Lumen Technologies: The Telecom Phoenix Rising from the Ashes

Introduction: The Most Unlikely AI Play of 2024

Picture Monroe, Louisiana, in the summer of 2024. A small city of 50,000 people nestled in the bayou country, best known for its duck calls and college football. Few would guess that this sleepy Southern town serves as headquarters for what may become the most consequential infrastructure company of the artificial intelligence era.

The Louisiana-based company has been around a long time, so it was a surprise to some that the stock was at risk of being delisted from the New York Stock Exchange when in 2023, its price per share briefly dipped under $1.00. Just eighteen months earlier, Lumen Technologies traded at levels that implied the company was worth less than zero—its stock price suggesting investors believed the debt-laden enterprise was headed for bankruptcy.

Then came the AI revolution.

From July 1, 2024, to September 30, 2024, the shares went on a tear. The stock, which was trading at just $1.11 at the start of the third quarter of 2024, surged 540% by the end of the third quarter. What happened? Lumen Technologies announced it had secured $5 billion in new business driven by major demand for connectivity fueled by AI.

The central mystery of the Lumen story is both improbable and illuminating: How did a declining rural telephone company from Louisiana—one founded when Franklin Roosevelt was in his first term—become a potential kingmaker in the AI infrastructure era? The answer reveals something profound about how technology cycles create unexpected winners and losers, how balance sheets determine destiny, and how fiber optic cable—the most boring of technologies—may prove to be the most valuable asset of the 2020s.

This is the story of ninety-five years of telecom history colliding with the most transformative technology wave since the internet itself. It spans six corporate names, dozens of acquisitions, hundreds of billions in debt, and one extraordinary bet that AI would save everything.

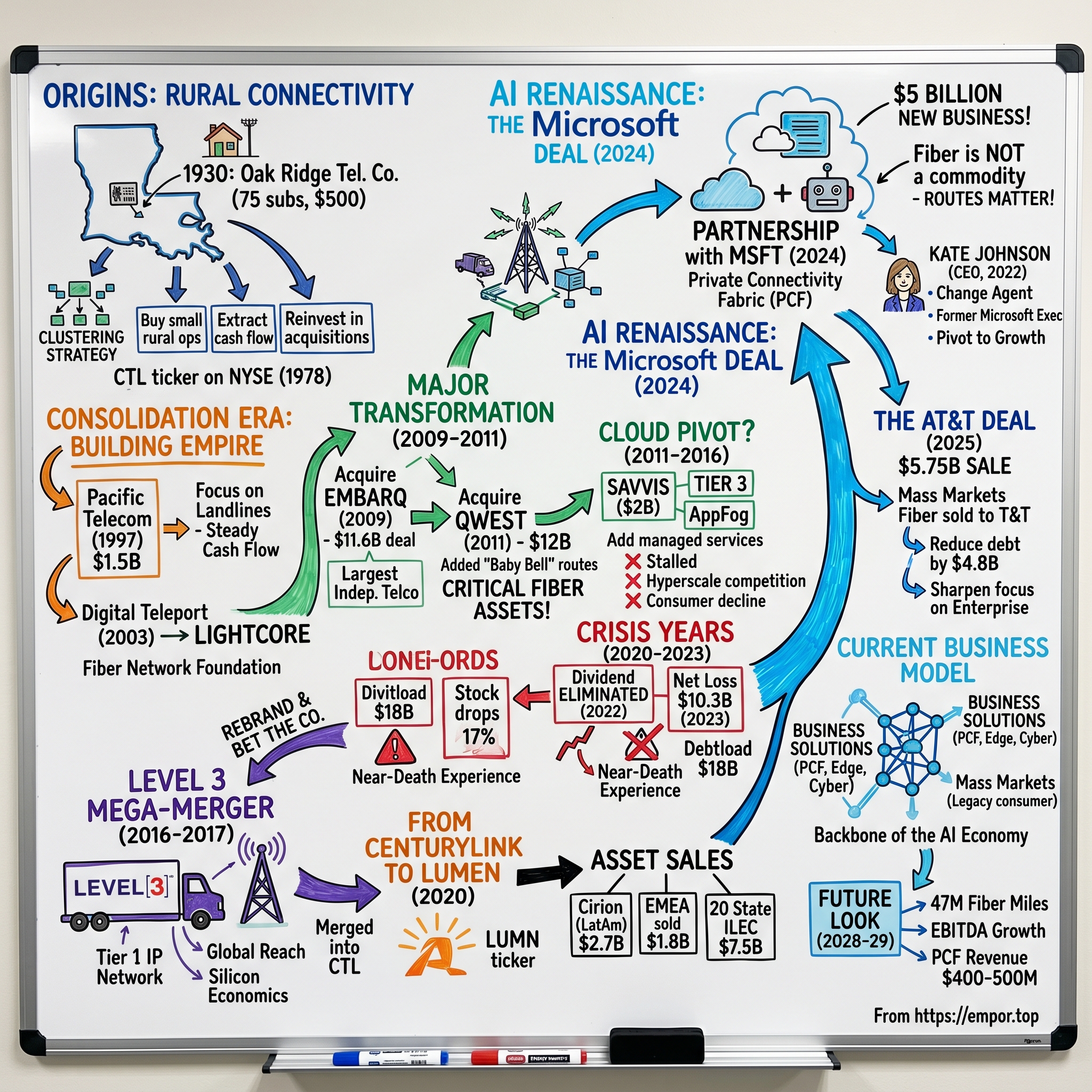

Origins: The Oak Ridge Telephone Company and the Business of Rural Connectivity

To understand where Lumen is going, you must understand where it came from. The earliest predecessor of CenturyLink was the Oak Ridge Telephone Company in Oak Ridge, Louisiana, which was owned by F. E. Hogan, Sr. In 1930, Hogan sold the company, with 75 paid subscribers, to William Clarke and Marie Williams, for $500. They moved the switchboard to the Williams family front parlor.

Five hundred dollars. Seventy-five subscribers. A switchboard in a front parlor. This is where a company that would one day control over 400,000 route miles of fiber optic cable began.

In 1946, the Williams' son, Clarke McRae Williams, received ownership of the family's telephone company as a wedding gift. In 1947, Clarke Williams learned the telephone company in Marion, Louisiana was for sale. With a loan from business associate Joe Sydney Carter, Clarke purchased the Marion Telephone Company and eventually made it his base of operation as he grew his company through more acquisitions.

The strategy that Clarke Williams developed in rural Louisiana would define the company for the next seven decades: buy small telephone operations in underserved markets, extract cash flow, reinvest in acquisitions, repeat. While AT&T and the Bell companies dominated urban America, independent operators like Williams saw opportunity in the territories the giants ignored—the small towns, the rural crossroads, the places where running copper wire was expensive and subscriber density was low.

The company remained as a family-operated business until it became incorporated in 1968. By 1968, Oak Ridge Telephone Company served three states with 10,000 access lines. That year the company was incorporated as Central Telephone and Electronics. In 1971, the company was renamed as Century Telephone Enterprises, Inc. In 1972, Century Telephone acquired the La Crosse Telephone Corporation, of Wisconsin. On October 24, 1978, Century Telephone moved to the New York Stock Exchange for the first time and began to trade under the ticker symbol CTL.

The telecom industry of this era operated under assumptions that seem quaint today. Voice calls were the only product that mattered. Regulation determined pricing. Geographic monopolies were the norm. And critically, telephone companies were valued as stable utilities that paid reliable dividends to investors who wanted income rather than growth.

Small telephone companies throughout the United States went up for sale during the 1970s, largely because descendants of the families that operated them held no interest in the tiny operations. A moratorium on acquisitions by Bell companies meant that many were eventually taken over by larger independent companies such as General Telephone and Consolidated Telephone. Several other smaller independents were involved in the consolidation of the industry at this time. Rochester Telephone, TDS and particularly Century among them, grew very quickly from these seemingly insignificant acquisitions.

This was Century Telephone's competitive moat: patience, discipline, and the willingness to buy what others ignored. Clarke Williams and his successor, Glen Post III, built what would become CenturyLink by understanding that in telecommunications, scale matters—but that scale can be built one small acquisition at a time, provided you manage debt carefully and operate efficiently.

The Consolidation Era: Building an Empire One Acquisition at a Time (1990s-2000s)

Through the 1990s, Century continued the rapid expansion of its customer base through a series of acquisitions aimed at gaining market share in fast-growing rural populations. The strategy was elegant in its simplicity: rural America was growing faster than urban America in key states, and Century positioned itself to capture that growth.

Century subsequently added several more smaller companies, building upon the company's contiguous property "clustering" strategy. These clusters comprised important rural areas which, unlike the saturated urban areas controlled by the Bell companies, had much higher potential for growth. Its strongest growth in the early 1990s was in Michigan, where it controlled cellular licenses for almost the entire state. Its second largest concentration of cellular properties was in northern Louisiana and southern Arkansas, including Texarkana, Shreveport, and Monroe. Century also owned cellular interests in a huge area covering southeastern Colorado, western New Mexico, and northern Arizona.

The Pacific Telecom acquisition in 1997 represented a step change in ambition. By purchasing a Portland, Oregon-based company for $1.5 billion, Century added 1.9 million cell lines and nearly doubled in size. After the acquisition, Century's network served 21 states and 2 million customers.

The 2000s brought both opportunity and strategic refocus. In 2000, the company acquired 490,000 telephone lines from Verizon for $1.5 billion. But in 2002, in a move that seemed counterintuitive at the time, Century sold "substantially all" of its wireless business to Alltel for $1.59 billion. The company sold its wireless business to ALLTEL, entering a new era as a leading U.S. pure-play rural local exchange carrier.

Why sell wireless at the dawn of the mobile era? Century's management saw something that many analysts missed: the economics of rural wireless were fundamentally different from the economics of rural wireline. Wireless required massive capital investment in spectrum and towers; wireline generated steady cash flow from existing infrastructure. By focusing on landlines, Century could concentrate its capital on accretive acquisitions rather than competitive bidding wars for spectrum.

In 2003, the company acquired Digital Teleport for $39 million, which formed some of its main assets and expanded the company's fiber network offering. In June, CenturyTel also acquired the fiber network of Digital Teleport, Inc., a 5,700-mile route running from Illinois to Texas, and adjoining states. CenturyTel renamed the network company LightCore. Closing out the year, in December CenturyTel acquired the Midwest Fiber Optic Network (MFON) from Level 3 Communications, Inc.

These fiber acquisitions would prove prescient. While voice traffic on copper lines would decline relentlessly over the following two decades, the demand for fiber capacity would explode beyond anyone's projections. Century was building the foundation for what Lumen would become—even if no one realized it at the time.

The First Major Transformation: Embarq, Qwest, and Becoming CenturyLink (2009-2011)

By 2008, the telecommunications landscape had shifted dramatically. The iPhone had launched. Broadband was becoming essential infrastructure rather than a luxury. And the financial crisis created opportunities for well-capitalized acquirers to buy distressed assets at attractive prices.

On July 1, 2009, the company began operating under the new name: CenturyLink. On July 1, 2009, CenturyTel completed its acquisition of Embarq Corporation in a tax free, stock-for-stock transaction creating one of the leading communications companies in the United States. This combination of two successful companies is viewed with excitement by customers, employees and communities alike. Among the benefits are the creation of an industry-leading communications provider; an expanded suite of products and solutions for our communities; enhanced employee opportunities over time from a larger company; greater financial strength and stability; and the uniting of an experienced, capable leadership team. This acquisition positions the combined company as the largest Independent Telecommunications Provider and fourth largest telecommunications provider in the United States – based on access lines – serving 33 states with 7.5 million access lines.

In October CenturyTel agreed to acquire EMBARQ for approximately $5.8 billion in stock based on the October 24, 2008, closing price of CenturyTel's common stock and the assumption of approximately $5.8 billion of debt. EMBARQ traces its roots back to 1899, when Cleyson Brown formed the Brown Telephone Company in Abilene, Kansas. By 1991, the company was known as Sprint. In December, 2004, Sprint announced a merger with Nextel and its subsequent plan to spin off its Local Telecommunications Division (LTD) into an independent company. The spin-off, Embarq Corporation, was formed on May 17, 2006.

The Embarq deal was transformative, but what came next was even more ambitious.

The Qwest acquisition represented a fundamental shift in CenturyLink's identity. Qwest Communications International traced its lineage back to the 1910s as Mountain State Telephone and Telegraph Company, later known as Mountain Bell. After the breakup of AT&T in 1984, the company became US West—one of the original "Baby Bells." Then Qwest Communications, an up-and-coming fiber-optic network company, acquired the much larger US West in 2000, only to get into trouble with regulators during the telecom bust.

With the Qwest acquisition, the network footprint of CenturyLink surged, adding critical fiber-optic network assets. This expansion provided a competitive advantage in both metropolitan and rural markets, offering broader services beyond CenturyLink's pre-existing markets, including an additional 14 million customers across 14 states.

The acquisition of Qwest Communications in April 2011 for $12 billion transformed CenturyLink into the third-largest telecommunications company in the United States. But it also brought something even more valuable than customer count: fiber. Qwest's fiber network, built during the 1990s tech boom when capital flowed freely into infrastructure, gave CenturyLink access to enterprise customers and intercity routes that would prove invaluable decades later.

On May 2010, the new corporate name of the combined CenturyTel/Embarq entity became CenturyLink, Inc. On April 1, 2011, CenturyLink acquired Qwest Communications International, Inc., one of the largest United States telecommunications carriers, in a stock-for-stock transaction. The merger made CenturyLink owner of one of "Baby Bells": Qwest included what was once US West, a Baby Bell company break up from the Bell System in 1984.

This was the strategic logic of the Qwest deal: gain fiber assets, enterprise customers, and geographic diversification. But the debt burden began to accumulate. CenturyLink was building scale, but it was doing so with borrowed money. This would haunt the company for the next decade.

The Cloud Pivot That Wasn't: Savvis and Enterprise Ambitions (2011-2016)

In July 2011, just months after closing Qwest, CenturyLink made another bold move. The company acquired Savvis, Inc., a global provider of cloud infrastructure and hosted IT services, for $2 billion, representing $40 per share for all outstanding Savvis common stock. This acquisition allowed CenturyLink to provide expanded managed hosting and cloud services.

On July 15, 2011, CenturyLink acquired Savvis, Inc., a global provider of cloud infrastructure and hosted IT services. On October 16, 2012 Savvis acquired ITO Business Division of Ciber thereby adding managed services to the portfolio. On November 19, 2013, CenturyLink announced the acquisition of Tier 3, a Seattle-based infrastructure as a service (IaaS), platform, and advanced cloud management company.

In June 2013, Savvis acquired AppFog, a Portland-based Platform as a Service provider. In November, CenturyLink acquired Tier 3, a Seattle-based infrastructure as a service (IaaS) provider. However, Tier 3 became part of CenturyLink Cloud rather than Savvis—an early sign of the organizational complexity that would plague these cloud initiatives.

The vision was compelling: transform from "dumb pipes" to a managed services provider. Rather than competing purely on price for commodity bandwidth, CenturyLink would add value through hosting, cloud services, and managed security. This is the pivot every legacy telecom has attempted—and nearly all have failed.

Why do telcos struggle with cloud? The business models are fundamentally different. Telecommunications sells capacity on long-term contracts with stable margins. Cloud computing requires continuous innovation, rapid iteration, and software engineering capabilities that telecommunications companies historically lack. The cultures clash. The incentive structures conflict. And hyperscale competitors like Amazon Web Services and Microsoft Azure possess technical capabilities and scale that legacy telcos cannot match.

By 2016, the cloud strategy had stalled. CenturyLink's data center business was generating revenue but not the growth rates that would justify the capital invested. The enterprise services business was performing adequately but not transformatively. And meanwhile, the consumer business continued its inexorable decline as wireless substitution accelerated and cord-cutting spread from cable television to landline phones.

The company needed another transformation. And this time, it would bet the company.

The Level 3 Mega-Merger: Doubling Down on Enterprise (2016-2017)

Level 3 Communications, Inc. was an American multinational telecommunications and Internet service provider company headquartered in Broomfield, Colorado. It ultimately became a part of CenturyLink (now Lumen Technologies), where Level 3 President and CEO Jeff Storey was installed as Chief Operating Officer, becoming CEO of CenturyLink one year later in a prearranged succession plan. Level 3 operated a Tier 1 network. The company provided core transport, IP, voice, video, and content delivery for medium-to-large Internet carriers in North America, Latin America, Europe, and selected cities in Asia. Level 3 was also the largest competitive local exchange carrier (CLEC) and the 3rd largest provider of fiber-optic internet access (based on coverage) in the United States.

Level 3's history was everything CenturyLink was not. Where CenturyLink grew organically through patient acquisition of rural telephone companies, Level 3 was born from ambition and capital markets enthusiasm. From its beginning, Level 3 Communications was founded on the principles of the Silicon Economics cycle: create a global telecommunications network with the scale to reduce unit costs, stimulate demand with these lower costs, support that demand by scaling even more. Level 3 created a network that serves as a foundation for the communications services of the 21st century by providing, among other things, information transmission over a fiber optic network and media delivery over a content delivery network. Level 3 was originally founded in 1985 as Kiewit Diversified Group Inc. (KDG), a wholly-owned subsidiary of Peter Kiewit Sons', Inc. Peter Kiewit Sons', Inc. is a 114-year-old construction, mining, information services and communications company headquartered in Omaha, Neb.

In early 1998, KDG announced it was changing its name to Level 3 Communications, Inc., after substantially increasing the emphasis it placed on and the resources devoted to its communications and information services business. On April 1, 1998, Level 3 common stock started trading on the NASDAQ Stock Market under the symbol LVLT. During 1998, Level 3 raised $14 billion and was called the "best funded start-up in history." The company constructed 19,600 route miles, and built the world's first continuously upgradeable network fully optimized for internet protocol (IP). Over the next few years, explosive demand for bandwidth fueled growth in sales. By the end of 2000, Level 3 provided service to 2,700 customers.

Level 3's journey through the dot-com bust, multiple near-death experiences, and relentless consolidation of failed fiber companies had forged something valuable: a Tier 1 internet backbone with global reach, enterprise relationships, and—critically—network architecture built from the ground up for IP traffic rather than legacy voice services.

On October 31, 2016, CenturyLink announced an agreement to acquire Level 3 Communications in a cash and stock transaction. On October 31, 2016, CenturyLink announced its intent to acquire Level 3 in a deal valued at around $34 billion. On October 3, 2017, the deal was approved by the United States Department of Justice on condition of selling some of Level 3's telecom holdings in three states. The deal officially closed and Level 3 became part of CenturyLink on November 1, 2017.

The deal mechanics were complex. The purchase consideration comprised $26.5 per share in cash and a fixed exchange ratio of 1.4286 CenturyLink shares for each Level 3 share. Current CenturyLink shareholders would own approximately 51% and Level 3 shareholders approximately 49% of the combined company. CenturyLink intended to finance the cash portion through cash on hand at both companies plus approximately $7 billion of additional debt.

CenturyLink's network now connected more than 350 metropolitan areas with more than 100,000 fiber-enabled, on-net buildings, including 10,000 buildings in EMEA and Latin America.

The executives divided the company into "Growth", "Nurture", "Harvest" sections, which correspond to high, low, and very-low/negative margins. The goal was to move customers from Nurture to Grow products and to sell off the Harvest products. Landline sales continued to fall but Lumen focused on growing the profitable fiber services.

But the Level 3 deal also brought something else: even more debt. And in a prescient decision, On May 2, 2017, CenturyLink, Inc. completed the previously announced sale of its data centers and colocation business to funds advised by BC Partners for approximately $1.86 billion. The company was already trimming non-core assets to manage its leverage.

From CenturyLink to Lumen: A Rebrand for the Fourth Industrial Revolution (2020)

On September 14, 2020, CenturyLink announced that it had changed its name to Lumen Technologies, Inc. Effective with the opening of the trading day on September 18, 2020, the company stock ticker changed from CTL to LUMN.

The name change was more than cosmetic. "Lumen" refers to a measure of the brightness of light—a reference to the company's fiber optic network stretching 450,000 route miles. As Lumen Technologies, the company positioned itself to help enterprises navigate the Fourth Industrial Revolution, a time when smart, connected devices would be everywhere.

The rebrand divided operations into three brands: Lumen Technologies for enterprise services, CenturyLink for legacy consumer services, and Quantum Fiber for the company's fiber-to-the-premises residential offering. This structure reflected the reality that these three businesses had fundamentally different economics, growth trajectories, and capital requirements.

The timing was terrible. The rebrand launched into a pandemic-ravaged economy where enterprise IT spending was uncertain, consumer broadband demand was spiking (but with pressure on margins), and the company's debt load constrained investment in growth.

The Crisis Years: Debt, Dividend Cut, and Near-Death Experience (2020-2023)

The years 2020-2023 represented Lumen's darkest period. The financial situation deteriorated relentlessly. In 2023, the company reported annual revenue of $14.6 billion, continuing a downward trend that started in 2018. But the staggering net loss of $10.3 billion that year stood out the most, accounting for more than two-thirds of the company's revenue.

Then came the unthinkable. Lumen Technologies eliminated its dividend entirely in 2022, shocking investors who had owned the stock for decades specifically for its income stream. The company increased its free cash flow forecast but decided to replace its dividend with stock repurchases—a decision that satisfied no one. The news caused significant turbulence for Lumen's stock price, which fell 17% in response.

The dividend cut was a watershed moment. For generations, telephone stocks had been income investments. Widows and orphans, as the saying went, could rely on their phone company dividends. By eliminating the payout, Lumen was signaling that survival trumped tradition—that the cash was needed for debt service and transformation rather than shareholder distributions.

The asset sales accelerated. This led to the $2.7 billion sale of its Latin American business which was rebranded as Cirion. In 2023, a deal was signed with Colt Technology Services in which Lumen EMEA, its subsidiary serving the Europe, Middle East, and Africa enterprise markets, would be sold to Colt for $1.8 billion. The deal allows Lumen to continue serving multinational enterprise customers via Colt's infrastructure.

On August 3, 2021, Lumen announced it would sell its incumbent local exchange carrier (ILEC) operations in 20 states to Apollo Global Management for $7.5 billion. Lumen structured the deal to retain infrastructure in urban and suburban areas—which they still wanted to upgrade from copper to fiber—and sell off areas that they deemed unworthy of further investment.

The Louisiana-based company has been around a long time, so it was a surprise to some that the stock was at risk of being delisted from the New York Stock Exchange when in 2023, its price per share briefly dipped under $1.00. Those struggles continued into 2024, but by mid-summer, the stock surged when demand for its high-speed fiber-network solutions began to grow. The company secured deals with Microsoft Corp. and other leading tech companies that are requiring increased connectivity between their data centers because of the explosive growth of artificial intelligence.

Lumen shares entered July 2024 trading for $1.10 and emerged at $3.15. They were down 40% through the first half of 2024 after losing 65% in 2023 and 58% in 2022. The bullish AI story only matters if Lumen survives long enough to realize it. For most of 2023–2024, the company's $18 billion debt load was the dominant concern.

The AI Renaissance: How Microsoft Saved Lumen (2024-Present)

Then, suddenly, everything changed.

Today, Lumen Technologies (NYSE: LUMN) and Microsoft Corp. (NASDAQ: MSFT) announced a new strategic partnership that will use the Microsoft Cloud to further drive Lumen's digital transformation. In addition, Microsoft has chosen Lumen to expand its network capacity and capability to meet the growing demand on its datacenters due to AI.

The announcement on July 24, 2024, marked a turning point not just for Lumen but for the entire telecommunications industry. For years, fiber had been treated as a commodity—interchangeable capacity that customers could source from whoever offered the lowest price. The AI infrastructure buildout was revealing that fiber is anything but a commodity: routes matter, latency matters, and capacity is finite.

"When the world has talked about what's needed for AI, you usually hear about power, space and cooling…[these] have been the scarce resources," Lumen's CMO Ryan Asdourian told Fierce. "Now with demand increasing at an incredible rate, I think what Microsoft was finding and what others are finding is that that demand for fiber and the routes and the network capacity and capabilities, that's becoming the scarce resource right now."

The Microsoft partnership was built around Lumen's Private Connectivity Fabric (PCF), a custom network that includes dedicated access to existing fiber in the Lumen network, the installation of new fiber on existing and new routes, and the use of Lumen's new digital services. This AI-ready infrastructure would strengthen connectivity capabilities between Microsoft's datacenters by providing the network capacity, performance, stability, and speed that customers need as data demands increase.

Two weeks later, on August 5, 2024, Lumen dropped the real bombshell. Lumen Technologies announced it has secured $5 billion in new business driven by major demand for connectivity fueled by AI. Large companies across industry sectors were seeking to secure fiber capacity quickly, as this resource was becoming increasingly valuable and potentially limited due to booming AI needs. Lumen was in active discussions with customers to secure another $7 billion in sales opportunities.

Following the announcement, shares of LUMN surged 46.7% in pre-trading on August 6th.

The company signed about $1 billion of new PCF deals in October alone, largely with a single major client. Total PCF contract value has climbed above $10 billion across roughly 15–16 customers, including hyperscalers and large enterprises. However, much of that PCF revenue will not be recognized until late fiscal 2028 and beyond, given multi-year deployment cycles.

"Lumen is building the backbone for the AI economy," CEO Kate Johnson said to investors in November. "The market now recognizes that AI needs data, data needs data centers, and those data centers need to be connected. And several of the biggest names in technology, including Microsoft, Meta, AWS, and Google have chosen Lumen as their trusted network for AI."

The strategic implications were profound. The Lumen deal will allow Microsoft to tap into Lumen's network technologies to help it support the massive growth of AI workloads in its cloud. Lumen, which counts Zoom and Amazon Web Services among its customers, offers over 6 million miles of fiber-optic cables via its Private Connectivity Fabric solution, as well as dedicated network access, under 5 milliseconds of latency at the edge, and 60 percent more capacity compared to legacy fiber.

Kate Johnson: The Change Agent Who Bet on Transformation

No understanding of Lumen's AI pivot is complete without understanding Kate Johnson. Joining Lumen Technologies in November 2022, Kate Johnson took on the role of Chief Executive Officer. Since then, she has been leading the company with her extensive experience in the technology sector.

From 2017-2021 Ms. Johnson served as President of Microsoft U.S. a division of Microsoft Corporation. From 2013-2017 she held various senior positions at GE Digital including Executive Vice President and Corporate Officer. She served as the Senior Vice President for North America Technology and Government Consulting at Oracle from 2007-2013 and as the Vice President of Global Services and Strategic Accounts for Red Hat from 2004-2007.

As the first female CEO in Lumen's history and one of just 52 women CEOs of Fortune 500 companies as of 2024, Johnson is a trailblazer in her industry. She believes in leading with courage and empathy, embracing change and approaching her work with a learn-it-all mentality. She has helped launch and lead change programs at several Fortune 500 companies.

Johnson's Microsoft background proved directly relevant to Lumen's AI pivot. Afterall, it is one of a handful of leaders in the AI realm, and it doesn't hurt that Lumen's CEO Kate Johnson is a former Microsoft exec. Her relationships, her understanding of hyperscaler needs, and her credibility with enterprise technology buyers gave Lumen an inside track that few competitors could match.

"The culture was play not to lose, and that was very Telco. So Telco, you know, old, copper infrastructure declining, no innovation. Preserve, preserve. He who dies last wins. So you play not to lose. You don't want to lose customers, you don't want to lose any money. You harvest the cash to pay the dividend. And my assignment from the board was completely different. We want you to pivot the company to growth and leverage this fiber asset."

Johnson's mandate was transformation, not preservation. "Think of my role as an instigator. I'm a catalyst," Johnson says. "I come in and I say, 'Hey, what got us here isn't going to get us where we need to go, so we need to change things.'"

The AT&T Deal: Sharpening Focus on Enterprise

In May 2025, Lumen announced the logical culmination of its enterprise-first strategy. Lumen confirmed it is selling its Mass Markets fiber-to-the-home business to AT&T for $5.75 billion in cash.

"We are sharpening our focus on enterprise customers and this transaction enhances our financial flexibility, enabling us to reimagine networking for enterprises in a multi-cloud, AI-first world," said Kate Johnson, President and CEO, Lumen. "As part of this deal, we are retaining the core infrastructure that allows us to continue innovating for enterprise customers, leap frogging traditional networking architectures to give customers the bandwidth, performance and security they need."

AT&T will acquire approximately 95% of Lumen's Quantum Fiber business, which consists of nearly 1 million subscribers and about 4 million passings across 11 states. Lumen will retain the assets that serve "as the foundation of its enterprise transformation," including all national, regional, state, and metro level fiber backbone network infrastructure, along with central offices and associated real estate. The operator will also keep and maintain its existing copper network that services consumers.

The financial impact was substantial. Upon closing, Lumen intends to use the net proceeds of approximately $4.2 billion and cash on hand to pay down approximately $4.8 billion in superpriority debt, reducing our interest expense by approximately $300 million annually.

Based on projected 2025 aEBITDA guidance, Lumen's net debt to aEBITDA ratio will be reduced from 4.9x to 3.9x. The transaction is expected to reduce Lumen's Mass Markets fiber-related capital expenditures by approximately $1 billion annually, enhancing cash flow and enabling Lumen to accelerate investments in the Company's enterprise offerings and further strengthen the balance sheet.

Following the $8.5 billion in AI-driven networking contracts with hyperscalers, Lumen plans to expand its vast nationwide footprint, scaling to 47 million intercity fiber miles by 2028. In addition, the Company will continue to scale the Lumen Digital platform to simplify customer experiences for businesses seeking quick, secure, effortless networking services.

Current Business Model: The Backbone of the AI Economy

Lumen Technologies today operates as a global communications services provider with a fundamentally different value proposition than it had five years ago. The company serves everyone from big businesses to households, split across two main segments: Business Solutions (edge cloud, cybersecurity, managed networks, unified communications, and dark fiber) and Mass Markets (voice, broadband, and data services to consumers and small businesses).

The primary driver behind last 12 months revenue was the Business segment contributing a total revenue of US$10.4b (79% of total revenue). Notably, cost of sales worth US$6.70b amounted to 51% of total revenue thereby underscoring the impact on earnings.

The Private Connectivity Fabric (PCF) represents Lumen's most strategically important product. Speaking on the Q3 earnings call, Lumen CEO Kate Johnson said the company expects its existing PCF contracts to generate a recurring revenue stream of $400-500 million by end of 2028. Aiming to further its enterprise AI reach, Lumen in the quarter inked a multi-year partnership with Palantir, "where we not only agreed to buy services from each other, but we committed to bring those capabilities to joint customers," Johnson added. Lumen will reportedly spend over $200 million on Palantir software over the next several years.

Lumen has now signed over $10B in PCF deals. Neoclouds are now in the mix alongside hyperscalers, said CFO Chris Stansbury. Most of Lumen's PCF customers thus far have been hyperscalers. But it's starting to get traction in the neocloud space, CFO Chris Stansbury told Fierce. Neoclouds are a new breed of cloud providers that focus on offering GPU-as-a-service for AI applications. Think companies like CoreWeave, Lambda and Nebius, though Stansbury declined to share any customer names. "I would simply say neocloud is now part of that mix," he said.

Lumen maintains and operates dark fiber within the United States for the Department of Defense, contracting announcements indicate. This is a continuation of CenturyLink's work.

Network services include SD-WAN, MPLS/IPVPN, hybrid WAN, Ethernet, Internet access, wavelength services, dark fiber, and private lines. On the security front, Lumen Security monitors more than a billion security events daily, offering cloud, infrastructure, DDoS, web application, email, and web security, along with analytics, threat management, and risk compliance support.

Financial Reality Check: The Path to Profitability

The optimism surrounding Lumen's AI pivot must be tempered by financial reality. In 2024 the company made a revenue of $13.10 Billion USD a decrease over the revenue in the year 2023 that were of $14.55 Billion USD. Lumen Technologies annual revenue for 2024 was $13.108B, a 9.95% decline from 2023. Lumen Technologies annual revenue for 2023 was $14.557B, a 16.71% decline from 2022.

Revenue has declined for seven consecutive years. The PCF contracts are transformative, but LUMN has secured over $10 billion in PCF contracts, but revenue growth from these deals is not expected until late FY28, while legacy business declines persist.

"We made material progress strengthening our financial position, transforming our corporate functions, and building the backbone for the AI economy," said Kate Johnson, president and CEO of Lumen.

Lumen Technologies long term debt for the quarter ending June 30, 2025 was $17.565B, a 4.6% decline year-over-year. Lumen Technologies long term debt for 2024 was $17.494B, a 11.78% decline from 2023. Lumen Technologies long term debt for 2023 was $19.831B, a 2.87% decline from 2022.

The debt burden remains the company's central vulnerability. High Debt Levels Persist: Total long-term debt remains substantial at $17.9 billion, with interest expense increasing 18% YoY to $1.4 billion, consuming a significant portion of operating income and limiting financial flexibility.

Reported Net Loss of $(621) million for the third quarter 2025, compared to reported Net Loss of $(148) million for the third quarter 2024. $2.4 billion debt refinancing, term loan repricing, and further debt reduction, saving $135 million in annual interest expense year to date.

Competitive Landscape: Porter's Five Forces Analysis

Supplier Power: Moderate We're building new routes funded by our customers, often multi-tenant, with great economics. We're partnering with Corning to use their latest fiber innovations, allowing us to get as much as four times more capacity from existing and new routes. Lumen's exclusive supply agreement with Corning for next-generation fiber gives it some protection, but networking equipment vendors retain significant leverage.

Buyer Power: High and Growing AT&T and Verizon are primary competitors, offering extensive network services, cloud connectivity, and managed solutions. These companies have substantial financial resources and established customer bases. They often compete directly with Lumen Technologies for major enterprise contracts. Hyperscalers like Microsoft, Amazon, and Google are sophisticated buyers with enormous leverage. However, Lumen's first-mover advantage in AI infrastructure connectivity may reduce buyer power temporarily.

Threat of Substitutes: Moderate While fiber remains the gold standard for high-bandwidth, low-latency connectivity, wireless alternatives (5G, satellite) continue to improve. For AI workloads requiring massive data throughput between data centers, however, fiber has no practical substitute at current technology levels.

Threat of New Entrants: Low Building fiber networks requires billions in capital, years of construction time, and rights-of-way that are difficult to secure. Lumen's existing infrastructure represents decades of accumulated investment that new entrants cannot easily replicate.

Competitive Rivalry: Intense AT&T led Vertical Systems Group's Year-End 2024 U.S. Business Fiber Lit Buildings Leaderboard for the ninth consecutive time. And AT&T's fiber presence is set to expand significantly with the acquisition of the mass markets fiber business of Lumen, which sits no. 5 on the board. The enterprise fiber market features well-capitalized competitors with overlapping capabilities. Lumen remains in second position based on port share. Verizon, Comcast Business and Cox Business also held onto their top Ethernet market share, according to Vertical Systems Group's 2023 U.S. Carrier Ethernet LEADERBOARD. To qualify for a LEADERBOARD ranking, these providers each have a four percent or more share of the U.S. retail Ethernet services market.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Lumen benefits from scale in network operations—more fiber miles allow fixed costs to be spread across greater capacity. However, competitors like AT&T and Verizon have even greater scale in aggregate.

Network Effects: Limited. Unlike platforms where users attract more users, fiber networks don't inherently become more valuable with additional customers. However, Lumen's ecosystem of hyperscaler partnerships may create indirect network effects as customers seek connectivity to the same partners.

Counter-Positioning: This is Lumen's strongest power. By divesting consumer operations and focusing entirely on enterprise AI infrastructure, Lumen has adopted a strategy that AT&T and Verizon—with their wireless businesses, consumer broadband, and content assets—would find difficult to fully replicate. "One of the things that really differentiates us right now is our focus on fiber as part of the core infrastructure to an edge experience versus a distraction with 5G or content," a Lumen executive said. "And being able to look an enterprise in the eye and say 'Not only do we have these capabilities, but we will build the fiber to you where you are.' That resonates with customers, and I think that's a differentiator."

Switching Costs: Moderate to high for PCF customers who have made long-term commitments. Once a hyperscaler builds workflows around Lumen's infrastructure, switching imposes real costs.

Branding: Weak. Lumen is not a consumer brand, and enterprise buyers make decisions based on capability and price rather than brand affinity.

Cornered Resource: Lumen's existing fiber routes—particularly intercity connections built decades ago—represent a cornered resource. Rights-of-way cannot easily be duplicated, and existing dark fiber is available for immediate activation.

Process Power: Uncertain. Whether Lumen can develop superior operational processes for building and managing AI-optimized networks remains to be proven.

Bull Case: The New Infrastructure Monopoly

The bull case for Lumen rests on three arguments:

1. AI Infrastructure Scarcity The AI buildout requires connectivity between data centers on a scale never before attempted. Lumen plans to increase its total inter-city fiber miles from 12 million in 2022 to 47 million by 2028, driven by new routes and innovative fiber solutions. The company expects network utilization to increase from 57% to 70% by 2028, with hyperscalers funding new builds and enterprise upgrading networks. If AI demand continues to accelerate, fiber may prove to be the true bottleneck—and Lumen is positioned as a critical supplier.

2. Financial Turnaround The AT&T transaction and PCF prepayments are rapidly deleveraging the balance sheet. CEO Kate Johnson projected the company's return to growth by 2029. With our 2025 investments and further execution on our modernization and simplification goals, we have confidence in margin expansion and total EBITDA returning to full year growth in 2026 and growing thereafter.

3. Enterprise Focus By shedding consumer operations, Lumen can allocate all capital and management attention to higher-margin enterprise business. The company aims for $1 billion in cost savings by the end of 2027 and expects to achieve run-rate cost savings exceeding $250 million by the close of 2025. Lumen anticipates returning to full-year EBITDA growth in 2026.

Bear Case: The Problems That Won't Go Away

The bear case is equally compelling:

1. Revenue Decline Hasn't Stopped Total Revenue was $3.087 billion for the third quarter 2025, compared to $3.221 billion for the third quarter 2024. Legacy revenue continues to decline faster than new business is growing. The PCF revenue recognition is years away.

2. Debt Remains Dangerous LUMN has secured over $10 billion in PCF contracts, but revenue growth from these deals is not expected until late FY28, while legacy business declines persist. Leverage remains a key risk, with net debt/EBITDA at 7.6x; planned divestitures may reduce this, but EBITDA interest coverage ratios may remain under pressure. LUMN trades at a rich EV/EBITDA multiple, and the stock's recent rally is driven by multiple expansion despite declining EBITDA expectations, which is indicative of hype.

3. Competition Is Intensifying The carrier isn't the only one pushing hard on fiber, with rivals Verizon and T-Mobile also carving out several deals in this space. Earlier this week, the Federal Communications Commission approved Verizon's $20 billion acquisition of Frontier Communications. Every major telecom is investing in fiber, and hyperscalers have the capital to build their own networks if supplier pricing becomes unreasonable.

4. Execution Risk Transformations of this magnitude frequently fail. Intense Competition and Pricing Pressure: Lumen faces intense competition across all segments. Competitive pricing pressure and technological shifts, especially in broadband (cable, wireless, satellite), necessitate continuous innovation and network upgrades to maintain market share and profitability.

Key Performance Indicators to Watch

For investors tracking Lumen's transformation, three KPIs matter most:

1. PCF Revenue Recognition Management guidance suggests $400-500 million in recurring PCF revenue by end of 2028. Quarterly updates on construction progress, contract milestones achieved, and revenue recognition timing will reveal whether this projection is realistic. Watch for any slippage in customer deployment schedules or contract renegotiations.

2. Net Debt to EBITDA Ratio Based on projected 2025 aEBITDA guidance, Lumen's net debt to aEBITDA ratio will be reduced from 4.9x to 3.9x. The AT&T deal should improve this ratio materially. Any failure to reduce leverage per the stated plan—or unexpected EBITDA compression—would be a significant warning sign.

3. Enterprise Segment Revenue Growth Rate The core thesis requires enterprise revenue to stabilize and eventually grow. While legacy products will continue to decline, "Grow" products (including PCF) must demonstrate acceleration. The ratio of Grow to Harvest revenue is the key metric for tracking the business mix transformation.

Regulatory and Legal Considerations

Investors should note several material overhangs:

Antitrust Review of AT&T Transaction: The transaction is expected to close in the first half of 2026, subject to any necessary approvals and closing conditions. While approval seems likely given AT&T's fiber-market position post-deal remains smaller than Verizon's, regulatory delays could impact timing and financial planning.

Pension Obligations: The company has pension and post-retirement benefit plans that are significantly underfunded by $645 million and $1.7 billion, respectively. These obligations represent real future cash requirements that could pressure free cash flow.

Customer Concentration: With $10+ billion in PCF contracts concentrated among 15-16 customers—predominantly hyperscalers—revenue is increasingly dependent on the capital spending decisions of a small number of technology giants. Any pullback in AI infrastructure investment would disproportionately impact Lumen.

The View from Monroe

Step back and consider the improbability of what has happened. A company born as a 75-subscriber telephone exchange in rural Louisiana—one that changed hands for $500 in 1930—now stands at the center of the most transformative technology shift since the internet itself.

The story of Lumen Technologies is, in many ways, the story of American telecommunications: consolidation and reconsolidation, debt-fueled growth and painful deleveraging, legacy businesses that decline and new opportunities that emerge. It is a story of patient capital meeting technological disruption, of infrastructure that seemed obsolete becoming suddenly essential.

Whether Kate Johnson's bet pays off depends on variables no one can predict with certainty. Will AI infrastructure demand continue to accelerate? Will Lumen execute its transformation before legacy revenue declines consume the company? Will competitors build sufficient alternative capacity to commoditize what Lumen is selling as a differentiated service?

Lumen is really the backbone of the AI economy. That's the way I think about it. That assessment may prove prophetic—or premature. But this much is clear: the fiber optic cables that Lumen accumulated over decades of acquisitions, the network routes built by Level 3 during the dot-com boom, the infrastructure inherited from US West and Qwest and Century Telephone—all of it has suddenly become valuable in ways that seemed impossible just two years ago.

The telecom industry has a saying: "No one ever got fired for choosing AT&T." Lumen is betting that in the AI era, that conventional wisdom is about to change. The hyperscalers have chosen Lumen as their trusted network for AI—and in doing so, they may have breathed new life into a company that many had written off for dead.

The phoenix, it seems, is rising from the ashes. Whether it can stay aloft remains the essential question.

Note: This analysis is for informational purposes only. Lumen Technologies faces significant risks including substantial debt obligations, ongoing revenue decline in legacy businesses, competitive pressure from larger telecommunications providers, and execution risk in its enterprise transformation strategy. The company's stock has experienced extreme volatility and carries correspondingly high risk.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube