GE HealthCare Technologies: From X-Ray Pioneer to Precision Care Leader

I. Introduction & Episode Roadmap

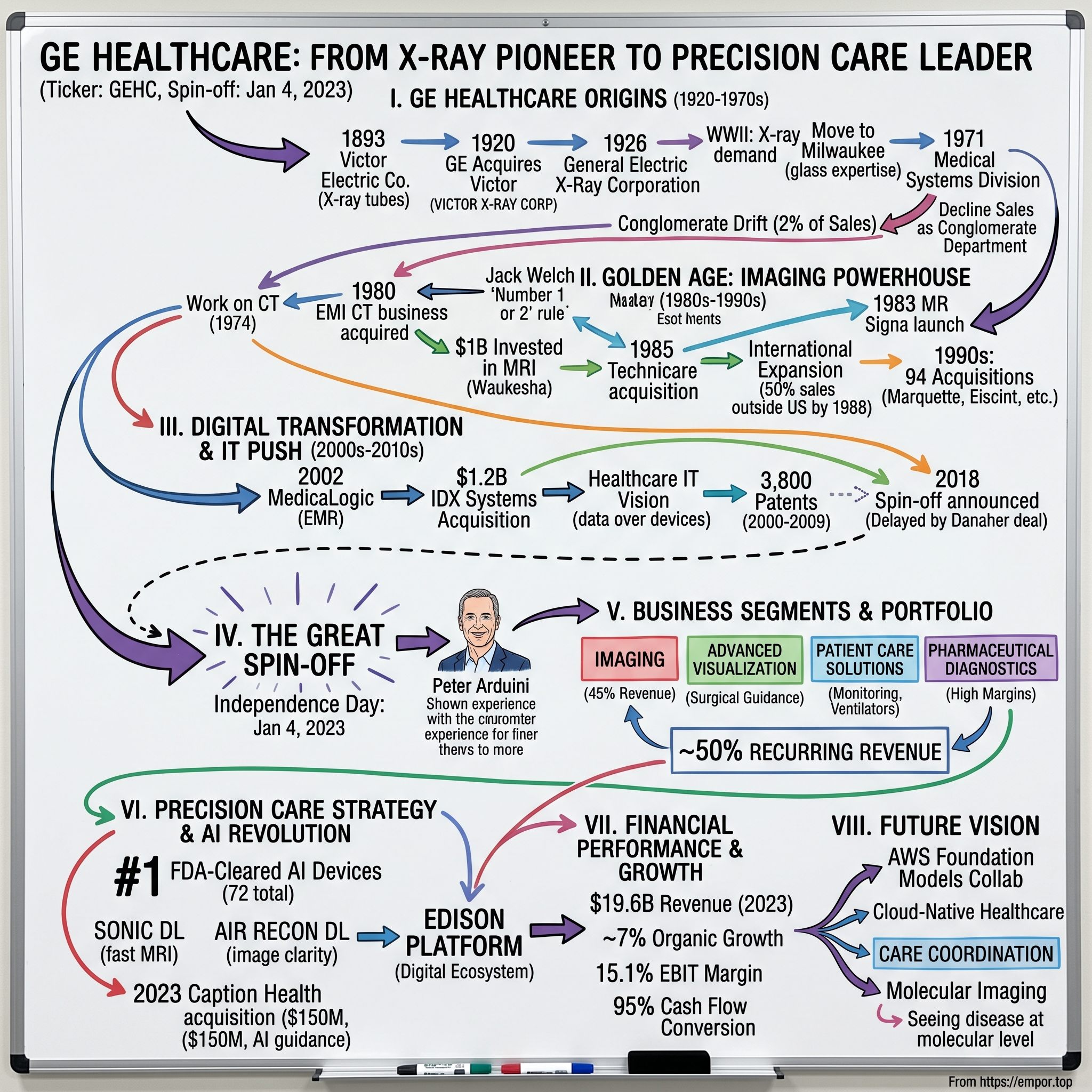

Picture this: January 4, 2023—after more than a century as part of the General Electric empire, GE HealthCare Technologies Inc. emerges as an independent entity, beginning trading on Nasdaq under the ticker symbol "GEHC". It's a moment that feels both like an ending and a beginning—the culmination of 100 years of medical innovation finally stepping into its own spotlight.

The scene at Nasdaq that morning carried a weight of history. Here was a company that had pioneered X-ray technology when Warren Harding was president, developed CT scanners during the Nixon administration, and revolutionized MRI imaging while Reagan was in office. Now, in the Biden era, it was declaring independence from one of America's most storied conglomerates.

H. Lawrence Culp Jr., GE's Chairman and CEO, captured the moment: "The successful spin-off of GE HealthCare marks a pivotal moment in our transformation into three independent companies focused on critical, growing sectors." But this wasn't just corporate restructuring—it was the unleashing of a healthcare giant that had been constrained within a conglomerate structure for decades.

The numbers tell a compelling story: $18 billion in annual revenue from MRI imaging, ultrasounds, and pharmaceutical diagnostics with a valuation of $31 billion at the time of spin-off. This wasn't some startup finding its footing—this was a mature powerhouse with operations in 160+ countries, serving over a billion patients annually, finally free to chart its own course.

But how did we get here? How did a division that started with simple X-ray machines in the 1920s evolve into a precision care leader leveraging artificial intelligence to transform healthcare? And perhaps more intriguingly, what does independence mean for a company that spent a century as part of the GE machine?

This is a story of technological revolutions and corporate evolution, of brilliant engineers and savvy executives, of surviving multiple recessions and emerging stronger. It's about how a company that once struggled to represent 2% of GE's sales transformed into one of the world's most important medical technology companies. And it's about what happens when you finally cut the corporate umbilical cord after 100 years.

II. The GE Healthcare Origins: X-Rays to Empire (1920–1970s)

The basement workshop at 418 Dearborn Street in Chicago, 1893. Charles F. Samms and Julius B. Wantz, two ambitious entrepreneurs, founded the Victor Electric Company in that cramped space, their vision centered on the emerging field of electrical medical equipment. Neither man could have imagined their modest startup would become the foundation of a global healthcare empire.

By 1896, just a year after Wilhelm Röntgen discovered X-rays, Victor Electric was already manufacturing electrostatic generators for exciting X-ray tubes and electrotherapeutic devices. The timing was perfect—medicine was entering the electrical age, and Victor positioned itself at the forefront. Their early X-ray tubes, crude by today's standards, represented cutting-edge technology that allowed doctors to peer inside the human body without cutting it open.

The company's growth was explosive. By 1903, Victor Electric had outgrown its facilities at 418 Dearborn St. and bought two floors at 55 Market Street. This proved temporary; by 1910 it was too small again, and in 1911 they moved to Jackson Blvd. and Damen Avenue—their first permanent home where they would stay for 35 years.

Then came the pivotal moment that would reshape medical imaging forever. October 1, 1920: General Electric completed its acquisition of Victor Electric Corporation, merging it with GE's X-ray interests to form the VICTOR X-RAY CORPORATION. By 1920, Victor had been renamed VICTOR X-RAY CORPORATION under GE ownership.

The marriage made strategic sense. The merger promised "full manufacturing, engineering and research co-operation between Victor X-Ray Corporation and General Electric Company with respect to X-Ray problems," extending the usefulness of both companies to meet growing demand for Coolidge tubes and other X-ray devices. Victor brought manufacturing expertise and market presence; GE brought research capabilities and capital.

The merger formally closed on July 28, 1926, when the company became "General Electric X-Ray Corporation." The consolidation brought renewed vitality, with equipment soon being sold and serviced in nearly 70 countries. By 1930, the Victor name was phased out from all branding, though advertisements still mentioned "formerly Victor X-Ray Corporation".

But then came decades of drift. Before the introduction of the CT scanner in the 1970s and the MRI scanner in the 1980s, the division declined to around 2% of GE's sales among the 120 departments in the conglomerate. X-rays, once revolutionary, had become commoditized. The division that had pioneered medical imaging was becoming an afterthought within the sprawling GE empire.

World War II briefly revitalized the business. X-rays found widespread use in non-destructive testing of war materials and as a medical tool for military services. As the war ended, GE X-Ray Corporation continued to grow. Greater production capacity and expertise were needed in building X-ray tubes. Since the tubes were made from hand-blown glass, the decision was made to move the company 90 miles north to Milwaukee, Wisconsin, to tap into the enormous glass-making expertise there.

The post-war years saw steady but uninspiring growth. In 1971, GE upgraded the department to The Medical Systems Division. A major expansion program started with the Waukesha factory planned in July 1972 and completed in 1973. This infrastructure would prove crucial for what came next.

In 1974, work on CT began, and the first CT machine was installed in 1976. Then in June 1980, the company acquired the CT scanner business of EMI—the British company that had invented the technology. Suddenly, GE Medical Systems was back in the game.

Enter Jack Welch. When he became CEO in 1981, he saw potential where others saw a sleepy division. In the 1970s, CT scanners were introduced, followed by MRI machines in the 1980s, with GE leading in both. The department, now named GE Medical Systems (GEMS), grew rapidly under Welch's management.

Welch's philosophy was simple but brutal: be number one or two in your market, or get out. For GE Medical Systems, this meant massive investment and aggressive expansion. The division that had been an afterthought suddenly found itself at the center of GE's growth strategy.

III. The Golden Age: Building the Medical Imaging Powerhouse (1980s–1990s)

The year 1983 marked a bet-the-company moment for GE Medical Systems. GE Medical invested nearly US$1 billion in a new plant in Waukesha for Magnetic Resonance Imaging (MRI) technology. To put this in perspective, this was a staggering sum for a division that had been a minor player just years earlier. The facility would produce the MR Signa, a machine that would revolutionize medical diagnostics.

The MRI investment was Jack Welch at his most audacious. While competitors hesitated, unsure if this expensive technology would find a market, Welch pushed all chips to the center of the table. His logic was compelling: aging populations in developed countries would drive demand for advanced diagnostics, and whoever owned the technology would own the market.

But technology alone wouldn't build an empire. GE Medical Systems embarked on an acquisition spree that would fundamentally reshape its portfolio. In 1985, GE acquired Technicare from Johnson & Johnson. Originally named Ohio Nuclear, Technicare had been producing rotate-stationary CTs with thousands installed, plus X-ray equipment and nascent MRI products.

The Technicare acquisition was masterful. Not only did GE eliminate a competitor, but it also acquired an installed base of customers who would need service, upgrades, and eventually replacement systems. This was Welch's genius—he understood that medical equipment wasn't just about the initial sale but about the decades-long relationship that followed.

International expansion accelerated dramatically. The division expanded globally through partnerships and acquisitions, growing to 50% sales outside the USA by 1988. In 1987, the Medical Systems Division reorganized from simple domestic and international divisions into three "poles": Americas, Europe, and Pacific. In 1988, GE Medical Europe merged with CGR, a French medical equipment supplier, forming General Electric CGR Medical Systems, moving European headquarters from Hammersmith, UK to Buc, near Paris.

The 1990s brought even more aggressive expansion. Between 1995 and 2017, the division executed 94 acquisitions, methodically building capabilities across the medical technology spectrum. Each acquisition wasn't just about adding revenue—it was about acquiring technology, talent, and market access.

September 1998 saw the acquisition of Marquette Medical Systems for $808 million, bringing critical patient monitoring capabilities. Two months later, in November 1998, GE acquired the Nuclear and MR businesses of Elscint for $100 million, further strengthening its imaging portfolio.

The service business model that emerged during this period was revolutionary. GE didn't just sell machines; it sold peace of mind. Service contracts guaranteed uptime, regular upgrades, and access to GE's global support network. A hospital buying a GE MRI wasn't just getting a machine—it was entering a partnership that could last decades.

By the late 1990s, GE Medical Systems had transformed from an also-ran into a colossus. The division that had once struggled to represent 2% of GE's revenue was now a crown jewel, generating billions in highly profitable revenue. The foundation was set for the next revolution: digital transformation.

This golden age wasn't just about financial success. It was about fundamentally changing how medical imaging was conceived, delivered, and serviced. GE had proven that medical technology could be both a force for good and a spectacular business. The question now was: what comes next?

IV. Digital Transformation & Healthcare IT Push (2000s–2010s)

The new millennium opened with GE Medical Systems making a strategic pivot that would define its next two decades. In 2001, the company acquired San Francisco-based CT maker Imatron for $210 million. Imatron's Electron beam tomography (EBT) scanner performed specialized imaging for cardiology, pulmonology, and gastroenterology, later incorporated into GE Healthcare's Diagnostic Imaging segment.

But the real transformation wasn't in hardware—it was in software. In March 2002, GE acquired MedicaLogic, creator of Logician, an ambulatory Electronic Medical Records system, for approximately $32 million. This seemingly modest acquisition signaled a fundamental shift: GE was no longer just an imaging company but a healthcare information company.

The push into healthcare IT accelerated dramatically in 2006 with the acquisition of IDX Systems Corporation for $1.2 billion. This wasn't just buying technology—it was buying a vision of integrated healthcare where imaging, patient records, and clinical decision support would merge into a seamless digital ecosystem.

Behind this transformation was a new generation of leaders who understood that data, not just devices, would drive healthcare's future. They invested heavily in R&D, generating over 3,800 patents between 2000 and 2009. These weren't just incremental improvements but fundamental reimaginings of how medical technology could work.

The financial crisis of 2008-2009 tested this strategy but ultimately validated it. While hospitals delayed equipment purchases, they continued investing in IT systems that could improve efficiency and reduce costs. GE Healthcare's diversified portfolio—spanning imaging, IT, and services—provided resilience that pure-play imaging companies lacked.

Then came a shocking announcement that would reshape the company's trajectory. In June 2018, GE first announced plans to spin off GE Healthcare, though these plans would be delayed after the company sold its biopharma business to Danaher for $21.4 billion. The writing was on the wall: GE Healthcare was becoming too important, too specialized to remain part of a conglomerate.

The 2010s also saw strategic bets on emerging technologies. In 2021, even as spin-off discussions intensified, GE Healthcare acquired Prismatic Sensors AB for its Deep Silicon detector technology and Zionexa for breast cancer biomarkers. December 2021 brought the acquisition of BK Medical from Altaris Capital Partners for $1.45 billion, adding advanced surgical visualization capabilities.

Throughout this period, GE Healthcare was laying the groundwork for something bigger: the precision care revolution. Every acquisition, every R&D investment, every strategic pivot was building toward a future where medical care would be personalized, predictive, and precise. The only question was whether GE Healthcare could achieve this vision while still tethered to its parent company.

V. The Great Spin-Off: Breaking Free from GE (2021–2023)

November 9, 2021: GE announces it will split into three public companies focused on aviation, healthcare, and energy. For GE Healthcare employees, it was a moment of both excitement and trepidation. After a century within the GE umbrella, they were about to venture out alone.

The architect of this independence was a surprising choice. In January 2022, GE announced Peter Arduini as president and CEO of GE Healthcare. Arduini joined from Integra LifeSciences, where he had served as president and CEO since January 2012. But this wasn't an outsider parachuting in—Arduini had spent 15 years at GE Healthcare earlier in his career in various leadership roles, including leading the Computed Tomography & Molecular Imaging business.

Larry Culp praised the appointment: "Pete has a proven track record of driving growth, margin expansion and overall financial performance. His broad and deep industry experience combined with his respected leadership and team-building style make him the right fit to continue our important work at GE Healthcare focused on precision health".

Arduini brought a unique perspective. At Integra LifeSciences from 2012 to 2021, the portfolio had evolved significantly to a faster growing and more profitable company through multiple acquisitions and sustainable R&D pipeline development. He understood how to run an independent medical technology company, experience that would prove invaluable.

The mechanics of the spin-off were complex but elegant. Holders of GE common stock received one share of GE HealthCare common stock for every three shares of GE common stock held. The distribution was a tax-free spin-off, providing tax efficiency for GE shareholders in the United States. GE retained approximately 19.9% of GE HealthCare shares, ensuring some continuity while allowing the new company to chart its own course.

The preparation was meticulous. Throughout 2022, Arduini and his team worked to establish GE HealthCare's identity, strategy, and operational independence. They had to create everything from scratch: IT systems, HR policies, investor relations, corporate governance. It was like building a $20 billion startup overnight.

December 8, 2022, at the company's Investor Day, management revealed ambitious plans: more than 35% of equipment orders in the recent year were for products introduced in the previous 12 months. This wasn't a tired division being cast off—this was a innovation engine ready to accelerate.

January 4, 2023, arrived with anticipation and anxiety. As GEHC began trading, employees gathered in offices worldwide to watch the first trades. The stock opened strong, validating years of preparation. Larry Culp would serve as non-executive chairman, providing continuity while allowing Arduini to run the company.

But Arduini understood that independence was just the beginning. "If you want to get into an industry where you're going to see more change in the next 10 years than the last 100, healthcare is the place you want to be", he told an audience at Northwestern's Kellogg School. The real work—transforming GE HealthCare into a precision care leader—was just beginning.

The spin-off represented more than corporate restructuring. It was a recognition that healthcare technology had become too complex, too specialized, too important to be one division among many. GE HealthCare needed the focus, agility, and specialized culture that only independence could provide. After 103 years, the child was finally leaving home.

VI. Business Segments & Strategic Portfolio

Walk into any major hospital today, and you'll encounter GE HealthCare technology at nearly every turn. The company's portfolio, refined over a century, now operates through four strategic segments that generated $19.7 billion in revenue in 2024.

The Imaging segment remains the company's crown jewel, accounting for about $2.4 billion in 2024 Q4 revenue and representing roughly 45% of total revenue. This is where GE HealthCare's heritage lives—from those first X-ray machines in Chicago basements to today's AI-powered MRI systems. The segment encompasses MRI, CT, molecular imaging, and X-ray, each category representing decades of innovation and refinement. When a radiologist reads a scan that saves a life, there's a good chance it came from this division.

Advanced Visualization Solutions (AVS), contributing $1.4 billion in 2024 Q4, represents the company's digital future. This isn't just about displaying images—it's about transforming raw data into actionable insights. The segment includes surgical navigation, procedure guidance, and quantification software that helps surgeons operate with superhuman precision. Think of it as the difference between looking at a map and having GPS navigation.

Patient Care Solutions generated $827 million in 2024 Q4, encompassing the unglamorous but essential technologies that keep patients alive: anesthesia delivery, respiratory care, patient monitoring. These aren't the machines that make headlines, but they're the ones that nurses and intensivists rely on every minute of every day. In the COVID-19 pandemic, this division's ventilators literally meant the difference between life and death for millions.

Pharmaceutical Diagnostics, at $646 million in 2024 Q4, might be the smallest segment but offers the highest margins. The division produces contrast agents and radiopharmaceuticals—the specialized chemicals that make certain types of imaging possible. It's a business with high barriers to entry, regulatory moats, and customer relationships measured in decades.

The geographic distribution tells its own story. In 2023, the company received 42% of revenue from the United States and 13% from China, with Europe, Middle East, and Africa contributing 26%. This global footprint provides both diversification and challenge—every market has different regulations, reimbursement systems, and competitive dynamics.

But the real strategic insight lies in the revenue mix. Approximately 50% of GE HealthCare's revenue is recurring—from servicing equipment (~33%), pharmaceutical diagnostics (~10-15%), and digital solutions (~5%). This isn't the feast-or-famine cycle of equipment sales but a steady stream of predictable revenue that provides stability and funds innovation.

The competitive landscape is fierce but fragmented. Siemens Healthineers, the closest peer, brings German engineering excellence. Philips leverages its consumer health expertise. Canon and Fujifilm apply their imaging heritage to medical applications. Yet GE HealthCare's integrated portfolio—spanning devices, software, and services—creates competitive advantages that are difficult to replicate.

What's most impressive is how these segments interconnect. An MRI machine (Imaging) generates images that are processed by AI software (AVS), while the patient is monitored (Patient Care Solutions) after receiving contrast agents (Pharmaceutical Diagnostics). It's an ecosystem, not just a collection of products, and that ecosystem is increasingly powered by artificial intelligence.

VII. The Precision Care Strategy & AI Revolution

"GE Healthcare's world-class portfolio and leadership in precision health positively impacts the lives of billions of patients worldwide", Peter Arduini declared upon taking the helm. But what exactly is "precision care," and why is it the cornerstone of GE HealthCare's future?

The numbers tell a stunning story of AI leadership. GE HealthCare has topped the FDA's list of AI-enabled medical devices for the third year in a row with 72 listed 510(k) clearances or authorizations. The company topped this list in 2022 and 2023 as well. This isn't just a vanity metric—it represents a fundamental transformation in how medical devices operate.

Consider Sonic DL, one of GE HealthCare's flagship AI innovations. The deep learning technology acquires high-quality MR images up to 12 times faster than conventional methods, enabling cardiac imaging within a single heartbeat, with up to an 83% reduction in scan time. For a patient with arrhythmia who previously couldn't hold still long enough for a cardiac MRI, this technology is literally life-changing.

Or take AIR Recon DL, which uses deep learning to reconstruct MRI images with unprecedented clarity in half the time. The technology can scan in half the time of a conventional scan while also improving image quality. The AI doesn't just speed things up—it sees patterns and details that human eyes might miss.

February 2023 brought a strategic masterstroke: GE HealthCare acquired Caption Health for $150 million. Caption Health was the first company ever to receive FDA approval for an AI-guided medical imaging acquisition system. The technology guides non-specialists through ultrasound procedures with simple visual prompts—like GPS for medical imaging. The software is as simple as the directions sent to guide an Uber driver.

The Edison platform represents the architectural foundation of this AI revolution. It's not just one product but a digital ecosystem that connects devices, aggregates data, and deploys AI applications across the enterprise. Think of it as the operating system for precision healthcare—a platform that gets smarter with every scan, every patient, every outcome.

Jim McNerney asked Arduini about this AI transformation at Kellogg: "You have more AI-enabled devices cleared or approved by the FDA than any other company in your industry, and you're transforming into an information systems company built on this base of medical imaging technology". Arduini's response was telling—this isn't about technology for technology's sake but about fundamentally reimagining healthcare delivery.

The company's R&D investment reflects this commitment. Since becoming independent, GE HealthCare has invested approximately $2.2 billion back into the business, with much of it focused on AI and digital capabilities. In 2023 alone, the company invested over $1 billion in R&D, driving more than 40 innovations.

But perhaps the most ambitious initiative is the company's work on foundation models for medical imaging. In collaboration with AWS, GE HealthCare is developing AI that can understand and interpret medical images at a fundamental level—not just identifying specific conditions but understanding the underlying anatomy and pathology. The model showed up to 30% accuracy in matching MRI scans with textual descriptions in image retrieval tasks—a significant improvement over the 3% capability demonstrated by similar models.

The precision care strategy goes beyond individual technologies. It's about creating an integrated ecosystem where AI enhances every step of the patient journey—from initial screening to diagnosis, treatment planning, intervention, and follow-up. Each patient interaction generates data that makes the system smarter, creating a virtuous cycle of continuous improvement.

VIII. Financial Performance & Growth Trajectory

The first earnings call as an independent company in May 2023 was a moment of truth. Wall Street was watching, skeptics were circling, and Peter Arduini stepped up to the microphone. "We saw strong revenue growth across all of our business segments and regions as supply chain challenges eased. We continue to expect 5% to 7% Organic revenue growth for 2023", he announced confidently.

The numbers validated the independence thesis. 2023 full year revenue hit $19.6 billion, up 7% year-over-year and 8% on an organic basis with growth across all segments and regions. This wasn't just maintaining momentum—it was acceleration. Adjusted EBIT margin for 2023 was 15.1%, up 60 basis points versus the estimated 2022 standalone margin of 14.5%.

But 2024 would bring challenges that tested the company's resilience. China, representing 13% of revenue, faced increasing competition and market softness. The strong dollar created headwinds for international sales. Healthcare systems globally were grappling with budget constraints and staff shortages.

2024 revenue came in at $19.7 billion, up just 1% on an organic basis. Growth in the U.S. and Pharmaceutical Diagnostics was partially offset by continued market softness in China. Yet margins continued to expand: Adjusted EBIT margin reached 16.3% for the full year, up 120 basis points from 2023.

The cash generation story was equally impressive. Free cash flow conversion hit 95% in 2023, demonstrating the quality of earnings. This wasn't revenue built on extended credit terms or channel stuffing—it was real cash that could fund innovation and return value to shareholders.

Management's medium-term outlook, unveiled at investor day, projected confidence: mid-single-digit organic revenue growth from 2026-2028, with continued margin expansion. The targets seemed achievable given the company's innovation pipeline and market position.

The breakdown by segment revealed strategic priorities. Imaging, despite being the largest segment, grew modestly as the company focused on margin improvement over volume. AVS showed strong momentum, reflecting the shift toward digital and AI solutions. Pharmaceutical Diagnostics, while smallest, delivered consistent high-margin growth.

What's remarkable is how different the financial profile looks as an independent company versus a GE division. "As a standalone company, we expect GE HealthCare to benefit from increased focus, better aligned management and incentives, and an improved corporate culture. We believe these changes will help drive higher margins and organic growth", noted one analyst.

The company's approach to capital allocation reflects this independence. Rather than competing for resources within a conglomerate, GE HealthCare can now invest strategically in high-return opportunities. The Caption Health acquisition, the R&D investments in AI, the expansion of service capabilities—all reflect a company investing for the long term.

"We've raised guidance twice now, and we've been able to deliver on our numbers. We've been successful in raising our EBIT, driving cash flow conversion about 85% plus. We've grown our revenues 6% to 8%, and we're building our future capabilities", Arduini reported to investors.

The stock market's reaction has been positive but measured. GEHC trades at a premium to some medical technology peers but a discount to high-growth med-tech leaders. The market seems to be saying: prove you can sustain growth and margin expansion, and we'll reward you accordingly.

IX. Playbook: Lessons from the Spin-Off

"Culture eats strategy for breakfast," Arduini likes to quote Peter Drucker, and nowhere is this more evident than in GE HealthCare's transformation from division to independent company. The playbook they've written offers lessons that extend far beyond healthcare.

Lesson 1: Timing is Everything The spin-off came at an inflection point—healthcare digitization accelerating, AI reaching commercial viability, and precision medicine moving from concept to reality. A decade earlier would have been too soon; a decade later, too late. Historical data shows spin-offs generally outperform, with one study finding "significantly positive" returns for both spin-offs and parents during the three years following separation.

Lesson 2: Leadership Continuity Matters Arduini's unique background—15 years at GE Healthcare, then a decade running an independent med-tech company—provided the perfect blend of institutional knowledge and independent company experience. Before returning to GE, he served as CEO of Integra LifeSciences from 2012 to 2021, and prior to that was at Baxter Healthcare from 2005 to 2010. He originally spent 15 years at GE Healthcare in various management roles, culminating in leading the global functional imaging business.

Lesson 3: Focus Unleashes Innovation As part of GE, healthcare competed for resources with aviation and power generation. Now, every dollar of investment goes toward healthcare innovation. The results are evident: In 2024, the company introduced approximately 40 innovations and closed more than 50 strategic enterprise deals globally.

Lesson 4: Recurring Revenue Provides Stability The ~50% recurring revenue base—from service contracts, software subscriptions, and pharmaceutical diagnostics—provides a cushion that pure equipment manufacturers lack. This predictability allows for longer-term planning and sustained R&D investment.

Lesson 5: Domain Expertise Trumps Financial Engineering Unlike financial spin-offs driven by activism or tax optimization, GE HealthCare's independence was about operational improvement. The board is packed with healthcare expertise, not financial engineers. Board members include Dr. Rodney Hochman, Dr. Risa Lavizzo-Mourey (former president of Robert Wood Johnson Foundation), and Dr. Tomislav Mihaljevic.

Lesson 6: Speed of Execution Matters From announcement to completion, the spin-off took just over a year—lightning speed for a transaction of this complexity. This minimized uncertainty for employees and customers while maintaining business momentum.

Lesson 7: Strategic Acquisitions Accelerate Transformation The Caption Health acquisition wasn't just about buying technology—it was a signal that the independent GE HealthCare would be aggressive in building capabilities. At the J.P. Morgan Healthcare Conference, CEO Peter Arduini said embedding AI into products would become much more common in the next few years.

Lesson 8: Communication is Currency Throughout the spin-off, management over-communicated with employees, customers, and investors. Town halls, customer visits, investor days—the message was consistent: GE HealthCare was ready for independence.

The playbook isn't without risks. Independence means no GE balance sheet to fall back on, no corporate umbrella during downturns. But as one employee noted at a town hall: "For the first time in my career, our success or failure is entirely in our hands."

X. Bear vs. Bull Case & Industry Analysis

The Bull Case: A Precision Care Juggernaut

The optimists see GE HealthCare as perfectly positioned for healthcare's AI revolution. With 72 FDA-cleared AI devices—more than any other medical technology company—the company has established clear technological leadership. The recurring revenue base of ~50% provides stability while the innovation engine accelerates.

Demographics alone make a compelling case. The global population over 65 will double by 2050, driving demand for diagnostic imaging and chronic disease management. In emerging markets, rising incomes and expanding healthcare access create massive growth opportunities. More than 95 million MRI scans are performed each year globally, and that number will only grow.

The precision medicine megatrend plays perfectly to GE HealthCare's strengths. As healthcare shifts from one-size-fits-all to personalized treatment, the company's integrated portfolio—devices that generate data, AI that analyzes it, and services that deliver insights—becomes increasingly valuable.

Valuation remains reasonable compared to high-growth med-tech peers. The company trades at roughly 15-16x forward earnings, a discount to pure-play AI healthcare companies. As margins expand and growth accelerates, multiple expansion seems likely.

The spin-off itself creates value. Studies show spin-offs beat the S&P 500 by an average of 10% over 18-24 months. With focused management, aligned incentives, and strategic flexibility, GE HealthCare can optimize its business in ways impossible within a conglomerate.

The Bear Case: Structural Headwinds

Skeptics point to real challenges. China, representing 13% of revenue, faces intensifying competition from local players and geopolitical tensions. The Chinese government's "Buy China" healthcare initiative threatens market share, while economic slowdown pressures healthcare spending.

Healthcare systems globally face budget constraints. In the U.S., hospital margins remain compressed post-COVID. In Europe, austerity measures limit capital equipment purchases. Emerging markets, while growing, often lack the infrastructure and financing for premium equipment.

Competition is intensifying across all segments. Siemens Healthineers has aggressive expansion plans. Philips is restructuring to regain competitiveness. Chinese manufacturers are moving upmarket with "good enough" products at fraction of the price. In AI, tech giants like Google and Microsoft are entering healthcare, potentially disrupting traditional players.

Regulatory and reimbursement pressures continue mounting. Despite the explosion in FDA approvals, CMS has only assigned payment codes for about 10 AI applications. Without reimbursement, even breakthrough technologies struggle to achieve adoption.

Integration risks from acquisitions remain real. Caption Health, BK Medical, MIM Software—each requires integration while maintaining innovation momentum. Cultural clashes, talent retention, and execution challenges could derail synergy realization.

The recurring revenue base, while stable, faces its own pressures. Hospitals are increasingly questioning service contract value, exploring third-party service options, and extending equipment replacement cycles. The shift to value-based care could pressure both equipment sales and service pricing.

Industry Analysis: Navigating Complexity

The medical imaging industry sits at a fascinating inflection point. Traditional hardware differentiation is diminishing—most vendors offer similar image quality and features. The battle has shifted to software, AI, and services.

Market structure is consolidating but remains fragmented. The top five players—GE HealthCare, Siemens Healthineers, Philips, Canon, and Fujifilm—control roughly 70% of the market. But hundreds of smaller players, particularly in emerging markets and specialized niches, provide competition.

Technology disruption accelerates. AI isn't just improving existing modalities—it's enabling entirely new approaches. Portable ultrasound with AI guidance democratizes imaging. Cloud-based image analysis reduces infrastructure requirements. These innovations could disrupt traditional business models.

The competitive dynamics vary dramatically by geography and segment. In the U.S., it's about AI and value-based care integration. In China, it's about localization and price. In emerging markets, it's about affordability and service coverage. Success requires not one strategy but dozens, tailored to local conditions.

XI. Future Vision: What's Next for GEHC

Standing at the precipice of transformation, GE HealthCare faces a future that would seem like science fiction to those Chicago basement inventors from 1893. As Arduini puts it: "If you want to get into an industry where you're going to see more change in the next 10 years than the last 100, healthcare is the place you want to be".

The AI transformation is just beginning. The company's vision for foundation models is to "put this model into the hands of technical teams working within health systems and academic medical centers globally, giving them a powerful new tool for developing research and clinical applications faster, better, and more cost-effectively than ever before". Imagine hospitals creating custom AI applications as easily as they now create spreadsheets.

The July 2024 collaboration with AWS for foundation models and generative AI represents a strategic bet on cloud-native healthcare. Rather than selling boxes, GE HealthCare increasingly sells intelligence—AI that lives in the cloud, learns from global data, and delivers insights anywhere.

Emerging markets present enormous opportunity. In India, Africa, and Southeast Asia, GE HealthCare isn't just selling equipment but helping build entire healthcare systems. The company's ability to provide not just machines but training, service, and digital infrastructure positions it as a partner, not just a vendor.

The molecular imaging revolution, exemplified by Flyrcado's recent FDA approval, opens new frontiers. This isn't just better imaging—it's seeing disease at the molecular level, catching cancer before it spreads, identifying Alzheimer's before symptoms appear. The convergence of imaging and molecular diagnostics could fundamentally change disease detection and treatment.

But perhaps the biggest opportunity lies in care coordination. Today's healthcare is fragmented—different devices, incompatible systems, siloed data. GE HealthCare's vision is seamless integration where a patient's journey from screening to diagnosis to treatment to monitoring is connected, intelligent, and personalized.

The challenges are real. Cybersecurity threats grow more sophisticated. Data privacy regulations become more complex. The ethical implications of AI in healthcare demand careful navigation. Success requires not just technological innovation but wisdom in deployment.

M&A will continue playing a crucial role. The company has the balance sheet and strategic clarity to make bold moves. Whether acquiring AI startups, entering adjacent markets, or consolidating fragmented segments, GE HealthCare has the flexibility that eluded it within GE.

Ten years from now, GE HealthCare may look radically different. Perhaps it's primarily a software company with hardware attachments. Perhaps it's merged with or acquired complementary businesses. Perhaps it's split again into focused units. The only certainty is change.

What remains constant is the mission that started in that Chicago basement: using technology to see inside the human body, understand disease, and save lives. The tools have evolved from simple X-ray tubes to AI-powered precision care platforms, but the purpose endures.

As we look toward 2034, GE HealthCare stands at an inflection point. Independent for the first time in a century, armed with leading technology and a clear strategy, the company that pioneered medical imaging is now pioneering precision care. The next decade won't just bring incremental improvement but fundamental transformation in how healthcare is delivered, and GE HealthCare intends to lead that transformation.

The story that began with two entrepreneurs in a basement isn't ending—it's just beginning a new chapter. And if the next century is anything like the last, it will be extraordinary.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube