Elanco Animal Health: From Lilly's Backroom to Animal Health Powerhouse

Introduction: A Question Worth $4 Billion

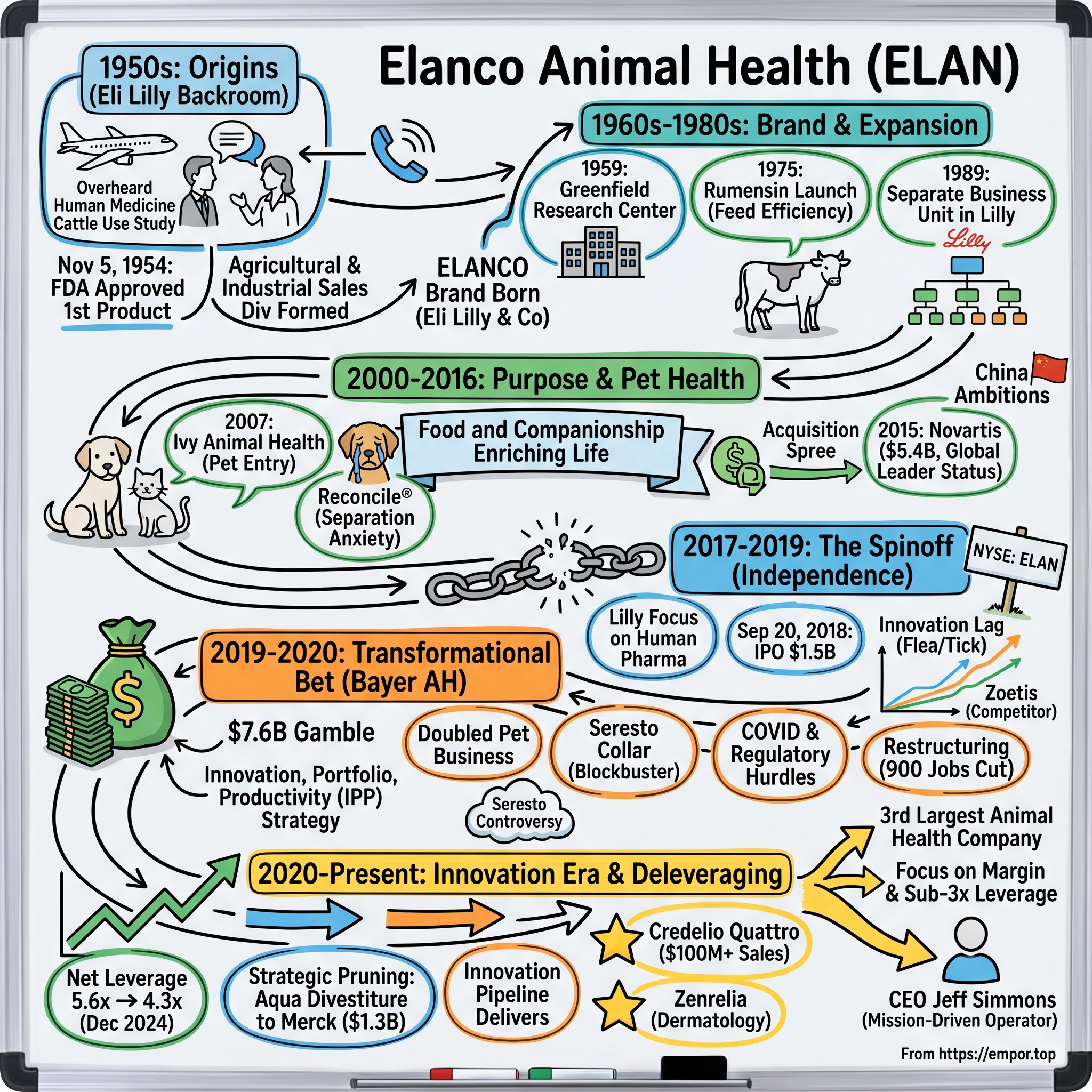

The rain was coming down hard on a commercial flight sometime in the early 1950s. Inside, an Eli Lilly employee overheard a conversation that would change the trajectory of American agriculture—and eventually create a $4 billion animal health enterprise. The conversation? A recently-presented study suggesting that a human medicine might have applications for cattle. The plane landed. A phone call was made. And before the week was out, Eli Lilly began working with Iowa State University to bring the science to market.

On November 5, 1954, the Food and Drug Administration approved Elanco's first product, solidifying its foundation. That serendipitous moment aboard an airplane would spawn what is today the third-largest animal health company in the world—a pure-play animal health business that navigates the intersection of food security, the human-animal bond, and climate sustainability.

The central question of this story: How did a side project born from an overheard conversation become a $4 billion revenue animal health giant? And what does its trajectory reveal about corporate spinoffs, transformational M&A, and the evolving animal health industry?

In 2018, Elanco officially separated from Eli Lilly & Company, listing on the New York Stock Exchange and launching onto the global stage as an independent public company. But that independence came with massive challenges—including an acquisition that nearly doubled the company's size and left it with dangerous leverage ratios that have only recently come under control.

This is a story about perseverance through skepticism, the strategic discipline of purpose-driven branding, the complexity of M&A integration, and the high-wire act of deleveraging while simultaneously launching new products. It's also a story about an industry—animal health—that sits at the convergence of several powerful secular trends: rising pet ownership, the humanization of pets, protein demand from an expanding global middle class, and the urgent need for sustainable agriculture.

Origins: The Accidental Animal Health Business (1892–1954)

When Veterinary Medicine Was a Frontier

In 1892, the veterinary profession in America was nascent at best. Most farmers relied on folk remedies and basic husbandry practices to keep their animals healthy. Formal veterinary education existed, but access to reliable medicines was severely limited. Elanco's roots in animal health go back to the earliest days of the veterinary profession in 1892. At that time, Lilly, the parent company to what would become Elanco, was one of the few providing rabies formulations to veterinarians.

This was not a strategic initiative. Eli Lilly and Company, founded in 1876 by Colonel Eli Lilly—a Union Army veteran and pharmaceutical chemist—was focused primarily on human health. The provision of animal health products was more a byproduct of scientific capability than deliberate market entry. But it planted a seed that would germinate six decades later.

The Post-War Agricultural Revolution

The context for Elanco's formal founding matters enormously. Post-World War II America was undergoing a fundamental transformation in food production. The GI Bill sent millions of young Americans to agricultural colleges. Mechanization was replacing animal labor. And most critically for our story, factory farming was emerging as the dominant model for meat and dairy production.

This industrialization created entirely new challenges. Dense animal populations meant diseases could spread catastrophically. Farmers needed not just medicine but prevention—antibiotics, vaccines, and growth promoters that could keep animals healthy and productive at scale. The pharmaceutical industry, flush with penicillin production capability from the war effort, was uniquely positioned to meet this demand.

In 1953, Lilly launched the first antibiotic for exclusive veterinary use. Shortly after, in 1954, the company formally organized its plant and animal science activities into the Agricultural and Industrial Sales Division, led by George Varnes.

The Plane Ride That Changed Everything

The company's founding story is worth dwelling on because it encapsulates something essential about innovation in corporate environments. A conversation overheard on a plane ride—about a recently-presented study suggesting a cattle application for a human medicine—turned into the first big bet that created an agriculture division. The plane landed, a phone call was made, and before the week was out, Lilly began working with Iowa State University to bring this science to the market.

This wasn't the result of a strategic planning process or a market analysis. It was the result of curiosity, opportunism, and a corporate culture that allowed employees to pursue promising ideas quickly. George Varnes, who would lead the new division, embodied this entrepreneurial spirit within the pharmaceutical giant.

The FDA approval on November 5, 1954, represented more than regulatory clearance—it validated an entirely new category of business for Eli Lilly. The company now had a formal stake in animal health, even if it remained a small fraction of overall operations.

For investors, this origin story illustrates a recurring theme in Elanco's history: the company's trajectory has been shaped as much by opportunism and serendipity as by deliberate strategy. This would remain true through the Novartis acquisition, the Bayer deal, and the IPO itself.

Building the Brand: Elanco Takes Shape (1954–1980s)

A Name Is Born

The Elanco brand, short for Eli Lilly and Company, came to be in 1960, following the reorganization of Eli Lilly and Company's Agricultural and Industrial Sales Division. The name itself was clever—an abbreviation that maintained connection to the parent while establishing distinct identity. The blue slash logo would come later, in the 1970s, but the foundation was laid.

Being the new company in the industry brought challenges, including some who questioned whether we had any business in animal agriculture. Perseverance, tenacity, and a commitment to innovation led Elanco to succeed, delivering value and solutions for our customers.

This skepticism was real. Eli Lilly was a human pharmaceutical company. Its expertise was in the complex biology of human disease. Why should farmers trust their livestock to a company whose primary customers were hospitals and pharmacies? Elanco had to prove itself in a market that was inherently skeptical of outsiders.

The Greenfield Era

In 1955, Eli Lilly purchased acreage adjoining its Biological Laboratories in Greenfield, Indiana. The facility was completed in 1959 and opened as the Agricultural and Veterinary Medicine Research Center. This wasn't just a real estate transaction—it was a signal that Lilly was serious about animal health as a long-term business.

Greenfield would become synonymous with Elanco. The company's headquarters remained there after the spinoff, and the animal health unit employs about 6,500 people, including about 775 at its headquarters in Progress Park, a business and life sciences park about three miles north of downtown Greenfield. Elanco has been based there since 2010, spread out in five buildings over 20 acres in a location highly visible from Interstate 70.

Expansion and Product Development

With the purchase of Corn State Laboratories, Lilly expands its line of veterinary products. This 1956 acquisition was the first of many that would characterize Elanco's growth strategy—building capability through targeted purchases rather than purely organic development.

In 1960, Elanco began growing rapidly into new countries and markets. The Agricultural and Sales Division was reorganized and Elanco Products Company was launched.

Key product launches included Treflan, a soybean herbicide, and Rumensin in 1975, an ionophore additive that improved cattle feed efficiency and controlled coccidiosis in livestock. The 1980s prioritized intensified research, manufacturing scale-up, and international infrastructure, such as regional offices and agricultural units, fostering steady revenue growth within Eli Lilly's broader operations.

Rumensin deserves particular attention. This feed additive became a foundational product for the company, improving feed conversion ratios in cattle and reducing the cost of beef production. It represented exactly the kind of product that would define Elanco's value proposition: not glamorous cures, but practical tools that made farming more efficient and profitable.

The Restructuring of the 1980s

Research and development shifts from plant science toward animal health, specifically on increasing the quality of animal-sourced protein. This was a critical strategic decision. The plant science business was increasingly competitive, and Lilly's comparative advantage lay in its pharmaceutical expertise—which translated more naturally to animal health than to crop protection.

In 1989, Elanco becomes a separate business unit within Eli Lilly and Company, allowing for more focused efforts on animal health research and development. This organizational change was significant. It gave Elanco its own P&L, its own leadership team, and its own strategic direction—even as it remained fully owned by the parent.

With a solid foundation in place, the 1960s through 1980s marked decades of expansion and innovation. Elanco developed regional offices in the U.S., entered global markets, and grew their product portfolio to focus on both farm animal and pet health.

For investors, this period established the template that Elanco would follow for decades: steady expansion through a combination of organic R&D and targeted acquisitions, with a focus on practical products that deliver measurable value to farmers and veterinarians rather than breakthrough therapies.

The Purpose Pivot & Pet Health Expansion (2000–2016)

Finding the "Why"

The early 2000s marked a philosophical turning point for Elanco. While the company had always been mission-driven in a general sense, leadership recognized the need for a more articulated purpose—something that could unify employees across dozens of countries and hundreds of product lines.

At that time, the team looked inward and found they shared one unifying motivation—purpose. From there, their purpose and company vision of "Food and Companionship Enriching Life" was born. Elanco became a company that focused on the "why" instead of the "what." This purpose-driven brand is what set them apart in 2000 and continues to set them apart today.

This wasn't empty corporate speak. The phrase "Food and Companionship Enriching Life" captured the dual nature of Elanco's business: farm animals that provide food security, and companion animals that provide emotional connection. It also positioned the company at the intersection of two powerful trends: the global demand for protein and the humanization of pets.

Entering the Pet Health Arena

For most of its history, Elanco had been primarily a farm animal company. Elanco has traditionally derived most of its revenue from farm animals—those products represented 63% of sales—but it has been working in recent years to boost its presence in the fast-growing companion animal side of the business.

The strategic logic was compelling. Pet health was growing faster than farm animal health. Pet owners were increasingly willing to spend significant sums on their animals' care. And the emotional bond between humans and pets created brand loyalty that was difficult to replicate in the commodity-driven farm animal market.

The company embarked on a significant era of expansion in 2007 upon the acquisition of Ivy Animal Health and the creation of their Pet Health business. Their first product—Reconcile®—addressed separation anxiety in pets, marking the beginning of their work exploring the human/animal bond.

Reconcile was a fascinating choice for a first pet health product. It wasn't a flea treatment or a vaccine—it was essentially Prozac for dogs. The product targeted a psychological condition that only matters when pets are viewed as family members with emotional needs. It was a bet on the humanization trend before that trend had a name.

The 2007 acquisition of Ivy Animal Health launched Elanco's pet segment, highlighted by Reconcile, the first FDA-approved fluoxetine for canine separation anxiety.

The Acquisition Spree

From 2010 to 2016, Elanco acquired multiple animal health companies and assets, building a diverse product portfolio.

The key acquisitions during this period included: - Lohmann Animal Health (2014): This acquisition made Elanco a global leader in poultry health - Novartis Animal Health (2015): A transformational deal that fundamentally changed Elanco's scale - Boehringer Ingelheim's dog and cat vaccines (2016): Further building out the pet health portfolio

The Novartis Deal: From Division to Industry Leader

Eli Lilly and Company today announced that it has completed the acquisition of Novartis Animal Health, which will further position Lilly's Elanco as a global leader in the animal health industry.

Under the terms of the agreement, Lilly acquired the Novartis Animal Health business in an all-cash transaction of approximately $5.4 billion, including anticipated tax benefits.

This was a bold move. Upon completion of the acquisition, Elanco became the second-largest animal health company in terms of global revenue, solidifying its number two ranking in the U.S., and improving its position in Europe and the rest of the world.

The combined organization increased Elanco's product portfolio, expanded its global commercial presence and delivered more innovation to customers. The acquisition also augmented Elanco's manufacturing and R&D capabilities with a total of 17 manufacturing sites and 14 R&D locations in the newly combined organization.

By improving efficiencies and reducing costs across both Elanco and Novartis Animal Health, Lilly expected to achieve estimated cost savings of approximately $200 million per year within three years of deal closing.

China Ambitions

In 2013, Elanco made a $100M investment in China Animal Healthcare. This reflected the strategic importance of emerging markets, where rising incomes were driving protein consumption and pet ownership. China's animal health market was growing rapidly, and Elanco was positioning itself to capture that growth.

For investors, the 2000-2016 period demonstrated management's ability to execute on a clear strategic vision: diversify from farm animal dependency, build pet health capability, and achieve global scale through disciplined M&A. The question that would loom over the next phase: could this same team execute a spinoff and an even larger acquisition while managing operational complexity?

The Spinoff: Breaking Free from Big Pharma (2017–2019)

Why Lilly Let Go

Saying goodbye to Elanco wasn't easy, Lilly CEO David Ricks said in the second-quarter conference call. Animal health, after all, has been part of Lilly since 1954. But the decision is part of a larger strategy to "take concrete actions to focus our resources and allocate capital to best serve our customers and create value for our stakeholders."

The strategic logic was straightforward. Eli Lilly was a human pharmaceutical company competing against giants like Pfizer, Merck, and Novartis for talent, capital, and pipeline assets. Every dollar invested in animal health was a dollar not invested in oncology, diabetes, or immunology. And Zoetis had demonstrated—through its own spinoff from Pfizer in 2013—that pure-play animal health companies could command premium valuations.

The completion of Eli Lilly & Co.'s exchange offer finalizes the journey Elanco began in 2017 when its former parent company first announced the exploration of potential strategic alternatives for the 64-year-old animal health company.

The IPO: A Company Reveals Itself

Elanco Animal Health Incorporated, a subsidiary of Eli Lilly and Company, announced the pricing of its initial public offering (IPO) of 62.9 million shares of its common stock at a price to the public of $24.00 per share. The shares began trading on the New York Stock Exchange on September 20, 2018 under the ticker symbol "ELAN."

The IPO was priced at $24.00 per share. Elanco stock was listed at $32.25 on September 20. Elanco raised $1.5 billion from this offering. On September 21, Elanco stock closed at $34.10.

The strong opening was encouraging, but the S-1 filing revealed some concerning trends. The company had $3 billion in 2017 sales and plenty of growing pains.

In 2017, Elanco generated revenue of $3.09 billion, 13 percent of Lilly's total. That was a 2 percent decline from the prior year. Through the first half of 2018, Elanco's revenue was $1.55 billion, flat from the same period a year earlier.

The Zoetis Comparison

Elanco had a long way to go to catch up to the largest pure-play animal health company on the Street, Zoetis, which was spun off from Pfizer in 2013. Zoetis brought in $2.8 billion in revenues in the first six months of 2018, up 11% year over year. That continued a strong growth trend: Zoetis' 2017 revenues grew 9% to $5.4 billion.

This comparison was unflattering. Zoetis was growing nearly four times faster than Elanco. Zoetis is the market leader and has grown faster over the past couple years. Over the past two years, ZTS has grown revenue at a 5.5% CAGR while ELAN revenue has been flat.

The valuation gap was equally stark. Zoetis traded at 20.5x '18 EBITDA and 7.9x revenue, a significant premium to ELAN.

The Exchange Offer: Lilly Exits

The exchange offer was 7.6x oversubscribed. Lilly shareholders were eager to swap their shares for Elanco stock, reflecting both confidence in the standalone business and the structural advantages of exchange offers.

This inducement almost always leads to "oversubscription," and the Eli Lilly split-off of Elanco was, as expected, heavily oversubscribed. Eli Lilly accepted for exchange 65 million shares of Eli Lilly common stock, over six percent of its outstanding stock, in exchange for its 293 million shares of Elanco common stock. Each share of Eli Lilly common stock accepted for exchange by Eli Lilly was exchanged for 4.5121 shares of Elanco common stock.

The share exchange was completed fewer than six months after Elanco's initial public offering, when 19.8% of its shares were sold to the public. Since that time, Elanco reported full-year 2018 revenue increasing 6% to $3.1 billion.

Innovation Lag

One issue loomed large: The company has been slow to catch onto emerging trends in veterinary medicine, and that's taken a hit out of sales. Between 2015 and 2017, Elanco suffered an "innovation lag" in flea and tick products. Competitors had launched next-generation parasiticides while Elanco's portfolio remained dated.

Elanco's ability to drive growth going forward would depend on its ability to deliver on its pipeline.

For investors, the spinoff represented both an opportunity and a warning. The opportunity was clear: a pure-play animal health company with global scale, purpose-driven culture, and diversified portfolio. The warning was equally clear: growth had stalled, the innovation pipeline was thin, and the Zoetis comparison highlighted just how far Elanco needed to travel.

The Transformational Bet: Bayer Animal Health Acquisition (2019–2020)

The $7.6 Billion Gamble

Less than a year after achieving independence, Elanco announced the biggest bet in its history. In 2019, the business announced it would acquire Bayer's animal health business for $7.6 billion.

Transaction valued at close at $6.89 billion, funded by $5.17 billion in cash and 72.9 million shares to Bayer. Elanco Animal Health Incorporated today announced it has closed the acquisition of Bayer Animal Health.

Bayer's former Animal Health business has about 4,400 employees and achieved sales of 1.57 billion euros in 2019.

"This transaction creates one of the global animal health leaders," said Werner Baumann, Chairman of the Board of Management of Bayer AG.

Strategic Rationale: The IPP Strategy

This acquisition strengthens Elanco's "Innovation, Portfolio, Productivity" (IPP) strategy, which the company has been executing on since before its initial public offering in 2018.

Scale and capabilities of the combined company position Elanco for the long term as a leader in the attractive, durable animal health industry. Combines Elanco's longstanding focus on the veterinarian with Bayer Animal Health's direct-to-consumer expertise to open new opportunities to fuel growth.

Elanco's research and development (R&D) pipeline is now bolstered with five expected launch equivalents from Bayer—bringing Elanco's anticipated total to 25 by 2024—with five of those expected to launch by the end of 2021. The transaction also adds new R&D capabilities, including innovative dosing and delivery technology platforms, and provides access rights to Bayer's Crop Science R&D pipeline and de-prioritized clinical pharma assets.

Pet Health: The combination elevates Elanco's pet business to approximately 50 percent of revenues and nearly triples the company's international pet health business. This expanded portfolio of care provides for pets at all ages and stages, from disease prevention and wellness for the youngest puppies to helping pets remain an active, central part of the family in their later years. The transaction also broadens Elanco's pet parasiticide portfolio with topical treatments and collars, making the blockbuster Seresto collar Elanco's top product globally.

Navigating COVID and Regulatory Hurdles

The acquisition closed in August 2020—in the midst of the global COVID-19 pandemic. "Nearly two years into our journey as an independent company, we have made significant progress in creating a purpose-driven, independent global company dedicated to animal health—all while weathering the century's most significant animal and human health pandemics: African Swine Fever and COVID-19," said Jeff Simmons.

In July 2020, the FTC required global suppliers of animal products, Elanco Animal Health, Inc. and Bayer Animal Health GmbH, to divest three animal health products to settle charges that Elanco's proposed $7.6 billion acquisition of Bayer would likely be anticompetitive in those markets.

The divested products had 2019 revenue in the range of $120-140 million.

The Integration Challenge

Just two months following the closing of its acquisition of Bayer Animal Health, Elanco announced its first business restructuring. As part of this effort, the company announced its intent to eliminate more than 900 positions across nearly 40 countries, primarily in Sales and Marketing, but also R&D, Manufacturing and Quality, and back office support.

Elanco expects to realize at least $100 million of annual compensation and benefits savings toward the planned synergy goal of $275 million to $300 million.

The Seresto Cloud

The acquisition brought with it a significant reputational challenge: the Seresto flea and tick collar. Elanco's flea and tick collar, branded "Seresto", which was developed by Bayer Animal Health and acquired by Elanco in 2020, has been linked to more than 98,000 incidents of poisoning by pesticide, including more than 2,000 pet deaths, according to a 2022 report by a subcommittee of the House Committee on Oversight and Reform. On July 13, 2023, following a multi-year review, the EPA announced that they were unable to determine whether Seresto was the cause of reported animal deaths. The EPA limited the collar's registration to five years instead of the normal fifteen years registration.

A comprehensive, multi-year review by the EPA, with support from the Food and Drug Administration, confirmed Seresto continues to meet EPA standards for product registration. EPA confirms continued registration of the collar. Comprehensive data affirms the safety profile of Seresto.

The agency limited the approval of the collar to five years and required Elanco—the manufacturer of Seresto—to conduct enhanced reporting for adverse events, conduct additional outreach to the veterinary community, and put new warnings on the collar's label, among other changes.

For investors, the Bayer acquisition was the defining bet of Elanco's independent history. It transformed the company's scale, filled critical pipeline gaps, and rebalanced the portfolio toward pet health. But it also loaded the balance sheet with debt at precisely the moment when rising interest rates would make that debt more expensive to service. The next several years would be dominated by one imperative: deleveraging.

The Innovation Era: New Products & Portfolio Transformation (2020–Present)

The Deleveraging Imperative

As of December 31, 2023, Elanco's net leverage ratio was 5.6x adjusted EBITDA, down slightly from 5.7x as of September 30, 2023.

This was dangerously high leverage for a company without the kind of blockbuster pipeline that could rapidly transform earnings. Pro forma EBITDA was set to come in around $1.1 billion which had to support a $7.3 billion net debt load, translating into sky-high leverage ratios in the mid-6s. The company rationalized this by pointing towards $300 million in potential synergies, being equivalent to 5% of pro forma sales, a huge ambition.

The Aqua Divestiture: Strategic Pruning

To address the leverage problem, management made a strategic decision: sell non-core assets. Elanco today announced it has entered into an agreement to sell its aqua business to Merck Animal Health for approximately $1.3 billion in cash, which represents approximately 7.4x the estimated 2023 revenue of the Elanco aqua business.

"Finalizing this transaction marks a significant milestone in concentrating our focus on high-value opportunities in pet health and livestock sustainability while creating balance sheet flexibility," said Todd Young, Executive Vice President and CFO.

Elanco's aqua business includes products across both warm-water and cold-water species, generating an estimated $175 million in revenue and approximately $92 million in adjusted EBITDA. The divestiture includes current marketed brands, aqua R&D projects, the transfer of manufacturing sites in Prince Edward Island, Canada and Dong Nai, Vietnam and approximately 280 commercial and manufacturing employees.

Combined with the expected $280 million to $320 million of cash generated from the base business, the company expects to pay down approximately $1.3 to $1.4 billion of debt in 2024, ending the year with net debt to adjusted EBITDA in the mid-4x range.

Innovation Pipeline Delivers

"We have a robust innovation portfolio and continue to expect to deliver $600 to $700 million of Innovation sales by the end of 2025," said Jeff Simmons, Elanco President and CEO.

Credelio Quattro: The Company continues to expect Credelio Quattro to be positively differentiated and is seeking approval for indications that would give the broadest parasite coverage including fleas, ticks, heartworms and other internal parasites, like tapeworm.

Credelio Quattro marked $100 million in net sales making it Elanco's fastest pet health blockbuster in history and one of the industry's fastest ever, especially with a single geographic approval. Credelio Quattro joins Experior® as Elanco's second of six recently launched blockbuster-potential products to reach the $100 million annual net sales milestone.

Elanco continues to prepare to take Credelio Quattro global, with numerous submissions made in Australia, Canada, the EU, the UK, and Japan, setting up the company's expected geographic expansion for the product starting in 2026.

Zenrelia (Canine Dermatology): For Zenrelia, the company received confirmation from FDA that all major technical sections (Effectiveness, Safety and Chemistry, Manufacturing, and Controls (CMC)) are complete as of late June 2024.

Zenrelia has also received its first approval in Brazil by the Brazilian Minister of Agriculture, Livestock and Food Supply, with launch planned for the fourth quarter of 2024.

Zenrelia, an effective, convenient, and safe once-daily oral JAK inhibitor, continues its launch progress globally, gaining approval from the United Kingdom's Veterinary Medicines Directorate in August. Additionally, launch progress continues across the EU and Great Britain with product supply now in market for veterinarians and pet owners.

2024 Financial Results

For the full year 2024, Elanco achieved a revenue of $4,439 million, slightly exceeding the analyst estimate of $4,424.97 million. The company reported a net income of $338 million and an adjusted net income of $452 million.

The adjusted EBITDA for the year was $910 million, or 20.5% of revenue.

"Elanco delivered a strong finish to 2024, achieving our sixth consecutive quarter of organic constant currency revenue growth—with the fourth quarter up 4%—and building momentum as we head into 2025," said Jeff Simmons. "For the year we grew in both Pet Health and Farm Animal, in our top five product franchises, and in nine of our top 10 countries, all on an organic constant currency basis, demonstrating the broad-based strength of our diverse portfolio."

Leverage Progress

As of September 30, 2024, Elanco's net leverage ratio was 4.3x adjusted EBITDA, a reduction of 1.3x compared to June 30, 2024.

As of December 31, 2024, Elanco's net leverage ratio was 4.3x adjusted EBITDA, flat to September 30, 2024.

Elanco has expressed its intention to reduce net leverage below 3x. Given the substantial debt repayment, suspension of share repurchases, and pressure from equity investors, S&P expects the company will continue prioritizing deleveraging and considers it unlikely that leverage will increase back above 4.5x.

For investors, the innovation pipeline has finally begun to deliver. Credelio Quattro's rapid path to blockbuster status validates the Bayer acquisition thesis, while the aqua divestiture and steady deleveraging demonstrate capital allocation discipline. The question now is whether management can sustain execution and continue driving leverage below 4x while simultaneously funding new product launches.

Industry Context: The Animal Health Market Landscape

A $60+ Billion Global Market

The global animal health market size was valued at USD 62.89 billion in 2024 and is projected to reach USD 112.33 Billion by 2030, growing at a CAGR of 10.46% from 2025 to 2030. North America animal health market held the highest share of about 35.69% in 2024.

Factors driving the market growth include rising animal health expenditure, the increasing inculcation of Artificial Intelligence (AI), evolving regulatory scenario, prevalence of diseases in animals, concerns over zoonoses, initiatives by key companies, uptake of pet insurance.

The Competitive Landscape

Zoetis: The Undisputed Leader Established in 2013 through a spin-off from top pharma company Pfizer's animal health division, Zoetis has quickly risen to prominence as a key player in the global animal health sector.

Zoetis reported total revenue of $9.3 billion in 2024, a 8% increase from $8.5 billion in 2023, with its companion animal segment contributing nearly two-thirds of total revenue.

Zoetis has provided a full-year 2025 revenue guidance of $9.225 billion to $9.375 billion. The company anticipates 6% to 8% organic operational growth in revenue.

Boehringer Ingelheim and Merck The global animal health market outlook is highly competitive, with key players including Zoetis, Elanco, Merck Animal Health, Boehringer Ingelheim, and Virbac.

Merck's Animal Health division's revenue reached USD 5.62 billion.

Industry Trends

Rise of Preventive Pet Healthcare: Growing awareness among pet owners is fueling demand for preventive care, including vaccinations, routine checkups, and wellness products. This trend is reshaping veterinary services, with increased spending on companion animal wellness, thereby driving innovation in diagnostics, digital tools, and early intervention therapies.

Digitization of Livestock Monitoring: Advanced technologies like IoT sensors and AI-based analytics are transforming livestock management.

Where Elanco Fits

Elanco achieving revenues of approximately $4.41 billion in fiscal year 2024, developing and delivering a wide array of products and services, from crucial pet parasiticides to essential farm animal health solutions, firmly establishing its relevance.

Elanco is the third-largest animal health company in the world.

For investors, the animal health industry offers secular growth drivers but intense competition. Zoetis's scale advantage is formidable—nearly double Elanco's revenue—and its margin profile is materially superior. Elanco's path to value creation runs through innovation execution, margin expansion, and continued deleveraging, not through trying to match Zoetis on scale.

Playbook: Business & Strategy Lessons

Corporate Spinoffs as Value Creation

The Elanco story is part of a broader pattern: pharmaceutical companies spinning off animal health divisions to unlock value. Pfizer did it with Zoetis in 2013. Lilly followed with Elanco in 2018. The playbook is consistent: human pharma businesses compete for resources with animal health, creating strategic misalignment that can be resolved through separation.

The results have been mixed. Zoetis became a stock market darling, compounding shareholder value at impressive rates. Elanco's journey has been rockier, weighed down by the Bayer acquisition debt. The lesson: spinoffs create optionality, but execution determines outcomes.

Purpose-Driven Branding

"Food and Companionship Enriching Life"—this vision has proven more than marketing. Jeff Simmons serves as President and CEO of Elanco Animal Health, an independent animal health leader with the ability to reach the world's animals—specifically 19 species in nearly 100 countries. The Elanco team has established a unique innovation engine grounded in a higher purpose.

Purpose-driven branding works in animal health because the customer base—farmers, veterinarians, pet owners—genuinely cares about animal welfare. This creates authentic differentiation that is difficult for competitors to replicate.

M&A Integration Complexity

The Bayer acquisition illustrates both the potential and the pitfalls of transformational M&A. The strategic logic was sound: fill innovation gaps, rebalance the portfolio, achieve scale. But execution proved challenging: - Restructuring announcements came just two months after closing - Leverage ratios remained elevated for years - The Seresto controversy emerged as an inherited liability

The Debt Management Imperative

Perhaps the most important lesson from Elanco's recent history is the danger of excessive leverage, particularly in a rising rate environment. Giving pro forma effect to the transaction for the full year 2023, including the expected debt paydown and excluding the EBITDA associated with the aqua business, the company estimates the net leverage ratio would have been 0.6x to 0.7x lower, at or slightly below 5.0x.

Management has shown discipline in addressing this, but the journey from 5.5x+ leverage to sub-4x has consumed years of strategic attention and required divesting the aqua business.

Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

1. Threat of New Entrants: LOW-MODERATE Regulatory barriers are substantial. FDA approval for animal health products requires years of clinical development and significant capital investment. Established distribution networks and veterinarian relationships create further barriers. However, biotech startups can create point solutions in specific therapeutic areas, occasionally disrupting established players.

2. Bargaining Power of Suppliers: LOW Raw materials for animal health products are largely commoditized. Elanco maintains manufacturing capability that reduces supplier dependency. Multiple API suppliers exist globally, limiting any single supplier's leverage.

3. Bargaining Power of Buyers: MODERATE Combines Elanco's longstanding focus on the veterinarian with Bayer Animal Health's direct-to-consumer expertise—this omnichannel approach reduces buyer power by diversifying distribution. However, veterinary buying groups and large distributors do exercise negotiating power, and pet owners are increasingly price-sensitive.

4. Threat of Substitutes: LOW-MODERATE Generic competition emerges after patent expiration, but pharmaceutical products generally face limited substitution. Some natural/holistic alternatives exist in pet health, but regulatory approval requirements protect prescription products.

5. Competitive Rivalry: HIGH Zoetis holds approximately 14.21% share of the global veterinary vaccines market, outpacing Boehringer Ingelheim and Merck. The R&D race for next-generation products is continuous. Zoetis's osteoarthritis monoclonal antibodies (Librela and Solensia) represent the kind of innovation that can shift market share rapidly.

Hamilton's 7 Powers Analysis

1. Scale Economies: MODERATE Post-Bayer, Elanco has meaningful manufacturing and distribution scale. In November 2024, Elanco acquired a manufacturing facility in Speke, UK, for $25 million to fortify its global supply chain for livestock products. The acquisition secures supply for products generating $160–$180 million annually. However, Zoetis's larger scale provides cost advantages Elanco cannot match.

2. Network Effects: LOW Animal health products don't benefit from traditional network effects. Veterinarian relationships create some switching costs, but these are relationship-based rather than structural.

3. Counter-Positioning: MODERATE Elanco's purpose-driven positioning ("Food and Companionship Enriching Life") and focus on sustainability represents a differentiated approach that larger competitors may be reluctant to fully embrace given their incumbent positions.

4. Switching Costs: MODERATE Once veterinarians are comfortable with a product's efficacy and safety profile, they are reluctant to switch. However, superior innovations can overcome this inertia.

5. Branding: MODERATE Brand matters in animal health, particularly in pet products where owners select based on trust. Seresto's brand was damaged by controversy but remains one of Elanco's largest products.

6. Cornered Resource: LOW No critical cornered resources exist in animal health. R&D talent, manufacturing capability, and distribution networks are available to well-capitalized competitors.

7. Process Power: EMERGING With 30 years of industry and life sciences experience, Jeff Simmons has spent the past 15 years as head of Elanco. This institutional knowledge and the purpose-driven culture represent emerging process power that may be difficult for competitors to replicate.

The Leadership Factor: Jeff Simmons

Jeffrey Simmons is President and CEO of Elanco and has served as a director since September 2018; he previously led Elanco within Eli Lilly from 2008–2018 after a 30+ year career in life sciences with roles spanning international marketing, country leadership, and R&D oversight.

In his nearly 30 years with the company, Simmons has held an array of roles, from sales and marketing to R&D across multiple continents. In these roles, Simmons gained a new perspective on food, agriculture and companionship that has sparked a deep conviction for the power of healthy animals.

Through his purpose-driven leadership, in 2018, Jeff navigated the company's separation from Eli Lilly and Company, culminating with Elanco's listing on the New York Stock Exchange as an independent, public company. Then in 2020, Jeff guided the acquisition of Bayer Animal Health, deepening Elanco's Pet Health business and bringing an equal balance between pets and livestock.

Simmons is not a finance-first CEO—he's a mission-driven operator who built his career on the ground in animal health. His LinkedIn profile emphasizes themes like "food security for all" and "climate neutral farms"—not the typical language of a corporate executive focused on quarterly earnings. This orientation permeates the organization.

Elanco's CEO Jeff Simmons, appointed in Jul 2018, has a tenure of 6.83 years. Total yearly compensation is $14.83M, comprised of 8.1% salary and 91.9% bonuses, including company stock and options. Directly owns 0.37% of the company's shares, worth $24.23M.

Bull Case, Bear Case, and Key Metrics

The Bull Case

-

Innovation pipeline finally delivering: Credelio Quattro's rapid path to blockbuster status validates years of R&D investment. Zenrelia's global rollout is proceeding on schedule. "We exceeded our innovation revenue target for 2024 and raised the goal for 2025, with six potential blockbuster products now launched."

-

Deleveraging on track: From 5.6x in 2023 to 4.3x at year-end 2024, with management targeting sub-3x. The aqua divestiture accelerated this trajectory.

-

Secular industry tailwinds: Pet humanization, rising protein demand, and sustainability requirements all favor animal health investments.

-

Margin expansion potential: As innovation products scale and synergies are fully realized, operating margins should improve.

-

Valuation discount to Zoetis: Despite improvement, Elanco trades at a material discount to the market leader, creating multiple expansion potential if execution continues.

The Bear Case

-

Zoetis's competitive moat: With nearly double the revenue and superior margins, Zoetis can outspend Elanco on R&D and marketing indefinitely.

-

Execution risk remains: The company has a history of missing expectations. Pipeline delays, integration challenges, and unexpected competitive pressures remain possibilities.

-

Regulatory overhang: Seresto's five-year registration expiring in 2028 creates uncertainty around a major product.

-

Macro sensitivity: U.S. veterinarian visits have declined 2-3% annually in 2024-2025 amid economic pressures, potentially impacting demand.

-

Currency headwinds: The company anticipates a headwind to revenue of approximately $110 million from the unfavorable impact of foreign exchange rates.

Key Metrics to Monitor

Investors should track three primary metrics to assess Elanco's ongoing performance:

-

Innovation Revenue Growth: Management has raised the 2025 target to $640-720 million. This metric directly measures whether the innovation strategy is working.

-

Net Leverage Ratio: Currently at 4.3x, with a target of sub-3x. Progress on deleveraging determines financial flexibility and risk profile.

-

Organic Constant Currency Revenue Growth: Stripping out FX and divestitures, this measures underlying business momentum. Management expects mid-single-digit growth in 2025.

Conclusion: The Ongoing Transformation

Seventy years after an overheard conversation on an airplane sparked the creation of Eli Lilly's animal health division, Elanco Animal Health stands as an independent public company navigating a critical transition. The Bayer acquisition that nearly doubled the company's size has been integrated. The innovation pipeline is finally producing blockbusters. The leverage ratio is declining toward manageable levels.

Yet significant work remains. Zoetis's competitive advantage is structural and substantial. The Seresto regulatory review in 2028 represents a known unknown. Currency headwinds continue to pressure reported results. And the fundamental question—whether Elanco can sustainably grow earnings fast enough to justify its capital structure—remains unanswered.

S&P could raise Elanco's ratings in the next 12-18 months if the company reduces leverage below 3.5x and maintains free cash flow to debt above 10%.

For long-term investors, Elanco represents a bet on continued execution of a clearly articulated strategy in a secularly attractive industry. The path is visible: innovation-driven revenue growth, margin expansion from mix shift and cost discipline, deleveraging from improving free cash flow. The destination—a sustainable competitor to Zoetis and Boehringer Ingelheim—remains achievable but not assured.

What began as an accidental business born from a chance conversation has become a purpose-driven enterprise with the scale, portfolio, and capabilities to compete globally. The next chapter depends on whether management can convert that potential into durable shareholder value.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube