Estée Lauder: The Beauty Empire Built on Touch and Tell

I. Introduction & Episode Roadmap

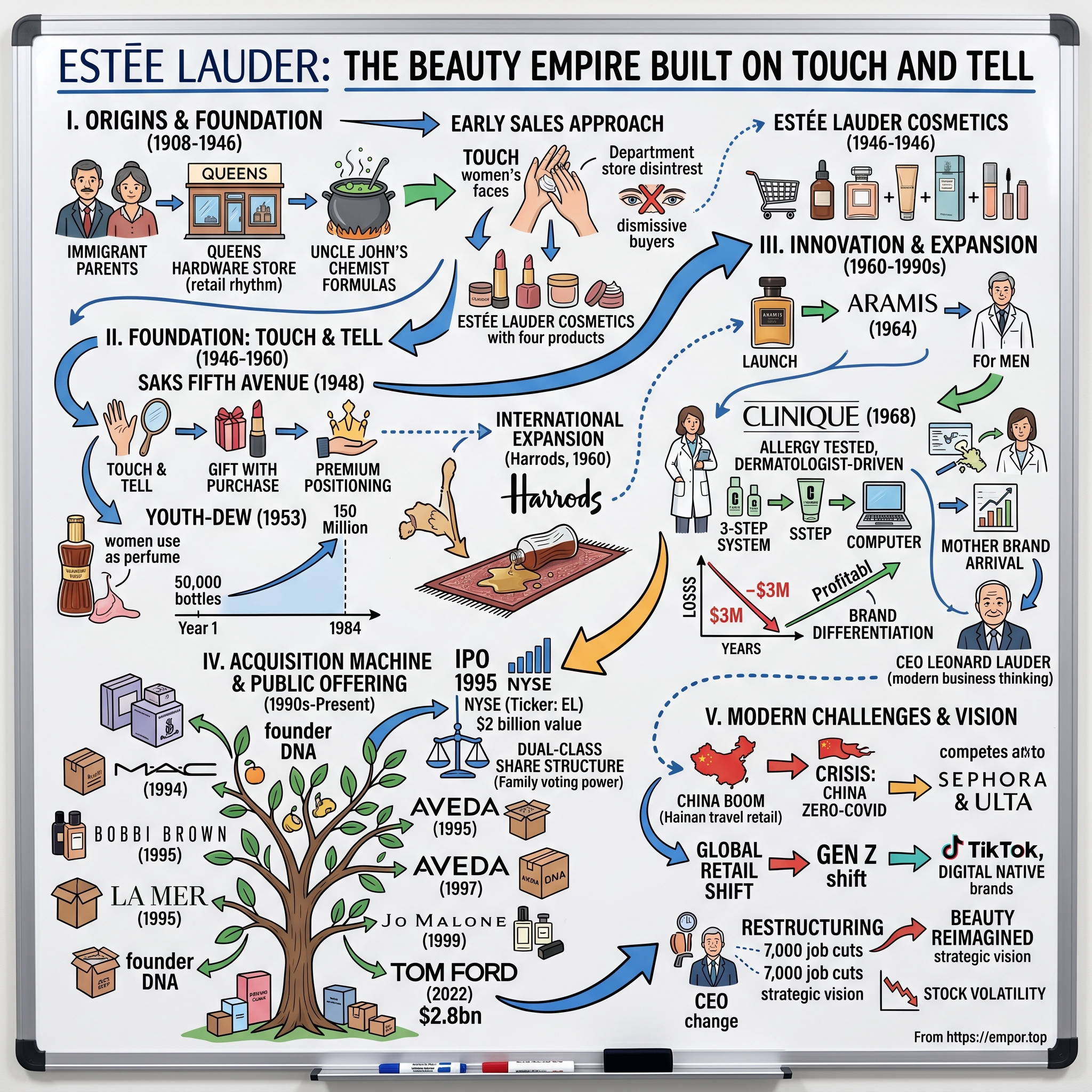

Picture this: A woman in a pristine white lab coat approaches you at Saks Fifth Avenue in 1948. She doesn't just describe her cleansing oil—she touches your face, massages it into your skin, and hands you a mirror. "Feel that?" she asks, as you marvel at your suddenly luminous complexion. That woman was Estée Lauder, and that simple gesture would revolutionize how beauty products were sold forever.

Today, Estée Lauder Companies stands as the second-largest cosmetics company in the world, trailing only L'Oréal, with a market cap hovering around $52 billion. The portfolio reads like a who's who of prestige beauty: Estée Lauder, Clinique, Origins, M·A·C, Bobbi Brown Cosmetics, La Mer, Aveda, Jo Malone London, TOM FORD, Too Faced, Dr.Jart+, and The Ordinary. Each brand operates with distinct positioning, price points, and customer tribes—yet all trace their DNA back to a Hungarian immigrant's daughter who started with four products and an unshakeable belief that every woman deserved to feel beautiful.

The central question that drives this story isn't just how Josephine Esther Mentzer became Estée Lauder, or how four skincare products became a global empire. It's how a company built on personal touch and department store relationships navigated the transition to digital commerce, how a family-controlled business balanced public market demands, and whether the playbook that worked for 75 years can survive the TikTok generation.

This is a tale of immigrant entrepreneurship at its finest—where old-world craftsmanship met American salesmanship. It's about building brands through acquisition while maintaining their founder DNA. And ultimately, it's about the tension between family control and public market accountability, a dual-class structure that has both protected the company's long-term vision and frustrated investors seeking change.

What emerges is a masterclass in patient capital, premium positioning, and the power of giving customers something extra—whether that's a free lipstick with purchase or the promise of transformation in a jar. But it's also a cautionary tale about channel concentration, geographic dependency, and what happens when your biggest growth driver—Chinese consumers and travel retail—suddenly vanishes overnight.

II. The Immigrant Dream & Early Years (1908–1946)

The American Dream often begins with a boat, a suitcase, and a surname that immigration officials can't quite spell correctly. For Rose Schotz Rosenthal, it began in Sátoraljaújhely, Hungary, a town whose name alone would challenge any Ellis Island clerk. She arrived in New York at the turn of the century, marrying Max Mentzer, a Czech immigrant who ran a hardware store in Corona, Queens. On July 1, 1908, they welcomed their ninth child: Josephine Esther Mentzer, though the world would come to know her simply as Estée.

The Mentzer household was a crucible of entrepreneurship. While other children played stickball in the streets of Queens, young Estée worked the register at her father's hardware store, learning the rhythm of retail: the importance of product placement, the art of the upsell, the delicate dance between inventory and cash flow. She watched her father extend credit to neighbors during tough times, understanding instinctively that business was about relationships, not just transactions.

But the real catalyst came in the form of her uncle, John Schotz, a chemist who arrived from Hungary with formulas and dreams. In 1924, he set up a makeshift laboratory in the stable behind the Mentzer home, transforming it into what young Estée called "a magical place of bubbling pots and mysterious jars." While her siblings saw a cramped, chemical-scented workspace, Estée saw alchemy. She became his eager apprentice, learning how to blend cold creams and skin treatments, understanding the precise temperatures needed to emulsify oils and waters, the patience required to achieve the perfect consistency.

Uncle John's creations weren't just functional—they were transformative. His Super Rich All-Purpose Cream didn't merely moisturize; it made skin feel like velvet. His Cleansing Oil didn't just remove makeup; it left faces glowing. For a teenage girl in 1920s Queens, watching her uncle create these potions was like discovering a superpower. She began testing products on herself, her sisters, anyone who would sit still long enough for a demonstration.

The summer of 1926 changed everything. During a holiday at Mohegan Lake in upstate New York, Estée met Joseph Lauter, a silk merchant's son with movie-star looks and business ambitions. Joe had his own immigration story—his father had fled Austria, and somewhere along the journey, "Lauter" had been mangled into various spellings. Years later, Joe would restore it to "Lauder," correcting what he called "an error that diminished our heritage."

They married on January 15, 1930, just as the Great Depression was tightening its grip on America. While Joe pursued various business ventures—first textiles, then other enterprises—Estée couldn't shake her fascination with beauty. She began selling her uncle's creations to friends, calling them by names she invented: "Super Rich All-Purpose Cream," "Six-In-One Cold Cream," "Dr. Schotz's Viennese Cream." Each name told a story, promised a transformation.

The marriage produced a son, Leonard, in 1933, but by 1939, Estée and Joe had divorced. She moved to Miami Beach, where she refined her sales technique at resort hotels and beach clubs. These venues became her laboratory for understanding luxury consumers—women with means who valued quality and were willing to pay for the promise of beauty. She learned that wealthy women didn't just want products; they wanted experiences, stories, a sense of belonging to something exclusive.

During this period, Estée developed what would become her signature sales approach. Rather than simply describing her creams, she would touch women's faces, applying products with her own hands. "Let me show you," became her catchphrase. In an era when cosmetics were often sold from behind glass cases by disinterested clerks, Estée's hands-on approach was revolutionary. She made beauty personal.

By 1942, Estée and Joe had remarried—she later called their temporary split "the smartest thing I ever did" because it made them both realize what they'd almost lost. Joe brought business acumen and operational discipline; Estée brought vision and an intuitive understanding of what women wanted. Together, they began to see the potential for something bigger than selling jars at beach clubs.

The war years provided unexpected opportunity. With European cosmetics cut off and domestic production focused on the war effort, there was a gap in the luxury beauty market. Estée saw her chance. She convinced Joe that they should formalize the business, moving from kitchen-table entrepreneurship to a real company. They pooled their savings—$50,000, mostly from Joe's various ventures—and in 1946, Estée Lauder Cosmetics was born.

They started with just four products: Cleansing Oil, Skin Lotion, Super Rich All-Purpose Creme, and Creme Pack. Each was based on her uncle's formulas but refined through years of testing on willing subjects at beauty salons and beach clubs. The products weren't cheap—Estée positioned them as premium from day one, understanding that in beauty, price often signals quality.

What set these products apart wasn't just their formulation but their promise. Estée didn't sell moisturizer; she sold "the aristocratic look." She didn't offer cleansing oil; she provided "the secret to luminous skin." Every product came with a story, a ritual, a transformation. And unlike her competitors who relied on magazine advertisements and department store displays, Estée had a secret weapon: herself.

As 1946 drew to a close, Estée Lauder stood at the threshold of something remarkable. She had products, a partner, and most importantly, a philosophy that would guide everything that followed: beauty wasn't about covering up; it was about bringing out what was already there. And the best way to sell beauty wasn't through advertisements or celebrity endorsements—it was through touch, through personal connection, through making every woman feel like she was the only customer in the world.

III. Foundation: Touch and Tell (1946–1960)

The first "no" came from Bonwit Teller. Then Bergdorf Goodman. B. Altman turned her away at the door. In 1946, Manhattan's most prestigious department stores wanted nothing to do with Estée Lauder's four products. She was, as one buyer dismissively put it, "just another woman with face cream." But Estée had learned from her father's hardware store that the first "no" was simply the beginning of a negotiation.

Instead of retreating, she deployed guerrilla tactics that would make modern growth hackers proud. At the Waldorf Astoria, she "accidentally" dropped a bottle of her perfume on the carpet during a charity luncheon. As the fragrance wafted through the room, women began asking, "What is that divine scent?" By the end of the lunch, she had a list of names and addresses. At the Plaza Hotel's beauty salon, she convinced the owner to let her give free facials to clients—but only to those who made appointments specifically to see her, creating artificial scarcity and buzz.

The breakthrough came through pure persistence and perfect timing. In 1948, Estée learned that Saks Fifth Avenue was renovating its cosmetics floor. She convinced Bob Fiske, the cosmetics buyer, to give her a tiny space—just enough for a small counter. Her opening order was $800, a modest sum even then. But Estée had a plan.

On launch day, she stationed herself behind the counter wearing her signature turquoise dress and pearls. But unlike other cosmetics saleswomen who waited for customers to approach, Estée stepped into the aisles. She would gently touch a woman's arm and say, "Madam, I can see you take care of your skin, but may I show you something that could make it even more beautiful?" Then came the magic: she would actually touch their faces, applying products with her own hands.

This was scandalous in 1948. Department stores were temples of formality where salespeople maintained professional distance. But Estée understood something fundamental about selling beauty: women didn't want to buy products; they wanted to buy transformation. And transformation required intimacy. She called it "Touch and Tell"—first touch the customer with your products, then tell them how beautiful they look.

The $800 worth of products sold out in two days. Fiske immediately placed a reorder for $2,000. Within six months, Estée Lauder had one of the most productive counters per square foot in Saks. The secret wasn't just the products—it was the theater.

Estée trained her saleswomen like Method actors. They wore white lab coats to convey scientific authority. They were taught to identify a customer's skin type within seconds of meeting them. Most importantly, they were instructed never to let a customer leave without something—if not a purchase, then a sample. This led to Estée's next innovation: the gift with purchase.

The idea came to her in 1953 when she noticed women at Saks hesitating over a $25 moisturizer purchase. She approached the buyer with a proposition: "What if we gave them a free lipstick when they buy the moisturizer?" The buyer thought she was crazy—giving away product would destroy margins. But Estée understood portfolio math better than anyone. The lipstick cost her $0.50 to make but retailed for $5. By giving it away, she wasn't losing $5; she was investing $0.50 to acquire a customer who would spend hundreds over her lifetime.

The gift-with-purchase promotion at Saks caused near-riots. Women lined up around the block. Competitors scrambled to copy the strategy, but Estée stayed ahead by constantly varying the gifts—sometimes a lipstick, sometimes a sample-sized perfume, always something that would require repurchase when it ran out. She had invented the beauty industry's version of the drug dealer's "first hit is free" strategy, except entirely legal and socially celebrated.

By 1953, Estée faced a different challenge. Skin care was growing, but slowly. She needed a product that would create recurring revenue, something women would buy monthly rather than every few months. The answer came from an unexpected source: her own bathtub.

Estée had been experimenting with bath oils that doubled as perfumes. Unlike traditional perfumes that women dabbed sparingly behind their ears (making a bottle last years), bath oil encouraged liberal use. She called it Youth-Dew, positioning it not as a perfume but as a bath oil that happened to smell divine. The naming was genius—"Youth" promised transformation, "Dew" evoked freshness and morning vitality. Youth-Dew launched like a rocket. In 1953, Lauder introduced her first fragrance, Youth-Dew, a bath oil that doubled as a perfume. Instead of using French perfumes by the drop behind each ear, women began using Youth-Dew by the bottle in their bath water. In the first year, it sold 50,000 bottles; by 1984, the figure had risen to 150 million.

The genius wasn't just the product but the psychology. Estée understood that American women in the 1950s wouldn't buy perfume for themselves—it was something men gave them. So she didn't call it perfume. She called it bath oil. Lauder created Youth-Dew Bath Oil in 1953. Captivating, rich and exceptionally lasting, women bought it for the bath, but, as Mrs. Lauder predicted, soon began wearing Youth-Dew as their fragrance as well. Because it was sold as a bath oil, not perfume, women felt free to enjoy and wear it every day.

The fragrance itself was revolutionary for its time—an intoxicating oriental blend of rose, jasmine, vetiver, and patchouli that was far more sensual than the light florals American women typically wore. Youth Dew sales reached an unprecedented volume of 5,000 units a week in the mid-1950s. Department store buyers who had once dismissed Estée now courted her for exclusive launches.

But Estée's ambitions extended beyond American shores. In 1960, she set her sights on London's Harrods, the most prestigious department store in Europe. The buyer initially refused to meet with her. So Estée deployed her signature move—she "accidentally" spilled Youth-Dew on the carpet near the cosmetics department. As the fragrance filled the air, customers began asking what it was. By the end of the day, Harrods had placed an order.

This wasn't just salesmanship; it was performance art. Estée understood that luxury wasn't about the product alone—it was about the story, the experience, the feeling of being special. She would personally appear at store openings, touching faces, telling women they were beautiful, making each customer feel like the only person in the room.

By 1960, Estée Lauder had graduated from a four-product startup to a serious player in American beauty. Annual sales exceeded $1 million. The company had accounts at Saks, Neiman Marcus, I. Magnin, and Marshall Field's. But more importantly, Estée had established the three pillars that would define the company for decades: premium positioning (never discount), personal service (touch and tell), and gift with purchase (customer acquisition disguised as generosity).

The foundation was set. The immigrant's daughter who started by selling face cream to her friends had built a business model that every beauty company would eventually copy. But copying the model was one thing; replicating the magic was another. Because at the heart of Estée Lauder's success wasn't just smart business tactics—it was an almost mystical understanding of what made women feel beautiful.

IV. The Youth-Dew Revolution & Going Big (1953–1967)

The Madison Avenue executives couldn't understand it. How could a bath oil outsell Chanel No. 5? In 1954, a year after Youth-Dew's launch, fragrance industry veterans gathered at the Plaza Hotel for their annual conference, and the only topic of conversation was Estée Lauder's runaway success. One executive from Coty reportedly said, "She's turned the entire fragrance business upside down. Women are bathing in perfume!"

He was right. The bath oil that doubled as a perfume took the cosmetics industry by storm. The company made over $50,000 that year just on Youth Dew itself. By 1984, that figure had jumped to over $150 million a year. What started as a clever positioning trick—calling perfume "bath oil" to circumvent cultural taboos—had become a cultural phenomenon.

The numbers told only part of the story. Youth-Dew didn't just change how women bought fragrance; it changed how they wore it. Instead of precious drops saved for special occasions, women were pouring it into their baths daily. A bottle that might have lasted a year was now consumed in weeks. Estée had discovered the holy grail of consumer products: transforming a luxury into a necessity.

But Youth-Dew's success created a new problem. Department stores that had once rejected Estée now wanted everything she could produce. Orders poured in faster than Joe's makeshift factory in Manhattan could fill them. Quality control became a nightmare. One batch of Youth-Dew came out green instead of amber. Another shipment to Neiman Marcus arrived with labels peeling off. Estée personally drove to Dallas to apologize to Stanley Marcus, arriving with a gift—a year's supply of properly labeled Youth-Dew for his wife.

This personal touch in crisis management became another Lauder signature. When Bergdorf Goodman complained about a delayed shipment, Estée didn't send a sales representative—she showed up herself, with samples for every saleswoman on the floor. When Lord & Taylor's cosmetics buyer mentioned her daughter's wedding, Estée sent a custom gift basket of products. She wasn't just building a business; she was building relationships that would last decades.

By 1957, the company faced a crossroads. Youth-Dew had made them rich, but it had also made them vulnerable. They were essentially a one-product company in an industry where novelty drove sales. Estée knew they needed to expand, but how? The answer came from an unexpected source: men.

Joe Lauder had noticed something interesting in the sales data. Women were buying Youth-Dew not just for themselves but for the men in their lives. They would dab it on their husbands' pillows, spray it on their boyfriends' scarves. "If women love this scent," Joe reasoned, "why wouldn't men want their own version?"

In 1964, they launched Aramis, named after an exotic Turkish root supposedly used as an aphrodisiac. The packaging was masculine—black and gold, heavy glass bottles that looked like they belonged in a gentleman's club. But the real innovation was the marketing. Instead of targeting men directly (who rarely bought their own grooming products), they targeted women buying gifts for men. Every Christmas, Aramis gift sets flew off the shelves.

The success of Aramis proved that Estée Lauder could be more than a one-brand company. But it also revealed a growing tension within the family business. Leonard, Estée's eldest son, had joined the company in 1958 after graduating from Wharton. He brought modern business thinking—market research, financial planning, organizational charts. Estée, who had built the company on intuition and personal relationships, was skeptical. "You can't run a beauty company from a spreadsheet," she would tell him.

The generational divide came to a head in 1965 when Leonard proposed expanding internationally beyond their single Harrods account. The investment would be massive—establishing subsidiaries, hiring local staff, adapting products for different markets. Estée worried it would dilute the brand's exclusivity. Joe played mediator, ultimately siding with Leonard. "The world is getting smaller," he argued. "If we don't go global, someone else will."

They started with Canada, then France, then Germany. Each market required different approaches. French women wanted lighter fragrances. German customers demanded extensive product information. British buyers expected formal presentations. Estée, now in her late fifties, threw herself into learning each market's peculiarities, traveling constantly, establishing the same personal relationships abroad that she had cultivated in America.

The international expansion coincided with another revolution: the changing role of women in society. By 1967, more women worked outside the home than ever before. They had their own money, their own careers, their own choices. The "touch and tell" philosophy that had worked in leisurely department stores was harder to maintain when women were shopping on lunch breaks.

Estée adapted again. She introduced "quick makeovers"—five-minute consultations for busy professional women. She created travel-sized products for the new jet set. Most presciently, she began recruiting a different type of saleswoman—not just elegant ladies who could discuss skincare, but trained professionals who understood both beauty and business.

By 1967, when business editors named Estée Lauder one of ten Outstanding Women in Business in the United States, the company's annual sales exceeded $14 million. They had 500 employees, accounts in 75 department stores, and a presence in 15 countries. The girl from Corona, Queens, had built an international empire.

But the real measure of success wasn't in the numbers. It was in how Estée had changed the industry itself. Before Lauder, cosmetics companies sold products. After Lauder, they sold experiences. Before Lauder, beauty was aspiration. After Lauder, it was accessible luxury. Before Lauder, women waited for men to buy them perfume. After Lauder, they bought it for themselves—by the bottle.

As 1967 drew to a close, Estée faced her biggest challenge yet. A young editor at Vogue named Carol Phillips had written an article that would change everything. The piece, titled "Can Great Skin Be Created?", suggested that beauty wasn't about covering up flaws but about skincare science. It was a direct challenge to everything Estée had built—the mystique, the emotion, the promise of transformation through faith rather than formulation.

But instead of fighting it, Estée would embrace it, leading to the creation of Clinique and the next phase of the Lauder empire.

V. Clinique: The First Brand Extension (1967–1975)

The Vogue article landed on Evelyn Lauder's breakfast table like a bomb. In 1967, American Vogue magazine published an article called "Can Great Skin Be Created?", written by beauty editor Carol Phillips with Norman Orentreich, discussing the significance of a skin-care routine. Evelyn, married to Leonard since 1959, had become Estée's unofficial scout for new trends. She immediately recognized this wasn't just another beauty article—it was a manifesto for a new generation of women who wanted science, not stories.

"Mother Lauder, you must read this," Evelyn said, using her pet name for her mother-in-law. Estée's first reaction was defensive. "We already create great skin," she huffed. But Leonard saw opportunity where his mother saw threat. The article's co-author, Dr. Norman Orentreich, was a legitimate dermatologist who had performed the first successful hair transplant. His involvement gave the piece scientific credibility that no beauty brand could match.

The family held a series of heated dinner meetings at Estée's apartment on East 62nd Street. Estée argued that creating a medical brand would undermine everything they'd built. "Women don't want to feel like patients," she insisted. "They want to feel beautiful." Leonard countered that a new generation of college-educated women wanted facts, not fairy tales. They wanted to know why a product worked, not just trust that it would.

Joe, ever the pragmatist, proposed a solution: create an entirely separate brand. Don't call it Estée Lauder. Give it its own identity, its own stores, its own philosophy. If it failed, it wouldn't damage the mother brand. If it succeeded, they'd own both ends of the market—emotion and science, romance and rationality.

They recruited both Carol Phillips and Dr. Orentreich to develop what would become Clinique. The name itself was carefully chosen—French enough to sound sophisticated, medical enough to convey authority. Phillips insisted on three non-negotiables: no fragrance (avoiding allergic reactions), extensive allergy testing (12,000 tests before launch), and complete transparency about ingredients.

The signature innovation was the 3-Step System: cleanse, exfoliate, moisturize. Today this seems obvious, but in 1968 it was revolutionary. Most women used one cream for everything. The 3-Step System taught them that skincare was a process, not a product. It was almost religious in its ritual—twice daily, without fail, in precise order. In April 1968, Clinique premiered as the world's first allergy tested, dermatologist-driven line at Saks Fifth Avenue in New York, launched with 117 products. Almost exactly 12 months later, in September 1968, Clinique was introduced to the world at New York's Saks Fifth Avenue. Clinique debuted with not one, not five, but 117 skincare and cosmetics products.

The visual presentation was unlike anything the beauty industry had seen. Clinical white lab coats worn by the Consultants, and the Clinique Computer, a non-electronic box of levers that determined one's skin type and skincare needs, offered women a highly informative and tailored consultation that was the first of its kind in department stores. Clinique sales women wore white lab coats, and each sales counter was fitted with "diagnostic" lamps and computers. The computer wasn't actually electronic—it was a clever system of levers and dials—but in 1968, having any kind of "computer" at a cosmetics counter was revolutionary.

The launch was both triumph and disaster. Crowds gathered, intrigued by the clinical aesthetic and the promise of dermatologist-developed products. But sales were disappointing. Women were confused: was this medicine or makeup? The white coats and lack of fragrance made products feel pharmaceutical rather than luxurious. Estée was privately furious. "We're selling aspirin, not beauty," she complained to Leonard.

But Leonard and Evelyn persisted, backed by data showing that college-educated women were Clinique's core customers—a demographic that would only grow. They refined the messaging, emphasizing that Clinique wasn't anti-beauty but pro-skin. The tagline became "Great skin is not a matter of luck. It's a matter of science."

The real crisis came in year three. A curious phenomenon occurred — in places where Clinique did well, Estée Lauder didn't, and in places where Clinique lagged behind, Estée Lauder excelled. The two brands were cannibalizing each other. Department stores complained about needing double the counter space. Some buyers forced the Lauders to choose: Estée or Clinique, but not both.

This was the moment that defined the company's future. Rather than retreat, they doubled down on differentiation. Estée Lauder would remain the emotional, aspirational brand—selling hope in a jar. Clinique would be rational and results-driven—selling science in a bottle. They even instituted a rule that no employee could work for both brands simultaneously, forcing complete separation of operations.

The gamble nearly bankrupted them. The company was also able to support the Clinique venture, which lost approximately $3 million over the first seven years. Joe Lauder, usually the voice of financial prudence, surprised everyone by backing the continued investment. "Sometimes you have to lose money to make money," he said, a philosophy that would become central to the company's acquisition strategy decades later.

The turning point came in 1972 with an unexpected product: Clinique's Dramatically Different Moisturizing Lotion. It looked like nothing special—a simple yellow cream in a pump bottle. But it worked. Women who had struggled with oily skin found it balanced without drying. Those with dry skin found it hydrating without heaviness. Word spread through college campuses and offices. By 1975 the Clinique line had become profitable.

The success validated Leonard's vision of a multi-brand portfolio, each targeting different psychographics. But it also created a template that would define the company for the next fifty years: patient capital, brand separation, and the willingness to lose money for years while building market position.

More importantly, Clinique proved that the Lauder magic wasn't just about Estée herself. The company could create entirely new brands, with different philosophies and aesthetics, and make them successful. This realization would fuel an acquisition spree that would transform a family business into a beauty conglomerate.

As the 1970s dawned, the Lauder empire had grown from one brand to three (Estée Lauder, Aramis, and Clinique), from one country to dozens, from family operation to professional corporation. But the biggest changes were yet to come. The beauty industry was about to explode with new competitors, new channels, and new consumers. And waiting in the wings was a new generation of Lauders, ready to take the company public and global.

VI. Going Public & The Acquisition Machine (1990s–2000s)

The boardroom at 767 Fifth Avenue was silent as Leonard Lauder laid out the numbers. It was 1994, and the family gathering felt more like a war council. Estée, now 86, sat at the head of the table in her signature pearls, flanked by her sons Leonard and Ronald, their wives Evelyn and Jo Carole, and the third generation—William, Aerin, and Jane. The question on the table would fundamentally change their company: Should Estée Lauder go public?

"We need capital to compete," Leonard argued. L'Oréal had been on an acquisition tear, snapping up Maybelline, Redken, and Helena Rubinstein. Procter & Gamble had entered beauty with Cover Girl and Max Factor. "If we don't grow, we die."

Estée was horrified. Going public meant opening their books, revealing secrets, answering to strangers. "We built this company by keeping our own counsel," she said. "Why should we change now?" But even she couldn't deny the math. To compete globally, they needed billions, not millions.

The compromise was quintessentially Lauder: go public, but maintain control. They structured a dual-class share system where the family's Class B shares carried ten times the voting power of public Class A shares. On November 16, 1995, the Estée Lauder Companies went public on the New York Stock Exchange at $26 a share ($6.50 on a post-split basis). Privately held for decades, Lauder's company went public in 1995. At the time, the business was valued at about $2 billion.

The IPO was a sensation. Shares popped 25% on the first day. Suddenly, the family's paper wealth exploded into real billions. But more importantly, they now had currency for acquisitions. And Leonard had a list.

The first major move had actually preceded the IPO. In 1994, they'd made a minority investment in M·A·C (Make-up Art Cosmetics), a Canadian brand founded by Frank Toskan and Frank Angelo. M·A·C was everything Estée Lauder wasn't—edgy, inclusive, beloved by makeup artists and drag queens. When Estée first saw the black packaging and bold colors, she reportedly said, "This is not beauty. This is theater. "But Leonard saw what his grandmother couldn't: the future of beauty wasn't just about making women feel beautiful in traditional ways. It was about self-expression, artistry, and inclusion. Brand acquisitions began with an investment in the Toronto-based MAC Cosmetics in 1994, which the company then acquired in 1998. The Estée Lauder Companies acquired a majority interest in M•A•C in 1994 and full ownership in 1998. In 1994, Estée Lauder acquired a 51% stake in MAC, a makeup artist cosmetics brand, and in 1998, it acquired the entire brand for an estimated $60 million.

The M·A·C acquisition became the template for everything that followed. Keep the founders involved (at least initially). Maintain brand independence. Don't impose Lauder culture—let each brand keep its DNA. Most importantly, be patient. M·A·C didn't contribute meaningful profits for three years, but by 2000 it was generating over $250 million in revenue.

The next acquisition came fast. Bobbi Brown Cosmetics, designed by the celebrated makeup artist, was acquired in 1995, as was La Mer – along with the original recipe for its supreme luxury product, Crème de la Mer, containing the nutrient-rich Miracle Broth. Bobbi Brown represented the "no-makeup makeup" look—natural, effortless beauty that was the antithesis of M·A·C's bold artistry. The brand came with its founder, Bobbi Brown herself, who insisted on maintaining creative control.

La Mer was different—a single product that sold for $450 a jar, making it one of the most expensive creams in the world. The origin story was irresistible: created by aerospace physicist Max Huber after suffering burns in a lab accident, using a mysterious fermentation process involving sound waves and moon phases. Whether the science was real or marketing genius didn't matter—women were willing to pay astronomical prices for the promise of transformation.

The company ventured into its first hair care and holistic beauty brand with Aveda in 1997. Founded by Horst Rechelbacher, Aveda brought environmental consciousness and aromatherapy to the portfolio. The $300 million price tag raised eyebrows, but Leonard saw the future: wellness and beauty converging, natural ingredients becoming premium, sustainability as luxury.

The fragrance house Jo Malone London was acquired in 1999, bringing British eccentricity and the art of fragrance combining to the portfolio. Jo Malone herself was kept on as creative director, maintaining the brand's quirky charm—scents like "Lime Basil & Mandarin" that shouldn't work but somehow did.

Each acquisition taught the company something new. M·A·C showed them how to market to younger consumers and minorities. Bobbi Brown demonstrated the power of founder stories and personal branding. La Mer proved that luxury had no ceiling if the story was compelling enough. Aveda brought expertise in alternative distribution through salons and spas. Jo Malone showed that fragrance could be playful rather than precious.

But the acquisition strategy also created challenges. By 2000, Estée Lauder Companies was running over a dozen brands, each with its own identity, distribution, and customer base. Department stores complained about needing multiple counters. The sales force was confused about priorities. Cannibalization was rampant—a customer buying Bobbi Brown was often one lost to Estée Lauder or Clinique.

The solution came from an unexpected source: Procter & Gamble. Leonard studied how P&G managed multiple detergent brands, each targeting different price points and psychographics. He implemented a similar portfolio approach: Estée Lauder for traditional luxury, Clinique for science-driven skincare, M·A·C for artistry and edge, Bobbi Brown for natural beauty, La Mer for ultra-luxury, Aveda for wellness, Jo Malone for fragrance connoisseurs.

The strategy required discipline. Brands couldn't overlap in positioning or price. Each needed distinct distribution strategies—M·A·C could be in freestanding stores, Aveda in salons, but Estée Lauder and La Mer stayed in department stores to maintain prestige. Marketing budgets were allocated based on growth potential, not legacy. Sacred cows were slaughtered—underperforming products were killed regardless of history.

By 2005, ten years after going public, the transformation was complete. Revenue had grown from $3.6 billion to $6.3 billion. The company operated in 130 countries. The portfolio included 25 brands. Market capitalization exceeded $20 billion. The family still controlled voting rights through their dual-class shares, but professional management ran day-to-day operations.

But success bred complacency. Department stores, once the company's fortress, were beginning to decline. Specialty retailers like Sephora and Ulta were growing rapidly, offering a different shopping experience that appealed to younger consumers. Digital commerce was emerging, threatening the high-touch service model that had defined Lauder for decades.

Most ominously, new competitors were emerging—not from established companies but from influencers and celebrities launching their own brands with nothing but social media and outsourced manufacturing. The barriers to entry that had protected Estée Lauder for fifty years were crumbling.

As the 2000s drew to a close, the company faced a choice: double down on what had always worked—prestige positioning, department store distribution, acquisition-led growth—or reimagine itself for a new era. The answer would come in the form of the company's largest acquisition ever, one that would either secure its future or accelerate its decline.

VII. The Tom Ford Deal & Modern Challenges (2010s–Present)

The Zoom call connected New York, Milan, and Los Angeles on a November morning in 2022. Fabrizio Freda, CEO since 2009, sat in the Lauder boardroom with William Lauder, executive chairman. On the Milan screen: Tom Ford himself, immaculate in a black suit. Los Angeles showed Domenico De Sole, Ford's business partner. The number they were discussing seemed surreal: $2.8 billion. In November 2022, the company announced it was to acquire the designer fashion house Tom Ford in a deal worth $2.8bn, with Ford remaining as creative director until at least 2023. In November 2022, the company announced it was to acquire the designer fashion house Tom Ford in a deal worth $2.8bn, with Ford remaining as creative director until at least 2023. The deal valued the total enterprise at $2.8 billion, and ELC paid approximately $2.25 billion at closing. As previously announced, the deal values the total enterprise at $2.25 billion. This amount was funded by cash on hand and proceeds from the issuance of commercial paper, as well as $250 million received from Marcolin.

This wasn't just the company's biggest acquisition—it was a statement about the future of luxury beauty. Tom Ford Beauty had been a licensed partner since 2006, but owning the brand outright meant capturing all the profits, not just licensing fees. In ELC's fiscal year ended June 30, 2022, TOM FORD BEAUTY achieved nearly 25% net sales growth as compared to the prior year, and over the next couple of years, we expect that the brand will achieve annual net sales of one billion dollars.

But the Tom Ford deal was just the latest move in a decade of transformation and crisis. The 2010s had started promisingly enough. China was booming, travel retail was exploding, and prestige beauty seemed recession-proof. By 2015, Asia-Pacific represented 23% of sales, with China leading growth at 30% annually. Hainan Island's duty-free shops became gold mines, with Chinese consumers buying multiple La Mer creams like they were stocking a pharmacy.

Then came the first warning sign. In 2016, China's anti-corruption campaign targeted luxury gifting. Suddenly, executives weren't buying Estée Lauder gift sets for government officials. Sales growth slowed from 30% to single digits overnight. The company pivoted, focusing on younger consumers and digital channels. They launched on Tmall, partnered with influencers on Weibo, created limited editions for Singles' Day.

Meanwhile, the competitive landscape was shifting dramatically. In November 2016, the company made its largest acquisition to date by acquiring California-based cosmetics company Too Faced for $1.45 billion. Founded by Jerrod Blandino and Jeremy Johnson, Too Faced brought millennial sensibility and social media savvy—products with names like "Better Than Sex Mascara" that traditional Estée would never have approved. In 2019, the company acquired Dr. Jart+. Founded in Korea in 2004, Dr. Jart+ pioneered the marketing of BB cream as a cosmetic. The $1.7 billion acquisition brought K-beauty expertise and Asian skincare innovation to the portfolio, crucial for competing in Asia where local brands were gaining ground.

But the most disruptive acquisition was yet to come. In 2021, the company acquired Canadian-based Deciem Beauty Group Inc. ELC first invested in DECIEM in 2017, increased its stake to become majority owner in 2021, and recently exercised its option to purchase the remaining interests in DECIEM after a three-year period. The total investment, net of cash, approximated $1.7 billion over the three tranches.

Deciem's flagship brand, The Ordinary, represented everything traditional Estée Lauder wasn't—radical transparency, scientific ingredient names, prices under $10. Products came in plain white packaging with names like "Niacinamide 10% + Zinc 1%" and "AHA 30% + BHA 2% Peeling Solution." The brand had been founded by Brandon Truaxe, a mercurial genius who died tragically in 2019, but his vision of democratizing skincare lived on through CEO Nicola Kilner.

The Ordinary was a phenomenon among Gen Z consumers who treated skincare like chemistry experiments, mixing and matching actives, sharing routines on TikTok. In fiscal 2024, The Ordinary ranked top two in prestige skin care in the U.S. and top four in the U.K. during the quarter ended March 31, 2024.

But as the company was building its acquisition machine, storm clouds were gathering. The first sign of trouble came in 2019 when Hong Kong protests disrupted travel retail—a channel that had become 10% of global sales. Then COVID-19 hit. Overnight, department stores closed, duty-free shopping vanished, and the high-touch service model that defined Estée Lauder became a health hazard.

The company pivoted hard to digital. Virtual consultations replaced in-store makeovers. Instagram Live became the new counter. They accelerated e-commerce investments, finally launching on Amazon after years of resistance. Digital sales jumped from 15% to 35% of revenue in a matter of months.

But the real crisis was China. The zero-COVID policy that lasted through 2022 devastated the business. Chinese consumers, who had driven growth for a decade, disappeared. Travel retail, dependent on Chinese tourists, collapsed. When China finally reopened in 2023, consumer behavior had changed. Local brands like Perfect Diary and Florasis had gained ground. The prestige premium that Western brands once commanded was eroding. The response was swift and brutal. In February 2024, Estée Lauder announced job cuts. Estee Lauder announced it's cutting 3% to 5% of its global workforce as part of a restructuring program that aims to increase profits and become more nimble in a challenging international environment. The layoffs were announced Monday as the New York cosmetic giant reported falling profits and revenue in the second quarter, and trimmed its annual profit forecast.

Then came an even bigger announcement in February 2025. Estée Lauder Companies plans to cut between 5,800 and 7,000 jobs as part of an expanded restructuring program, which includes a revamp of its executive team, the company announced Tuesday. The cuts represent up to 11% of its overall global workforce.

The challenges are multifaceted and interconnected. China, due to the ongoing softness in overall prestige beauty, including during key shopping moments. Net sales in Hong Kong SAR also declined, given the anniversary of the border reopening in the fiscal 2023 fourth quarter. Asia travel retail driven by the decrease in the first half of fiscal 2024, reflecting actions taken by the Company and its retailers to reset inventory levels, in part in response to changes in government policies that began in the second half of fiscal 2023, as well as lower conversion.

The new CEO, Stéphane de La Faverie, who took over from Fabrizio Freda in 2024, launched "Beauty Reimagined," a strategic vision aimed at restoring growth. "Today, we are excited to launch Beauty Reimagined, a bold strategic vision to restore sustainable sales growth and achieve a solid double-digit adjusted operating margin over the next few years as we aim to become the best consumer-centric prestige beauty company," said Stéphane de La Faverie, President and Chief Executive Officer. "While we recognize there is much work to do, we are confident that Beauty Reimagined is the way to realize our ambition. We are significantly transforming our operating model to be leaner, faster, and more agile, while taking decisive actions to expand consumer coverage, step-change innovation, and increase consumer-facing investments to better capture growth and drive profitability.

But the headwinds keep coming. Department stores, once the company's fortress, continue to decline. Sephora and Ulta have become the dominant beauty retailers, demanding different terms and disrupting the carefully cultivated relationships Estée built over decades. Digital natives like Glossier and Rare Beauty bypass traditional retail entirely, building billion-dollar valuations through social media alone.

Most concerning is the fundamental shift in consumer behavior. The traditional prestige beauty consumer—affluent, older, department store shopper—is being replaced by a younger, more diverse, digitally native consumer who values authenticity over aspiration, ingredients over imagery, TikTok reviews over magazine ads.

The family control structure, once a source of strength allowing long-term thinking, has become a lightning rod for criticism. That's an especially painful punch for the founding Lauder family, which holds nearly 35% of the company's outstanding shares (and 84% of voting power). Activist investors argue that the dual-class structure prevents necessary changes, protecting family interests at the expense of shareholders.

As 2024 draws to a close, Estée Lauder Companies faces an existential question: Can a company built on personal touch survive in a digital world? Can brands created for department stores thrive on social media? Can a family-controlled conglomerate move fast enough to compete with venture-backed startups?

The Tom Ford acquisition, at $2.8 billion, represents a massive bet that luxury still matters, that brand heritage has value, that there's still room at the top of the market. But with the stock down over 50% from its peak, investors are skeptical.

VIII. Playbook: Business & Investing Lessons

Walk into any department store cosmetics floor and you'll witness the Estée Lauder playbook in action, seven decades after its creation. A perfectly groomed consultant approaches with a warm smile. "Would you like to try our new serum?" she asks, already reaching for your hand. Before you can answer, she's applying product to your skin, telling you how beautiful you look, explaining the science behind the formula. Ten minutes later, you leave with a $200 purchase and a bag full of free samples. This is "Touch and Tell"—the original growth hack that built a $52 billion empire.

The genius of Touch and Tell wasn't just the physical contact, though that mattered in an era when cosmetics were sold from behind glass cases like jewelry. It was the psychological architecture: making luxury feel accessible, turning shopping into therapy, transforming saleswomen into confidantes. Estée understood that women weren't buying moisturizer; they were buying hope, transformation, the promise of a better version of themselves.

This philosophy scaled globally because it tapped into universal human desires while adapting to local contexts. In Japan, the touch was lighter, more formal. In Brazil, it was warmer, more intimate. In China, it came with education about Western beauty standards. The core remained constant: personal attention in an increasingly impersonal world.

But Touch and Tell was just the visible part of a deeper strategic framework. The real Lauder playbook was about patient capital—the willingness to lose money for years while building market position. Clinique lost $3 million over seven years before turning profitable. M·A·C took three years to contribute meaningful profits. The Ordinary seemed antithetical to everything Estée Lauder represented, yet they saw its potential and paid $1.7 billion for Deciem.

This patience was enabled by family control. Public companies rarely have the luxury of seven-year losses. Quarterly earnings calls demand immediate results. But the Lauder family's dual-class share structure—Class A shares for public investors, Class B shares with 10x voting rights for the family—created a fortress against short-term pressure. They could play the long game while competitors chased quarterly numbers.

The multi-brand portfolio strategy was perhaps their greatest innovation. L'Oréal might have pioneered it, but Lauder perfected it. Each brand occupied a distinct position: Estée Lauder for traditional luxury, Clinique for dermatological credibility, M·A·C for artistry and inclusivity, Bobbi Brown for natural beauty, La Mer for ultra-luxury, Tom Ford for modern glamour, The Ordinary for ingredient transparency.

This wasn't just segmentation; it was a sophisticated game of channel management and consumer psychology. Brands were deliberately kept separate—different management teams, different offices, even rules against employees moving between brands. This prevented homogenization while allowing each brand to maintain its founder DNA even after acquisition.

The department store relationship moat deserves special attention. For fifty years, Estée Lauder owned these relationships like a feudal lord owned land. They didn't just have counter space; they had the best counter space. They didn't just have sales associates; they had the most experienced ones. These relationships were built over decades of personal attention—Estée herself visiting store managers, remembering birthdays, sending gifts.

When digital commerce emerged, these relationships became albatrosses. Department stores demanded exclusivity that prevented online sales. They required minimum purchases that inflated inventory. They took 40-50% margins that made profitability challenging. Yet Lauder couldn't abandon them without destroying the premium positioning that justified their prices.

The acquisition discipline followed clear patterns: buy founder-led brands with authentic stories, maintain creative independence, provide operational infrastructure, be patient with profitability. They weren't buying products; they were buying founders, communities, and cultural relevance. Tom Ford wasn't just a fragrance brand; it was Tom Ford himself, his aesthetic, his Hollywood connections, his particular vision of glamour.

Premium pricing power was both a strength and a trap. La Mer at $2,000 per jar proved that price ceilings didn't exist if the story was compelling enough. But it also created vulnerability. When The Ordinary launched similar ingredients at 1/20th the price, it exposed the markup. When K-beauty brands offered innovation at lower prices, it challenged the premium-equals-quality equation.

The marketing innovations that seemed revolutionary in their time—gift with purchase, celebrity endorsements, department store exclusivity—became constraints in the digital age. Gift with purchase trained customers to never pay full price. Celebrity endorsements seemed inauthentic compared to influencer reviews. Department store exclusivity prevented the omnichannel experience digital natives expected.

The scientific innovation story is complex. Lauder spent hundreds of millions on R&D, creating legitimate breakthroughs like Clinique's Custom-Blend Foundation and La Mer's fermentation process. But much innovation was incremental—reformulations marketed as revolutions, new packaging for old formulas. The real innovation was in marketing science as science, making women feel smart for buying $300 serums.

What's most instructive for investors is how strengths became weaknesses as the market evolved. High-touch service became impossible during COVID. Department store relationships became barriers to digital transformation. Family control prevented necessary restructuring. Premium positioning left them vulnerable to value-conscious Gen Z consumers who saw through the markup.

The China dependency exemplifies the danger of concentration risk. By 2019, China and travel retail (mostly Chinese tourists) represented nearly 40% of growth. When both collapsed simultaneously—first Hong Kong protests, then COVID, then zero-COVID policy, then Chinese consumer sentiment shift—the company had no quick pivots. The inventory pipeline, designed for predictable growth, became a crushing burden of unsold products.

Yet the playbook still contains lessons for modern builders. The power of patient capital in building enduring brands. The importance of maintaining founder DNA post-acquisition. The value of portfolio diversification across price points and psychographics. The possibility of building emotional connections even in commodity categories.

The question isn't whether the Estée Lauder playbook is obsolete—it's which elements translate to a digital, diverse, direct-to-consumer world. Touch and Tell might not work on Instagram, but the principle of personal connection does. Department stores might be dying, but the need for experiential retail isn't. Celebrity endorsements might seem fake, but authentic founder stories still resonate.

For investors, the playbook reveals both the durability of well-positioned brands and the danger of strategy drift. Estée Lauder built moats that lasted decades, but moats can become prisons if you can't evolve beyond them. The company that pioneered so many industry innovations now struggles to innovate beyond its own successful formulas.

IX. Analysis & Bear vs. Bull Case

The investment case for Estée Lauder Companies in 2024 reads like a Rorschach test for how you view the future of prestige beauty. Bulls see a temporarily wounded giant with unmatched brand equity, ready to roar back as China recovers and digital transformation takes hold. Bears see a structurally challenged incumbent, hemorrhaging share to nimble competitors while clinging to a dying distribution model. Both are right—and that's the problem.

The Bull Case: Sleeping Beauty, Not Dead

Start with the portfolio. Twenty-four brands that collectively define prestige beauty. When someone thinks luxury cosmetics, they think Estée Lauder or La Mer. When they want clinical efficacy, they reach for Clinique. When they seek artistry, it's M·A·C. This isn't just market share; it's mind share accumulated over seven decades.

The Tom Ford acquisition demonstrates the bull thesis perfectly. While competitors hesitate, Lauder paid $2.8 billion for a brand that will generate $1 billion in annual sales. That's expensive but not crazy for a luxury brand with decades of growth ahead. More importantly, it shows the company can still attract premier assets. Tom Ford chose Lauder over Kering and L'Oréal—that means something.

China isn't dead; it's resting. The fundamentals remain intact: a growing middle class, increasing beauty consciousness, cultural premium on skincare. The current weakness reflects inventory destocking and consumer sentiment, not structural rejection of Western beauty brands. When sentiment turns—and it always does—Lauder is positioned to capture the rebound with established infrastructure and brand recognition.

The digital transformation is finally happening. After years of resistance, the company is embracing e-commerce, social commerce, and direct-to-consumer. Digital sales have grown from 15% to 35% of revenue. The Ordinary's success on TikTok proves they can win with younger consumers when they have the right brands and approach.

Emerging markets remain underpenetrated. India, Southeast Asia, Latin America, and Africa represent billions of potential consumers entering the beauty market. Lauder's portfolio approach—from The Ordinary's accessibility to La Mer's aspiration—allows them to capture consumers across the economic spectrum.

The fragrance category is booming. Fragrance has higher margins than skincare and stronger emotional attachment. The Tom Ford and Jo Malone acquisitions position Lauder to capture this growth. Fragrance is also more resistant to digital disruption—people still want to smell before buying.

Scientific credibility matters more than ever. As consumers become ingredient-literate, Lauder's decades of R&D investment and clinical testing become differentiators. Clinique's dermatologist heritage and La Mer's NASA connection aren't just marketing; they're moats against Instagram brands with no scientific backing.

The restructuring will work. Cutting 7,000 jobs and $1.6 billion in costs isn't just trimming fat; it's fundamental transformation. The new CEO brings fresh perspective. The organizational redesign—from brand silos to category clusters—will drive efficiency and innovation.

Valuation is compelling for patient capital. Trading at historic lows relative to earnings and book value. The dividend yield exceeds 3%. The family's aligned interests mean they won't let value erode indefinitely. This is a rare opportunity to buy a premium portfolio at a discount price.

The Bear Case: Sunset of an Empire

The China dependency is existential. This isn't a cyclical downturn; it's a structural shift. Chinese consumers have discovered domestic brands that offer similar quality at lower prices with better cultural relevance. Perfect Diary, Florasis, and Proya aren't just taking share; they're redefining the game.

Department stores are dying, and Lauder is dying with them. Macy's, Nordstrom, and Saks are closing stores and cutting inventory. The high-touch service model that defined Lauder is impossible to replicate online. Sephora and Ulta have won retail, and Lauder is just another brand on their shelves, not the crown jewel.

The portfolio is bloated and confused. Twenty-four brands create complexity without clarity. Cannibalization is rampant. The same consumer might buy Clinique, then Bobbi Brown, then The Ordinary, thinking they're exploring options when they're just shuffling Lauder's revenue. Meanwhile, operational complexity destroys margins.

Gen Z doesn't care about heritage. They want authenticity, sustainability, and inclusivity—areas where Lauder lags. Fenty Beauty redefined inclusivity. Glossier created community. Rhode skincare has Hailey Bieber. What does Estée Lauder have? A founder who died in 2004 and marketing that feels like your grandmother's perfume.

The innovation pipeline is dry. The last major breakthrough was... when? Clinique's 3-Step System in 1968? Everything since has been acquisitions or iterations. Meanwhile, Korean brands launch revolutionary ingredients monthly. Biotech companies are creating custom skincare from DNA analysis. Lauder is still selling hope in a jar while others sell proven science.

Management instability signals deeper problems. Three CEOs in five years. Constant restructuring. Mixed messages about strategy. The family control structure prevents real change—they can't sell underperforming brands, can't exit unprofitable markets, can't make hard choices that might diminish the Lauder legacy.

Competition is coming from everywhere. L'Oréal has deeper pockets and better digital capabilities. Shiseido owns Asia. Unilever and P&G are moving upmarket. Celebrity brands launch monthly with built-in audiences. Amazon is creating private-label beauty. The moats are gone.

The margin structure is breaking. Travel retail commanded premium prices because of captive audiences and duty-free psychology. That's gone. Department stores are demanding more support to offset their decline. Digital marketing costs are soaring as Apple and Google restrict targeting. Labor costs are rising. Where does margin expansion come from?

The Verdict: A Value Trap or Opportunity?

The truth lies between these extremes. Estée Lauder isn't going bankrupt, but it's also not returning to 2019 glory. This is a mature company in a mature industry facing structural headwinds and secular changes. The question isn't whether it survives but whether it thrives.

The investment case depends on your timeline and temperament. For value investors with five-year horizons, the risk-reward seems favorable. The brands have real value, the restructuring will yield results, and sentiment can't stay negative forever. But for growth investors seeking the next doubling, look elsewhere. The easy money in prestige beauty has been made.

The family control wildcard can't be ignored. The Lauders won't let their legacy crumble, but they also won't maximize shareholder value at any cost. This creates a ceiling on both downside and upside—protection from disaster but also from transformative change.

Competitive benchmarking reveals the challenge. L'Oréal trades at premium multiples with better growth. Shiseido offers pure-play Asian exposure. Coty provides turnaround optionality at lower valuations. Unilever's prestige beauty division grows faster with less complexity. Why choose Lauder's particular combination of challenges and opportunities?

The macro environment adds complexity. Inflation pressures discretionary spending. Recession fears loom. Geopolitical tensions threaten global trade. Currency fluctuations impact reported results. These aren't company-specific issues, but Lauder's geographic and price-point concentration amplifies their impact.

X. Epilogue & "If We Were CEOs"

Standing in the executive boardroom at 767 Fifth Avenue, looking out at the Manhattan skyline that Estée Lauder once conquered counter by counter, the new CEO faces choices that would have been unthinkable to the founder. Sell brands? Exit markets? Abandon department stores? The very questions would have appalled Estée, who built this empire on the principle of never retreating, only advancing.

But this is 2024, not 1946. The beauty industry has fundamentally changed, and nostalgic adherence to founder principles is a luxury even Estée Lauder Companies can't afford. If we were CEO, the transformation would be radical, swift, and probably painful—but necessary for survival.

Portfolio Rationalization: The Great Unbundling

First, we'd face the truth: twenty-four brands is about ten too many. The portfolio needs surgery, not bandages. Keep the core six: Estée Lauder (heritage), Clinique (dermatological), M·A·C (artistry), Tom Ford (modern luxury), La Mer (ultra-prestige), and The Ordinary (accessible innovation). Everything else goes on the block.

Jo Malone, Le Labo, and Kilian? Sell them to a fragrance specialist who can give them focus. Bobbi Brown? Perfect for a private equity rollup of natural beauty brands. Bumble and bumble, Aveda? Hair care deserves dedicated operators. Too Faced, Smashbox? Let them find homes where they're crown jewels, not afterthoughts.

The proceeds wouldn't go to shareholders—they'd fund transformation. This isn't financial engineering; it's strategic focus. Six brands can share infrastructure while maintaining distinct identities. Twenty-four brands create complexity that destroys value.

Digital Native Brand Strategy: Build, Don't Buy

Instead of acquiring the next hot Instagram brand for billions, we'd incubate our own. Create a venture studio within Lauder, staffed by people under 30 who actually understand TikTok. Give them $50 million, operational independence, and a mandate: build five brands that could never come from traditional Lauder.

One brand for sustainability zealots—refillable packaging, carbon-neutral shipping, ingredient transparency that makes The Ordinary look opaque. Another for the skinimalism movement—three products maximum, multifunctional, affordable luxury. A third for men who won't buy "cosmetics" but will buy "performance grooming." A fourth leveraging AI for custom formulations. A fifth that exists only in the metaverse, selling digital beauty for avatars before physical products.

Most will fail. That's fine. One success pays for five failures, and the learning transforms the core business. This isn't innovation theater; it's survival training.

China Recovery Playbook: Local for Local

The dream of selling American luxury to Chinese consumers is over. The new reality requires humility and partnership. We'd create a separate China entity, majority-owned but locally operated. Hire Chinese executives, develop China-specific products, partner with local influencers who've never heard of Estée Lauder.

Launch a new brand created in China, for China, by Chinese teams. Not a Western brand with Chinese characteristics, but a Chinese brand that happens to have Lauder's operational excellence behind it. Price it between domestic brands and Western imports. Make it a source of national pride, not foreign aspiration.

For existing brands, radical localization. Clinique becomes a telemedicine platform partnering with Chinese dermatologists. M·A·C collaborates with Chinese artists and museums. The Ordinary creates education content for Douyin, teaching chemistry alongside commerce.

Gen Z and Social Commerce: Meet Them Where They Are

The department store strategy was about going where customers shopped. Today's customers shop on their phones, in their feeds, during livestreams. We'd abandon the fiction that we can drive them to our channels and instead embed in theirs.

Every brand gets a Chief TikTok Officer—someone under 25 with full authority over brand presentation on the platform. Products designed for social sharing—packaging that photographs well, textures that look amazing on video, names that become hashtags.

Partner with gaming platforms. Sponsor esports teams. Create Roblox experiences. Sell virtual cosmetics in Fortnite before physical ones in stores. This isn't marketing; it's distribution. Gen Z doesn't distinguish between digital and physical reality—neither should we.

Launch "Estée Labs"—a direct-to-consumer platform for experimental products. Limited runs, community voting on what goes into production, radical transparency about costs and margins. Make customers co-creators, not just consumers.

The Future of Prestige Beauty: Redefining Luxury

Luxury used to mean exclusivity—high prices, limited distribution, aristocratic aspiration. That's dead. New luxury means efficacy, sustainability, and authenticity. We'd redefine prestige around results, not price.

Create an "Efficacy Institute"—independent testing that validates every claim with published, peer-reviewed research. Not marketing disguised as science, but actual science that happens to be marketable. Partner with universities, publish failures alongside successes, make transparency a competitive advantage.

Sustainability becomes table stakes. Every product gets a carbon score, a water score, a social impact score. Not buried in corporate reports but printed on packaging. Make the true cost visible and own it. Premium prices justified by premium responsibility.

Develop "Beauty as a Service"—subscription models that aren't just recurring revenue but ongoing relationships. Monthly consultations, quarterly reformulations based on seasonal needs, annual skin assessments using AI and computer vision. The products are almost secondary to the service.

What Would Estée Do? The Return to First Principles

Here's the paradox: truly honoring Estée Lauder's legacy means abandoning her tactics while embracing her principles. She didn't succeed by following industry conventions but by breaking them. She didn't accept the market as it was but created the market she wanted.

Estée would understand that Touch and Tell in 2024 doesn't mean physical touch but emotional connection. She'd recognize that department stores were just yesterday's channel, replaceable when something better emerged. She'd see that giving away samples was never about the free lipstick but about removing barriers to trial.

Most importantly, she'd understand that beauty is still about transformation—not just physical but psychological, not just individual but social. The products change, the channels evolve, the consumers transform, but the fundamental human desire to feel beautiful, confident, and valued remains constant.

The company that Estée Lauder built isn't dying—it's metamorphosing. The question is whether it emerges as a butterfly or gets stuck in the chrysalis. The answer depends on whether current leadership has the courage to be as revolutionary as their founder, to build the beauty company of 2050 rather than preserving the one from 1950.

If we were CEO, the north star would be simple: What would a 20-year-old Estée Lauder do if she were starting today? She wouldn't be selling door-to-door because doors are digital now. She wouldn't be courting department stores because influence lives online. She wouldn't be mixing creams in her kitchen because biotechnology exists.

But she would still be touching faces—through screens. She would still be telling women they're beautiful—through community. She would still be giving gifts with purchase—through experience. She would still be building an empire—just differently.

The Estée Lauder Companies doesn't need a CEO who manages decline gracefully. It needs a leader who channels the founder's revolutionary spirit, who understands that honoring legacy means creating the future, not preserving the past. The beauty empire built on touch and tell must become the beauty ecosystem built on connect and compel.

The foundation Estée laid remains solid. The question is whether her heirs—biological and corporate—have the courage to build something new upon it. Because in beauty, as in business, standing still is moving backward. And Estée Lauder never moved backward.

XI. Recent News

The recent news paints a picture of a company in deep transformation. On February 4, 2025, The Estée Lauder Companies Inc. (NYSE: EL) today launched Beauty Reimagined, its new strategic vision, and reported its financial results for the second quarter ended December 31, 2024. "Today, we are excited to launch Beauty Reimagined, a bold strategic vision to restore sustainable sales growth and achieve a solid double-digit adjusted operating margin over the next few years as we aim to become the best consumer-centric prestige beauty company," said Stéphane de La Faverie, President and Chief Executive Officer. "While we recognize there is much work to do, we are confident that Beauty Reimagined is the way to realize our ambition. We are significantly transforming our operating model to be leaner, faster, and more agile, while taking decisive actions to expand consumer coverage, step-change innovation, and increase consumer-facing investments to better capture growth and drive profitability.

The restructuring continues to expand. Estée Lauder Companies plans to cut between 5,800 and 7,000 jobs as part of an expanded restructuring program, which includes a revamp of its executive team, the company announced Tuesday. The cuts represent up to 11% of its overall global workforce, with plans to eliminate some positions after retraining and redeploying certain employees, the company said.

Financial performance remains challenged. The company reported its financial results for the third quarter ended March 31, 2025. Stéphane de La Faverie, President and Chief Executive Officer, said, "In the third quarter of fiscal 2025, we delivered our organic sales outlook and exceeded profitability expectations. However, the underlying trends show continued pressure, with Estée Lauder Companies (NYSE: EL) reported Q3 fiscal 2025 results showing a 10% decrease in net sales to $3.6 billion, with organic sales declining 9%. The company's gross margin expanded 310 basis points to 75.0%, while operating margin declined to 8.6% from 13.5%. Diluted EPS decreased to $0.44 from $0.91 in the prior year, with adjusted EPS falling to $0.65 from $0.97.

Looking ahead, the company faces significant headwinds from tariffs and geopolitical tensions. Estee aims to return to sales growth in fiscal 2026, its CEO said, adding that this depends on the resolution of the recently enacted tariffs to mitigate potential negative impacts. The U.S. has imposed 145% tariffs on China, while Beijing put a 125% levy on American imports into the country. To navigate the tariff situation, Estee expects to reduce imports into China from the U.S. to 10% from 25%.

Leadership changes continue as the company reshapes for the future. NEW YORK--(BUSINESS WIRE)--The Estée Lauder Companies Inc. (NYSE: EL) announced today that Aude Gandon has been appointed Chief Digital & Marketing Officer (CDMO), effective August 1, 2025. Additionally, The Estée Lauder Companies (NYSE: EL) has appointed Lisa Sequino as the new President of its Makeup Brand Cluster, effective June 9, 2025. In this role, she will lead the strategic direction and global growth of the company's makeup portfolio, including M·A·C, Bobbi Brown, Too Faced, Smashbox, and GLAMGLOW. Sequino, who brings over two decades of beauty industry experience, returns to Estée Lauder after previously serving in senior roles, including SVP positions.

Wall Street remains divided on the outlook. Based on 14 Wall Street analysts offering 12 month price targets for The Estée Lauder Companies in the last 3 months. The average price target is $95.29 with a high forecast of $110.00 and a low forecast of $84.00. The average price target represents a 6.03% change from the last price of $89.87. The consensus rating is Moderate Buy which is based on 6 buy ratings, 8 hold ratings and 0 sell ratings.

The stock's technical indicators suggest continued weakness. The Estee Lauder Companies Inc (The) stock holds sell signals from both short and long-term Moving Averages giving a more negative forecast for the stock. On corrections up, there will be some resistance from the lines at $90.66 and $89.64. A break-up above any of these levels will issue buy signals. A sell signal was issued from a pivot top point on Wednesday, August 13, 2025, and so far it has fallen -9.12%. Further fall is indicated until a new bottom pivot has been found.

XII. Links & Resources

Primary Sources and SEC Filings: - Estée Lauder Companies Investor Relations: elcompanies.com/investors - SEC EDGAR Database - EL Filings: sec.gov/edgar - Annual Reports (10-K) and Quarterly Reports (10-Q) - Proxy Statements (DEF 14A) for governance information

Key Books and Articles: - "Estée: A Success Story" by Estée Lauder (1985) - Founder's autobiography - "Estée Lauder: Beyond the Magic" by Lee Israel (1985) - Unauthorized biography - "The Company I Keep" by Leonard Lauder (2020) - Insider perspective from former CEO - Harvard Business School Case Studies on Estée Lauder Companies

Industry Reports: - Euromonitor International - Global Beauty and Personal Care Reports - McKinsey & Company - The State of Fashion: Beauty reports - Bain & Company - China Luxury Report series - NPD Group - Prestige Beauty Industry Reports - Circana (formerly IRI) - Beauty retail tracking data

Financial Analysis: - Bloomberg Terminal - EL US Equity analysis - FactSet - Consensus estimates and peer comparisons - S&P Capital IQ - Credit analysis and ratings - Morningstar - Independent equity research

Trade Publications: - Women's Wear Daily (WWD) - Beauty Inc. section - Glossy Beauty - Digital transformation coverage - Beauty Independent - Indie brand perspective - Cosmetics Business - Industry news and analysis - Happi Magazine - Technical and regulatory coverage

Interview Transcripts and Presentations: - Investor Day presentations (available on company website) - Earnings call transcripts (via Seeking Alpha, Bloomberg) - Industry conference presentations (CAGNY, Goldman Sachs Global Retailing) - Executive interviews (CNBC, Bloomberg TV, Forbes)

Competitive Intelligence: - L'Oréal annual reports and investor materials - Shiseido company filings and presentations - Coty turnaround plan documents - Unilever Prestige division updates - Private company analysis (via PitchBook, CB Insights)

Historical Archives: - The Estée Lauder Companies Archives (by appointment) - Smithsonian National Museum of American History - Cosmetics collection - Fashion Institute of Technology - Beauty Culture exhibition materials - New York Historical Society - Department store history

Digital and Social Media Analytics: - Tribe Dynamics - Earned Media Value tracking - Launchmetrics - Influencer and brand performance - Brandwatch - Social listening and sentiment analysis - SimilarWeb - Digital traffic and e-commerce data - Sensor Tower - Mobile app analytics

Regulatory and Compliance: - FDA Cosmetics regulation updates - EU Cosmetics Regulation (EC) No 1223/2009 - China NMPA (formerly CFDA) requirements - California Safe Cosmetics Act compliance - PCPC (Personal Care Products Council) guidelines

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube