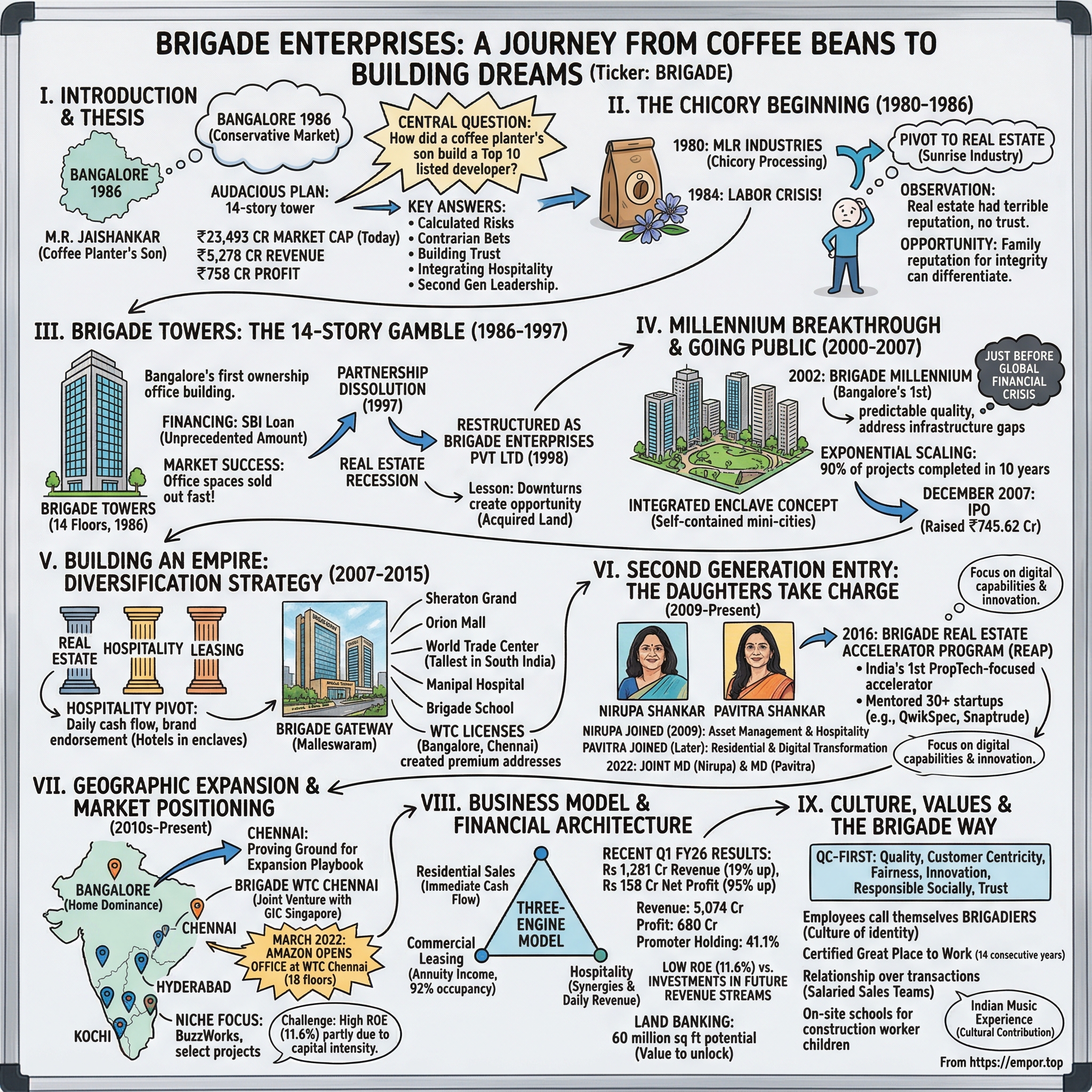

Brigade Enterprises: From Coffee Beans to Building Dreams

I. Introduction & Episode Thesis

Picture this: It's 1986 in Bangalore—a city of gardens, not yet the Silicon Valley of India. Office buildings rarely exceed four floors. The skyline is dominated by trees, not towers. Into this conservative real estate market walks M.R. Jaishankar, a coffee planter's son from Chikmagalur, with an audacious plan to build a 14-story office complex. His partners think he's lost his mind. The State Bank of India has never financed anything like this. Yet within two decades, this same man would build one of South India's most trusted real estate brands, Brigade Enterprises, now commanding a market capitalization of ₹23,493 crores. The story of Brigade Enterprises isn't just about building towers—it's about how a series of calculated risks, near-disasters, and contrarian bets created one of India's top 10 listed developers by market capitalization. With revenue of ₹5,278 crores and profit of ₹758 crores, Brigade stands as a testament to the power of vision in an industry notorious for broken promises and unfinished projects.

The central question driving this narrative: How did a coffee planter's son, armed with an MBA from a regional university and zero construction experience, build one of South India's most trusted real estate brands? The answer lies not in a single brilliant move, but in a series of unconventional decisions that repeatedly defied industry wisdom—from building Bangalore's first 14-story tower when the city had just one ownership office building, to integrating hospitality with real estate when others saw them as separate worlds, to bringing daughters into leadership roles in a male-dominated industry.

This is the story of Brigade Enterprises—a journey from chicory powder to concrete towers, from family partnerships to public markets, from Bangalore's leafy neighborhoods to Chennai's IT corridors. It's about understanding not just what was built, but why it endured when so many others crumbled during India's numerous real estate cycles. As we'll see, the Brigade playbook offers lessons far beyond real estate: about timing markets, building trust in low-trust industries, and managing the delicate transition from founder to second generation while maintaining the entrepreneurial edge that created the empire in the first place.

II. The Chicory Beginning: MR Jaishankar's Journey (1980-1986)

The year is 1984. In a small industrial unit on the outskirts of Bangalore, the acrid smell of roasting chicory fills the air. Workers are agitated, voices rising above the mechanical hum of the grinding machines. A labor leader pounds his fist on a makeshift table, demanding better wages, threatening to shut down operations. Standing across from him, a young entrepreneur named M.R. Jaishankar watches his carefully built chicory business—MLR Industries—teeter on the edge of collapse.

Years later, Jaishankar would tell interviewers with a wry smile: "I should warmly thank the labour leader who created the problem!" Because that crisis, that moment of near-ruin, would push him toward an industry he knew nothing about—real estate—and set in motion the creation of what would become Brigade Enterprises.

But let's rewind. M.R. Jaishankar came from a reputed family of coffee planters in Chikmagalur, a hill town nestled in Karnataka's Western Ghats where morning mist mingles with the aroma of coffee blossoms. His family had been in the coffee business for generations, known throughout the region not just for their agricultural prowess but for their business integrity and philanthropy—a reputation that would later prove invaluable when Jaishankar needed credibility in an industry riddled with fly-by-night operators.

After earning his MBA from Mysore University in 1977—not IIM Ahmedabad or Bangalore, but a solid regional institution—Jaishankar did what many ambitious young MBAs did: joined a corporate job. His brief stint as a Management Trainee at UB-MEC Batteries taught him the mechanics of running a business, but the entrepreneurial itch inherited from generations of independent coffee planters wouldn't let him rest.

In 1980, at age 27, Jaishankar launched MLR Industries. The business model was elegantly simple: manufacture chicory, the roasted root that South Indians blend with coffee powder to add richness and that distinctive bitter-sweet flavor to their morning filter coffee. It was a business he understood viscerally—coffee was in his blood, and chicory was coffee's essential companion in South Indian households. The growth was spectacular. Within four years, MLR Industries soon became the largest supplier to Brooke Bond India Ltd—then one of India's most prestigious consumer goods companies and part of the global Unilever empire. This wasn't just about making chicory; it was about earning the trust of a multinational corporation known for its exacting standards. For a small-scale entrepreneur from Karnataka, this was validation at the highest level.

But 1984 brought the crisis that would change everything. In 1984, the company faced serious industrial relations' problems and M.R. Jaishankar decided to diversify his entrepreneurial efforts. The labor unrest wasn't just a temporary disruption—it represented a fundamental challenge to the business model. In the small-scale manufacturing sector of 1980s India, labor problems could destroy a business overnight. Strikes, gheraos (where workers surround management), and militant union demands were common. For Jaishankar, watching his carefully built enterprise threatened by forces beyond his control was both terrifying and enlightening.

It was formed with no clear plan or vision for the business, at a time when I was planning to diversify from the chicory processing business I had started in 1980, because of a serious industrial relations problem in 1984. (In retrospect, I should warmly thank the labour leader who created the problem!)

The decision to pivot wasn't immediate. He continued to run MLR Industries till 1991, displaying the kind of prudent risk management that would later characterize Brigade's approach to real estate cycles. But even as he maintained the chicory business, Jaishankar's mind was racing toward something bigger. His market research confirmed what his intuition suggested: property development would be a sunrise industry in liberalizing India.

At that time, property developers were a suspect group; not known for trust and reliability, and notorious for focusing on short-term gains and totally lacking in a long-term vision. There were just a couple of organisations in the sector, struggling to earn respectability. Expecting people to pay even before the building was ready, was a counter-intuitive phenomenon in the business world.

This was the landscape Jaishankar surveyed in 1985: an industry with terrible reputation, no institutional financing, and a business model that required customers to pay upfront for something that didn't yet exist. Most sensible businessmen would have run in the opposite direction. But Jaishankar saw opportunity precisely where others saw obstacles. His family's century-old reputation for integrity in the coffee business could be the differentiator in an industry desperate for credibility.

The founder-CMD of Brigade Group, M.R. Jaishankar, comes from a reputed family of coffee planters from the hill town of Chikmagalur, in the Western Ghats, Karnataka. For over a hundred years, his family has been well known in the region for their business integrity and philanthropy.

The chicory crisis had taught him a crucial lesson: in manufacturing, you're at the mercy of labor, raw materials, and established competitors. But in real estate—if you could solve the trust problem—you could create value at a scale impossible in processing agricultural commodities. The margins were better, the asset creation was permanent, and most importantly, you could build a brand that transcended individual products.

III. Brigade Towers: The 14-Story Gamble (1986-1997)

October 10, 1986. Brigade Road, Bangalore. A small group gathers for a ground-breaking ceremony that would have seemed ludicrous to any rational observer. In a city where the tallest commercial building barely crossed four floors, where owning office space was an alien concept, where developers were viewed with the same suspicion as snake-oil salesmen, M.R. Jaishankar is laying the foundation stone for a 14-story office tower.

His partners think he's lost his mind. His partners were in favour of a cautious venture of a G+3 floors office complex since there was just one ownership office building in Bangalore at that time. But Jaishankar's vision was evident in the very first Brigade project, Brigade Towers that he launched. The conservative approach would have been sensible—test the market, minimize risk, build credibility gradually. But Jaishankar wasn't thinking incrementally. He was making a bet on Bangalore's future as India's emerging commercial hub.

Mr Jaishankar established a partnership firm, Brigade Investments (1986), with the idea of executing just one project. The structure was deliberately modest—a partnership with family and two family friends, conceived as a single-project venture. I started the partnership firm Brigade Investments, which created Brigade Towers, with the support of my family and two family friends. The firm was a single-project venture and the result of an earlier missed opportunity by the family to invest in a prime real estate project in Bangalore.

The financing challenge was monumental. Banks didn't lend to real estate developers—the sector was too risky, too unorganized, too riddled with failures. But Jaishankar managed to pull off what seemed impossible: convincing the State Bank of India to provide a Rs 10 million loan. This wasn't just any loan—it was an unprecedented amount for a property development project by SBI at that time. How did a chicory manufacturer with no track record in construction convince India's largest bank to make such a bet? The answer lay partly in Jaishankar's ability to paint a vision, partly in his family's reputation, but mostly in an audacious bet on scale itself. This collaborative space is situated on the 14th floor of the iconic and the first tallest commercial project Brigade Towers (1986) offering spectacular views of Bengaluru's cityscapes. By proposing something unprecedented—Brigade Towers, the first 14-storied building in Bangalore (and, at that point of time, one of the very few projects to market ownership offices) was an instant success.

The construction challenges were immense. In 1986 Bangalore, finding contractors who could build beyond four floors was difficult. Elevators had to be imported. Building materials for high-rise construction were scarce. Every aspect of the project pushed against the boundaries of what was possible in the city's nascent real estate market. Yet Jaishankar persisted, driven by a conviction that Bangalore was on the cusp of transformation.

The market response vindicated his vision spectacularly. Brigade Towers, the first 14-storied building in Bangalore (and, at that point of time, one of the very few projects to market ownership offices) was an instant success. Office spaces sold out before construction was complete—a phenomenon unheard of in Bangalore's conservative business community. Companies that had never considered owning their offices suddenly saw the appeal of controlling their real estate destiny. The building became a landmark, literally changing Bangalore's skyline and metaphorically changing its ambitions.

But success brought its own complications. The partnership that had enabled Brigade Towers began to fray. Mr Jaishankar established a partnership firm, Brigade Investments (1986), with the idea of executing just one project. The original conception was limited—execute one project, divide the profits, move on. But Jaishankar saw bigger possibilities. He wanted to build more, expand faster, take bigger risks. His partners, having achieved their goal, preferred caution.

The tension simmered through the early 1990s. While Brigade Towers generated steady returns, Jaishankar chafed at the constraints. He studied markets in Mumbai and Delhi where developers were building multiple projects simultaneously. He saw the opportunity to create not just buildings but integrated developments—offices, retail, residential, all interconnected. But every ambitious proposal met resistance from partners content with the status quo.

The breaking point came in 1997, at the worst possible time. India was in the grip of a real estate recession. Property prices had crashed. Several developers had gone bankrupt. It was precisely the wrong moment to dissolve a partnership and restructure a business. Yet that's exactly what happened. The lack of consensus on growth strategy with a partner led to the partnership firm Brigade Investments being dissolved in 1997, to be restructured as Brigade Enterprises Pvt Ltd in 1998, at the height of the real estate recession.

For Jaishankar, this was both liberation and terror. He was finally free to pursue his vision, but he was doing so when the entire industry was in retreat. Banks were calling in loans. Buyers had disappeared. Construction had ground to a halt across the city. Starting fresh as Brigade Enterprises Pvt Ltd in 1998 meant rebuilding everything—relationships, credibility, capital—during the industry's darkest hour.

Yet this crisis period would prove formative. Without partners to satisfy, Jaishankar could make contrarian bets. While others retreated, he quietly acquired land at distressed prices. While competitors downsized, he retained his core team. While the market obsessed over survival, he planned for the next upturn. The lessons from the chicory crisis had taught him that downturns create opportunities for those brave enough to see beyond the immediate pain. The foundation was being laid for Brigade's next transformation.

IV. The Millennium Breakthrough & Going Public (2000-2007)

The year 2002 marked a watershed moment not just for Brigade, but for Indian real estate itself. After surviving the recession that had decimated lesser developers, Jaishankar unveiled Brigade Millennium—a project so ambitious in scope that even his supporters questioned his sanity. This wasn't just another apartment complex or office building. It was Bangalore's first integrated enclave project, a self-contained mini-city that would redefine urban living. Brigade Millennium—Bangalore's first integrated enclave project, launched in 2002—brought cheer to Brigade Group. We have not looked back since then. The concept was revolutionary for its time: instead of building standalone apartments or offices, create a self-contained ecosystem where residents could live, work, shop, and play without leaving the complex. Located in JP Nagar, spread across 22 acres, Brigade Millennium wasn't just selling square feet—it was selling a lifestyle.

Brigade Group pioneered the concept of integrated enclaves in Bangalore and has already completed Brigade Millennium, Brigade Metropolis and Brigade Gateway that have become landmarks in Bangalore. The integrated enclave model addressed a fundamental problem in Bangalore's rapid urbanization: infrastructure couldn't keep pace with development. Roads were clogged, power was erratic, water was scarce. By creating self-sufficient mini-cities with their own amenities, Brigade could offer predictable quality of life in an unpredictable urban environment.

The numbers tell the story of transformation. Of the 20 million square feet promoted by the Group since inception, 90% (comprising a wide range of projects) was completed in the last ten years. This wasn't just growth—it was exponential scaling enabled by the integrated enclave model's higher margins and customer stickiness.

The period from 2002 to 2007 saw Brigade perfect this playbook. Each new project became more ambitious. Brigade Metropolis in Whitefield targeted the IT crowd. Brigade Gateway in Malleswaram aimed at established families. Each enclave was carefully positioned for different demographics, but all shared the core promise: complete lifestyle solutions, not just real estate products. The decision to go public in December 2007 represented the culmination of this growth phase. Brigade Enterprises IPO bidding started from December 10, 2007 and ended on December 13, 2007. The shares got listed on BSE, NSE on December 31, 2007. The timing seemed perfect—India's economy was booming, real estate was hot, and investor appetite was strong. The IPO raised ₹745.62 crores through a fresh issue of 1.91 crore shares at ₹390 per share.

But the timing proved to be a double-edged sword. The IPO came just months before the global financial crisis would devastate real estate markets worldwide. While Brigade had successfully transitioned from a partnership to a public company, it would soon face its greatest test yet. The integrated enclave model that had driven growth would now be tested in the crucible of a global recession. The question wasn't whether Brigade could grow, but whether it could survive what was coming.

V. Building an Empire: Diversification Strategy (2007-2015)

The 2008 financial crisis hit Indian real estate like a sledgehammer. Property prices crashed 40%. Buyers vanished. Banks stopped lending. For Brigade, now a publicly listed company with quarterly earnings pressure, this was trial by fire. But while competitors retreated to their core businesses, Jaishankar made a counterintuitive move: he doubled down on diversification.

It operates through the following segments; Real Estate, Hospitality, and Leasing. The Real Estate segment develops residential space and commercial space for sale. The Hospitality segment operates hotels, such as Grand Mercure and Holiday Inn RCR in Bengaluru, Sheraton Grand, Holiday Inn in Chennai, Grand Mercure in Mysore, Four Points by Sheraton in Kochi, and Grand Mercure in GIFT City, Ahmedabad. The Leasing segment consists of office and retail space.

The hospitality pivot wasn't random. Jaishankar had observed that in every real estate cycle, hotels suffered less volatility than residential or commercial properties. Hotels generated daily cash flows, provided stable employment, and most importantly, enhanced the value of Brigade's integrated enclaves. A Sheraton or Marriott wasn't just a hotel—it was a brand endorsement that elevated everything around it.

The crown jewel of this strategy emerged in Brigade Gateway, the flagship mixed-use development that would redefine Bangalore's Malleswaram neighborhood. For its mixed-use enclave Brigade Gateway, with unprecedented scale and scope, Brigade brought in the world-class expertise of the internationally renowned architectural firm HOK of New York resulting in the creation of one of the best mixed-use developments of the country. The numbers at Brigade Gateway were staggering: a 40-acre integrated enclave featuring the 128-meter tall World Trade Center (the tallest commercial building in South India at the time), the massive Orion Mall, Sheraton Grand Hotel (the first Sheraton to be crowned 'Grand' in South-Asia), Manipal Hospital, Brigade School, luxury residences, and even an artificial lake. Sheraton Grand Bangalore Hotel at Brigade Gateway, first Sheraton to be crown 'Grand' in South-Asia, is located in the neighbourhood of Malleswaram. The Hotel forms a part of the expansive Brigade Gateway lifestyle enclave comprising of the World Trade Centre office tower, the massive Orion Mall and Multiplex, green space, manmade lake, and more. Connected to the World Trade Center, Bangalore (WTC); and the Orion Mall, via a sky bridge.

The World Trade Center licenses represented another strategic coup. By securing WTC licenses for both Bangalore and later Chennai, Brigade wasn't just building office towers—it was creating globally recognized business addresses that commanded premium rents. At 128 m, the WTCB is the tallest commercial building in south India and was the tallest building in Bangalore between 2010 and 2013.

The hospitality partnerships with Marriott, Accor, and InterContinental Hotels Group transformed Brigade from a developer into a hospitality player. These weren't franchise arrangements where Brigade simply built and handed over—these were management contracts where Brigade retained ownership while international operators ran the hotels. This model provided multiple revenue streams: development profits, rental income, and a share of hotel operations.

By 2015, Brigade had created a virtuous cycle. Each hotel enhanced the value of surrounding residential and commercial properties. Each successful enclave made it easier to acquire land for the next project because landowners saw Brigade as a value creator, not just a builder. Banks, initially skeptical of mixed-use developments, now competed to finance Brigade projects because the diversified revenue streams reduced risk.

The financial architecture was equally sophisticated. While residential sales provided immediate cash flows, commercial leasing created annuity income, and hotels generated daily revenues. This three-engine model meant Brigade could weather downturns in any single segment—a critical advantage that would be tested repeatedly in India's volatile real estate market.

VI. Second Generation Entry: The Daughters Take Charge (2009-Present)

In 2009, as the world recovered from the financial crisis, M.R. Jaishankar made a decision that raised eyebrows in India's male-dominated real estate industry: he brought his younger daughter, Nirupa Shankar, into the business. This wasn't tokenism or a ceremonial role. With Ms Nirupa Shankar, the younger daughter of the founder, Mr M.R. Jaishankar joining the business in 2009, the business has witnessed the entry of the second-generation and diversification in the hospitality vertical. Nirupa has over 10 years of work experience and oversees the operations & strategy for Brigade's self-managed assets.

Nirupa didn't come in as the founder's daughter expecting a corner office. She had worked outside the family business, understood corporate dynamics beyond Brigade's walls, and brought fresh perspectives on asset management and hospitality operations. Her entry coincided with a crucial inflection point: Brigade needed to evolve from a developer that built and sold to an asset manager that built, owned, and operated.

The transformation accelerated when her sister, Pavitra Shankar, joined the leadership team. In 2022, she was appointed joint managing director, while her sister, Pavitra Shankar, became the managing director. This wasn't just succession planning—it was a deliberate restructuring of Brigade for the next generation of Indian real estate. The most visible manifestation of this new generation's approach came in 2016 with the launch of Brigade Real Estate Accelerator Program (REAP). In 2016, she oversaw the launch of the Brigade Real Estate Accelerator Program (REAP), an initiative aimed at supporting tech startups in real estate. This wasn't just corporate CSR or innovation theater—it was a strategic bet that technology would fundamentally transform real estate.

A brainchild of Nirupa Shankar, Director, Brigade Hospitality and daughter of Brigade Group's Chairman Mr. M. R. Jaishankar, Brigade REAP is the first initiative of its kind in India, set up with the aim to give innovators and inventors in India, in sectors relevant to real estate, an organized approach to help build sustainable and scalable businesses.

REAP became Asia's first PropTech-focused accelerator, mentoring over 55 startups across 11 cohorts by 2022. The accelerator has so far mentored 30 startups, of which 12 have received external funding. This includes startups like QwikSpec, Snaptrude, WEGoT, AKP, PParke, Renewate, Clairco, CREMatrix, PropsAMC, Exprs, Nanorama and PropVR.

The second generation brought a different lens to the business. Where Jaishankar had focused on building physical assets, his daughters saw the opportunity in building digital capabilities. BuzzWorks, Brigade's co-working arm, wasn't just about renting desks—it was about creating flexible workspaces that could adapt to post-pandemic realities. The push into PropTech wasn't just about investing in startups—it was about transforming Brigade's own operations with technology.

Family dynamics and succession planning in Indian businesses often destroy value. Brothers fight, children rebel, professional managers clash with family members. Brigade avoided these pitfalls through deliberate structure. The daughters didn't parachute into top roles—they worked their way up, earned credibility with professional teams, and brought complementary skills. Pavitra focused on residential strategy and digital transformation. Nirupa concentrated on hospitality and asset management.

The cultural transformation was equally significant. Employees adopting the identity of "brigadiers", as they preferred to be called, wasn't just corporate branding—it reflected a shift from hierarchical family business to professional organization with family stewardship. The second generation understood that attracting and retaining talent meant creating a culture that valued meritocracy alongside family values.

By bringing innovation to the core of Brigade's strategy through REAP and other initiatives, the second generation wasn't rejecting their father's legacy—they were extending it. Where Jaishankar had built trust through quality construction, his daughters built trust through technology adoption. Where he had created integrated enclaves, they created integrated ecosystems connecting physical and digital realms.

VII. Geographic Expansion & Market Positioning (2010s-Present)

While Brigade had established dominance in Bangalore, the real test of its model would come in expansion beyond its home market. The Brigade Group also has operations in Mangalore, Mysore, Chennai, Kochi, Hyderabad, Chikmagalur, Ahmedabad and a representative office in Dubai. Each city represented different challenges, different competitive dynamics, and different customer preferences.

Chennai became the proving ground for Brigade's expansion playbook. The Chennai market was dominated by established local players who understood Tamil sensibilities and had deep political connections. Brigade's approach wasn't to compete head-on but to bring something Chennai didn't have—the integrated enclave model perfected in Bangalore, anchored by a World Trade Center that would give Chennai global business credibility. The Chennai WTC became operational in March 2020—right as COVID-19 hit. Most developers would have panicked. But Brigade's partnership with Singapore's sovereign wealth fund GIC for the project provided financial stability. The project is a Joint Venture between Brigade & GIC (Singapore Investment Corporation). More importantly, the WTC's positioning as Chennai's tallest commercial establishment (28 floors) with 1.8 million square feet of office space attracted global tenants seeking post-pandemic safety and quality.

The gamble paid off spectacularly. In March 2022, Amazon opened its office at the WTC, occupying 18 floors across 77,000 square metres (830,000 sq ft) to accommodate 6,000 employees. This single lease validated Brigade's entire Chennai strategy—when Amazon chooses your building for thousands of employees, you've arrived as a serious player.

Hyderabad presented different challenges. The market was dominated by DLF, Prestige, and local powerhouses with deep political connections. Brigade couldn't compete on scale or relationships. Instead, it focused on niche segments—managed office spaces through BuzzWorks, select residential projects in emerging corridors, and hospitality assets that leveraged its operational expertise.

The geographic expansion revealed both Brigade's strengths and limitations. In markets where the integrated enclave model could be replicated—Chennai, Kochi—Brigade succeeded. In markets requiring different approaches—Hyderabad's land-aggregation game, NCR's scale requirements—progress was slower.

The concentration risk remains real. Despite expansion, Bangalore still dominates Brigade's portfolio and revenue. Company has a low return on equity of 11.6% over last 3 years partly reflects the capital intensity of geographic expansion without commensurate returns. Yet the expansion wasn't just about immediate returns—it was about de-risking the business from Bangalore's eventual maturation and creating optionality for future growth.

The most intriguing expansion wasn't geographic but vertical—into industrial parks and logistics. As e-commerce exploded and manufacturing returned to India, Brigade recognized that warehouses and industrial facilities were becoming the new office spaces. The same discipline applied to commercial real estate—location, quality, tenant relationships—translated perfectly to industrial properties.

VIII. Business Model & Financial Architecture

Understanding Brigade's financial architecture requires looking beyond the headline numbers. Revenue: 5,074 Cr · Profit: 680 Cr might seem straightforward, but the three-segment strategy—Development, Leasing, Hospitality—creates a complex interplay of cash flows, capital allocation, and risk management that's unique in Indian real estate. The recent Q1 FY26 results illustrate this complexity perfectly. Revenue from operations rose to Rs 1,281 crore with net profit jumping 95% to Rs 158 crore. But breaking down the segments reveals the real story: Real estate revenue rose 22% to Rs 892 crore, Leasing revenue stood at Rs 300 crore (15% growth), and Hospitality revenue hit Rs 141 crore (19% growth). Each segment operates on different cycles, margins, and capital requirements.

The pre-sales model drives the development business. Pre-sales for the quarter stood at Rs 1,118 crore, with collections totaling Rs 1,728 crore. This gap between pre-sales and collections reflects the working capital intensity of real estate—customers pay over construction periods, creating a natural hedge against cost escalations but requiring careful cash flow management.

The three-segment architecture serves multiple purposes. Development provides growth and profits but is cyclical. Leasing offers stable annuity income—portfolio occupancy of 92% from 9.38 million square feet generates predictable cash flows. Hospitality, while capital-intensive, creates synergies with other segments and enhances brand value.

Promoter Holding: 41.1% reflects a careful balance. The family retains control but has diluted enough to attract institutional investors and ensure liquidity. This isn't the 75% promoter holding typical of Indian family businesses, nor the sub-20% of professionally managed companies. It's a deliberate middle path that preserves entrepreneurial decision-making while ensuring market discipline.

The capital allocation philosophy has evolved significantly. Early Brigade focused on asset creation—build and hold. Modern Brigade thinks in terms of capital efficiency. The recent partnership to develop 1.4 million sq ft of leasable office space on Airport Road, expected to generate Rs 100 crore annual lease income with Rs 750 crore investment, represents a 13% yield—attractive in a world of 7% risk-free rates.

Company has a low return on equity of 11.6% over last 3 years raises questions but requires context. Real estate is capital-intensive. Brigade's focus on quality and integrated developments requires higher upfront investment than typical developers. The leasing portfolio takes years to stabilize. Hotels have long gestation periods. The low ROE partly reflects investments in future revenue streams not yet fully productive.

The financial architecture also reveals strategic choices. Brigade could juice returns by leveraging more aggressively, focusing only on residential development, or compromising on quality. It chooses not to. The conservative leverage, diversified model, and quality focus might depress near-term returns but create long-term resilience.

Working capital management has become increasingly sophisticated. The company maintains minimal residential debt—zero in recent quarters—reflecting strong pre-sales and collections. Commercial development is funded through construction finance repaid from lease revenues. Hotels use project-specific debt aligned with cash flow profiles.

The most interesting financial innovation is Brigade's approach to land banking. With 60 million square feet of development potential, the company sits on enormous value. But unlike peers who hoard land speculatively, Brigade actively develops or partners on most parcels, ensuring capital productivity while maintaining growth pipeline.

IX. Culture, Values & The Brigade Way

Walk into any Brigade property and you'll notice something unusual for an Indian real estate company: employees don't introduce themselves by designation but as "Brigadiers." This isn't corporate theater—it reflects a deliberate culture-building exercise that began in the late 1990s when Jaishankar realized that scaling beyond a family business required creating an identity that transcended family.

QC-FIRST, which stands for - Quality, Customer Centricity, Fairness, Innovation, Responsible Socially and Trust—isn't just a corporate acronym gathering dust in presentation decks. It's embedded in decision-making processes, from vendor selection to customer service protocols. When Brigade chose to honor apartment bookings at 2007 prices despite the 2008 crash, losing crores in potential profits, it was QC-FIRST in action.

The culture manifests in unexpected ways. Brigade Foundation's work in education and healthcare isn't typical CSR box-ticking. The Indian Music Experience museum, personally funded and championed by Jaishankar, seems bizarre for a real estate company. But it reflects a deeper philosophy: business success enables cultural contribution, not the other way around.

For over a hundred years, his family has been well known in the region for their business integrity and philanthropy. This heritage matters more than it might appear. In Indian business, family reputation opens doors that money cannot. When Brigade needed land in sensitive areas or government approvals for ambitious projects, the Jaishankar family's century-old reputation for integrity mattered more than corporate presentations.

The organizational structure reflects cultural values. Unlike typical Indian real estate companies with armies of commission-based brokers, Brigade invested in salaried sales teams trained in consultative selling. The difference seems minor but reflects a fundamental choice: relationships over transactions, salary over commission, consultation over pressure.

Employee retention in Indian real estate typically rivals investment banking for awfulness. Brigade's numbers tell a different story. Senior management stability spans decades. The company has been certified as a Great Place to Work for 14 consecutive years—remarkable in an industry known for toxic work environments.

The approach to construction workers—the invisible backbone of real estate—reveals cultural depth. Brigade provides on-site schools for workers' children, healthcare facilities, and skill development programs. This isn't altruism—it's recognition that treating workers well improves quality, reduces accidents, and ensures contractor loyalty during labor shortages.

The Brigade School system, operating within several Brigade enclaves, represents culture-building at its most ambitious. By controlling education within its communities, Brigade shapes not just buildings but the values of families living in them. It's social engineering through real estate—creating communities that share Brigade's values of quality and integrity.

Customer relationship management transcends typical developer behavior. Most Indian developers disappear after possession. Brigade maintains relationships through property management services, community events, and upgrade programs. The Brigade Plus loyalty program treats customers as members of an extended family, not transaction counterparties.

The response to COVID-19 revealed cultural resilience. While competitors laid off employees and halted construction, Brigade retained its workforce, provided vaccines to workers, and converted facilities into isolation centers. The short-term cost was enormous. The long-term benefit in loyalty and reputation: priceless.

Innovation culture, manifested through REAP and digital initiatives, shows how values evolve while staying rooted. Jaishankar's generation valued physical quality. The second generation adds digital excellence. But both share the core belief: innovation must solve real problems, not chase buzzwords.

The most telling cultural indicator might be how Brigade handles failure. When projects face delays or quality issues, the company's response—transparent communication, compensation, and corrective action—differs markedly from industry norms of denial, delay, and litigation. This approach costs more but builds trust that compounds over decades.

X. Playbook: Real Estate Lessons

The Brigade playbook offers lessons that transcend real estate, providing insights into building sustainable businesses in challenging industries. These aren't theoretical frameworks but battle-tested strategies refined over four decades of Indian real estate's boom-bust cycles.

The Integrated Enclave Model vs. Standalone Projects

Most developers think in projects. Brigade thinks in ecosystems. The integrated enclave model—combining residential, commercial, retail, and hospitality—creates value greater than the sum of parts. A Sheraton hotel doesn't just generate room revenue; it elevates residential prices, attracts commercial tenants, and drives retail footfalls. This network effect means Brigade can pay more for land, charge premium prices, and still deliver better value than competitors building standalone projects.

Managing Cyclicality in Indian Real Estate

Indian real estate cycles are vicious—prices can halve in downturns, liquidity disappears, projects stall. Brigade's three-engine model provides natural hedging. When residential sales slow, commercial leasing often remains stable. When both struggle, hospitality can benefit from economic uncertainty driving domestic tourism. This diversification isn't perfect—all segments suffered during COVID—but it provides resilience single-segment players lack.

Brand Building in a Trust-Deficit Industry

Real estate globally suffers trust issues. In India, with its history of project delays, quality compromises, and outright fraud, trust becomes competitive advantage. Brigade built trust through consistency: consistent quality across projects, consistent communication during problems, consistent delivery despite market cycles. The price of this consistency—lower margins, slower growth, opportunity costs—pays off through premium pricing, faster sales velocity, and customer lifetime value.

Family Business Succession in Listed Companies

The transition from founder to second generation destroys many family businesses. Brigade navigated this through deliberate structure: professional management for operations, family leadership for strategy, clear role separation, and merit-based progression even for family members. The daughters didn't become managing directors overnight—they worked their way up, earned credibility, and brought complementary skills.

Balancing Growth with Financial Prudence

Real estate rewards leverage until it doesn't. Brigade's conservative approach—minimal residential debt, project-specific commercial financing, careful land banking—seems suboptimal during booms but ensures survival during busts. The company could double ROE by doubling leverage. It chooses not to, prioritizing survival over optimization.

The Importance of Location and Timing

Brigade's success often came from being early to emerging locations—Brigade Road before it became prime, Whitefield before IT exploded, OMR Chennai before infrastructure improved. But early doesn't mean speculative. Each bet was grounded in fundamental analysis: infrastructure development, demographic shifts, economic trends. Timing matters as much as location—entering Chennai during the global financial crisis meant lower land costs and less competition.

The playbook extends beyond strategy to execution. Brigade's approach to construction—empaneling contractors for long-term relationships rather than squeezing margins, investing in worker welfare for quality and consistency, using technology for monitoring rather than cost-cutting—creates sustainable advantages. The premium customers pay isn't for marketing but for genuine quality differences.

Stakeholder management reveals another playbook element. Unlike developers who view regulations as obstacles, Brigade engages constructively with government, contributing to policy formation and urban planning. This investment in relationships pays off through faster approvals, better land parcels, and regulatory flexibility during crises.

The approach to capital markets demonstrates sophisticated thinking. Going public in 2007, just before the crisis, seemed terrible timing. But it provided capital to survive the downturn and acquire distressed assets. The recent Brigade Hotel Ventures IPO, raising Rs 885.60 crore, shows continued capital market savvy—spinning off capital-intensive businesses while retaining control.

Risk management permeates the playbook. Every integrated enclave includes multiple revenue streams, reducing project-specific risk. Geographic expansion beyond Bangalore, while maintaining concentration for operational efficiency. Partnership with global brands for hotels, transferring operational risk while retaining ownership upside. These aren't independent decisions but coordinated risk reduction.

The human capital strategy deserves attention. In an industry dominated by relationship-based hiring and family connections, Brigade's focus on professional management, systematic training, and merit-based progression creates competitive advantage. The Brigade Plus loyalty program for customers parallels internal programs building employee loyalty.

Perhaps the most important playbook lesson is patience. Real estate rewards patient capital—land appreciates, buildings generate cash flows, brands compound value. Brigade's willingness to hold assets, develop gradually, and build slowly but surely contrasts with developers chasing quick profits through rapid turnover.

XI. Bear vs. Bull Case Analysis

Bear Case: The Structural Challenges

The bear case for Brigade starts with uncomfortable mathematics. Company has a low return on equity of 11.6% over last 3 years in a market where investors expect 15-20% returns raises fundamental questions about capital allocation. Why invest in Brigade when fixed deposits offer 7-8% with zero risk, and other developers promise higher returns?

Geographic concentration presents existential risk. Despite expansion into Chennai, Hyderabad, and other cities, Bangalore still dominates Brigade's portfolio. A significant correction in Bangalore real estate—triggered by IT sector slowdown, infrastructure collapse, or water crisis—would devastate Brigade disproportionately. The city's water crisis isn't theoretical; it's an annual reality getting worse with climate change and urbanization.

Competition from national players intensifies yearly. DLF, Godrej Properties, and Prestige Estates operate at scales Brigade cannot match. These giants can bid higher for land, absorb losses to gain market share, and access capital more cheaply. In auctions for prime land parcels, Brigade increasingly finds itself outbid by deeper-pocketed competitors.

Interest rate sensitivity creates vulnerability. Real estate is leveraged buying—customers borrow to buy homes, developers borrow to build them. Rising rates increase EMIs, reducing affordability and demand. They also increase construction finance costs, squeezing developer margins. Brigade's diversified model provides some protection, but ultimately all segments suffer when rates rise significantly.

The technology disruption threat looms larger than most realize. PropTech startups promise to disintermediate traditional developers through platforms connecting land owners directly with contractors and buyers. While Brigade invests in PropTech through REAP, it's unclear whether incumbent developers can navigate disruption that eliminated incumbents in other industries.

Regulatory risks in Indian real estate never disappear. RERA improved transparency but increased compliance costs. GST added complexity. Environmental regulations tighten constantly. Any major regulatory change—wealth taxes, rent controls, land ceiling acts—could devastate profitability. Brigade's compliance focus helps but doesn't eliminate regulatory risk.

The succession question remains partially answered. While the second generation has proven competent, the transition isn't complete. Jaishankar's vision and relationships built Brigade. Can his daughters maintain momentum when he fully steps back? Family businesses often struggle in third generation. Will Brigade become another statistic?

Bull Case: The Structural Advantages

The bull case begins with brand value in a trust-deficit industry. In Indian real estate, where project delays and quality issues are endemic, Brigade's reputation for delivery becomes increasingly valuable. This brand premium—the ability to charge 10-15% more than competitors for similar products—drops directly to bottom line.

Diversified revenue streams provide resilience most developers lack. While ROE seems low, it's stable across cycles. Pure residential developers might show 25% ROE in good years but negative returns in downturns. Brigade's 11.6% ROE through COVID, demonetization, and RERA implementation demonstrates model resilience.

Second generation bringing innovation positions Brigade for future growth. REAP accelerator, BuzzWorks co-working, digital transformation initiatives show Brigade evolving beyond traditional development. These initiatives might seem marginal today but could become significant growth drivers as real estate digitizes.

Among the top 10 listed developers in India, by market capitalisation reflects market confidence. Despite bear arguments, Brigade's market cap has grown steadily, suggesting investors see value bears miss. The recent upgrade to AA (Stable) credit rating confirms institutional confidence in Brigade's model.

The integrated enclave competitive advantage deepens over time. As Brigade completes more enclaves, operational expertise compounds. Competitors can copy the concept but not the execution expertise developed over decades. Each successful enclave makes the next one easier to finance, faster to lease, and more profitable to operate.

Land bank value provides hidden upside. With 60 million square feet of development potential in prime locations, Brigade sits on enormous unrealized value. Current book value doesn't reflect appreciation in land acquired years ago. As projects develop, this value unlocks, providing earnings visibility for years.

Demographic tailwinds support long-term growth. India's urbanization, rising incomes, and young population create sustained housing demand. Nuclear families, female workforce participation, and migration to cities drive demand for quality housing. Brigade's positioned to capture this demand profitably.

The sustainability focus aligns with global trends. ESG investing, green buildings, and sustainable development aren't fads but fundamental shifts. Brigade's early investment in green building certification, water management, and sustainable practices positions it ahead of competitors scrambling to catch up.

Capital market access enables growth. The successful Brigade Hotel Ventures IPO demonstrates ability to access capital markets for expansion. Unlike private developers dependent on expensive debt, Brigade can raise equity capital for growth while maintaining conservative leverage.

Operational excellence in execution matters more than financial engineering. In real estate, execution determines success. Brigade's track record—250+ buildings, 70 million square feet delivered—demonstrates execution capability that financial metrics don't capture. This operational excellence becomes more valuable as projects become complex.

The Balanced View

Reality lies between extremes. Brigade isn't the high-growth story that momentum investors seek, nor the value trap that bears fear. It's a steady compounder in a cyclical industry, trading growth for stability, accepting lower returns for lower risk.

The key question isn't whether Brigade will grow—demographics ensure that. It's whether Brigade can accelerate returns while maintaining quality and conservative leverage. Early evidence from second-generation leadership suggests positive evolution, but transformation takes time.

For investors, Brigade represents a specific proposition: exposure to Indian real estate with lower volatility, reasonable returns, and limited downside. It won't double overnight, but it probably won't halve either. In a portfolio context, that stability has value beyond simple return metrics.

XII. Looking Forward: The Next Chapter

The future of Brigade Enterprises will be shaped by forces beyond its control and decisions entirely within it. Technology, demographics, regulations, and competition create the context. Strategy, execution, capital allocation, and leadership determine outcomes within that context.

PropTech Initiatives and Digital Transformation

The real digital transformation hasn't begun. While REAP accelerator and digital marketing represent progress, the fundamental processes—land acquisition, design, construction, sales—remain largely analog. The next chapter requires digitizing core operations, not peripheral activities.

Building Information Modeling (BIM), IoT sensors for construction monitoring, AI for demand prediction, blockchain for property transfers—these technologies exist but aren't widely deployed. Brigade's challenge: adopting technology while maintaining quality standards developed through traditional methods.

The customer experience transformation might matter more than operational digitization. Virtual reality property tours, augmented reality interior design, digital mortgage processing, automated property management—these innovations could differentiate Brigade from traditional competitors while defending against PropTech disruption.

Sustainability and Green Building Focus

Climate change transforms real estate from contributor to solution. Buildings consume 40% of global energy, emit 36% of greenhouse gases. Regulations tightening globally will reach India. Brigade's early sustainability investments position it well, but the next chapter demands more.

Net-zero buildings, renewable energy integration, water recycling, waste management—these shift from nice-to-have to must-have. Brigade's integrated enclave model enables community-level solutions impossible in standalone projects. A solar farm serving entire enclaves, community-level water treatment, district cooling systems—these become competitive advantages.

The sustainability narrative also attracts capital. ESG funds, impact investors, green bonds offer cheaper capital to sustainable developers. Brigade's track record positions it to access these sources, potentially improving returns while maintaining conservative leverage.

Expansion into New Geographies

The geographic expansion question isn't whether but how. Concentration risk in Bangalore demands diversification, but expanding too fast destroyed many developers. Brigade must balance growth with capability building.

Tier-2 cities offer opportunity with less competition. Coimbatore, Visakhapatnam, Pune—these cities need quality developers but can't attract national giants. Brigade's reputation and execution capability could dominate these markets. But managing remote operations challenges any organization.

The international question intrigues. Dubai office suggests ambition beyond India. Indian diaspora creates demand for trusted Indian developers internationally. But international expansion requires capabilities—regulatory knowledge, local partnerships, currency management—Brigade currently lacks.

REITs and Capital Market Evolution

Real Estate Investment Trusts transform global real estate. India's REIT regulations, though nascent, will mature. Brigade's commercial portfolio—9.38 million square feet generating steady rental income—seems perfect for REIT structure.

A Brigade REIT could unlock value, provide growth capital, and improve returns. Separating capital-intensive commercial assets into REITs while focusing development on higher-return residential projects could transform Brigade's financial profile. But REITs require scale, standardization, and yield focus that might conflict with integrated enclave model.

The capital market evolution extends beyond REITs. Fractional ownership, tokenization, crowd-funding—new models emerge constantly. Brigade must evaluate which innovations enhance its model versus those that threaten it.

Competition from New-Age Developers

The next generation of competitors won't be traditional developers but technology companies entering real estate. Amazon developing logistics facilities, Google building smart cities, Tesla creating energy-efficient communities—these represent different competition.

These new-age developers bring advantages: unlimited capital, technology expertise, global scale, customer data. But they lack local knowledge, execution capability, regulatory relationships that Brigade spent decades building. The question becomes: can Brigade learn technology faster than technology companies learn real estate?

The response requires fundamental transformation, not incremental improvement. Brigade must become a technology company that happens to develop real estate, not a real estate company that uses technology. This transformation challenges every aspect of current operations from hiring to culture to capital allocation.

The Leadership Transition

The ultimate question remains succession. Jaishankar built Brigade through vision, relationships, and reputation. The second generation brings complementary skills—professional management, technological sophistication, global perspective. But can they maintain the entrepreneurial edge while professionalizing operations?

The transition from founder to second generation succeeded. The challenge now: institutionalizing success beyond family leadership. Can Brigade create systems, processes, and culture that transcend individual leaders? Can it become a institution like DLF or Godrej Properties that survives generational transitions?

The answer determines whether Brigade remains a successful family business or evolves into an enduring institution. Early evidence—professional management, systematic succession planning, capability building—suggests positive evolution. But only time reveals whether Brigade can transcend its origins while maintaining its soul.

XIII. Recent News

The most recent developments paint a picture of strong operational performance amid market volatility:

Q1 FY26 Performance & Growth Momentum

Brigade reports 20% revenue, 95% PAT growth; ₹1,118 Cr pre-sales; hotel subsidiary IPO in Q1 FY26. The company has demonstrated remarkable resilience with consolidated revenue reaching Rs 1,281 crore in Q1 FY26, up 18.87% year-on-year, while net profit jumped 95% to Rs 158 crore.

Record FY25 Performance

Brigade Enterprises sold properties worth Rs 7,847 crore in FY25, an annual increase of 31%, marking its highest-ever real estate sales value. The company achieved a landmark completion of 100 million square feet of development across projects since inception—a significant milestone in its nearly four-decade journey.

Brigade Hotel Ventures IPO Success

Brigade Hotel Ventures Limited, a subsidiary of Brigade Enterprises Limited, launched an Rs 885.60 crore Initial Public Offering (including a Rs 126 crore pre-IPO placement). The IPO, which opened on July 24, 2025, at a price band of Rs 85-90 per share, demonstrates Brigade's ability to unlock value from its diversified portfolio.

Strategic Land Acquisitions & Partnerships

Brigade Enterprises buys 20-acre land in Bengaluru for Rs 588 crore (July 2025), continuing its strategic land banking in prime locations. The company also entered into a Joint Development Agreement with United Oxygen to develop Grade A office space on ITPL Road, Whitefield, with a leasable area of 3.0 lakh sq ft and GDV of Rs 340 crore.

Major Project Launches

Brigade launches ₹2,100 cr residential project 'Brigade Morgan Heights' in Chennai (June 2025), marking its continued expansion beyond Bangalore. The company has a robust pipeline of about 16 million square feet of new launches planned.

Financial Strength & Rating Upgrade

ICRA has upgraded Brigade's credit rating to AA (Stable), reflecting improved financial metrics. The company maintains a conservative debt-equity ratio of 0.14% as of March 31, 2025, compared to 0.62% in March 2024, with cash and cash equivalents of Rs 3,483 crore.

Market Performance & Investor Sentiment

Despite strong operational performance, Brigade's stock has faced volatility, trading at Rs 905-1,100 range with a market cap of approximately Rs 23,617 crore. The stock is trading at 4.19 times book value with analysts maintaining a "Hold" rating, suggesting cautious optimism about future prospects.

XIV. Conclusion

The Brigade story ultimately transcends real estate. It's about how businesses evolve from family enterprises to institutions, how trust becomes competitive advantage in trust-deficit industries, how patient capital creates enduring value in cyclical markets.

From chicory powder to Chennai skyscrapers, from partnership disputes to public markets, from father to daughters—Brigade's journey reflects India's own economic transformation. The company that began as a single-project venture in 1986 now shapes skylines across South India, housing thousands of families, employing hundreds directly and thousands indirectly.

The numbers tell one story: 250+ buildings completed, 70+ million square feet developed, Rs 5,278 crore revenue, among top 10 listed developers by market capitalization. But the deeper story lies in the model: integrated enclaves creating communities not just buildings, three-segment strategy providing resilience through cycles, second-generation leadership bringing innovation while preserving values.

Brigade isn't perfect. The 11.6% ROE disappoints investors seeking higher returns. Geographic concentration in Bangalore creates vulnerability. Competition from larger players intensifies. Technology disruption looms. Yet these challenges must be weighed against strengths: unmatched brand trust in South India, proven execution capability across cycles, successful generational transition rare in family businesses, and conservative balance sheet ensuring survival through downturns.

For investors, Brigade represents a specific proposition—not explosive growth but steady compounding, not maximum returns but managed risks. It's a bet on India's urbanization playing out over decades, on quality and trust ultimately commanding premiums, on family businesses successfully professionalizing while retaining entrepreneurial spirit.

The next chapter remains unwritten. Will Brigade successfully expand beyond South India? Can it accelerate returns while maintaining conservative leverage? Will PropTech initiatives create new growth engines? Can the second generation build on the founder's legacy while adapting to changing markets?

These questions won't be answered quarterly but over years, perhaps decades. Real estate rewards patience—land appreciates slowly but surely, buildings generate cash flows for generations, brands compound value over time. Brigade's playbook has always emphasized long-term value over short-term optimization.

As Bangalore transforms from garden city to global city, as Chennai emerges as manufacturing hub, as India urbanizes at unprecedented pace, Brigade stands positioned to capture this growth. Not through financial engineering or aggressive leverage, but through the same principles that built it: Quality, Customer Centricity, Fairness, Innovation, Responsibility, and Trust.

The Brigade story continues. From that rainy day when Jaishankar watched chicory workers strike to today's integrated enclaves housing thousands, the journey has been remarkable. But in real estate, as in life, the best buildings are those still being built. For Brigade Enterprises, the foundation is solid, the structure is rising, but the finest floors may yet be constructed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube