LMW Limited: The Textile Machinery Titan of Coimbatore

I. Introduction & Episode Roadmap

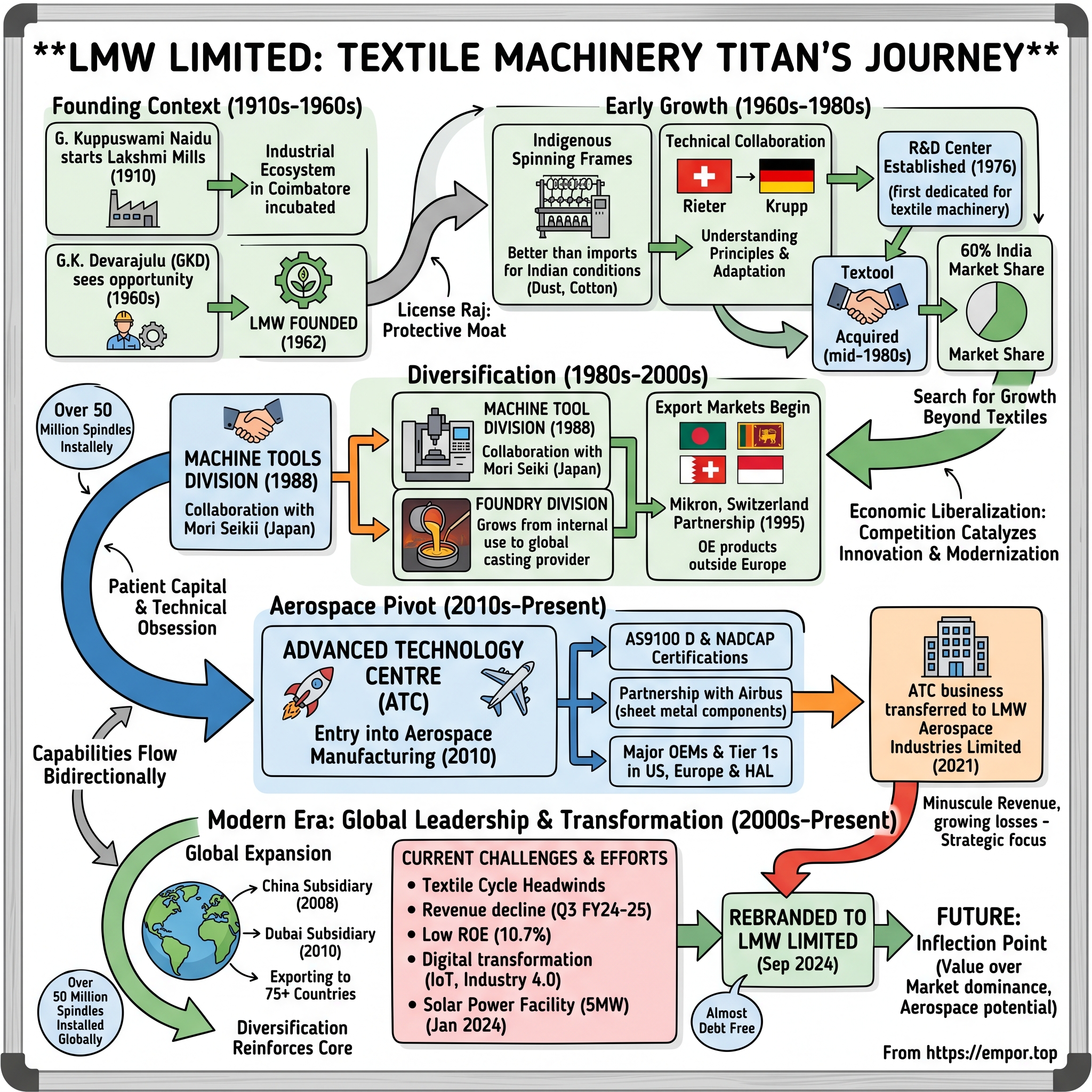

Picture this: It's 1962 in Coimbatore, the "Manchester of South India," where the rhythmic clatter of textile looms provides the soundtrack to a city's industrial ambitions. A young engineer named G.K. Devarajulu stands before a group of skeptical mill owners, promising them something audacious—that an Indian company could manufacture world-class spinning machinery, breaking the stranglehold of Swiss and German suppliers who had dominated the market since the British Raj. Six decades later, that promise has evolved into LMW Limited, a ₹15,807 crore industrial conglomerate that commands 60% of India's textile machinery market and has installed over 50 million spindles across the globe.

The question that drives this story isn't just how a company born in the License Raj era became one of only three manufacturers worldwide producing the entire range of textile spinning machinery. It's how LMW navigated India's economic liberalization, survived global competition, and then made the audacious leap from textile machinery into aerospace components—a journey from cotton to carbon fiber, from mills to missiles. Today, LMW has a market cap of ₹15,909 crore with revenue of ₹3,033 crore and profit of ₹103 crore. But these numbers tell only part of the story. The real narrative is one of industrial evolution, family dynasties, technological leaps, and the peculiar challenges of building a global manufacturing business from India's textile heartland. It's about how a company that started by reverse-engineering European spinning frames now manufactures precision components for Airbus and Boeing.

What makes LMW particularly fascinating for investors and business historians alike is its counterintuitive journey. While most Indian conglomerates expanded horizontally into unrelated businesses, LMW moved vertically up the precision engineering ladder. While textile machinery remains cyclical and challenging, the company has systematically built capabilities that place it at the intersection of India's manufacturing ambitions and global supply chain realignments.

Our journey through LMW's six-decade evolution will reveal how patient capital, technical obsession, and strategic patience created one of India's most underappreciated industrial stories. We'll explore the founding vision of the Lakshmi Mills dynasty, the brutal realities of competing with Swiss precision, the aerospace pivot that nobody saw coming, and why—despite recent headwinds with the stock trading at 5.73 times book value with a low ROE of 10.7% over the last 3 years—this company represents a unique lens into India's manufacturing future.

II. The Lakshmi Mills Origins & Founding Context

The year is 1910. In the dusty plains of Coimbatore, a visionary named G. Kuppuswami Naidu is building what would become the foundation of South India's textile revolution. Lakshmi Mills, incorporated that year as a composite textile mill, wasn't just another industrial venture—it was the seed of an industrial ecosystem that would transform Coimbatore from a small trading town into India's textile machinery capital.

G. Kuppuswami Naidu wasn't your typical industrialist. He understood that true industrial power didn't come from just running mills but from controlling the means of production itself. By the 1930s, Lakshmi Mills had evolved beyond just spinning cotton; it was incubating a network of ancillary companies that would support and eventually transcend the parent organization. This ecosystem approach—decades before Silicon Valley made it fashionable—would prove crucial to LMW's eventual emergence.

Enter Cavalier G.K. Devarajulu, or GKD as he was known in the boardrooms of Coimbatore. A mechanical engineer by training and an industrialist by ambition, GKD had spent years watching Indian textile mills struggle with aging European machinery, exorbitant spare part costs, and service engineers who flew in from Switzerland at princely fees. In 1962, armed with the backing of the Lakshmi Mills group and a vision that seemed almost delusional in the License Raj era, he founded Lakshmi Machine Works.

The timing was both terrible and perfect. Post-independence India in 1962 was a paradox: Nehru's socialist ideals dominated policy, import substitution was gospel, and getting an industrial license required navigating Byzantine bureaucracy. Yet this very protectionism created a captive market hungry for domestic alternatives. Indian textile mills, cut off from easy imports by foreign exchange shortages and high tariffs, desperately needed local solutions.

GKD's pitch to potential customers was simple but revolutionary: "Why should Indian cotton be spun on German machines maintained by Swiss engineers?" But the technical challenge was staggering. Textile machinery in the 1960s represented the pinnacle of mechanical engineering—thousands of precisely machined parts working in harmony at high speeds. A spinning frame's roving had to be drawn out to exact specifications, twisted at precise angles, and wound onto bobbins without breaking. The tolerances were measured in microns, and any deviation meant inferior yarn quality. The initial skepticism from the textile mill community was crushing. Born in 1911, he started LMW when India was a fledgling nation and through his untiring efforts raised it to great heights as the years passed. But GKD had something his competitors didn't—an intimate understanding of Indian mills' specific needs. European machines were designed for European cotton and European climate. Indian cotton was shorter staple, the humidity was different, and the operational conditions were far more challenging. GKD's team began by meticulously studying these differences, essentially building a new science of tropical textile engineering.

The License Raj, paradoxically, became LMW's protective moat. While it strangled many businesses with red tape, it also shielded domestic manufacturers from foreign competition. Every imported machine needed foreign exchange approval, which was scarce and tightly controlled. LMW positioned itself as the patriotic choice—supporting Indian industry while conserving precious foreign exchange. Lakshmi Machine Works was founded in 1962 by Cavalier Dr. GK Devarajulu based on a practical business model of offering indigenous end to end world class technology solutions to the Indian Spinning Industry.

By 1965, just three years after founding, LMW had achieved what many thought impossible—producing its first indigenous spinning frame that could match imported quality. The company's strategy was brilliantly counterintuitive: instead of trying to be cheaper than imports, they focused on being better for Indian conditions. This wasn't just import substitution; it was import improvement. The early success created a virtuous cycle: profits were plowed back into R&D, which improved products, which won more customers, which generated more profits.

III. Early Years: Building India's Textile Machinery Base (1962-1980s)

The workshop floor at LMW's Periyanaickenpalayam facility in 1968 was a study in contrasts. On one side, Swiss Rieter machines—dismantled, studied, measured to the last millimeter. On the other, LMW's first attempts at indigenous production—rough around the edges but improving with each iteration. It started its operation in 1962 in Periyanaickenpalayam in Coimbatore city with technical collaboration with Swiss-based textile machinery manufacturer Rieter for textile machines and German based Steel and Ammunition major Krupp. This technical collaboration wasn't just about copying; it was about understanding the fundamental engineering principles and then adapting them.

The learning curve was brutal. Early machines would work perfectly in the testing facility but fail mysteriously in customers' mills. The problem? Dust. Indian mills, especially in Gujarat and Maharashtra, operated in conditions far dustier than anything European engineers had imagined. LMW's engineers spent months living in these mills, observing, measuring, and redesigning. They developed new sealing mechanisms, different lubrication systems, and innovative dust extraction methods. These weren't sexy innovations that won international patents, but they were the unglamorous breakthroughs that won customers.

Financial success came faster than anyone anticipated. From a standing start in 1962, LMW achieved phenomenal growth in its first year of operations, validating GKD's vision. The company's early financial prudence—a trait that would define it for decades—meant that growth was funded through internal accruals rather than debt. This conservative approach seemed outdated to some observers, but it provided stability during the volatile 1970s when many debt-laden companies collapsed.

The mid-1970s brought an unexpected challenge: success bred complacency in the market. With limited competition and guaranteed demand, LMW could have coasted. Instead, GKD made a decision that seemed irrational at the time—he insisted on continuous improvement even when customers weren't demanding it. Engineers were sent to study at European technical institutes, not to copy but to leapfrog. The company established India's first dedicated R&D center for textile machinery in 1976, years before R&D became a corporate buzzword.

In the mid 1980s the company bought over its Coimbatore based longtime rival and much older Textile and engineering giant Textool. This acquisition wasn't just about eliminating competition; it was about acquiring decades of accumulated knowledge and customer relationships. Textool, established in the 1940s, had been the pioneer, and its acquisition gave LMW instant credibility with conservative mill owners who still viewed the company as an upstart.

By the early 1980s, LMW had achieved something remarkable: 60% market share in Indian textile spinning machinery. But this dominance came with a realization—the domestic market, while large, was ultimately limited. The next phase of growth would require thinking beyond India's borders, a daunting prospect for a company that had built its identity on serving Indian mills.

The technical capabilities built during this period went beyond mere manufacturing competence. LMW developed what management theorists would later call "architectural knowledge"—not just knowing how to make components, but understanding how they fit together into systems. This systems-thinking approach would prove crucial when the company later diversified into CNC machines and aerospace components. Every spinning frame contained thousands of precisely coordinated parts; mastering this complexity created organizational capabilities that transcended the textile industry.

The human capital developed during these early years was equally important. LMW became known as the "university of textile engineering" in India. Engineers who trained there went on to start dozens of ancillary units in Coimbatore, creating an ecosystem that reinforced the city's position as India's textile machinery hub. This wasn't planned strategy; it was emergent advantage, the kind that only becomes visible in hindsight.

IV. Expansion & Diversification: Beyond Textiles (1980s-2000s)

The boardroom at LMW in 1988 witnessed a heated debate that would define the company's next three decades. The textile machinery market was cyclical, margins were compressing, and global competition was intensifying. The younger generation of leadership, led by Dr. D. Jayavarthanavelu (who had succeeded his father GKD), proposed something radical: diversifying into CNC machine tools. The old guard was skeptical—what did textile machinery have to do with computer-controlled lathes? Everything, as it turned out.

To diversify operations, LMW collaborated with Japan's Mori Seiki Co. Ltd to establish the Machine Tool Division in 1988, which is the first of its kind plant in India manufactures CNC Lathes, Machining Centres and Turnmill Centres. This wasn't random diversification; it was calculated adjacency expansion. The precision engineering capabilities developed for textile machinery—working with tight tolerances, understanding metallurgy, managing complex assembly—translated directly to CNC machines. More importantly, LMW's reputation for reliability in textile machinery opened doors in the machine tools market.

The CNC division's early years were humbling. Japanese and Taiwanese manufacturers dominated the market with superior technology and aggressive pricing. LMW's initial strategy of competing on price failed spectacularly. The pivot came in 1992 when they decided to focus on customization—building machines specifically for Indian manufacturing conditions. Just as they had adapted textile machinery for Indian cotton, they now adapted CNC machines for Indian factories: better protection against power fluctuations, simplified maintenance procedures for less-skilled operators, and robust construction for harsh industrial environments.

Meanwhile, the Foundry Division was quietly becoming a technological powerhouse. What started as an in-house facility to cast components for textile machinery evolved into a precision casting operation serving global clients. By 1995, LMW Foundry was producing complex castings for industries worldwide, from automotive components to industrial pumps. The foundry's success illustrated a crucial principle: capabilities developed for internal use, when world-class, could become businesses in themselves.

In 1995, LMW joined hands with Mikron, Switzerland for manufacture of CNC Universal Boring and Milling machines for Tool Room. In addition to selling the machines in domestic market LMW had buy back arrangement with Mikron. This partnership marked a critical inflection point. LMW wasn't just manufacturing for India anymore; they were producing components that met Swiss quality standards for global markets. The psychological impact was profound—if LMW could satisfy Mikron's exacting standards, they could compete anywhere.

The late 1990s brought India's economic liberalization, removing many protective barriers that had shielded LMW. Suddenly, international manufacturers could sell directly in India without prohibitive tariffs. Many predicted LMW's demise. Instead, competition catalyzed innovation. The company launched a massive modernization drive, investing in CAD/CAM systems, robotics, and automated quality control. Between 1995 and 2000, LMW invested more in technology upgrading than in the previous two decades combined.

Export markets became the new frontier. LMW's international expansion started modestly—Bangladesh, Sri Lanka, countries with similar operating conditions to India. But by 2000, LMW machines were operating in Indonesia, Egypt, and Turkey. With greater efficiency and better return on investment for the customer, LMW has more than 50 million spindlage capacity installed worldwide. Each market taught new lessons: Indonesian humidity required different lubrication systems, Egyptian cotton needed modified drawing mechanisms, Turkish mills demanded higher automation levels.

The establishment of a wholly-owned subsidiary in China in 2008 represented both the apex of LMW's global ambitions and a recognition of new competitive realities. China wasn't just a market; it was the market, accounting for over 50% of global textile production. But entering China meant competing with local manufacturers who had government support, cost advantages, and home market protection. LMW's strategy was differentiation through quality—positioning itself as the premium option for high-end yarn production.

By the end of the 2000s, LMW had transformed from a single-product domestic company into a diversified industrial conglomerate with global reach. The three divisions—Textile Machinery, Machine Tools & Foundry, and the nascent Advanced Technology Centre—generated roughly equal contributions to profitability, providing resilience against sector-specific downturns. Till date, LMW MTD has supplied more than 14,000 CNC lathes and machining centres to a wide customer base spans Automobile industry, Aerospace, Indian Defence, Auto ancillaries, and general engineering industries.

V. The Aerospace Pivot: Advanced Technology Centre

The story of LMW's entry into aerospace manufacturing begins not in a boardroom but on a shop floor in 2009. A team from Hindustan Aeronautics Limited (HAL) was visiting LMW's CNC facility for a routine vendor assessment when they noticed something unusual: the precision levels achieved in manufacturing textile machinery components exceeded many aerospace specifications. The conversation that followed would lead to LMW's most audacious diversification yet.

In the year 2010, Lakshmi Machine Works (LMW) added to their formidable engineering manufacturing portfolio, a new plant to produce critical components and sub-assembli LMW Advanced Technology Center (ATC) is one stop solution to the Aerospace customer. The Advanced Technology Centre represented a fundamental shift in ambition. Textile machinery and CNC tools, however sophisticated, were still essentially mechanical engineering challenges. Aerospace components operated in a different universe—where failure wasn't just costly but potentially catastrophic, where materials were exotic composites and superalloys, where quality standards were written in blood.

The initial investment was staggering—over ₹100 crores in infrastructure alone, before producing a single component. The facility required clean rooms, five-axis machining centers, non-destructive testing equipment, and specialized heat treatment capabilities. But hardware was the easy part. The real challenge was building a quality culture that met aerospace's zero-defect standards. In terms of infrastructure and capability, ATC has world class facilities including Quality Assurance aligning to AS9100 D certification and NADCAP for special process viz Chemical Process, NDT, Welding and Heat treatment totaling more than 25 special processes.

The learning curve was near-vertical. Early batches had rejection rates that would have been acceptable in general engineering but were catastrophic by aerospace standards. Each rejection triggered root-cause analysis that often revealed issues invisible to conventional quality control. Temperature variations of a few degrees during heat treatment could cause microscopic changes in grain structure that affected fatigue life years later. LMW's engineers had to relearn their craft, thinking not in terms of immediate functionality but in terms of performance over decades under extreme conditions.

The breakthrough came through a partnership with Airbus for manufacturing sheet metal components. Starting with simple brackets and panels, LMW gradually moved up the complexity chain. By 2015, they were producing critical structural components. ATC has on going projects with major OEMs & Tier 1's in US, Europe and various divisions of Hindustan Aeronautics Limited as well as Defence Research & Development Organization. Each successful delivery built credibility, opening doors to more complex, higher-margin work.

The strategic rationale for aerospace went beyond diversification. It was about moving up the value chain in a way that enhanced the entire company. Aerospace's demanding standards forced improvements in every division. The foundry developed new alloys for aerospace applications that also improved textile machinery performance. The CNC division's machines became more precise to meet aerospace manufacturing requirements. Knowledge flowed bidirectionally, creating synergies that justified the massive investment. The Board's decision to approve the transfer of ATC business to LMW Aerospace Industries Limited in 2021 represented both opportunity and challenge. Lmw Aerospace Industries Limited was incorporated on Mar 16, 2021, is a public limited company and is wholly-owned subsidiary of the LMW, and is yet to commence operations in the intended Aerospace business vertical. LMW filed a scheme for transfer of Advanced Technology Centre (ATC) business undertaking as Slump Sale and going concern basis to its wholly-owned subsidiary LMWASIL, with the turnover of transferred undertaking at ₹ 28.88 Crores in FY 2020-21 and net worth of Rs 17.08 crores which is minuscule as compared to turnover and net worth of LMW.

The strategic logic was compelling: The ATC business undertaking of the Company has different capital, operating and regulatory requirements from the rest of the business verticals, and the Company is also desirous of scaling up the business operations within aerospace industry. Creating a separate entity would allow focused management, easier entry of strategic partners, and specialized regulatory compliance without affecting the core textile machinery business.

But the financials told a sobering story. ATC business is not only minuscule but also struggling to grow and as a result continuously growing losses as a percentage of Revenue, incurring expenses more than its revenue. This wasn't unusual for aerospace ventures—the industry demanded patient capital and accepted losses for years before profitability. But for a company accustomed to the steady cash flows of textile machinery, it required a fundamental shift in mindset.

The global aerospace supply chain disruptions of 2020-2022 didn't help. Orders were delayed, certifications took longer, and cash burn accelerated. Yet LMW persisted, viewing aerospace not as a profit center but as a capability platform—a way to build competencies that would define the company's next half-century. The bet was that as global aerospace companies diversified their supply chains away from China, India—and specifically companies like LMW with proven precision manufacturing capabilities—would benefit disproportionately.

VI. Global Expansion & Market Leadership (2000s-2020s)

The conference room at LMW's newly established Dubai subsidiary in 2010 overlooked the sprawling Jebel Ali Free Zone, where container ships from fifty nations converged daily. The location wasn't chosen for the view but for what it represented: LMW's transformation from an Indian company that exported to a global company with Indian roots. The establishment of LMW Global FZE wasn't just about having a Middle East presence; it was about reimagining how an Indian industrial company could compete globally.

The numbers told a story of remarkable international success. With greater efficiency and better return on investment for the customer, LMW has more than 50 million spindlage capacity installed worldwide. But behind each spindle was a battle won in factories from Bangladesh to Brazil, where LMW machines competed head-to-head with European manufacturers who had centuries-old reputations and Chinese competitors who undercut on price.

The China subsidiary, established in 2008, represented the ultimate audacity—competing in the backyard of the world's manufacturing superpower. Most Indian companies went to China to source; LMW went to sell. The initial years were brutal. Chinese textile mills, accustomed to local suppliers and skeptical of Indian quality, required extensive convincing. LMW's strategy was counterintuitive: instead of competing on price, they positioned themselves as the premium alternative to local manufacturers, emphasizing precision, durability, and after-sales service.

The breakthrough came through a focus on high-end yarn production. While Chinese manufacturers dominated commodity yarn, premium yarn for luxury fabrics required precision that many local machines couldn't deliver. LMW machines, engineered for the demanding Indian market where mills expected equipment to run 24/7 in harsh conditions, proved remarkably suited for China's quality-conscious premium segment.

LMW today caters to around 60% of India's demand for textile machinery and has emerged as a leader in the export of textile machinery from the country. But maintaining domestic dominance while expanding globally created unique challenges. Indian customers expected preferential treatment as the "home market," while international customers demanded equal priority. The solution was radical decentralization—creating autonomous regional teams with P&L responsibility, essentially running multiple companies within a company.

The partnership with Mikron of Switzerland marked a watershed moment. LMW became the only company in Asia outside Europe to manufacture OE products for Mikron—a validation that transcended mere business success. It signaled that LMW had graduated from being a good emerging market manufacturer to a peer of developed market leaders. The psychological impact within the organization was profound; engineers who had grown up believing European technology was inherently superior now saw their designs being shipped to Switzerland.

Export recognition followed naturally. Winning the Top Export Award in textile machine exports for several consecutive years wasn't just about vanity metrics; these awards opened doors in new markets where government recognition carried weight. In markets like Uzbekistan, Vietnam, and Egypt, where state-owned enterprises made purchasing decisions, LMW's awards provided crucial credibility. The global service network became LMW's hidden competitive advantage. While competitors sold machines and disappeared, LMW established service centers in key markets, staffed by engineers who understood local conditions. This wasn't just about fixing breakdowns; it was about continuous optimization, helping customers extract maximum value from their investments. In markets where skilled technicians were scarce, this service capability often determined purchasing decisions more than machine specifications.

By 2020, LMW's global footprint extended across 75 countries, with particularly strong positions in Turkey, Indonesia, and Bangladesh—markets that were becoming the new centers of global textile production as China moved up the value chain. The company's ability to serve these emerging textile powerhouses while maintaining leadership in the mature Indian market demonstrated remarkable strategic flexibility.

The recent restructuring of subsidiaries, with LMW completing the transfer of its equity stake in wholly owned subsidiary LMW Global FZE, UAE, to another wholly owned subsidiary, LMW Holding, UAE, and the incorporation of LMW Holding Limited on July 10, 2024, signals a new phase of international ambition. Lakshmi Machine Works Ltd has approved the creation of a wholly-owned subsidiary in the UAE with an initial investment of up to USD 25 million. This new subsidiary will focus on the aerospace industry. This isn't just corporate restructuring; it's positioning for the next wave of global expansion, particularly in aerospace where Middle East markets are experiencing explosive growth.

VII. Modern Era: Technology & Transformation (2020-Present)

September 25, 2024, marked more than a cosmetic change. The Company name has been changed from Lakshmi Machine Works Limited to LMW Limited on September 25 2024. The rebranding to LMW Limited reflected a fundamental identity shift—from a machine works company that happened to do other things to an industrial technology company where textile machinery was one of several core competencies. The timing wasn't coincidental; it came as the company grappled with the most challenging period in its six-decade history.

The numbers were sobering. LMW Q1 FY26: Revenue Rs 685 Cr (+4%), PBT Rs 32.5 Cr; challenges in textile machinery, steady order book Rs 2800 Cr. The textile machinery market, already cyclical, faced unprecedented headwinds from global overcapacity, weak demand, and technological disruption. The company's response was characteristically long-term: instead of cutting costs and waiting for recovery, LMW doubled down on technology investment.

The installation of 5MW Solar Power Generating facility at Vadasithur, Coimbatore in January 2024 exemplified this approach. While competitors focused on quarterly earnings, LMW invested in infrastructure that would reduce operating costs for decades. The solar installation wasn't just about sustainability credentials; it was about energy independence in a manufacturing environment where power costs could determine competitiveness.

Industry 4.0 became more than a buzzword at LMW. The company's smart manufacturing initiatives integrated IoT sensors into textile machinery, enabling predictive maintenance and remote monitoring. Mills could now track machine performance in real-time, predict failures before they occurred, and optimize production parameters from smartphones. This wasn't incremental improvement; it was reimagining the customer relationship from selling machines to providing manufacturing intelligence. The recent financial performance tells a story of transformation under pressure. LMW has released its financial results for Q3 FY24-25, highlighting ongoing challenges. While liquidity has improved with cash and cash equivalents reaching Rs 1,040.08 crore, net sales declined significantly to Rs 766.43 crore. Profit Before Tax and Profit After Tax also saw substantial year-on-year decreases, raising concerns about the company's sustainability. The 36.87% drop in net sales reflects the brutal reality of the current textile machinery cycle, but the strong cash position—the highest in six half-yearly periods—provides a buffer for strategic investments.

The paradox of LMW's current position is striking. On one hand, the company faces its most challenging operational environment in decades, with textile machinery demand at multi-year lows and margins under severe pressure. On the other, it has never been better positioned technologically or financially to weather the storm and emerge stronger. The almost debt-free status, combined with cash reserves exceeding ₹1,000 crores, provides extraordinary flexibility in a capital-intensive industry where competitors are struggling with leverage.

The restructuring with LMW Holding Limited in UAE signals ambitions beyond crisis management. This isn't defensive restructuring but offensive positioning, creating structures that can accommodate partnerships, joint ventures, and acquisitions as opportunities emerge from the current downturn. The focus on aerospace through the UAE entity particularly makes sense given the region's massive aerospace investments and India's growing role in global aerospace supply chains.

Digital transformation initiatives extend beyond products to processes. The company's entire value chain—from design to delivery—is being digitized. CAD files flow directly to CNC machines, reducing design-to-production time by 40%. Customers can configure machines online, track production progress in real-time, and access digital twins for training before physical delivery. This isn't just efficiency improvement; it's building switching costs and customer stickiness in an increasingly commoditized market.

The human dimension of transformation often goes unnoticed but is perhaps most critical. LMW is systematically upskilling its workforce, transforming mechanical engineers into mechatronics specialists, training operators in data analytics, and creating a culture where a 60-year-old company thinks like a startup. The average age of engineers has dropped by 15 years in the past decade, bringing fresh perspectives while retaining institutional knowledge through structured mentorship programs.

VIII. Business Model & Competitive Moat Analysis

LMW's business model appears deceptively simple: three divisions manufacturing industrial equipment. But beneath this simplicity lies sophisticated synergies that create competitive advantages invisible to casual observers. The Textile Machinery Division generates steady cash flows and customer relationships, the Machine Tool Division provides technological capabilities and diversification, while the Advanced Technology Centre represents the future—high-margin, high-growth potential that leverages capabilities from both traditional divisions.

Lakshmi Machine Works Limited (LMW) operates a diversified business model spanning multiple industrial sectors, primarily focusing on manufacturing high-quality, precision-engineered products. This diversification isn't random; each division reinforces the others. Foundry capabilities developed for textile machinery castings now serve aerospace clients. CNC machines manufactured by the Machine Tool Division are used internally to produce textile machinery components, ensuring quality control and cost advantages. Aerospace work demands precision that elevates standards across all divisions.

The financial architecture reveals disciplined capital allocation. Company is almost debt free. Company has been maintaining a healthy dividend payout of 26.7% This conservative financial approach—maintaining virtually no debt while paying consistent dividends—might seem outdated in an era of cheap capital, but it provides anti-fragility. During downturns, while leveraged competitors struggle with debt service, LMW can invest countercyclically, gaining market share and acquiring distressed assets.

The competitive moat has multiple layers. First, the installed base advantage: with over 50 million spindles installed globally, LMW has relationships with virtually every major textile manufacturer. These aren't transactional relationships but partnerships spanning decades, where LMW engineers know customers' operations intimately. Switching costs are high—not just financially but operationally, as mills have developed processes around LMW machines' specific characteristics.

Second, the ecosystem moat: LMW isn't just selling machines but providing complete solutions. Spare parts, service, upgrades, training—the lifetime revenue from a machine often exceeds its initial purchase price. This recurring revenue stream, while not explicitly broken out in financial statements, likely represents 30-40% of total revenue and carries higher margins than equipment sales.

Third, the knowledge moat: Six decades of manufacturing experience has created tacit knowledge that can't be easily replicated. This isn't just about blueprints and specifications but understanding how materials behave under stress, how to optimize designs for manufacturability, how to balance cost and performance. New entrants can copy designs but not this accumulated wisdom.

The R&D strategy deserves particular attention. Unlike peers who chase breakthrough innovations, LMW focuses on incremental improvements—1% better efficiency here, 2% lower power consumption there. These improvements compound over time, creating products that are demonstrably superior without requiring customers to radically change their operations. It's evolution, not revolution, and it works.

Capital allocation follows a clear hierarchy: maintain the core (textile machinery), invest in adjacencies (machine tools), and option the future (aerospace). The discipline to not chase hot sectors—LMW notably avoided the solar and wind energy bubbles that trapped many Indian industrials—reflects strategic clarity rare in family-controlled businesses where prestige projects often destroy value.

The recent financial stress test reveals both strengths and weaknesses. Stock is trading at 5.73 times its book value. Company has a low return on equity of 10.7% over last 3 years. The high price-to-book ratio despite low ROE suggests the market values something beyond current financial performance—perhaps the option value of aerospace, the strategic value of the installed base, or simply confidence in management's ability to navigate cycles.

IX. Playbook: Business & Investing Lessons

The LMW story offers a masterclass in building industrial capabilities in an emerging market, then leveraging them globally. The first lesson is the power of patient capital. The Lakshmi Mills group's willingness to accept lower returns initially while building capabilities created a compounding machine that now generates returns far exceeding what short-term optimization would have achieved.

The import substitution to global competitiveness journey reveals a counterintuitive truth: protection can create competence if—and only if—companies use the breathing room to build genuine capabilities rather than extract rents. LMW used India's License Raj not as a shield from competition but as a laboratory to develop products suited for local conditions that eventually found global markets.

The diversification strategy offers nuanced lessons. Related diversification (textile machinery to CNC tools) worked because it leveraged existing capabilities while accessing new markets. Unrelated diversification (into aerospace) is still unproven but follows a logical thread—leveraging precision engineering capabilities developed over decades. The key insight: diversify into areas where your core capabilities provide genuine advantage, not just where markets look attractive.

Building technical capabilities in emerging markets requires a different playbook than in developed markets. You can't assume ecosystem support—suppliers, technical institutes, skilled workers—that developed market companies take for granted. LMW had to build much of this ecosystem itself, establishing training centers, developing supplier networks, even funding technical education. This seems inefficient until you realize it creates competitive advantages: competitors can't easily replicate an entire ecosystem.

Managing cyclicality in capital goods industries requires financial conservatism that seems irrational during booms but proves invaluable during busts. LMW's almost debt-free status isn't financial timidity but strategic positioning. In cyclical industries, the ability to invest when others can't—because they're servicing debt or facing bankruptcy—creates extraordinary opportunities for market share gains and strategic acquisitions.

The family-owned business professionalization journey offers its own lessons. The transition from founder (GKD) to second generation (D. Jayavarthanavelu) to third generation (Sanjay Jayavarthanavelu) shows how family businesses can professionalize without losing entrepreneurial spirit. Key elements: bringing in professional managers for operational roles while family maintains strategic control, creating governance structures that protect minority shareholders, and most importantly, maintaining long-term orientation while improving operational discipline.

For investors, LMW presents a fascinating case study in value versus growth, cycles versus secular trends. The company trades at seemingly contradictory multiples—high P/B despite low ROE—suggesting the market is pricing in either a cycle recovery or transformation success. The lesson: in industrial companies, balance sheet strength and market position matter more than P&L during cycle troughs.

The technology transformation playbook is particularly relevant for traditional manufacturers. Instead of digital disruption, LMW pursues digital evolution—gradually integrating technology into existing products and processes rather than attempting radical transformation. This reduces execution risk while still capturing value from digitalization.

X. Analysis & Bear vs. Bull Case

Bull Case:

The bull thesis rests on five pillars, each reinforcing the others. First, the balance sheet fortress: Company is almost debt free with over ₹1,000 crores in cash provides extraordinary optionality. In a downturn, this becomes a weapon for market share gains through aggressive pricing, strategic acquisitions, or countercyclical investments. The company can afford to wait for the cycle to turn while competitors struggle with survival.

Second, the hidden value in the installed base. With 50 million spindles installed globally, even modest aftermarket revenue per spindle creates a substantial, high-margin revenue stream largely invisible in reported numbers. As these machines age, replacement demand becomes inevitable—not if, but when. The installed base is essentially an annuity that pays out irregularly but inevitably.

Third, the aerospace option. While currently loss-making, aerospace represents a call option on India's manufacturing ambitions. As global OEMs diversify supply chains from China, India becomes the logical alternative, and LMW's established capabilities position it to capture disproportionate value. The separate subsidiary structure allows strategic partnerships without diluting the core business.

Fourth, the cycle recovery potential. Textile machinery is deeply cyclical, currently at trough. Historical patterns suggest dramatic recovery potential—previous cycles saw revenue double from trough to peak. With LMW's dominant market position, even modest recovery drives significant operating leverage given the high fixed cost base.

Fifth, the valuation anomaly. Trading at 5.73 times book value seems expensive, but book value understates replacement cost of manufacturing facilities, land banks in Coimbatore (carried at historical cost), and intangible assets like customer relationships and technical knowledge. The real value lies not in assets but in the ability to generate returns when the cycle turns.

Bear Case:

The bear thesis is equally compelling, starting with the brutal current reality. net sales declined significantly to Rs 766.43 crore. Profit Before Tax and Profit After Tax also saw substantial year-on-year decreases, raising concerns about the company's sustainability. This isn't just a bad quarter; it's a trend that shows no signs of reversing. The textile machinery industry faces structural headwinds from global overcapacity, and LMW's dominant position means it has nowhere to hide.

The ROE problem is particularly concerning. Company has a low return on equity of 10.7% over last 3 years. For a company trading at nearly 6 times book value, generating 10% returns on equity is value-destructive. The market is pricing in dramatic improvement, but there's little evidence this is achievable given industry dynamics.

The aerospace distraction presents its own risks. ATC business is not only minuscule but also struggling to grow and as a result continuously growing losses as a percentage of Revenue. Further also note that it is incurring expenses more than its revenue. Aerospace requires patient capital and accepts losses for years, but LMW's investors may not share this patience. The opportunity cost of aerospace investment versus returning capital to shareholders is substantial.

The technological disruption risk looms large. Traditional textile machinery faces threats from automation, AI-driven optimization, and potentially revolutionary technologies like 3D weaving. LMW's incremental innovation approach may prove insufficient against discontinuous change. The company's R&D spending, while substantial in absolute terms, may be inadequate given the pace of technological change.

The corporate governance concerns, while not glaring, exist. Promoter Holding: 30.8% The relatively low promoter holding creates alignment issues—promoters have significant influence without proportionate economic interest. Related-party transactions with group companies, while disclosed, create potential conflicts of interest.

The Verdict:

The truth, as always, lies between extremes. LMW is neither the hidden gem bulls believe nor the value trap bears fear. It's a well-managed industrial company navigating structural challenges while attempting transformation. The key variables to watch: textile machinery order intake (leading indicator of cycle recovery), aerospace revenue trajectory (validation of diversification strategy), and ROE improvement (evidence of operational excellence).

For long-term investors, the risk-reward appears favorable at current valuations, provided one has the patience for cycle recovery and transformation success. For short-term investors, better opportunities likely exist elsewhere. The company's destiny depends on whether management's patient capital approach proves prescient or obsolete in an rapidly changing industrial landscape.

XI. Epilogue & "If We Were CEOs"

If we were sitting in the CEO's chair at LMW's Coimbatore headquarters, looking out at the factory floor where thousands of workers continue the legacy started by GKD six decades ago, what strategic choices would we make?

First, we'd accelerate the aerospace transformation with strategic boldness. The current approach—organic growth accepting losses—is too slow. We'd seek a transformative partnership with a global aerospace major, potentially offering them majority stake in the aerospace subsidiary in exchange for guaranteed orders and technology transfer. Yes, this dilutes upside, but it dramatically reduces execution risk and time to profitability.

Second, we'd radically restructure the textile machinery business for the new reality. Instead of fighting the cycle, we'd embrace it—creating a variable cost structure that expands and contracts with demand. This means painful decisions: converting fixed workforce to contract, outsourcing non-critical manufacturing, and focusing only on high-value, IP-protected components. The goal: maintain market leadership while improving through-cycle returns.

Third, we'd monetize the hidden assets. The vast land banks in Coimbatore, carried at historical cost, represent trapped value. We'd develop an industrial park, leasing space to suppliers and partners, creating an ecosystem that reinforces our competitive position while generating recurring revenue. The installed base would be monetized through IoT—every machine connected, generating data, creating subscription revenue streams.

Fourth, we'd address the innovation deficit through acquisition rather than internal R&D. Instead of trying to build digital capabilities organically, we'd acquire digital textile technology startups, particularly in Europe where financial distress creates opportunities. The combination of LMW's manufacturing scale and startup innovation could create a formidable competitor.

Fifth, we'd solve the capital allocation puzzle through explicit segmentation. Textile machinery would be run for cash, with every rupee of free cash flow either returned to shareholders or invested in growth areas. No more cross-subsidization, no more hiding poor performance. Each division would stand on its own merits, with separate KPIs and potentially separate equity structures.

The global versus domestic market focus would shift decisively toward exports, but not in traditional markets. We'd target the next wave of textile manufacturing destinations—Africa, Central America, Bangladesh's successors. These markets need not just machines but complete solutions: financing, training, maintenance. LMW could provide the full package, essentially becoming the infrastructure provider for emerging textile industries.

On capital allocation, we'd be more aggressive about returning cash to shareholders during cycle downturns when reinvestment returns are low. The current approach of maintaining large cash balances seems prudent but may be suboptimal. A variable dividend policy—high during downturns, low during growth periods—would better align capital allocation with opportunity.

The biggest surprise from studying LMW's history is how a company so successful in its core market—60% share in Indian textile machinery—struggled to translate that dominance into superior financial returns. The lesson is clear: market dominance without pricing power or operational excellence doesn't create value. The next chapter of LMW's story must be about converting market position into economic value.

Looking ahead, LMW stands at an inflection point. The easy growth from import substitution and domestic market expansion is over. The next phase requires different capabilities: global competitiveness, technological sophistication, and most importantly, the courage to cannibalize existing businesses before competitors do it for them. The company has the resources—financial, technical, human—to succeed. Whether it has the will remains to be seen.

The ultimate question for investors isn't whether LMW will survive—it will. It's whether the company can transform from a successful emerging market industrial into a global technology leader. The seeds are planted—aerospace capabilities, digital initiatives, global presence. But seeds need proper cultivation to bear fruit. The next decade will determine whether LMW becomes a case study in successful transformation or another example of industrial incumbents failing to adapt to changing times.

For all the challenges, we remain cautiously optimistic. The combination of patient capital, technical capabilities, and market position creates optionality that financial statements don't capture. In a world where supply chain resilience matters more than pure efficiency, where India's manufacturing ambitions align with global diversification needs, where traditional engineering excellence meets digital transformation, LMW has the potential to surprise. Whether it realizes that potential depends on choices made today in Coimbatore's boardrooms and factory floors.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube