Global Payments: The Evolution of a Payments Technology Giant

I. Introduction & Episode Roadmap

Picture this: It's 2001, and the dot-com bubble has just burst. Tech stocks are cratering, investors are fleeing anything remotely connected to the internet, and a small payments processing company is about to spin off from its parent into one of the worst market environments in recent memory. That company? Global Payments.

Fast forward to today, and Global Payments stands as a $45 billion financial technology behemoth, processing over 50 billion transactions annually across more than 100 countries. The company serves 3.5 million merchants and 1,300 financial institutions, quietly powering the payment infrastructure that makes modern commerce possible. When you tap your card at a coffee shop in Columbus, process a payment through your dentist's practice management software, or receive funds through your school's tuition system, there's a good chance Global Payments is humming away in the background. The company reached Fortune 500 status in June 2021, a testament to its relentless expansion strategy and ability to navigate the dramatic shifts in how the world moves money. But here's the central question that defines this story: How did a spin-off from a 1960s data processing company—launched at the worst possible moment—transform into one of the world's largest pure-play payments technology companies?

The answer lies in a series of calculated bets, transformative mergers, and a fundamental reimagining of what a payments company could be. This is a story about timing markets perfectly while others panicked, about seeing software eating the world before software ate payments, and about building a global empire through dozens of acquisitions while somehow maintaining operational discipline.

We'll trace Global Payments' journey from its origins within National Data Corporation through its independence, its aggressive M&A playbook, the game-changing TSYS merger, and its current position as it navigates the AI-powered future of financial technology. Along the way, we'll unpack the strategic lessons, examine the bear and bull cases, and explore what this company's evolution tells us about the broader payments industry transformation.

II. Pre-History: National Data Corporation & The Foundation

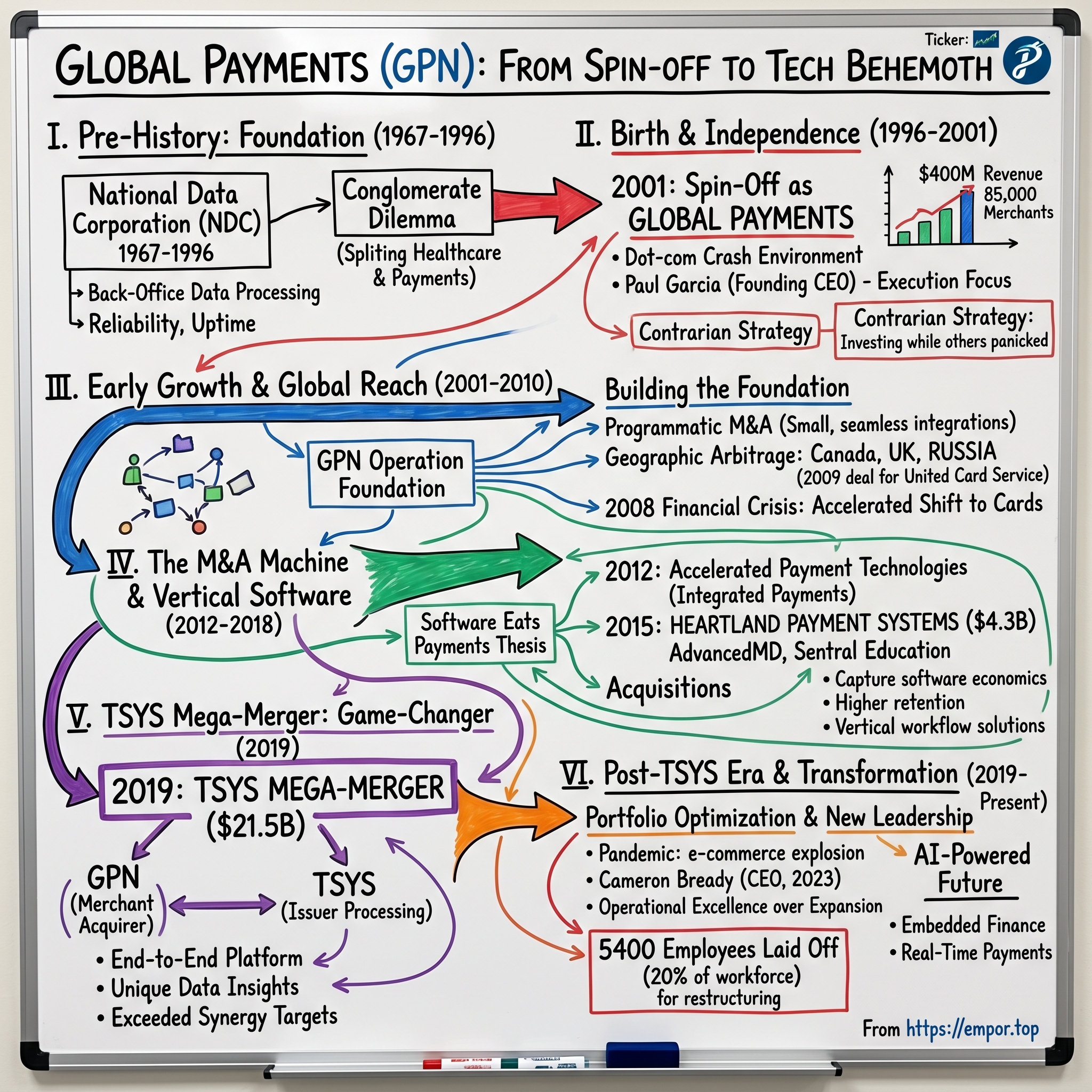

The year was 1967. While the Summer of Love captivated San Francisco and The Beatles released "Sgt. Pepper's," a less glamorous revolution was quietly beginning in Atlanta. National Data Corporation (NDC) was founded not as a payments company, but as a data processing firm serving the unglamorous but essential back-office needs of American businesses.

For its first three decades, NDC operated in the shadows of corporate America, processing health insurance claims and managing pharmacy benefits—the kind of mission-critical but invisible work that rarely makes headlines. The company built its reputation on reliability: when a pharmacy needed to verify insurance coverage at 2 AM, NDC's systems had to work. This obsession with uptime and accuracy would later prove invaluable in the payments world.

By the mid-1990s, NDC had quietly assembled two distinct empires under one roof. On one side sat the healthcare information services division, processing millions of medical claims and pharmacy transactions. On the other emerged something more intriguing: an electronic payment processing unit that had grown from a small experiment into a substantial business processing credit and debit card transactions for merchants across the country.

The late 1990s payments landscape was experiencing tectonic shifts. E-commerce was exploding—Amazon had just gone public, eBay was revolutionizing online auctions, and every business suddenly needed to accept cards online. Physical retail was also transforming as debit cards began displacing checks and cash. Transaction volumes were doubling every few years, and the infrastructure needed massive investment to keep pace.

NDC's management faced a classic conglomerate dilemma. The healthcare and payments businesses shared little beyond their data processing heritage. Healthcare required deep regulatory expertise and relationships with insurers and government agencies. Payments demanded speed, scale, and the ability to manage fraud in real-time. The capital needs were different, the competitive dynamics were different, and increasingly, the investor bases were different.

By 1999, as the dot-com boom reached fever pitch, NDC's board made a fateful decision: split the company. Let each business pursue its destiny without being constrained by the other. The healthcare business would remain as NDC, while the payments division would become something new—Global Payments.

III. The Birth of Global Payments: Spin-Off Story (1996–2001)

The boardroom at NDC's Atlanta headquarters buzzed with tension in early 2000. The spin-off announcement had been made, but the execution would prove far more complex than anyone anticipated. The timing, in retrospect, was almost comically bad—or brilliantly contrarian, depending on your perspective.

Global Payments was technically founded in 1996 as a subsidiary to house NDC's payments operations, but it existed more as a legal entity than an independent business. The real birth came with the spin-off announcement in 2000 and the actual separation on January 31, 2001. Shareholders would receive 0.8 Global Payments shares for each NDC share held—a ratio that reflected the relative valuations but also the uncertainty around this new entity.

Paul Garcia emerged as the founding CEO, a detail-oriented executive who had risen through NDC's ranks and understood both the technical complexities of payment processing and the relationship management required to keep merchants happy. Garcia wasn't a visionary Silicon Valley type—he was an operator who believed that in payments, perfect execution beat grand strategy every time.

The newly independent Global Payments faced immediate challenges. The company inherited aging mainframe systems that needed modernization, a primarily U.S.-focused merchant base when globalization was accelerating, and a business model under pressure from new entrants. The dot-com crash had vaporized hundreds of their e-commerce merchants overnight, and the surviving retailers were demanding lower rates.

But Garcia and his team saw opportunity where others saw crisis. While competitors were retrenching, Global Payments went on offense. They invested in new processing platforms, hired aggressively from struggling competitors, and most importantly, began acquiring small regional processors at distressed valuations. The playbook was simple: buy subscale processors, migrate them to Global Payments' platform, capture the cost synergies, and reinvest in growth.

The New York Stock Exchange approved the GPN ticker in late 2000, and when Global Payments began trading independently in February 2001, it marked not an ending but a beginning. The company had $400 million in revenue, processed for 85,000 merchants, and employed 1,000 people. Those numbers would soon look quaint.

IV. Building the Foundation: Early Growth & International Expansion (2001–2010)

September 11, 2001, changed everything. Eight months after Global Payments' independence, the terrorist attacks didn't just shock the nation—they fundamentally altered how businesses thought about payment processing. Suddenly, redundancy and geographic distribution weren't nice-to-haves but existential requirements. Global Payments' Atlanta base, far from New York's financial center, transformed from a limitation into an advantage.

The early 2000s became Global Payments' laboratory for what would become its signature strategy: programmatic M&A. While large competitors fought messy integration battles after mega-mergers, Global Payments perfected the art of acquiring $50-100 million revenue processors and seamlessly integrating them within quarters, not years. Each acquisition followed the same playbook: maintain the local sales presence, migrate the technology platform, eliminate duplicate costs, and move on to the next target.

By 2005, the company had quietly doubled its merchant base and expanded into Canada and the UK. But Garcia knew that to truly compete globally, Global Payments needed to go beyond the English-speaking world. The breakthrough came in 2009 with a deal that surprised the industry: $75 million for United Card Service, Russia's leading credit card processing company.

Russia in 2009 was not for the faint of heart. The financial crisis had devastated the ruble, oligarchs controlled much of the economy, and Western companies were often viewed with suspicion. But Global Payments saw what others missed: a massive population beginning to embrace electronic payments, limited competition, and the opportunity to build the rails for an entire country's payment infrastructure.

The United Card Service acquisition proved transformative beyond its financial impact. It demonstrated that Global Payments could operate in complex, non-Western markets. It provided a blueprint for emerging market expansion. And perhaps most importantly, in 2011, Global Payments's United Card Service bought Alfa-Bank's credit card processing unit, consolidating their Russian position and proving they could execute complex deals far from Atlanta.

The 2008 financial crisis had been a near-death experience for many financial services companies, but Global Payments emerged stronger. While banks were failing and consumers were deleveraging, the shift from cash to cards actually accelerated as people sought better transaction records and fraud protection. Global Payments' stock, which had dropped to $12 during the crisis, ended 2010 above $40.

V. The M&A Machine: Scale Through Acquisitions (2012–2018)

The conference room in October 2012 was electric. Global Payments had just announced its largest acquisition to date: $413 million for Accelerated Payment Technologies, a deal that would expand their presence in integrated payments and vertical software. But this was just the opening move in what would become a six-year acquisition spree that transformed the company's DNA.

The APT deal signaled a crucial strategic shift. Rather than just processing payments, Global Payments would embed itself into the software that businesses used daily. When a dentist updated patient records, scheduled appointments, or processed payments, it would all flow through Global Payments' technology. This wasn't just about processing transactions—it was about becoming indispensable to business operations.

Then came the deal that changed everything: Heartland Payment Systems. On December 15, 2015, Global Payments announced it would acquire Heartland Payment Systems for $4.3 billion. The industry was stunned. Heartland was nearly as large as Global Payments itself, processing for over 250,000 merchants. The combined entity would become the third-largest merchant acquirer in the United States.

The Heartland integration became a masterclass in merger execution. Rather than forcing immediate consolidation, Global Payments maintained Heartland's sales force and brand while gradually migrating backend systems. Customer attrition remained below 2%, far better than the 5-10% typically seen in large payment company mergers. By 2017, the combined company was generating over $400 million in cost synergies, exceeding all initial projections.

In 2017, Global Payments initiated acquiring divisions of Active Networks, pushing deeper into vertical software. In 2018, Global Payments completed the acquisition of AdvancedMD, a leading cloud-based practice management software provider for medical practices. Also in 2018, Global Payments completed the acquisition of Sentral Education, extending their reach into education technology.

These weren't random acquisitions—they followed a clear thesis. Find vertical markets with complex workflows, acquire the leading software provider, integrate payments seamlessly into the experience, and capture both the software economics and payment flow. A dental practice using Global Payments' software was 85% less likely to switch payment processors than one using standalone terminals.

By 2018, Global Payments had transformed from a pure payments processor into a software-powered commerce enabler. The company was processing over $400 billion in volume annually, operating in 30 countries, and generating over $3 billion in revenue. But the biggest transformation was yet to come.

VI. The TSYS Mega-Merger: Transformative Deal (2019)

May 28, 2019, 6:00 AM Eastern. The press release hit the wires like a thunderbolt: Global Payments announced a $21.5 billion merger with TSYS. This wasn't just another acquisition—it was a merger of equals that would create the world's largest pure-play payments technology company.

TSYS brought something Global Payments desperately needed: issuer processing. While Global Payments had focused on the merchant side (helping businesses accept payments), TSYS was the largest third-party payment processor for issuing banks in North America, with a 40% market share, and one of the largest in Europe. The combination would create the industry's only company with leading positions in both merchant acquiring and issuer processing.

The deal structure was elegant in its simplicity: TSYS shareholders would receive 0.8101 Global Payments shares for each share of TSYS common stock, representing an equity value for TSYS of approximately $21.5 billion. This reflected a price per share of $119.86 for each share of TSYS common stock, and an approximately 20% premium to TSYS' unaffected common share price as of the close of business on May 23, 2019. Upon closing, Global Payments shareholders would own 52% of the combined company, and TSYS shareholders would own 48% on a fully diluted basis.

The strategic rationale was compelling. In an increasingly digital world, the lines between issuing and acquiring were blurring. A unified platform could offer banks and merchants unprecedented insights into transaction flows, fraud patterns, and consumer behavior. The combined data set—seeing both sides of billions of transactions—would create a competitive moat that standalone players couldn't match.

The merger was expected to trigger a Federal Trade Commission investigation. However, no such investigation occurred. This surprising regulatory smooth sailing allowed the companies to close the deal faster than expected and begin integration immediately.

The integration challenge was massive. After merging with TSYS in 2019, Global Payments had nearly 24,000 employees, operated in over 100 countries, and processed for millions of merchants and over 1,300 financial institutions. But Jeff Sloan, who had become CEO in 2013, and the integration team had learned from years of acquisitions. They maintained separate brands where it made sense, focused on quick technology wins, and prioritized revenue synergies over cost cuts.

By early 2020, the combined company was already exceeding synergy targets. Cross-selling opportunities were materializing faster than expected—banks using TSYS for issuing were adopting Global Payments' merchant services, while Global Payments' enterprise merchants were leveraging TSYS's issuer connections for better authorization rates. The merger had created something truly unique in payments: an end-to-end platform that could see and optimize the entire transaction lifecycle.

VII. Post-TSYS Era: Portfolio Optimization & New Leadership (2019–Present)

The ink was barely dry on the TSYS merger when the world changed. COVID-19 hit in March 2020, just six months after the deal closed. Overnight, Global Payments faced a crisis: physical retail collapsed, travel and entertainment spending evaporated, and thousands of their small business merchants were fighting for survival.

But crisis revealed character. While transaction volumes initially plummeted 30%, e-commerce exploded. Global Payments' years of investment in omnichannel capabilities suddenly proved prescient. Restaurants pivoted to delivery, retailers launched buy-online-pickup-in-store programs, and B2B payments finally went digital. By the third quarter of 2020, volumes had not only recovered but were exceeding pre-pandemic levels.

The pandemic accelerated Global Payments' strategic evolution by years. In 2020, 63 percent of the company's revenue was derived from Merchant Solutions, 26 percent from Issuer Solutions, and 11 percent from the Business and Consumer Solutions segment, which operates as NetSpend. The geographic mix had also evolved significantly: Eighty percent of Global Payments Merchant Solutions revenue was from North America, 15 percent was from Europe, and five percent was from Asia.

In August 2022, Global Payments entered a definitive agreement to acquire EVO Payments Inc. for nearly $4 billion, further consolidating the merchant acquiring space and expanding their presence in international markets, particularly Poland and Mexico. The deal demonstrated that even post-TSYS, Global Payments maintained its M&A appetite.

Then came the leadership transition that would define the company's next chapter. On May 1, 2023, the company announced that CEO Jeffrey M. Sloan would resign, effective June 1, 2023. COO Cameron M. Bready succeeded him as CEO and president. Bready, who had been with the company since 2010 and served as CFO during the TSYS merger, brought a different philosophy: operational excellence over expansion.

The new approach became clear in 2024. Starting in early 2024 and continuing into September, Global Payments began laying off staff. These layoffs took place in the US, Canada, UK and India, as well as other smaller regional markets. Approximately 5400 employees were laid off during this time. This represented nearly 20% of the workforce—a dramatic restructuring aimed at eliminating redundancies from years of acquisitions and preparing for an AI-powered future where automation would handle routine tasks.

The transformation wasn't just about cost-cutting. Global Payments was fundamentally reimagining its operating model, consolidating dozens of regional platforms into unified global systems, and investing heavily in artificial intelligence and machine learning capabilities. The goal: become a technology company that happens to process payments, not a payments company trying to bolt on technology.

VIII. Business Model & Competitive Positioning

Walk into any modern business—a trendy coffee shop in Austin, a dental practice in Denver, a university bookstore in Boston—and you'll likely encounter Global Payments' technology, even if you never see their name. This invisibility is both their greatest strength and biggest challenge.

Global Payments operates through two segments, Merchant Solutions and Issuer Solutions. The Merchant Solutions segment offers authorization, settlement and funding, customer support, chargeback resolution, reconciliation and dispute management, terminal rental, sales and deployment, payment security, and consolidated billing and reporting services. But this clinical description misses the magic: they've built an ecosystem where payments disappear into business workflows.

Consider a modern medical practice using Global Payments' AdvancedMD platform. When a patient schedules an appointment, the system automatically verifies insurance eligibility. During the visit, the doctor updates records in the same system that will later process the payment. The insurance claim, patient copay, and payment plan all flow through integrated workflows. The practice never thinks about "payment processing"—they just run their business.

This software-led strategy has transformed Global Payments' economics. Traditional payment processing is a commodity business with razor-thin margins, where competitors fight over basis points. But when payments are embedded in mission-critical software, pricing power increases dramatically. A restaurant using Global Payments' point-of-sale system that manages inventory, employee scheduling, and customer loyalty isn't switching processors to save 10 basis points on processing fees.

The competitive landscape has consolidated into three giants: Global Payments, Fiserv (after acquiring First Data), and Fidelity National Information Services (after acquiring Worldpay). Each has pursued a similar strategy of combining merchant acquiring with software and technology services, but with different emphasis. Fiserv leans heavily on its bank technology heritage, FIS on its capital markets expertise, while Global Payments has gone deepest into vertical software.

But the real competition isn't from traditional players—it's from the edges. Stripe has built a $95 billion valuation by making payments invisible for developers. Square (now Block) has captured millions of small businesses with simple, elegant solutions. Adyen has won enterprise clients with a modern, unified platform. These new entrants don't carry the technical debt of decades-old mainframes or the complexity of dozens of acquisitions.

In 2020, the company was recognized as the first payment processor to win the J.D. Power Award for excellence in customer service, a remarkable achievement in an industry not known for customer satisfaction. This recognition validated their strategy of combining technology innovation with human support, rather than pursuing pure automation.

The company's geographic footprint has become a crucial differentiator. With 27,000 team members across 38 countries, Global Payments can serve multinational corporations with true global capabilities while maintaining local expertise. A U.S. retailer expanding to Europe doesn't need to find new payment partners—Global Payments can provide unified reporting, consistent technology, and local compliance expertise across all markets.

IX. Playbook: Strategic & Investing Lessons

The Global Payments story offers a masterclass in building a platform through serial acquisitions in a fragmented market. Their playbook, refined over two decades and dozens of deals, contains lessons that extend far beyond payments.

Lesson 1: Timing Market Consolidation Waves Global Payments didn't create the payment industry consolidation—they surfed it perfectly. They started with small deals when valuations were reasonable, built integration capabilities when mistakes were cheap, and then executed transformative mergers when they had the currency and expertise to succeed. Too many companies either move too early (overpaying without integration skills) or too late (when targets are picked over and expensive).

Lesson 2: The Power of Programmatic M&A While competitors swung for the fences with massive, bet-the-company mergers, Global Payments built muscle memory with dozens of smaller deals. Each $50-100 million acquisition was a repetition, refining the integration playbook. By the time they attempted the Heartland and TSYS deals, they'd already made every mistake at small scale. This programmatic approach also kept the organization perpetually ready for integration—it wasn't a special project but business as usual.

Lesson 3: Software Eats Payments Global Payments recognized before most that pure payment processing was a race to the bottom. Their aggressive move into vertical software—healthcare, education, hospitality—wasn't just about diversification. It was about changing the game entirely. When you control the software layer, payments become a feature, not a product. This insight drove superior economics and customer retention that pure processors could never match.

Lesson 4: Geographic Arbitrage The Russia expansion in 2009 seemed crazy at the time but revealed a crucial insight: emerging markets offer not just growth but the opportunity to build infrastructure from scratch. While developed markets required displacing entrenched competitors, emerging markets let Global Payments become the infrastructure. This pattern repeated in Eastern Europe, Latin America, and Asia-Pacific.

Lesson 5: Integration Excellence as Competitive Advantage Most acquisitions fail at integration, but Global Payments turned this into their superpower. They developed a systematic approach: maintain customer-facing continuity, quickly consolidate backend systems, capture cost synergies within 18 months, and reinvest savings into growth. This predictability let them pay higher multiples than competitors because they could reliably extract more value.

Lesson 6: Capital Allocation Discipline Despite their acquisition appetite, Global Payments maintained remarkable capital discipline. They walked away from deals when prices got crazy, returned capital through buybacks when their own stock was cheap, and maintained investment-grade ratings throughout. This wasn't growth at any cost—it was growth at the right cost.

Lesson 7: The Platform Paradox Building a platform requires standardization for efficiency but customization for customer value. Global Payments solved this paradox by standardizing infrastructure (processing rails, risk management, reporting) while allowing flexibility at the application layer. Each vertical got its specialized software, but it all ran on common plumbing.

X. Analysis & Bear vs. Bull Case

Looking at Global Payments today requires confronting a fundamental paradox: the company trades at compelling valuation metrics—a trailing PE ratio of 12.64 and forward PE ratio of 6.33, with a PE of 12.3x compared to peer average of 56.5x—yet the stock has underperformed, decreasing by 19.03% in the last 52 weeks. This disconnect between fundamentals and market perception creates both opportunity and risk.

The Bull Case: Platform Power and Operational Transformation

The optimistic thesis rests on several pillars. First, Global Payments has successfully transformed from a commodity processor into a software-driven platform. With gross margins of 62.87% and operating margins of 25.46%, the company demonstrates the economic power of this transition. These aren't the margins of a traditional processor—they're software company economics.

The valuation appears compelling on multiple metrics. The PEG ratio of 0.66 suggests the market is undervaluing future growth potential. The company generated $3.56 billion in operating cash flow and $2.90 billion in free cash flow in the last 12 months, demonstrating robust cash generation even amid restructuring.

The operational transformation under Cameron Bready could unlock significant value. The company has already identified $600 million in operating income benefits from their transformation program. With 5,400 employees removed from the cost base and systems consolidation underway, margin expansion seems inevitable.

Geographic diversification provides multiple growth vectors. While 80% of merchant revenue comes from North America, the international operations offer higher growth potential as electronic payments penetrate emerging markets. The company's presence in over 100 countries provides optionality that purely domestic players lack.

The integrated issuer-merchant platform from the TSYS merger creates unique cross-selling opportunities. Few competitors can offer both sides of the transaction, providing data insights and optimization capabilities that standalone players cannot match. This should drive both revenue synergies and customer stickiness.

The Bear Case: Structural Headwinds and Execution Risk

The pessimistic view starts with industry dynamics. Payment processing is becoming increasingly commoditized, with new entrants like Stripe and Square redefining customer expectations. These modern platforms lack the technical debt of legacy systems and can iterate faster than traditional players.

The company has $2.90 billion in cash against $16.94 billion in debt, giving a net debt position of $14.04 billion. This leverage limits financial flexibility and makes the company vulnerable to rising interest rates or economic downturns. The debt burden from serial acquisitions constrains capital allocation options.

The massive restructuring carries execution risk. Laying off 20% of the workforce while maintaining service levels and completing technology migrations is extraordinarily complex. Customer attrition could accelerate if the company stumbles during this transition.

Competition from Big Tech looms large. Apple Pay, Google Pay, and Amazon's payment ambitions threaten to disintermediate traditional processors. These companies have unlimited capital, massive customer bases, and technology capabilities that Global Payments cannot match.

Regulatory risks are intensifying globally. European regulations on interchange fees, U.S. scrutiny of payment processing fees, and data privacy requirements all pressure margins and increase compliance costs. The company operates in a highly regulated industry where rules can change quickly.

The vertical software strategy, while successful so far, faces platform risk. If Shopify, Salesforce, or other horizontal platforms add native payment capabilities, Global Payments could lose its differentiation in key verticals.

The Verdict: Transformation at an Inflection Point

Global Payments sits at a critical juncture. The company has the assets, scale, and market position to thrive in the evolving payments landscape. The valuation suggests significant upside if execution succeeds. But the transformation is complex, competition is intensifying, and the margin for error is shrinking.

For investors, this presents a classic risk-reward decision. The bull case offers potential 50%+ upside if the operational transformation succeeds and multiples re-rate toward software comparables. The bear case suggests further compression as commoditization accelerates and growth slows.

The key variables to watch: merchant same-store sales growth (indicating market share trends), software revenue mix (validating the platform strategy), margin progression (proving operational leverage), and integration success metrics from recent acquisitions.

XI. Epilogue & Future Outlook

Standing in Global Payments' gleaming Atlanta headquarters, you can feel the tension between heritage and transformation. The walls display artifacts from the NDC days alongside screens showing real-time transaction flows from around the globe. It's a physical manifestation of the company's challenge: honoring what got them here while building what comes next.

The payments industry's next frontier is already visible. Real-time payments, powered by new rails like FedNow and RTP, will compress settlement times from days to seconds. Central bank digital currencies could reshape cross-border payments. Buy-now-pay-later is redefining consumer credit at the point of sale. Each trend represents both threat and opportunity for incumbent players.

Artificial intelligence and machine learning aren't future technologies for Global Payments—they're current realities. The company processes billions of transactions that generate patterns invisible to human analysis but clear to algorithms. Fraud detection that once relied on simple rules now uses neural networks that learn and adapt in real-time. Customer service that required call centers is increasingly handled by AI agents that resolve issues before customers notice problems.

Embedded finance represents perhaps the biggest opportunity. Every software company wants to offer financial services—lending, insurance, payments—integrated into their platforms. Global Payments' combination of processing capabilities, regulatory expertise, and software integration positions them to power this transformation. Imagine construction management software that automatically finances equipment purchases, or healthcare platforms that instantly adjudicate insurance claims.

Under Cameron Bready's leadership, Global Payments has articulated clear strategic priorities: accelerate software-driven growth, expand international presence, complete the operational transformation, and maintain capital discipline. The company is betting that focus and execution matter more than grand visions in the pragmatic world of payments. The technology foundations are already in place. Global Payments' EVP of product, technology and enablement Adam Mitchell notes that generative AI will "help simplify important software integrations like shopping carts, CRMs, and email marketing tools," while enabling better fraud detection through synthetic examples that improve detection systems. As Chief Information Officer Guido Sacchi explains, "Generative AI is self-learning and offers improved predictive capabilities over time".

The key metrics to watch going forward tell the story of transformation: merchant retention rates (indicating platform stickiness), software revenue as a percentage of total revenue (validating the vertical strategy), adjusted operating margins (proving efficiency gains), and cross-sell penetration between merchant and issuer solutions (demonstrating platform synergies).

For long-term fundamental investors, Global Payments presents a fascinating case study in corporate evolution. This isn't a high-growth disruptor or a stable dividend aristocrat—it's a company in metamorphosis, shedding its processing past to emerge as a technology platform. The journey from that 2001 spin-off to today's global payments infrastructure demonstrates that in technology, the winners aren't always the flashiest innovators but often the disciplined executors who compound advantages over decades.

The payments industry will continue evolving at breakneck speed. New rails will emerge, regulations will shift, and customer expectations will rise. But companies that control the intersection of software and payments, that operate globally with local expertise, and that maintain the operational excellence to process billions of transactions flawlessly—these companies will endure.

Global Payments' story isn't finished. In many ways, with AI transformation, embedded finance opportunities, and global digital payment adoption still in early innings, the most interesting chapters may lie ahead. The company that began processing paper checks in the 1960s could well be processing virtual reality transactions in the metaverse by the 2030s.

The question for investors isn't whether Global Payments will survive—with its scale, diversification, and entrenchment in critical infrastructure, survival seems assured. The question is whether it can transform quickly enough to thrive in a world where every company is becoming a fintech, where payments are invisible, and where artificial intelligence makes decisions in microseconds.

That transformation is underway. Whether it succeeds will determine if Global Payments' next chapter rivals its remarkable past.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube