Hims & Hers Health: Disrupting Healthcare from Stigma to Scale

I. Introduction: The Unlikely Telehealth Giant

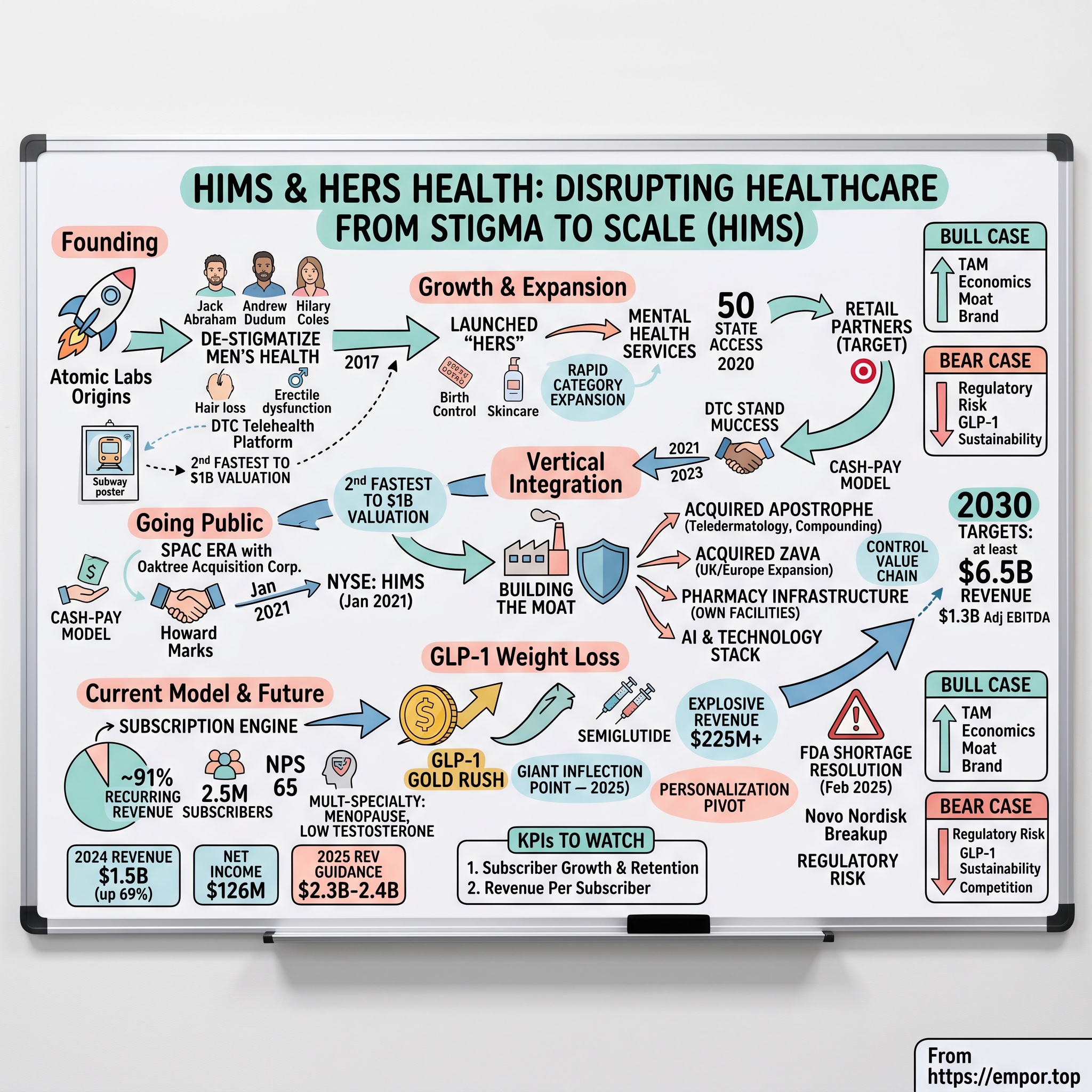

Picture New York City subway riders in late 2017, scrolling through their phones while surrounded by one of the cheekiest advertising campaigns the city had ever seen. Pastel-colored posters with playful phrasing asked men if they were ready to talk about hair loss, erectile dysfunction, and skin care—topics that most healthcare companies buried in sterile, clinical messaging. The ads came from an upstart called Hims, and they represented something far more ambitious than a marketing stunt. They were the opening salvo in a war to reinvent how Americans access healthcare.

Hims & Hers Health, Inc. is an American telehealth company established in 2017. The company provides prescription medications, over-the-counter medications, and personal care products, operating with a direct-to-consumer model. From those irreverent beginnings, the company has evolved into one of the most consequential players in digital healthcare—a $10+ billion enterprise that has fundamentally challenged how we think about the relationship between patients, providers, and pharmaceutical products.

The central question that animates this story: How did a startup selling erectile dysfunction pills become a telehealth juggernaut that challenges both Big Pharma and traditional healthcare? The answer lies in understanding a few intersecting forces: the power of de-stigmatization as a business model, the strategic value of vertical integration in healthcare, the GLP-1 weight loss gold rush, and the regulatory tightrope that defines the company's future.

Revenue of $1.5 billion, up 69% year-over-year in 2024. Net income of $126 million; Adjusted EBITDA of $177 million in 2024. The financial transformation has been staggering. For the full year 2024, the company achieved a revenue of $1.5 billion, up 69% from $872.0 million in 2023. Net income for the year was $126.0 million, a notable turnaround from a net loss of $(23.5) million in 2023.

Revenue of nearly $600 million, up 49% year-over-year in Q3 2025. Subscribers grew to almost 2.5 million, up 21% year-over-year in Q3 2025. The company has narrowed full year 2025 revenue guidance to $2.335 billion to $2.355 billion. By any measure, this represents one of the most remarkable growth trajectories in digital health history—a tenfold increase since going public.

But the Hims & Hers story is not simply a tale of growth metrics. It's a case study in how consumer brand-building, technological leverage, and regulatory arbitrage can combine to create a new category of healthcare company. And it's a story with significant unresolved questions about sustainability, regulatory risk, and the boundaries between innovation and exploitation. These themes—de-stigmatization as strategy, vertical integration as moat, the GLP-1 inflection point, and regulatory uncertainty—will guide our exploration of how Hims & Hers became what it is today, and what it might become tomorrow.

II. The Founders & Atomic Labs Origin Story

Andrew Dudum: From Classical Cellist to Healthcare Disruptor

Andrew Dudum is a Palestinian-American entrepreneur who is the founder and CEO of telehealth startup Hims & Hers Health, Inc. Dudum was born and raised in San Francisco, California. He is an American of Palestinian heritage. But his path to healthcare entrepreneurship was anything but linear.

He trained as a classical cellist and performed live across the United States and Europe, at hundreds of concerts and weddings, including at Carnegie Hall. He attended the Wharton School of the University of Pennsylvania, where he studied Management and Economics. Dudum did not finish his degree and is therefore a college dropout.

This blend of artistic sensibility and business acumen would prove crucial. The aesthetic dimension of Hims—the pastel packaging, the elevated visual identity, the willingness to make healthcare feel approachable—owes something to Dudum's background in performance and design thinking. He understood that healthcare's problems weren't purely medical; they were experiential and emotional.

Andrew Dudum was raised in a family of entrepreneurs—a background that has shaped his life from the start. Dudum grew up in a family of entrepreneurs which proved to have a strong impact on his ambitions and career. This entrepreneurial DNA, combined with his early exposure to technology, set him on a trajectory toward founding companies rather than joining them.

While in college, Dudum co-founded LendforPeace, a nonprofit microlending site for Middle Eastern entrepreneurs. He later worked at TokBox, a video-chat startup that was eventually acquired. The acquisition of TokBox freed Dudum up to pursue his goal to build a startup.

The Atomic Labs Venture Studio Model

In 2013, Dudum co-founded Atomic Labs, a San Francisco-based startup studio backed by investors such as Peter Thiel and Marc Andreessen. This wasn't just another venture fund—it was an entirely different model of company creation.

Atomic (also known as Atomic Labs, Atomic VC) is a startup studio and venture capital fund started by Jack Abraham in 2012. Atomic follows a studio fund model, a novel investing structure reportedly invented by Abraham. The studio fund model differs from traditional investment because the investor serves as a co-founder to hired "founders in residence" who develop business ideas. In addition to monetary support, the firm performs operational functions like accounting and legal via internal specialists.

In 2012, Abraham started Atomic Labs, a San Francisco-based startup studio and venture capital investment firm. Jack Abraham himself had a remarkable origin story—Raised in Great Falls, Virginia, Abraham dropped out of the Wharton School of the University of Pennsylvania in 2008 at age 22 to co-found Milo.com, an online shopping platform that aggregated local retailer prices. He sold Milo to eBay for $75 million in 2010 at age 24.

The Atomic model worked like a creative factory for startups. Altogether, Atomic has produced 14 companies over the last 12 months, and that's on top of nine that it formed the year earlier. Notably, it has done this with not enormous amounts of funding. The studio provided resources, expertise, and capital in exchange for significant equity stakes in each venture.

Jack Abraham is the Managing Partner and CEO of Atomic, and is a pioneer of Atomic's now popular studio fund model for exclusively investing in companies founded at the firm. Through Atomic, Jack has founded 2 of the 10 fastest growing companies (based on a recent study of Silicon Valley startups) – Hims & Hers and Bungalow. Hims & Hers was the second fastest company to achieve a $1B valuation in US history.

The Founding Team

Hims Inc. was established in 2017 by Jack Abraham, Andrew Dudum and Hilary Coles as a part of the Atomic Labs portfolio. The trio brought complementary skills: Abraham's company-building expertise, Dudum's vision and consumer sensibility, and Coles's operational acumen.

Hims launched officially December 2017. They shipped their first box in the first month of 2018. The company emerged from Atomic's framework with built-in advantages: access to operational infrastructure, a network of experienced investors, and a playbook for rapid scaling.

Atomic created Hims and Hers because access to quality healthcare should be convenient and affordable for all. Hims & Hers is a telehealth company eliminating stigmas and making it easier for people to access care and treatment for the conditions that impact their daily lives. The company, one of the fastest growing DTC brands ever, was the 2nd fastest in US history to reach a billion-dollar valuation.

The Atomic incubation model gave Hims & Hers something that most startups lack: a running start with institutional knowledge baked in. This allowed the company to focus its energy on the core insight that would define its trajectory—that healthcare could be reimagined as a consumer brand experience.

III. The Founding Insight: De-stigmatizing Men's Health (2017-2018)

Identifying the Gap

The insight that launched Hims was simple but powerful: millions of men needed help with deeply personal health issues, but shame kept them from seeking treatment. Hair loss affects roughly 50% of men by age 50. Erectile dysfunction impacts an estimated 30 million American men. Yet these conditions remained shrouded in embarrassment, discussed in whispers if at all.

Dudum had observed this gap for years. While he was fortunate to have maintained his hairline and was a longtime user of skincare products, he watched friends and colleagues struggle silently with these issues. The traditional healthcare system made matters worse—requiring men to schedule appointments, sit in waiting rooms, and have awkward face-to-face conversations with doctors about topics that made them profoundly uncomfortable.

The founders saw a chance to make healthcare more accessible and less awkward, especially for issues that people found embarrassing to discuss. The mission crystallized: solve the problem of men struggling to talk about and get help for common issues like hair loss and erectile dysfunction.

The Initial Product Strategy

The early product lineup was deliberately focused. Hims was incubated at San Francisco-based venture-builder, Atomic by Andrew Dudum and Jack Abraham in 2017. At first, the focus was on providing telehealth services, such as for erectile dysfunction and hair loss. But HIMS would quickly expand its platform.

Hims initially sold erectile dysfunction treatment sildenafil and hair loss treatments such as minoxidil, biotin vitamins and DHT-blocking shampoo. The company focused primarily on men's health, providing solutions for stigmatized conditions like erectile dysfunction and hair loss. They created a direct-to-consumer telehealth platform that connected users with healthcare professionals online, offering discreet delivery of medications and products.

The business model was elegant in its simplicity. Rather than navigating the labyrinthine insurance system, Hims offered a cash-pay model with transparent pricing. Customers could complete an online consultation, receive a prescription from a licensed physician, and have medications delivered directly to their door—all without stepping into a doctor's office.

Key Insight: Healthcare as a Consumer Brand

"When I look at healthcare, there's no part of the experience that I love. It's a cold experience, it's not personalized to you at all, it wastes your time and your money, and it makes you feel sick," said Dudum. "It's my belief that in the next 10 years, that's going to change. People are going to put their money towards brands and experiences they love."

This philosophy represented a fundamental departure from how healthcare companies approached their markets. The insight that healthcare could be treated like a D2C brand was revolutionary—and controversial. Critics argued that medical care shouldn't be marketed like sneakers or meal kits. Proponents countered that making healthcare more accessible and less intimidating was itself a public good.

"There's still so many barriers for why people are not getting treated, whether or not that's access or price or stigma or education or a lack of personalized choice. So I think we're continuing to go deeper in the core specialties," Dudum stated in the company's Q4 2023 earnings call.

The strategic bet was that treating healthcare as a consumer brand would unlock demand that the traditional system had suppressed. De-stigmatization wasn't just marketing—it was the core product innovation. By normalizing conversations about men's health, Hims could reach customers who would never have sought treatment through conventional channels.

Investor Takeaway: The de-stigmatization thesis proved prescient. By approaching taboo health topics with the sensibility of a lifestyle brand rather than a medical institution, Hims created demand rather than simply capturing it. This represents a potentially replicable playbook for other underserved healthcare categories.

IV. Rapid Scaling & The "Hers" Expansion (2018-2020)

Achieving Unicorn Status

The velocity of Hims's growth was exceptional even by Silicon Valley standards. In January 2019, Hims raised $100 million in a Series C funding round with a pre-money valuation of $1 billion. In the same month, Hims was launched in the United Kingdom.

Hims, known by many for its phallic New York subway advertisements, has raised an additional $100 million in venture capital funding on a pre-money valuation of $1 billion. The round was first reported by Recode and confirmed to TechCrunch by sources with knowledge of the deal.

Hims officially launched just over one year ago and has raised $197 million already, as well as incorporated a women's wellness brand, Hers, to go alongside its flagship men's wellness brand. The business sells sexual wellness products, skin care and hair loss treatments directly to consumers.

The billion-dollar valuation—achieved in roughly a year from launch—made Hims one of the fastest companies in U.S. history to reach unicorn status. The round attracted blue-chip investors including Founders Fund, Forerunner Ventures, Redpoint Ventures, and Thrive Capital.

Launching Hers: The Women's Health Play

The expansion into women's health was always part of the plan. And in 2018, there was the launch of Hers. Hims launched Hers, a brand targeted to women, selling birth control pills and flibanserin in 2018.

"Yeah, we started with Hims. We are now officially Hims and Hers, and so we've got a whole lineup of over 100 products across the platform for men and women, which is incredible," Dudum explained.

Initially, Hims focused on men's health products, as suggested by the name, but expansion into women's products was always part of the plan. At the 2020 Wharton Healthcare Business Conference, Dudum explained the brand's direction: "We have always had the vision of building the brand into Hims and Hers, which is quite frankly why we named the company Hims."

The Hers platform addressed similar friction points in women's healthcare—providing access to birth control, treatments for female sexual dysfunction, and dermatological products through the same direct-to-consumer model that had proven successful for the men's brand.

Expanding Categories

In 2020, Hims launched mental health services, including anonymous group therapy. The company expanded its services to all 50 states, and the Ohio-affiliated pharmacy facility opened. Hims & Hers products were also available for the first time in retail locations, starting at Target.

Under Dudum's leadership, Hims & Hers continued to grow and innovate. In 2020, the company introduced mental health support, including group therapy sessions. This was a significant step towards addressing the growing mental health crisis and making mental health services more accessible.

The move into mental health was particularly well-timed, arriving just as the COVID-19 pandemic began to dramatically accelerate telehealth adoption across all demographics. What had been a niche offering for tech-savvy millennials suddenly became essential infrastructure for healthcare delivery during lockdowns.

Investor Takeaway: The rapid category expansion demonstrated that the de-stigmatization playbook was transferable across health verticals. The company's ability to maintain brand consistency while expanding into adjacent categories suggested a durable competitive advantage.

V. The SPAC Era: Going Public with Howard Marks (2020-2021)

The Oaktree Deal

By late 2020, the pandemic had transformed Hims & Hers from an interesting startup into a company riding massive secular tailwinds. Telehealth adoption had accelerated by years in a matter of months. The company made a strategic decision to capitalize on this momentum by going public—but through an unconventional route.

Startup Hims & Hers is going public through a merger with a special purpose acquisition company (SPAC) in a blank check deal. The three-year old telehealth company will merge with Oaktree Acquisition Corp. in a deal that will value the company at about $1.6 billion.

Howard Marks, Co-Chairman of Oaktree stated: "We are very pleased to launch our Oaktree Acquisition Corp. franchise with this partnership with Hims & Hers, a rapidly-growing provider of much-needed innovation to the healthcare system."

The involvement of Howard Marks—one of the most respected value investors in the world, whose firm Oaktree Capital Management oversees over $100 billion in assets—lent immediate credibility. This wasn't a fly-by-night SPAC sponsor looking for a quick flip; it was a considered partnership with sophisticated institutional backing.

Deal Structure & Funding

The deal values Hims & Hers at $1.6 billion, equal to 8.9 times estimated 2021 revenue, and 12.2 times estimated 2021 gross profit. Of the $279.5 million in proceeds, about $204.5 million is cash from Oaktree Acquisition's trust account and $75 million is from private placement investors, including Franklin Templeton and other Oaktree clients.

Consumer-facing digital health startup Hims & Hers on Wednesday completed its merger with special purpose acquisition company Oaktree Acquisition Corp., in a deal valuing the company at $1.6 billion. Hims & Hers received proceeds of almost $280 million as a result of the deal, which it plans to reinvest in driving geographic growth and new product lines. Beginning Thursday, Hims & Hers will trade on the New York Stock Exchange under the symbol HIMS.

Hims & Hers' management and existing equity holders have also rolled between 90% and 100% of their equity into the combined venture, which will continue to be led by CEO and co-founder Andrew Dudum, along with much of its existing leadership team. Merging with SPACs to go public as opposed to a traditional IPO has become an increasingly popular route for healthcare companies.

The fact that leading existing institutional backers—including Founders Fund, Forerunner Ventures, IVP, Redpoint Ventures, Thrive Capital, McKesson Ventures, and the Canadian Pension Plan Investment Board—intended to roll 100% of their equity demonstrated strong conviction in the company's future.

Initial Challenges as a Public Company

Hims & Hers is entirely cash-pay and doesn't contract with any insurance, though the company has said that could change in the future. Instead, members pay a subscription of around $20 a month for access to unlimited online consultations and a supply of generic medications. Hims & Hers markets itself as a one-stop shop for consumers, allowing them to bypass the traditional in-person care delivery pathway. It can be more expensive than other telehealth offerings, but is still generally cheaper than the unbundled price of a doctor's visit and full-price prescription.

The competitive landscape presented real challenges. Beyond growing pains, Hims & Hers faced additional risk as it looked to scale in the increasingly crowded and rapidly evolving virtual care market, elbowing against telehealth giants like Teladoc and Amwell and technology behemoths and retail pharmacies interested in the lucrative space, such as Amazon and CVS Health. The company acknowledged in filings: "We operate in highly competitive markets and face competition from large, well-established healthcare providers and more traditional retailers and pharmaceutical providers with significant resources."

The company has seen rapid growth. Since its launch a little more than three years ago, Hims & Hers has run more than 2 million telehealth visits and seen 100% compounded annual revenue growth, from $27 million in 2018 to $83 million in 2019 and an expected $138 million this year.

Investor Takeaway: The SPAC structure provided capital for expansion while allowing existing investors to maintain exposure. The involvement of credible institutional partners like Oaktree signaled confidence in long-term fundamentals, but the competitive dynamics remained challenging.

VI. Building the Moat: Vertical Integration Strategy (2021-2023)

Acquisition Spree & Pharmacy Infrastructure

With public market capital in hand, Hims & Hers embarked on an aggressive vertical integration strategy. The company recognized that controlling more of the value chain—from customer acquisition to prescription fulfillment—would create both cost advantages and competitive barriers.

Hims & Hers has finalized the acquisition of teledermatology specialist, Apostrophe. With this closing, Hims & Hers will expand its ability to provide consumers with some of the most advanced and personalized dermatology treatments, faster and at scale.

The Apostrophe acquisition was strategic on multiple dimensions. Launched seven years earlier, Apostrophe made it easier for consumers to get prescription acne medications and treatments by connecting users with board-certified dermatologists. The company had a vertically integrated mail-order pharmacy, which was licensed to fulfill orders in 29 states. This compounding infrastructure, combined with best-in-class dermatology capabilities, expanded Hims & Hers' ability to provide consumers with some of the most advanced and personalized dermatology treatments.

Compounding Pharmacy Acquisitions

Hims & Hers plans to acquire a compounding pharmacy as the telehealth company doubles down on weight-loss drugs and expands into other categories. Why it matters: The growing GLP-1 space could increase sales for Hims & Hers. Driving the news: Hims & Hers, which said in May that it would begin selling compounded versions of GLP-1 injections, disclosed a plan to buy a U.S.-based compounding facility registered with the FDA.

"The acquisition will enable HIMS to scale quickly and drive efficiency by verticalizing operations that require sterile, compounded medications," as TD Cowen analyst Jonna Kim noted. "We continue to like HIMS' capabilities to provide personalized healthcare offerings at affordable price points, but monitor execution around GLP-1s and subscriber growth."

Following the company's past acquisitions of 503A and 503B facilities, this additional facility deepens the company's commitment to maintaining operations in the United States for better insight into cost, availability and quality, more fully verticalizing the efficiency and durability of the supply chain. In addition, the peptide capabilities made possible through this acquisition position the company in the coming years to explore exciting advances in peptide innovation. The acquisition closed in early February, and Hims & Hers expects to continue strengthening infrastructure capabilities as demand for personalized treatment continues to grow.

The company has acquired a US-based peptide facility based in California. The acquisition will enable the company to strengthen the long-term durability of its domestic supply chain to meet the growing demand from Americans for personalized healthcare and treatment options.

International Expansion: ZAVA Acquisition

This strategic move will expand Hims Hers' footprint in the United Kingdom and will officially launch the company into Germany, France, and Ireland, with more markets anticipated soon. Hims Hers Health, Inc. (NYSE: HIMS), the leading health and wellness platform, today announced a significant step in its global expansion through its agreement to acquire ZAVA, a leading digital health platform in Europe.

Hims & Hers Health will acquire Zava, expanding the company's services to Ireland, France and Germany, and growing its active customer base by roughly 50%.

The company raised $1 billion in mid-May through convertible senior notes, which founder and CEO Andrew Dudum said would help the company expand internationally and implement artificial intelligence. The acquisition of Zava will bring Hims & Hers to over a million customers in the European market and launch it for the first time in Germany, France and Ireland.

The ZAVA deal represented a critical milestone enabling Hims & Hers to enhance cross-border platform integration. This acquisition not only expands geographic reach, but also consolidates a shared model of 24/7 virtual care, centralized pharmacy fulfillment and robust electronic medical record (EMR) systems. The company touts that it delivered almost 2.3 million consultations in 2024 throughout the UK, Germany, France and Ireland.

The Technology & AI Stack

Hims & Hers emphasizes its proprietary algorithms, customizable technology stack and cloud-based fulfillment systems as the backbone of its platform. These systems enable scalable telehealth consultations, subscription-based prescription fulfillment and personalized care management. By combining AI-driven personalization with vertically integrated infrastructure, Hims & Hers positions itself to deliver cost-effective, high-quality care at scale.

On the pharmacy side, HIMS operates its own vertically integrated facilities while maintaining agreements with partner pharmacies like Curexa and ITC Compounding Pharmacy, ensuring flexibility and scale in prescription fulfillment.

Investor Takeaway: The vertical integration strategy created meaningful barriers to entry. Owning pharmacy and compounding facilities, rather than relying on third parties, provides both cost advantages and quality control—critical factors as the company expanded into more complex product categories.

VII. The GLP-1 Inflection Point: Weight Loss Gold Rush (2024-2025)

Entering the GLP-1 Market

No single product category has transformed Hims & Hers's trajectory more dramatically than weight loss medications—specifically, compounded versions of GLP-1 drugs like semaglutide, the active ingredient in Novo Nordisk's blockbuster medications Ozempic and Wegovy.

In May, Hims & Hers started prescribing compounded semaglutide, the active ingredient in Novo Nordisk's blockbuster GLP-1 medications Ozempic and Wegovy. The company was a breakout star within the digital health sector in 2024, in part because of the success of its popular new weight loss offering. The company said its GLP-1 offering generated more than $225 million in revenue in 2024.

In 2024, Hims announced it would add compounded GLP-1 injections to its product portfolio, giving customers a way to access weight loss treatment. Hims claimed to be able to provide them cheaper and with greater availability than the branded medications that often cost $1,000+ per month without insurance.

Explosive Revenue Impact

Revenue at the telehealth company increased 95% in the fourth quarter from $246.6 million during the same period last year. However, the company's gross margin, or the profit left after accounting for the cost of goods sold, was 77%, while analysts polled by StreetAccount were expecting 78.4%.

Revenue for non-GLP-1 products increased 43% to $1.2 billion for the full year, "meeting our previous 2025 revenue target a year early," Chief Financial Officer Yemi Okupe said in a release.

The weight loss offering transformed the company's financial profile. Shares of Hims & Hers jumped more than 170% last year, thanks to soaring demand for GLP-1s. They closed up 5% on Friday, lifting the company's market cap to about $9.5 billion.

Compounded GLP-1s are typically much cheaper and can serve as an alternative for patients who are navigating complex supply hurdles and spotty insurance coverage. Hims & Hers sells compounded semaglutide for under $200 a month.

The FDA Shortage Resolution Crisis (February 2025)

The good times hit a wall in February 2025. Shares of Hims & Hers Health closed down around 26% on Friday after the U.S. Food and Drug Administration announced that the shortage of semaglutide injection products has been resolved. Semaglutide is the active ingredient in Novo Nordisk's blockbuster weight loss drug Wegovy and diabetes treatment Ozempic. Those medications are part of a class of drugs called GLP-1s, and demand for the treatments has exploded in recent years.

As a result, digital health companies such as Hims & Hers have been prescribing compounded semaglutide as an alternative for patients who are navigating volatile supply hurdles and insurance obstacles. Compounded drugs are custom-made alternatives to brand-name drugs designed to meet a specific patient's needs, and compounders are allowed to produce them when brand-name treatments are in shortage. The FDA doesn't review the safety and efficacy of compounded products.

It is the second big stock drop for Hims & Hers in a matter of days. The shares tumbled 26% on Friday after the U.S. Food and Drug Administration announced that the shortage of semaglutide injection products has been resolved.

The Personalization Pivot: Regulatory Gray Zone

Faced with the prospect of losing its GLP-1 revenue stream, Hims & Hers pivoted to a strategy centered on "personalization." Several companies, including Noom, Hims & Hers, and Mochi Health, continued to offer compounded GLP-1 drugs to patients. According to Hims, "personalized" doses of GLP-1 drugs enable companies to continue providing patients with compounded versions. Under FDA regulations, compounders can still make alternative versions of the drugs if they modify the dosage, add other ingredients, or change how the medication is administered.

Hims & Hers expects its weight loss business to bring in $725 million in revenue in 2025, Okupe told investors Monday. But that figure excludes commercially available dosages of semaglutide, which the company will no longer offer after the first quarter, executives said. Hims & Hers will now pivot to focus on other weight loss products given the FDA's announcement that the semaglutide shortage is resolved.

Among the ways Hims expects to hit that revenue target is through "personalization" of semaglutide doses, a legally permitted approach to mitigate the drug's side effects and help people stay on the drug.

The 2025 Super Bowl & GLP-1 Tracker

The company saw an "unprecedented" surge in engagement, with traffic spiking over 650% in the hours post-airing. Also, according to data from EDO Inc., Hims & Hers' Super Bowl ad ranked #5 in engagement among all ads aired during the game.

In its 2025 Super Bowl commercial, "Sick of the System," telehealth company Hims & Hers accuses the U.S. pharmaceutical industry of price-gouging weight-loss drugs, thereby fueling the obesity crisis. To that end, Hims & Hers offers compounded GLP-1s starting at $165 per month. (Nurses, teachers, veterans, military, and first responders get a $99 per month deal.)

The ad sparked intense controversy. Sens. Dick Durbin, D-Ill., and Roger Marshall, R-Kan., wrote a letter to the U.S. Food and Drug Administration expressing concerns over an "upcoming advertisement" that "risks misleading patients by omitting any safety or side effect information when promoting a specific type of weight loss medication." The Hims & Hers ad, called "Sick of the System," sharply criticizes the $160 billion weight loss industry.

The Novo Nordisk Breakup

In a significant development in June 2025, Novo Nordisk, the manufacturer of semaglutide (Ozempic, Wegovy), publicly announced the termination of its collaboration with Hims & Hers Health, Inc. This decision stemmed from Novo Nordisk's concerns regarding what it described as "illegal mass compounding and deceptive marketing" related to Hims & Hers' semaglutide offerings.

Novo Nordisk announced the termination of its collaboration with telehealth provider Hims & Hers Health, Inc., ending the company's direct access to Wegovy through NovoCare Pharmacy. The decision comes approximately one month after the partnership began, following the FDA's April 2025 declaration that the Wegovy shortage had been resolved. The partnership dissolution stems from disagreements over distributing and marketing semaglutide products. Novo Nordisk claims that Hims & Hers engaged in "deceptive promotion and selling of illegitimate, knockoff versions of Wegovy."

In highlighting warning letters sent to 55 online websites/telehealth companies, including Hims & Hers and DirectMeds, for selling "unapproved and misbranded" compounded GLP-1 drugs (semaglutide and tirzepatide) over the internet.

Investor Takeaway: The GLP-1 story illustrates both the opportunity and risk inherent in Hims & Hers's model. The company demonstrated remarkable agility in capitalizing on market demand, but the regulatory and legal uncertainties remain material. The sustainability of the weight loss business depends on the company's ability to navigate an evolving regulatory landscape.

VIII. Current Business Model & Financial Performance

The Subscription Engine

Hims & Hers has approximately 91% recurring revenue, which is a good sign for investors due to its predictability. Its customers also like Hims & Hers, with a net promoter score of 65.

Subscription-based services are crucial to Hims & Hers's revenue generation, making up most of their online revenue. During the first quarter, our subscriber base grew to nearly 2.4 million, with over 1.4 million utilizing personalized solutions. Revenue increased 111% year-over-year as we continued to deliver access to more precise, personalized care at scale.

Since our founding in 2017, Hims & Hers has become a leading health and wellness platform with more than 2.4 million subscribers as of June 30, 2025.

Recent Financial Results

The company posted a profit of $126 million in 2024 compared to a net loss of $25 million a year ago. For the full year, Hims reported earnings of 53 cents per share. Adjusted EBITDA was $177 million in 2024 compared to $50 million in 2023.

Affirms full year 2025 revenue guidance of $2.3 billion to $2.4 billion and raises Adjusted EBITDA guidance to a range of $295 million to $335 million. Introduces 2030 targets of at least $6.5 billion in revenue and $1.3 billion in Adjusted EBITDA.

Full Year 2025 Revenue Guidance: Expected to be between $2.335 billion and $2.355 billion, reflecting a 58% to 59% year over year increase. Full Year 2025 Adjusted EBITDA Guidance: Expected to be between $307 million to $317 million, reflecting a 13% margin at the midpoint.

Revenue of $586.0 million, up 111% year-over-year in Q1 2025. Net income of $49.5 million; Adjusted EBITDA of $91.1 million in Q1 2025. Subscribers grew to 2.4 million, up 38% year-over-year in Q1 2025.

Profitability Milestone

The company reached a significant milestone when it turned profitable in its first quarter of 2024, with revenue climbing to $872 million for the full year. A significant catalyst was the company's entry into profitability, sparking increased investor interest and confidence.

Profit margin: 8.5% (up from net loss in FY 2023). The move to profitability was driven by higher revenue. EPS: US$0.58 (up from US$0.11 loss in FY 2023).

Multi-Specialty Expansion

Hims & Hers has also forged partnerships with major U.S. health systems such as Ochsner, Mount Sinai and Hartford Healthcare. These collaborations enhance customer experience by providing access to in-person care when needed, complementing the digital platform. Notably, these arrangements do not involve financial incentives but rather strengthen continuity of care and expand Hims & Hers' integration within traditional healthcare.

Hims & Hers Health Inc (NYSE:HIMS) is investing in new specialties like menopause and low testosterone, which are expected to drive long-term growth.

New product launches include low testosterone and menopause offerings.

Investor Takeaway: The financial trajectory demonstrates the power of the subscription model at scale. The key metrics to monitor going forward are subscriber retention rates (indicating product stickiness), revenue per subscriber (showing wallet share expansion), and the sustainability of the weight loss business.

IX. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces Analysis

1. Threat of New Entrants: MODERATE-HIGH

The telehealth market has relatively low capital requirements for basic platforms, enabling new entrants to emerge quickly. However, several factors create meaningful barriers:

On the pharmacy side, HIMS operates its own vertically integrated facilities while maintaining agreements with partner pharmacies like Curexa and ITC Compounding Pharmacy, ensuring flexibility and scale in prescription fulfillment.

The company's vertically integrated pharmacy infrastructure, regulatory expertise, and pharmacy licensing create significant barriers. Brand recognition in stigmatized health categories is particularly hard to replicate—Hims & Hers has spent years building trust around sensitive topics.

2. Bargaining Power of Suppliers: MODERATE

Generic drug manufacturers have limited pricing power, which benefits Hims & Hers. However, the acquisition of a US-based peptide facility will enable the company to strengthen the long-term durability of its domestic supply chain to meet the growing demand from Americans for personalized healthcare.

Compounding pharmacies have gained leverage in the GLP-1 era, but Hims's acquisitions of its own compounding facilities mitigate this risk.

3. Bargaining Power of Buyers: LOW-MODERATE

Customers pay out-of-pocket, increasing price sensitivity relative to insured care. However, the subscription model creates switching costs and the stigmatized nature of many conditions creates customer reluctance to switch providers once trust is established. The company focuses on health-conscious people aged 25-45 who value convenience and discretion.

4. Competitive Rivalry: HIGH

Teladoc Health is a comprehensive telehealth provider offering a wide range of medical services. It represents a broader telehealth platform that competes with Hims & Hers. Teladoc Health's revenue in 2024 is projected to be $2.6 billion.

While Ro and Hims & Hers command the spotlight as the billion-dollar titans of DTC telehealth, it would be a strategic error to view the market as a simple duopoly. A vibrant ecosystem of well-funded competitors is actively carving out defensible niches, often by pursuing more specialized, condition-specific strategies.

The company faces competition from telehealth giants (Teladoc, Amwell), DTC competitors (Ro, Noom), and well-capitalized entrants (Amazon, CVS).

5. Threat of Substitutes: MODERATE

Traditional healthcare remains an option, though less convenient. The emergence of GLP-1 drugs highlights both opportunity and threat—the company must continually adapt its offerings as new treatments emerge.

Hamilton's 7 Powers Framework

Scale Economies: Hims & Hers benefits from significant scale economies in customer acquisition (spreading marketing costs across a larger subscriber base), pharmacy operations, and technology infrastructure. While Teladoc maintains a larger member base (approximately 90 million members), Hims & Hers' direct-to-consumer model has delivered superior gross margins (79% versus Teladoc's 70%) and stronger growth momentum.

Network Effects: Limited direct network effects, though the company's data advantage grows with each customer interaction, improving personalization algorithms and clinical decision-making tools.

Counter-Positioning: The company's direct-to-consumer, cash-pay model represents genuine counter-positioning against traditional healthcare. Incumbent healthcare providers cannot easily adopt this model without cannibalizing existing insurance-based revenue streams.

Switching Costs: Moderate switching costs exist due to the subscription model and the difficulty of transitioning medical relationships, particularly for sensitive conditions where trust has been established.

Branding: Arguably Hims & Hers's strongest power. The company has built distinctive brand equity around accessibility, discretion, and modern aesthetics. Strong Brand and Customer Loyalty: High customer retention rates due to brand trust and a focus on discreet, convenient services. Efficient Operations: Streamlined digital platform and supply chain for quick and reliable service. Data-Driven Personalization: Use of data to tailor treatments, improving outcomes and user satisfaction.

Cornered Resource: The company's proprietary technology stack, data assets, and regulatory expertise represent potentially cornered resources. The compounding pharmacy infrastructure and pharmacy licenses provide additional moat elements.

Process Power: The company's ability to rapidly expand into new health categories while maintaining quality and brand consistency suggests meaningful process power in category development.

Key Competitive Dynamics

HIMS (down 13.3%) has outperformed TDOC (down 29.7%) over the past three months. In the past year, HIMS has rallied 158.5% against TDOC's decline of 44.3%.

The competitive positioning reveals important insights. More than 65% of new subscribers in 2024 benefited from personalized products. The platform's proprietary MedMatch AI tool aids in customizing treatment plans by considering factors like side effects and efficacy. Recent launches, including GLP-1-based weight-loss treatments with personalized titration schedules, showcase HIMS' ability to scale its personalized offerings while maintaining high retention rates.

X. Bull Case vs. Bear Case

The Bull Case

1. Massive TAM with Expanding Footprint

The acquisition of ZAVA is expected to expand Hims & Hers' market opportunity by $52 billion. The global digital health market presents enormous opportunity, with telehealth projected to grow significantly through 2030. Hims & Hers's international expansion through ZAVA and planned Canadian entry opens new markets while its domestic specialty expansion into menopause, testosterone, and weight loss addresses additional high-demand categories.

2. Proven Unit Economics

The subscription model demonstrates strong retention, and the company has achieved profitability while continuing to invest in growth. Its $74 monthly online revenue per average subscriber (up 30% year-over-year) demonstrates the scalability of recurring revenue streams.

3. Vertical Integration Moat

The compounding pharmacy acquisitions, peptide facility, and domestic supply chain investments create meaningful barriers to entry and cost advantages that competitors cannot easily replicate.

4. Brand Equity in Stigmatized Categories

The company has built distinctive brand equity around making healthcare accessible for embarrassing conditions—a moat that takes years to develop and is difficult to attack directly.

5. Long-Term Revenue Targets

Revenue of at least $6.5 billion by 2030. Adjusted EBITDA of at least $1.3 billion. These targets represent roughly 3x revenue growth from current levels, with significant margin expansion.

The Bear Case

1. Regulatory Risk

The recent narrowing of full-year 2025 revenue guidance signals some caution but does not materially alter the most important near-term catalyst: further expansion into weight-loss and daily health programs. The biggest near-term risk remains regulatory and pricing uncertainty in key categories like GLP-1.

Because of Novo Nordisk's patents, generic semaglutide products will not be able to enter the U.S. market until at least 2032 so price will continue to be an issue.

The FDA's evolving stance on compounded medications represents existential risk to the weight loss business. The warning letters issued to Hims & Hers and the Novo Nordisk partnership termination signal increasing regulatory scrutiny.

2. GLP-1 Revenue Sustainability Questions

The company's weight loss business, while generating substantial revenue, operates in a regulatory gray zone. The "personalization" strategy to continue offering compounded semaglutide faces uncertain legal challenges.

3. Competitive Intensity

Hims & Hers faces fierce competition from established telehealth giants like Teladoc and Amwell, as well as retail pharmacies like CVS Health and Amazon. These rivals have deeper pockets and broader ecosystems, complicating Hims & Hers' efforts to dominate niche markets. Moreover, its reliance on a subscription model—while profitable—exposes it to customer churn risks.

4. Valuation Concerns

Meanwhile, Hims & Hers is trading at a forward 12-month price-to-sales (P/S) ratio of 3.1X, above its median of 2.2X over the past three years.

HIMS' forward 12-month P/S of 4.1X is lower than the industry's average of 5.8X, but is higher than its three-year median of 2.4X. It carries a Value Score of D.

5. Margin Pressure

Gross margins declined over 2 points quarter over quarter to 74%, impacted by lower intra-quarter revenue recognized per shipment. General and administrative costs increased due to the integration of ZAVA and hiring of new leadership talent. The company is experiencing headwinds from the transition away from generic on-demand sexual health solutions. There are near-term margin headwinds expected from price reductions in compounded GLP-1 treatment plans.

XI. Key Performance Indicators for Investors

The complexity of Hims & Hers's business demands focus on the metrics that matter most. Given the subscription-based model and regulatory dependencies, investors should zero in on these two critical KPIs:

1. Subscriber Growth & Retention Rate

Why It Matters: The subscription model's value depends entirely on the company's ability to acquire and retain subscribers. The current base of ~2.5 million subscribers represents meaningful scale, but the trajectory and retention metrics reveal whether the model is sustainable.

This was supported by a 20% growth in its subscriber base, adding 30,000 new subscribers sequentially.

Watch for: Year-over-year subscriber growth rates, net subscriber additions per quarter, and any disclosure of churn metrics. Slowing growth or elevated churn would signal demand saturation or competitive pressure.

2. Revenue Per Subscriber (or Average Order Value)

Why It Matters: This metric captures the company's ability to expand wallet share with existing customers—through additional product categories, higher-priced offerings, or increased purchase frequency.

Its $74 monthly online revenue per average subscriber (up 30% year-over-year) demonstrates the scalability of recurring revenue streams.

The company's subscriber base is projected to reach 2.8 million by year-end, with an average order value climbing to $194 from $137, signaling strong customer retention and upselling potential.

Watch for: Trends in revenue per subscriber over time, and the contribution of different product categories (weight loss vs. legacy products) to this metric. Rising revenue per subscriber indicates successful category expansion; declining metrics suggest pricing pressure or product cannibalization.

XII. Conclusion: The Stakes and the Path Forward

Hims & Hers has executed one of the most remarkable growth stories in digital health, transforming from a cheeky erectile dysfunction startup into a multi-billion-dollar healthcare platform in less than eight years. The company has demonstrated that de-stigmatization can be a powerful business strategy, that healthcare can be delivered with the user experience of a consumer brand, and that vertical integration creates meaningful competitive advantages.

But the company now stands at an inflection point. The GLP-1 gold rush that powered its explosive 2024 growth has entered a period of uncertainty. Regulatory scrutiny has intensified. The Novo Nordisk partnership has collapsed. And the legal foundation for continued compounded semaglutide sales remains contested.

"This quarter we continued to prove that our vision of helping tens of millions of people around the world access best-in-class, personalized care, from the comfort of their own home is more real than ever. We're building a platform that gets more personal, more proactive, and resonates with more people as we scale," said Andrew Dudum, co-founder and CEO.

The path forward depends on the company's ability to: - Navigate regulatory challenges around compounded medications - Successfully diversify beyond GLP-1s into new high-value categories - Execute international expansion through ZAVA and Canadian market entry - Maintain subscriber growth and retention in an increasingly competitive landscape

For long-term investors, the Hims & Hers story offers both significant opportunity and meaningful risk. The company has proven it can build a healthcare brand that resonates with modern consumers, scale that brand profitably, and integrate vertically to create competitive moats. Whether it can sustain this trajectory through regulatory headwinds and competitive pressure remains the central question.

The next chapter of this story will be written in examining rooms, FDA hearing rooms, and courtrooms—as much as in earnings calls and investor presentations. For a company that built its brand on transparency and accessibility, the stakes have never been higher.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube