GXO Logistics: How Brad Jacobs Built the World's Largest Pure-Play Contract Logistics Company

I. Introduction & Episode Roadmap

On the morning of August 2, 2021, a small group of executives stood on the trading floor of the New York Stock Exchange, ready to ring the opening bell. GXO Logistics began its first day of "regular way" trading as its leadership team celebrated becoming an independent, publicly traded company. The ticker symbol "GXO" flashed across screens worldwide—three letters representing billions of dollars of warehouses, hundreds of thousands of workers, and a decades-long playbook for industrial transformation.

GXO is the former global logistics segment of XPO Logistics, and it successfully spun off that day as the world's largest pure-play contract logistics provider. "This is an exciting milestone in GXO's history," declared CEO Malcolm Wilson. "We consider it a privilege to launch GXO as a new company at the top of the industry."

But the story of GXO isn't really about that August morning in Lower Manhattan. It's about a singular entrepreneurial vision that began decades earlier—a pattern of industry transformation so reliable it has minted billions in shareholder value across waste management, equipment rental, and now logistics. The central question driving this deep dive: How did a serial entrepreneur turn a $72 million truck brokerage into three publicly traded logistics behemoths worth tens of billions?

GXO today operates as the world's largest pure-play contract logistics provider, with more than 150,000 team members across more than 1,000 facilities totaling more than 200 million square feet. The company serves the world's leading blue-chip companies to solve complex logistics challenges with technologically advanced supply chain and e-commerce solutions, at scale and with speed.

Despite its market leadership, GXO exists in a remarkably fragmented industry with enormous runway ahead. The global contract logistics market size was estimated at USD 324.6 billion in 2024 and is projected to reach USD 503.3 billion by 2030, growing at a CAGR of 7.8% from 2025 to 2030. GXO currently captures only a small fraction of this addressable market in Europe and North America—leaving what management describes as a "deep pool" of potential new business through both organic share gains and continued consolidation.

What follows is the complete story: from Brad Jacobs' first oil brokerage in 1979, through the roll-up decade that built XPO into a top-ten global logistics provider, to the strategic spinoffs that liberated GXO to pursue its independent future. We'll examine the technology bets, the competitive landscape, and the key performance indicators that will determine whether GXO can extend its leadership in the years ahead.

II. The Brad Jacobs Playbook: Serial Value Creation

The Pattern: Industry Roll-Ups Through Scale and Technology

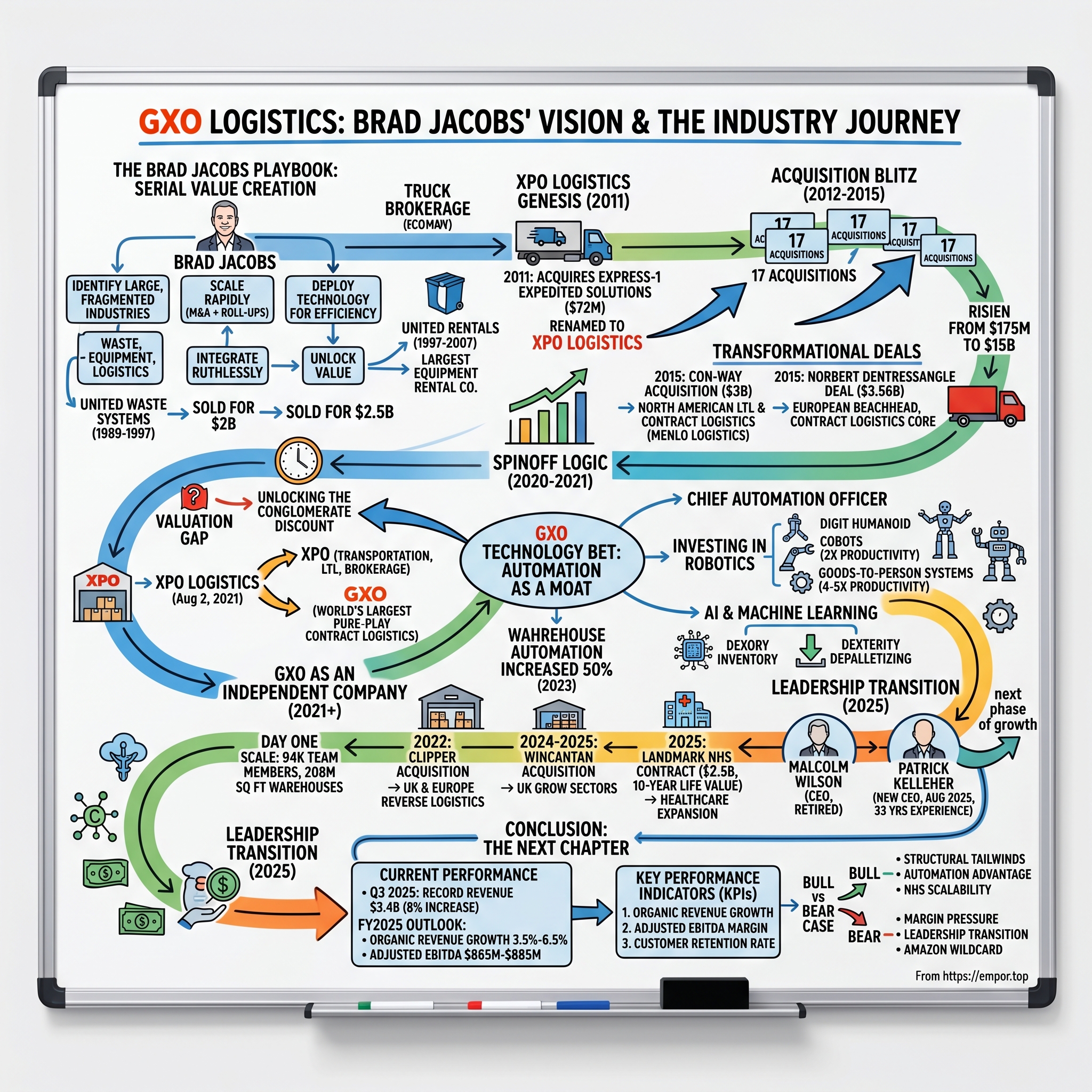

In the summer of 1979, a 23-year-old Brown University dropout named Bradley Jacobs found himself in Manhattan with an idea. He began his career that year with his first startup, Amerex Oil Associates, and led the team that grew it from a concept into one of the world's largest oil brokerage firms, with approximately $4.7 billion of annual gross contract volume and offices on three continents.

Jacobs was born in Providence, Rhode Island, the son of a fashion jewelry importer. He attended Northfield Mount Hermon School, then studied math and music at Bennington College and Brown University—however, he dropped out in 1976. That unconventional background—mathematics combined with musicianship—would prove to be foundational. The analytical rigor to parse complex markets. The pattern recognition to identify hidden opportunities. And perhaps most importantly, the discipline of practice: doing the same thing repeatedly, with small improvements, until mastery emerges.

In 1984, Jacobs went to England and founded Hamilton Resources (UK) Ltd., an oil trading company, using the bulk of his savings and a $1 billion line of credit from Banque Paribas. As chairman and chief operating officer, he grew the company to approximately $1 billion in annual revenue, before quitting the business in 1988 and moving back to the United States.

Then came the first industry transformation. In July 1989, Jacobs founded United Waste Systems in Greenwich, Connecticut, planning to consolidate small garbage collectors that had overlapping routes in rural areas. He served as chairman and CEO, and in 1992 he took the company public on the NASDAQ Stock Market. In August 1997, after the company had made 200 acquisitions, Jacobs sold United Waste Systems to USA Waste Services Inc. for $2.5 billion.

At the time of sale, United Waste was the fifth largest solid waste management company in the U.S., with its stock outperforming the S&P 500 by 5.6 times. The playbook was taking shape: identify a large, fragmented industry where scale brings genuine advantages. Acquire rapidly. Integrate ruthlessly. Deploy technology to create operational efficiencies competitors can't match.

In September 1997, Jacobs spearheaded $56.5 million in fundraising and formed United Rentals, serving as the new company's chairman and CEO. As with United Waste, he planned to grow through a rollup strategy. United Rentals went public in December 1997, and in June 1998 acquired U.S. Rentals Inc. for $1.3 billion, creating the largest equipment rental company in North America.

In the 10 years that Jacobs led United Rentals, the company completed approximately 250 acquisitions and its stock outperformed the S&P 500 Index by 2.2 times. By 2007, Jacobs and his team had built United Rentals into the 536th largest public corporation in America. United Rentals was the sixth best-performing Fortune 500 stock of the last decade, and became a "200-bagger"—the share price at inception was $3.50, and its stock now trades at more than 200 times that price.

The numbers are staggering when viewed in aggregate. During more than four decades as a CEO and serial entrepreneur, Brad Jacobs has created flagship companies across multiple industries, delivering tens of billions of dollars of value to shareholders. To date, he has founded eight billion-dollar or multibillion-dollar businesses, completed approximately 500 M&A transactions, and raised approximately 50 billion dollars of debt and equity capital, including three IPOs.

The Investment Thesis for Logistics

After departing United Rentals in 2007, Jacobs spent years surveying industries for his next opportunity. He told investors in 2011 that after leaving United Rentals, he started looking for a new industry. "I studied a lot of different industries, and I ended up concentrating on transportation and logistics," Jacobs said. "It's larger and more fragmented than the industries I've been involved with in the past. It was more than $3 trillion worldwide."

In 2010, he formed Jacobs Private Equity to make a substantial equity investment in a single company with the potential for superlative value creation and, in 2011, he identified the transportation and logistics industry as being large, fragmented and ripe for consolidation, with the right attributes to leverage scale and technology.

The insight was characteristic Jacobs: technology was about to transform logistics from a cost center into a competitive weapon. Companies that invested in automation, data analytics, and integrated systems would compound advantages over fragmented competitors for decades. The question was finding the right platform.

For investors evaluating GXO today, this history matters profoundly. The company emerged from a proven playbook with a specific architecture: fragmented industries transformed through scale, technology investment, and operational discipline. The critical question is whether that formula remains applicable as GXO operates independently—and whether new leadership can execute the next phase of growth.

III. The XPO Genesis: From Express-1 to Global Giant (2011-2015)

The Platform Acquisition

In the spring of 2011, a small freight services company called Express-1 Expedited Solutions traded on the American Stock Exchange with a market capitalization that barely registered on institutional radar screens. The company had a modest footprint: expedited transportation, some freight forwarding, basic brokerage operations. It was, by most measures, entirely unremarkable.

In 2011, the entrepreneur gained majority control of Express-1 Expedited Solutions, a freight-services provider with a market value of about $72 million that he renamed XPO Logistics.

Jacobs invested approximately $150 million in XPO (then named Express-1 Expedited Solutions), a transportation and third-party logistics provider. He became chairman of the board and CEO and gained ownership of approximately 71 percent of the company.

The mechanics of the deal were elegant in their simplicity. In connection with the closing of the Equity Investment, the company's name was changed from "Express-1 Expedited Solutions, Inc." to "XPO Logistics, Inc." on September 2, 2011. The company also effected a 4-for-1 reverse stock split that same day.

Jacobs subsequently outlined a detailed vision for XPO and where he wanted to take it. These steps included, first and foremost, building a multi-billion dollar transportation brokerage business in the coming years, growing organically and through acquisitions, building a comprehensive IT structure, and getting the right management team in place.

What Jacobs saw in Express-1 was something most observers missed entirely: a public company shell with clean balance sheet attributes, a basic operating platform, and a stock ticker that could serve as the foundation for something vastly larger. The ticker symbol "XPO" wasn't just branding—it was a promise of transformation.

The Acquisition Blitz

In 2012, Jacobs announced his intention to grow XPO's revenue from $175 million to $5 billion within five years, primarily through M&A. Instead, he grew revenue to $15 billion in just over four years.

Wall Street analysts greeted the announcement with skepticism bordering on derision. A $175 million freight brokerage was going to grow nearly 30-fold in half a decade? Through acquisitions? In one of the most capital-intensive industries in the American economy? The targets seemed not merely ambitious but mathematically improbable.

He bought a new base of operations, a Michigan logistics company, Express-1 Expedited Solutions. It had the stock ticker "XPO." He named the company XPO Logistics, and soon Jacobs was off, absorbing 17 companies from 2012 to 2015.

Each acquisition followed a specific pattern: identify targets with strategic value, execute quickly, integrate onto common technology platforms, extract synergies, move to the next deal. Through 17 acquisitions in the past four years as well as internal expansion, XPO had gone from a company that didn't exist in late 2010 to a $15 billion firm.

The Con-way Acquisition: Transformational Deal #1 (2015)

The acquisition that elevated XPO from ambitious upstart to industry heavyweight came in September 2015. XPO announced it would become the second largest provider of less-than-truckload (LTL) services in North America, and would expand its global contract logistics platform. The $3.0 billion transaction would increase XPO's revenue to $15 billion and would nearly double EBITDA to $1.1 billion.

Headquartered in Ann Arbor, Michigan, Con-way was a Fortune 500 company with a transportation and logistics network of 582 locations and approximately 30,000 employees serving over 36,000 customers.

The deal closed on October 30, 2015. The tender offer for all of the outstanding shares of Con-way common stock expired immediately after 12:01 a.m., New York City time. Approximately 81.1% of Con-way's outstanding shares were validly tendered into and not withdrawn from the tender offer. XPO completed its acquisition through a merger without a vote of Con-way's stockholders.

Bradley Jacobs said, "Our opportunistic acquisition of Con-way will make XPO the second largest provider of less-than-truckload transportation in North America, a $35 billion market. LTL is a non-commoditized, high-value-add business that's used by nearly all of our customers. Con-way is a premier platform that we will run with a fresh set of eyes as part of our broader offering."

The acquisition expanded the company's global contract logistics platform with the addition of 22 million square feet of space in 160 facilities. "Another crown jewel in this transaction is Con-way's subsidiary, Menlo Logistics, an asset-light top 30 global contract logistics provider with additional lines of business in freight brokerage and managed transportation."

For investors, the Con-way deal represented the Jacobs playbook in mature form: a transformational acquisition executed at a reasonable multiple (approximately 5.7x EBITDA), with clear synergy targets and immediate strategic benefits. The integration playbook was already well-practiced from prior deals.

IV. The Norbert Dentressangle Deal: The European Beachhead (2015)

The Strategic Logic

Before Con-way closed, Jacobs had already executed an even more audacious transaction—one that would fundamentally reshape XPO's geographic footprint and establish the foundation for what would eventually become GXO.

Brad Jacobs declared, "This is a defining moment in the growth of XPO. Our planned acquisition of Norbert Dentressangle will catapult XPO to a top ten global logistics company. It will more than triple our EBITDA to $545 million and increase our revenue to about $8.5 billion upon completion of the tender offer, nearly achieving our 2017 financial targets two years ahead of plan."

Norbert Dentressangle was a leading global provider of contract logistics, including e-commerce fulfillment; freight brokerage and transportation; and global forwarding services. Headquartered in Lyon, France, Norbert Dentressangle had 662 locations and approximately 42,350 employees.

On April 28, 2015, the group XPO announced a $3.56 billion (3.24 billion euros) deal to acquire Norbert Dentressangle, including acquired debt.

Execution and Integration

On June 8, 2015, XPO announced that it had consummated the previously announced agreement to purchase all of the shares of Norbert Dentressangle SA held by Mr. Norbert Dentressangle and his family, representing 67% of the company's outstanding shares, at a price of 217.50 euros per share.

Under the terms, XPO agreed to purchase a 67% stake held by the founding family at €217.50 per share, representing a 34% premium over the April 27, 2015 closing price.

The acquisition brought more than just scale. Acquiring Norbert Dentressangle SA, a company nearly twice the size of XPO, gave XPO a strong foothold in European markets, where ND's iconic red trucks had been serving logistics customers for decades. The combined company would have estimated revenues of about $8.5 billion per year.

Hervé Montjotin, chairman of the executive board and chief executive officer of Norbert Dentressangle, would serve as chief executive officer of XPO's European business and president of the parent company.

In Europe, the iconic red trucks formerly representing Norbert Dentressangle were being repainted to announce #WeAreXPO. XPO Logistics trucks debuted at the Grand Départ of the Tour de France in July, continuing a long-standing partnership as the official logistics partner of the Tour de France.

The European beachhead proved transformational for what would eventually become GXO. The contract logistics operations that came with Norbert Dentressangle—the warehouses, the customer relationships, the operational expertise—formed the core of GXO's European business today. Without this deal, GXO would be a fundamentally smaller, more geographically concentrated company.

For investors, the key lesson from this period is the importance of acquisitions as a growth engine. GXO's European presence, its scale advantages, and many of its most valuable customer relationships trace directly back to deals executed in 2015. The question for the future is whether similar transformational acquisitions remain available at reasonable valuations.

V. The Technology Bet: Automation as a Moat

Investing in Robotics and Automation

Inside a sprawling distribution center in Atlanta, Georgia, a scene plays out that would have seemed like science fiction just a decade ago. At GXO's Atlanta facility, Digit lifts heavy containers from a 6 River Systems robot and places them onto a conveyor belt. The humanoid robot—standing roughly five feet tall with articulated limbs and sensors scanning its environment—executes tasks that once required human labor exclusively.

As the industry leader in automated logistics solutions, GXO is among the first to collaborate with cutting-edge robotics developers to explore the game-changing potential of humanoid technology in the warehouse. As the first logistics provider in the world to deploy humanoid robots into live operations, GXO is paving the way for the entire logistics industry and beyond.

GXO is currently collaborating closely with three leading robotics developers—Agility, Apptronik, and Reflex—to incubate three different prototypes which are in different stages of development and bring distinct capabilities. Together, they are exploring a diverse array of practical applications to ensure that humanoid technology is fit for purpose by integrating, training, and testing these humanoids in their own warehouses.

The technology investment extends far beyond humanoids. GXO increased its overall units of warehouse automation in 2023 by 50%—this includes doubling its use of vision technology. Vision technology optimizes order validation and minimizes errors, and it can be rolled out across various operations without significant investment. The warehouse logistics company is looking for other practical applications of artificial intelligence and has piloted solutions for pick productivity and workforce management.

The Chief Automation Officer

The organizational commitment to technology is embedded at the executive level. Adrian Stoch, Chief Automation Officer at GXO, stated: "We're leading the charge on integrating automation into our customers' supply chains to help them grow and meet their strategic objectives. This pilot is especially exciting as it combines advanced robotics with artificial intelligence and machine learning into a practical application to make warehouse operations safer, more productive and more efficient."

Mobile, collaborative robots support workers in high-volume e-commerce warehouses, making the inventory picking process faster and more accurate. Employees work side by side with cobots that guide them to the correct storage areas, validate the inventory and transport it to designated packing stations—realizing an average 2x productivity improvement over workers alone.

Autonomous goods-to-person systems add value for customers in several ways. Inventory pickers can be repositioned at packing stations, and the robots bring units, in bulk, to each station. The robots can also climb shelves to retrieve fewer units in smaller bins. Robotic goods-to-person systems can deliver 4-5x productivity improvements and, importantly, enhance worker safety.

GXO's chief automation officer, Adrian Stoch, has faith that the humanoids could complete multiple tasks in a warehouse. "We are going really broad and aggressive on the category," Stoch told Business Insider. "It's because of where we see this going." The company is treating its warehouses as a "lab environment," deploying human-like robots to test their technological functions in real settings in order to provide feedback to robot makers.

Data Science and Machine Learning

Beyond physical automation, GXO invests heavily in software and analytics. GXO announced the successful conclusion of its collaborative pilot of an innovative AI-powered robot developed by Dexory, that performs automatic inventory reporting. As a result of the successful pilot, GXO is expanding deployment of the solution in the U.S. and Europe. "Customers turn to GXO to deploy cutting-edge automation that transforms warehouse operations and delivers real results," said Willem Veekens, Managing Director.

GXO is working with Dexterity, which leverages AI to power robots with human-like capabilities to depalletize, label and repalletize packages, optimizing the inbound and outbound processes in the warehouse. Because these smart robots utilize AI, they require virtually no instructions or setup prior to implementation, and they self-train on the job, improving their performance with every pick.

The company feels that AI-powered robots need to learn multiple tasks before they can run the entire operation. "We're not at wide-scale deployment and commercial viability yet, but we're not 10 years away, that's for sure," Stoch said.

For investors, the technology bet represents both opportunity and execution risk. GXO's automation investments create potential for margin expansion and competitive differentiation—but they also require substantial capital and carry integration complexity. The key metric to track is the percentage of technology-enabled warehouses relative to industry averages, which currently favors GXO substantially.

VI. The Spinoff Logic: Unlocking the Conglomerate Discount (2020-2021)

The Problem: Valuation Gap

By late 2019, XPO had become a logistics behemoth—but its stock price told a frustrating story. On January 15, 2020, Jacobs laid out his reasoning as to why XPO would seek a strategy that would ultimately lead to the GXO spinoff: "XPO is the seventh-best-performing stock of the last decade on the Fortune 500, based on Bloomberg market data. The share price has increased more than tenfold since our investment in 2011. Still, we continue to trade at well below the sum of our parts and at a significant discount to our pure-play peers."

Satish Jindel, president of SJ Consulting Group, believed Jacobs' plan would pay off, and Wall Street would better figure out how to assess the slimmed-down XPO and its GXO stock sibling. "Jacobs acquired a lot of companies and created a lot of synergies," said Jindel. "The market did not fully appreciate all of the units combined."

The conglomerate discount was real and measurable. Wall Street analysts struggled to value a company that spanned LTL trucking, freight brokerage, intermodal transportation, and contract logistics. Each business had different capital requirements, different growth profiles, different competitive dynamics. Investors who wanted pure exposure to the e-commerce logistics boom couldn't get it without also owning trucking assets.

The COVID Catalyst and E-commerce Boom

Then came 2020—and everything changed. In December, XPO finally said it would split into two companies. The company's North American logistics and LTL arms would remain as XPO, and the Europe-based contract logistics arm would become GXO.

The pandemic accelerated e-commerce adoption by years almost overnight. Consumers stuck at home ordered goods online in unprecedented volumes. Inventories were depleted. Retailers scrambled for warehouse capacity. The logistics industry—especially contract logistics providers who could stand up fulfillment operations rapidly—became essential infrastructure for the new economy.

XPO Logistics announced plans to spin off its logistics division in December 2020, with the intention of creating two pure-play entities focused on contract logistics (GXO) and freight transportation (XPO). In an interview, GXO Chief Investment Officer Mark Manduca said there is "massive scope" for growth both organically and through M&A activity. "A deep pool of potential new business exists for GXO, both through share gain and penetration," he added, explaining that companies are increasingly looking to outsource logistics as supply chains become ever complicated.

The Spinoff Execution

On August 2, 2021, XPO Logistics announced that it had completed the previously announced spin-off of GXO Logistics, creating two independent, publicly traded companies. The separation was completed through a distribution to XPO stockholders of one share of GXO common stock for every one share of XPO common stock held as of the close of business on the record date for the distribution, July 23, 2021. GXO shares were distributed at 12:01 a.m. Eastern Time on August 2, 2021 in a distribution intended to be tax-free to XPO stockholders.

In connection with the separation, GXO made a $794 million cash payment to XPO.

GXO Logistics, Inc. (NYSE: GXO) became the world's largest pure-play contract logistics provider. GXO committed to providing a world-class, diverse workplace for its 94,000 team members across 869 warehouse locations totaling 208 million square feet.

With several different businesses under its umbrella, XPO CEO Brad Jacobs believed that XPO's combined structure made the transportation stock difficult to value because the company had no true peers. The separation solved that problem. As a stand-alone company, GXO not only has a set of peers to make comparisons easy, but it is also four to eight times as big as its closest peers. That size gives the company a number of advantages, including in scalability, attractiveness to customers, and the ability to make acquisitions.

The spinoff represented pure financial engineering—no new assets were created, no new customers acquired—but the market responded enthusiastically. Separated from the trucking business, GXO could be valued against pure-play logistics peers. And by that measure, the company looked substantially undervalued.

VII. GXO as an Independent Company: The First Four Years (2021-2025)

Day One Scale

GXO said it launched with approximately 94,000 team members worldwide and more than 208 million square feet of warehouse space in 869 locations.

Wilson was named CEO in August 2021. GXO was formed when XPO Logistics spun off its logistics business into a separate, publicly traded entity. The newly created company was composed of XPO's North American and European logistics units.

Malcolm Wilson brought deep experience to the role. Malcolm Wilson has three decades of executive experience managing multinational supply chain operations in North America, Europe and Asia. Prior to the formation of GXO, he served as CEO of XPO Logistics Europe.

The customer roster from day one included some of the world's most recognizable brands—Apple, Nike, Boeing, Verizon, Whirlpool, and dozens of other blue-chip companies who trusted GXO to manage critical elements of their supply chains.

The Clipper Acquisition (2022)

GXO wasted no time pursuing the M&A strategy that investors expected. The transaction, announced on February 28, 2022, brought together two logistics industry leaders with highly complementary service offerings, customer portfolios, and footprints in the United Kingdom and Europe.

GXO announced that it received unconditional regulatory clearance from the U.K. Competition and Markets Authority (CMA) for its acquisition of Clipper Logistics plc. On May 24, 2022, GXO completed its offer, though both companies continued to be run independently pending completion of the regulatory review. GXO Chief Executive Officer Malcolm Wilson said, "GXO and Clipper are both industry leaders and together, we're even stronger. As one company, we expect to accelerate growth by expanding our geographic presence in key markets and verticals."

With Clipper, GXO gained more than 50 sites, 10 million square feet, 10,000 team members and added geographic presence in Germany and Poland, in the life sciences sector as well as expertise in premium services, including reverse logistics and repairs, which are key growth areas for GXO.

The Wincanton Acquisition (2024-2025)

The next major deal proved more complex. GXO announced that it had completed its acquisition of Wincanton plc. All conditions of the acquisition were met and GXO became the sole shareholder of Wincanton. On May 13, 2024, Wincanton shareholders received consideration of 605 pence for each Wincanton share held.

The acquisition expanded GXO's offering and customer base in several key strategic growth sectors in the UK, including Aerospace, Utilities, Industrial, and Healthcare. Additionally, the complementary infrastructure and offerings would enable GXO to manage the combined company more efficiently. GXO expected that the combination would lead to full annual net run-rate cost synergies of £45m (pre-tax) by the third year of integration.

The Competition and Markets Authority (CMA) cleared GXO's acquisition of Wincanton after its offer to sell Wincanton's dedicated grocery warehousing business. The sale of Wincanton to US giant GXO Logistics was completed for £762 million in April 2024, at which time the CMA issued an initial enforcement order. The CMA's 'phase one' investigation was completed in November 2024, when it suggested that the merger may result in a "substantial lessening of competition."

The UK's Competition and Markets Authority approved the merger between logistics providers GXO and Wincanton, subject to the sale of Wincanton's dedicated grocery warehousing business to a CMA-approved buyer. According to the CMA's final report, published on June 19, 2025, GXO's acquisition of Wincanton would "reduce competition in the supply of dedicated warehousing services to grocery customers in the UK." As a result, GXO agreed to sell Wincanton's dedicated grocery warehousing business.

The NHS Contract: Largest Deal in Company History

In May 2025, GXO announced a landmark contract that signaled its expansion into healthcare logistics. NHS Supply Chain, part of the National Health Service in the UK, selected GXO as its new logistics partner in a landmark 10-year, $2.5 billion contract. The agreement significantly expands GXO's presence in healthcare logistics, a strategic growth sector, where GXO's solutions are uniquely positioned to support the complex needs of these customers.

"We've finalized a landmark deal with England's National Health Service Supply Chain. This is our largest-ever contract and carries a total lifetime value of about $2.5 billion."

GXO will manage 8 NHS Supply Chain distribution centers and a dedicated fleet of more than 300 NHS Supply Chain vehicles to provide modern end-to-end logistics solutions to the NHS. Recently, GXO began a multi-year agreement in the U.S. with Siemens Healthineers to expand its Forward Stocking Network.

Current Performance and Leadership Transition (2025)

GXO Logistics reported its financial results for the third quarter of 2025, revealing a record revenue of $3.4 billion, an 8% increase year-over-year. In the third quarter of 2025, GXO delivered record revenue, up 8% year over year, of which 4% was organic.

For 2025, GXO expects to deliver organic revenue growth of 3.5% to 6.5%, adjusted EBITDA of $865 million to $885 million, adjusted diluted earnings per share of $2.43 to $2.63, and adjusted EBITDA to free cash flow conversion of 25% to 35%.

The company also navigated a significant leadership transition. GXO announced that Malcolm Wilson, chief executive officer, had informed the board of directors that he plans to retire in 2025. He would continue to lead the company during the executive search process for his successor.

During Wilson's tenure, GXO acquired Clipper Logistics and Wincanton; increased the company's revenue from $7.9 billion to $11 billion; increased adjusted EBITDA from $633 million to $757 million; and achieved a return on invested capital of more than 30% per year.

GXO announced the appointment of seasoned supply chain leader Patrick Kelleher as its new chief executive officer, effective August 19, 2025. Kelleher brings 33 years of global supply chain experience, having held senior executive roles at DHL Supply Chain, a division of Deutsche Post DHL Group. Most recently, he served as CEO, North America, where he oversaw significant growth and operational improvements across the business.

Brad Jacobs, chairman of GXO's board of directors, said: "Patrick is a world-class operator with the relevant experience to lead GXO through its next phase of growth. His proven track record and deep expertise in engineered solutions, automation, and cutting-edge contract logistics make him uniquely qualified to drive value for our customers and shareholders."

For investors, the leadership transition introduces both uncertainty and opportunity. Kelleher's background at GXO's largest competitor (DHL) brings deep industry knowledge and operational expertise. The question is whether he can maintain GXO's culture of innovation while accelerating organic growth and successfully integrating recent acquisitions.

VIII. Industry Context: The Contract Logistics Landscape

Market Size and Growth

The global contract logistics market size was estimated at USD 324.6 billion in 2024 and is projected to reach USD 503.3 billion by 2030, growing at a CAGR of 7.8% from 2025 to 2030. The rapid growth of e-commerce is a key market driver. In 2024, U.S. e-commerce sales reached USD 1.19 trillion, up 8.1% year-over-year, accounting for 16.1% of total retail sales. India's market is also expanding quickly, projected to grow from USD 123 billion in 2024 to USD 292.3 billion by 2028 at a CAGR of 18.7%. This growth is fueling demand for faster, scalable, and tech-enabled logistics.

The Asia Pacific contract logistics market accounted for 34.2% of the global share in 2024, driven by rapid e-commerce growth, mobile commerce adoption, and increasing cross-border trade. In India, efforts to modernize logistics infrastructure are further supported by international funding. In 2024, the Asian Development Bank approved a USD 350 million loan to bolster India's multi-modal logistics reforms.

Secular Tailwinds

Three structural trends are propelling the contract logistics industry forward:

Outsourcing acceleration: As supply chains grow more complex, companies increasingly recognize that logistics isn't a core competency. Outsourcing is anticipated to dominate the market as it is a low-cost strategy for expanding a business's international footprint and profitability.

E-commerce expansion: Online retail continues growing faster than brick-and-mortar, requiring fulfillment infrastructure that most retailers cannot build internally. In 2024, global e-commerce sales surpassed USD 6.5 trillion, increasing demand for flexible logistics solutions that can handle high order volumes and complex fulfillment requirements.

Automation adoption: Technology investments create economies of scale that smaller operators cannot match. Innovations such as automation, IoT, and AI are enhancing logistics operations, improving efficiency, and reducing costs.

The Competitive Landscape

DHL Supply Chain maintains its place as the global contract logistics market leader, with almost double the revenues of its nearest rival GXO.

DHL is the global market leader in the fragmented market of contract logistics, with a market share of 6.1% (2023) and operations in more than 50 countries.

In 2023, the contract logistics market sizes across regions totaled €280 billion, with Asia-Pacific at €99 billion, Europe at €87 billion, Americas at €82 billion, and Middle East/Africa at €12 billion; DHL Supply Chain captured a global share of 6.1%.

Key players operating in the contract logistics market include DHL Supply Chain (a division of Deutsche Post AG), GXO Logistics, Inc., United Parcel Service, Inc., DB Schenker, Kuehne + Nagel International AG, DSV A/S, Nippon Express Co., Ltd., CEVA Logistics, GEODIS SA, and Ryder System, Inc.

GXO's positioning as the "pure-play" leader is strategically important. Unlike DHL (which is part of Deutsche Post's broader postal and express operations) or UPS (which has parcel delivery as its core business), GXO focuses exclusively on contract logistics. This focus theoretically enables better capital allocation, clearer strategic priorities, and more relevant valuation comparisons.

IX. Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-LOW

Building a contract logistics operation at scale requires substantial capital and expertise. GXO operates over 200 million square feet of warehouse space—replicating that footprint would require billions in investment and years of construction. The technology barriers are equally significant: advanced automation, warehouse management systems, and analytics capabilities require sustained R&D investment.

Customer relationships create additional moats. Long-term contracts with blue-chip customers like Apple and Nike reflect years of relationship building and operational integration. New entrants would struggle to win business from established providers absent significant price concessions or service failures.

However, barriers aren't insurmountable. GXO's asset-light model (most facilities are leased rather than owned) means competitors don't need to acquire real estate. Regional players can compete effectively in specific geographies before expanding nationally.

2. Bargaining Power of Suppliers: MODERATE

GXO's most significant "supplier" is labor—the 150,000+ team members who operate warehouses daily. Labor represents the largest cost category, and tight labor markets can compress margins. GXO's financial results for the first quarter of 2025 show strong revenue growth but also highlight ongoing challenges related to profitability and cash flow management. Net losses widened to $95 million, compared to $36 million a year earlier.

Warehouse landlords have leverage in tight real estate markets, particularly in desirable locations near population centers. Automation equipment vendors—providers of robots, conveyor systems, and warehouse management software—face growing demand, which can lead to longer lead times and higher prices.

3. Bargaining Power of Buyers: MODERATE-HIGH

GXO serves sophisticated corporate customers with substantial negotiating leverage. Companies like Apple, Nike, and Boeing can credibly threaten to bring logistics in-house or switch to competitors. Multi-year contracts provide some protection, but renewal pricing remains intensely competitive.

Customer concentration creates additional risk. While GXO's customer base is diversified across hundreds of accounts, the loss of a major customer relationship could have material impacts on revenue and profitability.

4. Threat of Substitutes: LOW-MODERATE

The primary substitute for outsourced logistics is in-sourcing—companies bringing warehouse operations back in-house. However, the trend strongly favors outsourcing due to the complexity of modern supply chains and the technology investments required to compete effectively.

Amazon represents a unique dynamic. The e-commerce giant operates one of the world's largest logistics networks and has experimented with offering fulfillment services to third parties. Amazon could theoretically become a formidable competitor—or it could become a major customer. The relationship remains strategically important to monitor.

5. Competitive Rivalry: HIGH

The logistics industry is intensely competitive, with pressure on both pricing and service quality. GXO competes against global giants (DHL, Kuehne + Nagel), regional specialists, and emerging technology-enabled providers.

Price competition can compress margins, particularly in commoditized service categories. Differentiation through technology, service quality, and specialized capabilities becomes critical for maintaining pricing power.

X. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

GXO has more than 150,000 team members across more than 1,000 facilities totaling more than 200 million square feet.

This scale creates genuine cost advantages. Technology investments can be amortized across thousands of sites. Procurement leverage with automation equipment vendors reduces per-unit costs. Corporate overhead gets spread across a massive revenue base, improving operating leverage.

However, scale benefits have limits in contract logistics. Each customer relationship is somewhat unique, requiring customized operations and dedicated teams. Geographic dispersion means many facilities operate semi-independently rather than as integrated networks.

2. Network Effects: WEAK

Contract logistics lacks the classic network effects found in platform businesses. Adding one customer doesn't make the service more valuable to other customers. There's no viral growth or user-generated content that attracts additional participants.

However, weak network effects don't mean growth is impossible—just that it requires different mechanisms (sales, marketing, acquisitions, service quality) rather than self-reinforcing adoption curves.

3. Counter-Positioning: MODERATE

GXO's pure-play positioning creates genuine strategic differentiation. Contract Logistics: DHL Supply Chain leads globally with revenues nearly double those of GXO, its closest competitor, according to the 2024 Global Contract Logistics Report. This dominance in warehousing and distribution services provides stable, long-term revenue streams.

But GXO's pure-play focus means customers get a partner entirely dedicated to contract logistics—not distracted by express delivery, freight forwarding, or postal services. For diversified competitors like DHL or UPS, matching GXO's focus would require strategic restructuring that may not align with their broader business objectives.

4. Switching Costs: MODERATE

Customer relationships in contract logistics involve significant integration: systems connections, process customization, trained personnel, and operational learning curves. Switching providers means disrupting established workflows and accepting implementation risk.

Long-term contracts (often 3-7 years) provide some protection. However, at renewal time, customers can and do switch providers, particularly if competitors offer better pricing or capabilities.

5. Branding: WEAK

While GXO enjoys strong recognition among logistics professionals and corporate buyers, brand value doesn't translate into consumer-facing premiums the way it might in retail or consumer goods. The value proposition is operational performance, not brand prestige.

6. Cornered Resource: WEAK

GXO doesn't control scarce physical resources, intellectual property, or regulatory licenses that competitors cannot access. The company's advantages derive from scale, technology investment, and operational excellence—all of which can theoretically be replicated given sufficient capital and time.

7. Process Power: STRONG

This may be GXO's most defensible advantage. Decades of acquisition integration, technology implementation, and operational refinement have created institutional capabilities that are difficult to observe and replicate. The "how" of running 1,000+ warehouses efficiently represents accumulated knowledge that isn't captured in any single technology or process document.

XI. Key Performance Indicators: What Investors Should Track

For investors monitoring GXO's ongoing performance, three metrics warrant particular attention:

1. Organic Revenue Growth

Organic revenue growth (excluding acquisitions and currency effects) measures GXO's ability to win new business and expand existing customer relationships without depending on M&A. GXO delivered second quarter revenue of $3.3 billion, up 16% year over year, with organic revenue growth of 6%, the highest result in nine quarters.

Target: Mid-to-high single-digit organic growth indicates healthy competitive positioning and successful technology investments.

2. Adjusted EBITDA Margin

Profitability per dollar of revenue reveals whether GXO is capturing the benefits of scale and automation or facing margin pressure from competition and labor costs. GXO delivered adjusted EBITDA of $251 million in Q3 2025, up 13% from last year.

Target: Improving EBITDA margins year-over-year would validate the automation investment thesis and demonstrate pricing power.

3. Customer Retention Rate

Contract logistics relationships are measured in years, not quarters. High retention rates indicate customer satisfaction and switching cost moats. GXO has historically reported retention rates in the mid-90% range—a metric that warrants continued monitoring.

XII. Bull vs. Bear Case Summary

The Bull Case

Industry tailwinds are structural and durable. E-commerce penetration continues increasing. Supply chain complexity drives outsourcing. Companies that once managed logistics internally are recognizing the advantages of specialized providers.

Technology investments create compounding advantages. GXO's automation leadership expands over time as investments accumulate. Competitors face the choice of matching spending (compressing their margins) or ceding capability gaps.

Acquisition opportunities remain abundant. The contract logistics market remains highly fragmented. GXO's proven M&A playbook (inherited from the Jacobs era) can continue driving inorganic growth at reasonable valuations.

The NHS contract demonstrates scalability. GXO announced a significant expansion in the health sector with a landmark 10-year, $2.5 billion contract with NHS Supply Chain. The agreement significantly expands GXO's presence in healthcare logistics, a strategic growth sector. Healthcare represents a large, complex vertical where GXO's capabilities can command premium pricing.

The Bear Case

Margin pressure persists. Labor costs remain elevated, and automation investments require years to generate returns. Adjusted EBITDA rose to $163 million in Q1 2025, up from $154 million in Q1 2024. However, net losses widened to $95 million, compared to $36 million a year earlier.

Leadership transition introduces execution risk. CEO changes always create uncertainty. Patrick Kelleher arrives from DHL with strong credentials but must still prove he can maintain GXO's culture while accelerating growth.

Acquisition integration complexity. Wincanton and other recent acquisitions require successful integration to deliver promised synergies. Integration challenges could distract management and disappoint investors.

Amazon remains a wildcard. The e-commerce giant could expand its logistics offerings to compete directly with GXO. Alternatively, shifting Amazon priorities could benefit or harm GXO depending on how the relationship evolves.

XIII. Conclusion: The Next Chapter

In June 2024, Brad Jacobs did what he's done throughout his career: he moved on to the next challenge. Jacobs founded QXO with the intention to consolidate the $800 billion building products distribution industry. With the launch, he raised over $5 billion in equity, including what Bloomberg described as the largest equity offering ever in the building products sector.

The departure of Jacobs' active involvement (he remains chairman but is no longer CEO) marks the end of an era for GXO. The playbook that built XPO from a $72 million truck brokerage into three publicly traded companies must now be executed by new leadership—first Malcolm Wilson, now Patrick Kelleher.

The good news: the infrastructure is in place. GXO has more than 150,000 team members across more than 1,000 facilities totaling more than 200 million square feet. The company serves the world's leading blue-chip companies to solve complex logistics challenges with technologically advanced supply chain and e-commerce solutions, at scale and with speed.

The challenges are equally clear: margin pressure, integration complexity, competitive intensity, and the perpetual need to prove that scale advantages actually translate into superior returns.

"The overall economic market may not be growing, but the contract logistics industry is, and outsourcing is," GXO CEO Patrick Kelleher said.

For investors, GXO represents a classic growth-at-reasonable-price opportunity. The company operates in a structurally growing industry, holds a defensible competitive position, and trades at valuations that reflect uncertainty rather than perfection. The questions that remain—can new leadership execute? Will automation investments pay off? Are acquisition opportunities still available at reasonable prices?—will be answered in the quarters and years ahead.

The Brad Jacobs playbook has been written. The question now is whether the next generation can follow it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube