Fabrinet: The Hidden Giant Behind the AI Revolution

I. Introduction & Episode Roadmap

Picture a sprawling 4-million-square-foot manufacturing complex just outside Bangkok, where thousands of Thai technicians work in cleanrooms the size of football fields, assembling components so small they make a grain of sand look colossal. At this very moment, these workers are crafting the optical transceivers that power Nvidia's AI data centers, the cables that connect Amazon Web Services' cloud infrastructure, and the precision lasers used in everything from semiconductor fabrication to autonomous vehicles. Welcome to Fabrinet—the most important technology company you've probably never heard of.

In 2025, Fabrinet's revenue was $3.42 billion, an increase of 18.60% compared to the previous year's $2.88 billion. But the numbers alone don't capture the scale of what's happening here. The stock has surged approximately 930% over the past 10 years—more than tripling the performance of the broader tech sector. Fabrinet stock more than tripled the Zacks Tech sector over the last 15 years, soaring 2,660%. From its June 2010 IPO at $10 per share, the stock has delivered returns that would make most venture capitalists weep with envy.

How did a company founded by a controversial disk drive pioneer become the secret weapon powering Nvidia's AI data centers? How did a Thai manufacturer become indispensable to the most transformative technology wave of our lifetime?

The answer lies in understanding a deceptively simple business model that has proven remarkably difficult to replicate: Fabrinet is a specialist contract manufacturer based out of Bangkok, Thailand where they manufacture other people's products, products that are of high complexity. Specialist due to their specialization in precision assembly within the optical communication space—microelectronics, optoelectronics, and mechanical. High complexity due to complex products with precision down to submicron level assembly technologies.

"Submicron assembly is like crafting a delicate, intricate sculpture. It requires the hands of a surgeon and the precision of a watchmaker to handle these ultra-small building blocks. The components you're working with are incredibly tiny building blocks, much smaller than a grain of sand."

This is not Foxconn assembling iPhones at massive scale. This is not Jabil stamping out generic circuit boards. Fabrinet occupies a unique niche at the intersection of high precision and high complexity—a position that has made it irreplaceable to its customers and extraordinarily profitable for its shareholders.

The key themes that emerge from Fabrinet's story are timeless: the power of specialization in an age of diversification, the wisdom of building in geographic locations for reasons beyond labor cost, the strategic value of customer intimacy, and the patient discipline required to ride technology waves without building the technology yourself.

II. The Founder's Journey: Tom Mitchell & The Disk Drive Connection

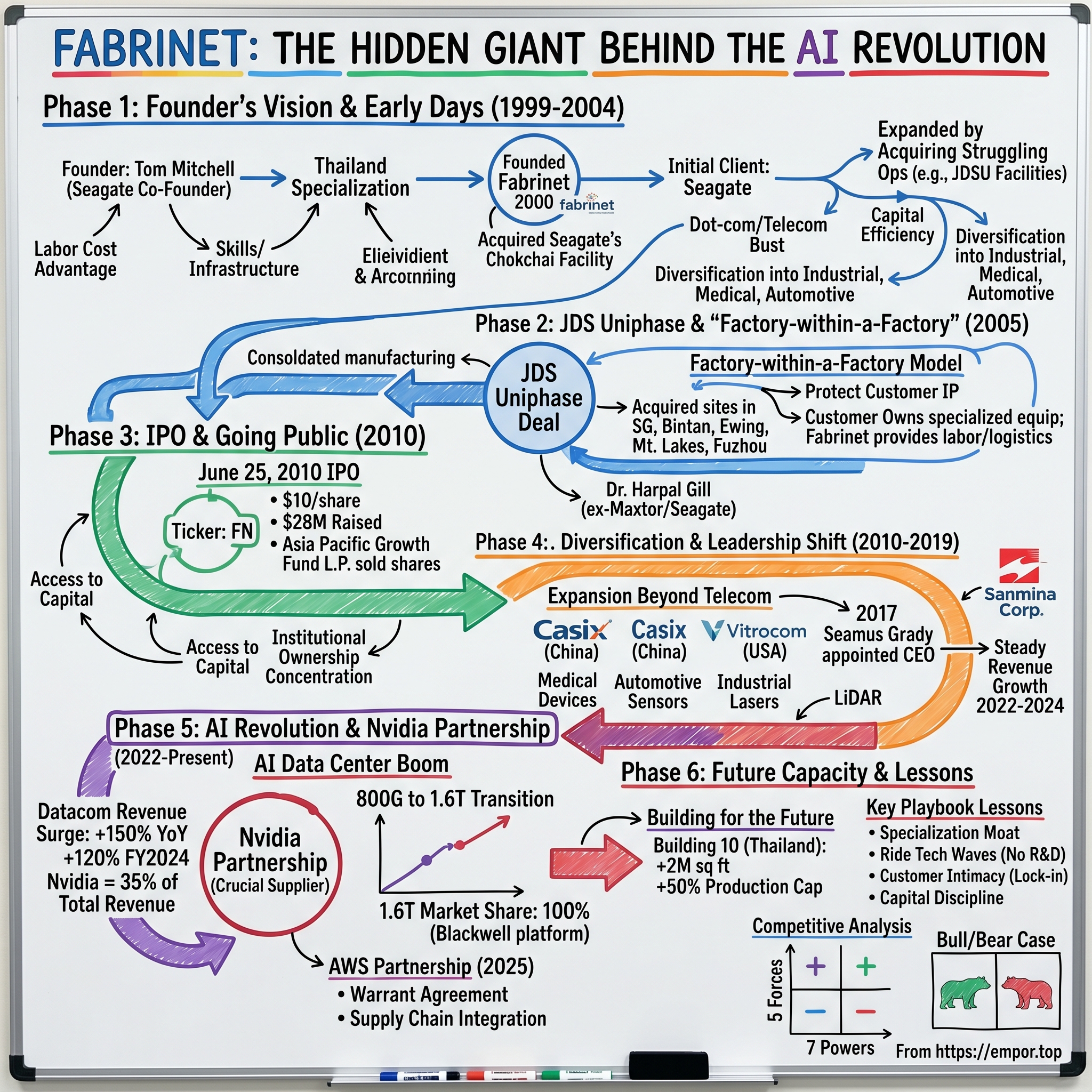

To understand Fabrinet, you must first understand David T. "Tom" Mitchell—a figure so colorful, so controversial, and so consequential that the storage industry still talks about him in hushed tones decades after he departed.

He founded Seagate Technology (with Al Shugart, Doug Mahon, Finis Conner and Syed Iftikar) in November 1, 1978 where he served as president from 1983 to 1991, resigning under pressure of the board of directors. The story of how Mitchell left Seagate is itself instructive: "The controversial Mitchell never tired of rubbing elbows in the foremost circles of the storage industry, first at Seagate and then at Conner Peripherals, before a disastrous spell at JTS. The ex-marine, described by an analyst as 'the Darth Vader of the hard drive industry,' is known to keep a grenade on his desk and made people work 365 days a year."

Mitchell was not a man who inspired lukewarm reactions. Stories about him border on the apocryphal: according to industry lore, when one of his salesmen got lost while driving him to meet a customer in the UK, the salesman "was immediately fired." Whether true or embellished, these tales reflect a personality defined by relentless intensity and an obsessive focus on execution.

Tom Mitchell served as Fabrinet's Executive Chairman from September 2017 through June 2018, and CEO and Chairman from the company's inception in 2000 until September 2017. He also served as President from 2000 to 2011. From 1992 to 1995, Mr. Mitchell served as COO of Conner Peripherals, another disk drive manufacturing company. From 1995 to 1998, he served as CEO of JTS Corp., a mobile disk drive manufacturing company. During his tenure in the data storage industry, Mr. Mitchell established manufacturing operations in Singapore, Thailand, Malaysia, the PRC, and India.

It was this last experience—the years spent building manufacturing operations across Asia—that would prove most valuable. By the late 1990s, Mitchell had accumulated more than two decades of knowledge about precision manufacturing in Asia. He understood something that many executives in Silicon Valley failed to grasp: that successful manufacturing in Asia wasn't simply about finding the cheapest labor. It was about building ecosystems.

"In Thailand, the annual salary of a senior engineer is $10,000, while semi-skilled labor earns $1,500 per year, according to the American Chamber of Commerce in Thailand. English is the second language. The infrastructure is well-developed and aided by strong investment support. Those factors, plus the ability to leverage the rapid launch and product transfer experience from the disk-drive industry, tipped the scale away from other countries."

The insight Mitchell carried into Fabrinet was multifaceted. Thailand offered not just cost advantages but also quality advantages: a workforce with an engineering orientation, an education system actively promoted by the government, and a cultural ethic that valued precision and consistency. "What's unique about the Thai workforce is that unlike many of their Asian counterparts who are educated outside of their country, Thais will return to Thailand to work. Additionally, the government works collaboratively with universities to ensure that the skills taught match the work available."

"I have been an avid supporter of Thailand as a center for precision manufacturing of complex devices for over twenty years," Tom Mitchell himself asserted. "The infrastructure, highly motivated and educated employees, stable political structure, and economic advantages of operating in Thailand make it the ideal country for Fabrinet's growth and business development."

When Mitchell founded Fabrinet in 1999, he wasn't just starting another contract manufacturer. He was applying everything he'd learned about Asian manufacturing to a new opportunity he saw emerging in the telecommunications industry.

Mr. Mitchell founded Fabrinet in 2000 and over the next 25 years grew the organization into a highly-respected public company. This impressive accomplishment was driven by an unwavering commitment to innovation, customer focus, and long-term value creation.

In October 2025, Fabrinet announced the retirement of company founder and Chairman, David T. ("Tom") Mitchell, after 25 years of visionary leadership. Mr. Mitchell, who previously co-founded Seagate Technologies, served as Fabrinet's CEO and Chairman from the company's inception until 2017, when Seamus Grady was appointed CEO. Mr. Mitchell returned to the role of Chairman in 2018, which he held since.

For investors, the founder transition matters. Mitchell built Fabrinet from a startup into a multi-billion-dollar enterprise. The fact that the company continued to thrive under new CEO Seamus Grady—with fiscal 2025 revenues hitting record highs—suggests the organizational capabilities Mitchell built have proven durable beyond his active leadership.

III. Genesis: Founding & Early Days (1999-2004)

The timing of Fabrinet's founding was both brilliant and perilous. The late 1990s saw the telecommunications industry in the midst of an unprecedented investment boom. Companies were laying fiber optic cables across oceans and continents, and demand for optical components was seemingly insatiable.

Mitchell established Fabrinet with the vision of creating a specialized manufacturing partner for optical communications companies during a period of rapid growth in the telecommunications industry. The company began operations with its first manufacturing facility in Chokchai, Thailand, strategically chosen for its skilled workforce, favorable business environment, and lower operating costs.

Fabrinet was founded in 2000 by David T. (Tom) Mitchell, one of the co-founders of Seagate Technology, as a low-volume, high-mix service provider for the manufacturing of complex optical components. The company set out to serve original equipment manufacturers on a contract basis.

The initial setup revealed Mitchell's pragmatic genius. With initial funding from Mr. Mitchell and Hambrecht & Quist Asia, Fabrinet took over the lease of Seagate's Chokchai, Thailand manufacturing site, making Seagate one of Fabrinet's first customers. Rather than building a factory from scratch, Mitchell acquired an existing facility from his former company—giving Fabrinet instant manufacturing capability and an immediate anchor customer.

The firm is a contract electronics manufacturer that took off with the acquisition of a facility in Chokchai, Thailand let go by Seagate. More specifically, the plant in question produces head-stack assemblies, established by Seagate in 1997 and employing 3,329 people in 1999. Located 3 miles north of Bangkok International Airport, the 200,000 square foot facility now boasts 1,500 people and features a 65,000 square foot clean room.

Then came the crash.

The dot-com bust of 2000-2001 and the subsequent telecom winter of 2001-2003 devastated the optical components industry. Companies that had seemed unstoppable—JDS Uniphase, Nortel, Lucent—saw their market values collapse by 90% or more. Hundreds of optical component suppliers went bankrupt.

Yet in the early 2000s, Fabrinet expanded its manufacturing capabilities beyond optical components to include more complex optical modules and subsystems. This expansion coincided with the telecommunications downturn, during which Fabrinet was able to grow by acquiring manufacturing operations from struggling optical companies looking to outsource production.

This is a pattern that would repeat throughout Fabrinet's history: when the industry contracted, Fabrinet expanded. The company's asset-light model—providing labor, logistics, and manufacturing expertise while customers owned their own production equipment—meant Fabrinet could absorb new business without taking on massive capital expenditures.

Fabrinet's operational commencement in January 2000, with the acquisition of a manufacturing plant in Thailand, was a direct result of this early backing. A pivotal moment in its nascent stages was taking over the lease of Seagate's manufacturing facility, which not only solidified its operational capabilities but also established Seagate as one of its first major clients. This strategic move provided Fabrinet with an immediate customer base and a strong operational footprint.

The telecom bust taught Mitchell and his team a crucial lesson that would shape Fabrinet's strategy for decades: diversification matters. The company began methodically expanding into adjacent markets—industrial lasers, automotive sensors, medical devices—even as it maintained its core competency in optical communications.

For investors watching this period, the key insight was the company's capital efficiency. While competitors were raising equity and burning cash to chase growth, Fabrinet was building a sustainable business by focusing on execution excellence.

IV. The JDS Uniphase Inflection Point (2005)

If Fabrinet's founding was Act One, the JDS Uniphase transfer was the moment the company's true potential became visible.

With the 2005 transfer of JDS Uniphase's manufacturing operations to Thailand, the company focused on manufacturing components and modules for optical communication systems as well as industrial lasers and sensors. Fabrinet introduced the "factory within a factory" operating model, creating a secure system where customers provided the equipment needed to build their products while Fabrinet provided the labor, logistics, manufacturing, and a supply chain.

The JDS Uniphase deal didn't happen in isolation. Fabrinet has been manufacturing datacom transceivers for JDS Uniphase at its Bangkok plant since 2002. The 2005 transfer was an expansion of an existing relationship.

Having announced its intention to further reduce its manufacturing "footprint" last month, JDS Uniphase consolidates transceiver assembly with the sale of two facilities to contract manufacturer Fabrinet. Optical component and subsystem vendor JDS Uniphase of San Jose, CA, is to sell two facilities to the manufacturing services company Fabrinet. The deal is part of JDSU's strategy to streamline its overall manufacturing base as it struggles to return to profitability. The agreement includes the sale of two datacom transceiver manufacturing sites to Fabrinet for an undisclosed sum. These facilities are located in Bintan, Indonesia, and Singapore, and affect 450 employees at the two plants. In return, the two companies have signed a "long-term" supply agreement.

In December 2004, the company acquired JDS Uniphase manufacturing facilities in Singapore and Bintan, Indonesia. Earlier this month, JDS Uniphase announced its intent to divest manufacturing facilities in Ewing and Mountain Lakes, New Jersey to Fabrinet as part of broader cost-savings initiatives.

Fabrinet announced its intention to purchase the JDS Uniphase manufacturing facilities located in Fuzhou, China. Under the terms of the arrangement, Fabrinet will acquire all assets and operations related to the Fuzhou plant including R&D and the manufacture of products such as crystals and precision optics. The 225,000 square foot Fuzhou plant employs over 500 engineers, technicians, and skilled operators, all of whom are expected to transfer to Fabrinet and continue their employment at the site. Fabrinet intends to utilize the existing core management and technical expertise at the site to grow its optical component business in China and in other regions the company serves.

The "factory within a factory" model deserves special attention because it addresses the core tension in contract manufacturing: how do you protect customer intellectual property while still achieving the cost efficiencies of outsourcing?

Traditional contract manufacturers like Foxconn or Jabil operate massive facilities where multiple customers' products are manufactured on shared equipment. This creates economies of scale but raises legitimate concerns about IP protection and cross-contamination of proprietary processes.

Fabrinet's model inverted this approach. Each major customer effectively operates their own mini-factory within Fabrinet's larger facility. The customer owns their specialized equipment and tooling. Fabrinet provides the facility, the trained workforce, the supply chain management, and the operational expertise. This creates natural switching costs—if a customer wants to move their production elsewhere, they need to physically relocate their equipment and retrain an entirely new workforce.

"As his first order of business, Harpal will be responsible for the transfer of recently acquired JDS Uniphase assembly operations from New Jersey to our factories in Thailand," said Tom Mitchell, Chairman and CEO of Fabrinet.

The executive Fabrinet brought in to manage this transition was no coincidence. Dr. Harpal Gill joined with over 25 years experience in mechanical design, process design and development, automation, and state of the art quality systems engineering in the United States, Europe, and Asia, serving as senior vice president of operations and managing director of Fabrinet's New Jersey, USA subsidiary. Dr. Gill's vast background includes positions as senior vice president of engineering for Maxtor Corporation, vice president of engineering for Read Rite Corporation in Bangkok, managing director of the JTS drive manufacturing plant in Chennai, India, as well as senior management positions with Seagate Technology.

Notice the pattern: Fabrinet's leadership team was populated with veterans from Mitchell's prior companies in the storage industry. These weren't just experienced executives—they were people who had worked together for years, who understood Mitchell's management philosophy, and who shared his obsession with precision manufacturing.

For investors, the JDS Uniphase deal marked Fabrinet's transformation from a scrappy startup into a serious industry player. The company gained scale, critical optical manufacturing expertise, and a template for future customer relationships.

V. The IPO & Going Public (2010)

Five years after the JDS Uniphase deal established Fabrinet as a serious player in optical manufacturing, the company took its next major step: accessing the public markets.

On June 25, 2010, Fabrinet announced the initial public offering of 8,500,000 shares of common stock at a price to the public of $10.00 per share. The shares began trading on the New York Stock Exchange under the ticker symbol "FN." Of the shares being offered, Fabrinet offered 2,830,000 shares and the majority shareholder, Asia Pacific Growth Fund III, L.P., a private equity fund managed by H&Q Asia Pacific, along with certain other shareholders, offered 5,670,000 shares. Additionally, the selling shareholders granted the underwriters a 30-day option to purchase up to an additional 1,275,000 shares.

The IPO structure reveals important details about Fabrinet's ownership history and capital discipline. The company itself raised approximately $28 million, while selling shareholders—primarily H&Q Asia Pacific's private equity fund—monetized a significant portion of their holdings. This reflected a company that didn't need massive external capital to grow but was providing liquidity to its early backers.

Fabrinet's ownership structure saw a significant shift with its New York Stock Exchange IPO in 2010 under the ticker symbol 'FN'. This event marked the beginning of its journey as a publicly traded entity, influencing its shareholder base and market presence.

The timing of the IPO was significant. By 2010, the telecom industry had largely recovered from the post-2001 downturn, and new drivers of optical component demand were emerging: the rise of data centers, the early stirrings of cloud computing, and the proliferation of smartphones driving mobile data traffic.

Fabrinet provides precision optical, electro-mechanical and electronic manufacturing services to original equipment manufacturers of complex products, such as optical communication components, modules and sub-systems, industrial lasers and sensors. Fabrinet offers a broad range of advanced optical capabilities across the entire manufacturing process, including process engineering, design for manufacturability, supply chain management, manufacturing, final assembly and test. Fabrinet focuses primarily on low-volume production of a wide variety of products, which it refers to as "low-volume, high-mix."

The value creation since that IPO has been extraordinary. A $10,000 investment at the IPO price would be worth over $400,000 today—a 40x return in 15 years, far exceeding even the spectacular returns of the broader tech sector.

As of mid-2025, Fabrinet's ownership is largely dominated by institutional investors, with their holdings exceeding the total shares outstanding, a common occurrence due to various reporting methodologies and short positions. Insider ownership also represents a substantial portion, while retail investor ownership is negligible. This concentration of institutional ownership can significantly influence the company's strategic direction and corporate governance through their voting power and engagement with management.

For fundamental investors, the post-IPO period demonstrated Fabrinet's ability to compound capital at exceptional rates. The company consistently generated strong cash flows, maintained a conservative balance sheet, and expanded its manufacturing footprint without diluting shareholders through repeated capital raises.

VI. The Business Model Deep Dive

Understanding Fabrinet's competitive position requires drilling into the specifics of how the company makes money and why that model has proven so durable.

The Low-Volume, High-Mix Model

"One is, we focus on a few key areas. So we're quite specialized. We don't try to do everything. We don't claim to be good at everything, but the things that we focus on, we try to be really excellent in those things. And I think customers come to us because we provide, we believe, really excellent quality delivery service with a main focus on the customer." Contract manufacturing is inherently a tough business—margins are razor thin.

The key strategic choice Fabrinet made was to focus on the hardest products in the hardest market segment. Rather than competing with Foxconn and Jabil on volume, Fabrinet positioned itself as the specialist you call when standard EMS providers can't meet your requirements.

"We believe there is no other manufacturing services provider with a similar breadth and depth of optical and electro-mechanical engineering and process technology capabilities that does not directly compete with its customers in their end-markets. As a result, we believe we are more closely aligned and better able to develop long-term relationships with our customers than our competitors."

This last point is crucial. Fabrinet doesn't compete with its customers. Companies like Lumentum and Coherent (formerly II-VI) are both customers and competitors of traditional contract manufacturers. They outsource some manufacturing while retaining capacity for their most strategic products. Fabrinet's pure contract manufacturing model eliminates this conflict.

Cost Structure Advantage

Fabrinet's financial structure is fundamentally different from traditional manufacturers.

The company operates with a lean cost base where over 80% of total costs are variable, originating from bills of material (BOM), while fixed costs constitute only about 7% of total sales. This structure enables Fabrinet to swiftly adapt to changes in demand—a critical capability in cyclical industries like optical communications.

When demand drops, Fabrinet's costs drop proportionally. When demand surges, the company can ramp production without needing to first invest in expensive capacity additions. This flexibility has allowed Fabrinet to maintain relatively stable profitability through multiple industry cycles.

Customer Relationships

The firm's latest annual report shows the impact of Nvidia's investment in AI-related datacoms infrastructure, with the technology giant accounting for 35 per cent of Fabrinet's sales revenues in the latest fiscal year—equivalent to just over $1 billion. That figure rose from 12.5 per cent, or approximately $330 million, in the prior year, with Cisco Systems the only other customer to account for more than 10 per cent of Fabrinet's latest annual sales.

The customer concentration numbers are striking. Nvidia alone accounts for over a third of Fabrinet's revenues—a relationship that has grown explosively with the AI boom. This creates both opportunity and risk.

The opportunity is obvious: as Nvidia's AI business continues to grow, Fabrinet participates in that growth. Analysts expect Fabrinet's business with Nvidia to increase from an estimated $990 million in 2024 to $1.4 billion in 2025. According to their calculations, Nvidia would only need to capture 25% of the back-end GPU transceiver market for Fabrinet to meet this target.

The risk is equally obvious: if Nvidia's business declines or the relationship sours, Fabrinet faces a significant revenue headwind.

Product Portfolio

Fabrinet's products include switching products, including reconfigurable optical add-drop multiplexers, optical amplifiers, modulators, and other optical components and modules that enable network managers to route voice, video, and data communications traffic through fiber optic cables at various wavelengths, speeds, and over various distances. The company's products also comprise transceivers, tunable lasers, and transponders; and active optical cables, which provide high-speed interconnect capabilities for data centers and computing clusters. In addition, it provides solid state, diode-pumped, gas, and fiber lasers used in semiconductor processing, biotechnology and medical device, metrology, and material processing industries; and differential pressure, micro-gyro, fuel, and other sensors used in automobiles. Further, the company designs and fabricates application-specific crystals, lenses, prisms, mirrors, laser components, and substrates; and other custom and standard borosilicate, clear fused quartz, and synthetic fused silica glass products.

The breadth of products is impressive, but the common thread is precision. These aren't commodity components—they're highly engineered devices that require submicron assembly tolerances.

Geographic Footprint

Headquartered in George Town, Grand Cayman, Cayman Islands, with principal executive offices in Bangkok, Thailand, Fabrinet operates primarily through its manufacturing facilities in Thailand, China, and the United States. The company employs approximately 14,213 people worldwide.

The Cayman Islands incorporation is standard for many international companies seeking tax efficiency and regulatory flexibility. The real action happens in Thailand, where Fabrinet operates massive manufacturing campuses.

One of the country's top 10 employers, Fabrinet continues to expand its manufacturing operations in Thailand. Approximately 10 years ago, Asian outsourcing guru Tom Mitchell, co-founder of Seagate and current CEO of Fabrinet, conducted an extensive around-the-world investigation for the location of its optical component manufacturing. He chose Thailand.

For investors, the key insight is that Fabrinet's business model—low-volume, high-mix precision manufacturing with a variable cost structure and deep customer relationships—creates durable competitive advantages. These advantages become more valuable as optical communications becomes more critical to the global economy.

VII. The Diversification Play: Beyond Telecom (2010-2019)

The decade following Fabrinet's IPO saw the company systematically expand beyond its original telecom-focused business, building resilience against the cyclical nature of optical communications.

Acquired Casix (Fuzhou, China) and Vitrocom (Mt. Lake, NJ.) Producing: Custom optics, Custom precision glass components and Connectorization solutions.

These acquisitions strengthened Fabrinet's vertical capabilities. Casix gave the company crystal and precision optics manufacturing expertise in China, while Vitrocom added specialty glass fabrication in the United States.

The diversification strategy extended to end markets as well. By the mid-2010s, Fabrinet was manufacturing:

- Industrial lasers used in semiconductor processing, biotechnology, medical devices, and material processing

- Automotive sensors including MEMS-based components for advanced driver assistance systems

- Medical devices requiring precision optical and electro-mechanical assemblies

- LiDAR components for autonomous vehicles

Fabrinet annual revenue for 2024 was $2.883B, a 8.99% increase from 2023. Fabrinet annual revenue for 2023 was $2.645B, a 16.93% increase from 2022. Fabrinet annual revenue for 2022 was $2.262B, a 20.37% increase from 2021.

The steady revenue growth through this period reflected both the success of diversification efforts and the underlying strength of demand for precision optical manufacturing.

A critical leadership transition occurred in 2017 when Seamus Grady became Fabrinet's Chairman and Chief Executive Officer. He joined Fabrinet in September 2017 as Chief Executive Officer. Prior to joining Fabrinet, Seamus served as Executive Vice President & Chief Operating Officer with Sanmina Corporation.

Mr. Grady brings broad and deep experience to Fabrinet in the electronics manufacturing services industry, having most recently served as Executive Vice President and Chief Operating Officer of the Mechanical Systems Division at Sanmina Corporation, where he oversaw 10 facilities in five countries. Mr. Grady's tenure at Sanmina spanned 13 years, including the past eight years with progressively increasing leadership responsibilities. Mr. Grady previously held operations, materials and supply chain management leadership positions at Lucent Technologies and Manufacturers Services.

The choice of Grady was strategic. Here was an executive who understood contract manufacturing from the inside—someone who had run global operations for one of Fabrinet's largest competitors. His operational expertise complemented Mitchell's entrepreneurial vision.

Originally from the West of Ireland, Seamus relocated to the USA with his family in 2013. Seamus is a graduate of the National University of Ireland, Galway (NUIG) where he earned a Bachelor's Degree in Manufacturing Technology.

For investors analyzing this period, the key takeaway was that Fabrinet was building optionality. By diversifying into automotive, medical, and industrial markets while maintaining its core optical communications business, the company reduced its dependence on any single end market or customer.

VIII. The AI Revolution: Nvidia Partnership & Datacom Explosion (2022-Present)

If Fabrinet's first two decades were about building capabilities and diversifying the customer base, the past three years have been about riding the most explosive demand wave in the company's history.

Fabrinet (NYSE:FN) is quietly becoming a crucial player in the AI industry. This original equipment manufacturer (OEM) is catching investor attention thanks to its strategic partnership with Nvidia Corp. It recently became a vital partner within Nvidia's data center operations. With AI applications demanding increasingly high data rates, Fabrinet's role in producing cutting-edge optical communication products has become indispensable.

The numbers tell the story. Fabrinet's datacom division, which supplies fiber-optic cables to AI data centers, has seen significant expansion over the past two years. Starting with $88 million in quarterly revenue in 2022, the company recently reported that its datacom revenue has skyrocketed to over $305 million, reflecting the strong surge in AI-driven demand. In the third quarter earnings call, Seamus Grady, the CEO of Fabrinet, underlined how this 150% jump in datacom revenue had benefited from the rise in demand for 800 gigs technology for AI applications.

Datacom revenues, 42% of Fabrinet's quarterly sales, surged by 150% year-over-year. This illustrates the significant impact of the Nvidia partnership on Fabrinet's bottom line.

"[Fiscal] 2024 was quite a remarkable year for Fabrinet," CEO Grady told investors. "Datacom revenue grew over 120 per cent, while telecom revenue declined more than 20 per cent for the year, due to the protracted inventory digestion across the telecom industry."

The 800G to 1.6T Transition

Fabrinet provides Nvidia with optical-based connections, networking cables, and related services, including very short-reach AOCs with 800G transceivers.

From 2023 to 2025, the company shifted its focus to high-speed optical components, particularly 800G and 1.6T transceivers, which are critical for hyperscale data centers and AI training. By 2025, Fabrinet had achieved a 100% market share in 1.6T transceivers for NVIDIA's Blackwell platform, a testament to its technical expertise and customer alignment.

The jump from 800G to 1.6T transceivers represents a generational shift in optical networking technology. These aren't incremental improvements—they're fundamental changes in how data moves within and between AI clusters. Fabrinet's ability to capture 100% market share in 1.6T transceivers for Nvidia's Blackwell platform demonstrates the depth of its manufacturing capabilities.

CEO Grady noted that Nvidia's latest architecture meant that 800G products would not be cannibalized by 1.6T products. "Normally… when a new technology comes along, it tends to cannibalize the old technology. But certainly, as we go to higher speeds, 1.6T and beyond, it doesn't seem like the 800G is going anywhere, is going to decline," Grady noted. This potentially relieves pressure on Fabrinet to wrap up the still-young 800G products in favor of 1.6T products.

The AWS Partnership (2025)

Fabrinet announced on Thursday that it has entered into a significant transaction with e-commerce giant Amazon.com, Inc. This strategic move involves the issuance of a warrant for Amazon to purchase up to 381,922 ordinary shares of Fabrinet at a price of $208.4826 per share. The warrant, which was issued on Wednesday, March 12, 2025, allows Amazon's wholly-owned affiliate to exercise the option on a cashless basis and will expire on March 12, 2032. Of the total shares, 38,192 have vested immediately with the remainder to vest based on future payments made to Fabrinet by Amazon or its affiliates.

On top of all that, Fabrinet and Amazon entered into an agreement in March for Amazon to buy warrants to purchase up to 381,922 shares of Fabrinet at $208.4826 per share. The deal incentivizes Fabrinet to deepen its role within Amazon's supply chain to help support the growth of AMZN's AI infrastructure.

This warrant structure is increasingly common in tech supply chain relationships. Amazon has executed similar deals with other manufacturing partners. The warrant gives Amazon skin in the game—if Fabrinet succeeds, Amazon profits not just from the products but from the equity appreciation.

CEO Seamus Grady described the scope of the relationship with AWS as broad contract manufacturing work, without delving into specific product categories. Fabrinet aims to perform margin-accretive contract manufacturing for AWS, starting from the component level with high value adds. The company is also considering full-system assembly for AWS servers, provided it can supply a significant portion of the bill of materials to ensure profitability. The ramp-up of AWS revenues for Fabrinet is expected to be steep compared to the gradual revenue increase from the company's other telecom customers.

For investors, the Nvidia and AWS partnerships represent transformational opportunities. These aren't just large customers—they're the two dominant players in AI infrastructure, each investing hundreds of billions of dollars in data center buildouts.

IX. Building for the Future: Capacity Expansion

The demand explosion has created a capacity challenge that Fabrinet is addressing with its most ambitious expansion ever.

Construction of Building 10 in Thailand, a 2 million-square-foot facility, is set to increase production by 50%, addressing the high-mix, low-volume demands of complex optical components.

With the continued strong performance—Fabrinet has posted record sales and earnings per share in each of its last four quarters—the company is set for further expansion, aiming to break ground on a new 2 million square-foot building at its Chonburi campus. Known as "Building 10", the latest facility is expected to cost around $110 million, and take 18 months to complete.

To put this in perspective: Fabrinet historically generated approximately $1,200 in annual revenues per square foot of manufacturing space. Building 10's 2 million square feet could theoretically support $2.4 billion in additional annual revenue—nearly doubling the company's current scale.

Grady added that multiple growth drivers were now pushing Fabrinet towards quarterly revenues of $1 billion, with the firm looking to accelerate the completion of part of its giant new "Building 10" facility in order to meet booming customer demand. Despite that positive demand environment, which now includes a significant deal with AWS driven by high-performance computing requirements, and little anticipated impact from new US trade tariffs, Fabrinet's stock price dropped in value by around 10 per cent following the latest update.

Building 10 Expansion—Construction of the 2 million-square-foot facility remains on track, with a portion being accelerated for mid-2026 completion to support growth capacity. With numerous growth drivers supporting our confidence, construction of Building 10, which will total 2 million square feet, remains on track for completion by the end of calendar 2026. We have accelerated the construction of a portion of Building 10, which we expect to be completed in mid-2026, in order to help ensure that we will have ample capacity to support our rapid growth.

The capacity expansion timing is critical. Fabrinet is racing to bring new capacity online before it constrains growth. The accelerated timeline for part of Building 10 reflects management's confidence that demand will continue to outpace supply.

For fundamental investors, capacity expansion represents both opportunity and risk. The opportunity is obvious: more capacity enables more revenue. The risk is that if AI investment slows or customer relationships change, Fabrinet could be left with expensive, underutilized facilities.

X. Financial Performance & The Numbers

The financial results tell a story of disciplined execution and accelerating growth.

Revenue Growth

Revenue for fiscal year 2025 was $3.42 billion, compared to $2.88 billion for fiscal year 2024. GAAP net income for fiscal year 2025 was $332.5 million, compared to $296.2 million for fiscal year 2024. GAAP net income per diluted share for fiscal year 2025 was $9.17, compared to $8.10 for fiscal year 2024.

Seamus Grady, Chief Executive Officer of Fabrinet, said, "Our fourth quarter was exceptional, capping off a remarkable year with strong momentum. We achieved record quarterly revenue of $910 million, exceeding our guidance range. Through excellent execution, our non-GAAP EPS also reached a new all-time high. For all of fiscal year 2025, we achieved record revenue of $3.4 billion, an increase of 19% from the prior year."

The most recent quarter shows continued acceleration. Revenue reached $978 million in Q1 FY2026, up 22% year-over-year and up 8% sequentially from Q4 FY2025, representing a new company record. Seamus Grady said, "We had an outstanding first quarter with revenue of $978 million dollars, which was above our guidance range. This record result was driven by another strong telecom performance, an early contribution from new High-Performance Computing revenue, and a smaller than anticipated sequential decline in datacom revenue. With continued strong execution, our revenue upside flowed directly to the bottom line, resulting in record earnings per share that also exceeded our guidance."

For the second quarter of fiscal 2026, the company forecasts revenue between $1.05 billion and $1.10 billion, well above the consensus estimate of $986.8 million. Adjusted earnings per share are expected to range from $3.15 to $3.30, compared to the analyst consensus of $2.99.

The guidance for Q2 2026 is remarkable—at the midpoint, it implies 29% year-over-year growth. "I think as you rightly point out, we had last year, we grew 19%. Last quarter, 22%. This quarter at the midpoint, as Csaba mentioned, we're projected to grow 29%. We're just going to focus on executing."

Profitability

Net Margin: The company's net margin is a standout performer, exceeding industry averages. With an impressive net margin of 9.32%, the company showcases strong profitability and effective cost control. Return on Equity (ROE): Fabrinet's ROE stands out, surpassing industry averages. With an impressive ROE of 4.34%, the company demonstrates effective use of equity capital and strong financial performance. Return on Assets (ROA): Fabrinet's ROA surpasses industry standards, highlighting the company's exceptional financial performance.

For a contract manufacturer, these margins are exceptional. The typical EMS company operates with gross margins in the single digits and net margins of 2-4%. Fabrinet's ability to generate nearly 10% net margins reflects its specialization in high-complexity products where pricing power is greater.

Balance Sheet Strength

Fabrinet is a well-run company with a stellar balance sheet, holding more cash and equivalents ($951 million) than total liabilities ($712 million).

Cash and investments: $934 million. Share repurchases: $126 million in fiscal 2025.

This balance sheet strength provides multiple advantages: the ability to fund expansion internally, the flexibility to weather downturns, and the capacity to return capital to shareholders through buybacks.

Key Metrics to Watch

For investors tracking Fabrinet's ongoing performance, three metrics stand out as most critical:

-

Datacom Revenue as a Percentage of Total Revenue: This metric captures Fabrinet's exposure to AI-driven demand. Currently around 52% of optical communications revenue, this ratio indicates how central Fabrinet has become to AI infrastructure.

-

Revenue Per Square Foot: With significant capacity expansion underway, this metric will indicate whether Fabrinet is successfully filling new facilities. Historical performance of ~$1,200/sq ft provides a benchmark.

-

Customer Concentration (Top Customer as % of Revenue): Nvidia at 35% represents significant concentration risk. Diversification of the customer base—particularly the AWS relationship—will be important for long-term stability.

XI. Playbook: Business & Investing Lessons

Fabrinet's journey offers several timeless lessons for business strategists and investors alike.

Lesson 1: The Power of Specialization

Fabrinet's strategy was simple—focus on 3-4 things that they're very good at, then try to be the best in it. Competitors on the other hand try to compete on all fronts and be a jack of all trades. This "master of one" strategy was and continues to be the fundamental element of differentiation between Fabrinet and other EMS players of the world.

In an era when business schools teach diversification and platform strategies, Fabrinet bet on extreme specialization. The company chose "low-volume, high-mix" when everyone else was chasing scale. The result: a defensible moat built on precision manufacturing capabilities that take decades to replicate.

Lesson 2: Riding Technology Waves Without Building the Technology

Fabrinet doesn't own any optical technology intellectual property. It doesn't design transceivers or develop new laser technologies. Instead, it provides the manufacturing expertise that allows customers to bring their innovations to market.

This approach offers significant advantages: lower R&D costs, reduced technology risk, and the ability to serve multiple competing customers. When the market shifted from telecom to datacom, Fabrinet pivoted seamlessly—same capabilities, new applications.

Lesson 3: Customer Intimacy as Strategy

The "factory within a factory" model isn't just about protecting IP—it's about creating deep, structural relationships with customers. When a customer has invested in specialized equipment installed in Fabrinet's facilities and trained Fabrinet workers to operate that equipment, switching costs become prohibitive.

This explains why Fabrinet's customer relationships often span decades. The investment required to relocate production creates natural lock-in that benefits both parties.

Lesson 4: Geographic Arbitrage Done Right

Tom Mitchell didn't choose Thailand simply because labor was cheap. He chose Thailand because it offered the right combination of workforce quality, infrastructure, political stability, and cost advantages. "Choosing Thailand has proven to be quite successful for Fabrinet, which recently built a fifth manufacturing facility on its campus near Bangkok to accommodate its expanding business. A major factor in Fabrinet's expansion has been the strength of Thailand's supply chain. 'Once you sign a contract, it is upheld,' Gill says. 'We don't need to worry about the quality of the products or whether it was built to the correct specifications.'"

Lesson 5: Capital Efficiency & Discipline

Throughout its history, Fabrinet has grown primarily through internal cash generation rather than equity raises. The company's variable cost structure enables flexibility, and strong cash generation funds growth without shareholder dilution.

XII. Competitive Analysis: Porter's 5 Forces

Threat of New Entrants: LOW

The barriers to entering Fabrinet's market are substantial. Submicron assembly requires specialized equipment, trained workers, and accumulated process knowledge that takes years to develop. "Submicron assembly is like crafting a delicate, intricate sculpture. It requires the hands of a surgeon and the precision of a watchmaker to handle these ultra-small building blocks. The components you're working with are incredibly tiny building blocks, much smaller than a grain of sand."

Customer relationships built over decades cannot be replicated quickly. Significant capital investment is required for precision manufacturing facilities. New entrants would face a chicken-and-egg problem: they can't build expertise without customers, and they can't attract customers without demonstrated expertise.

Bargaining Power of Suppliers: MODERATE

Over 80% of Fabrinet's costs come from bills of material—components purchased from suppliers. The company sources from multiple suppliers for most materials, reducing dependence on any single source. However, some specialized components may have limited suppliers, creating potential bottlenecks.

Bargaining Power of Buyers: MODERATE-HIGH

Customer concentration is Fabrinet's most significant structural risk. "Customer concentration and networked exposure create systemic risk." Nvidia alone accounts for 35% of revenues. However, the "factory within a factory" model creates significant switching costs that partially offset buyer power.

Threat of Substitutes: LOW-MODERATE

Nvidia, a significant customer, is moving towards copper-based solutions for its latest GPUs. This represents a potential threat—if copper can replace optical interconnects in some applications, demand for Fabrinet's products could decline. However, for high-bandwidth AI applications, optical remains superior for longer distances and higher speeds. In-house manufacturing by OEMs is an alternative but is generally more costly than outsourcing to specialists.

Competitive Rivalry: MODERATE

Fabrinet operates in the highly competitive electronic manufacturing services (EMS) industry, with a specialized focus on optical communications and advanced manufacturing services. In the optical communications segment, Fabrinet's primary competitors include Sanmina Corporation, Jabil Inc., Flex Ltd., and Celestica Inc. These companies offer similar manufacturing services but typically have a broader focus across multiple industries, whereas Fabrinet has maintained a more specialized approach centered on optical and precision manufacturing.

In the optical components and modules space, Fabrinet also competes with vertically integrated manufacturers such as Lumentum Holdings Inc., II-VI Incorporated (now Coherent Corp.), and Acacia Communications. However, many of these companies are also Fabrinet customers, creating a complex competitive landscape where Fabrinet serves both as a supplier and competitor.

XIII. Hamilton's 7 Powers Framework Analysis

1. Scale Economies: MODERATE

Fabrinet doesn't pursue scale in the traditional sense—its "low-volume, high-mix" strategy explicitly rejects high-volume commoditization. However, scale in Thailand operations creates cost advantages through workforce depth, supply chain relationships, and facility utilization. The company employs approximately 14,213 people worldwide.

2. Network Effects: WEAK

Limited direct network effects exist in contract manufacturing. However, some indirect effects emerge through ecosystem relationships—as Fabrinet becomes more central to the optical communications supply chain, it becomes a natural nexus for related capabilities.

3. Counter-Positioning: STRONG

This is perhaps Fabrinet's strongest power. Traditional EMS companies like Foxconn and Jabil built their businesses around high-volume production of relatively simple assemblies. They cannot easily pivot to precision optical manufacturing without cannibalizing their existing business models and retraining their entire workforce.

By 2025, Fabrinet had achieved a 100% market share in 1.6T transceivers for NVIDIA's Blackwell platform, a testament to its technical expertise and customer alignment. This vertical integration into advanced packaging and system-level solutions has allowed the company to move beyond traditional component manufacturing, offering end-to-end value that differentiates it from peers like Coherent and Lumentum.

4. Switching Costs: STRONG

The "factory within a factory" model creates substantial switching costs. Customers own specialized equipment installed in Fabrinet facilities, and Fabrinet workers are trained on customer-specific processes. Moving production requires physically relocating equipment and retraining an entirely new workforce—a multi-year, multi-million-dollar endeavor.

5. Branding: MODERATE

In B2B contract manufacturing, branding operates differently than in consumer markets. Fabrinet's reputation for quality, reliability, and customer service creates preference among OEMs, but this is more "industrial reputation" than consumer brand power.

6. Cornered Resource: MODERATE

Fabrinet's trained workforce in Thailand represents a cornered resource. The company has spent 25 years developing precision manufacturing skills in thousands of workers. This capability cannot be quickly replicated.

7. Process Power: STRONG

The accumulated knowledge of how to manufacture complex optical components at submicron tolerances represents significant process power. This expertise has been built over two decades and is embedded in institutional knowledge, documented processes, and skilled workers.

XIV. Bull Case vs. Bear Case

Bull Case

The AI infrastructure buildout is just beginning. Hyperscalers like Amazon, Microsoft, Google, and Meta have announced hundreds of billions in data center investments over the coming years. Every AI cluster requires optical interconnects, and Fabrinet manufactures many of the highest-performance products in the market.

Customer relationships create durability. The AWS partnership, adding to existing relationships with Nvidia, Cisco, Lumentum, and others, diversifies Fabrinet's customer base while deepening its role in AI infrastructure.

Telecom revenue surged 59% year-over-year, driven by data center interconnect (DCI) products, which nearly doubled to 14% of company revenue. The company introduced a new revenue category for high-performance computing (HPC) products, contributing $15 million to Q1 revenue, with expectations for significant growth. Fabrinet is optimistic about continued growth in Q2, with revenue projected to be between $1.05 billion and $1.1 billion, representing a 29% year-over-year increase at the midpoint.

Capacity expansion enables continued growth. Building 10 provides runway for revenue to potentially double from current levels without major additional capital investment.

Management has proven execution capability. CEO Seamus Grady has successfully navigated multiple industry cycles and technology transitions since taking over in 2017.

Bear Case

Customer concentration creates vulnerability. With Nvidia at 35% of revenues, any disruption to that relationship—whether from competitive dynamics, technology shifts, or business disputes—would significantly impact Fabrinet.

Technology shifts could reduce optical demand. Copper interconnects continue to improve, and Nvidia's exploration of copper-based solutions for some applications raises questions about the long-term optical opportunity.

Valuation reflects high expectations. The stock trades at a price-to-earnings (P/E) ratio of 42.60. This valuation assumes continued rapid growth—any deceleration could lead to multiple compression.

Geopolitical risks remain. While Thailand is generally stable, trade tensions between the US and China create uncertainty. Fabrinet's operations in China through Casix add exposure to potential sanctions or tariffs.

XV. Key Risks & Regulatory Considerations

Customer Concentration: The single largest risk factor. Nvidia and Cisco together represent roughly half of revenues. Loss of either relationship would significantly impact financial performance.

Technology Transition Risk: The shift from 800G to 1.6T transceivers is underway. Fabrinet appears well-positioned, but execution risk remains in ramping new products.

Supply Chain Dependencies: Supply constraints would temporarily restrict the firm's shipments of new 1.6 Tb/s optical transceivers over the next few months. Component shortages remain a potential constraint on growth.

Tariff and Trade Policy: While Thailand-based manufacturing currently benefits from favorable trade treatment, changing US trade policies could affect cost competitiveness relative to manufacturing in other locations.

Currency Exposure: With manufacturing in Thailand and significant costs in Thai baht, currency fluctuations can affect profitability.

XVI. Conclusion

Fabrinet represents a particular kind of business success story: the company that does one thing extraordinarily well and refuses to be distracted by opportunities outside its core competency.

From Tom Mitchell's controversial departure from Seagate to the founding of a small contract manufacturer in Thailand, through industry crashes and technology transitions, to the current moment as an essential enabler of the AI revolution—Fabrinet has demonstrated the enduring value of precision, specialization, and customer focus.

"Seeing Fabrinet grow from a start-up to a multi-billion-dollar organization has been the highlight of my professional career," said Tom Mitchell upon his retirement. "I have taken great pride in seeing the core values we established at inception—exceptional customer service, advanced manufacturing innovation, and delivering a compelling value proposition—continue to guide the business."

For investors, Fabrinet offers exposure to several powerful secular trends: the AI infrastructure buildout, the insatiable demand for data center bandwidth, and the continued growth of cloud computing. The company's differentiated business model, strong customer relationships, and proven management team provide reasonable confidence in execution.

The risks are real: customer concentration, technology transitions, and valuation expectations all warrant careful monitoring. But for long-term investors seeking exposure to the physical infrastructure underlying the AI revolution, Fabrinet deserves serious consideration.

The hidden giant behind the AI revolution isn't so hidden anymore. The question for investors is whether Fabrinet's best days are behind it—or whether the company is just getting started.

Key Performance Indicators to Track:

- Datacom Revenue Mix (currently ~52% of optical communications): Indicates exposure to AI-driven demand

- Customer Concentration (Nvidia at ~35%): Measures diversification risk

- Revenue per Square Foot: Tracks capacity utilization as Building 10 comes online

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube