IonQ: From Nobel Prize Physics to Wall Street's First Quantum Bet

I. Introduction: The Quantum Moment

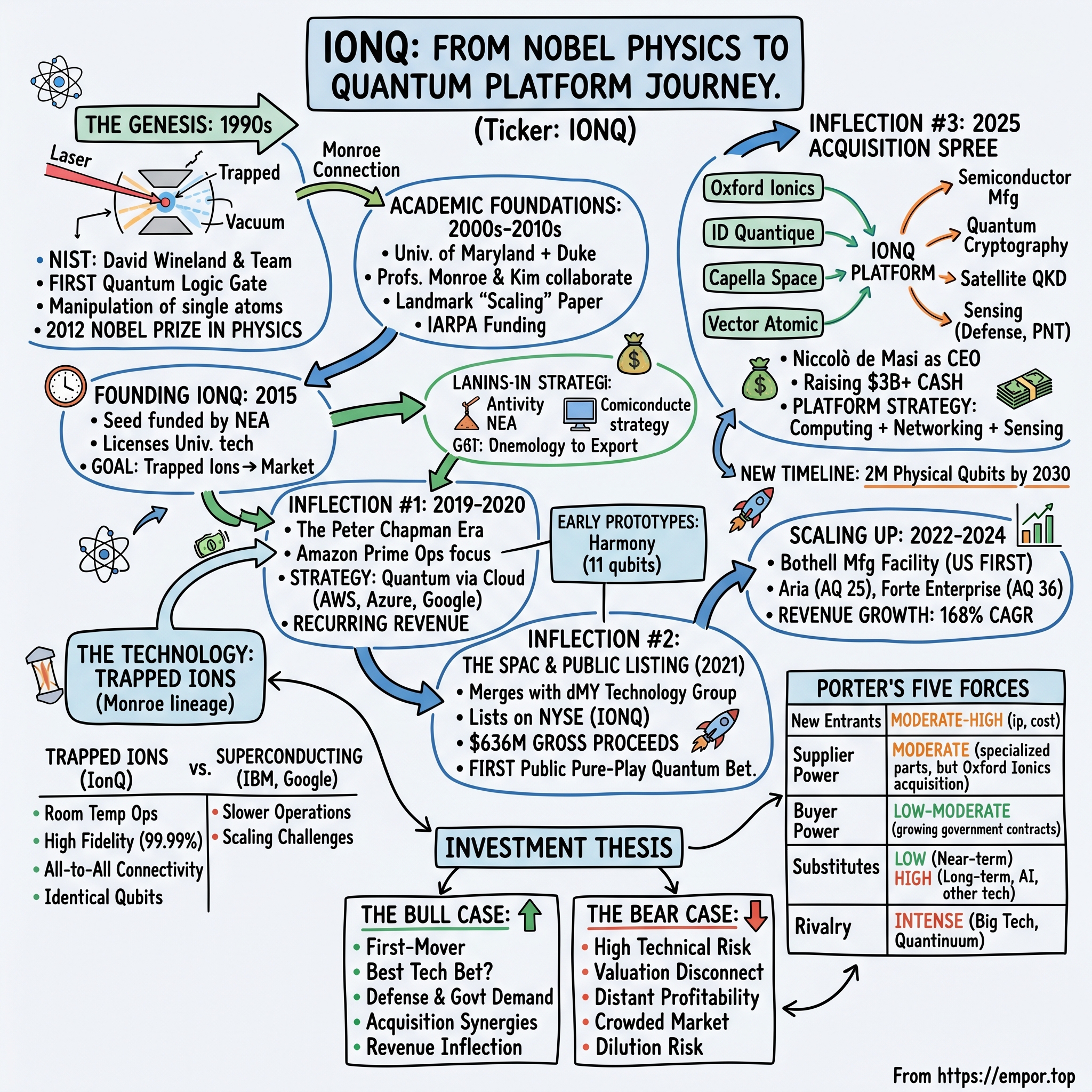

Picture a laboratory in Boulder, Colorado, in 1995. A physicist named David Wineland adjusts an ultraviolet laser beam, focusing it on a single beryllium ion suspended in a vacuum chamber—one atom, invisible to the naked eye, held captive by electromagnetic fields. With a precisely timed pulse, Wineland and his team demonstrate something the quantum physics community had only theorized: the first successful quantum logic gate operation. In that moment, the theoretical promise of quantum computing crossed from physics journals into the realm of engineering possibility.

David Wineland would receive the 2012 Nobel Prize in Physics, jointly with Serge Haroche, for "ground-breaking experimental methods that enable measuring and manipulation of individual quantum systems." Among the researchers working alongside Wineland at NIST was a young physicist named Christopher Monroe, who would spend the next two decades transforming this Nobel Prize-winning science into something the business world hadn't yet imagined: a publicly traded quantum computing company.

IonQ develops quantum computers and networks in the United States. It sells access to quantum computers of various qubit capacities. The company also makes access to its quantum computers through cloud platforms, such as Amazon Web Services (AWS) Amazon Braket, Microsoft's Azure Quantum, and Google's Cloud Marketplace, as well as through its cloud service.

The central question of this story is deceptively simple: How did two physics professors turn 25 years of academic research into Wall Street's first pure-play quantum computing bet? The answer involves Nobel Prize physics, billions of dollars in acquisitions, a strategic pivot from lab curiosity to commercial platform, and perhaps the most ambitious technology roadmap in the emerging quantum industry.

The quantum computing market is projected to reach USD 20.20 billion by 2030 from USD 3.52 billion in 2025, at a CAGR of 41.8% during the forecast period. McKinsey's projections reach even higher, suggesting quantum technologies could generate up to $97 billion in revenue worldwide by 2035. IonQ isn't just building quantum computers—it's betting that trapped ions, the same technology that won a Nobel Prize, will define how humanity computes for the next century.

IonQ recognized revenue of $39.9 million for the third quarter of 2025, which is 37% above the top end of the previously provided range and represents 222% year-over-year growth. That's explosive growth for a company selling access to machines that manipulate individual atoms. But the numbers only hint at the strategic transformation underway: IonQ is expanding rapidly, with a headcount passing 1,000 employees across a dozen sites. The growth is just one step of chief executive Niccolò de Masi's strategy to position IonQ not only as a hardware manufacturer, but as a vertically integrated quantum technology firm with operations spanning computing, secure communications and sensing.

This is the story of how trapped ions went from laboratory curiosity to Wall Street darling—and why the next five years will determine whether IonQ becomes the Intel of quantum computing or a cautionary tale of premature ambition.

II. The Scientific Genesis: Trapped Ions & Nobel Prize Physics (1990s-2010s)

The Wineland Connection

The story of IonQ doesn't begin in a startup garage or a venture capital boardroom. It begins in a government laboratory, with lasers and vacuum chambers and the painstaking work of manipulating individual atoms.

Christopher Monroe's quantum computing research began as a Staff Researcher at the National Institute of Standards and Technology (NIST) with Nobel-laureate physicist David Wineland where he led a team using trapped ions to produce the first controllable qubits and the first controllable quantum logic gate, culminating in a proposed architecture for a large-scale trapped ion computer.

To understand why this matters, you need to understand what trapped ions actually are. Imagine taking a single ytterbium atom—ytterbium is a rare earth element, atomic number 70—and stripping away one of its electrons. You now have an ion, a charged particle that responds to electromagnetic fields. Suspend that ion in a vacuum chamber using precisely calibrated electric fields, and you can hold it perfectly still, isolated from the thermal noise that plagues other quantum systems.

Wineland's group was the first in the world to demonstrate a quantum operation with two quantum bits. Since control operations have already been achieved with a few qubits, there is in principle no reason to believe that it should not be possible to achieve such operations with many more qubits.

The Nobel Prize committee recognized this work because Wineland and his colleague Serge Haroche had achieved something previously thought impossible: Haroche and Wineland have opened the door to a new era of experimentation with quantum physics by demonstrating the direct observation of individual quantum systems without destroying them. Through their ingenious laboratory methods they have managed to measure and control very fragile quantum states, enabling their field of research to take the very first steps towards building a new type of super fast computer, based on quantum physics.

Why trapped ions? The physics creates inherent advantages. On the practical side, Wineland's group in 1995 used trapped ions to perform logical operations in one of the first demonstrations of quantum computing. In the early 2000s Wineland's group used trapped ions to create an atomic clock much more accurate than those using cesium.

Monroe, working in this intellectual environment, absorbed not just the technical methods but the fundamental conviction that trapped ions represented the most promising path to scalable quantum computation. Unlike superconducting qubits—the approach favored by IBM and Google—trapped ions don't require exotic cooling to near absolute zero. They're identical to each other (a feature that simplifies scaling), and they can interact with any other ion in the system, not just their immediate neighbors.

Academic Foundations: Maryland & Duke

Monroe eventually left NIST for academia, but he didn't leave trapped ion research behind. Kim and Monroe, who was at the time a professor at the University of Maryland, College Park, began collaborating formally as a result of larger research initiatives funded by the Intelligence Advanced Research Projects Activity (IARPA).

Jungsang Kim brought complementary expertise. Kim is an internationally renowned pioneer in the field of quantum information sciences. A member of the Duke faculty for over 20 years, he leads the Multifunctional Integrated Systems Technology group and developed a commercially-viable approach to quantum computers by trapping atomic ions in a vacuum chamber and manipulating them with lasers.

The collaboration crystallized into a landmark publication. They wrote a review paper for Science Magazine entitled Scaling the Ion Trap Quantum Processor, pairing Monroe's research at UMD in trapped ions with Kim's focus on scalable quantum information processing and quantum communication hardware.

This wasn't just another academic paper. It was a blueprint—a detailed argument that trapped ion quantum computing could move from laboratory demonstration to commercial reality. The paper caught the attention of venture capitalists who saw something unusual: scientific founders with both deep technical expertise and a clear vision for commercialization.

The First Prototype

After over 25 years of academic research, IonQ was founded in 2015 by Chris Monroe and Jungsang Kim with $2 million in seed funding from New Enterprise Associates, a license to core technology from the University of Maryland and Duke University, and the goal of taking trapped ion quantum computing out of the lab and into the market.

The early prototype was modest by today's standards but groundbreaking at the time. Together, Monroe and Kim built a quantum computer at the University of Maryland that used the same trapped ytterbium ions for qubits as IonQ's later Aria system would use. This early prototype had only five qubits, but it ran the Deutsch–Jozsa algorithm with a 95% success probability and outperformed any other programmable quantum computer at the time.

The University of Maryland is now recognized across the globe as a leader in the field, propelled by a research partnership in quantum science with the National Institute of Standards and Technology and the Laboratory for Physical Sciences that began more than a decade ago. This ecosystem—government labs, academic research, intelligence community funding—created the foundation for what would become a multi-billion-dollar company.

For investors, the scientific genesis matters because it explains IonQ's technological moat. The group's pioneering quantum computing experiments have inspired researchers around the world to develop this potentially revolutionary technology. Dozens of trapped-ion groups now operate at various universities and research institutions. It's safe to say that most in the field use many of the techniques pioneered in the group's lab. IonQ didn't just license technology from universities—it licensed the foundational methods that shaped an entire field.

III. Founding IonQ: From Lab to Startup (2015-2018)

The Founding Decision

The transition from academic research to startup required more than scientific ambition. It required the right partners. IonQ was co-founded by Christopher Monroe and Jungsang Kim, professors at Duke University, in 2015, with the help of Harry Weller and Andrew Schoen, partners at venture firm New Enterprise Associates. The company is an offshoot of the co-founders' 25 years of academic research in quantum information science.

New Enterprise Associates wasn't a typical quantum investor—in 2015, there weren't typical quantum investors. The firm took a calculated bet on the scientific founders' track record. In 2015, New Enterprise Associates invested $2 million to commercialize the technology Monroe and Kim proposed in their Science paper.

Two million dollars isn't much in venture capital terms, but for quantum computing in 2015, it was a significant commitment. The field was still largely academic. Google and IBM had quantum research programs, but commercially-oriented startups were rare. NEA saw an opportunity to back founders with genuine scientific credibility and a clear path to differentiation.

Early Funding & Building the Team

The founders recognized early that academic scientists couldn't run a commercial operation alone. In 2016, they brought on David Moehring from IARPA—where he was in charge of several quantum computing initiatives—to be the company's chief executive.

Moehring's IARPA background was significant. IARPA—the Intelligence Advanced Research Projects Activity—is the research arm of the U.S. intelligence community, funding high-risk, high-reward research that conventional agencies won't touch. Someone who had managed quantum computing programs for IARPA understood both the technology's potential and the government's interest as a customer.

The company moved quickly to raise additional capital. In 2017, they raised a $20 million series B, led by GV (formerly Google Ventures) and New Enterprise Associates, the first investment GV has made in quantum computing technology. They began hiring in earnest in 2017, with the intent to bring an offering to market by late 2018.

GV's investment marked a crucial validation. Google's venture arm had access to expertise from Google's own quantum computing program, which pursued superconducting qubits. That GV would invest in a trapped-ion company suggested real technical merit independent of internal Google politics.

Key Technical Milestones

By 2017, IonQ had demonstrated results that vindicated the scientific bet. The company demonstrated the first fully connected 11-qubit quantum computer, showcasing its ability to scale up quantum systems.

In November 2017, IonQ presented a paper at the IEEE International Conference on Rebooting Computing describing their technology strategy and current progress. It outlines using a microfabricated ion trap and several optical and acousto-optical systems to cool, initialize, and calculate. They also describe a cloud API, custom language bindings, and quantum computing simulators that take advantage of their trapped ion system's complete connectivity.

The phrase "complete connectivity" deserves emphasis. In superconducting quantum computers, qubits can typically only interact with their immediate neighbors, requiring complex routing of operations. Trapped ions, by contrast, can interact with any other ion in the system directly. This architectural advantage simplifies certain quantum algorithms and reduces the overhead required for error correction.

IonQ and some experts claim that trapped ions could provide a number of benefits over other physical qubit types in several measures, such as accuracy, scalability, predictability, and coherence time. Others criticize the slow operational times and relative size of trapped ion hardware, claiming other qubit technologies are just as promising.

The honest acknowledgment of trade-offs matters. Trapped ions offer high fidelity but operate more slowly than superconducting qubits. IonQ's strategic bet was that fidelity would matter more than speed—that it's better to perform fewer operations accurately than many operations with errors. Time would tell whether this bet was correct.

By late 2018, IonQ had emerged from the academic chrysalis. The company had funding, a growing team, technical results, and a clear strategic direction. What it needed next was a leader who could bridge the gap between quantum physics and commercial operations.

IV. Inflection Point #1: The Peter Chapman Era & Cloud Strategy (2019-2020)

Leadership Transformation

In May 2019, IonQ announced a leadership change that signaled its commercial ambitions. Peter Chapman, former engineering director at Amazon Prime, has been named CEO of IonQ, a quantum computer startup backed by GV (formerly known as Google Ventures). He headed a 260-person technology team that handled "delivery experience" for Amazon Prime, the company's super-popular subscription business. But as of last Thursday, Chapman had made yet another career jump; he has been named the chief executive of IonQ, a College Park, Md.-based quantum computing startup backed by GV, the venture capital arm of Alphabet, parent of Google.

Chapman's background seemed incongruous at first glance. What did Amazon Prime's two-day delivery have to do with quantum computing? The answer: operations, scale, and customer experience. Previously, Peter was Director of Engineering for Amazon Prime. He has over 40 years of leadership in software engineering, from when he began his career at 16 working with Marvin Minsky and Seymour Papert in the MIT Artificial Intelligence Lab.

Working with Marvin Minsky—a founding father of artificial intelligence—at age 16 suggested Chapman wasn't a typical operations executive. He understood cutting-edge technology. His Amazon experience meant he understood how to make cutting-edge technology accessible to customers who don't want to understand the underlying complexity.

Quantum computing promises to address the same kinds of optimization problems that Chapman had to deal with for Amazon's next-day deliveries, but on a grand scale. It also doesn't hurt that Chapman previously worked for futurist Ray Kurzweil, or that he believes quantum computers provide the only path to strong, human-like artificial intelligence. "I really like that kind of bleeding edge," Chapman told GeekWire.

The Cloud Platform Bet

Chapman's strategic insight was that quantum computers wouldn't succeed by selling hardware to customers—they would succeed by selling access through the cloud. In the following three years, we raised an additional $20 million from GV, Amazon Web Services, and NEA, and built two of the world's most accurate quantum computers. In 2019, we raised another $55 million in a round led by Samsung and Mubadala, and announced partnerships with Microsoft and Amazon Web Services to make our quantum computers available via the cloud.

The cloud strategy was genius for several reasons. First, it eliminated the massive capital requirement for customers to buy quantum hardware. Second, it created recurring revenue rather than one-time sales. Third, it leveraged the existing cloud infrastructure of Amazon, Microsoft, and Google—turning potential competitors into distribution partners.

Chapman believes that quantum computing on the cloud and the ability for people to get access to real quantum hardware is accelerating faster than anyone initially anticipated. After spending an hour with him, I knew he was a visionary. He revealed that side of himself in one last quote I'd like to share: "There is one great thing I love about the quantum cloud environment, and that is the largest financial institu—financial institutions, presumably, were among the first to explore quantum computing for portfolio optimization and risk analysis.

By late 2019, IonQ had positioned itself uniquely. It was the only company with its quantum systems available through both the Amazon Braket and Microsoft Azure clouds, as well as through direct API access. Customers could write quantum code without ever touching quantum hardware.

First Commercial Systems

IonQ's progress to date has attracted attention from investors as well as from Microsoft. In October, the company said it secured $55 million in a funding round led by the Samsung Catalyst Fund and Mubadala Capital. Chapman's former employer, Amazon, joined in the round, as did Airbus Ventures, Hewlett Packard Pathfinder, GV (a Google spin-out) and other venture funds.

In late 2019, the company announced its first commercially available quantum computer, Harmony, featuring 11 qubits and accessible via cloud platforms, representing a pioneering step in making trapped-ion systems available beyond academic labs. In fall 2020, IonQ unveiled its next-generation quantum computer system and opened the Quantum Data Center in the Discovery District to expedite the development of even more powerful quantum computers for commercial use.

The Discovery District location—near the University of Maryland and federal agencies in the Washington, D.C. area—positioned IonQ for government contracts while maintaining proximity to its academic roots. It was strategic geography for a company that would increasingly depend on federal funding and defense applications.

Chapman's operational discipline transformed IonQ from a research-focused startup to a commercial entity. Revenue was still minimal—this was infrastructure for the future—but the foundation for the next inflection point had been laid.

V. Inflection Point #2: The SPAC & Going Public (2021)

Why Go Public via SPAC?

The year 2021 marked a turning point not just for IonQ, but for how Wall Street perceived quantum computing. IonQ, Inc. ("IonQ" or the "Company") (NYSE: IONQ), a leader in quantum computing, completed its previously announced business combination with dMY Technology Group, Inc. III ("dMY") (formerly NYSE: DMYI), a publicly traded special purpose acquisition company, on September 30, 2021. Starting this morning, the common stock and warrants of the combined company, IonQ Inc., will be listed on the New York Stock Exchange under the ticker symbols "IONQ" and "IONQ.WS," respectively.

Why a SPAC rather than a traditional IPO? For a pre-revenue quantum computing company, the traditional IPO roadshow would have been challenging. How do you explain trapped ions to institutional investors focused on quarterly earnings? SPACs allowed IonQ to go public with a story about the future rather than a track record of profitability.

This business combination provided IonQ with $636 million in gross proceeds to fund future growth and accelerate the commercialization of its industry-leading quantum computers. "Quantum is here, and IonQ is leading the industry with our revolutionary trapped-ion technology," said Peter Chapman, President and CEO of IonQ. "Over the past six years, we have taken this critical technology out of the lab and have developed it into a commercial product. This year, we are proud to have tripled our bookings expectations for 2021, and are further thrilled to have announced collaborations with Goldman Sachs, Fidelity Center for Applied Technology, GE Research and the University of Maryland.

The SPAC merger valued IonQ at $2 billion—remarkable for a company that had barely begun commercializing its technology. But the SPAC structure came with advantages beyond the capital raise. It provided liquidity for early investors and employees, created a public currency for acquisitions, and elevated IonQ's profile in a way that private funding rounds couldn't match.

The IPO Mechanics

The SPAC's stockholders granted final approval on the deal, with 97% approving—an overwhelming endorsement of the quantum computing thesis. As part of the deal, Harry You and Niccolo de Masi joined the board of directors for IonQ. De Masi's involvement would prove consequential: He later co-founded dMY Technology Group, which completed several special-purpose acquisition company (SPAC) mergers, including IonQ's 2021 public listing.

De Masi wasn't just a SPAC sponsor; he was a physicist by training with experience scaling technology companies. His presence on the board signaled that IonQ had attracted directors who understood both the technology and the path to commercial scale.

First-Mover Advantage in Public Markets

The public listing positioned IonQ as the first pure-play quantum computing company on the New York Stock Exchange. This first-mover advantage mattered enormously. When investors wanted exposure to quantum computing, IonQ was the only direct option. Competitors like Quantinuum (backed by Honeywell) and Rigetti remained private, while quantum divisions at IBM, Google, and Microsoft were buried within massive conglomerates.

The customer announcements accompanying the IPO demonstrated early commercial traction. In 2021, IonQ tripled its bookings expectations, and announced collaborations with Goldman Sachs, Fidelity Center for Applied Technology, GE Research and the University of Maryland.

Goldman Sachs and Fidelity exploring quantum computing for financial applications wasn't just validation—it was a preview of how quantum might transform industries. Portfolio optimization, risk analysis, options pricing—financial services had problems perfectly suited to quantum computational advantages.

For investors evaluating IonQ's public market debut, the key insight was strategic positioning. IonQ had established relationships with all three major cloud providers, secured Fortune 500 customers experimenting with quantum applications, and now had $636 million in capital to accelerate commercialization. The question wasn't whether quantum computing would matter—it was whether IonQ would be the company that captured the opportunity.

VI. Scaling Up: Product Evolution & Manufacturing (2022-2024)

Hardware Generations

The years following the IPO were characterized by rapid hardware advancement. IonQ developed a product hierarchy designed to address different customer needs.

The Aria system, IonQ's foundational cloud-accessible quantum computer, features 25 physical qubits and an #AQ score of 25, with median two-qubit gate fidelity of 99.4% and one-qubit gate fidelity of 99.94%. Launched in early access in 2021 and commercially available from 2022, Aria prioritized broad accessibility for algorithm development.

Understanding "Algorithmic Qubits" (#AQ) is essential for evaluating IonQ's progress. Traditional qubit counts can be misleading—a 100-qubit system with high error rates may be less useful than a 25-qubit system with exceptional accuracy. #AQ attempts to capture usable computational power by combining qubit count with gate fidelity. It's IonQ's answer to the metrics problem in quantum computing.

IonQ has introduced multiple quantum systems including IonQ Aria, Forte, and the enterprise-grade Forte Enterprise, which reached 36 algorithmic qubits (AQ36) as of December 2024. The Forte Enterprise represents the current commercial flagship—powerful enough for enterprise applications while manufacturable at scale.

Manufacturing Infrastructure

The transition from research prototypes to manufacturable products required new capabilities. IonQ today announced the opening of the United States' first quantum computing manufacturing facility, located in Bothell, Washington, a suburb of Seattle. As part of this announcement, the company also shared an expansion of its Seattle facilities, increasing its footprint from 65,000 square feet to an impressive 105,000 square feet. The facility will be IonQ's second quantum data center providing cloud access to IonQ customers, and the primary production engineering location in the U.S.

The Bothell facility marked a fundamental shift in how IonQ operated. This is the first factory in the U.S. that will manufacture quantum computers that are replicable and deployable in customers' data centers.

"I think we're the only company who's thinking about how the next generation needs to be half the cost of the previous generation," Chapman said. "So, what this place is really about is getting to a point where we can use contract manufacturers to build subassemblies for us, and then we do final assembly downstairs."

The cost discipline matters. Quantum computers today are expensive—multi-million-dollar systems requiring specialized installation and maintenance. IonQ's manufacturing strategy aims to make them affordable enough for widespread enterprise adoption. Chapman's Amazon background, with its relentless focus on cost reduction and scale economics, shaped this approach.

Chapman said the company will invest $80 million in the region this year, and a projected $1 billion over the next 10 years. That's a substantial commitment to manufacturing infrastructure in an era when many tech companies have outsourced production overseas.

Financial Growth Trajectory

The revenue trajectory validated the commercial strategy. IonQ recognized revenue of $43.1 million for full year 2024, exceeding the high end of guidance. This represents 95% annual growth compared to $22.0 million in the prior year. The company's revenue has soared by a compound annual growth rate of 168% since 2021.

For a company that barely generated revenue at the time of its IPO, this growth rate is remarkable. But context matters: IonQ remains deeply unprofitable, investing heavily in R&D and infrastructure. This follows a full-year 2024 net loss of $331.6 million. Revenue growth must eventually translate to sustainable unit economics—a transition that remains years away.

The revenue composition shifted meaningfully. Cloud access fees, hardware sales, and consulting services all contributed, with government contracts becoming increasingly significant. IonQ secured a $25.5 million project with the United States Air Force Research Lab to implement quantum computing systems at their facilities, demonstrating federal interest in quantum capabilities for defense applications.

VII. Inflection Point #3: The 2025 Acquisition Spree

Strategic Transformation Through M&A

2025 marked a dramatic strategic transformation. IonQ shifted from building quantum computers to building a quantum platform—a vertically integrated ecosystem spanning computing, networking, sensing, and security.

The acquisition pace was breathtaking:

IonQ has completed its acquisition of a controlling stake in ID Quantique, expanding its capabilities in quantum-safe networking and quantum detection systems. The completion of the IDQ acquisition builds on IonQ's recent momentum in the quantum networking industry, including the acquisition of Qubitekk, a quantum networking leader in the U.S.

IonQ will acquire Oxford Ionics for $1.075 billion in stock and cash, combining two of the leaders in trapped-ion quantum computing in a deal that could reshape the commercial quantum landscape. The combined company aims to scale to 256 high-fidelity qubits by 2026 and over 10,000 physical qubits by 2027, using Oxford Ionics' semiconductor-compatible ion-trap technology.

IonQ has completed its acquisition of Capella Space to begin developing a space-based quantum key distribution (QKD) network for secure global communications. The combined platform will integrate IonQ's quantum technology with Capella's satellite infrastructure to enable quantum-secure data transfer and quantum-enhanced Earth observation capabilities.

IonQ has completed its all-stock acquisition of Vector Atomic, a California-based quantum sensing company, expanding its capabilities in precision atomic clocks, inertial sensors, and synchronization technologies. The deal brings over 75 employees and 29 patents from Vector Atomic, whose sensing systems offer picosecond timing accuracy—up to 1,000 times more precise than GPS—and are used in space, submarine, and airborne applications.

Each acquisition served a strategic purpose. ID Quantique brought quantum-safe cryptography—essential as quantum computers threaten to break current encryption. Oxford Ionics brought semiconductor-compatible manufacturing techniques that could accelerate hardware scaling. Capella Space brought satellite infrastructure for space-based quantum key distribution. Vector Atomic brought quantum sensing for defense and navigation applications.

With the IDQ acquisition, IonQ's product portfolio now includes IDQ's quantum key distribution (QKD) systems, quantum random number generators (QRNGs), and single-photon detectors. The addition of nearly 300 granted and pending patents from IDQ brings the total number of patents IonQ controls to over 900, solidifying its intellectual property leadership in quantum technologies.

The Quantum Platform Strategy

The acquisition spree reflected a fundamental strategic insight: quantum computing alone isn't a platform. IonQ sets out to "build the world's best quantum computers to solve the world's most complex problems." "We're the only company in the world that does both quantum computing and quantum networking. Both of them are kind of equally large and important pieces of our business."

IonQ is focusing on all three areas—computing, communications, sensing—and bills itself as "the only quantum platform company in the world." Whether this claim holds up to scrutiny depends on how you define "platform," but the strategic ambition is clear.

By leveraging Oxford Ionics' chip-integrated ion traps and Lightsynq's photonic interconnects (IonQ's recent acquisitions), IonQ plans to boost its qubit counts by orders of magnitude. The company's new timeline projects a jump from today's tens of qubits to ~20,000 physical qubits by 2028, spread across two entangled chips, and reaching ~2,000,000 physical qubits by 2030. Crucially, IonQ estimates this will equate to about 1,600 error-corrected logical qubits in 2028, and on the order of 40,000–80,000 logical qubits by 2030 as error-correction improves.

These projections are aggressive—far more ambitious than IonQ's previous roadmaps. Whether they're achievable depends on successful integration of acquired technologies and continued R&D progress. The acquisitions provide the pieces; execution will determine whether they fit together.

Leadership Transition

The acquisition spree coincided with leadership change. Niccolò de Masi became president and chief executive officer of IonQ on February 26, 2025, after serving on the company's board since 2021. He succeeded Peter Chapman, who transitioned to the role of Executive Chair. On August 6, 2025, de Masi was unanimously appointed chairman of IonQ's board.

Chapman's departure from the CEO role after nearly six years raised questions about strategic direction. But de Masi's background suggested continuity with enhanced M&A capability. De Masi, a physicist by training, has extensive leadership experience in public companies and played a key role in taking IonQ public via SPAC merger in 2021. He has raised over $3 billion in equity across his career and aims to accelerate IonQ's growth in the quantum computing industry.

Niccolo is a physicist by training, holding a B.A. and Master of Science in Physics from Cambridge University and began his career with roles at both Siemens Solar and Technicolor.

A physicist who understands capital markets—exactly the profile needed to execute an aggressive acquisition strategy while maintaining technical credibility. De Masi's subsequent capital raises provided the firepower for M&A: IonQ reported $3.5 billion in cash and investments as of September 30, 2025 (pro forma for $1.98 billion of net proceeds from an equity issuance on October 14, 2025), with zero debt. This substantial cash position resulted from two significant capital raises in 2025: a $1.0 billion raise at a 25% premium to July 2025 trading prices and a $2.0 billion raise at a 20% premium to October 2025 trading prices.

Raising equity at premiums to market price—not typical for capital raises—suggested strong investor demand for IonQ's platform vision. The question for long-term investors: will the acquisitions generate value exceeding the dilution from share issuance?

VIII. The Technology Deep Dive: Why Trapped Ions?

The Trapped Ion Approach

To understand IonQ's competitive position, you need to understand the physics. What sets IonQ apart from its many rivals in the quantum computing space is its technology. Quantum computers typically require temperatures colder than outer space to keep the subatomic particles stable enough to minimize calculation errors. However, IonQ's systems can operate at room temperature.

This room-temperature operation is partly marketing—IonQ's systems still use lasers and vacuum chambers—but the contrast with superconducting qubits is real. IonQ uses vastly different technology from IBM. While Big Blue's quantum solutions require specialized cryogenic equipment, IonQ's tech can operate at room temperature. The feature is key to cost-efficient quantum computers, and as a result, IonQ estimates competitors are spending 30 times more for their equipment.

The 30x cost claim deserves scrutiny, but the directional point stands. Cryogenic systems—cooling qubits to temperatures near absolute zero—consume enormous amounts of energy and require complex infrastructure. Trapped ions avoid this overhead, potentially enabling more economical deployment.

Unlike superconducting circuits, which are affixed to the surface of a quantum computing chip, ions on Quantinuum's Helios chip can be shuffled around. Because the ions can move, they can interact with every other ion in the computer, a capacity known as "all-to-all connectivity." This connectivity allows for error correction approaches that use fewer physical qubits. In contrast, superconducting qubits can only interact with their direct neighbors, so a computation between two non-adjacent qubits requires several intermediate steps involving the qubits in between. "It's becoming increasingly more apparent how important all-to-all-connectivity is for these high-performing systems."

Technical Advantages & Trade-offs

The technology debates in quantum computing resemble religious wars, with partisans of different approaches claiming ultimate victory for their preferred qubit type. The honest assessment acknowledges trade-offs.

Trapped ion advantages: - High gate fidelity (IonQ claims 99.99% two-qubit gate performance) - All-to-all connectivity (any qubit can interact with any other) - Long coherence times (qubits maintain quantum states longer) - Identical qubits (simplifies scaling and error correction)

Trapped ion disadvantages: - Slower gate operations (microseconds vs. nanoseconds for superconducting) - Fewer qubits currently available (tens vs. hundreds for superconducting) - Complex optical control systems (lasers for each qubit operation)

Still, it's not clear what type of qubit will win in the long run. Each type has design benefits that could ultimately make it easier to scale. Ions (which are used by the US-based startup IonQ as well as Quantinuum) offer an advantage because they produce relatively few errors.

IonQ's strategic bet is that quality matters more than quantity—that fewer, more accurate qubits outperform more numerous, error-prone qubits. This bet becomes increasingly relevant as the industry moves toward fault-tolerant quantum computing, where error correction is essential.

The Path to Fault Tolerance

The ultimate goal isn't quantum computers that work sometimes—it's quantum computers that work reliably, with errors corrected automatically. This requires "fault-tolerant" quantum computation.

IonQ has unveiled an accelerated quantum computing roadmap that, if realized, could deliver a cryptographically relevant quantum computer (CRQC) as early as 2028. In a June 2025 announcement, the Maryland-based quantum startup – known for its trapped-ion technology – outlined dramatic scaling milestones enabled by recent acquisitions and technical breakthroughs.

The 2025 technical achievements validated progress toward this goal. Among its key achievements, IonQ announced record 99.99% two-qubit gate performance, which the company described as a world record for commercial quantum systems. The metric measures the accuracy of basic computational operations and is central to developing error-corrected, fault-tolerant machines. The company also said its Tempo quantum computer achieved an algorithmic qubit score of #AQ 64, the highest yet reported and three months ahead of schedule. The company explained that the #AQ score measures the effective computational power of a quantum system, capturing both qubit number and quality.

De Masi stated: "We delivered our 2025 technical milestone of #AQ 64 three months early, unlocking 36 quadrillion times more computational space than leading commercial superconducting systems. We achieved a truly historic milestone by demonstrating world-record 99.99% two-qubit gate performance, underscoring our path to 2 million qubits and 80,000 logical qubits in 2030."

Whether "36 quadrillion times more computational space" is meaningful depends on the specific computation. Quantum advantage isn't universal—it applies to particular problem classes. But the technical progress is genuine, and the roadmap is now more aggressive than ever.

IX. Competitive Landscape: The Quantum Computing Wars

The Big Tech Giants

IonQ operates in perhaps the most competitive technology landscape in existence. NVIDIA's latest move into quantum computing through a landmark investment in Honeywell-backed Quantinuum has jolted the sector, instantly lifting its profile among investors. Following the Sept. 4 announcement, the Defiance Quantum ETF (QTUM) rallied 2.3%. For public pure-plays like IonQ, Rigetti Computing and D-Wave Quantum, this development brings both opportunity and pressure. On the one hand, it sparks renewed investor attention and potential capital flows into the space. On the other hand, it raises the bar for technological execution and commercial traction.

The competitive set includes companies with effectively unlimited resources. Google, IBM, Microsoft, and Amazon all maintain significant quantum computing programs. Their advantage: they can sustain losses indefinitely while quantum matures. Their disadvantage: quantum represents a tiny fraction of their business, limiting organizational focus.

IBM's Superconducting Bet

IBM has pursued superconducting qubits with religious conviction, building progressively larger systems and establishing itself as the quantum computing thought leader for enterprise customers.

IBM: Aims to debut a full fault-tolerant quantum computer by 2029. IBM's June 2025 roadmap set a target of ≈200 logical qubits by 2029, with a clear path to ~1,000+ logical qubits in the early 2030s. IBM's approach involves scaling up its superconducting qubit processors (1,121-qubit "Condor" chip slated for 2024) and then multi-chip modular systems, combined with heavy investment in error-correction software.

IBM's qubit counts are impressive—over 1,000 physical qubits—but the useful computational power depends on error rates. IonQ argues that its 36 algorithmic qubits outperform IBM's larger systems for practical applications, a claim that's difficult to verify independently but reflects genuine architectural differences.

Google's Quantum AI

Google achieved the first widely-accepted demonstration of "quantum supremacy" in 2019, showing a quantum computer could solve a specific problem faster than any classical computer. More recently, Google has continued advancing.

By late 2024, Alphabet introduced a state-of-the-art quantum processor, Willow, that reduces errors exponentially with each additional qubit. Willow finished a benchmark test in less than five minutes that classical supercomputers could not compete with in less than the age of the universe.

Google's focus on demonstrating quantum advantage, even for narrow problems, validates the potential of quantum computing while also highlighting how far the technology remains from general utility.

Quantinuum: The Other Trapped Ion Player

IonQ's most direct competitor uses the same fundamental technology. Quantinuum (Honeywell): The leading trapped-ion competitor has focused on fidelity over quantity. Quantinuum achieved a fully error-corrected logical qubit (Steane code) back in 2021 and has kept one "alive" through multiple QEC cycles.

On Sept. 4, 2025, Honeywell announced that its quantum computing arm, Quantinuum, completed an approximately $600 million equity capital raise at a $10 billion pre-money valuation. Key new investors include Quanta Computer, NVentures (NVIDIA's venture capital arm) and QED Investors, alongside follow-on investments from existing backers such as JPMorgan Chase.

A $10 billion valuation for Quantinuum, backed by Honeywell's industrial might and NVIDIA's AI ecosystem, represents formidable competition. Even within the trapped-ion space, IonQ's 99.99% gate fidelity slightly surpasses Quantinuum's reported 99.92% for its Helios processor, intensifying competition.

Quantinuum plans to build another version of Helios in its facility in Minnesota. It has already begun to build a prototype for a fourth-generation computer, Sol, which it plans to deliver in 2027, with 192 physical qubits. Then, in 2029, the company hopes to release Apollo, which it says will have thousands of physical qubits and should be "fully fault tolerant," or able to implement error correction at a large scale.

IonQ's Differentiated Position

What distinguishes IonQ in this competitive landscape? IonQ stands as the crown jewel of quantum computing investments, representing the first pure-play quantum company to go public and maintaining its position as the industry leader. The company's trapped-ion quantum computing technology offers a unique competitive advantage, operating at near room temperature while achieving exceptional qubit fidelity rates. IonQ's recent technological breakthroughs have positioned the company for unprecedented commercial success.

The presentation highlights this revenue progression and emphasizes that IonQ's revenue scale is approximately 11 times greater than its nearest competitors in the quantum computing space.

The 11x revenue claim positions IonQ as the commercial leader among pure-play quantum companies. Combined with the platform strategy encompassing computing, networking, and sensing, IonQ has differentiated itself from both trapped-ion competitors like Quantinuum and superconducting-focused companies like IBM and Google.

X. Porter's Five Forces Analysis & Strategic Assessment

Threat of New Entrants: MODERATE-HIGH

The barriers to entry in quantum computing appear formidable but are eroding. High barriers include:

- Scientific expertise: IonQ's technology builds on 25+ years of research, including work with Nobel laureate David Wineland

- Capital requirements: IonQ raised $636 million at IPO and over $3 billion subsequently; replicating this is challenging

- Customer relationships: Partnerships with AWS, Microsoft, and Google create switching costs

- Intellectual property: IonQ controls over 900 patents following acquisitions

However, entry barriers are lowering:

Government agencies and regulatory bodies are playing a pivotal role, with initiatives such as the US National Quantum Initiative Act and the EU Quantum Flagship Program, as well as similar strategies in Asia, driving R&D funding, workforce development, and industry collaboration.

Government funding enables new competitors. According to research from SpinQ, quantum computing companies raised $3.77 billion in equity funding during the first nine months of 2025 — nearly triple the $1.3 billion raised in all of 2024. Capital is flowing into the sector, enabling well-funded startups like PsiQuantum (photonic qubits) to pursue alternative approaches.

Bargaining Power of Suppliers: MODERATE

IonQ's supply chain involves specialized components—laser systems, vacuum equipment, ion traps—often sourced from academic or government suppliers initially developed for research applications. The acquisition of Oxford Ionics, with its semiconductor-compatible manufacturing, aims to shift toward standard foundry manufacturing that would reduce supplier concentration.

The Pacific Northwest National Laboratory partnership for barium ions demonstrates how IonQ has cultivated strategic supplier relationships, but dependence on specialized inputs creates vulnerability.

Bargaining Power of Buyers: LOW-MODERATE

Currently, buyers (enterprises exploring quantum computing) have limited options. IonQ's cloud availability through AWS, Azure, and Google Cloud creates convenience that reduces switching incentives. However, as quantum computers become more capable, large customers like financial institutions or pharmaceutical companies may demand pricing concessions or exclusive capabilities.

Government customers—increasingly important to IonQ's revenue mix—have significant bargaining power but also provide multi-year contracts that create revenue visibility.

Threat of Substitutes: LOW (Near-Term), HIGH (Long-Term)

No classical computing substitute exists for the problems quantum computers are designed to solve. However, the timeline for quantum advantage remains uncertain. If classical computing advances—including AI-enhanced optimization—continue outpacing quantum progress, the perceived value proposition weakens.

The broader substitution threat is that quantum computing never achieves broad commercial relevance, remaining a niche technology for specialized applications.

Competitive Rivalry: INTENSE

IonQ and Quantinuum are on a collision course in the trapped-ion space, both vying to be first to a truly useful quantum computer. Quantinuum's backing by an industrial giant (Honeywell) plus recent investment from Japanese conglomerates means they are well-funded too. This rivalry is one to watch, even if investors can't directly invest in Quantinuum yet.

Rivalry extends beyond trapped ions. Google, IBM, and Microsoft compete with different technologies but pursue similar customers. Each competitor has different strengths: IBM's enterprise relationships, Google's AI integration, Microsoft's Azure ecosystem. IonQ's cloud partnerships position it as a complement rather than competitor to some of these players, but that positioning could shift as the market matures.

Hamilton Helmer's 7 Powers Framework

Examining IonQ through the 7 Powers framework reveals both strengths and gaps:

Counter-Positioning: IonQ's trapped-ion architecture creates genuine counter-positioning versus superconducting competitors. IBM and Google would have to abandon their existing technology investments to match IonQ's approach—a classic counter-positioning dynamic.

Scale Economies: Limited currently. Manufacturing scale economies may emerge as production volumes increase, but IonQ hasn't yet demonstrated classical hardware-style cost curves.

Network Effects: Modest. Developer ecosystems exist around IonQ's cloud platforms, but network effects aren't as strong as in consumer technology.

Switching Costs: Growing. As customers develop quantum algorithms on IonQ's systems, switching to competitors requires rewriting code and relearning platform-specific tools.

Branding: IonQ has established itself as the public market's quantum computing company, creating mindshare advantages with investors and customers.

Cornered Resource: The scientific talent—including Monroe and Kim's research lineage from Nobel Prize physics—represents a cornered resource. The acquisitions of Oxford Ionics, ID Quantique, and others add to this talent pool.

Process Power: Early evidence. The Bothell manufacturing facility aims to create proprietary manufacturing processes, but it's too early to claim defensible process advantages.

IonQ's strongest powers are counter-positioning and cornered resources. The platform strategy aims to develop switching costs and scale economies over time.

XI. Bull Case, Bear Case & Key Metrics

The Bull Case

1. First-Mover Platform Advantage: IonQ has established itself as the only publicly traded, pure-play quantum platform company spanning computing, networking, and sensing. This integrated approach could create a winner-take-most dynamic similar to how Amazon Web Services dominated cloud computing.

2. Trapped Ions Win the Technology Race: If gate fidelity proves more important than qubit count—which the physics suggests—IonQ's technology choice was correct. The 99.99% two-qubit gate performance, if sustained and improved, could enable fault-tolerant quantum computing years ahead of superconducting competitors.

3. Government and Defense Demand: Quantum computing has national security implications. IonQ's contracts with the Air Force Research Laboratory, intelligence community connections through IARPA alumni, and acquisition of Vector Atomic's defense-oriented sensing technology position the company for substantial government revenue as quantum becomes strategically critical.

4. Acquisitions Create Synergies: The 2025 acquisition spree assembled complementary technologies—Oxford Ionics' semiconductor manufacturing, ID Quantique's cryptography, Capella's satellites, Vector Atomic's sensors. If these pieces integrate successfully, IonQ could offer capabilities no competitor matches.

5. Revenue Inflection: For the full year 2025, IonQ is raising its revenue expectations to between $106 million and $110 million. Roughly tripling revenue from 2024 demonstrates commercial traction. Continued growth at this pace would validate the platform thesis.

The Bear Case

1. Technology Risk Remains Substantial: Quantum computing has been "five years away" for decades. IonQ's aggressive roadmap—2 million qubits by 2030—assumes technology progress that may not materialize. Competitors pursuing different approaches could leapfrog trapped ions.

2. Valuation Disconnected from Fundamentals: IonQ possesses compelling qualities to succeed in quantum computing, but note that its share price valuation is sky-high with a price-to-sales (P/S) ratio over 300. In contrast, Palo Alto Networks has a P/S multiple of 16, and IBM's is an attractive 4. Therefore, IonQ stock is only for investors with a high risk tolerance. At current valuations, years of growth are already priced in.

3. Profitability Remains Distant: IonQ reported third-quarter revenue of $39.9 million, up 222% year over year, while posting a net loss of $1.1 billion as it expanded investments in technology and global operations. The company burns significant cash and hasn't articulated a clear path to profitability.

4. Competition Intensifying: Quantinuum's $10 billion valuation and NVIDIA investment suggest the trapped-ion space is crowded. Google, IBM, and Microsoft have effectively unlimited resources to pursue quantum computing. PsiQuantum and other well-funded startups pursue alternative approaches.

5. Integration Risk: The 2025 acquisition spree assembled disparate companies across multiple geographies. Integration is notoriously difficult; combining research-oriented startups while maintaining innovation momentum is even harder.

6. Dilution Concerns: The $3+ billion raised in 2025 came through equity issuance, diluting existing shareholders. If further capital raises are required—likely given the company's burn rate—additional dilution will follow.

Key Performance Indicators to Monitor

For long-term fundamental investors, three KPIs matter most:

1. Algorithmic Qubits (#AQ) Progress: IonQ's proprietary metric captures both qubit count and quality. Progress from AQ36 to AQ64 in 2025 demonstrates technical advancement. Monitoring whether subsequent systems achieve AQ256 and beyond validates the roadmap. This is the most important leading indicator of technological competitiveness.

2. Revenue Growth Rate & Composition: Revenue growth demonstrates commercial traction. Beyond the topline, composition matters: what percentage comes from cloud access versus hardware sales versus government contracts? Growing enterprise revenue from cloud access would validate the platform strategy; over-reliance on one-time government contracts would suggest narrower opportunity.

3. Cash Burn Relative to Revenue: With $3.5 billion in cash and $110 million in projected 2025 revenue, IonQ has substantial runway. But the adjusted EBITDA loss guidance of approximately $211 million indicates significant ongoing investment. Monitoring whether operating leverage improves—revenue growing faster than expenses—reveals whether the business model scales.

XII. Conclusion: The Quantum Bet

The IonQ story encapsulates the fundamental tension in emerging technology investment: visionary potential versus execution risk.

On one side stands a company born from Nobel Prize-winning physics, led by a CEO with both scientific training and capital markets experience, pursuing a platform strategy that could define quantum computing for decades. "Quantum computing is the last phase of the computer revolution," de Masi told the Financial Times.

On the other side stands a company burning hundreds of millions annually, competing against well-funded rivals, and dependent on technology roadmaps that may prove overly optimistic.

The 2025 transformation—from quantum computing startup to integrated quantum platform company—represents a strategic bet that mirrors how the great technology platforms emerged. Amazon started with books before becoming the everything store. Apple built computers before building the iPhone ecosystem. IonQ is betting that trapped ions are its books, its computers—the foundation for something much larger.

According to de Masi, quantum is not a far-future technology in need of theoretical validation but a commercial tool solving problems today. He said growth in the mid-2020s will be defined by the expanding share of workflows that quantum machines absorb. Over time, he added, more of the task will shift from classical processors to quantum systems because of energy efficiency, cost advantages and the ability to solve computation previously deemed impossible.

The market will ultimately determine whether IonQ's vision materializes. For now, the company has positioned itself as the primary public market vehicle for investing in quantum computing's potential. As CEO de Masi stated in the Q3 2025 earnings call: "We are the largest pure-play quantum company by any measure: revenue, patents, PhDs, balance sheet, market capitalization."

Being the largest pure-play quantum company matters only if quantum computing matters. The next five years will reveal whether trapped ions—the technology David Wineland pioneered in a government laboratory decades ago—become the foundation for a new computing era. IonQ has bet the company on that outcome.

For investors, the question isn't whether quantum computing will eventually transform industries—the physics suggests it will. The question is whether IonQ will be the company that captures that transformation, whether the current valuation fairly reflects that probability, and whether you have the patience to find out.

MYTH VS. REALITY

Myth: "Quantum computers will replace classical computers." Reality: Quantum computers excel at specific problem types—optimization, simulation, cryptography—but won't replace classical computers for general-purpose computing. IonQ's opportunity depends on the size of those specific applications, not wholesale computing replacement.

Myth: "IonQ has technological advantages that competitors can't replicate." Reality: Quantinuum uses the same trapped-ion approach and achieved similar fidelity levels. IonQ's advantages are more about execution, partnerships, and capital access than proprietary physics. The technology is replicable; the commercial position may not be.

Myth: "Revenue growth proves the business model works." Reality: Revenue growth demonstrates customer interest but doesn't prove unit economics. IonQ's losses substantially exceed its revenue. The business model works only if eventually revenue grows faster than costs—a transition that remains unproven.

MATERIAL LEGAL AND REGULATORY CONSIDERATIONS

Accounting Judgments: IonQ's acquisition accounting involves significant judgment regarding fair value of acquired intangible assets and goodwill. The $1+ billion in acquisitions in 2025 created substantial goodwill that could face impairment if technology roadmaps don't materialize.

Export Controls: Quantum computing technology faces evolving export control regulations. IonQ's international expansion—including UK operations via Oxford Ionics—requires navigating complex regulatory frameworks that could constrain business development.

Government Contract Compliance: Growing dependence on U.S. government contracts subjects IonQ to government contractor regulations, cost accounting standards, and security clearance requirements that add compliance complexity.

Dilution Risk: The company's SEC filings should be reviewed carefully for authorized share counts and potential future equity raises that could dilute existing shareholders.

IonQ's supply chain requires specialized components that few suppliers provide. The company's collaboration with NKT Photonics aims to procure next-generation laser systems for IonQ's trapped-ion quantum computers and networking equipment. Through this partnership, NKT Photonics will develop and deliver three prototype optical subsystems to IonQ in 2025 to support the commercialization of data-center-ready quantum computers. NKT Photonics' systems are based on fiber-laser technology. According to IonQ, these lasers provide an advantage in performance, cost, lead time and SWaP (size, weight and power). Additionally, they will be modular and rack-mountable.

IonQ also joined forces with Ansys to make simulation accessible to both quantum experts and non-experts, planning to rely on Ansys' multiphysics technology—which includes structural, optical, photonic and electromagnetic simulation software—to design and optimize key components for scalable quantum computers.

Several factors could impact IonQ's future success, including the inability of suppliers to deliver components on time, changes in government spending, and difficulties scaling system capacity or reducing errors. The dependence on specialized suppliers creates vulnerability, but the Oxford Ionics acquisition—with its semiconductor-compatible manufacturing—aims to shift toward standard foundry processes that would reduce supplier concentration.

3. Bargaining Power of Buyers: LOW-MODERATE

Currently, buyers exploring quantum computing have limited options. IonQ's cloud availability through AWS, Azure, and Google Cloud creates convenience that reduces switching incentives. Quantum Computing as a Service (QCaaS) lowers the entry barrier by offering access to costly quantum systems through the cloud, enabling organizations to test, develop, and deploy quantum applications without the need for substantial infrastructure investments.

The banking & finance segment is likely to be the major end-user industry in the quantum computing market. In banking and finance, the drive for quantum computing stems from its ability to optimize portfolios, enhance risk analysis, accelerate simulations, and improve fraud detection. A major driver of the quantum computing market is the rising demand for high-performance computing to solve complex problems in drug discovery, financial modeling, and logistics optimization, where classical systems are limited.

On the application front, IonQ demonstrated a 20x acceleration in drug discovery workflows with AstraZeneca, AWS and NVIDIA. IonQ's current systems, including IonQ Forte and IonQ Forte Enterprise, have already delivered 20x performance improvements for customers like Amazon Web Services, AstraZeneca, and NVIDIA.

Government customers—increasingly important to IonQ's revenue mix—have significant bargaining power but also provide multi-year contracts that create revenue visibility. The company's strength in U.S. defense and networking projects includes four approximately $100 million U.S. Air Force Research Lab contracts in 2022, 2023, 2024, and 2025.

4. Threat of Substitutes: LOW (Near-Term), HIGH (Long-Term)

No classical computing substitute exists for the problems quantum computers are designed to solve. The phase from 2025 to 2030 will be characterized by accelerating quantum cloud service adoption democratizing access beyond specialized research institutions, error correction breakthroughs enabling longer coherence times and reliable computation, and enterprise pilot programs validating quantum advantage across specific use cases including portfolio optimization, logistics planning, and molecular simulation.

However, the timeline for quantum advantage remains uncertain. If classical computing advances—including AI-enhanced optimization—continue outpacing quantum progress, the perceived value proposition weakens. The broader substitution threat is that quantum computing never achieves broad commercial relevance, remaining a niche technology for specialized applications.

5. Competitive Rivalry: INTENSE

Major vendors in the quantum computing market include IBM (US), D-Wave Quantum Inc. (Canada), Microsoft (US), Amazon Web Services (US), Rigetti Computing (US), Fujitsu (Japan), Hitachi (Japan), Toshiba (Japan), Google (US), Intel (US), and Quantinuum (US).

The US quantum computing market is witnessing strong growth, driven by significant government funding and private sector investments. Leading technology giants such as IBM, Google, Microsoft, and Amazon are pioneering advancements in hardware, software, and cloud-based services. The country benefits from a strong research ecosystem supported by universities, defense agencies, and national labs. Increasing adoption across industries like finance, healthcare, aerospace, and defense is further accelerating demand. Overall, the US remains the global leader, shaping innovation and commercialization in the quantum computing space.

The competitive intensity creates pressure from multiple directions. Big Tech competitors have effectively unlimited resources and can pursue quantum computing as a strategic option rather than an existential bet. Meanwhile, pure-play competitors like Quantinuum (with its $10 billion valuation) and Rigetti compete for the same customers and talent.

XI. Future Outlook: The Race to Quantum Advantage

The 2025-2030 Strategic Window

The next five years represent a critical window for IonQ. The quantum computing market is projected to reach USD 20.20 billion by 2030 from USD 3.52 billion in 2025, at a CAGR of 41.8%. Rising demand for high-performance computing in industries such as healthcare and pharma, banking & finance, for complex optimization and simulation is projected to drive the market.

IonQ's roadmap positions the company to capture this growth. The company projects approximately 20,000 physical qubits by 2028 and 2 million physical qubits by 2030, translating to roughly 1,600 error-corrected logical qubits by 2028 and 40,000-80,000 logical qubits by 2030.

Recent Strategic Developments

The pace of IonQ's strategic expansion continues accelerating. In November 2025, IonQ announced a definitive agreement to acquire Skyloom Global, a U.S.-based provider of high-performance optical communications infrastructure. The acquisition is intended to accelerate IonQ's full-stack quantum-secure communications and distributed quantum entanglement capabilities by integrating Skyloom's Optical Communications Terminals (OCTs), which are expected to boost data throughput by up to 500%.

In leadership updates, IonQ appointed Mihir Bhaskar as SVP of Global R&D and General John W. "Jay" Raymond ("Father of the Space Force") to its Board. The addition of General Raymond—a four-star general who served as the first Chief of Space Operations—signals IonQ's focus on defense and space applications.

On November 10, 2025, the University of Chicago announced a partnership with IonQ on a groundbreaking initiative that will advance research and discovery in quantum science and engineering, helping develop technologies with the potential to improve lives. The collaboration further establishes UChicago as a global leader in quantum science and engineering—and Chicago and Illinois as a growing hub for cutting-edge quantum research and industry. The initiative will support faculty, postdoctoral and student researchers in fundamental quantum science at the UChicago Pritzker School of Molecular Engineering and establish a sponsored research program between UChicago and IonQ.

In recognition of the agreement, the building planned at 56th Street and Ellis Avenue will be named the IonQ Center for Engineering and Science. This collaboration will deploy the first production-grade quantum computer and entanglement distribution quantum network on a university campus, which is intended to fuel IonQ's product roadmap and position the company as a core partner of the Chicago Quantum Exchange.

IonQ also announced a new investment and strategic partnership with Heven AeroTech, a developer of advanced hydrogen-powered Unmanned Aerial System solutions for defense and aerospace missions. The agreement will enable Heven AeroTech to integrate IonQ's quantum computing, quantum networking, quantum sensing, and quantum security technologies into its autonomous aerial systems, helping redefine mission resilience, stealth, and operational performance in GPS-denied environments.

Classiq secured a strategic funding up-round of tens of millions of dollars, bringing its cumulative funding to over $200 million. The round included major strategic investors AMD Ventures, Qualcomm Ventures, and IonQ, signaling a focus on heterogeneous computing and accelerating Classiq's global go-to-market presence for its optimized quantum circuit synthesis technology.

The Defense and Government Opportunity

IonQ's defense partnerships continue expanding, extending the company's strength with its four approximately $100 million U.S. Air Force Research Lab contracts in 2022, 2023, 2024, and 2025. The systems deployed via these contracts will help drive scalable and secure quantum computers and networks in the U.S. and around the world.

IonQ was selected by the Defense Advanced Research Projects Agency (DARPA) to participate in Stage B of the Quantum Benchmarking Initiative, joining ten other leading companies in the quantum computing industry. This selection follows IonQ's successful completion of Stage A, which required participants to outline a path to developing utility-scale quantum computers.

The Vector Atomic acquisition strengthens IonQ's position in defense applications. Quantum sensors for positioning, navigation, and timing have immediate military applications—providing GPS-independent navigation capabilities that are resistant to jamming and spoofing.

Industry Recognition

The company's innovative technology and rapid growth were recognized in Fortune Future 50, Newsweek's 2025 Excellence Index 1000, and Forbes' 2025 Most Successful Mid-Cap Companies list. IonQ is the only quantum company on the 2025 Deloitte Technology Fast 500™, a ranking of the 500 fastest-growing technology, media, telecommunications, life sciences, fintech, and energy tech companies in North America.

XII. Investment Considerations: The Quantum Calculus

What Investors Must Understand

IonQ represents a unique asset class: a publicly traded company making a fundamental bet on physics that most investors cannot independently evaluate. The technical claims—99.99% gate fidelity, #AQ scores, roadmaps to millions of qubits—require accepting management's representations or trusting third-party validation.

Despite its rapid pace of innovation, clear roadmap in quantum technologies and solid capital base, IonQ carries a Zacks Rank #3 (Hold) because the company is still in a high-investment phase with substantial cash burn and limited near-term profitability. While recent acquisitions, partnerships and technology milestones strengthen its long-term outlook, the path to sustained earnings remains uncertain.

The financial profile presents stark contrasts. Revenue growth has been exceptional—from $22 million in 2023 to $43 million in 2024 to over $100 million expected in 2025. Yet losses remain substantial, with the Q3 2025 net loss reaching $1.1 billion (including non-cash charges). The $3.5 billion cash position provides substantial runway, but investors must decide whether the opportunity justifies the premium valuation.

Valuation Context

IonQ's forward 12-month price/sales ratio of approximately 90x is far above the industry average. However, the stock remained undervalued compared to D-Wave's P/S of 160x and Rigetti's P/S of 286.5x.

Relative valuation within the quantum computing sector provides some comfort—IonQ trades at a discount to smaller competitors with less mature technology. But the absolute valuation remains extreme by traditional metrics. Investors must believe in both the quantum computing opportunity and IonQ's ability to capture it.

The Information Asymmetry Problem

Quantum computing creates a fundamental information asymmetry. Most investors—including most institutional investors—lack the physics background to independently evaluate technical claims. This creates reliance on:

- Management credibility: De Masi's physics background and capital markets track record provide some assurance

- Customer validation: Enterprise customers like Goldman Sachs, AstraZeneca, and government agencies provide signal that the technology works

- Third-party benchmarks: DARPA selection and technical publications provide external validation

- Competitive positioning: The fact that sophisticated competitors like Quantinuum and Google pursue similar approaches validates the trapped-ion thesis

Several factors could impact IonQ's future success. These risks include the inability of suppliers to deliver components on time, changes in government spending, and difficulties scaling system capacity or reducing errors. The company acknowledges these uncertainties and provides cautionary statements regarding forward-looking projections, emphasizing that actual results may differ materially from expectations, highlighting inherent risks associated with rapid technological development.

XIII. Conclusion: The Quantum Bet Evaluated

The IonQ story encapsulates the fundamental tension in emerging technology investment: visionary potential versus execution risk, scientific promise versus commercial reality.

What began in David Wineland's laboratory in Boulder—the painstaking manipulation of individual atoms with lasers—has evolved into a multi-billion-dollar enterprise spanning quantum computing, networking, and sensing. The scientific pedigree is unimpeachable: Nobel Prize physics, 25 years of academic research, and a technical roadmap validated by some of the world's most sophisticated customers.

The 2025 transformation—from quantum computing startup to integrated quantum platform company—represents a strategic bet that mirrors how the great technology platforms emerged. The acquisition spree assembled complementary capabilities; the question now is whether execution can match ambition.

Three scenarios capture the range of outcomes:

Scenario 1: Quantum Platform Leader The trapped-ion approach proves optimal for fault-tolerant quantum computing. IonQ's integrated platform—spanning computing, networking, and sensing—creates sustainable competitive advantages. The acquisitions integrate successfully, the roadmap to millions of qubits materializes, and IonQ becomes the defining company of the quantum era. Current valuations prove justified; the company generates substantial returns for long-term shareholders.

Scenario 2: Niche Player Quantum computing develops more slowly than projected, or alternative approaches prove superior. IonQ maintains a viable business in government and specialized enterprise applications but never achieves the scale required to justify current valuations. The company survives but disappoints relative to expectations. Shareholders see modest returns or losses depending on entry point.

Scenario 3: Technology Disruption A competing technology—perhaps photonic qubits, neutral atoms, or an approach not yet commercialized—renders trapped ions obsolete. IonQ's technology investments become stranded assets. The aggressive acquisition strategy leaves the company overextended. Shareholders experience significant losses.

The probability-weighted expected value depends on assumptions that reasonable people can disagree about. What's certain is that IonQ has positioned itself as the primary vehicle for investors seeking exposure to quantum computing's transformative potential.

For those with conviction in quantum computing's future and patience to weather volatility, IonQ offers something rare: direct ownership of a company attempting to define a new computing paradigm. For those requiring near-term profitability and proven business models, the risks remain substantial.

The physics works. The question is whether the business does.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube