Doximity: The LinkedIn for Doctors That Defied Silicon Valley

I. Introduction & Episode Roadmap

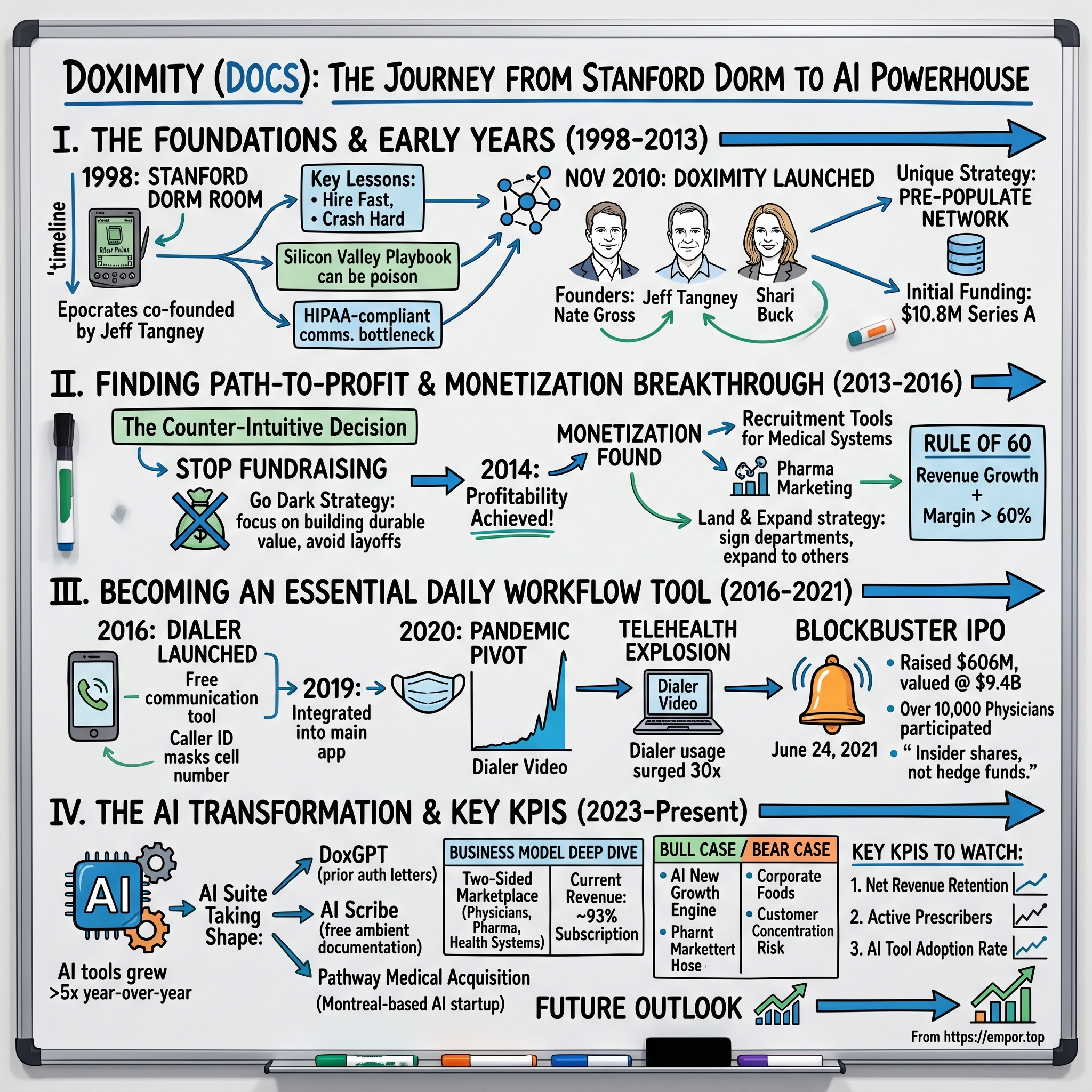

The screens at the New York Stock Exchange flickered with anticipation on June 24, 2021, as Jeff Tangney rang the opening bell. Within hours, Doximity's stock had more than doubled—the kind of first-day pop that makes venture capitalists reach for champagne. But what made this celebration different was who was actually popping the corks: over 10,000 physicians had bought shares at the IPO price, and by the closing bell, their $91 million investment had swelled to $185 million.

This wasn't just another tech IPO. The stock closed at $53, giving the company a market cap of $9.4 billion. It was vindication for a company that had spent seven years in deliberate obscurity, growing quietly while Silicon Valley preached growth-at-all-costs mantras that Doximity's founder found dangerous.

The central question this story answers: How did a company that deliberately ignored Silicon Valley's playbook become a $10 billion healthcare juggernaut?

Doximity closed fiscal year 2025 with $570.4 million in revenue and 20% annual revenue growth, posting a 50% EBITDA margin—rare profitability in health tech, where many companies trade growth for endless cash burns. The company's network members include over 80% of U.S. doctors and 50% of all nurse practitioners and physician assistants as verified members.

The Doximity story weaves together several threads that define the modern tech landscape: capital efficiency versus growth-at-all-costs, network effects in regulated industries, the "physician-first" philosophy in healthcare tech, and now, the AI transformation. Its AI tools grew more than fivefold year over year.

What follows is the story of a founder who learned the hard way that Silicon Valley's conventional wisdom could be poison, a founding team that bootstrapped in a workspace above a garage, and a company that quietly built the largest professional network in medicine—then bet everything on artificial intelligence.

II. The Founder's Origin Story: From Stanford Dorm Room to Epocrates

The Pre-History That Made Doximity Possible

In the late 1990s, Jeff Tangney was living in an un-air-conditioned New York apartment with a trained physician named Richard Fiedotin. The Palm Pilot had just hit the market—a chunky, stylus-driven device that would seem laughably primitive today but represented the cutting edge of mobile computing at the turn of the millennium.

In his Stanford dorm room, in the late '90s, Tangney had two physician roommates and together they built Epocrates, a Palm Pilot app for checking drug doses and interactions. "They wrote Latin (drug doses), and I wrote the database."

Tangney's journey started while he was living in New York with Fiedotin. From their un-air-conditioned apartment, the pair came up with the idea of creating an app for the Palm Pilot. Tangney and Fiedotin took that idea with them to Stanford Graduate School of Business, where they met another physician named Tom Lee. The three bonded over the intersection of tech and health care while on a teambuilding climbing trip for students in the program.

Tangney graduated summa cum laude from the Concordia University of Wisconsin with a B.S. in Economics and earned an M.B.A. from Stanford University's Graduate School of Business. Less widely known: Tangney was twice the Wisconsin State high school math champion.

In 1998, they started what became Epocrates, and over the next two years raised about $40 million from some of Silicon Valley's top health investors. As mobile moved to BlackBerry devices and then to iPhones, Epocrates gained traction as a way for doctors to make decisions about prescriptions and patient safety while on the move.

The app became a sensation among physicians. At a time when drug information lived in thick reference books, Epocrates put critical safety data in a doctor's pocket. The app let physicians check for dangerous drug interactions in seconds rather than minutes—a potentially life-saving innovation in emergency situations.

Then came the moment that would shape everything Tangney did next with Doximity. The app was a huge hit and they were eventually tapped by Steve Jobs directly to be one of the first four apps on iOS and presented onstage at the App Store launch. Steve Jobs' personal physician had reportedly told him she wouldn't switch to an iPhone until it had Epocrates.

The Painful Lessons of Epocrates

The heady days of 2000 didn't last. The venture capitalists told Tangney to hire like crazy, so he did. Then came the tech crash and the crisis from the 9/11 terrorist attacks. In 2002, Epocrates was forced to cut a bunch of jobs. The company held on, but it was a slog.

Fiedotin left a few years later, and Lee departed to start One Medical, a chain of primary care clinics that uses technology to improve the patient experience. Tangney stayed, grinding through years of rebuilding.

Tangney stuck around a bit longer, and tried to take Epocrates public. Then came the financial crisis of 2008, and the company had to withdraw its prospectus. Tangney finally left in late 2009, a year before the eventual IPO and four years before Athenahealth bought the company for $293 million.

When Tangney left, Epocrates was doing about $100 million in revenue, about $20 million in EBITDA. He had built a genuinely useful product used by millions of physicians, survived two market crashes, but the ending felt hollow. Epocrates ended up after a disappointing acquisition for less than $300 million.

"There was a point during the last couple years of my tenure where it felt like we were in this tunnel, marching toward a goal," Tangney said. "I wasn't having as much fun."

The Insight That Sparked Doximity

The decade at Epocrates hadn't just taught Tangney about mobile software development. He had spent years selling products to medical centers and talking to doctors about the challenges they faced. He kept those conversations going and learned that communication was a constant point of stress—whether getting in touch with patients, other doctors, administrators, or recruiters.

One particular pain point kept surfacing: referrals. How do you find the right specialist for a complex case? In an era of instant connectivity, physicians were still relying on word-of-mouth, fax machines, and hospital directories that were outdated before they were printed.

More than 2,000,000 physician-to-physician connections have been made on the Doximity network. According to The Joint Commission, communication breakdowns between care providers are the root cause of 65 percent of serious medical errors. Doximity addresses these communication challenges with the first online community built exclusively for medical professionals.

The insight was deceptively simple: doctors needed LinkedIn, but built for medicine. Not just a professional network, but a secure, HIPAA-compliant platform where they could find specialists, send encrypted messages, and coordinate patient care without the bureaucratic friction that slowed everything down.

But Tangney's real insight wasn't about the product—it was about the approach. He had watched the venture-backed growth machine nearly destroy Epocrates twice. He had seen what happens when companies hire like crazy at the urging of investors, then have to gut their teams when markets turn. For Doximity, he would do things differently.

III. Founding & Early Days: Building the Network (2010-2013)

Assembling the Dream Team

The company was launched in March 2011 by co-founders Nate Gross, Jeff Tangney and Shari Buck.

Shari Buck had worked with Tangney at Epocrates. She's one of the first people he approached with the idea of creating a professional network designed for doctors. Buck said she hopped on board "without reservation," joining as one of the three co-founders, along with Nate Gross, a doctor who is also the founder of health-tech incubator Rock Health.

The trio represented a potent combination. Tangney brought the founding vision and hard-won experience from Epocrates. Shari's career has always been at the intersection of healthcare and technology, holding product roles at a variety of health tech startups and Epocrates prior to Doximity. She would lead product and engineering.

Nate leads the company's long-term strategic vision and ensures the alignment of short and long-range plans, strategic investment roadmaps, and channel-level strategies and objectives. He is also co-founder of Rock Health, a full-service seed fund that supports startups working in digital health. Nate holds an M.D. from Emory University School of Medicine as well as an M.B.A.

As the only physician on the founding team, Gross brought deep understanding of the clinical world. Together, they formed a powerful trio—Tangney with the founding vision, Buck with the ability to craft products, and Gross as the continuous voice of the customer.

The "Above the Garage" Days

"Before we had an office, Jeff would drive up to Marin to meet me," Buck said. "We would meet in a workspace above the garage. We used to laugh at how Apple it was," she said, referring to the storied location where Steve Jobs and Steve Wozniak started their computer company.

The Apple comparison wasn't just about garage mythology. Like Jobs and Wozniak, the Doximity founders were obsessing over product quality and user experience in a market—healthcare—that had long accepted clunky, user-hostile software.

Tangney also turned to Lee as a sounding board and advisor. At One Medical, Lee had the perfect test audience for Tangney: A growing base of doctors who were enthusiastic about technology.

The Data Moat Strategy

Here was the genius insight: pre-populate the network with physician data to reduce friction for adoption.

By combining hundreds of medical databases and journals onto a single platform, Doximity would immediately contain information on nearly every U.S. physician, including their medical school, specialty, location, phone number, fax number, and associated journal articles. When doctors arrived, they wouldn't find an empty network—they'd find colleagues already listed, reducing the cold-start problem that kills most social networks.

Launched in November 2010, Doximity allows physicians to send HIPAA-compliant messages, fax directly from phone or web, search nationwide databases of health care facilities and find contact information for over 500,000 physicians. Doximity aims to prevent medical miscommunication by simplifying day-to-day physician communication.

Early Funding & Capital Discipline

Doximity received $10.8 million in venture capital funding from Emergence Capital Partners and InterWest Partners in March 2011, and $17 million in Series B funding led by Morgenthaler Ventures in September 2012.

InterWest Partners, a diversified venture capital firm based in Silicon Valley, was the lead investor in Tangney's previous company, Epocrates. "We have enormous confidence in the potential of Doximity to modernize medical communications," said Doug Pepper, an InterWest General Partner. Tangney was an entrepreneur-in-residence at InterWest for five months prior to starting Doximity.

Emergence Capital Partners, also based in Silicon Valley, has led venture financing for Salesforce.com, Yammer and SuccessFactors. "We believe the opportunity for innovation in healthcare has never been greater than today and Doximity represents the best of a new wave of health IT technologies," said Gordon Ritter, a founding partner at Emergence Capital.

Even during the Series A, when they did not know when revenue might materialize, Tangney's insistence on focusing first on building the best possible platform for healthcare workers convinced Emergence Capital to invest at the earliest stage possible. "Emergence has been instrumental to Doximity's success. Their partnership in building out our SaaS business and helping recruit key executives helped accelerate our path from Series A to IPO."

Explosive Early Growth

The network effects kicked in faster than anyone expected.

By the end of 2011, Doximity had managed to sign up over 30,000 physicians, equal to about five percent of all physicians in the United States. By 2013, it became one of the largest networks for U.S. healthcare professionals, with approximately 10 percent of U.S. doctors as members. By the beginning of 2014, 40 percent of U.S. physicians became members.

Since Doximity's Series A funding 17 months ago, Doximity has grown 15-fold to over 1 in 7 U.S. physicians on its network. This elite group has formed over 2 million colleague connections and conducts 1,000 searches daily to find the right expert for their patients. Notably, 3 out of the top 5 medical schools (Stanford, UCSF, University of Pennsylvania) partner with Doximity to run their own alumni networks.

Aside from the iPhone, there's never been a piece of technology adopted by clinicians as quickly as Doximity. This adoption curve—faster than electronic health records, faster than e-prescribing—signaled that Doximity had identified a genuine need.

The early growth also validated the pre-population strategy. By combining verified data from medical schools, licensing boards, and journal databases, Doximity had created the most comprehensive physician directory ever assembled—and physicians were claiming their profiles and adding colleagues at a rate that surprised even the founders.

IV. Key Inflection Point #1: The Monetization Breakthrough (2013-2014)

Finding Product-Market Fit

In early 2012, Doximity made a significant move by introducing its Newsfeed feature—curated medical news tailored to each physician's specialty and interests. The feature transformed Doximity from a directory into a destination, giving doctors a reason to return daily.

At the time, Tangney was not at all focused on revenue, but was rather pursuing an approach more akin to consumer internet start-ups, trying to build a big base of engaged users with the hope that money would eventually follow. They batted around ideas for future revenue opportunities. Helping medical recruiters find talent was a clear possibility.

The Revenue Model Emerges

Doximity capped the year off by finally starting to make money via a recruitment tool for medical professionals. The company discovered that its database of verified physicians—with their specialties, locations, and career histories—was extraordinarily valuable to healthcare recruiters struggling to fill positions.

The company makes money primarily by allowing drugmakers to promote products and services to doctors and as a recruiting tool for medical systems. DOCS doesn't generally charge medical workers to use the platform, making money instead from pharma companies, hospitals and other medical businesses that pay for marketing, job postings/recruiting, telehealth visits and other services.

Doximity became a profitable company from 2014 onwards—a remarkable achievement for a venture-backed startup, and a deliberate choice by Tangney to prove the business model worked before scaling.

The Counter-Intuitive Series C Decision

Doximity, an online professional social media marketing network for U.S. physicians, closed a $54 million Series C fundraising round co-led by Draper Fisher Jurvetson and T. Rowe Price. New investor Morgan Stanley Investment Management and returning investors Emergence Capital Partners, Morgenthaler Ventures and InterWest Partners also participated. The Series C funds brought Doximity's total to-date funding to about $81 million.

The IPO marks Doximity's first financing since 2014, when the company raised $54 million at a $355 million valuation, according to PitchBook.

What Tangney did next was almost unheard of in Silicon Valley: he stopped fundraising.

The "Go Dark" Strategy

Most companies would have parlayed that momentum into a massive Series D, hired aggressively, and expanded globally. Tangney did the opposite. Throughout the next few years, Doximity's executive team took the very deliberate decision of cutting down on its public exposure.

Seven years of quiet growth with no additional fundraising—an almost unheard-of approach in Silicon Valley. Tangney said that because Doximity is profitable it still hadn't touched the $50 million it raised seven years ago.

Tangney explained: "I did resist some of the Silicon Valley wisdom of, you need to go big, you need to hire 40 more sales people and do all these things."

The experience at Epocrates—the hiring binges followed by painful layoffs—had left a mark. Tangney believed that sustainable growth, funded by actual revenue rather than investor optimism, would create a more durable company. The strategy was contrarian to the point of seeming crazy, but it would prove prescient.

V. Key Inflection Point #2: The Dialer & Workflow Tools Era (2016-2019)

Transforming from Network to Utility

In 2016, Doximity built Dialer, a free communication tool for physicians to call their patients. The Doximity Dialer app allows physicians to call patients from their personal cell phone, and the patient sees the doctor's office number on caller ID.

This was a critical strategic shift: from a social network (like LinkedIn) to an essential daily workflow tool. The insight was simple but powerful. Doctors often needed to call patients from their personal cell phones—evenings, weekends, on call. But patients would see an unfamiliar number and ignore the call, or the doctor would expose their personal number.

Dialer solved this elegantly. A physician could call from their iPhone at 10 PM, and the patient would see the hospital's main line on caller ID. The call would connect, and the doctor's personal number remained private.

The company has offered a free service since 2016 that allows doctors to call patients using their work number on a mobile phone. Doximity moved the dialer service to its main app in 2019.

Building the Physician Cloud

In 2018, the company announced that it had reached 1 million members, accounting for more than 70 percent of U.S. physicians.

In November 2019, Doximity was listed on the Deloitte Technology Fast 500 list for the fourth consecutive year.

Doximity was the first outbound link to appear in Epic's mobile app Haiku in 2018—a significant partnership with the dominant EHR platform. This integration meant that physicians using Epic's mobile app could seamlessly find colleagues on Doximity, creating a powerful endorsement from the healthcare IT establishment.

The Rule of 60

Doximity retains growth and profitability by keeping marketing and sales expenses low. It uses "the rule of 60" to ensure it chalks up profits annually. This states that the sum of the revenue growth rate and profit margin must be greater than 60.

This operational discipline became a hallmark of the company. While competitors burned cash chasing growth, Doximity proved that disciplined spending could coexist with rapid expansion. The rule of 60 forced trade-offs—sometimes growth had to slow to preserve margins, sometimes margins compressed to fund growth—but it ensured the company never strayed into the territory of endless cash burns.

The approach reflected Tangney's hard-won wisdom from Epocrates. Companies that optimize solely for growth become vulnerable when markets turn. Companies that maintain profitability have options—they can weather downturns, make strategic acquisitions, or simply continue operating without depending on the kindness of investors.

VI. Key Inflection Point #3: COVID-19 & the Telehealth Explosion (2020-2021)

The Pandemic Pivot

In March 2020, the world changed. As COVID-19 spread and in-person visits became dangerous, the healthcare system scrambled to adopt telehealth. Doximity, which had been quietly building communication tools for years, found itself perfectly positioned.

On May 5, 2020, Doximity announced the launch of Doximity Dialer Video, the company's first telemedicine offering. With one easy click, Doximity Dialer Video lets doctors video call their patients, in an encrypted environment that complies with HIPAA privacy regulations. The new tool works with a doctor's personal iOS or Android smartphone and doesn't require any additional set up for physicians or patients.

In response to the COVID-19 crisis, Dialer Video is available for free through January 2021. A paid enterprise version, Doximity Dialer Pro, is also available for hospital-wide deployments.

The timing was extraordinary. Just weeks earlier, most physicians had viewed telehealth as a novelty. Now it was essential.

"In particular, we have seen a surge in usage of Doximity Dialer. For context, prior to the pandemic, we were facilitating about 1 million calls a month. Now we are averaging about 1 million calls a day. Our newsfeed has also seen over 60% jump in engagement since the crisis began," Phull told FierceHealthcare.

Doximity announced a surge in physician adoption of its telemedicine tool, Dialer Video. The company reports that over 100,000 U.S. physicians are already using the app since its launch for telemedicine regularly, making Dialer Video the most used telemedicine technology among U.S. physicians to date.

Strategic Acquisition: THMED/Curative

In June 2020, Doximity acquired THMED, a healthcare company. Following the purchase, THMED changed its name to Curative and started concentrating on customized medical-personnel queries.

The acquisition bolstered Doximity's recruiting capabilities at a moment when healthcare organizations were desperately seeking staff.

Financial Performance Explosion

For the years ended March 31, 2020 and 2021, Doximity recorded revenue of $116.4 million and $206.9 million, respectively, representing a year-over-year growth rate of 78%.

Net income was $29.7 million and $50.2 million for the years ended March 31, 2020 and 2021, respectively—not only growth, but profitable growth.

Doximity demonstrated a 153% net revenue retention rate as of March 31, 2021. This metric—which measures whether existing customers are spending more or less over time—signaled extraordinary customer satisfaction. Not only were customers renewing, they were dramatically expanding their spending.

The Blockbuster IPO

In May 2021, Doximity filed for an initial public offering (IPO) seeking to raise $100 million. Morgan Stanley, Goldman Sachs and J.P. Morgan Securities were the lead underwriters for the IPO. Doximity raised nearly $606 million in its IPO. In its June 2021 IPO on the NYSE, it gave it a market cap shortly after its debut of $9.4 billion.

Doximity announced the pricing of its initial public offering of 23,300,000 shares of its Class A common stock at a price to the public of $26.00 per share. Doximity's Class A common stock began trading on the New York Stock Exchange on June 24, 2021 under the ticker symbol "DOCS." The offering closed on June 28, 2021.

But what made this IPO truly distinctive was its physician participation.

As part of the offering, Doximity reserved 15% of the shares for doctors in the network. Assuming doctors maxed out their participation, they purchased about $91 million worth of Doximity stock and finished the day with shares valued at $185 million. Tangney said more than 10,000 physicians participated in the offering, purchasing up to $24,000 worth of shares. As a group, they own more stock than any single new investor.

"Physicians are sort of outsiders in the financial markets and business world," Tangney said. "Yet in our life and world they're the insiders, they're the people we care about most. We'd rather the shares go to them if there's a pop than to some hedge fund somewhere."

Health-care platform Doximity rocketed 104% in its trading debut after it priced its initial public offering above range to raise $606 million. Shares of the profitable San Francisco-based company closed Thursday at $53 apiece, giving the company a market value of $9.5 billion.

VII. Key Inflection Point #4: The AI Transformation (2023-Present)

DoxGPT Launch

Doximity, a digital platform for medical professionals, rolled out a beta version of a ChatGPT tool for doctors that helps streamline some of their time-consuming administrative tasks, such as drafting and faxing preauthorization and appeal letters to insurers. The open beta site, called DocsGPT.com, is an integration with ChatGPT that works with Doximity's free fax service. The company worked with doctors to fine-tune the product. Doximity engineers began working on the beta site over the holidays.

The initial version utilized AI to help doctors draft prior authorization letters, patient education materials, and research grant applications. For physicians, prior authorization—the process of getting insurance company approval before prescribing certain medications—represents one of the most frustrating administrative burdens. DoxGPT could draft these letters in seconds rather than minutes.

AI Scribe: The Free Disruptor

The ambient artificial intelligence medical scribe market has become crowded, with numerous players jostling for share. Doximity rolled out a new AI medical scribe that is available free of charge to all verified U.S. physicians, nurse practitioners, physician assistants and medical students with a verified Doximity account.

AI medical scribes can be pricey for healthcare organizations. Comparable scribe services can cost hundreds of dollars per month per user, totaling thousands of dollars per user annually.

Scribe is a HIPAA-compliant, AI-powered clinical documentation tool that automatically generates notes during patient visits. It's designed to ease administrative burden, improve note quality, and, most importantly, free up time for patient care.

Doximity Scribe has been in beta testing for more than a year. More than 10,000 Doximity members have used the beta version, creating millions of clinical notes, to help build the tool.

"The reality is, budgets are tight right now," said CEO Jeff Tangney. The free pricing was strategic—by removing cost barriers, Doximity could drive adoption across its massive physician network, deepening engagement and creating more opportunities for monetization through enterprise subscriptions and pharmaceutical marketing.

CEO Jeff Tangney notes a shift in sentiment among clinicians, saying, "In a short couple of years, we've seen AI tools like this truly change the mood in medicine from AI leery to AI cheery."

Pathway Medical Acquisition

In a $63M acquisition, Doximity announced that it has acquired Pathway Medical Inc., a Montreal-based startup specializing in medical AI and evidence-based clinical reference.

Physicians make up half of Pathway's team. Over the past seven years, they've assembled one of the largest structured datasets in medicine—purpose-built for AI—spanning nearly every guideline, drug, and landmark trial across all major specialties. Pathway's model outperforms others in clinical accuracy, recently scoring a record 96% on the U.S. Medical Licensing Examination (USMLE) benchmark.

The transaction closed on July 29, 2025 for cash consideration of $26 million and up to $37 million in additional equity grants.

"Our physician AI suite is now taking shape. Scribe takes your notes, GPT writes your letters, Pathway's Corpus helps answer your questions and they all work together in a three HIPAA compliance suite that's private to each physician," Tangney said. "We're excited to make AI our next act here at Doximity."

Explosive AI Adoption Metrics

"Our AI suite once again grew the fastest, up 5x year-over-year, while more than 630,000 prescribers used our workflow tools to save time."

Management reported over 50% quarter-on-quarter growth in active users of AI-powered tools, including DoxGPT and the Scribe feature. AI-driven offerings accounted for over 40% of recent bookings.

VIII. Business Model Deep Dive

The Two-Sided Marketplace

Doximity operates one of the most elegant two-sided marketplaces in healthcare technology. On one side: physicians who use the platform for free. On the other side: pharmaceutical companies, health systems, and recruiters who pay to reach those physicians.

Doximity also offers a tailored social news feed with medical topics. For example, medical professionals can find posts on the platform much like you would on LinkedIn that you can like or you can comment on or you can share. Medical providers can actually post their practices on the Doximity platform with contact information as well as their resume.

For pharmaceutical manufacturers, Doximity offers something extraordinarily valuable: targeted access to physicians. Unlike consumer advertising, which reaches millions of people who may never need a particular medication, Doximity allows drug companies to reach the exact specialists who prescribe their products.

Doximity's "Hiring Solutions" provide digital recruiting capabilities to health systems and medical recruiting firms, enabling them to identify, connect with, and hire from Doximity's network of both active and passive potential medical professional candidates. Doximity's AI and ML-supported platform enables customers to run highly targeted hiring campaigns across a range of medical specialties and sub-specialties. Doximity's "Telehealth Solutions," which are software tools that include voice and video Dialer, are designed to connect patients with care providers easily. Dialer Enterprise is sold as a subscription, with pricing based on the health system's size.

Revenue Streams

Doximity has a subscription-based business model. Approximately 93% of Doximity's revenue for FY24 was derived from subscription customers.

Doximity estimates a total addressable market (TAM) of $18.5 billion—and it has barely scratched the surface of this opportunity. Doximity estimates the opportunity for U.S. pharmaceutical marketing to medical professionals at $7.3 billion annually. Combining health-system staffing and telehealth software with pharma marketing inflates the company's total addressable market to $18.5 billion.

The Land and Expand Strategy

Doximity's subscription-based business model and strong relationships with both pharmaceutical manufacturers and health systems drive highly visible revenue. They do not generate revenue from membership of medical professionals. They are able to grow revenue from existing customers through an effective land and expand strategy, demonstrated by their 153% net revenue retention rate as of March 31, 2021. Their business model has delivered high revenue growth at scale, while increasing profitability.

The land-and-expand motion works like this: Doximity signs up the vascular surgery department. They walk to the next floor and sign up neurosurgery and orthopedic surgery. A master service agreement incorporates a reference selling model that makes it less costly to add a new department after the initial sale.

Current Financial Performance

All comparisons are to the three months ended September 30, 2024. Revenue: Revenue of $168.5 million, versus $136.8 million, an increase of 23% year-over-year.

Doximity is updating guidance for its fiscal year ending March 31, 2026 as follows: Revenue between $640 million and $646 million. Adjusted EBITDA between $351 million and $357 million.

The company pulled in a total revenue of $570.4 million for fiscal year 2025, marking a strong 20% year-over-year increase, but the real kicker is the bottom line: net income soared to $223.2 million, a massive jump that translates to a 51.23% increase from the previous year. That kind of profit growth, plus a robust $266.7 million in free cash flow (a 50% jump), shows Doximity is not just growing revenue, but converting it to real cash.

IX. Competitive Landscape & Strategic Analysis

Porter's Five Forces Analysis

Threat of New Entrants: LOW Doximity's network of 80%+ of U.S. physicians represents an almost insurmountable barrier. Building a competing network would require years and hundreds of millions of dollars—and even then, the network effects favor the incumbent. Physicians are unlikely to maintain profiles on multiple professional networks when one dominates.

Bargaining Power of Suppliers: LOW Doximity's primary "suppliers" are technology infrastructure providers (cloud computing, AI models) and data sources. None have significant leverage over the company, and Doximity has demonstrated the ability to switch partners or build in-house capabilities.

Bargaining Power of Buyers: MODERATE Large pharmaceutical companies represent significant revenue concentration. The top 20 pharmaceutical manufacturers account for a substantial portion of marketing spend. However, these buyers have limited alternatives—no other platform offers comparable access to verified physicians at scale.

Threat of Substitutes: MODERATE LinkedIn could theoretically expand into healthcare. Traditional pharmaceutical sales representatives compete for physician attention. But substitutes struggle to match Doximity's verification, HIPAA compliance, and embedded workflow tools.

Competitive Rivalry: LOW Doximity competitors include LinkedIn, Monstarlab, Healthgrades, and Medscape. However, none have achieved Doximity's combination of network scale, workflow integration, and verified membership. The demand has given rise to sites like Sermo, Doximity and QuantiaMD, among others. But Doximity has emerged as the clear winner.

Hamilton Helmer's 7 Powers Framework

Network Effects (STRONG) Doximity benefits from the network effect. The more physicians on its platform, the more attractive it becomes to its clients, and vice versa. Could there be a competing platform that takes significant market share away from the company? That's a definite maybe.

Scale Economies (STRONG) With 90%+ gross margins, Doximity's unit economics improve as it grows. Fixed costs (engineering, infrastructure) spread across a larger revenue base.

Switching Costs (STRONG) Physicians have built professional profiles, accumulated connections, and integrated Doximity into daily workflows. Switching requires rebuilding a network and learning new tools—significant friction.

Counter-Positioning (MODERATE) Doximity's physician-first approach contrasts with competitors who optimize for advertisers. Copying this approach would require existing players to cannibalize their own business models.

Cornered Resource (STRONG) The verified physician database—with credentials, specialties, prescribing patterns, and professional connections—represents a proprietary asset that cannot be easily replicated.

Process Power (MODERATE) Doximity's product development process, informed by physician feedback and integrated AI tools, creates sustained advantages in product quality.

Brand (DEVELOPING) Among physicians, Doximity has achieved significant brand recognition. Among investors and the general public, the brand remains less developed.

X. Bull Case vs. Bear Case

The Bull Case

AI Creates a New Growth Engine The rapid adoption of DoxGPT and Scribe demonstrates that Doximity can layer new products onto its existing network. If AI tools become as essential to physicians as Dialer became, Doximity's revenue per user could expand dramatically.

Pharmaceutical Marketing Shift to Digital Recent FDA reforms have introduced new channels of opportunities for businesses like Doximity, particularly as pharmaceutical spending patterns shift. As pharma companies move spend from field sales representatives to digital channels, Doximity captures an increasing share.

Expansion to Adjacent Professions While they will continue to grow their number of physician members, they are under-penetrated among other types of medical professionals, such as nurse practitioners, and have an opportunity to expand their offering to physical therapists, dentists, psychologists, and many other professions.

TAM Penetration Remains Low With a current revenue run rate of $500 million, that would leave Doximity less than 3% penetrated—a lot of open field for continued growth. When you consider that its largest advertisers—the pharmaceutical companies—spend only 5% of their marketing dollars with Doximity, the potential for continued growth is enticing.

The Bear Case

Customer Concentration Risk The core financial risk is structural: Doximity's revenue is heavily dependent on pharmaceutical and health system marketing budgets. But what if a major client cuts their marketing spend? The top 20 clients are their fastest-growing, which is great, but it also means a shift in strategy from just a few large players can create a significant headwind.

Net Revenue Retention Normalization Doximity has traditionally reported incredibly strong revenue retention rates over 150%, although this fell to 117% in the most recent quarter (still good, but not as impressive). This is a testament of the ongoing value it is providing to its paying customers.

The normalization from 150%+ to 116% suggests the extraordinary upselling momentum of the pandemic era may not be repeatable.

AI Commoditization Physician networking company Doximity released a free AI scribe Thursday, highlighting the subsector's lack of technical moat. If AI scribe technology becomes commoditized, Doximity's competitive advantage may erode.

Regulatory Risk This reliance on discretionary marketing spend is vulnerable to broader economic uncertainty and industry-specific pressures. The external risks are just as real, especially in a sector as regulated as healthcare. Any new legislation or policy change affecting how pharmaceutical companies market their products could directly impact Doximity's business model.

XI. Key Performance Indicators to Watch

For investors tracking Doximity's ongoing performance, three KPIs matter most:

1. Net Revenue Retention Rate This metric captures customer satisfaction, pricing power, and expansion ability in a single number. Net revenue retention rate is calculated by taking the trailing 12-month subscription-based revenue from customers that had revenue in the prior period. Our net revenue retention rate compares our subscription revenue from the same set of customers across comparable periods, and reflects customer renewals, expansion, contraction, and churn. Our net revenue retention rate is directly tied to our revenue growth rate.

Watch for: Sustained rates above 115% signal healthy expansion; rates below 110% may indicate commoditization or pricing pressure.

2. Active Prescribers Using Workflow Tools Doximity provides software tools for doctors and clinicians and its clinical workflow tools saw record use in the most recent quarter, with more than 620,000 unique active prescribers.

This metric captures the critical transition from "social network" to "essential workflow tool." The stickier Doximity becomes in daily physician routines, the more defensible the business.

3. AI Tool Adoption Growth Rate The company is rapidly scaling its AI efforts—its AI tools grew more than fivefold year over year.

As AI becomes central to Doximity's value proposition, tracking adoption curves for DoxGPT, Scribe, and integrated Pathway capabilities will signal whether the company is successfully executing its AI transformation.

XII. Conclusion: What Doximity Teaches Us

The Doximity story offers several lessons for observers of technology and healthcare:

Capital Efficiency Can Coexist with Growth. In an era when many tech companies treated venture funding as a competitive weapon—spending aggressively to capture market share before worrying about profitability—Doximity proved an alternative path. Seven years without fundraising, profitable operations from 2014 onward, and a "Rule of 60" that forced disciplined trade-offs.

Network Effects Are Especially Powerful in Professional Contexts. LinkedIn's dominance in professional networking demonstrated that business relationships create stickier networks than personal ones. Doximity applied this insight to healthcare, building a network that physicians genuinely need rather than merely enjoy.

The "Physician-First" Philosophy Creates Durable Differentiation. In healthcare technology, products are often designed for administrators, IT departments, or payers—the people who write checks. Doximity's relentless focus on physician needs created a user base that became the asset, making the platform valuable to everyone else.

AI Represents Both Opportunity and Risk. Doximity's aggressive AI investments position it well for the transformation reshaping healthcare. But AI also threatens to commoditize some of Doximity's competitive advantages—if any vendor can offer a good-enough AI scribe, the differentiation shifts elsewhere.

Jeff Tangney rang the opening bell at the NYSE on June 24, 2021, watching his company's stock more than double on its first day of trading. The 10,000 physicians who had bought shares at the IPO price celebrated alongside him. It was vindication for a decade of work, for the painful lessons of Epocrates, for the contrarian decision to ignore Silicon Valley's growth-at-all-costs wisdom.

Today, Doximity stands at another inflection point. The network is built, the monetization engine hums efficiently, and AI offers a new frontier for growth. Whether Doximity can sustain its remarkable trajectory depends on executing the AI transformation while maintaining the capital discipline and physician-first focus that got it here.

The "LinkedIn for doctors" that defied Silicon Valley now faces a familiar question: can a company built on contrarian principles continue to thrive in a world that keeps changing around it?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube