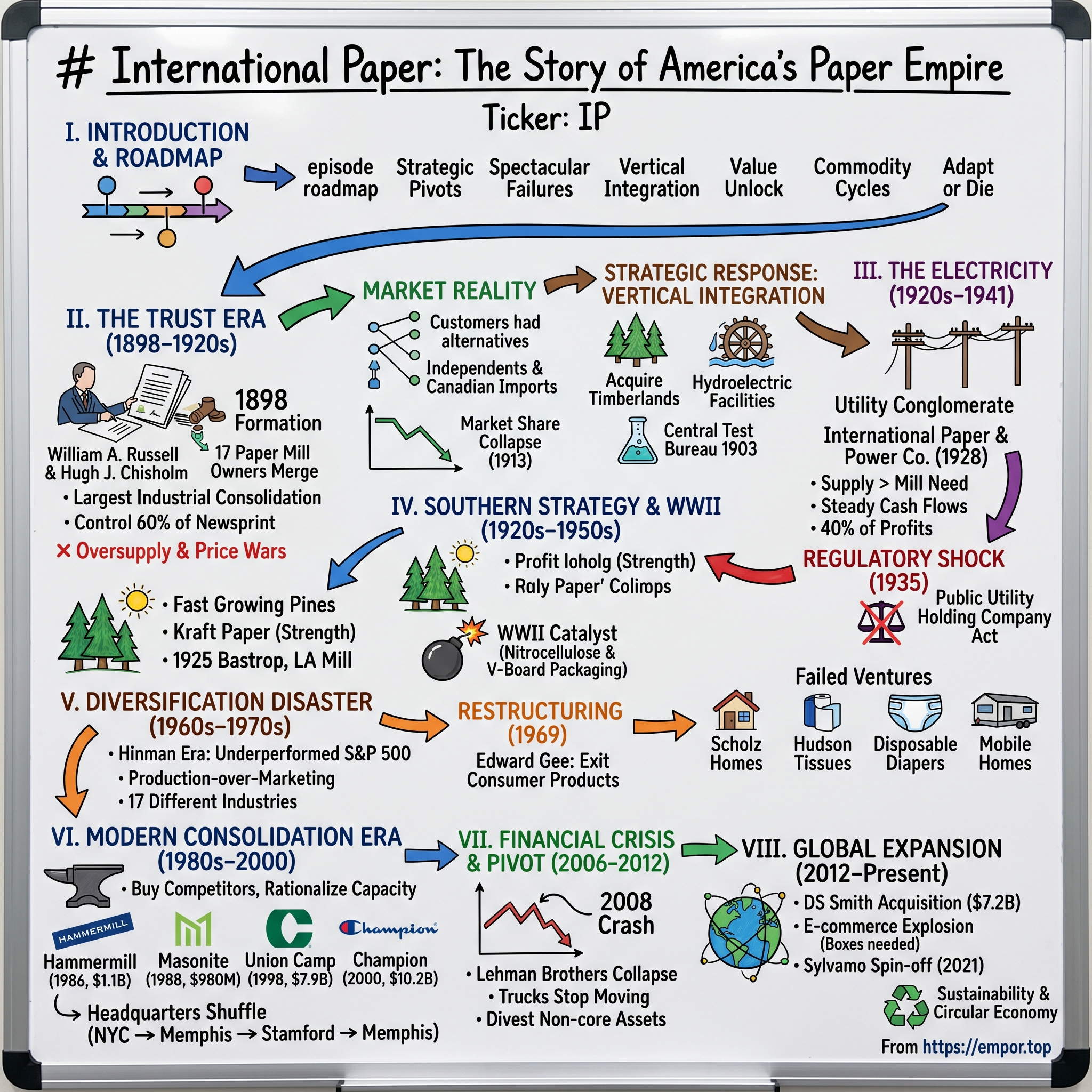

International Paper: The Story of America's Paper Empire

I. Introduction & Episode Roadmap

Picture this: January 31, 1898, New York City. In a mahogany-paneled boardroom, seventeen paper mill owners—fierce competitors just days before—are signing documents that will create the largest industrial consolidation America has ever seen. With a stroke of their pens, they're birthing International Paper Company, capitalized at an astronomical $40 million (over $1.4 billion in today's dollars). The architects of this audacious merger, William Augustus Russell and Hugh J. Chisholm, believe they've just solved the paper industry's existential crisis of oversupply and price wars. They control 60% of America's newsprint. They think they've won.

They haven't even begun to understand what they've created.

Today, International Paper stands as the world's largest pulp and paper company—but it looks nothing like what Russell and Chisholm envisioned. The newsprint monopoly they forged has morphed into a global packaging powerhouse, surviving antitrust battles, world wars, the death of newspapers, and the rise of digital everything. This is a company that once generated enough electricity to power all of New England, pioneered the southern forestry industry, and somehow transformed itself from serving newspapers to serving Amazon boxes.

The question isn't just how a 19th-century trust survived into the 21st century—it's how it thrived through every technological disruption that should have killed it. This is the story of industrial evolution at its most dramatic: a tale of strategic pivots, spectacular failures, and the relentless pursuit of what customers actually need versus what you're built to produce.

Over the next few hours, we'll trace IP's journey from monopolistic newsprint supplier to diversified conglomerate disaster to focused packaging giant. We'll explore how geography shapes strategy, why vertical integration can be both salvation and trap, and what happens when production capability races ahead of marketing wisdom. We'll examine billion-dollar acquisitions, spin-offs that unlocked value, and the brutal commodity cycles that separate industrial winners from casualties.

This isn't just a paper company story—it's an American industrial saga about adapting or dying, about the difference between controlling supply and understanding demand, and ultimately about how the most mundane products often build the most enduring empires.

II. The Trust Era: Formation & Early Dominance (1898–1920s)

The paper mills of upstate New York in 1897 were drowning—not in the Hudson River that powered their machines, but in their own production. Newsprint prices had collapsed from $42 per ton to barely $32. Mills ran at half capacity while their owners bled cash. The industry had built itself into oblivion: too many machines, too much output, too few buyers willing to pay sustainable prices. It was capitalism's classic tragedy—individual rationality producing collective insanity.

Enter Hugh J. Chisholm, a Canadian-born paper magnate who understood something his competitors didn't: in commodity businesses, consolidation isn't just strategy—it's survival. Chisholm had already built a paper empire at Rumford Falls, Maine, but he saw bigger opportunity in orchestrating industry-wide consolidation. His co-conspirator, William Augustus Russell, brought Wall Street connections and financial engineering expertise. Together, they pitched a radical solution to seventeen desperate mill owners: merge or perish.

The numbers were staggering. The combined entity would operate 101 paper machines across mills from Maine to Wisconsin, churning out 1,500 tons daily—60% of all American newsprint. The financial engineering was equally ambitious: $40 million in capitalization, split between preferred and common stock, with generous terms for the selling mill owners who would become shareholders in the new colossus. Wall Street, hungry for industrial consolidations in the McKinley era of trusts, devoured the offering.

But on day one, International Paper faced a brutal reality that would haunt industrial consolidators for the next century: market share isn't market power when customers have alternatives. The company's 60% newsprint share looked commanding on paper (pun intended), but newspapers quickly rebelled against monopolistic pricing. They sourced from independent mills, imported from Canada, and even threatened to build their own capacity. By 1913, IP's market share had hemorrhaged to just 26%—a stunning collapse that revealed the difference between controlling production and controlling markets.

The crisis deepened with tragedy. William Russell, the financial architect of the merger, died suddenly in 1899, just eighteen months after the company's formation. Chisholm, now alone at the helm, faced not just a business crisis but an existential question: what exactly had they created? A newsprint company? A forest products conglomerate? A vehicle for financial engineering?

Chisholm's answer would define IP's next chapter: when horizontal consolidation fails, go vertical. If you can't control prices through market share, control costs through the entire value chain. IP began acquiring vast tracts of timberland—not just for wood supply, but for the strategic flexibility of owning your primary input. The company built hydroelectric facilities on its mill sites, transforming rushing rivers into industrial power. Most innovatively, in 1903 it established the Central Test Bureau in Glens Falls, New York—one of America's first industrial research laboratories, predating even GE's famous research center.

This research focus wasn't academic curiosity; it was survival instinct. The newsprint market was commoditizing rapidly, with the 1913 Underwood Act eliminating tariffs on Canadian imports—a legislative atom bomb that would reshape North American paper markets forever. Canadian producers, blessed with virtually unlimited forests and hydroelectric power, could produce newsprint for 20-30% less than American mills. IP's response revealed strategic sophistication: if you can't beat Canadian economics, become Canadian. The company launched an aggressive expansion into Quebec, acquiring mills at Three Rivers in 1922 and Gatineau in 1927, operating through a new subsidiary, Canadian International Paper (CIP), formed in 1925.

The Canadian adventure would ultimately absorb $60 million in capital—more than IP's entire original capitalization. Chisholm was betting the company on a simple thesis: newsprint demand would grow forever as literacy and newspaper circulation expanded. He was building capacity for a future that would never arrive. The timing couldn't have been worse—IP completed its massive Canadian expansion just as two seismic shifts approached: the Great Depression and the rise of radio as a competing news medium.

Yet amid these strategic struggles, IP was quietly building capabilities that would matter decades later. The vertical integration into timberlands taught the company forestry management. The hydroelectric investments revealed an unexpected opportunity in power generation. The research laboratory pioneered innovations in paper chemistry and production efficiency. These weren't just operational improvements—they were options on futures the company couldn't yet imagine.

By the late 1920s, IP had transformed from a simple horizontal trust into something far more complex: a vertically integrated industrial system spanning forests to finished products, water power to wood pulp, research to manufacturing. The original monopolist's dream had failed, but something more interesting had emerged—a company learning to adapt, integrate, and innovate its way through commodity market brutality. The newsprint trust was dead, but International Paper was just beginning to understand what it might become.

III. Power Play: The Electricity Empire Years (1920s–1941)

The Glens Falls mill manager stared at his monthly reports in 1924, puzzled by an accounting anomaly. The hydroelectric turbines installed to power paper machines were generating far more electricity than the mill could use—and local utilities were paying handsomely for the excess. Revenue from selling power to the grid had quietly grown to rival profits from making paper. He fired off a telegram to headquarters: "Are we a paper company that sells electricity, or a power company that makes paper?"

It was the question that would transform International Paper into one of America's most unlikely utility conglomerates.

The evolution started innocently. Mills needed power, rivers provided it, and IP owned prime hydroelectric sites across New England and Quebec. But as household electricity demand exploded through the Roaring Twenties—growing 15% annually as Americans bought radios, refrigerators, and electric lights—IP's executives recognized an intoxicating opportunity. Their hydroelectric facilities, built for industrial self-sufficiency, could power entire cities.

The math was seductive. A modern paper mill might need 10 megawatts of power, but a properly developed river site could generate 50 megawatts or more. The surplus electricity, sold at regulated utility rates, generated returns that dwarfed the volatile paper business. Better yet, power revenues were stable, predictable, and recession-resistant—everything newsprint wasn't.

In 1928, IP formalized this dual identity by creating International Paper & Power Company, a Massachusetts holding company that would own International Paper as a subsidiary. The restructuring wasn't just corporate gymnastics—it was a declaration that IP saw itself as fundamentally transformed. Wall Street loved it, bidding up IP&P shares as investors recognized they were buying a utility company with a paper business attached, not vice versa.

The numbers were staggering. By 1929, IP's power generation capacity exceeded 500,000 horsepower—enough to light all of New England and large portions of Quebec and Ontario. The company operated major hydroelectric facilities on the Connecticut, Hudson, and St. Maurice rivers, selling power to utilities from Boston to Montreal. Power generation contributed nearly 40% of consolidated profits, cushioning the cyclical brutality of commodity paper markets.

But IP's power ambitions went beyond just selling excess capacity. The company began acquiring struggling utilities, building transmission networks, and even entering retail electricity distribution. They formed subsidiaries like New England Power Association and purchased controlling stakes in Canadian utilities. IP was constructing a vertically integrated electricity empire that stretched from generating stations to household light switches.

The strategic logic seemed bulletproof. Power and paper were perfect complements—both needed rivers, both required massive capital investment, both benefited from scale. The stable cash flows from selling electricity could finance paper mill modernization and expansion. Geographic overlap meant shared infrastructure and management. It was synergy before consultants invented the word.

Then came two shocks that would shatter IP's electricity dreams. First, the 1929 stock market crash and subsequent Depression crushed industrial power demand as factories closed and construction stopped. IP's newest power facilities, built for a boom that evaporated, operated at fractional capacity. The company had invested hundreds of millions in generating assets just as demand collapsed.

The second blow was regulatory. Franklin Roosevelt's administration, suspicious of utility holding companies after spectacular failures like Samuel Insull's empire, passed the Public Utility Holding Company Act of 1935. The law was surgical in its precision: companies could be either utilities or industrial firms, not both. IP had five years to choose between paper and power.

The boardroom debates were agonizing. Power generation provided steady returns and strategic flexibility. But paper was IP's heritage, its core competence, its identity. More pragmatically, selling the power assets in Depression-era markets would mean massive losses. Yet keeping them meant abandoning the paper business that employed thousands and defined the company's culture.

The Canadian expansion complicated everything. That $60 million investment in Quebec paper mills—financed largely through power company profits—was hemorrhaging cash as newsprint prices crashed. The mills at Three Rivers and Gatineau, built for newspaper growth that radio was destroying, operated at massive losses. IP faced the nightmare scenario of divesting profitable power assets to focus on unprofitable paper operations.

The resolution came through financial engineering that would make modern private equity proud. In June 1941, a new International Paper Company was incorporated to acquire the paper-making assets of International Paper & Power Company. The power generation facilities were spun off into independent utilities or sold to existing power companies. Shareholders received stock in both entities, theoretically preserving value while satisfying regulatory requirements.

But the real cost wasn't financial—it was strategic. IP's decade-long transformation into a diversified energy and industrial conglomerate had failed, forced apart by regulatory fiat rather than business logic. The company emerged from its power era financially weakened, strategically confused, and facing a world war that would demand every ounce of industrial capacity it could muster.

Yet the power years weren't wasted. IP had learned to think beyond traditional boundaries, to see assets as platforms for multiple businesses, to manage regulatory complexity and stakeholder conflicts. These lessons—about diversification's promises and perils, about the difference between operational synergies and financial engineering, about the vulnerability of strategic plans to political winds—would echo through IP's next eight decades of evolution.

IV. The Southern Strategy & WWII Transformation (1920s–1950s)

The Mississippi heat in August 1925 was suffocating, but IP's chief forester, watching pine seedlings grow in what had been cotton fields just years before, saw only opportunity. In eighteen months, these loblolly pines had grown six feet—triple the growth rate of Northern forests. The arithmetic was revolutionary: Southern trees reached pulping size in 15 years versus 40 years in Maine. The South's twelve-month growing season, abundant rainfall, and vast abandoned farmland offered what IP desperately needed—a sustainable, low-cost fiber supply that could compete with Canadian producers.

The Southern strategy began as a supply chain play but evolved into complete strategic transformation. IP acquired its first Southern mill in Bastrop, Louisiana, in 1925, then rapidly expanded across the Pine Belt from Texas to the Carolinas. But these weren't just any mills—they were kraft paper facilities, using a revolutionary chemical pulping process that produced stronger, more versatile paper than traditional newsprint operations.

Kraft paper was IP's gateway drug to packaging. Unlike newsprint, which was declining as radio gained audience share, kraft paper rode the consumer goods boom. Every product Americans bought—from groceries to appliances—needed packaging. The kraft process could use Southern pine's long fibers to create papers strong enough for shipping containers yet versatile enough for shopping bags. It was a product with a future, not a past.

The transformation accelerated with an unexpected catalyst: World War II. When military planners needed packaging that could survive Pacific island humidity and Atlantic convoy conditions, they turned to IP's kraft mills. The company developed "V-board" (Victory board), a water-resistant containerboard that replaced wooden crates for everything from ammunition to medical supplies. Military contracts drove IP's kraft production from 500,000 tons in 1940 to over 2 million tons by 1945.

But the real war story was more explosive—literally. IP's chemical pulping expertise proved invaluable for producing nitrocellulose, the key ingredient in smokeless gunpowder and artillery propellants. The company's mills were retrofitted with special digesters to produce high-purity cellulose for munitions. By 1943, IP was one of the largest suppliers of nitrate pulp to the Allied war effort, with production so sensitive that mill locations were classified military secrets.

The war taught IP lessons that would reshape its post-war strategy. First, packaging was recession-proof and war-proof—humans always need to move stuff. Second, technical innovation could transform commodity products into specialized, higher-margin offerings. Third, the South's cost advantages were structural and sustainable, not temporary arbitrage.

The 1946 opening of the Erling Riis Research Laboratory in Mobile, Alabama, symbolized IP's Southern commitment. Named after a pioneering chemical engineer who developed IP's kraft processes, the facility focused on extracting maximum value from Southern pine. Researchers developed new paper grades, pioneered recycling technologies, and created the coated papers that would dominate advertising and magazine printing for the next half-century.

The coated paper breakthrough deserves special attention. By applying thin layers of clay and chemicals to kraft base paper, IP created surfaces that could reproduce photographs and colors with unprecedented clarity. Life magazine's vivid photo essays, the explosion of color advertising in the 1950s, the rise of catalog shopping—all depended on IP's coated paper innovations. The company had transformed from newsprint supplier to enabler of America's visual culture.

The Southern mills also pioneered industrial ecology before environmentalists invented the term. The kraft process produced not just paper but tall oil (used in soaps and chemicals), turpentine (solvents and fragrances), and lignin (binders and adhesives). Mill waste heat powered local industries. Even the distinctive rotten-egg smell of kraft mills—from sulfur compounds—was captured and converted to industrial chemicals. IP was learning that in commodities, competitive advantage came from squeezing value from every molecule.

By 1950, IP's Southern operations generated more revenue than its traditional Northern mills. The company had successfully arbitraged geography, technology, and market evolution to rebuild itself around packaging and specialty papers rather than newsprint. The transformation looked brilliant in hindsight but was agonizing in execution—shuttering historic mills, relocating workers, abandoning communities that had defined IP's identity for half a century.

The human dimension was captured in the story of Mobile mill manager James "Big Jim" Patterson, who transformed from skeptical Northerner to Southern evangelist. Arriving in 1947 expecting a two-year assignment, Patterson stayed twenty-five years, building Mobile into IP's largest and most profitable facility. His management philosophy—"treat Southern workers with respect, not condescension"—helped IP avoid the labor strife that plagued other Northern companies moving South. Patterson pioneered integrated housing, education programs, and profit-sharing that made IP a preferred employer across the South.

The Southern strategy's success created new challenges. IP now competed directly with Southern-born rivals like Georgia-Pacific and Weyerhaeuser's Southern operations. The cost advantages that drew IP South also attracted every other paper company, eventually eroding margins through oversupply. Most critically, success in packaging and specialty papers obscured growing obsolescence in IP's remaining newsprint operations—a problem that would explode in the next decade.

V. The Diversification Disaster (1960s–1970s)

Richard Hinman III stood before IP's board in January 1969, his family's twenty-six-year control of the company about to end. The numbers told a story of spectacular strategic failure: IP stock had underperformed the S&P 500 by 60% during the go-go sixties, while competitors like Georgia-Pacific soared. The company that once dominated American paper couldn't even dominate its own strategy. Hinman's final words to the board were prophetic: "We tried to be everything to everyone and ended up being nothing to anyone."

The Hinman era began promisingly in 1943 when Richard Hinman Jr. took IP's helm, bringing Ivy League polish and strategic ambition to a company still run like a collection of mills. The Hinmans—father and son—believed IP's future lay in diversification, transforming from cyclical commodity producer to integrated consumer goods company. They studied DuPont's evolution from explosives to chemicals, GE's expansion from electricity to appliances. Why couldn't IP evolve from paper to... everything?

The diversification started logically enough. Residential construction seemed natural—IP owned forests, produced lumber, why not build houses? In 1962, IP acquired Development Corporation of America, entering prefabricated housing just as suburban expansion exploded. The company launched "Scholz Homes," factory-built houses promising affordability and quality. Marketing brochures showed happy families in front of IP-built homes, surrounded by IP-supplied materials—vertical integration reaching into American dreams.

But IP discovered what every industrial company learning consumer markets eventually realizes: selling to businesses and selling to families require completely different capabilities. IP knew how to negotiate with purchasing managers, not convince young couples to bet their life savings on prefabricated homes. The company's engineers designed technically superior houses that consumers found sterile and cheap-looking. Sales organizations built for bulk commodity transactions couldn't handle individual mortgage applications and customization requests.

The consumer products expansion grew more ambitious and more absurd. IP entered facial tissue, challenging Kleenex with "Hudson" brand tissues. The company launched disposable diapers, competing against Procter & Gamble's Pampers with a product called "Disposables" (the name alone revealed IP's marketing naivety). They produced nonwoven fabrics for everything from surgical gowns to car interiors. Each venture made sense in isolation—IP had fiber, manufacturing scale, distribution networks. Together, they created strategic chaos.

The numbers revealed the disaster. By 1968, IP operated in seventeen different industries, from milk cartons to mobile homes. Return on equity had declined from 15% in 1960 to barely 8% by decade's end. The company's paper mills—still generating most profits—were starved of capital as investment poured into consumer ventures that never achieved profitability. IP was subsidizing diversification disasters with commodity paper profits, the opposite of strategic logic.

The production-over-marketing mindset pervaded everything. IP's executives, raised in mills where efficiency meant everything, believed superior manufacturing would triumph over inferior marketing. They built state-of-the-art diaper factories producing high-quality products at low costs, then wondered why consumers still bought Pampers. They couldn't understand that P&G's advertising created emotional connections IP's production efficiency could never match.

The cultural mismatch was even worse. IP's DNA was industrial, engineering-focused, relationship-based. Mill managers who'd spent careers optimizing paper machines were suddenly responsible for fashion-conscious nonwoven fabrics. Sales teams accustomed to selling railcars of commodity paper were asked to pitch facial tissue to grocery chains. The company hired consumer marketing experts who fled within months, frustrated by IP's inability to move beyond production metrics to consumer insights.

The Weyerhaeuser comparison was devastating. While IP dispersed energy across random diversification, Weyerhaeuser focused ruthlessly on forest products, becoming the industry's low-cost producer. Georgia-Pacific similarly concentrated on paper and building products, using operational excellence to fund selective acquisitions. Both competitors' stocks doubled while IP's stagnated, proof that in commodities, focus beats diversification.

The boardroom coup that ended Hinman control in 1969 brought Edward Gee, an outsider from International Harvester, to salvage the wreckage. Gee's first analysis was brutal: IP had spent $500 million on diversification ventures worth maybe $200 million. The company's core paper business—still profitable despite neglect—was losing market share to focused competitors. Most damningly, IP's diversification hadn't reduced cyclical exposure; it had just added new sources of volatility.

Gee's restructuring was swift and merciless. Consumer products were sold or shuttered—facial tissue to Kimberly-Clark, disposable diapers written off entirely. Prefabricated housing was divested at massive losses. Nonwoven fabrics were refocused on industrial applications where IP's manufacturing expertise mattered more than marketing. By 1975, IP had retreated to its core: paper, packaging, and forest products.

The lessons were expensive but invaluable. Diversification without strategic logic is just distraction. Production excellence means nothing without market understanding. Most critically, commodity producers must accept their nature—trying to become consumer brands through acquisition or development usually destroys value rather than creating it. IP's lost decade proved that in industrial markets, boring focus beats exciting diversification every time.

VI. The Modern Consolidation Era (1980s–2000)

John Georges, CEO of Federal Paper Board, stared at the acquisition offer from International Paper in 1995, knowing resistance was futile. IP was offering $3.5 billion—a 40% premium to market price—and Georges had watched IP systematically acquire every independent player worth buying. Hammermill in 1986. Masonite in 1988. Now Federal Paper Board. Soon, Georges predicted to his board, it would be Union Camp and Champion. "IP isn't just consolidating the industry," he said. "They're rebuilding it in their image."

He was exactly right.

The modern consolidation era began with IP's 1985 recognition that the U.S. paper industry had a simple problem: too many players, too much capacity, too little pricing power. While IP had spent the 1970s recovering from diversification disasters, hundreds of regional paper companies had built competing mills, creating chronic oversupply. The solution was elegant if expensive: buy competitors, rationalize capacity, restore pricing discipline.

The Hammermill acquisition in 1986 was IP's opening move, bringing eleven paper mills and something more valuable—Hammermill's legendary sales force and brand equity in high-quality printing papers. IP paid $1.1 billion, considered outrageous for a company generating $150 million in annual profits. But IP wasn't buying current earnings; it was buying market position and the ability to shut redundant capacity while maintaining customer relationships.

The integration revealed IP's new strategic sophistication. Instead of immediately closing mills and slashing costs, IP spent eighteen months analyzing which Hammermill facilities complemented versus duplicated existing operations. Mills with unique capabilities or geographic advantages survived; redundant facilities were closed gradually, with production shifted to maintain customer supply. The human touch mattered too—IP retained Hammermill's sales leadership, recognizing that customer relationships were worth more than temporary cost savings.

Masonite in 1988 took IP in a different direction—engineered wood products for construction. The $980 million acquisition brought technology for converting wood chips and fiber into hardboard siding and interior panels. It was diversification, but logical diversification, leveraging IP's fiber expertise into higher-margin building products. Unlike the 1960s consumer products disasters, Masonite sold to IP's existing customer base—industrial buyers who valued performance over marketing.

But the real consolidation fireworks started in the late 1990s. IP's acquisition of Union Camp Corporation in 1998 for $7.9 billion was, at the time, the paper industry's largest merger. Union Camp brought 1.6 million acres of prime Southern timberland, six major paper mills, and most importantly, massive corrugated packaging operations serving the exploding e-commerce sector. The merger made IP the undisputed leader in American packaging.

The Union Camp integration showed how IP had matured as an acquirer. Instead of imposing IP culture wholesale, the company created integration teams mixing personnel from both companies. Best practices were identified regardless of origin—Union Camp's safety programs were superior, so they became the standard. IP's procurement was more efficient, so it took precedence. The companies achieved $400 million in annual synergies, double the original estimate, without the cultural warfare that usually accompanies mega-mergers.

Then came the biggest bet: Champion International in 2000 for $10.2 billion. Champion was IP's last major independent rival, with extensive operations in printing papers, newsprint (yes, still), and packaging. The merger would create a $25 billion behemoth controlling 35% of U.S. paper and packaging capacity. Antitrust concerns were obvious—the Department of Justice demanded divestitures worth $2 billion—but IP pressed forward, convinced that scale was survival in commodity markets.

The Champion deal revealed both the power and limits of consolidation. The good: IP achieved massive procurement savings, optimized logistics networks, and gained pricing power in key markets. The bad: integrating two massive, century-old cultures proved nearly impossible. Champion executives resented IP's dominance; IP managers viewed Champion as conquered territory. The promised revenue synergies never materialized as customers, wary of IP's market power, diversified suppliers.

The headquarters shuffle reflected deeper identity confusion. IP moved from New York to Memphis in 1987, seeking lower costs and proximity to Southern operations. Then to Stamford, Connecticut, in 1992, chasing corporate respectability. Then back to Memphis in 2000, acknowledging operational reality. Each move cost hundreds of millions and destroyed institutional memory. The joke among employees: "IP changes headquarters more often than it changes strategy."

Yet the consolidation strategy's financial logic was undeniable. IP's revenue grew from $5 billion in 1985 to $28 billion by 2000. Market capitalization increased five-fold. The company controlled massive market shares in corrugated packaging (35%), printing papers (30%), and market pulp (25%). IP had achieved what the 1898 founders dreamed of but never accomplished—genuine market power through scale and scope.

The hidden asset in these acquisitions was distribution. Through various deals, IP assembled xpedx, America's largest paper and packaging distribution network. With over 150 locations, xpedx gave IP direct customer access, market intelligence, and the ability to bundle products across categories. Competitors might match IP's manufacturing, but they couldn't replicate its distribution reach.

By 2000, IP had essentially completed American paper industry consolidation. The remaining independents were either too small to matter or too specialized to threaten. International expansion beckoned—Europe, Asia, Latin America offered fragmented markets ripe for IP's consolidation playbook. But first, IP would face its greatest test: the 2008 financial crisis and the digital destruction of paper demand. The empire was built; now it had to survive the apocalypse.

VII. The Financial Crisis & Strategic Pivot (2006–2012)

John Faraci, IP's CEO, stood before analysts in October 2008, his typical confidence shaken. Lehman Brothers had collapsed three weeks earlier. IP's stock had crashed from $40 to $12. More terrifying than financial metrics was a physical reality: trucks weren't moving. "When global trade stops," Faraci said, "demand for packaging doesn't decline—it disappears." IP's containerboard mills, running at 95% capacity in August, were at 60% by October. The company faced an existential question: was this cyclical downturn or structural collapse?

The pre-crisis period had actually started with shrewd positioning. In 2005-2006, IP executed one of history's greatest industrial asset swaps, selling 6 million acres of forestland to real estate investment trusts for $6.1 billion. The timing was perfect—REITs were desperate for hard assets, paying premium prices for timberland IP had owned for decades. IP retained long-term fiber supply agreements, securing raw materials without capital burden. It was financial engineering at its finest: monetizing assets at peak prices while maintaining operational control.

The forestland sale funded strategic repositioning. IP divested its coated papers business to AbitibiBowater, exiting the declining magazine paper market. The kraft paper operations went to private equity, eliminating commodity exposure. Wood products were sold to West Fraser Timber. Even the beverage packaging business—profitable but non-core—was divested to Carter Holt Harvey. By 2007, IP had shed $4 billion in revenue but eliminated massive capital requirements and cyclical volatility.

Then 2008 happened. The financial crisis wasn't just another recession—it was a demand shock that questioned paper's future. E-commerce collapsed as consumers stopped buying. Manufacturing ground to a halt, eliminating industrial packaging demand. Even food packaging declined as restaurants closed and grocery shopping shifted to basics. IP's mills, built for a physical economy, faced a world suddenly gone digital and dormant.

The numbers were catastrophic. IP's revenue dropped from $24 billion in 2007 to $21 billion in 2009. Operating profits fell 70%. The company burned through $1 billion in cash, suspended its dividend for the first time since the Depression, and laid off 20,000 employees—nearly 25% of its workforce. Mills that had run continuously for decades were indefinitely shuttered. Entire communities built around IP facilities faced economic extinction.

But Faraci saw opportunity in crisis. While competitors hoarded cash and hoped for recovery, IP made a contrarian bet: the physical economy would return, e-commerce would explode, and packaging—especially corrugated—would be the winner. The strategic logic was simple: every online purchase requires 7x more packaging than retail sales. Amazon was still growing despite the recession. Consumer habits were shifting permanently toward home delivery.

The Temple-Inland acquisition in 2012 was IP's all-in bet on this thesis. At $4.5 billion, it was IP's largest acquisition since Champion, but the strategic fit was perfect. Temple-Inland brought seven containerboard mills and fifty-nine box plants, expanding IP's corrugated packaging capacity by 40%. More importantly, Temple's mills were modern, efficient, and located near high-growth markets in the Southwest and Southeast.

The DOJ's response revealed how much had changed since IP's monopolistic origins. Regulators approved the deal with minimal divestitures—just three mills—recognizing that packaging markets were global and competitive despite IP's domestic scale. The antitrust cops who would have blocked this merger in 1990 now saw it as necessary consolidation in a globalizing industry.

The integration was IP's smoothest ever, partly because desperation focused minds. Both companies had suffered through the crisis; survivors understood that cultural battles were luxury nobody could afford. IP retained Temple's best practices in mill operations while imposing its superior logistics and procurement systems. Synergies reached $400 million annually, 50% above projections, achieved through operational excellence rather than brutal cost-cutting.

The strategic pivot went beyond acquisitions. IP fundamentally reimagined its business model around e-commerce and sustainability. Mills were reconfigured to produce lightweight but strong containerboard optimized for shipping. Box plants were relocated near Amazon fulfillment centers. Design centers were established to help brands create packaging that photographed well online—crucial when products were sold through screens rather than shelves.

The sustainability angle was equally strategic. As plastic packaging faced environmental backlash, IP positioned corrugated as the circular economy solution—made from renewable resources, endlessly recyclable, biodegradable if necessary. The company invested heavily in recycling infrastructure, reaching 70% recycled content in containerboard. Environmental liability was transformed into competitive advantage.

By 2012's end, IP had emerged from crisis radically transformed. The company that entered 2008 as a diversified paper manufacturer exited as a focused packaging powerhouse. Revenue was lower—$22 billion versus $24 billion—but returns were higher. The business mix had shifted from 40% packaging to 70% packaging. Most importantly, IP was positioned for the economy's physical-to-digital transformation, not victimized by it.

The Sylvamo spin-off, announced in 2021 but conceptualized during this period, represented the final break with IP's printing paper past. Creating a standalone company for printing and writing papers acknowledged reality: these businesses required different strategies, capital allocation, and management focus than packaging. The spin-off would unlock value by allowing each business to optimize independently—packaging for growth, printing for cash generation.

Faraci's retirement speech in 2014 captured the transformation: "We entered the crisis as the last nineteenth-century industrial giant. We exit as a twenty-first-century packaging solutions provider. The transition nearly killed us. But what doesn't kill you in commodities makes you stronger—if you're willing to change everything except your values."

VIII. Global Expansion & Transformation (2012–Present)

Mark Sutton, IP's CEO since 2014, faced the Mercedes-Benz board in Stuttgart in September 2024, making his final pitch for DS Smith. The British packaging giant's directors were skeptical—why merge with an American company when European consolidation seemed more natural? Sutton's answer was simple but powerful: "E-commerce is erasing borders. Amazon doesn't care if a box comes from Birmingham or Birmingham, Alabama. Neither should we." Four months later, IP announced the $7.2 billion acquisition, its boldest international expansion ever.

The DS Smith deal represents IP's recognition that packaging markets are globalizing as rapidly as the supply chains they serve. DS Smith brings 30,000 employees across thirty-four countries, with leading positions in European corrugated packaging and recycling. More strategically, it provides IP with something money can't easily buy: deep relationships with European consumer brands navigating sustainability regulations that make American environmental rules look permissive.

But we're getting ahead of ourselves. The modern transformation started with IP's 2016 acquisition of Weyerhaeuser's cellulose fibers division for $2.2 billion. This wasn't about paper—it was about fluff. The absorbent pulp used in diapers, feminine hygiene products, and medical supplies represents one of the few growing fiber markets. Global demand increases 3-4% annually as emerging markets adopt Western hygiene habits and aging populations drive adult incontinence products.

The cellulose fibers deal revealed IP's new strategic framework: find niches where fiber expertise creates competitive advantage and scale matters. Fluff pulp requires specialized manufacturing, consistent quality, and global logistics—capabilities IP had spent a century building. Better yet, customers like Procter & Gamble and Kimberly-Clark value supply security over price, creating stable, long-term relationships.

The real transformation catalyst was e-commerce explosion. COVID-19 accelerated existing trends by five years in five months. E-commerce penetration jumped from 15% to 25% of retail sales. Amazon became America's second-largest employer. Every physical retailer scrambled to build direct-to-consumer capabilities. And every online order needed corrugated packaging—IP's sweet spot.

IP's response went beyond just making more boxes. The company pioneered "right-sizing" technology, creating custom packaging for each shipment to minimize waste and shipping costs. Box-on-demand systems at fulfillment centers produced perfectly fitted containers in real-time. Frustration-free packaging eliminated wrap rage while reducing materials by 30%. IP wasn't just supplying boxes; it was solving the entire packaging equation.

The 2021 Sylvamo spin-off marked IP's final evolution from diversified paper company to focused packaging and fibers specialist. Sylvamo took IP's remaining printing and writing paper mills, creating a $3 billion standalone company optimized for cash generation in declining markets. IP shareholders received Sylvamo stock, preserving value while allowing each entity to pursue appropriate strategies. It was corporate surgery at its finest—separating growth from harvest, future from past.

The timing proved perfect. Freed from printing paper's capital demands and strategic distraction, IP could focus entirely on packaging innovation. The company developed antimicrobial coatings for food packaging, extending shelf life without chemicals. Breakthrough barrier coatings allowed corrugated to replace plastic in moisture-sensitive applications. Smart packaging with embedded sensors tracked temperature, humidity, and location through supply chains.

Sustainability became strategic weapon rather than compliance burden. IP's 2030 Vision committed to renewable energy for 50% of manufacturing, 75% recycled content in packaging, and carbon neutrality in operations. These weren't green-washing promises—they were competitive necessities as customers like Unilever and Walmart demanded sustainable supply chains. IP's circular economy positioning—renewable, recyclable, regenerative—resonated with consumers and regulators increasingly hostile to plastic packaging.

The financial results vindicated the transformation. IP's stock price rose from $35 in 2012 to over $50 by 2024, outperforming the S&P 500. Return on invested capital improved from 8% to 12%. Most impressively, IP achieved these returns while investing billions in capacity expansion and technology—proof that the business model was generating real value, not just financial engineering.

Geographic expansion accelerated beyond DS Smith. IP built new containerboard mills in Brazil and India, following multinational customers into emerging markets. Joint ventures in China provided market access without direct exposure to geopolitical risks. The company's packaging network spanned six continents, serving global brands that demanded consistent quality and service worldwide.

The competitive landscape had also transformed. WestRock, formed from the merger of RockTenn and MeadWestvaco, emerged as IP's primary rival in packaging. Packaging Corporation of America focused on operational excellence in domestic markets. Georgia-Pacific, owned by Koch Industries, leveraged private ownership for long-term investments. But IP's scale—nearly twice any competitor's—provided advantages in procurement, logistics, and technology investment that smaller rivals couldn't match.

Yet challenges loom. Chinese overcapacity threatens global containerboard pricing. Plastic packaging, despite environmental concerns, continues gaining share in many applications. Digital commerce platforms are experimenting with reusable packaging systems that could disrupt single-use models. Most fundamentally, IP must integrate DS Smith while navigating Brexit complications, European recession risks, and regulatory divergence between American and European markets.

The DS Smith integration will test whether IP has truly learned from past acquisition mistakes. Success requires maintaining DS Smith's European relationships while achieving operational synergies. Cultural integration across Atlantic divides challenges any merger. Regulatory scrutiny in concentrated markets could force unexpected divestitures. IP is betting it can create the world's first truly global packaging company—history suggests that's harder than it sounds.

IX. Playbook: Business & Investing Lessons

The power of industry consolidation isn't just about eliminating competitors—it's about timing the wave. IP's consolidation moves reveal a pattern: strike when industries face external shocks that weak players can't survive. The 1898 formation exploited newsprint oversupply. The 1980s-90s acquisition spree capitalized on environmental regulations that smaller mills couldn't afford. The 2012 Temple-Inland deal leveraged financial crisis distress. Lesson: consolidation works best when external forces are already winnowing the field.

Vertical integration versus focus presents a perpetual strategic tension. IP's history shows both extremes can work—if matched to market conditions. Vertical integration (timberlands to finished products) made sense when supply chains were local and predictable. Focused specialization (just packaging and fibers) works better in global, volatile markets. The key insight: vertical integration is about controlling uncertainty. When uncertainty is manageable, integration adds value. When uncertainty is overwhelming, focus provides flexibility.

Managing through commodity cycles requires a different playbook than stable businesses. IP learned to use downturns for transformation—selling assets at peak prices before crashes, buying distressed competitors at trough valuations, restructuring operations when demand weakness provides cover for difficult changes. The company's financial crisis navigation shows mastery: divest non-core assets before the storm, conserve cash during chaos, then acquire aggressively when competitors are paralyzed.

The production-marketing capability mismatch destroyed IP's 1960s diversification but explains its 2000s packaging success. When IP entered consumer products, it had world-class production but amateur marketing—fatal in brand-driven markets. But in packaging, production excellence matters more than marketing finesse because customers are businesses buying industrial products. The lesson: diversification only works when new markets value your existing capabilities.

Capital allocation in capital-intensive industries requires different metrics than asset-light businesses. IP's century-long evolution shows three allocation principles: First, maintenance capital is non-negotiable—deferred maintenance in commodity processing is corporate suicide. Second, growth capital must target markets with structural tailwinds (e-commerce), not just capacity additions. Third, return requirements should reflect cycle timing—accept lower returns at cycle bottoms when assets are cheap, demand higher returns at peaks when risks are elevated.

Geographic expansion strategies reveal that following raw materials beats following customers. IP's moves—from Northeast forests to Southern pines to global fiber sources—succeeded when they accessed cheaper inputs. Attempts to follow customers (Canadian newsprint expansion, European ventures) typically disappointed. The pattern is clear: in commodities, cost advantage trumps market access.

Government policy shapes industrial structure more than executives admit. The Underwood Act's Canadian newsprint tariff elimination forced IP's internationalization. The Public Utility Holding Act killed IP's power business. Environmental regulations drove industry consolidation. Chinese industrial policy created global overcapacity. Smart commodity companies don't fight policy changes—they anticipate and position accordingly.

Building and maintaining oligopoly positions requires subtle strategic thinking. IP learned that explicit coordination triggers antitrust action, but parallel behavior following price leaders is generally acceptable. Capacity discipline matters more than market share—better to run fewer mills at full utilization than more mills at partial capacity. Most importantly, oligopolies must provide customer value, not just extract rents, or they invite regulatory intervention and competitive entry.

The role of technology in commodities is enabling, not disrupting. IP's innovations—kraft processing, coating technologies, recycling systems—improved existing products rather than creating new categories. The company's highest returns came from incremental innovations that customers valued—frustration-free packaging, right-sizing systems, antimicrobial coatings—not breakthrough disruptions. In commodities, evolution beats revolution.

Financial engineering has its place but can't substitute for operational excellence. IP's timberland REIT transaction was brilliant financial architecture, monetizing assets while maintaining operational control. But the 1960s diversification disasters and 1920s power company adventures show financial engineering's limits. Sustainable value creation in commodities requires operational improvements—cost reduction, quality enhancement, service differentiation—that financial maneuvering can't replicate.

The importance of culture in industrial companies is underappreciated by financial analysts but determines long-term success. IP's culture evolved from monopolistic entitlement (1900s) to engineering excellence (1950s) to financial optimization (1980s) to customer solutions (2000s). Each cultural shift took a decade and required leadership changes, often from outside. The lesson: strategy changes quickly, operations change slowly, culture changes glacially—but culture ultimately determines what strategies and operations are possible.

Timing exits is as important as timing entries. IP's best divestitures—timberlands in 2006, coated papers in 2007, Sylvamo in 2021—happened before decline became obvious. The worst—consumer products in the 1970s, power assets in 1941—occurred under distress at terrible prices. The pattern: divest when assets are still strategic to others, not when they're obviously impaired.

Scale advantages in commodities are real but fragile. IP's scale provides procurement leverage, logistics efficiency, and technology investment capacity that smaller competitors can't match. But scale also brings complexity, bureaucracy, and antitrust scrutiny. The sustainable advantage isn't absolute scale but relative scale—being big enough to achieve efficiencies but focused enough to remain agile.

X. Analysis & Bear vs. Bull Case

The competitive landscape reveals IP's precarious dominance. WestRock's merger with Smurfit Kappa creates a $20 billion rival with stronger European presence. Packaging Corporation of America's operational excellence delivers higher margins despite smaller scale. Georgia-Pacific's private ownership enables long-term thinking IP's quarterly earnings focus prevents. Amazon's nascent packaging operations—ostensibly for internal use—could vertically integrate the industry's largest customer. IP leads today, but leads often prove temporary in commodities.

E-commerce tailwinds are powerful but not permanent. The 7x packaging intensity of online versus retail sales drove IP's transformation. But this advantage is moderating. Amazon's frustration with packaging waste is driving innovation in reusable systems. Retailers are fighting back with buy-online-pickup-in-store models that eliminate shipping. Consumer environmental consciousness questions every box's necessity. The e-commerce boom created IP's modern success—but booms, by definition, don't last forever.

Sustainability positioning cuts both ways. IP's renewable, recyclable narrative resonates today, but plastic packaging keeps innovating. New bio-plastics claim environmental superiority. Chemical recycling promises circular plastic economies. Reusable packaging systems could eliminate single-use entirely. IP's betting that fiber's inherent advantages—renewable source, established recycling infrastructure, consumer preference—will prevail. History suggests technology surprises usually defeat incumbents' assumptions.

Capital intensity remains IP's fundamental challenge. The DS Smith acquisition requires $7.2 billion. Annual maintenance capital exceeds $1 billion. Growth investments demand billions more. This capital intensity means IP needs massive scale to generate acceptable returns—but that same scale makes IP slow to adapt when markets shift. Competitors using asset-light strategies (converters, not mills) can pivot quickly while IP's fixed assets anchor strategic flexibility.

Return on invested capital stubbornly lags cost of capital. IP's ROIC hovers around 8-10%, barely exceeding capital costs in good years, falling below in downturns. Management argues this reflects conservative accounting and cycle timing. Skeptics see structural disadvantage in commodity manufacturing. The truth is probably both: IP generates adequate but not exceptional returns, acceptable for steady dividend investors but disappointing for growth seekers.

The DS Smith integration presents execution risk. Cross-border acquisitions fail more often than succeed. European labor regulations differ drastically from American approaches. Brexit complications add complexity. Cultural integration across Atlantic distances challenges any organization. IP's acquisition track record is strong, but DS Smith is IP's first major international deal. The company is betting its consolidation playbook translates globally—evidence suggests that's optimistic.

Environmental regulations are accelerating beyond IP's adaptation capacity. European single-use packaging restrictions spread globally. Carbon taxes make energy-intensive manufacturing uneconomic. Forest management regulations limit fiber access. IP frames these as opportunities for sustainable packaging, but compliance costs are real and rising. Regulatory complexity advantages scaled players theoretically, but also creates disruption opportunities for innovative entrants.

Digital disruption threatens paper demand across categories. Office printing is dying. Marketing materials are going digital. Even packaging faces digital threats through 3D printing and direct-to-consumer models that eliminate traditional distribution. IP has successfully navigated the print-to-packaging transition, but assuming packaging is immune to digital disruption seems dangerously complacent.

China's role creates strategic uncertainty. Chinese papermaking capacity exceeds American and European capacity combined. Chinese producers, often state-supported, can destroy global pricing when domestic demand weakens. IP has minimal Chinese presence, limiting direct exposure but also missing growth opportunities. The company must compete against Chinese exports without access to Chinese markets—a structural disadvantage that could prove decisive.

The bull case rests on three pillars: scale advantages in consolidating industry, e-commerce growth driving packaging demand, and sustainability trends favoring fiber over plastic. IP's global footprint, customer relationships, and operational excellence create moats competitors can't easily cross. The company's transformation from paper to packaging shows strategic adaptability. Management's capital allocation has improved dramatically. The dividend yield provides downside protection while optionality on packaging growth offers upside.

The bear case is equally compelling: commodity manufacturing generates inadequate returns, digital disruption will eventually reach packaging, and Chinese overcapacity will destroy pricing power. IP's capital intensity limits flexibility. The DS Smith integration could disappoint. Environmental regulations could force stranded assets. Most fundamentally, IP is betting physical commerce continues growing when digital alternatives keep emerging.

The realistic assessment lies between extremes. IP is a well-managed commodity company in structural growth markets (packaging) with sustainable competitive advantages (scale, customer relationships, sustainability positioning). But it's still a commodity company—subject to cycles, competition, and disruption. Returns will likely remain adequate but unexceptional. The company will survive and potentially thrive, but expecting technology-like multiples or growth seems unrealistic.

For investors, IP represents a classic value-versus-growth dilemma. The stock offers attractive dividend yield, trades at reasonable multiples, and provides inflation protection through pricing power. But growth is limited, returns are modest, and disruption risks are real. IP works for conservative income investors seeking commodity exposure. It disappoints growth investors expecting transformation. Like the corrugated boxes it produces, IP is functional, essential, and utterly unremarkable—which might be exactly what some investors want.

XI. Epilogue & Looking Forward

The circular economy isn't just environmental marketing—it's IP's next evolution. The company envisions closed-loop systems where every package is recycled into new packaging, where mills run entirely on renewable energy, where forests are carbon sinks rather than sources. This isn't altruism; it's anticipation. IP sees regulation, consumer preference, and technology converging to make linear take-make-waste models obsolete. The company that survived by adapting from newsprint to packaging now adapts from packaging to sustainable materials systems.

Automation and Industry 4.0 are transforming IP's mills from labor-intensive factories to algorithm-optimized systems. Digital twins simulate mill operations, predicting failures before they occur. Machine learning optimizes fiber recipes for specific applications. Autonomous vehicles move materials through facilities. Blockchain tracks recycled content through supply chains. IP is becoming a technology company that happens to make physical products—a transformation as profound as any in its history.

Climate change impacts everything IP does. Rising temperatures shift forest growth patterns, affecting fiber supply. Extreme weather disrupts mill operations and supply chains. Water scarcity threatens production processes. Carbon pricing makes energy-intensive manufacturing increasingly expensive. But IP also sees opportunity: managed forests sequester carbon, creating potential revenue streams. Packaging substitutes for plastic reduce emissions. The company is positioning for a carbon-constrained world, betting that fiber-based solutions become more valuable as carbon costs rise.

China's role in global paper markets remains IP's greatest strategic uncertainty. Chinese capacity continues expanding despite weak demand. Chinese producers are moving upmarket, competing in packaging not just commodity grades. Chinese environmental regulations are tightening, potentially shifting cost advantages. IP must navigate a world where China is simultaneously competitor, customer, and supplier—a complexity that defies simple strategic responses.

The 125-year survival story offers lessons beyond business. IP demonstrates that industrial companies can adapt through technological disruption, that commodity producers can create value, that focused execution beats grand strategy. The company that began as a newsprint monopoly and became a packaging leader shows that corporate evolution is possible—difficult, painful, sometimes nearly fatal—but possible.

Key lessons for industrial consolidators emerge from IP's journey. First, consolidation without operational improvement just creates bigger problems. Second, market power is temporary—technology, regulation, or competition always erodes monopolies. Third, culture matters more than strategy—IP's transformations succeeded when culture aligned with strategy, failed when they diverged. Fourth, patient capital is essential—industrial transformations take decades, not quarters. Finally, humility helps—IP's greatest disasters came from hubris, greatest successes from recognizing and adapting to reality.

Looking forward, IP faces existential questions. Will packaging follow printing into digital obsolescence? Can fiber compete with whatever materials science invents next? Does industrial consolidation make sense when supply chains are regionalizing? Is IP a survivor that will adapt again, or a relic whose time has passed?

The answer depends on whether IP's core capability—transforming fiber into useful products—remains valuable. Betting against IP means betting that physical goods stop needing packaging, that sustainability concerns disappear, that global supply chains vanish. Those seem like losing bets. But betting on IP means believing that a 127-year-old company can keep adapting, that commodity manufacturing can generate acceptable returns, that scale still matters in fragmenting markets.

The story continues. Every Amazon delivery, every sustainable packaging initiative, every mill modernization writes new chapters. IP has survived technological disruption (telegraph to internet), economic catastrophe (multiple depressions and recessions), and strategic confusion (diversification disasters). The company enters its next phase with clear strategy (packaging and fibers), strong market position (global leadership), and adequate finances (investment-grade credit).

But adequacy isn't inspiration. IP won't be the next technology disruption or innovation miracle. It will remain what it's always been—a reflection of the physical economy, prospering when things move, struggling when they don't. For investors seeking excitement, look elsewhere. For those valuing survival, adaptation, and steady returns from essential services, IP offers something increasingly rare: a company that has endured everything markets can inflict and emerged functional, if not triumphant.

The final lesson from IP's history is that boring businesses can be beautiful investments if bought at reasonable prices with appropriate expectations. IP makes boxes—unsexy, unglamorous, absolutely essential boxes. In a world obsessed with disruption, there's value in continuity. In markets chasing growth, there's wisdom in stability. In an economy increasingly virtual, there's opportunity in stubbornly physical businesses that enable everything else.

International Paper began with monopolistic ambition and evolved through competitive reality into sustainable competence. That's not an inspiring corporate slogan, but it's an investable business model. The paper empire became a packaging powerhouse not through revolution but evolution, not through genius but persistence, not through dominance but adaptation. In the end, that might be the most remarkable transformation of all—from extraordinary ambition to ordinary excellence, and discovering that ordinary, executed well over centuries, becomes its own form of extraordinary.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube