Kusurinomadoguchi: Japan's Pharmacy Platform Revolution

I. Introduction & Episode Roadmap

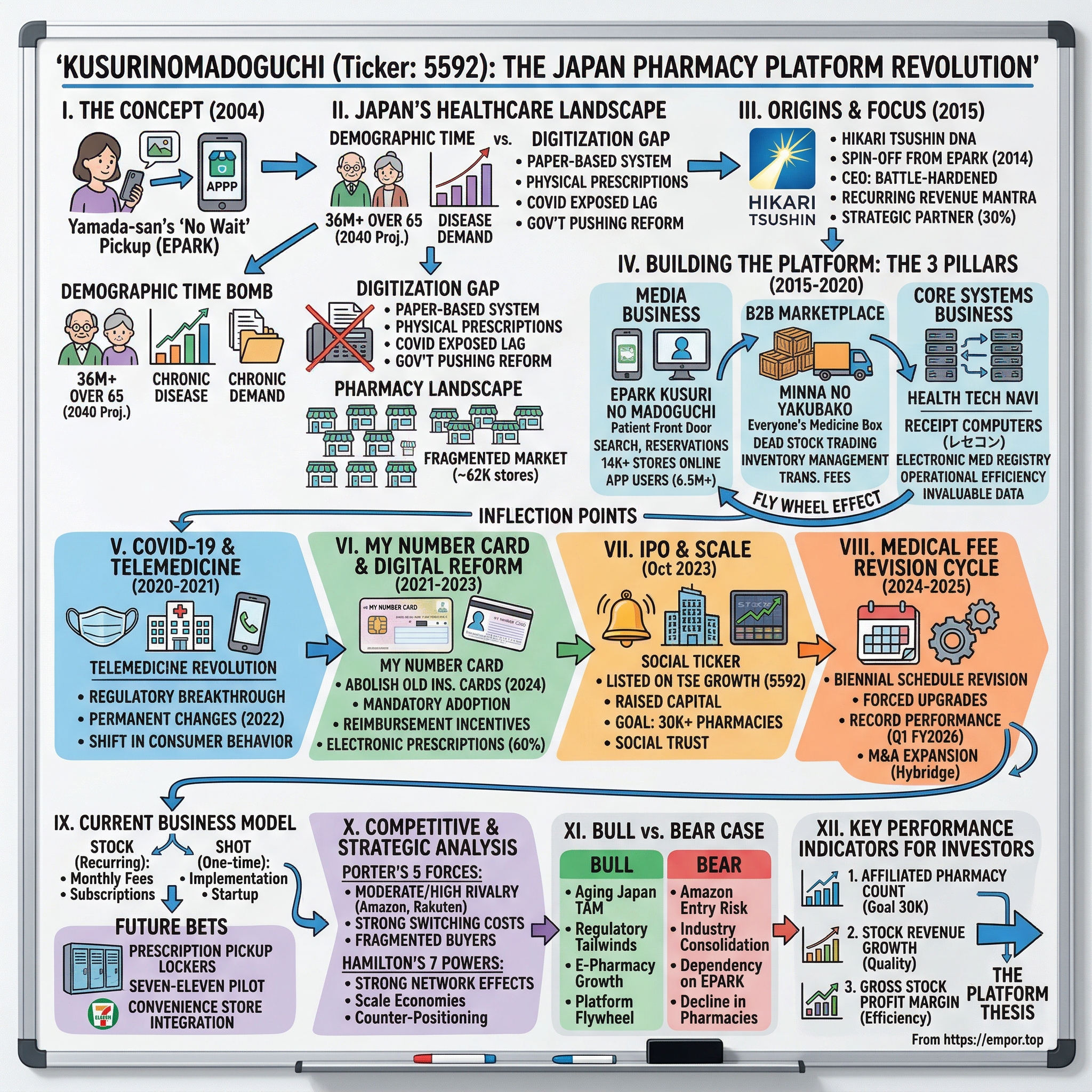

Picture this: It's 5:30 PM on a rainy Tuesday in Shibuya, Tokyo. A working mother named Yamada-san checks her phone during a brief pause in her commute. Her elderly mother's prescription refill is waiting at the pharmacy, but the thought of another 40-minute wait in a crowded dispensing area—with two children in tow and dinner to prepare—fills her with dread. Then she remembers: she can simply send a photo of the prescription to her phone app, select a pickup time, and collect the medication in under five minutes. No waiting room. No queue. This isn't some futuristic vision—this is Kusurinomadoguchi's EPARK system, operating today across more than 14,000 pharmacies in Japan.

The company was founded in 2004 and is headquartered in Tokyo, Japan. But what began as a modest corporate spin-off has evolved into something far more ambitious: a healthcare technology company that develops and operates a comprehensive platform connecting patients, pharmacies, and medical institutions. Today, the company's flagship consumer service, "EPARK Kusuri no Madoguchi," is one of Japan's largest search and prescription reservation platforms, enabling users to find pharmacies and minimize waiting times.

The big question at the heart of this story: How did a spin-off from a restaurant reservation company become Japan's largest pharmacy technology platform?

In 2024, Kusurinomadoguchi's revenue was 11.20 billion yen, an increase of 28.41% compared to the previous year's 8.72 billion. Earnings were 2.03 billion, an increase of 133.79%. These aren't incremental improvements—they represent a company that has reached escape velocity in one of the world's most complex healthcare markets.

This is a story about timing, patience, and the slow-burning regulatory revolution that is transforming how 126 million Japanese citizens interact with their healthcare system. It's about network effects in regulated industries, the power of vertical integration, and why digitizing something as mundane as pharmacy wait times can create billions of yen in enterprise value.

II. Japan's Healthcare Landscape: Setting the Stage

Before understanding Kusurinomadoguchi's opportunity, we must understand the peculiarities of the Japanese healthcare system—a system simultaneously admired for its universal coverage and criticized for its glacial pace of digital adoption.

The Demographic Time Bomb

Japan is the world's test case for what happens when a wealthy society ages rapidly. More than 1 in 10 people in Japan are now aged 80 or older, with nearly a third of the population (approximately 36.23 million) over 65. With one of the world's oldest populations, as recognized by the UN, the percentage of citizens aged 65 and older is projected to reach nearly 35% by 2040.

This isn't merely a demographic statistic—it's a fundamental reshaping of healthcare demand. The elderly population in Japan has a higher incidence of chronic diseases such as diabetes, hypertension, and cancer. This has created a high demand for pharmaceutical products that can treat these conditions effectively.

The Japan pharmacy retail market size reached USD 114.26 Billion in 2024 and is expected to hit USD 185.63 Billion with a CAGR of 5.54% during 2025–2033. The sheer scale of this market—larger than many countries' entire GDPs—creates opportunities for technology companies that can improve even marginal inefficiencies.

The Digitization Gap

The pandemic exposed Japan as a laggard in the development and use of medical big data systems. While countries like Estonia and South Korea raced ahead with digital health records and telemedicine, Japan's healthcare system remained stubbornly paper-based. Prescriptions moved physically from doctors to pharmacies. Patient records existed in isolated silos. The fax machine—yes, the fax machine—remained a critical piece of healthcare infrastructure.

This wasn't mere technological backwardness. The Japan Medical Association is firmly against making telemedicine permanent and will resist any move away from the status quo. Powerful institutional forces preferred the status quo, viewing digitization as a threat to the intimate doctor-patient relationship that defined Japanese medicine.

But COVID-19 changed everything. In response, the government has allocated over 100 billion yen in its FY2021 budget to further promote data health reforms needed to establish a resilient digitized social security system and promote data utilization to improve medical care.

The Pharmacy Landscape

Japan's pharmacy market is simultaneously concentrated and fragmented—a paradox that creates both challenges and opportunities. In fiscal year 2022, the total number of pharmacies in Japan amounted to around 62.4 thousand stores. That's approximately one pharmacy for every 2,000 people—one of the highest pharmacy densities in the developed world.

Japan's dispensing pharmacy market was worth roughly ¥8.3 trillion in fiscal 2024, but the market remains fragmented. While giants like Welcia and Tsuruha dominate drugstore retail, the dispensing pharmacy market—where patients collect prescription medications—remains populated by thousands of independent operators.

This fragmentation creates an opportunity for platform businesses. Independent pharmacies struggle to build consumer-facing technology, manage inventory efficiently, or compete for patient attention. A platform that could aggregate demand, standardize technology, and create network effects could fundamentally reshape the industry.

As of 2024, over 12,000 pharmacies in Japan have been certified as "Health Support Pharmacies" (HSPs), offering proactive health consultations, disease prevention education, and nutritional guidance. The pharmacy of the future in Japan isn't just a medication dispensary—it's a community health hub. And connecting those hubs requires technology.

For investors, the Japanese healthcare market represents a massive total addressable market with structural tailwinds (aging population), regulatory catalysts (mandatory digitization), and fragmented competition. The company that can become the "operating system" for this market will capture enormous value.

III. Origins: From EPARK to Pharmacy Focus (2004-2015)

The Hikari Tsushin DNA

To understand Kusurinomadoguchi, you must first understand Hikari Tsushin—one of Japan's most misunderstood conglomerates. Hikari Tsushin is a USD 10 billion market cap company that is unique in Japan for its highly rational capital allocation strategy. The company is one of the largest shareholders of Berkshire Hathaway in Japan.

Jiro and Patrick view it as one of the most avoided stocks by Japanese portfolio managers due to its checkered past. That "checkered past" includes the dot-com crash, when Hikari Tsushin's stock famously fell from over 200,000 yen to under 1,000 yen—one of the most spectacular corporate collapses in Japanese history. But from those ashes emerged a company with a singular focus: selling a variety of products that generate recurring revenue streams.

This is an interesting business that can be seen as a grandchild of Hikari Tsushin. It was spun off from one of Hikari's EPARK, which has been a subsidiary since 2014 under their Solution Segment. EPARK has been their division that focuses on IT business solutions in typical Hikari fashion, a business that focuses on recurring revenue. One of their primary service at EPARK has been a booking service for food retail concepts.

EPARK's business model was elegantly simple: eliminate wait times. At restaurants like Kura Sushi, customers could use the EPARK app to see real-time wait times and make reservations. No more standing in line for conveyor belt sushi. The service became wildly popular—EPARK eventually accumulated approximately 50 million members.

The Pharmacy Pivot

Kusurinomadoguchi was established soon after in 2015 as an offshoot of EPARK and further specialised in the healthcare vertical, as the name might suggest. In effect, they started as a booking service for pharmacies and drug stores, where customers can 'book' their prescription in advance. Again, the main attraction here is that it has a strong focus on recurring revenue.

The strategic logic was compelling: If "no-wait dining" appealed to time-pressed Japanese consumers, "no-wait prescription pickup" would appeal to the same demographic—especially the elderly, chronically ill, and busy parents who disproportionately needed pharmacy services.

The main Kusurinomadoguchi is a portal site for consumers to help search for nearby pharmacies, and with it the capability for patients to upload prescriptions digitally and book a pick-up ahead of time, either via website or mobile app. Streamlining this whole process. This adds value for pharmacies because the platform provides visibility for them. They know in advance what medication to prepare (i.e. better inventory control) and operational efficiency, where such entities are already quite stretched due to a shortage of personnel.

The CEO: Battle-Hardened by Hikari

The key link to Hikari here is this CEO who has been at Hikari Tsushin since 1999 and through the last 25 years he's held multiple management roles there. Now remember, the environment in which he operated was highly competitive, and he survived through all that. You could say he's been battle-hardened and taught the value of recurring revenue and IRR, which is pretty much a mantra for Hikari at this point. He eventually became the Vice President of EPARK in 2014, then Vice President of KMG in 2016, and eventually CEO in 2020.

This leadership pedigree matters. One thing I really like about Hikari is that they have been able to figure out how to sell recurring services/products well, and in doing so, generate an IRR of close to 30%. The discipline of pursuing recurring revenue—"stock" sales in Japanese corporate terminology—would prove to be the cornerstone of Kusurinomadoguchi's strategy.

Hikari remains a ~30% owner in KMG and I like to believe that the company will continue to support the growth of this company. This parent company relationship provides both capital support and strategic discipline—a powerful combination in a market where patience and long-term thinking are essential.

For investors, the Hikari Tsushin heritage signals a management team with deep experience in building recurring revenue businesses, rigorous capital allocation, and the patience to build value over decades rather than quarters.

IV. Building the Platform: The Three Pillars (2015-2020)

By 2020, Kusurinomadoguchi had evolved from a simple prescription reservation app into a comprehensive platform business organized around three distinct pillars. Understanding these pillars—and how they interconnect—is essential to understanding the company's competitive moat.

Pillar 1: Media Business (Patient-Facing)

The Media Business represents the consumer-facing "front door" of the Kusurinomadoguchi platform. The media business operates EPARK Kusuri no Madoguchi, a search site and application for pharmacies such as dispensing pharmacies and drugstores, and EPARK Oyaku Techo, an electronic medication registry application.

Think of this as "Google Maps for pharmacies"—but with real-time information on wait times, available services, and the ability to send prescriptions ahead of arrival. Prescriptions can be accepted online at more than 14,000 stores nationwide. Pharmacy information is posted for approximately 70,000 stores nationwide.

Whilst there are already 6.5 million app users for their Prescription app, there may be a ceiling. However, even this "ceiling" represents remarkable penetration in a market where most healthcare interactions still occur through paper-based systems.

The revenue model for the Media Business combines both "stock" (recurring) and "shot" (one-time) components. Pharmacies pay monthly listing fees for premium positioning on the platform, plus initial implementation costs. For patients, the service is free—a classic two-sided marketplace model where the consumer side is subsidized by the business side.

Pillar 2: Minna no Yakubako (Everyone's Medicine Box) - B2B Marketplace

The second pillar addresses one of the most vexing problems in pharmacy operations: pharmaceutical inventory management. The company offers EPARK drug counter, a pharmacy/drugstore search and reservation site; matching site to buy and sell dead stock medicines at dispensing pharmacies.

"Dead stock" medicines are pharmaceuticals that pharmacies have ordered but cannot sell before expiration. This is a significant problem in Japan, where the diversity of medications combined with uncertain demand means pharmacies often find themselves holding expired inventory. For small independent pharmacies with limited capital, dead stock represents both a financial burden and pharmaceutical waste.

Kusurinomadoguchi's solution: create a marketplace where pharmacies can trade surplus inventory with each other. A pharmacy in Osaka with excess antihypertensives can sell to a pharmacy in Tokyo that needs them. The platform takes a transaction fee, pharmacies reduce waste, and patients benefit from better availability.

It also provides Pharmacy Support, a customer management system for repeat patients in the pharmacy industry; system specialized for dispensing pharmacies; matching service that connects nursing care facilities and pharmacies; solution from the purchase of pharmaceuticals to the purchase of immovable inventory.

Pillar 3: Core Systems Business (Infrastructure)

The third pillar represents the "plumbing" of the pharmacy technology stack—and is arguably the most strategically important. The company offers Health Tech Navi, an electronic medication history system; Care Daisy system to link recording systems and ICT devices; solution for purchasing pharmaceuticals; and system that allows for centralized management of outpatient reception, outpatient reservations, and online medical treatment.

At the heart of this pillar is the "receipt computer" (レセコン)—specialized systems that generate medical fee statements for submission to insurance systems. In Japan, every pharmacy interaction with the national health insurance system flows through these receipt computers. Whoever controls this infrastructure has access to invaluable data about prescribing patterns, patient behavior, and pharmacy operations.

The Interconnected Flywheel

These three pillars don't exist in isolation—they form an interconnected flywheel where each business strengthens the others:

The Media Business drives patient traffic to pharmacies on the platform. This traffic makes the platform more valuable to pharmacies, who are then more likely to adopt Core Systems products. As more pharmacies use Core Systems, the company gains better data about inventory needs, which improves the Minna no Yakubako matching algorithm. Better matching attracts more pharmacies to the marketplace, which makes the Media Business more comprehensive, attracting more patients.

KMG consists of 3 operating segments. This segment's main concept has been to "Connect healthcare to patients" and can be seen as the genesis of KMG as it houses the main EPARK Kusurinomadoguchi biz. In a nutshell, this business aids pharmacies with customer acquisition and retention.

For investors, the three-pillar structure represents a classic platform strategy with multiple revenue streams and natural cross-selling opportunities. The key question is whether the network effects are strong enough to create durable competitive advantages.

V. Key Inflection Point #1: COVID-19 and the Telemedicine Revolution (2020-2021)

March 2020. Japan, like the rest of the world, is gripped by pandemic panic. Hospitals are overwhelmed. Elderly patients—Japan's most vulnerable and most pharmacy-dependent population—are terrified to leave their homes. The carefully maintained status quo of Japanese healthcare is about to shatter.

The Regulatory Breakthrough

Before COVID-19, telemedicine in Japan was legally complex and practically rare. Before the new regulation, the allowable use of telemedicine in Japan was restricted to patients with chronic diseases and not for first-visit patients, except for emergencies or underserved areas. As a result, telemedicine accounted for only 0.18% of all outpatient medical claims in fiscal year 2019.

Then came the emergency measures. On April 10, 2020, the Japanese government relaxed restrictions on telemedicine use as an exceptional measure to enable health care providers to reach patients during the COVID-19 pandemic. After April 2020, telemedicine was permitted for almost all patients, except for those receiving medications that required in-person supervision.

The Japanese government has developed these measures to promote telemedicine as temporal measures but made them permanent starting in April 2022. What began as emergency pandemic response became permanent structural change. The Minister of Health, Labour, and Welfare reached an agreement to make telehealth permanently available with the Minister in charge of regulation reform and the Minister of Digital Transformation. The Japan Medical Association (JMA) has expressed its opposition towards the decision.

The JMA's opposition—institutional resistance from the traditional healthcare establishment—is significant. It means the government was willing to override one of Japan's most powerful lobbies to push through digitization. This represented a fundamental shift in political will.

Patient Behavior Shift

Technological advancements and the rise of e-pharmacies are reshaping Japan's pharmacy retail market. In recent years, Japanese consumers have increasingly turned to digital platforms, including online pharmacies and health apps, to access medications and healthcare services more conveniently. This digital shift, accelerated by the COVID-19 pandemic, has seen more consumers opting for remote consultations and ordering prescription drugs online.

The Japan e-pharmacy market size reached USD 6.4 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 20.5 Billion by 2033, exhibiting a growth rate (CAGR) of 12.4% during 2025-2033.

A 12.4% CAGR in an economy growing at less than 2% represents massive relative outperformance. The pandemic didn't just accelerate existing trends—it fundamentally rewired consumer expectations around healthcare convenience.

Company Response

Kusurinomadoguchi was uniquely positioned to capitalize on this shift. The company already had the technology infrastructure to support online prescription reception. The patient-facing app already had millions of users accustomed to digital pharmacy interactions. The Core Systems business already connected thousands of pharmacies to digital infrastructure.

While competitors scrambled to build digital capabilities, Kusurinomadoguchi simply scaled what it had already built. The pandemic compressed years of expected adoption into months—and the company was ready.

For investors, COVID-19 represents a classic case of "luck favoring the prepared." Kusurinomadoguchi's pre-pandemic investments in digital infrastructure created optionality that paid off spectacularly when market conditions shifted.

VI. Key Inflection Point #2: My Number Card & Digital Reform (2021-2023)

If COVID-19 was an external shock that accelerated digitization, the My Number Card reform represents a structural policy change that makes digitization mandatory. This distinction matters enormously for long-term investors.

The My Number Revolution

The Japanese government has decided that the current health insurance card will be abolished on December 2, 2024. Health insurance cards will no longer be issued thereafter, and in principle, you will need to prepare a Myna health insurance card.

From December 2, 2024, the Japanese government will stop issuing traditional health insurance cards, transitioning entirely to the use of the My Number Card as a health insurance card. This multi-purpose card, referred to as the My Number Health Insurance Card, integrates health insurance and various government service functionalities. Introduced in 2016, the My Number Card serves as official identification card for identity verification purpose and grants access to a broad range of government services in Japan.

With the expiration of all health insurance cards on December 1, 2025, existing health insurance cards will no longer be available on and after December 2. After that, the system will shift to one based on My Number Card as the Health Insurance Certificate.

This is not optional. By late 2025, every Japanese citizen who wants to access the national health insurance system will need to use a My Number Card. This creates mandatory technology adoption across the entire healthcare system.

Implications for Pharmacies

Furthermore, starting in December 2024, the issuance of renewed traditional health insurance cards was discontinued, and the government began transitioning to the My Number Card as the primary form of health insurance identification. When used as a health insurance card and with the necessary consent, it allows doctors to access a patient's health information, enabling more personalised medical care. From 1 April 2025, under the facility requirements for the newly introduced "Medical DX Promotion Infrastructure Development Add-on", medical institutions and pharmacies are required to meet a minimum threshold for the use of the My Number Card as a health insurance card.

The number of points granted under the medical service fee schedule will vary depending on each facility's utilisation rate. This policy is designed to incentivise the adoption of digital infrastructure within the healthcare system and to accelerate broader use of the My Number Card nationwide.

The Japanese government is using the reimbursement system—the financial lifeblood of pharmacies—to force digital adoption. Pharmacies that resist digitization will receive lower reimbursements. Pharmacies that embrace digitization will receive financial rewards. This is regulatory compulsion with a velvet glove.

Electronic Prescriptions

Currently, 60% of pharmacies in Japan have implemented digital prescriptions systems, and aiming to implement at all pharmacies by the end of fiscal year in 2024.

Electronic prescriptions fundamentally change the pharmacy workflow. Instead of patients carrying paper prescriptions from doctors to pharmacies, prescriptions exist digitally and can be accessed by any connected pharmacy. This makes services like Kusurinomadoguchi's prescription reservation system even more valuable—patients can select any pharmacy in the network without worrying about physically delivering a paper prescription.

Strategic Position

Kusurinomadoguchi's pre-existing digital infrastructure positioned the company perfectly for this regulatory shift. Pharmacies that needed to upgrade their systems for My Number Card compliance found a company that already offered comprehensive digital solutions. The regulatory mandate became a sales tailwind.

For investors, the My Number Card transition represents a structural catalyst with a defined timeline. Unlike fuzzy predictions about "digital transformation," this is a regulatory mandate with specific dates and enforcement mechanisms. Companies positioned to benefit have rare visibility into future demand.

VII. Key Inflection Point #3: IPO and Scale (October 2023)

The Listing

IPO information about Kusurinomadoguchi, Inc. Opening price was 1580 Yen. On 2023/10/04 approval on Growth.

Kusurinomadoguchi listed on the Tokyo Stock Exchange Growth Market on October 4, 2023, with a public offering price of 1,700 yen. The company issued 1.8 million new shares and sold 1 million existing shares, raising approximately 2.89 billion yen through the public offering.

The IPO occurred during a period of strong interest in Japanese equities—Warren Buffett's investments in Japanese trading companies had sparked renewed international attention on the market. But Kusurinomadoguchi was not a typical TSE IPO. This was a healthcare technology platform with a clear growth trajectory, positioned at the intersection of demographic necessity and regulatory mandate.

Strategic Rationale for Going Public

The purpose of listing extended beyond capital raising. According to company statements, the IPO was designed to upload prescription data held by pharmacies and hospitals to the cloud and increase social trust. This would create an environment where medical institutions can safely entrust their data to the company.

Healthcare data is sensitive. Pharmacies considering whether to adopt Kusurinomadoguchi's Core Systems face legitimate questions about data security, corporate stability, and long-term viability. A public listing—with its disclosure requirements, governance standards, and regulatory oversight—provides reassurance that private companies cannot easily match.

The IPO funds were allocated primarily to system and software development for service improvements, including enhancing the medication notebook app functions. This investment in product development reflects the company's focus on deepening its technology moat rather than pursuing aggressive customer acquisition.

Five-Year Ambitions

The company's stated goal is to exceed 30,000 affiliated pharmacies within five years of listing. Given the current network of approximately 20,000 pharmacies (about 30% of nationwide pharmacies), this would represent a 50% expansion of the platform's reach—potentially capturing half of Japan's pharmacy market.

5592 reached its all-time high on Sep 29, 2025 with the price of 4,685 JPY, and its all-time low was 1,000 JPY and was reached on Aug 5, 2024. The stock's volatility since IPO reflects both the opportunity ahead and the uncertainty inherent in growth stage companies.

For investors, the IPO represents a transition from private to public market dynamics. The company now operates under public market scrutiny, with quarterly earnings expectations and analyst coverage. Whether this pressure proves beneficial (discipline) or detrimental (short-termism) remains to be seen.

VIII. Key Inflection Point #4: Medical Fee Revision Cycle (2024-2025)

Japan's healthcare system operates on a unique reimbursement rhythm that creates predictable demand cycles for pharmacy technology. Understanding this rhythm is essential for forecasting Kusurinomadoguchi's financial performance.

The Biennial Revision Cycle

Japan revises its medical and dispensing fee schedule every two years. These revisions adjust the reimbursement rates that pharmacies receive for various services—and they often require corresponding updates to pharmacy systems. Fiscal year ended March 2025 was a revision year, which created special demand and significantly boosted performance.

Think of it like a regulatory "refresh cycle" that forces pharmacies to evaluate and often upgrade their technology systems. For Kusurinomadoguchi, revision years are periods of elevated demand for Core Systems products and implementation services.

Record Performance

Kusurinomadoguchi Q1 FY2026 slides: sales up 11%, operating profit surges 65%. The company reported consolidated net sales of 2.91 billion yen in Q1 FY2026, an 11% increase compared to the previous period. Consolidated operating profit landed at 620 million yen, a 65% increase.

The gross profit margin improved from 39% in Q1 FY2025 to 47% in Q1 FY2026, marking the highest rate historically. This margin expansion reflects operating leverage—the company's platform costs scale slowly as revenue grows quickly.

Stock sales (recurring revenue) for Q1 FY2026 reached a record high as all three businesses achieved increased revenue compared to both the same period last year and the previous quarter. This emphasis on recurring revenue—the Hikari Tsushin DNA—provides visibility and predictability that investors value.

M&A Expansion

In January 2024, Kusurinomadoguchi made an additional investment in Hybridge Co., Ltd., which provides electronic medication history systems for dispensing pharmacies, making it a subsidiary. This acquisition extends the company's Core Systems capabilities and demonstrates willingness to use M&A strategically.

Kusurinomadoguchi maintains its annual forecast for fiscal year 2026, with targets of 12.3 billion yen in net sales, 2.2 billion yen in operating profit and 2.135 billion yen in ordinary profit. The company expects to achieve these objectives through continued growth in all business segments and further cost optimization.

For investors, the medical fee revision cycle creates predictable volatility in quarterly results. Revision years (even fiscal years) tend to show stronger performance; non-revision years may show temporary slowdowns. Understanding this rhythm helps contextualize quarterly surprises.

IX. Current Business Model Deep Dive

Revenue Model: Stock vs. Shot

Kusurinomadoguchi's revenue model distinguishes between "stock" (recurring) and "shot" (one-time) sales—a framework inherited from parent Hikari Tsushin's emphasis on predictable revenue streams.

Recurring sales include monthly listing fees for Rich Plans that provide top site positioning, and system fees for Pharmacy Support (a customer repeat promotion system). Shot sales include initial implementation costs for Rich Plans and Pharmacy Support.

The strategic shift toward recurring "stock" revenue provides predictability that investors value. The company measures growth based on stock sales and gross stock profit of each business rather than consolidated operating profit—focusing on recurring revenue quality over one-time revenue quantity.

Product Suite Walkthrough

The company offers EPARK drug counter, a pharmacy/drugstore search and reservation site; matching site to buy and sell dead stock medicines at dispensing pharmacies; site for medicine counter telephone medical treatment; Health Tech Navi, an electronic medication history system; Care Daisy system to link recording systems and ICT devices; solution for purchasing pharmaceuticals; and system that allows for centralized management of outpatient reception, outpatient reservations, and online medical treatment.

It also provides Pharmacy Support, a customer management system for repeat patients in the pharmacy industry; system specialized for dispensing pharmacies; matching service that connects nursing care facilities and pharmacies; solution from the purchase of pharmaceuticals to the purchase of immovable inventory; Online consultation by hospital support; online medication guidance; support solution to pharmacies; EPARK medicine notebook, a medication notebook that allows to make dispensing reservations and manage family medicines.

Network Effects & Competitive Moat

The receipt computer data accumulated in the core systems business integrates with medication notebooks and pharmacy inventory management systems, creating the source of convenience and competitive advantage. Each new pharmacy on the platform improves data quality, which improves services for all pharmacies, which attracts more pharmacies—a classic network effect.

Future Bets: Delivery & Convenience

Instead of making trips to the hospital and then the pharmacy every time an elderly person with a chronic illness needs medication, they can receive online medical care and then go to a nearby convenience store to pick up their prescription. Services for receiving prescription drugs outside of pharmacies are expanding rapidly.

In the convenience store industry, FamilyMart has implemented this service in approximately 4,500 stores in the Tokyo metropolitan area, and Lawson is also working with Qol Holdings, a major pharmacy company, to offer drug pickup and delivery services at dozens of stores with dispensing facilities. Drugstores and food delivery companies such as Uber Eats Japan are expanding their prescription drug services one after another. Seven-Eleven sees prescription drugs as a product that will motivate customers to visit its stores.

The company has been conducting pilot experiments with Seven-Eleven on prescription pickup, building prescription pickup lockers that allow patients to receive medications at their convenience. This represents a potential expansion of the platform's reach beyond traditional pharmacy locations.

X. Competitive Landscape & Strategic Analysis

Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-LOW

High switching costs once pharmacies integrate core systems create meaningful barriers. The network of ~20,000 pharmacies (30% of Japan's total) creates significant scale advantages. Regulatory complexity in healthcare creates barriers for pure tech entrants.

However, large platform companies represent potential threats. Amazon has launched an online service enabling customers in Japan to purchase prescription medications without having to visit physical pharmacies. In July 2024, Amazon announced the launch of online pharmacy and medicine delivery services in Japan, partnering with 2,500 drugstores. The service allows customers to obtain electronic prescriptions through the CLINICS app and receive medications via delivery or pickup.

Amazon's entry validates the market opportunity but also introduces a formidable competitor. Rakuten similarly operates pharmacy services with approximately 6,000 registered dispensing pharmacies.

2. Bargaining Power of Suppliers: LOW

Kusurinomadoguchi is primarily a software/platform business. Cloud infrastructure is commoditized. No critical supplier dependencies have been identified.

3. Bargaining Power of Buyers: MODERATE

February 2024: Tsuruha Holdings and Welcia Holdings announced an accelerated merger, expected to be completed by December 2025. The combined entity, backed by retail giant Aeon, will form Japan's largest pharmacy retail group, operating over 5,500 stores with annual sales exceeding JPY 2 trillion.

Tsuruha shareholders approved a merger plan with Welcia, which will result in an effective acquisition by supermarket chain Aeon. Tsuruha, based in Sapporo, has announced it will integrate its operations with Welcia, the biggest force within the Japanese pharmacy industry, in December.

This consolidation creates larger pharmacy chains with more negotiating power. However, the fragmented independent pharmacy market (~60,000 total pharmacies) provides a counterbalance. Switching costs for integrated systems create lock-in that limits buyer power.

4. Threat of Substitutes: MODERATE-LOW

Traditional paper-based processes still exist but are declining under regulatory pressure. The My Number Card mandate and electronic prescription requirements reduce substitute viability over time. Government policy is effectively eliminating paper-based alternatives.

5. Industry Rivalry: MODERATE-HIGH

The company operates in a competitive market with multiple pharmacy system providers and healthcare IT companies. Japan-specific competitors include established pharmacy system vendors. However, differentiation through integrated platform approach—combining patient-facing apps, B2B marketplace, and core systems—creates competitive separation.

Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG ✓

Partnership with approximately 20,000 pharmacies (about 30% of nationwide pharmacies) provides meaningful scale advantages. Platform development costs spread across a growing customer base. Data infrastructure investments benefit all users.

2. Network Effects: VERY STRONG ✓✓

The patient-pharmacy two-sided marketplace creates powerful network effects: More pharmacies → better patient experience → more patients → more valuable for pharmacies. Access to EPARK's ~50 million users creates a powerful acquisition channel. Medication data improves with more usage, enabling better services.

3. Counter-Positioning: MODERATE ✓

Traditional pharmacy system vendors focused on hardware/on-premise solutions face strategic challenges competing with Kusurinomadoguchi's cloud-first, patient-centric approach. Incumbents would need to cannibalize existing business to replicate this model.

4. Switching Costs: STRONG ✓

Receipt computer (レセコン) data integration with medication notebooks and inventory management creates deep system dependencies. Staff training investments create organizational switching costs. Patient data migration challenges create technical switching costs.

5. Cornered Resource: MODERATE

One of Japan's largest medication notebook apps and pharmacy media platforms provides privileged market access. First-mover advantage in prescription online reservation creates historical data assets. Patient medication history data represents a unique resource.

6. Process Power: DEVELOPING

As of Nov 10, 2025, the company has 484 employees. This lean operation for the scale achieved suggests efficient processes. Experience serving both patients and pharmacies creates institutional knowledge. However, process power typically develops over longer time periods.

7. Branding: MODERATE

EPARK brand recognition in Japan from restaurant/service reservations provides spillover benefits. "Kusurinomadoguchi" (Medicine Counter) is directly descriptive and memorable. Trust building with healthcare institutions continues through IPO governance and compliance investments.

XI. Bull vs. Bear Case

Bull Case

Massive TAM in Aging Japan: The Japan pharmaceuticals market size is projected to grow from $110.18 billion in 2025 to $206.70 billion by 2032, exhibiting a CAGR of 9.40%. Healthcare spending will continue growing as the population ages.

Regulatory Tailwinds: The My Number Card mandate, electronic prescription requirements, and telemedicine permanence create structural demand for digitization. These aren't predictions—they're scheduled policy implementations with enforcement mechanisms.

E-pharmacy Growth: The Japan e-pharmacy market size reached USD 6.4 Billion in 2024 and is expected to reach USD 20.5 Billion by 2033, exhibiting a CAGR of 12.4%. Digital pharmacy services represent one of the fastest-growing segments of Japanese healthcare.

Strong Financial Trajectory: 133% earnings growth in 2024, with continued growth in Q1 FY2026. Operating leverage is evident in margin expansion.

Platform Network Effects Compounding: Each new pharmacy strengthens the platform for all participants. Data advantages grow with scale.

M&A Runway: The fragmented pharmacy tech market offers consolidation opportunities for a well-capitalized public company.

Bear Case

Large Tech Platform Entry Risk: Amazon Pharmacy's July 2024 Japan launch represents a formidable competitor with massive resources. Based on the U.S. experience, Amazon Pharmacy is likely to significantly disrupt Japan's traditional pharmacy industry. As it has done in virtually every other business it has entered, Amazon will use its operational capabilities to increase competition, reduce costs, encourage innovation, and focus more on patient-centered care.

Pharmacy Industry Consolidation: The Tsuruha-Welcia merger creates a pharmacy giant with potential resources to build proprietary technology solutions, reducing dependence on third-party platforms like Kusurinomadoguchi.

Dependency on EPARK/Hikari Tsushin Ecosystem: Its direct parent EPARK also seems to have had to go through some restructurings in recent years. Though matters there seem to be isolated, it could potentially trickle down to KMG.

There are ALOT of pharmacies in Japan. Though it's always been something talked about widely, we may eventually see a decline in the number, whether due to industry consolidation or closures. This in turn, could be a headwind to growth for KMG.

Risk-Averse Healthcare Professionals: Small and medium-sized hospitals and pharmacies may struggle to adopt these systems, potentially leading to their closure. Digital adoption resistance among traditional healthcare providers could slow platform growth.

Regulatory Risk: Government policy changes—particularly around reimbursement rates for digital services—could disrupt the business model.

XII. Key Performance Indicators for Investors

For long-term investors tracking Kusurinomadoguchi's performance, three KPIs merit particular attention:

1. Affiliated Pharmacy Count

The company's stated goal of 30,000 affiliated pharmacies within five years of IPO provides a clear benchmark. As of recent reporting, the network includes approximately 20,000 pharmacies representing ~30% of Japan's market. Progress toward the 30,000 target—and beyond—indicates platform adoption and network effect strength.

Why it matters: Pharmacy count is a leading indicator of platform value. More pharmacies → more patient utility → more pharmacies (network effect). This metric captures the flywheel momentum.

2. Stock (Recurring) Revenue Growth

The company measures itself by stock sales and gross stock profit rather than consolidated operating profit. Recurring revenue growth—from monthly platform fees, system subscriptions, and ongoing services—indicates the sustainability and predictability of the business model.

Why it matters: Recurring revenue has higher quality than one-time revenue. It provides visibility, reduces volatility, and typically commands higher valuation multiples. The Hikari Tsushin DNA emphasizes this metric for good reason.

3. Gross Stock Profit Margin

The gross profit margin improved from 39% in Q1 FY2025 to 47% in Q1 FY2026, marking the highest rate historically. This margin expansion demonstrates operating leverage and pricing power.

Why it matters: Margin trends reveal whether growth is efficient. Expanding margins with growing revenue indicates scalable economics. Contracting margins may signal competitive pressure or investment needs.

XIII. Conclusion: The Platform Thesis

Kusurinomadoguchi represents a compelling case study in platform economics applied to a regulated healthcare market. The company has built a three-pillar business model connecting patients, pharmacies, and healthcare infrastructure—creating network effects that strengthen with scale.

The timing could not be more favorable. Japan's aging population creates inexorable demand growth. Government digitization mandates eliminate paper-based alternatives. COVID-19 accelerated consumer acceptance of digital healthcare services. The regulatory environment has shifted from resistance to active promotion of healthcare technology.

The Hikari Tsushin heritage provides strategic discipline—a focus on recurring revenue, patient capital allocation, and operational efficiency that many growth companies lack. The October 2023 IPO positions the company to capitalize on these trends while providing the governance and transparency that healthcare institutions require.

Challenges remain significant. Amazon's entry into Japanese pharmacy services introduces a fearsome competitor. Pharmacy industry consolidation may reduce the fragmented customer base that platforms serve best. Regulatory changes could alter the reimbursement landscape.

But the fundamental question for investors is straightforward: In a market of 62,000 pharmacies serving 126 million people, will digital platforms capture increasing share of healthcare interactions? The demographic, technological, and regulatory trends all point in the same direction.

Kusurinomadoguchi has positioned itself to be the operating system for Japanese pharmacy—the infrastructure layer connecting patients seeking convenience with pharmacies seeking efficiency. Whether that position proves durable depends on execution, competitive dynamics, and regulatory evolution.

The company's journey from EPARK spin-off to public platform demonstrates the power of patient capital, strategic focus, and timing regulatory change correctly. For investors willing to accept healthcare market complexity and emerging market volatility, Kusurinomadoguchi offers a differentiated exposure to one of the world's most significant demographic transformations.

The "no-wait" prescription pickup that benefits Yamada-san on that rainy Shibuya evening is just the beginning. The question is how much of Japan's healthcare infrastructure will flow through platforms like Kusurinomadoguchi—and what that infrastructure will be worth when the demographic tide fully arrives.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube