Equity LifeStyle Properties: America's Landlord of the Unconventional

I. Introduction: The Hidden Empire in Plain Sight

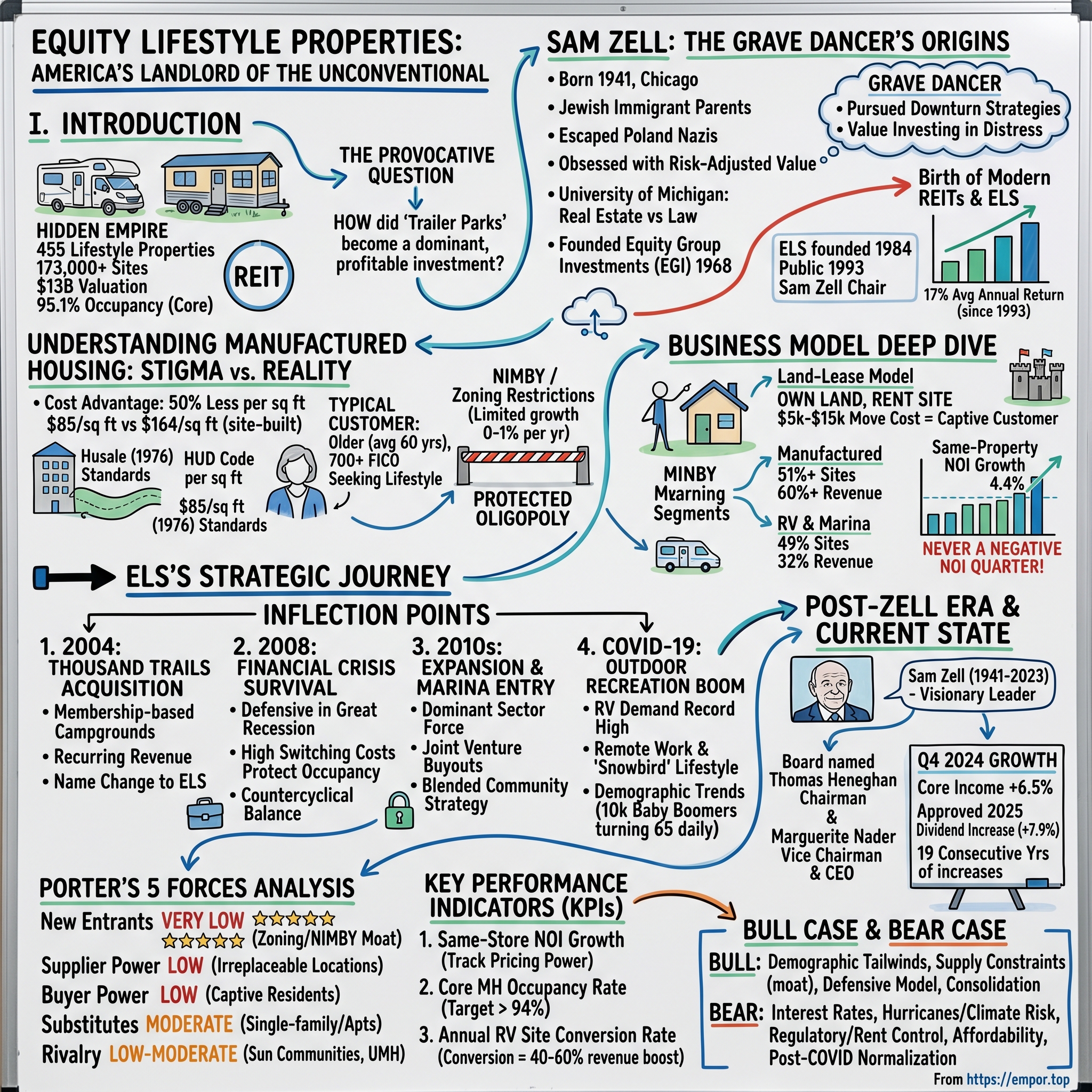

Picture this: A retired couple pulls their gleaming RV into a sun-drenched Florida resort, greeted by manicured streets, a sparkling pool, and neighbors waving from golf carts. Across the country, a young family excitedly tours their first manufactured home in a lakeside community, finally able to afford the American Dream of homeownership. In both cases, these residents are about to become customers of one of America's most quietly dominant real estate empires—one that most investors have never heard of, yet one that has outperformed nearly every other property type for over two decades.

Equity LifeStyle Properties, Inc.—known simply as ELS—operates as a real estate investment trust managing 455 lifestyle-oriented properties across the United States, encompassing 173,340 sites as of April 21, 2025. This Chicago-based company has achieved something remarkable: it has transformed an asset class once dismissed as "trailer parks" into one of the most coveted real estate investments in America.

As a prominent real estate investment trust valued around $13 billion, ELS showcases remarkable stability, achieving a core community base occupancy rate of 95.1% as reported in early 2024. That occupancy figure alone tells a story—in an industry where 90% occupancy is considered excellent, ELS consistently operates at near-capacity, year after year, recession after recession.

The provocative question at the heart of this story: How did an asset class that carries perhaps the most powerful pejorative in American housing—"trailer park"—become one of the most defensive, profitable, and demographically-advantaged real estate plays available to public market investors?

The answer lies at the intersection of several powerful forces: a contrarian investment philosophy pioneered by a legendary dealmaker, a REIT revolution that transformed how Americans invest in real estate, demographic tailwinds that will persist for decades, and structural supply constraints that virtually guarantee pricing power for incumbents. This is the story of how Sam Zell saw what others dismissed, how manufactured housing defied its stigma, and why ELS may represent one of the most misunderstood compounding machines in public markets.

II. Sam Zell: The Grave Dancer's Origins

To understand Equity LifeStyle Properties, one must first understand the man who built it. Samuel Zell (born Shmuel Zielonka; September 28, 1941 – May 18, 2023) was an American billionaire businessman and philanthropist primarily engaged in real estate investment.

But the story begins not in Chicago's gleaming office towers, but in the shadows of history's darkest chapter.

Zell was born on September 28, 1941, in Chicago. His parents, Ruchla, later Rochelle, and Berek, later Bernard, Zielonka, were Jews who immigrated from Poland four months before his birth to escape the Invasion of Poland by the Nazis. In Poland, his father was a grain trader. They immigrated to the United States with their young daughter, Leah, via Russia and Tokyo, pretending to be tourists at the Bolshoi Ballet so as not to stand out. They then moved from Seattle to Albany Park, Chicago, where his father became a wholesale jeweler who also made successful investments in real estate and the stock market.

This origin story—escaping Europe's horrors by mere months, arriving in America with nothing, rebuilding through shrewd investment—would shape Zell's entire worldview. He developed an obsession with risk-adjusted value, a contrarian streak that bordered on defiance, and an almost preternatural ability to see opportunity where others saw only distress.

The entrepreneurial instincts emerged early. In eighth grade, Zell took pictures at his prom and sold them. He later bought Playboy magazines in downtown Chicago and resold them to his classmates in Hebrew school for a 200% markup. When he was twelve, the family moved to Highland Park, Illinois, where he graduated from Highland Park High School.

At the University of Michigan, Zell discovered his true calling. While in school, Zell managed a 15-unit apartment building in return for free room and board. By the time of his graduation, he was managing several properties and was netting $150,000. Joined by his fraternity brother Robert H. Lurie, he won a contract with a large apartment development owner in Ann Arbor.

$150,000 in 1963 was roughly equivalent to over $1.5 million today—earned by a college student managing apartments. The young Zell had stumbled onto something profound: real estate wasn't just about buildings; it was about operating businesses that happened to involve physical structures.

In 1966, he graduated with a J.D. from the University of Michigan Law School. By that time, he and Lurie were managing over 4,000 apartments and owned 100–200 units outright.

The law career lasted precisely one week. After graduation, Zell worked as a lawyer for one week before deciding that the legal profession was not for him. With funding from one of the senior partners, Zell purchased a 99-unit apartment building in Toledo. In 1967, he purchased a profitable apartment complex in Reno, Nevada.

In 1968, Sam founded Equity Group Investments (EGI), a private investment firm headquartered in Chicago. A year later, Bob joined him as a partner at EGI.

But it was the economic turmoil of the early 1970s that forged Zell's legendary reputation. Zell's reputation for pursuing a robust investment strategy during industry downturns earned him the nickname, "the grave dancer." While others fled distressed properties and bankruptcies, Zell saw opportunity—not vulture investing, but value investing applied to real estate.

The 1973–1975 recession provided his proving ground. While lenders were desperate to avoid foreclosing on troubled properties (which would have forced them to recognize massive losses), Zell offered creative solutions. He would take over properties for almost nothing, provide realistic financial plans that enabled lenders to eventually be repaid, and then apply his operating expertise to turn around the assets. Both sides won—lenders avoided catastrophic write-offs, and Zell accumulated a portfolio at cents on the dollar.

This "grave dancing" philosophy would inform everything that followed. Zell didn't seek distress for its own sake; he sought mispriced assets where his operational expertise could unlock value that others couldn't see. And in the early 1980s, he turned his attention to an asset class that virtually everyone else dismissed: manufactured housing communities.

III. The Birth of Modern REITs & ELS

In 1984, Zell founded Equity Lifestyle Properties. It owns more than 400 trailer parks or mobile home parks.

That simple Wikipedia description obscures a revolutionary insight. Zell recognized that manufactured housing communities possessed characteristics that made them potentially superior investments to traditional apartment buildings or office towers—if you could overcome the stigma.

Consider the business model's structural advantages: In a manufactured housing community, the resident owns the home but rents the land beneath it. Moving a manufactured home costs $5,000 to $15,000 or more, making tenant turnover extraordinarily rare. Once a resident places their home on a site, they effectively become a captive customer for life. This creates pricing power that landlords of apartments or single-family rentals can only dream of.

The company traces its origins back to the late 1960s, but the modern entity, largely shaped by Sam Zell, began consolidating properties.

The company took its current form leading up to its public offering. Equity LifeStyle Properties (NYSE: ELS), the manufactured housing and resort REIT Zell founded and still chairs, is the largest public REIT in its sector and has generated an average 17 percent return since going public in 1993.

That 17% average annual return since 1993 is staggering. Across more than three decades—encompassing the dotcom bubble, the 2008 financial crisis, and the COVID pandemic—ELS delivered returns that rival the greatest growth stories in business history. A $10,000 investment at the 1993 IPO would be worth roughly $1.5 million today.

Chicago-based Equity LifeStyle Properties became a public company in 1993 with a portfolio of 41 manufactured home communities. For many years, the company's core business consisted of retirement communities in Sunbelt destinations—exactly the locations where Baby Boomers would eventually flock as they entered retirement.

Although his investments spanned industries across the globe, he was most widely recognized for his critical role in creating the modern real estate investment trust (REIT), which today is a more than $4 trillion industry.

The REIT structure was crucial. By organizing as a Real Estate Investment Trust and distributing at least 90% of taxable income to shareholders, Zell's vehicles avoided corporate-level taxation and passed through the economics of real estate ownership directly to investors. This structure, which Zell championed and popularized in the 1990s, allowed individual investors to participate in the ownership of large, income-producing real estate portfolios for the first time.

Back in the early 1990s when most of the traditional sources of capital for the real estate industry had dried up, the public capital markets were the only place to turn. But, in order for the modern REIT era to take hold, real estate's Wild West reputation had to change.

Zell's contribution wasn't just capital formation—it was governance. He insisted on transparency, aligned management incentives with shareholders, and built professional organizations that operated more like institutional-quality businesses than family fiefdoms. This reputation for shareholder-friendly governance became a competitive advantage in attracting capital.

The company established its headquarters in Chicago, Illinois, reflecting the base of its chairman. But its properties spread across the Sun Belt—Florida, Arizona, California, Texas—wherever retirees sought warm weather, low costs, and lifestyle-oriented communities. This geographic focus would prove prescient as America aged.

IV. Understanding Manufactured Housing: The Stigma vs. Reality

Perhaps no asset class in American real estate carries heavier baggage than manufactured housing. The term "trailer park" conjures images of rural poverty, crime, and transience—stereotypes reinforced by decades of popular culture. This stigma has created one of the most persistent mispricings in real estate: an asset class with exceptional fundamentals that most investors refuse to even consider.

The reality couldn't be more different.

Manufactured housing is one of the most affordable options for Americans to achieve the American dream of home ownership. New manufactured homes cost an average of $85 average price per square foot, compared with $164 per square foot for a single-family site-built home. Although manufactured homes cost 50% less per square foot to build than site-built homes, manufactured homes often include open floor plans and interior finishes that are indistinguishable from site-built interiors.

That cost advantage—roughly 50% less per square foot—isn't the result of inferior materials or construction. It flows from the fundamental economics of factory production. Unlike traditional site-built housing, where construction materials are brought to a site and assembled, factory-built housing is assembled in a factory, then shipped to a site and installed. Manufactured housing is a specific type of factory-built housing that meets national standards set by the Department of Housing and Urban Development (HUD), known as the HUD Code.

The HUD Code, established in 1976, transformed manufactured housing from the rickety trailers of earlier decades into genuinely high-quality homes. The Department of Housing & Urban Development has regulated and ensured standards for manufactured housing since 1976. All manufactured homes must meet this code. The performance code involves every aspect of the home including heating and air conditioning, fire safety, plumbing, electrical systems, structural design, construction, energy efficiency and even the transportation from factory to site. Today's manufactured homes are built to a standard of safety comparable to, and in some cases exceeding, standards for site-built housing.

For ELS's typical customer, the economics are compelling. In 2023, the average upfront cost for a manufactured home was approximately $127,000 with a monthly cost of about $797. Compare that to an average single-family home requiring approximately $106,000 as a 20% down payment on a $528,000 home, but carrying monthly costs of roughly $2,600. On a per-square-foot basis, manufactured home owners pay 25%-30% less.

The customer profile defies stereotypes. Typical manufactured housing customers of Equity LifeStyle are older—new home buyers average near 60 years old—with excellent credit scores (700+ FICO). These are often retirees who have sold traditional homes, accumulated equity, and are choosing manufactured housing communities for the lifestyle, not because they can't afford alternatives.

The stigma problem persists partly because regulatory barriers actively reinforce it. There is a growing trend of municipalities trying to use zoning and other land use regulations to restrict or eliminate manufactured housing in their jurisdictions. These actions could reduce the supply of critically-needed affordable housing for working families across the country and may be discriminatory under the Fair Housing Act.

Building new manufactured housing communities in moderately high-value areas is notoriously difficult, a function of local politics and restrictive zoning regulations. The total supply of manufactured housing sites is estimated to have grown at a rate of 0-1% per year over the past decade, compared to 1-2% per year supply growth in the major real estate sectors.

This regulatory hostility creates something remarkable: a near-impenetrable barrier to competition. Every restriction on new manufactured housing development enhances the value of existing communities. NIMBY ("Not In My Back Yard") opposition, originally intended to exclude manufactured housing, inadvertently created a protected oligopoly for incumbent operators like ELS.

Manufactured homes provide a cost-effective housing solution, particularly in rural areas where the transportation and material costs for site-built homes can be significantly higher. However, restrictive zoning laws often limit their placement in urban areas. Regulations such as bans on manufactured home communities and large lot size requirements can substantially increase costs, making it difficult to establish manufactured housing in cities. Reducing these zoning barriers could not only expand affordable housing options in high-cost urban areas but also improve access to essential services.

The irony is profound: an asset class stigmatized for housing lower-income Americans has become increasingly important as housing affordability has deteriorated nationwide. More than 22 million Americans currently live in manufactured housing. Manufactured housing units account for approximately 7 percent of occupied housing stock nationwide and 15 percent in rural areas. Manufactured housing is also the largest source of unsubsidized affordable housing in the country, making it a crucial piece of the nation's affordable housing stock.

For investors, the stigma creates opportunity. Because many institutional investors refuse to consider manufactured housing due to reputational concerns, the asset class trades at lower multiples than its fundamentals warrant. This persistent mispricing has been a source of alpha for contrarian investors willing to look past the pejorative.

V. The Business Model Deep Dive

The genius of ELS's business model lies in its elegant simplicity: own the land, let others own the depreciating asset (the home), and collect stable rent with embedded pricing power.

Equity LifeStyle Properties generates income primarily through the ownership and operation of manufactured home communities and recreational vehicle (RV) resorts across the United States and Canada. The company leases sites to residents who own their homes but rent the land, providing a stable revenue stream.

This "land-lease" model creates asymmetric economics heavily favoring the landlord. When a resident purchases a manufactured home and places it on an ELS site, the cost of moving that home elsewhere—typically $5,000 to $15,000—creates enormous switching costs. The resident effectively becomes a captive customer. Unlike apartment renters who can simply not renew their lease, manufactured home owners face the prospect of expensive relocation or outright loss of their home's value if they leave.

The portfolio breaks down into distinct segments:

Manufactured Housing (MH): The MH segment represents over 51% of total available sites and annual MH revenues constitute over 60% of property operating revenues. Since 2000, annual rate increases in the MH portfolio have averaged approximately 3.9%—consistent, predictable pricing power that compounds over decades.

The lease structures are particularly favorable. A quarter of the company's MH leases are linked to CPI growth, with half directly linked to CPI and the other half containing price increase floors of 3%. The remaining 75% of leases are market-driven, giving management flexibility to capture market rents as conditions change.

RV and Marina: The RV and Marina segment represents 49% of total available sites, and RV and marina revenues comprise 32% of property operating revenues. This segment operates differently than MH, with customers choosing among annual, seasonal (up to 6 months), or transient memberships.

The company's strategy focuses on converting transient RV customers to seasonal, then eventually to annual memberships. While the effective daily rate for annual memberships is lower than seasonal or transient, the occupancy rates are dramatically higher. Based on comparable data, occupancy rates for transient customers run roughly one-third that of annual customers. A successful conversion to annual membership results in a 40%-60% increase in revenues after the first year.

Annual RV rents average close to $500 per month, while transient rents run approximately double that on an effective daily basis. The stability of annual customers justifies the lower rate—ELS trades some upside for dramatically reduced volatility and more predictable cash flows.

Home Ownership Economics: Most of the company's MH customers own their home, with just 4% renting in 2022. This percentage has declined from 9% in 2013. The trend toward homeownership benefits ELS because homeowners have higher credit quality, lower turnover, and stronger community ties than renters. The company actively encourages rental-to-ownership conversions through new and used home sales programs.

Its portfolio features 203 manufactured home communities with 75,000 sites, 226 RV resorts and campgrounds with 91,000 sites (including 34,000 annual), and 23 marinas with 6,900 slips. These niche properties produce very resilient net operating income (NOI). For example, since 1998, Equity LifeStyle has grown its same-property NOI by an average of 4.4% per year. That's higher than the REIT sector average (3.3%) because its properties have performed much better during recessionary periods (it has never posted a quarter of negative NOI growth).

That last statistic deserves emphasis: ELS has never posted a quarter of negative NOI growth. Across the tech bust, the financial crisis, and the pandemic, the company maintained positive growth every single quarter. This defensive quality, combined with mid-single-digit growth, creates a compounding machine with remarkable consistency.

VI. Inflection Point #1: The 2004 Strategic Pivot & Thousand Trails Acquisition

By 2004, Equity LifeStyle Properties had established itself as the leading manufactured housing REIT. But CEO Thomas Heneghan and Chairman Sam Zell saw an opportunity to expand into a complementary asset class that would transform the company's strategic profile: membership-based campgrounds.

On November 10, 2004, Manufactured Home Communities, Inc. (NYSE:MHC) announced the acquisition of the entity that owns 57 properties and approximately 3,000 acres of vacant land. The purchase price was $160 million. These properties will be leased by Thousand Trails Operations Holding Company, L.P. (Thousand Trails), the largest operator of membership-based campgrounds in the United States. The Company has provided the long-term lease of the real estate (excluding the vacant land) to Thousand Trails, which will continue to operate the properties for the benefit of its approximately 108,000 members nationwide. The properties are located in 16 states (primarily in the western and southern United States) and British Columbia, and contain 17,911 sites.

Founded in 1969 with the purchase of 640 acres in Chehalis, Washington, Thousand Trails has become one of the largest networks of RV resorts and campgrounds in North America.

The Thousand Trails acquisition was transformative for several reasons. First, it diversified ELS's revenue base beyond manufactured housing into the rapidly growing RV and outdoor hospitality sector. Second, it introduced a membership model that created recurring revenue and customer lock-in. Third, it provided access to desirable vacation destinations that complemented the company's existing Sun Belt retirement focus.

The lease will generate $16 million in rental income to the Company on an absolute triple net basis, subject to annual escalations of 3.25%. The initial term of the lease is 15 years, with two five-year renewals.

The deal structure was elegant: ELS acquired the real estate while leasing it back to Thousand Trails' operator on a triple-net basis. This provided stable, escalating income while the operator continued managing day-to-day campground operations. The 3.25% annual escalations provided inflation protection embedded in the lease structure.

As previously announced, MHC is in the process of changing its name to Equity Lifestyle Properties, Inc. With this acquisition, the Company owns or has an interest in 272 quality communities in 25 states and British Columbia consisting of 100,203 sites.

The name change from Manufactured Home Communities, Inc. to Equity LifeStyle Properties, Inc. signaled the company's evolving identity. The word "lifestyle" captured the essence of what these properties offered: not just housing, but a way of living that appealed to active retirees and outdoor enthusiasts.

Our RV resorts and campgrounds operate under two well respected brands: Thousand Trails and Encore RV Resorts. Thousand Trails was established in 1969 with the goal of creating family-friendly campground destinations for outdoor enthusiasts. Today, we deliver on that same goal of family fun at more than 80 RV resorts and campgrounds within the Thousand Trails network.

In 2008, ELS consolidated its position by acquiring the Thousand Trails membership operations from Privileged Access. ELS, a Chicago-based real estate investment trust (REIT) that had previously purchased Thousand Trails' real estate assets in 2004, completed its acquisition of Thousand Trails' campground membership business and other assets of Privileged Access on Aug. 14 for $2 million.

The timing was fortuitous. As the 2008 financial crisis unfolded, ELS had already positioned itself in a sector—outdoor hospitality—that would prove remarkably resilient. The Thousand Trails acquisition planted seeds that would fully bloom during the COVID pandemic, when Americans desperate for safe outdoor recreation flooded into RV travel.

VII. Inflection Point #2: Surviving the 2008 Financial Crisis

When Lehman Brothers collapsed in September 2008, triggering the worst financial crisis since the Great Depression, conventional wisdom suggested that lower-income housing would be devastated. After all, the crisis had its roots in subprime mortgage lending to borrowers with marginal credit quality.

Going off the beaten path to focus on an underappreciated niche market can be a rewarding investment strategy. For example, manufactured home communities have quietly been one of the most resilient property classes to invest in over the decades.

Manufactured housing communities defied expectations. Instead of collapsing, they proved remarkably defensive. During the Great Recession in 2007-2010, the Trust performed very well. In 2008, FFO increased 5% from $0.76 per share 2007 to $0.80 per share in 2008.

How did an asset class associated with lower-income housing outperform during a housing-driven recession? The answer lies in the land-lease model's unique characteristics:

Switching costs protected occupancy: Residents couldn't easily move their homes. The cost and logistics of relocating a manufactured home meant that even financially stressed residents stayed put, continuing to pay lot rent even if they defaulted on other obligations.

Non-recourse housing debt: Unlike traditional mortgages, manufactured homes are often financed with chattel loans (personal property loans rather than real estate mortgages). When residents defaulted, the homes remained on ELS's lots—the company simply took ownership of the physical structure while continuing to collect lot rent from the next occupant.

Affordable housing demand increased: As the economy deteriorated and housing prices crashed, demand for affordable alternatives actually increased. Manufactured housing suddenly looked attractive to families who had previously aspired to traditional homeownership but now faced reduced incomes and tighter credit.

ELS steadily increased its "same store" occupancy rate from the great recession through 2019. The company navigated the crisis not just by surviving, but by strengthening its competitive position through opportunistic acquisitions and operational improvements.

[1][2] Through EGI, Zell targeted distressed and underperforming properties during economic downturns, leveraging creative financing like seller notes and assumable mortgages to acquire assets with limited upfront capital.

Sam Zell's "grave dancer" philosophy came into play. While competitors struggled with financing and deferred acquisitions, ELS had the balance sheet and expertise to acquire distressed properties at attractive valuations. The crisis that devastated much of the housing industry became a consolidation opportunity for the manufactured housing leaders.

The financial crisis also revealed an important characteristic of manufactured housing REITs: they exhibit countercyclical balance without sacrificing growth potential. Traditional housing prices crashed 30% or more in many markets; manufactured housing values remained relatively stable because they were already priced near replacement cost with minimal speculative premium.

VIII. Inflection Point #3: The 2010s Expansion & Consolidation

The decade following the financial crisis witnessed ELS's transformation from a large manufactured housing operator into the dominant force in its sector. The company pursued a multi-pronged growth strategy encompassing acquisitions, expansion at existing properties, and entry into the marina business.

Major deals, especially the MHC Inc. acquisition, transformed ELS from a large player into the dominant force in the sector. This scale brought operational efficiencies and significant market power.

The fragmented nature of the manufactured housing and RV industries provided ample opportunity. There are roughly ten million manufactured housing sites in the US and REITs own less than 3% of all sites. This meant plenty of runway for consolidation by professional operators with access to public market capital.

We invest in properties in sought-after locations near retirement and vacation destinations and urban areas across the United States with a focus on delivering value for residents and guests as well as stockholders. Over the last decade, we have continued to increase the number of Properties in our portfolio (including joint venture Properties), from approximately 307 Properties with over 111,000 Sites to 422 Properties with over 160,400 Sites as of December 31, 2020.

Most of the company's property growth in recent years has focused on RV and marina segments. Since 2017, when the company first disclosed acquisitions by segment type, MH sites have accounted for just 16% of total acquisitions. This strategic shift reflected the reality that new manufactured housing communities are extraordinarily difficult to develop due to zoning restrictions, while RV resorts and marinas offered better acquisition opportunities.

Marina Expansion: The marina portfolio emerged as a significant growth avenue. On September 10, 2019, we completed the acquisition of the remaining interest in the Loggerhead joint venture that owns 11 marinas for a purchase price of approximately $49.0 million. As part of the acquisition, we also funded the joint venture's repayment of its non-transferable debt of approximately $72.0 million. The transaction was funded with proceeds from our unsecured line of credit. Following the consummation of the transaction, we own 100% of the marinas.

In February 2021, we completed the acquisition of a portfolio of 11 marinas, containing 3,986 slips and 181 RV sites located in Florida, North Carolina, South Carolina, Kentucky and Ohio.

The marina business shares key characteristics with manufactured housing: high barriers to entry, limited supply growth, and stable demand from affluent customers. Building new marinas requires waterfront land, environmental permits, and substantial capital—constraints that protect existing operators from competition. The marina portfolio now consists of 23 marinas with approximately 6,900 slips, concentrated in highly desirable Florida locations with additional properties in the Carolinas and Midwest vacation destinations.

The Blended Community Strategy: ELS pioneered the concept of blending manufactured housing communities with RV resort amenities within single properties. This approach appeals to customers who may transition from RV travel to more permanent manufactured housing as they age—capturing customers at multiple life stages within the same community.

Throughout its history, ELS prioritized acquiring properties in desirable locations, often coastal or Sun Belt regions. This focus on quality real estate underpins the portfolio's long-term value and resilience, contributing to consistent occupancy.

The strategic focus on premium locations—coastal communities, Sun Belt retirement destinations, vacation areas—created a portfolio with demographic tailwinds built in. As Baby Boomers entered retirement in unprecedented numbers, ELS owned exactly the properties they wanted.

IX. Inflection Point #4: COVID-19 & The Outdoor Recreation Boom

When COVID-19 swept across America in early 2020, the initial impact on ELS was uncertain. With stay-at-home orders and travel restrictions, how would a company dependent on RV travel and vacation properties fare?

The answer arrived within months: COVID-19 proved to be an unexpected tailwind for outdoor hospitality.

In the topsy-turvy pandemic economy, RV demand is at a record high, with manufacturers set to ship upwards of 543,000 units in 2021, easily besting the previous record of 504,600 units shipped to dealers in 2017. The rise of the coronavirus' effect on what used to be considered normal life had a direct correlation with the sales of motor homes, camper trailers, and other travel trailers in 2020.

According to the Recreational Vehicle Industry Association (RVIA), RV shipments grew by 23.6% in the first quarter of 2020 when compared with the same period in 2019. Another report from the RVIA shows that total RV shipments in 2021 were 39.5% higher than the 2020 total, with travel trailers and motorhomes comprising the majority of RV sales in 2021.

The pandemic fundamentally changed how Americans thought about travel and leisure. According to a Kampgrounds of American Inc. Survey, people now consider camping the safest form of vacation in North America. Another survey by MMGY says that 68% of people feel safe traveling in a personal vehicle compared to 18% saying the same for domestic flights and 11% for international.

For ELS, the surge in RV travel translated directly into increased demand for its campground and resort properties. "People have just rediscovered the great outdoors, and that really spills over into the RV industry."

Remote work enabled what industry observers call "snowbird" lifestyles—seasonal migration to warmer climates—for a much broader population. No longer tied to offices, knowledge workers could spend winters in Florida RV resorts while maintaining their careers. This structural shift in work patterns appears permanent, creating sustained demand for ELS's seasonal and annual RV sites.

The pandemic also accelerated demographic trends already favoring ELS. Every day since January 1, 2011, some 10,000 American baby boomers have retired, and that will continue until 2030, when people over 65 will make up 19 percent of the population.

For the next 20 years, an average of 10,000 people each day will reach age 65. While that milestone no longer demands immediate retirement, certainly some of them will be ready to welcome the next phase of their life by taking things easier.

Equity LifeStyle Properties positioned well to take advantage of these demographic trends. Approximately 70 percent of its properties cater to Baby Boomers. This demographic alignment—aging Boomers seeking affordable housing, active lifestyles, and warm-weather destinations—represents a structural tailwind that will persist for decades.

X. The Post-Zell Era: Leadership Transition (2023)

The legendary commercial real estate mogul Sam Zell has died at the age of 81. Sam Zell, the renowned real estate magnate whose business acumen and pioneering spirit reshaped the landscape of the industry, passed away at the age of 81. With an indomitable entrepreneurial spirit, Mr. Zell became a titan in the world of real estate, leaving an indelible print on the market and forever altering the dynamics of the sector.

Equity LifeStyle Properties, Inc. (NYSE:ELS) announced the passing of Samuel Zell, the Company's Chairman. Sam served as Chairman of our Board of Directors since March 1995 and as our Chief Executive Officer from March 1995 to August 1996. Sam was an entrepreneur and investor with a global perspective and is recognized as a founder of the modern real estate investment trust industry.

"Sam leaves the real estate industry and the business community mourning the loss of a distinctive and generous mentor and an unparalleled leader who generously offered time and attention to develop those around him," ELS President and CEO Marguerite Nader stated. "He established an entrepreneurial culture focused on excellence, value creation, skilled and empowered teams and, most importantly, doing the right thing. He was a visionary who trusted his own sensibilities."

Consistent with the Company's long-standing succession plans, the Board of Directors named Thomas Heneghan to serve as Chairman of the Board of Directors.

Thomas Heneghan had served as the Company's Chief Executive Officer before accepting an offer to become Chief Executive Officer of Equity International in 2013. Marguerite Nader, the Company's current President and Chief Financial Officer, was elevated to President and CEO of the Company effective February 1, 2013.

Ms. Nader was President and CEO of the Company since February 2013. She was President and Chief Financial Officer from May 2012 to October 2012 and Executive Vice President and Chief Financial Officer from December 2011 to May 2012. She was employed with the Company since 1993.

Equity LifeStyle Properties' CEO is Marguerite Nader, appointed in Feb 2013, has a tenure of 12.25 years. Total yearly compensation is $4.24M, comprised of 16.2% salary and 83.8% bonuses, including company stock and options. Directly owns 0.14% of the company's shares, worth $17.65M. The average tenure of the management team and the board of directors is 12.3 years and 7.6 years respectively.

In April 2025, the company announced additional leadership enhancements. The Board of Directors named Marguerite Nader as Vice Chairman of the Board and promoted Patrick Waite as President, both effective immediately. Ms. Nader will continue serving as Chief Executive Officer, and Mr. Waite will continue in his role as Chief Operating Officer reporting to Ms. Nader. Mr. Waite has been Executive Vice President and Chief Operating Officer of the Company since January 2015.

Thomas Heneghan, the Chairman of the Board, said, "Today's announcement underscores the depth of experience within ELS' leadership team. Together, they have delivered REIT-leading results and built an extraordinary culture that drives our success, both of which are a tremendous source of pride for our Board."

The transition from founder-led to professional management represents a critical juncture for any company. Early indications suggest ELS has navigated this transition successfully. The management team has delivered consistent execution, and the strategic direction established under Zell continues to guide the company's growth.

Neithercut and Heneghan are respected leaders in the REIT universe with successful track records. "It's business as usual," said Michael Torres, former Equity LifeStyle board member and CEO of Adelante Capital Management. "Sam has built the organizations to survive him."

XI. The Current State & Financials

Equity LifeStyle Properties (ELS) has released its Q4 and full-year 2024 financial results, showing continued growth. The company reported Q4 2024 net income per share of $0.50, up 1.9% from $0.49 in Q4 2023. Normalized FFO per share increased 6.9% to $0.76 from $0.71 year-over-year. For the full year 2024, net income per share reached $1.96, marking a significant 16% increase from $1.69 in 2023. The annual FFO per share grew 9.5% to $3.03, while Normalized FFO per share rose 5.9% to $2.91. In a notable development, the Board of Directors has approved an increased annual dividend rate for 2025 at $2.06 per share, representing a 7.9% increase from the 2024 rate of $1.91.

The financial results demonstrate ELS's continued execution on its core strategy. Core portfolio generated growth of 6.5% in income from property operations, excluding property management, for the year ended December 31, 2024, compared to the year ended December 31, 2023. Core MH base rental income increased by 6.1% during the year. Manufactured home owners within our Core portfolio increased by 379 to 67,002 as of December 31, 2024, compared to 66,623 as of December 31, 2023. Core RV and marina base rental income for the year ended December 31, 2024 increased by 3.0%.

Looking at 2025 guidance, the company has set aggressive rate increases across its portfolio. By October month-end 2024, approximately 50% of MH residents received 2025 rent increase notices with an average expected rate increase of approximately 5.0%. The company has set RV annual rates for 2025 for more than 95% of annual sites. The average rate increase for these annual sites is approximately 5.5%.

The company has been increasing its dividend for nineteen consecutive years and has a current market capitalization of $13.9 billion.

Nineteen consecutive years of dividend increases places ELS among the elite "dividend aristocrats" in the REIT universe. This track record spans multiple recessions and market dislocations, demonstrating the durability of the business model.

XII. Porter's 5 Forces Analysis

1. Threat of New Entrants: VERY LOW ⭐⭐⭐⭐⭐

The barriers to entry in manufactured housing communities are among the highest in all of real estate. Local politics and restrictive zoning regulations have made it nearly impossible to add new affordable housing supply.

Manufactured housing adds to the affordable housing supply but often is blocked by restrictive zoning. Manufactured housing is affordable because it has a major cost advantage.

In the 50 years that have passed since the National Manufactured Housing Construction and Safety Standards Act of 1974 was signed into law, manufactured housing has remained an underexploited opportunity for providing millions of Americans with decent affordable housing. Only 18 states have laws that ensure local zoning codes do not discriminate against manufactured housing.

This regulatory environment creates what Warren Buffett might call an "economic moat"—a sustainable competitive advantage that protects incumbents from competition. New entrants face: - Zoning restrictions that often prohibit manufactured housing outright - NIMBY opposition from neighbors who associate manufactured housing with lower property values - High land costs in desirable locations - Environmental permits that can take years to obtain - Capital requirements that favor large, established operators

2. Bargaining Power of Suppliers: LOW

Land is the primary "input" for ELS's business—and ELS already owns it. The company has assembled a portfolio of irreplaceable locations over decades. Unlike a manufacturer that must continually purchase raw materials, ELS's land base is a fixed asset that generates income indefinitely.

Home manufacturers are fragmented, giving ELS leverage as a large buyer. The company purchases homes from multiple manufacturers, ensuring competitive pricing and supply security. No single manufacturer has sufficient market power to dictate terms.

3. Bargaining Power of Buyers: LOW

This is where ELS's business model truly shines. Once a resident places a manufactured home on an ELS site, they face switching costs of $5,000-$15,000 or more to move—assuming they can find an available site elsewhere. Most residents simply cannot afford to leave, making them captive customers with limited negotiating power.

The typical ELS resident is a retiree on a fixed income who has chosen the community for lifestyle reasons and established social connections. Moving would disrupt their entire life, not just their housing situation.

4. Threat of Substitutes: MODERATE

Alternative housing options exist—traditional single-family homes, apartments, 55+ communities, assisted living facilities. However, manufactured housing communities occupy a unique price point and lifestyle position that has limited direct substitutes.

For retirees seeking an active lifestyle in warm-weather destinations at affordable price points, few alternatives match what ELS communities offer. The combination of community amenities, social activities, and location quality creates a differentiated product.

5. Industry Rivalry: LOW TO MODERATE

With an $18B (but shrunken) market cap, Sun Communities is the established leader in the sector.

The manufactured housing REIT sector features a small number of public competitors. There are three U.S. exchange-listed Manufactured Housing REITs that collectively account for roughly $35 billion in market value: Equity LifeStyle (ELS), Sun Communities (SUI), UMH Properties (UMH).

Rather than competing on price—which would destroy value for all participants—the major players compete primarily on location quality, amenities, and customer service. The limited supply of quality communities means all major operators can maintain high occupancy without aggressive price competition.

XIII. Hamilton Helmer's 7 Powers Framework

Applying Hamilton Helmer's strategic analysis framework reveals why ELS has sustained above-average returns for decades:

1. Scale Economies: ELS benefits from spreading fixed costs across a larger property base. Corporate overhead, technology investments, brand building, and management expertise can serve 455 properties more efficiently than a smaller operator can serve 50.

2. Network Effects: Limited, but the Thousand Trails membership network creates modest network effects as members gain access to properties across the country.

3. Counter-Positioning: The stigma associated with manufactured housing causes most institutional investors to avoid the sector, even though fundamentals are excellent. This counter-positioning protects ELS from competition.

4. Switching Costs: Extremely high. The cost of relocating a manufactured home creates powerful customer lock-in that translates directly to pricing power.

5. Branding: The Thousand Trails and Encore brands carry recognition among RV enthusiasts. ELS communities are known for quality and amenities.

6. Cornered Resource: ELS has accumulated an irreplaceable portfolio of properties in prime locations—coastal communities, Sun Belt retirement destinations, and vacation areas—that would be nearly impossible to replicate today given zoning restrictions.

7. Process Power: Decades of operating experience have created institutional knowledge about community management, customer service, and property development that provides operational advantages over less experienced competitors.

XIV. Key Performance Indicators for Investors

For long-term fundamental investors, three KPIs capture the essence of ELS's ongoing performance:

1. Same-Store NOI Growth

This metric measures organic growth from existing properties, excluding acquisitions. ELS has averaged 4.4% same-store NOI growth annually since 1998—and remarkably, has never posted a quarter of negative same-store NOI growth. Track this metric to assess pricing power and operational execution.

2. Core MH Occupancy Rate

Currently running at approximately 95%, this metric captures the health of ELS's most stable and profitable segment. Manufactured housing occupancy is sticky due to switching costs, so changes here reflect either exceptional success or emerging problems. Target: sustained occupancy above 94%.

3. Annual RV Site Conversion Rate

This measures ELS's success in converting transient RV customers to higher-value annual memberships. Successful conversions drive revenue growth of 40-60% per site while dramatically reducing volatility. Track the mix shift toward annual sites as an indicator of portfolio quality improvement.

XV. Bull Case & Competitive Advantages

Demographic Tailwinds Are Just Beginning With 10,000 Baby Boomers turning 65 daily for the next decade, demand for affordable retirement housing and RV travel will grow structurally. ELS's portfolio is positioned exactly where these customers want to be.

Supply Constraints Create Pricing Power Zoning restrictions, environmental regulations, and NIMBY opposition make new manufactured housing communities nearly impossible to build. This supply constraint gives ELS pricing power that will persist indefinitely.

Defensive Business Model The land-lease structure with high switching costs creates recession-resistant cash flows. ELS has never posted a quarter of negative NOI growth—a track record unmatched in real estate.

Consolidation Opportunity With REITs owning less than 3% of manufactured housing sites nationally, substantial runway remains for accretive acquisitions.

XVI. Bear Case & Risk Factors

Interest Rate Sensitivity As a REIT, ELS is sensitive to interest rates. Higher rates increase borrowing costs and may reduce the attractiveness of REIT dividends relative to bonds.

Hurricane and Climate Risk Significant Florida exposure creates vulnerability to hurricanes. With heavy RV/MHC/marina exposure in Florida and the southeastern United States, ELS has endured repeated climate events that hampered operating results.

Regulatory Risk Changes to rent control laws, tenant protection regulations, or zoning policies could affect ELS's pricing power and development opportunities.

Affordability Concerns Rising lot rents may eventually price some customers out of manufactured housing communities, potentially affecting occupancy at lower-tier properties.

Post-COVID RV Normalization The pandemic-driven surge in RV travel has normalized. Transient RV demand faces headwinds as consumers return to traditional travel options.

XVII. Conclusion: The Unconventional Landlord

Equity LifeStyle Properties represents one of the most counterintuitive success stories in American business. An asset class dismissed by sophisticated investors as "trailer parks" has delivered REIT-leading returns for three decades. A company founded by a refugee family escaping the Holocaust has become one of America's largest landlords.

The lessons are profound: - Stigma can create opportunity by keeping competition at bay - Contrarian thinking, rigorously applied, generates exceptional returns - Business model quality matters more than asset class perception - Demographic trends, once in motion, persist for decades

Sam Zell saw what others missed: that manufactured housing communities possessed structural advantages—high switching costs, limited supply, defensive demand—that made them superior investments to traditional real estate. He built an organization capable of executing on that insight across multiple economic cycles.

The company now enters its post-founder era with proven leadership, a dominant market position, and demographic tailwinds that will persist for decades. For long-term investors willing to look past the stigma, ELS represents something rare: a compounding machine hiding in plain sight.

As Sam Zell might have said: sometimes the best investments are the ones that make everyone else uncomfortable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube