Houlihan Lokey: The Middle Market M&A Powerhouse That Thrives in Crisis

I. Introduction: The Investment Bank Nobody Knows—And Everybody Needs

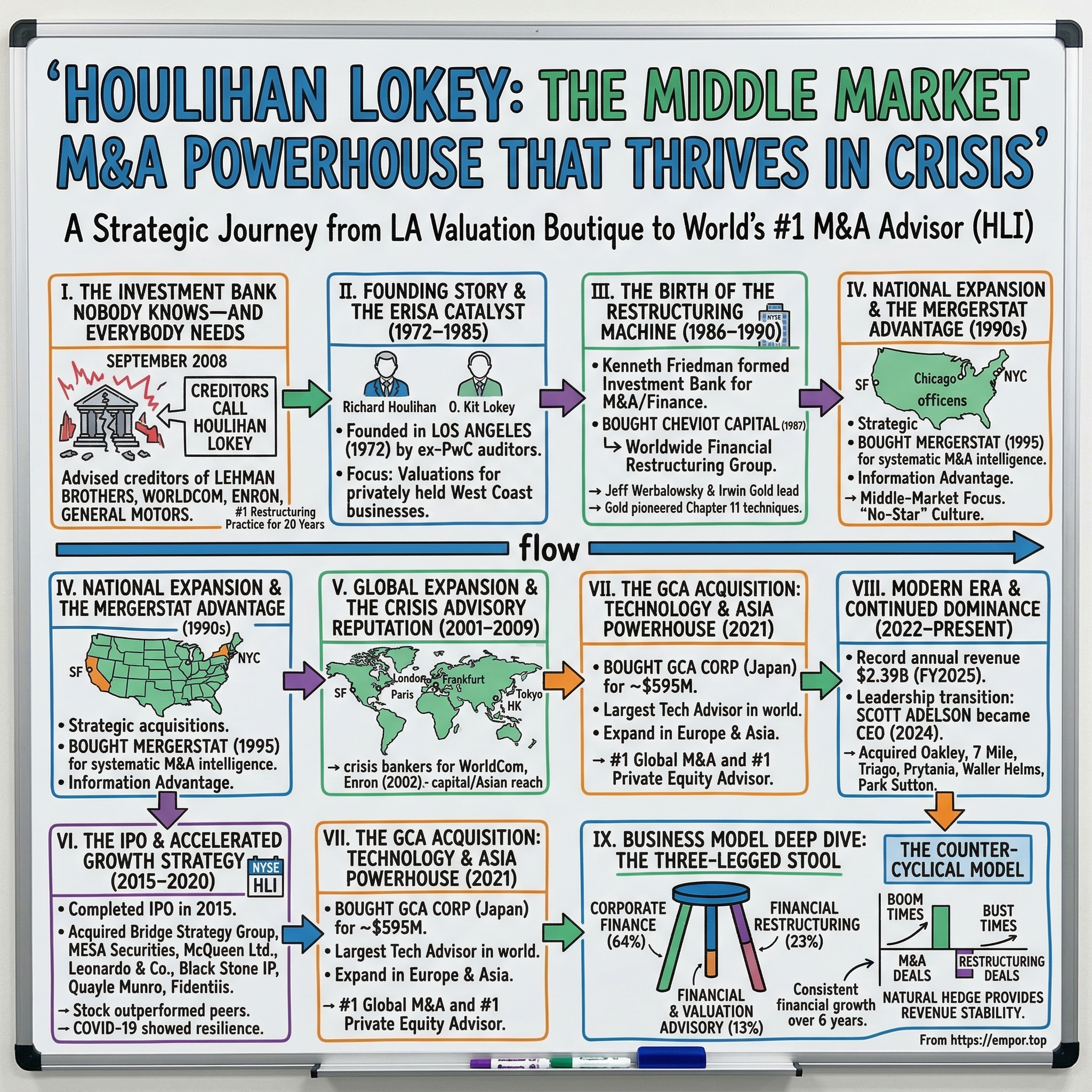

Picture the chaos of September 2008. Lehman Brothers—the fourth-largest investment bank in America—had just collapsed in the largest bankruptcy filing in U.S. history, with more than $600 billion in assets suddenly underwater. Wall Street's titans were reeling, the global financial system was in freefall, and creditors were scrambling to salvage what they could from the wreckage. In that moment of maximum financial terror, the firm these creditors called wasn't Goldman Sachs. It wasn't JPMorgan. It was Houlihan Lokey—a Los Angeles-based boutique that most retail investors had never heard of.

In 2008, Houlihan Lokey advised the creditors of Lehman Brothers. This wasn't a lucky break—it was the culmination of two decades building what would become the most formidable restructuring practice in global finance. Its Restructuring practice has been #1 for the past 20 years, having advised on 12 of the 15 largest bankruptcies, including Lehman Brothers and General Motors.

Today, as of 2024, Houlihan Lokey is the top investment bank for global M&A transactions, the top M&A advisor for the past 10 years in the U.S., the top global restructuring advisor for the past 11 years, and the top global M&A fairness opinion advisor over the past 25 years. In 2024, the 53-year-old, Los Angeles-based institution's 514 such transactions outpaced all rivals, including No. 2 Rothschilds, No. 3 Goldman Sachs, No. 4 JP Morgan and No. 5 Morgan Stanley.

This is the story of how two PricewaterhouseCoopers refugees built a counter-cyclical advisory empire by doing exactly what the bulge bracket banks didn't want to do: serving the middle market, building deep restructuring expertise, and creating a culture that prizes teamwork over individual stardom. It's a masterclass in strategic counter-positioning, patient capital allocation, and the power of thriving when others merely survive.

II. Founding Story & The ERISA Catalyst (1972–1985): Building the Valuation Foundation

The year was 1972. Richard Nixon was in the White House, the Dow Jones Industrial Average sat below 1,000 points, and two auditors at Price Waterhouse in Los Angeles had an idea. Houlihan Lokey, previously known as Houlihan Lokey Howard & Zukin, was co-founded in Los Angeles in 1972 by Richard Houlihan and O. Kit Lokey, both of whom left PricewaterhouseCoopers to start the company.

The firm they created wasn't particularly remarkable at first glance—just another advisory boutique serving privately held businesses on the West Coast. The firm's early operations centered on the West Coast, serving clients in sectors such as manufacturing, real estate, and entertainment, leveraging the region's economic landscape.

Two years later, something happened in Washington that would transform this modest consulting practice into a valuation powerhouse. The 1974 passage of the Employee Retirement Income Security Act launched the firm's valuation business by creating demand for independent valuations of private businesses, particularly those that had formed employee stock ownership programs.

ERISA was one of those regulatory changes that created an entirely new category of professional services. Suddenly, pension plans needed annual valuations. ESOPs required independent assessments. And few firms were positioned to provide the rigorous, defensible business valuations that the new law demanded. This shift positioned the firm as a specialist in financial advisory services, particularly for institutional investors and pension funds, establishing a foundation for its valuation expertise amid growing demand for compliance-driven assessments.

The founding team expanded to match the opportunity. Co-founders Robert "Bob" F. Howard joined the company in 1974, followed by James H. Zukin in 1976—hence the firm's original moniker, "Houlihan Lokey Howard & Zukin."

Through the late 1970s and early 1980s, as the leveraged buyout boom transformed Wall Street, Wall Street's large investment banking firms began calling on Houlihan Lokey for independent valuation expertise in fairness, solvency, and employee stock ownership plan (ESOP) opinions. The firm advised on transactions valued at more than $100 billion during this period.

What made Houlihan Lokey different from the bulge bracket banks? Early on, the firm carved a niche by focusing intensely on middle-market M&A, restructuring, and valuation advisory, areas often underserved by bulge-bracket banks. This strategic focus built a strong reputation and deal flow.

The Los Angeles location—thousands of miles from Wall Street—proved to be a strategic asset rather than a handicap. The West Coast gave Houlihan Lokey proximity to the entertainment, real estate, and manufacturing sectors that were driving California's economy. It also meant the firm developed a distinct culture, one that emphasized analytical rigor and team-based collaboration rather than the star-banker model that dominated New York.

By the mid-1980s, Houlihan Lokey had established itself as the go-to firm for ESOP valuations and fairness opinions in the middle market. But the next chapter of its history would require something more: the vision to see that booming deal markets inevitably create the seeds of future distress.

III. The Birth of the Restructuring Machine (1986–1990): Building the Counter-Cyclical Engine

If the ERISA boom gave Houlihan Lokey its foundation, the leveraged buyout frenzy of the 1980s gave it the opportunity to build something truly distinctive: a world-class restructuring practice that would become its competitive moat for decades to come.

In 1986, Kenneth Friedman founded and became President of Houlihan Lokey's investment banking broker dealer to provide M&A advisory services and to raise debt and equity financing. Friedman formed the investment bank to provide Wall Street level expertise to the expanding investment banking demands of Houlihan Lokey's clients and other middle market companies.

This wasn't just about adding another service line. Friedman's investment bank represented a fundamental expansion of Houlihan Lokey's ambitions—from valuation specialist to full-service middle-market investment bank. But the truly prescient move came the following year.

By 1987, many of the highly leveraged transactions completed earlier in the decade were starting to exhibit signs of financial distress. Accordingly, a market was developing for financial restructuring advisory services. To position itself to serve this market, the investment banking broker-dealer purchased Cheviot Capital Corporation in 1987 and, led by Jeff Werbalowsky and Irwin Gold, began assembling what would become an active, dominant, worldwide financial restructuring group.

Think about the timing: 1987. The same year Black Monday wiped out 22% of the stock market in a single day. While other firms were reeling from the crash, Houlihan Lokey was investing in capability that would pay off precisely when others were suffering. This is counter-positioning in its purest form—building strength in an area that competitors view as unattractive during good times but becomes essential during bad times.

Irwin Gold, who would later become Executive Chairman, was one of the key architects of this restructuring engine. In 1988, Gold co-founded the Financial Restructuring Group of Houlihan Lokey and is today considered a leading expert in corporate debt restructuring. In the past 30 years, Gold has redefined the role of investment bankers in financially distressed transactions and pioneered the use of now common restructuring and liability management techniques, such as pre-arranged and pre-packaged Chapter 11 cases, larger-scale 363 asset sales and creative exchange offer structures.

Gold's background is instructive: In Gold's early career, he spent three years as a lawyer with Gibson, Dunn & Crutcher in its corporate department. In 1985, Gold became a senior officer of Woods Bros. Homes, Inc., a Denver-based real estate company, where he led the workout and sale of the company. Gold was a Principal of the Seneca Group from 1986 until he joined Houlihan Lokey in 1988.

This combination—legal training, hands-on workout experience, and investment banking acumen—became the template for the restructuring practice. And the strategic insight was profound: while other banks chased boom-time deals, Houlihan Lokey invested in capability that would pay off during downturns. Houlihan Lokey established itself as a global leader in financial restructuring advisory, advising on some of the largest and most complex bankruptcies and reorganizations worldwide. This counter-cyclical business provides stability.

The beauty of this model became apparent in the early 1990s, as the S&L crisis and early-decade recession sent waves of highly leveraged companies into distress. Houlihan Lokey's restructuring team was ready, and they were learning with every engagement—building the institutional knowledge and creditor relationships that would prove invaluable in future crises.

IV. National Expansion & Building the Playbook (1990s): The Mergerstat Advantage

With a valuation foundation and restructuring capability in place, Houlihan Lokey turned its attention in the 1990s to geographic expansion and information advantage. The firm's growth during this period reveals a sophisticated understanding of how data and relationships create sustainable competitive advantages in advisory businesses.

Houlihan Lokey opened eight offices across the U.S. in the 1980s and 1990s as it expanded. In addition, the firm opened several offices in the 1980s in New York City, San Francisco, and Chicago.

But the most strategically significant move of the decade was an acquisition that most observers might have overlooked. In 1995, to grow its information services division, Houlihan Lokey acquired Mergerstat, a publishing company with a 30-year history in analytical M&A research, from Merrill Lynch.

Why would a middle-market investment bank buy a data publishing company? Because Mergerstat gave Houlihan Lokey something invaluable: systematic intelligence on deal multiples, transaction structures, and market trends before anyone else had access to them. In an era before Bloomberg terminals democratized financial data, this was a genuine information advantage.

The Mergerstat acquisition exemplifies a principle that would guide Houlihan Lokey's growth for decades: strategic acquisitions that deepen capabilities rather than simply adding scale. The firm wasn't trying to become a bulge bracket bank—it was trying to become the best possible version of a middle-market specialist.

During this period, Houlihan Lokey also refined what would become its signature cultural attribute: the "no-star" approach to team building. Unlike the rainmaker model prevalent at many investment banks—where a few senior bankers controlled relationships and received outsized compensation—Houlihan Lokey emphasized collaboration and institutional client relationships. This meant clients belonged to the firm, not to individual bankers, reducing the risk of defections and creating more stable revenue streams.

The middle-market focus also proved strategically astute. Companies valued between $250 million and a few billion dollars represent a vast and underserved market. They're too small to attract sustained attention from Goldman Sachs or Morgan Stanley, but complex enough to require sophisticated advisory services. This created a natural market position that was both defensible and scalable.

By the end of the 1990s, Houlihan Lokey had built the playbook it would execute for the next two decades: deep industry expertise, counter-cyclical restructuring capability, data-driven advisory, team-based culture, and unwavering middle-market focus. The question was whether this playbook could translate from national to global scale.

V. Global Expansion & The Crisis Advisory Reputation (2001–2009): From Regional Player to Global Leader

The new millennium brought both international expansion and the defining assignments that would cement Houlihan Lokey's reputation as the crisis banker of choice.

In 2001, Houlihan Lokey launched its first non-U.S. office by expanding into London. It also expanded its industry group platform and private equity coverage program in keeping with investment banking trends.

The timing of the London expansion proved fortuitous—and not because of deal activity in Europe. In 2002, Houlihan Lokey advised the official creditors committees in three large bankruptcies: WorldCom, Enron, and Conseco.

Consider what this meant for the firm's reputation. These weren't just large bankruptcies—they were epoch-defining scandals that reshaped American corporate governance. WorldCom's accounting fraud represented the largest in U.S. history at the time. Enron's collapse redefined how investors thought about off-balance-sheet risk. And Houlihan Lokey was there, representing creditors, navigating through complexity, and building relationships with the distressed debt investors who would become key clients for decades.

One major restructuring deals Gold was involved in was WorldCom in 2002. With a debt of $40 billion, it was the largest Chapter 11 filing in US history. By 2004, the company emerged from bankruptcy under the name MCI.

The European expansion continued: In 2005, the firm opened a Paris office. In 2006, the firm opened a Frankfurt office.

But the most significant development of 2006 wasn't a new office—it was a transaction that would fundamentally alter Houlihan Lokey's capital structure and global ambitions. Also in 2006, Houlihan Lokey agreed to merge with Orix USA, the U.S. corporate lending operations of ORIX Corp. of Japan, to address the growing international demand for middle-market investment banking services. In 2007, Houlihan Lokey expanded into Asia, opening offices in Hong Kong and Tokyo.

Los Angeles-based investment banking firm Houlihan Lokey Howard & Zukin has agreed to be acquired by Tokyo-based Orix Corp. for $500 million in cash and stock. Under the terms of the pact, Houlihan and Orix's U.S. arm will combine their operations into a company with $2.5 billion in assets that will keep the Houlihan name. Orix's U.S. arm will hold 70 percent of the new company, while Houlihan's partners will own the remaining 30 percent.

This wasn't an outright sale—it was a strategic partnership that gave Houlihan Lokey access to Asian markets and deep pockets for expansion while allowing the firm to maintain its culture and independence. ORIX, a Japanese financial services conglomerate, was looking for advisory capabilities; Houlihan Lokey was looking for capital and geographic reach. The marriage made sense.

Then came 2008, and with it, the assignment that would define Houlihan Lokey's generation.

When Lehman Brothers collapsed on September 15, 2008—in what remains the largest bankruptcy filing in U.S. history—Houlihan Lokey advised the creditors of Lehman Brothers. The firm was suddenly at the center of the most consequential financial event since the Great Depression.

The company got the job for 12 out of the 15 largest bankruptcies from 2000 to 2018 (including Lehman Brothers, Worldcom, Enron, and General Motors).

The 2008 financial crisis validated everything Houlihan Lokey had built over the previous two decades. The company's expertise in financial restructuring has made it a go-to advisor during periods of economic stress, including the 2008 financial crisis and the COVID-19 pandemic.

Today, Houlihan Lokey's financial-restructuring practice is the largest of any investment banking firm in the world. Since 1988 it has advised on more than 1,800 restructuring transactions and helped resolve aggregate debt claims of more than $3.8 trillion.

The counter-cyclical model worked exactly as designed: while other banks saw deal flow collapse during the crisis, Houlihan Lokey's restructuring practice surged. Revenue stability during the worst financial crisis in modern history built institutional investor confidence and positioned the firm for the next phase of its evolution.

VI. The IPO & Accelerated Growth Strategy (2015–2020): Going Public and Fueling the Acquisition Engine

By 2015, Houlihan Lokey had grown into a global force, but remained largely unknown to public investors. The IPO would change that—and provide the currency for an aggressive acquisition strategy.

On August 13, 2015, Houlihan Lokey completed its initial public offering, beginning trading as HLI on the NYSE.

The IPO, which served as a payout for current investors, generated $220.5 million in proceeds, or at least 30 percent less than the price originally marketed. The smaller deal helped Houlihan shares get a boost on their first day of trading, and they climbed 6.7 percent to $22.40 in New York.

As for the IPO itself, it won't bring any funds directly into the company. This is because it's essentially a cash-out by the majority shareholder, Japanese conglomerate Orix. The Asian firm bought a 70% stake in 2006 for a mix of cash and stock worth roughly $500 million.

What did the IPO buy? Strategic flexibility. With a public currency and access to capital markets, Houlihan Lokey could pursue acquisitions more aggressively. And pursue them it did.

In 2015, Houlihan Lokey acquired management consulting firm Bridge Strategy Group, digital media and entertainment focused investment bank MESA Securities, London-based consumer-focused firm McQueen Ltd., and operations of the Continental European investment bank Leonardo & Co.

The acquisition spree continued: In January 2017, Houlihan Lokey acquired Black Stone IP, a leader in Tech+IP advisory work. In January 2018, Houlihan Lokey acquired Quayle Munro Limited, an independent advisory firm focused on providing corporate finance advisory services to companies in the data & analytics sector.

In November 2019, Houlihan Lokey acquired Fidentiis Capital, growing Houlihan Lokey's Corporate Finance business in Europe.

Each acquisition followed a consistent pattern: relatively small deals that added specific industry expertise or geographic presence without diluting culture. Houlihan Lokey wasn't trying to transform itself through mega-mergers—it was layering capabilities onto its existing platform.

The stock performance validated the strategy. Houlihan Lokey has seen its stock outperform fellow investment banks since going public in 2015. Since its first day of trading, this undiscovered investment bank has delivered investors gains of more than 300%, crushing its peers as well as the broader market, which has gained more than 120% during the same period.

Then came COVID-19, and once again, the counter-cyclical model proved its worth. Houlihan Lokey says that its business mix gives it resiliency with both cyclical and countercyclical businesses. Last year was a good example of this. In spring 2020, the global pandemic wreaked havoc on the business environment and threw the economy into a tailspin. Financial restructuring activity saw a big increase in activity in the face of much uncertainty, and Houlihan Lokey benefited. During this same period, M&A activity fell. Then, in the fall, the trends shifted. Restructuring activity was on the decline, but M&A activity saw a pickup. As a result, the company posted solid results for its fiscal 2021.

VII. The GCA Acquisition: Becoming a Technology & Asia Powerhouse (2021)

If the previous acquisitions were about adding capability incrementally, the GCA deal was about transformation. Houlihan Lokey Inc. agreed to buy Japanese rival GCA Corp. for about 65 billion yen ($595 million), amid a growing wave of consolidation between boutique banks eager to compete with larger Wall Street rivals.

"The acquisition of GCA will create one of the largest technology advisors in the world, one that more closely matches the size and importance of this sector in today's global economy. In addition, this combination would significantly expand our presence in Europe and Asia and establish Houlihan Lokey as one of the most geographically diversified investment banking firms among our peer group," said Scott Beiser, CEO of Houlihan Lokey.

Houlihan Lokey, Inc., the global investment bank, has acquired GCA Corporation following the successful completion of a tender offer process resulting in the firm acquiring approximately 90% of GCA's common stock. With effect from today, GCA becomes part of Houlihan Lokey. More than 500 talented individuals across 24 locations join the firm, creating one of the largest and most experienced technology advisory firms globally, and significantly expanding the firm's presence in Asia and in Europe.

The strategic rationale was compelling. Technology had become the dominant driver of M&A activity globally, and GCA had built precisely the technology-focused advisory practice that Houlihan Lokey lacked. The deal also addressed geographic gaps: GCA was strong in Japan and had meaningful European presence, complementing Houlihan Lokey's Americas-heavy footprint.

"GCA has proved itself to be a leader in its field, led by an extraordinarily impressive management team. We share a similar business philosophy and a belief in the importance of a strong, client-centric corporate culture. This complementarity is paramount to effectively integrating the two firms, enhancing the services we offer our clients, and maintaining our continued success," said Scott Adelson, Co-President of Houlihan Lokey.

Following this integration, Houlihan Lokey is now: The most active technology M&A advisor in the world, with a Technology Group consisting of 225 financial professionals across a global network of now 38 offices around the globe. The No. 1 most active global M&A advisor. The No. 1 most active advisor to private equity globally. "Today is a momentous day for the firm, as we are now able to work seamlessly with our new partners across regions, products, and sectors to establish the most client-focused, independent advisory firm in the investment banking arena. Houlihan Lokey is now the most active technology advisor in the world as well as a global leader in industrials; business services; consumer, food, and retail; healthcare; and financial services M&A," said Scott Adelson, Co-President of Houlihan Lokey.

VIII. Modern Era & Continued Dominance (2022–Present): Record Results and New Leadership

The post-GCA era has been marked by record financial performance and a leadership transition. Houlihan Lokey annual revenue for 2025 was $2.389B, a 24.81% increase from 2024.

For the fiscal year, revenues were $2.39 billion, compared with $1.91 billion for the fiscal year ended March 31, 2024. Net income was $400 million, or $5.82 per diluted share, for the fiscal year ended March 31, 2025, compared with $280 million, or $4.11 per diluted share, for the fiscal year ended March 31, 2024. Adjusted net income for the fiscal year ended March 31, 2025 was $434 million, or $6.29 per diluted share, compared with $310 million, or $4.49 per diluted share, for the fiscal year ended March 31, 2024.

The company has consistently grown its managing director headcount with a CAGR of 9% over the last 20 years, increasing from 65 MDs in 2005 to 339 in 2025. At the same time, revenue per MD has remained strong, reaching $7.0 million in FY2025.

The acquisition strategy continued unabated: In February 2023, Houlihan Lokey acquired Oakley Advisory. In December 2023, Houlihan Lokey acquired 7 Mile Advisors, increasing the firm's IT services capabilities and expanding its Business Services Group. In May 2024, Houlihan Lokey acquired Triago, expanding the firm's Capital Solutions Group and its private capital advisory and private placement capabilities. In October 2024, Houlihan Lokey acquired Prytania Solutions Ltd. (PSL). This acquisition strengthened Houlihan Lokey's Financial and Valuation Advisory business and expanded its presence in Europe. In December 2024, Houlihan Lokey acquired Waller Helms Advisors and Park Sutton Advisors.

In March 2024, Houlihan Lokey announced a significant leadership transition. Houlihan Lokey today announced that Scott Beiser will step down as Chief Executive Officer, a role he has held since 2003. Scott Adelson, Co-Head of Corporate Finance, will succeed Mr. Beiser as Chief Executive Officer.

"Leading Houlihan Lokey for the past two decades, and working alongside my talented and dedicated partners, has been one of the most gratifying experiences of my career," said Mr. Beiser. "I am extraordinarily proud of the firm we have built, from a small valuation firm to one of the largest and most successful independent investment banks in financial services. I'm delighted to hand the reins to my longtime partner Scott, who has been instrumental in the firm's overall success and has built the firm's Corporate Finance business into the market leader it is today."

Scott Adelson (born 1960) is an American business executive who has served as the chief executive officer (CEO) of Houlihan Lokey since June 2024. Prior to this role, he served as co-president and global co-head of corporate finance. Adelson joined Houlihan Lokey in 1987.

Adelson's background reflects the firm's collaborative culture: He earned his Bachelor of Science in Business and Entrepreneurship from the University of Southern California. After graduating in 1984, he continued his education at the University of Chicago Booth School of Business, where he obtained his Master of Business Administration in Finance and Marketing. Following his academic pursuits, Adelson joined Houlihan Lokey in 1987, where he has been a key contributor to the firm's growth and culture.

A graduate of the University of Southern California and University of Chicago Booth School of Business, Adelson, a nearly four-decade veteran of Houlihan Lokey, took over from long-time CEO Scott Beiser in March 2024. Adelson considers his appointment a signal to investors that Houlihan Lokey very much intends to stick to its core values and maintain a team that has driven growth and change at the company for years.

Today, the company ranks #1 in global M&A deals by number of transactions in 2024 with 415 deals, ahead of Rothschild & Co with 406 deals. Its 88 Global Distressed Debt & Bankruptcy Restructuring Deals in 2024 were nearly 50% greater than the next biggest competitor, PJT Partners with 59 deals.

IX. Business Model Deep Dive: The Three-Legged Stool

Houlihan Lokey's business model is structured around three complementary segments that provide both growth and stability through economic cycles.

The Three Business Segments:

Houlihan Lokey's business is diversified across three main segments: Corporate Finance (64% of revenue), Financial Restructuring (23%), and Financial and Valuation Advisory (13%). This diversification has helped the company maintain stability through market cycles.

Corporate Finance, the largest segment, has shown the highest growth rate with a 5-year revenue CAGR of 19%, while Financial Restructuring (9% CAGR) and Financial and Valuation Advisory (15% CAGR) have also contributed to the company's overall growth. The Financial Restructuring segment maintains the highest revenue per managing director at $9.5 million.

Geographic & Client Diversification:

The company's business is well-diversified across geography (Americas 71%, EMEA 23%, Asia 6%), client type (Financial Sponsors 53%, Private Non-Sponsor 28%, Public Companies 19%), and industry sectors.

The financial sponsor relationship is particularly significant. With more than half of revenue coming from private equity firms and other financial sponsors, Houlihan Lokey has built recurring relationships with repeat deal-makers who generate consistent transaction flow.

The Counter-Cyclical Model:

The genius of Houlihan Lokey's business model is that its segments move counter-cyclically. When M&A markets are booming, Corporate Finance thrives. When the economy contracts and companies become distressed, Financial Restructuring surges. This natural hedge has produced remarkable revenue stability:

Houlihan Lokey has demonstrated consistent financial growth over the past six years, with revenues increasing from $1.159 billion in 2020 to $2.389 billion in 2025.

Compensation Economics:

This resulted in an adjusted compensation ratio of 61.5% for both the second quarter ended September 30, 2024 and the second quarter ended September 30, 2023. This stable compensation ratio demonstrates disciplined expense management—the firm scales compensation with revenue rather than maintaining fixed costs that could pressure margins during downturns.

X. Porter's Five Forces Analysis: Where Does Houlihan Lokey's Competitive Advantage Come From?

1. Threat of New Entrants: LOW-MEDIUM

The barriers to entering middle-market investment banking are substantial. Houlihan Lokey, Inc. has made itself one of the world's most active and consistently profitable investment banks by focusing its M&A and finance businesses on the universe of mid-cap companies underserved by larger rivals. Building the reputation, relationships, and specialized expertise required to compete takes decades. The restructuring moat is particularly defensible—you can't simply hire a few senior bankers and declare yourself a restructuring expert. You need institutional knowledge built through hundreds of complex engagements.

2. Bargaining Power of Buyers (Clients): MEDIUM

Corporate clients can technically engage any investment bank, but switching costs during active transactions are high, and reputation matters enormously in advisory. Middle-market companies have fewer alternatives than large corporations, who might receive attention from bulge bracket banks. The firm's position as the #1 middle-market advisor by deal count suggests strong client preference.

3. Bargaining Power of Suppliers (Talent): HIGH

This is where Houlihan Lokey faces its greatest challenge. Investment banking talent is highly mobile, and managing directors can take client relationships with them. The firm addresses this through its team-based culture and by ensuring institutional (rather than individual) client relationships. Revenue per MD has remained strong, reaching $7.0 million in FY2025, suggesting the firm can afford competitive compensation while maintaining profitability.

4. Threat of Substitutes: LOW-MEDIUM

In-house corporate development teams are growing more sophisticated, and private equity firms sometimes run their own sale processes. However, complex restructurings require specialized external advice. "If you take a look at our restructuring business, for example, one of the great exports of the United States that nobody really talks about is complicated balance sheets," Adelson said. "As complicated balance sheets have worked their way around the world, some percentage of those ultimately wind up in restructurings."

5. Competitive Rivalry: HIGH

For larger transactions, Houlihan Lokey faces competition from major investment banks including Goldman Sachs Group, Morgan Stanley, and JPMorgan Chase. In the financial restructuring segment, Houlihan Lokey is considered one of the market leaders alongside firms such as Lazard and PJT Partners. The firm is the No. 1 global restructuring advisor, having made 106 deals in 2020. This puts it well ahead of its next two competitors, PJT Partners and Lazard, with 63 and 50 deals respectively.

XI. Hamilton's 7 Powers Framework Analysis: The Sources of Durable Advantage

1. Scale Economies: MODERATE

Pure scale economies are limited in advisory businesses—adding another deal doesn't reduce the cost of the previous one. However, scale in data and research (exemplified by the Mergerstat acquisition) provides information advantages. Global footprint enables cross-border deal sourcing that smaller competitors can't replicate.

2. Network Economies: STRONG

Adelson sees particularly good opportunities in Houlihan Lokey's restructuring business and the company can draw on decades of dealing with some of the most complicated restructurings in North American and international corporate history. Those include Enron, WorldCom and Lehman Bros. where it represented creditor groups.

Each restructuring engagement builds relationships with creditors who become clients in future deals. Financial sponsors (53% of clients) create recurring deal flow—when a PE firm completes a portfolio company transaction with Houlihan Lokey, that firm becomes a likely client for future deals.

3. Counter-Positioning: VERY STRONG — THE KEY POWER

This is Houlihan Lokey's most significant competitive advantage. "Obviously, the economy grows and contracts in cycles, but we focus on the mid-cap segment − companies worth between $250 million and about a few billion dollars − while most bulge bracket banks focus elsewhere.

The counter-positioning operates on two dimensions: - Market segment: Middle-market focus vs. bulge bracket large-cap focus - Cycle position: Restructuring expertise provides counter-cyclical revenue when M&A slows

Bulge bracket banks can't easily copy this strategy because their economics depend on large-cap transactions with higher per-deal fees. Goldman Sachs isn't going to staff up for $300 million M&A deals—the fee economics don't work for their cost structure.

4. Switching Costs: MODERATE-HIGH

Once engaged on a transaction, switching advisors mid-deal is extremely costly and disruptive. Multi-year relationships with financial sponsors create stickiness. Proprietary valuation methodologies and 25 years of fairness opinion track record create defensible positioning.

5. Cornered Resource: MODERATE

The firm's restructuring expertise—built through decades of handling the most complex bankruptcies in history—represents a form of cornered resource. Since 2000, we have advised on more than 1,000 restructuring transactions, including advising major parties-in-interest in 12 of the 15 largest corporate bankruptcies in the United States, such as the bankruptcies of Lehman Brothers, Worldcom, Enron, the CIT Group and General Motors.

6. Process Power: MODERATE

The team-based culture and institutional client relationship model represent process advantages that are difficult to replicate. Most investment banks organize around star rainmakers; Houlihan Lokey organizes around collaborative teams and firm-owned relationships.

7. Branding: STRONG in Restructuring, Growing in M&A

In restructuring, Houlihan Lokey's brand is unmatched—creditors committees call them first. In middle-market M&A, the brand has strengthened significantly with market share leadership, but brand awareness among retail investors remains limited (which arguably creates opportunity).

XII. Competitive Landscape: How Houlihan Lokey Stacks Up

The investment banking competitive landscape varies significantly by product and transaction size. Houlihan Lokey has delivered total shareholder returns of 26.4% a year over the past decade, beating such fellow boutiques as Lazard (5.9%), Jefferies (13.2%), Moelis (17.2%), and Evercore (22%), while also waxing big guys Citigroup (9.3%), Bank of America (14.5%), Goldman Sachs (18.0%), Morgan Stanley (19.9%), and J.P. Morgan (20.3%). Back in the fall of 2015, Houlihan's market cap trailed those of Jefferies, Lazard, and Evercore. Now at $13.6 billion, it's bigger than all three.

Against Bulge Bracket Banks:

The bulge bracket banks—Goldman Sachs, Morgan Stanley, JPMorgan—focus on mega-cap transactions where fees per deal are highest. Houlihan Lokey rarely competes head-to-head for $50 billion deals but dominates in the $250 million to $2 billion range where these firms are largely absent.

Against Elite Boutiques:

In restructuring and special situations advisory, PJT Partners is considered one of the leading firms alongside Houlihan Lokey, Lazard, and Evercore. The firm's restructuring practice has gained significant market share since its formation, particularly during periods of economic stress such as the COVID-19 pandemic.

However, Houlihan Lokey's 88 restructuring deals in 2024 compared to PJT's 59 demonstrates clear market leadership in the restructuring space.

Against Middle-Market Peers:

In the middle-market M&A space, the company competes directly with firms such as Jefferies Financial Group, Piper Sandler Companies, and William Blair. Houlihan Lokey's advantage here is the combination of M&A capability with restructuring expertise—a dual capability that most middle-market banks lack.

XIII. Key KPIs for Investors to Monitor

For investors tracking Houlihan Lokey, three metrics deserve particular attention:

1. Deal Count by Segment

The number of transactions closed in Corporate Finance, Financial Restructuring, and Financial & Valuation Advisory tells the story of market positioning and growth. Watch the mix: if restructuring surges while M&A declines, that's the counter-cyclical model working. If both grow together, that's even better.

2. Revenue per Managing Director

Revenue per MD has remained strong, reaching $7.0 million in FY2025. The Financial Restructuring segment maintains the highest revenue per managing director at $9.5 million.

This metric captures both productivity and pricing power. Declining revenue per MD could signal either talent issues or fee pressure. Sustained growth indicates the firm is adding productive capacity and maintaining pricing.

3. Compensation Ratio

This resulted in an adjusted compensation ratio of 61.5% for both the fiscal year ended March 31, 2025 and March 31, 2024.

Investment banking is a people business, and compensation is the largest expense. A stable ~61.5% ratio demonstrates disciplined expense management. Material increases could pressure profitability; significant decreases might signal under-investment in talent.

XIV. Bull Case vs. Bear Case

The Bull Case:

Houlihan Lokey has built a genuinely differentiated business model with multiple competitive moats:

- Restructuring dominance provides counter-cyclical revenue stability unmatched by peers

- Middle-market focus positions the firm in a segment with durable demand and limited competition from bulge brackets

- Acquisition playbook has proven ability to integrate tuck-in acquisitions that add capability without diluting culture

- Technology capability post-GCA acquisition positions the firm in the highest-growth M&A sector

- Management continuity with Adelson's nearly four decades at the firm ensures strategic consistency

With elevated interest rates and significant corporate debt maturities ahead, the restructuring business has tailwinds. Meanwhile, the M&A recovery from 2022-2023 lows provides growth opportunity in Corporate Finance.

The Bear Case:

Several risks warrant consideration:

- Talent concentration in a relationship-driven business creates key-person risk

- Premium valuation leaves little margin for error—the stock trades at elevated multiples relative to historical norms

- Cyclical exposure remains despite counter-cyclical offsets; a prolonged M&A drought could pressure growth

- Integration risk from aggressive acquisition pace could dilute culture or create operational complexity

- Compensation pressure in a tight labor market could squeeze margins

XV. Key Risks and Regulatory Considerations

Talent Retention and Competition:

Company insiders own 22.83% of the company's stock, which aligns management incentives but also concentrates decision-making. The investment banking industry remains highly competitive for talent, and star rainmakers at competitors continue to recruit Houlihan Lokey professionals.

Cyclical Revenue Exposure:

While the counter-cyclical restructuring business provides stability, Corporate Finance (64% of revenue) remains tied to M&A activity levels that can decline sharply in recessions. The firm navigated 2020 well, but future downturns may not coincide with restructuring surges.

Integration Execution:

The firm has made 19 acquisitions over the last 12 years to deepen industry coverage, expand geographic reach, and add service offerings. Each acquisition carries integration risk, and the cumulative complexity of managing a global platform has increased substantially.

Regulatory Environment:

Antitrust scrutiny of M&A transactions and potential changes to bankruptcy law could impact deal flow in both core segments. The firm's advisory-only model (no balance sheet lending or proprietary trading) reduces regulatory complexity compared to full-service banks.

XVI. Conclusion: A Different Kind of Wall Street Story

Houlihan Lokey's 53-year journey from Los Angeles valuation boutique to global M&A leader offers lessons that extend beyond investment banking. The firm succeeded not by trying to become Goldman Sachs, but by becoming the best version of something Goldman Sachs couldn't easily copy.

The strategic choices were consistent and patient: middle-market focus when everyone else chased mega-deals, restructuring investment when boom times made bankruptcy seem obsolete, team-based culture when star-driven models generated headlines, and disciplined acquisitions when empire-building was fashionable.

Today, the firm stands as the world's largest investment bank for midsize private companies. It's also been the top performer on Wall Street for rewarding investors over the past decade.

"Fiscal 2025 was a record year for our firm as all three groups ended the year with a strong fourth quarter. While current volatility makes meaningful forecasts difficult, we are well positioned to handle the uncertainty of current market conditions," stated Scott Adelson, Chief Executive Officer of Houlihan Lokey.

For investors, Houlihan Lokey represents a business with genuine competitive moats, counter-cyclical characteristics, and a management team with decades of experience executing a consistent strategy. The question, as always, is whether the price adequately reflects those advantages—and what happens when the next crisis inevitably arrives.

History suggests Houlihan Lokey will be ready. They always have been.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube