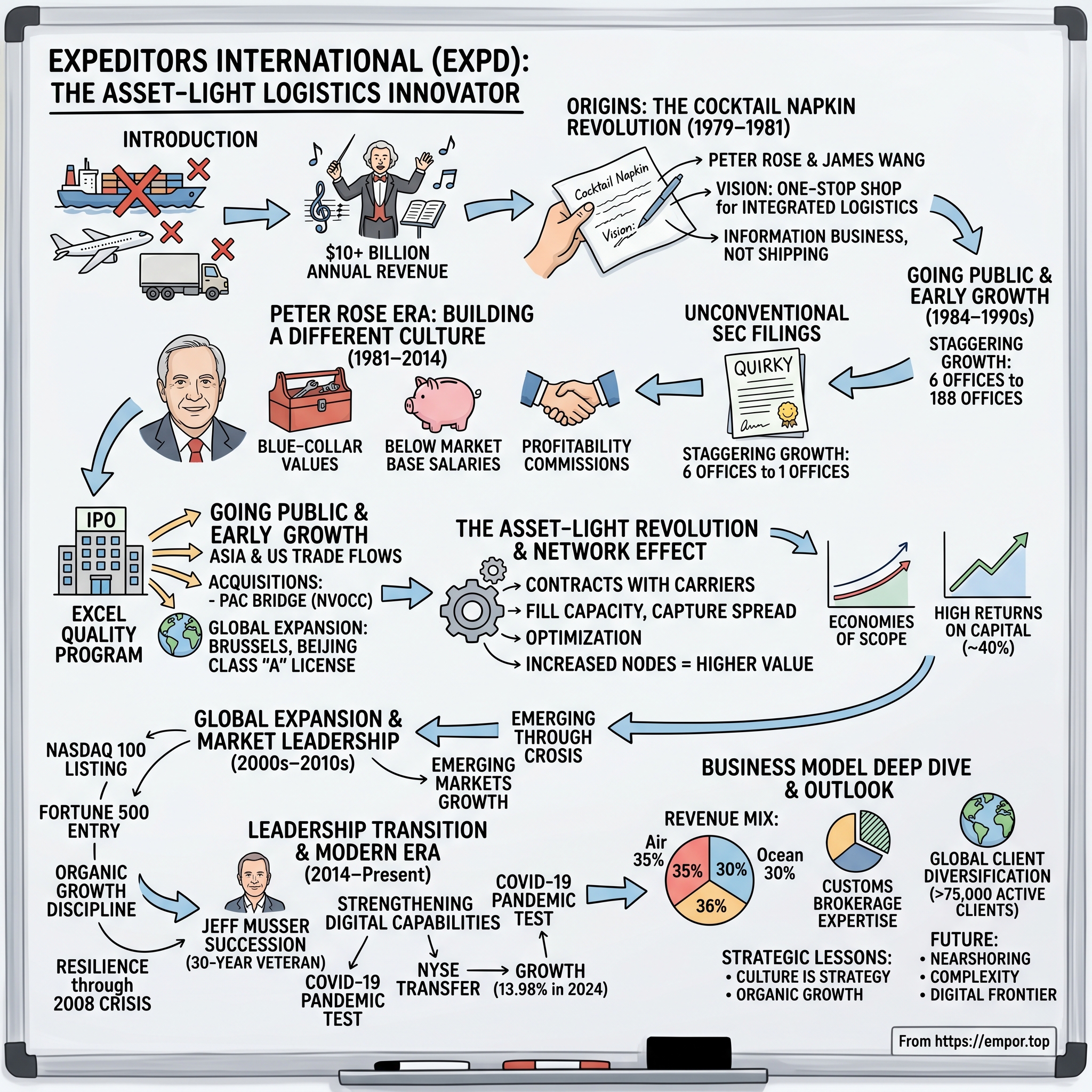

Expeditors International: The Asset-Light Logistics Innovator

I. Introduction & Episode Roadmap

Picture this: It's 2024, and somewhere in the Pacific Ocean, a massive container ship carries thousands of tons of cargo. Above, a Boeing 747 freighter slices through the night sky loaded with electronics. On highways across continents, trucks rumble toward distribution centers. None of these assets—not a single ship, plane, or truck—belongs to Expeditors International, yet the company orchestrates their movements like a maestro conducting a global symphony, generating over $10 billion in annual revenue.

This is the paradox at the heart of our story today. How does a company that owns virtually none of the physical infrastructure of global trade become one of the world's most powerful logistics companies? How did a Seattle startup sketched on a cocktail napkin in Hong Kong transform into a Fortune 500 giant that moves the goods powering the global economy?

Expeditors International (EXPD) represents something unique in the business world—a service company that built an empire not through owning assets, but through owning relationships, data, and most importantly, a culture so distinctive that Wall Street analysts have spent decades trying to decode it. With headquarters still in Bellevue, Washington, this logistics powerhouse has quietly compounded wealth for shareholders while maintaining an almost monastic devotion to its founding principles.

Today's journey takes us from that fateful bar meeting in Hong Kong to boardrooms across six continents. We'll explore how Expeditors pioneered the asset-light model before "asset-light" became a Silicon Valley buzzword, how it built network effects without writing a line of consumer-facing software, and why its unconventional approach to everything from compensation to SEC filings has created one of the most durable competitive moats in global logistics.

The themes we'll unpack aren't just about freight forwarding—they're about the power of culture in building a global business, the economics of networks, and why sometimes the best businesses are the ones that seem the most boring on the surface. As we'll discover, there's nothing boring about 40% returns on capital sustained over decades.

II. Origins: The Cocktail Napkin Revolution (1979–1981)

The summer humidity in Hong Kong can be oppressive, the kind that drives people into air-conditioned bars for relief. On one such evening in July 1981, on Lantau Island—before it became home to Hong Kong International Airport—two men sat nursing drinks and discussing the inefficiencies plaguing international shipping. Peter Rose and James Wang weren't just complaining; they were sketching solutions on a cocktail napkin that would reshape global logistics.

But let's rewind two years. In 1979, John Kaiser founded what would become Expeditors as a small ocean freight forwarding operation in Seattle. The original company was modest—a single office handling documentation and logistics for companies shipping goods across the Pacific. Kaiser saw opportunity in the growing trade between Asia and the United States, but the company remained a traditional forwarder, one of hundreds competing on price and relationships.

The transformation began with that cocktail napkin. Rose, who had literally grown up in the transportation business—he fondly recalled wearing an adult-sized trucker's cap at age five while helping his father deliver packages—brought operational expertise. Wang brought deep connections in Asia and an understanding of how fragmented the freight forwarding industry had become. Together, they envisioned something radical: a "one-stop shop" for international freight forwarding and customs brokerage services.

This wasn't just about convenience. In 1981, moving goods internationally meant dealing with multiple vendors—one for ocean freight, another for air, a customs broker at each port, trucking companies for the last mile. Each handoff created delays, lost information, and finger-pointing when things went wrong. Rose and Wang's insight was that by integrating these services under one roof, they could capture value at each step while providing accountability that clients desperately wanted.

The duo quickly assembled a team of five additional founders, each bringing complementary skills: Kevin Walsh with his sales expertise, Hank Wong's operational excellence, George Ho's Asian market knowledge, Robert Chiarito's customs expertise, and Glenn Alger's financial acumen. Together, these seven individuals didn't just create a company—they crafted a philosophy that would guide Expeditors for decades.

The timing was perfect. The early 1980s marked an inflection point in global trade. Manufacturing was shifting to Asia, just-in-time inventory systems were gaining adoption, and companies needed partners who could navigate the complexity of international logistics. While established players were constrained by legacy systems and traditional thinking, Expeditors could build from scratch.

Within months, they had established offices in strategic locations: San Francisco to capture West Coast trade, Chicago for the Midwest manufacturing belt, and crucially, Hong Kong, Taipei, and Singapore to anchor their Asian operations. Each office wasn't just a sales outpost but a node in an emerging network that would become Expeditors' greatest asset.

The founding vision was deceptively simple yet revolutionary: treat freight forwarding not as a commodity service but as a consultative partnership. Don't own the assets—own the expertise, the relationships, and most importantly, the data about how goods actually move through the global supply chain. As Rose would later say, "We're not in the shipping business; we're in the information business."

III. Peter Rose Era: Building a Different Kind of Company (1981–2014)

Peter Rose didn't look like a typical Fortune 500 CEO. He avoided the spotlight, rarely gave interviews, and when he did speak publicly, he was more likely to quote philosophy than quarterly earnings. Yet from 1981 to 2014, he built one of the most successful logistics companies in history through a management philosophy that violated nearly every rule taught in business schools.

Rose's background shaped his worldview. That five-year-old boy in the oversized trucker's cap learned early that transportation wasn't glamorous—it was about reliability, relationships, and relentless execution. When he assumed the title of President and CEO of the newly restructured Expeditors, he brought those blue-collar values to white-collar freight forwarding.

The compensation system Rose implemented would make modern HR departments faint. Base salaries were intentionally below market—sometimes 30-40% below competitors. But here's where it got interesting: employees could earn multiples of their base through commissions tied directly to the profitability of their accounts. Branch managers' bonuses weren't linked to revenue but to net revenue growth and operating profit. The message was clear: think like an owner, get paid like one.

This wasn't just about incentives; it was about selection. The system naturally filtered for entrepreneurial types who bet on themselves. It repelled those seeking comfortable corporate jobs and attracted hunters willing to eat what they killed. One early employee recalled Rose telling him, "If you want a high base salary, go work for our competitors. If you want to get rich, stay here and build something. "The culture Rose built showed up most visibly in the company's SEC filings. They became known in the financial services community for their unconventional and entertaining SEC filings, rumored to be written by Peter Rose himself. In an industry where regulatory documents are typically written by lawyers to say as little as possible, Expeditors' 8-K forms became must-reads on Wall Street. In filings that answered questions from investors, the company would drop a wide range of names and take stabs at competitors, large banks and their teams of smart MBAs.

One memorable example involved a question about currency hedging. The response started by talking about Ben Stein's book and then said about currency trading: "Just because we have the wherewithal to speculate, doesn't mean we have to make some banker rich". Another filing discussing competitors' acquisition strategies noted how these deals are "feted as 'brilliant' and 'accretive'" only to later be "divested, de-emphasized or closed outright" amid layoffs and writeoffs.

The results spoke louder than any SEC filing. During their first year as a public company in 1984, Expeditors reported more than $50 million in gross revenues and $2.1 million in net earnings. By the time Rose announced his retirement in 2014, he had transformed that company into a $6 billion-a-year global powerhouse. Since going public in 1984, Expeditors generated double-digit annualized growth in earnings before interest and taxes in all but four years.

The numbers were staggering. Under Rose's leadership, the company grew from six offices with 20 people and $300,000 in capital to 188 offices across six continents with more than 13,000 employees. From March 1990 through October 2013, Expeditors stock rose 5,591 percent. This wasn't achieved through financial engineering or aggressive acquisitions—it was pure operational excellence driven by a culture that treated every employee like an owner.

Rose's management philosophy extended to his personal conduct. Peter Rose actually paid to park his car in Expeditors' headquarters building—which was 100% owned by the company—just as he paid his own utility bills and bought his own tickets to Seattle Thunderbirds hockey games. As the company noted in one filing, "long before corporate governance became trendy, we just assumed that personal expenses should be paid for by personal funds".

The culture wasn't just about frugality; it was about alignment. Every decision, from compensation to expansion, was filtered through a simple question: What would an owner do? This created a company where bureaucracy couldn't take root, where every office operated like a startup, and where success was measured not by revenue but by profitability. As we'll see, this foundation would prove remarkably durable through multiple economic cycles and industry disruptions.

IV. Going Public & Early Growth (1984–1990s)

The NASDAQ trading floor in 1984 was a different world—no high-frequency trading, no algorithmic orders, just human market makers shouting prices across a crowded room. When Expeditors went public that year under the ticker EXPD, few noticed. The offering raised modest capital, but more importantly, it created a currency for growth and a scorecard for performance that would drive the company's unique culture.

The IPO timing was fortuitous. The mid-1980s marked the beginning of a fundamental shift in global manufacturing. Japan's economic miracle was in full swing, South Korea and Taiwan were emerging as manufacturing powerhouses, and American companies were beginning to source components and finished goods from Asia at unprecedented scales. Expeditors sat at the intersection of these trade flows, perfectly positioned to capture value.

One of the company's first major strategic moves post-IPO was the acquisition of Pac Bridge, a significant non-vessel ocean common carrier (NVOCC). This wasn't just about adding capacity—it was about gaining critical mass in ocean freight that would allow Expeditors to negotiate better rates with actual vessel operators. The NVOCC license meant Expeditors could consolidate smaller shipments from multiple customers into full container loads, capturing margins on both ends of the transaction.

The geographic expansion strategy during this period reveals the company's sophisticated understanding of global trade patterns. The Brussels office, opened as Expeditors' first location in continental Europe, wasn't chosen randomly. Brussels was emerging as the bureaucratic heart of the European Union, and being there meant understanding regulatory changes before competitors. It also served as a gateway to the massive European consumer market that was increasingly hungry for Asian-manufactured goods.

But the real coup came when Beijing granted Expeditors a rare Class "A" license to operate in China. In the late 1980s, China was still largely closed to foreign businesses. The Class "A" license was like winning a golden ticket—it allowed Expeditors to operate as a freight forwarder within China, not just at its borders. While competitors were still trying to figure out how to work with Chinese partners, Expeditors was building direct relationships with manufacturers in Shenzhen, Guangzhou, and Shanghai.

The company formalized its approach to quality with the EXCEL program—"100% customer satisfaction 100% of the time." This wasn't corporate platitude; it was backed by real metrics and compensation. Every shipment was tracked, every delay analyzed, every customer complaint dissected. Branch managers' bonuses depended not just on profitability but on customer satisfaction scores. The message was clear: growth without quality was worthless.

By the early 1990s, Expeditors had become one of the largest U.S.-based forwarders of air freight from the Far East. This wasn't achieved through owning aircraft or exclusive contracts with airlines. Instead, Expeditors built something more valuable: expertise in consolidation and route optimization that allowed it to offer better prices and reliability than competitors who owned their own planes.

The 1990s brought new challenges and opportunities. The fall of the Berlin Wall opened Eastern European markets. The North American Free Trade Agreement (NAFTA) created new trade corridors. The Asian Financial Crisis of 1997 tested the company's risk management. Through each event, Expeditors' asset-light model proved its worth—when trade flows shifted, the company could pivot without being weighed down by stranded assets. One anecdote captures the era perfectly: during the 1991 Gulf War, when many logistics companies pulled back from the Middle East, Expeditors opened an office in Kuwait. While competitors saw risk, Rose saw opportunity. The company placed representatives in Istanbul, Cairo, Athens, and Dubai, betting that post-war reconstruction would drive massive logistics demand. They were right, and being first gave them relationships that competitors couldn't replicate.

V. The Asset-Light Revolution & Network Effect

To understand Expeditors' business model, imagine you're a manufacturer in Shenzhen with a container of electronics destined for Best Buy's distribution center in Minnesota. You could try to coordinate with an ocean carrier, customs brokers on both sides of the Pacific, a trucking company, and hope everything connects smoothly. Or you could make one call to Expeditors and let them handle everything. That's the power of the asset-light model—not owning the ships, planes, or trucks, but owning the orchestration.

Here's how the model actually works: Expeditors contracts with airlines and ocean carriers for cargo space at wholesale rates, negotiating volume discounts that individual shippers could never achieve. They then fill that capacity with customers' freight, capturing the spread between wholesale and retail rates. But the real magic isn't in the buying and selling of space—it's in the optimization.

Consider a typical transaction: Expeditors might consolidate shipments from ten different manufacturers in Guangzhou, all heading to various U.S. destinations. By combining these into a single container, they reduce costs for everyone while earning fees at multiple points—consolidation in China, ocean freight, deconsolidation in Los Angeles, customs clearance, and final mile delivery. Each step adds margin without adding assets.

The flexibility of this approach became evident during market disruptions. When ocean rates spiked during the 2021 supply chain crisis, asset-heavy competitors with long-term vessel leases were stuck with fixed costs. Expeditors could dynamically shift between carriers, modes, and routes to find the best solution for each shipment. This means Expeditors can be highly flexible in their approach to supply chain management, and very effective at finding the best route and pricing options.

The network effect in Expeditors' business is subtle but powerful. Every new office location increases the value of every other location. A customer shipping from Vietnam to Germany benefits from Expeditors' presence in Singapore (for transshipment), Dubai (for documentation), Rotterdam (for European distribution), and Frankfurt (for final delivery). The more nodes in the network, the more routing options available, and the better the service becomes.

This network density creates what economists call "economies of scope"—the ability to serve diverse customer needs efficiently. A pharmaceutical company shipping temperature-controlled vaccines and a fashion retailer moving seasonal inventory have completely different requirements, but Expeditors can serve both using the same network infrastructure, spreading fixed costs across a broader revenue base.

Technology investments amplified these network effects. While never a technology company per se, Expeditors understood early that information was as valuable as physical goods movement. Their proprietary systems tracked not just where shipments were, but why they were there—capturing data on delays, customs issues, and carrier performance that could be analyzed to optimize future shipments.

The returns on capital tell the story best. Over the past decade, Expeditors has generated returns on capital near 40%—extraordinary for any business, but particularly impressive for a logistics company. These returns weren't achieved through financial leverage (the company operated with minimal debt) but through operational leverage—the ability to grow revenue faster than costs by utilizing the same network more intensively.

The moat around this business model proved remarkably durable. Competitors could replicate individual pieces—anyone could lease cargo space or hire customs brokers. But replicating the entire network, with its density of locations, depth of relationships, and decades of operational data, was nearly impossible. As one competitor executive admitted off the record, "We could copy what Expeditors does, but we can't copy what Expeditors is."

VI. Global Expansion & Market Leadership (2000s–2010s)

The new millennium opened with Expeditors joining an exclusive club. In 2002, the company was named to the NASDAQ 100, recognition that a logistics company could stand alongside the technology giants that dominated the index. This wasn't just symbolic—it reflected how integral global supply chains had become to the modern economy, and how central Expeditors was to those supply chains.

Expeditors enters Fortune 500 list for the first time with $4.6 billion in revenue. Fortune also names Expeditors the Number One Most Admired Company in our industry. The Fortune 500 entry marked a transformation from scrappy startup to establishment player, but the company's approach remained decidedly unconventional. While competitors pursued growth through mega-acquisitions—DHL bought Airborne Express, FedEx acquired multiple ground carriers—Expeditors stuck to organic growth.

This emphasis on organic expansion wasn't ideological stubbornness; it was strategic discipline. Every new Expeditors office was started by experienced employees who understood the culture and systems. They didn't inherit legacy problems or have to integrate incompatible technologies. Each office was built from the ground up to fit seamlessly into the global network, maintaining the cohesive infrastructure that was Expeditors' true competitive advantage.

The 2008 financial crisis tested every assumption about global trade. Lehman Brothers collapsed in September; by October, global shipping volumes were in freefall. Container ships sat idle in ports. Airlines parked planes in the desert. For asset-heavy logistics companies, this was catastrophic—they still had to pay for ships and planes that weren't generating revenue.

Expeditors' response revealed the resilience of its model. Without fixed asset costs to cover, the company could scale down operations in line with demand. More importantly, while competitors were laying off thousands, Expeditors protected its workforce. The company understood that logistics expertise—knowing how to route a shipment through Vietnam during monsoon season or which customs officer to call in Rotterdam—resided in people's heads, not in spreadsheets. Keeping that expertise intact would pay dividends when recovery came.

Recovery came faster than expected, driven by unprecedented stimulus and the beginnings of the e-commerce boom. By 2010, Expeditors was positioning itself for a new era of trade. The company expanded aggressively in emerging markets—not just China, but Vietnam, India, and Eastern Europe. Each new location was chosen based on trade flow data and customer demand, not speculative growth projections.

The first quarter of 2015 is the most profitable in the history of the company. This milestone reflected not just recovery from the financial crisis but a fundamental strengthening of Expeditors' position. The company had emerged from the downturn with greater market share, stronger customer relationships, and a reputation for reliability when others had faltered.

By the mid-2010s, Expeditors operated across six continents with over 340 locations in more than 100 countries. But unlike the colonial-style expansion of some competitors, each Expeditors office was deeply embedded in its local market. The Singapore office understood Southeast Asian trade patterns. The São Paulo office navigated Brazil's Byzantine import regulations. The Dubai office knew how to move goods through the Middle East's complex political landscape. This local expertise, connected through a global platform, created capabilities that no purely local or purely global competitor could match.

VII. Leadership Transition & Modern Era (2014–Present)

Change at the top of any founder-led company creates uncertainty, but Peter Rose's retirement announcement in March 2014 was handled with characteristic Expeditors precision. Rose announced his retirement in March 2014 as CEO, with his retirement as Chairman effective May 2015. The succession plan had been years in the making, ensuring continuity of culture and strategy.

Jeff Musser, the new CEO, wasn't an outside turnaround artist or a McKinsey consultant with a mandate for change. He was a 30-year Expeditors veteran who had risen through the ranks, running offices in Asia and understanding the business from the ground up. His appointment sent a clear message: Expeditors would evolve, not revolutionize.

The Musser era began with subtle but important shifts. While maintaining the core asset-light model and performance-based culture, he recognized that technology was becoming central to logistics competitiveness. Expeditors had always been strong operationally but needed to strengthen its digital capabilities to serve customers who increasingly expected real-time visibility and predictive analytics.

The COVID-19 pandemic became the defining test of Musser's leadership. When the virus emerged in Wuhan—a major logistics hub—Expeditors' local team was among the first to alert global headquarters about potential supply chain disruptions. By February 2020, before most Western companies understood the magnitude of what was coming, Expeditors was helping clients reroute supply chains and build inventory buffers.

The pandemic created unprecedented volatility in logistics markets. Ocean freight rates increased tenfold. Air cargo capacity evaporated as passenger flights (which carry significant cargo in their bellies) were grounded. Ports backed up with weeks-long delays. For Expeditors, this chaos was both challenge and opportunity. The company's ability to find alternative routes, secure scarce capacity, and navigate constantly changing regulations became invaluable to clients whose supply chains were breaking down.

In November 2023, Expeditors transferred the listing of its common stock to the New York Stock Exchange NYSE, keeping the same symbol "EXPD". The move from NASDAQ to NYSE after nearly 40 years was more than symbolic—it reflected Expeditors' evolution from growth stock to blue-chip dividend payer, attracting a different class of institutional investors.

In 2024 the company made a revenue of $10.60 Billion USD an increase over the revenue in the year 2023 that were of $9.30 Billion USD. This 13.98% growth demonstrated that even as a mature company, Expeditors could capture value in expanding global trade. The growth came not from market share gains but from solving increasingly complex logistics challenges—managing semiconductor supply chains, handling e-commerce returns, navigating new trade regulations.

Looking at today's Expeditors, you see a company that has successfully navigated the transition from founder-led startup to professionally managed corporation without losing its entrepreneurial edge. The district offices still operate with significant autonomy. Managers still eat what they kill through performance-based compensation. The culture that Rose and his co-founders embedded in the company's DNA remains intact, even as the company adapts to new realities of digital commerce and changing trade patterns.

VIII. Business Model Deep Dive

To truly understand Expeditors, you need to examine how money flows through the business. The revenue mix tells a story of diversification and balance: roughly 35% from airfreight, 30% from ocean freight, and 36% from customs brokerage and other services. This isn't accidental—it's a portfolio approach that provides stability when individual segments face pressure.

The airfreight business is Expeditors' highest-margin segment but also its most volatile. When companies need something moved quickly—a production line stopped for want of a part, a fashion retailer catching a trend—they pay premium rates for air cargo. Expeditors captures value by consolidating these urgent shipments, negotiating volume rates with airlines, and managing the complex logistics of international air cargo, including dangerous goods handling, customs pre-clearance, and last-mile delivery.

Ocean freight operates on thinner margins but massive volumes. A single container ship can carry 20,000 TEUs (twenty-foot equivalent units). Expeditors doesn't need to own the ship to profit from those containers—they need to fill them efficiently. The company's NVOCC operations allow it to buy space wholesale and sell retail, but the real value creation comes from services layered on top: cargo insurance, supply chain financing, vendor management, and increasingly, carbon footprint tracking.

The "customs brokerage and other services" segment is perhaps the most underappreciated. Customs clearance isn't just paperwork—it's expertise in thousands of product classifications, constantly changing regulations, and relationships with customs officials worldwide. When a shipment gets held at customs, every day of delay costs money. Expeditors' ability to clear shipments quickly and compliantly creates value that clients gladly pay for.

The company serves over 75,000 active clients across virtually every industry. This diversification provides resilience—when automotive manufacturing slows, e-commerce might accelerate. When oil prices spike and energy sector logistics boom, consumer goods might soften. No single client represents more than 3% of revenue, insulating Expeditors from customer concentration risk.

The compensation philosophy remains the secret sauce. In an industry where logistics coordinators are often treated as interchangeable cogs, Expeditors treats them as entrepreneurs. A coordinator who identifies a new customer opportunity, wins the business, and manages it profitably can earn multiples of their base salary. This creates a workforce that thinks like owners, not employees.

Technology at Expeditors isn't about press releases or buzzwords—it's about operational excellence. The company's systems provide real-time visibility into shipments, but more importantly, they capture and analyze patterns. Which routes consistently face delays during monsoon season? Which carriers have the best on-time performance for pharmaceuticals requiring cold chain management? This institutional knowledge, encoded in systems and processes, becomes more valuable over time.

The capital efficiency of this model is striking. Expeditors generates over $10 billion in revenue with less than $3 billion in total assets. Compare this to asset-heavy competitors who might have $20 billion in assets to generate similar revenue. This capital efficiency translates directly to returns—without planes to buy or ships to maintain, most of Expeditors' earnings can be returned to shareholders or reinvested in high-return opportunities.

IX. Playbook: Strategic & Investing Lessons

The Expeditors story offers a masterclass in building a durable competitive advantage in a seemingly commoditized industry. The first lesson: culture is strategy. While competitors focused on assets and acquisitions, Expeditors focused on aligning incentives. Every employee, from the Seattle headquarters to a small office in Bangladesh, operates under the same principle: profitability matters more than revenue.

The power of this cultural alignment compounds over time. compound annual growth rates in net revenue—revenue after the costs of purchased transportation—and earnings per share of 10 percent and 12 percent, respectively, over the past decade. These aren't the spectacular returns of a software company, but they're remarkably consistent for a logistics business exposed to global economic cycles.

Capital allocation at Expeditors follows a simple philosophy: no debt, high returns, shareholder-friendly. The company has operated without significant debt throughout its history, achieving high returns on equity through operational excellence rather than financial engineering. This conservative balance sheet proved invaluable during crises—when credit markets froze in 2008 or when COVID disrupted cash flows, Expeditors had the financial flexibility to support customers and capture market share from distressed competitors.

The organic growth strategy deserves special attention. While the logistics industry consolidated through mega-mergers, Expeditors grew office by office, customer by customer. This approach took longer but created a more cohesive organization. Every Expeditors office runs the same systems, follows the same processes, and shares the same culture. There are no legacy technology platforms to integrate or conflicting corporate cultures to reconcile.

The network effect in Expeditors' business model creates a virtuous cycle. More locations mean better service, which attracts more customers, which justifies more locations. But unlike digital network effects that can be disrupted by new technology, Expeditors' physical network—with its relationships, local knowledge, and operational expertise—has proven remarkably durable.

For investors, Expeditors offers a case study in the power of boring businesses. No one gets excited about freight forwarding at cocktail parties. The company doesn't make products that consumers love or technologies that change the world. It simply moves goods from point A to point B, taking a small margin for solving a complex problem. But those small margins, earned on massive volumes with minimal capital investment, compound into serious wealth creation.

The sustainability of Expeditors' model comes from its adaptability. When trade patterns shift—manufacturing moving from China to Vietnam, for instance—Expeditors shifts with them. When new regulations emerge—environmental reporting, security requirements, trade restrictions—Expeditors turns compliance into a service offering. The company doesn't predict the future; it builds capabilities to serve whatever future emerges.

X. Analysis & Future Outlook

Expeditors operates in a fragmented industry where the top 10 global freight forwarders control less than 50% of the market. This fragmentation creates both opportunity and challenge. The opportunity lies in continued consolidation and market share gains. The challenge comes from new entrants, particularly digital freight forwarders promising to "Uber-ize" logistics.

Against traditional competitors—Kuehne + Nagel, DHL Global Forwarding, DB Schenker—Expeditors holds its own through superior returns and operational efficiency. These competitors often carry legacy infrastructure, union obligations, and in some cases, government ownership that constrains decision-making. Expeditors' entrepreneurial culture and variable cost structure provide advantages in agility and profitability.

The digital disruption threat is real but often overstated. Companies like Flexport and Freightos have raised billions in venture capital to build digital-first freight forwarders. They offer slick interfaces, instant quotes, and promise to eliminate traditional brokers. But moving a container from Shanghai to Chicago involves more than software—it requires relationships with carriers, expertise in customs clearance, and the ability to solve problems when (not if) something goes wrong.

Expeditors' response to digital disruption has been measured. Rather than panic-investing in consumer-facing apps, the company has focused on digitizing core operations. Their carrier allocation platform, developed with Walmart, shows how Expeditors can leverage technology to enhance, rather than replace, human expertise. The platform uses machine learning to optimize carrier selection, but experienced logistics coordinators make final decisions based on factors algorithms might miss.

The changing nature of global trade presents both risks and opportunities. The trend toward nearshoring—moving production closer to consumption—could reduce long-haul shipping volumes that are Expeditors' bread and butter. But it also creates new complexity as supply chains fragment across more countries, each with unique regulations and infrastructure challenges. Complexity is where Expeditors thrives.

Environmental regulations represent another evolution in logistics. As companies face pressure to reduce carbon footprints, they need partners who can optimize routes for emissions, not just cost. Expeditors' ability to provide detailed environmental reporting and offer lower-carbon alternatives (like sea-air combinations instead of pure air freight) becomes a differentiator.

The bull case for Expeditors rests on three pillars. First, global trade continues to grow despite periodic disruptions, and increasing complexity favors sophisticated intermediaries. Second, the company's returns on capital and cash generation remain exceptional, providing flexibility to adapt to market changes. Third, the culture and business model have proven resilient through multiple cycles, suggesting durability going forward.

The bear case can't be ignored. Trade wars and protectionism could reduce international shipping volumes. Digital disruptors might capture share in simple, standardized shipments. Margin pressure from both customers seeking lower costs and carriers seeking higher rates could squeeze profitability. A severe global recession would impact volumes and pricing power simultaneously.

Yet examining Expeditors' history suggests the company thrives on chaos. The Asian Financial Crisis, 9/11, the 2008 financial crisis, COVID-19—each disruption became an opportunity to demonstrate value and capture share. In a world that seems increasingly volatile, the ability to navigate uncertainty might be Expeditors' greatest asset.

XI. Epilogue & Reflections

From March 1990 through October 1 of this year, Expeditors stock rose 5,591 percent. This extraordinary return—turning $10,000 into nearly $570,000—wasn't achieved through explosive growth or revolutionary technology. It came from compound growth, operational excellence, and the patient accumulation of competitive advantages.

The lasting impact of Expeditors' founder-led culture cannot be overstated. Even years after Peter Rose's retirement, employees still reference his philosophies. The company's 8-K filings maintain their unconventional style. The compensation system that aligns employee and shareholder interests remains intact. This cultural continuity is rare in corporate America, where new CEOs often feel compelled to make their mark through dramatic changes.

Expeditors proves a fundamental truth about business: you don't need to own assets to dominate an asset-intensive industry. By focusing on what truly creates value—expertise, relationships, and information—rather than physical infrastructure, the company built a more profitable and resilient business than asset-heavy competitors. This lesson extends beyond logistics to any industry where coordination and knowledge matter more than physical ownership.

For entrepreneurs, Expeditors offers a template for building defensible service businesses. Start with a clear value proposition (one-stop shopping for international logistics). Build a culture that aligns incentives (pay for performance, think like owners). Expand methodically (organic growth, maintain culture). Focus on operational excellence rather than financial engineering. And perhaps most importantly, be patient—real competitive advantages compound over decades, not quarters.

The Expeditors story also challenges conventional wisdom about what makes a great investment. The company has never been particularly cheap on traditional metrics. It operates in a cyclical industry with thin margins. It faces constant competition and disruption threats. Yet patient shareholders who understood the quality of the business and the durability of its model have been richly rewarded.

Looking forward, Expeditors seems almost anachronistic—a company that still believes in offices, relationships, and human judgment in an era of remote work, automation, and artificial intelligence. But perhaps that's precisely the point. In a world where everyone is trying to eliminate human touchpoints, the ability to solve complex, ambiguous problems through expertise and relationships becomes more valuable, not less.

The ultimate lesson from Expeditors might be this: in business, as in life, the most important things are often the most boring. Moving freight from one place to another isn't glamorous. Building a network one office at a time isn't exciting. Focusing on profitability over revenue growth isn't popular. But done consistently over decades, these boring disciplines create extraordinary outcomes. In a world obsessed with disruption, Expeditors reminds us that sometimes the best strategy is simply to execute the basics better than anyone else.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube