Eagle Materials: The Quiet Compounder in Cement & Wallboard

I. Introduction & Episode Roadmap

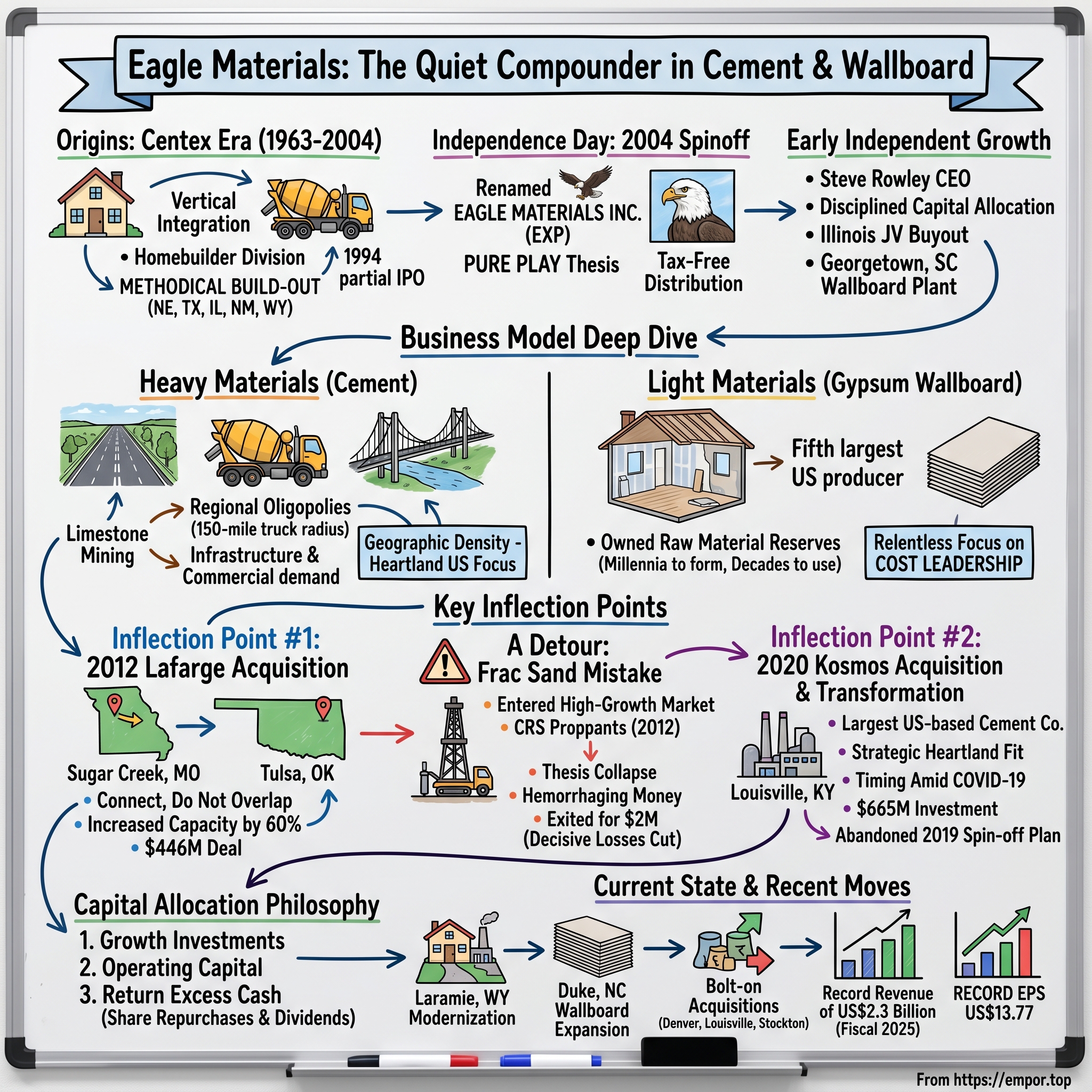

In the glass canyons of Wall Street, where algorithms hunt for the next high-flying tech darling, a different kind of wealth creation unfolds in the American heartland. It happens slowly, methodically, one truckload of cement at a time. It happens without fanfare, without magazine covers, without viral tweets. And for patient shareholders, it has happened extraordinarily well.

Eagle Materials Inc. is a leading U.S. manufacturer of heavy construction products and light building materials. Eagle's primary products, Portland Cement and Gypsum Wallboard, are essential for building, expanding and repairing roads, highways, and residential, commercial and industrial structures across America. Headquartered in Dallas, Texas, Eagle manufactures and sells its products through a network of more than 70 facilities spanning 21 states.

This is a company that most retail investors have never heard of—and that's precisely the point. While the market obsesses over moon-shot bets and narrative-driven momentum plays, Eagle Materials has quietly compounded shareholder wealth for over three decades. The question worth asking: How did a boring spinoff from a homebuilder become one of the best-performing building materials stocks of the last two decades?

In fiscal 2025, they generated record revenue of $2.3 billion and gross profit margin of 29.8%, continued to advance their long-term growth and value-creation strategies, and achieved important milestones in employee health and safety. These aren't flashy numbers by Silicon Valley standards, but they represent something increasingly rare in American capitalism: predictable, profitable, purpose-built operations that throw off cash year after year.

The Eagle Materials story illuminates several timeless business principles. First, the power of owning irreplaceable physical assets—in this case, limestone quarries and gypsum deposits that took millennia to form and will take decades to deplete. Second, the strategic genius of regional density in commodity businesses where transportation costs create natural moats. Third, the compounding magic of disciplined capital allocation over long time horizons.

What follows is a deep dive into Eagle Materials: its origins as a captive supplier to a homebuilder, its transformation into an independent compounder, its strategic acquisitions and honest mistakes, and the durable competitive advantages that underpin its success. The playbook here isn't revolutionary—it's relentlessly disciplined execution of unglamorous fundamentals. And therein lies its power.

II. Origins: The Centex Construction Products Era (1963-2004)

Birth as a Homebuilder Division

To understand Eagle Materials, you must first understand the strategic logic of vertical integration in homebuilding. The company was founded in 1963 as a division of Centex Construction Company. This wasn't an accident of corporate history—it was calculated industrial strategy.

In the early 1960s, Centex was building its empire as one of America's largest homebuilders. Every house required cement for foundations and wallboard for interior walls. These weren't optional line items; they were fundamental inputs. By owning their own cement plants and wallboard facilities, Centex could control costs, ensure supply reliability, and capture margin that would otherwise flow to third-party suppliers.

The Company was founded in 1963 as a building materials subsidiary of Centex Corporation. This parent-subsidiary relationship would define the company's early decades. Centex provided the capital, the strategic direction, and—crucially—a guaranteed customer base hungry for building materials.

The asset base took shape through the 1970s and 80s in a methodical buildout across the American West and Midwest. Construction and start-up of the Nevada Cement plant occur, along with the purchase of Centex Materials, a concrete and aggregates business in Austin, TX. Nevada provided access to fast-growing Western markets. Texas anchored the heartland presence that would become central to the company's identity.

The Illinois Cement Company joint venture is formed, and the plant's start-up occurs two years later. This joint venture model—taking 50% stakes to share risk and capital requirements while maintaining operational control—would become a recurring theme in Eagle's playbook.

The geographic expansion continued with strategic precision. A gypsum wallboard plant in Albuquerque, NM, is purchased, forming Centex American Gypsum. New Mexico brought access to high-quality gypsum deposits and positioned the company to serve the booming Southwest. A cement plant in Laramie, WY, is purchased, becoming Mountain Cement Company. Wyoming extended the footprint into the Rocky Mountain region, serving markets from Denver to Salt Lake City.

What emerges from this period is a pattern of patient asset accumulation—buying or building plants near raw material reserves, then serving customers within a regional radius defined by transportation economics. Cement and wallboard are heavy, bulky products with low value-to-weight ratios. You can't ship them economically across the country. This geographic reality creates local oligopolies—and Centex Construction Products was building precisely such regional strongholds.

The 1994 IPO

The Initial Public Offering of 49% of Centex Construction Products's stock is completed. The year was 1994, and this partial IPO marked the first step in a gradual separation that would take another decade to complete.

Why would Centex sell nearly half of its building materials subsidiary to the public? The answer reveals important lessons about corporate structure and capital allocation.

First, the IPO created a market-tested currency for acquisitions. With publicly traded stock, Centex Construction Products could pursue deals without relying solely on parent company cash or debt capacity. Second, public markets impose discipline. Quarterly earnings reports, analyst coverage, and stock price feedback loops force management to justify decisions and track performance. Third, public listing created liquidity for executives and early employees, aligning incentives with shareholder value creation.

The partial structure was also strategic. By retaining 65% ownership, Centex maintained control while still capturing the benefits of public markets. This is a classic conglomerate playbook: spin off enough to create independence and accountability, retain enough to preserve strategic optionality.

From April 19, 1994, to January 30, 2004, at which time Centex completed a tax-free distribution of its shares to its shareholders, and the Company was renamed Eagle Materials Inc. (NYSE: EXP). For nearly a decade, the company operated in this hybrid state—technically public, practically a controlled subsidiary. But forces were building that would push toward full independence.

III. Independence Day: The 2004 Spinoff

The Separation from Centex

Between April 1994 and January 30, 2004, the company was known as Centex Construction Products, Inc. On January 30, 2004, Centex distributed its shares in the company to its shareholders and the company was renamed Eagle Materials Inc.

Why did full independence happen in 2004? Several factors converged. By the early 2000s, Centex was increasingly focused on its core homebuilding business. The building materials subsidiary, while profitable, didn't fit the strategic narrative that Wall Street demanded. Conglomerate discounts were real—analysts covering homebuilders didn't necessarily understand cement economics, and vice versa.

Centex today distributed to its stockholders all of the shares of Class B Common Stock and the remaining shares of Common Stock held by Centex. As a result of this distribution, CXP is no longer affiliated with Centex Corporation. In addition, CXP has changed its name to Eagle Materials Inc.

The "pure play" thesis was simple but powerful: building materials and homebuilding have different capital intensity profiles, different cycle dynamics, and different optimal capital structures. Separating them would allow each business to optimize for its own economics rather than compromising for corporate portfolio balance.

Under the terms of the agreement reached with Centex in July 2003, CXP and Centex agreed that the spin-off would be accomplished only on a tax-free basis. Centex has informed CXP that it has received approval from the Internal Revenue Service that the spin-off will receive tax-free treatment. The tax-free structure was essential—it meant shareholders received Eagle stock without triggering capital gains, preserving the full value of the separation.

The new company celebrated its independence with appropriate symbolism. Eagle Materials Inc., a publicly held company formerly known as Centex Construction Products, Inc., was spun-off by Centex Corporation effective January 30, 2004. At that time the name change occurred and the company changed the trading symbol for its common stock to EXP and EXP.B. Calendar 2004 also marks the 10th anniversary of the company's listing on the NYSE.

The naming choice was deliberate. "Eagle Materials" projected strength and independence—American iconography for an American manufacturer. The dual trading symbols (EXP and EXP.B) reflected a capital structure with two share classes, designed to provide takeover protection while the newly independent company found its footing.

Early Post-Spin Strategy

Steve Rowley, then CEO, declared: "Eagle Materials Inc. has been a steadily growing business for over forty years by remaining focused on trust and value, with our customers, our employees, and our shareholders. We are proud to mark this special anniversary on the New York Stock Exchange as a completely independent company with a new name. As we continue to implement our strategy of disciplined growth, we are confident that we will maintain a position of strength in our industries and further improve our financial position."

These weren't empty words. The newly independent Eagle moved quickly to consolidate its position and signal its strategic priorities.

Centex Corporation spins off its 65% interest in CXP, and upon completion, the company's new name becomes Eagle Materials Inc., trading on the NYSE under the symbol "EXP." Eagle Materials purchases the remaining 50% interest in the Illinois Cement Company joint venture. This was a classic independence move—buying out joint venture partners to gain full control and capture 100% of cash flows.

The board of directors approves a $65 million expansion and modernization project for the Illinois Cement Company plant in LaSalle, IL. Capital spending began immediately—signaling confidence in the business and commitment to maintaining cost leadership through operational excellence.

American Gypsum announces plans to build a new high-speed, environmentally friendly wallboard plant near Georgetown, SC, and construction begins in late 2005. The Georgetown plant represented geographic expansion into the Southeast—a region with strong population growth and limited wallboard capacity.

The template was set: disciplined capital allocation, regional expansion, operational excellence. These weren't innovative strategies—they were timeless principles executed with unusual discipline. And they would define Eagle Materials for the next two decades.

Since the Eagle Materials spin-off from Centex Corporation on January 30, 2004 approximately 2.2 million shares (or 12% of Eagle Materials stock) have been repurchased. The number of Eagle shares currently outstanding is approximately 16.8 million (on a pre-split basis). Reflecting the strength of Eagle's stock performance since the spin-off from Centex Corporation in January 2004, the Board of Directors of Eagle has declared a 3-for-1 stock split in the form of a 200% stock dividend on its Common Stock and on its Class B Common Stock.

The early returns validated the separation thesis. Independent management, focused strategy, and disciplined capital allocation began producing results that had been obscured within the Centex conglomerate.

IV. The Business Model Deep Dive

The Two Pillars: Heavy vs. Light Materials

Eagle Materials Inc., through its subsidiaries, manufactures and sells heavy construction products and light building materials in the United States. The company operates in four segments: Cement, Concrete and Aggregates, Gypsum Wallboard, and Recycled Paperboard.

Understanding Eagle Materials requires understanding the fundamental distinction between "Heavy Materials" (cement, concrete, aggregates) and "Light Materials" (gypsum wallboard, recycled paperboard). These businesses share some characteristics—both involve mining raw materials, processing them into construction products, and distributing regionally—but they serve different end markets with different cycle dynamics.

Heavy Materials tracks primarily with infrastructure spending and commercial construction. When state highway departments resurface roads, when cities build bridges, when commercial developers pour foundations—that's cement demand. This business is tied to government budgets, infrastructure legislation, and non-residential construction cycles.

Light Materials tracks primarily with residential construction and remodeling activity. When builders finish homes, when homeowners renovate, when commercial spaces retrofit interiors—that's wallboard demand. This business is tied to housing starts, interest rates, and consumer spending patterns.

By combining both, Eagle creates portfolio balance. When residential construction slumps (as it did in 2008-2011), infrastructure spending often increases as governments stimulate the economy. When housing booms, infrastructure may lag. The diversification isn't perfect hedging, but it smooths cycles and provides more stable cash flows.

Cement Business ("Heavy Materials")

The company engages in the mining of limestone for the manufacture, production, distribution, and sale of portland cement, including Portland limestone cement; grinding and sale of slag; and mining of gypsum for the manufacture and sale of gypsum wallboards used to finish the interior walls and ceilings in residential, commercial, and industrial structures.

Portland cement is one of civilization's most essential materials. It's the binding agent in concrete—the most widely used man-made substance on Earth. Roman engineers used proto-cement to build aqueducts that still stand. Modern engineers use Portland cement to build everything from interstate highways to skyscraper foundations.

Cement is the basic binding agent for concrete, a primary construction material. The principal sources of demand for cement are public infrastructure, commercial construction, and residential construction, with public infrastructure accounting for nearly 50% of cement demand. Because of its low-value-to-weight ratio, the relative cost of transporting cement on land is high and limits the geographic area in which each producer can market its products profitably.

This geographic limitation is the key to understanding cement economics. Management believes shipments by truck are generally limited to a 150-mile radius from each plant up to 300 miles by rail, and further by barge. Therefore, the U.S. cement industry comprises numerous regional markets rather than a single national market.

This is not a national commodity market like oil or wheat. It's a collection of regional oligopolies. Within each region, the players are limited by transportation economics. Beyond the 150-mile truck radius, your cement is no longer competitive regardless of production efficiency. This creates local pricing power for well-positioned plants.

Their plants are located near both their raw material reserves and customers in high-growth U.S. markets. The proximity to raw materials and customers lowers transportation costs and carbon footprint. The location of their plants across several high-growth regions within the United States provides geographic diversification, reducing exposure to individual regional construction cycles, and enabling them to move product between different plants in their network as needed. The integrated nature of their plant network enables them to supply customers from more than one plant when desirable.

Gypsum Wallboard ("Light Materials")

Gypsum wallboard (also called drywall or sheetrock) is another fundamental construction material. Walk into almost any modern building and look up at the ceiling, then look at the walls. That smooth, paintable surface? Almost certainly gypsum wallboard.

The manufacturing process involves mining gypsum (a naturally occurring mineral), calcining it (heating to remove water), mixing with additives, pressing between paper facings, and drying. The finished product is lightweight, fire-resistant, and perfect for interior construction.

Eagle Materials' gypsum wallboard division, American Gypsum Company, currently operates manufacturing facilities in Colorado, New Mexico, Oklahoma, and South Carolina. Eagle is the nation's fifth-largest wallboard producer, with an annual wallboard production capacity of nearly four billion square feet. Much of American Gypsum's competitive advantage lies in its access to low-cost raw materials, modern, efficient dryers, and energy-efficient calciners.

In addition, the company has improved the strength, weight, and quality of its gypsum wallboard while reducing the amount of waste generated. Because of attention to detail and focus on continuously improving the low-cost production of gypsum wallboard, American Gypsum has remained profitable through cycles.

That last sentence is critical: "profitable through cycles." Building materials businesses are notoriously cyclical. During housing busts, wallboard demand collapses and industry capacity utilization plummets. Marginal producers lose money; only low-cost producers stay profitable. Eagle's relentless focus on cost position ensures survival and even profitability in the worst years.

Vertical Integration & Raw Material Ownership

Their cement business is supported by their concrete and aggregates business, and their gypsum wallboard business is supported by their recycled paperboard business.

This vertical integration serves multiple purposes. In cement, the company operates ready-mix concrete plants that consume its own cement production—guaranteed demand at favorable economics. In wallboard, the company manufactures the recycled paperboard used as facing material—reducing dependence on external suppliers and capturing additional margin.

The business enjoys long-lived, owned raw material reserves that will sustain its operations over the long term. This raw material ownership is crucial. Limestone and gypsum deposits don't replenish on human timescales. Owning "many decades" of supply means competitors cannot replicate Eagle's position by simply building plants—they would need to acquire comparable deposits, which may not exist in the relevant geographic regions.

V. Key Inflection Point #1: The 2012 Lafarge Acquisition

The Deal

September 2012 marked a transformative moment in Eagle Materials' history. The company announced a definitive agreement with Lafarge North America to purchase Lafarge's Sugar Creek, Missouri and Tulsa, Oklahoma cement plants, as well as related assets, which include six distribution terminals, two aggregates quarries, eight ready-mix concrete plants and a fly ash business. Eagle will also enter into a transition sales agreement to supply certain Lafarge operations with cement for four to five years, and an agreement with a Lafarge affiliate to supply low-cost alternative fuels to the acquired operations. The purchase price is $446 million, subject to customary post-closing adjustments.

Trailing 12-month revenues through June 30, 2012 for the cement plants and related assets were $178 million. The acquisition will increase Eagle's US cement capacity by roughly 60%. The transaction is expected to close in November or December 2012, pending regulatory approvals.

The strategic rationale was elegant. Steven Rowley, Eagle Materials Inc. President and Chief Executive Officer, said the agreement represents a major milestone event for the Company. "Our stated strategy has been to grow the cement and aggregates side of our business. Our first priority has been to acquire cement plants that connect but do not overlap with the market reach of our existing plants. These two high-quality Lafarge cement plants are a compelling fit with our objectives—and the transaction meets our stringent criteria for new investment."

Why This Mattered

The Lafarge acquisition established what would become Eagle's signature acquisition strategy: buying plants that "connect but do not overlap." This isn't about national scale—it's about regional density.

Consider the geographic logic. Before Lafarge, Eagle had cement plants in Texas, Illinois, Wyoming, and Nevada. The Sugar Creek (Kansas City) and Tulsa plants filled the gap between these positions. Suddenly Eagle could serve customers across a contiguous swath from the Rockies to the Midwest. If demand spiked in one region, they could shift supply from adjacent plants. If a plant went down for maintenance, nearby facilities could cover customer needs.

The acquisition will increase Eagle's U.S. cement capacity by about 60 percent (or 1.6 million metric tons) and is expected to close by December 2012, pending regulatory approvals.

In November 2012, EXP acquires two cement plants, one in Kansas City, MO, and the other in Tulsa, OK, increasing its cement production capacity by 60% and expanding its market reach into the south-central US. The transaction also includes eight ready-mix concrete plants, two aggregates quarries, and six distribution terminals.

The deal also demonstrated Eagle's financial discipline. At $446 million for $178 million in trailing revenues, the purchase price represented roughly 2.5x revenues. For cement assets with strategic fit and integration potential, this multiple proved highly accretive over time.

Why was Lafarge selling? The French cement giant was restructuring its global portfolio, retreating from certain North American markets to focus on higher-growth regions. Eagle's regional focus and operational expertise made them the logical buyer for assets that didn't fit Lafarge's multinational strategy.

For investors, the Lafarge deal signaled that Eagle's management would pursue growth aggressively when opportunities aligned with their strategy, while maintaining financial discipline on valuations. This balance—aggressive strategic pursuit with conservative financial execution—would characterize Eagle's approach for years to come.

VI. The Frac Sand Detour: An Honest Mistake

The Opportunity

Not every Eagle Materials initiative succeeded. The company's foray into frac sand—the specialized silica sand used in hydraulic fracturing of oil and gas wells—represents an honest mistake that provides valuable lessons about competitive advantage and capital allocation.

Eagle Materials Inc. has entered into a definitive agreement to acquire CRS Proppants LLC and its subsidiaries, including Great Northern Sand LLC (CRS Proppants), an established supplier of high-quality northern-white frac sand to the energy industry. The transaction aligns well with Eagle Materials' growth strategy, according to the company. CRS Proppants' operations are highly complementary with Eagle Materials' existing frac-sand operations.

The cash purchase price of approximately $225 million is subject to adjustments for working capital and other items, and will be funded by operating cash flow and borrowings under Eagle's bank credit facility. The acquisition will roughly double Eagle's frac-sand production capacity and expand Eagle's frac-sand reserves.

The thesis seemed logical. Eagle already operated sand mines (producing construction aggregates) and had expertise in mining operations. The shale boom was driving explosive demand for frac sand. Northern white sand—the highest-quality material for fracking—commanded premium prices. Why not leverage existing capabilities into a high-growth adjacent market?

Steven Rowley, Eagle Materials' president and chief executive officer, said, "The acquisition represents another key step in Eagle's growth strategy for the frac sand business. We are building a low delivered-cost frac sand supply-system that will serve a number of targeted shale plays with the highest-quality northern white sand. This acquisition will enable us to immediately serve the Permian basin, in particular, with increased production, while creating synergies with our other operations in Texas that are currently serving the Eagle Ford with sand from our Illinois mine."

The Unraveling

The frac sand thesis collapsed as the oil market shifted and technology changed the competitive landscape. Local "in-basin" sand—lower quality but dramatically cheaper to transport—began displacing premium northern white sand. Oil producers optimized for cost rather than quality, and the logistics advantage of northern white sand evaporated.

Eagle's Oil and Gas Proppants segment began hemorrhaging money. By fiscal 2019, the segment was generating operating losses as pricing collapsed and demand shifted to cheaper alternatives.

The Exit

Smart Sand, Inc., a fully integrated frac sand supply and services company, announced that it has completed the acquisition of the Oil and Gas Proppants Segment of Eagle Materials Inc. The acquisition was completed on September 18, 2020 for aggregate consideration of $2 million, consisting of 1,503,759 shares of newly-issued Smart Sand common stock.

The acquisition was completed for aggregate consideration of $2 million. According to Smart Sand, the segment's primary assets include frac sand mines and related processing facilities in Utica, Illinois, and New Auburn, Wisconsin.

Read that again: $2 million. Eagle had invested over $225 million to build its frac sand position—and exited for essentially zero. This was a catastrophic write-off by any measure.

Yet there's something admirable in how Eagle handled the exit. They didn't throw good money after bad trying to salvage a failed investment. They recognized that the thesis had broken—that the frac sand market no longer offered the economics that justified their investment—and cut their losses decisively.

The Company continues to evaluate strategic alternatives with respect to its frac sand business. This disclosure appeared in early 2020 as Eagle prepared to exit. By September 2020, the exit was complete.

The lesson: competitive advantage doesn't transfer automatically to adjacent markets. Eagle's advantages in cement and wallboard—owned raw materials, regional density, vertical integration—didn't apply in frac sand. The commodity economics were different, the customer base was different, and technology disruption moved faster than anticipated.

For investors, the frac sand episode demonstrates that even excellent management teams make mistakes. What matters is how they respond—and Eagle's willingness to acknowledge failure and reallocate capital to higher-return opportunities reflects well on leadership discipline.

VII. Key Inflection Point #2: The 2020 Kosmos Acquisition & Transformation

The Deal

On March 6, 2020, Eagle completed its acquisition of substantially all of the assets of Kosmos Cement Company (the "Kosmos Acquisition") (a joint venture between Cemex S.A.B. de C.V. and Buzzi Unicem S.p.A), which includes a cement plant in Louisville, Kentucky with annual capacity of 1.7 million tons, as well as seven distribution terminals and substantial raw-material reserves (the "Kosmos Cement Business"). The purchase price paid by Eagle in the Kosmos Acquisition was $665 million in cash, subject to a customary post-closing inventory adjustment.

The plant has the capacity to produce nearly 1.7 million tons of cement annually. The purchase price is $665 million, subject to customary post-closing adjustments. Eagle anticipates certain tax benefits arising from the transaction, the net present value of which is expected to be approximately $120 million.

The Kosmos deal was Eagle's largest acquisition to date. In 2020, Kosmos Cement Company was purchased by Eagle Materials Inc., adding 1.7MT of cement production to the Eagle's Heavy Materials Sector portfolio. The Kosmos Portland Cement Company began shipping cement from this location in 1905. Eagle was acquiring over a century of operational heritage.

Strategic Impact

In early 2020, EXP acquires the Kosmos cement plant, located in Louisville, KY, along with seven distribution terminals. The acquisition of Kosmos Cement positions EXP as the largest US-based cement company and the sixth-largest cement operator in the US.

This positioning mattered enormously. Eagle had transformed from a regional player to a national force—the largest U.S.-based cement producer. Unlike global competitors (CEMEX, Heidelberg, Holcim), Eagle operated exclusively in America, with management and capital allocation decisions made in Dallas for American markets.

Mike Nicolais, Eagle Materials Board Chairman, added, "This acquisition is an exceptional geographic fit with our existing system of heartland-US cement assets. It not only extends our reach in key US markets, but also enhances the near and long-term cash flow generation capabilities of our businesses."

Since 2012, we have invested approximately $2.4 billion to expand the Heavy Materials sector. These investments have more than doubled our U.S. cement capacity.

The timing was audacious. Kosmos closed on March 6, 2020—days before COVID-19 shutdowns paralyzed the global economy. Management couldn't have known a pandemic was coming, but they moved forward with conviction based on long-term strategic logic.

The Abandoned Spin-off

The Kosmos acquisition occurred against the backdrop of Eagle's planned corporate separation. Board of Directors approved a plan in 2019 to separate its heavy and light materials businesses into independent, publicly-traded companies by means of a tax-free spin-off to Eagle shareholders.

Eagle Materials Inc. today announced that its Board of Directors has approved a plan to separate its Heavy Materials and Light Materials businesses into two independent, publicly traded corporations by means of a tax-free spin-off to Eagle shareholders. The separation is expected to be completed in the first half of calendar 2020. The Company also announced that it is actively pursuing alternatives for its Oil and Gas Proppants business with the support of an independent financial advisor.

Mike Nicolais, Eagle's Chairman stated, "The Eagle Board and management team has maintained a regular evaluation of the strategic and financial options to best position the Company to drive value for shareholders. Historically, our Light and Heavy businesses have provided Eagle with balance and financial strength; however, the Board recognized that our industry-leading performance is not adequately reflected in the market value of the combined company. We engaged with shareholders and took their input into account in coming to this conclusion. Based upon our recent comprehensive review of various strategic, operational and financial alternatives, the Eagle board and management team believe this separation will provide each of the businesses with the financial flexibility to pursue its own growth strategies and operating priorities."

Then COVID-19 hit. On May 30, 2019, the Company plans to separate its Heavy Materials and Light Materials businesses into two independent, publicly traded corporations by means of a tax-free spin-off to Eagle shareholders. We remain committed to the separation, although the timing is uncertain.

The separation never happened. As markets stabilized and Eagle's integrated model proved resilient through the pandemic, the urgency to separate faded. Today, Eagle operates both Heavy and Light Materials under one roof—and the combination has served shareholders well.

The abandoned spin-off reveals management pragmatism. When circumstances change, strategy should change. Dogmatic adherence to pre-pandemic plans would have distracted management during a crisis. Instead, they focused on integrating Kosmos, navigating pandemic uncertainty, and preserving financial flexibility.

VIII. The COVID Test & Capital Allocation Mastery

Navigating the Crisis

Eagle Materials Inc., through its subsidiaries, is a leading manufacturer of heavy construction materials and light building materials in the United States. Our primary products, portland cement and gypsum wallboard, are commodities that are essential in commercial and residential construction; public construction projects to build, expand, and repair roads and highways; and repair and remodel activities. Demand for our products is generally cyclical and seasonal, depending on economic and geographic conditions. We distribute our products throughout most of the United States, except the Northeast, which provides us with regional economic diversification.

When COVID-19 shut down global economies in March 2020, construction activity—Eagle's lifeblood—faced profound uncertainty. Would projects halt? Would customers default? Would credit markets freeze?

Eagle's geographic positioning proved advantageous. Operations in "heartland" states—where construction was generally deemed essential and lockdowns less severe—continued operating with minimal disruption. The company's decentralized structure, with local profit center managers making operational decisions, allowed nimble responses to local conditions.

Financial discipline paid dividends. Eagle entered the crisis with manageable debt levels and available liquidity. The Kosmos acquisition had been financed conservatively, leaving room for uncertainty.

The Capital Allocation Philosophy

Eagle seeks to maintain a disciplined capital allocation process to enhance shareholder value. Our allocation priorities remain: 1. Investing in growth opportunities that are consistent with our strategic priorities and meet our strict financial return standards; 2. Making operating capital investments to maintain and strengthen our low-cost producer position; and 3. Returning excess cash to shareholders, primarily through our share repurchase program.

This hierarchy matters. Growth investments come first—but only if they meet strict return standards. Operating capital is second—maintaining cost leadership requires continuous investment in efficiency. Shareholder returns are third—but only with "excess" cash after funding the first two priorities.

Over the past five fiscal years, we have invested $388 million in acquisitions, $546 million in organic capital expenditures, and $1.8 billion in share repurchases and dividends.

This disciplined capital allocation, including share repurchases that have reduced outstanding shares by 30% over time, supports long-term success and enhances its operational capabilities.

Share repurchases are the signature move. Unlike dividends—which create tax consequences for shareholders—buybacks reduce share count and increase per-share ownership for continuing shareholders. Over time, this compounding effect becomes significant.

Historically, Eagle Materials (NYSE: EXP) has maintained a long-standing commitment to returning capital to shareholders, with a dividend payment history extending back to 1998.

The combination of buybacks and dividends reflects different purposes. Dividends signal stability and provide income. Buybacks signal management confidence in intrinsic value and return capital efficiently when shares trade below fair value. Eagle uses both, with buybacks dominating.

In addition, we returned $332 million of cash to shareholders through share repurchases and dividends and maintained our balance sheet strength, ending the year with debt of $1.2 billion and a net leverage ratio (net debt to Adjusted EBITDA) of 1.5x.

A 1.5x net leverage ratio is conservative for an asset-intensive business with stable cash flows. This conservatism provides flexibility—capacity to pursue acquisitions or weather downturns without financial distress.

IX. Recent Strategic Moves & Current State (2020-Present)

Bolt-on Acquisitions

Since the transformative Kosmos deal, Eagle has pursued smaller "bolt-on" acquisitions that extend its regional footprint incrementally.

In 2022, EXP completes the acquisition of a concrete and aggregates business serving the Greater Denver market, now known as Raptor Materials. Denver is one of America's fastest-growing metropolitan areas, with strong construction demand.

In 2023, EXP takes over the Battletown quarry operation in Louisville, KY, further expanding its aggregates operations. In May 2023, EXP completes the acquisition of the Stockton import cement terminal, further serving its customer base in Northern California and Northern Nevada.

Eagle Materials made several strategic moves during the year, including the acquisition of two pure-play aggregates businesses in Kentucky and Western Pennsylvania for a combined investment of $175 million.

These acquisitions share common characteristics: geographic fit with existing operations, reasonable valuations, and potential for operational synergies. They're not transformative individually, but collectively they strengthen regional density and market position.

Growth Investments

Beyond acquisitions, Eagle is investing heavily in organic capacity expansion and modernization.

The expansion will increase the plant's annual manufacturing capacity by 50% to approximately 1.2 million tons of cement and is expected to reduce manufacturing costs by approximately 25%. Expected cost reductions from the modern kiln line will be generated by replacing the use of solid fuels with lower cost alternative fuels and natural gas, simplified maintenance programs, and improved operating efficiencies. Additionally, the CO2 intensity from the Laramie, Wyoming facility is expected to decline by nearly 20% once the project is complete.

The project investment, which includes an additional distribution facility in northern Colorado, is estimated to be approximately $430 million. The existing plant, which became operational in 1927, has an annual capacity of 800,000 tons of cement.

Planning for the project has been completed, primary regulatory approvals have been received and construction is expected to begin immediately with startup scheduled for the second half of calendar year 2026.

At our Laramie, Wyoming cement plant, we are on track to complete our $430 million modernization and expansion project by the end of calendar 2026. The Laramie, Wyoming plant is also one of the oldest and therefore, a higher cost cement plant in our network. Modern cement kiln technology is much more efficient than the 1960s vintage kilns currently used at our Laramie facility. This allows us to reduce our manufacturing cost by 25%.

The Laramie modernization illustrates Eagle's operational philosophy. The existing plant dated to 1927—nearly a century old. Rather than operating obsolete equipment until it fails, Eagle invests proactively in modernization. The result: lower costs, higher capacity, reduced environmental footprint.

On the wallboard side, a similar modernization is underway.

Upon completion, the project will increase the plant's annual wallboard manufacturing capacity by 300 million square feet, or 25%, to approximately 1.5 billion square feet, and will enable, with moderate additional investment in the future, a further 500 million square feet of capacity expansion, for a total of 2.0 billion square feet of manufacturing capacity. The facility will be upgraded with state-of-the-art technology that will increase operating efficiencies, simplify maintenance programs, and reduce natural gas usage, resulting in manufacturing cost savings of almost 20%.

The total project investment is estimated to be $330 million. Planning for the project has been completed, all regulatory approvals have been received, and construction is expected to begin immediately, with startup scheduled for the second half of calendar year 2027.

Combined, the Laramie cement and Duke wallboard projects represent over $760 million in capital investment—a massive commitment that will take years to complete but should strengthen Eagle's cost position for decades.

Current Financial Performance

Record Revenue of US$2.3 billion, up slightly from the prior year. Net Earnings of US$463.4 million, down 3%. Record net earnings per diluted share of US$13.77, up 1%. Adjusted net earnings per diluted share (Adjusted EPS) of US$13.94, up 2%.

Fiscal 2025 revenue in the Heavy Materials sector, which includes Cement, Concrete and Aggregates, as well as Joint Venture and intersegment Cement revenue, was down 2% to $1.4 billion, and annual operating earnings decreased 11% to $310.7 million.

Fiscal 2025 revenue in the Light Materials sector, which includes Gypsum Wallboard and Recycled Paperboard, increased 3% to $969.2 million, driven by record Recycled Paperboard sales volume and higher Gypsum Wallboard and Recycled Paperboard net sales prices. Gypsum Wallboard annual sales volume was 3.0 billion square feet (BSF) up slightly from the prior year, and the average net sales price was up 1% to $236.04 per MSF. Recycled Paperboard annual sales volume was up 5% to 350,000 tons.

The fiscal 2025 results demonstrate both the portfolio balance and cyclical nature of Eagle's businesses. Heavy Materials faced headwinds from lower cement volumes, while Light Materials offset with higher pricing and volumes. The combination delivered record revenue and near-record earnings per share.

X. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

Building a cement plant is not a weekend project. Federal and state environmental regulations make it increasingly difficult to permit greenfield or brownfield cement capacity additions, and we have not seen any loosening of restrictions.

Plants cost $500 million or more and take 3-5 years to permit and construct. Environmental reviews are exhaustive. Community opposition ("NIMBY") is intense. Even if a competitor had unlimited capital, they would struggle to replicate Eagle's position in regions where the company already owns permitted facilities and raw material reserves.

The permitting moat is underappreciated. Limestone quarries and gypsum deposits are finite resources in fixed geographic locations. Once permitted, they're nearly impossible to replicate nearby. The business enjoys long-lived, owned raw material reserves that will sustain its operations over the long term. This isn't just competitive advantage—it's permitting advantage, resource advantage, and time advantage compounded.

2. Bargaining Power of Suppliers: LOW

Eagle owns its key raw materials. Limestone, gypsum, and aggregates come from company-owned quarries and mines. There's no external supplier who can squeeze margins or disrupt supply.

Our cement business is supported by our concrete and aggregates business, and our gypsum wallboard business is supported by our recycled paperboard business. Vertical integration further reduces supplier power—Eagle manufactures paperboard for wallboard facing rather than buying it externally.

Energy costs matter—cement production is energy-intensive—but these costs generally pass through in pricing. When fuel prices rise, cement prices adjust. When fuel prices fall, Eagle captures margin improvement.

3. Bargaining Power of Buyers: MODERATE

Eagle's customers include contractors, ready-mix concrete producers, and building materials distributors. No single customer dominates. The customer base is fragmented, limiting buyer power.

However, cement and wallboard are commodities. Within a given region, multiple suppliers compete on price, quality, and service. Customers can switch suppliers relatively easily if pricing gets out of line.

The regional nature of markets provides some insulation. A contractor in Kansas City can't easily switch to a supplier in Denver—transportation costs would make the distant supplier uncompetitive. This geographic lock-in creates soft switching costs that moderate buyer power.

4. Threat of Substitutes: LOW

What substitutes for concrete? In most applications, nothing. Roads, bridges, foundations, parking structures—they require concrete, which requires cement. There's no viable alternative material at scale.

Wallboard faces limited competition from plaster (more expensive, harder to install) and wood panels (different aesthetic, different applications). For mainstream interior construction, gypsum wallboard remains dominant.

Management noted that approximately two-thirds of Infrastructure Investment and Jobs Act (IIJA) funds remain to be spent, providing a substantial pipeline of future projects. Federal infrastructure legislation mandates cement use for decades of roadway and bridge projects. This isn't demand that can shift to substitutes—it's locked in by engineering requirements and legislative appropriations.

5. Competitive Rivalry: MODERATE

The top cement companies include CEMEX, Heidelberg Materials (formerly Lehigh Hanson Inc.), Buzzi Unicem, Ash Grove Cement Company (acquired by CRH in 2018), Argos USA Corp., Eagle Materials Inc., CalPortland Co., Martin Marietta Materials, Inc., and GCC of America, Inc. In 2017, the top 5 companies produced 59 percent of US portland cement; the top 10 companies produced 79 percent.

The U.S. cement industry is consolidated but not monopolistic. Major players include global giants (CEMEX, Heidelberg, CRH, Holcim) and U.S.-focused operators (Eagle, Martin Marietta, Vulcan).

While the Company's markets include most of the United States, except the Northeast, approximately 65% of total revenue is generated in ten states: Colorado, Illinois, Kansas, Kentucky, Missouri, Nebraska, Nevada, Ohio, Oklahoma, and Texas. Population growth is a major driver of construction products and building materials demand. The population in these ten states is expected to increase approximately 11% between the 2020 census and 2050, compared with 7% for the United States as a whole.

Eagle's strategic footprint in growing heartland and Sunbelt regions provides favorable competitive dynamics. These markets benefit from population growth, infrastructure needs, and relatively fragmented competition compared to coastal urban areas.

Industry discipline typically maintains pricing power. Cement and aggregates competitors understand that price wars destroy value for everyone. The regional nature of markets—where the same competitors face each other repeatedly—encourages rational behavior.

XI. Hamilton Helmer's 7 Powers Analysis

1. Scale Economies: STRONG

Cement kilns have massive fixed costs and operate 24/7. A kiln running at 90% capacity generates far better unit economics than one running at 60%. Each incremental ton of production dramatically improves profitability.

Distribution networks also exhibit scale economies. More trucks serving more customers from more terminals creates loading efficiency and route density. Eagle's integrated network—where adjacent plants can shift product between regions—amplifies these advantages.

2. Network Effects: NOT APPLICABLE

Building materials don't exhibit network effects. The value of Eagle's cement to a contractor doesn't increase because other contractors also use Eagle cement. This power simply doesn't apply to the business model.

3. Counter-Positioning: MODERATE (Historically)

When Eagle spun from Centex, it adopted a "pure-play" strategy focused exclusively on building materials while competitors maintained diversified portfolios. This focus enabled superior operational execution that diversified competitors struggled to match.

The frac sand foray was an attempted counter-position that failed. Eagle tried to leverage existing sand mining expertise into oil and gas markets—but the competitive dynamics were different enough that existing advantages didn't transfer.

Current pure-play focus on U.S. domestic production is a form of counter-position versus global competitors. CEMEX, Heidelberg, and Holcim allocate management attention across dozens of countries. Eagle's Dallas-based management focuses exclusively on American markets.

4. Switching Costs: LOW

Cement and wallboard are largely commodities. Customers can switch suppliers relatively easily. There's no proprietary technology or format lock-in.

However, logistics relationships create soft switching costs. A ready-mix producer with established delivery patterns from Eagle plants faces coordination costs in switching suppliers. Reliability matters—a supplier who consistently delivers on time earns business that's sticky even without contractual lock-in.

5. Branding: WEAK

This is a B2B commodity business. Contractors don't choose wallboard based on brand recognition—they choose based on price, availability, and product specifications. Brand matters far less than it would in consumer products.

Quality and consistency matter more than brand. Eagle's reputation for reliable product quality earns customer loyalty, but this is operational excellence rather than brand power.

6. Cornered Resource: STRONG (Key Power)

The business enjoys long-lived, owned raw material reserves that will sustain its operations over the long term.

This is Eagle's most durable competitive advantage. Limestone and gypsum deposits are finite, geographically fixed resources. Once you own them, competitors cannot replicate your position by simply building plants—they would need comparable deposits in relevant geographic regions.

Permitting new quarries is nearly impossible in many areas due to environmental regulations and community opposition. Eagle's existing permits—granted decades ago under different regulatory regimes—represent unreplicable assets.

The "many decades" of supply provides extraordinary visibility and security. While competitors face potential reserve exhaustion or permitting challenges, Eagle can plan and invest with confidence in long-term resource availability.

7. Process Power: STRONG (Key Power)

Eagle's operational performance—margins, free cash flow, returns on invested capital—consistently exceeds industry averages. This reflects accumulated process knowledge that's difficult for competitors to replicate.

In addition, the company has improved the strength, weight, and quality of its gypsum wallboard while reducing the amount of waste generated. Because of attention to detail and focus on continuously improving the low-cost production of gypsum wallboard, American Gypsum has remained profitable through cycles.

"Profitable through cycles" represents process power in action. During industry downturns, marginal producers lose money while Eagle stays profitable. This allows Eagle to invest countercyclically—acquiring distressed assets, upgrading facilities, building market share—while competitors retrench.

Capital allocation discipline is also process power. The systematic approach to buybacks, acquisitions, and organic investment reflects institutional knowledge about value creation that took decades to develop.

Summary: Eagle's Durable Competitive Advantage

The combination of Cornered Resources (owned raw materials with long reserve life), Process Power (operational excellence and capital allocation discipline), and Scale Economies (fixed cost leverage in production and distribution) creates a durable moat.

The regional nature of cement markets means national scale matters less than regional dominance. Eagle's heartland positioning provides favorable competitive dynamics without requiring presence in all 50 states.

XII. Playbook: Business & Investing Lessons

The "Boring Business" Advantage

Eagle Materials teaches a counterintuitive lesson: boring businesses can generate extraordinary returns. Cement and wallboard lack the narrative appeal of disruptive technology or high-growth software. Yet patient shareholders have been richly rewarded.

The "boring business" advantage has several components:

Reduced competition for talent and capital. The best MBA graduates don't dream of running cement plants. Private equity firms don't aggressively bid up building materials assets. This leaves more opportunity for disciplined operators to acquire and build value.

Predictable demand patterns. Society needs cement and wallboard regardless of technology trends, consumer preferences, or fashion cycles. This demand stability enables confident long-term planning and investment.

Operational leverage compounds over time. Small improvements in kiln efficiency, maintenance practices, or logistics coordination accumulate into significant cost advantages. This compounding is invisible in any single quarter but transformative over decades.

Alignment between management and shareholders. Without flashy growth narratives or stock-based compensation tied to revenue growth, management focuses on what actually creates value: profits, cash flow, and returns on capital.

Myth vs. Reality: The Commodity Business Misconception

Common narrative: Cement and wallboard are commodities where no one can differentiate, so returns are poor.

Reality: Geographic constraints create regional oligopolies. Low-cost producers generate excellent returns through cycles. Raw material ownership and permitting advantages create durable moats.

Eagle's consistent profitability and above-average returns demonstrate that "commodity" doesn't mean "no competitive advantage." The advantages are just different—operational rather than brand-based, geographic rather than network-based.

Key KPIs for Investors to Track

For investors following Eagle Materials, three metrics matter most:

1. Cement price per ton and volume trends. Cement pricing directly impacts Heavy Materials profitability. Volume trends indicate end-market demand. Watch for pricing discipline during weak periods—competitors who cut prices destroy industry economics.

2. Wallboard square footage and price per MSF (thousand square feet). These metrics track Light Materials performance. Housing starts correlate with wallboard demand, but R&R (repair and remodel) activity provides baseline demand even in housing downturns.

3. Share count trajectory. Eagle's capital allocation emphasizes buybacks. Declining share count magnifies per-share value creation. Watch for management discipline in repurchasing shares at reasonable valuations—not paying any price for buyback optics.

XIII. Bull Case & Bear Case

Bull Case

Infrastructure tailwinds persist for years. Approximately two-thirds of Infrastructure Investment and Jobs Act (IIJA) funds remain to be spent. This represents years of federally-funded cement demand with minimal sensitivity to economic cycles or interest rates. Eagle's heartland positioning captures this demand directly.

Modernization investments generate returns. The $430 million Laramie cement modernization and $330 million Duke wallboard expansion will improve cost position and increase capacity simultaneously. As these projects come online (2026-2027), Eagle should enjoy margin expansion and volume growth without proportional capital spending.

Housing underbuilding requires eventual correction. America has underbuilt housing for over a decade. Demographic trends (millennial household formation) support eventual housing recovery. When housing normalizes, wallboard demand increases significantly.

Capital allocation discipline continues. Management's track record of disciplined buybacks at reasonable valuations creates compounding shareholder returns. Each percentage of share count reduction permanently increases remaining shareholders' ownership.

Pricing power in regional oligopolies. Transportation economics limit competitive entry. Permit constraints prevent new capacity. Rational industry behavior maintains pricing discipline. These factors support margin stability and potential expansion.

Bear Case

Housing affordability crisis persists. High mortgage rates and elevated home prices have suppressed residential construction. If affordability remains constrained—due to sustained high rates or insufficient supply response—wallboard demand growth could disappoint for extended periods.

Infrastructure spending plateaus post-IIJA. Federal infrastructure programs are politically negotiated. Future administrations may prioritize different spending areas. State and local budgets face constraints from pension obligations and healthcare costs.

Energy cost spikes pressure margins. Cement production is energy-intensive. Extended periods of elevated natural gas, coal, or electricity prices could compress margins faster than price increases offset.

Regional economic concentration creates risk. Approximately 65% of total revenue is generated in ten states. Regional downturns—oil price collapse affecting Texas, for example—could disproportionately impact Eagle compared to geographically diversified competitors.

Competition from imports or new capacity. While transportation costs limit domestic competition, coastal markets remain vulnerable to imported cement. Technological changes (carbon capture subsidies, for example) could alter the economics of new capacity construction.

XIV. Conclusion: The Quiet Compounder's Edge

Eagle Materials represents something increasingly rare in American business: a company that does the boring things extraordinarily well, year after year, decade after decade.

At Eagle Materials we believe success is a result of sound strategic choices, strong execution decisions by our decentralized profit center leaders, and the wise stewardship of resources. Focusing on these basics is how we get results and serve the best interests of our shareholders.

There's no magic here—just disciplined execution of timeless principles. Own irreplaceable assets. Build regional density in transportation-constrained markets. Invest continuously in operational excellence. Return excess capital to shareholders. Repeat for decades.

Michael Haack joined Eagle Materials in December 2014 as Chief Operating Officer. He was promoted to President and Chief Operating Officer in August 2018 and was appointed President and Chief Executive Officer in July 2019. Previously Mr. Haack spent 17 years at Halliburton Energy Services, holding successively important operating positions, most recently as Global Operations Manager at Halliburton's Sperry Drilling division.

Mr. Haack holds a Master of Science degree from Texas A&M University and a Bachelor of Science degree from Purdue University, both in Industrial Engineering, and an MBA from Rice University.

Current CEO Michael Haack brings operational expertise from his Halliburton background and industrial engineering training. This isn't a flashy Silicon Valley founder—it's a quiet operator focused on continuous improvement.

The frac sand detour teaches humility: even excellent management teams make mistakes. The Kosmos acquisition demonstrates conviction: when opportunities align with strategy, move boldly even amid uncertainty. The abandoned spin-off shows pragmatism: when circumstances change, reconsider plans without ego.

For investors seeking exposure to America's infrastructure renaissance and housing recovery, Eagle Materials offers a differentiated vehicle. Unlike pure-play aggregates companies (Vulcan, Martin Marietta), Eagle provides cement exposure. Unlike global cement giants (CEMEX, Heidelberg), Eagle operates exclusively in growing American markets. Unlike homebuilders, Eagle captures construction spending without single-family housing concentration risk.

The company trades at reasonable valuations relative to peers and the broader market, though cyclical businesses deserve cyclical awareness. Patient investors who can stomach quarterly volatility may find Eagle Materials' long-term compounding attractive.

Eagle Materials Inc., a supplier of construction materials, has outperformed the S&P 500 with a 34.7% rise since January 2022.

In a world obsessed with disruption, Eagle Materials disrupts nothing. It simply makes cement and wallboard, year after year, profitably through cycles. Sometimes the quiet path is the most rewarding one.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube