State Street Corporation: The Silent Giant of Global Finance

I. Introduction & Cold Open

Picture this: Every single day, $46.6 trillion worth of assets flow through the systems of a company most people have never heard of. That's more than twice the GDP of the United States, managed by a firm that started when George Washington was still president. While BlackRock and Vanguard dominate headlines as the titans of passive investing, their lesser-known peer quietly processes one out of every ten dollars traded globally and custody services for 15% of the world's investable assets.

State Street Corporation isn't just another bank—it's the invisible infrastructure that makes modern capital markets possible. From its headquarters on Congress Street in Boston, this 232-year-old institution has transformed from a merchant bank serving New England sea captains into the backbone of global finance. Today, it manages $4.7 trillion in assets and administers another $46.6 trillion, making it systemically critical to markets from Tokyo to London to New York. The paradox is striking: How does a company processing $46.6 trillion in assets under custody and administration remain virtually unknown outside finance circles? The answer lies in State Street's unique position as the plumbing rather than the faucet—the infrastructure that enables trillions in transactions but rarely touches retail investors directly.

Consider the scale: If State Street were a country, its assets under custody would dwarf the combined GDP of every nation on Earth. Every trading day, institutional investors from Tokyo to London rely on State Street's systems to settle trades, calculate net asset values, and safeguard securities. When CalPERS needs to move billions in pension assets, when Fidelity needs custody for mutual funds, when sovereign wealth funds need to execute complex cross-border transactions—they turn to State Street.

Yet this invisibility is precisely what makes State Street fascinating. While Warren Buffett preaches about moats, State Street has built something more fundamental: it's become the bedrock itself. You can't disrupt what everyone stands on. The company doesn't just have network effects; it IS the network—processing, verifying, and safeguarding the rivers of capital that flow through global markets every millisecond of every trading day.

The story we're about to unfold isn't just about a bank that got lucky or smart. It's about a series of non-obvious strategic pivots, each one seemingly risky at the time, that transformed a regional lender into an irreplaceable cog in the global financial machine. From pioneering mutual fund custody in 1924 to inventing the ETF structure that would reshape investing forever, State Street has consistently been first to recognize where finance was heading—and more importantly, what infrastructure it would need when it got there.

This is the untold story of how State Street became the silent giant of global finance, processing one out of every ten dollars traded worldwide while remaining a mystery to most. It's a tale of transformation, technology, and the tremendous power of being boring but essential.

II. Colonial Roots & Banking Origins (1792-1920s)

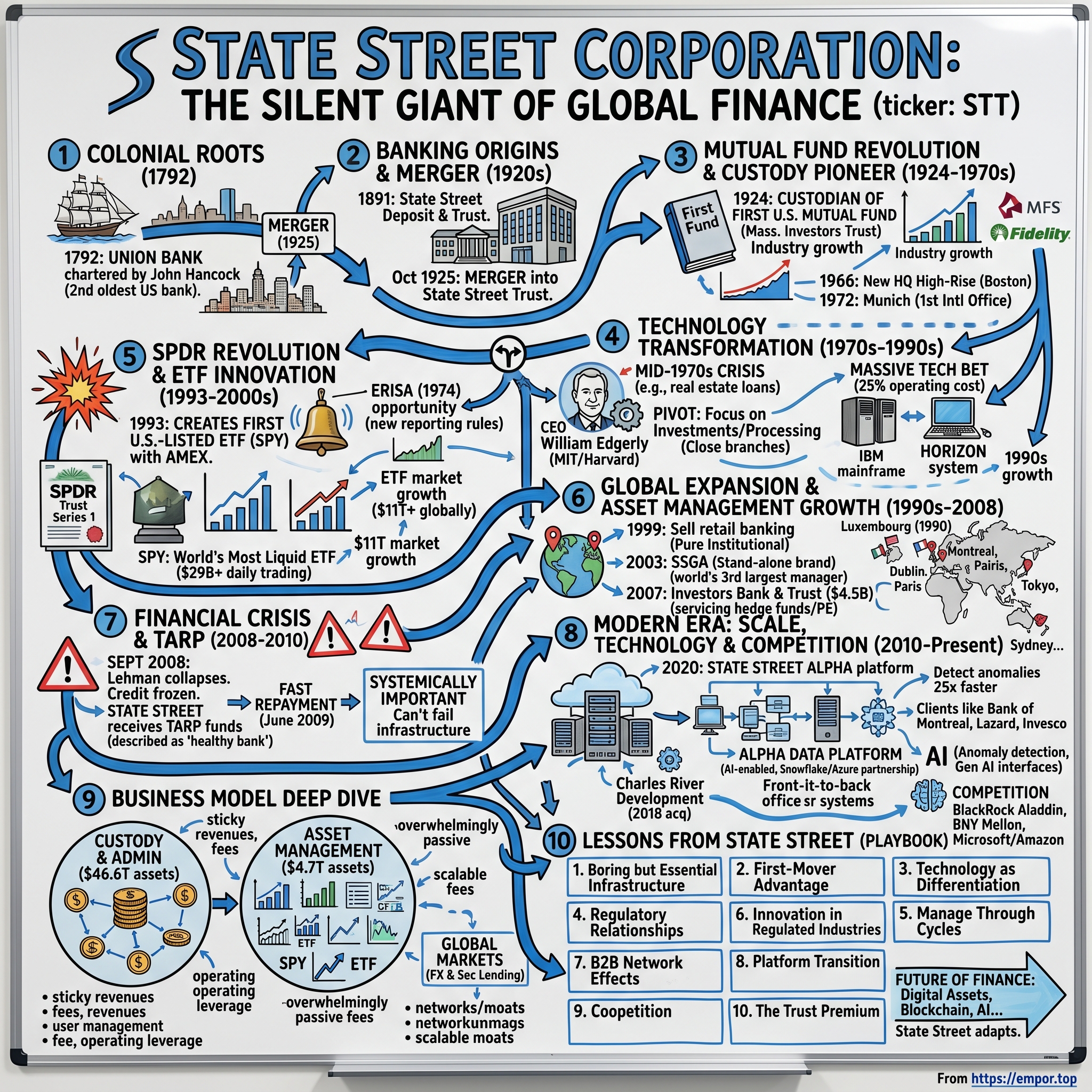

The year was 1792. George Washington was serving his first term as president, and in Boston, a group of merchants gathered to solve a problem that would echo through centuries: how to finance the booming maritime trade that was transforming the young nation into a commercial power. Their solution was Union Bank, chartered that year by none other than Massachusetts Governor John Hancock—yes, the same Hancock whose signature dominates the Declaration of Independence. Union Bank, chartered in 1792, wasn't just the second-oldest continuously operating U.S. bank—it was the third bank chartered in Boston. The timing was no accident. Boston was experiencing an explosion in maritime commerce, with clipper ships carrying New England timber, rum, and manufactured goods to Europe and returning with precious metals, textiles, and luxury items. The city's merchants needed a reliable institution to finance voyages that could take months or even years to complete.

John Hancock signed the bank's charter on June 25, 1792, and the institution set up shop at the corner of State and Exchange Streets with Massachusetts Lieutenant Governor Moses Gill as its first president. The location was deliberate and symbolic. State Street wasn't just any thoroughfare—it was the main thoroughfare in colonial Boston and a significant crossroads in the new nation. Bracketed by the State House at one end and the Long Wharf at the other, State Street was a center of both commerce and politics.

This was the street where the first public reading of the Declaration of Independence took place. It was where the famous trial of Captain Kidd took place. And perhaps most importantly for a bank, it was where the first Boston merchant, John Coggan, had set up shop. By choosing this location, Union Bank positioned itself at the literal and figurative center of American commerce.

The early years reveal a fascinating portrait of Boston's financial aristocracy. The bank had real estate deals with such notable local families as the Parkmans, Sargents, and Quincys, and among its early officers was Oliver Wendell, the great-grandfather of Oliver Wendell Holmes. These weren't just bankers—they were the merchant princes of a city that saw itself as the Athens of America, combining commercial ambition with intellectual refinement.

The bank's conservatism proved to be its greatest asset. Through the War of 1812, the Panic of 1819, and the tumultuous Jackson administration's Bank War, Union Bank maintained an almost boring stability. Despite wars and the fluctuating fortunes of the new country, the bank thrived, and it is a mark of its stability that it never failed to declare semi-annual dividends. This reliability made it the financial anchor for Boston's merchant class, who valued predictability over rapid growth.

In 1865, as the Civil War drew to a close and the nation began its transformation into an industrial power, the directors applied for and received a National Charter. The bank was renamed the National Union Bank of Boston, aligning itself with the new national banking system that would finance America's gilded age. The bank had already moved to 40 State Street, cementing its association with the street that would give its eventual successor its name.

But Union Bank wasn't alone on State Street for long. On July 1, 1891, National Union would have a new neighbor and banking competitor on State Street. State Street Deposit & Trust Company was chartered and began business, with offices in the Exchange Building on State Street. The company was started by a group of directors and officers from the Third National Bank, and it opened for business with a capital of $300,000.

The new institution represented a different vision of banking. While National Union embodied tradition and stability, State Street Trust (as it became known after the bank's name was shortened to State Street Trust Company in 1897) was entrepreneurial and growth-oriented. From 1900 to 1925, deposits increased from roughly $2 million to over $40 million—a twenty-fold increase that reflected both Boston's economic boom and the bank's aggressive pursuit of new business.

The convergence came in October 1925, when these two institutions—one representing Boston's conservative banking tradition, the other its entrepreneurial spirit—merged. State Street and National Union merged in October 1925. The merged bank took the State Street name, but National Union was the nominal survivor, and it operated under National Union's charter. This clever structure allowed the combined entity to claim the mantle of being the second oldest bank in the United States while adopting the more modern, forward-looking State Street brand.

The merger was more than a corporate combination—it was a bridge between eras. The old Boston of merchant princes and maritime trade was giving way to a new world of industrial finance and institutional investing. And State Street, with its dual heritage of stability and innovation, was uniquely positioned to navigate this transformation. Little did anyone know that this Boston bank, born from the merger of two State Street neighbors, would soon stumble upon an innovation that would transform not just its own future, but the entire structure of American finance.

III. The Mutual Fund Revolution & Custody Pioneer (1924-1970s)

The year 1924 should have been unremarkable for State Street. Calvin Coolidge was president, the economy was roaring, and banks across America were making fortunes financing everything from automobiles to radios. But in a back office on State Street, something revolutionary was happening: It became the custodian of the first U.S. mutual fund in 1924, the Massachusetts Investors Trust (now MFS Investment Management)

. No one quite understood what they were witnessing.

The year 1924 proved an historic turning point for State Street, though it would take many years before the significance of the event would be fully appreciated. In that year, Massachusetts Investors Trust chose the bank as custodian of the country's first mutual fund. The fund's creators—L. Sherman Adams, Charles H. Learoyd, and Ashton L. Carr—needed someone to hold the securities, process transactions, and maintain records for their revolutionary investment vehicle. State Street Trust Co. is listed as the original custodial and transfer agent.

What made this arrangement revolutionary wasn't immediately obvious. Custody services—holding securities for others—had existed for decades. But the Massachusetts Investors Trust was different. Unlike the closed-end trusts popular at the time, this fund allowed continuous redemption and subscription of shares. Every day, investors could buy in or cash out at net asset value. This meant State Street had to calculate the exact value of the fund's holdings daily, process trades in real-time, and maintain perfect records of who owned what.

Some of the early recorded investments include shares in Boston Insurance Co., General Electric Co., American Radiator, Standard Oil, Lowell Bleachery and Edison Electric of Boston. These weren't speculative plays but solid, dividend-paying companies—a radical departure from the get-rich-quick schemes dominating the Roaring Twenties.

The operational challenges were immense. In an era of paper certificates and manual bookkeeping, State Street had to track every transaction, calculate daily valuations across dozens of holdings, and ensure perfect accuracy in an environment where a single misplaced decimal could mean disaster. The bank essentially invented modern fund administration from scratch, creating processes that would become industry standard.

As the mutual fund concept proved successful, State Street found itself at the center of a revolution. The fund's creation largely went unnoticed at the time – and yet today is considered the crucial beginning of an industry that now dominates Boston and even defines it in many parts of the world. The fund, which still exists and is run by founder MFS Investment Management of Boston, spawned an entire sector that now includes Fidelity Investments, Putnam Investments, Eaton Vance and other mutual-fund firms that provide tens of thousands of local jobs and manage trillions of dollars.

Through the Great Depression and World War II, State Street quietly built expertise in what others saw as back-office drudgery. While competitors chased commercial lending profits, State Street perfected the unglamorous art of securities processing. By 1945, they were handling custody for dozens of mutual funds, each requiring daily valuations, shareholder record-keeping, and dividend distributions.

The post-war boom accelerated everything. The GI Bill, suburban expansion, and rising middle-class wealth created millions of new investors. Mutual funds transformed from an obscure Boston innovation into America's favorite investment vehicle. And behind every fund stood State Street, processing the paperwork, safeguarding the assets, calculating the values.

The company merged with Second National Bank in 1955 and with the Rockland-Atlas National Bank in 1961. These mergers weren't about branch expansion but about scale—building the infrastructure to handle exponentially growing transaction volumes.

In 1960, recognizing that its future lay in financial services rather than traditional banking, the company incorporated as State Street Boston Financial Corp., a one-bank holding company structure that would give it flexibility to expand beyond conventional banking. In 1966, the company completed construction of the State Street Bank Building, a new headquarters building, the first high-rise office tower in downtown Boston. The gleaming modernist tower was a statement: State Street was no longer a quaint Boston bank but a major player in the emerging world of institutional finance.

In 1972, the company opened its first international office in Munich. This wasn't random expansion—German institutions were beginning to invest in U.S. markets and needed a custody partner who understood both American securities and European requirements. State Street was building a global network before globalization became a buzzword.

By the early 1970s, State Street had discovered something profound: in finance, the real money wasn't in taking risks but in helping others manage theirs. Every mutual fund needed custody. Every pension fund needed administration. Every institutional investor needed someone to handle the mundane but critical work of settlement, safekeeping, and record-keeping. State Street had stumbled upon the ultimate business model—becoming indispensable infrastructure for an entire industry.

IV. The Technology Transformation (1970s-1990s)

Since the 1970s, State Street has become one of American banking's great success stories. Beginning in that period, through a strategy of aggressive diversification and the use of the most advanced technologies, State Street rapidly evolved from a traditional, gentlemanly, old-line Massachusetts financial institution into a global banking powerhouse.

The transformation began under crisis. By the mid-1970s, the bank was suffering from major real estate lending problems. Fortunately, a new chief executive officer, William Edgerly, took control in 1975 and began hammering out an ambitious new strategy to turn the company around. Edgerly wasn't a typical banker—he had a degree in engineering from MIT, as well as his M.B.A. from Harvard, and had come to State Street from a petrochemical firm, Cabot Co., rather than from the banking ranks.

Edgerly brought in new managers to help propel the bank into the direction that it had to go if it was to continue to hold its own in the competitive New England banking community. At that time, the bank had four major lines of business: commercial banking, financial services, investment management, and regional banking. Instead of continuing on its present path, Edgerly decided State Street should move away from its traditional commercial role and, rather than expand its branches, shut them down to concentrate on building up its business in investments, trusts, and securities processing.

This was heresy in 1975. While competitors like Bank of Boston and Fleet were expanding branch networks, State Street was closing them. While others chased consumer deposits, State Street was exiting retail banking entirely. Edgerly saw what others missed: the future wasn't in competing for checking accounts but in becoming the invisible infrastructure for institutional investing.

For one thing, it had an early start in the mutual funds market and was ideally situated to build upon its substantial reputation and assets in that area. State Street pushed aggressively into an area that many banks had shunned—the complex, high-technology processing of asset management, global custody, 401(k) retirement plan accounting, and trusteeship of debt securities based on securitized assets.

The technology bet was massive and risky. At the same time, Edgerly recognized that State Street needed to develop its technology if it was going to create a niche for itself with its data processing and telecommunications abilities. So the company began investing in a big way—an estimated 25 percent of its operating costs—in technology. For context, most banks spent 5-10% of operating costs on technology. State Street was betting the farm.

In 1973, the company had already made a key move in developing its technical know-how by buying 50 percent of Boston Financial Data Services and then using the software and data processing company for its shareholder-accounting and customer-service functions. The technological command post for the company became the bank's data-processing headquarters, an office complex opened in Quincy, Massachusetts, a suburb of Boston, in 1974.

The hardware backbone of State Street's numbers crunching was an IBM-mainframe-based Horizon computer system. Built from thousands of modules loaded into a mainframe, each module in Horizon was designed for a specific task and could be accessed at personal computer workstations, using a variety of software. This modular architecture was revolutionary for banking—it meant State Street could customize solutions for each client while maintaining standardized processing underneath.

Edgerly's IBM obsession went beyond technology. At State Street he recruited many top-ranking executives from IBM, and by the early 1990s it was estimated that more than 100 veterans from IBM were serving in senior management positions at State Street. Beyond IBM's devotion to technical innovation, Edgerly also admired the company's aggressive approach to sales, and he designed the State Street Institute based on a sales training class at IBM.

The timing proved perfect. In 1974, the Employee Retirement Income Security Act (ERISA) was passed and, as a result, companies now had new responsibilities when it came to reporting to the government on their pension plans. Recognizing a window of opportunity, State Street developed software that emphasized more advanced record-keeping abilities. While competitors scrambled to comply with new regulations, State Street already had the systems in place.

By the late 1980s, State Street's technology investments were paying off spectacularly. The bank could process trades faster, calculate valuations more accurately, and handle volumes that would have crushed traditional back-office operations. One client described State Street's systems as "magic"—they could get end-of-day reports that competitors couldn't deliver for three days.

Then came Marshall N. Carter, and everything accelerated.

From 1992-2001, he was chairman and CEO of the State Street Bank and Trust Co., and its holding company, State Street Corporation. He joined State Street in July 1991 as president and chief operating officer, became CEO in 1992 and chairman in 1993. Carter wasn't just another banker either—he was a decorated Marine who'd earned the Navy Cross in Vietnam, worked as a White House Fellow, and most importantly, had built Chase Manhattan's global custody business into the nation's largest.

During his nine years as CEO, the company grew more than sixfold. In 1991 when I joined STT it had 8,000 employees, was doing business in 32 countries and had a market cap of $2.3 billion. During Carter's tenure, State Street grew assets under custody to $6.2 trillion, assets under management to $712 billion, and enjoyed a compound earnings per share growth rate of 17 percent, increasing its business base from 32 to 90 countries. Adopting a new global strategy that significantly broadened its product line and use of information technology, State Street tripled the size of its business during this period, emerged as a dominant global player in the world of financial asset servicing and management, and increased its market capitalization from $2.3 billion to $21 billion.

The transformation was remarkable. A February 1992 American Banker described State Street as "less a bank than a provider of information processing services." Most of State Street's revenue now came from fees for holding securities, settling trades, record keeping, accounting (including multicurrency accounting) and net asset value computation. The result was a balance sheet in which income derived from selling fiduciary services accounted for 70 percent of overall revenues.

This wasn't banking anymore—it was technology services wrapped in a banking charter. State Street had discovered that in the information age, data processing was more valuable than deposit gathering, and custody was more profitable than lending. Every trade needed settlement, every fund needed valuation, every institution needed someone to handle the boring but critical work of keeping track of who owned what.

One signal win demonstrated State Street's new competitive advantage: the California Public Employees Retirement System, a $67 billion custody account. State Street showed the ability to offer a sophisticated package while charging less in fees to such institutional investors, an edge that the company's leadership attributed to superior technology and economies of scale. When you could process trades at a fraction of competitors' costs, you could undercut their prices while maintaining higher margins.

By the early 1990s, State Street had become something unique in American finance: a technology company that happened to have a banking license, processing information at a scale and speed that traditional banks couldn't match. They had built the rails on which trillions of dollars would flow. And they were about to invent an entirely new vehicle to run on those rails.

V. The SPDR Revolution & ETF Innovation (1993-2000s)

The seeds of the ETF revolution were planted on October 19, 1987—Black Monday. Global markets plummeted so abruptly that the resulting stock market damage is believed to have been more significant than the Great Depression. The Dow Jones Industrial Average lost 22.6% in a single day. The crash exposed a critical weakness in market structure: when institutions tried to sell baskets of stocks simultaneously, the system couldn't handle it. Program trading, where computers automatically sold entire portfolios, had overwhelmed the market's ability to find buyers.

The American Stock Exchange (AMEX) saw an opportunity in this crisis. They envisioned a product that could trade an entire index as a single security—providing the diversification of a mutual fund with the tradability of a stock. But creating such a product required capabilities no exchange possessed: portfolio management expertise, massive custody infrastructure, and most critically, the ability to move money and securities in real-time.

AMEX had initially approached State Street, the indexing pioneer and custody/clearing giant, because of its proven portfolio management expertise and money movement capabilities. Several other firms had been approached, but State Street was the only one willing to take the concept from theory to reality.

It's the culmination of a three-year collaboration between State Street and AMEX, later acquired by the New York Stock Exchange (NYSE) in 2008. The project was shrouded in secrecy, code-named internally as teams worked through unprecedented technical and regulatory challenges. Jim Ross, a 27-year-old State Street employee who would become known as "the Plumber" for his behind-the-scenes work, led the operational team from their fourth-floor cubes in Quincy, Massachusetts.

But the ETF presented some unique challenges. While ETFs trade on the exchange like stocks and bonds, the underlying fund must have the actual holdings. "If it was a US$100 million fund," Jim shares, "it needed to have US$100 million in assets comprised primarily of the index."

The technical hurdles were staggering. Complicating matters, because both the money and securities must move and be settled in real time, a day-of audit had to be conducted. "Given that we were seeded not just with cash but with S&P 500® securities as well, we had to audit 500 individual securities," Jim explains. "Normally, this whole process takes 45 days. But for the ETF to work, it needed to be completed in about 16 hours — between the 4 p.m. market close and the next morning's open.

The night before launch revealed how close they came to disaster. Hours before their SEC filing was due, the team realized they had only 499 securities listed instead of 500—someone had missed a stock. They fixed it just in time, but it underscored the complexity of what they were attempting.

The SPDR® S&P 500® ETF (SPY), a basket of securities tracking the performance of the S&P 500® Index, made its debut in 1993 as the first US-listed ETF. A group of financial executives ring the opening bell at the American Stock Exchange (AMEX), officially launching the first US-listed exchange traded fund (ETF). The ticker SPY flashes on screen for the first time.

On January 29, 1993, our product was officially listed as "SPDR Trust, Series 1" with $6.53 million in securities. The initial seeding was modest—the largest holdings were AT&T, Exxon, and General Electric, the smallest was Westmoreland Coal. But this small beginning would transform global investing.

The name itself—SPDR, pronounced "spider"—came from a Harvard-trained Ph.D. named Bloom on the AMEX product development team. They needed something catchy that could be "tossed around the trading floor." Initially, they considered "SPIRs" (pronounced "spears"), but as Bloom noted, "we didn't like the imagery of spears being thrown around the floor."

Early adoption was brutal. The original sales team crisscrossed the country trying to explain this strange new product. One mutual fund executive told them bluntly: "I like it, I own it and my firm is never, ever going to sell it. And to be honest, I hope you fail." The mutual fund industry saw SPY as an existential threat—and they were right.

Processing was nightmarish in the pre-digital age. Gary Eisenreich, a specialist at Spear, Leeds & Kellogg tasked with making a market in SPY, recalls clerks using punch cards to process creations and redemptions. Every basket creation or redemption required manual entry of 500 securities. A single error could break the entire system.

But slowly, SPY gained traction. One of the institutions in the original roll call was Daiwa Securities America, a unit of Japan's Daiwa Securities Group. On June 30, 1993, the AMEX announced that Daiwa had deposited $90 million of securities into the trust, increasing total assets 50% to $278 million. By the end of summer 1993, SPY rarely saw a sub-100,000 share trading day.

State Street had invented something revolutionary: a mutual fund that traded like a stock, with real-time pricing, instant liquidity, and perfect transparency. Unlike traditional mutual funds that priced once daily after market close, SPY traded continuously. Unlike closed-end funds that could trade at premiums or discounts, SPY's creation/redemption mechanism kept prices aligned with net asset value.

The innovation went deeper than product structure. State Street had to invent entirely new operational processes. The creation/redemption mechanism—where authorized participants could exchange baskets of stocks for ETF shares and vice versa—required State Street to simultaneously be custodian, transfer agent, and market maker support system. They had to calculate indicative values every 15 seconds, process in-kind transfers throughout the day, and maintain perfect inventory management across 500 securities.

More than thirty years later, SPY is the most liquid and most heavily traded ETF in the world, with an average trading volume of $29.3 billion each day. SPY democratized investing — opening the door to markets that were inaccessible to the majority of investors prior to 1993.

The success of SPY triggered an explosion. Competitors rushed to market: Barclays Global Investors (later BlackRock) launched iShares, Vanguard entered with their own ETFs. But State Street maintained first-mover advantage in the most liquid products. They expanded the SPDR family—sector SPDRs, international SPDRs, fixed income SPDRs. Each new product leveraged the same operational infrastructure State Street had built for SPY.

SSGA invented the investment vehicle known as the exchange-traded fund (ETF) in 1993 with the introduction of the S&P 500 SPDR product (Ticker: NYSE Arca: SPY), which is traded on the American Stock Exchange. This wasn't just a new product—it was a new category that would reshape finance. By 2000, ETF assets had grown to $65 billion. By 2010, over $1 trillion. Today, the global ETF market exceeds $11 trillion, with SPY alone holding over $500 billion in assets.

State Street's gamble on building the infrastructure for a product that didn't exist had paid off spectacularly. They hadn't just created a successful fund; they had invented an entirely new way of investing. The same custody and technology capabilities that made SPY possible now processed trillions in ETF assets globally. State Street had become not just a participant in the ETF revolution but its essential infrastructure—the rails on which an entire industry runs.

VI. Global Expansion & Asset Management Growth (1990s-2008)

The late 1990s marked State Street's transformation from an American custody bank into a global financial powerhouse. Having conquered ETFs and technology, the company now set its sights on geographic expansion and building out its asset management capabilities.

In 1999, State Street sold its retail and commercial banking businesses to Citizens Financial Group for $350 million. This was the final break with traditional banking—State Street was now purely an institutional services company. The sale freed up capital and management focus for aggressive international expansion.

The biggest move came with strategic acquisitions that would double State Street's scale. First founded in 1969 as an offshoot of Eaton Vance, Investors Bank & Trust was purchased by State Street Corporation in 2007 as an all-stock deal valued at nearly $4.5 billion. This wasn't just about size—Investors Bank & Trust brought expertise in servicing hedge funds and private equity, markets State Street had struggled to penetrate.

Some of IBT's more well-known clients included Aegon, Barclays Global Investors, Eaton Vance, and MassMutual. The acquisition immediately positioned State Street as a major player in alternative investments custody, a rapidly growing segment that demanded specialized expertise.

But State Street's ambitions went beyond custody. State Street Global Advisors, the asset management division of State Street Corporation, was founded in 1978 in Boston, Massachusetts, initially focusing on index funds for institutional clients. By the early 2000s, SSGA had grown into a formidable asset manager, but it remained overshadowed by giants like Fidelity and BlackRock.

The 2003 launch of State Street Global Advisors as a standalone brand marked a strategic shift. No longer content to be just the back-office provider, State Street wanted to compete directly in asset management. The timing was perfect—passive investing was exploding, and State Street's expertise in indexing and ETFs gave it unique advantages.

Geographic expansion accelerated through the decade. In 1990, State Street Bank Luxembourg was founded, and as of 2018 is the largest player in the country's fund industry by assets. Offices sprouted across the globe—Montreal, Toronto, Dublin, London, Paris, Dubai, Sydney, Wellington, Hong Kong, and Tokyo. Each location wasn't just a sales office but a full-service operation capable of providing custody, fund administration, and asset management to local clients.

The global expansion strategy was sophisticated. Rather than simply exporting American products, State Street localized its offerings. In Europe, they adapted to UCITS regulations. In Asia, they partnered with local institutions to navigate complex regulatory environments. The company became expert at what it called "glocalization"—global capabilities with local expertise.

Meanwhile, State Street was building what it called the "three-legged stool"—custody services, asset management, and trading/markets. Each leg reinforced the others. Custody clients became asset management prospects. Asset management products needed custody services. Trading capabilities enhanced both businesses. The synergies were powerful—State Street could offer integrated solutions no competitor could match.

The technology investments of the 1990s were paying massive dividends. State Street's systems could handle volumes that would have been unimaginable a decade earlier. They were processing trades in 100+ markets, calculating valuations in dozens of currencies, and providing real-time reporting to clients globally. The company's data processing center in Quincy had grown into a global network of technology hubs operating 24/7.

By 2007, State Street was riding high. Assets under custody had grown to over $15 trillion. State Street Global Advisors managed nearly $2 trillion. The company was generating record profits, and its stock price had quintupled since 2000. The Investors Bank & Trust acquisition seemed to cap a perfect decade of growth.

But storm clouds were gathering. The subprime mortgage crisis was beginning to metastasize through the financial system. Complex structured products that State Street serviced were becoming impossible to value. Counterparty risk—the possibility that trading partners might fail—was spiking. State Street's role as a systemically important financial institution was about to be tested like never before.

VII. The Financial Crisis & TARP (2008-2010)

September 2008. Lehman Brothers had just collapsed. AIG was teetering. Credit markets had frozen completely. State Street found itself at the epicenter of a global financial earthquake, not as a failing institution but as critical infrastructure that absolutely could not be allowed to fail.

State Street was among the eight large U.S. banks to receive the Treasury Department's initial round of capital investments -- money described by Treasury officials not as a bailout, but rather as funds to help bolster "healthy" banks in tough times. The distinction mattered. State Street wasn't insolvent or even particularly troubled. But as a custodian for $15 trillion in assets and a crucial node in the global payment system, its failure would have been catastrophic.

The systemic importance was stark. If State Street couldn't settle trades or value securities, mutual funds couldn't calculate NAVs. Pension funds couldn't move assets. The entire infrastructure of institutional investing would seize up. A State Street failure wouldn't just hurt investors—it would paralyze markets globally.

State Street Corp. says it was among the banks to repay $2 billion it received last fall as part of the government's $700 billion bank investment program. Boston-based State Street received the money as part of the Treasury Department's Troubled Asset Relief Program, aimed at reviving the stagnant credit and lending markets.

The TARP investment came with strings attached. The government provided banks with capital in exchange for preferred stock and warrants to purchase common shares. The preferred stock carried an interest rate of 5 percent. The investment also included certain restrictions, such as caps on executive compensation that left some banks pushing to repay the loan as quickly as possible.

For State Street, the compensation restrictions were particularly galling. Unlike investment banks that had gambled and lost, State Street had been conservative. They hadn't originated subprime mortgages or traded exotic derivatives. They were being punished for others' sins, forced to accept government money to maintain system stability.

The custody crisis revealed State Street's unique vulnerability. While they didn't take credit risk like traditional banks, they faced massive operational and counterparty risks. Every day, State Street had to advance billions to settle trades, trusting that counterparties would make good. When Lehman failed, State Street faced potential losses not from bad loans but from trades that couldn't settle, securities that couldn't be delivered, collateral that suddenly became worthless.

State Street's technology systems, built to handle normal market volatility, were pushed to breaking point. Trading volumes spiked as panicked investors fled to safety. Securities that normally traded smoothly became impossible to value. Complex derivatives required manual intervention. The company had to hire hundreds of temporary workers just to handle the volume of failed trades and disputed valuations.

But State Street's response demonstrated why it was considered systemically important. Throughout the crisis, not a single mutual fund failed to calculate NAV. Not a single pension payment was missed. The plumbing held, even as the financial system above it convulsed.

The rapid repayment of TARP funds became a priority. Last week, the government granted 10 of the country's largest banks approval to pay back a total of $68 billion in TARP funds. Wednesday was the first day those banks were eligible to repay the loans, and all 10 did so. The banks are JPMorgan Chase, Goldman Sachs, Morgan Stanley, U.S. Bank, Northern Trust, Capital One, BB&T, American Express, Bank of New York Mellon, and State Street.

State Street Corp. paid $60 million to repurchase warrants held by the US Treasury, becoming the first major financial firm to exit the government's $700 billion rescue program. State Street, the world's largest money manager for institutions, previously bought back $2 billion in preferred shares it received in October under the Troubled Asset Relief Program. The Treasury released details yesterday about the warrant sale to the Boston-based lender.

The speed of State Street's exit from TARP—less than nine months from investment to full repayment—sent a powerful signal. This wasn't a troubled bank limping back to health but a strong institution that had taken government money only to maintain system stability. The $60 million warrant repurchase represented a reasonable return for taxpayers while allowing State Street to escape the stigma of bailout recipient.

The crisis had unexpected consequences. While State Street emerged relatively unscathed financially, its reputation took hits. In 2009, California alleged on behalf of its pension funds CalPERS and CalSTRS that State Street had committed fraud on currency trades handled by the custodian bank. The allegation—that State Street had overcharged on foreign exchange transactions during the crisis—highlighted how even conservative institutions had sought profits in complex ways.

On February 28, 2012, State Street Global Advisors entered into a consent order with the Massachusetts Securities Division. The Division was investigating the firm's role as the investment manager of a $1.65 billion (USD) hybrid collateralized debt obligation. These post-crisis investigations revealed that State Street, despite avoiding the worst excesses of the financial bubble, had still participated in the complex structured products that nearly destroyed the system.

The financial crisis transformed State Street's strategic thinking. The company realized that being boring and essential wasn't enough—they needed to be antifragile, growing stronger from stress rather than merely surviving it. This led to massive investments in risk management, stress testing, and operational resilience. State Street built redundant data centers, enhanced cybersecurity, and created "living wills" showing how the company could be wound down without systemic disruption.

More fundamentally, the crisis accelerated State Street's evolution from service provider to technology company. If human traders and manual processes had nearly broken the system, then automation and artificial intelligence would be essential for preventing future crises. State Street began pouring billions into what it called "State Street Alpha"—a platform combining custody, fund administration, and data analytics into an integrated digital ecosystem.

The crisis also revealed the double-edged sword of systemic importance. Yes, State Street was too big to fail, guaranteeing government support in extremis. But that status brought intense regulatory scrutiny, higher capital requirements, and public opprobrium. State Street had survived the financial crisis, but it emerged into a world where being essential infrastructure meant being forever under the microscope.

VIII. Modern Era: Scale, Technology & Competition (2010-Present)

The post-crisis decade transformed State Street from a custody bank into a technology platform. The catalyst was a simple realization: in the digital age, financial services are really data services. Every trade, every valuation, every risk calculation is just data manipulation at scale. State Street's future would depend not on processing paper but on processing information.

Our Alpha platform is moving the industry forward, delivering revolutionary technology, software and AI-driven advancements that help keep our clients ahead of the curve. State Street Alpha, launched in earnest in 2020, represents the culmination of a decade-long digital transformation. It's not just a technology upgrade but a complete reimagining of what a financial services company can be.

The heart of State Street Alpha platform is our front- and middle-office technology, from Charles River Development, working seamlessly with our middle- and back-office services. Clients in more than 30 countries rely on Charles River to manage more than US$58 trillion* in assets. The 2018 acquisition of Charles River Development for $2.6 billion was the key piece—it gave State Street front-office capabilities to match its back-office dominance.

The ambition is staggering. The State Street Alpha Data Platform is the cloud-based, AI-enabled data solution that helps investment managers globally simplify the essential, but increasingly complex process of managing investment data. This isn't just digitizing existing processes but creating entirely new capabilities that were impossible in the analog world.

With banking roots dating back to 1792, State Street has long been at the forefront of financial breakthroughs. From serving as custodian of America's first mutual fund to launching the first multicurrency accounting platform, the Boston-based bank has always focused on new technologies to help create better outcomes for the world's institutional investors. Responsible for servicing 10% of global assets, State Street knows better than most how much data investment firms generate — and how siloed it can be.

The technical challenges were immense. When initial development for the Alpha Data Platform began, State Street quickly realized that tuning and managing on-premises databases for optimal performance would have been time-consuming and complex — especially when multiplied across all of State Street Alpha's users. Sharing raw data sets with clients would have involved replicating and moving data via custom extract, transform, load (ETL) pipelines.

State Street partnered with cloud giants to build a modern architecture. To provide this modern data backbone for Alpha, State Street turned to Snowflake on Azure. With Snowflake's secure data sharing capabilities and seamless third-party data integrations, State Street built an industry-leading product.

The results have been transformative. Snowflake data sharing allows the exchange of live data, versus requiring data to be updated on a daily or weekly basis. State Street also securely shares vendor data into a client's environment in less than 10 minutes — a job that would normally take months with competing technologies. Efficient onboarding both reduces the Alpha Data Platform team's total cost of labor by 50% and elevates client satisfaction.

Major clients are adopting the platform. Since the platform's launch in 2020, investment and wealth management firms, pension funds, and insurance companies such as Bank of Montreal, Lazard, Janus Henderson and Legal & General Investment Management have adopted State Street Alpha. In 2021, Invesco announced it would transition its entire front-to-back investment servicing to the Alpha platform, a massive validation of State Street's strategy.

But technology alone isn't State Street's differentiator—it's the combination of technology with domain expertise. Detect anomalies 25x faster than existing static-based rules · 100% error detection rates and 87% reduction of false alerts. These aren't just technical metrics but transformative capabilities for investment managers drowning in data.

The AI integration is particularly ambitious. At State Street, our Alpha Data Platform serves as the foundation for AI initiatives, capturing and curating data across the client's front, middle and back office, and enriching it with third-party analytics, benchmark, pricing and index data. It's critical that the data is consistent and accurate, so deploying AI for data validation and anomaly detection became one of our first important use cases.

According to State Street CTO Aman Thind, "Gen AI will become the new standard to augment how we communicate to clients and the rest of the industry." State Street engineers are developing a conversational interface to enable end users to ask complex questions about their investment portfolios. Imagine a portfolio manager asking in plain English, "What's my exposure to Chinese tech stocks across all funds?" and getting an instant, accurate answer. That's the future State Street is building.

The competitive landscape has intensified dramatically. BlackRock's Aladdin platform processes over $20 trillion in assets. BNY Mellon, State Street's traditional rival in custody, has invested billions in its own digital transformation. Tech giants like Microsoft and Amazon are eyeing financial services. Blockchain threatens to disintermediate custody entirely.

State Street's response has been to embrace "coopetition"—competing in some areas while partnering in others. They provide services to BlackRock even while competing in ETFs. They partner with Microsoft on cloud infrastructure while building proprietary capabilities on top. The strategy recognizes that in the platform economy, ecosystem beats isolation.

The ETF business remains a crown jewel. SPY still dominates as the world's most liquid ETF, trading nearly $30 billion daily. But competition from Vanguard and BlackRock has compressed fees to near zero. State Street has responded by launching innovative products—sector SPDRs, smart beta ETFs, ESG-focused funds. The "Fearless Girl" statue, installed facing Wall Street's Charging Bull in 2017, became a viral sensation promoting State Street's gender diversity ETF.

But controversies persist. In October 2017, the company paid $5 million to settle a lawsuit charging that it had paid certain female and black executives less than their male and white peers—an embarrassing contradiction to the Fearless Girl messaging. Regulatory scrutiny remains intense, with ongoing investigations into fee structures, securities lending practices, and ESG claims.

The workforce transformation has been dramatic. State Street now employs more software engineers than traditional bankers. The company has shifted thousands of jobs from Boston to lower-cost locations in Poland, India, and China. Traditional custody operations that once required hundreds of people now run with dozens, augmented by AI and automation.

Looking forward, State Street faces an existential question: In a world where technology companies can replicate financial services, what's the value of being a financial services company with technology? The answer lies in trust, regulatory expertise, and deep domain knowledge—assets that can't be coded.

Our research indicates that the revenue and savings benefits anticipated by the investment industry from digital assets and distributed ledger technology (DLT)-based trading and custody are potentially transformational. Across a wide range of core asset management business areas, from the front, middle and back office, respondents to the third annual State Street Digital Assets Study said they expected major increases in their earnings and reductions in their cost of operations from integrating the technology into their processes.

State Street is betting that the future of finance isn't about choosing between traditional and digital but integrating both. They're building bridges between the $100 trillion traditional asset market and the emerging world of digital assets, positioning themselves as the essential translator between old and new finance.

IX. Business Model Deep Dive & Competitive Analysis

State Street's business model is deceptively simple: they make money by holding other people's money. But the execution of this model has created one of finance's most powerful network effects and most defensible moats.

As of 2024, State Street is one of the world's largest asset managers and custodians, with approximately US$4.7 trillion in assets under management and US$46.6 trillion under custody and administration. State Street operates globally through three main divisions: Global Services (custody and fund administration), Global Advisors (asset management), and Global Markets (trading and research).

The custody business remains the foundation. At its core, custody is about trust—institutions entrust State Street with securities worth more than twice the GDP of the United States. The business model is brilliantly sticky. Switching custody providers is expensive, risky, and time-consuming. It requires remapping thousands of data feeds, retraining staff, and risking operational disruption. Most clients stay for decades.

The economics are compelling. State Street charges basis points on assets under custody—tiny percentages that add up to billions when multiplied by $46 trillion. The marginal cost of adding assets is near zero; the same systems that custody $1 trillion can custody $10 trillion. This creates enormous operating leverage—revenues grow with markets while costs remain relatively fixed.

But custody is just the entry point. Once State Street holds a client's assets, they can offer fund administration, performance analytics, risk management, securities lending, foreign exchange, and dozens of other services. Each service deepens the relationship and increases switching costs. A client might start with basic custody and end up with State Street running their entire middle and back office.

Securities lending exemplifies the model's elegance. State Street holds trillions in securities that sit idle most of the time. They lend these securities to short sellers and keep a portion of the lending fees. It's pure profit from assets they're already holding. The program generates hundreds of millions annually with minimal additional cost.

The asset management division (State Street Global Advisors) leverages the custody base differently. SSGA manages $4.7 trillion, making it the world's third-largest asset manager. The business is overwhelmingly passive—index funds and ETFs that track benchmarks rather than pick stocks. This is intentional. Active management would put State Street in competition with custody clients. Passive management complements the custody business while avoiding channel conflict.

The SPDR ETF franchise is the crown jewel. SPY alone has over $500 billion in assets, generating hundreds of millions in management fees. The beauty of ETFs is their scalability—managing $500 billion costs barely more than managing $50 billion. And because State Street invented the structure, they have expertise competitors struggle to match.

The trading and markets division is the newest leg of the stool but increasingly important. State Street is one of the world's largest foreign exchange traders, handling trillions in currency transactions annually. They're not speculating—they're facilitating client trades and earning spreads. The FX business naturally extends from custody; if you're holding international securities, you need currency conversion.

The network effects are powerful and compounding. More custody clients mean more securities to lend, more FX volume to intermediate, more data to analyze. The data itself becomes valuable—State Street sees flows before they happen, understands positioning better than anyone. They monetize this information through research and analytics products, careful to avoid conflicts but extracting value from their unique vantage point.

Competition comes from multiple angles. BNY Mellon is the most direct competitor, with $47 trillion under custody. The rivalry is intense but rational—both companies understand that price wars would destroy profitability. They compete on service, technology, and capabilities rather than racing to the bottom on price.

JPMorgan and Citigroup compete in custody but focus on different segments. They're stronger in prime brokerage and hedge fund services; State Street dominates in mutual funds and pension funds. Northern Trust is a boutique competitor, focusing on ultra-high-net-worth and specialized mandates. They lack State Street's scale but compensate with high-touch service.

The real threat comes from technology companies. Bitcoin and blockchain promise to eliminate custody entirely—if securities exist on distributed ledgers, why do you need a custodian? State Street's response has been to embrace blockchain rather than fight it. They're building custody services for digital assets, betting that even decentralized systems need trusted intermediaries.

Cloud providers like Amazon and Microsoft are partners today but could become competitors tomorrow. They have the technology and scale to offer custody services. But they lack the regulatory licenses, client relationships, and domain expertise. State Street is betting these barriers remain high enough to protect their position.

The regulatory moat is formidable. State Street operates under banking licenses in dozens of countries, each with unique requirements. They're subject to capital requirements, stress tests, and endless compliance obligations. New entrants would need years and billions of dollars to replicate this regulatory infrastructure.

But regulation is a double-edged sword. It is considered a systemically important bank by the Financial Stability Board and ranks among the "Big Three" index fund managers alongside BlackRock and Vanguard. This designation brings enhanced scrutiny, higher capital requirements, and public pressure. State Street can never take excessive risks because its failure would threaten the entire financial system.

The business model's genius is its inevitability. As long as institutional investors exist, they need someone to hold their securities, process their trades, and calculate their returns. State Street has positioned itself as that someone for a significant portion of global assets. They're the rails on which modern finance runs—boring, essential, and incredibly profitable.

The challenges are real but manageable. Fee compression continues across all business lines. Clients demand more services for lower prices. Technology spending requirements keep rising. Regulatory costs never decrease. But State Street's scale allows them to absorb these pressures better than smaller competitors.

The ultimate question is whether State Street is a technology company or a financial services company. The answer is both and neither—they're an infrastructure company that happens to operate in finance. Like utilities or telecommunications companies, they provide essential services that modern society can't function without. And like those industries, the winners will be those with the best infrastructure, the most scale, and the deepest moats.

X. Playbook: Lessons from State Street

State Street's 232-year evolution from merchant bank to global financial infrastructure offers profound lessons about strategy, innovation, and survival in capitalism's most competitive arena.

Lesson 1: The Power of Boring but Essential Infrastructure

State Street discovered that the most profitable position in finance isn't taking risks but enabling others to take risks safely. While investment banks crashed and burned through cycles, State Street steadily processed transactions, held securities, and collected fees. The lesson: unsexy infrastructure businesses often generate the best returns. Everyone wants to be Goldman Sachs; few want to be the plumbing. But plumbing doesn't go out of style.

Lesson 2: First-Mover Advantage in New Financial Products

State Street didn't just adopt innovations; they created them. First custody for mutual funds in 1924. First ETF in 1993. First to embrace technology transformation in the 1970s. Each time, being first meant defining the standards, building the expertise, and capturing the most valuable clients before competitors understood the opportunity. The lesson: in financial services, the first mover often becomes the standard setter.

Lesson 3: Technology as Competitive Differentiation

State Street's transformation began when they realized they weren't a bank but a technology company. Spending 25% of operating costs on technology in the 1970s was radical. Building IBM-mainframe systems for custody was unprecedented. Today's Alpha platform continues this tradition. The lesson: in service businesses, technology investment isn't optional overhead—it's the core differentiator.

Lesson 4: The Importance of Regulatory Relationships

State Street cultivated deep regulatory relationships over decades. They didn't fight regulation; they embraced it, often helping write the rules. This made them trusted partners rather than adversaries. When crisis hit, regulators turned to State Street for solutions. The lesson: in highly regulated industries, regulatory expertise is as valuable as operational excellence.

Lesson 5: Managing Through Cycles and Crises

State Street survived the Panic of 1819, the Great Depression, and the 2008 Financial Crisis. Each time, they emerged stronger. The secret wasn't avoiding damage but maintaining reserves, staying conservative during booms, and having the capital to acquire weakened competitors during busts. The lesson: survival requires preparing for crisis during prosperity.

Lesson 6: The Paradox of Innovation in Regulated Industries

State Street proves you can innovate within regulatory constraints. ETFs required SEC approval. Digital assets need regulatory clarity. But State Street didn't wait for perfect rules—they worked with regulators to create frameworks that enabled innovation while maintaining stability. The lesson: regulation isn't innovation's enemy if you make regulators your partners.

Lesson 7: Network Effects in B2B

State Street built powerful network effects in institutional finance. More clients meant more securities to lend, more data to analyze, more liquidity to provide. Unlike consumer networks that grow virally, B2B networks grow deliberately, client by client, service by service. The lesson: B2B network effects are slower to build but harder to disrupt.

Lesson 8: The Platform Transition

State Street's evolution from service provider to platform is instructive. They didn't abandon services; they platformized them. Alpha isn't replacing custody; it's making custody programmable. The lesson: traditional businesses can become platforms by making their capabilities accessible via APIs and ecosystems.

Lesson 9: Coopetition in Concentrated Industries

State Street competes with BlackRock in ETFs while servicing BlackRock's funds. They partner with Microsoft on cloud while building proprietary systems. This "coopetition" recognizes that in concentrated industries, pure competition is destructive. The lesson: sometimes your biggest competitors must also be your closest partners.

Lesson 10: The Trust Premium

State Street charges premium prices not for superior technology but for trust. Clients pay extra knowing State Street won't fail, won't commit fraud, won't lose their assets. This trust took centuries to build and can't be replicated quickly. The lesson: in financial services, trust is the ultimate differentiator and commands the highest premiums.

XI. Bear vs. Bull Case

Bear Case: The Disruption Scenario

The bear case for State Street starts with fee compression. ETF fees have fallen 90% in twenty years. Custody fees face similar pressure. As passive investing becomes commoditized, the race to zero accelerates. State Street's main revenue sources are all experiencing structural decline.

Blockchain poses an existential threat. If securities become tokenized and self-custodied, traditional custody becomes obsolete. Smart contracts could replace fund administration. Decentralized exchanges could eliminate clearing and settlement. State Street's entire business model could evaporate within a decade.

Technology giants have State Street's capabilities without its constraints. Amazon could offer custody services at massive scale. Google could provide better analytics. Microsoft already runs much of State Street's infrastructure. These companies have deeper pockets, better technology, and no regulatory baggage.

Concentration risk is severe. State Street's top 10 clients represent a significant portion of revenues. Losing any major client would hit profitability hard. As clients consolidate, they gain negotiating leverage, demanding more services for lower fees.

Regulatory changes could destroy profitability. Higher capital requirements reduce returns on equity. Transaction taxes could kill trading revenues. Restrictions on securities lending could eliminate a major profit center. State Street has little control over these political decisions.

Competition from sovereign wealth funds and central banks is emerging. These institutions are bringing capabilities in-house rather than outsourcing. As they build internal expertise, State Street loses its largest, most profitable clients.

The talent war is unwinnable. State Street competes with tech companies paying multiples of financial services salaries. The best engineers go to Google, not State Street. Without top technology talent, State Street can't maintain its technology edge.

Cybersecurity risk is catastrophic. A major breach could destroy client confidence overnight. As State Street becomes more digital, attack surfaces multiply. One successful hack could trigger client exodus and regulatory sanctions.

Bull Case: The Inevitability Scenario

The bull case starts with scale. $46 trillion under custody creates insurmountable advantages. State Street can spread costs across a base no startup can match. They process trades at costs competitors can't achieve. Scale economics improve every year.

Network effects are accelerating. Every new client makes State Street more valuable to existing clients. More assets mean more liquidity, better pricing, superior analytics. The platform dynamics create winner-take-all markets where State Street is already winning.

Digital transformation multiplies opportunities. Yes, blockchain threatens traditional custody, but someone must custody digital assets. State Street is best positioned to bridge traditional and digital finance. They're not being disrupted; they're becoming the disruptor.

Global wealth continues growing. Pension assets, sovereign wealth funds, and institutional investments all expand faster than GDP. State Street captures this growth automatically. Demographics guarantee decades of asset accumulation.

Passive investing's dominance benefits State Street disproportionately. As active management dies, index funds grow. State Street invented the ETF and maintains structural advantages. The shift to passive is still early globally.

Technology investments are paying off. Alpha platform wins major clients and generates recurring revenues. AI and automation reduce costs while improving service. State Street is becoming a technology company with financial services margins.

Regulation protects incumbents. New entrants face years of regulatory approval and billions in compliance costs. State Street's licenses and relationships create barriers no technology company can quickly overcome.

ESG and sustainable investing create new opportunities. State Street's scale allows them to offer sophisticated ESG analytics and reporting. As sustainable investing mainstreams, State Street captures flows and fees.

The custody business is stickier than ever. Switching costs keep rising as relationships deepen. Clients use dozens of State Street services, making replacement nearly impossible. Churn rates remain near zero despite fee pressure.

China and emerging markets offer massive growth. State Street is expanding internationally just as these markets institutionalize. Trillions in new assets need custody and administration. State Street's global platform captures this growth.

The Verdict

The bear and bull cases aren't mutually exclusive—both dynamics operate simultaneously. State Street faces real disruption threats while benefiting from powerful competitive advantages. The outcome depends on execution: Can State Street transform fast enough to remain relevant while maintaining the stability clients demand?

The most likely scenario is neither complete disruption nor total dominance but continued evolution. State Street will lose some traditional business to technology competitors while gaining new digital opportunities. Margins will compress but volumes will expand. The company will become more technology-focused while remaining fundamentally a trust business.

The key question isn't whether State Street survives—they're too essential to fail—but whether they thrive. Can they maintain premium margins, or do they become a utility earning regulated returns? Can they lead the digital transformation, or do they become junior partners to technology giants?

History suggests betting against State Street is dangerous. They've survived every financial crisis, adapted to every technological shift, and emerged stronger from every challenge. But history also shows that eventually, every dominant company faces disruption. State Street's next decade will determine whether they're the exception or the rule.

XII. Conclusion: The Future of Financial Infrastructure

State Street's story is far from over. At 232 years old, this institution stands at another inflection point, perhaps its most critical yet. The company that began serving Boston merchants now processes one-tenth of global financial transactions. The bank that pioneered mutual fund custody now builds AI platforms for managing $58 trillion in assets. The firm that invented the ETF now grapples with blockchain and digital assets.

The transformation ahead will be more radical than anything in State Street's history. Traditional custody—the physical safekeeping of paper certificates—evolved into electronic record-keeping. Now it must evolve again into something we can barely imagine: a world where assets exist natively in digital form, where smart contracts automate administration, where artificial intelligence makes investment decisions.

State Street's response reveals the profound challenge facing all financial incumbents. They must cannibalize their own business before others do it for them. They must invest billions in technologies that might eliminate their core services. They must partner with companies that could become competitors. They must maintain perfect operational reliability while experimenting with unproven innovations.

The Alpha platform represents State Street's bet on this future. It's not just a technology upgrade but a complete reimagining of financial services as a data and intelligence business. The platform assumes that value will shift from processing transactions to providing insights, from holding assets to optimizing portfolios, from manual operations to automated intelligence.

But technology alone won't determine State Street's fate. The company's greatest asset remains trust—the confidence of institutions worldwide that State Street will safeguard their assets, settle their trades, and calculate their values accurately. This trust, built over centuries, can't be coded or downloaded. It must be earned transaction by transaction, crisis by crisis.

The competitive dynamics are fascinating. State Street must simultaneously cooperate and compete with the world's most powerful companies. They service BlackRock while competing in ETFs. They rely on Microsoft while building proprietary systems. They enable Goldman Sachs while disintermediating traditional banking. This complex dance requires strategic sophistication rare in any industry.

The regulatory environment adds another layer of complexity. State Street must innovate within constraints that technology companies ignore. They must maintain fortress balance sheets while investing aggressively in transformation. They must serve public policy objectives while maximizing shareholder returns. Threading these needles requires political skill as much as business acumen.

Looking ahead, several scenarios could unfold. In the optimistic case, State Street successfully transforms into a technology-first financial platform, leveraging its trust and expertise to dominate digital finance as thoroughly as traditional finance. The Alpha platform becomes the operating system for institutional investing, as essential as Windows or iOS.

In the pessimistic case, State Street becomes the Kodak of finance—a formerly dominant company disrupted by digital transformation it saw coming but couldn't navigate. Blockchain eliminates custody, AI replaces administration, and State Street shrinks to a regulated utility earning minimal returns.

The most likely outcome lies between these extremes. State Street will probably remain a critical but less dominant player in a more fragmented ecosystem. They'll share the pie with technology companies, blockchain protocols, and new entrants we can't yet imagine. They'll be essential but not irreplaceable, profitable but not dominant.

What makes State Street's story universally relevant is that every company now faces similar challenges. Digital transformation isn't optional. Platforms are eating linear businesses. Software is devouring entire industries. The questions State Street grapples with—how to digitize without losing identity, how to platform without commoditizing, how to innovate without destabilizing—are questions every established company must answer.

State Street's journey also illustrates the importance of timing in business transformation. They digitized custody just as mutual funds exploded. They built processing systems just as ERISA created demand. They launched SPY just as passive investing began its ascent. The lesson isn't about predicting the future but positioning to capitalize when change arrives.

The human element deserves recognition. Behind State Street's transformation are thousands of individuals who chose disruption over comfort. Engineers who joined a bank instead of a tech company. Executives who cannibalized profitable businesses. Regulators who enabled innovation despite risks. Their collective courage transformed a stodgy Boston bank into critical global infrastructure.

As we witness State Street's next chapter, we're really watching the future of finance itself unfold. Will traditional institutions successfully transform into technology companies? Can regulated entities compete with unconstrained innovators? Is trust still valuable in a trustless, blockchain world? State Street's success or failure will help answer these defining questions.

The company that started with a charter from John Hancock now processes transactions that would have seemed magical to its founders. The bank that once financed clipper ships now manages assets in the cloud. The institution that survived the Civil War now battles in cyberspace. Through it all, State Street has demonstrated that adaptation, not age, determines survival.

Whether State Street thrives for another 232 years or disrupts itself into something unrecognizable, its impact on global finance is indelible. They didn't just witness financial history; they wrote it. From mutual funds to ETFs, from paper ledgers to AI platforms, State Street has consistently stood at the frontier of financial innovation.

The ultimate lesson from State Street's story is that infrastructure companies, while unglamorous, shape the possible. By building the rails, they determine where trains can go. By processing the transactions, they enable the economy. By holding the assets, they underpin the system. State Street reminds us that sometimes the most powerful position isn't at the top of the pyramid but at its foundation.

As State Street enters its third century, it faces its greatest test: Can an institution born in the age of sail navigate the age of silicon? Can a company that perfected analog finance master digital finance? Can trust, expertise, and relationships remain valuable in an automated, algorithmic world?

The answers will shape not just State Street's future but the future of finance itself. And if history is any guide, State Street will not merely adapt to that future—they'll help create it, one transaction at a time, one innovation at a time, maintaining their essential role in the global financial system while transforming everything about how they fulfill it.

The silent giant of global finance may remain silent, but it will not remain still. State Street's story continues, and its next chapter may be its most important yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube