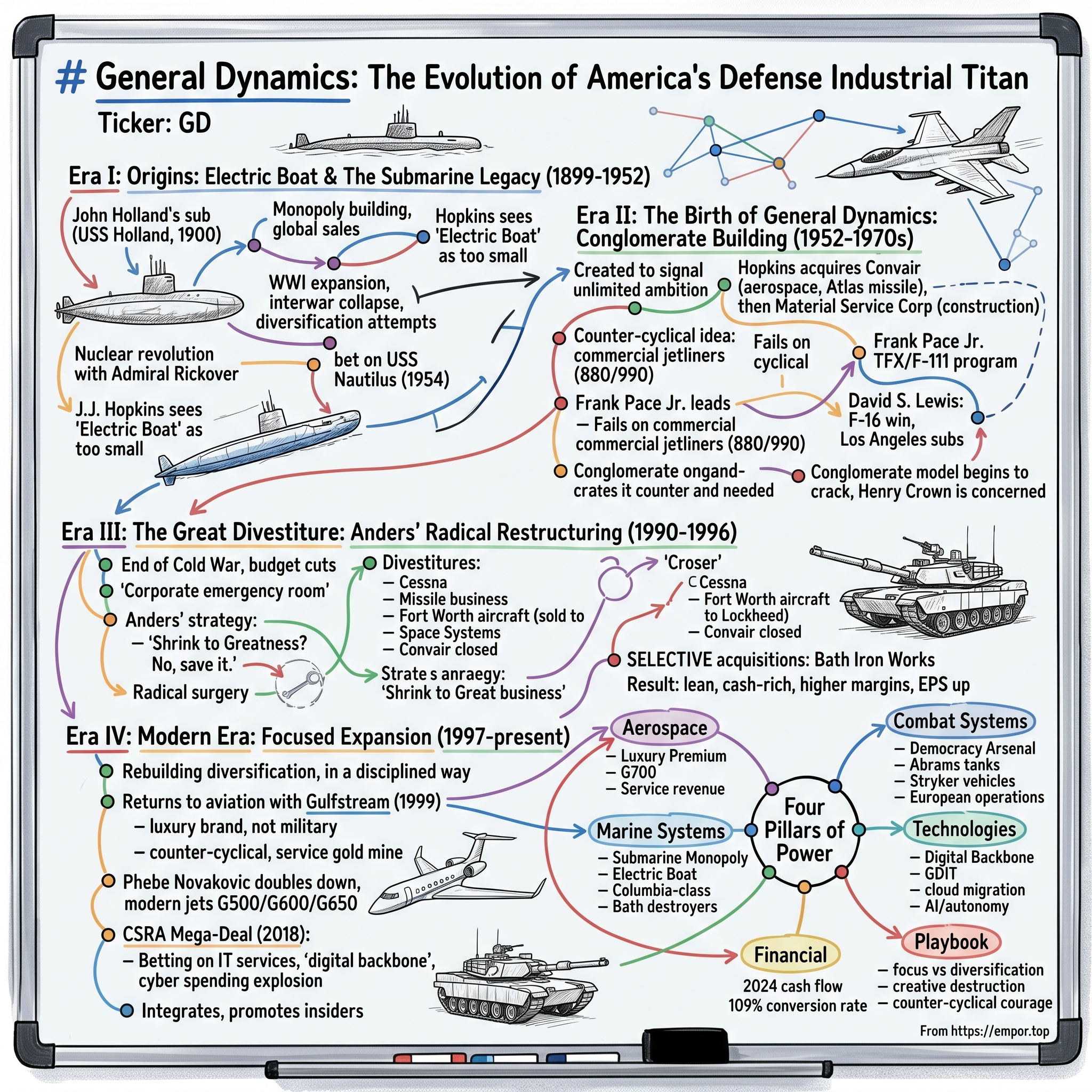

General Dynamics: The Evolution of America's Defense Industrial Titan

I. Introduction & Episode Roadmap

Picture this: It's 1899, and a former Irish Christian Brother turned inventor named John Philip Holland is watching nervously as his experimental submarine—a 54-foot cigar-shaped vessel powered by a gasoline engine on the surface and electric motors underwater—prepares for its first U.S. Navy trials. Holland has already bankrupted himself twice pursuing this dream. His backers, a shadowy group of Irish revolutionaries called the Fenian Brotherhood, have abandoned him after he refused to let them use his earlier submarine designs to sink British warships. Now, everything rides on this demonstration.

That submarine, the USS Holland, would become the U.S. Navy's first commissioned submarine in 1900. The company that built it—after several ownership changes and reinventions—would transform into General Dynamics, today's third-largest contractor to the U.S. federal government with $47.7 billion in revenue and over 110,000 employees worldwide.

How did a scrappy submarine startup founded by an Irish schoolteacher become a defense industrial titan that builds everything from Gulfstream luxury jets to M1 Abrams tanks, from Virginia-class nuclear submarines to classified IT systems for the intelligence community? The answer involves multiple near-death experiences, radical portfolio surgery, counter-cyclical acquisitions that Wall Street hated but later loved, and a succession of leaders who understood that in defense, your biggest customer—the U.S. government—is also your most demanding shareholder proxy.

This is the story of General Dynamics—a company that has reinvented itself more dramatically than perhaps any other major defense contractor. While competitors like Lockheed Martin and Northrop Grumman largely grew through consolidation in their core markets, General Dynamics has played a different game entirely. It has built conglomerates, torn them apart, exited entire industries only to re-enter them decades later, and somehow emerged stronger each time.

The company's evolution breaks into distinct eras, each marked by a fundamental strategic pivot. There's the submarine monopolist era (1899-1952), when Electric Boat Company dominated underwater warfare. The conglomerate-building phase (1952-1990), when the newly renamed General Dynamics tried to become everything from a commercial airline manufacturer to a space contractor. The radical restructuring under Bill Anders (1991-1996), who sold off two-thirds of the company in what remains one of the most dramatic corporate transformations in American business history. And finally, the modern era of focused expansion (1997-present), where successive CEOs have built a more disciplined but still diverse defense portfolio that generates extraordinary cash flows.

Today's General Dynamics operates through four major segments that would each be formidable standalone companies. Marine Systems, anchored by the original Electric Boat submarine yards, commands 30% of revenues and holds a near-monopoly on U.S. nuclear submarine production. Combat Systems, built through acquisitions starting with Chrysler's tank division, generates 19% of revenues from armored vehicles and munitions. Technologies, supercharged by the $9.7 billion CSRA acquisition in 2018, represents 28% of revenues from IT services and mission systems. And Aerospace, centered on Gulfstream's luxury business jets, contributes 23% of revenues while serving as the company's most visible consumer-facing brand.

What makes General Dynamics particularly fascinating from an investment perspective is how it has defied conventional wisdom about defense contractors. While pure-play defense companies trade on government budget cycles and program wins, General Dynamics has deliberately cultivated revenue streams that zig when defense spending zags. Gulfstream's business jets serve Fortune 500 CEOs and ultra-high-net-worth individuals who care nothing about Pentagon budgets. The company's IT services benefit from the inexorable digitization of government, regardless of whether defense spending rises or falls. Even within traditional defense, General Dynamics has positioned itself in markets—like nuclear submarines—where barriers to entry are so high that competition is essentially impossible.

The financial architecture that supports this strategy is equally distinctive. In 2024, the company generated $4.1 billion in operating cash flow, representing 109% of net earnings—a cash conversion rate that would make even the best software companies envious. Management has deployed this cash with discipline, investing $916 million in capital expenditures while returning $3 billion to shareholders through dividends and buybacks. The company maintains a fortress balance sheet with a debt-to-equity ratio that gives it flexibility to pursue large acquisitions when opportunities arise.

As we trace General Dynamics' 125-year journey, we'll explore not just what happened, but why it matters for understanding defense, industrial strategy, and capital allocation. We'll meet characters like John Jay Hopkins, the visionary who created General Dynamics because he believed "Electric Boat" was too limiting a name for his ambitions. Bill Anders, the Apollo 8 astronaut turned CEO who looked at General Dynamics' sprawling portfolio in 1991 and decided to blow it up. And Phebe Novakovic, the former CIA operative who has led the company since 2013 and orchestrated its largest acquisition ever while maintaining industry-leading margins.

This is ultimately a story about adaptation—how a company survived the transition from World Wars to Cold War to the War on Terror to today's great power competition. It's about the paradox of peacetime preparation, where democracies must invest billions in weapons they hope never to use. And it's about the peculiar dynamics of an industry where your customer concentration would terrify any MBA student—69% of revenues from a single client—yet that customer is the most creditworthy entity on Earth: the United States government.

II. Origins: Electric Boat & The Submarine Legacy (1899-1952)

The year is 1897, and John Philip Holland is standing waist-deep in the Passaic River in New Jersey, watching his sixth submarine prototype slowly sink—not in the controlled manner he intended, but in the catastrophic way that means another fortune lost and another round of ridicule from the press. The New York Times has taken to calling him "the eccentric Irishman with his fantastic schemes." His financial backers, the Fenian Brotherhood—Irish revolutionaries who wanted submarines to sink British ships—have long since abandoned him after he refused to weaponize his earlier designs for their cause. Holland is 56 years old, nearly deaf from years of working in engine rooms, and down to his last few hundred dollars.

But Holland possesses something more valuable than money: a vision of underwater warfare that every major navy has dismissed as impossible. Submarines, the experts claim, are suicide machines—unstable on the surface, blind underwater, and prone to killing their crews through carbon monoxide poisoning or simple drowning. The French have tried with the Gymnote, the Spanish with the Peral, the Russians with the Drzewiecki—all failures or curiosities at best. Yet Holland believes he has solved the fundamental problem that plagued them all: how to create a vessel that is equally stable on the surface and underwater, switching seamlessly between gasoline engines for surface running and electric motors for submerged operations.

His solution emerges in 1898 with the Holland VI, a 54-foot vessel that looks like a steel cigar with a small conning tower. It displaces just 64 tons on the surface, can dive to 75 feet, and carries three torpedoes. More importantly, it actually works. In demonstration after demonstration, Holland proves his submarine can dive, surface, maneuver, and—critically—allow its crew to survive the experience.

Enter Isaac Rice, a German-American lawyer, entrepreneur, and chess enthusiast who has already made one fortune in railroad reorganizations and another in storage batteries. Rice sees what the admirals don't: that Holland has created not just a novel weapon but an entirely new dimension of warfare. In February 1899, Rice orchestrates the consolidation of Holland's Holland Torpedo Boat Company with his own Electric Storage Battery Company, creating the Electric Boat Company with $7 million in capital—enormous money for that era.

Rice's timing proves impeccable. The Spanish-American War of 1898 has just demonstrated America's emergence as a naval power, and Assistant Secretary of the Navy Theodore Roosevelt is pushing for a modern fleet. On April 11, 1900, after exhaustive trials, the U.S. Navy purchases the Holland VI for $150,000, commissioning it as the USS Holland (SS-1)—the first submarine in the American fleet.

What follows is one of the most remarkable monopoly-building exercises in American industrial history. Electric Boat doesn't just sell submarines; it sells the very concept of submarine warfare. Between 1900 and 1914, the company builds 35 submarines for the U.S. Navy and another 24 for foreign navies including Britain, Russia, Japan, and the Netherlands. Rice and his successor, Henry Carse, pursue a strategy that would make today's defense contractors envious: they maintain design expertise in-house while subcontracting actual construction to established shipyards, collecting both design fees and licensing royalties.

The foreign sales, however, trigger the first of many controversies that would dog the company. When World War I erupts in 1914, Electric Boat finds itself in the awkward position of having armed multiple belligerents. British submarines based on Electric Boat designs are hunting German U-boats, which are hunting British vessels, while Electric Boat–designed submarines in various other navies prowl the same waters. Congress launches investigations into war profiteering, though Electric Boat escapes serious sanction by arguing it was simply serving American foreign policy by strengthening allied navies.

World War I transforms Electric Boat from a boutique submarine designer into a genuine defense contractor. The company's workforce at its Groton, Connecticut shipyard swells from 2,000 to over 13,000. Between 1914 and 1918, Electric Boat delivers 85 submarines to the U.S. Navy alone—more than doubling the size of America's submarine fleet. The company pioneers assembly-line techniques for submarine construction, cutting build times from 18 months to under six months for standard designs.

But the Armistice of November 1918 brings catastrophe. Naval treaties limit submarine construction, and the U.S. Navy, believing the submarine threat has been contained, slashes orders. Electric Boat's workforce collapses to barely 1,000 by 1922. Revenue plummets from $35 million in 1918 to under $2 million in 1923. The company survives only by branching into civilian work—building yachts for millionaires, ferry boats for New York Harbor, and even all-aluminum rail cars for the New Haven Railroad.

The interwar years become a case study in the challenges of being a specialized defense contractor during peacetime. Henry Carse, who takes over as president in 1925, keeps the company alive through a combination of foreign sales (particularly to Peru and Argentina), maintenance contracts for existing submarines, and increasingly desperate diversification attempts. Electric Boat tries everything: speedboats, motors for industrial applications, even a brief foray into aircraft with the acquisition of Canadair. Most fail, but they keep the design teams intact and the shipyard operational.

Salvation comes from an unexpected source: Admiral Hyman G. Rickover and the nuclear revolution. In the late 1940s, Rickover—a difficult, demanding, and visionary naval officer—becomes convinced that nuclear power can revolutionize submarine warfare. A nuclear submarine wouldn't need to surface to recharge batteries or refresh air; it could stay submerged essentially indefinitely, limited only by food supplies for the crew. Rickover chooses Electric Boat as the primary contractor for this ambitious project, partly because of its submarine expertise but mostly because its Groton shipyard is one of the few facilities capable of handling the complex construction.

The program nearly bankrupts Electric Boat again. Building the USS Nautilus (SSN-571) requires not just new construction techniques but entirely new supply chains for nuclear-grade components. The company invests millions it doesn't have, betting everything on Rickover's vision. John Jay Hopkins, who becomes president in 1947, mortgages essentially every asset the company owns to finance the nuclear submarine program.

On January 21, 1954, First Lady Mamie Eisenhower christens the Nautilus with the traditional breaking of a champagne bottle, and speaks the historic words: "I christen thee Nautilus." When the submarine slides into the Thames River, it represents more than just a new vessel—it's the beginning of the nuclear navy and Electric Boat's transformation into something much larger than a submarine builder.

Hopkins, watching from the platform, has already decided that Electric Boat is too small a vision for what he wants to build. He has spent years studying the emerging military-industrial complex, recognizing that future wars will be fought not just underwater but in the air, on land, in space, and increasingly in the electromagnetic spectrum. A company called "Electric Boat" can't credibly bid on aircraft contracts or missile systems. It needs a new identity that signals broader ambitions.

III. The Birth of General Dynamics: Conglomerate Building (1952-1970s)

John Jay Hopkins was not supposed to be running Electric Boat. A lawyer by training who had worked his way up through the company's legal department, Hopkins had the mild manner of a tax attorney and the strategic mind of a chess grandmaster. In 1947, when he became president at age 53, Electric Boat was essentially a one-product company in a one-customer market—building submarines for the U.S. Navy. Hopkins looked at the emerging Cold War landscape and saw both enormous opportunity and existential risk. "A company dependent on submarines alone," he told his board, "is like a farmer with one crop—vulnerable to any change in weather."

Hopkins had spent the previous five years quietly studying the strategies of the great conglomerates being built across American industry. He was particularly fascinated by Textron, which Royal Little had transformed from a textile company into a diversified industrial holding company through aggressive acquisitions. But Hopkins envisioned something different—not just a collection of unrelated businesses, but an integrated defense contractor that could offer the Pentagon complete weapons systems rather than individual components.

On February 21, 1952, Hopkins executed the corporate reorganization he had been planning for years. Electric Boat Company was reorganized as a subsidiary of a new holding company with a name chosen to signal unlimited ambitions: General Dynamics Corporation. The name itself was Hopkins' masterstroke—"General" suggested comprehensive capability while "Dynamics" implied cutting-edge technology and constant motion. It was deliberately vague enough to encompass anything from submarines to spacecraft.

Hopkins wasted no time putting his vision into action. On March 4, 1953—barely a year after creating General Dynamics—he announced the acquisition of Consolidated Vultee Aircraft Corporation (Convair) from the Atlas Corporation for $200 million. It was a staggering sum for a company with Electric Boat's balance sheet, requiring complex financing that pushed General Dynamics' debt-to-equity ratio to levels that made Wall Street analysts nervous.

Convair brought General Dynamics instant credibility in aerospace. Based in San Diego with major facilities in Fort Worth, Convair was already building the F-102 Delta Dagger interceptor and had won the contract for what would become the F-106 Delta Dart—the ultimate expression of the "Century Series" fighters. More intriguingly, Convair was developing the Atlas intercontinental ballistic missile, which would become America's first operational ICBM and later launch John Glenn into orbit.

But Hopkins saw Convair as more than just a military aircraft builder. The company had ambitious plans for commercial aviation with the Convair 880 and 990 jetliners—sleek, fast aircraft designed to compete with Boeing's 707 and Douglas' DC-8. Hopkins believed that General Dynamics could leverage defense technology to dominate commercial markets, creating a virtuous cycle where civilian sales would smooth out the volatility of defense contracts.

The Convair jetliner program would become one of the most spectacular failures in aviation history. The 880 and 990 were engineering marvels—faster than their competitors, with innovative features like leading-edge slats and area-ruled fuselages that reduced drag. But they were also fuel-hungry, expensive to operate, and arrived just as the market was shifting toward larger, more economical aircraft. General Dynamics lost $425 million on the program—roughly $4 billion in today's dollars—forcing the company to take what was then the largest corporate write-off in American history in 1961.

Yet even as the commercial aircraft program hemorrhaged money, other parts of Hopkins' empire-building succeeded brilliantly. In 1959, he orchestrated a merger with Henry Crown's Material Service Corporation, a Chicago-based construction materials company that brought not just diversification but also Crown himself—a legendary investor and dealmaker who would become General Dynamics' largest shareholder and most influential board member for the next three decades.

The Crown merger exemplified Hopkins' approach to building General Dynamics: find successful entrepreneurs, give them autonomy to run their businesses, but integrate them into a larger strategic vision. Crown's construction materials business had nothing to do with defense, but it generated steady cash flows that could support the enormous capital requirements of weapons development. It also brought political connections in Chicago and the Midwest that complemented General Dynamics' existing relationships on the coasts.

Hopkins didn't live to see his vision fully realized. He died suddenly of a heart attack in May 1957 at age 63, leaving behind a company that had grown from $100 million to over $1 billion in revenue but was struggling to digest its rapid expansion. His successor, Frank Pace Jr.—a former Secretary of the Army under Truman—inherited a company with brilliant individual pieces that didn't quite fit together.

Pace's tenure from 1957 to 1962 was marked by both triumph and near-disaster. On the triumph side, General Dynamics' Fort Worth division won the competition for the TFX (Tactical Fighter Experimental) program in 1962, which would become the F-111 Aardvark. It was the largest military aircraft contract ever awarded at that time—potentially worth $7 billion. The F-111 was supposed to be everything to everyone: a fighter for the Air Force, a fleet interceptor for the Navy, a strategic bomber for Strategic Air Command, and even a close-air-support aircraft for the Army.

The F-111 program became a cautionary tale about the perils of trying to create a universal military aircraft. The Navy version was cancelled after building just seven prototypes—too heavy for carrier operations. The Air Force variants suffered from cost overruns, technical problems, and tragic crashes during the Vietnam War. Yet paradoxically, the F-111 eventually matured into an excellent aircraft, serving with distinction in Libya, Desert Storm, and numerous other operations until its retirement in 1996. But by then, the program had become synonymous with procurement dysfunction, and General Dynamics had lost hundreds of millions on fixed-price contracts that didn't account for the technical risks.

Roger Lewis, who took over as CEO in 1962, tried to restore discipline while maintaining Hopkins' diversification strategy. Under Lewis, General Dynamics acquired Liquid Carbonic Corporation, a major producer of industrial gases, and continued expanding its electronics and telecommunications divisions. The company even briefly entered the nuclear power industry, building reactor vessels and components for civilian power plants.

But the real action was in Fort Worth, where General Dynamics was simultaneously building F-111s, developing the YF-16 (which would become the F-16 Fighting Falcon), and maintaining production of the B-58 Hustler supersonic bomber. The Fort Worth facility became one of the largest aircraft manufacturing complexes in the world, employing over 30,000 workers at its peak.

David S. Lewis (no relation to Roger) became CEO in 1970 and would lead the company through one of its most successful periods. A legendary aerospace engineer who had previously run McDonnell Douglas, David Lewis understood both the technical and political dimensions of defense contracting. He fixed the F-111 program's execution problems, won the F-16 competition against Northrop's YF-17, and expanded Electric Boat's submarine construction to include the new Los Angeles-class attack submarines.

The F-16 victory in 1975 was particularly sweet. The Air Force had initially resisted the idea of a lightweight fighter, preferring the heavy, complex F-15 Eagle. But a group of defense reformers known as the "Fighter Mafia"—including maverick designer Pierre Sprey and test pilot Chuck Yeager—pushed for a simpler, more maneuverable aircraft. The YF-16's fly-by-wire controls, bubble canopy, and side-mounted control stick made it revolutionary. When it defeated Northrop's YF-17 in the fly-off competition, General Dynamics won not just a U.S. Air Force contract but eventual sales to dozens of allied nations. The F-16 would become the most successful Western fighter jet of its generation, with over 4,600 built.

Yet even as the F-16 program succeeded, cracks were appearing in the conglomerate model. General Dynamics by 1985 had become almost impossibly complex: submarines in Connecticut and Rhode Island, aircraft in Fort Worth and San Diego, tanks in Michigan (after acquiring Chrysler Defense in 1982), missiles in California, electronics in dozen locations, and various commercial businesses scattered across the country. The company had also acquired Cessna Aircraft in 1985 for $663 million, adding general aviation to its portfolio.

Henry Crown, who had remained the company's largest shareholder and most influential director, was growing concerned. In private board meetings, he questioned whether any management team could effectively run such a diverse enterprise. The stock price languished despite strong revenue growth, suggesting that investors saw the conglomerate structure as destroying rather than creating value. Crown began looking for new leadership—someone who could make the hard decisions about what General Dynamics should and shouldn't be.

IV. The Great Divestiture: Anders' Radical Restructuring (1990-1996)

William Anders had already lived several lifetimes before becoming CEO of General Dynamics in January 1991. As an Apollo 8 astronaut, he had taken the famous "Earthrise" photograph—the first color image of Earth from deep space that became an icon of the environmental movement. As a nuclear engineer, he had worked on reactor designs for the Air Force. As a businessman, he had run Textron's aerospace division and served as U.S. Ambassador to Norway. But nothing in his varied career had prepared him for what he found when he arrived at General Dynamics' headquarters.

"It was like walking into a corporate emergency room," Anders would later recall. "The patient was bleeding from multiple wounds, and everyone was arguing about which one to treat first."

The numbers were stark. The Berlin Wall had fallen in 1989, and with it, the fundamental rationale for America's massive defense buildup of the 1980s. Defense Secretary Dick Cheney had announced plans to cut defense spending by 25% over five years. The "peace dividend" that politicians promised voters meant disaster for defense contractors. General Dynamics' stock had fallen from $65 to $25. The company's commercial aircraft division was losing money. The Space Systems division was struggling. Even the vaunted F-16 program faced declining orders as the Air Force shifted resources to the stealthy F-22.

Anders spent his first month visiting every major General Dynamics facility, talking to engineers, walking production lines, and reviewing financial statements. What he found convinced him that incremental change wouldn't save the company. At a board meeting in March 1991, he presented a radical proposal: General Dynamics should sell or close two-thirds of its operations, focusing only on businesses where it had clear competitive advantages.

The board was stunned. General Dynamics had spent four decades building itself into a diversified defense conglomerate. Now Anders wanted to tear it apart? Henry Crown, then 94 years old but still sharp, asked the crucial question: "Bill, are you trying to shrink this company to greatness?"

"No, Mr. Crown," Anders replied. "I'm trying to save it."

Anders' strategy was elegant in its simplicity but brutal in its execution. He divided General Dynamics' businesses into three categories: core businesses to keep and strengthen, valuable businesses to sell at maximum price, and troubled businesses to close or give away. The key insight was timing—Anders recognized that other defense contractors were still in acquisition mode, believing they could weather the defense downturn through consolidation. He would sell to them before they realized the party was over.

The first major divestiture came in December 1992: Cessna Aircraft to Textron for $600 million. General Dynamics had bought Cessna just seven years earlier for $663 million, so the sale represented a modest loss. But Anders saw that general aviation had no synergies with defense and that Textron, which already owned Bell Helicopter, would pay a fair price for the prestigious Cessna brand.

Next came the missile business. In May 1992, Anders sold General Dynamics' missile operations to Hughes Aircraft (then owned by General Motors) for $450 million. The business included the Standard Missile, Stinger, and several classified programs. Critics argued that General Dynamics was selling irreplaceable technology. Anders countered that the company lacked the scale to compete with Raytheon and Hughes in missiles—better to exit with dignity than slowly bleed to death.

The real shock came in December 1992 when Anders announced the sale of General Dynamics' Fort Worth aircraft division to Lockheed for $1.5 billion. Fort Worth was where General Dynamics built the F-16, one of the most successful fighter jets in history. The division had a backlog worth billions and relationships with air forces worldwide. Employees in Fort Worth burned Anders in effigy. Texas politicians accused him of betraying American aerospace workers. But Anders had run the numbers: without new fighter programs, Fort Worth would become a wasting asset. Lockheed, which needed production capacity for the F-22, would pay premium price.

The Fort Worth sale marked a turning point in defense consolidation. It signaled that even crown jewel assets were for sale if the price was right. Within months, Martin Marietta bought General Dynamics' Space Systems division for $209 million. McDonnell Douglas acquired the Convair aircraft structures business for $100 million. By the end of 1994, Anders had sold over $3 billion in assets.

But Anders wasn't just selling—he was also buying, selectively. In 1995, he acquired Bath Iron Works, a Maine shipyard that built Arleigh Burke-class destroyers, for $300 million. The acquisition gave General Dynamics a second major shipyard to complement Electric Boat, creating the foundation for what would become Marine Systems. He also invested heavily in upgrading Electric Boat's facilities, positioning the company to build the next generation of nuclear submarines.

The most painful decision was closing what remained of Convair. The San Diego operation that had once built Atlas rockets and conceived the Convair 880 was reduced to building fuselages for other companies' aircraft. In March 1994, Anders announced Convair would cease operations entirely by 1996. Over 8,000 jobs would be eliminated. San Diego, which had been an aerospace center since the 1920s, lost one of its iconic companies.

Anders faced withering criticism from multiple quarters. Labor unions accused him of destroying American industrial capacity. Politicians said he was sacrificing long-term competitiveness for short-term profits. Even some board members questioned whether he had gone too far. But Anders had a powerful ally in Henry Crown's son Lester, who had succeeded his father as the family's representative on the board. Lester Crown understood that Anders was performing necessary surgery to save the patient.

The financial results vindicated Anders' strategy. By recycling capital from low-return businesses to high-return ones, he improved General Dynamics' operating margins from 5% to over 15%. The company's debt fell from $1.4 billion to essentially zero. Most remarkably, even as revenue shrank from $10 billion to $3 billion, earnings per share actually increased. The stock price rose from $25 when Anders arrived to over $100 when he retired as CEO in 1996.

Anders had one more surprise for his critics. Throughout the restructuring, he had insisted that General Dynamics maintain its dividend and actually increase it when possible. He also initiated massive share buybacks, reducing the share count by 30%. Shareholders who had stuck with the company through the painful restructuring were richly rewarded. A dollar invested when Anders became CEO was worth four dollars when he stepped down.

The Anders transformation became a Harvard Business School case study in corporate restructuring. He had taken a bloated conglomerate on the edge of crisis and transformed it into a focused, highly profitable defense contractor. But perhaps more importantly, he had demonstrated that in defense, as in any industry, sacred cows could be slaughtered if the logic was compelling enough.

Nicholas Chabraja, who succeeded Anders as CEO in 1996, inherited a company that was lean, focused, and cash-rich—perfectly positioned for the next phase of its evolution. The question was: what should General Dynamics become next? The answer would surprise everyone, including Chabraja himself.

V. The Gulfstream Acquisition: Return to Aviation (1999)

Nicholas Chabraja was in his corner office overlooking the Potomac River when the call came through in early 1999. Theodore "Ted" Forstmann, the legendary leveraged buyout pioneer, wanted to discuss something confidential. Forstmann owned Gulfstream Aerospace, the premier manufacturer of business jets, and he was ready to sell. The asking price: $5 billion.

Chabraja's first instinct was to laugh. Just three years earlier, General Dynamics had completed Bill Anders' radical restructuring by selling its last aerospace asset—the Fort Worth division that built F-16 fighters. The company had publicly declared it was exiting aviation to focus on ships, submarines, and land systems. Now Forstmann wanted General Dynamics to pay $5 billion to get back into aerospace?

"Ted, you know we just got out of the airplane business," Chabraja said.

"Nick, you got out of the military airplane business," Forstmann replied. "This is completely different. These planes are sold to CEOs and billionaires, not generals and admirals. The margins are better, the customers pay cash, and there's no such thing as a peace dividend in the business jet market."

Forstmann had a point. Gulfstream operated in an entirely different universe from military aviation. Its customers were Fortune 500 corporations, ultra-high-net-worth individuals, and fractional ownership companies like NetJets. The company's flagship G-V could fly 6,500 nautical miles—New York to Tokyo nonstop—while cruising at Mach 0.88. It wasn't just transportation; it was a flying boardroom, a productivity tool for executives who measured time in millions of dollars per hour.

Chabraja assembled a small team to evaluate Gulfstream, keeping the project so secret that they code-named it "Project Golf"—a reference both to Gulfstream's G-series aircraft and to the fact that many of its customers bought jets to reach golf courses worldwide. What they found was intriguing. Gulfstream had 45% gross margins on new aircraft sales and 20% operating margins overall—far better than General Dynamics' defense businesses. The company had a backlog worth $6 billion and was developing the G550 and G500, next-generation aircraft that would extend its technological lead.

But what really caught Chabraja's attention was the business model. Unlike commercial aviation, where Boeing and Airbus engaged in ruinous price competition for airline orders, business jet manufacturers could maintain pricing discipline. Gulfstream's only real competitors were Bombardier and Dassault, and each had carved out distinct market segments. Gulfstream owned the ultra-long-range, large-cabin segment—the most profitable part of the market.

The due diligence team discovered something else: Gulfstream's service business was a gold mine. The company didn't just sell jets; it provided maintenance, upgrades, and support for the entire fleet. This generated recurring revenue with even higher margins than new aircraft sales. As one team member put it, "It's like selling razors and razor blades, except the razors cost $50 million and the blades cost $5 million a year."

On May 18, 1999, Chabraja announced that General Dynamics would acquire Gulfstream for $5.3 billion—$2.5 billion in cash and $2.8 billion in assumed debt. The stock market's reaction was swift and brutal. General Dynamics' shares fell 10% in a single day. Analysts questioned why a defense contractor would buy a business jet manufacturer. Several major shareholders called for an emergency board meeting.

The criticism was particularly harsh because of the price. Forstmann had bought Gulfstream just nine years earlier for $850 million (including debt). Now he was selling it for more than six times that amount. The financial press portrayed Chabraja as a sucker who had enriched Forstmann at shareholders' expense.

But Chabraja had done his homework. In a series of investor presentations, he laid out the strategic logic. First, Gulfstream would diversify General Dynamics away from pure defense dependency. In 1999, 95% of the company's revenue came from the U.S. government. Gulfstream would immediately drop that to below 80%. Second, business jets were countercyclical to defense spending. When defense budgets fell, corporate profits and wealth creation typically rose, driving business jet demand. Third, Gulfstream's international sales would give General Dynamics exposure to global wealth creation, particularly in emerging markets like China, Russia, and the Middle East.

The integration of Gulfstream proved smoother than anyone expected. Chabraja made the brilliant decision to leave Gulfstream's management team intact and its Savannah, Georgia headquarters autonomous. He didn't try to impose General Dynamics' government contracting culture on a company that sold to movie stars and hedge fund titans. Instead, he provided capital for product development and used General Dynamics' balance sheet to offer attractive financing to customers.

The results exceeded even Chabraja's optimistic projections. In 2000, its first full year under General Dynamics ownership, Gulfstream delivered 91 aircraft and generated $3.2 billion in revenue. By 2008, it was delivering 156 aircraft annually and generating $5.5 billion in revenue. The G550, launched in 2003, became the best-selling ultra-long-range business jet in history. The G650, introduced in 2012, pushed the boundaries even further—flying 7,000 nautical miles at Mach 0.925, just below the speed of sound.

Gulfstream's success wasn't just about building better aircraft. The company understood that business jet ownership was as much about status and service as transportation. Gulfstream's customer service operation became legendary. The company maintained service centers worldwide, stockpiled spare parts worth hundreds of millions of dollars, and guaranteed that any Gulfstream aircraft anywhere in the world could be serviced within 24 hours. When a G-V owned by a Saudi prince broke down in Kazakhstan, Gulfstream flew a repair team and parts from Germany within six hours.

The company also mastered the art of selling to the ultra-wealthy. Gulfstream's sales process was more like selling luxury real estate than aircraft. Potential customers were invited to Savannah for personalized demonstrations, where they could configure custom interiors with exotic woods, hand-stitched leather, and even gold-plated fixtures. The company maintained relationships with interior designers who specialized in creating flying palaces for Middle Eastern royalty and Silicon Valley billionaires.

The 2008 financial crisis provided the ultimate test of Chabraja's diversification strategy. As Wall Street collapsed and corporate America retrenched, business jet orders evaporated. Gulfstream's order book shrank by 40% in six months. Critics said General Dynamics would rue the day it bought a luxury product company. But two things saved Gulfstream. First, international demand, particularly from China and the Middle East, remained relatively strong. Second, General Dynamics' defense businesses were booming thanks to Iraq and Afghanistan war spending. The company could afford to carry Gulfstream through the downturn without cutting research and development.

By 2010, Gulfstream had not only recovered but emerged stronger. Competitors like Cessna and Hawker Beechcraft had slashed employment and cancelled new aircraft programs during the recession. Gulfstream had continued developing the G650, which entered service in 2012 to extraordinary demand. The aircraft had a three-year waiting list, and used G650s were selling for more than new ones—unheard of in aviation.

Phebe Novakovic, who became CEO in 2013, doubled down on Gulfstream. She approved development of the G500 and G600, which filled the gap between Gulfstream's mid-size and ultra-long-range aircraft. She also expanded Gulfstream's service network, acquiring aviation services companies that could maintain not just Gulfstream jets but competitors' aircraft as well. The message was clear: Gulfstream wasn't just participating in the business jet market; it intended to dominate it.

The COVID-19 pandemic initially seemed like it would devastate business aviation. Commercial airlines grounded flights, corporations banned travel, and economic uncertainty froze capital spending. But something unexpected happened. Wealthy individuals and corporations, desperate to avoid crowded commercial airports and flights, turned to private aviation. Gulfstream's order book actually grew during the pandemic. By 2021, the company had a record backlog worth over $18 billion.

Today, Gulfstream contributes roughly $8 billion annually to General Dynamics' revenue—making it the company's second-largest segment after Marine Systems. More importantly, it generates operating margins above 15%, the highest of any General Dynamics division. The business that Wall Street hated in 1999 has generated over $15 billion in operating profit since the acquisition, multiples of the purchase price.

The Gulfstream acquisition validated a crucial lesson: sometimes the best strategic moves are the ones that seem to contradict previous strategies. Anders had been right to exit military aviation in the 1990s when General Dynamics lacked competitive advantage. Chabraja was equally right to enter business aviation in 1999 when a unique asset became available. The key was recognizing that Gulfstream wasn't really an aerospace company—it was a luxury brand that happened to make aircraft.

VI. The CSRA Mega-Deal: Betting Big on IT Services (2018)

Phebe Novakovic was reviewing classified intelligence reports in her secure office when the idea crystallized. It was late 2017, and the General Dynamics CEO—a former CIA intelligence officer who had spent years analyzing Soviet submarine capabilities—was seeing patterns that others missed. Every military program, every intelligence operation, every government function was becoming fundamentally dependent on information technology. Yet most defense contractors were running away from IT services, viewing it as a low-margin commodity business.

"Everyone else is zagging," she told her strategy team. "Maybe it's time we zig."

The IT services landscape in federal contracting had become a graveyard of failed ambitions. Lockheed Martin had spun off its IT business. L-3 Communications was desperately trying to sell its services division. Northrop Grumman had divested most of its IT operations. The conventional wisdom was clear: IT services was a scale business with single-digit margins, intense competition from pure-play providers like SAIC and Booz Allen, and constant pricing pressure from government customers demanding more for less.

But Novakovic saw something different. She had run General Dynamics' Marine Systems division before becoming CEO, overseeing the construction of Virginia-class submarines that were as much software platforms as steel vessels. A modern submarine contained more lines of code than Windows 10. The F-35 fighter had 8 million lines of code. The challenge wasn't just building hardware anymore—it was integrating impossibly complex systems, securing them against cyber threats, and maintaining them through decades of software updates.

CSRA—Computer Sciences Corporation's government services business that had merged with SRA International in 2015—appeared on Novakovic's radar in mid-2017. The company was struggling as a standalone entity, with its stock price languishing despite $5 billion in annual revenue and decent margins. The market didn't know how to value a pure-play government IT services company that lacked the growth profile of commercial technology firms but also lacked the stability of traditional defense contractors.

Novakovic dispatched a team to quietly assess CSRA. What they found was intriguing. CSRA had prime positions on massive government-wide acquisition contracts worth potentially hundreds of billions over their lifetimes. The company held top-secret facility clearances and employed thousands of engineers with the highest security clearances—assets that took decades to build and couldn't be replicated by commercial IT companies trying to enter the federal market. Most importantly, CSRA's customer base overlapped significantly with General Dynamics' existing defense and intelligence customers.

In November 2017, Novakovic made her first approach to CSRA's CEO, Larry Prior. The initial conversations were exploratory—feeling out whether a combination made strategic sense. Prior was receptive but cautious. CSRA had already been through one major merger, and employees were exhausted from integration efforts. Any acquirer would need to offer not just a good price but a compelling vision for the combined entity.

On February 14, 2018—Valentine's Day—General Dynamics announced it would acquire CSRA for $9.6 billion, including $2.8 billion in debt assumption. It was the largest acquisition in General Dynamics' history, 40% bigger than the Gulfstream deal that had defined Chabraja's tenure. The offer price of $41.25 per share represented a 32% premium to CSRA's closing price the day before.

The reaction was mixed, to put it mildly. General Dynamics' stock fell 4% on the announcement. Analysts questioned why the company would pay such a rich premium for a business that generated operating margins of 8%—half of General Dynamics' overall margins. One analyst called it "an expensive bet on a commoditizing business." Another worried that General Dynamics was trying to buy growth because its traditional defense businesses were maturing.

But within 48 hours, the plot thickened. CACI International, another government IT services provider, announced an unsolicited bid for CSRA at $44 per share—7% higher than General Dynamics' offer. Suddenly, what looked like an overpriced acquisition became a bidding war. CACI argued that it had better synergies with CSRA and could offer a higher price with more cash and less stock.

Novakovic faced a crucial decision. She could raise her bid and risk overpaying for CSRA. She could walk away and preserve capital for other opportunities. Or she could find a creative solution that would make General Dynamics' offer more attractive without simply throwing more money at the problem.

Her response was masterful. Instead of immediately raising the price, General Dynamics accelerated the timeline for closing the deal and offered CSRA shareholders more certainty. The company pointed out that its bid was all-cash, while CACI's higher offer included stock that might fluctuate. General Dynamics also emphasized its track record of successful acquisitions and its commitment to keeping CSRA's workforce intact—a crucial consideration for a company whose primary assets were its people and their security clearances.

On March 27, 2018, Novakovic raised General Dynamics' offer to $41.25 per share—a modest increase—but coupled it with iron-clad commitments about timing and integration. CSRA's board, after extensive deliberation, recommended General Dynamics' offer to shareholders. The deal closed on April 3, 2018, in one of the fastest major acquisitions ever completed in the defense industry.

The integration of CSRA into what became General Dynamics Information Technology (GDIT) proved that Novakovic had learned from her predecessors' successes and failures. Rather than trying to merge CSRA into General Dynamics' existing Mission Systems unit, she kept it separate, preserving its culture and customer relationships. She appointed Amy Gilliland, a CSRA veteran, to run GDIT, signaling continuity to both employees and customers.

The strategic logic of the acquisition became apparent almost immediately. GDIT wasn't just providing IT services; it was becoming the digital backbone of American national security. The division worked on everything from modernizing the Pentagon's logistics systems to securing classified intelligence networks to building cloud infrastructure for civilian agencies. When the COVID-19 pandemic struck, GDIT was instrumental in enabling massive government telework initiatives, helping agencies maintain operations despite lockdowns.

What really validated Novakovic's vision was the explosion in cybersecurity spending. Every government agency, from the Department of Defense to the Social Security Administration, was under constant cyber attack from nation-states and criminal groups. GDIT's expertise in securing classified networks became invaluable. The company won multi-billion-dollar contracts to modernize and secure government IT infrastructure, with margins that steadily improved as the work became more specialized and critical.

By 2024, GDIT was generating over $13 billion in annual revenue—more than double CSRA's standalone revenue at the time of acquisition. More impressively, operating margins had improved from 8% to nearly 11%, approaching General Dynamics' overall margins. The division that analysts had dismissed as a low-margin commodity business was generating over $1.4 billion in annual operating profit.

The CSRA acquisition also transformed General Dynamics' competitive position. The company was no longer just a platform provider—building ships, aircraft, and vehicles. It was now a comprehensive solutions provider that could offer integrated packages of hardware, software, and services. When the Navy needed new submarines, General Dynamics could provide not just the boat but also the combat management system, the training simulators, and the lifecycle support. This integration capability became a powerful differentiator in competitions for major programs.

Novakovic's bet on IT services looked even smarter as artificial intelligence and machine learning became critical to military superiority. GDIT was at the forefront of integrating AI into defense systems, from predictive maintenance for military vehicles to pattern recognition in intelligence analysis. The company's Project Maven work—using AI to analyze drone footage—became a template for how machine learning could enhance military capabilities.

The cultural integration proved surprisingly smooth. GDIT's workforce of software engineers and data scientists found that working for a major defense contractor provided stability and resources that standalone IT services firms couldn't match. General Dynamics' other divisions discovered that having an in-house IT powerhouse helped them win competitions by offering more comprehensive solutions. The synergies that skeptics had questioned materialized in ways that even Novakovic hadn't fully anticipated.

VII. Modern Operations: Four Pillars of Power

Walking through General Dynamics' operations today is like touring four different companies that happen to share a corporate parent. At Electric Boat's Groton shipyard, welders in protective gear work on submarine hulls so secret that photography is forbidden even for corporate executives. At Gulfstream's Savannah facility, craftsmen hand-stitch leather interiors for jets that will carry Hollywood celebrities and tech billionaires. At the Lima Army Tank Plant in Ohio, M1 Abrams tanks roll off assembly lines headed for Poland and Taiwan. And in secure facilities across Northern Virginia, software engineers write code that protects America's most sensitive intelligence networks.

Each of these businesses would be a Fortune 500 company on its own. Together, they form a carefully orchestrated portfolio that generates $47.7 billion in annual revenue while maintaining the flexibility to adapt to changing defense priorities and global threats. Understanding how these four pillars operate—and more importantly, how they interact—reveals why General Dynamics has consistently outperformed both pure-play defense contractors and diversified industrials.

Aerospace: The Luxury Premium

Gulfstream's Savannah headquarters feels more like a luxury hotel than a manufacturing facility. The customer center features marble floors, original artwork, and a full-scale mock-up of a G700 interior where prospective buyers can experience what $75 million buys in private aviation. This is intentional. As Gulfstream president Mark Burns explains, "We're not selling transportation. We're selling time, privacy, and possibility."

The numbers back up this positioning. Gulfstream's average selling price per aircraft has risen from $35 million in 2010 to over $65 million in 2024, even as production volumes have remained relatively stable at 120-140 aircraft per year. This pricing power comes from relentless product improvement. The new G700, certified in 2024, can fly 7,750 nautical miles at Mach 0.90—far enough to connect virtually any two cities on Earth with just one stop. Its cabin altitude at 41,000 feet is just 2,916 feet, reducing passenger fatigue on ultra-long flights.

But the real magic happens in Gulfstream's service business. The company maintains a fleet of over 3,000 aircraft in service worldwide, each requiring regular maintenance, upgrades, and support. Service revenues now exceed $2 billion annually with margins above 20%. When a Gulfstream needs an engine replacement in Dubai or avionics upgrade in Shanghai, the company's global service network responds within hours. This creates switching costs that make customers reluctant to change manufacturers—once you're in the Gulfstream ecosystem, leaving means giving up a support infrastructure that no competitor can match.

The acquisition of Jet Aviation in 2019 for $580 million expanded this service footprint dramatically. Jet Aviation operates fixed-base operations (FBOs) at major airports worldwide, providing fueling, hangar space, and concierge services not just for Gulfstream jets but for all business aircraft. This gives General Dynamics intelligence on competitor aircraft movements, customer preferences, and market trends that inform both product development and sales strategies.

Marine Systems: The Submarine Monopoly

Electric Boat's Quonset Point facility in Rhode Island looks like something from science fiction. Inside massive buildings the size of multiple football fields, sections of Virginia-class submarines take shape using modular construction techniques that would have amazed the shipbuilders of John Holland's era. Each submarine contains over 1 million parts, 425 miles of cable, and enough steel to build 1,200 automobiles. Yet Electric Boat and its workforce of 22,000 can now deliver two Virginia-class submarines per year, with plans to increase to three annually by 2028.

The economics of submarine construction are unlike anything else in manufacturing. A single Virginia-class submarine costs approximately $3.5 billion and takes six years to build. The Columbia-class ballistic missile submarines now in early production will cost over $8 billion each. These are not products where customers comparison shop or negotiate aggressively on price. The U.S. Navy needs these submarines for strategic deterrence, and Electric Boat (along with partner Newport News Shipbuilding) are the only companies on Earth capable of building them.

This monopoly position creates extraordinary pricing power but also enormous responsibility. When Electric Boat fell behind schedule on Virginia-class deliveries in 2020-2021, it created a strategic vulnerability for the United States as China rapidly expanded its submarine fleet. The company responded by investing $1.8 billion in facility improvements, hiring 5,000 new workers annually, and partnering with community colleges to create submarine manufacturing training programs. The investment is paying off—delivery delays have been reduced from 12 months to 3 months, with further improvements expected.

Bath Iron Works, acquired during the Anders restructuring, provides crucial diversification within Marine Systems. The Maine shipyard builds Arleigh Burke-class destroyers, the backbone of the Navy's surface fleet. While Bath faces competition from Huntington Ingalls' Ingalls Shipbuilding, the Navy deliberately maintains two sources for destroyers to ensure competition and reduce risk. Bath has also pioneered digital shipbuilding techniques, using 3D modeling and augmented reality to reduce construction time and improve quality.

NASSCO, General Dynamics' San Diego shipyard, occupies a unique niche building auxiliary ships for the Navy and commercial vessels for civilian customers. The shipyard's ESB (Expeditionary Sea Base) vessels serve as floating military bases that can be positioned anywhere in the world. Its commercial business building container ships and oil tankers provides valuable diversification and helps maintain workforce skills during gaps in military contracts.

Combat Systems: The Democracy Arsenal

The Lima Army Tank Plant tells the story of American industrial resilience. In the 1990s, as the Cold War ended, the facility nearly closed as tank orders evaporated. General Dynamics kept it alive by rebuilding older M1 Abrams tanks, maintaining the crucial industrial base for when it would be needed again. That foresight is paying off spectacularly. The war in Ukraine has demonstrated that tanks remain essential for ground warfare, and orders are pouring in from NATO allies and Pacific partners worried about Chinese aggression.

The modern M1A2 SEPv3 Abrams is a far cry from the original 1980s design. It features depleted uranium armor that can defeat any known anti-tank weapon, a 120mm smoothbore gun that can destroy targets at 3,000 meters, and a digital battle management system that networks with other vehicles and aircraft. Each tank costs approximately $10 million and requires a complex supply chain of specialized suppliers that General Dynamics has cultivated over decades.

But Combat Systems is about more than just tanks. The division's Stryker wheeled combat vehicles have become the workhorse of the U.S. Army, providing protected mobility for infantry units. The latest Stryker variants include a 30mm cannon version that can engage light armor and helicopters, and a directed-energy variant that uses lasers to destroy drones—a capability that has become crucial as small unmanned aircraft proliferate on modern battlefields.

General Dynamics' European operations, built through acquisitions of Steyr-Daimler-Puch's military vehicle business, Santa Bárbara Sistemas in Spain, and Mowag in Switzerland, provide both geographic diversification and technology transfer. The Piranha wheeled armored vehicle family, developed by Mowag, has been sold to dozens of countries and forms the basis for the U.S. Marine Corps' LAV (Light Armored Vehicle) fleet. European operations also produce advanced ammunition, including the programmable airburst rounds that can defeat enemies behind cover.

The integration of these formerly independent companies into a coherent Combat Systems organization demonstrates General Dynamics' acquisition expertise. Rather than forcing American designs on European customers or vice versa, the company maintains distinct product lines while sharing technology and best practices. This approach has made General Dynamics the only defense contractor with significant ground vehicle market share on both sides of the Atlantic.

Technologies: The Digital Backbone

GDIT's operations are largely invisible to the public, hidden behind classified programs and secure facilities. But the division's impact is enormous. When veterans check their benefits online, they're using systems GDIT maintains. When intelligence analysts sift through satellite imagery looking for threats, they're using GDIT-developed software. When the Pentagon moves applications to the cloud, GDIT often provides the migration services and security architecture.

The crown jewel of Technologies is its position on government-wide acquisition contracts like DEOS (Defense Enterprise Office Solution), potentially worth $11.7 billion over 10 years. These contracts give GDIT preferred vendor status for IT services across entire departments, providing steady revenue streams and opportunities to expand into new areas. The company's $7.6 billion COMPASS contract to modernize the Navy's IT infrastructure demonstrates the scale and complexity of modern government technology programs.

Mission Systems, the other half of Technologies, focuses on hardware and software for specific military applications. The division produces everything from nuclear submarine combat systems to satellite communication terminals to ruggedized computers for armored vehicles. What distinguishes Mission Systems is its ability to integrate components from multiple suppliers into functioning systems. When the Army needs a new command-and-control system for artillery units, Mission Systems can design the architecture, source the components, write the software, and provide training and support.

The synergies between GDIT and Mission Systems have exceeded expectations. GDIT's expertise in enterprise IT helps Mission Systems design military systems that can connect to broader networks. Mission Systems' experience with military requirements helps GDIT understand what capabilities warfighters actually need. Together, they can offer comprehensive solutions that pure-play IT companies or traditional defense contractors struggle to match.

VIII. Financial Architecture & Capital Allocation

The conference room on the 20th floor of General Dynamics' Reston headquarters has witnessed some of the most important capital allocation decisions in American industry. It's here that Phebe Novakovic and her CFO, Jason Aiken, review the monthly cash flow reports that would make most CEOs envious. In 2024, General Dynamics generated $4.1 billion in operating cash flow—a 109% conversion rate from net earnings that rivals the best software companies while operating in the capital-intensive world of ships, planes, and tanks.

Understanding how General Dynamics achieves this cash generation—and more importantly, how it deploys that cash—reveals why the company has delivered a 380% total return over the past decade, dramatically outperforming both the S&P 500 and the aerospace & defense index.

The Cash Generation Machine

The magic starts with contract structure. Unlike commercial businesses that deliver products and hope customers pay, General Dynamics typically receives progress payments from the U.S. government as work proceeds. On a $3.5 billion Virginia-class submarine that takes six years to build, the Navy provides periodic payments tied to construction milestones. This means General Dynamics often has negative working capital—it collects cash before incurring all the costs, using customer money to finance operations.

This dynamic is even more pronounced in Gulfstream's business. When a customer orders a G700 for delivery in three years, they typically provide a non-refundable deposit of 10-30% of the purchase price. Gulfstream holds these deposits—currently totaling over $3 billion—and invests them conservatively while building the aircraft. It's essentially an interest-free loan from customers that funds product development and facility expansion.

The company's 2024 performance illustrates this cash-generating power. On revenues of $47.7 billion, General Dynamics generated earnings of $3.8 billion—a healthy 8% net margin. But through working capital management and disciplined capital spending, it converted those earnings into $4.1 billion of free cash flow. This over-100% conversion rate has been consistent for years, not a one-time anomaly.

Contract accounting also provides unusual visibility into future cash flows. General Dynamics ended 2024 with a backlog of $90.6 billion—nearly two years of revenue already contracted. Beyond that, the company has "potential contract value" of $53.4 billion, representing options and extensions that customers are likely to exercise. This $144 billion total potential revenue provides a cash flow stream that's more predictable than most industrial companies and even many utilities.

Capital Deployment Discipline

With billions in annual free cash flow, how General Dynamics allocates capital determines shareholder returns. The company follows a strict hierarchy that has remained consistent across multiple CEOs:

First priority: Organic investment in the business. In 2024, General Dynamics spent $916 million on capital expenditures, focused on expanding submarine production capacity, developing new Gulfstream aircraft, and modernizing manufacturing facilities. This 1.9% of revenue capital intensity is remarkably low for a manufacturing company, reflecting both the government's willingness to fund facility improvements and the company's efficient use of existing assets.

The Columbia-class submarine program exemplifies this approach. The Navy is providing $5 billion in facility improvements at Electric Boat to support construction of the new ballistic missile submarines. General Dynamics contributes expertise and management but doesn't bear the full capital cost. Similarly, when the Army needed to increase tank production, it funded upgrades to the Lima plant rather than expecting General Dynamics to invest speculatively.

Second priority: Strategic acquisitions that strengthen existing businesses or add new capabilities. Since the CSRA acquisition in 2018, General Dynamics has been selective, making smaller "tuck-in" acquisitions that don't strain the balance sheet. The $1.1 billion acquisition of Alion Science and Technology in 2021 added specialized engineering capabilities to GDIT. The purchase of Bluefin Robotics brought unmanned underwater vehicle technology to Marine Systems.

Novakovic has explicitly ruled out transformational acquisitions in the near term, telling investors that "at current valuations, buying back our own stock provides better returns than acquiring competitors." This discipline has prevented General Dynamics from overpaying in the current environment where defense assets trade at premium multiples.

Third priority: Return excess cash to shareholders through dividends and buybacks. General Dynamics has increased its dividend for 33 consecutive years, earning inclusion in the S&P 500 Dividend Aristocrats index. The current quarterly dividend of $1.42 per share yields approximately 2.1%, attractive in a low-rate environment but with room to grow as earnings expand.

Share repurchases provide additional flexibility. In 2024, General Dynamics bought back $1.5 billion worth of stock, reducing the share count by 2.3%. Over the past decade, the company has reduced shares outstanding by 18% through consistent buybacks, meaningfully increasing earnings per share even in years when total earnings grew modestly.

Balance Sheet Fortress

General Dynamics maintains a conservative balance sheet that provides flexibility to weather downturns or pursue opportunities. Total debt of $10.9 billion seems substantial in absolute terms but represents just 0.9x EBITDA—among the lowest leverage ratios in the defense industry. The company's credit ratings of A2/A/A reflect this financial strength, allowing it to borrow at rates just slightly above Treasury yields when needed.

The debt structure is equally conservative. Most borrowings are fixed-rate notes with staggered maturities extending to 2054. This protects against rising interest rates while providing predictable interest expense. The company also maintains a $2 billion undrawn credit facility for additional flexibility, though it hasn't needed to use it in years given strong cash generation.

Pension obligations, often a hidden liability for industrial companies, are well-managed at General Dynamics. The company's defined benefit plans are 95% funded, with assets of $12.8 billion against obligations of $13.5 billion. Investment returns have generally exceeded assumptions, and the company has been able to reduce pension expense through disciplined asset-liability matching.

Segment-Level Returns

Analyzing returns by segment reveals the wisdom of General Dynamics' portfolio construction:

Marine Systems generates the highest return on invested capital at over 25%, reflecting the monopoly economics of submarine construction and minimal capital requirements given government funding of facilities. The business requires specialized expertise that creates barriers to entry, allowing sustained high returns.

Aerospace delivers returns around 20%, impressive for a manufacturing business but reflecting the capital intensity of new product development. Each new Gulfstream model requires $1-2 billion in development costs before the first delivery. However, once developed, these aircraft generate returns for decades through both new sales and service revenue.

Technologies produces returns approaching 15%, lower than other segments but still well above the cost of capital. The CSRA acquisition diluted returns initially as General Dynamics paid a premium for the business, but returns are improving as synergies materialize and margins expand.

Combat Systems generates returns around 18%, benefiting from government-furnished facilities and equipment for many programs. The international operations provide geographic diversification while maintaining attractive returns through disciplined pricing and cost management.

Working Capital Wizardry

General Dynamics has mastered the art of working capital management in ways that aren't immediately obvious from financial statements. The company's Days Sales Outstanding (DSO) of 28 days seems unremarkable until you realize this includes multi-year submarine and aircraft contracts. Through milestone-based billing and aggressive collection, General Dynamics actually collects cash faster than most industrial companies despite the long-cycle nature of its products.

Inventory management is equally sophisticated. The company maintains just $7.3 billion in inventory against $47.7 billion in revenue—a 56-day supply that's remarkably lean for a company building submarines and jets. This is achieved through just-in-time delivery from suppliers, modular construction that allows parallel work streams, and careful production planning that minimizes work-in-process inventory.

The company has also pioneered innovative financing structures that reduce capital requirements. For Gulfstream aircraft, General Dynamics offers customers lease financing through third-party partners, earning origination fees without tying up capital. For military programs, the company negotiates progress payment terms that can exceed 80% of costs incurred, minimizing working capital needs.

Tax Optimization

General Dynamics' effective tax rate of 17.5% in 2024—well below the statutory 21% federal rate—reflects sophisticated tax planning that's entirely legal and appropriate. The company benefits from research and development tax credits, foreign tax credits from international operations, and deductions for domestic manufacturing. The 2017 Tax Cuts and Jobs Act was particularly beneficial, allowing immediate expensing of capital investments and reducing the corporate rate.

International operations are structured to minimize global tax liability while remaining compliant with all regulations. European subsidiaries benefit from lower corporate tax rates in countries like Switzerland and Ireland. Transfer pricing between segments is carefully documented to withstand scrutiny from tax authorities while optimizing the overall tax burden.

IX. Playbook: Business & Leadership Lessons

The boardroom at General Dynamics headquarters features portraits of the company's CEOs dating back to John Jay Hopkins. Each led during different eras, faced unique challenges, and left distinct legacies. Yet patterns emerge from studying their decisions—timeless principles about portfolio management, capital allocation, and leadership that transcend defense contracting and apply to any complex industrial enterprise.

The Portfolio Management Paradox

The central tension in General Dynamics' history is between focus and diversification. Hopkins built a conglomerate believing diversification would smooth cycles. Anders destroyed that conglomerate believing focus would improve returns. Chabraja and Novakovic rebuilt diversification but in a more disciplined way. Who was right?

The answer is they all were—for their times. Hopkins operated in an era when conglomerates could access capital more efficiently than standalone companies, and when investors valued stability over growth. By the 1990s, capital markets had evolved to penalize conglomerate discounts, and Anders' radical surgery was necessary. Today's General Dynamics has found a middle path: diverse enough to weather defense spending cycles but focused enough that each business reinforces the others.

The key insight is that portfolio strategy must evolve with market conditions, competitive dynamics, and institutional capabilities. Hopkins couldn't have successfully run today's General Dynamics because the information systems and management processes didn't exist to coordinate such complexity. Novakovic couldn't have built today's portfolio in the 1950s because the defense market wasn't sophisticated enough to value integrated solutions.

This suggests a broader principle: the "right" portfolio strategy depends not on abstract theory but on specific context. The question isn't "Should we diversify?" but rather "Given our capabilities, market position, and the current environment, what portfolio structure maximizes value?" General Dynamics has succeeded by repeatedly asking and honestly answering this question, even when the answer required painful changes.

The Anders Doctrine: Creative Destruction

Bill Anders' transformation of General Dynamics from 1991-1996 remains one of the most dramatic corporate restructurings in American business history. His willingness to sell crown jewel assets like the Fort Worth division shocked employees and investors alike. But Anders understood something profound: in declining industries, the first seller gets the best price.

When Anders sold Fort Worth to Lockheed for $1.5 billion in 1993, critics accused him of giving away the F-16 franchise. But Anders had run the numbers. Without new fighter programs, Fort Worth would generate declining cash flows as F-16 production wound down. Lockheed, needing production capacity for the F-22, would pay a strategic premium. By selling early, General Dynamics captured value that would have evaporated had it waited.

This principle—sell good assets into strength rather than weak assets into weakness—runs counter to most executives' instincts. The natural tendency is to sell underperforming divisions while keeping winners. But Anders recognized that good assets command premium prices precisely because they're good. Weak assets often can't be sold at any reasonable price and must be shut down at considerable cost.

The Anders Doctrine extends beyond just timing. He understood that in restructuring, speed matters more than perfection. By moving quickly to sell multiple divisions simultaneously, Anders prevented buyers from waiting each other out. He created urgency and competition among potential acquirers. The alternative—a slow, deliberate sale process—would have allowed buyers to coordinate and drive down prices.

Counter-Cyclical Courage

General Dynamics' best acquisitions have come when others were fearful. Chabraja bought Gulfstream in 1999 just as the business jet market was peaking and about to enter a devastating downturn. Novakovic acquired CSRA in 2018 when investors were fleeing IT services contractors. Both deals were criticized at announcement but proved brilliant in hindsight.

This counter-cyclical approach requires two forms of courage. First is the analytical courage to trust your own analysis when the market disagrees. When General Dynamics announced the Gulfstream acquisition, sell-side analysts produced dozens of reports explaining why it would fail. Chabraja had to trust his team's assessment that business jets were a secular growth market temporarily experiencing cyclical weakness.

Second is the institutional courage to accept short-term pain for long-term gain. General Dynamics' stock underperformed for two years after the Gulfstream acquisition as the business jet market crashed following 9/11. Lesser CEOs might have panicked and sold Gulfstream at a loss. Chabraja held firm, continued investing in new products, and was rewarded when the market recovered.

The pattern holds across industries: the best acquisitions are usually unpopular at announcement. If everyone agrees a deal makes sense, the seller has probably extracted full value. The acquisitions that create the most value are those where the buyer sees something the market doesn't—either unrecognized assets, fixable problems, or strategic combinations that create value beyond what either company could achieve alone.

The Novakovic Integration Playbook

Phebe Novakovic has overseen multiple significant acquisitions, and her integration approach has become a model for the industry. The key principles:

Preserve the culture of what you're buying. When General Dynamics acquired CSRA, many expected wholesale changes to align with defense contracting practices. Instead, Novakovic kept CSRA's more agile, commercial-style culture intact. She recognized that CSRA's value lay partly in its different approach to problem-solving and customer service.

Promote insiders to maintain continuity. Rather than installing General Dynamics executives to run acquired companies, Novakovic typically promotes leaders from within the acquired organization. This signals to employees that their careers aren't dead-ended and maintains relationships with customers who trust familiar faces.

Integrate gradually and selectively. Instead of forcing immediate integration, Novakovic allows acquired companies to operate independently while slowly introducing General Dynamics' processes and systems. Financial reporting might be standardized immediately, but sales processes and customer interfaces remain unchanged for years.

Capture synergies through collaboration, not consolidation. Rather than eliminating redundant functions, Novakovic encourages acquired companies to collaborate with existing General Dynamics units. GDIT and Mission Systems maintain separate sales forces but jointly pursue opportunities where their capabilities complement each other.

Managing the Monopsony

General Dynamics derives 69% of its revenue from the U.S. government—a customer concentration that would terrify most businesses. But the company has mastered the art of managing this unique relationship through several key strategies:

Never surprise the customer. General Dynamics maintains constant communication with government program offices, flagging potential problems early rather than hoping they'll resolve themselves. This transparency builds trust and often leads to collaborative solutions rather than adversarial contract disputes.

Invest ahead of contracts. The company regularly invests its own money in capabilities the government will eventually need but hasn't yet funded. Electric Boat began developing the Virginia-class submarine design before the Navy had formally approved the program. This positions General Dynamics to win competitions by offering more mature solutions.

Maintain bipartisan relationships. The company carefully cultivates relationships across the political spectrum, ensuring support regardless of which party controls Congress or the White House. This isn't about campaign contributions—it's about consistently delivering on promises and being seen as a reliable partner rather than a partisan actor.