Jacobs Solutions: From One-Man Shop to Global Engineering Powerhouse

I. Introduction & Episode Roadmap

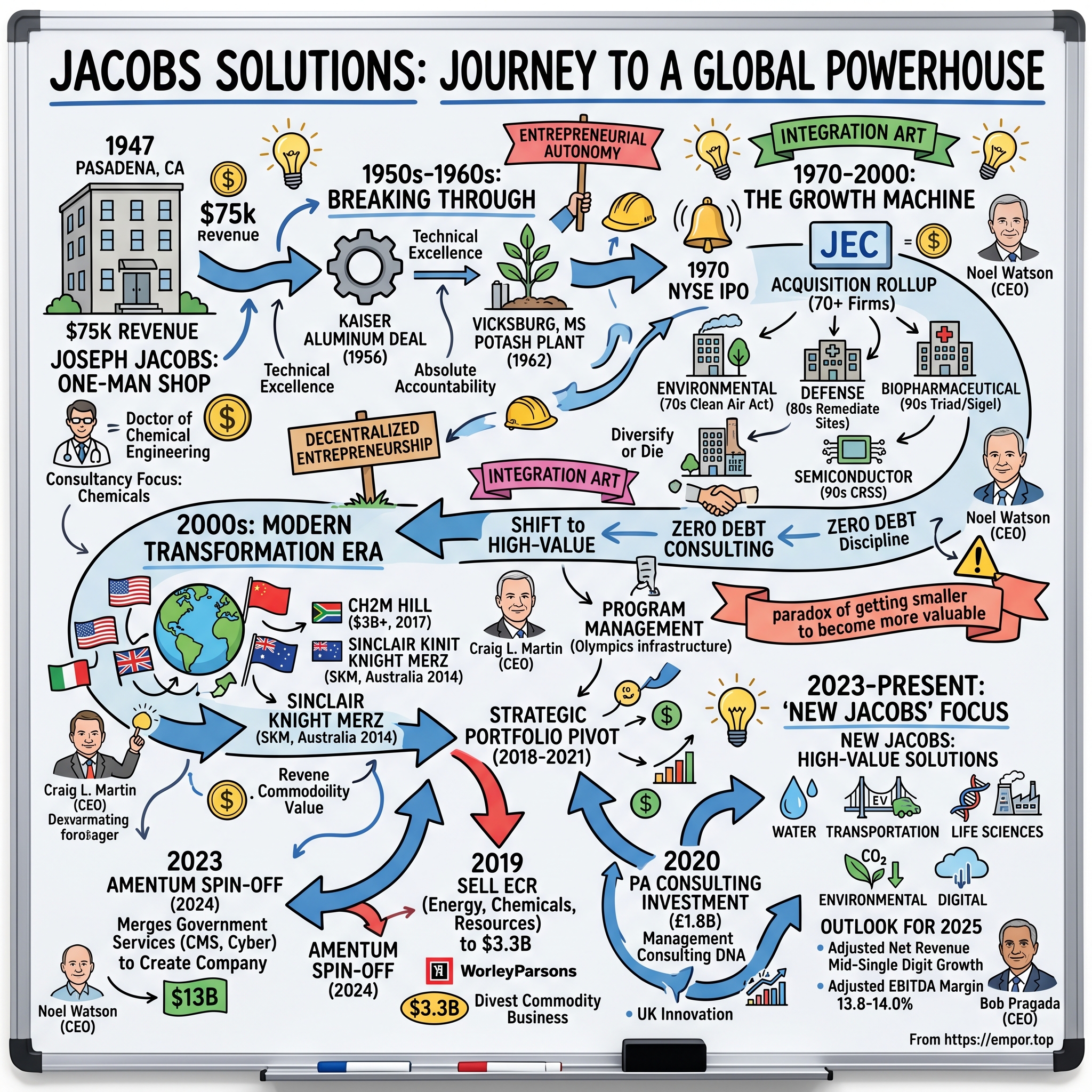

Picture this: It's 1947 in Pasadena, California. A young chemical engineer with a doctorate from Brooklyn sits alone in a tiny office, armed with nothing but a slide rule, a telephone, and an unshakeable belief that American industry needs better engineering consulting. Joseph Jacobs has just quit his secure job at Merck & Company—where he helped develop penicillin and DDT during World War II—to start his own consultancy. His first-year revenue? A modest $75,000. Fast forward to today, and that one-man operation has morphed into Jacobs Solutions, a $12 billion revenue colossus with 45,000 employees spanning the globe. The story of Jacobs is really three transformations woven into one: from consultant to constructor, from constructor to conglomerate, and finally—in a dramatic recent pivot—from conglomerate to focused high-value solutions provider. With approximately $12 billion in annual revenue and a talent force of almost 45,000, the company that trades under the simple ticker "J" on the NYSE represents one of the most successful yet underappreciated business metamorphoses in American engineering.

But here's what makes Jacobs fascinating for students of business strategy: unlike the typical Silicon Valley disruption narrative, this is a story of patient accumulation, strategic retreats, and the rare corporate courage to sell crown jewel assets at their peak. It's about knowing when to zag while competitors zig, when to buy aggressively, and perhaps most importantly, when to walk away from billions in revenue to chase higher margins.

This is also a story about timing—how a company founded in the shadow of World War II rode successive waves of American industrial expansion: the chemical boom of the 1950s, the environmental movement of the 1970s, the defense buildup of the 1980s, the infrastructure renaissance of the 2000s, and now, the sustainability revolution of the 2020s. Each era demanded different capabilities, and Jacobs, like a corporate chameleon, adapted.

Over the next several hours, we'll unpack how Joseph Jacobs' one-man shop evolved into today's global powerhouse, examining the pivotal decisions, near-death experiences, and strategic masterstrokes that shaped its journey. We'll explore why Jacobs chose to spin off a $6 billion government services business at its peak, how it turned a struggling Australian engineering firm into a transformative acquisition, and what its recent pivot toward consulting tells us about the future of professional services.

The themes we'll return to throughout: the power of decentralized entrepreneurship, the art of integration, and the paradox of getting smaller to become more valuable. Because in the end, Jacobs' story challenges the conventional wisdom that bigger is always better—sometimes, the boldest move is knowing what to leave behind.

II. Joseph Jacobs: The Immigrant's Son Who Built an Empire

The Brooklyn tenement was cramped, the walls thin enough to hear the neighbors arguing in three different languages. It was 1925, and thirteen-year-old Joseph Jacobs was hunched over his chemistry textbook, trying to block out the noise. His father, a Lebanese immigrant who'd made a small fortune selling straight razors to American doughboys during World War I, had just watched his wealth evaporate with the invention of the safety razor. The family's reversal of fortune was swift and brutal—from comfortable middle class to scraping by in a matter of months.

"You must study, Joseph," his mother would say in her accented English, pressing him back to his books whenever he mentioned dropping out to work. "Education is the only thing they cannot take from you." It was a refrain that would echo through his life, driving him to not just survive the Great Depression but to build something that would outlast him by generations.

Joseph John Jacobs was born in Brooklyn in 1916, the son of Lebanese immigrants who embodied the American dream's promise and peril. His father had arrived in America with little more than ambition, building a small empire selling straight razors during World War I when every soldier needed a clean shave. But innovation is merciless—Gillette's safety razor destroyed the family business almost overnight. Young Joseph watched his father struggle to reinvent himself, a lesson in adaptability that would prove prophetic.

Despite the family's financial struggles, Jacobs' mother insisted on education above all else. He enrolled at the Polytechnic Institute of Brooklyn (now NYU Tandon), working nights and weekends to pay tuition. The year was 1933—the depths of the Great Depression—and even washing dishes felt like winning the lottery compared to the breadlines outside. Jacobs graduated in 1937 with a chemical engineering degree, but jobs were scarcer than hope.

Unable to find steady work, Jacobs made a counterintuitive decision: go deeper into academia. He began teaching at Polytechnic while pursuing graduate degrees, living on a stipend that barely covered rent. But the classroom became his laboratory for understanding how to explain complex technical concepts simply—a skill that would later prove invaluable when pitching to industrial clients. By 1942, he'd earned his doctorate in chemical engineering, just as America's war machine was spinning up.

His timing was impeccable. Merck & Company in Rahway, New Jersey, was desperately seeking chemical engineers for their wartime production. Jacobs joined as a senior chemical engineer, suddenly thrust into work of national importance: developing processes for mass-producing penicillin (saving countless Allied lives), synthesizing vitamins for soldiers' rations, and even manufacturing DDT (then considered a miracle pesticide for preventing typhus in war zones). The Merck years were Jacobs' finishing school in industrial-scale problem-solving.

But by 1947, something was gnawing at him. The corporate hierarchy at Merck felt stifling. Jacobs watched brilliant ideas die in committee meetings, saw politics trump performance. At age 31, with a pregnant wife and a mortgage, he made the kind of decision that separates entrepreneurs from everyone else: he quit his secure job to start a one-man consulting firm.

The "office" was a card table in his home. The entire staff was him. The business plan fit on a napkin: help chemical companies solve problems they couldn't solve themselves. His first-year revenue was $75,000—respectable for a solo consultant but hardly empire-building money. What Jacobs had, though, was something rarer than capital: a reputation for both technical brilliance and absolute integrity.

His early clients read like a who's who of American industry: Eston Chemical needed help with a production bottleneck, Southwest Potash Company (later AMAX Inc.) wanted to optimize their extraction process, and Kaiser Aluminum & Chemical had heard about this Brooklyn engineer who could solve the unsolvable. Each project was a referendum on his reputation. Jacobs would often work 18-hour days, sleeping on factory floors, personally overseeing every calculation.

The consulting model was deliberately lean. Rather than hiring full-time staff, Jacobs would bring in specialists for specific projects—a radical approach in an era of corporate bloat. This "Hollywood model" (assembling teams for specific productions, then disbanding) would later become Silicon Valley orthodoxy, but in 1940s industrial America, it was heretical.

One early project nearly ended everything. A chemical plant design had a flaw that only revealed itself after construction began. The client was furious, threatening lawsuits. Jacobs mortgaged his house, liquidated his savings, and spent three months on-site fixing the problem at his own expense. The plant eventually worked perfectly. The client, stunned by this display of accountability, became Jacobs' biggest evangelist, referring dozens of future projects.

This pattern—taking personal responsibility for outcomes, not just advice—became the Jacobs Engineering DNA. While competitors hid behind consulting reports, Jacobs would stake his reputation on results. It was a high-wire act that required both technical excellence and nerves of steel. But it worked. By the early 1950s, the one-man shop had grown to a dozen engineers, all hand-picked for both brilliance and what Jacobs called "the religion of responsibility."

The philosophical foundation was set: entrepreneurial culture, technical excellence, and absolute accountability. These weren't just corporate values to be framed on a wall—they were survival mechanisms forged in the crucible of near-failure. As Jacobs would later write in his autobiography, "The difference between success and failure is usually not talent or even hard work—it's the willingness to stake everything on your convictions."

As the 1950s dawned, America was entering its great industrial expansion. The suburban boom needed chemicals for everything from plastics to pesticides. The Cold War demanded strategic materials. The economy was rocket fuel looking for a match. And Jacobs Engineering, still small but now battle-tested, was perfectly positioned for what would become its breakout decade.

III. Breaking Through: The Kaiser Aluminum Deal & Going Big (1950s–1960s)

Henry J. Kaiser was not a patient man. The industrialist who'd built Liberty Ships in four days during World War II was standing in his Oakland office in 1956, frustrated. Kaiser Aluminum needed a massive new alumina plant—the kind of facility that would dwarf anything in the western United States—but his in-house engineers were telling him it couldn't be done with existing technology. "Find me someone who doesn't know it's impossible," he barked at his lieutenants.

That someone turned out to be Joseph Jacobs.

The call came on a Tuesday. By Thursday, Jacobs was on a plane to California with two of his best engineers, sketching preliminary designs on cocktail napkins during the flight. Kaiser Aluminum wanted to build an alumina plant using a novel process that would require engineering capabilities their internal team simply didn't possess. The project fee alone would exceed Jacobs Engineering's entire previous year revenue. It was the kind of opportunity that could transform a boutique consultancy into a real engineering firm—or destroy it entirely.

Jacobs' pitch to Kaiser was audacious in its simplicity: "We've never built anything this big, but neither has anyone else. The difference is, we're not afraid to try." Kaiser, who'd built his empire on similar logic, loved it. The contract was signed within a week.

The Kaiser project required Jacobs to scale faster than ever before. Twenty new designers were hired in a month, many poached from larger competitors with promises of equity and autonomy. Jacobs instituted what he called "the war room"—a vast open space where all the engineers worked together, hierarchies flattened, ideas flowing freely. It was chaotic, exhausting, and wildly effective.

The technical challenges were staggering. The alumina extraction process required precise temperature controls across massive vessels, novel filtration systems, and chemical processes that had only been proven at laboratory scale. Jacobs himself would spend nights recalculating heat transfer equations, catching errors that could have led to catastrophic failures. His attention to detail became legendary—engineers joked that he could spot a misplaced decimal point from across the room.

When the plant came online in 1957, it worked perfectly on the first try—almost unheard of for a facility of its complexity. Kaiser was so impressed that he immediately commissioned two more projects. Word spread through the industrial grapevine: Jacobs Engineering had pulled off the impossible.

But 1962 brought a crisis that nearly ended everything. Southwest Potash had hired Jacobs to build a facility in Vicksburg, Mississippi, using an innovative process for producing potassium nitrate. The plant was Jacobs' most ambitious project yet, incorporating untested technology that promised to revolutionize fertilizer production. When it started up, it failed spectacularly. The chemical reactions weren't proceeding as designed, equipment was corroding at alarming rates, and the output was a fraction of what was promised.

The easy move would have been to blame the theoretical process, collect the consulting fee, and walk away. That's what the lawyers advised. Instead, Jacobs made a decision that would define his company's culture forever: he moved to Vicksburg.

Not visited—moved. Jacobs, along with six of his top engineers, relocated their families to Mississippi for six months. They worked 16-hour days, sleeping in trailers on the plant grounds, personally rebuilding equipment, adjusting processes, testing thousands of variations. Jacobs' wife would bring dinner to the plant, finding her husband covered in chemical residue, obsessing over pressure readings.

The Vicksburg summer was brutal—100-degree heat, humidity that felt like breathing soup, and mosquitoes the size of hummingbirds. The engineers were exhausted, their families strained. Three months in, one of Jacobs' top lieutenants suggested they cut their losses. Jacobs' response became company lore: "We don't build our reputation on successes. We build it on what we do when we fail."

By month five, they had cracked it. The issue wasn't the chemistry but the engineering—subtle interactions between materials and processes that only revealed themselves under real-world conditions. The plant began producing high-quality potassium nitrate at design capacity. Southwest Potash, which had been preparing litigation, instead became Jacobs' most vocal champion, telling everyone who'd listen about the engineering firm that had moved mountains (and families) to make things right.

The Vicksburg victory transformed Jacobs Engineering's reputation from competent to legendary. The story spread through industrial America: here was a firm that would stake everything on client success. New contracts poured in—not because Jacobs was the cheapest or even the most experienced, but because clients knew they would never be abandoned.

By 1967, the company had opened offices in Houston (oil and chemicals), Denver (mining and minerals), and Chicago (manufacturing). But these weren't traditional branch offices. Jacobs instituted what he called "entrepreneurial autonomy"—each office operated almost like an independent company, with its own P&L, its own business development, and most importantly, its own culture adapted to local markets.

The Houston office, for instance, developed a swagger that matched the Texas oil industry—big promises, bigger delivery. The Denver team became known for innovative environmental solutions, crucial as mining companies faced new regulations. Chicago specialized in process optimization for heavy industry. Yet all shared the core Jacobs DNA: technical excellence, absolute accountability, and the willingness to bet the firm on doing the right thing.

This decentralized model flew in the face of 1960s management theory, which preached standardization and control. But Jacobs had learned from his father's razor business: adaptability beats efficiency every time. He would visit each office monthly, not to micromanage but to cross-pollinate ideas. An innovation in Houston might solve a problem in Denver. A client relationship in Chicago could open doors in Los Angeles.

The numbers tell the story: from $75,000 in revenue in 1947 to over $10 million by 1969. But the real asset was invisible on any balance sheet—a reputation for engineering integrity that money couldn't buy. Competitors might undercut on price or promise faster delivery, but when projects absolutely had to work, clients called Jacobs.

As the 1960s ended, Joseph Jacobs faced a new challenge. The company had grown beyond what one man could personally oversee. The family feeling that had defined the early years was harder to maintain across multiple offices and hundreds of employees. It was time for a new chapter—one that would test whether the Jacobs culture could survive the transition from founder-led startup to public corporation.

IV. Going Public & The Growth Machine (1970–2000)

The New York Stock Exchange at opening bell, October 15, 1970. Joseph Jacobs stood on the trading floor, watching his company's ticker symbol—JEC—flash across the board for the first time. At 54, the son of a failed razor salesman was taking his engineering firm public, not for the money (the family retained 40% of shares) but for a more radical reason: to make every employee an owner.

"I don't want hired hands," Jacobs had told his board. "I want 500 entrepreneurs who happen to work under one roof." The IPO raised $15 million, modest by today's standards but transformative for a firm that had bootstrapped its way to prominence. More importantly, it created a currency—stock options—that would help Jacobs compete for talent against industrial giants like Bechtel and Fluor.

The timing seemed terrible. The 1970s opened with stagflation, an oil crisis, and environmental regulations that were reshaping American industry. But Jacobs saw opportunity where others saw obstacles. The Clean Air Act of 1970 and Clean Water Act of 1972 created massive demand for environmental engineering—exactly the kind of complex, high-stakes projects where Jacobs excelled.

By 1974, Jacobs had quietly acquired three small environmental engineering firms, paying mostly in stock. The rollup strategy was subtle but brilliant: buy specialized expertise, integrate it into the Jacobs platform, then cross-sell to existing clients. A chemical company that hired Jacobs for process design might now also need environmental compliance. A mining client could add water treatment. The synergies were real, not PowerPoint fiction.

The acquisition playbook that would eventually encompass over 70 companies began to take shape: First, target firms with excellent technical reputation but poor business development. Second, retain the founders and key employees with generous equity packages. Third, maintain the acquired firm's culture while grafting on Jacobs' business systems. Fourth, and most importantly, integrate client relationships immediately—the first call after closing was always to introduce combined capabilities.

One acquisition nearly ended in disaster. In 1978, Jacobs bought Pace Engineers, a Colorado firm specializing in mineral processing. The culture clash was immediate—Pace's cowboys versus Jacobs' engineers. Projects were delayed, clients complained, and key Pace employees started leaving. Joseph Jacobs personally intervened, spending two months in Colorado. His solution was radical: instead of forcing integration, he let Pace operate as a "rebel division," maintaining their identity while accessing Jacobs' resources. Within a year, Pace was the company's most profitable division. The lesson was clear: integration didn't mean homogenization. The 1980s brought a new challenge: the oil crash. By 1982, petroleum-related work had accounted for 60% of Jacobs' revenue. When oil prices collapsed from $37 to $10 per barrel, the company's backlog evaporated almost overnight. Revenue plummeted 40% in eighteen months. The board discussed bankruptcy. Joseph Jacobs, now 66, made a decision that would define the company's future: diversify or die.

The pivot was radical. Instead of chasing the remaining oil work at cut-rate prices, Jacobs targeted entirely new sectors. The biopharmaceutical industry was emerging, needing specialized clean rooms and production facilities. Defense contractors required environmental remediation at Cold War sites. State governments needed infrastructure modernization. Each market demanded different expertise, which Jacobs acquired through targeted purchases.

As the young biotech industry matured in the 1990s, Jacobs purchased Triad Technologies and Sigel Group in the early 1990s, two companies that expanded Jacobs' pharmaceutical capabilities. In 1994 Jacobs bought CRS Sirrine Engineers and CRSS Constructors for $38 million. The purchase moved Jacobs Engineering into design and construction for the paper and semiconductor industries.

The financial discipline during this period was extraordinary. Between 1987 and 1991 Jacobs Engineering returned an industry best 22.4 percent on shareholders equity while also managing to increase sales by an average of 37 percent annually. Annual reports in the early 1990s revealed that the company had literally zero debt; according to a 1992 Forbes index of leading engineering firms which listed the median debt to capital ratio as 25 percent, with several companies reporting figures well over 40 percent, Jacobs Engineering's ratio was given as 0.0 percent.

This wasn't financial engineering—it was operational excellence. Jacobs ran projects with military precision, often completing them under budget and ahead of schedule. The savings were returned to clients, building loyalty that transcended contracts. One client famously said, "We don't hire Jacobs because they're the cheapest. We hire them because they make us look good to our boards."

In 1992 Jacobs stepped down as CEO, and Noel Watson, an employee at Jacobs Engineering for 32 years, replaced him at the head of the company. Watson focused the company on two of its most profitable and growing segments: government-financed environmental cleanup jobs and facilities design and construction for the biopharmaceutical industry. In 1993 ten percent of Jacobs' annual revenue came from government contracts, but those contracts generated 20 percent of the company's pretax profits.

The government work was particularly lucrative. In a joint venture with industry leader Fluor, Jacobs was awarded a contract in 1993 to clean up former uranium production facilities in Fernold, Ohio. The $2.2 billion contract was expected to generate as much as $40 million in profit for Jacobs. These weren't just cleanup jobs—they were complex technical challenges requiring security clearances, regulatory expertise, and the ability to work in hazardous environments. Jacobs' reputation for safety and reliability made them the contractor of choice.

The acquisition pace accelerated through the late 1990s. On December 10, 1998, it was announced that Jacobs would acquire closely held engineering firm, Sverdrup Corporation for $200 million. Sverdrup brought aerospace and defense capabilities that would prove invaluable as military spending increased. Each acquisition followed the same playbook: identify technical excellence, preserve culture, integrate client relationships, cross-sell capabilities.

By 2000, Jacobs Engineering had transformed from a chemical engineering specialist into a diversified technical services powerhouse. Revenue exceeded $2 billion. The company operated in 15 countries. The employee count had grown to over 20,000. But more importantly, the company had proven something counterintuitive: in professional services, disciplined growth beats aggressive expansion every time.

Joseph Jacobs, now in his eighties, would still occasionally visit project sites, chatting with young engineers about technical challenges. His philosophy hadn't changed since that first year as a solo consultant: take responsibility, deliver excellence, and treat every project like your reputation depends on it—because it does. As the new millennium dawned, that philosophy would be tested by the company's most ambitious expansion yet.

V. The Modern Transformation Era: CH2M & Strategic Repositioning (2000–2017)

The boardroom at CH2M Hill's Denver headquarters was tense. It was February 2017, and CEO Jacqueline Hinman was facing a stark reality: after 71 years of independence, her storied engineering firm needed a partner. The company that had built the Panama Canal expansion and managed the London 2012 Olympics infrastructure was struggling with compressed margins and fierce competition. When her phone rang with Jacobs CEO Steve Demetriou on the line proposing a "merger of equals," she knew it was really an acquisition. The question was whether CH2M's 20,000 employees would see it as a rescue or a surrender.

The 2000s had begun with grand ambitions for Jacobs. Under Noel Watson's leadership, Jacobs grew from a mid-sized U.S. engineering firm into a global player. Watson emphasized diversification and geographic expansion – overseeing numerous acquisitions in the 1990s and early 2000s that extended Jacobs' reach across Europe, Asia, and the Middle East. During his tenure, Jacobs' revenues and workforce expanded dramatically, and the company solidified its reputation as a top-tier engineering and construction services firm.

The international expansion was methodical. In 2001, Jacobs acquired the international operations, including the international consultancy Sir Alexander Gibb & Partners (Gibb Ltd) based in the UK, from Law Engineering and Environmental Services in Atlanta. Gibb brought something invaluable: Commonwealth connections and British engineering pedigree that opened doors from Singapore to South Africa.

Craig L. Martin took over as CEO in 2006, continuing the growth trajectory and guiding Jacobs through a period of record backlog and integrating various acquisitions. He championed broadening Jacobs' skill sets into areas like architecture, infrastructure planning, and telecommunications. Martin's tenure included preparing the organization for larger design-build projects and global programs.

The financial crisis of 2008 should have devastated Jacobs. Commercial construction froze. Industrial projects were cancelled. Competitors laid off thousands. But Jacobs had a secret weapon: government work. The American Recovery and Reinvestment Act pumped $831 billion into infrastructure, environmental remediation, and energy projects—exactly Jacobs' sweet spots. While competitors retreated, Jacobs hired aggressively, acquiring talent at discount prices.

In FY 2007, Jacobs acquired the privately held planning, engineering and design firm, Edwards and Kelcey of Morristown, New Jersey for an undisclosed amount. In FY 2008, Jacobs spent $264 million to acquire Carter and Burgess, Lindsey Engineering and a 60% stake in Zamel and Turbag Consulting Engineers. These weren't panic buys but strategic additions, adding transportation planning and Middle Eastern presence at attractive valuations.

The real transformation accelerated when Steve Demetriou became CEO in 2015. A chemical engineer who'd run the company's process and industrial division, Demetriou saw something others missed: the engineering industry was bifurcating. At one end, commoditized EPC (engineering, procurement, construction) work was seeing margins compress to single digits. At the other, specialized consulting and program management commanded premium prices. Jacobs was stuck in the middle—too big to be boutique, too small to compete with Bechtel on mega-projects.

Demetriou's strategy was bold: buy scale in high-value sectors while divesting commodity businesses. The crown jewel of this strategy would be CH2M Hill.

A pivotal moment came in 2017 with the acquisition of CH2M HILL, a leading engineering and consulting firm known for its work in water, environmental, transportation, and program management (notably CH2M had managed programs like the London 2012 Olympics infrastructure). The CH2M deal, worth over $3 billion, brought tens of thousands of new employees and significantly expanded Jacobs' advisory and environmental services portfolio.

The CH2M acquisition was transformative beyond its size. CH2M brought premier water expertise—crucial as climate change made water infrastructure a global priority. They had program management capabilities that allowed Jacobs to bid on massive, multi-year government programs. Most importantly, they brought a consulting-first culture that would help reshape Jacobs' identity.

Integration was delicate. CH2M employees feared being absorbed into a faceless corporation. Jacobs people worried about culture dilution. Demetriou's approach was counterintuitive: rather than forcing integration, he created "centers of excellence" where CH2M's strongest practices remained intact while gradually sharing resources and clients with Jacobs. The London water team kept their identity. The transportation group in Denver maintained their culture. But behind the scenes, back-office functions merged, procurement synergies materialized, and cross-selling began.

In FY 2014, Jacobs announced it completed a merger transaction with Sinclair Knight Merz (SKM), a 6,900-person professional services firm headquartered in Sydney. The purchase price was an enterprise value of AUS$1.2 billion (US$1.1 billion) plus adjustments for cash, debt and other items. SKM had given Jacobs a platform in Asia-Pacific; CH2M made them a global power.

But Demetriou wasn't finished. He saw that Jacobs' Energy, Chemicals and Resources (ECR) division—once the company's core—was becoming an albatross. Oil price volatility made revenue unpredictable. Competition from Korean and Chinese firms drove margins toward zero. The capital requirements for large EPC projects strained the balance sheet. In a move that would have been heretical to Joseph Jacobs, Demetriou decided to sell ECR.

Around the same time, Jacobs strategically divested its Energy, Chemicals and Resources (ECR) division in 2019, selling it to WorleyParsons. This move was aimed at pivoting away from lower-margin commodity engineering (like oil & gas EPC work) and focusing on higher-value sectors and consulting-rich services.

The sale to WorleyParsons for $3.3 billion was masterful financial engineering. Jacobs received $2.6 billion in cash plus WorleyParsons stock, effectively getting paid to eliminate earnings volatility. The market loved it—Jacobs' stock jumped 25% on the announcement. But internally, it was traumatic. ECR employees felt betrayed. Veterans who'd built their careers in chemicals and energy felt the company had lost its soul.

Demetriou's response was to paint a bigger picture: Jacobs wasn't abandoning its heritage but evolving for the future. The proceeds from ECR would fund investments in digital capabilities, data analytics, and high-margin consulting. The company would focus on sectors with long-term growth: water scarcity, sustainable infrastructure, life sciences, aerospace, and defense. It was a bet that solving complex societal challenges would be more profitable than building commodity infrastructure.

As 2017 ended, Jacobs stood transformed. Revenue approached $15 billion. The company operated in 40 countries. But more importantly, the business mix had shifted dramatically. Consulting and program management now represented 40% of revenue but 60% of profit. Government work provided steady, high-margin income. The company that Joseph Jacobs founded to solve chemical engineering problems was now advising governments on climate resilience and managing billion-dollar infrastructure programs.

Yet questions remained. Could a company built on engineering excellence truly become a consulting powerhouse? Would the market value Jacobs' transformation or see it as an identity crisis? And most pressingly, how could Jacobs compete with both specialized boutiques and giant integrators? The answer would come from an unexpected source: a centuries-old British consulting firm that most Americans had never heard of.

VI. The Great Portfolio Pivot: From Commodity to Consulting (2018–2021)

The London offices of PA Consulting seemed frozen in time. Wood-paneled walls, leather-bound books, portraits of Victorian engineers who'd advised on the first underground railway. It was December 2020, and Jacobs CEO Steve Demetriou was sitting across from PA's leadership team, proposing something audacious: Jacobs, the American engineering giant, wanted to buy Britain's oldest consulting firm. The price tag—£1.825 billion—would make it Jacobs' largest acquisition since CH2M. But this wasn't about size. It was about completing a metamorphosis.

The journey to that London boardroom began two years earlier with a decision that shocked the industry. In October 2018, Jacobs agreed to sell its Energy, Chemicals and Resources (ECR) segment to WorleyParsons, a company in North Sydney, Australia. The division that Joseph Jacobs had built his company on—the unit that still generated $6 billion in annual revenue—was being sold.

Inside Jacobs, the ECR sale felt like patricide. Engineers who'd spent decades designing refineries and chemical plants watched their life's work get packaged for sale. The Houston office, once the crown jewel of Jacobs' energy practice, saw half its staff prepare for new WorleyParsons badges. Veterans called it "the great betrayal."

But Demetriou had run the numbers obsessively. ECR's operating margins had compressed to 4%—half the company average. Return on invested capital was negative after accounting for working capital needs. Worst of all, the volatility was killing Jacobs' valuation. Every oil price swing sent the stock tumbling, even though ECR was now less than 40% of profits. The market was pricing Jacobs like a cyclical commodity business when half the company was actually steady, high-margin consulting.

The WorleyParsons deal structure was elegant. WorleyParsons completed the $3.2-billion acquisition of Jacobs Engineering Group Inc.'s Energy, Chemicals and Resources division. Jacobs received mostly cash, immediately strengthening the balance sheet. The company also took a stake in WorleyParsons, allowing participation in any upside while removing the operational risk. It was financial jujitsu—using the buyer's eagerness to eliminate Jacobs' biggest strategic weakness.

With ECR gone, Demetriou could finally articulate his vision: Jacobs would become the world's premier solutions company for society's most critical challenges. Not an engineering firm that also consulted, but a consulting firm with deep engineering capabilities. The difference wasn't semantic—it was fundamental. Engineering firms sell hours and drawings. Consulting firms sell outcomes and transformation.

The transformation required new capabilities. Jacobs had engineering excellence but lacked true management consulting DNA—the ability to advise C-suites, shape government policy, and drive organizational change. They needed strategic consulting expertise, digital capabilities, and most importantly, access to decision-makers beyond procurement departments.

Enter PA Consulting. In December 2020, Jacobs announced it would be investing in PA Consulting based in London, in a deal valued at £1.825 billion. Completion of the deal was expected to take place by the end of Q1 2021. Founded in 1943 to help rebuild post-war Britain, PA had evolved into an innovation and transformation consultancy with particular strength in defense, healthcare, and consumer sectors. They'd designed the world's first pocket calculator, helped create the UK's National Health Service, and advised on Brexit preparations.

PA wasn't just another acquisition—it was a culture injection. Where Jacobs was process-driven, PA was creative. Where Jacobs solved technical problems, PA solved business problems. Where Jacobs worked with project managers, PA worked with CEOs and ministers. The combination was either brilliant or insane, depending on your perspective.

The integration challenge was unprecedented. PA's 3,000 consultants were used to autonomy, creativity, and London salaries. Jacobs' 55,000 employees were used to process, hierarchy, and American corporate culture. PA's Cambridge technology center, where PhD scientists developed breakthrough innovations, seemed alien to Jacobs engineers who built things that actually existed.

Demetriou's integration strategy was radical: don't integrate. PA would operate as a separate brand, maintaining its culture and identity. But behind the scenes, careful connections were made. PA consultants would bring Jacobs engineers into strategy engagements. Jacobs would introduce PA to its government relationships. The goal wasn't to merge but to create a constellation of capabilities that clients could access seamlessly.

The pandemic, ironically, helped. With everyone working remotely, the Atlantic Ocean became irrelevant. PA consultants in London collaborated with Jacobs engineers in Dallas as easily as if they were in the same office. Virtual workshops replaced flying. Zoom replaced conference rooms. The forced digital transformation that COVID created made the PA-Jacobs combination more natural than it would have been in normal times.

Early wins validated the strategy. The UK government hired PA-Jacobs to develop its net-zero infrastructure strategy—PA's policy expertise combined with Jacobs' engineering knowledge. A pharmaceutical company engaged them to design and build a new vaccine facility—Jacobs' construction capabilities backed by PA's life sciences consulting. The synergies were real, not PowerPoint promises.

But the real transformation was in Jacobs' business model. By 2021, recurring revenue from long-term consulting relationships exceeded 60% of total revenue. Operating margins expanded to 15%—unheard of for a traditional engineering firm. The stock price, which had languished in the $60s when ECR was dragging down multiples, shot past $140. The market was finally pricing Jacobs as a high-value professional services firm.

The cultural evolution was harder to measure but equally real. Young engineers who once aspired to design the biggest refinery now wanted to solve climate change. Recruiting from top universities became easier—MIT graduates saw Jacobs-PA as a place to combine technical expertise with strategic impact. The company that had built its reputation on engineering execution was becoming known for intellectual leadership.

Yet challenges remained. Competitors mocked Jacobs' identity crisis—neither fish nor fowl, neither pure consultant nor pure engineer. Employees struggled with the new positioning. Clients were confused about what Jacobs actually did anymore. The company needed one more move to crystallize its transformation, to make clear that the old Jacobs was truly gone and something new had emerged.

That clarity would come from an unexpected source: a spin-off that would divide the company yet again, creating two pure plays from one conflicted giant. It would be Demetriou's final, most dramatic act—and perhaps his most brilliant.

VII. The Amentum Spin-off: Creating Two Pure Plays (2023–2024)

The PowerPoint slide was simple: one company becoming two. On the left, "New Jacobs"—focused on consulting and high-value solutions. On the right, the Critical Mission Solutions and Cyber & Intelligence businesses that would merge with Amentum. It was May 2023, and Steve Demetriou was explaining to analysts why Jacobs was voluntarily giving up $6 billion in revenue. One portfolio manager interrupted: "You're spinning off your most stable business during a potential recession. Have you lost your mind?"

Demetriou smiled. He'd anticipated the question. For months, he'd been wrestling with a paradox: Jacobs' government services business was performing brilliantly—steady growth, high margins, multi-year contracts with the Department of Defense and intelligence agencies. But it was also holding back Jacobs' valuation. The market couldn't figure out how to value a company that was part McKinsey, part Bechtel, part Booz Allen. The conglomerate discount was real and persistent.

Jacobs announced today it has entered into a definitive agreement to spin-off and combine its Critical Mission Solutions and Cyber & Intelligence government services businesses with Amentum, a leading global engineering and technology solutions provider, to create a new, publicly-traded player in the government services sector. In May, Jacobs first announced the intent to separate its CMS business to create two separate companies, each positioned for greater success. Today's transaction announcement is the outcome of a comprehensive review of all alternatives.

The decision to spin off CMS wasn't made lightly. This division had been Jacobs' safety net during economic downturns—government contracts don't disappear in recessions. It included some of Jacobs' most sophisticated capabilities: nuclear operations, space systems, cybersecurity, and classified intelligence work. The employees held security clearances that took years to obtain. The customer relationships, particularly with NASA and the Pentagon, had been cultivated over decades.

But Demetriou saw what others missed: these businesses required different strategies, different capabilities, and most importantly, different valuations. Government services companies traded at 12-15x EBITDA. High-value consulting firms traded at 15-20x. By keeping them together, Jacobs was getting the lowest multiple for everything. It was like selling diamonds and coal in the same bag—the buyer only pays coal prices.

The structure of the deal was masterful. Rather than a simple spin-off, Jacobs engineered a Reverse Morris Trust transaction—a tax-efficient structure that would merge CMS with Amentum while giving Jacobs shareholders majority ownership of the combined entity. The transaction is being structured as a Reverse Morris Trust transaction intended to be tax-free to Jacobs' shareholders for U.S. federal tax purposes.

The ownership math was carefully calibrated. Jacobs shareholders would own 51% of the new Amentum, ensuring they participated in future upside. Jacobs itself would retain a 7.5-12% stake, depending on performance targets. And crucially, Jacobs would receive $1 billion in cash at closing—capital to invest in higher-margin businesses or return to shareholders.

Amentum wasn't a random partner. The private equity-owned government services firm brought complementary capabilities: facilities management, logistics, and maintenance services that dovetailed perfectly with Jacobs' mission-critical engineering. Together, they would create a $13 billion revenue government services powerhouse—large enough to compete for mega-contracts, specialized enough to maintain margins.

The combination creates a robust, leading government technology solutions business with ~$13 billion annual revenue. A large majority of future EBITDA of the combined company is expected to come from higher growth, higher margin intelligence, cyber, energy, digital engineering, and science and technology sectors, with a strong foundation of long-term and large-scale DoD contracts.

The employee reaction was mixed. CMS staff felt abandoned—they'd been told they were core to Jacobs' future, now they were being spun off. Some worried about private equity ownership, fearing cost cuts and cultural change. Others saw opportunity—a pure-play government services company could move faster, invest more strategically, and potentially command a higher valuation than when buried inside Jacobs.

Bob Pragada, who'd taken over as CEO from Demetriou in 2023, handled the messaging carefully. This wasn't a divestiture but a liberation. Both companies would be stronger apart than together. CMS employees would join a company entirely focused on their market. Jacobs employees would work for a pure-play solutions company. Customers would get more focused service. Everyone wins—at least in theory.

The execution timeline was aggressive. Announced in November 2023, the deal needed to close by September 2024. That meant separating IT systems, dividing shared services, allocating corporate costs, and somehow maintaining business momentum while restructuring everything. One integration executive called it "performing heart surgery while running a marathon."

The complexity was staggering. CMS and Jacobs shared everything from email systems to health insurance plans. Contracts had to be reviewed to determine which entity they belonged to. Employees with split responsibilities had to choose sides. Intellectual property had to be divided. Even the corporate art collection had to be allocated.

But the hardest part was cultural. Jacobs had spent 75 years building an integrated culture. Now it was voluntarily splitting itself apart. Town halls turned emotional. Long-time colleagues realized they'd soon work for different companies. The company softball league had to figure out if they'd have two teams next year.

On September 27, Jacobs announced the completion of the spin-off of its Critical Mission Solutions and Cyber & Intelligence government services businesses and merger of the Separated Business with Amentum Parent Holdings LLC, forming an independent, publicly traded company called Amentum Holdings, Inc. The financial results of the Separated Business are reflected in Jacobs' discontinued operations.

When the deal closed in September 2024, the transformation was complete. The new Amentum began trading on the NYSE, immediately valued at over $7 billion. Jacobs shareholders owned the majority stake, validating the structure. The $1 billion cash payment strengthened Jacobs' balance sheet. Most importantly, both companies could now tell clear stories to investors.

The immediate market reaction was positive. Jacobs' stock rose 15% in the weeks following completion. Without the government services complexity, investors could finally value Jacobs as a pure-play solutions company. Amentum attracted government services specialists who'd never invested in Jacobs. The sum of the parts truly exceeded the whole.

But the real test would come in execution. Could "New Jacobs" grow without the stability of government contracts? Could Amentum compete against established players like SAIC and Leidos? Would customers accept the separation or demand the integrated capabilities they'd grown accustomed to?

As 2024 ended, early signs were encouraging. New Jacobs was winning major infrastructure advisory contracts. Amentum secured a multi-billion-dollar defense contract that might have been too government-focused for old Jacobs to pursue. The financial engineering had worked. Now came the hard part: proving that two focused companies could outperform one conflicted giant. The next chapter would determine whether Demetriou's grand restructuring was visionary or reckless.

VIII. New Jacobs: The High-Value Solutions Provider (2024–Present)

The Dallas headquarters feels different now. Gone are the displays of oil platforms and refineries that once lined the lobby. In their place: interactive screens showing water treatment innovations, sustainable infrastructure projects, and life sciences facilities. It's January 2025, and Bob Pragada is presenting to investors for the first time as CEO of a pure-play Jacobs—no government services, no commodity engineering, just high-value solutions for the world's most pressing challenges.

"We're not the company Joseph Jacobs founded," Pragada tells the audience, a statement that would have been heresy just five years ago. "We're the company he would found today."

The numbers tell a compelling story. In the fiscal year ending September 27, 2024, Jacobs Solutions had annual revenue of $11.50B with 5.99% growth. But revenue is the wrong metric for understanding New Jacobs. The real story is in the margins and mix. The Company's outlook for fiscal 2025 is for adjusted net revenue to grow mid-to-high single digits over fiscal 2024, adjusted EBITDA margin to range from 13.8-14.0%, adjusted EPS to range from $5.80-$6.20 and for reported free cash flow (FCF) conversion to exceed 100% of net income.

Those margins—approaching 14%—would have been fantasy for the old engineering-heavy Jacobs. They're reality because the business has fundamentally transformed. Today's Jacobs doesn't just design water treatment plants; it advises governments on water strategy. It doesn't just build life sciences facilities; it helps pharmaceutical companies optimize their entire development process. It doesn't just engineer infrastructure; it shapes smart cities policy.

The portfolio is focused on five core markets, each chosen for growth potential and margin profile:

Water has become Jacobs' crown jewel. Climate change makes water scarcity the defining challenge of the next century. Jacobs doesn't just treat water—it helps cities reimagine their entire water cycle. The Singapore water strategy project, where Jacobs is advising on achieving water independence by 2061, commands consulting-level fees while leveraging deep engineering expertise.

Transportation isn't about building roads anymore—it's about mobility transformation. Jacobs advises cities on autonomous vehicle integration, designs smart traffic systems, and helps governments navigate the transition to electric vehicles. The Los Angeles Metro advisory contract, worth $400 million over five years, is pure consulting with 25% EBITDA margins.

Life Sciences & Advanced Manufacturing leverages PA Consulting's expertise combined with Jacobs' facility design capabilities. As pharmaceutical companies race to develop personalized medicines and cell therapies, they need partners who understand both the science and the infrastructure. Jacobs' work designing modular vaccine facilities during COVID has evolved into a strategic advisory practice helping companies build flexible, future-proof manufacturing networks.

Environmental & Sustainability has evolved from compliance to transformation. Jacobs doesn't just clean up contaminated sites—it helps companies achieve net-zero emissions. The work with Microsoft on carbon-negative data centers combines engineering, consulting, and program management in a way few competitors can match.

Digital & Data Solutions represents the future. Every physical infrastructure project now has a digital twin. Every water system needs predictive analytics. Every transportation network requires real-time optimization. Jacobs' acquisition of Buffalo Group's data analytics capabilities, combined with PA's digital expertise, positions them at the intersection of physical and digital infrastructure.

Jacobs has consistently ranked No. 1 on both Engineering News-Record (ENR)'s 2018, 2019, 2020, 2021, 2022, and 2023 Top 500 Design Firms and Trenchless Technology's 2018, 2019, 2020, and 2021 Top 50 Trenchless Engineering Firms. But Pragada isn't satisfied with industry rankings. He wants Jacobs mentioned alongside Accenture and McKinsey, not Fluor and Bechtel.

The competitive positioning is unique. Against pure consultants like McKinsey or BCG, Jacobs offers something they can't: the ability to actually implement recommendations. Against traditional engineers like AECOM or WSP, Jacobs provides strategic advisory that shapes projects before RFPs are written. It's a sweet spot that few occupy successfully.

The cultural transformation continues. Jacobs now recruits from business schools, not just engineering programs. The Dallas headquarters hosts a "Solutions Lab" where clients co-create innovations with Jacobs experts. The performance review system rewards outcomes delivered, not hours billed. Even the dress code has evolved—suits and sneakers are as common as hard hats once were.

Technology integration accelerates everything. AI models predict infrastructure failure before it happens. Digital twins allow virtual testing of solutions. Automated design tools cut project timelines in half. But technology isn't the strategy—it's an enabler. The strategy is to be indispensable to clients facing existential challenges.

The financial model has also evolved. Recurring revenue from multi-year advisory relationships now exceeds 65% of total revenue. This isn't traditional engineering backlog that depends on project milestones—it's subscription-like revenue from ongoing partnerships. A water utility might pay Jacobs $10 million annually for continuous optimization and advisory services, regardless of specific projects.

Capital allocation has shifted dramatically. Without capital-intensive EPC projects, Jacobs generates enormous free cash flow—over 100% of net income. The choices are luxurious: invest in capability acquisitions, return cash to shareholders, or both. The recent $1 billion share buyback authorization signals confidence in the model.

Yet challenges persist. The war for talent is fierce—Jacobs competes with tech companies for data scientists, with consultancies for MBAs, and with traditional engineering firms for technical experts. The value proposition—work on meaningful challenges with real-world impact—resonates with purpose-driven millennials but requires constant reinforcement.

Client education remains ongoing. Procurement departments still sometimes see Jacobs as an engineering firm and balk at consulting-level fees. Government RFPs still often separate advisory from implementation, forcing Jacobs to choose roles. The market positioning—"solutions company"—sometimes feels too vague, too all-encompassing.

The macroeconomic environment presents both opportunities and risks. The Infrastructure Investment and Jobs Act promises $1.2 trillion in U.S. spending, perfectly aligned with Jacobs' capabilities. But government spending can be fickle, subject to political winds and budget battles. The push for sustainability seems inexorable, but implementation timelines keep shifting.

Competition intensifies from unexpected directions. Technology companies like Microsoft and Amazon are moving into smart cities. Private equity is rolling up engineering firms to create new competitors. Chinese firms are expanding globally with state backing. The comfortable oligopoly of global engineering firms is fracturing.

As 2025 unfolds, Pragada's vision is crystallizing. Jacobs won't be the biggest engineering firm or the most prestigious consultancy. Instead, it will be the essential partner for organizations navigating humanity's greatest challenges—climate change, water scarcity, healthcare access, sustainable development. It's a position no one else quite occupies, which might be exactly the point. Joseph Jacobs built a company to solve technical problems. New Jacobs solves civilizational ones.

IX. Playbook: Business & Investing Lessons

What can we learn from Jacobs' 77-year journey from a card table in Pasadena to a $12 billion global solutions provider? The playbook isn't just about engineering or consulting—it's about portfolio management, capital allocation, and the courage to destroy what you've built to create something better.

The M&A Machine: Integration as a Core Competency

We are able to continuously improve and grow through acquisition. We have acquired more than 70 businesses, and each one has contributed to our reach and capabilities. Seventy acquisitions over seven decades—but this isn't growth for growth's sake. The Jacobs acquisition playbook has evolved into a science:

First, they buy capabilities, not just revenue. Every acquisition fills a specific gap or opens a new market. PA Consulting brought innovation consulting. CH2M brought water expertise. SKM brought Asia-Pacific presence. The discipline to walk away from deals that don't fit strategically—even at attractive prices—has been crucial.

Second, integration starts before closing. Jacobs identifies the top 50 client relationships from each acquisition and assigns executive sponsors immediately. Within 30 days of closing, every major client has been contacted about expanded capabilities. This front-loaded commercial integration drives synergies faster than back-office consolidation.

Third, cultural preservation matters more than standardization. The Pace Engineers lesson from 1978—letting them maintain their cowboy culture while accessing Jacobs' resources—became doctrine. PA Consulting kept its brand. CH2M offices maintained their identity. This isn't weakness but wisdom: professional services firms are just people and relationships. Destroy the culture, lose the value.

Portfolio Management: The Courage to Shrink

The ECR divestiture violated every conventional growth imperative. Selling a $6 billion revenue stream, giving up thousands of employees, abandoning markets you've served for decades—it seems like retreat. But Jacobs understood something profound: in professional services, portfolio purity beats portfolio breadth.

The math is compelling. ECR generated $6 billion in revenue at 4% EBITDA margins—$240 million in EBITDA. The proceeds were invested in PA Consulting, which generates perhaps $400 million in revenue at 20% margins—only $80 million in EBITDA. But the market values that $80 million at 18x versus the 8x multiple for ECR's $240 million. Value creation through subtraction.

This requires exceptional executive courage. Demetriou faced internal revolt, customer confusion, and investor skepticism. The easy path was keeping everything, managing the complexity, accepting the conglomerate discount. The hard path was admitting certain businesses—no matter how historic—no longer fit.

Margin Expansion: Moving Up the Value Chain

Jacobs' margin journey from 4% to 14% isn't about cost cutting—it's about value migration. Each step up the value chain commands better economics:

- Basic engineering design: 6-8% EBITDA margins

- Complex engineering & project management: 8-10% margins

- Program management & integration: 10-12% margins

- Strategic consulting & advisory: 15-20% margins

- Outcome-based solutions: 20%+ margins

The progression seems obvious in hindsight but required fundamental business model changes. Engineers had to become advisors. Project managers had to become strategists. The company had to sell outcomes, not hours. Most engineering firms talk about this transition. Jacobs actually did it.

Government Contracting: Stability with Strings

Jacobs' government business provided ballast during every recession. Federal contracts don't disappear in downturns. Cost-plus structures protect margins. Multi-year awards provide visibility. But the Amentum spin-off revealed the hidden costs: lower multiples, procurement complexity, and security requirements that constrain flexibility.

The lesson isn't to avoid government work but to be clear about its role. As a standalone business (Amentum), it can optimize for government success. Inside a solutions company (Jacobs), it was a drag on valuation. The same business can be both essential and incompatible depending on corporate context.

Building Resilience Through Diversification

Jacobs survived the 1982 oil crash, the 2008 financial crisis, and the 2020 pandemic because no single market determines its fate. When oil collapsed, government work sustained them. When commercial construction froze, infrastructure spending continued. When COVID hit, life sciences boomed.

But diversification at Jacobs isn't random—it's orchestrated around capabilities. Water expertise applies to utilities, mining, and manufacturing. Digital capabilities enhance transportation, defense, and healthcare projects. Each market contributes different cycles, margins, and growth rates, creating portfolio resilience.

Cultural Integration: The Soft Stuff is the Hard Stuff

Every Jacobs acquisition faced the same challenge: how to preserve entrepreneurial culture while achieving corporate scale. The solution was paradoxical—maintain distinct cultures while building connective tissue. Business units keep their identity. Shared services provide efficiency. Cross-selling happens organically through relationships, not mandates.

This requires tolerating messiness. Different offices have different cultures. Pay scales vary by geography and practice. Systems aren't fully standardized. But this controlled chaos enables innovation and retention that standardization would destroy.

Capital Allocation: The Power of Patience

Jacobs' capital allocation evolved with its business model. As an engineering firm, capital went to working capital and equipment. As a solutions company, capital funds capability acquisition and shareholder returns. The discipline to match capital allocation to strategy—rather than maintaining historical patterns—has been crucial.

The current model is elegant: generate 100%+ free cash flow conversion, invest in high-return acquisitions, return excess to shareholders. No grand monuments, no vanity projects, just relentless focus on return on invested capital.

The Ultimate Lesson: Identity is Destiny

Jacobs' transformation worked because it changed its identity, not just its portfolio. It stopped thinking like an engineering firm that also consulted and started thinking like a consultancy with engineering capabilities. This isn't semantic—it drives every decision from hiring to pricing to market positioning.

Most companies tinker at the margins, afraid to challenge their core identity. Jacobs had the courage to acknowledge that what made them successful for 70 years wouldn't work for the next 70. They didn't just evolve—they metamorphosed. And in professional services, where identity determines destiny, that made all the difference.

The playbook isn't complete—it's still being written. But the lessons are clear: buy capability not size, divest what doesn't fit, move relentlessly up the value chain, and have the courage to destroy what you've built when it no longer serves your future. It's a playbook that turned a one-man consultancy into a global solutions provider. The question is who will have the courage to follow it.

X. Analysis & Bear vs. Bull Case

The stock trades at $145, up 40% year-to-date. The transformation appears complete. But is Jacobs a compelling investment at current levels? The answer depends on whether you believe the metamorphosis is sustainable or simply financial engineering that will unravel during the next downturn.

Bull Case: The Megatrends Alignment

The bulls see Jacobs as perfectly positioned for the defining challenges of the next decade. Start with infrastructure. The American Society of Civil Engineers gives U.S. infrastructure a C- grade, requiring $2.6 trillion in investment. The Infrastructure Investment and Jobs Act provides $1.2 trillion in federal funding. Jacobs doesn't just build infrastructure—it advises on strategy, designs solutions, and manages programs. They're selling shovels in a gold rush.

Water scarcity affects 2 billion people today, projected to reach 5 billion by 2050. Every drop needs treatment, recycling, and optimization. Jacobs' water practice, enhanced by CH2M, isn't just engineering—it's strategic advisory on humanity's most precious resource. Singapore pays Jacobs tens of millions annually just for advisory services. Multiply that by every water-stressed city globally.

The energy transition requires $130 trillion in investment by 2050. Not just renewable generation but grid modernization, storage solutions, and industrial decarbonization. Jacobs sits at the intersection—advising utilities on strategy, designing infrastructure, managing massive transformation programs. The PA Consulting acquisition brought UK renewable expertise that's increasingly valuable globally.

Life sciences is experiencing a golden age. mRNA technology, personalized medicine, and cell therapies require entirely new manufacturing approaches. Jacobs doesn't just build facilities—it helps companies design flexible, modular production networks. Every biotech unicorn needs what Jacobs offers. The margins on this work approach 20%.

The business model transformation is perhaps most compelling. Adjusted EBITDA margin to range from 13.8-14.0%—approaching software-like margins for what was once a commodity business. The subscription-like revenue model provides visibility and stability. Free cash flow conversion exceeding 100% enables aggressive capital returns while still investing in growth.

Valuation remains reasonable despite the run-up. At 15x forward EBITDA, Jacobs trades at a discount to pure-play consultancies (18-20x) while commanding a premium to traditional engineers (10-12x). If the market fully recognizes the transformation, multiple expansion alone could drive 30% upside.

The competitive moat is widening. Few firms combine strategic consulting with engineering execution. Fewer still have the security clearances, regulatory approvals, and client relationships Jacobs has built over 77 years. PA Consulting brought innovation capabilities that would take decades to build organically. The combination is genuinely unique.

Management execution has been flawless. Every promised synergy has been delivered. Every margin target has been hit. Every strategic initiative has been completed. Pragada, having been COO during the transformation, provides continuity. The board, having overseen the portfolio transformation, won't tolerate backsliding.

Bear Case: The Complexity Curse

The bears see a company that's neither fish nor fowl, trying to be McKinsey and Bechtel simultaneously. Start with the identity crisis. Jacobs calls itself a "solutions company"—what does that even mean? Clients hire specialists, not generalists. When cities need water strategy, they hire specialized consultancies. When they need treatment plants, they hire engineers. Jacobs' attempt to do both creates confusion, not value.

Competition is intensifying from every direction. Accenture is moving into engineering. WSP is building consulting capabilities. Private equity is creating new competitors through rollups. Chinese firms are expanding globally with state backing and cost advantages. Jacobs' comfortable niche is getting very crowded.

The talent challenge is existential. Jacobs needs to recruit top-tier consultants who typically join McKinsey or Bain. They need software engineers who prefer Google or Microsoft. They need specialized engineers who might choose boutique firms. Competing for talent across multiple categories while maintaining cost discipline seems impossible.

Customer concentration remains concerning. While diversified across sectors, Jacobs depends heavily on large government and corporate clients. Losing a major framework agreement or key client relationship could devastate entire practice areas. The UK water sector, for instance, faces regulatory pressure that could reduce spending.

The integration risks are mounting. PA Consulting's culture is radically different from engineering-centric Jacobs. CH2M integration took years and significant management attention. Cultural misalignment could lead to talent exodus, destroying the value these acquisitions were meant to create.

Margin expansion may have peaked. Moving from 4% to 14% EBITDA margins was impressive, but the easy gains are captured. Further expansion requires either cutting costs (risking talent retention) or moving further from engineering (abandoning core competency). The 13.8-14% guidance suggests management sees limited upside.

The macro environment is deteriorating. Government budgets face pressure from rising debt costs. Corporate clients are cutting discretionary spending. The sustainability momentum could stall if economic pressures mount. Infrastructure spending, while legislated, depends on appropriations that could be delayed or reduced.

Execution risk in the new model is significant. Consulting requires different project management than engineering. Fixed-price contracts for outcomes carry more risk than time-and-materials engineering. One major project failure could destroy reputation and margins.

The valuation already reflects perfect execution. At $145, the stock prices in successful transformation, margin maintenance, and continued growth. Any disappointment could trigger significant multiple compression. The downside might be larger than the remaining upside.

The Verdict: Transformation Risk vs. Transformation Reward

The investment case ultimately depends on whether you believe professional services firms can successfully transform their business models. History suggests it's incredibly difficult. Arthur Andersen's attempt to balance audit and consulting ended in disaster. Most engineering firms that attempt to move upstream fail.

But Jacobs has already done the hardest part—divesting legacy businesses, acquiring new capabilities, and changing the revenue mix. The question isn't whether transformation is possible but whether it's sustainable. Can they maintain consulting margins while delivering engineering projects? Can they retain entrepreneurial talent in a corporate structure? Can they convince clients to pay premium prices for integrated solutions?

The bulls bet that megatrends overwhelm execution risks—that demand for water, infrastructure, and sustainability solutions will forgive minor stumbles. The bears bet that complexity ultimately defeats strategy—that Jacobs will neither match pure consultancies' margins nor traditional engineers' efficiency.

At current valuations, the market is cautiously optimistic—pricing Jacobs above engineers but below consultants, reflecting transformation progress but not completion. For investors, the key is monitoring margin trajectory, talent retention, and win rates on strategic advisory work. If margins expand beyond 14%, talent stays, and advisory wins accelerate, the bulls are right. If margins compress, talent leaves, and Jacobs retreats to traditional engineering, the bears win.

The next 24 months will determine whether Jacobs' transformation is a template for professional services evolution or a cautionary tale about the limits of corporate reinvention. Either way, it's one of the most fascinating business experiments in modern corporate history.

XI. Epilogue & "If We Were CEOs"

Imagine you've just been handed the keys to Jacobs. The transformation is complete, the portfolio is focused, and the market finally understands your story. But the hardest question remains: what's next? How do you build on this foundation without destroying what made the transformation successful?

The Geographic Imperative

If we were running Jacobs, the first priority would be geographic expansion—but not the traditional way. Instead of opening offices and hoping for work, we'd execute targeted acquisitions in high-growth markets. India needs $1.4 trillion in infrastructure investment. Southeast Asia faces acute water stress. Africa requires massive healthcare infrastructure. But entering these markets requires local relationships, regulatory knowledge, and cultural understanding that can't be built organically.

The acquisition template would mirror PA Consulting: buy premier local consultancies with government relationships, maintain their brand and culture, but integrate capabilities. Imagine acquiring India's leading infrastructure advisory firm, maintaining its identity, but backing it with Jacobs' global expertise. The synergies would be immediate—local knowledge with global capability.

The Technology Platform

The future of infrastructure isn't just physical—it's digital. Every bridge needs sensors. Every water system needs AI optimization. Every building needs a digital twin. But Jacobs currently partners for technology rather than owning it. That's a mistake.

We'd build or buy a technology platform specifically for infrastructure intelligence. Not generic IoT or analytics, but purpose-built solutions for the built environment. This isn't about becoming a software company but about owning the interface between physical and digital infrastructure. The company that controls this interface controls the future of infrastructure services.

Consider predictive maintenance. Jacobs designs infrastructure that lasts decades. Adding sensors and analytics that predict failure before it happens transforms the business model from periodic inspection to continuous monitoring. The recurring revenue opportunity is massive—every asset Jacobs has ever designed could generate ongoing analytics revenue.

The Sustainability Accelerator

Climate change isn't just a market opportunity—it's an existential imperative that will reshape every industry. Jacobs advises on sustainability, but we'd go further: become the transformation partner for net-zero transitions.

This means acquiring capabilities in carbon accounting, renewable energy development, and circular economy design. But more importantly, it means developing outcome-based business models. Don't just advise on emissions reduction—guarantee it. Share in the savings from energy efficiency. Take equity positions in sustainable infrastructure projects.

The boldest move would be creating a $1 billion sustainability fund, co-investing with clients in transformation projects. Jacobs provides expertise and capital, sharing both risk and reward. This aligns incentives perfectly and transforms Jacobs from advisor to partner.

The Talent Revolution

Professional services firms are just people. Yet Jacobs still operates with industrial-era HR practices. We'd revolutionize the talent model, starting with ownership. Every professional would receive meaningful equity, not token options. The PA Consulting model—where employees own 35% of the company—should be the template, not the exception.

Career paths would become radically flexible. Engineers could rotate through consulting. Consultants could lead construction projects. The artificial boundaries between practices would dissolve. This cross-pollination would create professionals who truly understand integrated solutions, not just their narrow specialty.

Compensation would shift from billable hours to value created. A team that helps a city save $100 million through better water management should share in those savings. This requires new metrics, new systems, and cultural change, but it aligns everyone with client outcomes.

The Next Divestiture

The transformation isn't complete. Within Jacobs' portfolio remain businesses that don't fit the high-value solutions vision. Traditional construction management, while profitable, commands commodity multiples. Routine engineering design faces automation pressure. These businesses generate cash but constrain valuation.

We'd execute one more divestiture—spinning off or selling traditional engineering and construction management. This would reduce revenue by perhaps $3 billion but remove the last drag on multiples. The proceeds would fund acquisitions in pure consulting and technology. The end state: a $8 billion revenue company trading at 20x EBITDA rather than a $12 billion company trading at 15x.

The Moonshot: Infrastructure as a Service

The boldest vision would be transforming Jacobs from a services company to an infrastructure platform. Instead of designing and building assets for others to own, Jacobs would develop, own, and operate infrastructure, selling outcomes as a service.

Imagine offering "Water as a Service" to cities—Jacobs finances, builds, and operates water infrastructure, charging for clean water delivered rather than plants built. Or "Mobility as a Service"—managing entire transportation networks for outcomes-based fees. This requires massive capital, new capabilities, and risk tolerance. But it represents the ultimate value capture.

The model exists in other industries. Software moved from licenses to subscriptions. Manufacturing moved from products to solutions. Why shouldn't infrastructure move from assets to outcomes? The company that figures this out will dominate the next century of infrastructure.

The Cultural North Star

Through all these moves, maintaining cultural cohesion would be paramount. The risk in any transformation is losing what made you special while chasing what might make you successful. Jacobs' culture—entrepreneurial, accountable, client-obsessed—enabled the transformation. Losing it while scaling would be catastrophic.

We'd institute "founder's days"—quarterly sessions where Joseph Jacobs' principles are reinforced. Not empty corporate speak but real discussions about taking responsibility, delivering excellence, and betting the firm on doing right by clients. Every new hire would spend a week on project sites, understanding that Jacobs' solutions ultimately become physical reality.

The Risks We'd Accept

This aggressive agenda carries enormous risks. Geographic expansion could dilute focus. Technology investments might fail. Sustainability bets could prove premature. The next divestiture could go too far. Infrastructure as a Service might be impossibly capital intensive.

But the bigger risk is incrementalism. The engineering services industry is consolidating. Technology is automating routine work. Clients are demanding more value for less cost. Standing still means falling behind. The choice isn't between risk and safety—it's between bold risk and timid risk.

The Legacy Question

Joseph Jacobs built a company that solved his generation's challenges—industrial expansion, chemical processing, environmental remediation. Today's Jacobs must solve this generation's challenges—climate change, water scarcity, sustainable development. The question isn't whether Jacobs can maintain its transformation but whether it can lead the next one.

If we were CEOs, the north star would be simple: make Jacobs synonymous with solving humanity's greatest infrastructure challenges. Not the biggest engineering firm or the most profitable consultancy, but the essential partner for organizations navigating existential challenges. The company that cities call when facing water crisis. That governments engage for energy transition. That corporations trust with their sustainability transformation.

It's an audacious vision that would make Joseph Jacobs proud—or terrified. Probably both. But that's exactly the kind of bet he would make. Because in the end, the greatest risk isn't failure—it's irrelevance. And Jacobs, having transformed once, must transform again. The only question is whether they'll lead the change or follow it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube