Domino's Pizza: From College Dorm Pizza to Global Tech-Powered Empire

I. Introduction & Opening

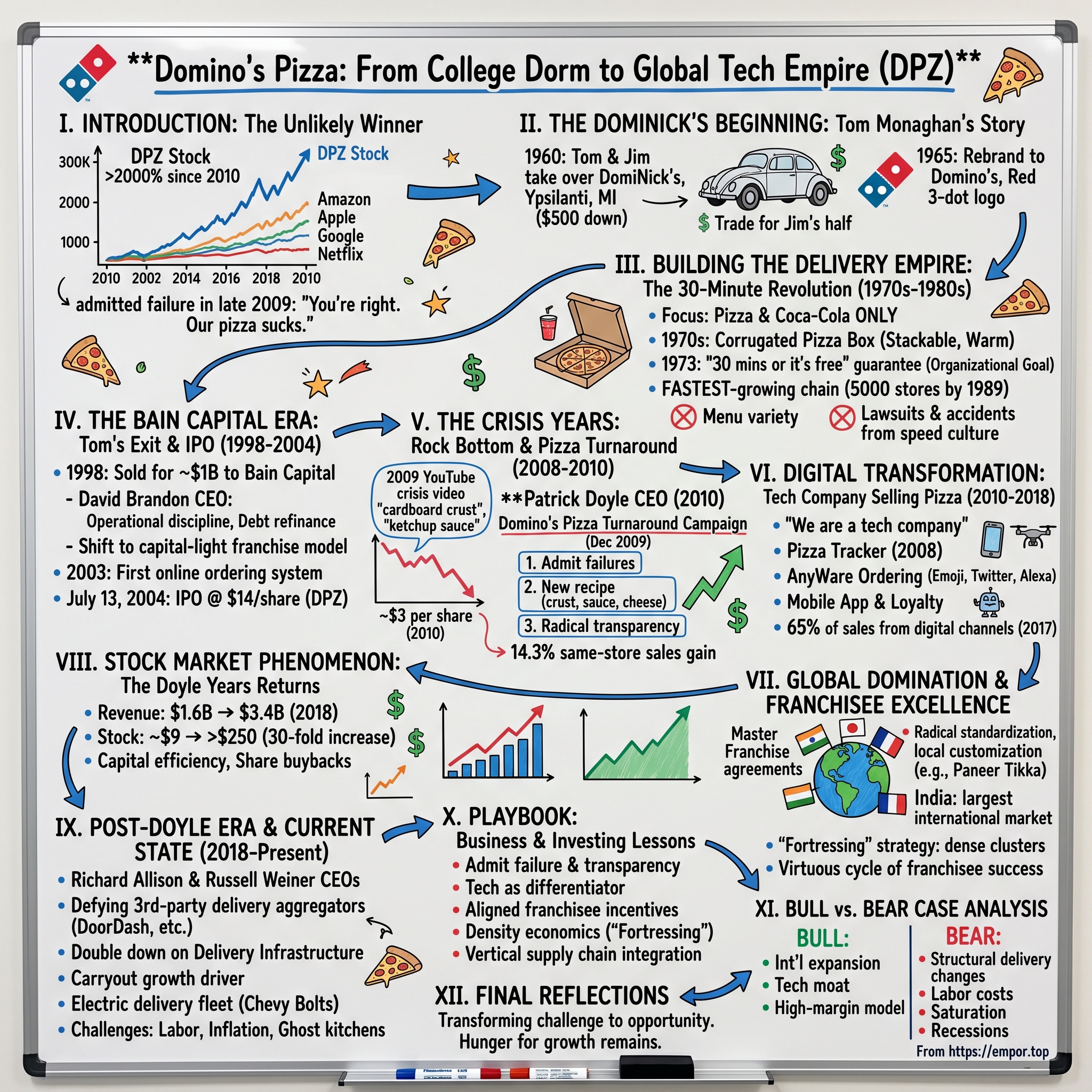

Picture this: It's 2017, and a Wall Street analyst is staring at their Bloomberg terminal in disbelief. Over the past seven years, a pizza delivery company—yes, a pizza company—has outperformed Amazon, Apple, Google, and Netflix in stock returns. The company? Domino's Pizza, the same brand that customers had mercilessly mocked online just years earlier for serving "cardboard crust" and "ketchup sauce."

This isn't just a turnaround story. It's the tale of how a single pizza shop in Ypsilanti, Michigan, founded by a orphanage-raised college dropout with $500 down, transformed into the world's largest pizza delivery empire. Along the way, Domino's would pioneer the 30-minute delivery guarantee, survive near-bankruptcy, endure private equity ownership, and ultimately reinvent itself as a technology company that happens to sell pizza. The story of Domino's isn't merely about impressive numbers—though the numbers are staggering. Since 2010, the company's stock appreciated more than 2,000%, outperforming Amazon, Apple, Netflix, and Alphabet. But step back further, and the returns become almost unfathomable: A $1,000 investment at Domino's July 13, 2004 IPO would be worth more than $56,000 by February 2020.

What makes this transformation remarkable isn't just the financial engineering or operational excellence. It's that Domino's achieved these returns by doing something most corporations never dare: admitting complete failure. In late 2009, with their stock languishing and customers openly mocking their product online, Domino's did the unthinkable. They looked America in the eye and said, "You're right. Our pizza sucks. We're sorry."

From that moment of brutal honesty emerged one of the greatest corporate transformations in modern business history—a story that holds profound lessons for investors, entrepreneurs, and anyone who's ever wondered whether a legacy brand can truly reinvent itself in the digital age.

II. The DomiNick's Beginning: Tom Monaghan's Origin Story

The rain was coming down hard in Jackson, Michigan, in 1943 when six-year-old Tom Monaghan and his younger brother Jim arrived at St. Joseph Home for Children. Their father had died two years earlier, leaving their mother unable to care for them alone. For the next six years, the Felician Sisters would raise the boys, instilling in Tom a devotion to Catholic faith that would shape his entire life—and eventually, the culture of a pizza empire.

Fast forward to December 9, 1960. Tom, now 23 and fresh out of the Marines, stands inside a small pizza shop at 507 Cross Street in Ypsilanti, Michigan, snow swirling outside. He and his brother Jim have just taken over DomiNick's, a failing pizza joint near Eastern Michigan University. The price? A $500 down payment and $900 in borrowed money. The previous owner, Dominick DeVarti, probably thought he was getting the better end of the deal, unloading a struggling operation on two brothers with no restaurant experience.

Within eight months, the partnership would fracture in the most American way possible. Jim, exhausted by the grueling hours and slim profits, wanted out. Tom, seeing something his brother didn't—or perhaps driven by something deeper, that orphanage-instilled determination—made him an offer: a used Volkswagen Beetle for his half of the business. Jim took the car and ran. It might be the worst trade in business history.

Now alone, Tom threw himself into the operation with monastic dedication. He slept in the store. He lived on pizza. He studied every aspect of the business with the intensity of someone who had grown up with nothing and was determined never to go back. By 1965, he had opened two additional locations, and it was time for a rebrand. DomiNick's was DeVarti's name, not his. An employee suggested "Domino's," and Tom loved it.

The logo he designed was deceptively simple: three dots on a red domino, each dot representing one of his three stores. His plan was to add a new dot with each new location—a visual scoreboard of his empire's growth. That plan lasted exactly as long as you'd expect for someone with Tom's ambition. The dots would have covered the entire logo within a few years.

But success bred conflict. In 1975, Amstar Corporation, the maker of Domino Sugar, came calling with lawyers in tow. They claimed trademark infringement, arguing that a pizza company using "Domino's" would confuse consumers. The case dragged on for five years, threatening to crush the growing chain under legal fees. Tom fought with the tenacity of someone who had already lost everything once as a child and refused to lose it again as an adult.

On May 2, 1980, the Fifth Circuit Court of Appeals in New Orleans delivered its verdict: Domino's Pizza could keep its name. Tom had won. But the real victory wasn't in the courtroom—it was in what he'd built while the lawyers argued. By the time the gavel fell, Domino's had grown from three stores to 200, spreading across college towns like wildfire.

The orphan from Jackson had discovered something profound: America's college students didn't need great pizza. They needed pizza that showed up.

III. Building the Delivery Empire: The 30-Minute Revolution (1960s-1980s)

Tom Monaghan had a theory about pizza that would have horrified any self-respecting Italian chef: quality was negotiable, but time was not. This wasn't cynicism—it was genius product-market fit. While competitors focused on expanding menus with subs, salads, and pasta, Tom went the opposite direction. In 1973, he made a decision that seemed insane: he stripped the menu down to just pizza and Coca-Cola. Nothing else.

"We're not trying to be everything to everybody," he'd tell franchisees. "We're trying to be one thing done faster than anyone else."

The simplification was strategic brilliance disguised as limitation. Fewer ingredients meant easier inventory management. One product meant streamlined training. But the real innovation came from Tom's obsession with the physics of pizza delivery. He noticed drivers stacking pizza boxes in their cars, crushing the bottom pizzas under the weight. The industry accepted this as the cost of doing business. Tom saw it as an engineering problem.

Working with corrugated cardboard manufacturers, Domino's developed a revolutionary new pizza box in the early 1970s. Unlike the flimsy chipboard predecessors that collapsed under pressure, this box could be stacked without crushing. The corrugated design created air pockets that kept pizzas warm during delivery. Drivers could now carry twice as many pizzas per trip without quality degradation. It was the kind of innovation that seemed obvious in retrospect but required someone to care enough about the unglamorous details.

Then came the guarantee that would define Domino's for a generation and nearly destroy it: "30 minutes or it's free."

Launched in 1973, the guarantee wasn't just marketing—it was organizational psychology. Every employee, from the phone operator to the driver, now had a clear, measurable goal. The entire operation restructured around speed. Stores were located based on delivery radius calculations. Drivers memorized street layouts like their lives depended on it. The make line became a carefully choreographed dance where every movement was optimized to shave seconds.

The numbers were staggering. By 1985, Domino's was opening a new store every day and a half. The company had grown to 2,841 locations, making it the fastest-growing restaurant chain in America. The franchise model was printing money—franchisees paid $6,500 for the rights to a territory, and Domino's provided the blueprint for turning that investment into a six-figure annual income.

But the model had a dark side that wouldn't fully manifest until later. The 30-minute guarantee created a culture of speed at any cost. Drivers ran red lights. They drove on sidewalks. By the late 1980s, Domino's drivers were involved in dozens of serious accidents annually. The company faced hundreds of lawsuits. In one tragic case in 1989, a Domino's driver struck and killed a woman, resulting in a $78 million judgment against the company.

Yet even as the lawsuits mounted, the model kept working. Why? Because Tom had discovered something fundamental about American consumer behavior: we'll forgive a lot for convenience. The pizza might be mediocre, but it would be mediocre at your door in less time than it took to watch a sitcom.

The franchise model itself was a masterwork of aligned incentives. Domino's didn't just sell franchise rights; they controlled the supply chain. Franchisees had to buy ingredients, equipment, and supplies from Domino's commissaries. This gave corporate two revenue streams—royalties on sales and margins on supplies. It also meant quality control. Every Domino's pizza in America used the same cheese blend, the same sauce recipe, the same dough formula. A pizza in Ypsilanti tasted identical to one in San Diego.

By 1989, Domino's had 5,000 stores and $2.3 billion in sales. Tom Monaghan was worth an estimated $500 million. He owned the Detroit Tigers, having purchased the team for $53 million in 1983. He collected Frank Lloyd Wright artifacts and built a corporate headquarters that looked like a prairie-style mansion. The orphan from Jackson had become one of the richest men in Michigan.

But success was taking its toll. The lawsuits from the 30-minute guarantee were mounting. Competition was intensifying as Pizza Hut and Little Caesars expanded aggressively. Most troubling for Tom, his Catholic faith was increasingly at odds with his business empire. He had everything he'd ever wanted, and it was making him miserable.

IV. The Bain Capital Era: Tom's Exit and Corporate Evolution (1998-2004)

In September 1998, Tom Monaghan stood before a room full of Domino's executives and made an announcement that stunned everyone: he was selling the company. Not to a competitor, not to another food conglomerate, but to Bain Capital, the Boston private equity firm co-founded by a young consultant named Mitt Romney.

The price was approximately $1 billion for 93% of the company, with Tom retaining a small stake. For Bain, it was their largest investment to date. For Tom, it was liberation. He'd grown increasingly devoted to Catholic philanthropy, pouring hundreds of millions into Ave Maria University in Florida. The pizza empire had become a distraction from what he saw as his true calling.

"I want to die broke," he told confidants, a strange ambition for someone who'd grown up in poverty.

Bain Capital didn't buy Domino's for its pizza recipe. They bought it for what private equity firms always buy: inefficiency that could be wrung out through financial engineering and operational discipline. The firm immediately installed David Brandon, former CEO of Valassis Communications, as the new chief executive. Brandon was everything Tom Monaghan wasn't—a University of Michigan MBA with a background in marketing and a comfort with corporate buzzwords.

The Bain playbook was predictable but effective. First, they refinanced Domino's debt, taking advantage of lower interest rates to reduce capital costs. Then they attacked the cost structure with surgical precision. Commissaries were consolidated. Underperforming stores were closed. Corporate headcount was slashed. The famous 30-minute guarantee, now a legal liability generating millions in lawsuit settlements, was quietly discontinued in 1993, before Bain's arrival, but its cultural aftermath still needed cleaning up.

But Bain's smartest move was recognizing what Domino's actually was: not a restaurant company, but a logistics and real estate business that happened to involve pizza. They doubled down on the franchise model, selling off company-owned stores to franchisees. By 2004, 90% of Domino's locations were franchised, up from 75% in 1998. This transformed Domino's into a capital-light business with predictable royalty streams—exactly the kind of company public markets would love.

The technology investments during this period were modest but prescient. In 2003, Domino's became one of the first major chains to accept orders online. The system was primitive—customers had to create accounts, the interface was clunky, and it frequently crashed. But it worked just well enough to prove a concept: pizza customers would trade human interaction for convenience. By 2004, Bain had transformed Domino's into an IPO-ready machine. On July 13, 2004, David Brandon rang the opening bell at the New York Stock Exchange. Domino's began trading under the ticker symbol "DPZ," with an initial public offering price of $14.00 per share for 24,221,929 shares. In the offering, 9,375,000 shares were being sold by Domino's Pizza, Inc. and 14,846,929 shares were being sold by selling stockholders—primarily Bain Capital funds cashing out their investment.

The IPO was, by any measure, underwhelming. The stock came in at $14 a share—a dollar shy of the low end of the company's estimated $15 to $17 range, and the stock's day-one price slipped from $14 to $13.50. The timing couldn't have been worse. "This was not the ideal time for a pizza company to go public," said analyst Rick Munarriz. "Krispy Kreme has had its implosion, which is bad news for anyone making dough in the tactical sense. Papa John's isn't doing so incredibly well right now, either. It's all a matter of bad timing."

But Bain had extracted their returns through financial engineering, not stock appreciation. They'd bought Domino's for roughly $1 billion, loaded it with debt, collected management fees, and were now selling shares to public investors while keeping control. It was a textbook private equity play, executed flawlessly. For Bain, the IPO was a success regardless of the stock price.

For everyone else, Domino's looked like damaged goods—a debt-laden pizza chain going public just as the low-carb craze was decimating bread-based businesses. No one could have imagined that this mediocre IPO would become one of the greatest investments of the next decade.

V. The Crisis Years: Rock Bottom and the Patrick Doyle Revolution (2008-2010)

The YouTube video posted in April 2009 was brutal in its simplicity. A grainy cell phone camera showed two Domino's employees in Conover, North Carolina, doing unspeakable things to food that would soon be delivered to customers. One employee stuck cheese up his nose before placing it on a sandwich. Another passed gas on salami. They narrated their actions with juvenile glee, apparently thinking it was hilarious.

Within days, the video had millions of views. Domino's stock, already struggling in the depths of the financial crisis, cratered further. But this wasn't the cause of Domino's problems—it was merely a symptom of a company that had lost its way so completely that even its own employees held it in contempt. When Patrick Doyle took over as CEO of Domino's Pizza in 2010, the company was struggling. Its stock was languishing around $3 per share, customer satisfaction was low, and the brand was seen as a mediocre fast-food option. But the real crisis went deeper than bad financials. It was existential.

Patrick Doyle wasn't supposed to be CEO. He'd joined Domino's in 1997 as Senior Vice President of Marketing after stints at Gerber and First Chicago Bank. A University of Michigan economics grad with a University of Chicago MBA, he was cerebral, methodical, and utterly lacking in the bombast typically associated with pizza executives. When David Brandon stepped down in March 2010, the board turned to Doyle almost by default—he was the insider who understood the problems best. The real problem became crystal clear when Doyle started taking a closer look at why their shares were dropping so much. To their shock, they discovered that there were multiple blog posts criticising Domino's. Some said that the crust tasted like cardboard, while others said that their sauce tasted like ketchup. The criticisms were so widespread that when Domino's ran its own consumer tests, it found that people liked the same pizza less if they knew it was from Domino's than if they thought it was a pizza from another chain.

"We had somehow created a situation," Doyle said, "where people liked our pizza less if they knew it was from us."

What happened next would become one of the most studied marketing campaigns in business history. Rather than quietly fixing the problem behind closed doors—the playbook every other corporation would follow—Domino's did something unprecedented. They took their harshest criticism and turned it into advertising.

The now-famous video called "Domino's Pizza Turnaround" premiered in December 2009. It opened with ominous music as real customer comments filled the screen. In the video, Domino's leaders and employees read scathing critiques of the company and its pizza. Marketing Director Karen Kaiser appeared on screen, reading reviews. Product manager Meredith Baker almost choked up. "It's hard to watch," she said.

But the masterstroke wasn't just the admission of failure—it was what came next. The executive kitchen staff tried ten new crust types. They created 15 different sauces. They reviewed dozens of new cheeses before they got it right. After months of testing, the company rolled out a new and improved formula with garlic-seasoned crust, richer sauce, and better cheese.

The TV spot posted the highest Millward Brown ad-testing score ever recorded at that time. It was so successful that it yielded an industry record for same-store sales gains, of 14.3% in the first quarter after the launch. From December 2009 to December 2010, Domino's stock shot up 130%.

The transparency built trust in a way that traditional advertising never could have. It was corporate vulnerability as competitive advantage—a playbook that would be studied in business schools for years to come.

VI. Digital Transformation: Becoming a Tech Company That Sells Pizza (2010-2018)

"We are as much a tech company as we are a pizza company," Patrick Doyle declared in 2015, standing in front of a room full of skeptical Wall Street analysts. It was a bold claim for a company that five years earlier couldn't even make edible pizza. But Doyle wasn't bluffing—he was describing a transformation already well underway.

The digital revolution at Domino's had actually begun before Doyle's tenure, with a primitive innovation that would become the foundation of everything: the Pizza Tracker. Pizza Tracker (2008, expanded under Doyle) – Letting customers follow their order in real-time. The system was revolutionary in its simplicity. It showed customers exactly where their pizza was in the preparation process—from "Order Placed" to "Prep" to "Bake" to "Quality Check" to "Out for Delivery."

The psychology was brilliant. By making the black box of pizza delivery transparent, Domino's transformed waiting from an anxiety-inducing unknown into entertainment. Customers would gather around screens, watching their pizza's progress like a sporting event. The tracker didn't actually make pizzas arrive faster, but it made the wait feel shorter.

But Doyle understood something deeper: in the age of smartphones, convenience wasn't just about speed—it was about reducing friction to zero. Every click, every form field, every moment of hesitation was a potential lost sale. Domino's needed to be everywhere their customers were, ready to take an order with minimal effort.

The innovations came in rapid succession:

AnyWare Ordering (2015) – Allowing orders via Twitter, smartwatches, Alexa, and even texting a pizza emoji. The pizza emoji ordering system was particularly inspired—customers could literally text a pizza emoji to Domino's and their regular order would be on its way. It was gimmicky, sure, but it was also genius marketing. Every time someone used a pizza emoji in any context, they were reminded of Domino's.

Domino's Mobile App – Streamlining ordering and loyalty rewards. The app wasn't just functional; it was addictive. Domino's gamified the ordering process, adding features like saving favorite orders, tracking loyalty points, and even a "Pizza Builder" that let customers watch their creation come together virtually.

By 2017, 65% of Domino's sales came from digital channels, far outpacing competitors. For context, Pizza Hut, their largest competitor, was still struggling to get customers to adopt online ordering at all. Papa John's had a functional website but nothing approaching Domino's sophistication. But the most audacious innovation wasn't digital—it was physical. In October 2015, Domino's unveiled the DXP™ (Delivery Expert), a specially designed and built pizza delivery vehicle. The car holds up to 80 pizzas and features a warming oven, as well as storage areas designed for easy loading and unloading of pizzas and other menu items. It was born out of a three-year design process that started with a crowdsourcing competition hosted by Local Motors, fielding 385 entries from designers around the world.

The DXP was absurd, impractical, and absolutely brilliant from a marketing perspective. Only 100 units were built and deployed across 25 markets, but the earned media was worth millions. Every tech blog, car magazine, and local news station ran stories about the "pizza car." It reinforced the message: Domino's cared about delivery in a way no other pizza company did.

The autonomous vehicle experiments pushed the envelope even further. Domino's tested drone delivery, partnered with Ford on self-driving delivery vehicles, and experimented with robot delivery. Most of these were publicity stunts that never scaled, but that wasn't the point. Each announcement reinforced Domino's position as the innovation leader in pizza delivery.

The real genius of Doyle's strategy was understanding that Domino's didn't need to be first to market with every technology—they just needed to be perceived as the most innovative. While competitors scrambled to catch up with basic online ordering, Domino's was already three steps ahead, talking about AI and autonomous vehicles.

By the time Doyle stepped down in 2018, Domino's had achieved something remarkable: they'd transformed from a company known for bad pizza and fast delivery into a company known for technology and fast delivery. The pizza quality improvements were table stakes—the technology moat was what separated them from everyone else.

"We are as much a tech company as we are a pizza company," wasn't just a slogan. It was a reality that manifested in every aspect of the business, from the supply chain management systems to the franchisee point-of-sale terminals to the customer-facing apps. Domino's had become what every traditional company claims to want to be but rarely achieves: a genuine digital-first business that happened to operate in a traditional industry.

VII. Global Domination and Franchisee Excellence

Walk into a Domino's in Mumbai, India, and you'll find something surprising on the menu: a pizza topped with paneer tikka and tandoori chicken. Travel to Japan, and you might encounter a Mayo Potato pizza. In France, they serve a Savoyarde with reblochon cheese and lardons. Yet despite these local variations, the operational DNA—the ordering system, the delivery promise, the kitchen layout—remains unmistakably Domino's.

This is the paradox at the heart of Domino's global strategy: radical standardization wrapped in local customization. As of 2018, Domino's had approximately 15,000 stores, with 5,649 in the United States, 1,500 in India, and 1,249 in the United Kingdom. Domino's has stores in over 83 countries and 5,701 cities worldwide. But unlike McDonald's or KFC, which often struggle to translate American fast food to global palates, Domino's cracked the code by being flexible on product and inflexible on process.

The international expansion accelerated dramatically under Doyle's leadership, but the foundation was laid much earlier through master franchise agreements. Rather than trying to manage thousands of international stores directly, Domino's partnered with large, sophisticated operators who understood local markets. Jubilant FoodWorks runs the India operation. Domino's Pizza Enterprises manages Australia, New Zealand, and several European markets. Each master franchisee has significant autonomy on menu and marketing but must adhere to Domino's core operational standards.

India became the crown jewel of international operations—and a case study in adaptation. When Domino's entered India in 1996, the conventional wisdom was that Indians wouldn't pay for pizza delivery. The country had a robust street food culture and domestic help was affordable for middle-class families. Why would anyone pay a premium for delivered pizza?

Domino's India CEO Ajay Kaul saw it differently. He recognized that India's emerging middle class, particularly young professionals in cities like Bangalore and Gurgaon, valued time as much as their Western counterparts. But the product needed radical localization. Beef was out for religious reasons. Pork too. Even the cheese needed adjustment—Indians preferred a milder flavor profile.

The solution was brilliant: keep the operational excellence, change everything else. Domino's India developed an entirely vegetarian menu alongside meat options. They introduced pizzas with tandoori paneer, pepper barbecue chicken, and spicy vegetables that would horrify Italian purists but delighted Indian customers. They even adjusted portion sizes, recognizing that Indian families often shared meals differently than Americans.

But here's where it gets interesting from an investor's perspective: the franchise model in international markets often delivered better unit economics than in the U.S. Labor costs were lower. Real estate was cheaper. And in many emerging markets, Domino's faced less sophisticated competition. A Domino's franchise in India could generate 30-40% EBITDA margins compared to 15-20% in the U.S.

The supply chain strategy internationally mirrors but doesn't replicate the U.S. model. Domino's operates 25 domestic and five Canadian dough manufacturing and supply chain facilities. Internationally, they partner with local suppliers while maintaining quality standards through rigorous auditing. This capital-light approach allows rapid expansion without massive infrastructure investment.

The "fortressing" strategy—a term Doyle popularized—deserves special attention. Rather than spreading stores thinly across new territories, Domino's clusters them densely in specific areas. A neighborhood might have three or four Domino's locations within a two-mile radius. This seems counterintuitive—wouldn't they cannibalize each other's sales?

In practice, fortressing drives three critical advantages. First, delivery times shrink dramatically when stores are closer to customers. Second, marketing efficiency improves—one billboard or TV ad reaches multiple store territories. Third, and most importantly, it creates a network effect. The more Domino's stores in an area, the more top-of-mind the brand becomes. Customers default to Domino's not because it's the best pizza, but because it's the most convenient and reliable.

The franchise model itself is a masterwork of aligned incentives. Franchisees pay an initial fee (ranging from $25,000 to $75,000 depending on the market), ongoing royalties (5.5% of sales), and contribute to a national advertising fund (6% of sales). But here's the key: Domino's makes money primarily from royalties and supply chain, not from selling franchises. This means corporate success depends entirely on franchisee success.

The average Domino's franchisee in the U.S. owns about nine stores, generating roughly $1 million in annual revenue per location. With EBITDA margins around 15-20%, a well-run franchise can generate $150,000-$200,000 in annual cash flow. For a franchisee with nine stores, that's $1.3-1.8 million in annual EBITDA. The payback period on a new store is typically 3-5 years—attractive enough to encourage expansion but not so attractive that it creates unsustainable growth.

This model creates a virtuous cycle. Successful franchisees want to open more stores. They have the capital and operational expertise to do so. They become advocates for the brand, recruiting other franchisees. And because they're invested for the long term, they maintain standards that protect brand value.

The international franchise agreements add another layer of financial engineering. Master franchisees typically pay higher royalty rates (up to 7% in some markets) but get exclusive territorial rights for entire countries or regions. They're responsible for sub-franchising, marketing, and supply chain in their territories. This creates a multi-level revenue stream for Domino's corporate while minimizing operational complexity.

By 2017, this model had propelled Domino's past Pizza Hut to become the largest pizza company globally by sales. The achievement was particularly sweet given Pizza Hut's decades-long head start in international markets. But Domino's had turned its latecomer status into an advantage, learning from Pizza Hut's mistakes and building a more efficient, technology-enabled operation from the start.

VIII. Stock Market Phenomenon: The Doyle Years Returns

The numbers are so staggering they bear repeating: When Doyle became CEO in 2010, Domino's stock was at $8.76 (pre-split). By the time he left in 2018, it had soared to over $250 (post-split, equivalent to $500+ today). During a period when the S&P 500 roughly doubled, Domino's increased nearly 30-fold. Revenue grew from $1.6B (2010) to $3.4B (2018). Stock outperformed Amazon, Apple, and Google during his tenure.

To understand why the market fell so deeply in love with Domino's, you need to understand what Wall Street values above all else: predictable, high-margin, capital-light growth. Under Doyle, Domino's delivered all three in abundance.

The predictability came from the franchise model. With 90% of stores franchised, Domino's corporate revenues consisted primarily of royalties—a 5.5% cut of every pizza sold. This transformed volatile restaurant sales into steady, recurring revenue streams. Even if same-store sales were flat, new store openings guaranteed revenue growth. And because franchisees bore the capital costs, Domino's could grow without diluting returns on invested capital.

The margins were exceptional by restaurant standards. While a typical restaurant operates at 5-10% net margins, Domino's corporate consistently delivered 25-30% EBITDA margins. The supply chain business, which sells ingredients and equipment to franchisees, operated at lower margins but generated substantial cash flow with minimal capital requirements. Every basis point improvement in cheese costs or delivery efficiency dropped straight to the bottom line.

But the real magic was in the capital efficiency. After the chain kept its growth to a relative minimum, adding just 150 locations between 2010 and 2014, expansion took off. Domino's has added 500 locations since, according to Technomic data. Yet corporate spent almost nothing on these new stores—franchisees funded them entirely. This allowed Domino's to generate returns on invested capital exceeding 25%, astronomical for a "restaurant" company.

The technology investments amplified these advantages. Digital ordering reduced labor costs in stores. The supply chain systems minimized waste and inventory carrying costs. Dynamic pricing algorithms optimized promotional spending. Every efficiency gain improved franchisee profitability, which encouraged more store openings, which generated more royalties—a beautiful flywheel that Wall Street couldn't resist.

The share buyback program turbocharged returns further. With minimal capital needs for growth, Domino's returned massive amounts of cash to shareholders. Between 2010 and 2018, the company repurchased over $2 billion worth of shares, reducing the share count by nearly 40%. This financial engineering meant that even modest earnings growth translated into spectacular earnings-per-share growth.

Analysts struggled to find appropriate comparisons. Was Domino's a restaurant company? Its asset-light model looked nothing like McDonald's or Yum Brands. Was it a technology company? It certainly had the growth rates and margins of one. Was it a franchise company? Yes, but one with control over supply chain that most franchisors could only dream of.

The multiple expansion was breathtaking. In 2010, Domino's traded at roughly 10x earnings, appropriate for a struggling restaurant chain. By 2018, it commanded a 30x multiple, more typical of a high-growth technology company. The rerating alone accounted for a threefold increase in stock price, on top of the earnings growth.

Hedge funds and growth investors piled in. By 2015, institutional ownership exceeded 90%. Tiger Global, Pershing Square, and other prominent funds took major positions. The stock became a momentum darling, rising on every earnings beat and brushing off any negative news. When same-store sales growth slowed from 10% to 8%, the stock rose anyway—8% was still exceptional by restaurant standards.

The international growth story provided another leg of the bull thesis. With only 40% of stores outside the U.S., compared to 60%+ for McDonald's, Domino's had a clear runway for expansion. Markets like India, China, and Brazil offered decades of potential growth. And unlike the U.S., where delivery competition was intensifying, Domino's often enjoyed first-mover advantages internationally.

The all-time high Domino's Pizza Inc stock closing price was $538.35 on December 31, 2021. Even after Doyle's departure, the momentum continued for several years, a testament to the durability of the transformation he engineered.

IX. Post-Doyle Era and Current State (2018-Present)

Domino's Pizza president and CEO Patrick Doyle will step down on June 30, the company said Tuesday, after eight years leading the operator in what's widely regarded as a groundbreaking turnaround for the pizza chain. Richard Allison, president of Domino's International, will take over as CEO.

Richard Allison's inheritance in July 2018 was both blessing and curse. He took over a company firing on all cylinders, with 29 consecutive quarters of same-store sales growth and a stock price that had made early investors wealthy beyond imagination. But he also inherited sky-high expectations and new challenges that Doyle hadn't faced.

The most pressing was third-party delivery. DoorDash, Uber Eats, and Grubhub were transforming food delivery from a pizza-dominated category into an everything category. Suddenly, Domino's wasn't just competing with Pizza Hut and Papa John's—they were competing with every restaurant within a five-mile radius, all accessible through a single app.

Allison's response was quintessentially Domino's: double down on what you do best. While competitors signed up with third-party platforms, accepting 15-30% commission rates that destroyed margins, Domino's refused to participate. They had spent decades building delivery infrastructure. Why hand over that advantage—and customer data—to Silicon Valley startups?

Instead, Domino's accelerated its fortressing strategy, opening stores at an even faster pace to ensure no customer was more than 10 minutes from hot pizza. They introduced "Hotspots"—designated delivery locations at parks, beaches, and other public spaces where traditional delivery was impractical. It has introduced its "hotspots" program, which allows for delivery to nearly 200,000 parks, sports fields and other outdoor locations.

But cracks began to show. Labor shortages hit Domino's particularly hard. Unlike restaurants that could limit hours or reduce service, Domino's promise of fast delivery required full staffing at all times. Wage inflation squeezed franchisee margins. Some stores reduced operating hours—anathema to a brand built on availability.

Russell Weiner took over as CEO in 2022, bringing a different energy to the role. Where Doyle was cerebral and Allison operational, Weiner was a marketer at heart, having served as Domino's Chief Marketing Officer during the turnaround years. His first major move was acknowledging what everyone knew but Domino's had been reluctant to admit: delivery wasn't enough anymore.

The pandemic had accelerated changes in consumer behavior. Carryout, long considered secondary to delivery, was growing faster. Customers who'd grown comfortable with curbside pickup during lockdowns weren't reverting to delivery. Weiner's response was to treat carryout as a growth driver rather than an afterthought, introducing aggressive promotions and even redesigning stores to make pickup more convenient. Technology continued to play a crucial role. Domino's electrified pizza delivery by announcing the rollout of more than 800 custom-branded 2023 Chevy Bolt electric vehicles across select stores in the U.S. – making it the largest electric pizza delivery fleet in the country! The move addressed multiple challenges simultaneously: reducing emissions, cutting delivery costs, and most importantly, attracting drivers who didn't own their own vehicles.

But the current environment presents unprecedented challenges. Competition from DoorDash and Uber Eats has fundamentally changed consumer expectations. Why order from one pizza place when you can browse dozens of restaurants in a single app? Labor shortages continue to pressure operations. Inflation has pushed ingredient costs to record highs, squeezing franchisee margins even as corporate maintains its royalty rates.

The stock market has noticed. After peaking at $538.35 on December 31, 2021, Domino's stock has retreated, trading in the $400s as of 2025. While still representing massive gains from the Doyle era lows, the easy money has been made. The question facing investors now isn't whether Domino's is a good company—it clearly is—but whether it can continue to grow at rates that justify premium valuations.

International expansion remains the brightest spot. With operations in over 90 countries but still underpenetrated relative to McDonald's or KFC, Domino's has decades of growth runway in emerging markets. India continues to boom. China, despite multiple false starts, represents enormous potential. Africa is virtually untapped.

Yet challenges loom. Ghost kitchens—delivery-only operations with no storefront—threaten Domino's fortress model. Aggregators continue to condition consumers to value choice over brand loyalty. And perhaps most concerning, a new generation of consumers has no particular attachment to pizza as the default delivery food.

X. Playbook: Business & Investing Lessons

After studying Domino's transformation, certain lessons emerge that transcend the pizza business entirely. These aren't just observations—they're actionable insights for operators and investors alike.

The Power of Admitting Failure and Radical Transparency

Most companies facing criticism follow a predictable playbook: deny, deflect, or quietly fix problems while hoping nobody notices. Domino's did the opposite. They took their worst reviews and turned them into advertising. This wasn't just clever marketing—it was a fundamental reset of customer expectations. By admitting how bad they were, any improvement would exceed expectations. The lesson: when you're at rock bottom, transparency can be more powerful than spin.

Technology as the Ultimate Differentiator in Commoditized Markets

Pizza is the definition of a commoditized product. The ingredients are identical across competitors. The recipes are hardly secret. Yet Domino's created massive differentiation through technology—not in the product, but in the experience of ordering and receiving it. The Pizza Tracker didn't make pizza taste better, but it made waiting for pizza more enjoyable. The lesson: in commodity markets, win on experience, not product.

Franchise Model Excellence: Aligned Incentives

Domino's franchise model is a masterclass in incentive alignment. Corporate makes money from royalties and supply chain, not from selling franchises. This means corporate only succeeds when franchisees succeed. Compare this to brands that make money upfront from franchise fees—they're incentivized to sell franchises, not ensure their success. The lesson: in any partnership model, ensure your success depends on your partners' success.

The Fortressing Strategy: Density Economics

Conventional wisdom says don't cannibalize your own sales. Domino's proved this wrong by clustering stores densely in the same neighborhoods. The network effects—faster delivery, marketing efficiency, brand dominance—more than offset the cannibalization. The lesson: sometimes the best defense against competition is competing with yourself.

Supply Chain Vertical Integration in QSR

While most franchisors let franchisees source their own supplies, Domino's controls the entire supply chain. This seems restrictive but actually benefits everyone. Franchisees get consistent quality and competitive prices through scale. Corporate gets a second revenue stream and quality control. The lesson: strategic vertical integration can align interests rather than create conflict.

Marketing Genius: From Apology to "Pizza Theater"

Domino's marketing evolution from "30 minutes or free" to "Pizza Turnaround" to "Pizza Tracker" shows masterful brand positioning. Each campaign addressed the company's current challenge while building toward the next phase. The lesson: great marketing doesn't just sell products—it repositions entire companies.

When to Pivot vs. When to Double Down

Domino's shows both sides brilliantly. They pivoted completely on product quality, admitting failure and starting over. But they doubled down on delivery when others were abandoning it for dine-in. The lesson: pivot on weaknesses, double down on structural advantages.

XI. Bull vs. Bear Case Analysis

Bull Case:

The bulls see Domino's as a technology-enabled growth story still in its middle innings. International expansion alone could double the store count over the next decade. With only 20,000 stores globally compared to McDonald's 40,000, the runway is clear. India is adding 200+ stores annually. China remains largely untapped. Africa is virgin territory.

The technology moat continues to widen. While competitors struggle with basic online ordering, Domino's is deploying AI for phone orders and testing autonomous delivery. Each innovation increases customer stickiness and operational efficiency. The fortressing strategy creates local monopolies that are nearly impossible to dislodge.

Unit economics remain best-in-class. New stores generate 30%+ cash-on-cash returns for franchisees. This ensures continued demand for franchises and steady royalty growth for corporate. The capital-light model means growth requires minimal corporate investment.

Inflation actually helps Domino's relative position. While independent pizzerias struggle with volatile cheese costs, Domino's supply chain scale provides stability. Franchisees can maintain margins while independents fail. Market share gains accelerate during tough times.

Bear Case:

The bears see a mature business facing structural headwinds. Third-party delivery platforms have permanently changed consumer behavior. Why order from Domino's when DoorDash offers 100 options? The exclusive delivery advantage that defined Domino's for 60 years has evaporated.

Labor shortages aren't temporary—they're structural. Young workers have better options than delivering pizza. Wage increases are destroying franchisee economics. Some franchisees are already closing stores or reducing hours. The model breaks if franchisees can't make money.

The U.S. market is saturated with 6,500+ stores. Same-store sales growth is slowing. New stores increasingly cannibalize existing ones. The fortressing strategy has reached its limits in major markets.

Commodity price volatility is intensifying. Cheese, wheat, and fuel costs are all rising. Franchisees can't raise prices indefinitely without losing customers. The value perception that drove growth is eroding.

Consumer discretionary spending is under pressure. Pizza delivery is a luxury for many households. In a recession, it's the first thing cut. The COVID bump in delivery demand was artificial and is already reversing.

XII. Final Reflections

Standing back from the numbers and narratives, Domino's transformation represents something profound about American business. This was a company that literally served cardboard-tasting pizza, admitted it publicly, and somehow turned that admission into the foundation of one of the great corporate turnarounds in history.

What would different ownership have meant? If Tom Monaghan had never sold to Bain, would Domino's have achieved its potential? Unlikely. Monaghan was a visionary operator but struggled with the financial engineering needed for public markets. Bain provided the corporate discipline. Doyle provided the transformation vision. Each era built on the previous one's foundation.

The role of crisis in transformation cannot be overstated. Without the 2009 collapse—the viral videos, the plummeting sales, the existential threat—would Domino's have had the courage to reinvent itself so radically? Crisis creates permission for change that success never allows.

For other legacy brands, the lessons are clear but difficult to execute. Admitting failure requires courage most corporate boards lack. Investing in technology requires vision most CEOs don't possess. Cannibalizing existing sales through fortressing requires faith in long-term strategy over quarterly earnings.

The future of QSR and delivery remains uncertain. Will aggregators dominate, reducing restaurants to commodity suppliers? Will ghost kitchens eliminate the need for storefronts? Will autonomous delivery finally arrive at scale? Domino's has navigated every disruption for 60 years by maintaining two simple principles: deliver fast and embrace change.

Perhaps that's the ultimate lesson. In a world of constant disruption, the only sustainable advantage is the ability to adapt. Domino's went from DomiNick's to pizza empire, from cardboard crust to category leader, from restaurant company to technology platform. Each transformation was painful, risky, and ultimately necessary.

The orphan from Jackson who started with $500 and a used pizza oven would barely recognize today's Domino's. But he would understand the driving force behind it: the relentless pursuit of giving customers what they want, when they want it, however they want to order it. That hasn't changed in 60 years. It's unlikely to change in the next 60 either.

For investors, Domino's represents a fascinating study in value creation through operational excellence rather than financial engineering. The spectacular returns weren't generated through multiple expansion alone—they came from fundamentally reimagining what a pizza company could be.

Whether Domino's can continue its remarkable run remains to be seen. The challenges are real, the competition is intensifying, and the easy gains have been captured. But betting against a company that turned "our pizza sucks" into a growth strategy seems unwise. If history is any guide, Domino's will find a way to transform challenge into opportunity once again.

The pizza may no longer taste like cardboard, but the hunger for growth remains just as intense.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube