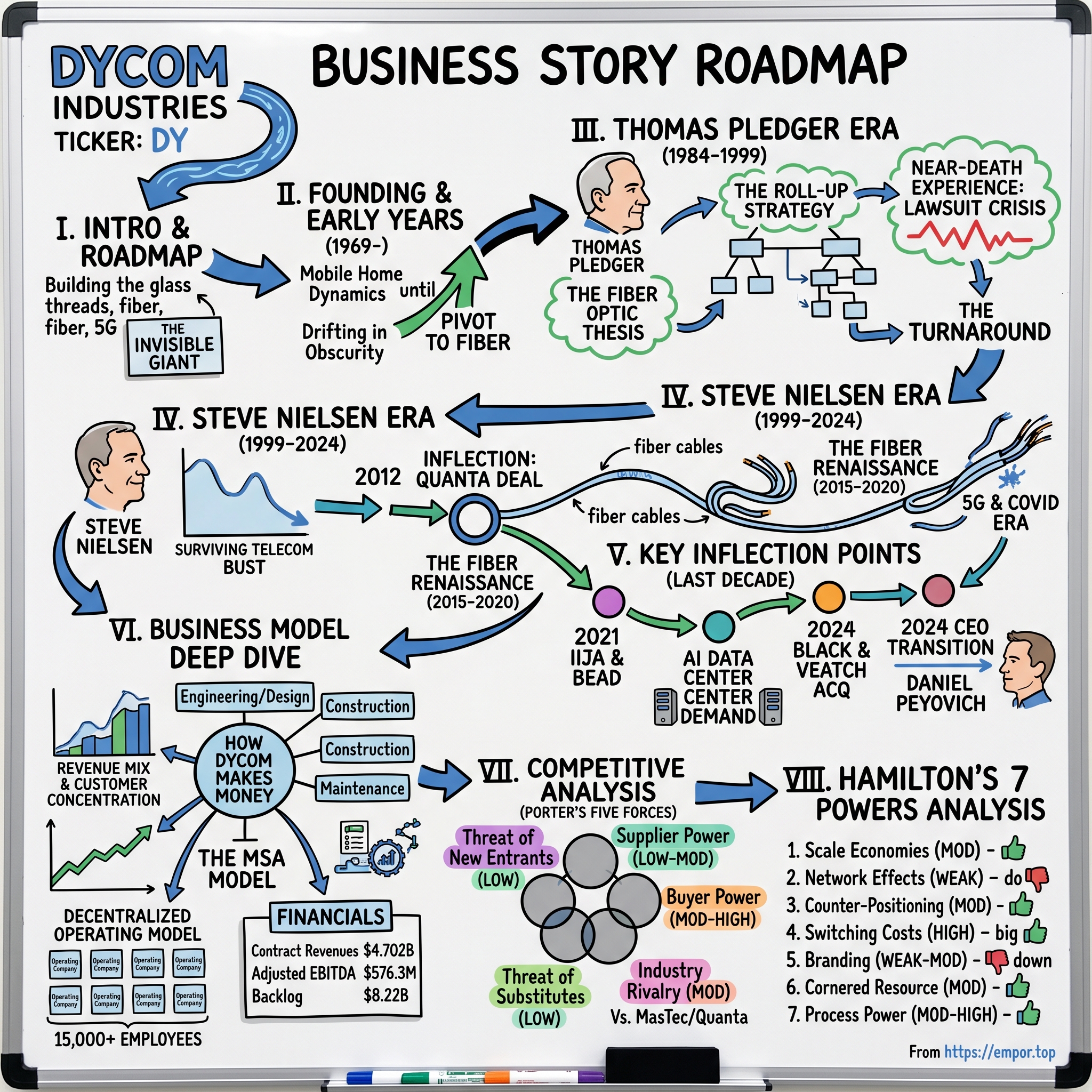

Dycom Industries: America's Invisible Infrastructure Giant

I. Introduction & Episode Roadmap

Picture this: You're scrolling through TikTok at 3 AM, streaming a 4K movie while your neighbor downloads a massive game update and your smart home devices chatter away with distant servers. Somewhere beneath your feet or strung across telephone poles, a network of impossibly thin glass threads carries billions of bits per second to make it all possible. But who actually built that network? Who climbed those poles, dug those trenches, and spliced those fiber strands that power America's digital economy?

The answer is probably a company you've never heard of: Dycom Industries.

This specialty contracting powerhouse doesn't just lay cable; they provide comprehensive program management, engineering, construction, maintenance, and installation services, primarily for major telecommunications providers undertaking significant network upgrades and expansions. From the fiber cables connecting your home to the 5G towers on your commute, Dycom's crews are likely the hands that built it.

The numbers tell a remarkable story. For fiscal year 2025, contract revenues grew 12.6% to $4.702 billion. Annual Adjusted EBITDA increased to $576.3 million (12.3% of revenues). The current market capitalization of DY is $10.22B. And the company is just getting started—fiscal 2026 guidance projects another 10-13% revenue increase.

Here's the paradox worth examining: How did a sleepy Florida contractor, incorporated when Nixon was in his first year and fiber optics was science fiction, become America's dominant "picks and shovels" play for the digital infrastructure revolution? The story involves visionary leadership, near-death experiences, transformational acquisitions, and positioning for what management calls "a generational deployment of digital infrastructure."

This article will trace Dycom's journey from obscurity to market leadership, examining how the company navigated telecom booms and busts while building something far more valuable than cables—it built irreplaceable relationships with every major carrier in America. We'll explore Thomas Pledger's roll-up strategy that defined the company's DNA, Steve Nielsen's 25-year reign that transformed Dycom into an industry juggernaut, and the new leadership team now positioning for the AI data center opportunity that could dwarf everything that came before.

For long-term investors, Dycom represents a fascinating case study in the power of specialization, the economics of infrastructure contracting, and how to surf generational technology waves without taking the direct technology risk.

II. Founding & Early Years: Before the Pivot

Dycom Industries, Inc. was incorporated in 1969 and is based in Palm Beach Gardens, Florida. Yet the founding year itself reveals little about the Dycom we know today. Incorporated in 1969 as Mobile Home Dynamics, Inc.—hardly an auspicious name for a future telecommunications infrastructure giant.

Although Dycom was founded in 1969, the company did not begin to show signs of becoming an industry leader until the mid-1980s. For fifteen years, Dycom drifted in relative obscurity, a small player in a fragmented industry where local contractors served local telephone companies. In part, the delay of its rise was attributable to finding its niche within the telecommunications infrastructure industry. The company did not begin to grow meaningfully until it shaped itself into a fiber-optics specialist, and it could not mount a campaign of aggressive growth until the industry it served embraced fiber optics as an alternative to copper wiring.

To understand why Dycom languished for so long, consider the telecommunications landscape of the 1970s. AT&T's regulated monopoly, affectionately known as "Ma Bell," controlled virtually all American telephone infrastructure. Local carriers maintained cozy relationships with preferred contractors, often unionized shops with decades of local history. Copper wire remained king—reliable, well-understood, and requiring no technological leaps. For a small Florida contractor, competing against entrenched local players for work with the telephone monopoly was a fool's errand.

While formed in 1969, Dycom's significant scale and structure evolved through consolidation and acquisitions, notably under leaders like Thomas Pledger who drove major growth phases. It wasn't founded by a single small team in the traditional startup sense but rather emerged through strategic combinations.

The telecommunications infrastructure contracting business of that era operated on a simple model: telephone companies, cable operators, and utilities needed physical infrastructure installed and maintained. They could do it themselves with expensive union labor, or they could contract it out. Most chose a mix, keeping core capabilities in-house while farming out surge work to local specialists. The result was a hyper-fragmented industry—hundreds of small contractors, each with a handful of trucks and a geographic turf they called home.

Information on the specific initial capitalization in 1969 is not readily available, typical for companies formed through mergers and acquisitions over time rather than venture funding. Growth was heavily financed through operations and subsequent stock offerings and debt following its establishment and public listings.

The company that would become Dycom spent its early years surviving rather than thriving, waiting for two things that would change everything: a technology shift to fiber optics, and a leader capable of seeing the opportunity before others did.

III. The Thomas Pledger Era: Finding the Fiber Optic Bet (1984-1999)

The Visionary Arrives

Both of these conditions for growth, when existent, created a fertile climate for Dycom's rise, but one crucial ingredient still remained: a leader capable of foreseeing and seizing the business opportunity. That individual arrived at Dycom in 1984. Through the vision and commitment to growth displayed by Thomas Pledger, Dycom began its assault on the telecommunications industry.

In 1984 he became President and Chief Executive Officer of the Company. Under Mr. Pledger's direction, sales have grown from $12.4 million to $166.7 million while net income has risen from $493,000 for FY84 to $9.6 million for FY90. In just six years, Pledger transformed a sleepy $12 million contractor into a $167 million powerhouse with nearly $10 million in profits. But the numbers only tell part of the story.

The Fiber Optic Thesis

What made Pledger different from the dozens of other contractor executives of his era? He saw the fiber optic revolution coming before it arrived, and he understood its implications for the contracting business.

Telephone companies such as AT&T, MCI, and Sprint were starting the long process of replacing copper wiring with fiber-optic lines in their long-distance lines. Pledger knew he could install the lines for far less cost than could the telephone companies.

Pledger's conviction was justified, based on reason more than biased hope. Telephone companies, with their unionized workforces, carried very expensive manpower, unable to compete with low-cost, nonunion enterprises such as Dycom. Telephone companies realized as much and eventually outsourced nearly all of their installation and service work to other firms.

This insight—that telecom carriers would increasingly outsource infrastructure work—proved prescient. The wave of outsourcing that began in the late 1980s continues today. Carriers have concluded that their core competency lies in operating networks and serving customers, not in operating fleets of bucket trucks.

The Roll-Up Strategy

In the years following Pledger's arrival at Dycom, the company completed a series of acquisitions. The company chose to grow through acquisitions rather than through internal means for a reason. "If the guy in the next territory is happy and the telephone company is happy," Pledger explained in a September 3, 1991 interview with Financial World, "then he is going to be very hard to unseat." Consequently, growth through acquisitions was adopted as Dycom's mode of attack.

This quote captures a fundamental truth about infrastructure contracting: relationships matter enormously. A telephone company that has worked with a contractor for decades, knows its crews, trusts its quality, and has established systems for dispatching work isn't going to switch to a competitor offering marginally lower prices. The switching costs are too high, the risks too great.

The company's march, completed territory by territory, region by region, began in 1984. Typically, Pledger acquired selected companies, many of which were quite small, by purchasing them with Dycom stock. The owners of the acquired businesses became Dycom managers, creating a decentralized organizational structure. To lend accountability and drive to the company's operations, the managers were awarded bonuses when specific performance objectives were achieved.

Pledger's acquisition strategy was elegant in its simplicity. Rather than trying to compete against entrenched local contractors, simply buy them. Pay with stock rather than cash—preserving capital while aligning incentives. Keep the former owners running their businesses—preserving relationships and local expertise. Pay bonuses for performance—ensuring accountability without micromanagement.

On the eve of an encouraging turning point in the telecommunications infrastructure industry, Dycom completed the acquisition of Ansco & Associates, LLC in 1990, marking a juncture but not the culmination of the acquisition spree touched off in 1984. Awarded its first master contract in 1981, Greensboro, North Carolina-based Ansco & Associates operated as long-distance and local loop fiber-optic cable installer in the southeastern United States.

Near-Death Experience: The Lawsuit Crisis

Just as Dycom seemed poised to capitalize on the fiber revolution, corporate drama nearly destroyed the company. In late 1991, Dycom's rival, Burnup & Sims Inc., launched an unsolicited attempt to merge with Dycom, an attempt aided in part by Pledger's fellow executive, Dycom President William Stover.

In November 1992, Stover appeared at the company's shareholder meeting and tried to oust Pledger. He failed. Finally, in February 1993, both parties agreed to settle, but considerable damage already had been done. In 1993, from revenues of $136.9 million, Dycom recorded a massive loss of $31.5 million. In 1994, when revenues slipped to $122.5 million, the company lost nearly $8 million.

Although Dycom ranked as one of the largest companies in the country devoted to installing fiber optics for telephone access as well as cable transmission lines, the toll incurred during the first half of the 1990s was severe. The company lost $45.6 million during a four-year period, while its stock collapsed, plummeting from $16 per share to $2 per share.

The Stover saga offers a cautionary tale about misaligned incentives in roll-up strategies. When Pledger acquired Ansco & Associates, Stover came with the deal. The subsequent power struggle, lawsuits, and SEC investigations consumed management attention at precisely the moment Dycom should have been expanding aggressively.

The Turnaround

After the debacle, Pledger entered the second half of the 1990s trying to forget the sting of the preceding years. "We've got most of our problems behind us now," he said in an October 20, 1995 interview with the South Florida Business Journal. Pledger's words were not entirely convincing, but Dycom's actions during the second half of the 1990s unequivocally demonstrated the erasure of the problems earlier in the decade. In 1996, the company generated $145 million in sales and recorded net income of $4.6 million. By the end of the decade, the company's annual revenue volume eclipsed $600 million. Annual profits flirted with the $50 million mark.

The conversion to fiber-optic technology fueled Dycom's growth, making the 1980s the company's signal decade of success. Between 1996 and the end of the decade, the company's role as a leader in providing the specialized services of a fiber-optic installer enabled it to post annual revenue growth of 48 percent.

The 1992 acquisition of Burnup & Sims significantly increased the company's size, scope, and geographic reach, marking a major step in its consolidation strategy. Ironically, Burnup & Sims—the very company that had tried to acquire Dycom—eventually became part of what is now MasTec, one of Dycom's primary competitors.

By 1999, Pledger had built Dycom from a $12 million company to a $600 million enterprise, establishing the decentralized operating model that persists today. But at 15 years in the CEO seat, it was time for fresh leadership.

IV. The Steve Nielsen Era: Building an Empire (1999-2024)

Leadership Transition

In 1999, he gave up his title as chief executive officer, scaling back his duties to those accorded to a chairman. His replacement was Steve Nielsen, who was appointed president and chief executive officer in March 1999. Nielsen, hired in 1993 to manage the company's Atlanta office, joined Dycom during the company's contentious struggle with Stover and shareholders.

In 2000, Pledger retired, paving the way for Nielsen's appointment as Dycom's chairman of the board. The succession of a new leader and the departure of Pledger, who had directed the company's course for more than 15 years, marked the beginning of a new era.

Steve Nielsen would lead Dycom for the next 25 years—an extraordinarily long tenure in an era of revolving-door CEOs. He arrived having witnessed the Stover debacle firsthand, understanding both the potential and the risks of Dycom's decentralized model. Where Pledger was the visionary roll-up artist, Nielsen would prove to be the disciplined operator who transformed Dycom from a regional consolidator into a national infrastructure giant.

Surviving the Telecom Bust (2000-2003)

Nielsen's timing could hardly have been worse. Within a year of taking the CEO role, the dot-com bubble burst, taking the telecom industry down with it. WorldCom collapsed in what was then the largest bankruptcy in American history. Global Crossing followed. Carriers that had been laying fiber at breakneck pace suddenly stopped spending entirely.

The telecom bust of 2001-2003 was a massacre for infrastructure contractors. Companies that had grown fat on the fiber build-out suddenly found themselves with expensive equipment, bloated workforces, and no work. Many went bankrupt. Dycom survived for a critical reason: its focus on "last mile" and maintenance work rather than long-haul fiber.

When a carrier cuts capital spending, it cuts new construction first. But existing networks still need maintenance—cables still get cut, equipment still fails, storms still knock down lines. Dycom's mix of construction and maintenance work provided a floor under revenues that pure construction players lacked.

The 2012 Inflection Point: Quanta Services Deal

Dycom Industries, Inc. announced that it has entered into a definitive agreement with Quanta Services, Inc. to acquire substantially all of Quanta's domestic telecommunications infrastructure services subsidiaries for approximately $275 million in cash.

The 2012 Quanta acquisition marked a turning point. Principal business facilities are located in Arizona, California, Florida, Georgia, Minnesota, New York, Pennsylvania, and Washington. The acquired subsidiaries currently operate in 49 states, serve over 300 individual customers and employ more than 2,400 personnel.

Dycom announced that it has completed its acquisition of the telecommunications infrastructure services subsidiaries of Quanta Services, Inc. for $275 million in cash plus an adjustment estimated to be $25 million to $40 million for working capital and other specified items.

Why did Quanta—itself an infrastructure giant—divest its telecom business? The transaction enables further focus on Electric Power & Pipeline Infrastructure Markets. Quanta concluded that its core competency lay in electric utilities, not telecommunications. For Dycom, the acquisition was transformational, cementing its position as the dominant pure-play telecom infrastructure contractor.

"This transaction strategically strengthens our customer base, geographic scope, and technical service offerings," said Steven Nielsen, President and Chief Executive Officer of Dycom. "It significantly enhances our rural telecommunications engineering and construction capabilities, provides additional construction resources for wireless carriers and reinforces our already robust competence in broadband construction. Given recent industry announcements indicating growing expenditures from our customers and a very attractive financing environment, we believe this is the right time to increase our scale."

The Fiber Renaissance (2015-2020)

The period from 2015-2020 represented a fiber renaissance for Dycom. AT&T's commitment to fiber-to-the-home for 12.5 million locations created enormous demand. Verizon's Fios expansion continued. Charter, Comcast, and other cable operators began fiber builds of their own.

The economics were shifting. Streaming video, cloud computing, and the proliferation of connected devices were driving bandwidth demand at rates that copper simply couldn't satisfy. For carriers, the choice became increasingly clear: deploy fiber or lose customers to competitors who would.

Dycom positioned itself as the go-to partner for these builds. Its decentralized structure—dozens of operating companies with local expertise, local relationships, and local workforces—proved ideal for the fiber build-out. No single competitor could match Dycom's combination of national scale and local execution capability.

The 5G and COVID Era Transformation (2020-2024)

The COVID-19 pandemic, paradoxically, proved a boon for Dycom. As millions of Americans suddenly worked from home, the inadequacy of existing broadband infrastructure became painfully apparent. Government stimulus poured into broadband expansion. Carriers accelerated their fiber plans.

During Mr. Peyovich's tenure, he has been instrumental in improving the Company's operations, deepening customer relationships, enhancing workplace safety, and delivering strong program management and oversight. All of this has been accomplished as revenue has grown by over $1.0 billion from $3.1 billion for fiscal year 2021 to $4.2 billion for fiscal year 2024, with Adjusted EBITDA growing 62% from $311 million to $505 million.

Nielsen's 25-Year Legacy

Dycom announced that after 25 years of service as Chief Executive Officer, Steven E. Nielsen will retire on November 30, 2024.

"The Board is exceptionally grateful to Steve for his significant contributions to Dycom over the past 25 years as CEO, including his unwavering commitment to the Company, its customers and employees."

Mr. Nielsen concluded, "I am proud of all that Dycom has accomplished during my more than 30 years working for the Company, and I want to express my heartfelt thanks to all the Dycom family for your support and commitment during my tenure as CEO. It has been an incredible honor to lead such an outstanding group of people. I am as excited today about Dycom's prospects as ever and am convinced that together you and Dan will take Dycom to greater heights and to a very successful future."

Nielsen's record speaks for itself: he took a $600 million company and built it into a $4.7 billion enterprise, navigating the telecom bust, the Great Recession, and a global pandemic along the way. More importantly, he positioned Dycom for what may be its greatest opportunity yet.

V. Key Inflection Points in the Last Decade

Inflection #1: Infrastructure Investment and Jobs Act (2021)

The 2021 Infrastructure Investment and Jobs Act included $65 billion for broadband—the largest federal investment in connectivity in American history. The Broadband Equity Access and Deployment Program (BEAD) Program, funded by the IIJA, is a $42.45 billion federal grant program that aims to connect every American to high-speed internet by funding partnerships to build infrastructure.

For Dycom, this represented a potential game-changer. Only 43% of U.S. households currently have access to fiber connectivity—a glaring gap that BEAD funding aims to close. The question isn't whether this money will be spent; it's how quickly and through which providers.

Inflection #2: The BEAD Program Opportunity

The $42.5 billion BEAD program calls for building rural broadband networks in unserved and underserved areas across the country. Thus far, 35 states and territories have completed all ten approval steps as required by the NTIA while 21 others have completed 9 of the 10.

The Broadband Equity, Access and Deployment (BEAD) program is the United States government's initiative aimed at expanding high-speed Internet access across the country. The final BEAD deployment plans for 15 states and three U.S. territories have been approved, with about $26 billion to be used to serve roughly two-thirds of the total locations with fiber or HFC infrastructure. Dycom believes that the market is in the early stages of a generational deployment of digital infrastructure.

"We have a broad footprint for both cable and telephone companies where we provide master services agreements across broad sections of the country," Nielsen said.

Inflection #3: AI Data Center Demand

Perhaps the most exciting opportunity for Dycom lies in AI infrastructure. Dycom believes this build cycle will extend deep into the next decade, with annual investments increasing over time. The company estimates the addressable market for Dycom from the spend on outside-plant data center network infrastructure is over $20 billion for the next five years alone, with spend backloaded over that period, and likely increasing further as we enter the next decade.

As hyperscalers look to scale their data center footprint, it will drive up power demands. By 2035, analysts estimate that U.S. power demand from AI data centers will grow more than 30-fold, reaching 123 gigawatts from just 4 gigawatts in 2024.

While broadband builds are key to Dycom's growth engine, the construction company is in the thick of new inter and intracity fiber builds to support hyperscaler data center providers.

Inflection #4: Black & Veatch Acquisition (2024)

Dycom Industries bought Black & Veatch's public carrier wireless telecommunications infrastructure business for $150 million in cash. The acquired firm provides wireless construction services primarily in New York, New Jersey, Missouri, Kansas, Colorado, Utah, Wyoming, Idaho and Montana and is Dycom's largest-ever wireless services acquisition.

The acquisition strategically strengthens Dycom's customer base and expands geographic scope to more broadly address growth opportunities in wireless network modernization, including Open RAN transformation initiatives, and deployment services. For fiscal 2026, the acquired business is expected to contribute $250 million to $275 million of contract revenues.

Inflection #5: CEO Transition to Daniel Peyovich (2024)

After 25 years of service as Chief Executive Officer, Steven E. Nielsen will retire on November 30, 2024. In preparation for his retirement, Mr. Nielsen worked closely with the Board of Directors on a comprehensive multi-year succession plan. As a result of that process, Daniel S. Peyovich, the Company's Executive Vice President and Chief Operating Officer, has been appointed the Company's next CEO.

Prior to joining the Company in January 2021, Mr. Peyovich spent 21 years in various leadership and management roles at Balfour Beatty Construction, ultimately serving as President of its Northwest Division.

Peyovich represents an interesting choice—an outsider with deep construction industry experience but fresh eyes on Dycom's telecom-specific business. His background at Balfour Beatty, a major construction firm, suggests the board wanted operational excellence and fresh perspectives for the next phase of growth.

VI. The Business Model Deep Dive

How Dycom Makes Money

Dycom Industries, Inc. is a leading provider of specialty contracting services to the telecommunications infrastructure and utility industries throughout the United States. Since our incorporation in the State of Florida in 1969, we have expanded our scope and service offerings organically and through acquisitions. Today, Dycom is made up of more than 40 operating companies that serve a diverse customer base across all 50 states from hundreds of field offices.

Dycom's family of companies supply telecommunications providers with a comprehensive portfolio of specialty services, including program management; planning; engineering and design; aerial, underground, and wireless construction; maintenance; and fulfillment services.

The service mix is crucial to understanding Dycom's durability. Engineering and design come first—Dycom helps carriers plan their network builds. Construction follows, whether aerial (on poles) or underground (in trenches). Maintenance ensures ongoing relationships after the initial build completes. Fulfillment services—the actual installation inside customer premises—adds another layer of recurring work.

Revenue Mix & Customer Concentration

The company's top five customers combined produced 55.7% of revenue and grew organically 16.7%. AT&T remained Dycom's largest customer, with $265.6 million or 20.9% of revenue, and grew organically 58.4%. Lumen was its second largest customer, with $146.4 million or 11.5% of revenue.

AT&T, Lumen, Verizon, Comcast, Brightspeed, Charter, and Windstream remain Dycom's top customers. All these providers are expanding their last-mile fiber networks to serve broadband and extend metro routes for data center customers.

Customer concentration represents both Dycom's greatest strength and its primary risk. Approximately 90% of the Company's revenues are from the telecommunications industry with customers such as AT&T, Lumen Technologies, Comcast, Charter Communications, Verizon, and Frontier Communications. Approximately 78% of contract revenues are multi-year master service agreements ("MSAs").

The Master Service Agreement (MSA) Model

The MSA model provides Dycom with visibility and relationship stickiness that pure project-based contractors lack. Under an MSA, Dycom agrees to provide specified services at specified rates whenever the carrier needs them. The carrier isn't obligated to any minimum volume, but they have a pre-qualified contractor ready to execute whenever work arises.

This arrangement benefits both parties. Carriers get reliable execution without lengthy procurement processes for every project. Dycom gets a steady stream of work and deep relationships that make displacement difficult. Once Dycom's crews are embedded with a carrier—knowing their systems, their standards, their people—switching to a competitor becomes costly and risky.

The Decentralized Operating Model

Dycom Industries Inc is a leading provider of specialty contracting services to the telecommunications infrastructure and utility industries throughout the United States. The company is headquartered in Palm Beach Gardens, Florida, and employs approximately 15,623 people across its operations.

Dycom operates through more than 40 subsidiary companies, each often retaining its local brand identity. A customer in Arizona might work with one Dycom subsidiary; the same carrier's operations in Georgia might use a different Dycom company with a different name. This structure preserves the local relationships that made each subsidiary valuable in the first place while providing centralized access to capital, equipment, and best practices.

Financials: The Recent Trajectory

For the full fiscal year 2025, contract revenues grew 12.6% to $4.702 billion, with organic growth of 6.8%. Annual Adjusted EBITDA increased to $576.3 million (12.3% of revenues), and net income reached $233.4 million ($7.92 per common share diluted). The company generated Operating Cash Flow of $349.1 million, up 34.8%.

Dycom's backlog at the fiscal 2025 end totaled $7.760 billion compared with $6.917 billion at the fiscal 2024 end. Of the backlog, $4.6 billion is projected to be completed in the next 12 months.

As of October 2025, DY's total backlog grew 4.7% year over year to $8.22 billion, with the next 12-month backlog rising 11.4%.

VII. Competitive Analysis: Porter's Five Forces

1. Threat of New Entrants: LOW

Starting a telecommunications infrastructure contracting business from scratch is exceptionally difficult. The barriers to entry include:

Specialized equipment: Bucket trucks, directional boring machines, fiber splicing equipment, and fleet vehicles represent millions in capital requirements. More importantly, operators need training on this specialized equipment.

Trained workforce: Fiber splicers, aerial linemen, and directional boring operators require years of training. With unemployment low and skilled trades in demand, finding and retaining qualified workers is a major challenge.

Safety certifications: Carriers require extensive safety certifications before contractors can touch their networks. Building this track record takes years.

Customer relationships: As Pledger noted, "If the guy in the next territory is happy and the telephone company is happy, then he is going to be very hard to unseat."

2. Bargaining Power of Suppliers: LOW-MODERATE

Dycom's primary inputs are labor, equipment, and materials (fiber/cable from manufacturers). Labor is the critical constraint—skilled workers are scarce and command premium wages. Equipment suppliers are fragmented. Materials (fiber, cable) come from multiple vendors with relatively standardized products.

3. Bargaining Power of Buyers: MODERATE-HIGH

The customer base is highly concentrated. Dycom's top customers have significant negotiating leverage—they're sophisticated buyers who understand the market and can credibly threaten to shift work to competitors.

However, switching costs exist. Training Dycom's replacement to a carrier's specific standards, systems, and processes takes time and introduces risk. MSAs provide some pricing protection but can be renegotiated.

4. Threat of Substitutes: LOW

Physical fiber must be physically installed. There's no software workaround, no technological substitute for putting glass strands in the ground or on poles. Satellite and fixed wireless can complement fiber but cannot replace it for high-bandwidth, low-latency applications—particularly the data center connectivity driving Dycom's growth.

5. Industry Rivalry: MODERATE

The company's primary competitors include MasTec Inc. (MTZ), which provides similar telecommunications construction services and has a broader infrastructure focus. Quanta Services Inc. (PWR) is another major competitor, offering specialty contracting services across multiple infrastructure sectors. The competitive landscape is characterized by companies competing on technical expertise, geographic coverage, customer relationships, and operational efficiency.

Quanta has a broader portfolio spanning electric power, utilities, pipelines and renewables. Its telecom exposure is smaller and less concentrated, giving DY a sharper strategic focus in the very segment experiencing its strongest secular tailwinds. MasTec is diversified across energy, power and clean-energy construction. It participates meaningfully in telecom but lacks the same level of direct fiber-to-the-home density and outside-plant expertise that Dycom has built over decades.

Porter's Verdict: Favorable industry structure with moderate profitability, improving as secular tailwinds increase demand. Low substitution threat and high barriers to entry protect incumbents; customer concentration remains the primary risk.

VIII. Hamilton's 7 Powers Analysis

1. Scale Economies: MODERATE

Dycom benefits from national scale in equipment purchasing, insurance, and access to capital markets. Larger projects justify specialized equipment investments that smaller competitors can't match. However, construction is ultimately a local business—scale advantages in one region don't necessarily translate to competitive advantages in another.

2. Network Effects: WEAK

Limited direct network effects exist in infrastructure contracting. However, Dycom's reputation among carriers creates an indirect effect—success with AT&T opens doors with Verizon, and vice versa.

3. Counter-Positioning: MODERATE

Dycom's pure-play telecom focus represents a form of counter-positioning versus diversified competitors like Quanta and MasTec. Those companies can't match Dycom's depth of telecom expertise without sacrificing focus on their other markets. Conversely, Dycom can't match their breadth—a tradeoff that works in Dycom's favor when telecom infrastructure demand is strong.

4. Switching Costs: HIGH

This is Dycom's strongest power. Once embedded with a carrier through MSAs, switching becomes costly and risky. Dycom's crews know the carrier's systems, standards, and people. Replacing them means retraining a new contractor while accepting elevated execution risk during the transition.

5. Branding: WEAK-MODERATE

Infrastructure contracting isn't a consumer-facing business. Branding matters primarily in recruiting and in reputation among procurement teams at carrier customers. Dycom's track record provides an advantage, but it's not a sustainable moat in isolation.

6. Cornered Resource: MODERATE

Skilled labor—particularly fiber splicers and directional boring operators—represents a scarce resource. Dycom's training programs and employment stability help attract and retain these workers, but competitors can bid away talent with higher wages.

7. Process Power: MODERATE-HIGH

Dycom's decentralized operating model, refined over decades, represents genuine process power. The ability to execute complex projects at scale while maintaining local relationships and accountability is difficult to replicate. New entrants can't simply copy this structure—it evolved through decades of acquisitions and cultural development.

7 Powers Verdict: Dycom's primary competitive advantages stem from switching costs (MSA relationships) and process power (decentralized execution model). These provide meaningful but not insurmountable moats. Customer concentration and labor market dynamics remain the primary vulnerabilities.

IX. Bull Case vs. Bear Case

The Bull Case

Generational Infrastructure Investment: The combination of BEAD funding, carrier fiber expansion, and AI data center demand creates a decade-plus runway for growth. Dycom estimates the addressable market from outside-plant data center network infrastructure alone is over $20 billion for the next five years.

Positioned for AI Data Center Boom: "While a large portion of new investments will go to power infrastructure and the data center buildings themselves, a massive amount of fiber infrastructure will be required," Peyovich said. Dycom is moving beyond traditional carrier work to serve hyperscalers directly—a potentially transformative expansion of its addressable market.

Operational Excellence: "Over the past three years, we have increased our revenues by 50% and expanded our EBITDA margin by approximately 450 basis points." The margin expansion demonstrates that Dycom isn't just growing revenue—it's improving profitability through operating leverage.

Strong Backlog Visibility: Dycom has a strong backlog of $7.8 billion, with $4.6 billion expected to be completed over the next 12 months, indicating robust future revenue potential.

The Bear Case

Customer Concentration Risk: AT&T represented 24.9% and Lumen Technologies 11.7% of contract revenues for the quarter. If either carrier significantly reduces spending, Dycom's revenues would suffer meaningfully.

Carrier Financial Health: Several of Dycom's key customers face their own challenges. Lumen has struggled with legacy business declines. Frontier emerged from bankruptcy. Windstream is merging with Uniti. Carrier financial stress could translate to reduced capital spending.

BEAD Program Delays: The BEAD program has experienced significant administrative delays. While funding is allocated, actual construction is still ramping. Dycom Industries Inc (NYSE:DY) is not including any potential revenue from the BEAD program in its fiscal 2026 outlook, indicating uncertainty in this area.

Labor Market Tightness: Skilled telecom construction workers are scarce. Wage pressure could compress margins, particularly if work volumes increase faster than Dycom can scale its workforce.

Competition from Diversified Players: While Dycom's telecom focus is currently advantageous, Quanta and MasTec have greater financial resources and could aggressively pursue telecom opportunities if the market becomes attractive enough.

X. Key KPIs to Track

For long-term investors monitoring Dycom, three metrics matter most:

1. Total Backlog and Next-12-Month Backlog

Backlog provides the best forward visibility into Dycom's revenue trajectory. Total backlog indicates overall contracted work; next-12-month backlog indicates near-term revenue conversion. Dycom's backlog reached $8.22 billion, with $4.99 billion expected to be completed within the next 12 months. Watch for quarterly changes—a growing backlog signals strong demand; a shrinking backlog signals potential trouble.

2. Customer Concentration Trend

Is Dycom diversifying its customer base or becoming more concentrated? "In that same time period, we further diversified our customer base, shifting our top five customers to 55% of revenue in fiscal 2025, from 66% in fiscal 2022." Continued diversification reduces risk; increasing concentration elevates it.

3. Adjusted EBITDA Margin

Revenue growth means nothing if margins compress. Adjusted EBITDA grew 19.8% to $576.3 million from fiscal 2024. Adjusted EBITDA margin rose by 70 bps to 12.3%. Margin expansion indicates operating leverage and disciplined cost management; compression signals pricing pressure or labor cost inflation.

XI. Regulatory and Accounting Considerations

BEAD Program Risks: Federal broadband funding flows through state programs with varying implementation timelines. The new administration's approach to BEAD could accelerate or delay deployment. Dycom has deliberately excluded BEAD from its fiscal 2026 guidance, providing conservatism but also suggesting meaningful uncertainty.

Customer Contract Terms: Dycom's MSAs typically allow customers to terminate or reduce volumes without penalty. While relationships are sticky, they're not contractually guaranteed.

Goodwill and Intangibles: Dycom's acquisition history has accumulated goodwill on the balance sheet. Significant deterioration in the telecom infrastructure market could trigger impairment charges.

Labor Classification: Infrastructure contracting relies heavily on both employees and subcontractors. Regulatory changes affecting independent contractor classification could impact Dycom's cost structure and flexibility.

XII. Conclusion: America's Digital Backbone Builder

Dycom Industries represents a fascinating investment case—a pure-play infrastructure builder positioned at the intersection of multiple secular trends. The thesis is straightforward: America needs vastly more fiber, and someone has to install it. Dycom has spent five decades becoming the best-positioned company for that job.

The opportunity ahead is genuinely exceptional. Dycom believes that the market is in the early stages of a generational deployment of digital infrastructure. BEAD funding will connect millions of underserved Americans. Carrier fiber expansion continues. And AI data centers—perhaps the most capital-intensive infrastructure buildout in history—are just beginning.

Yet the risks are real. Customer concentration leaves Dycom vulnerable to spending decisions by a handful of carriers. Competition from well-capitalized diversified players will intensify as the opportunity grows. And Dycom must execute flawlessly to capture its share of a market that will attract every infrastructure contractor in America.

For long-term investors, Dycom offers exposure to America's digital infrastructure buildout without the technology risk inherent in carrier stocks. When AT&T deploys fiber, it's betting on consumer adoption of faster broadband. When Dycom deploys fiber, it gets paid regardless of whether consumers ultimately subscribe. That "picks and shovels" positioning—profitable regardless of which carriers win—represents Dycom's fundamental appeal.

From Thomas Pledger's roll-up strategy in the 1980s to Steve Nielsen's quarter-century of empire building to Daniel Peyovich's new mandate for the AI era, Dycom has consistently evolved to serve America's communications needs. The company that began as "Mobile Home Dynamics" in 1969 now builds the invisible infrastructure connecting hundreds of millions of Americans. Not bad for a company you've probably never heard of.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube