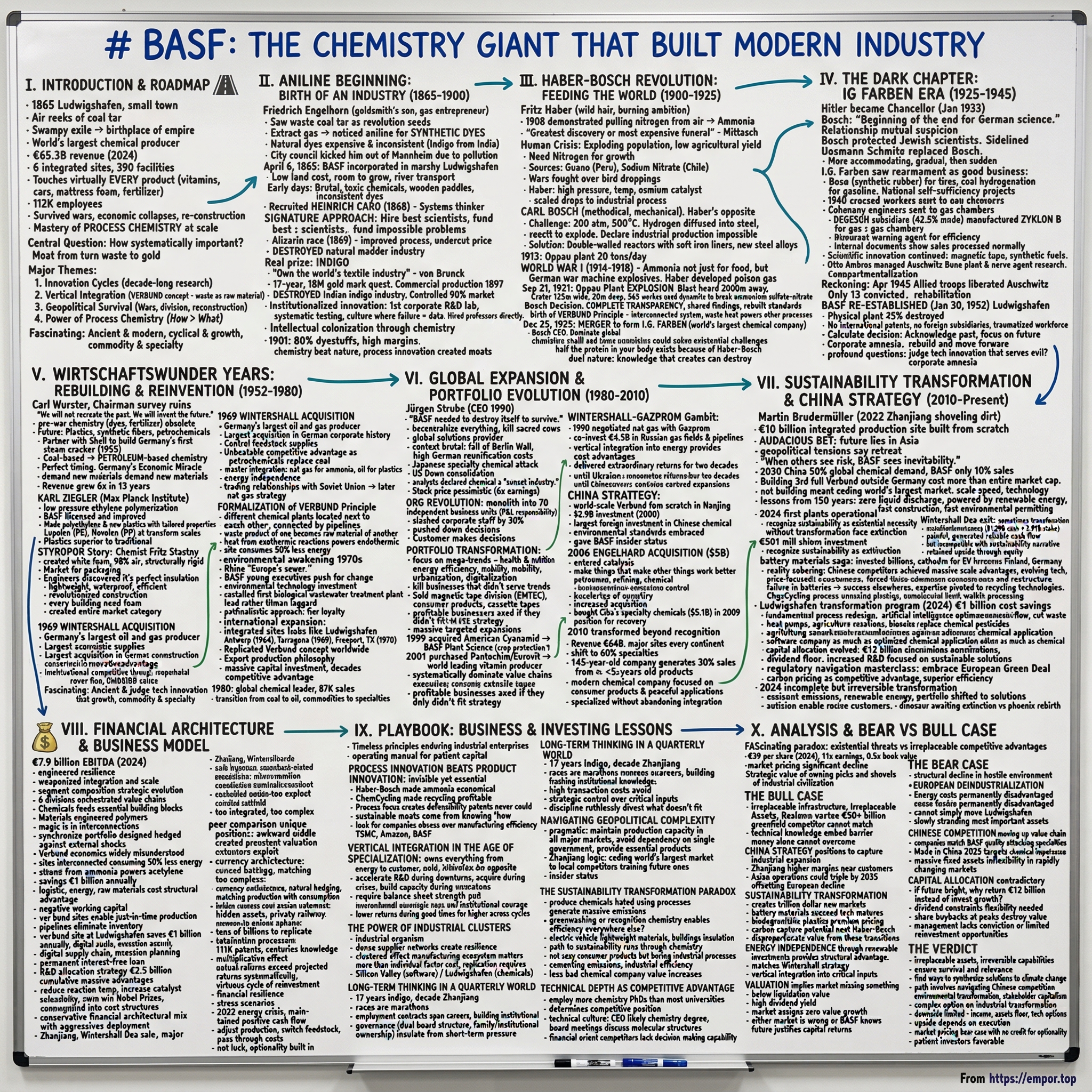

BASF: The Chemistry Giant That Built Modern Industry

I. Introduction & Episode Roadmap

Picture this: It's 1865 in Ludwigshafen, a small town on the west bank of the Rhine. The air reeks of coal tar and industrial fumes. Friedrich Engelhorn, a gas entrepreneur who's been lighting the streets of Mannheim, stands before a patch of marshy land that everyone else has rejected. Across the river, the burghers of Mannheim have just kicked him out—too much pollution, they said. But Engelhorn sees something different in this swampy exile: the birthplace of an empire that would literally create the building blocks of modern civilization.

Today, BASF is the world's largest chemical producer, with €65.3 billion in revenue for 2024, operating six massive integrated production sites and 390 other production facilities across the globe. The company touches virtually every manufactured product on Earth—from the vitamins in your morning supplement to the catalysts in your car, from the foam in your mattress to the fertilizer that grows your food. It employs over 112,000 people and has survived two world wars, multiple economic collapses, radical technological shifts, and the complete destruction and reconstruction of its main facilities—twice.

But here's what's remarkable: While tech companies rise and fall in decades, while entire industries get disrupted overnight, BASF has not just survived but thrived for 159 years by mastering something profoundly unsexy yet absolutely essential—process chemistry at scale. This is the story of how a tar distillery became the foundation of global industry, how chemistry became the ultimate platform business, and how a company can reinvent itself across three centuries while maintaining its core DNA.

The central question we're exploring: How did a dye factory on the Rhine become so systematically important that modern industrial civilization literally cannot function without it? The answer involves assassination attempts, exploding factories, Nobel Prize-winning science, dark chapters of collaboration with evil, and ultimately, the power of turning waste products into gold through sheer intellectual capital and engineering prowess.

We'll trace four major themes throughout this journey. First, the innovation cycles—how BASF repeatedly bet the company on decade-long research projects that others deemed impossible. Second, vertical integration as strategy—the famous "Verbund" concept where the waste of one process becomes the raw material for another, creating unassailable economic moats. Third, geopolitical survival—how a company navigates being on the wrong side of history, literally blown up, divided, and reconstructed. And finally, the power of process chemistry—why knowing how to make something at scale matters more than knowing what to make.

What makes BASF particularly fascinating for investors and business historians is that it's simultaneously ancient and modern, cyclical and growth-oriented, commodity and specialty. It's a company that makes both the most basic industrial chemicals and the most sophisticated battery materials for electric vehicles. It's German to its core yet generates most of its revenue outside Europe. It's environmentally problematic by nature yet positioning itself as essential to solving climate change.

II. The Aniline Beginning: Birth of an Industry (1865–1900)

The year is 1865. The American Civil War has just ended. Japan is emerging from centuries of isolation. And in the German state of Baden, Friedrich Engelhorn is about to make a decision that would reshape global industry. Engelhorn wasn't a chemist—he was a goldsmith's son who'd built a gasworks business lighting the streets of Mannheim. But he understood something profound: the black, sticky coal tar that everyone else saw as waste contained the seeds of a revolution.

Here's the scene that changed everything: Engelhorn had been extracting gas from coal to light Mannheim's streets when he noticed the tar byproduct contained aniline—a chemical that, when processed correctly, could create synthetic dyes. At the time, the textile industry depended entirely on natural dyes: indigo from India, cochineal from Mexico, madder root from Turkey. These were expensive, inconsistent, and controlled by colonial supply chains. Engelhorn saw an opportunity to literally create color from waste.

But Mannheim wanted nothing to do with his stinking factories. The city council, representing the refined burghers of Baden, essentially told him to take his pollution elsewhere. So on April 6, 1865, Engelhorn incorporated Badische Anilin- & Soda-Fabrik—BASF—in Ludwigshafen, a marshy, undeveloped area across the Rhine. The land was cheap precisely because nobody wanted it. This rejection by Mannheim would prove to be a blessing—Ludwigshafen had room to grow, access to river transport, and no established interests to placate.

The early days were brutal. The company started with 30 workers stirring vats of toxic chemicals with wooden paddles, no safety equipment, guided more by intuition than science. The first aniline dyes were inconsistent—batches would come out different colors, fabrics would fade, customers complained. BASF was hemorrhaging money. Engelhorn realized he needed something he didn't have: actual scientific expertise.

Enter Heinrich Caro, recruited in 1868—a move that would transform BASF from a chemical workshop into a research powerhouse. Caro wasn't just a chemist; he was a systems thinker who understood that competitive advantage came not from making dyes, but from making them better, faster, and cheaper than anyone else. Under Caro's leadership, BASF developed what would become its signature approach: hire the best scientists, give them seemingly impossible problems, and fund them until they succeed.

The alizarin story captures this perfectly. In 1869, BASF entered a patent race with William Perkin in England to synthesize alizarin, the red dye from madder root. Both filed patents on the same day—literally hours apart. But here's where BASF's approach diverged from its competitors: instead of fighting over the patent, Caro improved the process, making it so efficient that BASF could undercut everyone else on price. By 1877, the price of alizarin had fallen 90%, destroying the natural madder industry and establishing synthetic chemistry as economically superior to agriculture.

But the real prize was indigo. This blue dye, extracted from plants in India, was the most valuable colorant in the world—the color of royalty, uniforms, and eventually, blue jeans. In 1880, BASF began what would become a 17-year, 18-million-gold-mark quest to synthesize it—a sum that exceeded the company's entire share capital. CEO Heinrich von Brunck famously told researchers: "Gentlemen, if we can make indigo, we own the world's textile industry."

The indigo project nearly broke BASF multiple times. Year after year, researchers would claim breakthroughs only to find their processes impossible to scale. The board revolted. Shareholders demanded the project be killed. But von Brunck persisted, and in 1897, BASF finally began commercial production of synthetic indigo. Within a decade, the Indian indigo industry—which had existed for millennia—was essentially destroyed. By 1913, BASF controlled 90% of the world's indigo market.

What's remarkable about this period is how BASF institutionalized innovation. They created the world's first corporate research laboratory, established systematic testing protocols, and most importantly, developed a culture where failure was seen as data, not disaster. They hired professors directly from universities—unheard of at the time—and gave them industrial-scale resources. By 1900, BASF employed more chemistry PhDs than most universities.

The international expansion strategy was equally systematic. Rather than just export from Germany, BASF established production facilities in Russia (1877), France (1878), and the United States (1880s). They didn't just sell products; they transferred knowledge, creating local technical expertise that would entrench their methods globally. This wasn't just market expansion—it was intellectual colonization through chemistry.

By 1901, 80% of BASF's production was dyestuffs, generating margins that would make today's software companies jealous. But more importantly, they had created something unprecedented: a scalable innovation machine that could take any chemical challenge and systematically solve it through applied research. The pattern was established: identify a natural product that's expensive and supply-constrained, spend whatever it takes to synthesize it, then destroy the natural industry through superior economics.

The foundation was set. BASF had proven that chemistry could beat nature, that process innovation could create moats, and that patient capital deployed against impossible problems could generate extraordinary returns. But dyes were just the beginning. The company was about to tackle something far more ambitious: the very basis of life itself.

III. The Haber-Bosch Revolution: Feeding the World (1900–1925)

The meeting that would save billions of lives—and enable millions of deaths—took place in a Karlsruhe hotel room in 1908. Fritz Haber, a Jewish chemistry professor with wild hair and burning ambition, demonstrated to BASF executives that he could pull nitrogen from thin air and turn it into ammonia. The executives were skeptical. Alwin Mittasch, BASF's research director, allegedly whispered: "This is either the greatest discovery of the century or the most expensive funeral we'll ever attend."

To understand why this mattered, consider the crisis facing humanity in 1900. The world's population was exploding, but agricultural yields were hitting a wall. Crops need nitrogen to grow, but most nitrogen exists as an inert gas in the atmosphere—78% of the air we breathe, yet completely unavailable to plants. The only significant source of agricultural nitrogen was guano from Peru and sodium nitrate from Chile's Atacama Desert. Wars were fought over bird droppings. Germany, in particular, was vulnerable—it imported all its nitrates, which were needed not just for fertilizer but for explosives. The German general staff calculated they had perhaps two years of nitrate supplies in case of war.

Haber had achieved the impossible in his laboratory: using high pressure and temperature with an osmium catalyst, he could combine atmospheric nitrogen with hydrogen to form ammonia—the building block of all nitrogen compounds. But his apparatus produced mere droplets per hour. BASF's challenge was to scale this from laboratory curiosity to industrial process. Enter Carl Bosch, BASF's 35-year-old technical director, whose name would forever be linked with Haber's in what many consider the most important technological development of the 20th century.

Bosch was Haber's opposite—where Haber was theatrical and theoretical, Bosch was methodical and mechanical. His first challenge: Haber's process required pressures of 200 atmospheres at 500°C. Under these conditions, hydrogen would diffuse into steel, making it brittle and causing reactors to explode. British experts declared industrial-scale production impossible. Bosch's solution was elegant: he designed double-walled reactors with soft iron liners that could be replaced, and developed new steel alloys resistant to hydrogen embrittlement. It took four years and countless explosions, but by 1913, BASF's Oppau plant was producing 20 tons of ammonia per day.

The timing was perfect—and terrible. In 1914, World War I erupted. Suddenly, BASF's ammonia synthesis wasn't just about feeding the world; it was about feeding the German war machine. Without Chilean nitrates, Germany should have run out of explosives by 1916. Instead, the Haber-Bosch process allowed Germany to fight for four years. Haber himself would go on to develop poison gas, forever complicating his legacy. The same process that would save billions from starvation enabled millions of deaths.

The war years transformed BASF into something resembling a state within a state. The Oppau plant expanded massively, operating under military protection. Bosch, now in charge of the entire operation, pushed his engineers to impossible extremes. They developed high-pressure compressors that shouldn't have worked, catalysts from rare metals smuggled through neutral countries, and production techniques that violated every safety principle—because the alternative was national defeat.

Then came September 21, 1921—a date seared into BASF's institutional memory. At 7:32 AM, a massive explosion ripped through the Oppau plant. The blast was heard in Munich, 300 kilometers away. Where the warehouse had stood was a crater 125 meters wide and 20 meters deep. 565 people died, 2,000 were injured. The town of Oppau essentially ceased to exist. The cause? Workers had been using dynamite to break up caked ammonium sulfate-nitrate mixture—a practice that had been done 20,000 times before without incident. But that morning, the mixture's composition was slightly different. Chemistry, BASF learned, doesn't forgive complacency.

The Oppau disaster could have ended BASF. The public was horrified, the government launched investigations, competitors circled. But Bosch, now Chairman since 1919, made a remarkable decision: complete transparency. BASF published all its findings, shared safety protocols with competitors, and rebuilt with new standards that would become industry norms. This response—turning disaster into intellectual leadership—would become a BASF pattern.

Under Bosch's leadership from 1919 to 1925, BASF didn't just recover; it redefined what chemical companies could be. While others focused on single products, Bosch saw chemistry as an interconnected system. The ammonia from Haber-Bosch became the starting point for dozens of other chemicals. Waste heat from one process powered another. This was the birth of the Verbund principle—though it wouldn't be formally named until later.

By 1925, BASF faced a strategic crossroads. The German chemical industry was fragmented, competing against growing American giants like DuPont. On December 25, 1925—Christmas Day, deliberately chosen for symbolic rebirth—BASF merged with Hoechst, Bayer, Agfa, and three smaller firms to form I.G. Farben, creating the world's largest chemical company. Bosch became its first CEO. The ambition was breathtaking: to create a chemical conglomerate that could dominate global markets through combined research, shared technology, and massive scale.

The Haber-Bosch process had demonstrated something profound: chemistry could solve humanity's existential challenges. Today, it's estimated that half the protein in your body exists because of Haber-Bosch—without synthetic fertilizer, Earth could support perhaps 3-4 billion people, not 8 billion. But it also showed chemistry's dual nature: the same knowledge that creates can destroy, the same process that feeds can kill. This duality would soon be tested in ways that would forever stain BASF's history.

IV. The Dark Chapter: IG Farben Era (1925–1945)

The boardroom of I.G. Farben's Frankfurt headquarters, January 1933. Carl Bosch, now chairman of the world's most powerful chemical company, receives news that Adolf Hitler has become Chancellor. Bosch, who had Jewish colleagues and opposed the Nazi ideology, reportedly told his board: "This is the beginning of the end for German science." He was both wrong and right—wrong about the immediate impact, catastrophically right about the moral destruction that would follow.

The relationship between I.G. Farben and the Nazi regime began with mutual suspicion. Bosch actively protected Jewish scientists, even meeting Hitler personally in 1934 to argue against their dismissal. Hitler reportedly flew into a rage, and Bosch was gradually sidelined. By 1935, Hermann Schmitz had replaced Bosch as chairman—a man more willing to accommodate the regime. Bosch, increasingly isolated and dependent on alcohol, would die in 1940, spared from seeing the full horror of what his company would become.

The transformation was gradual, then sudden. Initially, I.G. Farben saw the Nazi rearmament as simply good business—synthetic rubber for tires, synthetic fuel for vehicles, chemicals for explosives. The company developed the Buna synthetic rubber process, critical since Germany had no natural rubber access. They perfected coal hydrogenation to create gasoline, making Germany less dependent on imported oil. These were presented as technical achievements, national self-sufficiency projects. The moral complications were rationalized away.

But by 1940, I.G. Farben had crossed lines from which there was no return. The company established Buna-Werke, a synthetic rubber plant at Auschwitz, specifically to utilize slave labor from the concentration camp. This wasn't passive complicity—I.G. Farben actively negotiated with the SS for workers, paid per prisoner per day, and when workers were too exhausted to continue, they were sent to the gas chambers and replaced. Company engineers supervised construction, company managers reviewed productivity reports that casually mentioned deaths.

The most damning evidence: Degesch, a pest control subsidiary in which I.G. Farben held a 42.5% stake, manufactured Zyklon B. Originally developed as a pesticide, it was sold to the SS knowing full well its use in the gas chambers. Internal documents show the company even removed the warning agent that would have caused irritation, making the gas more "efficient" for mass murder. The sales were processed through normal commercial channels, with invoices and receipts—the banality of evil in accounting ledgers.

Yet even during this moral darkness, the scientific innovation continued. I.G. Farben scientists developed magnetic tape (later essential for computing), synthetic fuels that would influence post-war petrochemistry, and polyurethane chemistry that would transform materials science. Otto Ambros simultaneously managed the Auschwitz Buna plant and pioneered nerve agent research. This compartmentalization—brilliant chemistry alongside war crimes—remains one of history's most troubling examples of how technical excellence can be divorced from moral responsibility.

The reckoning came in April 1945. American troops liberated the Auschwitz complex, finding detailed I.G. Farben records. The Frankfurt headquarters was occupied, its 500,000 documents seized. The Allies faced a dilemma: I.G. Farben's knowledge was invaluable for reconstruction and competing with the Soviets, but the company was irredeemably tainted. The solution: destroy the conglomerate but preserve the components.

The Nuremberg I.G. Farben trial of 1947-48 saw 24 executives prosecuted. Only 13 were convicted, with sentences ranging from 18 months to 8 years—shockingly lenient given their crimes. Otto Ambros served just three years before being released and later consulting for American chemical companies. The trial established the principle of corporate criminal responsibility but also revealed how difficult it was to prosecute "desk perpetrators" who never personally pulled triggers.

Allied Control Council Law No. 9 ordered I.G. Farben's dissolution. The company was split into its original components: BASF, Bayer, Hoechst, and several smaller entities. But here's what's remarkable: the Allies needed these companies operational. The Marshall Plan required chemicals for reconstruction. The Cold War demanded German industrial capacity. So while I.G. Farben died, its children were quickly rehabilitated.

BASF was formally re-established on January 30, 1952, in Ludwigshafen. The physical plant was 45% destroyed from Allied bombing. The company had no international patents (all seized), no foreign subsidiaries (all confiscated), and a workforce traumatized by war and morally compromised by collaboration. The first post-war board made a calculated decision: acknowledge the past when legally required, but focus relentlessly on the future. No Truth and Reconciliation Commission, no systematic reckoning—just rebuild and move forward.

This period raises profound questions that echo today. How do we judge technical innovation that serves evil ends? Can institutions be redeemed, or do they carry permanent moral stains? BASF's post-war strategy was essentially corporate amnesia—new management, new structure, new narrative. They would spend the next decades building a different kind of chemical company, one focused on consumer products and peaceful applications. But the I.G. Farben period remains inescapable—a reminder that technological power without ethical constraints leads to catastrophe.

The lessons for modern companies are stark. When technical excellence becomes the only measure of success, when commercial logic overrides moral boundaries, when incremental compromises accumulate into atrocity—that's the I.G. Farben path. Today's tech companies wrestling with surveillance, AI companies building military applications, biotech firms editing genomes—they all face similar choices. The BASF story shows that "we were just following orders" or "we were just selling products" doesn't absolve corporate responsibility.

V. The Wirtschaftswunder Years: Rebuilding & Reinvention (1952–1980)

Carl Wurster stood in the ruins of Ludwigshafen in 1952, BASF's newly appointed chairman, surveying what Allied bombing had left behind. The main factory looked like a skeleton—twisted metal, shattered concrete, entire production blocks simply gone. His first executive decision seemed insane to observers: rather than just rebuild what was destroyed, BASF would build something entirely new. "We will not recreate the past," he declared. "We will invent the future."

This wasn't mere rhetoric. Wurster understood that the pre-war chemical industry—focused on dyes, fertilizers, and basic chemicals—was already obsolete. The future belonged to plastics, synthetic fibers, and petrochemicals. While competitors rebuilt their old plants, BASF used its destruction as an opportunity for complete transformation. They partnered with Shell to build Germany's first steam cracker in 1955, jumping directly from coal-based to petroleum-based chemistry.

The timing was perfect. Germany's Wirtschaftswunder—the economic miracle—was creating insatiable demand for new materials. Cars needed plastics, buildings needed insulation, households wanted synthetic fabrics. BASF's strategic pivot meant they were producing exactly what the reconstruction economy needed. Revenue grew from 814 million DM in 1952 to 4.8 billion DM by 1965—a six-fold increase in thirteen years.

But the real revolution was happening in the research labs. In 1953, Karl Ziegler at the Max Planck Institute discovered catalysts that could polymerize ethylene at low pressure. BASF immediately licensed the technology and improved it. Their chemists discovered that Ziegler's catalysts could make not just polyethylene but entirely new plastics with tailored properties. By 1958, BASF was producing Lupolen (polyethylene) and Novolen (polypropylene) at scales that transformed entire industries. Suddenly, plastics weren't just substitutes for traditional materials—they were superior.

The Styropor story captures this transformation perfectly. In 1951, BASF chemist Fritz Stastny was experimenting with expandable polystyrene when he created a white foam that was 98% air yet structurally rigid. BASF branded it Styropor and initially marketed it for packaging. But engineers discovered it was also perfect insulation—lightweight, waterproof, and incredibly efficient. By 1960, Styropor was revolutionizing construction. Every modern building suddenly needed foam insulation. BASF had created not just a product but an entire market category.

The 1969 Wintershall acquisition marked BASF's coming of age as a global power. Wintershall wasn't a chemical company—it was Germany's largest oil and gas producer, with extensive natural gas reserves and distribution networks. The price tag of 1.4 billion DM made it the largest acquisition in German corporate history. Critics called it insane—why would a chemical company buy an energy company? But BASF's logic was prescient: controlling feedstock supplies would provide unbeatable competitive advantages as petrochemicals replaced coal-based chemistry.

The integration was masterful. Wintershall's natural gas became feedstock for ammonia production. Its oil operations provided raw materials for plastics. Most importantly, it gave BASF something no other chemical company had: energy independence. When the 1973 oil crisis hit, competitors scrambled for supplies while BASF kept running at full capacity. The acquisition also brought an unexpected bonus: Wintershall's trading relationships with the Soviet Union, which would become crucial for BASF's later natural gas strategy.

This period also saw the formalization of BASF's famous Verbund concept. The idea was simple but powerful: locate different chemical plants next to each other, connected by pipelines, where the waste product of one becomes the raw material for another. Heat from exothermic reactions powers endothermic processes. A single infrastructure serves multiple plants. The Ludwigshafen site became the prototype—by 1970, it had over 200 plants interconnected by 2,000 kilometers of pipelines. The efficiency gains were staggering: BASF could produce chemicals at 20-30% lower cost than standalone plants.

The environmental awakening of the 1970s hit BASF particularly hard. The Rhine, which had been BASF's lifeline, was dying—so polluted that journalists called it "Europe's sewer." In 1971, dead fish floating past Ludwigshafen prompted massive protests. BASF's initial response was defensive, arguing that chemicals meant prosperity. But younger executives, led by future CEO Jürgen Strube, pushed for change. BASF began investing heavily in environmental technology—not from altruism but from recognition that environmental opposition could destroy their social license to operate.

By 1975, BASF had installed its first biological wastewater treatment plant, then the world's largest. They developed catalytic converters for cars, sulfur recovery systems for refineries, and CFC-free foam technologies. The environmental investments were expensive—over 1 billion DM through the 1970s—but they positioned BASF as a leader rather than laggard when regulations tightened. More importantly, many environmental technologies became profitable businesses themselves.

The corporate culture during this period was distinctly German yet surprisingly progressive. BASF introduced co-determination in 1976, giving workers half the supervisory board seats—radical for a major corporation. They built entire neighborhoods for employees, with subsidized housing, schools, and cultural centers. The Ludwigshafen site had its own fire department, hospital, and even symphony orchestra. This paternalistic approach created fierce loyalty—multiple generations of families worked for BASF, creating institutional knowledge that competitors couldn't replicate.

The international expansion strategy was methodical. Rather than scattered acquisitions, BASF built integrated sites modeled on Ludwigshafen—Antwerp (1964), Tarragona (1969), and Freeport, Texas (1970). Each replicated the Verbund concept, creating mini-Ludwigshafens worldwide. They didn't just export products; they exported an entire production philosophy. This approach required massive capital investment but created competitive advantages that lasted decades.

By 1980, BASF had transformed from a war-shattered German company into a global chemical leader with 87,000 employees and 20 billion DM in sales. They had successfully navigated the transition from coal to oil, from commodities to specialties, from national to international. But more challenges loomed: globalization was accelerating, Asian competitors were emerging, and the chemical industry was about to undergo its greatest restructuring. The Wirtschaftswunder years had rebuilt BASF, but staying on top would require constant reinvention.

VI. Global Expansion & Portfolio Evolution (1980–2010)

Jürgen Strube entered the BASF boardroom as CEO in May 1990 with a radical proposition that shocked the conservative supervisory board: BASF needed to destroy itself to survive. Not literally, but organizationally. The company had become a bureaucratic behemoth—decisions took months, innovations were smothered by committees, and younger talent was fleeing to American competitors. Strube, an unusual CEO who had started as a lawyer, not a chemist, proposed the unthinkable: decentralize everything, kill sacred cows, and transform BASF from a German chemical company into a global solutions provider.

The context was brutal. The fall of the Berlin Wall had just reunified Germany, bringing massive costs. Japanese competitors were attacking specialty chemicals with superior quality. American companies like DuPont and Dow were consolidating, creating giants with massive R&D budgets. Most threateningly, the entire chemical industry was being declared a "sunset industry" by analysts who saw no growth potential. BASF's stock price reflected this pessimism—trading at just 6 times earnings in 1990.

Strube's first move was organizational revolution. He broke BASF's monolithic structure into 70 independent business units, each with its own P&L responsibility. Sacred headquarters functions were slashed—the corporate staff was cut by 30%. Decision-making was pushed down to operational levels. The old joke that "BASF needs three signatures to buy a pencil" was no longer funny—it was an existential threat. The new mantra: "Those who know the customer make the decisions."

The portfolio transformation was even more radical. Strube identified five mega-trends that would drive chemical demand: health and nutrition, energy efficiency, mobility, urbanization, and digitalization. Everything that didn't serve these trends would be sold or shut down. This meant killing businesses that had defined BASF for decades. The magnetic tape division—once cutting-edge—was sold to EMTEC. The consumer products division, including cassette tapes loved by millions, was divested. Even profitable businesses were axed if they didn't fit the strategy.

But Strube wasn't just shrinking—he was simultaneously executing massive expansions in targeted areas. The 1999 acquisition of American Cyanamid's agricultural products business for $3.8 billion created BASF Plant Science, instantly making BASF a major player in crop protection. The 2001 purchase of Pantochim/Eurovit for €2.15 billion established BASF as the world's leading vitamins producer. These weren't random acquisitions—they were systematic moves to dominate specific value chains.

The Wintershall-Gazprom gambit revealed Strube's geopolitical sophistication. In 1990, as the Soviet Union collapsed, BASF negotiated directly with Gazprom for long-term gas supplies. But Strube went further: BASF would co-invest €4.5 billion in Russian gas fields and pipelines, essentially betting that energy would become a weapon and BASF needed to be on the inside. Critics called it dangerous exposure to Russian political risk. Strube saw it differently: vertical integration into energy would provide cost advantages no competitor could match. For two decades, this strategy delivered extraordinary returns—until Ukraine changed everything.

The China strategy was equally bold but different in execution. Rather than just export to China, BASF decided to build a world-scale Verbund site from scratch. In 2000, they announced a $2.9 billion investment in Nanjing—the largest foreign investment in Chinese chemical history. The negotiations took five years, requiring Strube to personally meet Chinese premiers and navigate Byzantine bureaucracy. The deal terms were unprecedented: BASF would transfer its most advanced technology in exchange for market access and local partnerships.

The Nanjing site, operational by 2005, represented a new model: the "Verbund with Chinese characteristics." It combined BASF's integration concept with Chinese speed and scale. Construction that would take eight years in Germany was completed in three. Environmental standards that would trigger protests in Europe were embraced by Chinese authorities eager for clean technology. Most importantly, it gave BASF insider status in the world's fastest-growing chemical market.

The 2006 Engelhard acquisition for $5 billion marked BASF's entry into catalysis—the business of making things that make other things work better. Engelhard's catalysts were essential for petroleum refining, chemical production, and especially automotive emissions control. This wasn't just buying products; it was buying the knowledge of how to speed up chemical reactions. As environmental regulations tightened globally, catalyst technology became increasingly valuable. The acquisition would pay for itself within five years.

The financial crisis of 2008-2009 tested everything Strube and his successor Jürgen Hambrecht had built. Chemical demand collapsed 20% in six months. BASF's stock price halved. The company faced its worst crisis since World War II. But the decentralized structure Strube had created proved its worth: business units could react instantly to local conditions. The Verbund sites provided cost advantages that kept BASF profitable even as competitors posted losses. Most importantly, BASF had the balance sheet strength to keep investing while others retreated.

The response to the crisis revealed BASF's evolution. Instead of mass layoffs (the American approach) or government bailouts (the banking approach), BASF implemented "Kurzarbeit"—reduced working hours with government wage support. They accelerated R&D spending, reasoning that downturns were the best time to develop next-generation products. They even increased acquisition activity, buying Ciba's specialty chemicals business for $5.1 billion in 2009 when nobody else had capital. This countercyclical strategy would position BASF perfectly for the recovery.

By 2010, BASF had transformed beyond recognition from its 1980 incarnation. Revenue had grown from 30 billion DM to €64 billion. The company operated major sites on every continent. The portfolio had shifted from 70% commodities to 60% specialties. Most remarkably, despite being a 145-year-old company, BASF was generating 30% of sales from products less than five years old. The transformation wasn't complete—it never would be—but BASF had proven that even industrial giants could reinvent themselves.

The Strube-Hambrecht era (1990-2011) would be remembered as BASF's great modernization. They had globalized without losing German roots, specialized without abandoning integration, and grown without losing financial discipline. But new challenges were emerging: climate change was redefining the chemical industry's social license, China was becoming a competitor not just a customer, and digitalization was threatening traditional business models. The next transformation would be even more fundamental: from chemical company to sustainability solutions provider.

VII. The Sustainability Transformation & China Strategy (2010–Present)

Martin Brudermüller stood before 500 Chinese officials in Zhanjiang, Guangdong Province, in November 2022, shoveling ceremonial dirt for BASF's most audacious bet ever: a €10 billion integrated production site built entirely from scratch. Behind him, the South China Sea stretched to the horizon. This wasn't just another chemical plant—it was BASF's declaration that its future lay in Asia, even as geopolitical tensions suggested every reason to retreat. "When others see risk," Brudermüller told the assembled dignitaries, "BASF sees inevitability."

The Zhanjiang decision had been years in the making, starting under Brudermüller's predecessor Kurt Bock in 2017. The logic was compelling yet controversial: by 2030, China would represent 50% of global chemical demand but BASF generated only 10% of sales there. Building a full Verbund site—only the third outside Germany—would cost more than BASF's entire market cap in some years. But not building it meant ceding the world's largest market to local competitors who were rapidly climbing the technology curve.

What made Zhanjiang remarkable wasn't just its scale but its speed and technology. The site incorporated every lesson from 150 years of chemical production: zero liquid discharge, powered partially by renewable energy, and digitally integrated from day one. Construction that would take 10 years in Europe was scheduled for 5 years in China. Environmental permitting that would trigger decades of lawsuits in Germany was approved in months. By 2024, the first plants were operational—on time and on budget, a rarity in mega-projects.

But Zhanjiang represented something deeper: BASF's recognition that sustainability wasn't optional greenwashing but existential necessity. The chemical industry produces 7% of global greenhouse gas emissions. Without dramatic transformation, BASF faced extinction through regulation, stranded assets, or social rejection. Brudermüller's response was typically BASF—massive, systematic, and rooted in process innovation rather than promises.

The €501 million investment in Vattenfall's Hollandse Kust Zuid wind farm in 2024 exemplified this approach. BASF didn't just buy renewable energy credits like most companies—they bought 49.5% of the wind farm itself, securing 300 megawatts of dedicated capacity. This wasn't philanthropy; it was vertical integration into energy, the same strategy that had driven the Wintershall acquisition 50 years earlier. By controlling their renewable energy sources, BASF could guarantee green electricity for chemical production while hedging against carbon prices.

The Wintershall Dea exit told the opposite story—sometimes transformation means abandoning successful businesses. In 2024, BASF sold its oil and gas subsidiary to Harbour Energy for $1.29 billion cash plus a 39.6% stake in the combined entity. This was painful; Wintershall Dea generated reliable cash flows that subsidized chemical R&D. But owning fossil fuel assets had become incompatible with BASF's sustainability narrative. The elegance was in the structure: BASF got immediate cash while retaining upside through equity, essentially having their cake and eating it too.

The battery materials saga revealed the complexity of sustainability transformations. BASF had invested billions in cathode active materials for electric vehicle batteries, building plants in Finland, Germany, and planning others globally. The logic seemed impeccable: EVs would explode, batteries would be the bottleneck, and whoever controlled cathode materials would print money. By 2024, the reality was sobering—Chinese competitors had achieved massive scale advantages, battery chemistry was evolving rapidly, and automotive customers were brutally price-focused. BASF was forced to write down investments and restructure the entire division.

Yet failure in batteries led to success elsewhere. The same expertise in materials science pivoted to recycling technologies. BASF's ChemCycling process could break down plastic waste into original molecules, creating virgin-quality materials from garbage. This wasn't mechanical recycling (melting and reshaping) but chemical recycling—literally unmaking plastics at the molecular level. By 2024, BASF was processing 60,000 tons of plastic waste annually, with plans to scale to 1 million tons by 2030.

The Ludwigshafen transformation program announced in 2024—€1 billion in cost savings by 2026—seemed like typical corporate cost-cutting until you examined the details. This wasn't about firing workers or closing plants but about fundamental process redesign. Using artificial intelligence to optimize chemical reactions, reducing energy consumption by 30%. Replacing batch processes with continuous flow, cutting waste by 90%. Installing heat pumps to capture and reuse waste heat. The program would eliminate 2,800 jobs but create 2,000 new ones in digital and sustainability roles—transformation, not just reduction.

The agricultural solutions division showcased how sustainability could drive growth, not just cost. As climate change disrupted farming, crops needed new traits—drought resistance, heat tolerance, nitrogen efficiency. BASF's biosolutions replaced chemical pesticides with biological alternatives. Their digital farming platform, xarvio, used satellite imaging and AI to optimize chemical application, reducing usage by 20% while improving yields. By 2024, digital farming services had 7 million users covering 90 million hectares—BASF as much a software company as a chemical producer.

The capital allocation philosophy had evolved remarkably. The 2024 announcement of €12 billion in shareholder distributions from 2025-2028 seemed to contradict the massive investments in sustainability. But Brudermüller's logic was sophisticated: BASF needed to fund transformation while maintaining investor support. The €2.25 per share dividend provided stability for institutional investors while share buybacks created flexibility. Meanwhile, R&D spending increased to €2.5 billion annually, focused overwhelmingly on sustainable solutions.

The regulatory navigation was masterclass-level. The European Green Deal threatened to destroy European chemical production through carbon prices and environmental restrictions. Rather than fight it, BASF embraced it—publicly supporting carbon pricing while quietly ensuring their superior efficiency would create competitive advantages. When competitors complained about regulations, BASF was already compliant and selling them the technology to catch up.

By 2024, BASF's transformation was incomplete but irreversible. Carbon emissions had decreased 35% from 2018 levels despite production growth. Renewable energy powered 20% of global operations. The product portfolio had shifted toward solutions that enabled customers' sustainability—lightweight materials for vehicles, insulation for buildings, biodegradable plastics. The company that had once symbolized industrial pollution was positioning itself as essential to solving climate change.

But contradictions remained. BASF still produced massive amounts of basic chemicals using fossil feedstocks. The Zhanjiang investment was in China, increasingly seen as a strategic rival by Western governments. The sustainability investments hadn't yet generated returns justifying their costs. Critics argued BASF was simply greenwashing while continuing business as usual. Supporters countered that transformation at this scale took decades, not quarters.

VIII. Financial Architecture & Business Model

The numbers tell a story of engineered resilience: €7.9 billion EBITDA before special items in 2024, up 2% despite wars, inflation, and energy crises that should have destroyed a European chemical producer. But drill deeper into BASF's financial architecture and you discover something more sophisticated—a company that has weaponized integration and scale into a economic moat that grows stronger during turbulence. This isn't financial engineering; it's industrial engineering expressed through numbers.

Start with the segment composition, which reveals BASF's strategic evolution. The six divisions aren't random collections of businesses but carefully orchestrated value chains. Chemicals (€8.1 billion sales, €320 million EBITDA) appears to be a low-margin commodity business until you realize it feeds every other division with essential building blocks at transfer prices that create group-wide advantages. Materials (€10.8 billion sales, €835 million EBITDA) seems like cyclical plastics until you understand these aren't commodities but specifically engineered polymers for automotive and construction that command premium pricing.

The magic happens in the interconnections. When oil prices spike, the Chemicals division suffers but Materials benefits from inventory gains. When automotive production slumps, Industrial Solutions pivots to construction. When European energy costs explode, Asian operations compensate. This isn't diversification—it's synchronization, where the portfolio is designed to be naturally hedged against external shocks.

The Verbund economics deserve special attention because they're widely misunderstood. At Ludwigshafen alone, BASF operates 200 plants so interconnected that the site consumes 50% less energy and produces 50% less waste than if plants operated independently. The steam from ammonia production powers the acetylene plant. The hydrogen byproduct from chlorine production feeds hydrogenation reactions. The carbon dioxide from ethylene oxide becomes feedstock for carbonates. This integration saves €1 billion annually in logistics, energy, and raw materials—a structural advantage no financial engineering could replicate.

Consider the working capital dynamics, which seem boring until you understand their elegance. BASF runs with negative working capital in many businesses—customers pay before suppliers are paid. This isn't just good management; it's architectural. The Verbund sites enable just-in-time production because feedstocks move directly from one plant to another through pipelines, eliminating inventory. Digital supply chain management predicts demand weeks in advance, allowing precise production planning. The result: €2 billion less capital tied up in operations, effectively a permanent interest-free loan from the business.

The R&D allocation strategy—€2.5 billion annually, 3.8% of sales—appears standard for a chemical company until you examine where it goes. 80% funds incremental process improvements that individually seem trivial but cumulatively create massive advantages. Reducing reaction temperature by 10°C saves millions in energy. Increasing catalyst selectivity by 2% eliminates entire purification steps. These aren't breakthroughs that win Nobel Prizes but they compound into cost structures competitors can't match.

The capital allocation philosophy reflects German conservatism mixed with opportunistic aggression. BASF maintains investment-grade credit ratings (A2/A) religiously, viewing financial flexibility as strategic capability. But when opportunities arise—financial crises, competitor distress, technological discontinuities—BASF deploys capital with shocking speed. The €10 billion Zhanjiang investment during U.S.-China tensions, the Wintershall Dea sale at peak energy prices, the battery materials pivot when others retreated—these aren't random bets but calculated applications of patient capital.

The dividend policy—€2.25 per share minimum through 2028—seems generous until you realize it's strategic communication. BASF's shareholder base includes German pension funds, sovereign wealth funds, and index trackers who prize stability over growth. The dividend commitment signals confidence without constraining flexibility—notice it's a floor, not a ceiling. Meanwhile, the €4 billion share buyback program provides adjustment mechanism for excess cash without creating future obligations.

Peer comparison reveals BASF's unique position. DuPont (0.7x sales) trades at premium valuations for its specialty focus but lacks BASF's integration advantages. Dow Chemical matches BASF's scale but remains U.S.-centric, missing Asian growth. Chinese competitors like Wanhua Chemical grow faster but lack technological depth. BASF occupies an awkward middle—too integrated for pure-play investors, too complex for simple analysis—which creates persistent valuation discounts that patient investors can exploit.

The currency architecture is particularly sophisticated. With 60% of sales outside the eurozone but most costs in euros, BASF faces massive translation exposure. Their solution isn't financial hedging but operational hedging—matching production with consumption geographically. The Zhanjiang site serves Asian customers with local production. The Freeport site supplies American markets with dollar costs. This natural hedging means currency fluctuations affect translation but not competitive position.

The hidden assets are worth examining. BASF owns one of the world's largest private railway networks (1,100 railcars), operates its own power plants (2,000 MW capacity), and controls critical pipeline infrastructure. These aren't on the balance sheet at replacement value but would cost tens of billions to replicate. The intellectual property portfolio—111,000 patents and applications—represents centuries of accumulated knowledge. The customer relationships, many dating back decades, create switching costs that transcend price competition.

The capital intensity—€4.5 billion annual capex—seems problematic until you understand the returns. BASF targets 20% IRR on growth investments, 15% on maintenance. But the real return comes from the network effects of integration. A new plant at Ludwigshafen doesn't just generate its own returns but improves economics of connected plants. This multiplicative effect means actual returns exceed projected returns systematically, creating a virtuous cycle of reinvestment.

The financial resilience shows in stress scenarios. During 2009's financial crisis, BASF remained profitable while competitors posted losses. During 2022's energy crisis, when European gas prices increased 10x, BASF maintained positive cash flow by instantly adjusting production, switching feedstocks, and passing through costs. This isn't luck—it's optionality built into the business model, where multiple paths to profitability exist regardless of external conditions.

IX. Playbook: Business & Investing Lessons

The BASF story, stripped of its chemical complexity, reveals timeless principles about building enduring industrial enterprises. These aren't MBA frameworks or consultant theories but hard-won insights from 159 years of navigating technological disruption, geopolitical catastrophe, and market cycles that destroyed countless competitors. Think of this as the operating manual for patient capital in cyclical industries.

Process Innovation Beats Product Innovation

Everyone remembers the iPhone; nobody knows who makes the gorilla glass. BASF embodies this paradox at massive scale—invisible yet essential. Their greatest innovations aren't new molecules but new ways to make existing molecules. The Haber-Bosch process didn't invent ammonia; it made ammonia economical. The ChemCycling process doesn't create new plastics; it makes plastic recycling profitable. This focus on process over product creates defensibility that patents alone never could. Competitors can copy your products, but they can't copy decades of accumulated process knowledge embedded in equipment, personnel, and culture.

The investing insight: look for companies that obsess over manufacturing efficiency rather than just R&D headlines. The sustainable moats come from knowing how to do something, not just what to do. TSMC understands this. Amazon's logistics network embodies it. BASF has institutionalized it.

Vertical Integration in the Age of Specialization

Modern business theory preaches focus, outsourcing, and asset-light models. BASF does the opposite—owning everything from energy supplies to customer technical centers. This seems anachronistic until you understand the economics. In stable industries, specialization wins through efficiency. In volatile industries with complex interdependencies, integration wins through resilience and optimization. Chemical production involves such extreme conditions—temperatures, pressures, toxicities—that transaction costs between independent entities would be prohibitive.

But BASF's integration isn't mindless empire-building. Each integration decision follows clear logic: Does this create network effects with existing operations? Can we manage this better than specialists? Will this provide strategic control over critical inputs? The Wintershall acquisition made sense; consumer products didn't. The discipline to integrate strategically while divesting ruthlessly is rare.

Managing Cyclicality: The Countercyclical Paradox

Chemical markets are violently cyclical—demand swings 20%, prices swing 50%, profits swing 200%. Most companies respond pro-cyclically: investing at peaks when cash is plentiful, cutting at troughs when cash is scarce. BASF does the opposite systematically. They accelerate R&D during downturns when technical talent is available. They acquire during crises when assets are cheap. They build capacity during recessions when construction costs are low.

This requires two things most companies lack: balance sheet strength to survive troughs and institutional courage to invest when everything looks terrible. BASF maintains higher cash reserves than optimal during booms specifically to deploy during busts. They accept lower returns during good times to achieve higher returns across cycles. This patient capital approach only works with aligned shareholders who understand the strategy.

The Power of Industrial Clusters

Ludwigshafen isn't just a production site; it's an industrial organism. With 39,000 employees, 2,000 kilometers of pipelines, and 200 interconnected plants, it has evolved emergent properties that transcend planning. Knowledge spillovers between adjacent operations accelerate innovation. Shared infrastructure reduces costs below standalone economics. Dense supplier networks create resilience against disruptions.

This clustering effect explains why manufacturing doesn't simply move to lowest-cost locations. The ecosystem matters more than individual factor costs. BASF's attempt to replicate Ludwigshafen in China acknowledges this—you can't just build plants, you must cultivate ecosystems. Silicon Valley understands this for software; Ludwigshafen demonstrates it for chemicals.

Long-term Thinking in a Quarterly World

BASF spent 17 years and 18 million gold marks developing synthetic indigo. They're spending a decade and €10 billion building Zhanjiang. These timeframes seem insane in an era of quarterly earnings calls and activist investors. But they reflect a fundamental truth about industrial competition: the important races are marathons, not sprints.

This long-term orientation manifests everywhere. Employment contracts that span careers, creating institutional knowledge. Customer relationships maintained through cycles, building trust that transcends transactions. Technology development that anticipates regulations years before they're enacted. This patient approach only works with appropriate governance—BASF's dual board structure and significant family/institutional ownership insulate management from short-term pressure.

Navigating Geopolitical Complexity

BASF has survived two world wars, operated through the Cold War, and now navigates US-China tensions. Their approach isn't ideological but pragmatic: maintain production capacity in all major markets, avoid dependency on any single government, and provide such essential products that political actors need you regardless of tensions.

The Zhanjiang investment during rising China tensions seems risky, but consider the alternative: ceding the world's largest chemical market to local competitors who will eventually challenge you globally. By building in China with Chinese partners, BASF gains insider status that pure exporters never achieve. Similarly, maintaining U.S. operations despite European headquarters provides optionality regardless of Atlantic relations.

The Sustainability Transformation Paradox

BASF produces chemicals that environmentalists hate using processes that generate massive emissions. Yet they're positioning as essential to solving climate change. This isn't greenwashing but recognition that chemistry enables efficiency everywhere else. Electric vehicles need lightweight materials. Buildings need insulation. Renewable energy needs storage. The path to sustainability runs through chemistry, not around it.

The investment implication: the most important climate technologies won't be sexy consumer products but boring industrial processes. Companies that reduce cement emissions, improve industrial efficiency, or enable circular economies will generate enormous value. BASF's bet is that being the least bad chemical company becomes enormously valuable as regulations tighten.

Technical Depth as Competitive Advantage

BASF employs more chemistry PhDs than most universities. This seems excessive until you understand that in process industries, technical depth determines competitive position. The ability to solve customer problems, optimize reactions, and develop new catalysts requires knowledge that can't be outsourced or automated. This technical culture—where the CEO likely has a chemistry degree and board meetings discuss molecular structures—creates decision-making capability that financially oriented competitors lack.

X. Analysis & Bear vs. Bull Case

The investment case for BASF presents a fascinating paradox: a company simultaneously facing existential threats and possessing irreplaceable competitive advantages. At €39 per share in late 2024, trading at 11x earnings and 0.5x book value, the market is pricing in significant decline. But this pessimism may be overlooking the strategic value of owning the picks and shovels of industrial civilization.

The Bull Case: Irreplaceable Infrastructure for Global Growth

BASF's bull case rests on a simple observation: modern civilization literally cannot function without chemicals, and BASF has spent 159 years building advantages that would take decades and hundreds of billions to replicate. The Verbund sites alone represent €50+ billion in replacement value, engineered with integration that no greenfield competitor could match. The technical knowledge embedded in 111,000 patents and three generations of chemical engineers creates a barrier that money alone cannot overcome.

The China strategy, while risky, positions BASF to capture the most significant industrial expansion in history. By 2030, China will represent 50% of global chemical demand. The Zhanjiang site, operational by 2030, will generate €10 billion in annual revenue at higher margins than European operations due to lower energy costs and proximity to customers. If China grows at just 5% annually, BASF's Asian operations could triple by 2035, more than offsetting European decline.

The sustainability transformation creates new markets worth trillions. Battery materials for EVs, despite current struggles, will eventually succeed as technology matures and scale economics emerge. Biodegradable plastics will capture premium pricing as regulations ban conventional plastics. Carbon capture technologies, still nascent, could become BASF's next Haber-Bosch—a process innovation that defines an industry. The company investing €2.5 billion annually in R&D will capture disproportionate value from these transitions.

Energy independence through renewable investments provides structural advantages as carbon prices rise. The Hollandse Kust wind farm and similar projects will provide BASF with green electricity at stable prices while competitors face volatile spot markets. By 2030, BASF targets 60% renewable energy, creating a 20% cost advantage in energy-intensive processes. This mirrors the Wintershall strategy—vertical integration into critical inputs.

The valuation implies the market is missing something fundamental. At 0.5x book value, BASF trades below liquidation value. The dividend yield of 7.8% exceeds corporate bond yields, implying the market expects cuts that management explicitly denies. The free cash flow yield of 12% suggests the market assigns zero value to growth. Either the market is wrong, or BASF knows something about its future that justifies capital returns over growth investment.

The Bear Case: Structural Decline in a Hostile Environment

The bear case starts with European deindustrialization. Energy costs in Europe are structurally 3-4x higher than the U.S. or China post-Ukraine war. Chemical production is energy-intensive, making European operations permanently disadvantaged. BASF can't simply move Ludwigshafen—the site represents centuries of accumulated infrastructure and knowledge. As European chemical production declines, BASF faces the slow-motion stranding of its most important assets.

Chinese competition is moving up the value chain faster than expected. Companies like Wanhua Chemical have matched BASF's quality in commodity chemicals and are attacking specialties. The Chinese government's "Made in China 2025" explicitly targets chemical independence. BASF's Zhanjiang investment might be training future competitors, similar to how Western technology transfers created today's Chinese manufacturing dominance. Within a decade, BASF could face Chinese competitors with similar technology but lower costs.

Environmental liabilities could prove catastrophic. BASF operates on land contaminated by 159 years of chemical production. Cleanup costs, while provisioned, could explode as regulations tighten. The company faces thousands of lawsuits over PFAS "forever chemicals" that could mirror asbestos or tobacco litigation. Climate regulations could impose carbon costs that destroy profitability. The social license to operate is eroding as younger generations view chemicals as inherently harmful.

The business model may be obsolete. The Verbund concept assumes stable, large-scale production, but customers increasingly want flexibility and customization. Digital natives are disrupting distribution with platforms that disintermediate producers. Biotechnology could replace chemical synthesis for many products. The massive fixed assets that once provided advantages now create inflexibility in rapidly changing markets.

Management's capital allocation seems contradictory. If the future is so bright, why return €12 billion to shareholders instead of investing in growth? The dividend commitment constrains flexibility precisely when maximum agility is needed. The share buybacks at cyclical peaks destroy value. Either management lacks conviction in their strategy or they see limited reinvestment opportunities—both bearish signals.

The Verdict: Valuable but Vulnerable

The truth lies between extremes. BASF possesses irreplaceable assets and capabilities that ensure its survival and relevance. The company that synthesized indigo and ammonia will find ways to synthesize solutions to climate change. But the path forward involves navigating between Scylla and Charybdis—Chinese competition and European decline, environmental transformation and industrial necessity, stakeholder capitalism and shareholder returns.

For investors, BASF represents a complex option on industrial transformation. The downside seems limited—the dividend provides income, the assets provide floor value, the technology provides strategic options. The upside depends on execution—whether management can navigate geopolitical complexity, whether sustainability investments generate returns, whether Chinese expansion offsets European decline.

At current valuations, the market is pricing in the bear case with no credit for optionality. For patient investors who believe in industrial civilization's continued need for chemicals and BASF's ability to evolve, the risk-reward appears favorable. For those who see structural decline and stranded assets, even these low valuations may prove excessive.

XI. Epilogue: The Next 150 Years

Standing in BASF's archive in Ludwigshafen, you can hold Friedrich Engelhorn's original 1865 incorporation documents—handwritten in elaborate German script, sealed with wax, imagining a joint-stock company for aniline production. Engelhorn couldn't have imagined that his tar distillery would feed the world through synthetic fertilizer, or that his dye works would enable everything from plastics to pharmaceuticals. The question facing BASF today is equally profound: What transformations lie ahead that we cannot yet imagine?

The immediate future is knowable, even if challenging. By 2030, BASF will complete its largest transformation since post-war reconstruction. Zhanjiang will be fully operational, generating 25% of group revenue. European operations will be radically restructured—smaller, specialized, and sustainable. The portfolio will shift further toward solutions that enable rather than supply—selling knowledge, not just molecules. Carbon neutrality, targeted for 2050, will require technologies that don't yet exist at scale.

But the real future lies in convergences we're just beginning to glimpse. Artificial intelligence is revolutionizing molecular discovery—what took decades of trial and error now takes months of simulation. BASF's quantum computing partnerships with IBM and others could crack problems like room-temperature superconductivity or efficient nitrogen fixation without fossil fuels. Synthetic biology could enable production of complex molecules using engineered organisms instead of chemical reactors. The company that mastered synthetic chemistry must now master synthetic biology or be displaced by it.

Climate technology represents the most obvious opportunity. Direct air capture of CO2, still economically impossible, could become BASF's next ammonia synthesis—a process that seems impossible until someone cracks it. Chemical recycling could eliminate the concept of waste, creating circular economies where BASF doesn't sell products but leases molecules, taking them back for reprocessing infinitely. Energy storage beyond batteries—synthetic fuels, chemical heat storage, innovative materials—could solve renewable energy's intermittency problem.

The geopolitical realignment will force fundamental choices. A world dividing into technological blocs—American, Chinese, European—challenges BASF's universal presence. They may need to split into regional entities with firewalls between them, sacrificing integration for access. Or they might become truly supranational, incorporated nowhere and everywhere, a chemical cloud floating above nation-states. The company that survived two world wars must now navigate a new cold war fought through technology and trade.

The ownership and governance evolution could be equally dramatic. BASF's current structure—public company with dispersed ownership—may prove inadequate for long-term transformation. We might see sovereign wealth funds take major stakes, providing patient capital for decade-long investments. Chinese partners might demand deeper integration. Climate activists might gain board seats. The company might even split into "GoodChem" (sustainable solutions) and "BadChem" (necessary but problematic products), allowing different investor bases for different futures.

Ultimately, BASF's next 150 years depend on solving a fundamental contradiction: How do you grow a chemical company in a world that needs fewer chemicals? The answer lies not in producing more but enabling more—chemicals that make solar panels 50% more efficient, materials that make buildings carbon-negative, catalysts that turn waste into resources. BASF must transform from a company that makes things into a company that makes things possible.

The historical parallel is instructive. In 1865, BASF began by replacing natural dyes with synthetic ones—seemingly a niche market that became foundation for entire industries. Today, BASF must replace unsustainable processes with sustainable ones—a transformation that could be equally foundational. The company that fed the world with synthetic fertilizer might now save it with synthetic solutions to climate change.

For investors and observers, BASF represents something larger than a chemical company. It's a test case for whether industrial giants can evolve, whether 159-year-old companies can be reborn, whether the creators of problems can become sources of solutions. The pessimists see a dinosaur awaiting extinction. The optimists see a phoenix preparing for rebirth. The truth, as always with BASF, lies in the chemistry—the careful combination of elements that separately seem inert but together catalyze transformation.

The story that began with Friedrich Engelhorn standing in the marshes of Ludwigshafen continues with Martin Brudermüller standing in the wetlands of Zhanjiang. Both men faced the same question: How do you build something that lasts beyond any individual, any government, any era? The answer BASF has discovered—through war and peace, boom and bust, triumph and tragedy—is deceptively simple: You create value so fundamental that civilization cannot function without you. You embed yourself so deeply in the fabric of industry that removing you would unravel everything else.

Whether BASF survives another 150 years depends on whether they can pull off one more transformation—from the chemistry of things to the chemistry of solutions. The tar distillery that became a global giant must now become something else entirely: a sustainable innovation engine for a resource-constrained world. The odds are long, the challenges immense, but then again, BASF has always specialized in making the impossible merely difficult, and the difficult routine.

The next chapter in BASF's story won't be written in Ludwigshafen or Zhanjiang but in laboratories where scientists are creating materials that don't yet have names, solving problems we don't yet know we have, enabling futures we cannot yet imagine. The company that began with aniline will end—if it ever ends—with something we cannot pronounce, do not understand, but cannot live without.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube