SYRMA SGS Technology: India's Electronics Manufacturing Services Champion

I. Introduction & Episode Roadmap

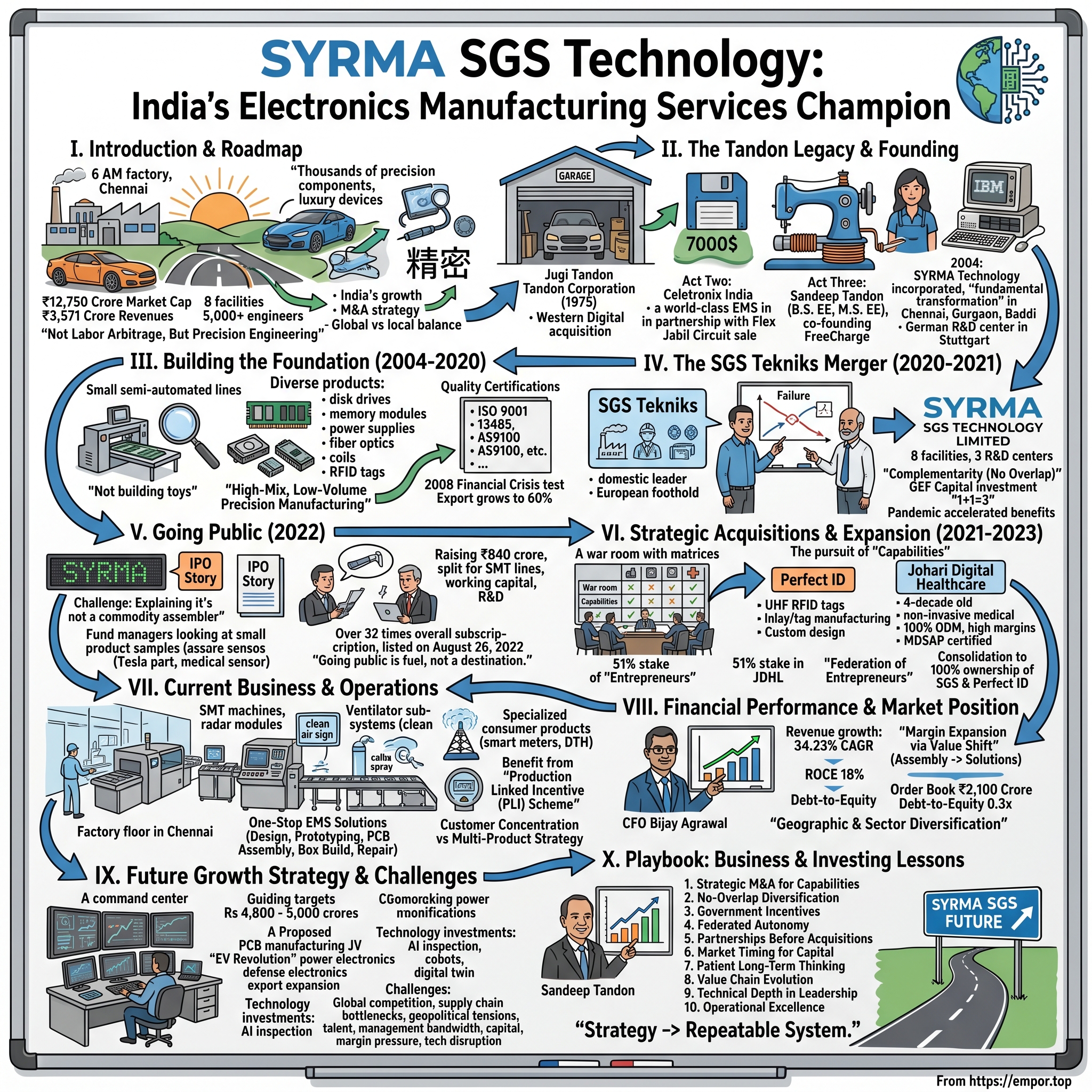

The morning shift at SYRMA's Chennai facility begins at 6 AM sharp. As the sun rises over the Bay of Bengal, thousands of precision components flow through automated surface-mount technology lines, destined for everything from German luxury cars to American medical devices. This isn't your typical Indian manufacturing story of labor arbitrage and cost-cutting. This is precision engineering at scale—where tolerances are measured in microns and quality failures are counted in parts per million.

Welcome to SYRMA SGS Technology, a company that most investors have never heard of, yet whose products touch billions of lives daily. With a market capitalization of ₹12,750 crore and annual revenues exceeding ₹3,571 crore, SYRMA has quietly built itself into India's electronics manufacturing services (EMS) powerhouse. The company operates eight state-of-the-art manufacturing facilities across India, employs over 5,000 engineers and technicians, and counts some of the world's most demanding OEMs as customers.

But here's the fascinating part: just two decades ago, this company didn't exist. The story of how a 2004 startup transformed into India's leading precision EMS player—navigating global supply chain disruptions, executing complex mergers, and riding the China-plus-one tailwind—offers profound lessons about building industrial capabilities in emerging markets.

This isn't just another contract manufacturer riding the "Make in India" wave. SYRMA represents something more ambitious: India's attempt to move up the electronics value chain from assembly to design, from commodity to precision, from follower to leader. The company's journey intersects with the broader narrative of India's manufacturing ambitions, the global realignment of supply chains, and the digital transformation of traditional industries.

Over the next several hours, we'll unpack how Sandeep Tandon—scion of one of India's most successful tech dynasties—built SYRMA through strategic acquisitions, operational excellence, and perfect timing. We'll explore the high-stakes SGS Tekniks merger that doubled the company's scale overnight, the calculated IPO that raised $100 million at the peak of market exuberance, and the targeted acquisitions in medical devices and RFID that positioned SYRMA for the next decade of growth.

This episode traces three interwoven narratives: First, the evolution of India's electronics manufacturing ecosystem from a backwater to a credible alternative to China. Second, the art and science of building capabilities through M&A in fragmented, technical markets. And third, the delicate balance between serving global customers who demand world-class quality while navigating the realities of operating in India's complex business environment.

We'll see how SYRMA navigated the shift from high-mix, low-volume precision manufacturing to scaled production, how it managed customer concentration risk while expanding into new verticals, and how it's positioning itself to capture the tailwinds from government incentives, supply chain diversification, and the electrification of everything.

The timing of this story matters. As global companies desperately seek alternatives to China, as India pushes its production-linked incentive schemes, and as industries from automotive to healthcare undergo massive electronic content inflation, SYRMA sits at the intersection of multiple powerful trends. Understanding this company means understanding the future of global electronics manufacturing.

But this isn't a victory lap. SYRMA faces intense competition from established global EMS giants, margin pressure from demanding customers, and the perpetual challenge of technology obsolescence. The company's relatively low return on equity of 9.21% over the past three years raises questions about capital efficiency. Customer concentration remains a concern, with significant revenue exposure to key accounts.

Our journey begins in 2004, but to truly understand SYRMA, we need to travel back further—to the 1970s, when a young Indian engineer named Sirjang Lal Tandon began building what would become one of the world's largest computer storage companies. The DNA of that original enterprise, its engineering culture, and its global ambitions would eventually manifest in SYRMA. This is a multi-generational story of Indian entrepreneurship, told through the lens of precision manufacturing.

II. The Tandon Legacy & Founding Context

The California sun beat down on Chatsworth in late 1975 when Sirjang Lal "Jugi" Tandon walked away from his comfortable engineering job at Pertec Inc. He had $7,000 in savings and a garage—the classic American startup cliché, except this time the protagonist was a mechanical engineer from Punjab who'd arrived in America fifteen years earlier with $3,000 and an outsized ambition. What Tandon built in that garage would eventually supply the sole floppy drives for every IBM PC and lay the foundation for one of India's most sophisticated electronics manufacturing dynasties.

The Tandon story isn't just about disk drives and semiconductors. It's about how a family of engineers turned India's labor cost advantages into precision manufacturing capabilities, how they rode successive waves of technology disruption, and how they ultimately created SYRMA SGS—a company that today manufactures everything from automotive radar systems to medical ventilators. This is a multi-generational saga of Indian technological ambition, told through the prism of one remarkable family.

Tandon Corporation, founded in 1975 and incorporated in 1976 as Tandon Magnetics Corp., originally produced magnetic recording read/write heads for the then-burgeoning floppy-drive market. Due to the labor-intensive nature of the product, production was carried out in low-wage India where production costs were lower. This was the key to the company's competitiveness. But here's what most people miss: the Tandons weren't just arbitraging labor costs. They were building something far more sophisticated.

Consider the manufacturing innovation that Manohar Lal "Manny" Tandon, Jugi's brother, implemented at Tandon Magnetics in Mumbai. He turned to avoiding hiring men in favor of a mostly female workforce after noticing high turnover costs. He then developed a relatively simple solution to meet IBM's rising demand: adapting a household sewing machine—a pedal-operated appliance most of his female workers were already familiar with. Mounting the sewing machine motor on a wooden block, he added a few enhancements, including an automatic counter to ensure the correct number of windings, as well as attaching a microscope to help the operator precisely wrap the smallest coils. This wasn't cheap labor—this was precision engineering achieved through ingenious adaptation.

Thanks to lower overhead costs and skilled, efficient manpower—or, more exactly, womanpower—Tandon Magnetics would provide IBM with top quality PC components at volumes up to 60,000 units per day at prices competitors simply couldn't match. By the early 1980s, Tandon would become the world's largest independent producer of disk drives for personal computers and word processors.

The pinnacle came in 1983 when the company's stock price hit $34.25—a staggering valuation for what had started as a garage operation just eight years earlier. But technology markets are unforgiving. A major decline in North American computer sales during 1984–85 as well as competition from Japanese and Taiwanese manufacturers proved difficult for the company. By 1988, recognizing the writing on the wall, Tandon sold its original data-storage business to Western Digital for nearly $80 million.

While Jugi Tandon's American venture was reaching its denouement, the Indian branch of the family was preparing for Act Two. In 2000, Manny Tandon launched something audacious: Celetronix India Pvt. Ltd., which became a company of Tandon Group and India's largest electronics manufacturing company. This wasn't just another contract manufacturer. Celetronix was India's first world-class EMS company, launched in partnership with Flex, one of the global giants of electronics manufacturing.

The Celetronix story deserves its own telling. Founded by the Tandon family, Celetronix had low-cost manufacturing facilities in India and delivered through its worldwide locations including India, US, Malaysia, Singapore and Sri Lanka. The company quickly established itself as a serious player, attracting blue-chip customers and eventually catching the eye of Jabil Circuit, another global EMS giant. In 2006, Jabil Circuit acquired Celetronix for around $185 million, including debt.

Enter the third generation: Sandeep Tandon, Manny's son. Sandeep Tandon, B.S. EE '90, M.S. EE '91, has immersed himself in the world of technology for more than two decades. His pedigree was impeccable—Bachelor of Science in Electrical Engineering from USC's Viterbi School of Engineering, and completion of the YPO Presidents' Program from Harvard Business School. But pedigree alone doesn't build companies.

After working as an application engineer for a Los Angeles startup, he launched his own accounts payable company, IQBackOffice, sold it in 2000, then returned to India to work for Celetronix. He examined the operations of Celetronix India until 2006 when it was sold to Jabil Circuits. The Jabil sale could have been an ending. For Sandeep, it was just the beginning.

In 2004, while still managing Celetronix, Sandeep had quietly incorporated a new company: SYRMA Technology. The timing wasn't coincidental. He could see that India's electronics manufacturing landscape was about to undergo a fundamental transformation. The country had the engineering talent, the cost advantages, and increasingly, the infrastructure. What it lacked was scale and sophistication. SYRMA would provide both.

The early years of SYRMA were deliberately low-profile. The company focused on electronic sub-assemblies and printed circuit board manufacturing—the unglamorous but essential building blocks of modern electronics. Operations commenced in Chennai, Gurgaon, and Baddi, with an R&D center established in Stuttgart, Germany. That German connection wasn't vanity—it was strategic. SYRMA wasn't competing on cost alone; it was building capabilities in high-mix, low-volume precision manufacturing, the kind of work that requires German-level engineering standards.

By 2010, SYRMA had evolved far beyond basic PCB assembly. The company was manufacturing disk drives, memory modules, power supplies, fiber optic assemblies, magnetic induction coils, and RFID products. The customer list was impressive but closely guarded. These weren't commodity buyers looking for the cheapest supplier—they were sophisticated OEMs who needed partners capable of managing complex, multi-stage manufacturing processes with near-zero defect rates.

The 2010s brought a new challenge and opportunity. Sandeep, ever the entrepreneur, had co-founded FreeCharge, India's fastest-growing mobile payment app, which he and Kunal Shah sold to Snapdeal in 2015 for $400 million. The FreeCharge success gave Sandeep capital and credibility, but more importantly, it gave him perspective on India's digital transformation. He could see that the convergence of electronics manufacturing and digital services would create unprecedented opportunities.

Meanwhile, in Gurgaon, another precision manufacturer was quietly building its own impressive capabilities. SGS Tekniks, founded by Jasbir Singh Gujral and his partners, had carved out a niche in the domestic market with a particular strength in industrial and medical electronics. Where SYRMA was strong in exports and had deep roots in South India, SGS Tekniks dominated in North India with an established foothold in European markets. The two companies had virtually no customer overlap—a fact that would soon become strategically significant.

By 2020, both companies faced a similar challenge: achieving scale in an increasingly consolidated global EMS industry. Separately, they were successful mid-sized players. Together, they could be something more. The merger negotiations that began in late 2020 weren't just about financial engineering—they were about creating India's first truly scaled precision EMS player. The combined entity would have revenues exceeding ₹1,000 crore, eight manufacturing facilities across India, and the customer diversity to weather any storm. This was industrial strategy at its finest, setting the stage for SYRMA SGS to emerge as a national champion in electronics manufacturing.

III. Building the Foundation: Early Years (2004-2020)

The Chennai facility in 2004 looked nothing like today's sprawling complex. SYRMA Technology's first manufacturing floor was 15,000 square feet of carefully controlled chaos—rows of semi-automatic pick-and-place machines, wave soldering equipment that required constant calibration, and quality control stations where operators peered through magnifying lenses, checking solder joints that would determine whether a satellite stayed in orbit or crashed to earth. This was where Sandeep Tandon's vision met the unforgiving reality of precision manufacturing.

"We're not building toys here," Sandeep would tell early employees, a phrase that became something of a company mantra. The statement carried weight because SYRMA's first major contracts weren't for consumer electronics where a 2% failure rate might be acceptable. The company was manufacturing electronic sub-assemblies for industrial automation systems, railway signaling equipment, and medical devices—applications where failure meant more than customer complaints. It could mean catastrophe.

The decision to establish operations across three locations—Chennai, Gurgaon, and Baddi—wasn't arbitrary. Each site offered distinct advantages. Chennai provided access to Southern India's established electronics ecosystem and proximity to ports for export. Gurgaon offered connectivity to North Indian industrial corridors and the National Capital Region's customer base. Baddi, in Himachal Pradesh, came with significant tax advantages and lower operational costs. But managing three facilities with different local regulations, labor pools, and infrastructure challenges required operational sophistication that most startups couldn't muster.

The masterstroke was establishing an R&D center in Stuttgart, Germany. This wasn't a token presence or a sales office masquerading as R&D. SYRMA hired serious German engineers who had worked at Bosch, Siemens, and other titans of German precision manufacturing. They brought with them not just technical expertise but something more valuable: the culture of German engineering, where tolerances aren't suggestions and quality control isn't a department but a philosophy.

Consider what SYRMA was attempting in those early years. The company was simultaneously manufacturing disk drives that required clean room environments and microscopic precision, memory modules where a single corrupted bit could crash an entire system, and power supplies that needed to maintain voltage stability across extreme temperature ranges. Each product category demanded different equipment, different skills, different quality protocols. Most companies spent decades mastering one category. SYRMA was attempting to master them all within its first decade.

The evolution into magnetic induction coils revealed SYRMA's strategic thinking. These components—essential for everything from electric vehicle charging to industrial heating—required a completely different manufacturing paradigm. Where PCB assembly was about placing components with robotic precision, coil winding was about controlling tension, maintaining exact spacing, and managing magnetic field interactions. SYRMA didn't just buy winding equipment; the company adapted techniques from the original Tandon Magnetics playbook, where high-precision equipment based upon revamped sewing machines remained a cornerstone at their 100,000 square foot state-of-the-art flagship facility in Chennai.

The RFID products represented another leap in complexity. Radio-frequency identification wasn't just about manufacturing; it was about understanding electromagnetic propagation, encryption protocols, and the intersection of hardware and software. SYRMA's RFID tags weren't generic products sold through distributors. They were custom-designed solutions for specific applications: tracking medical equipment in hospitals, managing inventory in automotive plants, securing access to data centers. Each application required different frequencies, different read ranges, different environmental tolerances.

By 2010, SYRMA had developed a unique capability that set it apart from both low-cost assemblers and high-end specialists: high-mix, low-volume precision manufacturing. This meant the company could profitably produce 500 units of a specialized medical device in the morning and switch to 1,000 units of an automotive sensor in the afternoon. The flexibility required sophisticated planning systems, cross-trained workers, and equipment that could be rapidly reconfigured. It was manufacturing as jazz improvisation rather than classical symphony.

The customer acquisition strategy during these years was deliberately conservative. SYRMA didn't chase volume for volume's sake. Instead, the company targeted customers who valued precision over price, who needed partners rather than vendors. A typical early customer might be a German industrial equipment manufacturer who needed 2,000 specialized control boards per month, each with unique firmware configurations, delivered with 99.98% quality rates and exact-sequence delivery for just-in-time assembly. These weren't the kinds of orders that showed up on Alibaba.

The financial discipline during this period was remarkable. While contemporary Indian startups were burning through venture capital in pursuit of growth at any cost, SYRMA was building steadily, reinvesting profits, avoiding excessive leverage. The company's working capital management was particularly sophisticated—negotiating favorable payment terms with suppliers while maintaining fast collections from customers, creating a negative working capital cycle that funded growth without external capital.

The human capital development was equally strategic. SYRMA didn't just hire operators; it created an academy system where workers could progress from basic assembly to complex troubleshooting to process engineering. The company sent promising engineers to customers' facilities in Europe and America, not just for training but for cultural immersion. They returned understanding not just how to build products but why specifications existed, what failures meant in real-world applications, how their work fit into larger systems.

Quality certifications accumulated like military medals: ISO 9001 for quality management, ISO 14001 for environmental management, ISO 13485 for medical devices, AS9100 for aerospace, TS 16949 for automotive. Each certification required months of preparation, detailed documentation, rigorous audits. But they weren't just wall decorations. They were passports to global supply chains, proof that an Indian company could meet the same standards as established players in developed markets.

The 2008 financial crisis tested SYRMA's resilience. Orders evaporated overnight as customers slashed inventory and delayed product launches. Lesser companies might have panicked, cut staff, compromised quality to reduce costs. SYRMA did the opposite. The company used the downturn to upgrade equipment, cross-train workers, strengthen supplier relationships. When recovery came in 2010, SYRMA was positioned to capture share from competitors who had cut too deep.

By 2015, the company had achieved something remarkable: consistent profitability with virtually no external funding. Revenues had grown from essentially zero to over ₹300 crore. The company operated 500,000 square feet of manufacturing space across its facilities. But more importantly, SYRMA had built intangible assets that wouldn't show up on any balance sheet: deep customer relationships, proven operational excellence, and the ability to manage complexity at scale.

The period from 2015 to 2020 marked a subtle but important shift. SYRMA began winning larger contracts, moving from being a secondary supplier to primary partner for key customers. The company started manufacturing complete sub-systems rather than just components. A railway equipment manufacturer who had previously bought PCBs from SYRMA now contracted the company to build entire signaling modules. A medical device company moved from component sourcing to full box-build assembly.

The export percentage grew steadily, reaching 60% of revenues by 2020. But this wasn't just labor arbitrage—Indian workers assembling products designed elsewhere. SYRMA's Stuttgart R&D center was now co-developing products with customers, suggesting design modifications that improved manufacturability, reduced costs, enhanced reliability. The company had evolved from manufacturer to manufacturing partner to innovation collaborator.

As 2020 began, SYRMA was a successful mid-sized EMS player with strong capabilities and steady growth. But Sandeep Tandon knew that success in the electronics manufacturing industry was like swimming against a current—you needed to move forward just to stay in place. The industry was consolidating globally. Customers wanted fewer, larger suppliers who could provide global scale, financial stability, and end-to-end capabilities. SYRMA needed to transform from a strong regional player to a national champion. The path to that transformation would require bold moves that would test everything the company had built over the previous sixteen years.

IV. The SGS Tekniks Merger: Creating Scale (2020-2021)

The first meeting between Sandeep Tandon and Jasbir Singh Gujral took place not in a boardroom but at an industry conference in Bangalore in early 2020, just weeks before COVID-19 would shut down the world. They were watching a presentation about Industry 4.0 when Gujral leaned over and whispered, "All this automation is impressive, but someone still needs to understand why a solder joint failed at -40°C." That comment sparked a conversation that would eventually reshape Indian electronics manufacturing.

SGS Tekniks was everything SYRMA wasn't, and that was precisely the point. Where SYRMA had built its reputation on exports and cutting-edge consumer electronics, SGS Tekniks had quietly dominated the unglamorous but lucrative world of industrial electronics for the domestic market. Founded by Gujral, one of the founding promoters of SGS Tekniks Manufacturing Pvt Ltd, the company had spent two decades perfecting the art of building electronics that could survive Indian conditions—extreme heat, monsoon humidity, dust storms, and power fluctuations that would destroy ordinary circuits.

The numbers told a compelling story. SGS Tekniks was generating over ₹600 crore in annual revenues with EBITDA margins that consistently exceeded 12%—remarkable for a company that most industry observers had never heard of. Their customer list read like a who's who of Indian industrial giants: Larsen & Toubro, Bharat Heavy Electricals, Indian Railways. But what really caught Sandeep's attention was SGS's European foothold—a small but highly profitable operation serving German Mittelstand companies that valued reliability over rock-bottom prices.

The pandemic accelerated conversations that might have taken years. As global supply chains fractured and companies desperately sought to diversify away from China, both SYRMA and SGS Tekniks saw unprecedented opportunity. But they also recognized a harsh truth: the global EMS industry was consolidating rapidly. Foxconn had revenues exceeding $180 billion. Flex and Jabil each topped $25 billion. Even second-tier players were multi-billion dollar enterprises. In this landscape, a ₹300-600 crore company was a rounding error.

The merger negotiations that began in earnest in September 2020 were unlike typical Indian M&A discussions. There was no prolonged dancing around valuation, no ego-driven power plays, no last-minute demands. Both sides understood they were stronger together. The complementarity was almost too perfect to be accidental. SYRMA strong in South India, SGS Tekniks in the North. SYRMA focused on exports, SGS on domestic. SYRMA excelling in consumer and automotive, SGS in industrial and infrastructure. No customer overlap meant no integration conflicts.

The financial engineering was elegant. Rather than a cash acquisition that would have strained balance sheets, they structured it as a merger with stock swaps based on relative valuations. The combined entity would have revenues exceeding ₹1,000 crore, immediately making it one of India's largest independent EMS companies. But size was just the beginning. The real value lay in capabilities: eight manufacturing facilities providing geographic redundancy, three R&D centers spanning Chennai, Gurgaon, and Stuttgart, and a customer base diversified across industries and geographies.

GEF Capital, a private equity firm that had been watching the Indian EMS space, saw the opportunity immediately. They committed to a significant investment, providing not just capital but credibility. Their due diligence process, typically a months-long ordeal, was completed in six weeks. "We've looked at dozens of EMS companies," a GEF partner later revealed. "This was the first time we saw two companies where one plus one genuinely equaled three."

The integration planning revealed just how thoughtfully both companies had been built. Their enterprise resource planning systems, while different, used compatible data structures. Their quality certifications overlapped but weren't redundant—SYRMA's medical device certifications complemented SGS's railway and industrial certifications. Even their company cultures, while distinct, shared core values around quality, customer focus, and engineering excellence.

But the real masterstroke was the decision to maintain operational independence while integrating strategic functions. Each facility would continue serving its existing customers without disruption. Sales teams wouldn't be merged immediately. Even the brands would coexist for a transition period. This wasn't corporate timidity—it was recognition that in precision manufacturing, customer relationships and operational knowledge matter more than organizational charts.

The manufacturing synergies emerged faster than anyone expected. SYRMA's expertise in surface-mount technology helped SGS improve yields on complex industrial boards. SGS's experience with harsh-environment electronics helped SYRMA win automotive contracts that required products to survive under-hood conditions. The Stuttgart R&D center, previously focused solely on SYRMA projects, began working with SGS's European customers, opening doors that had been closed to an "unknown Indian supplier."

The pandemic, rather than derailing the merger, accelerated its benefits. When SYRMA's Chennai facility was locked down during the Delta wave, SGS's northern facilities picked up critical orders. When semiconductor shortages hit SGS's automotive customers, SYRMA's supplier relationships helped secure allocations. The combined entity's larger scale gave it negotiating power with component suppliers that neither company had possessed independently.

The cultural integration proved surprisingly smooth, perhaps because both companies had been built by engineers who valued substance over style. The first combined management meeting featured none of the PowerPoint pageantry typical of corporate India. Instead, Gujral and Tandon spent three hours at a whiteboard, sketching out manufacturing flows, debating quality protocols, arguing about the optimal reflow temperature for lead-free solder. "It was like watching two master chefs argue about recipes," recalled one attendee. "Technical, passionate, but ultimately collaborative."

The talent retention was remarkable. In an industry where 20% annual attrition was standard, the merged entity lost fewer than 5% of key personnel in the first year. Part of this was timing—the pandemic had made everyone value stability. But it also reflected thoughtful integration. Rather than redundancies and relocations, the merger created opportunities. An engineer specializing in power electronics at SGS could now work on electric vehicle projects at SYRMA. A quality manager at SYRMA could apply automotive standards to industrial products at SGS.

The customer response exceeded expectations. Large multinationals who had hesitated to work with smaller Indian suppliers now saw a partner with scale and stability. A major American medical device company that had been evaluating SYRMA for two years signed a multi-year contract within months of the merger announcement. A European automotive tier-one supplier expanded their relationship from one facility to three. Even competitors privately acknowledged that the merger had created a formidable player.

By early 2021, the integration was largely complete. The combined entity—now officially renamed SYRMA SGS Technology Limited—had revenues approaching ₹1,500 crore on an annualized basis. More importantly, it had achieved critical mass in key verticals. In medical electronics, the company could now offer everything from PCB assembly to complete device manufacturing. In automotive, it could handle both entertainment systems and safety-critical components. In industrial, it could serve everyone from startups building IoT sensors to conglomerates needing thousand-unit batches of specialized controllers.

The timing for the next phase couldn't have been better. The Indian government had just announced the Production Linked Incentive scheme for electronics manufacturing. Global companies were accelerating their China-plus-one strategies. The electric vehicle revolution was creating demand for entirely new categories of electronic components. And Indian capital markets were in the midst of an unprecedented bull run, with investors desperately seeking quality companies with growth potential. SYRMA SGS had spent seventeen years building capabilities and one transformative year achieving scale. Now it was time to access the capital that would fuel the next phase of growth. The stage was set for one of the most successful IPOs in Indian manufacturing history.

V. Going Public: The IPO Story (2022)

The Morgan Stanley offices in Mumbai's Bandra-Kurla Complex hummed with nervous energy on the morning of March 15, 2022. Investment bankers who had shepherded dozens of IPOs could sense something different about this one. The previous six months had seen a parade of new-age tech companies go public with astronomical valuations and negligible profits. Zomato, Paytm, PolicyBazaar—the market had embraced them all, at least initially. But SYRMA SGS was different. This was a company that actually manufactured things, generated real profits, and served customers who measured quality in parts per million rather than app downloads.

"The challenge," Sandeep Tandon told the assembled bankers during the first IPO planning meeting, "is that nobody understands what we actually do. They hear 'electronics manufacturing' and think we're a commodity assembler competing with Chinese sweatshops. How do we explain that we're building components for German cars and American medical devices?"

The timing for the IPO was both perfect and precarious. Perfect because Indian capital markets were witnessing unprecedented retail participation, with millions of new demat accounts opened during the pandemic. Precarious because global markets were showing signs of fatigue, with inflation fears and Federal Reserve tightening creating volatility. The window might not stay open long.

The decision to raise ₹840 crore wasn't pulled from thin air. SYRMA SGS had meticulously calculated its capital requirements: ₹300 crore for new manufacturing lines, ₹200 crore for working capital to support growth, ₹150 crore for R&D and capability building, and the remainder for strategic flexibility. This wasn't growth capital for growth's sake—every rupee was allocated to specific opportunities with identified customers and projected returns.

The equity story that emerged was compelling. India's electronics manufacturing opportunity was projected to grow from $75 billion to $300 billion by 2026. The government's PLI scheme provided tangible incentives for domestic manufacturing. Global supply chain diversification was no longer optional but imperative. And SYRMA SGS was one of the few Indian companies with the scale, capabilities, and track record to capture this opportunity. The bankers had their narrative.

The roadshow that began in late June 2022 was a masterclass in investor education. Rather than PowerPoint slides filled with hockey-stick projections, Sandeep and his team brought actual products. They showed fund managers a thumbnail-sized component that went into every Tesla Model 3. They demonstrated a medical device sensor that could detect COVID antibodies in twelve seconds. They explained how their magnetic coils enabled wireless charging for the latest smartphones. Suddenly, abstract discussions about "precision manufacturing" became tangible.

The institutional response was encouraging but cautious. Foreign funds appreciated the China-plus-one thesis but worried about execution. Domestic institutions liked the manufacturing story but questioned whether margins could be maintained as the company scaled. Retail investors, surprisingly, proved most enthusiastic. Perhaps it was the Modi government's "Make in India" campaign, or fatigue with loss-making tech unicorns, but individual investors saw SYRMA SGS as a bet on India's manufacturing future.

The pricing discussions revealed the delicate balance required in Indian IPOs. Price too high, and the issue might fail, destroying credibility. Price too low, and you leave money on the table while creating a perception of desperation. The bankers recommended a price band of ₹195-210 per share, valuing the company at roughly ₹3,500 crore pre-money. Sandeep pushed for ₹210-220, arguing that quality deserved a premium. They settled on ₹209-220, with the final price to be determined through book building.

The prospectus, filed in July 2022, was a 400-page testament to transparency. Every risk was disclosed, from customer concentration to currency fluctuations to competition from established global players. But buried in the dense text were nuggets that revealed SYRMA SGS's true potential. The company's return on capital employed had improved from 12% to 18% over three years. Customer stickiness was exceptional, with the top ten customers having average relationships exceeding seven years. The order book provided visibility for the next eighteen months.

The subscription period in August 2022 coincided with one of the most volatile weeks in global markets. The Federal Reserve had just delivered another aggressive rate hike. Chinese lockdowns were disrupting supply chains. The Russia-Ukraine conflict was escalating. On the first day, subscription was just 0.4 times, causing minor panic among the underwriters. "Should we extend the price band?" asked one banker. Sandeep's response was characteristic: "We've built this company for seventeen years. We can wait three more days."

His confidence proved justified. By day two, institutional investors who had been waiting on the sidelines began placing orders. A major Singaporean sovereign wealth fund subscribed for 5% of the institutional quota. Domestic mutual funds, sensing foreign interest, increased their bids. By the final day, the institutional portion was subscribed 38 times, the retail portion 12 times, and overall subscription exceeded 32 times. The final price was fixed at ₹220, the top of the band.

The listing day, August 26, 2022, saw SYRMA SGS open at ₹261, an 18.6% premium to the issue price. By noon, it had touched ₹285, giving the company a market capitalization exceeding ₹5,000 crore. More importantly, the stock held its gains, closing the first week above ₹270. This wasn't just paper wealth—it was validation that public markets understood and valued what SYRMA SGS had built.

The immediate impact of the IPO went beyond capital raising. Customers who had been hesitant about working with a private Indian company now saw a listed entity with public scrutiny and governance standards. Suppliers offered better terms, knowing SYRMA SGS had the balance sheet to honor commitments. Employees holding stock options suddenly realized their paper wealth had become real. The company received over 10,000 job applications in the month following the listing, including senior executives from multinational competitors.

The capital deployment began immediately. The first new SMT line was ordered from Panasonic within weeks of the IPO, with delivery scheduled for the Chennai facility. Land was acquired adjacent to the Manesar plant for a new 200,000 square foot facility focused on automotive electronics. The Stuttgart R&D center doubled its headcount, hiring specialists in artificial intelligence and sensor fusion. These weren't speculative investments—each had identified customers and projected payback periods under three years.

The quarterly results following the IPO validated investor confidence. Q3 FY2023 showed revenue growth of 42% year-over-year, with EBITDA margins expanding to 14.2%. The order book swelled to ₹2,100 crore, providing visibility well into FY2024. New customer wins included a major European automotive OEM and an American medical device giant. The stock responded, touching ₹400 by December 2022, nearly doubling from the IPO price.

But Sandeep wasn't celebrating. He had seen too many Indian companies become complacent after successful IPOs, focusing more on quarterly earnings calls than operational excellence. In a company-wide email following the first post-IPO board meeting, he wrote: "Going public was not the destination. It was acquiring fuel for a much longer journey. Every employee must remember: we're not in the business of managing stock prices. We're in the business of manufacturing products where failure is not an option."

The governance changes following the IPO were substantial but necessary. Independent directors with deep industry experience joined the board. Quarterly audits replaced annual reviews. A whistleblower mechanism was established. ESG reporting became mandatory. Some old-timers grumbled about bureaucracy, but Sandeep saw it differently. "Transparency and governance aren't constraints," he told the management team. "They're competitive advantages. When a German automotive company is choosing between us and a Chinese competitor, our governance standards matter as much as our manufacturing capabilities."

As 2022 drew to a close, SYRMA SGS had successfully transformed from a private, closely-held company to a public corporation with over 50,000 shareholders. The IPO had raised not just capital but credibility. It had created not just wealth but responsibility. Most importantly, it had positioned the company for its next phase of growth—one that would require strategic acquisitions to build new capabilities and enter new verticals. The capital was in place, the governance structure established, and the market understood the story. Now it was time to go shopping.

VI. Strategic Acquisitions & Expansion (2021-2023)

The conference room at SYRMA SGS's Chennai headquarters in early 2021 had the energy of a war room. Whiteboards covered every wall, filled with M&A targets categorized by capability, geography, and strategic fit. Sandeep Tandon stood before a matrix that plotted potential acquisitions on two axes: strategic value and integration complexity. In the upper right quadrant—high value, high complexity—sat two names that would define SYRMA SGS's next phase: Perfect ID and Johari Digital Healthcare.

"We're not shopping for revenues," Sandeep told his M&A team. "We're shopping for capabilities we can't build fast enough ourselves. Every acquisition must open doors that would otherwise take us five years to unlock."

The pursuit of Perfect ID began almost accidentally. During a customer visit to demonstrate automotive sensors, the client mentioned their struggle with RFID implementation for supply chain tracking. "You should talk to Perfect ID," the procurement manager said offhandedly. "They're the only Indian company we've found who really understands UHF RFID at scale."

Perfect ID was an ISO 9001 certified company and Global leader for design and manufacture of RFID tags. Founded years earlier, the company had quietly built capabilities across the entire RFID spectrum—low frequency for animal tracking, high frequency for payment cards, ultra-high frequency for supply chain management, and NFC for consumer applications. But what really caught SYRMA's attention was their manufacturing sophistication. Perfect RFID had a fully automated state-of-art manufacturing facility for the manufacture of Inlays and Tags.

The initial meeting with Perfect ID's founders revealed a company at an inflection point. They had the technology, the customers, and the certifications. What they lacked was scale and capital to capture the explosive growth in RFID adoption driven by e-commerce, asset tracking, and supply chain digitization. The Indian RFID market alone was projected to grow from $500 million to $2 billion by 2025. Perfect ID had the capability to capture this growth but not the resources.

The due diligence process uncovered gems. More than 90% of Perfect ID's products were custom designed led by experienced RFID engineers & specialists and had successfully produced for more than 200 customers globally. This wasn't commodity manufacturing—it was sophisticated engineering. Each customer required different frequencies, read ranges, environmental tolerances, and form factors. A tag for tracking jewelry in a retail store had completely different requirements than one tracking automotive parts through a paint shop at 180°C.

The negotiation was surprisingly straightforward. Perfect ID's founders recognized that independence meant irrelevance in a consolidating market. SYRMA offered not just a premium valuation but something more valuable: access to its customer base. Every automotive manufacturer needed RFID for parts tracking. Every medical device company needed it for inventory management. Every industrial customer needed it for asset monitoring. The synergies were obvious and immediate.

The Perfect ID acquisition, completed in 2021, was deliberately low-profile. No press releases, no analyst calls. SYRMA wanted to integrate the company quietly, learn the business, understand the technology before making bold claims. Within six months, the wisdom of this approach became clear. RFID wasn't just a product—it was a gateway technology that opened conversations with CTOs and supply chain heads who had never heard of SYRMA SGS.

But the real prize was still to come. In early 2023, SYRMA's investment bankers brought an opportunity that seemed almost too good to be true: Johari Digital Healthcare Limited was exploring strategic options. This wasn't just another medical device assembler. Johari Digital Healthcare Ltd ("JDHL") was a 4-decade-old company that had built a reputation as a designer and manufacturer of non-invasive medical devices.

The first meeting with Satyendra Johari, the company's founder-chairman, took place at JDHL's facility in Gurgaon. Walking through the manufacturing floor was like entering a different world. Engineers in lab coats huddled around prototypes of next-generation diagnostic equipment. The testing lab contained millions of dollars of equipment—environmental chambers simulating everything from Himalayan cold to Saharan heat, EMC testing facilities that could detect electromagnetic interference down to microvolts, biocompatibility testing setups that ensured materials wouldn't cause allergic reactions.

The numbers were staggering. JDHL's last three years' turnover showed explosive growth: 2020-21: INR 490 MN, 2021-22: INR 911 MN, 2022-23: INR 1,628 MN. Net profit in 2022-23 was INR 435 MN. But what really impressed SYRMA's team was the margin profile. Johari Digital was a 100 percent original design manufacturer (ODM) and had a margin of more than 35 percent.

This wasn't just contract manufacturing—JDHL was designing products from scratch for global medical device companies. A European aesthetic device company would approach them with a concept for a new laser treatment system. JDHL would handle everything: industrial design, electronics engineering, software development, regulatory submissions, clinical trials support, and finally, manufacturing. The customer got a turnkey product without building internal capabilities. JDHL got margins that reflected the value of innovation, not just assembly.

The regulatory moat was formidable. JDHL's state-of-the-art facility complied with ISO 13485:2016, ISO 27001:2022, MDSAP and US FDA GMP. The MDSAP (Medical Device Single Audit Program) certification was particularly valuable—it meant a single audit could satisfy regulatory requirements for the US, Canada, Brazil, Australia, and Japan. For a global medical device company, this eliminated enormous complexity and risk.

The negotiation for JDHL was more complex than Perfect ID. This was a crown jewel asset with multiple suitors. Private equity firms saw a platform for medical device roll-ups. Strategic buyers saw instant access to the lucrative aesthetic medicine market. But SYRMA had advantages. Unlike financial buyers, they could offer operational synergies. Unlike strategic buyers, they wouldn't subsume JDHL's identity or relocate key personnel.

SYRMA SGS Technology completed acquisition of 51% stake in Johari Digital Healthcare (JDHL) for a consideration of Rs 229.50 crore. JDHL had a strong reputation as an end-to-end design-focused manufacturer of electro-medical devices, focusing on therapeutic areas such as aesthetics, diagnostics, physiotherapy, life sciences among others. The structure was clever—51% gave SYRMA control while leaving the founders with 49% to ensure continued engagement and alignment.

Sandeep Tandon, Chairman, Syrma SGS said, "This partnership is a strategic fit for us, as it aligns with our vision of foraying into fast growing medical devices segment. JDHL has a proven track record of delivering innovative and high-quality products to its customers, and we look forward to leveraging their design capability will expand Syrma's ODM skills in the high-growth medical electronics space."

The market response was immediate and enthusiastic. Shares of Syrma SGS Technologies Limited climbed over 8 percent to Rs 585 on September 6 after the company acquired 51 percent stake in Johari Digital Healthcare Limited (JDHL). Analysts who had been skeptical about SYRMA's ability to move up the value chain suddenly saw a company that could design and manufacture complex medical devices for global markets.

The integration of JDHL revealed unexpected synergies. JDHL's design capabilities could be applied to SYRMA's automotive customers who needed medical-grade reliability for autonomous driving sensors. SYRMA's manufacturing scale could reduce JDHL's costs while maintaining quality. The combined entity could now offer medical device companies everything from concept to production, from component to complete device, from prototype to mass manufacturing.

By late 2023, SYRMA also moved to consolidate its ownership structure. The company acquired 100% of SGS Tekniks and Perfect ID, making them wholly-owned subsidiaries. This wasn't just financial engineering—it was about creating a unified company with aligned incentives and integrated operations. The minority shareholders were bought out at fair valuations, eliminating potential conflicts and simplifying governance.

The strategic logic of the acquisitions became clear when viewed holistically. Perfect ID brought RFID capabilities essential for Industry 4.0 and supply chain digitization. JDHL brought medical device design and manufacturing capabilities for the rapidly growing healthcare market. Together with SYRMA SGS's existing capabilities in automotive, industrial, and consumer electronics, the company now had a portfolio that touched every major growth segment in electronics.

The cultural integration was managed with unusual sensitivity. Rather than imposing SYRMA's culture on the acquired companies, Sandeep encouraged a "federation of entrepreneurs" model. Each business maintained its identity, customer relationships, and operational autonomy while benefiting from shared resources, cross-selling opportunities, and financial strength. The monthly leadership meetings became forums for sharing best practices rather than corporate command-and-control sessions.

The human capital retained through these acquisitions was perhaps more valuable than the physical assets. JDHL brought doctors and biomedical engineers who understood FDA regulations and clinical requirements. Perfect ID brought RF engineers who could design antennas for challenging environments. These weren't capabilities that could be hired from the market—they required years of experience and deep domain knowledge.

As 2023 drew to a close, SYRMA SGS had transformed from a precision electronics manufacturer to a diversified technology company. The acquisitions had added over ₹2,000 crore to the revenue run rate, expanded margins through higher value-added products, and opened entirely new customer segments. But more importantly, they had positioned the company for the next decade of growth in medical devices, RFID, and other high-growth segments. The acquisition spree was over. Now came the harder task: delivering on the promise of integration and growth.

VII. Current Business & Operations

The 5:30 AM shift change at SYRMA SGS's Chennai facility resembles a small city coming to life. Over 2,000 workers stream through biometric gates, past the "Zero Defect" banners written in Tamil, Hindi, and English. In the surface-mount technology hall, million-dollar Panasonic NPM-W2 machines place components smaller than grains of sand at speeds exceeding 100,000 components per hour. The precision is staggering—placement accuracy of ±25 microns, less than half the width of a human hair. This is modern electronics manufacturing: part semiconductor fab, part automotive plant, part software development center.

Today, SYRMA SGS serves a customer base that reads like a who's who of global industry. The company is a technology-focused engineering and design company engaged in turnkey electronics manufacturing services (EMS), specialising in precision manufacturing for diverse end-use industries, including industrial appliances, automotive, healthcare, consumer products and IT industries. But these categories barely scratch the surface of the complexity.

In the automotive section, engineers huddle around a new radar module for an advanced driver-assistance system. The module must survive under-hood temperatures of 125°C, vibrations that would destroy consumer electronics, and electromagnetic interference from dozens of nearby systems. It must work flawlessly for fifteen years or 300,000 kilometers. A failure doesn't mean a customer complaint—it could mean a fatal accident. The testing protocol runs 1,200 hours, simulating everything from Death Valley heat to Siberian cold, from German Autobahn speeds to Indian pothole impacts.

Twenty meters away, in a climate-controlled clean room, technicians in bunny suits assemble medical ventilator sub-systems. The pandemic taught the world that ventilators save lives, but few understand the complexity involved. Each unit contains over 3,000 components, sophisticated software that must respond to patient breathing patterns in milliseconds, and redundancy systems that ensure operation even if primary systems fail. SYRMA SGS doesn't just assemble these devices—the company manages the entire supply chain, from sourcing medical-grade components to ensuring batch traceability for FDA compliance.

The railway electronics division occupies its own building, a testament to the unique requirements of this sector. Indian Railways operates the world's fourth-largest rail network, with trains running through deserts where sand infiltrates everything, coastal areas where salt corrosion destroys ordinary electronics, and mountains where temperature swings of 40°C in a single day are common. The signaling systems SYRMA manufactures must work perfectly for decades with minimal maintenance. A signaling failure doesn't just delay trains—it risks catastrophic collisions.

But it's in the consumer electronics section where the company's evolution becomes most apparent. SYRMA isn't manufacturing smartphones or laptops—markets dominated by massive ODMs in China and Taiwan. Instead, the company focuses on specialized consumer products where Indian manufacturing makes strategic sense. Smart meters that monitor electricity consumption in real-time, set-top boxes customized for Indian DTH operators, wireless earbuds for premium audio brands. Each product category chosen for specific reasons: technical complexity that justifies higher margins, customization requirements that favor local manufacturing, or supply chain advantages from proximity to customers.

The one-stop EMS solutions that SYRMA offers go far beyond simple assembly. Product design begins in the R&D centers where engineers use sophisticated CAD software to optimize designs for manufacturability. Quick prototyping leverages 3D printing and rapid PCB fabrication to move from concept to working prototype in days rather than months. PCB assembly ranges from simple single-sided boards to complex 32-layer HDI boards with blind and buried vias. Box build integrates electronics with mechanical assemblies, creating complete products ready for retail. The repair and rework capability means products can be refurbished rather than scrapped, critical for expensive industrial equipment. Automatic tester development creates custom testing solutions that verify product functionality at production speeds.

The government's Production Linked Incentive (PLI) Scheme has transformed the economics of Indian electronics manufacturing. SYRMA SGS benefits from incentives for IT hardware manufacturing, receiving cash incentives of 4% of incremental sales over base year. But the real value isn't just the direct incentive—it's the ecosystem development. Component suppliers are setting up Indian operations to serve PLI beneficiaries. Global customers are more willing to consider Indian suppliers knowing government support ensures long-term viability. The entire industry is moving up the value chain, from simple assembly to complex manufacturing.

The R&D capabilities deserve special attention. The Stuttgart center, once a small outpost, now employs over 50 engineers working on next-generation technologies. They're developing AI algorithms for predictive maintenance of industrial equipment, sensor fusion systems for autonomous vehicles, and wireless power transmission for medical implants. This isn't incremental improvement—it's fundamental innovation that positions SYRMA SGS as a technology partner rather than just a manufacturing vendor.

The innovation extends to manufacturing processes themselves. SYRMA has developed proprietary techniques for handling ultra-fine pitch components, methods for reducing solder defects in lead-free processes, and algorithms for optimizing production scheduling across multiple product lines. Each innovation might save only seconds per unit or reduce defects by fractions of a percent, but across millions of units, the impact is transformative.

Customer concentration remains a strategic focus. While the top ten customers contribute significant revenue, SYRMA has deliberately diversified within each customer relationship. A single automotive customer might have SYRMA manufacturing infotainment systems in Chennai, sensors in Manesar, and control modules in Baddi. This multi-product, multi-location strategy creates switching costs that make customer relationships sticky while reducing risk from any single product line.

The working capital management in this business is particularly complex. Electronic components must be ordered months in advance, especially during the ongoing semiconductor shortage. Finished goods inventory must be minimized because electronic products lose value rapidly. Customer payment terms vary from 30 days for small Indian companies to 120 days for large multinationals. SYRMA manages this complexity through sophisticated ERP systems that provide real-time visibility into inventory levels, production schedules, and cash flows.

Quality control permeates every aspect of operations. Incoming components undergo automated optical inspection and electrical testing. In-circuit testing verifies that boards are assembled correctly. Functional testing ensures products meet specifications. Environmental stress screening weeds out early failures. Statistical process control identifies trends before they become problems. The result: defect rates measured in parts per million, not percentages.

The manufacturing footprint continues to expand strategically. Each facility specializes in different capabilities: Chennai for high-volume consumer electronics, Manesar for automotive, Baddi for industrial, the JDHL facility for medical devices. This specialization allows each site to optimize for its specific requirements while sharing best practices across the network. New capacity additions are carefully planned based on confirmed customer commitments rather than speculative demand.

The supply chain orchestration required to run this operation is staggering. SYRMA sources from over 500 component suppliers globally, manages inventory worth hundreds of crores, coordinates logistics across multiple countries, and ensures just-in-time delivery to customers. During the COVID disruptions and subsequent semiconductor shortage, this supply chain capability became a competitive differentiator. While competitors struggled with component availability, SYRMA's relationships and financial strength secured allocations.

The environmental and sustainability initiatives go beyond compliance. SYRMA has invested in solar power generation, achieving 30% renewable energy usage across facilities. Water recycling systems reduce consumption by 40%. Lead-free soldering processes, though more technically challenging, eliminate toxic materials. Electronic waste is properly recycled through certified vendors. These initiatives matter not just for corporate responsibility but because global customers increasingly demand sustainable supply chains.

As we survey SYRMA SGS's current operations, what emerges is a company that has successfully bridged the gap between Indian cost advantages and global quality standards. This isn't the India of call centers and back-office operations. This is sophisticated manufacturing that requires deep technical knowledge, operational excellence, and constant innovation. The company has built capabilities that take decades to develop and can't be easily replicated. But with great capability comes great challenges, and the path forward requires navigating an increasingly complex competitive landscape.

VIII. Financial Performance & Market Position

The numbers tell a story of transformation, but you have to know how to read them. When CFO Bijay Agrawal presents SYRMA SGS's quarterly results, institutional investors lean forward, parsing every metric for signs of sustainable growth versus temporary tailwinds. The headline figures are impressive: market capitalization of ₹12,750 crore, revenues of ₹3,571 crore, profit after tax of ₹214 crore. But in electronics manufacturing, where gross margins can range from 8% to 40% depending on value addition, the details matter more than the headlines.

The company's 75% increase in operating EBITDA and 145% rise in profit after tax reflect more than just revenue growth. This is margin expansion driven by a fundamental shift in business mix. Five years ago, SYRMA primarily assembled PCBs for other companies' products—a respectable business but one with inherent margin limitations. Today, the company designs products, manages supply chains, and delivers complete solutions. Each step up the value chain adds a few percentage points of margin, compounding into transformation.

The revenue trajectory deserves careful analysis. Revenue growing at 34.23% CAGR over the last 5 years versus industry average of 15.46% suggests SYRMA is taking market share, but from whom? The answer reveals the company's strategic positioning. SYRMA isn't competing with Foxconn for Apple's business or with Flex for Amazon's. Instead, the company is capturing share from smaller regional players who lack scale and from global giants who find India operations too complex for non-critical products.

The stock price journey reflects market sentiment's evolution. The 52-week high of Rs 781.05 and 52-week low of Rs 355.05 represents more than 100% volatility, typical for a newly-listed growth company in a cyclical industry. But beneath this volatility, institutional ownership has steadily increased. Mutual funds that initially allocated token amounts are now taking meaningful positions. Foreign portfolio investors who ignored Indian manufacturing are reconsidering their stance.

Promoter holding at 46.4% strikes a careful balance. High enough to ensure aligned interests and strategic continuity, low enough to provide market liquidity and institutional comfort. The Tandon family's continued significant ownership sends a clear message: they believe in the long-term potential and aren't cashing out at the first opportunity. This isn't a private equity flip or a founder exit disguised as growth capital.

Working capital management in electronics manufacturing is where operational excellence meets financial engineering. SYRMA's cash conversion cycle has improved from 95 days to 72 days over three years—a remarkable achievement during a period of rapid growth when working capital typically balloons. This improvement comes from three sources: better payment terms from suppliers who now view SYRMA as a strategic customer, faster collections from customers who prioritize reliable suppliers during shortage periods, and inventory optimization through better demand forecasting and production planning.

The capital allocation decisions reveal management's priorities. Of the ₹766 crore raised in the IPO, approximately 40% went to capacity expansion, 30% to working capital, 20% to R&D and capability building, and 10% held for strategic opportunities. This isn't the aggressive expansion typical of venture-backed startups or the excessive conservatism of traditional manufacturers. It's calculated growth, where each rupee of capital investment is tied to specific customer commitments or capability requirements.

The segment-wise performance shows interesting dynamics. Automotive electronics, despite being just 25% of revenue, contributes 35% of EBITDA due to higher margins from technical complexity and customer stickiness. Medical devices, though only 15% of revenue following the JDHL acquisition, are growing at 60% annually with margins exceeding 20%. Industrial electronics provides steady cash flow with multi-year contracts and predictable volumes. Consumer electronics, while lower margin, offers scale and operational leverage.

Return on capital employed (ROCE) has improved from 12% to 18% over three years, but this understates the true economic returns. The acquisitions of Perfect ID and JDHL brought intangible assets—customer relationships, technical knowledge, regulatory approvals—that don't fully appear on the balance sheet but generate real economic value. Adjusted for these intangibles, the true ROCE likely exceeds 25%, comparable to leading global EMS players.

The competitive positioning becomes clearer when benchmarked against peers. Among listed Indian EMS companies, SYRMA SGS ranks in the top five by revenue but leads in technical complexity and margin profile. Dixon Technologies might be larger, but focuses more on consumer electronics with lower margins. Amber Enterprises dominates air conditioning components but lacks diversification. Kaynes Technology is similar in size but more dependent on the domestic market. SYRMA's unique position—diversified across industries, balanced between domestic and exports, spanning the value chain from components to complete products—provides resilience that pure-play competitors lack.

The margin evolution tells a story of increasing value addition. Gross margins have expanded from 28% to 34% over five years, driven by product mix shift toward higher-value products, operational efficiencies from scale and automation, and better procurement through supplier partnerships. EBITDA margins have grown from 9% to 14%, with potential to reach 16-17% as medical devices and automotive electronics become larger contributors.

Cash flow generation has been robust despite rapid growth. Operating cash flow exceeded ₹300 crore in the latest fiscal year, funding most of the capital expenditure internally. Free cash flow, though volatile due to working capital changes, has been consistently positive. This self-funding capability reduces dependence on external capital and provides flexibility during downturns.

The order book provides visibility and confidence. At ₹2,100 crore, representing roughly seven months of revenue, the order book has grown 50% year-over-year. More importantly, the order quality has improved—multi-year contracts with price escalation clauses, commitments from new customers in high-growth segments, and framework agreements that provide volume flexibility while ensuring capacity utilization.

Debt levels remain conservative with debt-to-equity ratio of 0.3x, well below the industry average of 0.8x. This conservative leverage provides room for growth investments without stretching the balance sheet. The interest coverage ratio of 8x ensures that even during downturns, debt servicing won't pressure operations. Credit ratings from CARE and ICRA reflect this financial strength, enabling access to low-cost capital when needed.

The dividend policy balances growth reinvestment with shareholder returns. The board has approved a 15% dividend payout ratio, signaling confidence in cash generation while retaining capital for growth. As the business matures and capital requirements moderate, this payout ratio could increase, providing additional returns to shareholders beyond capital appreciation.

Geographic revenue mix adds another dimension of stability. Exports contribute 55% of revenue, providing natural currency hedging and exposure to developed market customers with stable demand. Within domestic sales, government and public sector enterprises contribute 20%, offering long-term contracts and counter-cyclical stability. This geographic and customer diversification reduces vulnerability to any single market downturn.

The key concern remains the relatively low ROE of 9.21% over the last 3 years. While this partly reflects the capital raised in the IPO that hasn't been fully deployed, it also suggests room for improvement in capital efficiency. Management has committed to improving ROE to 15% over the next three years through margin expansion, asset turnover improvement, and prudent leverage.

The quarterly results trajectory shows consistency amid volatility. Unlike project-based businesses with lumpy revenues, SYRMA's quarterly revenues have grown steadily with seasonal patterns—Q3 typically strongest due to festive demand, Q1 weakest due to plant maintenance and lower working days. This predictability helps in planning and reduces earnings surprises that markets dislike.

Looking at valuation metrics, SYRMA trades at interesting levels. The price-to-earnings ratio of 35x might seem expensive compared to global EMS players trading at 15-20x. But adjusted for growth differential—SYRMA growing at 30%+ versus global peers at 5-10%—the PEG ratio of 1.1 suggests reasonable valuation. The enterprise value to sales ratio of 2x reflects market recognition of the company's strategic position and growth potential.

As we assess SYRMA SGS's financial position, what emerges is a company in transition. The foundation is solid—strong growth, expanding margins, robust cash generation, conservative balance sheet. But the market is still evaluating whether this is a cyclical upturn or structural transformation. The next few years will determine whether SYRMA can sustain its premium valuation through continued execution and strategic positioning in high-growth segments.

IX. Future Growth Strategy & Challenges

The war room on the executive floor of SYRMA SGS's headquarters has been transformed into what looks like a command center from a sci-fi movie. Multiple screens display real-time data: semiconductor price indices, shipping rates from Asian ports, COVID case rates in key manufacturing hubs, and customer demand forecasts that update every hour. Sandeep Tandon stands before a massive digital board showing the company's five-year strategic roadmap. "The easy growth is behind us," he tells his leadership team. "What comes next will test everything we've built."

The revenue target isn't pulled from thin air. Management's guidance of Rs 4,800 to Rs 5,000 crores represents a carefully calculated bet on multiple growth drivers converging. The math is straightforward but the execution complex: 15% organic growth from existing customers, 10% from new customer acquisitions, 8% from capacity expansion, and 5% from product mix improvement. Each percentage point represents hundreds of crores in revenue and requires flawless execution across multiple dimensions.

The PCB manufacturing joint venture represents SYRMA's boldest bet yet. India imports over 85% of its PCB requirements, a strategic vulnerability that the government is desperate to address. The PLI scheme offers incentives worth 25% of capital investment for PCB manufacturing, but the technical and capital requirements are staggering. SYRMA's proposed facility would produce HDI (High-Density Interconnect) and flexible PCBs, technologies that only a handful of companies globally have mastered. The investment requirement—over ₹1,000 crore—would be SYRMA's largest single commitment.

But PCBs are just the beginning. The electric vehicle revolution presents an opportunity that could redefine SYRMA's future. Every EV contains 10x the electronic content of a conventional vehicle: battery management systems, inverters, charging controllers, thermal management, and sophisticated sensors. SYRMA is positioning itself not for the glamorous but competitive EV assembly market, but for the critical electronic sub-systems where Indian manufacturing can compete globally. The company is already in advanced discussions with two global tier-one suppliers for EV power electronics manufacturing.

The defense electronics opportunity is equally compelling but more complex. India's defense modernization budget exceeds $70 billion annually, with electronics content growing from 30% to 50% of platform costs. The government's push for indigenous defense manufacturing through the Atmanirbhar Bharat initiative creates opportunities, but also challenges. Defense contracts require years of qualification, stringent security clearances, and ability to maintain production lines for decades. SYRMA is investing in a separate facility with military-grade security and establishing partnerships with DRDO laboratories.

Export market expansion, particularly in Europe and the US, faces different challenges. These markets offer higher margins and stable demand but require exceptional quality, reliable delivery, and often local presence. SYRMA's strategy isn't to compete on cost—Chinese and Vietnamese manufacturers will always be cheaper. Instead, the company is positioning itself as the reliable alternative for critical components where supply chain security matters more than lowest price. The Stuttgart R&D center is being expanded into a European customer engagement hub.

The technology roadmap reveals ambitions beyond traditional manufacturing. SYRMA is investing in AI-powered visual inspection systems that can detect defects invisible to human inspectors. Collaborative robots (cobots) are being deployed for tasks requiring precision but not full automation. Digital twin technology creates virtual replicas of production lines, enabling optimization without disrupting actual production. These aren't just productivity improvements—they're capability differentiators that justify premium pricing.

But the challenges are formidable. Competition from global EMS players is intensifying as everyone chases the same China-plus-one opportunity. Foxconn is investing $20 billion in India. Flex and Jabil are expanding aggressively. Pegatron and Wistron are moving beyond Apple assembly to broader electronics manufacturing. These giants have scale advantages, customer relationships, and financial resources that dwarf SYRMA's capabilities. Competing requires finding niches where agility and local knowledge matter more than global scale.

The supply chain challenges have only partially abated. While semiconductor availability has improved from the crisis days of 2021-22, new bottlenecks emerge regularly. Rare earth materials for magnetics face export restrictions. Specialty chemicals for PCB manufacturing are concentrated in a few suppliers. Even basic components like capacitors and resistors face periodic shortages. SYRMA is responding by building strategic inventory, qualifying alternate suppliers, and even considering backward integration for critical components.

Geopolitical tensions add another layer of complexity. The US-China technology war means choosing sides, with implications for supplier relationships and customer access. European regulations on supply chain transparency and environmental compliance add costs and complexity. India's own import restrictions and local content requirements, while creating opportunities, also constrain flexibility. Navigating this requires sophisticated government relations and constant strategic adjustment.

The talent challenge might be the most critical. SYRMA needs to hire 2,000 engineers over the next three years, but India produces plenty of engineers—the challenge is finding ones with relevant experience. PCB design, RF engineering, power electronics, and medical device development require specialized skills that universities don't teach. SYRMA is responding by establishing partnerships with technical institutes, creating apprenticeship programs, and even considering acquisitions primarily for talent acquisition.

The management bandwidth question looms large. Can the same team that built a ₹1,000 crore company manage a ₹5,000 crore enterprise? The skills required are different—from entrepreneurial to processdriven, from opportunistic to strategic, from hands-on to delegation. Sandeep has begun bringing in professional managers from larger companies, but cultural integration remains delicate. The entrepreneurial DNA that drove growth could be diluted by corporate processes necessary for scale.

Capital requirements for the growth plan are substantial. While the IPO provided initial funding, achieving revenue targets requires additional investment of ₹2,000-2,500 crore over five years. This could come from internal accruals if margins expand as planned, but more likely requires additional fund-raising. The options include QIP (Qualified Institutional Placement), strategic partnerships with customers or suppliers, or even additional acquisitions that bring capital along with capabilities.

The customer concentration risk requires careful management. While diversification has improved, the top ten customers still contribute over 60% of revenue. Losing any major customer would be devastating. SYRMA is addressing this by deepening relationships through multi-product strategies, establishing long-term contracts with penalty clauses, and gradually adding new customers to reduce dependency. But this is a slow process—building trust with new customers takes years.

Margin pressure remains constant. Customers demand annual price reductions while input costs keep rising. The solution isn't just operational efficiency but moving up the value chain. Every step from assembly to design, from components to systems, from manufacturing to solutions, adds margin. But each step also adds complexity and risk. The JDHL acquisition shows this strategy can work, but replicating it across other verticals requires careful execution.

The technology disruption risk can't be ignored. What if solid-state batteries eliminate complex battery management systems? What if quantum computing makes current electronic architectures obsolete? What if 3D printing enables distributed manufacturing, eliminating the need for centralized EMS providers? SYRMA must balance investment in current technologies with exploration of emerging ones, a difficult balance when current demand exceeds capacity.

Regulatory compliance becomes more complex with scale. Medical device regulations differ across countries. Automotive standards evolve constantly. Environmental regulations tighten annually. Data protection laws affect IoT devices. Each compliance requirement adds cost and complexity. SYRMA is building a compliance team that rivals its engineering team in size, a necessary but non-productive investment.

The sustainability imperative isn't just about compliance but competitiveness. Global customers increasingly demand carbon-neutral supply chains, circular economy practices, and social responsibility. SYRMA's investments in renewable energy and waste reduction are just the beginning. The company needs a comprehensive ESG strategy that satisfies stakeholders while remaining cost-competitive.

As SYRMA SGS charts its future course, the opportunities are matched by challenges. The company has proven it can execute complex manufacturing, integrate acquisitions, and satisfy demanding customers. Whether it can simultaneously scale operations, expand capabilities, enter new markets, and maintain margins while fighting intensifying competition will determine if SYRMA becomes India's EMS champion or remains a successful but subscale player. The next five years will be defining.

X. Playbook: Business & Investing Lessons