Digital Realty: The Infrastructure Backbone of the Digital Economy

I. Introduction & Episode Framework

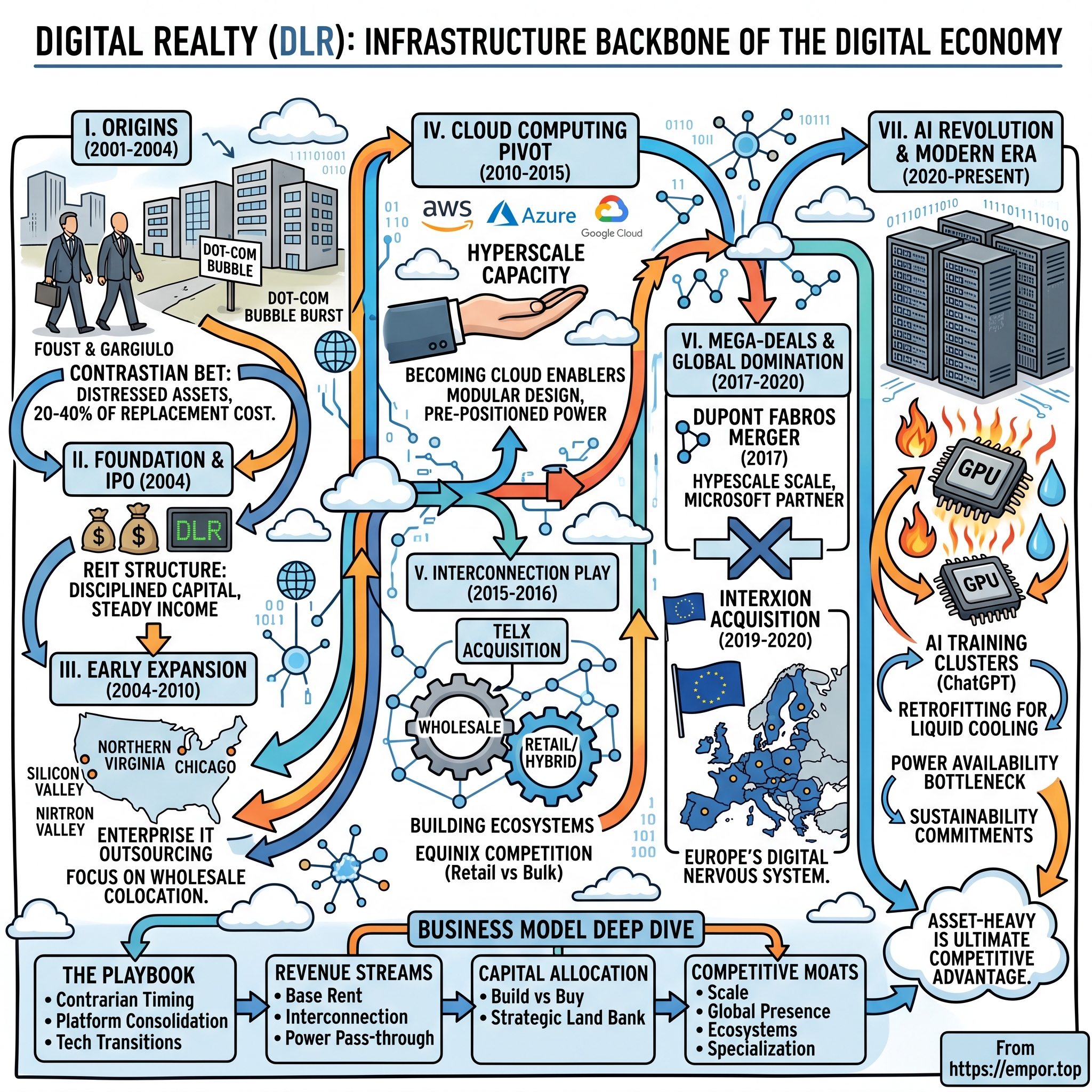

Picture this: It's 2001, and the dot-com bubble has just burst. Across Silicon Valley, data centers built for the "new economy" sit empty—monuments to hubris, their raised floors gathering dust, their cooling systems humming for servers that will never arrive. In San Francisco, two real estate veterans, Michael Foust and Giulio Gargiulo, walk through one of these ghost towns of the digital age. Where others see failure, they see opportunity. Not sexy opportunity—not the kind that gets you on magazine covers—but the kind that builds fortunes: distressed assets selling for 20 to 40 cents on the dollar.

Fast forward to August 2025. Digital Realty commands a market capitalization of $59.79 billion, operates 308 data centers across six continents, and generates $5.63 billion in trailing twelve-month revenue. The company that started as a contrarian bet on physical infrastructure has become the landlord to the cloud giants—Microsoft, Amazon, Meta, Google—powering everything from your Netflix stream to ChatGPT's responses.

How did a distressed asset roll-up transform into the world's largest data center REIT? How did a company founded on the ruins of the first internet bubble position itself perfectly for the AI revolution two decades later? This is the story of Digital Realty—a masterclass in timing contrarian bets, building physical moats in a digital world, and understanding that even in the cloud, somebody needs to own the ground.

What you're about to learn isn't just a corporate history. It's a playbook for recognizing when everyone else is wrong, when picks-and-shovels beat gold mining, and why sometimes the best technology investment is real estate. We'll explore how Digital Realty navigated three major technology transitions—enterprise IT outsourcing, cloud computing, and now artificial intelligence—each time emerging stronger and more valuable.

The central question we'll answer: In an era when every startup wants to be asset-light, how did being asset-heavy become the ultimate competitive advantage?

II. The GI Partners Origin Story & Formation (2001-2004)

The conference room at GI Partners in 2003 felt like a wake. The private equity firm, known for its contrarian infrastructure plays, was reviewing a spreadsheet that would make most investors nauseated. Data center after data center, bleeding cash, abandoned by dot-com dreams. Global Crossing, Exodus Communications, WorldCom—the casualties read like a who's who of the telecom bust. But where others saw toxic assets, GI Partners saw something different: mission-critical infrastructure selling at garage sale prices.

The founding team that would become Digital Realty's DNA wasn't your typical Silicon Valley lineup. Michael Foust brought deep real estate expertise from CB Richard Ellis, understanding location value and development economics. Giulio Gargiulo added operational know-how from running technology infrastructure. Together, they weren't trying to build the next hot startup—they were building the foundation everyone else would need.

Between 2001 and 2004, GI Partners quietly assembled a portfolio that would make any modern cloud company jealous. Twenty-one data centers, acquired through bankruptcy auctions and distressed sales, each purchased at 20-40% of replacement cost. Think about that math: buildings that cost $50 million to construct, fully equipped with power infrastructure, cooling systems, and connectivity, selling for $15 million. It was like buying Manhattan real estate in 1975.

The strategy was deceptively simple but required conviction that ran counter to every trend. While the tech world proclaimed "bits not atoms" and celebrated virtual everything, Foust and team bet on physics: data needs somewhere to live, servers generate heat, and latency is bound by the speed of light. They focused on wholesale colocation—large spaces for enterprise customers—rather than retail colocation's smaller, higher-touch model. Less sexy, more scalable.

By 2004, the portfolio had grown to 23 properties comprising 5.6 million square feet. The timing for going public couldn't have been better—or more contrarian. The market was just beginning to believe in tech again, but data centers? That was still the province of the walking wounded. The November 4, 2004 IPO, priced at $12 per share on October 28, raised eyebrows. A REIT focused on data centers? The structure seemed almost quaint.

But the REIT structure was genius. It provided tax advantages, forced disciplined capital allocation through dividend requirements, and most importantly, it attracted a different investor base—one that understood real estate fundamentals and appreciated steady cash flows over growth stories. This wasn't about disruption; it was about being the arms dealer in every tech war to come.

The early portfolio tells the story: properties in Silicon Valley, Northern Virginia, Chicago, Dallas. Not random selections, but strategic beachheads in what would become the neural centers of the digital economy. Each location chosen for power availability, fiber connectivity, and proximity to both enterprises and network hubs. The foundation was set for what would become a three-decade run of perfectly timed expansions.

III. Going Public & Early Expansion (2004-2010)

The morning of November 4, 2004, Digital Realty's executives gathered at the New York Stock Exchange. The opening bell wasn't just ceremonial—it was vindication. The $12 IPO price implied a modest valuation, but what mattered was access to capital markets. In the data center business, capital isn't just king; it's the entire kingdom.

The REIT structure immediately proved its worth. Unlike traditional tech companies burning cash for growth, Digital Realty generated predictable rental income from day one. The dividend requirement—REITs must distribute 90% of taxable income—forced a discipline that would become the company's signature: grow, but grow profitably. No moonshots, no pivots, just relentless execution.

The August 2006 Phoenix acquisition for $175 million marked a strategic evolution. This wasn't a distressed purchase but a competitive bid for a premium asset. Phoenix offered something California couldn't: abundant land, cheaper power, and a more business-friendly environment. It was Digital Realty's first major bet on the geographic arbitrage that would define data center economics—put the computers where the power is cheap and the regulations are light.

Building data centers isn't like building offices. The infrastructure requirements are staggering: 10-50 megawatts of power capacity, N+1 or 2N redundancy on every critical system, cooling that can handle heat densities that would melt conventional buildings. Digital Realty developed a competency that sounds boring but became a massive moat: they could deliver power and cooling at scale, reliably, anywhere in the world.

The 2008 financial crisis should have been catastrophic. Real estate was ground zero, REITs were getting demolished, and IT spending froze. But something unexpected happened: Digital Realty's occupancy barely budged. Why? Because once you move your servers into a data center, moving them out is expensive, risky, and disruptive. The switching costs created natural customer retention that traditional real estate could only dream of.

This period also saw the rise of enterprise IT outsourcing—companies realizing they shouldn't run their own data centers any more than they should generate their own electricity. Digital Realty positioned itself perfectly: not as a technology company trying to manage your servers, but as a real estate company providing the physical infrastructure. Let IBM, HP, and others handle the complex services; Digital Realty would handle the foundational layer.

By 2010, the company had expanded to 94 properties across three continents. Revenue had grown from $265 million in 2005 to $849 million. But more importantly, the tenant roster was evolving. Early customers were predominantly enterprises and financial services firms. But quietly, a new category was emerging: companies with names like Amazon Web Services, Microsoft Azure, and Google Cloud Platform. The hyperscalers had arrived.

The transition from the post-bubble recovery to the cloud era wasn't obvious at the time. Most saw cloud computing as a threat to data center operators—if everything moves to the cloud, who needs colocation? But Digital Realty's leadership understood something crucial: the cloud isn't ethereal; it's just someone else's computer, and those computers need to live somewhere.

IV. The Cloud Computing Revolution & Strategic Pivot (2010-2015)

The atmosphere at AWS re:Invent 2012 was electric. Amazon's cloud conference had grown from a gathering of early adopters to a movement. On stage, Andy Jassy (before he became CEO) was explaining how AWS was adding computing capacity equivalent to Amazon's entire 2003 infrastructure every single day. In the audience, Digital Realty's executives weren't worried—they were taking notes on where to build next.

The cloud revolution presented an existential question: Would enterprises bypass colocation entirely and go straight to public cloud? The answer turned out to be beautifully complex. Yes, workloads were moving to the cloud, but the cloud providers themselves needed massive amounts of data center capacity. And they needed it fast, at scale, in specific locations, with guaranteed power and cooling specifications that made traditional real estate look simple.

Digital Realty's pivot was subtle but profound. Instead of fighting the hyperscalers, they became their enablers. The company developed products specifically for cloud giants: entire buildings pre-configured for massive power draws, locations chosen for network topology rather than corporate proximity, and most importantly, the ability to deliver at the pace of cloud growth—not real estate timelines.

The numbers were staggering. A single hyperscale deployment might require 10-50 megawatts of power—enough to power a small city. Traditional data center operators would take 18-24 months to deliver this. Digital Realty compressed it to 6-9 months through modular designs, pre-positioned equipment, and relationships with utilities that bordered on partnerships.

Geographic expansion followed the cloud topology map. Frankfurt for European data sovereignty. Singapore for Asian interconnection. Sydney for Australian compliance requirements. Each location wasn't just about land and power—it was about understanding the regulatory, latency, and interconnection requirements that made that location strategic for cloud delivery.

The competition with Equinix during this period was fascinating. Equinix focused on interconnection—becoming the meeting point where networks, clouds, and enterprises connected. Digital Realty focused on scale—becoming the wholesale provider of raw capacity. It was retail versus wholesale, boutique versus bulk. Both strategies worked, but Digital Realty's approach aligned better with the hyperscale tsunami approaching.

By 2015, the transformation was complete but not obvious to outsiders. Digital Realty still looked like a real estate company—same REIT structure, same dividend focus. But underneath, it had become critical infrastructure for the three companies (AWS, Azure, Google Cloud) that would define the next decade of technology. The client concentration that would terrify most businesses became a moat—when your customers are growing 50% annually and have essentially unlimited capital, concentration is a feature, not a bug.

The cloud pivot also changed the competitive landscape. New entrants couldn't just build a data center and compete. They needed global scale, hyperscale expertise, utility relationships, and most importantly, the track record that made cloud giants comfortable betting their infrastructure on you. The barriers to entry had shifted from capital (anyone can raise money) to capability (few can execute at this scale).

V. The Telx Acquisition & Interconnection Play (2015-2016)

The October 2015 boardroom discussion about acquiring Telx for $1.886 billion was heated. Digital Realty had built its empire on wholesale, large-footprint deployments. Telx was the opposite: retail colocation, interconnection focus, smaller deployments but higher margins. It was like Walmart contemplating buying Tiffany's. The cultures, the operations, the customer bases—everything was different.

But CEO Bill Stein saw what others missed. The future wasn't wholesale or retail—it was hybrid. Enterprises weren't going all-in on public cloud; they were building hybrid architectures that required both hyperscale capacity and interconnection density. Telx brought 20 data centers in strategic markets, but more importantly, it brought interconnection ecosystems—communities of carriers, clouds, and enterprises already connected and transacting.

The strategic rationale was "Equinix envy" in the best sense. Equinix's interconnection model commanded premium valuations because it created network effects. Every new participant made the ecosystem more valuable for everyone else. Digital Realty had the scale, but Telx brought the connectivity tissue that would transform buildings full of servers into living, breathing digital ecosystems.

Integration was brutal. Telx's entrepreneurial, high-touch culture clashed with Digital Realty's institutional, process-driven approach. Customer requirements were different—Telx clients wanted 2-10 racks with complex cross-connects; Digital Realty clients wanted 2-10 megawatts with simple connectivity. The sales forces spoke different languages, literally and figuratively.

But the payoff was immediate in strategic terms. Digital Realty could now offer the full stack: hyperscale capacity for cloud providers, wholesale space for enterprises, retail colocation for smaller deployments, and interconnection to tie it all together. When Microsoft needed 30 megawatts for Azure but also wanted to peer with 200 networks, Digital Realty was the only provider that could deliver both.

The July 2016 acquisition of eight European data centers from Equinix for $874 million was the perfect follow-on. Equinix was required to divest these assets for regulatory approval of its own acquisitions. Digital Realty swooped in, paying a fair price for assets that perfectly complemented the Telx strategy. The message to the market was clear: Digital Realty wasn't just playing wholesale anymore.

The business model evolution was profound. Revenue per square foot increased as interconnection revenue layered on top of space and power. More importantly, customer stickiness increased exponentially. Moving servers is hard; moving hundreds of network connections is nearly impossible. The Telx acquisition transformed Digital Realty from a landlord into a platform—one where leaving meant disconnecting from an entire ecosystem.

VI. The DuPont Fabros Mega-Deal (2017)

Chris Eldredge, CEO of DuPont Fabros Technology, must have felt conflicted as he signed the merger agreement in June 2017. His company, built specifically to serve hyperscale customers, was at peak performance. But he also knew the game was changing. The $7.8 billion all-stock deal would create a colossus—157 data centers, $25.2 billion market cap, and more importantly, unprecedented leverage with the hyperscale giants.

DuPont Fabros wasn't just any acquisition. With 12 data centers in three markets spanning 3.5 million square feet and 301.5 megawatts, it was a hyperscale pure play. Their client list read like a who's who of big tech: Microsoft (their largest customer), Facebook, Amazon. These weren't traditional lease agreements but partnerships where DuPont Fabros essentially built to suit for specific hyperscale requirements.

The strategic logic was compelling. In the hyperscale game, size matters exponentially. Cloud providers want partners who can deliver 100 megawatts across multiple continents, not 10 megawatts in one city. The combined entity would have the scale to negotiate better power agreements, the diversification to manage concentration risk, and the platform to serve global deployments seamlessly.

But the real genius was the timing. The hyperscale land grab was accelerating—AWS, Azure, and Google Cloud were in an arms race for global coverage. They needed data center capacity faster than they could build it themselves. Digital Realty plus DuPont Fabros could deliver more capacity, in more locations, faster than any competitor. It was like consolidating arms dealers during a war.

Integration was smoother than Telx because the businesses were more complementary. DuPont Fabros brought hyperscale expertise and relationships; Digital Realty brought global reach and capital access. The combined company could approach Microsoft and say, "We can deliver 50 megawatts in Virginia, 30 in Amsterdam, and 20 in Singapore, all with consistent design and operations." No other provider could match that promise.

The customer concentration that resulted—Microsoft becoming the second-largest client, Facebook the third—would terrify traditional REITs. But in hyperscale, concentration is a competitive advantage. These customers have unlimited demand, multi-year visibility, and investment-grade credit. They're not tenants; they're partners in building the internet's infrastructure.

The financial engineering was equally clever. The all-stock structure preserved capital for growth, the REIT structure provided tax efficiency, and the combined scale lowered the cost of capital. Digital Realty could now fund massive developments that smaller competitors couldn't touch, creating a virtuous cycle of scale begetting scale.

Post-merger execution validated the thesis. The company successfully integrated operations, retained key customers, and most importantly, accelerated the development pipeline. By 2018, they were delivering new capacity at a pace that would have seemed impossible just years earlier. The DuPont Fabros deal didn't just add assets; it transformed Digital Realty into the indispensable partner for hyperscale growth.

VII. The Interxion Acquisition & European Domination (2019-2020)

David Ruberg, CEO of Interxion, had built something special. From Amsterdam, he'd created Europe's most connected data center platform—53 facilities across 11 countries, each one a dense ecosystem of carriers, clouds, and enterprises. When Digital Realty announced the $8.4 billion acquisition in October 2019, it wasn't just buying real estate. It was buying Europe's digital nervous system.

The deal was audacious in scope—the largest data center merger ever, funded entirely by stock swap. But the strategic rationale was even bolder. Europe wasn't just another geography; it was becoming a regulatory island with GDPR, data sovereignty requirements, and a growing skepticism of American tech dominance. Interxion offered something money couldn't quickly build: trusted, local, connected infrastructure with deep community roots.

Frankfurt told the story best. Interxion's campus there wasn't just data centers but the DE-CIX—one of the world's largest internet exchanges. Every major carrier, cloud provider, and enterprise in Germany connected there. It was LinkedIn, eBay, and the New York Stock Exchange rolled into one. You couldn't replicate this with capital; you needed decades of relationship building and trust.

The timing seemed terrible—announcing a massive merger just as COVID was emerging. By March 2020, when the deal closed, the world was in lockdown. Integration meetings happened over Zoom, due diligence site visits became virtual tours, and the carefully planned cultural integration programs were scrapped. Yet somehow, it worked better than anyone expected.

COVID accelerated every digital trend by five years. Video conferencing, e-commerce, streaming, remote work—all drove explosive demand for data center capacity. While other real estate sectors cratered, Digital Realty and Interxion were adding capacity as fast as they could build. The pandemic wasn't a headwind; it was rocket fuel.

The integration strategy was brilliant in its simplicity: don't integrate. Keep the Interxion brand, keep David Ruberg running EMEA, keep the local teams and relationships intact. "Interxion, a Digital Realty company" wasn't corporate speak—it was recognition that in Europe, local trust matters more than global scale. The teams that had spent decades building relationships with Deutsche Telekom, BT, and Orange stayed in place.

The combined platform was transformative. Digital Realty could now offer truly global solutions—a customer could deploy in Silicon Valley, Northern Virginia, Frankfurt, and Singapore with one contract, one technical standard, and one relationship. For American companies expanding to Europe or European companies going global, Digital Realty became the obvious choice.

Financially, the accretion was immediate. Interxion's premium interconnection revenue boosted margins, the European exposure diversified the revenue base, and the strategic value to hyperscalers—who needed European capacity for regulatory compliance—justified premium pricing. The $8.4 billion price tag that seemed rich in 2019 looked prescient by 2021.

VIII. The AI Revolution & Modern Era (2020-Present)

The January 2021 announcement that Digital Realty would relocate its headquarters to Austin, Texas, wasn't about tax savings. It was about power—literally. Texas had abundant electricity, renewable energy options, and a regulatory environment that could approve new substations in months, not years. As CEO Bill Stein put it, "We go where the electrons are."

Then came November 30, 2022. ChatGPT launched, and suddenly everyone understood AI wasn't tomorrow's technology—it was today's reality. Within weeks, Digital Realty's phones were ringing off the hook. Not for standard deployments but for AI training clusters requiring power densities that made traditional hyperscale look quaint. Where normal racks consumed 5-10 kilowatts, AI training clusters needed 50-100 kilowatts. The physics of cooling that much heat in confined spaces pushed data center design to its limits.

The portfolio had grown to staggering proportions: 308 data centers, 41.8 million square feet across North America, Europe, South America, Asia, Australia, and Africa. But size wasn't the story—adaptation was. Digital Realty was retrofitting facilities for liquid cooling, developing new designs for GPU clusters, and most critically, securing power allocations that would take competitors years to match.

The AI boom created a new bottleneck: power availability. In Northern Virginia, the wait for new electrical service stretched to 2028. In Dublin, the grid operator stopped accepting new data center connections. Digital Realty's existing power allocations—secured years earlier—became as valuable as the buildings themselves. It was like owning water rights in the desert.

Sustainability added another dimension. The AI revolution was colliding with corporate carbon commitments. Digital Realty's renewable energy initiatives—solar installations, wind power agreements, innovative cooling technologies—transformed from nice-to-have to must-have. Customers weren't just asking about price and availability; they wanted to know the carbon footprint per computation.

The competitive landscape shifted dramatically. Traditional competitors like Equinix remained formidable, but new entrants backed by infrastructure funds posed different challenges. More concerning, hyperscalers like AWS and Google were increasingly building their own facilities. The question became: Would Digital Realty be disintermediated by its largest customers?

The answer lay in specialization and flexibility. While hyperscalers could build vanilla capacity for predictable workloads, they relied on partners like Digital Realty for specialized needs—interconnection hubs, edge deployments, burst capacity, and increasingly, AI training infrastructure that required expertise they hadn't developed internally.

By 2024, CEO Stein could credibly claim it had been "a remarkable year for Digital Realty." Record leasing was driving growth in revenue backlog, and the interconnection segment—once a small experiment—was generating substantial high-margin revenue. The company had successfully navigated yet another technology transition, emerging stronger and more valuable.

The modern Digital Realty is unrecognizable from the distressed asset roll-up of 2004. It's a technology infrastructure platform masquerading as a REIT, a critical supplier to the companies building our AI future. The 1.3% revenue growth to $5.55 billion in 2024 might seem modest, but in the REIT world, steady growth at this scale is exceptional.

IX. Business Model & Unit Economics Deep Dive

The genius of Digital Realty's business model lies in its simplicity: collect rent. But underneath this straightforward framework operates one of the most complex physical infrastructure businesses in the world. The REIT structure forces transparency—90% of taxable income must be distributed as dividends—which means no hiding behind adjusted metrics or growth stories. The numbers must work today, not in some promised future.

Revenue streams break into three categories, each with distinct economics. Base rental revenue—the monthly payments for space and power—provides the foundation, typically on 3-10 year contracts with annual escalators. Interconnection revenue, though smaller in absolute terms, generates margins above 70% and creates the stickiness that drives renewal rates above 85%. Metered power reimbursements pass through costs but increasingly include markup as power scarcity creates pricing power.

Customer concentration appears alarming on paper—the top 10 customers represent roughly 70% of revenue. But these aren't your typical commercial tenants. Microsoft, Amazon, Meta, and Google have investment-grade credit, multi-decade time horizons, and infrastructure needs growing 30-50% annually. Concentration with customers like these is a feature, not a bug. The risk isn't them leaving; it's not being able to build fast enough to meet their demand.

The capital allocation decision tree is fascinating. Build versus buy isn't just about cost—it's about speed, location, and competitive dynamics. Developing a greenfield data center takes 18-24 months and $300-500 per square foot but provides exact specifications and prime locations. Acquiring existing facilities costs $200-400 per square foot and delivers immediately but might require retrofitting for modern requirements. The sweet spot: buying land in strategic locations, holding it for option value, then developing when demand materializes.

The power arbitrage game separates winners from losers. Digital Realty might secure power at $0.05 per kilowatt-hour through long-term utility agreements, then charge customers $0.12-0.15 after adding reliability, backup systems, and cooling. With a large facility consuming 50 megawatts continuously, that spread generates millions in annual margin. But the real value lies in having power when others don't—in constrained markets, access to power is worth more than the buildings themselves.

Operating leverage in this business is remarkable. Once a data center is built, the incremental cost of adding customers is minimal—the cooling runs whether 50% or 90% occupied, security costs are fixed, and maintenance scales marginally. This drives EBITDA margins from 30% at opening to 65%+ at maturity. A facility losing money in year one can generate 40% cash-on-cash returns by year five.

The competitive moats compound over time. Scale enables better power agreements and equipment purchasing. Global presence attracts multinational customers. Interconnection ecosystems create network effects. Technical expertise in specialized deployments (AI clusters, edge computing, liquid cooling) commands premium pricing. Most importantly, the installed base and power allocations create barriers that new entrants can't overcome with capital alone.

Capital markets mastery distinguishes Digital Realty from traditional real estate companies. They've accessed debt markets at investment-grade rates, issued equity at premium valuations during growth windows, and structured joint ventures that preserve capital while maintaining control. The REIT structure that once seemed limiting became a strategic advantage—forcing discipline, attracting patient capital, and providing tax efficiency that pure-play tech companies can't match.

X. Playbook: Lessons for Builders & Investors

The Digital Realty story offers a masterclass in contrarian infrastructure investing. The first lesson: timing matters, but not how you think. The best time to buy infrastructure isn't when everyone wants it but when everyone's abandoning it. GI Partners' 2001-2004 accumulation phase—buying data centers from bankruptcy at 20-40% of replacement cost—required seeing through the despair to fundamental value.

Patient capital in physical assets creates compounding advantages. While software companies fight for attention in 18-month cycles, Digital Realty built a 20-year runway. Physical infrastructure doesn't iterate like code; it appreciates like wine. The data centers Digital Realty bought for $15 million in 2003 are worth $150 million today—not from speculation but from scarcity, strategic location, and improved operations.

Platform consolidation follows a predictable pattern that Digital Realty executed flawlessly. Start with distressed assets to build scale cheaply. Add strategic capabilities through targeted acquisitions (Telx for interconnection). Achieve market leadership through transformative mergers (DuPont Fabros, Interxion). Then leverage the platform for organic growth at returns no competitor can match. Each phase builds on the previous, creating cumulative advantages.

Managing through technology transitions requires embracing rather than resisting change. When cloud computing emerged, Digital Realty didn't fight it—they became the arms dealer. When AI arrived, they didn't wait—they retrofitted for GPU clusters. The lesson: in infrastructure, you don't need to predict the future perfectly; you need to be flexible enough to serve it when it arrives.

Global versus local execution remains a delicate balance. Digital Realty succeeded by being globally capable but locally sensitive. The Interxion brand preservation in Europe, local teams maintaining carrier relationships, and regional power strategies all reflect understanding that infrastructure is inherently local even when customers are global.

Being asset-heavy when everyone goes asset-light seems counterintuitive but creates the ultimate moat. Every startup wants to be capital-light, but someone needs to own the physical layer. Digital Realty chose the harder path—billions in capital investment, complex operations, regulatory compliance—and that difficulty became their protection. You can't disrupt physics with software.

Capital markets mastery amplifies operational excellence. Digital Realty's ability to access debt at 3%, issue equity at premium valuations, and structure creative joint ventures meant they could always fund growth profitably. The REIT structure forced discipline—no burning cash on moonshots—while providing tax advantages that pure operations could never achieve.

The final lesson might be the most important: boring businesses with exciting customers can generate extraordinary returns. Digital Realty never tried to be sexy. They focused on execution, reliability, and scale while their tenants—the cloud giants, AI pioneers, and streaming services—captured headlines. Sometimes the best position in a gold rush isn't mining for gold but selling picks and shovels.

XI. Bear vs. Bull Case Analysis

The Bull Case: Infinite Demand Meets Finite Supply

The AI revolution isn't just another technology cycle—it's a step function in computational demand. Training a single large language model requires thousands of GPUs running for months, consuming megawatts of power. Inference at scale—billions of ChatGPT queries, image generations, autonomous vehicle decisions—requires distributed infrastructure that dwarfs current capacity. Digital Realty's existing footprint and power allocations position them to capture disproportionate value from this explosion.

Secular growth in data consumption continues accelerating. Video streaming, IoT devices, autonomous vehicles, metaverse applications—each new use case drives exponential data growth. Cisco projects global data traffic will grow from 4.2 zettabytes per month in 2022 to 17.5 zettabytes by 2027. That data needs to live somewhere, be processed somewhere, and be accessible everywhere. Digital Realty owns the "somewhere."

The barriers to entry have never been higher. Northern Virginia has a seven-year wait for new power connections. Singapore has banned new data center construction. Frankfurt's grid is at capacity. Digital Realty's existing power allocations and land banks are irreplaceable assets. A new entrant with unlimited capital still can't overcome physics and permitting.

Platform network effects compound value. Every new carrier connection makes Digital Realty's facilities more valuable to enterprises. Every new cloud on-ramp attracts more customers. Every new customer justifies more carrier investment. This virtuous cycle, built over two decades, can't be replicated quickly regardless of capital availability.

The Bear Case: Disintermediation and Disruption Risks

Hyperscalers building their own facilities represents an existential threat. AWS, Google, and Microsoft have unlimited capital and engineering talent. As their needs become more specialized—custom chip designs, proprietary cooling systems, specific security requirements—the economic logic of outsourcing weakens. Digital Realty's largest customers could become its biggest competitors.

Power constraints might limit growth regardless of demand. The electrical grid wasn't designed for data centers consuming 100+ megawatts. Utility companies move at geological pace. Environmental opposition to new power generation grows stronger. Digital Realty might have land and buildings but without power, they're expensive warehouses.

Rising interest rates impact REIT valuations disproportionately. As risk-free rates rise, dividend yields must increase to remain attractive, pressuring valuations. The cost of capital for new developments increases, reducing returns. REITs suffered in previous rate cycles, and Digital Realty, despite its quality, isn't immune to sector rotation.

Edge computing could fragment the market. If computation moves to thousands of micro data centers at cell towers and local hubs, Digital Realty's large facilities become less strategic. The company is adapting with edge offerings, but their core competency—large-scale facilities—might become less relevant in a distributed computing world.

Valuation Framework and Key Metrics

The valuation debate centers on whether Digital Realty is a real estate company or a technology infrastructure platform. Traditional REIT metrics—price to funds from operations (FFO), dividend yield, cap rates—suggest fair valuation. But platform metrics—customer lifetime value, replacement cost, strategic value to hyperscalers—imply significant undervaluation.

Key metrics to watch include power development pipeline (megawatts under construction), interconnection revenue growth (the highest margin segment), and customer concentration evolution (diversification versus deepening hyperscale relationships). The renewal rate above 85% and rising price per kilowatt indicate pricing power that traditional real estate rarely achieves.

XII. Epilogue & "What Would We Do?"

Standing at the intersection of physical and digital infrastructure, Digital Realty faces the next decade with unprecedented opportunities and challenges. The AI revolution is driving demand that makes previous cycles look quaint—training clusters requiring 100+ megawatts, inference infrastructure supporting billions of users, and edge deployments bringing computation closer to data creation. The company that started by buying distressed assets now shapes how humanity's digital future gets built.

The emerging markets opportunity is tantalizing but complex. India, Southeast Asia, Africa, and Latin America are digitalizing rapidly but lack infrastructure. Digital Realty must balance growth potential with political risk, currency exposure, and infrastructure challenges. The playbook that worked in Frankfurt won't translate directly to Jakarta or Lagos.

Edge computing strategy requires different DNA. Managing thousands of small facilities differs fundamentally from operating hundreds of large ones. The economics, operations, and customer requirements all change. Digital Realty's acquisition strategy might accelerate here—buying edge specialists rather than building capabilities organically.

The energy innovation imperative can't be ignored. Nuclear power—particularly small modular reactors—could solve the power constraint problem. Digital Realty's scale justifies direct investment in power generation. Imagine data centers with dedicated nuclear plants, providing carbon-free, reliable, affordable power. It sounds like science fiction but might be necessary reality by 2030.

Vertical integration temptations will grow stronger. As margins in basic colocation compress, moving up the stack—managed services, cloud on-ramps, AI infrastructure-as-a-service—becomes attractive. But this risks channel conflict with customers and dilutes the beautiful simplicity of the real estate model.

If we were running Digital Realty, we'd double down on what made them successful: being the most reliable, scaled, connected provider of data center infrastructure globally. Let others chase sexy narratives. Focus on execution, expand strategically, and remember that in technology infrastructure, boring and essential beats exciting and optional every time.

The next decade will test whether Digital Realty can navigate another technology transition as successfully as they've handled the previous three. The company that emerged from the ashes of the dot-com bust to become essential infrastructure for the cloud era now faces the AI revolution. Their track record suggests they'll not just survive but thrive, continuing to build the physical foundation for our digital world.

What would we do? We'd recognize that Digital Realty isn't really in the real estate business—they're in the business of making the impossible possible, enabling technologies we can't yet imagine, and owning the ground truth of the digital economy. In a world accelerating toward artificial intelligence, quantum computing, and technologies not yet invented, someone needs to own the infrastructure that makes it all work. Digital Realty has spent two decades proving they're that someone.

The story that began with two real estate veterans walking through abandoned data centers in 2001 has become the foundation for humanity's digital infrastructure. It's a reminder that sometimes the biggest opportunities hide in the wreckage of others' failures, that patient capital and operational excellence beat hype cycles, and that even in the cloud, somebody needs to own the ground.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube