for the final act of consolidation. Glass-Steagall was dying, killed not by legislation but by regulatory reinterpretation and market pressure. Technology was enabling banks to operate at previously unimaginable scale. And a new generation of leaders—hungrier, more aggressive, less bound by tradition—was taking power.

The old world of relationship banking, where David Rockefeller could fly to Cairo and negotiate with Nasser as an equal, was ending. The new world would belong to those who could manage complexity at scale, who could turn banking from an art into a science, who could build machines that printed money.

Into this world would step Jamie Dimon, a banker unlike any who had come before—neither aristocrat nor technocrat, but something new: the banker as operating genius. His arrival would complete the transformation that began when Aaron Burr snuck banking into a water company charter. The question was no longer whether American banking would consolidate into megabanks, but who would run them and how they would wield their unprecedented power.

V. The Dimon Era Begins: Bank One & The Modern Chase (1998–2006)

Jamie Dimon sat in his Park Avenue apartment on a November evening in 1998, unemployed for the first time in his adult life. At 42, he had just been fired from Citigroup by his mentor, Sandy Weill, in what Wall Street would later call the most shocking executive termination in modern banking history. Dimon's wife Judy found him in his study, creating spreadsheets—not of job opportunities or financial projections, but of his daughter's third-grade basketball team's statistics. The man who had been running one of the world's largest financial conglomerates was now calculating shooting percentages for nine-year-olds.

The firing had been brutal and public. After building Citigroup together through a series of audacious mergers—transforming a Baltimore commercial lender called Commercial Credit into a financial empire—Weill had turned on his protégé. The reasons remain murky: Dimon's refusal to promote Weill's daughter, tension with Weill's wife, or simply that the empire wasn't big enough for two emperors. Whatever the cause, Dimon was out, with a $30 million severance and a reputation in tatters.

But Dimon's exile would prove to be American banking's most consequential termination. It freed him to take the lessons learned building Citigroup—the good and the bad—and apply them elsewhere. The question was where.

For fifteen months, Dimon considered his options. He turned down CEO positions at Amazon (too early-stage), Home Depot (not his expertise), and several investment banks (too small). He taught classes at Harvard Business School, where students were struck by his command of minute operational details—this wasn't a CEO who managed from 30,000 feet.

Then, in March 2000, Bank One called. The Chicago-based bank, itself the product of multiple mergers, was a mess. Its stock had fallen 50% in two years. It had no unified technology platform—different acquisitions ran different systems. Credit card losses were mounting. The board had just fired the CEO. They needed someone who could do more than run a bank—they needed someone who could rebuild one.

Dimon's first day at Bank One's headquarters was vintage Dimon theater. He arrived at 5:30 AM, before even the security guards. When executives arrived for the 8 AM meeting he'd called, they found him already deep in credit reports, having read hundreds of pages of internal documents. His first question: "Why are we losing so much money on credit cards when everyone else is printing money?"

What followed was a masterclass in operational transformation. Dimon didn't bring in an army of consultants or announce a grand strategy. Instead, he went granular. He discovered that Bank One was using seven different deposit systems. He found credit card marketing campaigns that lost money on every customer acquired. He identified branches that hadn't been profitable in years but stayed open for "community relations."

His approach was ruthlessly meritocratic. He instituted what he called "boot camps"—grueling sessions where business heads had to defend every line item in their budgets. One executive recalled presenting for six hours straight, with Dimon challenging every assumption. "Why do we need 23 people in that department?" "What would happen if we cut this spending by 30%?" "Show me the math."

But Dimon wasn't just cutting. He was building. He unified technology platforms, creating what he called a "fortress balance sheet"—excess capital and reserves that could withstand any crisis. He invested heavily in risk management, hiring PhDs to build models that could stress-test every loan portfolio. He redesigned products from first principles, asking why a checking account needed 15 different fee types when three would suffice.

The results were dramatic. Bank One's stock rose 80% in his first three years. Return on equity jumped from 5% to 15%. The credit card business, once a disaster, became industry-leading. By 2003, Bank One was the most efficient large bank in America, with an overhead ratio that competitors couldn't match.

Meanwhile, in New York, JPMorgan Chase was struggling with its own identity crisis. The 2000 merger between J.P. Morgan & Co. and Chase Manhattan had created a prestigious but unwieldy giant. The investment bank (J.P. Morgan) clashed with the commercial bank (Chase). Technology systems didn't communicate. Different divisions competed rather than collaborated.

CEO William Harrison, who had engineered the merger, recognized the problems but struggled with solutions. The combined entity had the pieces of greatness—J.P. Morgan's investment banking intellect, Chase's retail network, a powerful brand—but couldn't make them work together. The stock languished. Talented bankers left. The firm that had once saved American capitalism was now a chronic underperformer.

In late 2003, Harrison made a call that would reshape American banking. He approached Dimon about merging Bank One with JPMorgan Chase. The logic was compelling: Bank One's operational excellence combined with JPMorgan's franchise could create something formidable. But everyone understood the subtext—this was Harrison hiring his eventual successor.

The negotiation was delicate. Dimon wanted guarantees about succession timing. Harrison wanted to remain CEO initially. The board wanted assurance that two strong personalities could coexist. The solution was a detailed succession plan: Harrison would remain CEO, Dimon would be president and COO, and in two years, Dimon would take over.

When the $58 billion merger was announced in January 2004, the market was skeptical. JPMorgan Chase had already struggled to integrate previous mergers. Bank One and JPMorgan had different cultures, different systems, different approaches. The New York Times called it "a merger of mismatched parts."

But Dimon had learned from Citigroup's mistakes. Instead of declaring victory and moving on, he treated integration as the main event. He created 30 integration teams, each with specific mandates and metrics. He personally reviewed every major decision. He moved between Chicago and New York weekly, making sure both sides felt heard.

More importantly, he began instilling his philosophy throughout the organization. Banking wasn't about financial engineering or regulatory arbitrage—it was about operational excellence. Risk wasn't something to be hidden or ignored—it was to be understood and priced. Complexity wasn't a sign of sophistication—it was often a sign of confusion.

His town halls became legendary. Unlike most CEO presentations—scripted, polished, distant—Dimon's were raw and interactive. He'd stand for hours answering any question. When an employee asked about job security, he didn't offer platitudes. "If you're good at your job and our business is strong, you're secure. If either changes, you're not. That's reality."

By December 2005, when Dimon officially became CEO, the integration was largely complete. But he wasn't satisfied with improvement—he wanted transformation. He began positioning JPMorgan Chase for something bigger, though even he couldn't have foreseen what was coming.

The conventional wisdom in 2006 was that banking had become a mature, predictable industry. The economy was stable. Housing prices only went up. Complex financial instruments had distributed risk so widely that systemic crises were impossible. The biggest concern was that banking had become boring.

Dimon disagreed. In his 2006 shareholder letter—his first as CEO—he warned about growing risks. Housing prices were unsustainable. Leverage was excessive. Competitors were making loans that didn't make sense. While others celebrated record profits, Dimon was building reserves.

He instituted a practice that seemed paranoid at the time: every week, his team would run scenarios about what could go wrong. What if housing prices fell 20%? What if a major competitor failed? What if funding markets froze? The exercises seemed academic—until suddenly they weren't.

As 2007 began, JPMorgan Chase looked strong but not spectacular. It was profitable but not the most profitable. It was big but not the biggest. It was respected but not feared. That was about to change. The financial crisis that would destroy some of Wall Street's proudest names would transform JPMorgan Chase from a successful bank into something more: the indispensable institution of American finance.

VI. The 2008 Financial Crisis: Savior or Opportunist?

At 6 PM on Thursday, March 13, 2008, Jamie Dimon was celebrating his 52nd birthday with his family at a Greek restaurant in Manhattan when his phone rang. It was Alan Schwartz, CEO of Bear Stearns, and his voice was shaking. "We need to talk. Tonight. It's urgent."

Two hours later, in a conference room at JPMorgan Chase's headquarters at 270 Park Avenue, Schwartz laid out the unthinkable: Bear Stearns, the 85-year-old investment bank that had survived the Great Depression, would be bankrupt by Monday morning without immediate help. They had maybe $2 billion in cash left. Repo lenders were pulling credit lines. Hedge fund clients were yanking prime brokerage accounts. The fifth-largest investment bank in America had days—maybe hours—to live.

Dimon's team worked through the night, sending dozens of analysts to Bear's offices to examine the books. What they found was terrifying: not just illiquid mortgage securities, but derivatives positions so complex that no one fully understood the exposure. Bear's balance sheet was a "spaghetti bowl," as one JPMorgan executive later described it, with trades layered upon trades, assumptions built on assumptions.

By Friday morning, the Federal Reserve was involved. Fed Chairman Ben Bernanke and New York Fed President Tim Geithner understood the implications: if Bear failed in a disorderly way, it could trigger a cascade that would bring down the entire financial system. They needed a buyer, and they needed one immediately.JPMorgan wasn't alone in examining Bear's books. Bank of America sent teams too, but after reviewing the numbers, CEO Ken Lewis called Paulson to decline. "I don't think we can do this," he said. That left JPMorgan as the only viable bidder for Bear Stearns.

Saturday turned into a marathon negotiation. The Fed was represented by Tim Geithner, the Treasury by Hank Paulson (calling in from Washington), Bear Stearns by Alan Schwartz, and JPMorgan by Dimon. The sticking point wasn't whether to do a deal—everyone agreed Bear couldn't open Monday without one—but the price and structure.

Dimon's initial instinct was to walk away. The risks were enormous: unknown derivative exposures, potential lawsuits, integration challenges. But Geithner and Paulson made clear that this wasn't just about Bear Stearns. This was about preventing a systemic collapse. They needed JPMorgan, and they were prepared to make it worth their while.

The solution was unprecedented: The Fed agreed to fund up to $30 billion of Bear Stearns' less liquid assets. This wasn't a loan to JPMorgan—it was the Fed essentially buying the toxic waste so JPMorgan could acquire the rest. Even with this sweetener, Dimon insisted on a price that reflected the risks: $2 per share, or less than 7 percent of Bear Stearns' market value just two days before.

The announcement on Sunday, March 16, sent shockwaves through the financial world. Bear's stock had traded at $172 a share as late as January 2007, and $93 a share as late as February 2008. Now it was being sold for less than the price of a cup of coffee. The message was clear: no financial institution was safe.

But there was a problem with the hastily drafted agreement—a potentially catastrophic one. JPMorgan's lawyers had made an error: the guarantee of Bear's trading obligations was binding immediately, but the merger required shareholder approval that could take weeks. JPMorgan could be on the hook for Bear's liabilities even if shareholders rejected the deal. Dimon was described as being "apoplectic" about the mistake.

The solution was to renegotiate. A week later, JPMorgan raised its offer to $10 a share, partly to ensure shareholder approval and partly to address the legal vulnerability. The Fed's support remained at $30 billion. Even at the higher price, it was a steal—if JPMorgan could manage the risks.

Dimon's approach to integration was surgical. Unlike the chaotic Citigroup mergers he'd witnessed, this would be methodical. He divided Bear's businesses into three categories: keep, kill, or sell. Prime brokerage, despite client defections, was a keeper—it fit perfectly with JPMorgan's ambitions. The mortgage trading desk, ground zero for toxic assets, would be wound down. Everything else would be evaluated on its merits.

The human cost was severe. Of Bear's 14,000 employees, thousands would lose their jobs. Dimon didn't sugarcoat it. In a town hall with Bear employees, he was blunt: "This isn't a merger of equals. You were bought because you were failing. Some of you will stay, many won't. Those who stay need to adapt to our culture immediately."

But Dimon also saw opportunity. Bear had talented bankers, valuable client relationships, and prime Manhattan real estate. Integrated properly, these assets could accelerate JPMorgan's growth by years. The key was speed—move fast enough that competitors couldn't poach clients or talent.

As spring turned to summer, the wisdom of the acquisition seemed confirmed. JPMorgan completed the acquisition on May 30, 2008. The integration was proceeding smoothly. The Fed's support had contained the immediate crisis. Markets had stabilized. Dimon was hailed as Wall Street's savior, the banker who stepped up when the system needed him.

Then came September.

Lehman Brothers collapsed on September 15, triggering the full-scale financial crisis that Bear Stearns had merely previewed. But while other banks scrambled for survival, JPMorgan was ready. The Bear Stearns acquisition, for all its challenges, had given Dimon and his team invaluable experience in crisis management. They knew how to evaluate distressed assets quickly. They had relationships with regulators. They had capital to deploy.

When Washington Mutual failed on September 25, 2008, JPMorgan was ready. They acquired WaMu's banking operations for $1.9 billion, adding 2,200 branches and $300 billion in assets. It was the largest bank failure in U.S. history, but for JPMorgan, it was just another opportunity to grow stronger while competitors weakened.

The government's response to the crisis—TARP funds, stress tests, enhanced regulation—treated all banks as if they were equally weak. But JPMorgan wasn't weak. It took $25 billion in TARP funds not because it needed them but because regulators insisted all major banks participate to avoid stigmatizing the weak. JPMorgan repaid the funds as soon as allowed, in June 2009.

But the real cost of Bear Stearns wouldn't become clear for years. JPMorgan faced more than $19 billion in mortgage and crisis-related legal costs, with about 70% tied to Bear Stearns and Washington Mutual. The sins of the acquired were visited upon the acquirer. Every bad mortgage Bear had written, every deceptive practice, every corner cut became JPMorgan's liability.

"No we would not do something like Bear Stearns again — in fact I don't think our Board would let me take the call," Dimon would later write to shareholders. The deal that had seemed like opportunistic genius in 2008 looked more like a poisoned chalice by 2015.

Yet the acquisition fundamentally transformed JPMorgan Chase. It demonstrated that the bank could act decisively in a crisis, absorb massive operations quickly, and work effectively with regulators. It established Dimon not just as a successful banker but as a quasi-governmental figure—the private sector's first responder in financial emergencies.

The Bear Stearns acquisition also crystallized a new reality in American finance: the age of "too big to fail" had officially arrived. When institutions became distressed, they wouldn't be allowed to collapse in disorderly fashion. Instead, they would be absorbed by the strong, making the strong even stronger. The logic was compelling—better concentration than contagion—but the implications were profound.

JPMorgan Chase emerged from the crisis not just intact but dominant. It had demonstrated that it could digest any competitor, manage any risk, navigate any crisis. The bank that had saved Bear Stearns from collapse had saved itself from mediocrity. In the process, it had become something new: not just a bank, but a pillar of the system itself—too big to fail, too important to constrain, too powerful to challenge.

VII. The Dimon Decade: Consolidating Power (2009–2020)

Jamie Dimon stood before 300 managing directors in the JPMorgan Chase auditorium on May 14, 2012. Four days earlier, he had announced $2 billion in trading losses through "egregious mistakes" in what would become known as the London Whale scandal. The man who had navigated the financial crisis without a single quarterly loss now faced his biggest self-inflicted wound.

"Less than a month ago, CEO Jamie Dimon called media coverage of this trade 'a tempest in a teapot.'" Now he stood before his top executives, visibly angry—not just at the traders who had lost billions, but at himself for not seeing it coming. "The portfolio has proved to be riskier, more volatile and less effective as an economic hedge than we thought," Dimon said. "There were many errors, sloppiness and bad judgment."

The losses would eventually total $6.2 billion, triggering $920 million in fines to US and UK authorities and threatening to undermine everything Dimon had built since 2005. But the London Whale was just one crisis in what would become a decade of consolidating power while navigating an increasingly hostile regulatory environment.

The post-crisis world that emerged after 2009 was paradoxical for JPMorgan Chase. On one hand, the bank had proven its superiority during the crisis, emerging stronger while competitors faltered. On the other, it faced unprecedented scrutiny from regulators determined to ensure that 2008 never happened again.

Dodd-Frank, signed into law in July 2010, fundamentally changed the banking landscape. The Volcker Rule banned proprietary trading. The Consumer Financial Protection Bureau added a new layer of oversight. Stress tests became annual public spectacles where banks had to prove they could survive hypothetical disasters.

For most banks, these regulations were constraints. For Dimon, they were competitive advantages. JPMorgan's scale meant it could afford the armies of compliance officers that smaller banks couldn't. Its technology infrastructure could handle the reporting requirements that overwhelmed regional competitors. What was meant to constrain the megabanks actually created a moat around them.

But first, Dimon had to clean up the crisis's aftermath. The mortgage-related settlements were staggering. In November 2013, JPMorgan agreed to a $13 billion settlement with the Justice Department—the largest settlement with a single entity in American history. In a 2015 letter to shareholders, Dimon wrote that the bank's legal costs related to mortgage-backed securities totaled nearly $19 billion, 70 percent of which he said came — not from bad acts at JPMorgan — but from Bear Stearns and another bank it'd acquired, Washington Mutual.

The irony was bitter. JPMorgan was being punished for the sins of the companies it had acquired at the government's request during the crisis. "I think having pressed JPMorgan Chase to take over Bear Stearns, it was unfair to penalize them for the bad acts," said former U.S. Rep. Barney Frank, who co-authored the Dodd-Frank reforms.

Yet even as legal costs mounted, JPMorgan's underlying business was thriving. The bank was gaining market share in virtually every business line. Investment banking fees were growing. The retail network was expanding. Trading revenues, despite new restrictions, remained robust.

The London Whale incident in 2012 was particularly galling because it was self-inflicted. Trader Bruno Iksil, nicknamed the London Whale, accumulated outsized CDS positions in the market. What was supposedly a hedging strategy in the Chief Investment Office had morphed into a massive directional bet.

The trade's discovery revealed multiple failures. Risk models had been manipulated—Manual data entry and copying and pasting of data in Excel spreadsheets were inherently risky practices. Traders had hidden losses. Management had been kept in the dark. For a bank that prided itself on risk management, it was humiliating.

JPMorgan Chase cut chief executive Jamie Dimon's 2012 pay in half, from US$23 million to $11.5 million, as a consequence for the $6 billion trading loss. But the real punishment was reputational. The bank that had been the gold standard for risk management now looked fallible.

Dimon's response was characteristic: take responsibility, fix the problem, move forward. The Chief Investment Office was restructured. Risk controls were tightened. The traders responsible were terminated. Neither the Whale himself, Bruno Iksil, nor any senior managers faced criminal charges. (Iksil, who says the losses weren't his fault, is cooperating with prosecutors.)

But the London Whale had broader implications. It gave ammunition to those arguing for stricter regulations. It demonstrated that even the best-managed banks could lose billions on a single trade. Most importantly, it showed that the complexity of modern banking had outpaced the ability of even sophisticated managers to fully understand their risks.

Yet JPMorgan's response to the crisis demonstrated its institutional strength. While the London Whale dominated headlines, the bank was quietly building capabilities that would define the next decade. Technology spending ramped up dramatically. Digital banking platforms were launched. Data analytics capabilities were enhanced.

The bank was also consolidating its dominance in traditional banking. In investment banking, JPMorgan consistently ranked first or second globally in fees. In trading, despite the Volcker Rule restrictions, it maintained leading positions in currencies, rates, and credit. In retail banking, it was gaining share in deposits, mortgages, and credit cards.

Dimon's management philosophy evolved during this period. The brash cost-cutter of the Bank One days had become more strategic, more political, more conscious of JPMorgan's systemic importance. His annual shareholder letters became must-read documents—part financial analysis, part policy prescription, part philosophical treatise on American capitalism.

He positioned JPMorgan not just as a bank but as a national champion. When America needed infrastructure investment, JPMorgan was ready to finance it. When small businesses needed support, JPMorgan was there with lending programs. When communities were struggling, JPMorgan announced philanthropic initiatives.

This wasn't just public relations. Dimon understood that JPMorgan's success was inextricably linked to public perception and political support. A bank deemed too big to fail needed to demonstrate why its existence benefited society, not just shareholders.

The financial performance validated the strategy. By 2019, JPMorgan was earning over $36 billion annually—more than the GDP of many countries. Return on tangible equity consistently exceeded 15%. The stock price had more than tripled since Dimon became CEO.

But new challenges were emerging. Technology companies were encroaching on traditional banking. Cryptocurrencies threatened the payments system. Fintech startups were unbundling banking services. Climate change was creating new risks and opportunities.

Dimon's response was to embrace disruption rather than resist it. JPMorgan's technology budget ballooned to over $11 billion annually. The bank hired thousands of technologists. It launched digital-only banking products. It even created its own cryptocurrency, JPM Coin, for institutional payments.

The approach to talent also evolved. JPMorgan began competing directly with Silicon Valley for engineers and data scientists. It established innovation labs. It partnered with fintech companies. The bank that had once been the embodiment of traditional finance was transforming itself into a technology company that happened to have a banking license.

By early 2020, JPMorgan Chase stood at the apex of global finance. It was the most valuable bank in the world by market capitalization. It had weathered the financial crisis, the European debt crisis, the London Whale, billions in legal settlements, and countless regulatory changes. Under Dimon's leadership, it had not just survived but thrived.

Then came COVID-19, and with it, another opportunity for JPMorgan to demonstrate why it had become indispensable to the American economy. The pandemic would test every institution, but for JPMorgan, it would become another chance to consolidate power while serving as the financial system's anchor in turbulent times.

VIII. Modern Dominance & Strategic Positioning (2020–Present)

On March 10, 2020, Jamie Dimon stood in an emergency operations center that JPMorgan had activated for the first time since Hurricane Sandy in 2012. But this threat wasn't a storm—it was COVID-19, and within days, the entire global economy would shut down in ways no one had imagined possible.

"We need to be prepared to operate the entire bank remotely," Dimon told his leadership team. "Not for weeks. For months, maybe longer." Within 72 hours, JPMorgan would send home 200,000 employees—the largest remote work transition in banking history.

The pandemic represented a unique test for JPMorgan Chase. Unlike 2008, this wasn't a financial crisis—it was a health crisis that became an everything crisis. The bank would need to serve as both a commercial enterprise and a quasi-governmental institution, channeling federal relief while maintaining its own operations.

The Paycheck Protection Program (PPP) became JPMorgan's first major pandemic challenge. When the program launched on April 3, 2020, the Small Business Administration's systems crashed within hours. JPMorgan had built its own platform, anticipating the government's technology wouldn't handle the volume. Even so, the bank processed 280,000 applications in the first round alone, ultimately distributing over $30 billion to small businesses.

But PPP also exposed the tensions in JPMorgan's role. Smaller banks accused it of prioritizing larger clients. Politicians criticized it for taking a fee on government-guaranteed loans. The bank that had positioned itself as essential to America's economy found itself defending its very success.

Dimon himself became a pandemic casualty—not from the disease, though he would later contract COVID, but from emergency heart surgery in March 2020. The timing couldn't have been worse. As he recovered, his lieutenants ran the bank through the most volatile markets in history. Trading revenues soared as volatility spiked. Credit losses, surprisingly, remained manageable as government stimulus kept consumers afloat.

What emerged from the pandemic was a JPMorgan Chase that had proven its digital transformation was real. Branches had closed, but mobile banking usage exploded. Traders worked from kitchen tables but still executed billions in daily volume. The bank that had spent $14 billion annually on technology found that investment validated overnight.

The pandemic also accelerated trends that had been building for years. Digital payments exploded. Cryptocurrency went mainstream. Fintech valuations soared. Every assumption about banking—that it required physical presence, that customers needed branches, that traders needed trading floors—was challenged.

Dimon's response was characteristic: lean into change. JPMorgan launched Chase UK, a digital-only bank competing directly with fintech challengers. It acquired Nutmeg, a robo-advisor. It built JPM Coin for institutional blockchain payments. The bank that traced its roots to 1799 was reimagining itself for the digital age.

But technology investments were just part of the strategy. When the regional banking crisis erupted in March 2023, the government again turned to JPMorgan. "Our government invited us and others to step up, and we did," said Jamie Dimon, Chairman and CEO of JPMorgan Chase, after acquiring First Republic Bank.

First Republic is the largest U.S. lender to fail since Washington Mutual in 2008, which was also acquired by JPMorgan Chase. The parallels were uncanny—another bank failure, another weekend rescue, another expansion of JPMorgan's empire. But this time was different. The 2023 regional banking crisis wasn't about subprime mortgages or complex derivatives. It was about simple duration risk—banks had bought long-term bonds when rates were low, and those bonds had lost value as rates rose.

JPMorgan Chase acquired the substantial majority of assets and assumed the deposits and certain other liabilities of First Republic Bank from the Federal Deposit Insurance Corporation (FDIC). As part of the purchase, JPMorgan Chase is assuming all deposits – insured and uninsured. The acquisition included the "assumption of approximately $92 billion of deposits" held by First Republic and the acquisition of about $173 billion of its loans and around $30 billion of its securities."

The transaction is expected to be modestly EPS accretive and generate more than $500 million of incremental net income per year, not including the approximately $2.6 billion one-time post-tax gain or approximately $2.0 billion of post-tax restructuring costs expected over the course of 2023 and 2024. Once again, JPMorgan was profiting from others' distress while positioning itself as the system's savior.

The First Republic acquisition highlighted a fundamental tension in modern banking. JPMorgan's acquisition of First Republic means further consolidation in a banking sector that has already been marked by the dominance of "too-big-to-fail" institutions. "JPMorgan Chase is now too big to be 'too-big-to-fail,'" Gordon said. The bank that was already the largest in America had gotten even larger, absorbing its competitors whenever they faltered.

JPMorgan Chase had $3.7 trillion in assets and $303 billion in stockholders' equity as of March 31, 2023. To put this in perspective, JPMorgan's assets exceeded the GDP of Germany. Its market capitalization was larger than the entire banking sectors of most countries. It had become not just a bank but a parallel financial system.

The modern JPMorgan Chase operates at a scale that would have been incomprehensible to J.P. Morgan himself. It serves 84 million U.S. consumers and 7 million small businesses. It processes $10 trillion in payments daily—more than 40% of America's GDP moving through its systems every single day. When JPMorgan's technology has even minor issues, entire sectors of the economy feel the impact.

The bank's technology transformation has been staggering. It employs over 50,000 technologists—more than most Silicon Valley giants. It runs 35 data centers globally, processing 5 billion transactions daily. Its mobile app has become the primary banking interface for tens of millions of Americans. The bank that Aaron Burr created to circumvent banking restrictions has become the digital backbone of American commerce.

But scale brings scrutiny. Regulators worry about concentration risk—what happens if JPMorgan fails? Politicians question whether any institution should have this much power. Competitors argue that JPMorgan's advantages—regulatory capture, funding advantages, too-big-to-fail status—create an unfair playing field.

Dimon addresses these concerns directly but without apology. In his view, America needs large banks to compete globally. Chinese banks are larger. European banks are consolidating. If America fragments its banking system, it will lose global financial leadership. JPMorgan's size isn't a bug—it's a feature, essential for America's economic competitiveness.

The bank's strategic positioning for the future reflects this global ambition. JPMorgan is investing heavily in Asia, where it sees the next century's growth. It's building quantum computing capabilities for trading and risk management. It's developing AI systems that can predict credit losses before they materialize. The bank is preparing not just for the next crisis but for the next era of finance.

Climate change has become a central focus, though Dimon's approach is pragmatic rather than ideological. JPMorgan finances both renewable energy and fossil fuels, arguing that the transition must be gradual and realistic. The bank has committed $2.5 trillion to sustainable development through 2030, but it also remains the largest financier of oil and gas projects. This balance—or contradiction, depending on perspective—reflects JPMorgan's fundamental nature: commercially driven but systemically important.

The modern Chase retail experience has also transformed. Branches still exist but serve different purposes—advisory rather than transactional. The bank has opened new formats: smaller locations in urban centers, advisory offices for wealth management, community centers that offer financial education. Physical banking hasn't disappeared; it's evolved.

Meanwhile, the investment bank continues to dominate. JPMorgan consistently ranks first or second globally in investment banking fees. Its trading operations, despite Volcker Rule restrictions, generate billions in revenue. The firm that once saved America's railroads now advises on trillion-dollar technology mergers and finances the companies reshaping the global economy.

As 2024 progresses, JPMorgan Chase stands at an inflection point. Interest rates are normalizing, benefiting the bank's core lending business. Technology disruption continues, but JPMorgan has proven it can compete with fintech challengers. Regulatory pressure persists, but the bank has shown it can turn compliance into competitive advantage.

The question isn't whether JPMorgan will remain dominant—that seems assured. The question is whether American society is comfortable with this dominance. Can a single institution be this powerful in a democracy? Should any bank be too big to fail? These aren't new questions, but they become more urgent as JPMorgan's power grows.

What's certain is that JPMorgan Chase has achieved something unprecedented in American capitalism. It has become simultaneously the most regulated and most profitable bank, the most systemic and most innovative, the most criticized and most essential. It embodies all the contradictions of modern finance: private but public, competitive but collaborative, American but global.

The empire that began with Aaron Burr's deception has become, quite literally, the foundation of the American financial system. Whether this represents capitalism's greatest success or its fundamental failure depends on your perspective. But there's no denying the reality: JPMorgan Chase isn't just too big to fail—it's too integral to even imagine failing.

IX. Playbook: The JPMorgan Chase Operating System

In the executive conference room at 270 Park Avenue, Jamie Dimon regularly holds what insiders call "boot camps"—grueling, six-hour sessions where business unit heads defend every line item in their budgets, every strategic decision, every basis point of return. One executive described it as "intellectual combat," where assumptions are challenged, sacred cows are slaughtered, and only data-driven arguments survive.

This is the JPMorgan Chase operating system in microcosm: relentless, meritocratic, and obsessed with what Dimon calls "the fortress balance sheet." But understanding how JPMorgan actually works—how it consistently generates 15-20% returns on tangible equity while competitors struggle, how it gains market share in crisis while others retreat—requires unpacking a management philosophy that's part military discipline, part Silicon Valley iteration, and part old-fashioned banking prudence.

The fortress balance sheet isn't just a marketing phrase—it's a religion. Tangible Common Equity has grown significantly, with a compound annual growth rate (CAGR) of 9% since 2005. Jamie Dimon, the CEO of JPMorgan & Co, who came up with the term describes it as a balance sheet that has the ability to withstand financial shocks while giving companies flexibility in deal-making. The term implies a company making its balance sheet shockproof by building liquidity.

But what does this actually mean in practice? It means holding more capital than regulations require—not because regulators demand it, but because Dimon believes excess capital is cheap insurance against black swans. It means maintaining liquidity buffers that could fund the bank for months even if all funding markets froze. It means stress-testing not just for regulatory scenarios but for "Dimon scenarios"—what if unemployment hits 15%? What if commercial real estate values fall 50%? What if multiple major counterparties fail simultaneously?

This conservatism seems paradoxical for a bank that consistently generates industry-leading returns. The secret is operational excellence that creates room for the fortress. JPMorgan Chase demonstrates strong efficiency with a lower overhead ratio compared to peers. The bank's ROTCE is competitive. While competitors might generate similar gross returns, JPMorgan's efficiency ratio—the cost of generating each dollar of revenue—is consistently lower. This efficiency doesn't come from cutting corners but from scale, technology, and ruthless process optimization.

Consider how Dimon approaches decision-making. In his shareholder letters, he repeatedly emphasizes core principles: "Assess everything honestly, assemble effective leadership team, have humility, have grit." But the real insight comes from his approach to data: "Don't try to use numbers to prove what you think. Try to use numbers to understand what you are doing."

This manifests in JPMorgan's famous "morning call"—a 7:15 AM daily ritual where senior executives review every major position, every significant risk, every market movement. Unlike the theatrical morning meetings at some banks, JPMorgan's call is clinical. Positions are marked to market ruthlessly. Losses are acknowledged immediately. There's no hiding behind hopeful projections or complex explanations.

The risk management philosophy extends beyond trading floors. Every business line has embedded risk officers who report both to business heads and to independent risk management. This dual reporting creates natural tension—business wants to grow, risk wants to protect—but Dimon sees this tension as healthy. "If everyone agrees all the time, someone's not doing their job," he's fond of saying.

Technology isn't just support at JPMorgan—it's the business. The bank spends $14 billion annually on technology, with half dedicated to new investments. But unlike banks that outsource to vendors or rely on consultants, JPMorgan builds internally. They employ over 50,000 technologists, run 35 data centers, and process 5 billion transactions daily. This isn't about having the latest technology—it's about owning the entire stack, controlling every element of the customer experience.

The integration philosophy is equally distinctive. While most banks struggle for years to integrate acquisitions, JPMorgan has turned integration into a core competency. The playbook is consistent: identify synergies before the deal closes, appoint integration leaders with real authority, set aggressive timelines with specific milestones, and measure everything obsessively.

When JPMorgan acquired Bank One, Dimon unified seven different deposit systems into one. When it bought Washington Mutual, it converted 2,200 branches over a single weekend. When it acquired First Republic, it retained 90% of clients within six months. This isn't luck—it's systematic execution of a refined process.

The cross-selling machine at JPMorgan is perhaps the most sophisticated in banking. But unlike the aggressive, quota-driven cross-selling that destroyed Wells Fargo's reputation, JPMorgan's approach is data-driven and client-centric. The bank knows that a client who uses five products is exponentially more profitable and loyal than one who uses two. But rather than pushing products, they use analytics to identify genuine needs.

A small business client taking out a loan might be offered cash management services—not because there's a quota, but because the data shows similar businesses benefit from these services. A wealthy individual with a checking account might be introduced to private banking—not randomly, but because their transaction patterns suggest complex financial needs. This seems obvious, but executing it across 84 million consumers requires extraordinary technological sophistication.

Capital allocation at JPMorgan follows what Dimon calls "intelligent conservatism." The bank maintains capital ratios well above regulatory minimums, but this isn't dead money. It's optionality. When Silicon Valley Bank failed, JPMorgan had the capital to bid immediately. When markets dislocate, JPMorgan has the balance sheet to provide liquidity and earn extraordinary returns. The fortress balance sheet isn't just defense—it's the foundation for opportunistic offense.

The approach to regulation is similarly strategic. While peers complain about regulatory burden, JPMorgan has turned compliance into competitive advantage. The bank employs thousands of compliance officers, spends billions on regulatory technology, and maintains relationships with regulators globally. This isn't just about avoiding fines—it's about being the bank regulators trust in a crisis.

When regulators need a private sector partner to execute a rescue, they call JPMorgan. When new regulations are being drafted, JPMorgan's input is sought. When systemic risks emerge, JPMorgan's views carry weight. This influence isn't bought—it's earned through decades of competent execution and constructive engagement.

Talent management at JPMorgan reflects Dimon's meritocratic philosophy. The bank recruits aggressively from top schools but also promotes internally. Performance reviews are brutal in their honesty. High performers are rewarded generously; underperformers are managed out quickly. There's little patience for politics or bureaucracy. "Bad news travels fast here," one executive noted. "Good news travels faster."

Dimon's own management style sets the tone. He reads voraciously—not just financial reports but history, biography, science. He can discuss the minutiae of credit card processing or the geopolitics of Asian banking with equal fluency. He's known for calling branch managers directly, for dropping into trading floors unannounced, for reading customer complaint letters personally.

This hands-on approach scales through what JPMorgan calls "cascading accountability." Every major initiative has a senior sponsor who's personally accountable to Dimon. That sponsor has direct reports who own specific workstreams. Those managers have teams with clear deliverables. Everyone knows what they own, what success looks like, and what happens if they fail.

The customer acquisition strategy differs by business line but follows consistent principles. In retail banking, it's about convenience and trust—more branches, better apps, superior service. In investment banking, it's about capability and execution—can JPMorgan execute a complex cross-border M&A deal better than competitors? In asset management, it's about performance and stability—can JPMorgan deliver consistent returns with lower volatility?

But the real competitive advantage might be integration. A corporate client doing an IPO might also need foreign exchange hedging, cash management, and employee stock plan administration. A wealthy entrepreneur selling a business might need investment banking for the transaction, private banking for wealth management, and commercial banking for their next venture. JPMorgan can provide all of these services with seamless handoffs between divisions.

Risk management post-2008 has evolved from defense to competitive advantage. While all banks stress test, JPMorgan stress tests more scenarios. While all banks have risk limits, JPMorgan's are more granular. While all banks mark to market, JPMorgan does it more frequently and more conservatively. This isn't paranoia—it's preparation.

The bank maintains what it calls a "risk appetite framework"—a detailed document defining exactly what risks the bank will and won't take. Unlike the vague risk statements at many banks, JPMorgan's framework includes specific metrics, clear escalation procedures, and regular updates based on market conditions. Every trader knows their limits. Every lender knows their authority. Every executive knows their boundaries.

The approach to innovation is pragmatic rather than revolutionary. JPMorgan doesn't try to be first—it tries to be best. When blockchain emerged, JPMorgan didn't launch a cryptocurrency. Instead, it built JPM Coin for institutional payments—a practical application of new technology to an existing business need. When fintech challengers emerged, JPMorgan didn't panic. It studied them, hired talent from them, and then built better versions of their products with JPMorgan's scale advantages.

This measured approach to innovation extends to partnerships and acquisitions. JPMorgan partners with fintechs when it makes sense but builds internally when core capabilities are at stake. The bank acquires selectively, focusing on capabilities or assets it can't build efficiently. Every decision is filtered through a simple question: does this make our fortress stronger?

The JPMorgan Chase operating system isn't perfect. The bank's size creates complexity that even superior management struggles to control. The London Whale showed that even JPMorgan can lose billions on a single trade. The mortgage settlements proved that even JPMorgan can't fully control the actions of acquired entities. But what distinguishes JPMorgan isn't the absence of problems—it's the speed and effectiveness of response.

When problems emerge, JPMorgan acknowledges them quickly, fixes them systematically, and learns from them institutionally. This combination—fortress balance sheet, operational excellence, strategic clarity, and learning culture—creates a system that's remarkably resilient. It's not unbreakable, but it's the closest thing to unbreakable that modern banking has produced.

X. Analysis & Investment Case

The investment case for JPMorgan Chase presents a paradox: it's simultaneously the most obvious and most complex bet in American finance. Obvious because the bank's dominance seems unassailable—$800 billion market cap, consistent 15-20% returns on tangible equity, growing market share across all business lines. Complex because that very dominance creates unique risks that could fundamentally alter the investment thesis.

Start with the moat, which is less a single barrier than a series of interlocking fortifications. Scale is the most visible: JPMorgan processes $10 trillion in payments daily, giving it unmatched insight into economic activity and customer behavior. This data advantage compounds—better data enables better credit decisions, which generate superior returns, which fund more technology investment, which captures more data. It's a virtuous cycle that competitors can't replicate without similar scale.

But scale alone doesn't explain JPMorgan's premium valuation. Citigroup has scale. Bank of America has scale. What JPMorgan has is scale plus execution. We earned revenue in 2024 of $180.6 billion1 and net income of $58.5 billion, with return on tangible common equity (ROTCE) of 20%2, reflecting strong underlying performance across our businesses. This isn't just about being big—it's about converting size into superior returns consistently.

The regulatory moat might be even more powerful than scale. JPMorgan operates under the most stringent regulations in global banking—higher capital requirements, more intensive supervision, constant stress testing. But what's meant to constrain has become a barrier to entry. Smaller banks can't afford the compliance infrastructure. Foreign banks struggle with the complexity. Even large American rivals find the regulatory burden challenging. JPMorgan has turned regulation from headwind into moat.

Consider the numbers: JPMorgan employs over 3,000 compliance officers and spends roughly $3 billion annually on compliance technology and personnel. For a bank with $180 billion in revenue, that's manageable. For a regional bank with $5 billion in revenue, proportional spending would be crippling. The regulatory framework designed to constrain megabanks has instead protected them.

Network effects amplify these advantages. Consumer & Community Banking serves 84M U.S. consumers and 7M small businesses. Each customer relationship creates data, reduces acquisition costs for additional products, and increases switching costs. A small business using JPMorgan for checking, credit cards, loans, and cash management won't switch banks to save 10 basis points on a loan. The inconvenience overwhelms the savings.

The investment banking franchise operates on similar dynamics. Commercial & Investment Bank ranks #1 in global investment banking fees for 16 consecutive years. CEOs choose JPMorgan for critical transactions not because it's cheapest but because it has the highest probability of successful execution. This reputation took decades to build and would take decades to erode.

Technology spending has become another moat. At $14 billion annually, JPMorgan's technology budget exceeds the total revenue of many fintech unicorns. But it's not just the amount—it's the focus. Half goes to new investments, creating capabilities competitors can't match. JPMorgan's mobile app isn't just competitive with fintech challengers—it's better, with more features, better security, and seamless integration with other services.

The bear case, however, is compelling in its own right. Start with regulatory risk—not traditional regulatory risk of fines or restrictions, but existential regulatory risk. What if populist politics leads to breaking up the megabanks? What if capital requirements increase to levels that destroy returns? What if the government decides no bank should have more than $500 billion in assets?

These aren't fantasy scenarios. Senators from both parties have proposed variations of these ideas. The political appeal is obvious: David versus Goliath, Main Street versus Wall Street, democracy versus oligarchy. JPMorgan's very success makes it a target. The bank that's too big to fail might also be too big to tolerate in a democracy.

Size constraints present another challenge. JPMorgan already has 10% of American deposits—the legal maximum. It can't acquire another large U.S. bank without divesting assets. Organic growth is limited by market size. International expansion faces regulatory and competitive challenges. Where does growth come from when you're already everywhere?

The succession question looms largest. Dimon turns 69 in 2025. He's been CEO since 2005, the longest-serving major bank CEO. He's repeatedly said he'll stay five more years, but he's been saying that for five years. The succession plan remains opaque. The bench is deep—Jennifer Piepszak, Troy Rohrbaugh, Mary Erdoes are all capable executives—but none have Dimon's combination of technical mastery, political savvy, and crisis credibility.

History suggests CEO transitions at megabanks are treacherous. Bank of America struggled for years after Hugh McColl retired. Citigroup cycled through CEOs after Sandy Weill. Even JPMorgan stumbled between David Rockefeller and Dimon. The institution is strong, but the Dimon premium in the stock price is real and will evaporate when he leaves.

Technology disruption presents a different threat. While JPMorgan has successfully competed with fintech challengers so far, the next wave might be different. Central bank digital currencies could disintermediate commercial banks entirely. Cryptocurrency could create parallel financial systems. Big Tech companies have the scale and technology to compete if regulations allow.