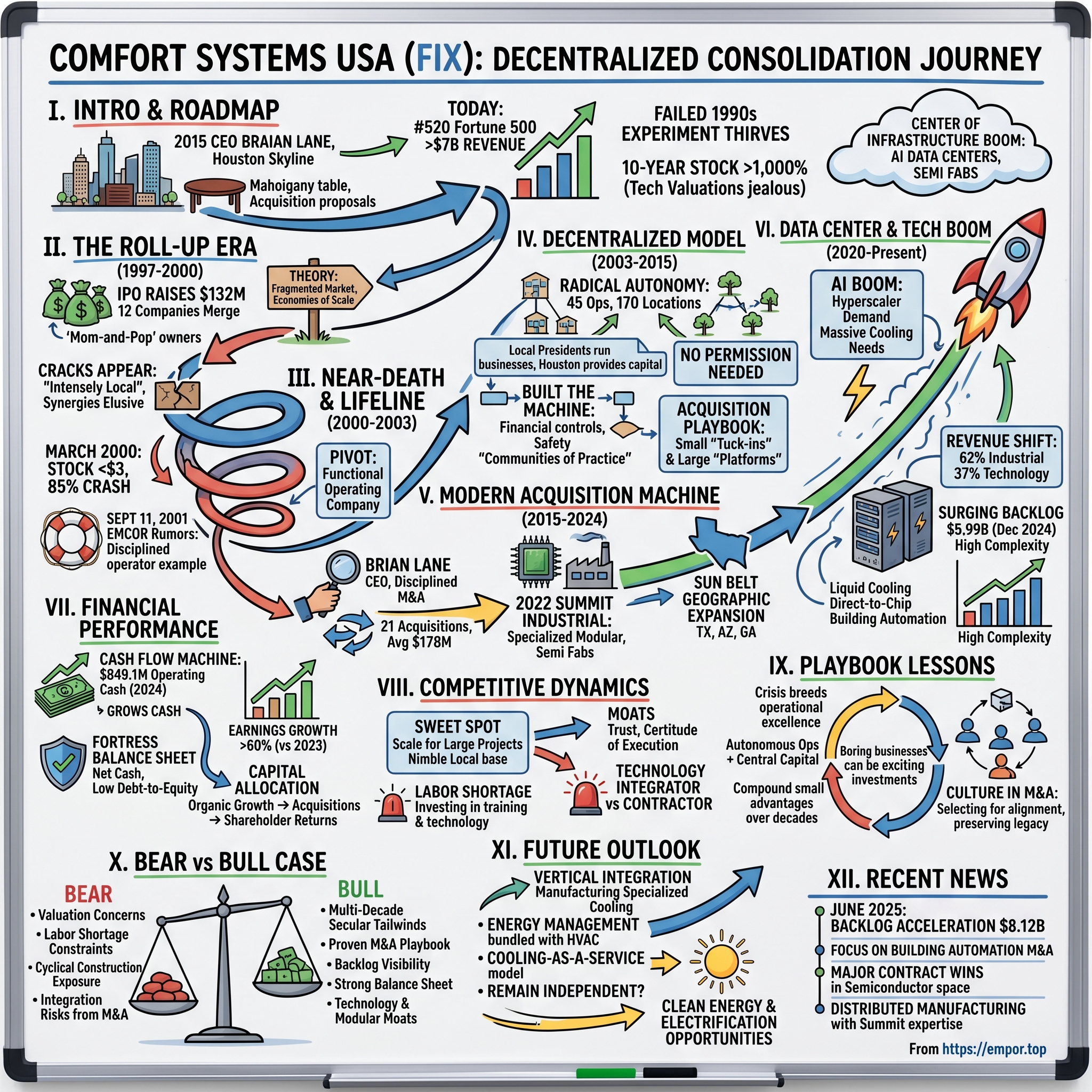

Comfort Systems USA: Building America's HVAC Empire Through Decentralized Consolidation

I. Introduction & Episode Roadmap

Picture this: It's 2015, and you're sitting in a conference room overlooking Houston's sprawling skyline. The air conditioning hums quietly—so quietly you barely notice it. That's the thing about HVAC systems: when they work perfectly, they're invisible. But Brian Lane, CEO of Comfort Systems USA, knows that invisible infrastructure is often the most valuable. He's staring at acquisition proposals scattered across the mahogany table, each representing another family-owned HVAC business ready to join what would become one of the most unlikely success stories in American industrial consolidation.

Fast forward to today, and Comfort Systems USA sits at #520 on the Fortune 500, with revenues exceeding $7 billion for the twelve months ended December 31, 2024. Not bad for a company that nearly died in the consolidation crash of 2000, when Wall Street's love affair with roll-ups turned into a massacre. While flashier tech companies grab headlines, this "boring" HVAC installer has quietly delivered returns that would make Silicon Valley jealous—its stock up over 1,000% in the past decade.

But here's what makes this story fascinating: Comfort Systems USA shouldn't exist. It was born during the late-1990s roll-up mania, a period when investment bankers convinced everyone that you could take fragmented, local service businesses, smash them together, and create instant value through "synergies." Most of these experiments ended in tears. Names like U.S. Office Products, Metals USA, and dozens of others became cautionary tales taught in business schools. Yet somehow, Comfort Systems not only survived—it thrived.

The company's journey from near-death to dominance reveals profound lessons about decentralized management, patient capital allocation, and the power of betting on unsexy infrastructure at exactly the right moment. Today, as data centers proliferate across America to feed our AI-hungry future, and as semiconductor fabs rise in Arizona deserts thanks to the CHIPS Act, Comfort Systems finds itself at the center of the most important infrastructure buildout since the interstate highway system.

This is the story of how a failed 1990s financial engineering experiment transformed into a decentralized operating machine, why boring businesses often make the best investments, and what happens when old-economy trades meet new-economy demand. It's about family businesses selling to public companies, local relationships trumping national scale, and why the companies that keep our buildings at 72 degrees might be more important to the digital revolution than the chip designers themselves.

We'll explore how Comfort Systems built a playbook for serial acquisition that actually works, why its decentralized model succeeds where command-and-control fails, and what the explosion in data center construction means for a company that most investors still categorize as "just another construction stock." Along the way, we'll uncover management decisions that saved the company, acquisitions that transformed it, and the strategic pivots that positioned it perfectly for the AI infrastructure boom.

II. The Roll-Up Era: Founding & Initial Consolidation (1997–2000)

June 1997. The Nasdaq is soaring, Alan Greenspan's "irrational exuberance" warning is being gleefully ignored, and investment bankers are peddling a seductive new narrative: industry consolidation through public market roll-ups. The pitch was elegant in its simplicity. Take a fragmented industry dominated by mom-and-pop operators, use public market currency to buy them up, achieve economies of scale, and watch the multiple expansion magic happen. Fred Ferreira, a veteran of the HVAC industry, was about to become the face of this experiment in the mechanical services sector.

The formation of Comfort Systems USA happened with remarkable speed. Twelve companies across the Sun Belt—from Texas to Florida to the Carolinas—simultaneously merged into a new entity that immediately went public. These weren't distressed assets or turnaround situations. They were successful, profitable HVAC contractors, many run by second or third-generation owners who saw an opportunity to cash out while still running their businesses. The IPO raised $132 million, valuing the company at roughly $400 million. Wall Street loved the story.

The original thesis seemed bulletproof. The U.S. HVAC services market was approaching $100 billion annually, yet the largest player had less than 1% market share. The top 50 companies combined controlled maybe 10%. This was an industry begging for consolidation, or so the bankers argued. Comfort Systems would create a national platform, leverage purchasing power, share best practices, and cross-sell services to national accounts. The playbook had worked in waste management with Waste Management Inc., in funeral homes with Service Corporation International. Why not HVAC?

But almost immediately, cracks appeared in the foundation. The company discovered that HVAC services aren't like collecting garbage or managing funeral homes—they're intensely local, relationship-driven businesses where the owner's last name on the truck matters more than national scale. Several bumps in the road emerged: integration proved harder than expected, some acquired companies saw key employees leave, and the promised synergies remained elusive. The stock, which had peaked near $20 in early 1998, began a slow, grinding descent.

By 1999, the consolidation fever was breaking. The market was littered with failed roll-ups—companies that had spent hundreds of millions acquiring businesses only to discover they'd created unwieldy, unprofitable conglomerates. Comfort Systems found itself lumped in with these failures, its stock price reflecting Wall Street's growing skepticism about the entire consolidation thesis. Management faced a choice: double down on the roll-up strategy or fundamentally reimagine what the company could become.

The lessons from this period would prove invaluable. First, financial engineering without operational excellence creates no lasting value. Second, in service businesses, culture and relationships matter more than spreadsheet synergies. Third, and most importantly, successful consolidation requires patience—something Wall Street rarely provides. As the dot-com bubble reached its frenzied peak in early 2000, Comfort Systems was about to face its darkest hour, one that would either destroy it or forge it into something entirely different.

III. Near-Death Experience & The EMCOR Lifeline (2000–2003)

The new millennium opened with Y2K fears proving overblown, but for Comfort Systems USA, the real catastrophe was just beginning. By March 2000, the company's stock had cratered to under $3, down 85% from its highs. The roll-up model wasn't just broken—it was toxic. Wall Street had moved from skepticism to outright hostility toward anything that smelled like a 1990s-style consolidation play. Credit markets tightened. Vendors grew nervous. Competitors circled like vultures.

Then came September 11, 2001. Beyond the human tragedy, the attacks triggered an economic shock that rippled through the construction industry. Commercial construction projects were cancelled or postponed. Companies slashed capital budgets. The mechanical services industry entered its worst downturn since the early 1990s recession. For a young, heavily leveraged roll-up trying to find its footing, this should have been the death blow.

Yet something remarkable happened in those conference rooms in Houston: management refused to panic. Bill Murdy, who had taken over as CEO, made a counterintuitive observation that would save the company. "Banks would have stuck with Comfort Systems USA because of its positive cash flow and the company asset structure," he would later reflect. "It would have been very rough, but we would still have worked hard at it and been successful. We had proven we could generate cash."

This wasn't wishful thinking. Despite the brutal market conditions that lasted from September 2001 through the end of 2003, Comfort Systems remained profitable and cash flow positive. How? The answer lay in a fundamental pivot that few noticed at the time. Instead of trying to be a "loose-knit consolidator"—essentially a holding company for independent HVAC businesses—management began transforming Comfort Systems into what Murdy called a "functioning operating company."

The transformation was surgical and deliberate. Underperforming acquisitions were shut down or sold. Back-office functions were selectively centralized—not to create the mythical synergies promised in the IPO prospectus, but to establish basic financial controls and reporting standards. Most crucially, the company stopped making acquisitions entirely, using the downturn to digest what it had already bought and figure out what actually worked.

The EMCOR rumors that swirled during this period—that the larger competitor might acquire Comfort Systems—served as both a potential lifeline and a wake-up call. EMCOR, which had gone through its own near-death experience in the early 1990s, had emerged as the disciplined operator that Comfort Systems aspired to become. While a deal never materialized, the possibility forced management to ask hard questions: What would make us valuable to a strategic buyer? What capabilities do we have that are worth preserving? What would we build if we were starting from scratch?

The answers shaped everything that followed. First, the strength of Comfort Systems USA was indeed in local operations. The presidents of individual operating units knew their markets best—many were the same entrepreneurs who had sold their companies to Comfort Systems in 1997. Second, the company's geographic footprint in the Sun Belt, initially seen as random, was actually prescient—these were the markets that would boom in the coming decades. Third, and most importantly, the decentralized model wasn't a bug to be fixed but a feature to be enhanced.

By late 2003, as the economy began recovering, Comfort Systems had emerged from its crucible transformed. It was leaner, more focused, and had developed something invaluable: institutional memory of what doesn't work. The company that entered 2004 bore little resemblance to the roll-up that had gone public seven years earlier. It was about to embark on one of the most successful transformations in American industrial history, but first, it had to build the machine that would power its second act.

IV. The Decentralized Operating Model: Building the Machine (2003–2015)

Inside the headquarters of one of Comfort Systems' Dallas operating companies, you'd never know you were in a billion-dollar public company. The walls are covered with photos of local high school football teams the company sponsors. The president, who's been running this operation for twenty years, knows every customer by name and most of their kids' names too. When he needs to hire a project manager, he doesn't call Houston for permission—he just does it. This radical autonomy, which would terrify most corporate executives, is precisely what makes Comfort Systems work.

"The strength of Comfort Systems USA is the local operations," management would repeatedly emphasize to skeptical investors. "The presidents operate in largely an autonomous fashion. They know their markets the best." This wasn't corporate speak—it was the hard-won wisdom from the near-death years. Many of these presidents were the same entrepreneurs who had sold their companies during the 1997 formation. Instead of forcing them into a corporate straightjacket, Comfort Systems had learned to let them run.

The model that emerged was elegantly simple yet fiendishly difficult to execute. Comfort Systems would maintain 45 operating companies across 170 locations, each functioning as a quasi-independent business. Local presidents had full P&L responsibility, controlled their own hiring and firing, and decided which projects to bid on. They kept their local brands, their local relationships, and most importantly, their entrepreneurial spirit. Houston's role? Provide capital, share best practices when requested, and otherwise stay out of the way.

But this wasn't anarchy. Behind the scenes, Comfort Systems was building sophisticated systems for financial reporting, safety protocols, and knowledge sharing. Monthly operating reviews became forums for presidents to learn from each other's successes and failures. A project that worked in Phoenix might be adapted for Atlanta. A new technology tested in Dallas could be rolled out in Charlotte. The company created what it called "communities of practice"—informal networks where specialists in areas like building automation or industrial refrigeration could share expertise across operating units.

The acquisition playbook that developed during this period was remarkably disciplined. Comfort Systems distinguished between "tuck-in" acquisitions—small companies that would be folded into existing operations—and "platform" acquisitions that would become new standalone operating units. Typical tuck-ins ranged from $5-20 million in revenue; platforms were $30-100 million. The sweet spot? Successful family businesses where the second generation wanted liquidity but the third generation wanted to keep running the company.

The three-part strategy that emerged—productivity improvements, service growth, and measured acquisition—became the company's mantra. Productivity meant doing more with less, using technology and training to improve project margins. Service growth meant building recurring revenue streams through maintenance contracts, moving beyond the feast-or-famine cycle of construction. Measured acquisition meant being disciplined about price, strategic about geography, and patient about integration.

Between 2003 and 2015, Comfort Systems quietly executed this playbook with remarkable consistency. Revenue grew from under $1 billion to over $1.5 billion. More importantly, margins expanded, cash flow improved, and the balance sheet strengthened. The company that had nearly died from indigestion was now one of the most disciplined acquirers in American industry. But the real test was coming. The acquisition machine was about to shift into high gear, and the stakes would be higher than ever.

V. The Modern Acquisition Machine (2015–2024)

Brian Lane's first major move as CEO in 2012 wasn't an acquisition—it was a decision not to acquire. A large mechanical contractor in California was available, the numbers looked good, and the bankers were pushing hard. But Lane, who had risen through the financial ranks at Comfort Systems and witnessed the dark days firsthand, said no. "Wrong market, wrong time, wrong culture fit," he told the board. That discipline would define the next chapter of Comfort Systems' story.

When the modern acquisition engine finally kicked into gear around 2015, it operated with Swiss watch precision. Over the next nine years, Comfort Systems would complete 21 acquisitions with an average acquisition amount of $178 million. But these weren't the scattershot deals of the 1990s. Each acquisition was strategically targeted, culturally vetted, and operationally integrated with a patience that would have been impossible in the roll-up era.

The year 2022 marked a watershed moment with three major acquisitions, but the crown jewel was Summit Industrial Construction. This wasn't just another HVAC contractor—Summit was a specialized modular construction expert with deep relationships in the semiconductor industry. "Summit is a trusted supplier to some of the world's largest advanced technology, power and industrial companies," Lane noted with barely contained enthusiasm. Summit brought what Comfort Systems had been searching for: "a stellar reputation as a modular technology leader in growing end markets, including multiple ongoing and large semiconductor projects."

The Summit deal revealed how sophisticated Comfort Systems' acquisition strategy had become. This wasn't about buying revenue or eliminating competition. It was about acquiring capabilities that would position the company for the next decade's infrastructure boom. Summit's expertise in clean room construction, process piping, and modular assembly perfectly complemented Comfort Systems' traditional strengths. More importantly, Summit's relationships with semiconductor companies opened doors that would have taken years to unlock organically.

The geographic expansion strategy was equally deliberate. While competitors chased projects in expensive coastal markets, Comfort Systems doubled down on the Sun Belt—Texas, Arizona, North Carolina, Georgia, Florida. These weren't just high-growth markets; they were the epicenters of the reshoring boom, where semiconductor fabs, battery plants, and data centers were being built at unprecedented scale. Every acquisition expanded Comfort Systems' footprint in these critical geographies.

But the real art was in the integration—or rather, the deliberate lack of integration. Summit kept its name, its management team, and its unique culture. The president who had built Summit's semiconductor relationships over decades continued running the business, now with access to Comfort Systems' balance sheet and bonding capacity. This allowed Summit to bid on larger projects while maintaining the agility that made it successful. It was the best of both worlds: entrepreneurial energy backed by corporate resources.

The proof was in the results. Comfort Systems' growth wasn't accidental—it was engineered through this methodical acquisition strategy. Revenue grew from $1.6 billion in 2015 to over $7 billion by 2024. But more impressively, margins expanded even as the company scaled. The acquisition machine wasn't just buying companies; it was building an empire, one carefully selected piece at a time. And perfect timing was about to make this empire exponentially more valuable.

VI. The Data Center & Technology Boom (2020–Present)

The email arrived at 2 AM on a Tuesday in March 2023. A hyperscaler—one of the massive cloud computing companies whose names you know but whose data centers you've never seen—needed Comfort Systems to accelerate deployment of a 100-megawatt facility in Phoenix. Not in six months. Now. The AI boom had arrived, and with it, an insatiable demand for the sophisticated cooling systems that keep humanity's digital infrastructure from melting down.

Comfort Systems' revenue mix tells the story of a dramatic transformation. Industrial and technology clients now account for 62% and 37% of total revenue, respectively—a complete reversal from a decade ago when commercial office buildings dominated the mix. This isn't your grandfather's HVAC company installing rooftop units on strip malls. This is complex, mission-critical infrastructure where a single degree of temperature variance can cost millions in damaged equipment.

Consider what actually happens inside a modern data center. Rows upon rows of servers generate heat equivalent to thousands of hair dryers running simultaneously. The power density—measured in kilowatts per square foot—has increased tenfold in the past decade. Traditional air cooling isn't enough anymore. These facilities require liquid cooling systems, elaborate hot-aisle/cold-aisle configurations, and increasingly, direct-to-chip cooling solutions that would have seemed like science fiction just five years ago.

The modular construction revolution that Summit brought to Comfort Systems proved perfectly timed. Instead of building cooling systems on-site, Comfort Systems pre-fabricates entire mechanical rooms in controlled factory environments, then ships them to data center sites for rapid deployment. This modular approach cuts construction time by 30-50% while improving quality and reducing costs. For hyperscalers racing to deploy AI infrastructure, this speed advantage is worth its weight in gold—or perhaps more accurately, in GPU compute cycles.

The numbers are staggering. Comfort Systems' backlog—the leading indicator of future revenue—surged to $5.99 billion as of December 2024, up 14% year-over-year. But here's the remarkable part: the same-store backlog, excluding recent acquisitions, grew by 8.5% to $5.60 billion. This isn't growth through acquisition; it's organic expansion driven by seemingly infinite demand for cooling the infrastructure of the digital age.

The integration of IoT-enabled HVAC systems and energy efficiency technology adds another layer to this story. Modern data centers don't just need cooling—they need intelligent cooling that can dynamically adjust to workload patterns, predict maintenance needs, and optimize energy usage. Comfort Systems isn't just installing equipment; it's deploying sophisticated building automation systems that use machine learning to minimize power usage effectiveness (PUE), the holy grail metric for data center operators.

First-mover advantages in complex technical projects create powerful moats. When Comfort Systems successfully delivers a 100-megawatt data center cooling system on time and on budget, it doesn't just earn a fee—it earns trust. That trust translates into sole-source contracts for expansion projects, preferred vendor status for new builds, and early involvement in design phases where the real value is created. The company that nearly died trying to be everything to everyone has found its calling serving the most demanding customers in the world.

VII. Financial Performance & Capital Allocation

The numbers tell a story that would make any CFO weep with joy. Revenue for the twelve months ending December 31, 2024 hit $7.027 billion, a 34.97% increase year-over-year. But revenue is vanity; profit is sanity, and cash flow is reality. Operating cash flow for the same period was $849.1 million—real money that can be deployed for growth, returned to shareholders, or held as dry powder for the next opportunity.

The per-share earnings growth is even more remarkable: 2024 earnings were over 60% higher than what management had called "spectacular results" in 2023. This isn't the kind of growth you expect from a company that installs air conditioners. It's the kind of growth you see when a business hits an inflection point where everything—market position, operational excellence, and industry tailwinds—aligns perfectly.

But perhaps the most impressive number is the one that doesn't get headlines: Comfort Systems maintains a net cash position of $241 million with a debt-to-equity ratio of just 0.16x. This fortress balance sheet isn't just conservative financial management—it's a strategic weapon. In an industry where bonding capacity and financial strength determine which projects you can bid on, Comfort Systems' balance sheet is like bringing a gun to a knife fight.

The capital allocation strategy reflects a mature management team that has learned from both success and failure. The framework is simple but disciplined: First, invest in organic growth through equipment, technology, and talent. Second, pursue acquisitions that meet strict return thresholds and strategic criteria. Third, return excess capital to shareholders. It's the third piece that signals confidence—the board approved a 50% dividend hike to $0.45 per share and executed $111 million in share repurchases year-to-date.

Why did the market undervalue FIX for so long? The answer lies in a common cognitive bias: investors pattern-match based on historical analogies. For years, Comfort Systems was lumped in with other construction companies, cyclical businesses that boom and bust with the economic cycle. The market missed the transformation into a technology infrastructure play with recurring service revenue and mission-critical customer relationships. Even today, with the stock trading at 24.5x P/E—a premium to peers like EMCOR (21.0x) and Limbach Holdings (18.0x)—there's an argument that the market still doesn't fully appreciate what Comfort Systems has become.

The cash flow generation capability deserves special attention. In the construction industry, cash flow is often negative as companies float working capital for projects. Comfort Systems has engineered its operations to be cash-generative even during rapid growth. This isn't financial engineering—it's operational excellence in project selection, payment terms negotiation, and working capital management. The company that nearly died from poor cash management has become a cash flow machine.

VIII. Competitive Dynamics & Industry Analysis

The HVAC services landscape looks deceptively simple from 30,000 feet: it's a fragmented, $150 billion annual market where the largest player has less than 5% share. But zoom in closer, and you'll find a complex ecosystem where local relationships, technical capabilities, and financial strength create surprising competitive dynamics. Comfort Systems operates in the sweet spot—large enough to handle billion-dollar projects, nimble enough to compete with local contractors.

The labor shortage crisis that keeps industry executives awake at night is real and getting worse. The average age of a skilled HVAC technician is 45 and rising. For every five technicians who retire, the industry attracts maybe two replacements. It's a demographic time bomb that threatens to constrain growth across the sector. Yet for Comfort Systems, this crisis is also an opportunity. The company's scale allows it to invest in training programs, apprenticeships, and technology that smaller competitors can't afford. When you can offer a clear career path from apprentice to project manager to operating company president, you attract talent that others can't.

Technology disruption in building systems isn't coming—it's here. Smart buildings that automatically adjust temperature based on occupancy patterns. IoT sensors that predict equipment failures before they happen. Building automation systems that can reduce energy consumption by 30% while improving comfort. These aren't futuristic concepts; they're table stakes for new construction. Comfort Systems' early investments in these capabilities, particularly through acquisitions of specialized building automation contractors, position it as a technology integrator, not just a mechanical contractor.

Climate change, ironically, is a growth driver for the HVAC industry. Rising temperatures increase cooling demand. Extreme weather events damage existing systems. New energy efficiency mandates require retrofitting older buildings. The Inflation Reduction Act's billions in efficiency incentives create a multi-year tailwind for retrofits and upgrades. For Comfort Systems, with its strong presence in the Sun Belt's cooling-dominated markets, climate change is an unfortunate but undeniable growth catalyst.

Private equity's interest in the HVAC space has intensified dramatically. PE firms see what Comfort Systems proved: you can successfully consolidate this industry if you do it right. But PE-backed competitors face challenges Comfort Systems has already solved. They need to build reporting systems, develop acquisition playbooks, and create cultures that balance autonomy with accountability. They're using leverage while Comfort Systems uses cash. They're racing against fund lifecycles while Comfort Systems plays the long game. It's not that PE-backed consolidators can't succeed—it's that Comfort Systems has a 25-year head start.

The competitive moat that matters most might be trust. When a hyperscaler needs someone to install cooling for a $1 billion data center, they're not shopping on price. They're looking for certainty of execution. Comfort Systems' track record, balance sheet, and bonding capacity make it one of the few companies that can credibly bid on these projects. This isn't a winner-take-all market, but it's definitely a winner-take-most dynamic at the high end where Comfort Systems increasingly operates.

IX. Playbook: Business & Investing Lessons

The first lesson from Comfort Systems' journey is counterintuitive: sometimes the best thing that can happen to a company is nearly dying. The near-death experience of 2000-2003 burned away the fantasy of easy synergies and forced management to discover what actually creates value. Without that crisis, Comfort Systems might have limped along as a mediocre roll-up, never forced to develop the operational excellence that defines it today.

The power of decentralized operations with centralized capital allocation is the second crucial insight. Most companies fail at one extreme or the other—either they're so decentralized they're really just holding companies with no operational leverage, or they're so centralized they crush the entrepreneurial spirit that made their acquisitions successful. Comfort Systems found the sweet spot: radical autonomy in operations coupled with disciplined oversight of capital deployment. Local presidents can decide which projects to bid on, but they can't make acquisitions without Houston's approval. They control their P&L, but they report financial results in standardized formats. It's controlled chaos that somehow works.

Building competitive advantages in commoditized industries is possible, but it requires patience and discipline. HVAC installation seems like the ultimate commodity—how different can one company be from another? But Comfort Systems proved that small advantages compound over time. Better training programs lead to better technicians. Better technicians lead to better project execution. Better execution leads to repeat customers. Repeat customers provide stable cash flow to invest in technology. Technology enables higher-margin projects. It's a flywheel that took decades to build but is now nearly impossible to replicate.

The transformation of boring businesses into exciting investments is a recurring pattern worth studying. Waste Management, Copart, Old Dominion Freight Line—these aren't sexy businesses, but they've been spectacular investments. They share common characteristics: fragmented industries, operational complexity that rewards scale, and mission-critical services that customers can't easily replace. Comfort Systems fits this pattern perfectly. The lesson for investors: look for boring businesses at inflection points where industry dynamics are shifting in their favor.

Culture in serial acquisitions might be the most underappreciated factor in successful consolidation. Comfort Systems doesn't try to change the culture of acquired companies—it selects for cultures that already align. The entrepreneurs who sell to Comfort Systems aren't looking for the highest price; they're looking for a home where their employees will be treated well and their legacy will be preserved. This selection bias creates a self-reinforcing culture where new acquisitions quickly feel at home. You can't spreadsheet culture, but it might be the most important factor in making serial acquisition work.

Cash flow truly is the ultimate scorecard. Revenue can be manipulated, earnings can be adjusted, but cash flow doesn't lie. Comfort Systems' focus on cash flow generation—even during rapid growth—is what separates it from companies that grow themselves into bankruptcy. This isn't just about financial metrics; it's about operational discipline. Every project selection, every payment term negotiation, every working capital decision is made with cash flow in mind. In industries with long project cycles and complex revenue recognition, this cash flow focus is the difference between success and failure.

X. Bear vs. Bull Case

The Bear Case:

Valuation concerns are legitimate and mounting. After a spectacular run that has seen the stock price increase over 1,000% in the past decade, Comfort Systems trades at premium multiples that assume continued exceptional execution. At 24.5x P/E, the market is pricing in perfection. Any stumble—a bad acquisition, a project gone wrong, a slowdown in data center construction—could trigger a violent repricing. The bears argue that the easy money has been made and that future returns will necessarily disappoint given the starting valuation.

Labor shortage constraints could throttle growth just when demand is highest. The demographic crisis in skilled trades isn't getting better, and Comfort Systems' growth ambitions require thousands of additional technicians. Training programs help but take years to bear fruit. Immigration restrictions limit one source of workers. Competition for skilled labor is intensifying, driving up wages and potentially crushing margins. The bears see a company that might win projects but can't staff them profitably.

Cyclical exposure to construction markets remains a fundamental risk. Yes, data centers and semiconductor fabs are booming now, but these markets have historically been volatile. The commercial construction market, still a meaningful part of Comfort Systems' business, is showing signs of stress as office vacancies remain elevated and interest rates bite. A recession would hit construction spending hard, and Comfort Systems, despite its strategic positioning, wouldn't be immune.

Integration risks from aggressive M&A are escalating. Twenty-one acquisitions since 2015 is a lot of digestion, even for a company with Comfort Systems' track record. Each acquisition brings integration challenges, cultural friction, and execution risk. The Summit acquisition was the largest in company history—if integration goes poorly, it could derail the entire growth story. The bears worry that management is getting overconfident, paying higher multiples, and taking on more integration risk just as the cycle peaks.

Competition from larger players and PE-backed consolidators is intensifying. EMCOR, with its larger scale and similar capabilities, is aggressively pursuing the same data center opportunities. Private equity firms are rolling up HVAC contractors at a furious pace, creating new scaled competitors with deep pockets and aggressive growth targets. The bears see Comfort Systems' first-mover advantages eroding as competition intensifies for both projects and acquisitions.

The Bull Case:

Secular tailwinds from data centers, reshoring, and infrastructure spending are multi-decade trends just getting started. The AI revolution requires massive data center buildout—estimates suggest $1 trillion in global data center investment over the next five years. The CHIPS Act and Inflation Reduction Act are driving the largest manufacturing construction boom since World War II. These aren't cyclical trends that will reverse in a recession; they're structural shifts that will drive demand for decades. Comfort Systems is perfectly positioned to capture this growth.

The proven acquisition and integration playbook de-risks future M&A. After 21 successful acquisitions, Comfort Systems has developed muscle memory for integration. They know which cultures fit, which capabilities to prioritize, and how to maintain entrepreneurial energy post-acquisition. This isn't their first rodeo—it's their twenty-first, and they've gotten better with each one. The bulls see continued consolidation opportunities with Comfort Systems as the natural acquirer of choice for family-owned contractors looking for succession solutions.

The backlog provides exceptional visibility and growth momentum. At $8.12 billion as of June 30, 2025—a 40.7% increase from $5.77 billion in Q2 2024—the backlog represents more than a year of revenue already contracted. This isn't speculative demand; these are signed contracts for specific projects. The mix is increasingly weighted toward large, multi-year projects that provide stable, predictable revenue streams. For bulls, the backlog alone justifies the premium valuation.

The strong balance sheet enabling continued consolidation is a strategic advantage that compounds over time. With $241 million in net cash and minimal debt, Comfort Systems can continue acquiring without diluting shareholders or taking on risky leverage. In a rising rate environment, this financial strength becomes even more valuable. The company can be opportunistic, swooping in when PE-backed competitors are constrained by their debt service obligations.

Technology and modular construction capabilities are creating real moats. This isn't just about installing equipment anymore—it's about designing, manufacturing, and deploying complex integrated systems. The modular construction expertise acquired through Summit gives Comfort Systems capabilities that traditional HVAC contractors can't match. Building automation and IoT integration require software expertise that takes years to develop. Bulls see these technical moats widening as projects become more complex and customers more demanding.

XI. Future Outlook & Strategic Options

The next frontier might not be geographic expansion internationally, as some suggest, but rather vertical integration into manufacturing. Comfort Systems already pre-fabricates modular cooling systems, but it still relies on equipment manufacturers for core components. Acquiring or developing manufacturing capabilities for specialized cooling equipment could capture more value chain margin while providing supply chain control during shortages. Management has hinted at this possibility, noting that the line between contractor and manufacturer is blurring in complex technical projects.

Technology investments in building automation, predictive maintenance, and AI-driven optimization represent the highest-return opportunities. Comfort Systems isn't going to become a software company, but embedding software capabilities into its service offering creates stickiness and recurring revenue streams. Imagine a future where Comfort Systems doesn't just install and maintain equipment but provides cooling-as-a-service, using AI to optimize energy usage and predict failures before they happen. The building systems industry is ripe for this kind of disruption, and Comfort Systems' scale and customer relationships position it to lead rather than follow.

Vertical integration opportunities extend beyond manufacturing into energy management. As data centers and industrial facilities become increasingly concerned about sustainability and energy costs, there's an opportunity to bundle HVAC services with energy procurement, on-site generation, and carbon management. Comfort Systems could evolve from a mechanical contractor into a comprehensive facility solutions provider, capturing a larger share of customer wallet while deepening relationships.

The ultimate end game—strategic buyer versus continued independence—is a question worth pondering. At a $10+ billion market cap, Comfort Systems is too large for most strategic buyers except the industrial conglomerates. But does it make sense as part of a larger platform? The successful decentralized model suggests independence might be the better path. The company has proven it can access capital markets, execute acquisitions, and generate returns as a standalone entity. Why sell now when the best growth years might be ahead?

What management should prioritize for the next decade is clear: maintain the culture that makes decentralization work, invest aggressively in technology and training to address labor challenges, and resist the temptation to over-centralize as the company scales. The formula that got Comfort Systems here—local autonomy, disciplined capital allocation, and patient integration—is the formula that will take it forward. The biggest risk isn't competition or market cycles; it's abandoning what works in pursuit of what sounds good in a boardroom.

The transition to clean energy and electrification presents both challenges and opportunities. Heat pumps replacing gas furnaces, electric vehicle charging infrastructure, and renewable energy integration all require expertise that overlaps with Comfort Systems' capabilities. The company that helps America cool its data centers could also help it transition to a cleaner energy future. Management's decisions in the next 24 months about where to invest and what capabilities to develop will determine whether Comfort Systems rides this wave or watches from the shore.

XII. Recent News & Developments

The June 2025 backlog announcement sent shockwaves through the analyst community—$8.12 billion represented not just growth but acceleration. The 40.7% year-over-year increase from Q2 2024's $5.77 billion suggested that demand for Comfort Systems' services was not just strong but potentially accelerating. The composition of this backlog—heavily weighted toward data center and semiconductor projects—provides unusual visibility for a construction services company.

Recent acquisition activity has focused on building automation and controls capabilities, suggesting management sees the convergence of mechanical and digital systems as a key growth vector. These aren't the large platform deals that grab headlines but strategic tuck-ins that add technical capabilities and customer relationships in high-growth verticals. Each small acquisition is a bet on where the industry is heading, and collectively, they paint a picture of a company preparing for a more digital, automated future.

Major contract wins in the semiconductor space validate the Summit acquisition thesis. Comfort Systems is now the go-to mechanical contractor for several major fab projects, relationships that could be worth billions in revenue over the next decade. These aren't just construction projects; they're long-term partnerships that include ongoing maintenance, upgrades, and expansion work. The recurring nature of these relationships transforms Comfort Systems from a project-based business into something more akin to an industrial services company.

The quiet expansion of modular construction capabilities across the platform shows management thinking several moves ahead. By spreading Summit's expertise to other operating companies, Comfort Systems is creating a distributed manufacturing network that can serve customers across its entire geographic footprint. This isn't just about efficiency—it's about speed to market in an environment where customers measure delays in millions of dollars per day.

The strategic focus on energy efficiency and sustainability, while not grabbing headlines, positions Comfort Systems for the next wave of regulatory and customer demands. As buildings face increasing pressure to reduce carbon footprints and energy costs, the company that can deliver both comfort and efficiency will win. Comfort Systems' investments in energy management capabilities and efficient system design are bets on where the market is heading, not where it's been.

The story of Comfort Systems USA is far from over. What started as a failed 1990s roll-up has transformed into one of America's most important infrastructure companies, keeping the digital economy cool while generating exceptional returns for patient shareholders. In an era of AI hype and cryptocurrency speculation, there's something refreshing about a company that creates value the old-fashioned way: by solving real problems for real customers with real expertise.

As data centers proliferate and America rebuilds its industrial base, Comfort Systems sits at the intersection of multiple secular growth trends. The company that almost died learning how to consolidate an industry is now reaping the rewards of that painful education. For investors seeking exposure to the AI infrastructure boom without the volatility of semiconductor stocks, for operators studying successful consolidation strategies, and for anyone interested in how boring businesses become great investments, Comfort Systems USA offers lessons worth learning.

The next chapter will be written by decisions made today—about technology, talent, and capital allocation. But if history is any guide, the company that survived the dot-com crash, thrived through the financial crisis, and positioned itself perfectly for the AI boom will continue to find ways to grow, evolve, and compound value. In the end, the most important infrastructure is often the most invisible—and the companies that build it, the most valuable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube